40031-033: Rajasthan Urban Sector Development Investment ...Rajasthan Urban Sector Development...

80

Completion Report Project Number: 40031-033 Loan Number: 2506 June 2019 India: Rajasthan Urban Sector Development Investment Program (Tranche 2) This document is being disclosed to the public in accordance with ADB’s Access to Information Policy.

Transcript of 40031-033: Rajasthan Urban Sector Development Investment ...Rajasthan Urban Sector Development...

Completion Report

Project Number: 40031-033 Loan Number: 2506 June 2019

India: Rajasthan Urban Sector Development

Investment Program (Tranche 2) This document is being disclosed to the public in accordance with ADB’s Access to Information Policy.

CURRENCY EQUIVALENTS

Currency unit – Indian rupee/s (₹)

At Appraisal At Project Completion

13 August 2008 30 June 2017 ₹1.00 = $0.0236 $0.0154 $1.00 = ₹42.375 ₹64.785

ABBREVIATIONS

ADB – Asian Development Bank CAPP – community action and participation program CFC – Central Finance Commissions CTO – consent to operate DMF – design and monitoring framework DSC – design and construction supervision consultant EIRR – economic internal rate of return EMMP – environmental monitoring and management plan GOR – Government of Rajasthan IEE – initial environmental examination IPIU – investment program implementation unit IPMC – investment program management consultant IPMU – investment program management unit IPPMS – investment program performance and management system MFF – multitranche financing facility O&M – operation and maintenance PHED – Public Health Engineering Department PWD – Public Works Department ROB – rail over bridge RUSDIP – Rajasthan Urban Sector Development Project SFC – State Finance Commission SOE – statement of expenditure STP – sewage treatment plant SWM – solid waste management UFW – unaccounted-for water ULB – urban local body WTP – water treatment plant

WEIGHTS AND MEASURES

km – kilometer lpcd – liters per capita per day m – meter mld – million liters per day

NOTES

(i) The fiscal year (FY) of the Government of India ends on 31 March. FY before a calendar year denotes the year in which the fiscal year ends, e.g., FY2019 ends on 31 March 2019.

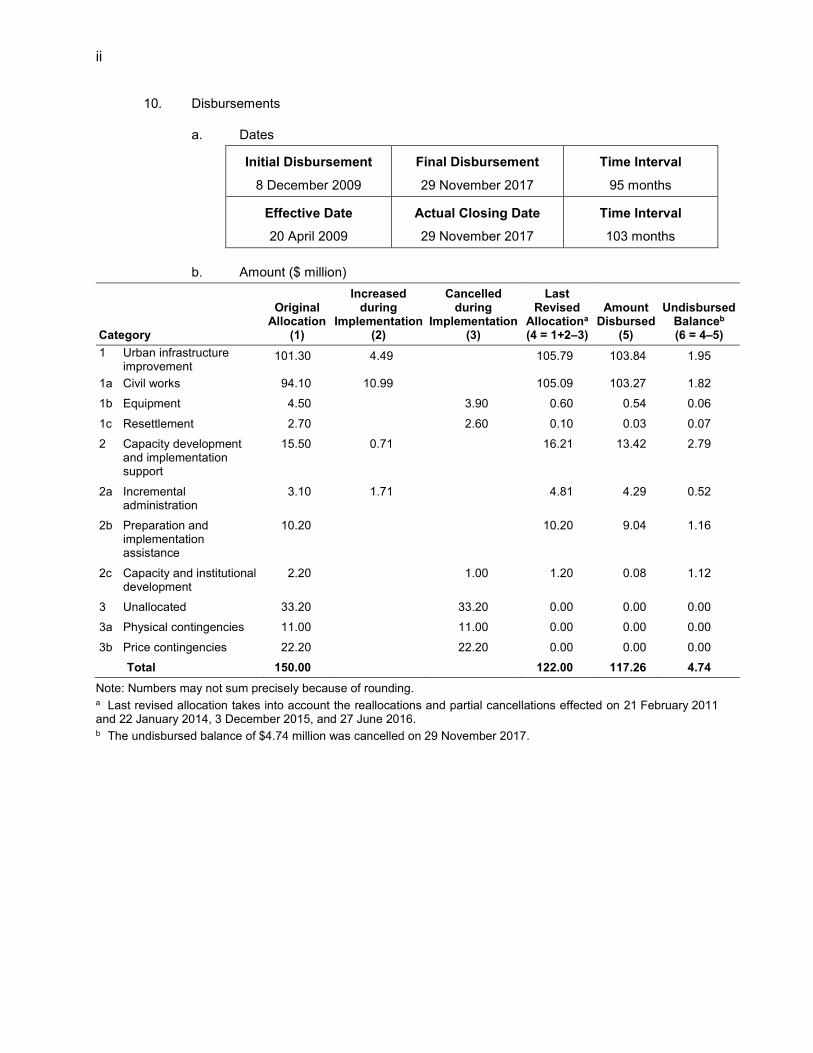

(ii) In this report, “$” refers to United States dollars.

