4 q16 earnings presentation final

33

4Q16 EARNINGS PRESENTATION NYSE: DOOR

-

Upload

masoniteinvestors -

Category

Investor Relations

-

view

3.095 -

download

0

Transcript of 4 q16 earnings presentation final

4Q16 EARNINGS PRESENTATION

NYSE: DOOR

2 2

Safe Harbor / Non-GAAP Financial Measures

SAFE HARBOR / FORWARD LOOKING STATEMENT

This investor presentation contains forward-looking information and other forward-looking statements within the meaning of applicable Canadian and/or U.S. securities laws, including our discussion of

our 2017 outlook or long term growth framework, housing and other markets, and the effects of our strategic initiatives. When used in this Investor Presentation, such forward-looking statements may

be identified by the use of such words as “may,” “might”, “could,” “will,” would,” “should,” “expect,” “believes,” “outlook,” “predict,” “forecast,” “framework,” “objective,” “remain,” “anticipate,” “estimate,”

“potential,” “continue,” “plan,” “project,” “targeting,” or the negative of these terms or other similar terminology.

Forward-looking statements involve significant known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements of Masonite, or industry

results, to be materially different from any future plans, goals, targets, objectives, results, performance or achievements expressed or implied by such forward-looking statements. As a result, such

forward-looking statements should not be read as guarantees of future performance or results, should not be unduly relied upon, and will not necessarily be accurate indications of whether or not such

results will be achieved. Factors that could cause actual results to differ materially from the results discussed in the forward-looking statements include, but are not limited to, our ability to successfully

implement our business strategy; general economic, market and business conditions; levels of residential new construction; residential repair, renovation and remodeling; and non-residential building

construction activity; the United Kingdom passage of legislation authorizing its exit from the European Union; competition; our ability to manage our operations including integrating our recent

acquisitions and companies or assets we acquire in the future; our ability to generate sufficient cash flows to fund our capital expenditure requirements, to meet our pension obligations, and to meet our

debt service obligations, including our obligations under our senior notes and our ABL Facility; labor relations (i.e., disruptions, strikes or work stoppages), labor costs and availability of labor; increases

in the costs of raw materials or any shortage in supplies; our ability to keep pace with technological developments; the actions taken by, and the continued success of, certain key customers; our ability

to maintain relationships with certain customers; the ability to generate the benefits of our restructuring activities; retention of key management personnel; environmental and other government

regulations; and limitations on operating our business as a result of covenant restrictions under our existing and future indebtedness, including our senior notes and our ABL Facility.

NON-GAAP FINANCIAL MEASURES

Our management reviews net sales and Adjusted EBITDA (as defined below) to evaluate segment performance and allocate resources. Net assets are not allocated to the reportable segments.

Adjusted EBITDA is a non-GAAP financial measure which does not have a standardized meaning under GAAP and is unlikely to be comparable to similar measures used by other companies. Adjusted

EBITDA should not be considered as an alternative to either net income or operating cash flows determined in accordance with GAAP. Additionally, Adjusted EBITDA is not intended to be a measure of

free cash flow for management's discretionary use, as it does not include certain cash requirements such as interest payments, tax payments and debt service requirements. Beginning with the third

quarter of 2015, we revised our calculation of Adjusted EBITDA to separately exclude loss (gain) on disposal of subsidiaries. This definition of Adjusted EBITDA differs from the definitions of EBITDA

contained in the indenture governing the 2023 Notes and the credit agreement governing the ABL Facility. Adjusted EBITDA, as calculated under our ABL Facility or senior notes would also include,

among other things, additional add-backs for amounts related to: cost savings projected by us in good faith to be realized as a result of actions taken or expected to be taken prior to or during the

relevant period; fees and expenses in connection with certain plant closures and layoffs; and the amount of any restructuring charges, integration costs or other business optimization expenses or

reserve deducted in the relevant period in computing consolidated net income, including any one-time costs incurred in connection with acquisitions. The tables in the appendix to this presentation

reconcile Adjusted EBITDA to net income (loss) attributable to Masonite for the periods indicated. We are not providing a quantitative reconciliation of our Adjusted EBITDA outlook to the corresponding

GAAP information because the GAAP measures that we exclude from our Adjusted EBITDA outlook are difficult to predict and are primarily dependent on future uncertainties.

