4 Annual BSP UP Professorial Chair LectureBSP Professorial Chair Lecture Felipe M. Medalla February...

29

4 th Annual BSP‐UP Professorial Chair Lecture LECTURE NO. 7 LECTURE NO. 7 LECTURE NO. 7 Is Philippine Economic Growth Lower and More Unequal than Indicated by Official Statistics? Dr. Felipe Medalla BSP‐UP Centennial Professor of Money and Banking

Transcript of 4 Annual BSP UP Professorial Chair LectureBSP Professorial Chair Lecture Felipe M. Medalla February...

4th Annual BSP‐UP Professorial Chair Lecture

LECTURE NO. 7LECTURE NO. 7LECTURE NO. 7

Is Philippine Economic Growth Lower and More Unequal than Indicated by Official Statistics?

Dr. Felipe MedallaBSP‐UP Centennial Professor

of Money and Banking

Is Philippine Economic Growth Lower and More Unequal than Indicated by Official Statistics?

BSP Professorial Chair Lecture

Felipe M. Medalla

February 23, 2011

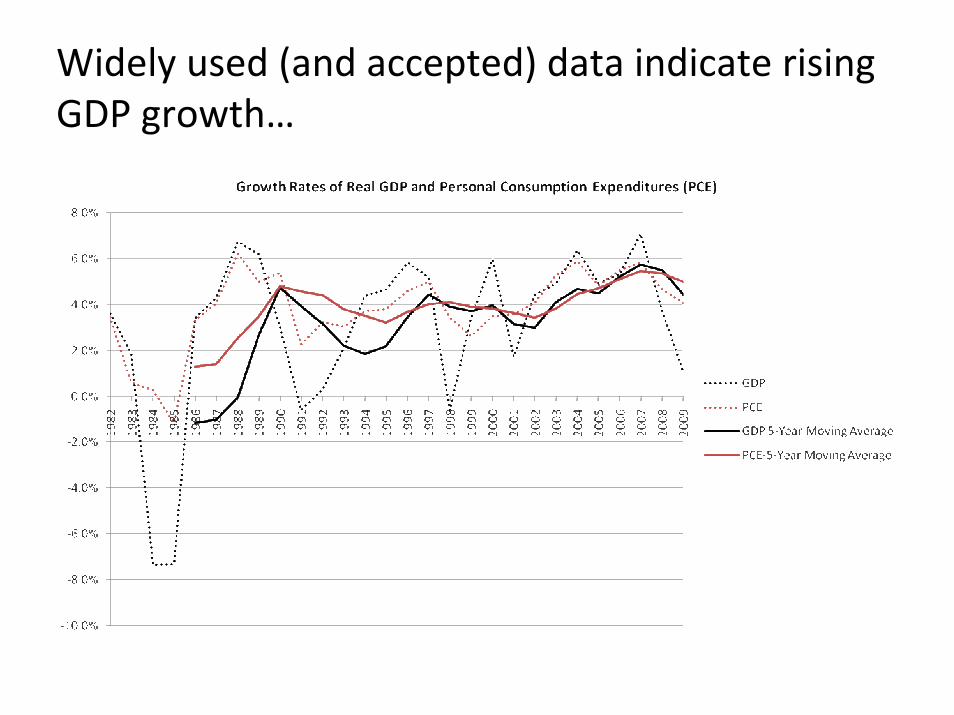

Widely used (and accepted) data indicate rising GDP growth…

and falling income inequality after the Asian Financial Crisis.

At current prices, the growth rates of Family Expenditures from the FIES and the growth rates of PCE from the NIA don’t seem contradictory.

However, the real growth rate of PCE has been significantly higher than that of TFE after the Asian Crisis. The growth of PCE accelerated after the AFC but the growth rate of TFE fell. Either TFE growth after the AFC is understated or the growth of PCE is over‐stated.

To the extent that an increasing proportion of richer households refuse to participate in income and expenditure surveys, the FIES might under‐estimate expenditure growth. It is hard to believe that total real expenditures of rich families were only slightly higher in 2009 compared to 2000.

