4.1.1 Federal Debt Held by the Public - Front page · 4.1.1 Federal Debt Held by the Public. Note:...

155

0 30 60 90 120 150 0 30 60 90 120 150 1940 1950 1960 1970 1980 1990 2000 2010 2020 Source: CBO, Haver Analytics As Of: 2016 Percent of GDP 4.1.1 Federal Debt Held by the Public Note: Data for fiscal years. Years after 2016 are projected. Percent of GDP CBO Baseline Projection

Transcript of 4.1.1 Federal Debt Held by the Public - Front page · 4.1.1 Federal Debt Held by the Public. Note:...

0

30

60

90

120

150

0

30

60

90

120

150

1940 1950 1960 1970 1980 1990 2000 2010 2020

Source: CBO, Haver Analytics

As Of: 2016Percent of GDP4.1.1 Federal Debt Held by the Public

Note: Data for fiscal years. Years after 2016 are projected.

Percent of GDP

CBO Baseline Projection

Percent As Of: 31-Oct-20174.1.2 10-Year Treasury Yields

Source: U.S. Department of the Treasury

-2

-1

0

1

2

3

4

5

-2

-1

0

1

2

3

4

5

2009 2010 2011 2012 2013 2014 2015 2016 2017

Percent

Treasury Notes

Treasury Inflation-Protected Securities

Percent As Of: 31-Oct-20174.1.3 2-Year Treasury Yields

Source: U.S. Department of the Treasury

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2009 2010 2011 2012 2013 2014 2015 2016 2017

Percent

0

50

100

150

200

250

300

0

50

100

150

200

250

300

2005 2007 2009 2011 2013 2015 2017

Merrill Lynch Option Volatility Estimate

(MOVE) Index

1994-PresentMOVE Average

4.1.4 Fixed Income Implied VolatilityBasis Points Basis Points

Source: Bloomberg, L.P.

As Of: 31-Oct-2017

Note: Implied volatility is calculated using a yield curve-weighted index of the normalized implied volatility on 1-month Treasury options.

-1

0

1

2

3

4

5

-1

0

1

2

3

4

5

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

2016Q3

2016Q4

2017Q1

2017Q2

2017Q3

4.2.1 Advanced Economies Real GDP GrowthPercent PercentAs Of: 2017 Q3

Source: Eurostat, CAO, BEA, Haver Analytics

Note: Data represents seasonally adjusted quarter-over-quarter annualized real GDP growth rates.

United KingdomJapan

Euro Area

United States

-4

-2

0

2

4

6

8

10

-4

-2

0

2

4

6

8

10

2000 2004 2008 2012 2016 2020

Source: IMF, Haver Analytics

As Of: 2016Percent4.2.2 Real GDP Growth

Note: Year-over-year percent change.Data after 2016 are projected.

Percent

Advanced Economies

EmergingEconomies

-6

-4

-2

0

2

4

6

-6

-4

-2

0

2

4

6

2002 2005 2008 2011 2014 2017 2020

Source: IMF, Haver Analytics

As Of: 2016Percent4.2.3 Euro Area Real GDP Growth

Note: Year-over-year percent change. Data after 2016 are projected.

Percent

SpainFranceEuro AreaItalyGermany

-8

0

8

16

24

32

40

-4

0

4

8

12

16

20

2010 2011 2012 2013 2014 2015 2016 2017

Source: Bloomberg, L.P.

As Of: 31-Oct-2017Percent4.2.4 European 10-Year Yields

Percent

Greece (right axis)Portugal (left axis)Spain (left axis)Italy (left axis)United Kingdom (left axis)Germany (left axis)

-18

-12

-6

0

6

12

-18

-12

-6

0

6

12

2014Q1

2014Q3

2015Q1

2015Q3

2016Q1

2016Q3

2017Q1

2017Q3

4.2.5 Contributions to Japanese GDP GrowthPercent Percent

Source: Cabinet Office of Japan, Haver Analytics

As Of: 2017 Q3

Private DemandPublic Demand

GDP

Net ExportsInventories

Note: Data represents seasonally adjusted quarter-over-quarter annualized real GDP growth rates.

-3

-2

-1

0

1

2

3

-3

-2

-1

0

1

2

3

1998 2001 2004 2007 2010 2013 2016

4.2.6 Japanese Consumer Price InflationPercent Percent

Source: Bank of Japan, Haver Analytics

As Of: Sep-2017

Note: Data represents year-over-year percent change. CPI is adjusted for the consumption tax increase that took effect in April 2014.

0

10

20

30

40

50

0

10

20

30

40

50

A.1 European Non-Performing Loan RatiosPercent Percent

Source: European Banking Authority

As Of: Jun-2017

Note: Ratio of non-performing loans and advances to total gross loans and advances. Weighted averages by country.

Weighted Average

0

3

6

9

12

15

18

0

3

6

9

12

15

18

2000 2003 2006 2009 2012 2015

4.2.7 Chinese Real GDP GrowthPercent Percent

Source: China National Bureau of Statistics, Haver Analytics

As Of: 2016

Note: Year-over-year percent change.

Percent As Of: 20164.2.8 Chinese Manufacturing and Services Growth

Source: China National Bureau of Statistics, Haver Analytics

5

8

11

14

17

5

8

11

14

17

2000 2003 2006 2009 2012 2015

Percent

Manufacturing

Services

Note: Year-over-year percent change.

As Of: 31-Oct-20174.2.9 Chinese Equity Market (CSI 300 Index)

Source: Capital IQ

1000

2000

3000

4000

5000

6000

1000

2000

3000

4000

5000

6000

2010 2011 2012 2013 2014 2015 2016 2017

Index Index

Percent As Of: Oct-20174.2.10 Chinese Credit Growth

Source: The People’s Bank of China, Haver Analytics

0

10

20

30

40

50

0

10

20

30

40

50

2010 2011 2012 2013 2014 2015 2016 2017

Total Social Financing

Percent

Note: Year-over-year monthly change. Total credit is defined as the sum of total social financing (TSF) and local government bond issuance. TSF refers to the total volume of financing provided by the financial system to the real economy.

+ Local Gov’t Bond Issuance

0

40

80

120

160

200

240

0

40

80

120

160

200

240

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

4.2.11 Credit to the Chinese Nonfinancial Private Sector Percent of GDP Percent of GDPAs Of: 2017 Q1

Source: China National Bureau of Statistics, BIS, Haver Analytics Note: Rolling 4-quarter sum of GDP.

-300

-100

100

300

500

-300

-100

100

300

500

2006 2008 2010 2012 2014 2016

Net Flows

Portfolio InflowsBank Inflows

Foreign Direct Investment

4.2.12 Gross Foreign Investor Capital Inflows to EMEsBillions of US$ Billions of US$

Source: IMF, Haver Analytics

As Of: 2017 Q2

0

100

200

300

400

500

600

700

0

100

200

300

400

500

600

700

2005 2007 2009 2011 2013 2015 2017

4.2.13 Emerging Market Gross Global Bond IssuanceBillions of US$ Billions of US$

Source: Dealogic

As Of: 31-Oct-2017

Note: Bonds have maturities greater than one year and have been internationally marketed or placed. “ Public” includes issuance by municipal and state-owned enterprises.

PrivatePublic

Sovereign

YTD

0

200

400

600

800

1000

0

200

400

600

800

1000

2008 2010 2012 2014 2016Source: JP Morgan,Haver Analytics

As Of: 31-Oct-2017Basis Points4.2.14 Emerging Market Bond Spreads

Note: JP Morgan EMBI+ Sovereign Spreads indices for each region.

Basis Points

Latin AmericaEuropeAsia

-6

-3

0

3

6

9

12

-6

-3

0

3

6

9

12

1998 2001 2004 2007 2010 2013 2016

4.2.15 Change in State and Local Government Tax RevenuesPercent Percent

Source: Census Bureau

Note: Data represents year-over-year change. Revenue measures includes revenues from property, individual income, corporate income, and sales taxes. Gray bars signify NBER recessions.

As Of: 2017 Q2

-20

-15

-10

-5

0

5

10

15

-20

-15

-10

-5

0

5

10

15

2007 2009 2011 2013 2015 2017

Source: ICI, Haver Analytics

As Of: Sep-2017Billions of US$ Billions of US$4.2.16 Long-Term Mutual Fund Flows: Municipal Bonds

4.2.17 Municipal Bond Spreads

Source: Thomson Reuters MMD, Haver Analytics

-200

0

200

400

600

-200

0

200

400

600

2005 2007 2009 2011 2013 2015 2017

Basis Points Basis PointsAs Of: 31-Oct-2017

Note: Spreads between municipal and Treasury securities of comparable maturities.