Adjusted EBITDA margin is defined as Adjusted EBITDA divided by Net Sales. Management believes this measure provides supplemental information on how successfully we operate our business.

Adjusted EPS for the quarter ended January 1, 2017 and January 3, 2016 is diluted earnings per common share attributable to Masonite (EPS) less asset impairment charges, loss (gain) on disposal of

subsidiaries and loss on extinguishment of debt, net of related tax expense (benefit). Management uses this measure to evaluate the overall performance of the Company and believes this measure

provides investors with helpful supplemental information regarding the underlying performance of the Company from period to period. This measure may be inconsistent with similar measures

presented by other companies.

3

Agenda

1. Company Overview

2. 2016 Financial Review

3. Financial Outlook

4. Summary / Q&A

4

COMPANY OVERVIEW

5 5

$105.9

$137.1

$204.2

$252.5

6.1%

7.5%

10.9%

12.8%

2013 2014 2015 2016

2016 Full Year Highlights

Strong NA Residential sales volume

Continued strength at DSI despite

uncertainty in UK

6th consecutive year of positive AUP

Q4 was the 15th consecutive quarter of

positive AUP

Digital Innovation Center opened

Transformation projects in Architectural

business

Execution of share repurchase program

$150 million authorized on 2/24/16

$109 million, or 1.7 million shares,

purchased in 2016

Authorized up to an additional $200

million on February 22, 2017

Adj. EBITDA* Growth & Margin Expansion

2016 Adjusted EBITDA* increased 24%

2016 incremental margins >45%

Solid progress toward achieving long term

growth framework objectives

(*) – See safe harbor/non-GAAP financial measures on page 2 for definitions and other information and appendix for non-GAAP reconciliations

($ in millions)

6 6

New Business Wins

2016 Execution

2017 Wins

Approx. $50mm of incremental net sales

Successful shift from Reliabilt private label

to Masonite branded products

Outperformed the millwork category at

new stores

Millwork partner of the year at Home

Depot Canada (2015 & 2016)

Home Depot Florida business win

New products and assortment

improvements to drive higher AUP

Transition plans to new Masonite brand

imagery

7 7

8 8

Brand Re-Launch

Change the conversation around

doors

Make the door

category more relevant

Take a leadership

position by creating a

differentiated Masonite brand

experience

Rise above the sea of sameness

and stand apart from others in the

category

9 9

Brand Re-Launch – Brand Pillars

Exceptional Quality

Unmatched Service

Customer-Driven

Innovation

Trend Leadership

10 10

Brand Re-Launch – Key Enablers

Innovative Products

Innovative Marketing

Innovative Routes to Market

Masonite Innovation Center, W. Chicago, IL

11 11

Brand Re-Launch – All New Website

Innovating the digital approach on how to buy

a door at the new masonite.com

12 12

Digital Innovations

Opened Digital Innovation

Center in Ybor City, Tampa

USA Wood Door – All new

web-based door configurator

Continued roll out of ERP in

Architectural business

13 13

Manufacturing Capabilities

New fiberglass press lines

Digital Initiatives

ERP, configurator tools

Automation Initiatives

UK paint line

Investing in the Business

Previous Projects Capex Spending

30%

70%

Maintenance Capex Strategic/Growth Capex

Future Projects

Productivity Improvements

Interior plant re-configuration

Manufacturing Efficiency

Harmonize architectural product

specifications

Cost Reduction

Optimize wood components yield

Increased investment in 2016 and

2017 to support:

Market growth

Digital capabilities

Product development

Operational excellence

14

FINANCIAL REVIEW

15 15

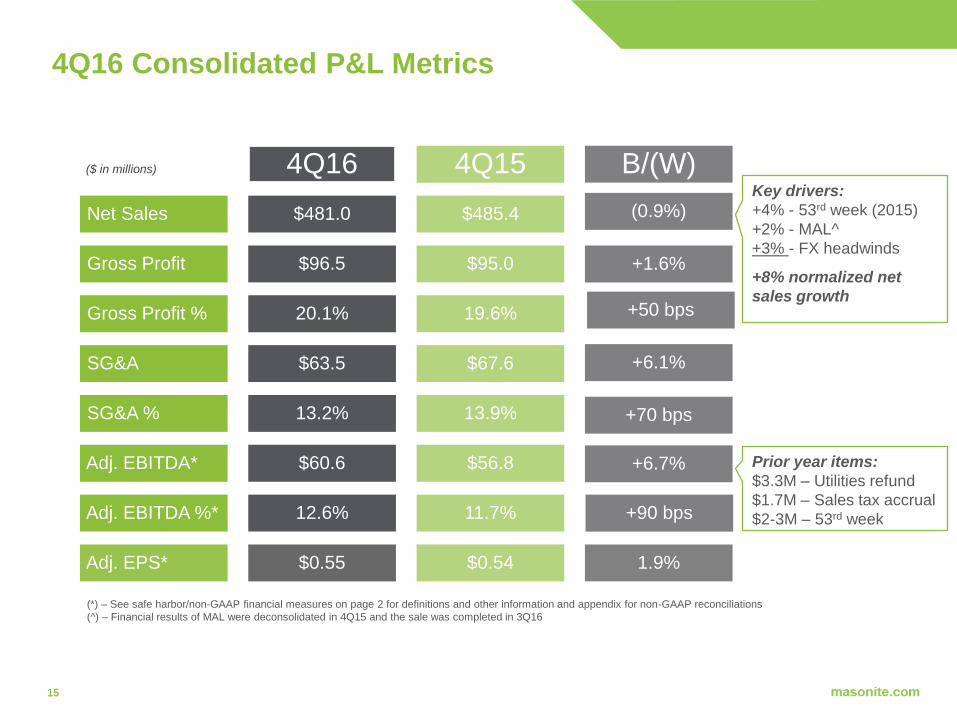

4Q16 Consolidated P&L Metrics

Net Sales

Gross Profit

Gross Profit %

SG&A

SG&A %

Adj. EBITDA*

Adj. EBITDA %*

Adj. EPS*

4Q16

$481.0

$96.5

20.1%

$63.5

13.2%

$60.6

12.6%

$0.55

4Q15

$485.4

$95.0

19.6%

$67.6

13.9%

$56.8

11.7%

$0.54

B/(W)

(0.9%)

+1.6%

+50 bps

+6.1%

+70 bps

+6.7%

+90 bps

1.9%

($ in millions)

Key drivers:

+4% - 53rd week (2015)

+2% - MAL^

+3% - FX headwinds

+8% normalized net

sales growth

Prior year items:

$3.3M – Utilities refund

$1.7M – Sales tax accrual

$2-3M – 53rd week

(*) – See safe harbor/non-GAAP financial measures on page 2 for definitions and other information and appendix for non-GAAP reconciliations

(^) – Financial results of MAL were deconsolidated in 4Q15 and the sale was completed in 3Q16

16

North American Residential

9% sales volume growth in 4Q

Double digit growth in retail

-0.2% AUP in 4Q16, +1.2% AUP in FY16

Stronger relative growth continues in interior vs.

entry creating AUP headwind

Decline in Mexican peso negatively impacted net sales

by approximately $2 million in 4Q16.

Notified of additional business wins in retail and

wholesale to begin in 2017

($ in millions) 2016 2015 Diff 2016 2015 Diff

Net Sales $336.7 $310.9 +8% $1,351.3 $1,193.2 +13%

Net sales ex-Fx +9% +15%

Adj. EBITDA $49.9 $45.6 +9% $212.6 $165.6 +28%

Margin 14.8% 14.7% +10bps 15.7% 13.9% +180bps

Fourth Quarter Full Year

(*) – See safe harbor/non-GAAP financial measures on page 2 for definitions and other information and appendix for non-GAAP reconciliations