Total Income of Families by National Income Decile* (billion pesos, 2000 price level)

2000 2003 2006 2009

Poorest 30 178 165 193 220

2nd 30 342 317 366 408

3rd 30 670 613 718 779

Richest 10% 602 495 580 618

Total 1,791 1,589 1,857 2,024

Share of Richest 10% 33.6% 31.1% 31.2% 30.5%*Deciles in original table

It is quite unlikely that expenditures of the richest families grew at a slower rate than the rest of families (0.3% compounded growth rate compared to 1.4% of all families and 4.9% for PCE.)

Real Compounded Annual Growth Rate of Family Expenditures by National Income Decile

2000‐03 2003‐06 2006‐2009 2000‐09

Philippines ‐3.9% 5.3% 2.9% 1.4%First Decile ‐2.4% 6.0% 4.2% 2.5%Second Decile ‐2.6% 5.4% 4.9% 2.5%Third Decile ‐2.3% 5.1% 4.3% 2.3%Fourth Decile ‐2.7% 5.1% 4.2% 2.1%Fifth Decile ‐2.3% 5.0% 3.7% 2.1%Sixth Decile ‐2.5% 4.9% 3.1% 1.8%Seventh Decile ‐3.1% 5.2% 3.0% 1.7%Eighth Decile ‐2.9% 5.5% 2.9% 1.7%Ninth Decile ‐2.8% 5.6% 2.6% 1.7%Tenth Decile ‐6.3% 5.4% 2.1% 0.3%

Memo: Real CAGR of PCE 4.3% 5.4% 4.9% 4.9%

But if it is assumed that expenditures of the richest 10% of the families account for all the difference between the growth rate of TFE and PCE, the share of the richest decile in total expenditures will rise from around one‐third to slightly less than one half in 2009!

Hypothetical * Total Income of Families by National Income Decile** (billion pesos, 2000 price level)

2000 2003 2006 2009

Poorest 30 178 165 193 220

2nd 30 342 317 366 408

3rd 30 670 613 718 779

Richest 10% 602 939 1,104 1,338

Total 1,791 2,033 2,381 2,745

Share of Richest 10% 33.6% 46.2% 46.4% 48.8%** Assumes that FIES Family Expenditures would grow at the same rate as PCE but all the adjustments in expenditures would be attributed to the richest decile.. *Deciles in original table

It would imply that expenditures of the richest decile grew at a compounded annual rate of 9.3% between 2000 and 2009. In other words, economic growth is both less equitable and lower than what most analysts think.

Hypothetical* Real Compounded Annual Growth Rate of Family Expenditures by National Income Decile

2000‐03 2003‐06 2006‐2009 2000‐09

Philippines 4.3% 5.4% 4.9% 4.9%

First Decile ‐2.4% 6.0% 4.2% 2.5%

Second Decile ‐2.6% 5.4% 4.9% 2.5%

Third Decile ‐2.3% 5.1% 4.3% 2.3%

Fourth Decile ‐2.7% 5.1% 4.2% 2.1%

Fifth Decile ‐2.3% 5.0% 3.7% 2.1%

Sixth Decile ‐2.5% 4.9% 3.1% 1.8%

Seventh Decile ‐3.1% 5.2% 3.0% 1.7%

Eighth Decile ‐2.9% 5.5% 2.9% 1.7%

Ninth Decile ‐2.8% 5.6% 2.6% 1.7%

Tenth Decile 15.9% 5.5% 6.6% 9.3%

Memo: Real CAGR of PCE 4.3% 5.4% 4.9% 4.9%

*Family Expenditures of the 10th decile adjusted to equate the growth rates of FIES Family Expenditures and PCE.

The rise of our GDP growth after the AFC does not fit the normal pattern. Growth rose as demand growth (consumption, government expenditures, investments plus exports) fell because the fall in demand affected only imports. (In fact, there was consumers and firms seemed to have substituted domestic goods for imported goods.)

The rise in GDP growth after the AFC was also accompanied by a fall in the investment rate.

It also appears that the rise in the growth rate of GDP is due to an unprecedented rise in labor and total factor productivity in all sectors of the economy (agriculture, industry and services). Since the investment ratio declined, total factor productivity must have increased.