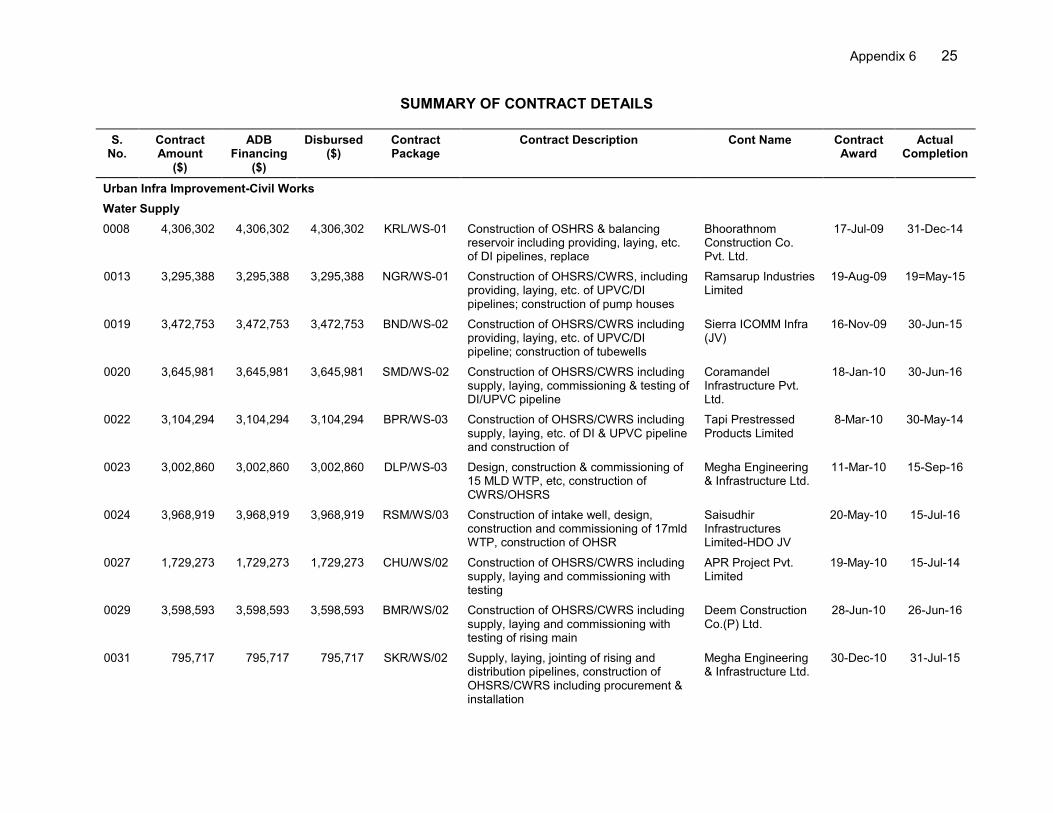

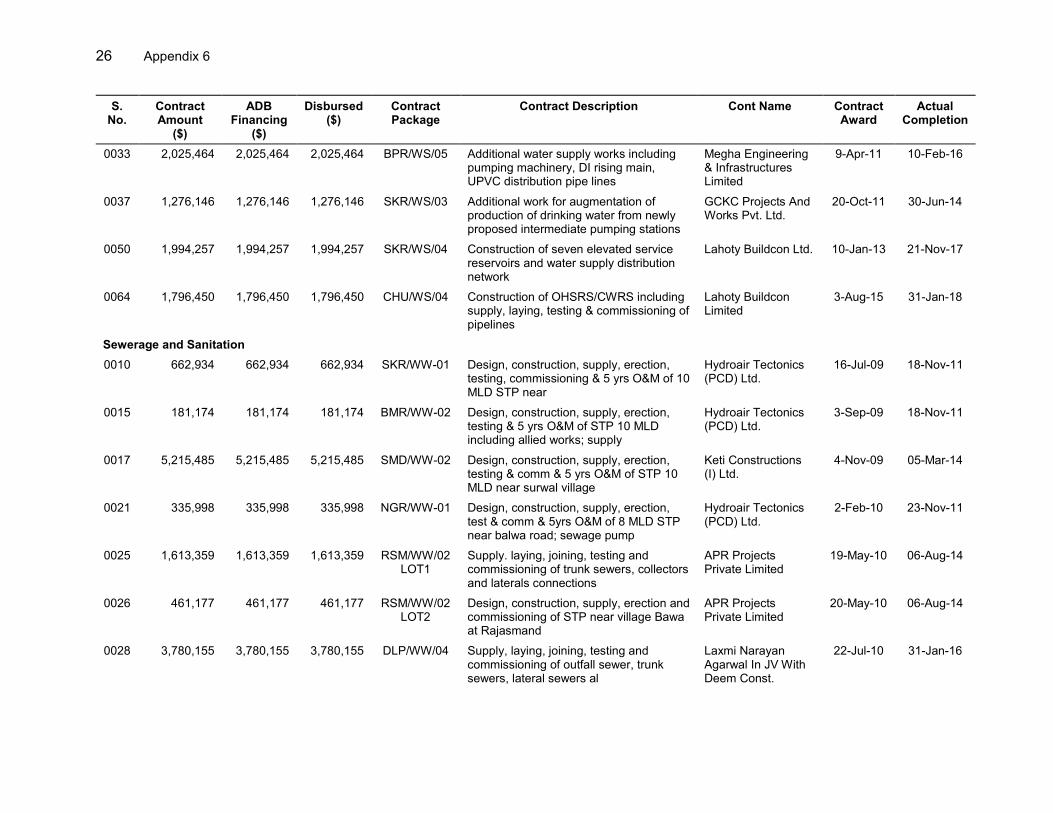

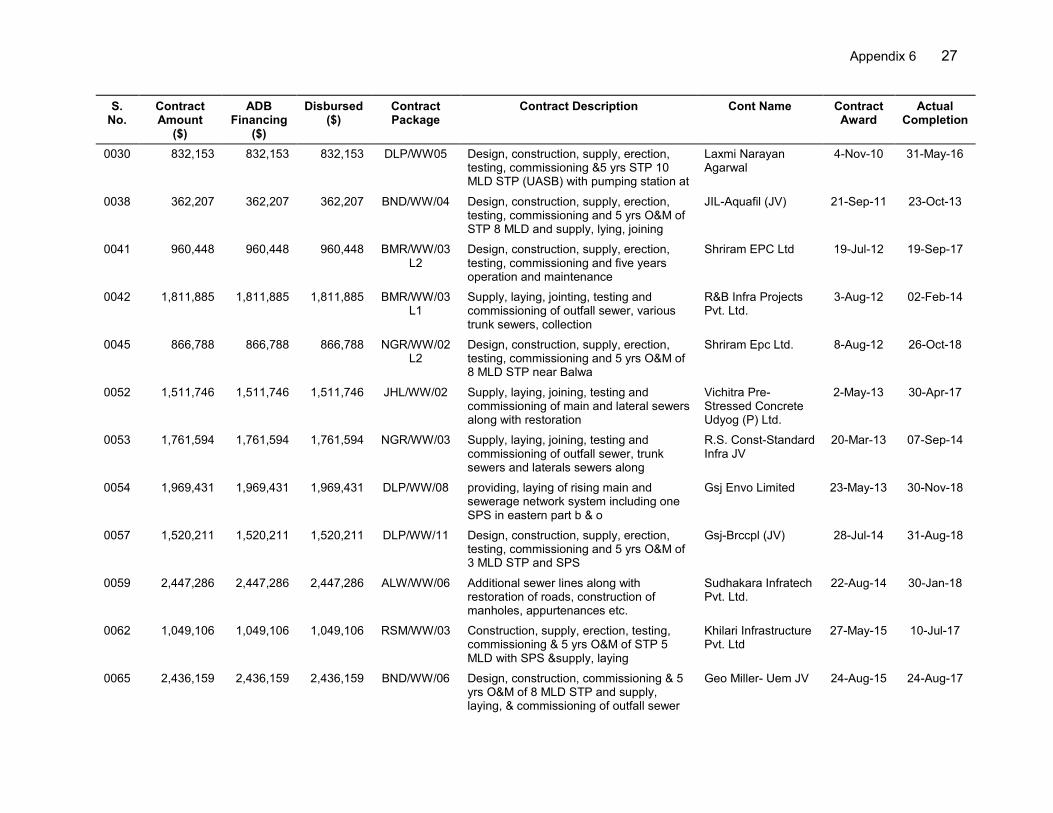

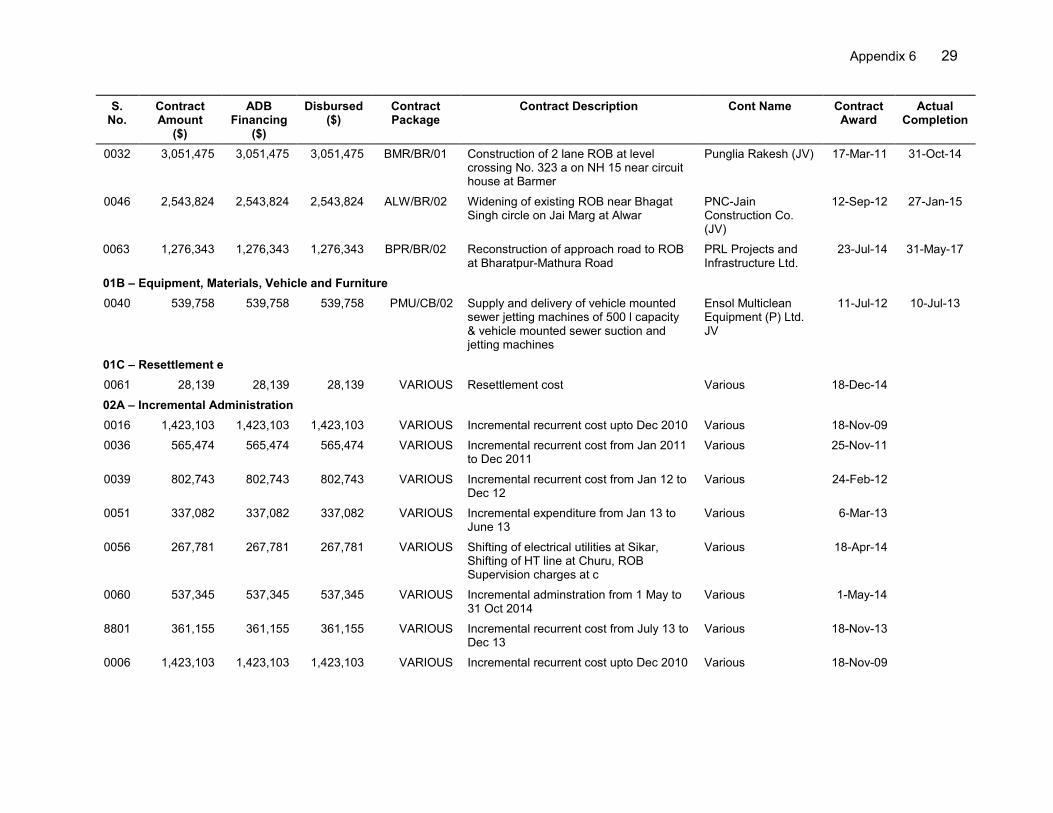

Vice-President Shixin Chen, Operations 1 Director General Hun Kim, South Asia Department (SARD) Director Kenichi Yokoyama, India Resident Mission, SARD Team leader Pushkar Srivastava, Senior Project Officer, SARD Team members Bhawna Kulshreshtha, Executive Assistant, SARD

Girish Mahajan, Senior Environment Officer, SARD Suhail Mircha, Safeguard Officer, SARD

In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area.

CONTENTS Page

BASIC DATA i

I. PROJECT DESCRIPTION 1

II. DESIGN AND IMPLEMENTATION 1 A. Project Design and Formulation 1 B. Project Outputs 3 C. Project Costs and Financing 5 D. Disbursements 5 E. Project Schedule 5 F. Implementation Arrangements 6 G. Consultant Recruitment and Procurement 6 H. Safeguards 7 I. Monitoring and Reporting 7

III. Evaluation of Performance 8 A. Relevance 8 B. Effectiveness 8 C. Efficiency 10 D. Sustainability 10 E. Development Impact 11 F. Performance of the Borrower and the Executing Agency 12 G. Performance of the Asian Development Bank 12 H. Overall Assessment 13

IV. ISSUES, LESSONS, AND RECOMMENDATIONS 13 A. Issues and Lessons 13 B. Recommendations 14

APPENDIXES 1. Design and Monitoring Framework for Project 2 16 2. Project Cost at Appraisal and Actual 21 3. Project Cost by Financier 22 4. Disbursements of ADB Loan Proceeds 23 5. Contract Awards of ADB Loan Proceeds 24 6. Summary of Contract Details 25 7. Safeguards Assessment 31 8. Status of Compliance with Loan Covenants 34 9. Economic and Financial Analysis 43

BASIC DATA A. Loan Identification 1. Country 2. Loan number and financing source 3. Project title 4. Borrower 5. Executing agency 6. Amount of loan 7. Financing modality

India 2506, ordinary capital resources Rajasthan Urban Sector Development Investment Program (Tranche 2) India Local Self Government Department, Government of Rajasthan $150 million Multitranche financing facility

