36200-013: Project Completion Report · SSPD TA – – SME and ... Project Completion Report...

47

Completion Report Project Number: 36200-013 Loan Number: 2549 August 2015 Bangladesh: Small and Medium-Sized Enterprise Development Project This document is being disclosed to the public in accordance with ADB’s Public Communications Policy 2011.

Transcript of 36200-013: Project Completion Report · SSPD TA – – SME and ... Project Completion Report...

Completion Report

Project Number: 36200-013 Loan Number: 2549 August 2015

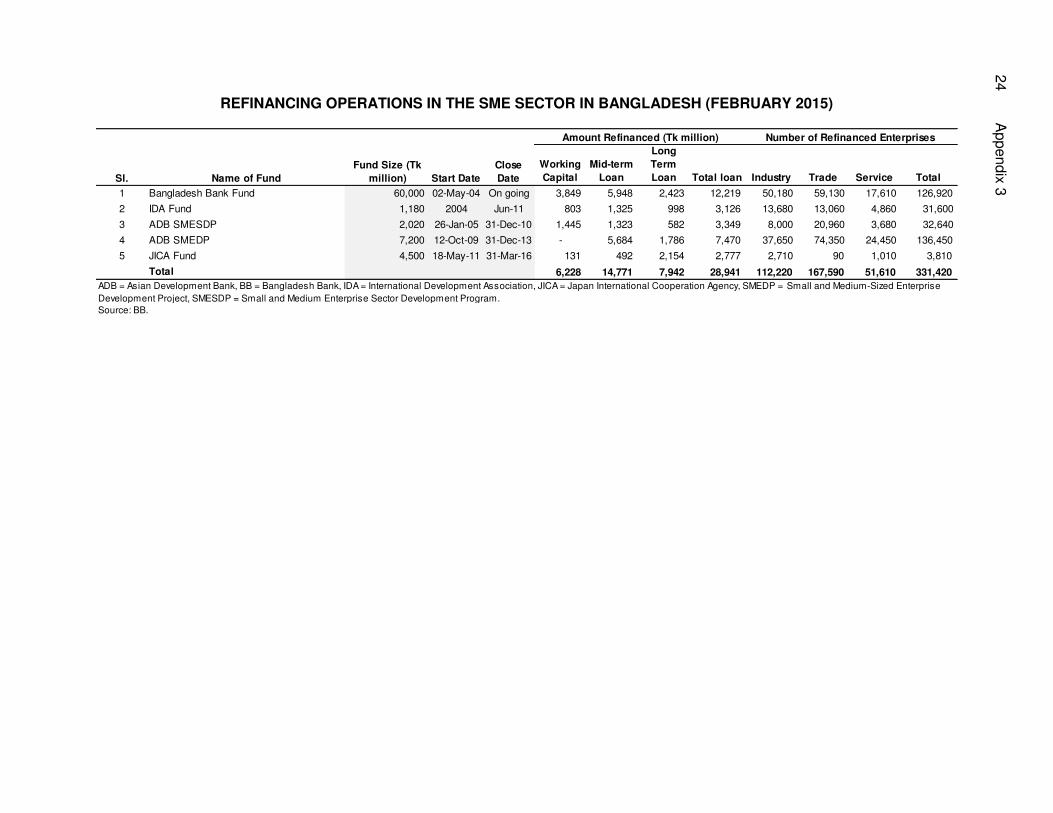

Bangladesh: Small and Medium-Sized Enterprise Development Project This document is being disclosed to the public in accordance with ADB’s Public Communications Policy 2011.

CURRENCY EQUIVALENTS

Currency Unit – taka (Tk)

At Appraisal At Project Completion 25 August 2009 31 December 2013

Tk1.00 = $0.0144812 $0.012874 $1.00 = Tk69.05500 Tk77.675

ABBREVIATIONS

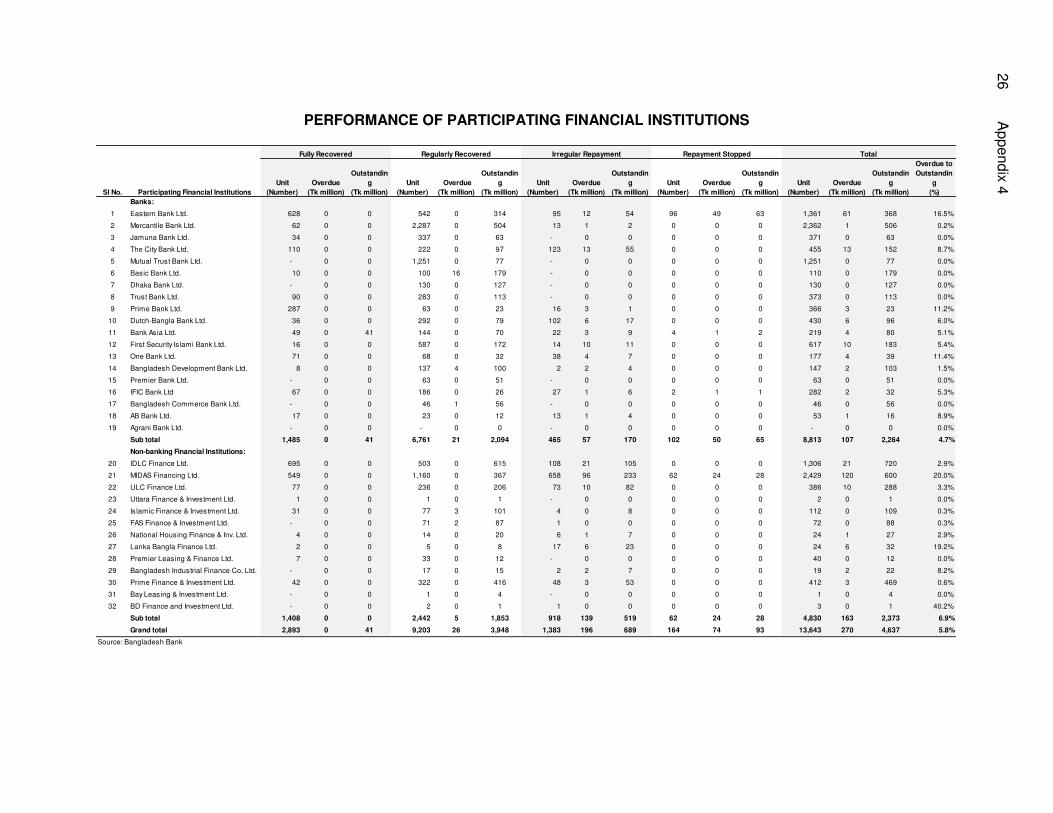

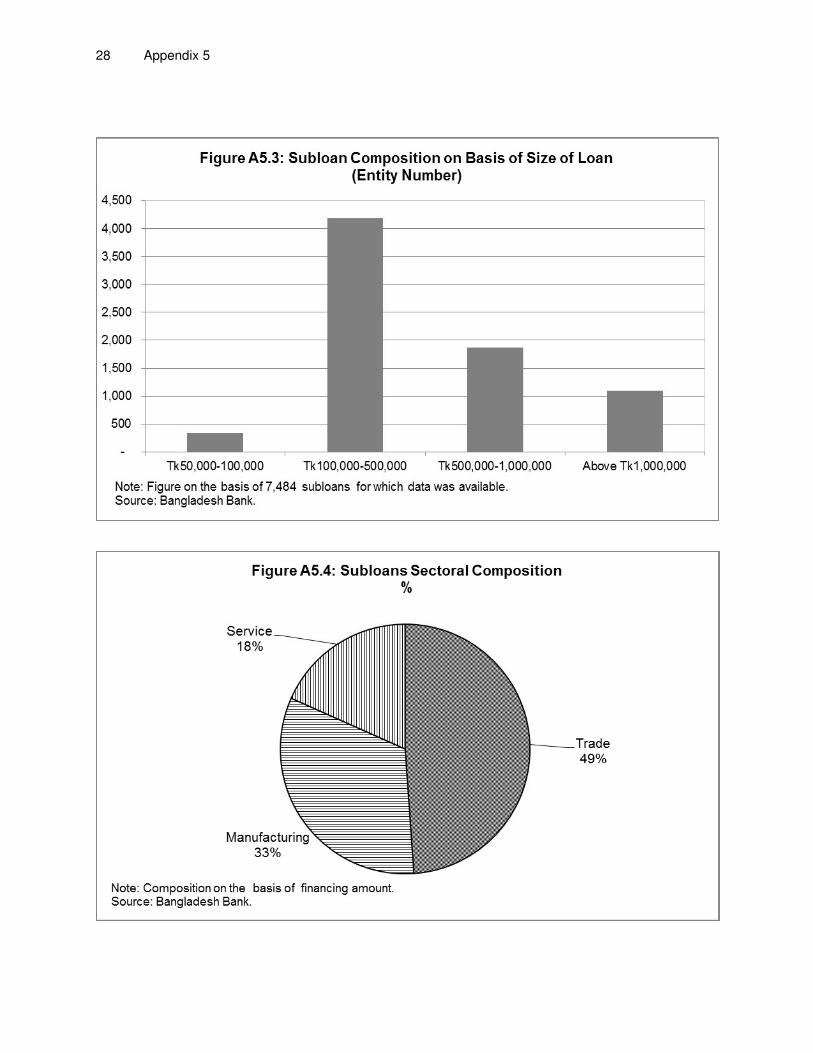

ACSPD – Agricultural Credit and Special Programmes Department ADB – Asian Development Bank BB – Bangladesh Bank BFID

