3rd November 2011 - ACostE - Association of Cost Engineers 2011/DLewisEACE.pdf · DGA (Fr) Eumetsat...

55

Association Of Cost Engineers 50 th Anniversary 3 rd November 2011 EACE & The 2 C’s Dave Lewis FAcostE – Chairman EACE Dave Lewis November 2011 1

Transcript of 3rd November 2011 - ACostE - Association of Cost Engineers 2011/DLewisEACE.pdf · DGA (Fr) Eumetsat...

Association Of Cost Engineers 50th Anniversary

3rd November 2011

EACE & The 2 C’s

Dave Lewis FAcostE – Chairman EACE

Dave Lewis November 2011 1

Agenda

1. Brief History Of the EACE

2. CECIM & Benchmarking Estimating practices

3. CECAM

Dave Lewis November 2011 2

EACE – The European Aerospace Cost Engineering Working Group

- A brief History

Dave Lewis FAcostE – Chairman EACE

Dave Lewis November 2011 3

Establishment

The EACE was established in March 1998 as a non-profit, voluntary organisation to promote the function of Cost Engineering in Europe.

WHY

ESA/Eurospace initiative to improve cost forecasting in the Space business in Europe.

We (Estimating / Cost Engineering) perceived as poorly represented by professional institutes. Preceded EMC in ACostE

Dave Lewis November 2011 4

Terms Of Reference

Provide a forum for the exchange of experience, information and ideas relating to Cost Engineering activities.

Stimulate and contribute to improvement in tools, databases and methodologies applied in the Cost Engineering process.

Maintain cognisance of industry approaches to cost reduction trade-offs, including technology application, manufacturing process, etc

Dave Lewis November 2011 5

Skills

The majority of participants are engaged in all aspects of Cost Management support including

cost and resource estimating scheduling performance measurement cost analyst knowledge management risk design to cost value engineering investment appraisal supplier or subcontractor evaluation Parametrics Project management

Dave Lewis November 2011 6

Participation

We are a truly European Group.

In experience terms we cover the whole spectrum from entry into the profession to director level.

Participants work for manufacturing companies, design & system houses, institutional and government agencies, training suppliers, consultancies and tool suppliers

Dave Lewis November 2011 7

Participation

Aerospace/Defence Suppliers Astrium (UK,FR,DE)

Airbus (UK,FR,DE)

Agusta Westland (UK)

MBDA (UK)

BAe Systems(UK)

Rolls-Royce (UK)

SEA (UK)

SSI (Italy)

The Aerospace Corporation (USA)

– MCR (USA)

Tools/Consultancies Price Systems International

(UK,FR,DE)

Galorath (UK,Holland)

YTAE (Fr)

Polaris Consulting (UK)

Qinetiq (UK)

Vose Software (BE)

4Cost GMBH (DE)

Cost Engineering BV (Holland)

Dave Lewis November 2011 8

Participation

Institutional/Agencies

ESA (Holland)

ASI (Italy)

CNES (FR)

DLR (DE)

MOD (UK)

Eurocontrol (BE)

DGA (Fr)

Eumetsat (DE)

Academia

University Of Bath (UK)

Southampton University (UK)

Cranfield (UK)

Dave Lewis November 2011 9

Participation –non aero

Sony Visual products (UK)

Nissan (UK)

Philips Healthcare (Holland)

Intellienergia Renewable Energy Solutions(Italy)

Ferrari (Italy)

Landrover – Jaguar (UK)

Dave Lewis November 2011 10

Participation

Dave Lewis November 2011 11

Mailing List – approx 180

Linkedin – approx 80

Venues

Meets yearly at venues hosted by one of the members.

ESTEC Noordwijk (Netherlands)

Mod Abbey Wood (UK)

Cranfield University (UK)

ESRIN (Frascati Italy)

Astrium (Bremen Germany)

Astrium (Toulouse Fr)

Bath University(UK)

Dave Lewis November 2011 12

Deliverables

CECIM Developed by SIG of The European Aerospace Working Group On Cost

Engineering (EACE)

CECIM “White Paper” published 2001.

Expert Development team representing 9 best practice companies in aerospace cost forecasting

European Training Supplier Manual

Schedule & Cost Overrun White paper

Dave Lewis November 2011 13

Dave Lewis November 2011 14

Can your suppliers estimate?

“Delivering Capability in the Cost Forecasting Process”

David Lewis FAcostE

Agenda

Definitions

Problem Statement

Characteristics Of Effective Cost Engineering

Why we should measure

Capability/Benchmarking Initiatives CEVEP

CECIM

CECAM

Dave Lewis November 2011 15

Dave Lewis November 2011 16

Definition - Cost Estimating

Cost Estimating is a planned and systematic process for identifying and predicting costs within

the varying levels of uncertainty and for an identified scope.

Good quality estimates are those which are neither conservatively high, due to excessive

contingencies, nor optimistically low, due to lack of proper scope definition or unrealistic.