10-Year AAA GO

10-Year BBB GO30-Year BBB GO

30-Year AAA GO

Billions of US$

0

100

200

300

400

500

600

0

100

200

300

400

500

600

2005 2007 2009 2011 2013 2015 2017YTD

New CapitalRefunding

4.2.18 Municipal Bond IssuanceBillions of US$

Source: Thomson Reuters, SIFMA

As Of: Oct-2017

Note: Excludes maturities of 13 months or less and private placements.

25

30

35

40

45

50

16

18

20

22

24

26

28

1980 1985 1990 1995 2000 2005 2010 2015Source: Federal Reserve, Haver Analytics

As Of: 2017 Q2Percent4.3.1 Debt Ratios for Nonfinancial Corporations

Note: Gray bars signify NBER recessions.

Percent

Debt to GDP (right axis)

Debt to Total Assets (left axis)

0

1

2

3

4

5

6

7

0

1

2

3

4

5

6

7

1980 1985 1990 1995 2000 2005 2010 2015

4.3.2 Liquid Assets to Assets for Nonfinancial CorporationsPercent Percent

Source: Federal Reserve, Haver Analytics

Note: Liquid assets includes foreign deposits, checkable deposits and currency, time and savings deposits, money market fund shares, security repurchase agreements, debt securities, and mutual fund shares.

As Of: 2017 Q2

-100

-50

0

50

100

-100

-50

0

50

100

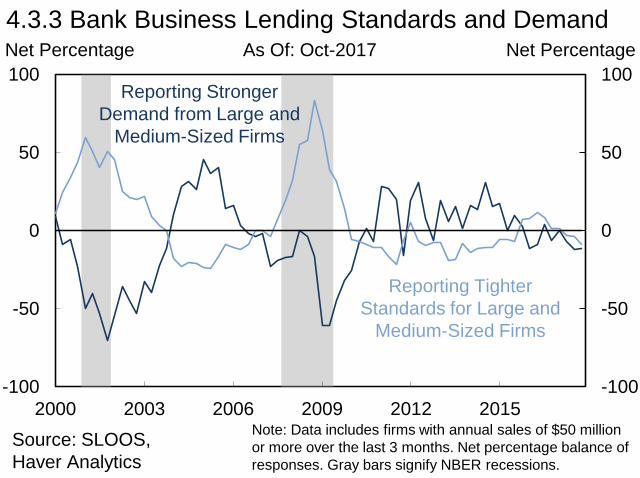

2000 2003 2006 2009 2012 2015Source: SLOOS, Haver Analytics

As Of: Oct-2017Net Percentage4.3.3 Bank Business Lending Standards and Demand

Note: Data includes firms with annual sales of $50 million or more over the last 3 months. Net percentage balance of responses. Gray bars signify NBER recessions.

Net Percentage

Reporting Stronger Demand from Large and

Medium-Sized Firms

Reporting Tighter Standards for Large and

Medium-Sized Firms

0

1

2

3

4

0

1

2

3

4

2000 2003 2006 2009 2012 2015

Source: FDIC, Haver Analytics

As Of: 2017 Q2Percent4.3.4 Noncurrent Commercial and Industrial Loans

Note: Percent of total C&I loans. Gray bars signify NBER recessions.

Percent

0

3

6

9

12

15

18

0

3

6

9

12

15

18

2001 2003 2005 2007 2009 2011 2013 2015 2017

4.3.5 Rolling 12-Month Speculative-Grade Default RatePercent PercentAs Of: Oct-2017

Source: Moody’s Investors Service

Note: Issuer-weighted default rate. “Speculative-grade” refers to non-investment grade instruments.

BondsLoans

Trillions of US$

0.0

0.4

0.8

1.2

1.6

2.0

0.0

0.4

0.8

1.2

1.6

2.0

2005 2007 2009 2011 2013 2015 2017YTD

Investment GradeHigh-Yield

4.3.6 Corporate Bond IssuanceTrillions of US$

Source: Thomson Reuters, SIFMA

As Of: Oct-2017

Note: Includes all non-convertible corporate debt, MTNs, and Yankee bonds, but excludes all issues with maturities of 1 year or less and CDs.

0

200

400

600

800

1000

0

100

200

300

400

2010 2011 2012 2013 2014 2015 2016 2017

4.3.7 U.S. Cash Corporate Credit Spreads

Source: Bank of America Merrill Lynch, Federal Reserve, S&P LCD

As Of: 31-Oct-2017

Leveraged Loans (right axis)High-Yield (right axis)Investment Grade (left axis)

Basis Points Basis Points

Note: Secondary market spreads. Investment grade and high-yield data represent option-adjusted spreads. Dotted lines represent 1997-present median.

0

20

40

60

80

100

0

20

40

60

80

100

1997 2001 2005 2009 2013 2017

4.3.8 Distressed RatiosPercent Percent

Source: S&P LCD, Merrill Lynch

Note: S&P LSTA Index Distress Ratio depicts the percentage of performing loans trading below 80. Merrill Lynch High-Yield Index Distress Ratio depicts the percentage of performing high-yield bonds with yields over Treasuries of 1,000 or more basis points. The high-yield index uses data from the Merrill Lynch High-Yield Index from Jan-1997 through Jul-2017 and data from the S&P U.S. High-Yield Corporate Bond Index from Aug-2017 to present.

As Of: Oct-2017

High-Yield Index Distress RatioS&P LSTA Index Distress Ratio

0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

140

2001 2005 2009 2013 2017

4.3.9 CLO IssuanceBillions of US$ Billions of US$

Source: S&P LCD

As Of: Oct-2017

YTD

4.3.10 Leveraged Loan Primary Market by Investor Type

Source: S&P LCD

0

10

20

30

40

50

60

70

0

10

20

30

40

50

60

70

2005 2007 2009 2011 2013 2015

Percent Percent

Finance & Security Companies

As Of: 2017 Q3

CLOs

Insurance CompaniesLoan Mutual Funds Hedge Funds

Banks

0

25

50

75

100

125

150

0

25

50

75

100

125

150

1992 1996 2000 2004 2008 2012 2016

Source: BEA, Federal Reserve, Haver Analytics

As Of: 2017 Q2Percent

4.4.1 Household Debt as a Percent of Disposable Personal Income

Note: Other Household Credit includes debts of both households and nonprofits.

Percent

Other Household CreditConsumer CreditMortgages

0

200

400

600

800

1000

1200

1400

0

200

400

600

800

1000

1200

1400

2003 2006 2009 2012 2015Source: FRBNY Consumer Credit Panel/Equifax, Haver Analytics

As Of: 2017 Q3Billions of US$4.4.2 Components of Consumer Credit

Note: Gray bar signifies NBER recession.

Billions of US$

Credit Card Debt

Auto Loans

Student Loans

Other HouseholdDebt

9

10

11

12

13

14

9

10

11

12

13

14

1980 1986 1992 1998 2004 2010 2016

Source: Federal Reserve,Haver Analytics

As Of: 2017 Q2Percent4.4.3 Household Debt Service Ratio

Note: Ratio of debt-service payments to disposable personal income. Seasonally adjusted. Gray bars signify NBER recessions.

Percent

30

40

50

60

70

30

40

50

60

70

1990 1994 1998 2002 2006 2010 2014

1990-Present Average

4.4.4 Owners’ Equity as Share of Household Real EstatePercent Percent

Source: Federal Reserve, Haver Analytics

Note: Gray bars signify NBER recessions.

As Of: 2017 Q2

0

3

6

9

12

15

0

3

6

9

12

15

2003 2005 2007 2009 2011 2013 2015 2017

Source: FRBNY Consumer CreditPanel/Equifax, Haver Analytics

As Of: 2017 Q3Percent4.4.5 Share of Household Debt by Delinquency Status

Note: Severely derogatory loans are loans for which there are reports of a repossession, charge off to bad debt, or foreclosure.

Percent

Severely Derogatory120+ Days Late90 Days Late60 Days Late30 Days Late

Index As Of: Aug-20174.5.1 House Prices by Census Region

Source: FHFA, Haver Analytics

50

100

150

200

250

300

350

50

100

150

200

250

300

350

1991 1995 1999 2003 2007 2011 2015

Index

MountainPacificWest South CentralSouth AtlanticWest North CentralTotal U.S.New EnglandEast South CentralMiddle AtlanticEast North Central

Note: Purchase-only price index. Jan-1991 = 100.

0

2

4

6

8

10

12

0

200

400

600

800

1000

1200

1992 1996 2000 2004 2008 2012 2016

30-Year Mortgage Rate (right axis)

4.5.2 Mortgage Originations and RatesBillions of US$ Percent

Source: Mortgage Bankers Association, Freddie Mac Primary Mortgage Market Survey

As Of: 2017 Q3

Refinance (left axis)Purchase (left axis)

Note: Originations represent all 1-4 family homes. Originations calculated as 4-quarter moving averages. Mortgage rates calculated as quarterly averages.