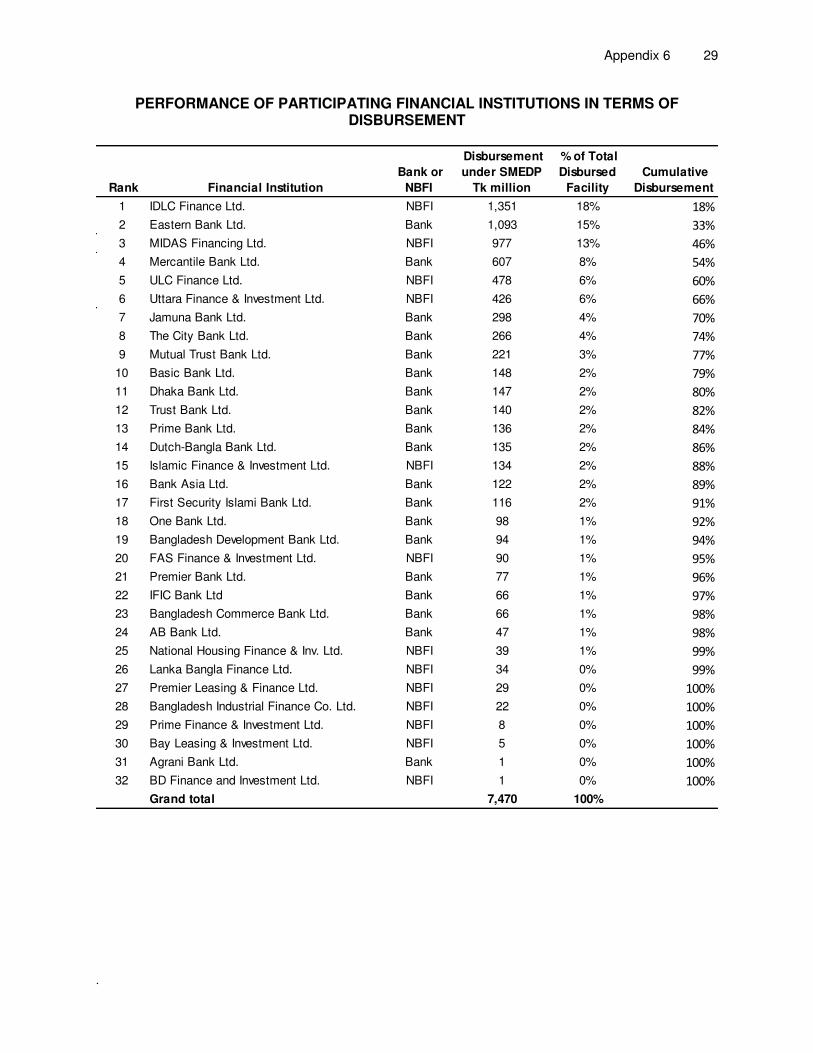

BWCCI – –

Bank and Financial Institutions Division Bangladesh Women Chamber of Commerce and Industry

DMF FAPAD

– –

design and monitoring framework Foreign Aided Project Audit Directorate

GAP GDP

– –

gender action plan gross domestic product

MOF NBFI

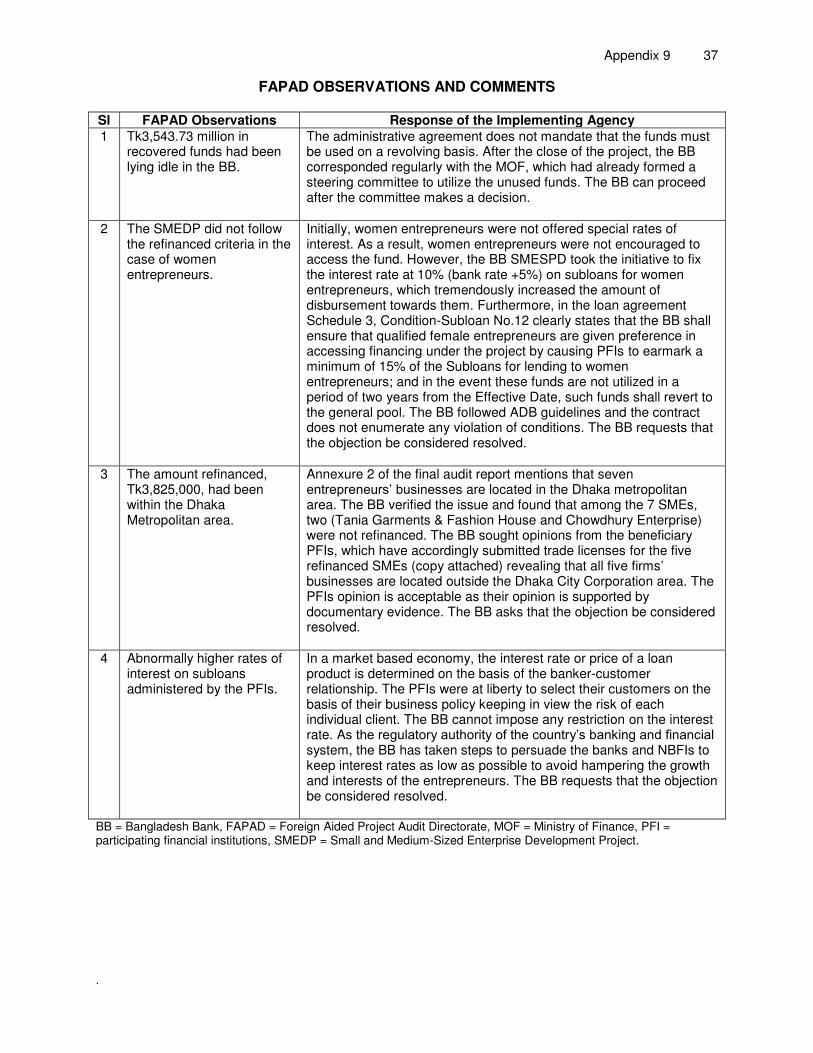

– –

Ministry of Finance nonbank financial institution

NPL – non-performing loan PFI – participating financial institution RRP

SDR – –

report and recommendation of the President special drawing right

SME – small and medium-sized enterprise SMEDP

SMESDP – –

Small and Medium-Sized Enterprise Development Project Small and Medium Enterprise Sector Development Program