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

1992:4

1993:3

1994:2

1995:1

1995:4

1996:3

1997:2

1998:1

1998:4

1999:3

2000:2

2001:1

2001:4

2002:3

2003:2

2004:1

2004:4

2005:3

2006:2

2007:1

2007:4

Manufacturing Agri Services

Growth Rate of Labor Productivity

The growth rate of GDP after the Asian Financial Crisis was higher than the growth rate of the gross sales of the Top 1000 and Top 5000 corporations.

Comparison of Nominal GDP Growth with the Revenue Growth of Large Corporations

1996 to 2008 1998 to 2008

Revenue of Top 1000 9.2% 8.5%

Revenue of Top 5000 9.2% 8.7%

GDP 10.8% 10.8%

GDP vs Top 1000 1.6% 2.2%

GDP vs Top 5000 1.6% 2.1%

Similarly, the growth rate of manufacturing value added in GDP was higher than the growth rate of the sales of manufacturing firms in the Top 1000 and 5000 corporations.

Comparison of manufacturing value‐added growth with the revenue growth of large manufacturing corporations

1996 to 2008 1998 to 2008Revenue of Manufacturing Corporations in the Top 1000

2.8% 2.7%

Revenue of Manufacturing Corporations in the Top 5000

2.9% 2.8%

Manufacturing Value added in GDP 4.4% 4.8%

GDP vs Top 1000 1.5% 2.1%

GDP vs Top 5000 1.5% 2.0%

The Volume of Production Index (VOPI) and real manufacturing value added follow opposite long‐term trends.

Estimates of agricultural gross output and value added are based on very old benchmarks and out‐dated census frames. These have resulted in statistical trends that are very hard to reconcile. For instance, estimated agricultural output has increased faster than rural population but rural poverty has worsened while palay output has increased faster than the country’s population but imports of rice grew faster than the country’s population.

A Large part of GDP is imputed, not measured. Estimates are based on very old, possibly obsolete, census frames and parameters. See quotes below from a study on the Philippine National income accounts done by Ross Harvey, an expert in national income accounting. (“Assessment Report on the Philippine System of National Accounts” 25 September, 2008).

• “Very old benchmarks derived from the 1988 Census of Establishments and the 1980 Census of Agriculture and Fisheries are still being used in the compilation of current price GDP using the production approach. For some industries Gross Value Added Ratios (GVAR) obtained from the 1988 Census of Establishments are still being used to derive current price estimates of value added using output indicators obtained from the Quarterly Survey of Philippine Business and Industry (QSPBI) and other sources.”

• “The general approach to compiling estimates for the unorganized sector is to derive an estimate of employment not covered in the establishment collections and to assume that value added per employee in the unorganized sector is the same as that for small establishments operated by a sole proprietor.”

• “The use of a base year of 1985 for constant price estimates is likely to be distorting measures of economic growth for recent years. International guidelines suggest that base years should be updated every 5 years. However, an even more desirable approach is to adopt chain volume measures.”

This may result in over‐estimation of output growth unfortunate since the growth rates of GDP and in the number of self‐employed and unpaid family workers are negatively correlated. Inother words, a significant percentage of what is officially referred to as employment is really disguised unemployment.

It could be that self and family employment is increasingly not true employment.

The manufacturing sector which used to account for more than ten percent of total employment, accounted for only 6% of the increase in employment.

In spite of rapid urbanization and the rising share of NCR , Region III and Calabarzon in total population and GDP, the share of wage and salary employment in total employment has barely increased.