Why do we Estimate ?

Dave Lewis November 2011 17

the purpose of cost estimating is to help the business maximise its resources, become more competitive and achieve profitability targets.

The quality and accuracy of the estimate is important as estimates that are too low can reduce profits, and estimates that are too high will diminish the businesses ability to compete in the marketplace.

The estimator must be objective and not introduce any bias or prejudice –get it wrong and it will jeopardise the financial outlook of the business.

Poor estimating designs failure into the project The main way to stay in budget is making sure you have a good estimate before you start

Dave Lewis November 2011 18

Problem Statement (1)

Cost Engineers are typically under funded, not appreciated and their capabilities not recognised.

Companies are uncertain of the performance of their cost modelling practices and how their approach compares to other businesses and industry sectors.

Project Managers/Others (think ?) can do estimates.

Dave Lewis November 2011 19

Problem Statement (2) Where are we ?

All types of projects predicting large overspends. Who gets the blame)?

Company management / clients request “single” point numbers.

However enlightened clients seek better predictability of cost outturn.

Initiatives by institutional customers to help supply chain improve capability in estimating - CECIM

Introduce confidence modelling

Customer Demands

WLC Estimates

Support bid/no bid with cost analysis

Storage of Actuals

Supplier Cost validation

Risk Analysis

Cost Modelling

Cost Allocation

Cost Control & Analysis

Value Engineering

DTC/CAIV

Inputs to Project Management

Make/Buy Analysis

Budget Forecasts

Cost Estimation & Proposal Management

Scheduling

Systems and Software Acquisition and Maintenance

Audit

Business Case Development

Dave Lewis November 2011 20

Dave Lewis November 2011 21

Characteristics of Effective Cost Estimating (1)

Estimates predict cost of work to be carried out at a future date. The estimate has to recognise the reality that all relevant details cannot be known exactly and therefore uncertainty will exist about the total costs.

Items that make up an estimate can be categorised Known items i.e. Firm, identified scope with values based on measured or calculated quantities.

Unknown items i.e. Scope which cannot be quantified but is firmly believed to exist

Contingency i.e. An unspecified provision for the whole estimate to cover minor errors or omissions, as well as the uncertainty associated with quantities, unit rates and productivity.

Risk

Dave Lewis November 2011 22

Characteristics of Effective Cost Estimating

An estimate should be viewed as a set of values within a range of possible outcomes. Accuracy is best described by a probability statement/curve. (More often “Classes Of Estimate”)

In addition to quantities and unit rates, key factors which influence an estimate include:-

Project execution strategy

Project schedule

Expenditure phasing and cash flow (including escalation assumptions)

Location factors

Ex rates

Allowances for overheads and profit

The level of contingency required to take the estimate to the required level of confidence

Dave Lewis November 2011 23

Characteristics of Effective Cost Estimating

Formal review and approval process Capture Scope & Technical Solution

Schedule

Capture Assumptions (MDAL) Risk Consistent estimating framework to satisfy all users Feedback loops to improve the quality of future estimates includes provision for data collection as part of routine cost control and strict change control Ongoing reconciliation throughout the project life cycle Competence Formal & Stringent Review & Approval Process

Dave Lewis November 2011 24

Capability and Competence The 2 C’s

We need to do more

As individuals (improve competence) - CECAM

As functions (improve capability) - CECIM

Measure/Control/Manage

If you cannot manage it, you cannot control it, if you cannot control it you cannot manage it, if you cannot manage it you cannot improve it.

Measuring is the starting point for process improvement, because you are able to understand where you are and set goals that help you get where you want to go by an

appropriate measurement system.

Dave Lewis November 2011 25

Benefits Of Measuring Capability

To highlight strengths and weakness in the process

Can use the results to evaluate the performance of the supply chain or to compare yourself against average performance

Goal is to manage cost more effectively and direct activities to improve cost management (Improve Performance)

Benchmarking (Best Practice)

Dave Lewis November 2011 26

Capability / Benchmarking Initiatives

Cost Estimating Value Enhancement Practice – European Construction Institute – 2000

Cost Engineering Capability Improvement Model (CECIM) – EACE - 2001.

Cost Engineering Capability Assessment. Knowledge West. Collaborative initiative between higher education

institutions and industry (West Country – 2006)

Dave Lewis November 2011 27

CEVEP Recommendations (1) There should be a clear understanding of the scope of work with

boundaries and exclusions to the estimates For every estimate the methodology adopted should be fit for purpose All key assumptions should be documented, and, for larger projects a

methodology report produced which documents the project execution strategy. This takes account of commercial issues, contracting arrangements, local issues, sourcing of design/other services and construction philosophy/constraints. The strategy would be agreed with the major project stakeholders.

An assessment should be made on the quality of information available on

Project Scope Project specification Quantities Cost data (rates) Project Schedule Project Location Factors Cost Escalation

Dave Lewis November 2011 28

CEVEP Recommendations (2)

Cross checks should be made against published data, check lists, other current estimates and past project outturn data to compare level of estimate

A formal estimate review and approval process should be undertaken.