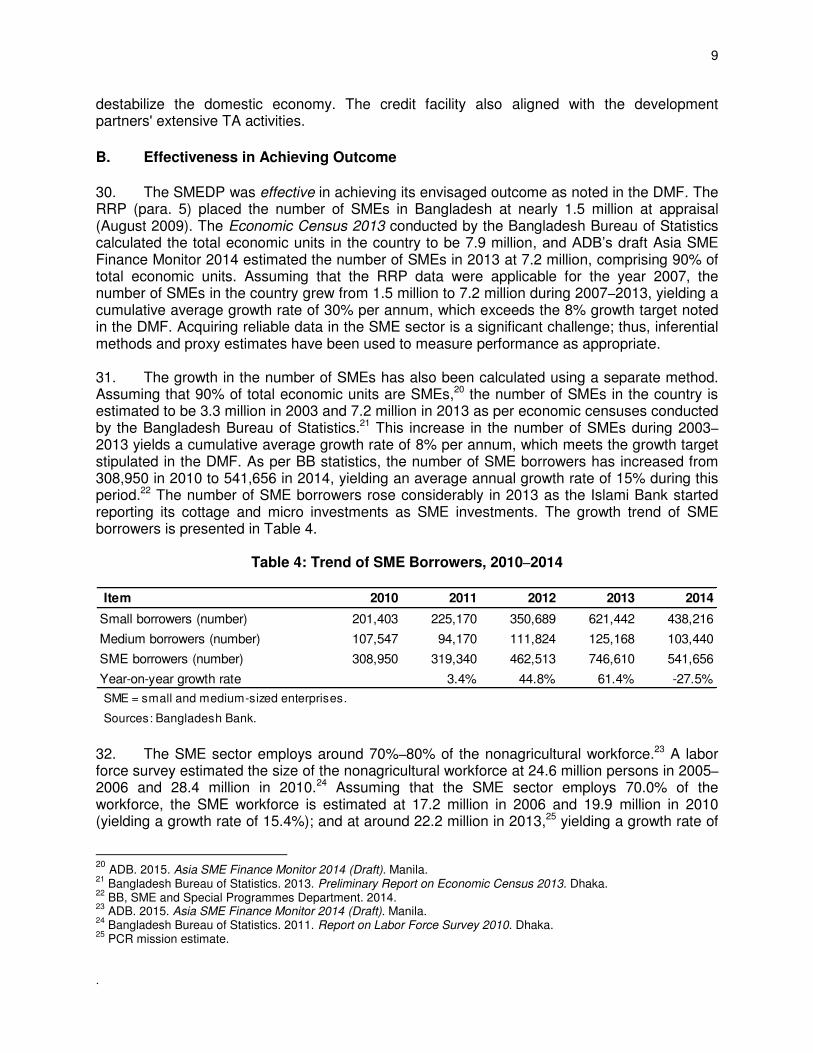

SSPD TA

– –

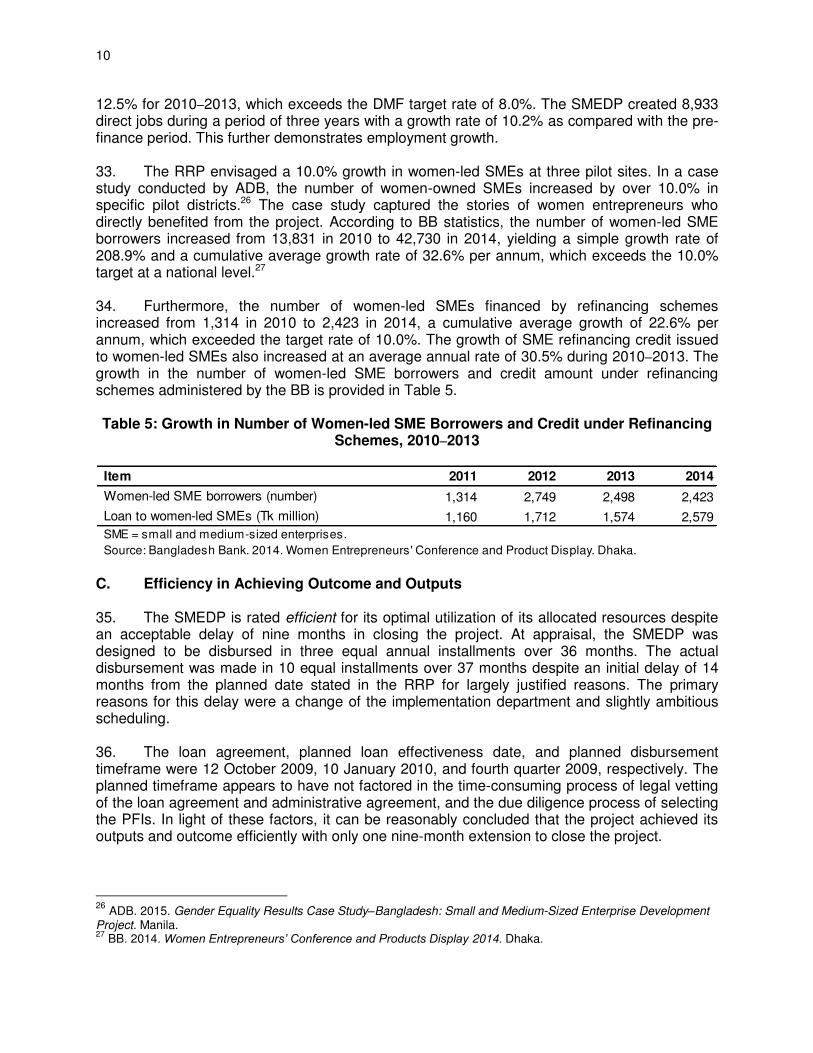

SME and Special Programmes Department technical assistance

NOTES (i) The fiscal year (FY) of the Government of Bangladesh ends on 30 June. FY before a

calendar year denotes the year in which the fiscal year ends, e.g., FY2015 ends on 30 June 2015.

(ii) In this report, "$" refers to US dollars. Vice-President W. Zhang, Vice President, Operations 1 Director General H. Kim, South Asia Department (SARD) Director K. Higuchi, Bangladesh Resident Mission (BRM), SARD Team leader B. Saha, Senior Project Officer, SARD Team members N. Alam, Associate Project Officer, SARD

N. Aziz, Operations Assistant, SARD In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area.

CONTENTS

Page

BASIC DATA i

I. PROJECT DESCRIPTION 1

II. EVALUATION OF DESIGN AND IMPLEMENTATION 1

A. Relevance of Design and Formulation 1

B. Project Outputs 3

C. Project Costs 5

D. Disbursements 6

E. Project Schedule 6

F. Implementation Arrangements 6

G. Conditions and Covenants 7

H. Related Technical Assistance 7

I. Consultant Recruitment and Procurement 7

J. Performance of Consultants, Contractors, and Suppliers 7

K. Performance of the Borrower and the Executing Agency 8

L. Performance of the Asian Development Bank 8

III. EVALUATION OF PERFORMANCE 8

A. Relevance 8

B. Effectiveness in Achieving Outcome 9

C. Efficiency in Achieving Outcome and Outputs 10

D. Preliminary Assessment of Sustainability 11

E. Impact 11

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS 12

A. Overall Assessment 12

B. Lessons 12

C. Recommendations 13 APPENDIXES 1. Design and Monitoring Framework 16 2. Analysis of Achievements of Gender Action Plan 20 3. Refinancing Operations in the SME Sector in Bangladesh (February 2015) 24 4. Performance of Participating Financial Institutions 25 5. Characteristics of Subloans 27 6. Performance of Participating Financial Institutions in Terms of Disbursement 29 7. Implementation Schedule and Disbursement 30 8. Status of Compliance with Loan Covenants 31 9. FAPAD Observations and Comments 37 10. Technical Assistance Completion Report 38 11. Definition of Cottage, Micro, Small, and Medium-Sized Enterprises 41

BASIC DATA A. Loan Identification 1. Country 2. Loan Number 3. Loan Title 4. Borrower 5. Executing Agency 6. Amount of Loan 7. Project Completion Report Number

Bangladesh 2549-BAN(SF) Small and Medium-Sized Enterprise Development Project People’s Republic of Bangladesh Bank and Financial Institutions Division, Ministry of Finance SDR48,927,000 BAN 1525

B. Loan Data 1. Appraisal – Date Started – Date Completed 2. Loan Negotiations – Date Started – Date Completed 3. Date of Board Approval 4. Date of Loan Agreement 5. Date of Loan Effectiveness – In Loan Agreement – Revised – Number of Extensions 6. Closing Date – In Loan Agreement – Revised – Number of Extensions 7. Terms of Loan – Interest Rate – Maturity (number of years) – Grace Period (number of years)

20 July 2009 22 July 2009 17 August 2009 18 August 2009 17 September 2009 12 October 2009 10 Jan 2010 3 May 2010 3 30 March 2013 31 December 2013 1 1% per annum during grace period 1.5% per annum thereafter 32 8

8. Disbursements a. Dates Initial Disbursement

28 February 2011

Final Disbursement

9 April 2014

Time Interval

37.9 months

Effective Date

3 May 2010

Original Closing Date

30 March 2013

Time Interval

35.4 months

ii

b. Amount (SDR)

Category No. (1)

Category or

Subloan (2)

Original Allocation

(3)

Partial Cancellations

(4 = 3 – 5)

Last Revised Allocation

(5)

Amount Disbursed

(6)

Undisbur-sed

Balance

(7 = 5 – 6)

01 Subloan 48,927,000 0 48,927,000 48,927,000 0 Total (local

currency)

48,927,000 48,927,000

0 0

48,927,000 48,927,000

48,927,000 48,927,000

0 0

Total ($ equivalent)

48,927,000 76,000,000

a

0 0

48,927,000 74,973,161

b

48,927,000 74,973,161

0 0

a US dollar equivalent as per the report and recommendation of the President.

b US dollar equivalent as of date of closing the loan account. Amount varies due to exchange rate fluctuation from SDR to $, and from $ to Tk.