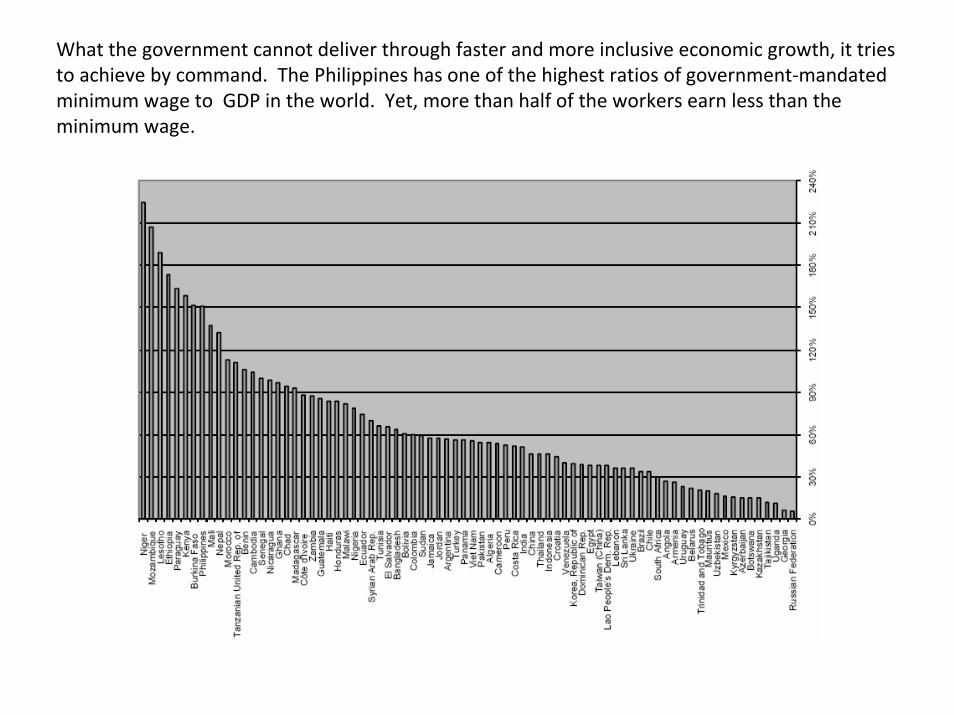

What the government cannot deliver through faster and more inclusive economic growth, it tries to achieve by command. The Philippines has one of the highest ratios of government‐mandated minimum wage to GDP in the world. Yet, more than half of the workers earn less than the minimum wage.

Judging by low elementary and high school enrollment ratios, the next generation of adults will no longer be better educated than the present.

If statistics on enrollment are reliable, elementary school enrollment has lagged behind the number of school‐aged children.

This is probably related to the fact that less educated mothers account for a disproportionate share in child births.

Mothers’ Education and Fertility (No. of Children)

Desired Fertility Actual FertilityNo education 4.1 5.3Elementary 3.3 5.0High school 2.5 3.5College or higher 2.2 2.7

Corruption, pork barrel driven budgets and poor tax collections have resulted in a low quality road network.

Quantity and Quality of Roads:Selected Asian Countries

CountryKilometers of road

per capitaPercent High

QualityPhilippines 2.45 18Korea 2.09 87Malaysia 3.97 78Pakistan 1.7 88Thailand 0.9 98

Can these favorable macro‐economic trends result in a rise in the Philippines’ long‐term economic growth prospects? The experience of many countries shows that macroeconomic instability can destroy growth, but once macroeconomic stability has been attained, more difficult reforms have to be done to do better than the current modest rate of economic growth. Moreover, a lot of reforms also have to be done to make the economic growth more inclusive (which the Philippines has never done).

“The large literature on national policies and growth established some statistical association between national economic policies and growth. ….However, I find that the associations seem to depend on extreme values of the policy variables, …. are consistent with other theoretical models that predict only modest effects of national policies, (and) with the view that the ….growth differences….likely reflect deep‐seated institutions that are not very amenable to change in the short run.” From Easterly, William. 2005. “National Policies and Economic Growth: A Reappraisal.” (italics added)

But improving the rule of law and ouir institutions would be a difficult and would take a long time, especially if the justice system itself is very weak.

‘ When I was writing this book, there were times I was gripped by surprise and disbelief. I did not idealize the Supreme Court as a perfect place. But I did not expect it, either, to be a place so tolerant of men and women who seem to take integrity lightly.

It is impossible to pore over this book without developing a keen awareness of how important change is in an institution we like to call the “last bulwark of democracy.” ’

pp. 245‐6, Marites Vitug,

Shadow of Doubt: Probing the Supreme Court