*

17

Europe

Uneven UK new housing market

Private housing market remains relatively stable

Public housing market weaker on Brexit-related

uncertainty

RRR demand remains robust, with DSI delivering 15%

sales volume growth in 4Q

Weakness in Pound Sterling negatively impacted net

sales by approximately $13 million in 4Q16

Price increase across all UK brands effective as of

January 1, 2017

($ in millions) 2016 2015 Diff 2016 2015 Diff

Net Sales $68.3 $81.3 -16% $301.2 $311.8 -3%

Net sales ex-Fx +0.5% +6%

Adj. EBITDA $7.9 $9.9 -20% $38.8 $30.5 27%

Margin 11.6% 12.2% -60bps 12.9% 9.8% +310bps

Fourth Quarter Full Year

(*) – See safe harbor/non-GAAP financial measures on page 2 for definitions and other information and appendix for non-GAAP reconciliations

*

18

Architectural

Strong 4Q15 December sales volume contributed to

difficult 4Q16 comparable

AUP growth driven by mix shift to higher end doors

Demand increase of high end doors through our

Harring brand

High demand in lower end stock doors

experienced in 4Q15

Digitizing the quick ship model at USA Wood Door

($ in millions) 2016 2015 Diff 2016 2015 Diff

Net Sales $70.2 $74.8 -6% $297.9 $291.8 +2%

Net sales ex-Fx -6% +3%

Adj. EBITDA $5.8 $4.9 +18% $25.2 $23.3 +8%

Margin 8.3% 6.6% +170bps 8.4% 8.0% +40bps

Fourth Quarter Full Year

(*) – See safe harbor/non-GAAP financial measures on page 2 for definitions and other information and appendix for non-GAAP reconciliations

*

19 19

2016 Consolidated P&L Metrics

Net Sales

Gross Profit

Gross Profit %

SG&A

SG&A %

Adj. EBITDA*

Adj. EBITDA %*

Adj. EPS*

2016

$1,974.0

$409.6

20.8%

$260.4

13.2%

$252.5

12.8%

$3.03

2015

$1,872.0

$350.9

18.7%

$244.1

13.0%

$204.2

10.9%

$1.49

B/(W)

+5.4%

+16.7%

+210 bps

(6.7%)

(20 bps)

+23.7%

+190 bps

+103.4%

($ in millions)

Net sales +11%

excluding Fx and

adjusted for MAL

(*) – See safe harbor/non-GAAP financial measures on page 2 for definitions and other information and appendix for non-GAAP reconciliations

20 20

Liquidity, Credit & Debt Profile

Credit & Debt (millions of USD)

TTM Adj. EBITDA* $252.5 $204.2

TTM Interest Expense $28.2 $32.9

Total Debt $470.7 $468.9

Net Debt^ $399.0 $379.7

2016 2015

12 months

ended 1/1/2017

12 months

ended 1/3/2016

Unrestricted cash $71.7 $89.2

Total available liquidity $222.8 $234.0

Cash flow from operations $174.0 $161.0

Capital expenditures $82.3 $51.1

Share repurchases $109.2 NA

Liquidity & Cash Flow (millions of USD)

(*) – See safe harbor/non-GAAP financial measures on page 2 for definitions and other information and appendix for non-GAAP reconciliations

(^) – Net debt equals total debt less unrestricted cash

21 21

2017 Viewpoints*

Continued U.S. housing market growth

Expect mid to high-single digit growth in

U.S. housing completions

Expect mid-single digit growth in the

U.S. RRR market

PLR wins accretive to 2017

Market outperformance from Door Stop

International

New products and value-added services

continue supporting higher AUP

Price increases in all business

segments

Tightening labor market in U.S.

Increased hiring costs

Lower productivity from recent

employee hires

Uncertainty in UK new housing market

Modest commodities increases

Uncertainty around U.S. tax and

regulatory environment

Tailwinds Headwinds

(*) – Our 2017 viewpoints are a forward-looking statement and subject to risks and uncertainties. See "Safe Harbor/Forward Looking Statement”

22 22

2017 Outlook*

2017 P&L Metrics

Net Sales

Adjusted EPS^

+ 7% - 9% (+ 8% - 10% excl. Fx)

$4.10 - $4.60

Adjusted EBITDA ^ $285 - $305M

Capital Expenditures $80 - $85M

Tax Rate 19% – 23%

Cash Taxes $9 - $12M

Other Key Items

(*) – Based on 2017 viewpoints highlighted on prior page. Our 2017 outlook is a forward-looking statement and subject to risks and uncertainties. See "Safe

Harbor/Forward Looking Statement”

( )̂ – See definition of non-GAAP financial measures on page 2. We are not providing a quantitative reconciliation of our Adjusted EBITDA or Adjusted EPS outlook to the

corresponding GAAP information because the GAAP measures that we exclude from our Adjusted EBITDA and Adjusted EPS outlook are difficult to predict and are

primarily dependent on future uncertainties.

