4 th SAP Meeting, GRI SSE Milano, 4 May 2011 GRI South South-East Region.

30

4 th SAP Meeting, GRI SSE Milano, 4 May 2011 GRI South South-East Region

-

Upload

jewel-griffin -

Category

Documents

-

view

214 -

download

1

Transcript of 4 th SAP Meeting, GRI SSE Milano, 4 May 2011 GRI South South-East Region.

4th SAP Meeting, GRI SSE

Milano, 4 May 2011

GRI South South-East Region

24th SAP Meeting, Milan, 4 May 2011

Agenda

Agenda Topics Rapporteur

Arrival and registration

1. EU Gas Target Model and SSE region Co-chairs

2. Future role of the Regional Initiatives Co-chairs

3. Energy Work Plan 2012-2014 SAP

4. AoB Co-chairs

34th SAP Meeting, Milan, 4 May 2011

1. EU Gas Target Model and SSE region

44th SAP Meeting, Milan, 4 May 2011

Internal EU gas market

• What do we want to achieve?• Internal EU gas market

• How we want to achieve this?• First we need to enable functioning wholesale

markets (“markets”), where they do not exist yet.• As second step we need to connect these markets

better to move forward to an integrated market.

Basic conditions need to be established in all countries

No one size fits all solution possible

54th SAP Meeting, Milan, 4 May 2011

Overview of the MECO-S model for EU gas market integration

Improve effectiveness by realizing economic pipeline investments

MECO-S Model

Pillar 1:Enable functioning wholesale markets

Pillar 2:Tightly

connect markets

Pillar 3:Enable secure

supply patterns

Pillar 1: Structuring network access to the European gas grid in a way that enables functioning wholesale markets so that every European final customer is easily accessible from such a market.

Pillar 2: Fostering short- and mid-term price alignment between the functioning wholesale markets by tightly connecting the markets through facilitating cross-market supply and trading and potentially implementing market coupling as far as the (at any time) given infrastructure allows.

Pillar 3: Enabling the establishment of secure supply patterns to the functioning wholesale markets.

Foundation: Improving the effectiveness of pillars 1 to 3 by making sure that economic investments in pipelines are realized.

64th SAP Meeting, Milan, 4 May 2011

Where do we have functioning wholesale markets yet?

• Depending on the definition applied between 1 and 5 functioning gas markets exist in Europe today!

• Shall we strive to create 25 functioning gas markets?

• Will this foster competition in the retail markets?

• Would the German gas market have developed the same if we had not reduced the number of zones (~20) by merging them?

• Would the French gas market have developed the same if we had not reduced the number of zones (5) by merging them?

Can markets be enabled without liquidity only via better connection?