Full account must be taken of commercial factors e.g. Cash flow/expenditure phasing Project financing to compensate for differing profiles of cashflow and

expenditure Exchange rates, where costs are to be incurred in more than one

currency Bonds, guarantees and insurance Forwards escalation

A risk review should be undertaken, identifying those items subject to uncertainty and range of potential outcomes for the total estimate

Dave Lewis November 2011 29

Cost Engineering Capability Improvement Model (CECIM)

Developed by SIG of The European Aerospace Working Group On Cost Engineeing (EACE)

CECIM “White Paper” published 2001. Expert Development team representing Airbus ASI (Italian Space Agency) Matra Marconi Space (UK & Fr) – now Astrium Bae Systems Cost Engineering Solutions ESA/ESTEC MOD DPA/PFG Westland Helicopters Anglian Enterprises

Dave Lewis November 2011 30

31 Dave Lewis November 2011 31

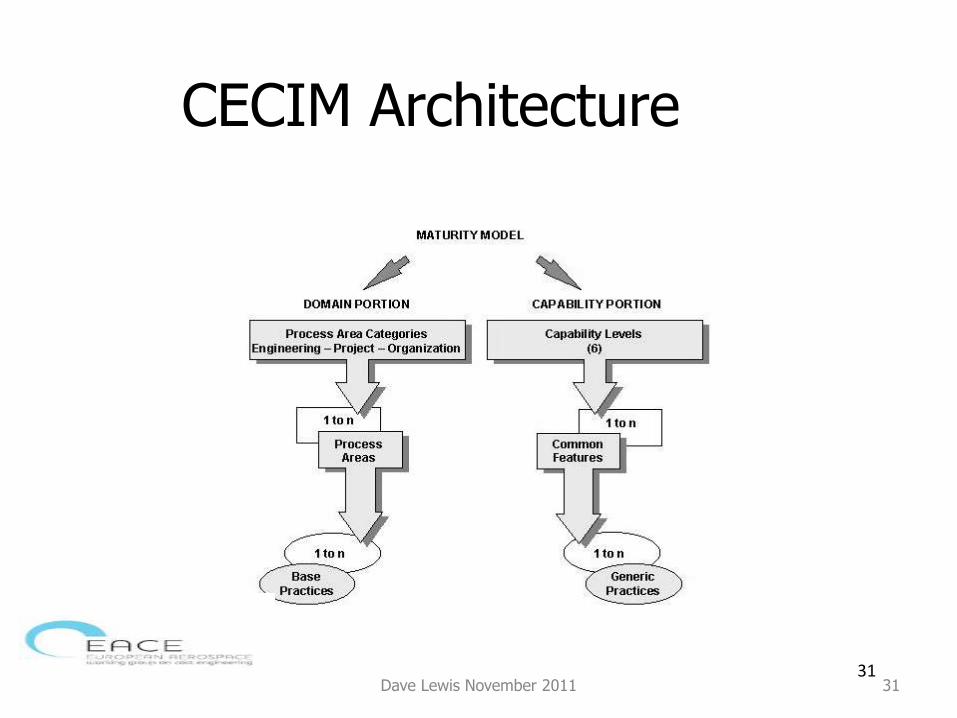

CECIM Architecture

32 Dave Lewis November 2011 32

The Domain Portion - “What Should The Organisation Be Doing?”

Defines the processes of the CE discipline related to:

– The discipline itself;

– Integration within the project;

– Organisation-wide processes.

Decomposes the discipline into “Process Areas” (PAs).

– Decomposes the PAs into “Base Practices” (BPs).

Process Areas (PA)

A process Area is a set of related Cost Engineering process characteristics, which, when performed collectively facilitate the overall cost engineering function.. The PA’s are composed of Base Practices (BP), which are defined as activities that are essential to the achievement

of the purpose of the Process Area.

Dave Lewis November 2011 33

Process Areas

Cost Estimating

Cost Modelling

Cost Control & Analysis

VA /VE & Cost Reduction

Planning

Risk management

Competence Management

Define the Process

Improve the Process

Integrate Disciplines

Ensure Quality Design to Cost & CAIV Supply Chain Management Knowledge Management Capital Asset & Resource

Management Business Analysis Business Case Development Audit Cost Allocation

Dave Lewis November 2011 34

Example – PA Description Cost Estimating

Requires that a detailed analysis of the scope of work is performed and that the project objectives are clearly identified. Cost Estimating includes estimation of the cost of the typical product Outputs, the resources required, consideration of lessons learned, risk assessment, currency exposure considerations and presentation of costs to senior management. It is important to fully understand the class of estimate required and tailor the process accordingly before commencing any estimate.