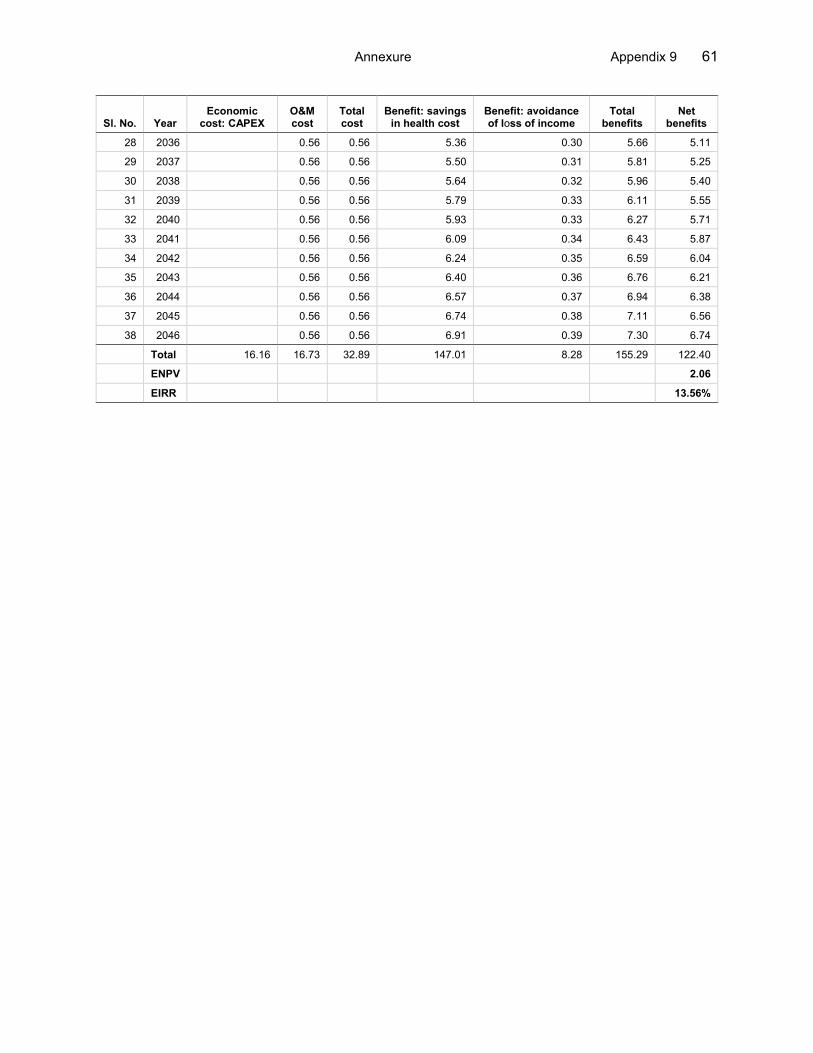

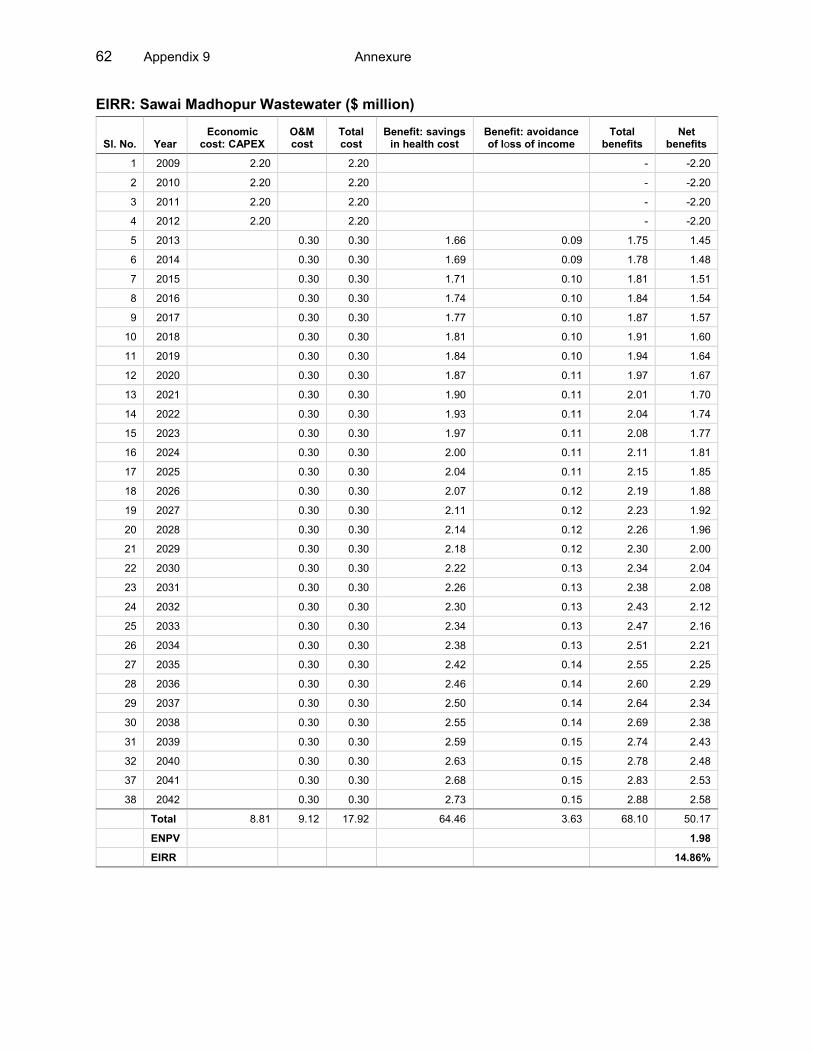

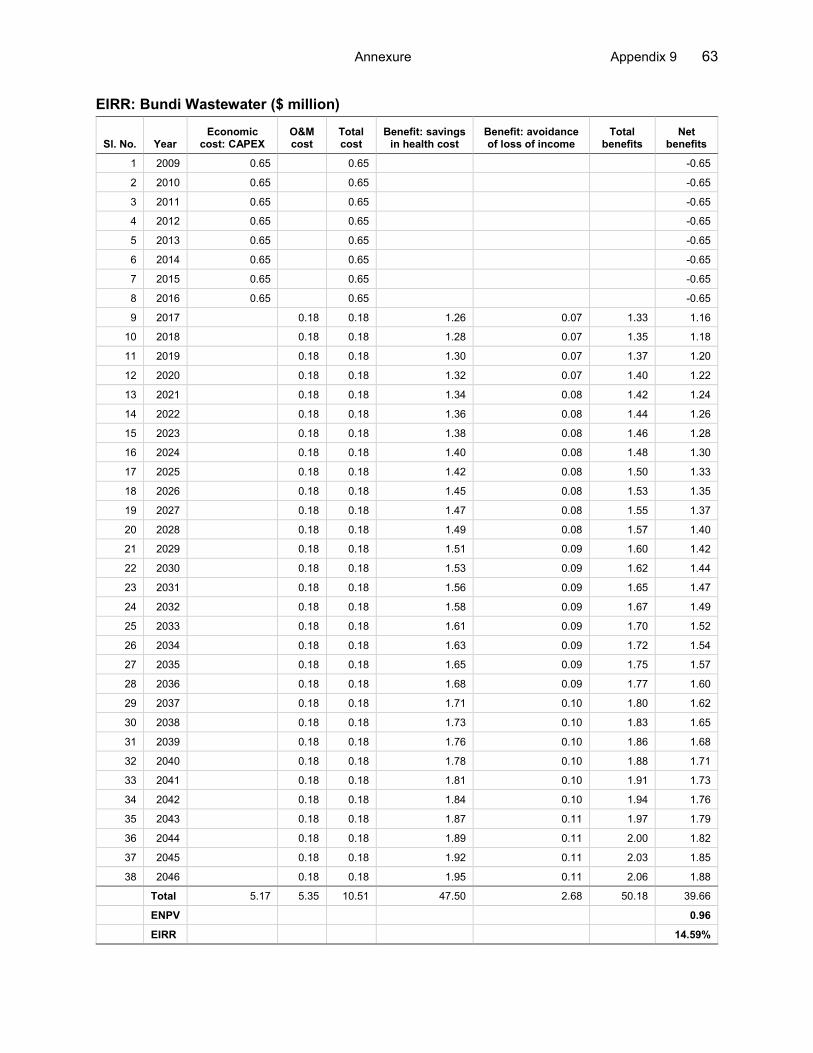

B. Loan Data 1. Appraisal – Date started – Date completed 2. Loan negotiations – Date started – Date completed 3. Date of Board approval 4. Date of loan agreement 5. Date of loan effectiveness – In loan agreement – Actual – Number of extensions 6. Project completion date – Appraisal – Actual 7. Loan closing date – In loan agreement

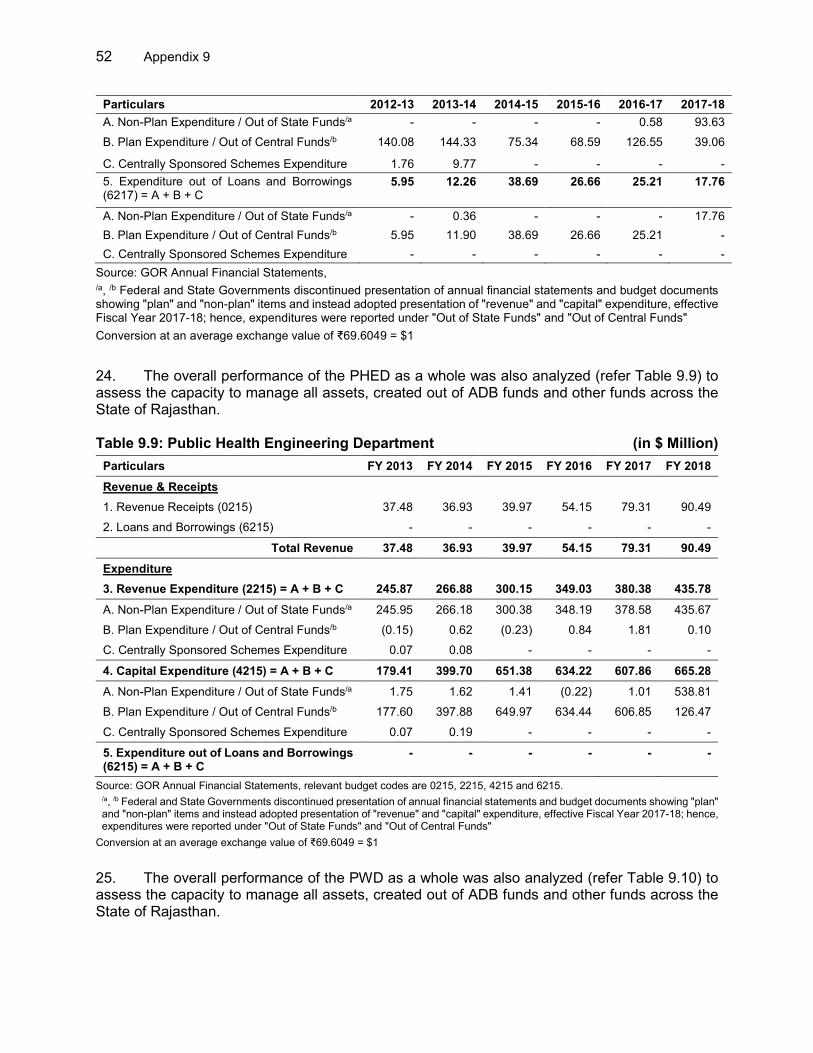

– Actual – Number of extensions 8. Financial closing date – Actual 9. Terms of loan –Interest rate – Maturity (number of years) – Grace period (number of years)

25 July 2008 13 August 2008 2 December 2008 3 December 2008 19 January 2009 18 February 2009 19 May 2009 20 April 2009 None 31 December 2013 30 June 2017 30 June 2014 30 June 2017 4 29 November 2017 London interbank offered rate (LIBOR)-based (floating) + 0.60% 25 5

ii

10. Disbursements

a. Dates

Initial Disbursement

8 December 2009

Final Disbursement

29 November 2017

Time Interval

95 months

Effective Date

20 April 2009

Actual Closing Date

29 November 2017

Time Interval

103 months

b. Amount ($ million)

Category

Original Allocation

(1)

Increased during

Implementation (2)

Cancelled during

Implementation (3)

Last Revised

Allocationa (4 = 1+2–3)

Amount Disbursed

(5)

Undisbursed Balanceb (6 = 4–5)

1 Urban infrastructure improvement

101.30 4.49 105.79 103.84 1.95

1a Civil works 94.10 10.99 105.09 103.27 1.82

1b Equipment 4.50 3.90 0.60 0.54 0.06

1c Resettlement 2.70 2.60 0.10 0.03 0.07

2 Capacity development and implementation support

15.50 0.71 16.21 13.42 2.79

2a Incremental administration

3.10 1.71 4.81 4.29 0.52

2b Preparation and implementation assistance

10.20 10.20 9.04 1.16

2c Capacity and institutional development

2.20 1.00 1.20 0.08 1.12

3 Unallocated 33.20 33.20 0.00 0.00 0.00

3a Physical contingencies 11.00 11.00 0.00 0.00 0.00

3b Price contingencies 22.20 22.20 0.00 0.00 0.00

Total 150.00 122.00 117.26 4.74

Note: Numbers may not sum precisely because of rounding. a Last revised allocation takes into account the reallocations and partial cancellations effected on 21 February 2011 and 22 January 2014, 3 December 2015, and 27 June 2016. b The undisbursed balance of $4.74 million was cancelled on 29 November 2017.

iii

C. Project Data

1. Project cost ($ million)

Cost Appraisal Estimate Actual

Foreign exchange cost 17.00 4.44

Local currency cost 202.00 179.75

Total 219.00 184.19

2. Financing plan ($ million)

Cost Appraisal Estimate Actual

Implementation costs

Borrower financed 52.00 62.49

ADB financed 150.00 117.26

Total implementation cost 202.00 179.75

Financing charges during implementation

Borrower financed 17.00 4.44

Total financing charges during implementation 17.00 4.44

ADB = Asian Development Bank.

3. Cost breakdown by project component ($ million)

Component Appraisal Estimate Actual

Part A Base Cost

Component A: Urban infrastructure improvements

Water supply 53.10 53.30

Sewerage and Sanitation 45.30 48.07

Urban drainage 4.40 2.46

Urban transport 17.00 51.86

Resettlement 3.60 0.08

Subtotal of Component A 123.40 155.77

Component B: Capacity development and implementation support

Incremental administration 6.20 8.08

Preparation and implementation assistance 10.20 11.12

Capacity and institutional development 2.20 0.09

Subtotal of Component B 18.60 19.29

Part B Contingencies

Physical contingencies 13.40

Price contingencies 26.90

Subtotal of Part B 40.30

Part C Taxes and duties 19.70 4.69

Part D Financing charges during implementation 17.00 4.44

Total 219.00 184.19

iv

4. Project Schedule

Item Appraisal Estimate Actual

Date of contract with consultants

Investment program management consultant Continued from project 1 20 April 2009

Design and supervision consultant-I Continued from project 1 20 April 2009

Design and supervision consultant-II Continued from project 1 20 April 2009

Design and supervision consultant-II Continued from project 1 20 April 2009

Investment program performance monitoring system consultant Continued from project 1 20 April 2009