74th SAP Meeting, Milan, 4 May 2011

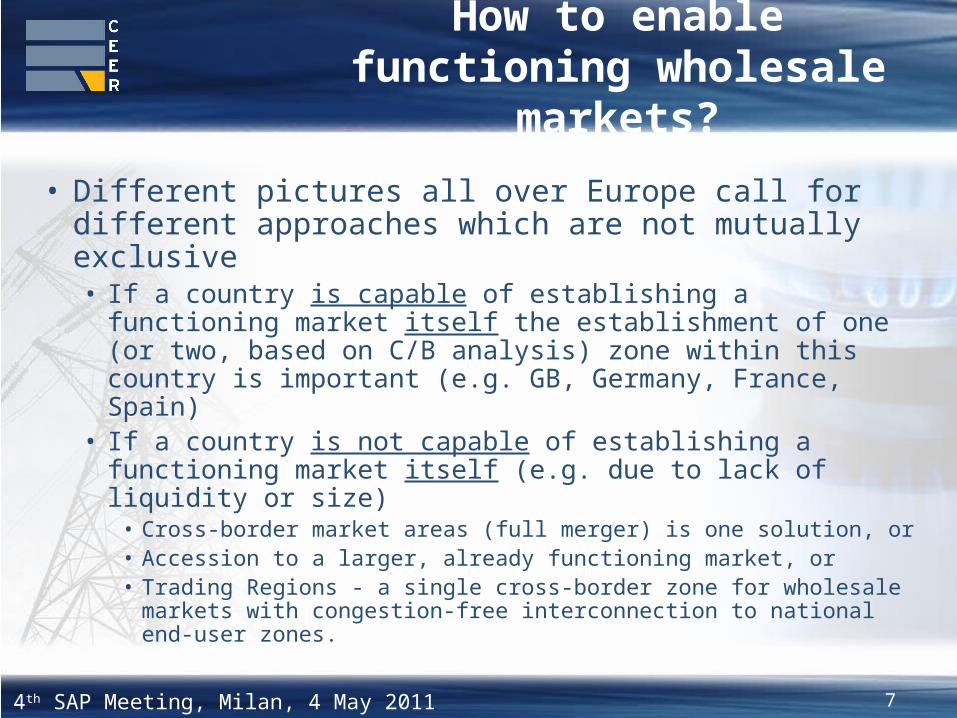

How to enable functioning wholesale markets?

• Different pictures all over Europe call for different approaches which are not mutually exclusive• If a country is capable of establishing a functioning

market itself the establishment of one (or two, based on C/B analysis) zone within this country is important (e.g. GB, Germany, France, Spain)

• If a country is not capable of establishing a functioning market itself (e.g. due to lack of liquidity or size)

• Cross-border market areas (full merger) is one solution, or • Accession to a larger, already functioning market, or• Trading Regions - a single cross-border zone for wholesale

markets with congestion-free interconnection to national end-user zones.

84th SAP Meeting, Milan, 4 May 2011

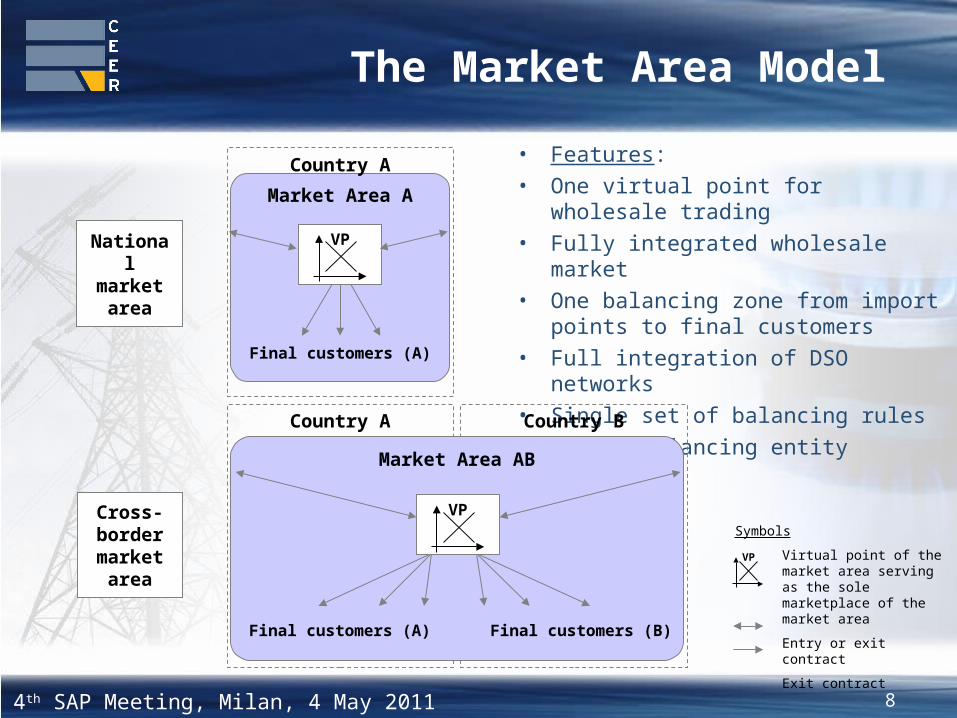

The Market Area Model

• Features:

• One virtual point for wholesale trading

• Fully integrated wholesale market

• One balancing zone from import points to final customers

• Full integration of DSO networks

• Single set of balancing rules

• Single balancing entity

Symbols

Virtual point of the market area serving as the sole marketplace of the market area

Entry or exit contract

Exit contract

Market Area A

Country A

Country A Country B

Market Area AB

Cross-border market

area

National market

area

VP

Final customers (A) Final customers (B)