23 23

Long-Term Growth Framework*

Margin Factors

Cost Factors

Volume Leverage

~25% incremental margin on

volume

Return to 1.5M housing starts in

U.S. by 2019

Flat housing market in Canada

Mid single digit growth in RRR

market

Mid single digit growth in

non-residential construction

Uneven growth in UK new

residential construction

Introduction of new products at

higher price points

Leverage new branding to bring

focus to richer mix of products

Value-added services with higher

margin profiles

Pre-hanging and

pre-finishing

Quick ship options

Custom machining and

finishing

Tightening labor market

Longer term materials cost

inflation

Focus on increasing factory

productivity

Continued investments in R&D

(*) - Company long term growth framework is a forward-looking statement and subject to risks and uncertainties. See "Safe Harbor/Forward Looking Statement”

24 24

12.8%

2016 2019

$2.0

2016 2019

Long-Term Growth Framework

7% - 9%

CAGR

16% - 17%

Adjusted EBITDA* Margin

Net Sales

( )̂ - Company long term growth framework is a forward-looking statement and subject to risks and uncertainties. See "Safe Harbor/Forward Looking Statement”

(*) – See definition of Adjusted EBITDA on page 2. We are not providing a quantitative reconciliation of our Adjusted EBITDA or Adjusted EPS outlook to the corresponding GAAP information because the GAAP

measures that we exclude from our Adjusted EBITDA and Adjusted EPS outlook are difficult to predict and are primarily dependent on future uncertainties.

Cash Flow Deployment

CapEx to Support Growth

Opportunistic Share

Repurchase

Strategic Acquisitions

Fund Working Capital

25

SUMMARY

26 26

• More efficient footprint

• Simplify the product

offering

• Improve productivity

• Decrease lead times

Architectural Transformation Improving Productivity Elevating the Door Category

• Efficient routes to market

• Automate the process

• Digital tools to improve

ordering, manufacturing,

and delivery

• Inspiring consumers

• Trend leaders

• Elevate the experience

• Drive higher AUP

STRATEGIC OUTLOOK

27

SUMMARY

Strong 2017 outlook: +7-9% Net Sales and

$285 - $305 million Adjusted EBITDA*

2016 Net sales of +11%, excluding Fx and adjusted

for the deconsolidation of MAL

Sixth consecutive year of positive AUP

Adjusted EBITDA +24%

Adjusted EBITDA margin of 12.8%

190bp adjusted EBITDA* margin expansion

More than 2x margins since going public

Repurchased $109 million of shares & additional

$200 million authorized

Investing to elevate the Door Category, Transform

Architectural and Improve Productivity

(*) – See safe harbor/non-GAAP financial measures on page 2 for definitions and other information and appendix for non-GAAP reconciliations

28

APPENDIX

29 29

4Q15 Net Sales

Forex

Volume*

AUP

Other

4Q16 Net Sales

NA Residential

$310.9

($1.9)

$27.6

($0.6)

$0.7

$336.7

Europe

$81.3

($13.4)

($1.2)

$2.8

($1.2)

$68.3

Architectural

$74.8

--

($9.5)

$5.3

($0.4)

$70.2

C&O

$18.5

($0.1)

($12.0)

--

($0.4)

$5.9

Segment Sales Walks

+9% ex Fx +0.5% ex Fx -6% Reflects sale of S.