SDR = special drawing right. Source: The Asian Development Bank’s Loan Financial Information System.

C. Project Data

1. Project Cost ($ million)

Cost Appraisal Estimate Actual

ADB Project Loan 76.00 74.97 Government (BB) Contribution 19.00 19.00 PFI Contribution 19.00 19.00 SME Contribution Contingencies Financing Charges during Implementation

12.67 0.00 0.00

12.60 0.00 0.00

Total 126.67 125.57 ADB = Asian Development Bank; BB = Bangladesh Bank, PFI = participating financial institution, SME = small and medium-sized enterprises. Source: BB, SME and Special Programmes Department. 2013. Project Monitoring Report (PMR). Dhaka.

2. Financing Plan ($ million) Source Appraisal Estimate Actual

ADB 76.00 74.97 Government (BB) 19.00 19.00 PFIs 19.00 19.00 SMEs 12.67 12.60 Total 126.67 125.57

ADB = Asian Development Bank, BB = Bangladesh Bank, PFI = participating financial institution, SME = small and medium-sized enterprises. Sources: BB, SME and Special Programmes Department. 2013. Project Monitoring Report (PMR). Dhaka; ADB’s Loan Financial Information System.

3. Breakdown of Subloans ($ million) Component Projected

a Actual

Banks 38.91 Non-banking Financial Institutions 36.06 Total 74.97 a No projection in the report and recommendation of the President.

Source: Bangladesh Bank, SME and Special Programmes Department. 2013. Project Monitoring Report (PMR). Dhaka.

iii

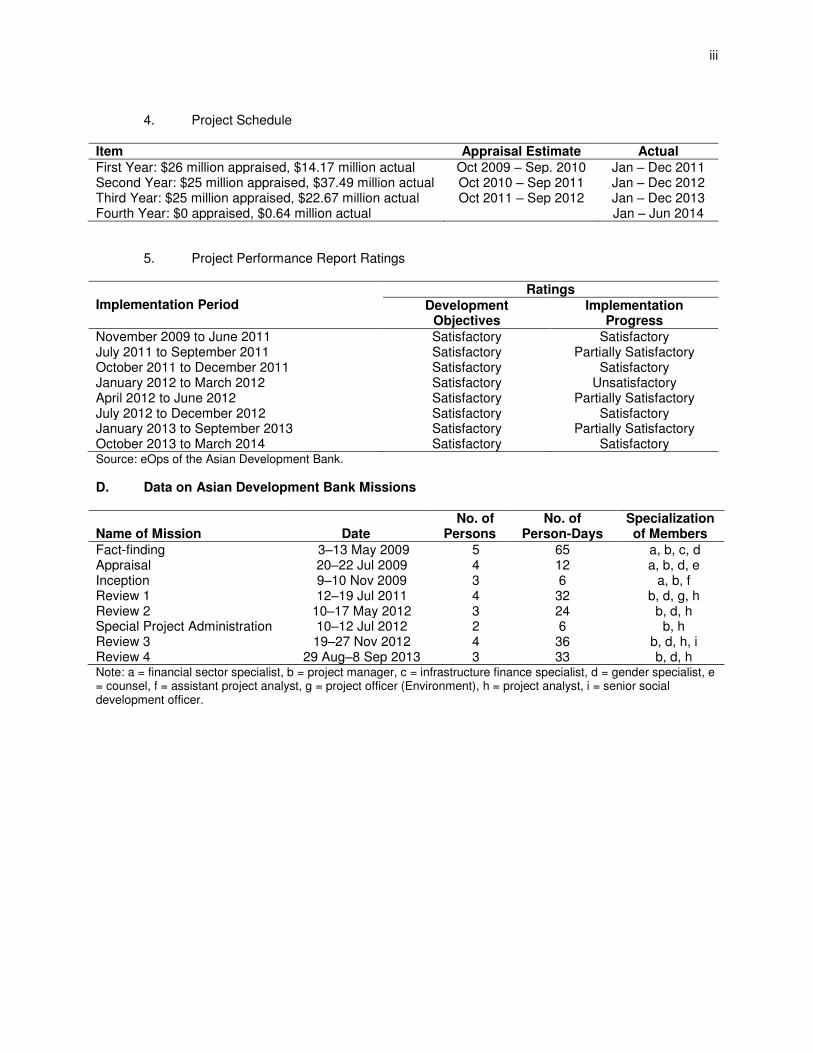

4. Project Schedule Item Appraisal Estimate Actual

First Year: $26 million appraised, $14.17 million actual Oct 2009 – Sep. 2010 Jan – Dec 2011 Second Year: $25 million appraised, $37.49 million actual Oct 2010 – Sep 2011 Jan – Dec 2012 Third Year: $25 million appraised, $22.67 million actual Oct 2011 – Sep 2012 Jan – Dec 2013 Fourth Year: $0 appraised, $0.64 million actual Jan – Jun 2014

5. Project Performance Report Ratings Implementation Period

Ratings

Development Objectives

Implementation Progress

November 2009 to June 2011 Satisfactory Satisfactory July 2011 to September 2011 Satisfactory Partially Satisfactory October 2011 to December 2011 Satisfactory Satisfactory January 2012 to March 2012 Satisfactory Unsatisfactory April 2012 to June 2012 Satisfactory Partially Satisfactory July 2012 to December 2012 Satisfactory Satisfactory January 2013 to September 2013 Satisfactory Partially Satisfactory October 2013 to March 2014 Satisfactory Satisfactory Source: eOps of the Asian Development Bank.

D. Data on Asian Development Bank Missions

Name of Mission

Date

No. of Persons

No. of Person-Days

Specialization of Members

Fact-finding 3–13 May 2009 5 65 a, b, c, d Appraisal 20–22 Jul 2009 4 12 a, b, d, e Inception 9–10 Nov 2009 3 6 a, b, f Review 1 12–19 Jul 2011 4 32 b, d, g, h Review 2 10–17 May 2012 3 24 b, d, h Special Project Administration Review 3

10–12 Jul 2012 19–27 Nov 2012

2 4

6 36

b, h b, d, h, i

Review 4 29 Aug–8 Sep 2013 3 33 b, d, h Note: a = financial sector specialist, b = project manager, c = infrastructure finance specialist, d = gender specialist, e = counsel, f = assistant project analyst, g = project officer (Environment), h = project analyst, i = senior social development officer.

I. PROJECT DESCRIPTION 1. On 17 September 2009, the Asian Development Bank (ADB) approved a $76 million equivalent loan to Bangladesh from ADB’s Special Funds to implement a Small and Medium-sized Enterprise Development Project (SMEDP).1 The credit facility aimed to accelerate the development of small and medium-sized enterprises (SMEs)—especially in rural and nonurban areas outside the metropolitan areas of Dhaka and Chittagong, Bangladesh’s two largest cities—by improving their access to medium- and long-term credit through participating financial institutions (PFIs), which would reduce regional disparities. The project also particularly emphasized the development of women’s entrepreneurship by allocating a minimum amount of funds for financing women-led SMEs. The project was executed by the Bank and Financial Institutions Division (BFID) and implemented by the SME and Special Programmes Department (SSPD) of the Bangladesh Bank (BB), the country’s central bank. The project closing date was extended by nine months to 31 December 2013. The design and monitoring framework (DMF) containing the impact, outcome, and output parameters along with the status of achievements is in Appendix 1. 2. To enhance the sustainability of the project, an associated technical assistance (TA) grant of $500,000 was approved through regional TA 6337 (Development Partnership Program for South Asia), funded under the Australia–ADB South Asia Development Partnership Facility, and administered by ADB.2 The objective of this TA subproject was to enhance the capacity of women entrepreneurs to have full access to the financial resources and services earmarked for women-led SMEs under the project. The TA was implemented by the Bangladesh Women Chamber of Commerce and Industry (BWCCI), and the Finance Division, Ministry of Finance (MOF) acted as the executing agency. The subproject was closed on 31 August 2013. The gender action plan (GAP) along with the status of achievements is in Appendix 2.