VP

Final customers (A)

VP

94th SAP Meeting, Milan, 4 May 2011

The Trading Region Model

Country A Country B

Trading Region AB

End userzone A

End userzone B

Final customers (A) Final customers (B)

VP

Legend and Symbols

End user zone = National balancing zone for national final customers, no matter the system (distribution or transmission) they are connected to

Trading Region AB = Cross-border entry/exit system including all nominated points on the transmission systems of countries A and B

Entry or exit contract

Exit contract

Virtual point of the trading region serving as the sole marketplace of the trading region and all attached end user zones. Shifting of gas between trading region and end user zone is done by nominating a virtual exit on the VP.

VP

Features:• One virtual point for wholesale

trading• Fully integrated wholesale market• Trading region is basically kept free

of imbalances• Final customers are balanced in

national end user zones that may reflect national specifics

• End user balancing may be done by national balancing entity

• Congestion-free interconnection between trading region and end user zones through the common virtual point ( virtual exit to end user zone)

104th SAP Meeting, Milan, 4 May 2011

What needs to be done in all approaches?

• Prerequisite for merging market areas and creating trading regions:• Absence or at least limited physical congestion

• As soon as we are talking about cross-border integration the following issues have to be analysed• Entry / Exit Tariffication• Redistribution of revenues and costs• Alignment of regulatory framework• Investments• TSO as well as NRA cooperation