Completion of Engineering Designs 31 March 2009 31 March 2014

Civil works contracts

Date of award 1 April 2008 6 July 2009

Completion of work 31 December 2012 30 June 2017

Equipment and supplies

Dates

First procurement 1 April 2008 11 July 2012

Last procurement 31 December 2010 11 July 2012

Completion of equipment installation 30 September 2011 31 December 2012

Start of operations

Completion of tests and commissioning 31 December 2011 31 March 2013

Beginning of start-up 1 January 2012 1 July 2012

5. Project Performance Report Ratings

Implementation Period

Ratings

Development Objectives Implementation Progress

From 30 Jan 2009 to 31 December 2009 Satisfactory Satisfactory

From 1 Jan 2010 to 31 December 2010 Not available Not available

From 1 Jan 2011 to 31 March 2011 Not available Not available

Single Project Rating

From 1 April to 30 June 2011 On track

From 1 July to 31 December 2011 Potential problem

From 1 January to 30 June 2012 Potential problem

From 1 July to 31 December 2012 On track

From 1 January to 31 December 2012 On track

From 1 January to 31 December 2013 On track

From 1 January to 31 December 2014 On track

From 1 January to 31 December 2015 On track

From 1 January to 31 December 2016 On track

From 1 January to 30 June 2017 On track

v

D. Data on Asian Development Bank Missions

Name of Mission Date No. of

Persons No. of

Person-Days Specialization of

Members

Loan appraisal 24 Jul–12 Aug 2008 10 139 a, b, c, d, e, f, g, h, i, j

Loan review 3–11 Nov 2009 3 21 a, k, l

Loan review 9–15 July 2010 2 12 f, k

Loan review 9–13 Aug 2010 1 4 f

Loan review 16–20 Aug 2011 2 8 m, k

Training and capacity building mission 19–20 Aug 2011 4 8 l, n, o, p

Loan review 29 Aug–2 Sep 2011 2 8 q, r

Loan review 10–14 Oct 2011 2 10 q, r

Safeguard review mission 19–22 Nov 2011 1 4 s

Loan review 28 Nov–5 Dec 2011 2 14 q, r

Special project administration 12–13 Jul 2012 2 4 m, k

Disbursement mission 3–7 Sep 2012 2 10 t, u

Safeguard review mission 4–7 Sep 2012 2 8 q, r

Loan review 29 Nov–5 Dec 2012 3 17 m, c, v

Special project administration 23–31 Jan 2013 3 18 m, c, v

Midterm review 28 Feb–8 Mar 2013 3 18 m, c, s

Special project administration 16–26 Sep 2013 2 10 m, v

Special project administration 4–6 Jun 2014 2 6 m, v

Loan review 1–5 Sep 2014 3 15 m, w, v

Loan review 10–14 Nov 2014 3 15 m, w, v

Loan review 22–27 Apr 2015 3 12 m, w, v

Special project administration 30 Sep–1 Oct 2015 2 4 m, x

Special project administration 2–3 Dec 2015 2 4 m, v

Special project administration 18–29 Feb 2016 2 16 y, z

Loan review 23 Feb–3 Mar 2016 6 36 m, w, aa, ab, ac, x

Loan review 13–14 Jul 2016 2 4 m, ad

Loan review 29 Aug–9 Sep 2016 3 18 m, ab, ad

Review mission 28–30 Jun 2017 2 6 m, ad

Project completion review 17–21 Dec 2018 4 20 m, ad, ae, af

Project completion review 11–15 Feb 2019 4 20 m, ad, ae, af

Project completion review 2–4 Apr 2019 6 18 m, ad, ae, af, ab, ag

a = urban development specialist/mission leader, south Asia urban development division; b = senior counsel, office of general counsel; c = safeguard specialist; d = urban development specialist, south Asia urban development division; e = urban economist, south Asia urban development division; f = project implementation officer, India resident mission; g = project management specialist (staff consultant); h = senior engineer (staff consultant); i = finance specialist (staff consultant); j = environmental specialist (staff consultant); k = assistant project analyst; l = climate change specialist; m = senior project officer (urban); n = capacity development technical advisor; o = capacity development expert; p = capacity development consultant; q = senior safeguards officer; r = senior environmental officer; s = environmental specialist; t = financial control officer; u = associate financial control analyst; v = associate project officer (urban); w = senior safeguards specialist; x = gender consultant; y = operations communications specialist; z = south Asia operation division officer; aa = associate project analyst; ab = social safeguard officer; ac = environmental consultant; ad = project analyst (consultant); ae = consultant, urban development; af = consultant, finance and economics; ag = associate environment officer.

I. PROJECT DESCRIPTION 1. The Rajasthan Urban Sector Development Investment Program (RUSDIP) was designed to improve the urban environment and promote ongoing reforms for sustainable, efficient, and responsive urban service delivery. RUSDIP sought to close the development gap in the state with increased economic growth, reduced poverty, and sustained improvements in the urban environment—impacting the quality of life of 1.6 million people in 15 urban local bodies (ULBs) with potential for economic growth and tourism. RUSDIP, supported by the Asian Development Bank (ADB), included physical improvements in water supply, wastewater management, solid waste management (SWM), urban drainage, urban transport and roads, social infrastructure, cultural heritage, and capacity development to enable ULBs to implement ongoing institutional, financial, and service delivery reforms. 2. ADB approved RUSDIP as a multitranche financing facility (MFF) on 31 October 2007 at an estimated cost of $390 million, with a loan component of $273 million and a Government of Rajasthan (GOR) contribution of $117 million.1 Project 2 under the MFF, designed as a sector loan of $150 million, was approved on 19 January 2009, signed on 18 February 2009, and declared effective on 20 April 2009.2 The original loan closing date of 30 June 2014 was extended to 30 June 2017. 3. The investment program, including project 2, comprised the following:3

(i) Part A: Urban infrastructure improvements. This component aimed to improve (a) water supply, (b) wastewater management, (c) SWM, (d) urban drainage, (e) urban transport and roads, (f) social infrastructure, and (g) support infrastructure for cultural heritage.

(ii) Part B: Capacity development and implementation support. This component involved (a) capacity development, and (b) investment program management.

4. At appraisal, project 2 was expected to benefit 12 ULBs by (i) improving access to treated, piped water supply of 135 liters per capita per day (lpcd) to 90% of the population (1.2 million) in 10 ULBs; (ii) providing sewerage facilities, including sewage treatment plants (STPs) in high-density areas and 135 lpcd of water supply in seven ULBs, and reducing the volume of wastewater discharged to water bodies; (iii) rehabilitating drainage outfalls and constructing new roadside drains in three ULBs with a high risk of flooding; (iv) improving the traffic flow and travel times between zones in five ULBs; and (v) improving institutional capacity, including technical and financial resources.

II. DESIGN AND IMPLEMENTATION A. Project Design and Formulation 5. Project 2 was relevant to the government and ADB sector strategies at appraisal and remains relevant at completion. It was aligned with the country strategy and program, 2003 for India; and supported the 2004 country strategy and program update, which highlighted

1 ADB. 2007. Report and Recommendation of the President to the Board of Directors: Proposed Multitranche Financing

Facility to India for the Rajasthan Urban Sector Development Investment Program. Manila. 2 ADB. 2009. Project Administration Memorandum for India: Rajasthan Urban Sector Development Investment

Program – Project 2. Manila (Loan 2506-IND). At appraisal, project 2 was expected to benefit 12 ULBs and was later expanded to 14 ULBs.

3 Project 2 interventions did not include SWM and heritage components.

2

interventions to address interregional disparities, recognized Rajasthan as a state with one of the lowest human poverty indices, and recognized infrastructure as one of the vehicles to achieve its goals. 4 Project 2 was also aligned with ADB’s strategy toward developing sustainable mechanisms for the delivery of social services, particularly in the water sector.5 At appraisal, it was consistent with the emphasis of India’s Tenth and Eleventh Five-Year Plans, 2002–2007 and 2007–2012, on improving and augmenting economic and social infrastructure and providing improved municipal services to a larger number of people in urban areas.6 It was also consistent with the GOR approach and strategy, in its 10th plan, for achieving national average levels in critical quality of life indicators through reducing poverty and regional disparities, providing basic minimum services, and developing infrastructure.7 6. At appraisal, while the design was appropriate to achieve the expected outcomes, it could have considered incorporating 24/7 water supply. The MFF modality addressed the state’s medium- and long-term requirements and facilitated a long-term partnership for socioeconomic development between ADB and the GOR. The sector loan approach for project 2 was appropriate under the MFF, as it reflected the GOR’s capacity to address large-scale development challenges effectively in the urban sector, besides offering flexibility in subproject selection and timelines for implementation. 7. Lessons from the first ADB loan in Rajasthan, the Rajasthan Urban Infrastructure Development Project, the previous tranche under the MFF, and other ADB projects in India were applied and areas of focus were delineated. The availability of all the required land was ensured before project commencement (except Sikar [paras. 11 and 19]), the investment program implementation units (IPIUs) were established in the ULBs of project 2, and project consultants were mobilized before loan signing.8 ULBs and subprojects were identified according to the subproject selection criteria of the MFF. All sample subprojects appraised during the processing of project 2 were implemented. Loan funds were reallocated in 2011, based on a minor change in scope that enhanced the allocation for urban infrastructure improvements, allowing for eight additional infrastructure works to be implemented, leading to increased coverage of urban infrastructure services, and adding new subprojects in two ULBs (Alwar and Jhalawar)—thus enhancing the project’s relevance (para. 28).9 8. While the results chain for the design and monitoring framework (DMF) of project 2 was logical, it had weaknesses in its numeric targeting, its consistency with the facility DMF, and its classification of indicators. The assessment of impact achievements (increase in the population served) was constrained by the nonavailability of baseline data for impact indicators in the DMF. The population of the 12 ULBs under project 2 totaled 1.2 million while the population of the

4 ADB. 2003. Country Strategy and Program: India. 2003–2006. Manila; and ADB. 2003. Country Strategy and

Program Update. India. 2004–2006. Manila. 5 ADB. 2001. Water for All: The Water Policy of the Asian Development Bank. Manila; and ADB. 2011. Water

Operational Plan, 2011–2020. Manila. 6 Government of India, Planning Commission. 2002. Tenth Five-Year Plan, 2002–07. New Delhi; and Government of

India, Planning Commission. 2008. Eleventh Five-Year Plan, 2007–12. New Delhi. 7 Government of Rajasthan, Planning Department. 2002. Tenth Five-Year Plan, 2002–07. Jaipur. 8 ADB.1998. Report and Recommendation of the President to the Board of Directors: Proposed Loan to India for the

Rajasthan Urban Infrastructure Development Project. Manila (Loan 1647-IND). 9 ADB. 2011. Amendment to the Loan Agreement: Rajasthan Urban Sector Development Investment Program,

Project 2. Manila (Loan 2506-IND). The additional subprojects are construction of (i) storm water drainage in Sikar, (ii) sanitary landfill in Sikar, (iii) road widening in Sikar and Bundi, (iv) railway over bridges in Chittorgarh, Baran, Alwar and (v) minor bridge at Karauli. In all, 30 subprojects were implemented — 10 water supply, 8 wastewater, 2 drainage, and 10 roads and transport subprojects.

3

15 ULBs under the MFF was 1.6 million, according to the census.10 Therefore, the target of 1.5 million beneficiaries in the project 2 DMF was incorrect and inconsistent with the facility DMF. Accordingly, the beneficiaries of the water supply interventions totaled 0.9 million in 10 planned ULBs (90% of the population) and the beneficiaries of the wastewater interventions totaled 0.7 million in 7 ULBs (100% of the population). However, while sewage treatment facilities will benefit 100% of the population, the DMF outputs for household sewer connections were provided using government grants and limited to priority areas covering a population of 0.19 million in seven ULBs (para. 11). As project 2 was a sector loan, the DMF described the range of interventions in lieu of setting numerical targets. Unlike the DMF of the MFF, the DMF for project 2 did not cover the beneficiaries of social infrastructure. While the objective of the MFF and its projects are the same in terms of impacts, sector outcomes, and outputs, some impact indicators and multiple outcome indicators vary between the MFF and project 2. Moreover, some outcome indicators reflect outputs rather than outcome, while others reflect project selection requirements as an outcome instead of coverage as target. The details of the achievements with respect to the DMF of project 2 are in Appendix 1. B. Project Outputs 9. The contribution of project 2 to the ADB results framework is described in para. 37 and the output targets achieved (11 out of 12) are summarized below.

1. Part A: Urban Infrastructure Improvements 10. Water supply. The interventions or outputs described in the DMF of project 2 were achieved in the planned 10 ULBs by (i) rehabilitating existing systems, refurbishing or replacing old pumping machinery, and reducing unaccounted-for water (UFW); (ii) installing 63 electromagnetic flow meters and 87,010 consumer water meters in 100% of the water supply connections provided under the project; (iii) providing chlorination facilities to achieve 100% disinfection of supply; (iv) augmenting the source in Bundi and Rajsamand by 44 million liters per day (mld); (v) commissioning two water treatment plants (WTPs) in Rajsamand (17 mld) and Dholpur (15 mld); (vi) creating 87 storage reservoirs (clear water reservoirs and overhead storage reservoirs) with cumulative capacity of 71 million liters; (vii) replacing leaking carrier mains and laying distribution mains totaling 1,185 kilometers (km); (viii) rehabilitating existing facilities and constructing new facilities to cover 93% of households with piped water supply against the DMF target of 90%.11

11. Sewerage. A sewerage system—including outfall, trunk sewers, and tertiary networks—totaling 506.3 km was laid in priority areas of eight ULBs compared with the target of seven ULBs. 12 Sewerage interventions were not undertaken in Sikar because of the nonavailability of land for STP, and sewer networks were instead undertaken in Alwar and Jhalawar (para. 7), which already had STPs. The treatment capacities of STPs, estimated at 68 mld for seven ULBs in the DMF, were refined to 54 mld in six ULBs (excluding Sikar’s 10 mld STP) during the detailed engineering design and fully achieved as designed. Household connections in priority areas were provided in all the ULBs using government grants, not funded under the MFF based on the subproject

10 Government of India, Office of the Registrar General and Census Commissioner. 2001. Census of India, 2001.

New Delhi. 11 Water supply subprojects were undertaken in Barmer, Bharatpur, Bundi, Churu, Dholpur, Karauli, Nagaur,

Rajsamand, Sawai Madhopur, and Sikar. 12 Sewerage subprojects were undertaken in Alwar, Barmer, Bundi, Dholpur, Jhalawar, Nagaur, Rajsamand, and

Sawai Madhopur.