II. EVALUATION OF DESIGN AND IMPLEMENTATION A. Relevance of Design and Formulation 3. SMEs as the backbone of the economy. Bangladesh’s economy is driven by the private sector, which comprised 93% of domestic consumption and 83% of investment in FY2009.3 SMEs are the backbone of the private sector, accounting for approximately 99% of private enterprises and employing about 70%–80% of the nonagricultural labor force. Nonmetropolitan SMEs comprise 60%–65% of the country’s 1.5 million SMEs and account for most of the private sector in rural and nonurban areas. These SMEs are a key means of reducing poverty in the country since they generate nonfarm activities that provide more than 50% of the rural population’s employment and income.4 4. Strengthening of SMEs as a key development agenda. Considering the role of SMEs in sustained growth, poverty reduction, and employment generation, the Government of

1 ADB. 2009. Report and Recommendation of the President to the Board of Directors: Proposed Loan to the People’s Republic of Bangladesh for the Small and Medium-Sized Enterprise Development Project. Manila (Loan 2549-BAN).

2 ADB. 2006. Proposed Technical Assistance for the Development Partnership Program for South Asia. Manila. (RETA 6337).

3 MOF, Government of Bangladesh. 2015. Bangladesh Economic Review 2015. Dhaka.

4 ADB. 2009. Report and Recommendation of the President to the Board of Directors: Proposed Loan to the People’s Republic of Bangladesh for the Small and Medium-Sized Enterprise Development Project. Manila. (Loan 2549-BAN) (para. 5).

2

Bangladesh has accepted SME development as an integral part of its development strategy. The government recognizes the private sector as the engine of economic growth and emphasizes supporting SMEs as a dynamic sector with a pivotal role to play in achieving the national goal of accelerated pro-poor growth, sustained poverty reduction, and faster economic development and social progress.5 The Industrial Policy 2010 clearly states that SME development will be one of the cornerstones of the government’s industrialization strategy. 5. Access to financing as a main constraint. An investment climate assessment conducted by the World Bank in 2008 indicated that the scarcity of certain resources (energy, financing, land, and labor skills) is starting to strain Bangladesh’s growth and productivity gains. The demand–supply gap for SMEs was estimated at Tk165 billion against an estimated demand of Tk255 billion at project appraisal.6 The demand–supply gap for SME credit was more pronounced in nonmetropolitan areas where only 6% of SMEs had been able to access formal financing as compared with 51% in metropolitan areas. SMEs were also hindered from obtaining the right type of financing, i.e., medium- and long-term credit, because of the relatively small equity market, virtually non-existent debt market, and asset-liability mismatch in the banking sector. The Sixth Five-Year Plan also recognized the availability of credit as one of the most important factors for SME development and included comprehensive measures addressing the credit needs of SMEs.7 In addition to all the barriers encountered by SMEs, women entrepreneurs are disadvantaged further as they are more frequently poorly educated. 6. Project design. Designed broadly at appraisal, the project addressed one key constraint—access to financing—by making a $76 million credit line available to PFIs for on-lending to eligible SMEs. To address financing discrimination, the project focused on SMEs located in nonmetropolitan areas and ambitiously allocated 15% of total facility for women entrepreneurs. However, the DMF framework could have defined, set, and monitored performance metrics more specifically. The TA design was appropriate as it complemented the loan facility by supporting women’s entrepreneurship. The project was aligned with the development partners' extensive TA activities. The landscape of SME refinancing schemes is in Appendix 3. 7. Alignment with ADB’s country strategy. ADB’s country strategy and program for Bangladesh during 2006–2010 identified the finance sector in general, and the SME sector in particular as key assistance priorities.8 Apart from recognizing a lack of large and long maturity loans, especially in the rural market, the country partnership strategy midterm review also identified the failure to consider women a distinct target group as a major constraint on the SMEs.9 Although the project attained its key objectives, SMEs must maintain development momentum to achieve accelerated investment, growth, and employment in the economy. In a recent survey, 60.2% of the respondents cited lack of access to financing as a major constraint faced by the SMEs.10 In this context the project is as relevant as it was at appraisal. 5 Government of Bangladesh. 2008. Moving Ahead: National Strategy for Accelerated Poverty Reduction II. Dhaka.

6 Ferrari, A. 2008. Increasing Access to Rural Finance in Bangladesh: The Forgotten “Missing Middle.” Washington,

DC. 7 Government of Bangladesh, Planning Commission, Ministry of Planning. 2011. Sixth Five-Year Plan: FY2011–

FY2015. Dhaka. 8 ADB. 2005. Country Strategy and Program (2006–2010): Bangladesh. Manila.

9 ADB. 2009. Country Partnership Strategy Midterm Review: Bangladesh, 2006–2010. Manila.

10 Bangladesh Integrated Support to Poverty and Inequality Reduction through Enterprise Development (INSPIRED).

2013. The State of the SME Sector – the Manufacturing SME Sector in Bangladesh – Working Paper #3. Dhaka.

3

.