0

1

2

3

4

5

6

0

1

2

3

4

5

6

2000 2003 2006 2009 2012 2015Source: Mortgage Bankers Association, Haver Analytics

As Of: 2017 Q3Percent4.5.3 Mortgage Delinquency and Foreclosure

Note: Percent of all mortgages.

Percent

MortgageForeclosure

InventoryMortgage Payments90+ Days Past Due

0

5

10

15

20

25

30

0

150

300

450

600

750

900

2010 2011 2012 2013 2014 2015 2016 2017

Value of Negative Equity in Residential Mortgages

(left axis)

Percent of Residential

Mortgages with Negative Equity

(right axis)

4.5.4 Mortgages with Negative EquityBillions of US$ Percent

Source: CoreLogic

As Of: 2017 Q2

0

20

40

60

80

100

0

20

40

60

80

100

2000 2002 2004 2006 2008 2010 2012 2014 2016

4.5.5 Purchase Origination Volume by Credit ScorePercent of Originations Percent of Originations

Source: McDash, FHFA calculations

As Of: 2016

Note: Includes first lien purchases only.

<600

600-659

660-699

700-719

720-759

>760

0

20

40

60

80

100

0

20

40

60

80

100

2000 2003 2006 2009 2012 2015

4.5.6 Mortgage Originations by ProductPercent of Originations Percent of Originations

Source: Inside Mortgage Finance

As Of: 2017 Q3

FHA / VA

GSE

Private Portfolio and Securitized

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2002 2005 2008 2011 2014 2017

4.5.7 RMBS IssuanceTrillions of US$ Trillions of US$

Source: Fannie Mae, Freddie Mac, Ginnie Mae, Bloomberg, L.P., Thomson Reuters, SIFMA

As Of: Oct-2017

Non-AgencyAgency

YTD

0

2

4

6

8

10

0

2

4

6

8

10

2011 2012 2013 2014 2015 2016 2017

4.5.8 Mortgage Servicing MarketTrillions of US$ Trillions of US$

Source: Inside Mortgage Finance

As Of: 2017 Q3

NonbankBank

Note: Data covers top 25 servicers in each quarter.

40

60

80

100

120

140

160

40

60

80

100

120

140

160

2008 2010 2012 2014 2016

4.5.9 Commercial Property Price IndicesIndex Index

Source: Real Capital Analytics

National

Note: Jan-2008 = 100.

Major Markets

As Of: Oct-2017

0

1

2

3

4

0

1

2

3

4

2000 2003 2006 2009 2012 2015

4.5.10 CRE Loans by Institution Trillions of US$ Trillions of US$As Of: 2017 Q2

Source: Federal Reserve, Haver Analytics

Government AgenciesCMBS Issuers and REITsInsurers

Banks

-100

-75

-50

-25

0

25

50

75

100

-100

-75

-50

-25

0

25

50

75

100

2000 2003 2006 2009 2012 2015

4.5.11 Percent of Banks Tightening Loan StandardsNet Percentage Net PercentageAs Of: Oct-2017

All CRE Loans

Source: Federal Reserve, Haver Analytics

Other CRE TypesConstr./Land Dev.Multifamily

Net % Banks Reporting Stronger

Demand

0

50

100

150

200

250

0

50

100

150

200

250

2001 2003 2005 2007 2009 2011 2013 2015 2017YTD

4.5.12 CMBS IssuanceBillions of US$ Billions of US$

Source: Inside Mortgage Finance

As Of: 2017 Q3

AgencyNon-Agency

4.5.13 CMBS Senior Debt SpreadsBasis Points Basis Points

Source: J.P. Morgan

As Of: 27-Oct-2017

Note: Spreads are 10-year Swaps to Senior AAA CMBS.

0

50

100

150

200

0

50

100

150

200

2012 2013 2014 2015 2016 2017

0

100

200

300

400

500

600

2

4

6

8

10

12

1995 1998 2001 2004 2007 2010 2013 2016

B.1 CRE Capitalization Rates and SpreadsPercent Basis Points

Source: CoStar Group

Aggregate CRE Cap Rate

(left axis)

CRE Cap Rate Spread to 10-Year Treasury

(right axis)

As Of: 2017 Q2

Note: Dotted lines represent 1995-present average.

0

2

4

6

8

0

2

4

6

8

2002 2004 2006 2008 2010 2012 2014 2016

B.2 CRE Loan Levels to GDPPercent Percent

Source: FDIC, BEA, Haver Analytics

As Of: 2017 Q3

Construction and Land Development

Multifamily

Nonfarm Nonresidential

Note: Loans held at FDIC-insured commercial banks.

90

100

110

120

130

140

90

100

110

120

130

140

1998 2001 2004 2007 2010 2013 2016

Source: Federal Reserve, Haver Analytics

As Of: Oct-2017Index4.6.1 Nominal U.S. Dollar Trade-Weighted Index

Note: Nominal U.S. Dollar Trade-Weighted Index is a weighted average of the foreign exchange value of the U.S. dollar against the currencies of a broad group of major U.S. trading partners.

Index

50

70

90

110

130

150

50

70

90

110

130

150

2008 2010 2012 2014 2016

Source: Federal Reserve, Haver Analytics

As Of: 31-Oct-2017Index4.6.2 U.S. Dollar Performance

Note: 1-Jan-2008 = 100. EM is a weighted average of the FX values of the dollar against a subset of currencies in the broad index that do not circulate widely outside the country of issue.

Index

Vs. EuroBroad Dollar IndexVs. EMVs. Yen

-60

-40

-20

0

20

40

-60

-40

-20

0

20

40

4.6.3 Change in U.S. Dollar Exchange RatesPercent Percent

Source: Wall Street Journal, Haver Analytics

As Of: 31-Oct-2017

Year-over-Year ChangeChange Since Mid-2014

Change from31-Oct-2016 to 31-Oct-2017

Annual growth rate from 31-Oct-2012 to

31-Oct-2017Major EconomiesU.S. (S&P) 21.1% 12.8%Euro (Euro Stoxx) 20.9% 9.9%Japan (Nikkei) 26.3% 19.8%U.K. (FTSE) 7.7% 5.3%Selected EuropeGermany (DAX) 24.0% 12.7%France (CAC) 22.0% 9.9%Italy (FTSE MIB) 33.1% 8.0%Spain (IBEX) 15.1% 6.1%Emerging MarketsMSCI Emerging Market Index 23.3% 2.3%Brazil (Bovespa) 14.5% 5.4%Russia (MICEX) 3.8% 7.7%India (Sensex) 18.9% 12.4%China (Shanghai SE) 9.4% 10.4%Hong Kong (Hang Seng) 23.2% 5.5%South Korea (KOSPI) 25.7% 5.7%

4.7.1 Returns in Selected Equities Indices

Source: Capital IQ

1.0

1.5

2.0

2.5

3.0

3.5

10

15

20

25

30

2007 2009 2011 2013 2015 2017

4.7.2 S&P 500 Key RatiosRatio Ratio

Source: Bloomberg, L.P.

P/B Ratio (right axis)

Trailing P/E Ratio (left axis)

As Of: 31-Oct-2017

Note: Dotted lines represent Sep 1997-present median.

0

20

40

60

80

100

0

20

40

60

80

100

2007 2009 2011 2013 2015 2017

4.7.3 S&P 500 VolatilityIndex Index

Source: Capital IQ

As Of: 31-Oct-2017

Note: In Sep 2003, CBOE revised the methodology to calculate VIX.

Oct 1997 -Present Average

VIX

0

25

50

75

100

125

150

175

200

0

25

50

75

100

125

150

175

200

2008 2010 2012 2014 2016Source: Energy Information Administration, S&P, Haver Analytics

As Of: 31-Oct-2017Index4.8.1 Commodities

Note: 02-Jan-2008 = 100.

Index

Agriculture (S&P GSCI Agricultural Spot Index)Industrial Metals (S&P GSCI Industrial Metals Spot Index)Crude Oil (WTI)Natural Gas

0.0

0.5

1.0

1.5

2.0

2.5

0.0

0.5

1.0

1.5

2.0

2.5

2001 2004 2007 2010 2013 2016

4.9.1 Commercial Paper OutstandingTrillions of US$ Trillions of US$As Of: 25-Oct-2017

Domestic FinancialDomestic NonfinancialForeign Financial

Asset-Backed

OtherForeign Nonfinancial

Source: Federal ReserveNote: Domestic includes CP issued in the U.S. by entities with foreign parents.