4

selection criteria. Vehicle mounted sewer-suction-cum-jetting machines and sewer-jetting machines were also provided to 12 ULBs. 12. Urban drainage. Drainage master plans were prepared for Baran, Bharatpur, and Sikar. Based on these plans, drainage outfalls and stormwater drains totaling 11.8 km were rehabilitated or constructed to facilitate stormwater runoff. In addition, 15.7 km of roadside drains were constructed in Bundi. Drainage interventions were not undertaken in Baran based on the assessed risks of flooding. 13. Urban roads and transport. The output targets were fully achieved as planned—two-lane road over bridges (ROBs) were constructed in six ULBs (against a target of four ROBs in four ULBs) and two bridges over river were constructed in one ULB. Additionally, 75.1 km of roads were strengthened in four ULBs. 14. Social infrastructure. While the DMF did not define social infrastructure outputs, project 2 interventions provided 0.15 million people living in identified slums in 14 ULBs with access to improved basic urban services, including water supply and sanitation infrastructure—improving the living conditions of the poor and vulnerable.

2. Part B: Capacity Development and Implementation Support 15. Capacity development. A structured institutional and capacity development plan (ICDP) for all program ULBs and concerned state-level bodies was developed based on a detailed study identifying the gaps and measures required for strengthening the institutional structure. Actions under the plan included the use of contractual staff for municipal services such as SWM and urban drainage, and the use of contractors to manage the STPs through provisions for operation and maintenance (O&M) embedded in their contracts—resulting in more effective allocation of human resources. More than 650 trainings were provided to the staff of program ULBs and state-level bodies in municipal services on topics such as responsive grievance redressal, construction management, safeguards, gender mainstreaming, O&M of municipal services, asset management, financial management, urban governance, and service delivery. The assets and responsibilities of sewerage systems were handed over to program ULBs. A sustainable user charge structure was implemented for water supply services across the state and is being levied incrementally for sewerage as and when households are provided with sewer connections. The fee for door-to-door waste collection services, provided to nearly 100% of the population, does not accrue to the program ULBs but to the outsourced agencies. 16. Implementation support. The investment program management consultant (IPMC) and three design and supervision consultants (DSCs) supported program implementation by preparing the design documents, managing the bidding process, and supervising the construction works. The IPMC provided technical support to the investment program management unit (IPMU) in managing contracts, monitoring safeguards, and preparing progress reports. The 15 program ULBs were divided into three groups of five program ULBs, based on their geographical location, and a group was allotted to each of the three DSCs. The community action and participation program (CAPP) consultants delivered information, education, and communication program; assisted in implementing the ICDP; and contributed to the improved acceptability of sewerage services by the residents. Social acceptance of paid sewerage services and community mobilization for SWM were achieved under the CAPP. The investment program performance and management system (IPPMS) consultants monitored program implementation at the baseline, midterm, and end-term.

5

C. Project Costs and Financing 17. The estimated project cost at appraisal was $219.00 million, comprising an ADB loan of $150.00 million and GOR contribution of $69.00 million. At completion, the actual project cost reduced to $184.19 million, without curtailment of the project outcomes or outputs, comprising an ADB loan of $117.26 million and GOR contribution of $66.93 million. Financing charges decreased by $12.56 million because of lower interest rates. Loan savings resulting from the appreciation of the United States dollar and overestimation of contingencies were leveraged to increase the allocation for civil works from $94.10 million to $103.27 million for expanding coverage, adding new subprojects and ULBs (para. 7), and meeting marginal cost overruns in a few contracts. The extended implementation period (36 months) increased the cost of incremental administration by $1.19 million. Costs decreased by (i) $3.96 million for SWM equipment because of the deferment of procurement to project 3, (ii) $2.67 million for resettlement because of the avoidance of social impacts and use of counterpart funds, (iii) $2.12 million for capacity and institutional development as state training resources were used, and (iv) $1.16 million for preparation and implementation assistance. A total of $28.00 million was cancelled and $4.74 million remained unused at loan closing.13 The ratio of the ADB loan to GOR contribution changed from 70:30 at appraisal to 64:36 at completion. Appendix 2 details the project cost at appraisal and actual. Appendix 3 provides the project cost by financier. D. Disbursements 18. A total of $117.2 million (96% of the revised loan amount of $122.0 million) was disbursed by project completion. Loan disbursements were on track from the first disbursement on 8 December 2009, evenly spread out (11% to 19% per year) from 2010 to 2015, and reached 68% of the revised loan amount by the end of the original loan closing date (88% by 2015). This included an imprest advance of $15.00 million, which the GOR availed of in 2010. Following the GOR’s decision to make payments through Treasury procedures, the imprest account was liquidated against claims from the third quarter of 2012 to the first quarter of 2013. Contract award and disbursement achievements fell below 90% of projections from July 2011 to June 2012, resulting in a potential problem project rating for the period. Appendix 4 and Appendix 5 provides the annual and cumulative disbursements and contract awards of the loan proceeds. The statement of expenditure (SOE) procedure allowed up to $100,000 equivalent per individual payment, which could have been enhanced considering the capacity of the IPMU. E. Project Schedule 19. The original loan closing date of 30 June 2014 was extended twice by 1 year each, followed by another two extensions of 6 months each (i) to optimize loan utilization by awarding additional contracts (in 2013 and 2014) to use the additional funds available as a result of the appreciation of the United States dollar, (ii) to enable the completion of works, and (iii) to complete re-tendered and slow-moving contracts. The project had no significant start-up delays, which reflects the state’s preparedness at appraisal, as requisite lands were identified for STPs (except Sikar [paras. 7 and 11]) and other facilities, permission was obtained from the concerned authorities for bridges over river, and detailed project reports were prepared. IPMU’s capacity for implementation and interdepartmental coordination led to the smooth execution of utility shifting and timely issuance of necessary permissions and clearances. However, contract duration affixed for water supply and wastewater works was ambitious considering that works were in existing

13 Partial loan cancellations were made as follows: $18.70 million on 6 August 2013, $7.09 million on 3 December 2015,

and $2.21 million on 27 June 2016. This reduced the net loan amount to $122.00 million.

6

unplanned towns and needed to be executed without undue disruption to service delivery and traffic movement or public inconvenience (para. 22). By loan closure on 30 June 2017, only six of the 57 contracts were ongoing and these were completed using GOR funds (paras. 22 and 38). All contracts were completed at the time of the project completion report mission (Appendix 6). F. Implementation Arrangements 20. The project’s implementation arrangements proved appropriate to achieve the envisaged outputs. The arrangements comprised the Local Self Government Department, GOR as the executing agency; a state-level and interministerial empowered committee; a works finalization committee chaired by the principal secretary for urban governance; the IPMU as the implementing agency for RUSDIP headed by the project director; IPIUs in each project town; and city-level committees, which also functioned as grievance redress committees, chaired by district collectors. The IPMU and IPIUs were assisted by the IPMC, three DSCs, the CAPP, and IPPMS consultants (para. 16). The project assets, once developed, were handed over to line agencies and ULBs for O&M, including the management of extant O&M contracts. Water supply assets are managed by the public Health Engineering Department (PHED) while major roads and transport assets are managed by the Public Works Department (PWD). ULBs manage wastewater, drainage, internal municipal roads and streetlights, and SWM. G. Consultant Recruitment and Procurement 21. Consultants recruited under project 1 following the quality- and cost-based selection procedure and ADB’s Guidelines on the Use of Consultants (2007, as amended from time to time) continued for the subsequent tranches. The IPMU was familiar with ADB procedures for the procurement of civil works and goods and conformed to ADB’s Procurement Guidelines (2007, as amended from time to time). Standard bid documents prepared under project 1 for the procurement of civil works and goods were used in the MFF, leading to standardization and quality control. In October 2012, ADB assessed and approved the GOR e-portal for contracts procured following national competitive bidding and shopping methods under the MFF. Procurement activities were executed smoothly and were among the IPMU’s core strengths. End-to-end e-procurement and contract management systems would have further strengthened IPMU’s capacity. Cumulative contract awards exceeded annual projections throughout the loan period. 22. The overall performance of the consultants is rated generally satisfactory. The performance of the IPMC and DSCs was satisfactory. The performance of the DSCs was initially hampered by slow internal mobilization and frequent replacement of team members, leading to some delays in the planning, design, and implementation of the project. Close monitoring of DSCs and the removal of a few nonperforming DSC personnel by the IPMU led to optimal utilization of the DSC services and improved delivery of outputs by DSCs. The performance of the IPPMS consulting firm engaged to prepare baseline, midterm, and end-term project performance monitoring reports was less than satisfactory and had to be terminated. Following the termination, the performance of the consulting firm appointed to complete the remaining tasks was rated satisfactory. Overall, the performance of the contractors is rated satisfactory. However, the ambitious contract periods exacerbated contractors’ poor mobilization of resources, resulting in six water supply and sewerage contracts (10% of the total contracts) being extended beyond the original contract period (paras. 19 and 38). The performance of the suppliers is rated satisfactory.

7

H. Safeguards 23. Project 2 was classified category B for environment, involuntary resettlement, and indigenous peoples according to the ADB safeguard policies.14 An environmental assessment and review framework, resettlement framework, and indigenous peoples planning framework were prepared during loan processing. ADB approved six sample sector-specific town-specific initial environmental examination (IEE) reports and short resettlement plans, based on which additional IEEs and short resettlement plans were prepared during implementation.15 The IPMU confirmed that no issues and/or court cases related to safeguards were outstanding at completion. The management of safeguard compliance under institutional arrangements—including information disclosure, participation, consultation activities, grievance redressal, and regular submission of semiannual safeguard monitoring reports—was rated effective.16 24. ADB responded to a complaint from an agency by obtaining information from the IPMU and investigating the grievance within a reasonable time, and obtained feedback from the complainant about resolution before closing the grievance log.17 Additional due diligence rectified the omission of an environmentally sensitive area, and four IEEs were updated accordingly and implemented. Three households belonging to the scheduled tribe category suffered temporary income loss during project implementation and were provided compensation for livelihood loss and additional vulnerability assistance. While the implementation of safeguards was initially weak because of lack of specialized personnel, the safeguard implementation and monitoring improved with the engagement of full-time professionals in the IPIUs, DSCs, and contractors. Except for the continued renewal of consents to operate (CTOs) the WTPs and STPs after loan closure, the overall safeguard compliance was found to be satisfactory. The IPMU has agreed to ensure the renewal of CTOs by 30 September 2019 (para. 44). Details on safeguards are in Appendix 7. I. Monitoring and Reporting 25. All but two of the 73 loan covenants were complied with. The covenant on the levy of sustainable user tariffs was partly complied with. Enhanced water tariffs, infrastructure development tax or urban development tax are being levied, while sewerage cess are being levied as household sewer connections are provided (para. 15). However, the fee for door-to-door waste collection services does not accrue to the ULBs but to the outsourced agencies (para. 15). The covenant related to audited project financial statements was partly complied with. Although annual audits were conducted by statutory auditors and furnished to ADB in a timely manner (para. 26), separate accounts for each project were not maintained and reconciled with ADB’s loan financial information services, and the statutory auditor’s opinions were unclear. Monitoring and reporting arrangements, including quarterly progress reports, semiannual safeguard reports, and project completion report, were complied with. Baseline and end-term surveys were also conducted, and reported by IPMU. Appendix 8 provides the status of compliance with loan covenants.