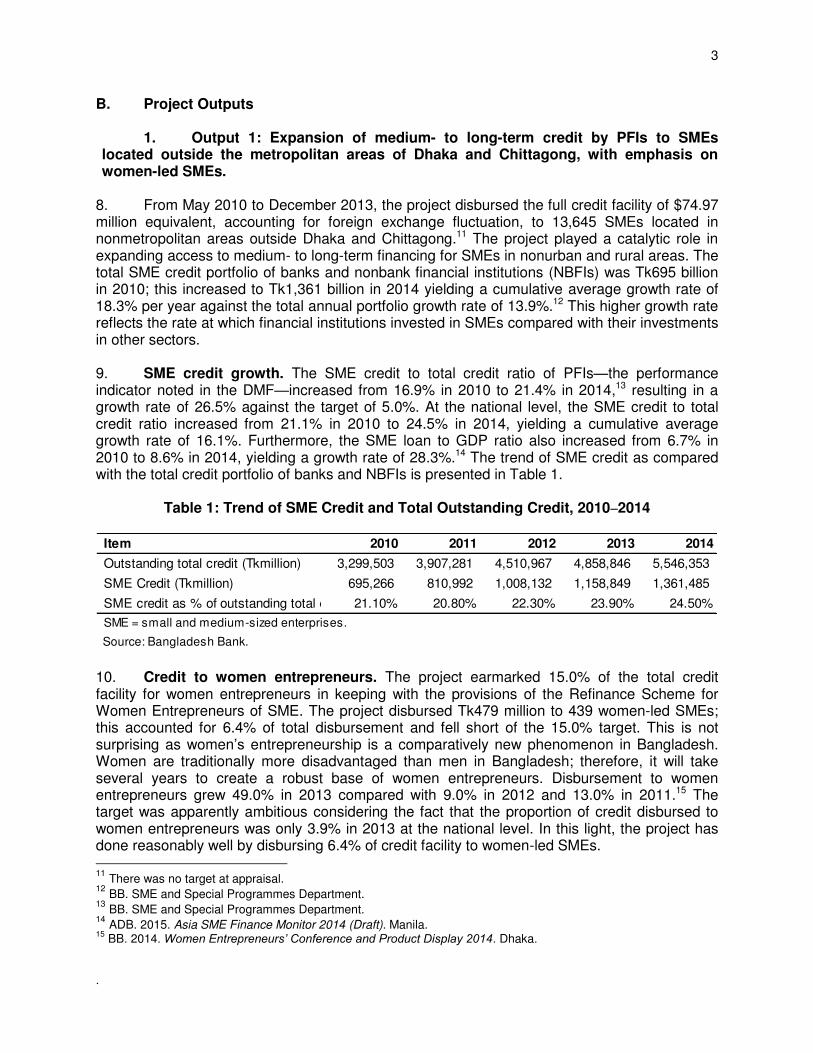

B. Project Outputs

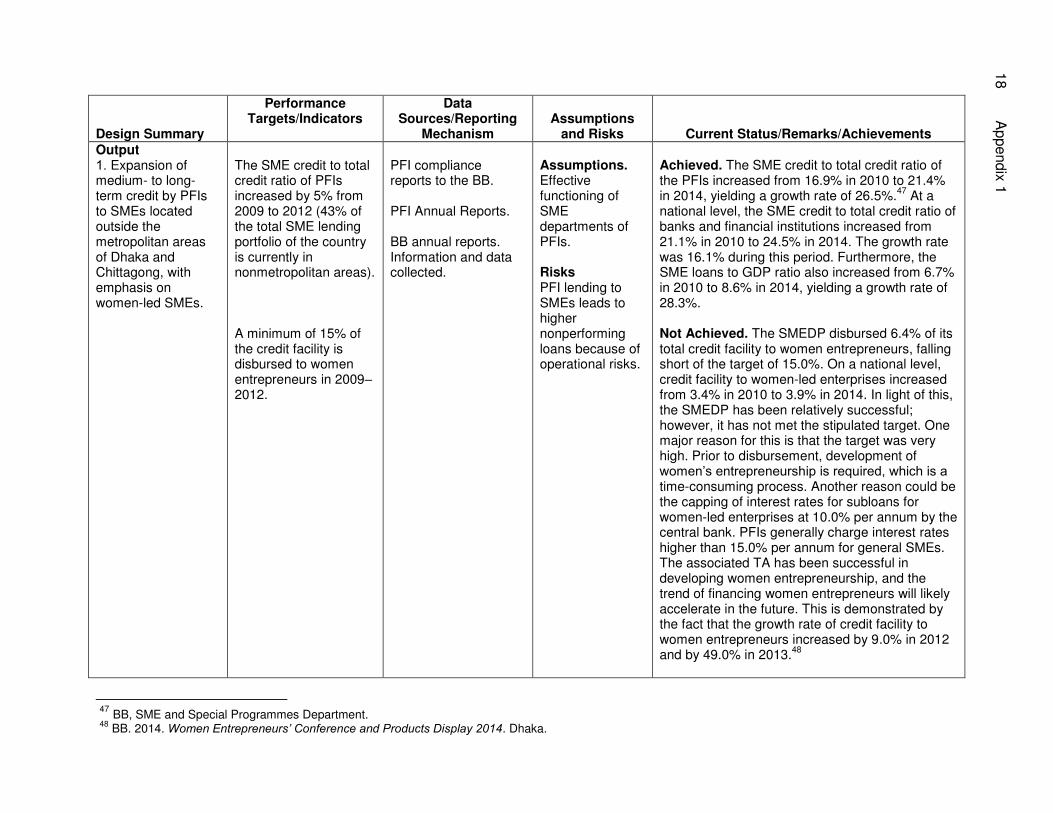

1. Output 1: Expansion of medium- to long-term credit by PFIs to SMEs located outside the metropolitan areas of Dhaka and Chittagong, with emphasis on women-led SMEs.

8. From May 2010 to December 2013, the project disbursed the full credit facility of $74.97 million equivalent, accounting for foreign exchange fluctuation, to 13,645 SMEs located in nonmetropolitan areas outside Dhaka and Chittagong.11 The project played a catalytic role in expanding access to medium- to long-term financing for SMEs in nonurban and rural areas. The total SME credit portfolio of banks and nonbank financial institutions (NBFIs) was Tk695 billion in 2010; this increased to Tk1,361 billion in 2014 yielding a cumulative average growth rate of 18.3% per year against the total annual portfolio growth rate of 13.9%.12 This higher growth rate reflects the rate at which financial institutions invested in SMEs compared with their investments in other sectors. 9. SME credit growth. The SME credit to total credit ratio of PFIs—the performance indicator noted in the DMF—increased from 16.9% in 2010 to 21.4% in 2014,13 resulting in a growth rate of 26.5% against the target of 5.0%. At the national level, the SME credit to total credit ratio increased from 21.1% in 2010 to 24.5% in 2014, yielding a cumulative average growth rate of 16.1%. Furthermore, the SME loan to GDP ratio also increased from 6.7% in 2010 to 8.6% in 2014, yielding a growth rate of 28.3%.14 The trend of SME credit as compared with the total credit portfolio of banks and NBFIs is presented in Table 1.

Table 1: Trend of SME Credit and Total Outstanding Credit, 2010–2014

10. Credit to women entrepreneurs. The project earmarked 15.0% of the total credit facility for women entrepreneurs in keeping with the provisions of the Refinance Scheme for Women Entrepreneurs of SME. The project disbursed Tk479 million to 439 women-led SMEs; this accounted for 6.4% of total disbursement and fell short of the 15.0% target. This is not surprising as women’s entrepreneurship is a comparatively new phenomenon in Bangladesh. Women are traditionally more disadvantaged than men in Bangladesh; therefore, it will take several years to create a robust base of women entrepreneurs. Disbursement to women entrepreneurs grew 49.0% in 2013 compared with 9.0% in 2012 and 13.0% in 2011.15 The target was apparently ambitious considering the fact that the proportion of credit disbursed to women entrepreneurs was only 3.9% in 2013 at the national level. In this light, the project has done reasonably well by disbursing 6.4% of credit facility to women-led SMEs. 11

There was no target at appraisal. 12

BB. SME and Special Programmes Department. 13

BB. SME and Special Programmes Department. 14

ADB. 2015. Asia SME Finance Monitor 2014 (Draft). Manila. 15

BB. 2014. Women Entrepreneurs’ Conference and Product Display 2014. Dhaka.

Item 2010 2011 2012 2013 2014

Outstanding total credit (Tkmillion) 3,299,503 3,907,281 4,510,967 4,858,846 5,546,353

SME Credit (Tkmillion) 695,266 810,992 1,008,132 1,158,849 1,361,485

SME credit as % of outstanding total c 21.10% 20.80% 22.30% 23.90% 24.50%

SME = small and medium-sized enterprises.

Source: Bangladesh Bank.

4

11. Regional disparities. The project emphasized the importance of enhancing rural SMEs’ access to finance by allocating the entire fund for nonmetropolitan SMEs. During 2011–2014, SME financing in the urban sector increased at an average rate of 24.3% per annum, compared with 20.9% for rural SMEs.16 According to the Asia SME Finance Monitor database, in 2014, 74.8% of all SME loans in Bangladesh were disbursed in urban areas while only 25.2% were disbursed in rural areas. This indicates the geographical gap in SME finance and the need for further assistance in the country.

12. Subloan characteristics. The SMEDP provided subloans to 13,645 SMEs, of which 6,589 (48%) were new companies. Of the total credit line, 48.9% was disbursed to the trading sector, 32.8% to the manufacturing sector, and 18.3% to the service sector. Trading enterprises have fewer difficulties in securing financing from commercial banks. The repayment performance of subloans was good with an aggregate overdue of 5.8% against the national non-performing loan (NPL) ratio of 11.6% in 2014.17 Interest rates were market-based, excluding loans for women entrepreneurs, which were capped at 10% by the central bank. The pricing of subloans does not have any obvious correlation with industrial sectors and location. The majority of disbursed subloans (76.1%) were mid-term loans with a tenor of 2–3 years, while 23.9% were long-term with a tenor of 3 years or more. Subloan performance with regard to the banks is detailed in Appendix 4, and some important characteristics of the subloan portfolio are provided in Appendix 5. 13. Performance of PFIs. The BB selected 32 banks and NBFIs as the PFIs according to eligibility criteria provided by ADB. Of the total disbursed amount of Tk7,470 million, the banks disbursed Tk3,877 million (52%) while the NBFIs disbursed Tk3,592 million (48%). This disbursement structure represents a significant shift from the previous $30 million Small and Medium-sized Enterprise Sector Development Program (SMESDP) through which banks disbursed 80% of the total credit facility and NBFIs 20%, indicating the increased focus of NBFIs on SME financing. NBFIs find refinancing schemes particularly useful because of their higher cost of deposits and lack of fee-based income as compared with banks. The disbursement performance of banks and NBFIs is shown in Table 2.

Table 2: Disbursement Performance of Banks and NBFIs

14. IDLC Finance Ltd., an NBFI, emerged as the leading financial institution in terms of disbursements, followed by Eastern Bank Ltd. The top 11 financial institutions disbursed 80% of the total credit facility while 21 financial institutions disbursed the remaining 20%, indicating the 16

ADB. 2015. Asia SME Finance Monitor 2014 (Draft). Manila. 17

BB. SME and Special Programmes Department.

Item

Amount in Tk

million

% of Total

Facility

Amount in Tk

million

% of Total

Facility

Banks 2,694 80% 3,877 52%

NBFIs 655 20% 3,592 48%

Total 3,349 100% 7,470 100%

SMESDP (2010) SMEDP (2013)

SMESDP = Small and Medium Enterprise Sector Development Program, SMEDP = Small and Medium-Sized

Enterprise Development Program, NBFIs = nonbank financial institutions.

Source: Bangladesh Bank.

5

.

extent to which financial institutions’ capability for and/or interest in utilizing the project facility are skewed. The league table according to rate of disbursement is provided in Appendix 6.