0.0

0.3

0.6

0.9

1.2

1.5

0.0

0.3

0.6

0.9

1.2

1.5

Jan:15 Jul:15 Jan:16 Jul:16 Jan:17 Jul:17

4.9.2 Commercial Paper Interest RatesPercent PercentAs Of: 31-Oct-2017

90-Day AA-Rated ABCP90-Day AA-Rated Financial90-Day AA-Rated NonfinancialOvernight AA-Rated ABCPOvernight AA-Rated FinancialOvernight AA-Rated Nonfinancial

Source: Federal Reserve Bank of St. Louis

0

1

2

3

4

5

0

1

2

3

4

5

2000 2003 2006 2009 2012 2015

4.9.3 Primary Dealer Repo AgreementsTrillions of US$ Trillions of US$As Of: 25-Oct-2017

Source: FRBNY

Overnight/ContinuingTerm

1.0

1.2

1.4

1.6

1.8

2.0

1.0

1.2

1.4

1.6

1.8

2.0

2011 2012 2013 2014 2015 2016 2017

4.9.4 Value of the Tri-Party Repo MarketTrillions of US$ Trillions of US$

Source: FRBNY, Haver Analytics

As Of: Oct-2017

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2011 2012 2013 2014 2015 2016 2017

4.9.5 Collateral in the Tri-Party Repo MarketTrillions of US$ Trillions of US$

Source: FRBNY, Haver Analytics

As Of: Oct-2017

Note: Other includes CDOs, international securities, money markets, municipal debt, and whole loans.

U.S. Treasury StripsAgency MBSAgency Debentures and Strips

U.S. Treasuries excluding StripsCorporatesABSPrivate Label CMOs

Equities

OtherAgency CMOs

0

1

2

3

4

5

0

1

2

3

4

5

2008 2010 2012 2014 2016

4.9.6 Value of Securities on LoanTrillions of US$ Trillions of US$

Source: Markit Group Limited

Global Market (including U.S.)

U.S. Market

As Of: 31-Oct-2017

Note: Data is based on a survey of agent-based lenders.

9

10

11

12

13

0

300

600

900

1200

1500

Oct 9, 2015 Nov 10, 2015 Dec 31, 2015

4.9.7 Securities on Loan Against Cash and Noncash CollateralBillions of US$ PercentAs Of: 31-Dec-2015

Cash Collateral (left axis)Noncash Collateral (left axis) Percent of Total Assets

Available for Lending(right axis)

Source: OFR/Federal Reserve/SEC Securities Lending Data Collection Pilot

4.9.8 Securities on Loan by Owner Type

Source: OFR/Federal Reserve/SEC Securities Lending Data Collection Pilot

Investment Firms ($174)

Pension Funds and

Endowments($332)

Governmental Entities ($327)

Insurance Companies

($36)

Other($134)Banks and

Broker-Dealers ($16)

Note: All figures in billions of US$. Averages of data collected on three reporting dates. Other includes securities owners not identified by pilot participants.

As Of: 31-Dec-2015

4.9.9 Securities on Loan by Asset Class

Source: OFR/Federal Reserve/SEC Securities Lending Data Collection Pilot, Markit Group Limited

U.S. Corporate Bonds($62)

U.S. Treasury and AgencySecurities

($302)

U.S. Equities($315)

ForeignSovereign and Supranational

Securities($121)

Foreign Corporate Bonds($17)

Foreign Equities ($156)

Note: All figures in billions of US$. Averages of data collected on three reporting dates. Not Available includes securities that could not be classified.

As Of: 31-Dec-2015

Not Available($46)

4.9.10 Securities Lending Cash Collateral Reinvestment

Money Market Funds(9.3%)

Repo(36.6%)

Money Market Securities(20.1%)

Cash Delivered to Securities

Lender (8.6%)

Liquidity Funds (6.0%)

Short-Term Investment Funds

(6.8%)

Note: Averages of data collected on three reporting dates. Other includes private structured debt, corporate bonds, sovereign bonds, and agency securities.

As Of: 31-Dec-2015

Other(12.6%)

Source: OFR/Federal Reserve/SEC Securities Lending Data Collection Pilot

4.10.1 Normalized Futures Prices

Source: Bloomberg, L.P.

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Jan:14 Jul:14 Jan:15 Jul:15 Jan:16 Jul:16 Jan:17 Jul:17

Index IndexAs Of: 31-Oct-2017

U.S. DollarE-mini S&P 50010-Year Treasury FuturesS&P Commodity Index

Note: 2-Jan-2014 = 1.0.

4.10.2 Market Volatility Indices

Source: Bloomberg, L.P.

0

10

20

30

40

50

60

70

80

0

3

6

9

12

15

Jan:14 Jul:14 Jan:15 Jul:15 Jan:16 Jul:16 Jan:17 Jul:17

Index IndexAs Of: 31-Oct-2017

Treasury VIX (left axis)VIX (right axis)Crude Oil VIX (right axis)

4.10.3 Normalized Futures Exchange Volume

Source: CFTC

0.8

1.0

1.2

1.4

1.6

0.8

1.0

1.2

1.4

1.6

2010 2011 2012 2013 2014 2015 2016

Index IndexAs Of: 2016

New York Mercantile ExchangeICE Futures U.S.Commodity Exchange Inc.Chicago Mercantile ExchangeChicago Board of Trade

4.10.4 Normalized Futures Exchange Open Interest

Source: CFTC

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2010 2011 2012 2013 2014 2015 2016

Index IndexAs Of: 2016

New York Mercantile ExchangeICE Futures U.S.Commodity Exchange Inc.Chicago Mercantile ExchangeChicago Board of Trade

4.10.5 Normalized Futures Exchange Number of Products

Source: CFTC

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2010 2011 2012 2013 2014 2015 2016

Index IndexAs Of: 2016

New York Mercantile ExchangeICE Futures U.S.Commodity Exchange Inc.Chicago Mercantile ExchangeChicago Board of Trade

4.10.6 Automation in Futures Markets

Source: CFTC

40

50

60

70

80

40

50

60

70

80

2012 2013 2014 2015 2016

Percent PercentAs Of: 2016

New York Mercantile ExchangeCommodity Exchange Inc.Chicago Mercantile ExchangeChicago Board of Trade

4.10.7 Automation in Options Markets

Source: CFTC

20

30

40

50

60

70

80

20

30

40

50

60

70

80

2012 2013 2014 2015 2016

Percent PercentAs Of: 2016

New York Mercantile ExchangeCommodity Exchange Inc.Chicago Mercantile ExchangeChicago Board of Trade

0

2

4

6

8

0

2

4

6

8

1998 2001 2004 2007 2010 2013 2016

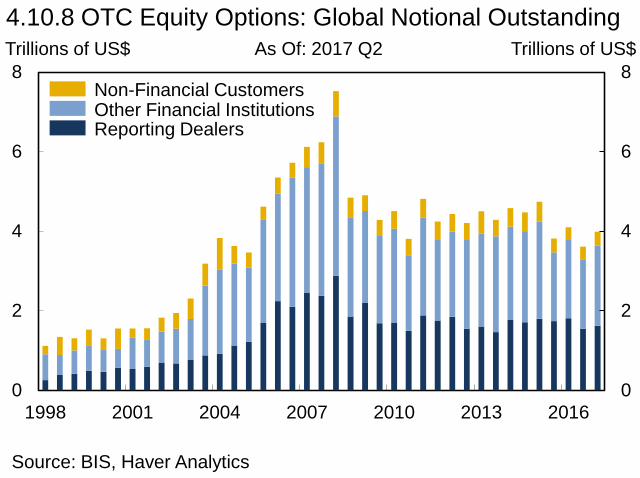

4.10.8 OTC Equity Options: Global Notional OutstandingTrillions of US$ Trillions of US$

Source: BIS, Haver Analytics

As Of: 2017 Q2

Other Financial InstitutionsNon-Financial Customers

Reporting Dealers

As Of: 2017 Q24.10.9 OTC Equity Option Share of All OTC Derivatives

Source: BIS, Haver Analytics

0.0

0.5

1.0

1.5

2.0

0.0

0.5

1.0

1.5

2.0

1998 2001 2004 2007 2010 2013 2016

Percent Percent

0

200

400

600

800

1000

1200

0

200

400

600

800

1000

1200

1998 2001 2004 2007 2010 2013 2016

4.10.10 OTC Equity Options: Global Market ValueBillions of US$ Billions of US$

Source: BIS, Haver Analytics

As Of: 2017 Q2

Other Financial InstitutionsNon-Financial Customers

Reporting Dealers

0

100

200

300

400

0

2

4

6

8

10

Jan:14 Jul:14 Jan:15 Jul:15 Jan:16 Jul:16 Jan:17 Jul:17

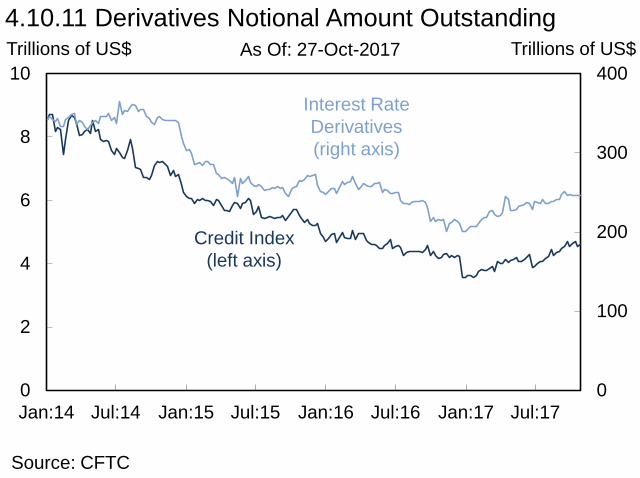

4.10.11 Derivatives Notional Amount OutstandingTrillions of US$ Trillions of US$

Source: CFTC

Interest Rate Derivatives(right axis)