14 ADB. 2002. Environment Policy of the Asian Development Bank. Manila; ADB. 1995. Involuntary Resettlement.

Manila; and ADB. 1998. The Bank’s Policy on Indigenous Peoples. Manila. 15 Two affected households were compensated ₹3.74 million for land and 510 affected households were compensated

₹5.86 million for temporary loss of livelihood. 16 Adequate safeguard monitoring and management was ensured by officers at the IPMU, supported by safeguard

experts of the IPMC. The officers at the IPIU, supported by the social and environmental experts of the concerned design and supervision consultants, were responsible for safeguard implementation, monitoring, and management in the project ULBs. All contractors engaged environment officers during construction.

17 An agency, Gharial Conservation Alliance, claimed in 2012 regulatory noncompliance and inadequate environmental assessment. However, all the requisite regulatory compliances were found to be in place during ground truthing.

8

26. The financial management arrangements of the borrower and the executing agency were robust and included timely counterpart funding. All audited project financial statements (para. 25) were submitted within the specified time, except for delays of (i) 0.4 months in 2011, (ii) 2.6 months in 2014, and (iii) 1.2 months in 2018, which were within the 6-month grace period (para. 25 and Appendix 8; project agreement, section 2.09).

III. EVALUATION OF PERFORMANCE A. Relevance 27. The project is relevant to the government’s development objectives and ADB’s country and sector strategies both at appraisal and completion (para. 6). Although the project predated ADB’s Strategy 2030, it remains relevant to the strategy, with its focus on building livable cities and providing safe and effective water and sanitation services.18 At completion, the project remains relevant to ADB’s policy focus in India on areas of inclusive growth, infrastructure, and environmental sustainability.19 It is aligned with the government’s successive five-year plans; the NITI Aayog three year action agenda, 2017–18 to 2019–20; and the GOR 12th plan, which prioritized the supply of potable water to its urban population, wastewater management, and urban poverty alleviation.20 It is in line with the state’s priorities for poverty reduction through improved access to potable water and sanitation, good governance, and private enterprise participation. 28. Processing the project as a sector loan (para. 6) was relevant and responsive to the state’s agenda. Despite design weaknesses in determining indicators (para. 8), the project results chain was sound—sample subprojects were indicative of project interventions and were appropriate to achieve the intended outcomes. The results chain continued to form the basis for identifying and assessing subsequent subprojects, resulting in realistic numbers of interventions at appropriate locations. Minor changes in the scope of the project (para. 7, footnote 9) were timely and in response to emerging project realities, which optimized the use of loan funds (para. 17) and enhanced the project’s relevance. The project introduced wastewater services in towns that were previously not covered and was instrumental in inducing awareness and raising community demand for such services (para. 16). B. Effectiveness 29. Overall, the project is rated effective as all its outcome targets have been achieved (Appendix 1).21 The water supply component resulted in asset creation; production, pumping and distribution improvements; and UFW and O&M cost reduction, thereby providing all households in project 2 areas with regular and reliable service, and additional quantity of water. The six outcome targets of the water supply subsector have been achieved: (i) an average supply of 137 lpcd of treated piped water to a population of 1.44 million (93%) in the 10 planned ULBs;

(ii) 100% metered connections to all households connected under the project; (iii) bulk water

18 ADB. 2018. Strategy 2030: Achieving a Prosperous, Inclusive, Resilient, and Sustainable Asia and the Pacific.

Manila. 19 ADB. 2018. Country Partnership Strategy: India, 2018–2022—Accelerating Inclusive Economic Transformation.

Manila; and ADB. 2018. Country Operations Business Plan: India, 2018–2020. Manila. 20 Government of India, NITI Aayog. 2017. India Three Year Action Agenda, 2017–18 to 2019–20. New Delhi;

Government of Rajasthan, Planning Department. 2012. Twelfth Five-Year Plan, 2012–17. Jaipur. 21 The outcome pertaining to the provision of toilets and water connections to schools where project facilities are

constructed is not applicable, as the GOR provided such facilities to all schools using national program funds.

9

meters at bulk supply points; (iv) chlorination facilities to ensure the supply of 100% disinfected water to all consumers; (v) adequate storage capacities to ensure a minimum of 20% supply in overhead storage reservoirs and 2 hours of supply in clear water reservoirs (para. 10); and (vi) UFW reduced by 20% (in nine of the 10 ULBs). These also contributed toward the achievement of Goal 6 of the Sustainable Development Goals.22 The wastewater management component resulted in asset creation, systemic improvements, and developed safe disposal systems for sewage and protected water bodies. Sewerage facilities developed in eight hitherto unserved ULBs exceeded the target of seven ULBs, benefiting 0.82 million (100%) of the ULB population, whereas 36,186 of the planned 44,044 households (82%) benefitted in parts of the eight ULBs where sewerage networks were laid (paras. 8 and 11).23 The discharge of untreated wastewater to water bodies has reduced by more than 20 mld (of the 54 mld treatment capacity created). The sewer suction and jetting equipment supplied helped maintain the sewerage network. The detailed project reports for sewerage and drainage, prepared for the entire municipal area of the project ULBs, are being used as the basis for network expansion by the ULBs with state resources. Besides the construction of new roadside drains, the urban drainage component rehabilitated drainage outfalls in two ULBs with high risks of flooding and had drainage master plans—reducing the incidence of flooding and the number of days the ULBs are impacted, and benefitting more than 0.68 million people (para. 12). The urban transport component improved mobility for more than 1.76 million residents in nine ULBs, exceeding the target of five ULBs in the DMF (para. 13 and footnote 9), including access to economic opportunities for the poor, by eliminating vehicle idling time and traffic congestion. It also reduced travel times from an average of 40 minutes per crossing to less than 5 minutes during peak hours, cut travel costs, and reportedly reduced accidents at the intervention sites. ROBs constructed in six ULBs eliminated high-traffic gated railway level crossings (25–40 trains per day). 30. The project design recognized the risk that ULBs might not be able to generate adequate revenues from internal resources to manage and maintain the existing and newly acquired assets. Therefore, it was covenanted that the GOR shall ensure adequate funds toward the O&M of the project facilities through budgetary allocations or other means, to be provided to the IPMU, the appropriate ULB, or line agencies, during and after subproject completion (Appendix 8; Loan Agreement, Schedule 5, para. 9). ULBs and state-level bodies meet the O&M costs of all urban services through well-structured and planned budgetary allocations based on a revenue-sharing model between the three tiers of government (footnote 24), regular transfers from the State Finance Commissions (SFCs) and Central Finance Commissions (CFCs), tariff enhancements, and improved tax collection. The project led to on-the-job learning for IPMU and IPIU staff, consultants, and contractors. The capacities of program ULBs and concerned state-level bodies were also strengthened by implementing a structured ICDP developed under the facility. Actions taken, such as outsourcing the operational functions of some municipal services (SWM and water billing, including sewerage cess) freed up human resources for urban governance and the management of municipal service delivery (para. 15). Financial management systems were improved with double entry accounting systems, municipal asset register management, and structured budgets that are disclosed to the public—improving transparency, accountability, and governance. The training programs effectively reoriented the staff of ULBs and state-level bodies toward the professionalization of municipal services and better urban governance. Safeguard compliance reporting, monitoring, and management were rated effective (para. 23).

22 United Nations, Sustainable Development Goals, Goal 6: Ensure access to water and sanitation for all.

https://www.un.org/sustainabledevelopment/water-and-sanitation/. 23 The beneficiary population and households exclude Alwar, which was included under project 1.

10

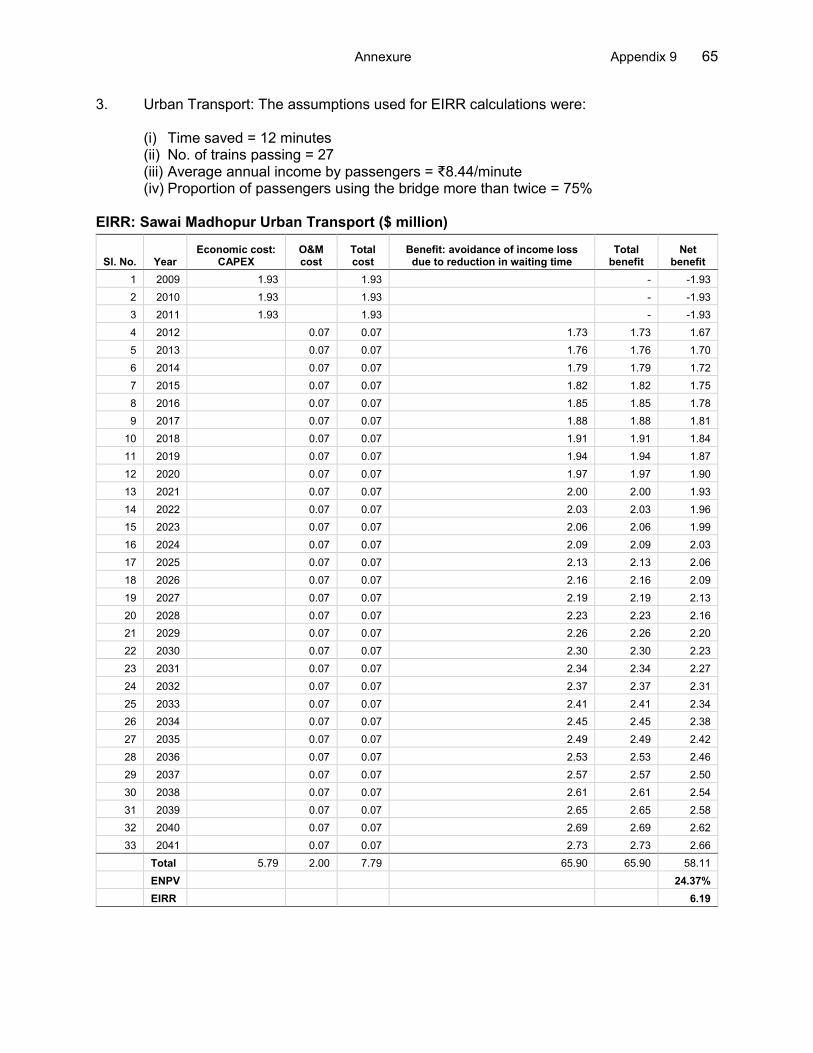

C. Efficiency 31. Overall, the project is rated efficient. The economic internal rates of return (EIRRs) of the subprojects identified at appraisal were reevaluated as follows: (i) water supply—Nagaur 23.9% (appraisal 10.8%) and Bundi 22.1% (appraisal 13.0%); (ii) wastewater—Sawai Madhopur 14.9% (appraisal 24.1%) and Bundi 14.6% (appraisal 17.0%); and (iii) urban transport—Sawai Madhopur 24.4% (appraisal 27.9%) (Appendix 9). All subprojects were evaluated at project completion and the EIRRs ranged from 12.9% to 38.1%, all being above the 12% threshold. The estimated EIRRs of the project components at completion were (i) water supply 20.0%, (ii) wastewater 15.3%, and (iii) urban transport 20.9%. The estimated EIRR for the total project combining all subprojects was 19.2%. The project EIRR remained above the threshold with a 20% reduction in future benefits. The economic net present values for selected subprojects at completion were positive, applying a 12% discount rate. The delays in executing some contracts (para. 22) and marginal cost overruns (para. 17) did not affect the EIRR, as they were counterbalanced by efficient contract awards and fund disbursements and increased service area coverage and project ULBs. The institutional efficiencies and grievance redress mechanisms developed in the ULBs and line agencies reduced transaction costs and time, improved the transparency and accountability of governance, and significantly augmented the administrative capacities of the respective institutions (paras. 15 and 30).