Dave Lewis November 2011 35

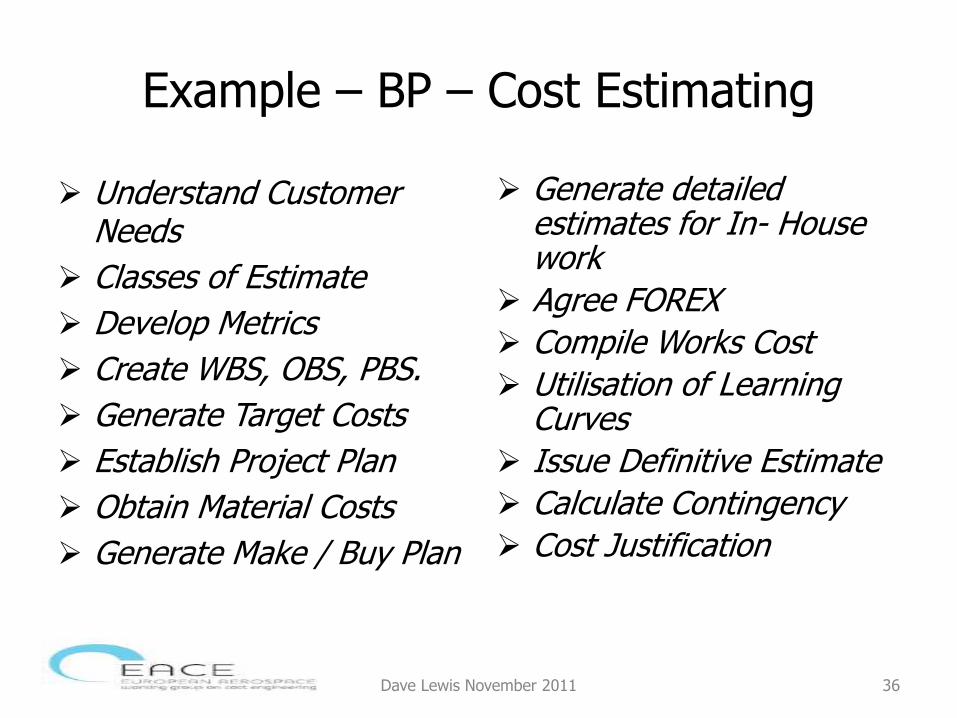

Example – BP – Cost Estimating

Understand Customer Needs

Classes of Estimate

Develop Metrics

Create WBS, OBS, PBS.

Generate Target Costs

Establish Project Plan

Obtain Material Costs

Generate Make / Buy Plan

Generate detailed estimates for In- House work

Agree FOREX

Compile Works Cost

Utilisation of Learning Curves

Issue Definitive Estimate

Calculate Contingency

Cost Justification

Dave Lewis November 2011 36

37 Dave Lewis November 2011 37

The Capability Portion – “How Well Is It Performing?”