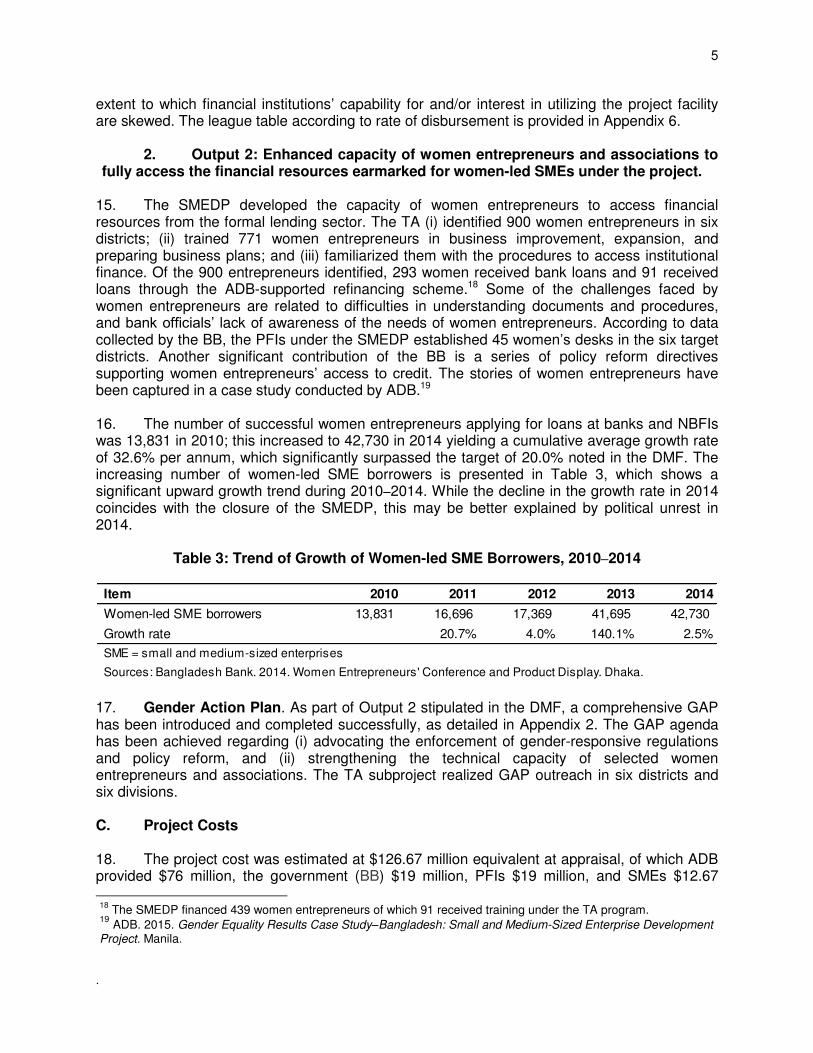

2. Output 2: Enhanced capacity of women entrepreneurs and associations to fully access the financial resources earmarked for women-led SMEs under the project.

15. The SMEDP developed the capacity of women entrepreneurs to access financial resources from the formal lending sector. The TA (i) identified 900 women entrepreneurs in six districts; (ii) trained 771 women entrepreneurs in business improvement, expansion, and preparing business plans; and (iii) familiarized them with the procedures to access institutional finance. Of the 900 entrepreneurs identified, 293 women received bank loans and 91 received loans through the ADB-supported refinancing scheme.18 Some of the challenges faced by women entrepreneurs are related to difficulties in understanding documents and procedures, and bank officials’ lack of awareness of the needs of women entrepreneurs. According to data collected by the BB, the PFIs under the SMEDP established 45 women’s desks in the six target districts. Another significant contribution of the BB is a series of policy reform directives supporting women entrepreneurs’ access to credit. The stories of women entrepreneurs have been captured in a case study conducted by ADB.19 16. The number of successful women entrepreneurs applying for loans at banks and NBFIs was 13,831 in 2010; this increased to 42,730 in 2014 yielding a cumulative average growth rate of 32.6% per annum, which significantly surpassed the target of 20.0% noted in the DMF. The increasing number of women-led SME borrowers is presented in Table 3, which shows a significant upward growth trend during 2010–2014. While the decline in the growth rate in 2014 coincides with the closure of the SMEDP, this may be better explained by political unrest in 2014.

Table 3: Trend of Growth of Women-led SME Borrowers, 2010–2014

17. Gender Action Plan. As part of Output 2 stipulated in the DMF, a comprehensive GAP has been introduced and completed successfully, as detailed in Appendix 2. The GAP agenda has been achieved regarding (i) advocating the enforcement of gender-responsive regulations and policy reform, and (ii) strengthening the technical capacity of selected women entrepreneurs and associations. The TA subproject realized GAP outreach in six districts and six divisions. C. Project Costs 18. The project cost was estimated at $126.67 million equivalent at appraisal, of which ADB provided $76 million, the government (BB) $19 million, PFIs $19 million, and SMEs $12.67

18

The SMEDP financed 439 women entrepreneurs of which 91 received training under the TA program. 19

ADB. 2015. Gender Equality Results Case Study–Bangladesh: Small and Medium-Sized Enterprise Development Project. Manila.

Item 2010 2011 2012 2013 2014

Women-led SME borrowers 13,831 16,696 17,369 41,695 42,730

Growth rate 20.7% 4.0% 140.1% 2.5%

SME = small and medium-sized enterprises

Sources: Bangladesh Bank. 2014. Women Entrepreneurs' Conference and Product Display. Dhaka.

6

million. The credit facility has been fully disbursed at $74.97 million (the difference from $76 million is due to exchange rate fluctuations between SDR and the US dollar). The BB disbursed $19 million as planned and ensured, by way of agreement, the contributions of the PFIs and SMEs. D. Disbursements 19. The SMEDP was designed to be disbursed in three equal annual installments in three successive years. However, actual disbursement was 19%, 50%, and 30% in the first three years with the remaining 1% disbursed in the fourth year. The first disbursement was delayed by 14 months due to an administrative changeover in the implementing agency by which implementation responsibilities were switched to a new department. At appraisal, the Agricultural Credit and Special Programmes Department (ACSPD) was selected as the implementing agency; however, the BB created a new division, the SSPD, for this role in December 2010. Although this changeover required lengthy administrative procedures that delayed the first disbursement of the project, the project gained momentum quickly and disbursed 50% of the funds in the second year. Despite these initial delays, the total fund was almost fully disbursed in the three years projected. The implementation and disbursement schedule is in Appendix 7. E. Project Schedule 20. As estimated at appraisal, the project began in July 2009; however due to procedural delays involving legal vetting of the project documents, the effectiveness of the project was delayed by four months with three extensions. The first disbursement was delayed by 14 months from the date estimated at appraisal. The estimate was highly optimistic as it did not account for the fact that the selection of PFIs is a time-consuming process. The changeover of responsibilities to a new implementing team was also a major reason for this delay. The project closed in December 2013, nine months after the projected date at appraisal with only one extension. The project schedule is provided in Appendix 7. F. Implementation Arrangements 21. The implementation arrangements, as mentioned in the report and recommendation of the President (RRP) (para. 49) were followed by minor changes to improve them. As per the RRP, the ACSPD was the planned implementing agency. After the signing of the loan agreement, the BB created a new SME-focused department, the SSPD, intended to focus specifically on SME development in the country. The administration of the new department was linked with the BFID of the MOF, which therefore acquired the role of executing agency. The implementation arrangement was found to be adequate and effective as a result of these changes, which had no effect on the covenants. A high-level project steering committee was formed with the BFID Secretary as the chairperson. The committee met as and when necessary to guide the project and resolve any issues that required a decision from high-level government officials. An ADB representative sat on the committee as an observer. The project implementation arrangements were appropriate. ADB contracted the BWCCI to implement the TA subproject, and the Finance Division of the MOF had overall responsibility of supervision as the executing agency.

7

.

G. Conditions and Covenants 22. The loan agreement contained 25 conditions and covenants under 12 broad categories: implementation arrangements, PFI eligibility criteria, qualified enterprise, qualified subproject, subloan, safeguards, GAP, anticorruption, project performance monitoring and evaluation, reporting, and project review. A minor change was made to the implementation arrangements reassigning the implementation and execution responsibilities to the newly established SSPD and the BFID. The loan covenants were relevant to the project design and implementation. All major loan covenants were generally complied with as outlined in Appendix 8; however, the Foreign Aided Project Audit Directorate (FAPAD) made four minor observations that were addressed by the implementing agency and are expected to be resolved. The list of FAPAD audit observations and responses of the implementing agency is in Appendix 9. The BB reported no issues with regard to the PFIs’ compliance with the environmental management system framework under the credit line. In keeping with the loan agreement, the implementing agency did not provide an annual environmental compliance monitoring report, and this topic was not raised by the ADB review missions as reported by the implementing agency. The implementing agency requested project management support for better implementation and compliance with all covenants in the future. H. Related Technical Assistance 23. The TA subproject was developed to address challenges faced by women entrepreneurs in accessing financial resources and refinancing schemes. The TA completion report rated the project highly successful as the subproject achieved its intended impact by developing women’s entrepreneurship in six selected districts and achieved its outcome by enhancing the capacity of women entrepreneurs and associations to access the financial resources and services earmarked for women-led SMEs under the project. The subproject outputs were achieved by identifying constraints on women entrepreneurship, creating advocacy initiatives, building capacity, and disseminating findings to relevant stakeholders. The TA completion report of the subproject is in Appendix 10.