D. Sustainability 32. Overall, the project is rated likely sustainable. As it was not designed for capital cost recovery, the operating ratios (revenue to O&M cost ratio) calculated for the five sample ULBs averaged 1.0:0.9, indicating that the ULBs have the financial capacity to meet their operating expenses out of their internal revenues and assigned compensations (para. 30). 24 The Constitution of India (Article 243X) mandates the state to allocate to the ULBs the associated sources of finance and functionaries required to manage the assigned functions and sustain service delivery. ULBs’ finances are structured through fiscal transfers from the state in the form of (i) compensation grants (in lieu of octroi, a tax on goods since abolished, and other taxes subsumed under the Goods and Service Tax Act, 2017); (ii) transfers from CFCs and the SFC; (iii) tariff enhancement; and (iv) improved performance in the collection of taxes and user charges. CFC transfers account for about 30%–40% of ULB finances, of which up to 90% may be used for the O&M of municipal assets. However, less than requisite ownership levels by project ULBs of STPs has led to delayed O&M payments to contractors, resulting in less than optimal maintenance of the STPs. A review of the overall finances of the PHED and PWD indicates the ability of the two departments to meet the O&M requirements of the existing assets and the inclusion of new projects through state budgetary allocations and water and sewerage tariffs.25 Further, the GOR has been consistent and timely in its release of O&M funds, as providing water is a fundamental duty of the state. 33. The institutional capacities of ULBs and state-level bodies were strengthened as part of the ongoing reforms and under the facility (paras. 15 and 30). Systemic improvements in the

24 The CFC allocates 42% of the funds of the general pool to ULBs and Panchayati Raj institutions (rural bodies), which

are distributed based on population (55%), area (15%), and weaker local bodies (30%). The CFC also provides an additional 5% of ULBs’ fund utilization as performance incentives. CFC funds can be used toward O&M (minimum 90%) with a ceiling of 10% toward capital works. The SFC allocates about 7.18% of net state tax revenue to ULBs using the same distribution weightages (e.g., population, area). The SFC funds can be used for capital investments (85%), administration (10%), and management reforms (5%).

25 PHED, GOR. 2019. Notice. http://phedwater.rajasthan.gov.in/content/dam/doitassets/water/Public%20Health%20 Engineering%20Department/pdf2017/citizencorner/water%20tariff.pdf

11

administrative capacities of the ULBs and lines agencies strengthened internal processes (such as accounting systems and grievance redress mechanisms), transparency and accountability of governance (para. 30). PHED has adequate human resources and institutional capacities for the O&M of water supply assets; and the water supply interventions have improved the system efficiency and minimized losses, enabling PHED to manage a more sustainable system focused on service delivery benchmarking and water conservancy. ULBs have benefitted significantly from the finance and urban governance reforms, and need to continue their human resources and institutional capacity augmentation initiatives for better municipal asset management and governance. 34. The project is assessed to be environmentally sustainable as it contributes to water- and fuel-resource conservation; the control of vector-borne diseases; and air, water, and noise pollution abatement—improving the quality of life and the urban environment. The project is also assessed to be socially sustainable, as the infrastructure interventions ensure continuous access to project benefits and economic opportunities. E. Development Impact 35. The development impact is rated satisfactory as the project contributed to the impact indicator of increased economic growth and sustained improvement in the urban environment and quality of life in the project ULBs (Appendix 1). The provision of basic infrastructure and services in the project ULBs contributed significantly to increased access to economic opportunities, inclusive economic growth, social inclusion of the marginalized, and improving the overall quality of life indices of its residents. Urban infrastructure services covered by the project reached an additional 0.5 million people, representing 36% of the population of the 14 project ULBs, against a target of 20%. The project addressed the basic needs of the poor, particularly benefitting women, through reduced time and energy spent on water collection and more time for economic activities. As planned under the MFF, the provision of water connections for the poor and monthly consumption of 15 kiloliters of have been made free, contributing significantly toward achieving Goal 6 of the Sustainable Development Goals (footnote 22). Annual incidence of sanitation-related diseases decreased by nearly 35% against the 20% target in the eight ULBs where sanitation subprojects were undertaken. Improvements in sanitation have led to overall improvements in public health, particularly impacting the poor through a reduced burden of diseases, decreased treatment costs, and a fall in productivity losses. However, the long-term impacts of addressing deficiencies in environmental sanitation on reducing high morbidity and mortality among the poor can be quantified at a later stage. More than 375,547 people living below the poverty line have benefitted from access to improved urban infrastructure services, which constitutes 21% against the 20% target. Drainage interventions significantly reduced flooding in low-lying areas while urban transport interventions improved the riding quality and pedestrian safety; and reduced traffic congestion, travel time, and vehicle operating costs—contributing to improved health and urban environment quality, and thereby helping to achieve the strategic objectives of the project. The environmental impacts of project 2 are assessed in para. 34. 36. The IPMU has developed significant institutional capacities since implementing the first ADB loan for the Rajasthan Urban Infrastructure Development Project and the first tranche of this MFF to plan and formulate projects; procure and manage contracts; and monitor safeguards and implementation. It has consolidated its position in the state as the preeminent organization in managing large-scale externally aided and government-funded projects, and substantially increased contract award and disbursement performance, while enhancing the capacities of other government departments. The IPMU has evolved to manage subsequent ADB loans to the GOR as a combination of policy-based lending and project loan, with greater flexibility to identify

12

infrastructure gaps and capacity building needs, develop and design subprojects, and to support sustainable urban sector reforms at the state level. 26 Enhancing the asset transfer process requires continued support from the IPMU, especially with the exit of the IPIU on completion, which has been well managed by the IPMU. The IPMU is now part of the state-level nodal agency for implementing urban infrastructure projects.27 37. The contributions of project 2 to the ADB results framework are (i) households with new or improved water supply (number) in 10 ULBs = 259,208; (ii) wastewater treatment capacity added or improved (mld) = 54; (iii) water supply pipes installed or upgraded (length of network in km) = 1,185; and (iv) land improved through drainage and/or flood management (hectares) in Bharatpur and Sikar = 400. F. Performance of the Borrower and the Executing Agency 38. The overall performance of the borrower and the executing agency is rated satisfactory. The borrower, represented by the Government of India’s Department of Economic Affairs, provided timely guidance and decisions to GOR on the project and undertook regular tripartite review meetings with ADB, the GOR, and the IPMU, which helped identify bottlenecks, resolve issues, and monitor progress. The GOR provided strong support to the IPMU, including timely counterpart funding (including funds to complete spillover works after loan closure) and adequate human resources throughout the project period. However, the financial management performance of the borrower and the executing agency is rated less than satisfactory, as audit shortcomings persisted over the years and separate project accounts were not maintained by the IPMU (paras. 25 and 26). The IPMU established project implementation procedures for planning and implementation early in the project cycle. It also established effective monitoring and implementing mechanisms through IPIUs in each project ULB, headed by executive engineers. This helped in interagency coordination, monitoring, and progress reporting from the field, and strengthened the information flow to ADB and the project ULBs. The IPMU exhibited strong leadership with the placement of senior officers from the state government in its management, which helped in change management—critical for the implementation of reforms. The contract periods estimated by the IPMU for water supply and sewerage contracts were ambitious and led to contractors exceeding implementation milestones (paras. 19 and 22). Although the IPMU spent considerable time and effort on managing arbitration and other legal issues in the absence of techno-legal personnel, the IPMU was effective in managing the overlapping policy, regulatory, technical, administrative, and financial management aspects of project implementation, including safeguard compliance. G. Performance of the Asian Development Bank 39. The performance of ADB is rated satisfactory. ADB undertook regular review missions, disbursement review missions, midterm review missions, and project completion review missions to assess progress and provide advice on the resolution of outstanding issues. Monitoring, capacity building, and guidance by ADB throughout the project cycle helped define processes, address issues through time-bound actions and targets, and expedite project implementation. However, the financial management performance of ADB is rated less than satisfactory, as audit shortcomings were identified and commented on, but missions were not fielded over the years to

26 ADB. 2014. Report and Recommendation of the President to the Board of Directors: Proposed Loans and Technical

Assistance Grant and Administration of Grant to India for the Rajasthan Urban Sector Development Program. Manila. 27 The GOR has set up the Rajasthan Urban Drinking Water, Sewerage, and Infrastructure Corporation (RUDSICO),

amalgamating the IPMU, the Rajasthan Awas Vikas Nigam, and the Rajasthan Urban Infrastructure Finance and Development Corporation.

13

resolve these issues (paras. 25, 26, and 38). The IPMU found ADB’s support and advice effective in resolving project management issues and safeguard management (para. 24). ADB also provided training and supported the exposure visits of IPMU and IPIU personnel to other ADB-supported projects in India and abroad. ADB monitoring ensured adherence to due processes and transparency in procurement, disbursements, and safeguards, while upholding integrity and ethical standards. H. Overall Assessment 40. Overall, project 2 is rated successful. The project was relevant to the government’s overall development objectives and ADB’s policies at appraisal and continues to remain so at completion. It is assessed effective as all envisaged outcome targets were achieved. The project is rated efficient, as the EIRRs for all the interventions were reassessed to be higher than the economic opportunity cost of capital of 12%. It is rated likely sustainable as the O&M costs of the project assets are met through statutory transfers from the SFC and CFCs, and the collection of municipal taxes and user charges. The development impacts are rated satisfactory, as the project has contributed significantly to all the impact indicators, resulting in improved quality of life indices, poverty reduction, and economic and social inclusion in the project ULBs. The performance of the borrower, the executing agency, and ADB is rated satisfactory. These are summarized in the table:

Overall Ratings Criteria Rating Relevance Relevant Effectiveness Effective Efficiency Efficient Sustainability Likely sustainable Overall assessment Successful Development impacts Satisfactory Borrower and executing agency Satisfactory Performance of Asian Development Bank Satisfactory

Source: Asian Development Bank.

IV. ISSUES, LESSONS, AND RECOMMENDATIONS

A. Issues and Lessons 41. The following important lessons emerge from the project:

(i) While the design was appropriate, it could have been further enhanced by the addition of recent developments and best practices such as 24/7 water supply (para. 6 and footnote 29) while synchronizing the provision for sewer network and household property connections (paras. 8 and 11) to realize the project benefits in a timely manner.

(ii) Continued renewal of CTOs and payment of O&M fees for WTPs and STPs by PHED and project ULBs after the IPMU handed over the assets is necessary for compliance with statutory requirements (para. 24) and optimal maintenance of the plants (para. 32).28

(iii) Having a dedicated cadre in the IPMU, instead of staff on deputation, would have ensured continuity in implementation; and a legal cell in the IPMU would have improved handling of techno-legal cases (para. 38).

28 Under the State AMRUT Action Plan 2015–2016, the GOR is committed to 10-year O&M, the induction of contractual

staff, and e-governance. Eleven of the project towns are part of AMRUT.

14

(iv) The SOE threshold of $100,000 equivalent per individual payment should consider the institutional capacity and the size and nature of contracts (para. 18).

(v) The optimal contingency allocation could have avoided partial loan cancellation or loan extension (para. 17).

(vi) Consistency with the facility DMF, numerical targets, and the classification of indicators would have enabled easy measurement of outputs and outcomes (para. 8).

(vii) The project design was informed by a strong interplay among factors such as (a) the capacity of executing agencies to develop project components, and safeguard management; (b) the scope of project interventions and determination of performance targets; and (c) the selection of implementation arrangements (paras. 7, 16, 20, 23, 26, 28, and 38).

(viii) Close monitoring of consultants’ performance is necessary for optimal use of consulting services and timely delivery of outputs (para. 22).

(ix) Determination of the contract period needs to be realistic to ensure adherence to implementation milestones (paras. 19 and 38).

(x) End-to-end e-procurement and contract management systems would augment the IPMU’s capacity (para. 21).

(xi) Enhancing project preparedness before the contract award (e.g., through the preparation of detailed designs, finalization of the land required, and coordination for utility shifting) helps deliver projects in a timely, responsive, and efficient manner (paras. 7, 16, 19, 20, and 38).