Defines 6 increasing levels of process maturity

Defines Generic Practices for each Capability Level

38 Dave Lewis November 2011 38

Domain + Capability = Maturity

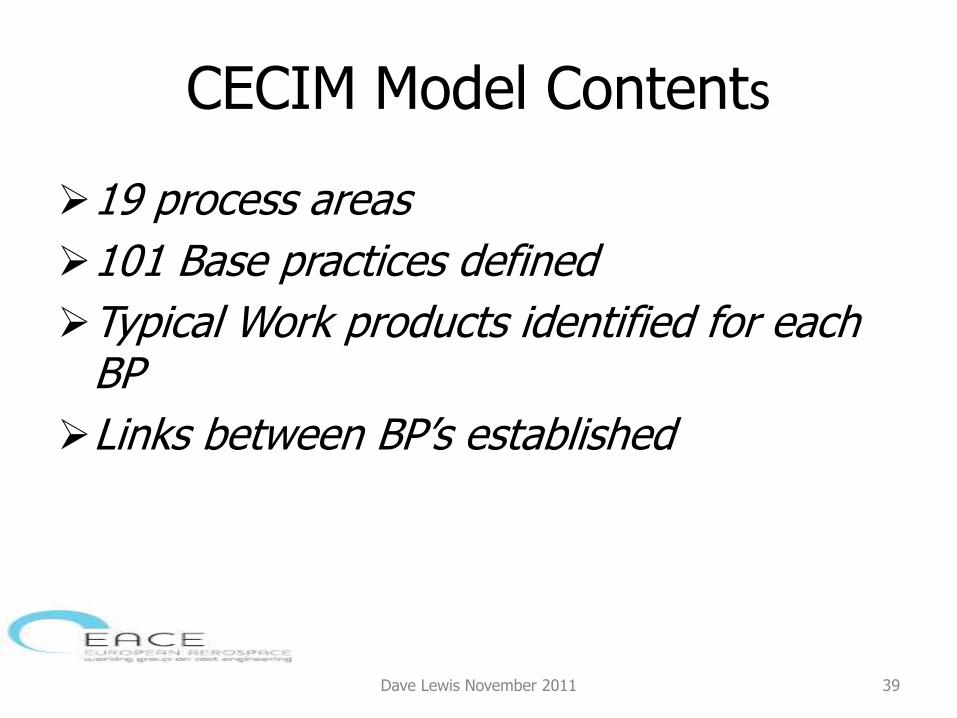

CECIM Model Contents

19 process areas

101 Base practices defined

Typical Work products identified for each BP

Links between BP’s established

Dave Lewis November 2011 39

40

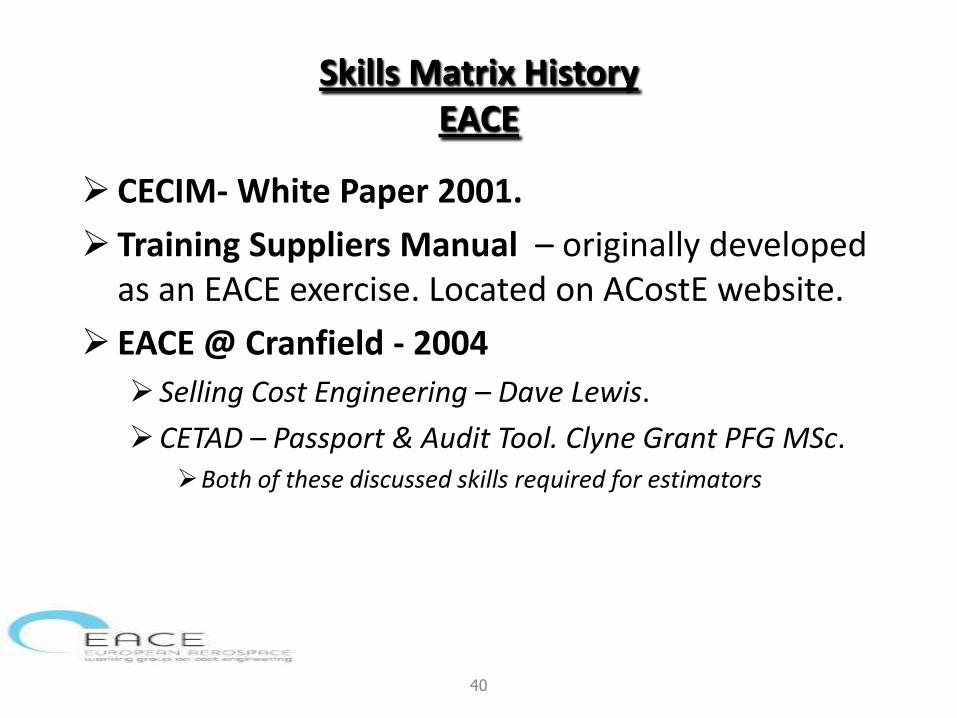

Skills Matrix History EACE

CECIM- White Paper 2001.

Training Suppliers Manual – originally developed as an EACE exercise. Located on ACostE website.

EACE @ Cranfield - 2004

Selling Cost Engineering – Dave Lewis.

CETAD – Passport & Audit Tool. Clyne Grant PFG MSc. Both of these discussed skills required for estimators

41

Training and Education

Cost estimating is rarely taught as a profession within Europe, instead we learn engineering, accounting, statistics, management, etc. –all useful.

Outside Europe training can be gained through symposia or more formally through certification programmes offered by ISPA and SCEA.

Very few introductory courses available. Some associations and societies exist to promote the

profession – SCAF, ACostE, DACE and EACE. In the UK ACostE Professional Qualifications(Certification) in

Cost Engineering becoming available

In UK NVQ in Project Control (TASC) – includes estimating.

© 2009 Decision Analysis Services Ltd

42

The Changing Role of the Cost Estimator

Industry finds it difficult to keep up with rapid changes in technology –the same is true for cost estimators.

To meet the challenge we must be able to adapt We now apply more sophisticated methodologies than those

traditionally used. Estimating is one of the most challenging of all professions because

the environment is constantly changing. We should not sit back–but accept the challenge of improving

techniques and tools that can be applied. Estimators must continually strive to improve their quantitative

skills. But, we need to ensure that any new technique is practical,

productive and can be applied using sound judgment.

© 2009 Decision Analysis Services Ltd

43

CECAM - Objective (1)

To provide Cost Estimators / Engineers with a means to :

Assess their current competence and determine areas for development. Identify and plan development objectives that are realistic and achievable Develop their knowledge, understanding and skills in line with their plan. Review their performance regularly and use the outcome to plan future

development activities Seek and obtain constructive feedback from others and use it to maintain

and improve performance Agree with line and/or project management the time and other resources

needed to help them achieve the development objectives.

GOAL – TO ENSURE THE COST ESTIMATING/ENGINEERING FUNCTION MEETS THE REQUIREMENTS FOR THE ORGANISATION AS A BUSINESS

44

CECAM - Objective (2)

It will enable Cost Estimators/Engineers to Identify the skills and knowledge required for their current role

Identify the skills and knowledge required for their planned future roles- leads to a career development.