Credit Index(left axis)

As Of: 27-Oct-2017

0

1

2

3

4

5

6

7

8

0.0

0.2

0.4

0.6

0.8

1.0

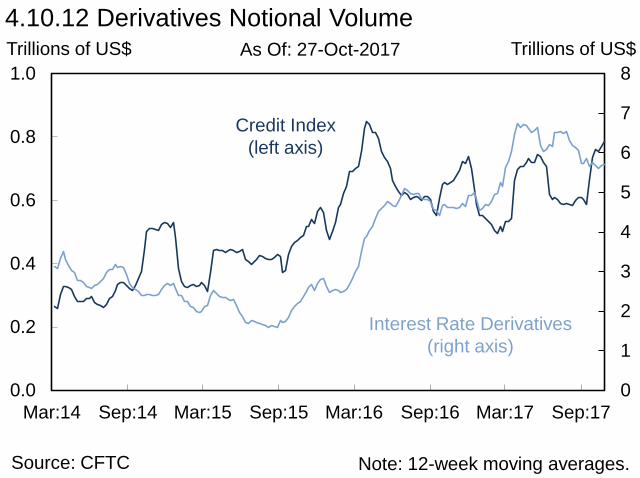

Mar:14 Sep:14 Mar:15 Sep:15 Mar:16 Sep:16 Mar:17 Sep:17

4.10.12 Derivatives Notional VolumeTrillions of US$ Trillions of US$

Source: CFTC

Interest Rate Derivatives(right axis)

As Of: 27-Oct-2017

Note: 12-week moving averages.

Credit Index(left axis)

0

100

200

300

400

500

600

700

800

900

1000

0

100

200

300

400

500

600

700

800

900

1000

2000 2004 2008 2012 2016

Source: BIS, Haver Analytics

As Of: 2017 Q2Trillions of US$4.10.13 Global OTC Derivatives Market

Note: Notional amounts.

Trillions of US$

Unallocated

Interest Rate Contracts

Commodity ContractsCredit Default Swaps

Equity-linked Contracts

FX Contracts

Trillions of US$

0

100

200

300

400

500

600

700

0

100

200

300

400

500

600

700

2012 2013 2014 2015 2016

4.10.14 Interest Rate Derivatives: Global Notional OutstandingTrillions of US$

Source: BIS, Haver Analytics

As Of: 2017 Q2

Q4 Q4 Q4 Q4 Q4

Trillions of US$

0

50

100

150

200

250

0

50

100

150

200

250

2003 2005 2007 2009 2011 2013 2015 2017

CCPNon-CCP

4.10.15 Interest Rate Derivative Compression VolumeTrillions of US$

Source: TriOptima

As Of: Oct-2017

Note: Gross notional is represented as single-counted for notional compressed outside of a CCP and double-counted for notional compressed inside of a CCP.

Trillions of US$4.10.16 Global Cleared OTC Interest Rate Derivatives

Trillions of US$

Source: ClarusFT CCPView, TriOptima, LCH.SwapClear

As Of: Oct-2017

Note: Maturity weighted cumulative compression volume is calculated as the sum of the current and previous year’s compression volume, estimating with two year average maturity for the compressed trades. 2017 data is year-to-date.

0

200

400

600

800

0

200

400

600

800

2008 2010 2012 2014 2016

Cleared NotionalMaturity Weighted Cum. Compression Volume

Trillions of US$4.10.17 Credit Derivatives by Counterparty

Trillions of US$As Of: Oct-2017

0

5

10

15

20

25

0

5

10

15

20

25

2013 2014 2015 2016 2017

Dealer to Non-DealerNon-Dealer to Non-DealerCCP to Dealer

Interdealer

CCP to Non-Dealer

YTDNote: Gross notional outstanding.Source: DTCC

Trillions of US$

0

10

20

30

40

0

10

20

30

40

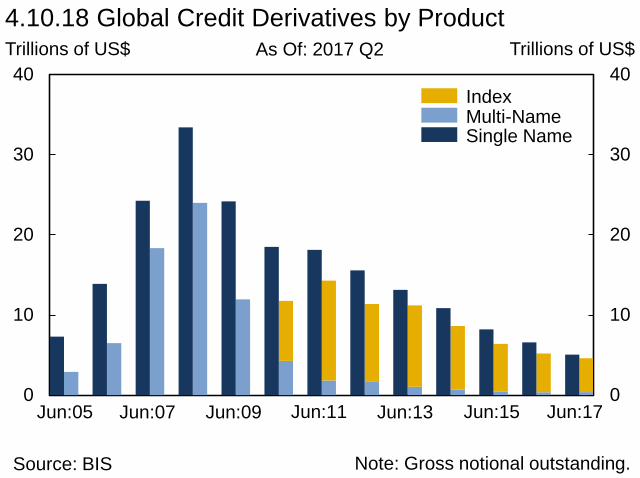

Jun:05 Jun:07 Jun:09 Jun:11 Jun:13 Jun:15 Jun:17

4.10.18 Global Credit Derivatives by ProductTrillions of US$

Source: BIS

As Of: 2017 Q2

Note: Gross notional outstanding.

Multi-NameIndex

Single Name

0

10

20

30

40

0

400

800

1200

1600

Jul:15 Jan:16 Jul:16 Jan:17 Jul:17

4.10.19 Interest Rate Derivatives Inflation Swap ClearingBillions of US$ Billions of US$

Cleared Volume

(right axis)

Cleared Notional Outstanding

(left axis)

As Of: 27-Oct-2017

Uncleared Swap Margin Rule Implementation Date

Source: ClarusFT CCPViewNote: 12-week moving averages for volume data.

0

50

100

150

0

300

600

900

Jul:15 Jan:16 Jul:16 Jan:17 Jul:17

4.10.20 FX Non-Deliverable-Forward ClearingBillions of US$ Billions of US$

Cleared Volume

(right axis)

Cleared Notional Outstanding

(left axis)

As Of: 27-Oct-2017

Uncleared Swap Margin Rule Implementation Date

Source: ClarusFT CCPViewNote: 12-week moving averages for volume data.

0

100

200

300

400

500

0.0

0.2

0.4

0.6

0.8

1.0

IRD FX Credit Equity

Not Cleared (left axis)Cleared (left axis)

4.10.21 Global OTC Central Clearing Market ShareShare Trillions of US$

Source: BIS

As Of: Jun-2017

Total Notional Outstanding (right axis)

Percent As Of: 2017 Q34.10.22 U.S. Central Clearing Market Share

Source: CFTC

0

20

40

60

80

100

0

20

40

60

80

100

Dec:13 Jun:14 Dec:14 Jun:15 Dec:15 Jun:16 Dec:16 Jun:17

Percent

Cleared Interest Rate Derivatives

Note: Percentage of transaction dollar volume.

Cleared CDS Index Swaps

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

350

2002 2004 2006 2008 2010 2012 2014 2016

4.10.23 Margin Funds Held at FCMsBillions of US$ Billions of US$

Source: CFTC, FIA

Part 30Swaps

Futures

As Of: Sep-2017

Count As Of: Sep-20174.10.24 FCMs Holding Client Funds

Source: CFTC, FIA

0

25

50

75

100

125

150

0

25

50

75

100

125

150

2002 2004 2006 2008 2010 2012 2014 2016

Count

SwapsPart 30Futures

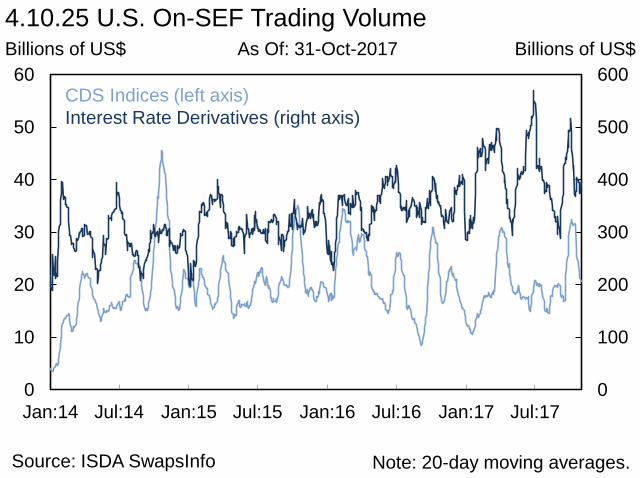

Billions of US$ As Of: 31-Oct-20174.10.25 U.S. On-SEF Trading Volume

Source: ISDA SwapsInfo

0

100

200

300

400

500

600

0

10

20

30

40

50

60

Jan:14 Jul:14 Jan:15 Jul:15 Jan:16 Jul:16 Jan:17 Jul:17

Billions of US$

CDS Indices (left axis)Interest Rate Derivatives (right axis)

Note: 20-day moving averages.