114th SAP Meeting, Milan, 4 May 2011

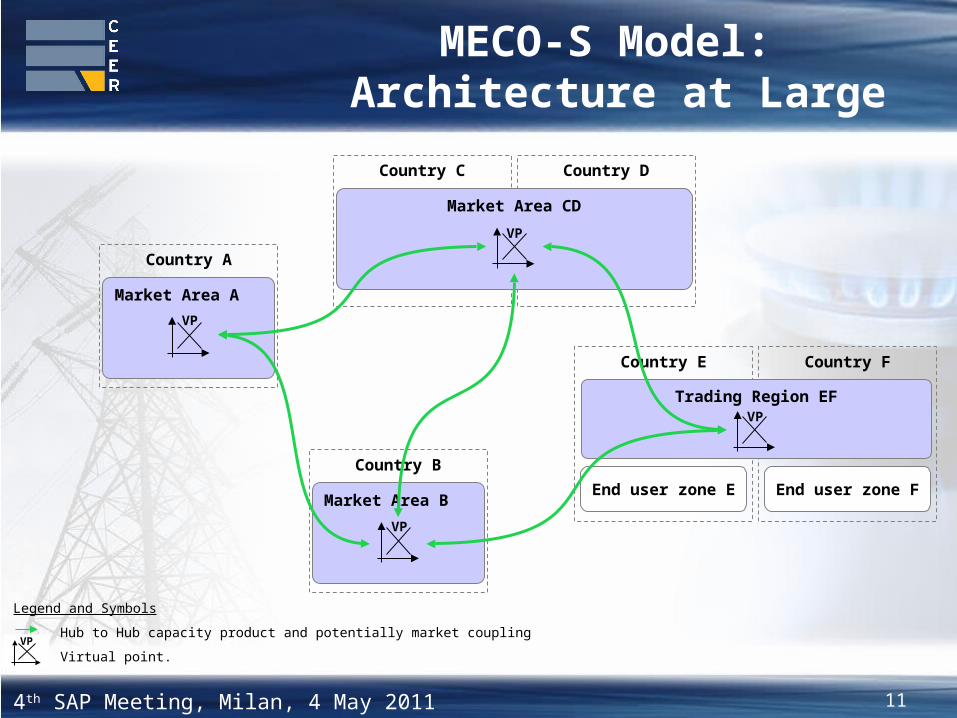

MECO-S Model: Architecture at Large

Legend and Symbols

Hub to Hub capacity product and potentially market coupling

Virtual point.VP

Country E Country F

Trading Region EF

End user zone E End user zone F

Country C Country D

Market Area CD

Market Area A

Country A

Market Area B

Country B

VP

VP

VP

VP

124th SAP Meeting, Milan, 4 May 2011

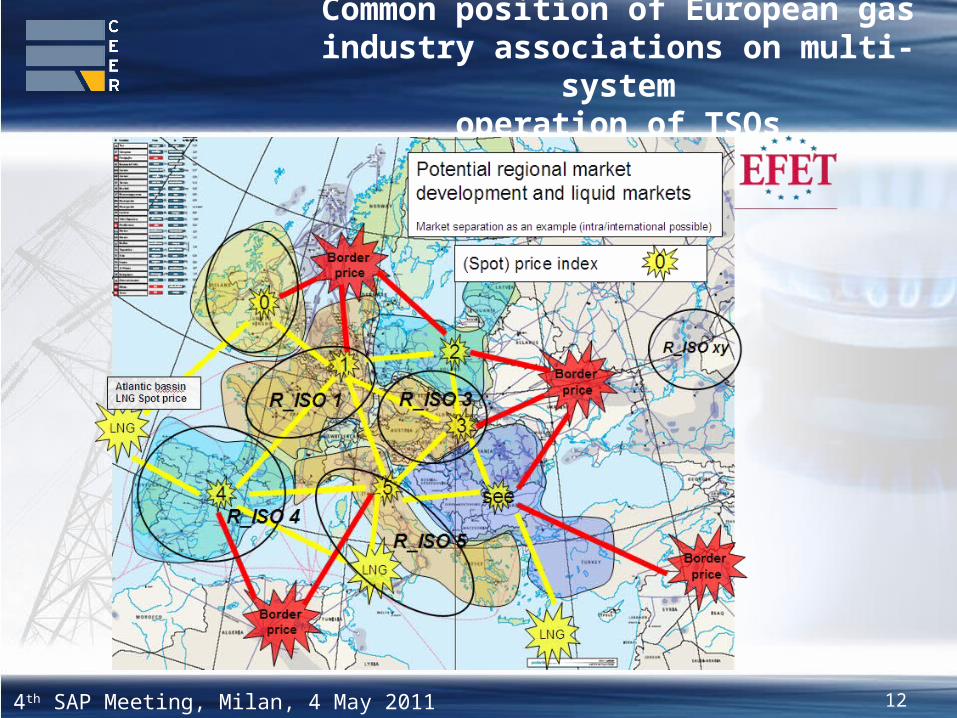

Common position of European gas industry associations on multi-system

operation of TSOs

134th SAP Meeting, Milan, 4 May 2011

The second step: connecting markets

• Connecting markets means price alignment between functioning markets and thereby driving market efficiency and public welfare on a European scale

• Connecting markets can happen at different timescales.• In the afternoon session we will discuss a

measure for short-term trading.

144th SAP Meeting, Milan, 4 May 2011

2. Future role of the Regional Initiatives

154th SAP Meeting, Milan, 4 May 2011

2. Tasks of the Regional Initiatives

• Majority of the respondents are in favour of the tasks proposed by the Commission

• (early) implementation of Network Codes • Infrastructure development• Test bed for new ideas

• Better alignment with follow-up to Infrastructure Package and Security of Supply Regulation is needed

• Doubts on market coupling as part of target model – more analysis needed

164th SAP Meeting, Milan, 4 May 2011

2. Composition of the Regional Initiatives

• Most of respondents favour flexibility - no need for a legislative initiative

• Mixed views on the proposal to include Italy in the South Region

• Mixed views on the proposal to split the South-South East Region. More focussed agenda needed versus fear that split might be counterproductive in terms of efficiency. Coherence with infrastructure package needed