Identify learning opportunities and resources available

Aid in development objective setting

Aid in personal development and skills development training progress assessments.

Provide sources of guidance and advice on training and technical skills development that are available.

Ensure skills are aligned to support corporate goals for profitability.

Enable individuals to grow to their potential

It is not a tool for management

45

Industry Specific (1)

Cost Estimators have to acquire a broad range of skills and these can change dependent on the

industrial base or organisation. The skills we

Companies = Profit

Institutions = Budget setting

46

Summary Skill Processes

Estimator

Specific Knowledge Technical Knowledge

Commercial Awareness Financial Awareness

Enabling Knowledge Management & Process Skills

IM

Supporting Knowledge Understand Project Management

Understand your Business Communications & Interpersonal Skills

47

Technical Competence Scoping the Estimate

Detailed Estimating Learning Curves Cash Flow Development Cost Plans/Milestones Estimate Review & Evaluation Develop Metrics/CERs Target Costing PERT/COST Inflation/Escalation Procedures Manual DTC/CAIV Planning & Scheduling Change Control Value Engineering Software Estimating Confidence Modelling Investment Appraisal Health & Safety Issues Estimate Classifications

Capture Historical Data Estimating Allowances Control Estimate / EAC0 WBS/OBS/RAM FOREX RISK Analysis Analogous Estimates Parametrics Basic Statistics Cost Brochure Software Estimating Cost Report Preparation Range Estimates(3 Point Estimating) WLC Cost Engineering plan Cost Control Methods Acquisition Operating Framework Federal Acquisition Requirements Productivity factors Method Of Measurements (QS)

Approx 110 tasks identified.

48

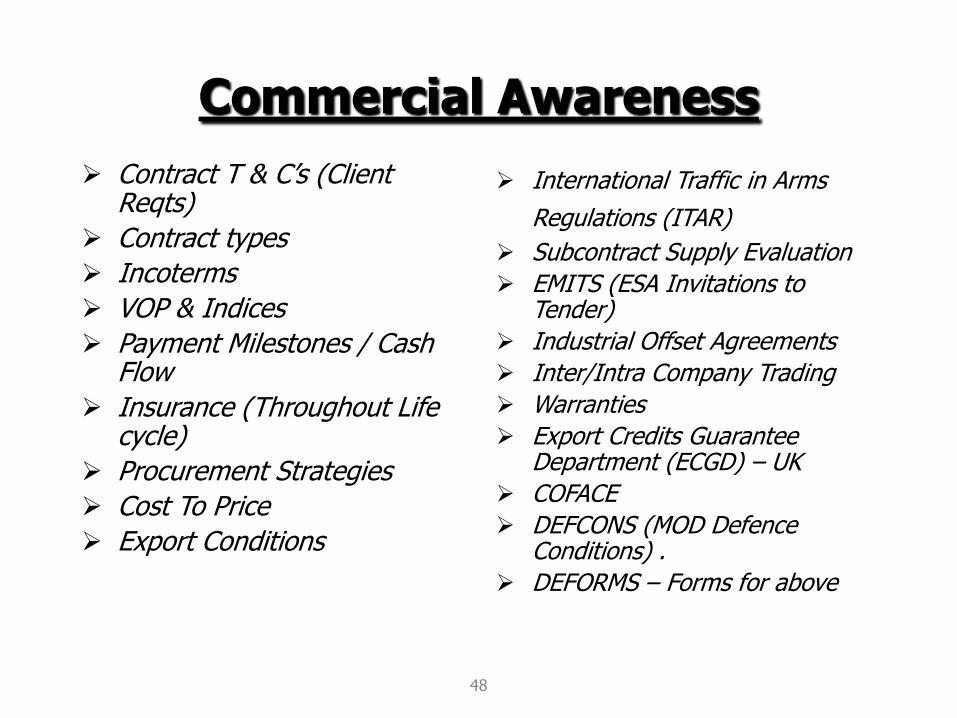

Commercial Awareness

Contract T & C’s (Client Reqts)

Contract types

Incoterms

VOP & Indices

Payment Milestones / Cash Flow

Insurance (Throughout Life cycle)

Procurement Strategies

Cost To Price

Export Conditions

International Traffic in Arms

Regulations (ITAR) Subcontract Supply Evaluation

EMITS (ESA Invitations to Tender)

Industrial Offset Agreements

Inter/Intra Company Trading

Warranties

Export Credits Guarantee Department (ECGD) – UK

COFACE

DEFCONS (MOD Defence Conditions) .

DEFORMS – Forms for above

49

Skill Descriptions Target Costing Decomposes the target cost for a product or project as a

whole into cost targets for each element in the

WBS.