Percent As Of: 31-Oct-20174.10.26 U.S. On-SEF Trading Share

Source: ISDA SwapsInfo

0

20

40

60

80

100

0

20

40

60

80

100

Jan:14 Jul:14 Jan:15 Jul:15 Jan:16 Jul:16 Jan:17 Jul:17

Percent

CDS IndicesInterest Rate Derivatives

Note: Share of notional volume. 20-day moving averages.

0

4

8

12

16

0

4

8

12

16

CCAR banks Other banks withassets greater than

$10B

Banks with assetsless than $10B

4.11.1 BHC Total AssetsTrillions of US$ Trillions of US$

Source: FR Y-9C

As Of: 2017 Q2

4

6

8

10

12

14

4

6

8

10

12

14

2001 2003 2005 2007 2009 2011 2013 2015 2017

4.11.2 Common Equity Tier 1 RatiosPercent PercentAs Of: 2017 Q2

Greater than $50B

Less than $50B

Source: FR Y-9C

Note: Prior to 2014:Q1, the numerator of the common equity tier 1 ratio is tier 1 common capital. Beginning in 2014:Q1 for advanced approaches BHCs and in 2015:Q1 for all other BHCs, the numerator is common equity tier 1 capital.

0

10

20

30

40

50

60

0

10

20

30

40

50

60

2001 2003 2005 2007 2009 2011 2013 2015 2017

4.11.3 Selected Sources of Funding at CCAR BanksPercent of Total Assets Percent of Total AssetsAs Of: 2017 Q2

Long-Term FundingDeposits Excluding Foreign Deposits and Large Time Deposits

Source: FR Y-9C

Note: Long-term funding includes other borrowed money, subordinated notes, and large time deposits with maturities >1 year. Short-term funding includes such liabilities with maturities <1 year plus trading liabilities, repos, CP, and foreign deposits.

Short-Term Funding

0

50

100

150

200

250

0

50

100

150

200

250

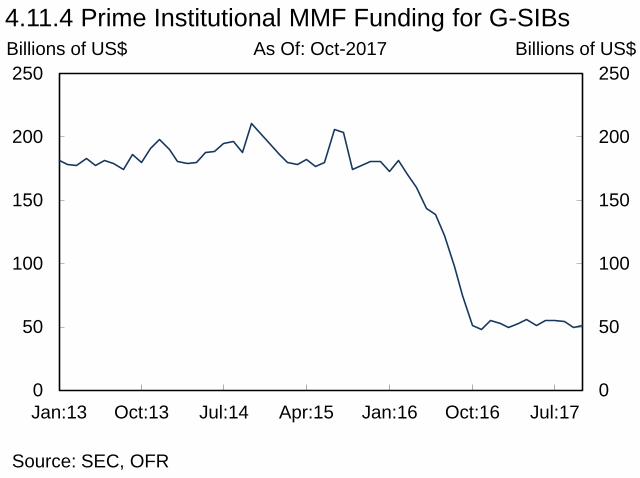

Jan:13 Oct:13 Jul:14 Apr:15 Jan:16 Oct:16 Jul:17

4.11.4 Prime Institutional MMF Funding for G-SIBsBillions of US$ Billions of US$

Source: SEC, OFR

As Of: Oct-2017

-125

-100

-75

-50

-25

0

25

50

-125

-100

-75

-50

-25

0

25

50

2013 2014 2015 2016 2017

4.11.5 LIBOR and Deposit Rate Spreads to OISBasis Points Basis PointsAs Of: 30-Oct-2017

Source: FDIC, Federal Reserve Bank of St. Louis, Bloomberg, L.P.

Small Retail CD SpreadJumbo Retail CD SpreadLIBOR-OIS Spread

Note: 3-month CD and LIBOR spreads to OIS.

-30

-15

0

15

30

-2

-1

0

1

2

1997 2000 2003 2006 2009 2012 2015

4.11.6 Return on Equity and Return on AssetsPercent PercentAs Of: 2017 Q2

ROE (right axis)

ROA (left axis)

Source: FR Y-9C

Note: Return on equity is equal to net income divided by average equity. Return on assets is equal to net income divided by average assets.

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2000 2003 2006 2009 2012 2015

4.11.7 Net Interest MarginsPercent PercentAs Of: 2017 Q2

Greater than $50B

Less than $50B

Source: FR Y-9C

Note: Net interest margin is equal to net interest income divided by the quarterly average of interest-earning assets.

0

2

4

6

8

10

12

14

0

2

4

6

8

10

12

14

2011 2012 2013 2014 2015 2016 2017

4.11.8 Legal Expenses at Largest BHCsBillions of US$ Billions of US$As Of: 2017 Q2

Note: Legal expenses includes litigation expense and legal fees and expenses. Includes legal expenses at BAC, C, GS, JPM, MS, and WFC.Source: FR Y-9C

0

2

4

6

8

0

2

4

6

8

1997 2000 2003 2006 2009 2012 2015

Greater than $50B

4.11.9 Non-Performing LoansPercent of Total Loans Percent of Total LoansAs Of: 2017 Q2

Less than $50B

Source: FR Y-9C

0

50

100

150

200

250

0

50

100

150

200

250

1997 2000 2003 2006 2009 2012 2015

4.11.10 Loan-Loss ReservesPercent of NPLs Percent of NPLsAs Of: 2017 Q2

Less than $50B

Greater than $50B

Source: FR Y-9C

0

10

20

30

40

50

0

10

20

30

40

50

2001 2003 2005 2007 2009 2011 2013 2015 2017

4.11.11 Higher-Risk SecuritiesPercent of Total Securities Percent of Total Securities

Source: FR Y-9C

As Of: 2017 Q2

Greater than $50B

Less than $50B

0

1

2

3

4

5

6

0

1

2

3

4

5

6

2010 2011 2012 2013 2014 2015 2016 2017

4.11.12 Loans to Nondepository Financial Institutions Percent of Total Loans Percent of Total LoansAs Of: 2017 Q2

Greater than $50B

Less than $50B

Source: FR Y-9C

4

8

12

16

20

24

4

8

12

16

20

24

2010 2011 2012 2013 2014 2015 2016 2017

4.11.13 Selected High-Quality Liquid Assets at BHCsPercent of Assets Percent of Assets

Source: FR Y-9C, FR 2900

As Of: 2017 Q2

Standard LCR BHCs

Note: HQLA is estimated by adding excess reserves to an estimate of securities that qualify for HQLA. Securities are estimated from the FR Y-9C. Haircuts and level 2 asset limitations are incorporated into the estimate.

Modified LCR BHCsOther

0

2

4

6

8

10

0

2

4

6

8

10

2010 2011 2012 2013 2014 2015 2016 2017

4.11.14 Selected Liquid Assets at Standard LCR BHCsPercent of Assets Percent of Assets

Source: FR Y-9C, FR 2900

As Of: 2017 Q2

Reserves

Treasury Securities

Fannie Mae and Freddie Mac MBS

4.11.15 Weighted-Average Duration Gap

Source: FR Y-9C

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2001 2003 2005 2007 2009 2011 2013 2015 2017

Years Years

Between $50B and $250B

As Of: 2017 Q2

Less than $50B

Greater than $250B

Note: Duration gap is the approximate weighted-average time of cash inflows less the approximate weighted-average time of cash outflows.

4.11.16 P/B and P/E Ratios of Six Large Complex BHCs

Source: Bloomberg, L.P.

0

10

20

30

40

50

60

0

1

2

3

4

5

2000 2003 2006 2009 2012 2015

Ratio RatioAs Of: 31-Oct-2017

P/B Ratio (left axis) P/E Ratio

(right axis)

Note: Market cap-weighted average of BAC, C, GS, JPM, MS, and WFC.

Basis Points

0

100

200

300

400

500

600

700

0

100

200

300

400

500

600

700

2009 2010 2011 2012 2013 2014 2015 2016 2017

4.11.17 CDS Spreads of Six Large Complex BHCsBasis PointsAs Of: 31-Oct-2017

Source: Markit Group LimitedNote: CDS spreads of BAC, C, GS, JPM, MS, and WFC.

Maximum ValueEqual-Weighted AverageMinimum Value

0

2

4

6

8

10

12

14

0

2

4

6

8

10

12

14Pre-StressPost-Stress Minimum

4.11.18 Initial and Stressed Tier 1 Common Capital RatiosPercent Percent

Source: Federal Reserve

As Of: Jun-2017

Note: DFAST 2013-2015 bars depict Tier 1 Common Capital Ratio. DFAST 2016-2017 bars depict Common Equity Tier 1 Ratio.