• Mixed views on overlapping countries

174th SAP Meeting, Milan, 4 May 2011

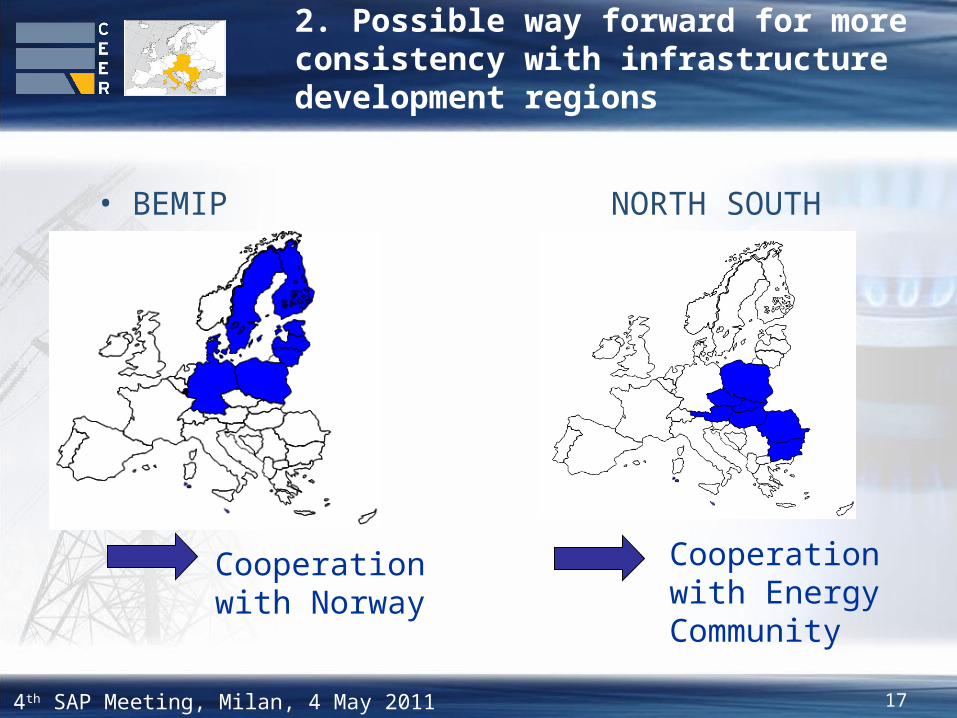

2. Possible way forward for more consistency with infrastructure development regions

• BEMIP NORTH SOUTH

Cooperation with Energy Community

Cooperation with Norway

184th SAP Meeting, Milan, 4 May 2011

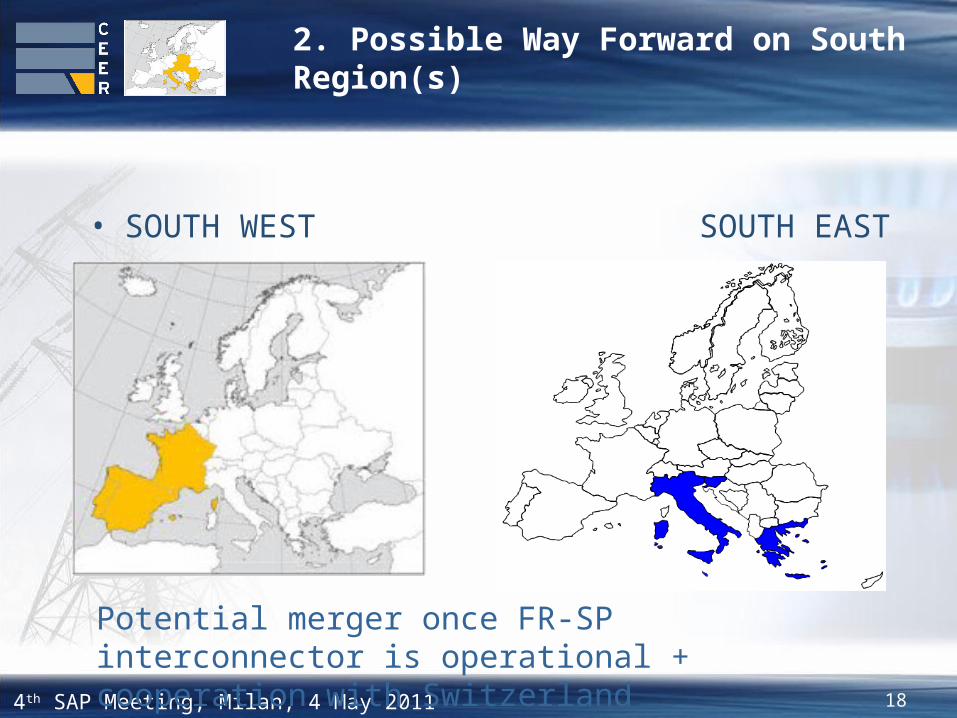

2. Possible Way Forward on South Region(s)

• SOUTH WEST SOUTH EAST

Potential merger once FR-SP interconnector is operational + cooperation with Switzerland