DTC / CAIV Process that constrains design options to a fixed cost

limit. The cost limit is usually what the buyer can

pay or what the marketplace demands. Cost as an

independent variable (CAIV) is a strategy that

involves both the company and the customer

establishing realistic cost objectives relative to a

product’s function.

Cost Estimate Classification / Maturity Matrix Method to categorize estimates by degree of project

definition. The discrete levels of project definition

corresponds to the typical phases of a project

Detailed (Bottoms Up) Estimating Involve breaking the work down into discrete elements

that that are described in terms of labour, time,

materials, and expenses. These elements may

represent individual operations or conveniently

grouped activities. This form of estimate requires a

lot of information and detailed knowledge of the

materials and processes involved.

50

Tool Structure

Commercial Skills Knowledge - Definitions No

Knowledge Know About

Work

Supervised

Work

Unsupervised

Problem

Solve Teach

Cost Engineering Skills Matrix - Definitions.

Knowledge Understanding Application Analysis Synthesis Evaluation

Analogy Estimating √

Parametric Estimating √

Parametric Estimating - Use PRICE √

Detailed (Bottoms Up)Estimating √

Develop Norms / Metrics √

Planning/Scheduling

For each skill assess level of understanding

51

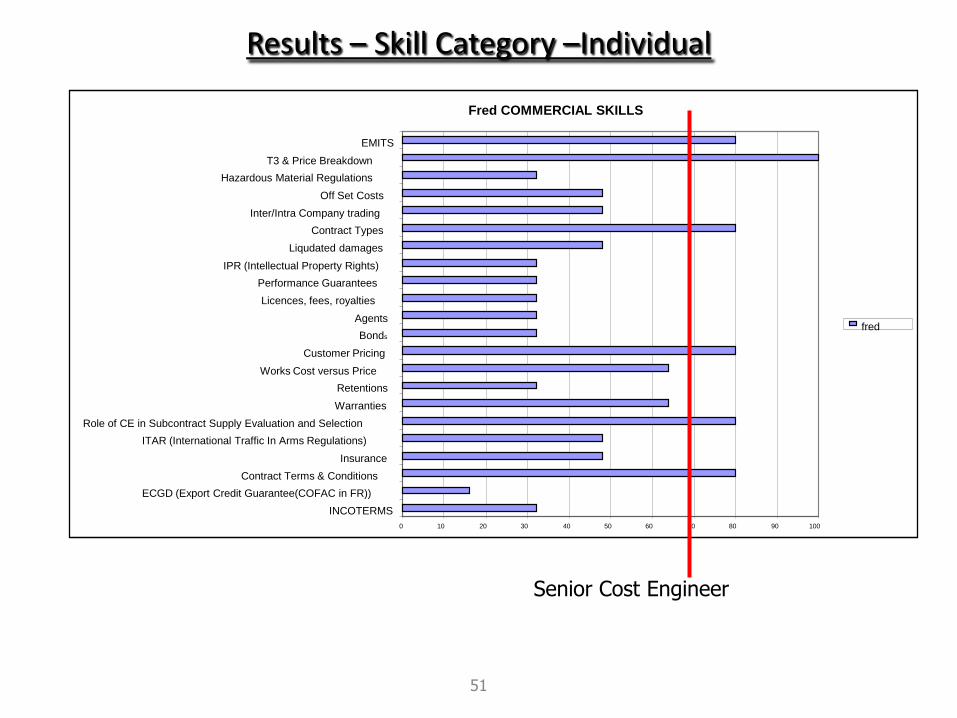

Results – Skill Category –Individual

Fred COMMERCIAL SKILLS

0 10 20 30 40 50 60 70 80 90 100

INCOTERMS

ECGD (Export Credit Guarantee(COFAC in FR))

Contract Terms & Conditions

Insurance

ITAR (International Traffic In Arms Regulations)

Role of CE in Subcontract Supply Evaluation and Selection

Warranties

Retentions

Works Cost versus Price

Customer Pricing

Bonds

Agents

Licences, fees, royalties

Performance Guarantees

IPR (Intellectual Property Rights)