Africa

($ in millions)

30 30

2015 Net Sales

Forex

Volume*

AUP

Other

2016 Net Sales

NA Residential

$1,193.2

($17.8)

$160.4

$14.2

$1.3

$1,351.3

Europe

$311.8

($28.0)

($4.8)

$24.2

($2.0)

$301.2

Architectural

$291.8

($1.3)

($5.4)

$10.4

$2.4

$297.9

C&O

$75.1

($0.3)

($50.4)

--

($0.3)

$23.6

Segment Sales Walks

+15% ex Fx +6% ex Fx +3% ex Fx Reflects sale of S.

Africa

($ in millions)

31 31

Reconciliation of Adj. EBITDA to net income

(loss) attributable to Masonite

Three Months Ended January 1, 2017

(In thousands)

North American

Residential Europe Architectural Corporate &

Other Total

Adjusted EBITDA $ 49,930 $ 7,905 $ 5,828 $ (3,014 ) $ 60,649

Less (plus):

Depreciation 7,447 1,972 2,797 2,010 14,226

Amortization 870 1,997 1,773 888 5,528

Share based compensation expense — — — 6,868 6,868

Loss (gain) on disposal of property, plant and equipment 252

391

378

—

1,021

Restructuring costs — (2 ) 1,313 3 1,314

Asset impairment — — 1,511 — 1,511

Interest expense (income), net — — — 7,028 7,028

Other expense (income), net — 411 — (1,156 ) (745 )

Income tax expense (benefit) — — — 6,196 6,196

Loss (income) from discontinued operations, net of tax —

—

—

144

144

Net income (loss) attributable to non-controlling interest 767

—

—

1,361

2,128

Net income (loss) attributable to Masonite $ 40,594

$ 3,136

$ (1,944 ) $ (26,356 ) $ 15,430

Three Months Ended January 3, 2016

(In thousands)

North American

Residential Europe Architectural Corporate &

Other Total

Adjusted EBITDA $ 45,615 $ 9,905 $ 4,925 $ (3,605 ) $ 56,840

Less (plus):

Depreciation 7,896 2,157 2,145 2,692 14,890

Amortization 1,295 2,806 2,311 1,069 7,481

Share based compensation expense — — — 6,261 6,261

Loss (gain) on disposal of property, plant and equipment 53

292

436

5

786

Restructuring costs 2 87 — 1,106 1,195

Loss (gain) on disposal of subsidiaries — — — 30,263 30,263

Interest expense (income), net — — — 7,165 7,165

Other expense (income), net (50 ) 882 — 950 1,782

Income tax expense (benefit) — — — (1,595 ) (1,595 )

Loss (income) from discontinued operations, net of tax —

—

—

247

247

Net income (loss) attributable to non-controlling interest 866

—

—

717

1,583

Net income (loss) attributable to Masonite $ 35,553

$ 3,681

$ 33

$ (52,485 ) $ (13,218 )

Year Ended January 1, 2017

(In thousands)

North American

Residential Europe Architectural Corporate &

Other Total

Adjusted EBITDA $ 212,619 $ 38,795 $ 25,160 $ (24,061 ) $ 252,513

Less (plus):

Depreciation 31,159 8,480 9,622 8,343 57,604

Amortization 4,383 9,069 7,999 3,276 24,727

Share based compensation expense — — — 18,790 18,790

Loss (gain) on disposal of property, plant and equipment 1,094

564

484

(31 ) 2,111

Restructuring costs — 19 1,313 113 1,445

Asset impairment — — 1,511 — 1,511

Loss (gain) on disposal of subsidiaries — (1,431 ) — (5,144 ) (6,575 )

Interest expense (income), net — — — 28,178 28,178

Other expense (income), net — 557 — (2,516 ) (1,959 )

Income tax expense (benefit) — — — 21,787 21,787

Loss (income) from discontinued operations, net of tax —

—

—

752

752

Net income (loss) attributable to non-controlling interest 3,389

—

—

2,131

5,520

Net income (loss) attributable to Masonite $ 172,594

$ 21,537

$ 4,231

$ (99,740 ) $ 98,622

Year Ended January 3, 2016

(In thousands)

North American

Residential Europe Architectural Corporate &

Other Total

Adjusted EBITDA $ 165,560 $ 30,468 $ 23,281 $ (15,112 ) $ 204,197

Less (plus):