(xii) Emphasis on financial management requirements by the borrower’s auditors, project authorities, and ADB is required for continued compliance with financial covenants (paras. 25, 26, 38, and 39).

B. Recommendations 42. The project-specific recommendations for project implementation are as follows:

(i) The subproject design should incorporate the latest developments (e.g., 24/7, UFW reduction) (para. 6 and footnote 29) and ensure comprehensive end-to-end sector interventions (STPs, sewerage network, and HSCs) (paras. 8 and 11) for maximizing project benefits.29

(ii) The line departments should ensure the renewal of CTOs and payment of O&M fees for WTPs and STPs after taking over the assets (paras. 24 and 32).

(iii) The IPMU should be strengthened with a techno-legal cell to handle contract arbitration (para. 38).

(iv) The SOE threshold may be set based on the institutional capacity of the IPMU to manage funds (para. 17).

(v) The allocation of large sums under contingencies should be rationalized (para. 6). (vi) Consistency with numerical targets and the classification of indicators across

DMFs of the MFF and its component projects should be ensured to assess the respective and cumulative contributions toward overall achievements and objectives (para. 8).

43. General recommendations for future projects are:

(i) A realistic matrix of the executing agency’s capacity and implementation arrangements against the project scope and achievable performance targets

29 This is incorporated into subsequent ADB loans to Rajasthan (footnote 26) and a proposed project for smaller towns,

where property connections are included in the scope of the project to ensure concurrent completion.

15

should be determined at the project design stage for project success (paras. 19, 22, and 38).

(ii) A hybrid payment structure involving deliverable-based payments for designs, reports, and documents, and input-based payments for supervision would improve the accountability and effectiveness of consultants’ performance (para. 22).

(iii) Realistic contract periods should be provided for complex contracts involving multiple stakeholders and implementation complexities (paras. 19 and 38).

(iv) Robust procurement and contract management should be established by extending e-procurement beyond e-submission and establishing a database for contractors’ performance (para. 21).

(v) For improved sustainability and alignment with Strategy 2030, Operational Priorities 6 (Strengthening Governance and Institutional Capacity), future project should strengthen the public financial management at the state and the ULB level (para. 32).

(vi) Clear identification of interventions and the requisite technical detailing and regulatory clearances before the award of contract will ensure smooth and timely execution (paras. 7, 19, and 38).

(vii) ADB should develop a supplementary financial procedures manual with specific sections on project accounting, including reconciliation with ADB’s disbursement records and ADB’s financial reporting and audit requirements. Inclusion and continued capacity building of the executing agency, including its financial management specialists and statutory auditors, in ADB’s financial management requirements from project inception through implementation is necessary (paras. 25, 26, and 38). ADB’s financial management specialist should field regular missions, recommend actions for improvement, and ensure continued compliance (para. 39).

44. Future monitoring. The IPMU should provide details of the renewal of CTOs for STPs and the payment of O&M fees to contractors by 30 September 2019. 45. Covenants. The covenants relating to the levy of SWM charges by ULBs should be ensured. 46. Timing of the project performance evaluation report. The project performance evaluation report should be prepared in 2020, by which time the subprojects will have been operational for more than 3 years.

16 Appendix 1

DESIGN AND MONITORING FRAMEWORK FOR PROJECT 2

Design Summary Performance Indicators/Targets Achievements

Impacts By the end of 2016: By the end of 2018:

Increased economic growth and sustained improvement in the urban environment and quality of life in the identified urban local bodies (ULBs) in Rajasthan (the Project ULBs).

Urban infrastructure services covered by the Project reaching an additional 20% population in the Project ULBs;

Achieved. Urban infrastructure services covered by project reached an additional 619,729 people, representing additional 39% of 14 ULBs’ population, exceeding 20% target;1

Number of sanitation related diseases in Project ULBs taking up sanitation subprojects decreased by 20%; and

Achieved. Annual incidence of sanitation related diseases decreased from 58,669 incidences in 2008 to 37,922 incidences in 2017 –an average 35% decrease in project 2 ULBs exceeding 20% target;2 and

Number of population below poverty line (BPL) with access to improved urban infrastructure services in the Project ULBs increased by 20%.

Achieved. 95% of BPL population (274,937) benefitted with access to improved urban infrastructure services in 10 ULBs.3 It is deemed that increase in access to improved urban infrastructure services to BPL population is proportionate (39%) to overall increase in access to urban services.

Outcomes By the end of 2013: By the end of 2018:4

Increased access to sustainable urban infrastructure and services for approximately 1.5 million people in the identified 12 Project ULBs by the end of the Project (2013).5

Water Supply:

90% population of the project ULBs (approximately 1.2 million people) are provided with treated piped water supply of 135 litres per capita per day (lpcd);

Achieved. 93% population or 1.44 million people in all 10 planned ULBs provided with treated piped water supply of 137 lpcd exceeding targets;

All connected households in the Project ULBs have water meters;

Achieved. 100% households connected under the project provided with water meters;

100% disinfected water supplied to connected consumers;

Achieved. Chlorination facilities provided in all 10 planned ULBs to ensure supply of 100% disinfected water to all connected consumers;

1 Source: PCR Mission. 2 Source: IPPMS Endterm Report. December 2018. 3 Source: Project ULBs. ULB-level baseline data on BPL not available. Current BPL data for Baran and Sikar also not

available. 4 Source: Investment Program Management Unit (IPMU), Government of Rajasthan. 5 Project 2 DMF envisaged to cover 12 ULBs with total population of 1.25 million. Water supply interventions were

planned in 10 ULBs to benefit 1.08 million population while wastewater interventions were planned in 7 ULBs to benefit 0.70 million population. At completion, project 2 covered 14 ULBs as wastewater interventions were dropped in Sikar but undertaken in Alwar and Jhalawar and widening of a railway-over-bridge was included in Alwar.

Appendix 1 17

Design Summary Performance Indicators/Targets Achievements

All water supply points in the Project ULBs connected with bulk meters;

Achieved. Water supply points in project ULBs connected with 63 bulk electro-magnetic flow meters;

Project ULBs have adequate storage facilities for water supply – minimum 20% of supply at the overhead storage reservoirs (OHSRs) and 2 hours supply at the clearwater reservoirs (CWRs); and

Achieved. Adequate storage facilities (87 reservoirs with 71 million liters cumulative capacity) developed and 2 hours supply at the CWRs made available in project ULBs; and

Unaccounted for water (UFW) in the Project ULBs is reduced by 20%.

Achieved. Fully achieved in 9 of the 10 ULBs and yet to be achieved in 1 ULB (Bharatpur).

Sewerage and Sanitation:

Areas with population density of 150 households/hectare & water supply of 135 lpcd are provided with sewerage facilities including sewage treatment plants (STPs) in selected project ULBs;

Achieved. Sewerage facilities provided in 8 ULBs, including STPs in 6 ULBs (STPs existed in remaining 2 ULBs) benefitted over 0.82 million (100%) of the ULB population;

Reduction in the volume of wastewater discharged to water bodies; and

Achieved. Volume of wastewater discharged to water bodies reduced by over 20 million liters per day (mld); and

Schools are provided with toilets and water connections where Project related facilities are constructed.

Toilets and water connections available in 100% schools in all program ULBs using government funds.

Urban Drainage:

Drainage outfalls rehabilitated and newly constructed roadside drains provided in the Project ULBs that are identified as having high risks of flooding and/or have drainage masterplans.

Achieved. Drainage outfalls provided in Bharatpur and Sikar based on the masterplan and assessed risks of flooding. New roadside drains were provided in Bundi and other ULBs where road works were undertaken.

Urban Transport

Improved traffic flow within the Project ULBs and travel times between zones maintained at present levels or reduced in Project ULBs taking up urban roads and transport subprojects.

Achieved. Traffic flow improved and travel times between zones reduced from average 40 minutes per crossing to less than 5 minutes during peak hours in 9 ULBs where transport subprojects were taken up benefiting over 1.76 million residents. Railway-over-bridges constructed in 6 ULBs eliminated high traffic (25-40 trains per day) gated railway level-crossings. Two bridges were constructed over a river in 1 ULB.

18 Appendix 1

Design Summary Performance Indicators/Targets Achievements

Improved capacities of, and sustainable management of urban services by, the Project ULBs by the end of the Project

Improved Institutional Capacity:

Project ULBs meet O&M costs of all urban services and have sound financial management practices; and

Achieved. ULBs and public health engineering department (PHED) meet O&M costs of all urban services through well-structured and planned budgetary allocations based on revenue-sharing model between the three tiers of the government, regularity of transfers from State and Central Finance Commissions, tariff enhancements, and improved tax collections; and

Project ULBs and state-level bodies have adequately trained and skilled human resources to operate and maintain the urban facilities and services.

Achieved. ULBs’ and PHED’s capacities strengthened under a structured capacity building plan; staff effectively reoriented towards professionalization of municipal services and urban governance.

Outputs Water Supply

Water supply subprojects successfully implemented

Existing system rehabilitation and UFW reduction program, including, replacement of excessively leaking carrier mains; distribution mains and house connections, refurbishment/ replacement of pumping machinery, etc.

Achieved. UFW reduction undertaken through rehabilitation of existing system, replacement of leaking carrier mains; distribution mains (totaling 1,185 km), metered house connections, and old pumping machinery in 10 project ULBs;

Installation/ replacement of consumer water meters in 100% of the water supply connections, and installation of flow meters at all supply points;

Achieved. Over 87,000 consumer water meters and 63 bulk electro-magnetic flow meters at water supply points installed in 10 ULBs;

provision of chlorination facilities to achieve 100% disinfection of supply;

Achieved. Chlorinators or online chlorination facilities provided in all 10 planned ULBs to achieve 100% disinfection of supply;

Source augmentation of Bundi and Rajsamand; storage reservoirs (CWRs and OHSRs) and distribution networks in Bharatpur, Bundi, Dholpur, Karauli, Rajsamand, Sawai Madhopur, Churu, Barmer, Nagaur, and Sikar; water treatment plant (WTP) in Dholpur and Rajsamand; and

Achieved. Source augmentation works (44 mld) in Bundi and Rajsamand; 87 storage reservoirs (CWRs and OHSRs) of cumulative 71 million liters storage capacity and 1,185 km of distribution system in the 10 planned ULBs; and 2 WTPs (17 mld in Rajsamand and 15 mld in Dholpur) completed; and

Rehabilitation of existing and construction of new facilities to increase piped water supply coverage to 90% of the households.

Achieved. Rehabilitation of existing and construction of new facilities increased piped water supply coverage to 250,521 households (93%), exceeding target.

Appendix 1 19

Design Summary Performance Indicators/Targets Achievements

Sewerage and sanitation subprojects successfully implemented

Sewerage and Sanitation

Sewerage system – outfall, trunk sewers, tertiary networks and household connection in priority areas – completed and STPs constructed in Bundi (10 mld), Barmer (10 mld), Dholpur (10 mld), Nagaur (10 mld), Sawai Madhopur (10 mld), Rajsamand (8 mld) and Sikar (10 mld).

Achieved. 506.31 km of sewer network, including outfall, trunk sewers and tertiary networks laid in priority areas in 8 ULBs (Alwar, Barmer, Bundi, Dholpur, Jhalawar, Nagaur, Sawai Madhopur and Rajsamand), exceeding the target of 7 ULBs (footnote 5 of Appendix 1);

Substantially achieved. STPs constructed in 6 out of targeted 7 ULBs – Bundi (8 mld), Barmer (10 mld), Dholpur (10 and 3 mld), Nagaur (8 mld), Rajsamand (5 mld) and Sawai Madhopur (10 mld) – based on capacities refined during detailed engineering design totaling 54 mld as against the 68 mld target.

Urban drainage subprojects successfully implemented

Urban Drainage

Storm-water drains constructed in Baran, Bharatpur and Sikar