Liqudated damages

Contract Types

Inter/Intra Company trading

Off Set Costs

Hazardous Material Regulations

T3 & Price Breakdown

EMITS

fred

Senior Cost Engineer

Skills Matrix – Heat Map Department Summary

Abbreviations

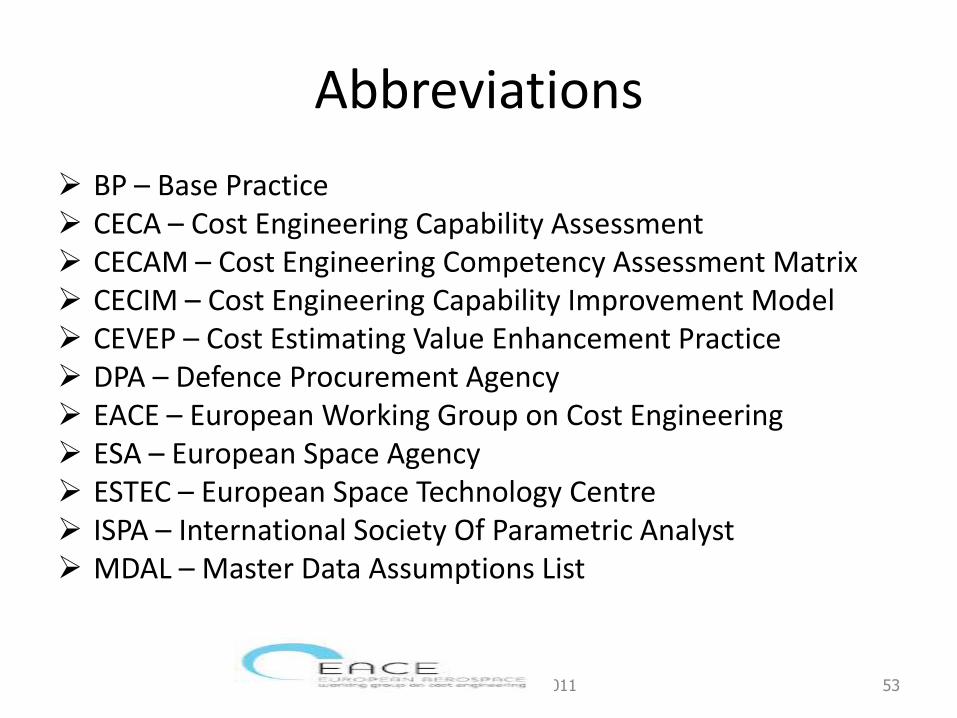

BP – Base Practice CECA – Cost Engineering Capability Assessment CECAM – Cost Engineering Competency Assessment Matrix CECIM – Cost Engineering Capability Improvement Model CEVEP – Cost Estimating Value Enhancement Practice DPA – Defence Procurement Agency EACE – European Working Group on Cost Engineering ESA – European Space Agency ESTEC – European Space Technology Centre ISPA – International Society Of Parametric Analyst MDAL – Master Data Assumptions List

Dave Lewis November 2011 53

Abbreviations

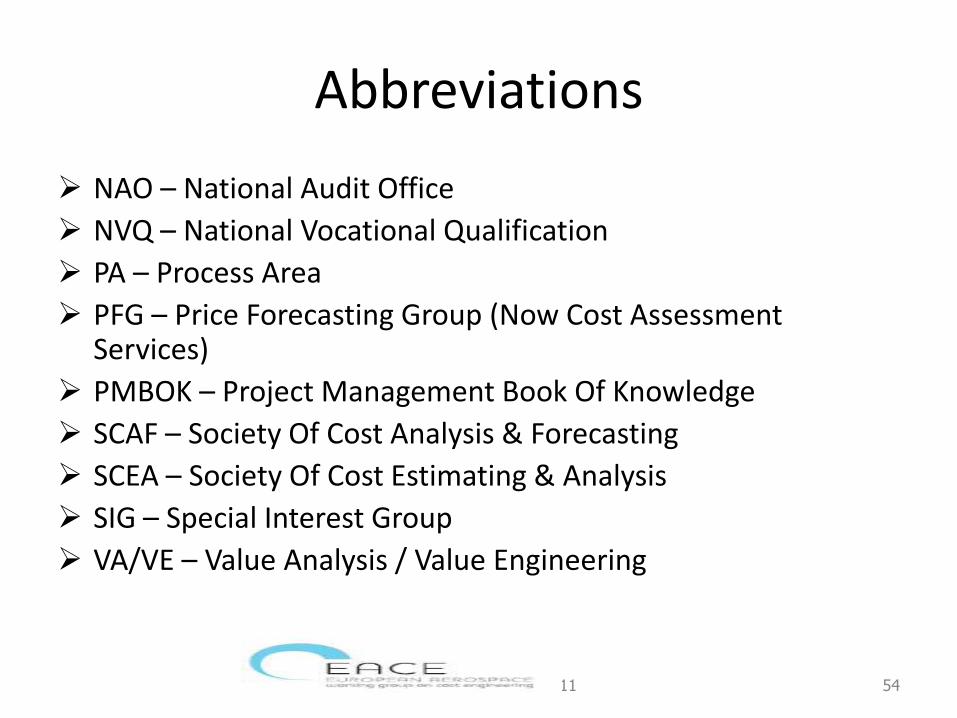

NAO – National Audit Office

NVQ – National Vocational Qualification

PA – Process Area

PFG – Price Forecasting Group (Now Cost Assessment Services)

PMBOK – Project Management Book Of Knowledge

SCAF – Society Of Cost Analysis & Forecasting

SCEA – Society Of Cost Estimating & Analysis

SIG – Special Interest Group

VA/VE – Value Analysis / Value Engineering

Dave Lewis November 2011 54

Contact Details.

Dave Lewis November 2011 55