DFAST 2013 2014 2015 2016 2017

4.11.19 Federal Reserve's Actions in CCAR 2016

Source: Federal Reserve

Non-Objection to Capital PlanAlly Financial Citizens Financial MUFG AmericasAmerican Express Comerica Northern TrustBancWest Discover Financial PNC FinancialBank of America Fifth Third Bancorp Regions FinancialBank of New York Mellon Goldman Sachs State StreetBB&T HSBC North America SunTrustBBVA Compass Huntington Bancshares TD Group U.S.BMO Financial JPMorgan Chase U.S. BancorpCapital One Financial KeyCorp Wells FargoCitigroup M&T Bank Zions

Conditional Non-Objection to Capital PlanMorgan Stanley

Objection to Capital PlanDeutsche Bank Santander Holdings USA

Note: Morgan Stanley’s capital plan received a non-objection upon resubmission.

4.11.20 Federal Reserve's Actions in CCAR 2017

Source: Federal Reserve

Non-Objection to Capital PlanAlly Financial Comerica MUFG AmericasAmerican Express Deutsche Bank Northern TrustBancWest Discover Financial PNC FinancialBank of America Fifth Third Bancorp Regions FinancialBank of New York Mellon Goldman Sachs Santander Holdings USABB&T HSBC North America State StreetBBVA Compass Huntington Bancshares SunTrustBMO Financial JPMorgan Chase TD Group U.S.CIT Group KeyCorp U.S. BancorpCitigroup M&T Bank Wells FargoCitizens Financial Morgan Stanley Zions

Conditional Non-Objection to Capital PlanCapital One Financial

0

1

2

3

4

5

0

100

200

300

400

500

600

1980 1985 1990 1995 2000 2005 2010 2015

Source: BEA, FDIC, Haver Analytics

As Of: 2017 Q2Number of Institutions4.11.21 FDIC-Insured Failed Institutions

Note: No FDIC-insured institutions failed during 2005 and 2006. Failed institutions in 2017 through June 30.

Percent

Number of Institutions (left axis)

Assets of Failed Institutions as a Percent

of Nominal GDP (right axis)

-1000

-750

-500

-250

0

250

500

750

1000

-1000

-750

-500

-250

0

250

500

750

1000

2009 2011 2013 2015 2017

Noninterest IncomeNet Interest Income

Noninterest ExpenseProvisions

4.11.22 Commercial Bank and Thrift Pre-Tax IncomeBillions of US$ Billions of US$

Source: FDICNote: Includes all FDIC-insured commercial banks and thrifts.

As Of: 2017 Q2

Total Pre-Tax Income

Realized Gains/Losses on Investments

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2004 2006 2008 2010 2012 2014 2016Source: Federal Reserve, Haver Analytics

As Of: 2017 Q2Trillions of US$

4.11.23 U.S. Branches and Agencies of Foreign Banks: Assets

Note: Other assets includes government securities, asset-backed securities, and other trading assets.

Trillions of US$

Cash and Balances Due from Depository Institutions (excluding Reserve Balances)Non-C&I Loans

C&I LoansNet Due From Related Depository Institutions

Reserve Balances

Other Assets

Securities Purchased with Repos & Fed Funds Sold

0.0

0.2

0.4

0.6

0.8

0.6

0.8

1.0

1.2

1.4

1.6

2013 2014 2015 2016 2017

4.11.24 Cash Assets and Net Due to Related EntitiesTrillions of US$ Trillions of US$

Source: Federal Reserve

As Of: 25-Oct-2017

Cash Assets (left axis)

Net Due to Related Entities(right axis)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2004 2006 2008 2010 2012 2014 2016Source: Federal Reserve, Haver Analytics

As Of: 2017 Q2Trillions of US$

4.11.25 U.S. Branches and Agencies of Foreign Banks: Liabilities

Note: Other liabilities includes transaction accounts, non-transaction accounts, and other borrowed money.

Trillions of US$

Deposits & Credit BalancesNet Due to Related Depository Institutions

Other LiabilitiesSecurities Sold with Repos & Fed Funds Purchased

-60

-45

-30

-15

0

15

30

45

60

-60

-45

-30

-15

0

15

30

45

60

2007 2009 2011 2013 2015 2017

Net Income

4.11.26 Credit Union IncomeBillions of US$ Billions of US$

Source: NCUA

As Of: 2017 Q2

Noninterest IncomeNet Interest Income

Note: Federally-insured credit unions.

Noninterest ExpenseProvisions Realized Gains/Losses

on Investments

45

50

55

60

65

20

24

28

32

36

2005 2007 2009 2011 2013 2015 2017

4.11.27 Credit Union DepositsPercent Percent

Source: NCUA

As Of: 2017 Q2

Money Market and IRA Deposit Share

(left axis)

Interest-Sensitive Deposit Share

(right axis)

Note: Federally-insured credit unions. Interest-sensitive deposit share includes money market and IRA deposit share, share certificates, and certain other deposits.

0

10

20

30

40

50

0

10

20

30

40

50

2005 2007 2009 2011 2013 2015 2017

4.11.28 Credit Union Net Long-Term AssetsPercent of Total Assets Percent of Total Assets

Source: NCUA

As Of: 2017 Q2

Mortgage Loans Maturing in 5+ Years

Long-Term InvestmentsBusiness LoansFixed Assets

Note: Federally-insured credit unions. Long-term investments mature in three or more years.

0

5

10

15

20

25

30

35

0

5

10

15

20

25

30

35

2007 Q2 2013 Q2 2015 Q2 2017 Q2

4.11.29 Credit Union Investments by MaturityPercent of Total Assets Percent of Total Assets

Source: NCUA

As Of: 2017 Q2

1-3 Years3-5 Years

5-10 Years<1 Year

>10 Years

Note: Federally-insured credit unions. Investments <1 year exclude securities with maturities <3 months.

0

10

20

30

40

50

3000

3500

4000

4500

5000

2009 2010 2011 2012 2013 2014 2015 2016

4.12.1 Number of Broker-Dealers and Industry Net Income Number of Firms Billions of US$As Of: 2016

Source: FINRA

Net Income (right axis)Number of Broker-Dealers (left axis)

0

100

200

300

400

0

100

200

300

400

2009 2010 2011 2012 2013 2014 2015 2016

Sale of Investment Company Shares

Margin InterestOther

Underwriting

Fees – Supervision, Advisory, Administration

Commissions

4.12.2 Broker-Dealer RevenuesBillions of US$ Billions of US$

Source: FINRA

As Of: 2016

0

1

2

3

4

5

6

7

2005 2007 2009 2011 2013 2015 20170

8

16

24

32

40

4.12.3 Broker-Dealer Assets and LeverageTrillions of US$ Ratio

Source: FINRA

As Of: 2017 Q2

Note: Leverage is the ratio of total assets to total ownership equity. 2017 data as of second quarter 2017.

Total Assets (left axis)

Leverage (right axis)

15

20

25

30

35

40

0

1

2

3

4

5

2010 2011 2012 2013 2014 2015 2016 2017

4.12.4 Large Broker-Dealer Assets and Leverage by AffiliationTrillions of US$ Ratio

Source: FINRA

As Of: 2017 Q2

Note: Data covers BHC- and FBO-affiliated broker-dealers that are among the 25 largest broker-dealers by assets as of second quarter 2017.

BHC-Affiliated Assets (left axis)FBO-Affiliated Assets (left axis)

BHC-Affiliated Leverage (right axis)FBO-Affiliated Leverage (right axis)

0

15

30

45

60

75

0

15

30

45

60

75

2010 2011 2012 2013 2014 2015 2016 2017YTD

4.12.5 Insurance Industry Net IncomeBillions of US$ Billions of US$

Source: SNL Financial

As Of: 2017 Q2

LifeP&C

Note: Life includes accident and health.

2

3

4

5

6

2010 2011 2012 2013 2014 2015 2016 20172

3

4

5

6

4.12.6 Net Yield on Invested AssetsPercent Percent

Source: SNL Financial, Bank of America Merrill Lynch, Haver Analytics

Life

P&C

Yield on A-Rated Corporate Debt

As Of: 2017 Q2

Note: Life includes accident and health.