194th SAP Meeting, Milan, 4 May 2011

2. Governance of the RIs

• Large support for stronger involvement of Member States

• Industry regulator dialog should remain driving axe

• Added value of Regional Steering Committee is

questioned ; structures should remain lean and effective

• Stakeholders, including ENTSO-G, to be involved in

decision making and not only in information sessions of

stakeholder group

• Support for increased involvement of Commission and

ACER

• Support for mandatory presentation of work plan to ACER

204th SAP Meeting, Milan, 4 May 2011

2. Possible way forward for Governance

Regional Coordination CommitteePresidency: designated NRA or Commission

NRAsACERCommissionRepresentative ENTSOGRepresentative EurogasAt least one meeting per year with Member States

Stakeholder Group Implementation

Group

Ad hoc composition

214th SAP Meeting, Milan, 4 May 2011

2. Preliminary conclusions

• Request to existing GRIs to send work program 2012-2014 to ACER and Commission by September

• Commission could envisage to draft by end of the year interpretative note clarifying role and responsibilities of RIs, including governance and composition

224th SAP Meeting, Milan, 4 May 2011

2. Summary of Coordination meeting with ACER

• The elaboration of concrete, ambitious, realistic and consistent roadmaps should be our top-priority for the next 2 months

• Their endorsement by all stakeholders, including MS, is essential

• More focused on projects than on regions• When relevant, designation of a NRA to lead and report

on each identified project should be promoted• Close monitoring, transparency and effectiveness should

be continuously looking for in order to maintain stakeholders' confidence

234th SAP Meeting, Milan, 4 May 2011

3. Energy Work Plan 2012-2014

• Energy Council on February 4th: “we will have achieved an IEM by 2014”

• Coordination meeting by Lead Regulators of ERI and GRI with ACER

• European Commission requested a 3 year Road Map (The Energy Work Plan) aimed at achieving an IEM by 2014

244th SAP Meeting, Milan, 4 May 2011

3. Energy Work Plan 2012-2014

1. Enabling functioning Wholesale Markets

2. Connecting Wholesale Markets

3. Enable secure supply patterns

4. Action Points and Pilot Projects

• The presented topics will be forwarded to ACER and the European Commission who then will combine the Work Plans from all regions in order to gather an overview of the pan-European Status-quo and to create an outlook for the next 3 years.

254th SAP Meeting, Milan, 4 May 2011

3. Energy Work Plan 2012-2014

Questions to SAP

1. Is it realistic to have one fully integrated market area?

2. In which MS of the region a fully functioning wholesale market can be established by 2014?

3. Alternatively, with which MS a closer integration would be necessary to achieve a functioning wholesale market by 2014? What will be the impact of merging market areas (eliminating capacity booking on some IPs)?

4. Which pilot projects to start with in order to establish this closer integration?

264th SAP Meeting, Milan, 4 May 2011

3. Energy Work Plan 2012-2014

Questions to regulators

5. Who is involved in the project?

6. Is the regulator taking the lead in this project?

Questions collected right here and in written

Communication – then a draft European Work Plan will be

circulated in order to present it to the EC by end of June

274th SAP Meeting, Milan, 4 May 2011

3. Energy Work Plan 2012-2014

Action Points and Pilot Projects

GRI-SSE-AP-1: Trading Points

GRI-SSE-AP-2: Improvement of Hub-to-Hub Trading

GRI-SSE-AP-3: Implementation of OBAs at IPs

GRI-SSE-AP-4: Reverse Flow Investments

GRI-SSE-AP-5: MS’ improvement of Regional Solidarity

GRI-SSE-AP-6: TSO Regional 10 Year Network

Development Plan (2012)

284th SAP Meeting, Milan, 4 May 2011

4. AoB

• Probably – SoS meeting, beginning of December (one year after SoS Regulation)

• Polish Network Grid

294th SAP Meeting, Milan, 4 May 2011

Closure

Thank you very much!

304th SAP Meeting, Milan, 4 May 2011

Michael Schmöltzer

Head of Gas Department E-Control Austria+43(0)1 – 24 7 24 / [email protected]

www.e-control.atwww.ceer.org

Contact