Depreciation 31,456 8,105 8,223 11,376 59,160

Amortization 4,954 6,860 8,428 3,483 23,725

Share based compensation expense — — — 13,236 13,236

Loss (gain) on disposal of property, plant and equipment 796

325

548

(298 ) 1,371

Restructuring costs 10 2,501 — 3,167 5,678

Asset impairment — 9,439 — — 9,439

Loss (gain) on disposal of subsidiaries — 29,721 — 30,263 59,984

Interest expense (income), net — — — 32,884 32,884

Loss on extinguishment of debt — — — 28,046 28,046

Other expense (income), net (50 ) 1,087 — (2,794 ) (1,757 )

Income tax expense (benefit) — — — 14,172 14,172

Loss (income) from discontinued operations, net of tax —

—

—

908

908

Net income (loss) attributable to non-controlling interest 3,323

—

—

1,139

4,462

Net income (loss) attributable to Masonite $ 125,071

$ (27,570 ) $ 6,082

$ (150,694 ) $ (47,111 )

32 32

Reconciliation of Adj. EBITDA to net income

(loss) attributable to Masonite

(In thousands)

January 1,

2017

January 3,

2016

December 28,

2014

December 29,

2013

December 30,

2012

January 1,

2012

January 2,

2011

Adjusted EBITDA 252,513$ 204,197$ 137,087$ 105,877$ 97,261$ 81,994$ 80,678$

Less (plus):

Depreciation 57,604 59,160 60,622 62,080 63,348 60,784 58,633

Amortization 24,727 23,725 21,722 17,058 15,076 10,569 8,092

Share based compensation expense 18,790 13,236 9,605 7,752 6,517 5,888 9,626

Loss (gain) on disposal of property, plant and equipment 2,111 1,371 3,816 (1,775) 2,724 3,654 1,301

Registration and listing fees — — — 2,421 — — —

Restructuring costs 1,445 5,678 11,137 10,630 11,431 5,116 7,000

Asset impairment 1,511 9,439 18,202 1,904 1,350 2,516 —

Loss (gain) on disposal of subsidiaries (6,575) 59,984 — — — — —

Interest expense (income), net 28,178 32,884 41,525 33,230 31,454 18,068 245

Loss on extinguishment of debt — 28,046 — — — — —

Other expense (income), net (1,959) (1,757) (587) 2,316 528 1,111 1,030

Income tax expense (benefit) 21,787 15,168 4,533 (21,377) (13,365) (21,560) (11,396)

Loss (income) from discontinued operations, net of tax 752 908 630 598 (1,480) 303 1,718

Net income (loss) attributable to non-controlling interest 5,520 4,462 3,222 2,050 2,923 2,079 1,390

Net income (loss) attributable to Masonite 98,622 (48,107) (37,340) (11,010) (23,245) (6,534) 3,039

Twelve months ended,

33 33

Reconciliation of Adj. EPS to net income

(loss) attributable to Masonite

Three Months Ended Year Ended

(In thousands) January 1,

2017 January 3,

2016 January 1,

2017 January 3,

2016

Net income (loss) attributable to Masonite $ 15,430 $ (13,218 ) $ 98,622 $ (47,111 )

Add: Asset impairment 1,511 — 1,511 9,439

Add: Loss (gain) on disposal of subsidiaries — 30,263 (6,575 ) 59,984

Add: Loss on extinguishment of debt — — — 28,046

Tax impact of adjustments — — 737 (3,248 )

Adjusted net income (loss) attributable to Masonite $ 16,941 $ 17,045 $ 94,295 $ 47,110

Diluted earnings (loss) per common share attributable to Masonite ("EPS") $ 0.50

$ (0.43 ) $ 3.17

$ (1.56 )

Diluted adjusted earnings (loss) per common share attributable to Masonite ("Adjusted EPS") $ 0.55

$ 0.54

$ 3.03

$ 1.49

Shares used in computing diluted EPS 31,010,490 30,402,479 31,101,076 30,266,747

Incremental shares issuable under share compensation plans and warrants —

1,171,874

—

1,304,745

Shares used in computing diluted Adjusted EPS 31,010,490 31,574,353 31,101,076 31,571,492