0

250

500

750

1000

2010 2011 2012 2013 2014 2015 2016 2017YTD

0

10

20

30

40

50

60

4.12.7 Insurance Industry Capital and SurplusBillions of US$ Percent of Total Assets

Life Capital and Surplus / Assets (right axis)P&C Capital and Surplus / Assets (right axis)Life Capital and Surplus (left axis)P&C Capital and Surplus (left axis)

As Of: 2017 Q2

Note: C&S/Assets is calculated as capital and surplus as a percent of net admitted assets less net admitted separate account assets. Life includes accident and health.Source: SNL Financial

0.0

0.5

1.0

1.5

2.0

2.5

0.0

0.5

1.0

1.5

2.0

2.5

2001 2004 2007 2010 2013 2016

Source: Federal Reserve, Haver Analytics

As Of: Oct-2017Trillions of US$4.12.8 Consumer Loans and Leases Outstanding

Note: Loans and leases owned and securitized. Series breaks in December 2010 and 2014 due to change in data collection methodology. Gray bars signify NBER recessions.

Trillions of US$

Commercial Banks

Finance Companies

0.0

0.5

1.0

1.5

2.0

2.5

0.0

0.5

1.0

1.5

2.0

2.5

2001 2004 2007 2010 2013 2016

Source: Federal Reserve, Haver Analytics

As Of: Oct-2017Trillions of US$4.12.9 Business Loans and Leases Outstanding

Trillions of US$

Commercial Banks

Finance Companies

Note: Loans and leases owned and securitized. Series break in December 2010 due to change in data collection methodology. Gray bars signify NBER recessions.

0

50

100

150

200

250

300

350

400

450

0

50

100

150

200

250

300

350

400

450

2008 2010 2012 2014 2016

4.12.10 ABS IssuanceBillions of US$ Billions of US$

Source: Thomson Reuters, SIFMA

As Of: Oct-2017

Credit CardCDO

Auto

Student LoansOther

Equipment

Note: 2017 data is year-to-date.Note: 2017 data is year-to-date.

0

50

100

150

200

250

300

0

50

100

150

200

250

300

2010 2011 2012 2013 2014 2015 2016 2017

4.12.11 Selected ABS SpreadsBasis Points Basis Points

Source: J.P. Morgan

Prime Auto Fixed BBB 3-YearCredit Card Fixed BBB 3-YearPrime Auto Fixed AAA 3-YearCredit Card Fixed AAA 3-Year

As Of: 31-Oct-2017

Note: Spreads to swaps.

As Of: 2017 Q2

0

100

200

300

400

500

0

3

6

9

12

15

18

2000 2003 2006 2009 2012 2015

4.12.12 Agency REIT Assets and LeverageRatio Billions of US$

Source: Bloomberg, L.P.

Leverage(left axis)

Total Assets (right axis)

Note: Leverage is the ratio of total assets to equity. Not all agency REITs existed in all time periods in the figure.

0.0

0.5

1.0

1.5

2.0

0.0

0.5

1.0

1.5

2.0

2000 2003 2006 2009 2012 2015

4.12.13 Agency REIT Price-to-Book RatioRatio Ratio

Source: Bloomberg, L.P.

As Of: 2017 Q2

Note: Price-to-book ratio is weighted by market capitalization. Not all agency REITs existed in all time periods in the figure.

0

1

2

3

4

0

1

2

3

4

2011 2012 2013 2014 2015 2016 2017

C.1 MMF Assets by Fund TypeTrillions of US$ Trillions of US$

Source: SEC

As Of: Oct-2017

PrimeGovernment and TreasuryTax-Exempt

0

100

200

300

400

500

0

100

200

300

400

500

Jan:16 Apr:16 Jul:16 Oct:16 Jan:17 Apr:17

Billions of US$ Billions of US$

Source: FRBNY

As Of: 30-Jun-2017C.2 ON RRP Take-Up by MMFs

20

30

40

50

60

70

20

30

40

50

60

70

2011 2012 2013 2014 2015 2016 2017

C.3 Liquid Asset Shares of Prime MMFsPercent of Total Assets Percent of Total Assets

Source: SEC

As Of: Oct-2017

Daily Liquidity

Weekly Liquidity

Note: Weighted by fund size.

0

10

20

30

40

50

0

10

20

30

40

50

Jan:16 Apr:16 Jul:16 Oct:16 Jan:17 Apr:17 Jul:17 Oct:17

Basis Points Basis Points

Source: Bloomberg L.P.

As Of: 31-Oct-2017C.4 LIBOR-OIS Spread

0

5

10

15

20

25

0

5

10

15

20

25

1996 1999 2002 2005 2008 2011 2014 2017YTD

4.13.1 Net Assets of the Investment Company IndustryTrillions of US$ Trillions of US$As Of: 2017 Q3

ETFsOther

Equity Mutual FundsBond/Hybrid Mutual FundsMMFs

Note: Other is composed of unit investment trusts and closed-end funds. 2017 YTD figures include 2016 UIT data, which is reported annually. Source: ICI, Haver Analytics

-80

-60

-40

-20

0

20

40

-80

-60

-40

-20

0

20

40

2013 2014 2015 2016 2017

Source: ICI, Haver Analytics

As Of: Sep-2017Billions of US$4.13.2 Monthly Bond Mutual Fund Flows

Billions of US$

Tax-ExemptTaxable

-40

-30

-20

-10

0

10

20

30

40

-40

-30

-20

-10

0

10

20

30

40

2013 2014 2015 2016 2017

Source: ICI, Haver Analytics

As Of: Sep-2017Billions of US$4.13.3 Monthly Equity Mutual Fund Flows

Billions of US$

-30

-15

0

15

30

45

60

75

-30

-15

0

15

30

45

60

75

2005 2007 2009 2011 2013 2015 2017

4.13.4 Bank Loan Mutual Funds: Annual FlowsBillions of US$ Billions of US$

Source: Morningstar, Inc.

As Of: Oct-2017

YTD

-30

-20

-10

0

10

20

30

-30

-20

-10

0

10

20

30

2005 2007 2009 2011 2013 2015 2017

4.13.5 High-Yield Mutual Funds: Annual FlowsBillions of US$ Billions of US$

Source: Morningstar, Inc.

As Of: Oct-2017

YTD

-10

0

10

20

30

40

50

60

-10

0

10

20

30

40

50

60

2005 2007 2009 2011 2013 2015 2017

4.13.6 Alternative Mutual Funds: Annual FlowsBillions of US$ Billions of US$

Source: Morningstar, Inc.

As Of: Oct-2017

YTD

-1.2

-0.8

-0.4

0

0.4

0.8

1.2

-1.2

-0.8

-0.4

0

0.4

0.8

1.2

2009 2010 2011 2012 2013 2014 2015 2016 2017

4.13.7 Cumulative Equity Fund FlowsTrillions of US$ Trillions of US$

Source: Morningstar, Inc.

As Of: Oct-2017

Note: Includes ETFs and mutual funds.

International Passively ManagedU.S. Passively ManagedInternational Actively ManagedU.S. Actively Managed

-0.5

0.5

1.5

2.5

3.5

-0.5

0.5

1.5

2.5

3.5

2009 2010 2011 2012 2013 2014 2015 2016 2017

4.13.8 U.S.-Listed ETP AUMTrillions of US$ Trillions of US$

Source: Morningstar, Inc.

As Of: Oct-2017

Cumulative Flows to ETFsCumulative Market AppreciationAUM

0

4

8

12

16

20

24

28

0

4

8

12

16

20

24

28

2007 2009 2011 2013 2015 2017

Source: Federal Reserve, Haver Analytics

As Of: 2017 Q1Trillions of US$4.13.9 Retirement Fund Assets by Plan Type

Trillions of US$

Private Defined Benefit Plans

Individual AccountsPrivate Defined Contribution Plans

State and LocalFederal

60

70

80

90

100

110

120

60

70

80

90

100

110

120

2002 2004 2006 2008 2010 2012 2014 2016

4.13.10 Public and Private Pension Funding Levels

Source: Public Fund Survey, Milliman 2016 Pension Funding Study

Percent Percent

Public Defined Benefit Plans

Private Defined Benefit Plans

As Of: 2016

0.0

0.4

0.8

1.2

1.6

0.0

0.4

0.8

1.2

1.6

2005 2007 2009 2011 2013 2015 2017

4.13.11 North American Private Equity AUMTrillions of US$ Trillions of US$

Source: Preqin

As Of: 2017 Q1

YTD

Undeployed CapitalExisting Investments

0

50

100

150

200

0

50

100

150

200

2011 2012 2013 2014 2015 2016 2017 YTD

4.13.12 M&A Loan Volume for Private Equity-Backed IssuersBillions of US$ Billions of US$

Source: S&P LCD

As Of: Oct-2017

LBONon-LBO

0

20

40

60

80

100

0

20

40

60

80

100

1989 1993 1997 2001 2005 2009 2013

4.14.1 U.S. Consumer Adoption of Payment InstrumentsPercent of Consumers Percent of ConsumersAs Of: 2014

Source: Federal Reserve Bank of Boston

Note: Survey of Consumer Finances data from 1989 to 2007. Survey of Consumer Payment Choice data from 2008 to 2014.

CashCheckOnline Banking Bill PaymentsChecking AccountCreditDebit