I. Consultant Recruitment and Procurement 24. There was no recruitment of consultants or procurement of any items (goods or works) under the loan component. To implement the TA subproject, ADB recruited the BWCCI following the Guidelines on the Use of Consultants by ADB and its Borrowers and using single source selection. The team of consultants included the team leader, training coordinator, advocacy coordinator, and accounts officer (each for 36 months); and the monitoring consultant (intermittent for six months over 36 months). J. Performance of Consultants, Contractors, and Suppliers 25. There was no recruitment of consultants in the loan component. The consultants’ performance under the TA subproject was rated satisfactory. The BWCCI project office in Dhaka and women chamber members in the six districts implemented the project in a timely and professional fashion. The team generally performed well. As agreed with ADB, after the closing of the TA the consultants retained the office equipment that they procured under the contract. The suppliers’ performance was also satisfactory in that they supplied the equipment according to the required specifications and in a timely manner.

8

K. Performance of the Borrower and the Executing Agency 26. The performance of the borrower (the government), executing agency, and implementing agency is rated satisfactory. Developing SMEs and women’s entrepreneurship is a priority of the government, which has demonstrated its commitment to this goal by availing the full facility amount in a structured manner. The executing agency, the BFID, guided the implementation of the major outputs, while the BB as the implementing agency implemented the project proactively throughout its duration. The quality of execution and implementation has been satisfactory. L. Performance of the Asian Development Bank 27. ADB’s performance is rated satisfactory. It fielded the inception mission, four review missions, and one special project administration mission. ADB consistently maintained a good relationship with the executing and implementing agencies ensuring the timely implementation of project activities. Due to good progress in the project implementation stage, a semi-annual review mission was not required.

III. EVALUATION OF PERFORMANCE A. Relevance 28. The project was rated relevant at appraisal as it contributed to poverty reduction, remained consistent with government priorities, and aligned with ADB policies and timing. The private sector is the driving force of Bangladesh’s economy, accounting for 93% of consumption and 83% of investment in 2008–2009. SMEs constitute almost all (up to 99%) of private sector enterprises, employing the vast majority (70%–80%) of the non-agrarian workforce and accounting for a quarter of the country's GDP. Nonmetropolitan SMEs are a key means of reducing poverty by generating rural nonfarm activities that provide more than 50% of the rural population’s employment and income. The demand-supply gap for SME credit was more pronounced in nonmetropolitan areas where only 6% of SMEs had access to formal financing as compared with 51% in metropolitan areas. The SMEDP provided nonmetropolitan SMEs with much-needed long-term financing, thus helping to reduce income disparity between the rural and urban population. It also placed special emphasis on women’s entrepreneurship by allocating a designated fund for women entrepreneurs, who are more likely to be disadvantaged than men. The SMEDP not only addressed one of the most pressing problems faced by SMEs, it also focused its resources on the most disadvantaged areas—nonmetropolitan SMEs and women-led SMEs—to achieve greater and more equitable development impact. 29. The SMEDP is highly consistent with government strategies that consider SME development an integral driver of sustained growth, poverty reduction, and employment generation. The National Strategy for Accelerated Poverty Reduction II emphasized the pivotal role of SMEs in achieving the national goal of accelerated pro-poor growth, and the Industrial Policy 2010 clearly states that SME development will be one of the cornerstones of the government’s industrialization strategy. The project also conforms closely to ADB's country strategy for Bangladesh, which identified the SME sector as a key assistance priority. The country partnership strategy midterm review identified the failure to consider women a distinct target group as a major limitation of the SMEs. Moreover, the timing of the project was appropriate in the aftermath of the global financial crisis of 2009–2010, which threatened to

9

.

destabilize the domestic economy. The credit facility also aligned with the development partners' extensive TA activities.

B. Effectiveness in Achieving Outcome

30. The SMEDP was effective in achieving its envisaged outcome as noted in the DMF. The RRP (para. 5) placed the number of SMEs in Bangladesh at nearly 1.5 million at appraisal (August 2009). The Economic Census 2013 conducted by the Bangladesh Bureau of Statistics calculated the total economic units in the country to be 7.9 million, and ADB’s draft Asia SME Finance Monitor 2014 estimated the number of SMEs in 2013 at 7.2 million, comprising 90% of total economic units. Assuming that the RRP data were applicable for the year 2007, the number of SMEs in the country grew from 1.5 million to 7.2 million during 2007–2013, yielding a cumulative average growth rate of 30% per annum, which exceeds the 8% growth target noted in the DMF. Acquiring reliable data in the SME sector is a significant challenge; thus, inferential methods and proxy estimates have been used to measure performance as appropriate. 31. The growth in the number of SMEs has also been calculated using a separate method. Assuming that 90% of total economic units are SMEs,20 the number of SMEs in the country is estimated to be 3.3 million in 2003 and 7.2 million in 2013 as per economic censuses conducted by the Bangladesh Bureau of Statistics.21 This increase in the number of SMEs during 2003–2013 yields a cumulative average growth rate of 8% per annum, which meets the growth target stipulated in the DMF. As per BB statistics, the number of SME borrowers has increased from 308,950 in 2010 to 541,656 in 2014, yielding an average annual growth rate of 15% during this period.22 The number of SME borrowers rose considerably in 2013 as the Islami Bank started reporting its cottage and micro investments as SME investments. The growth trend of SME borrowers is presented in Table 4.

Table 4: Trend of SME Borrowers, 2010–2014

32. The SME sector employs around 70%–80% of the nonagricultural workforce.23 A labor force survey estimated the size of the nonagricultural workforce at 24.6 million persons in 2005–2006 and 28.4 million in 2010.24 Assuming that the SME sector employs 70.0% of the workforce, the SME workforce is estimated at 17.2 million in 2006 and 19.9 million in 2010 (yielding a growth rate of 15.4%); and at around 22.2 million in 2013,25 yielding a growth rate of

20

ADB. 2015. Asia SME Finance Monitor 2014 (Draft). Manila. 21

Bangladesh Bureau of Statistics. 2013. Preliminary Report on Economic Census 2013. Dhaka. 22

BB, SME and Special Programmes Department. 2014. 23

ADB. 2015. Asia SME Finance Monitor 2014 (Draft). Manila. 24

Bangladesh Bureau of Statistics. 2011. Report on Labor Force Survey 2010. Dhaka. 25

PCR mission estimate.

Item 2010 2011 2012 2013 2014

Small borrowers (number) 201,403 225,170 350,689 621,442 438,216

Medium borrowers (number) 107,547 94,170 111,824 125,168 103,440

SME borrowers (number) 308,950 319,340 462,513 746,610 541,656

Year-on-year growth rate 3.4% 44.8% 61.4% -27.5%

SME = small and medium-sized enterprises.

Sources: Bangladesh Bank.

10

12.5% for 2010–2013, which exceeds the DMF target rate of 8.0%. The SMEDP created 8,933 direct jobs during a period of three years with a growth rate of 10.2% as compared with the pre-finance period. This further demonstrates employment growth. 33. The RRP envisaged a 10.0% growth in women-led SMEs at three pilot sites. In a case study conducted by ADB, the number of women-owned SMEs increased by over 10.0% in specific pilot districts.26 The case study captured the stories of women entrepreneurs who directly benefited from the project. According to BB statistics, the number of women-led SME borrowers increased from 13,831 in 2010 to 42,730 in 2014, yielding a simple growth rate of 208.9% and a cumulative average growth rate of 32.6% per annum, which exceeds the 10.0% target at a national level.27

34. Furthermore, the number of women-led SMEs financed by refinancing schemes increased from 1,314 in 2010 to 2,423 in 2014, a cumulative average growth of 22.6% per annum, which exceeded the target rate of 10.0%. The growth of SME refinancing credit issued to women-led SMEs also increased at an average annual rate of 30.5% during 2010–2013. The growth in the number of women-led SME borrowers and credit amount under refinancing schemes administered by the BB is provided in Table 5. Table 5: Growth in Number of Women-led SME Borrowers and Credit under Refinancing

Schemes, 2010–2013

C. Efficiency in Achieving Outcome and Outputs 35. The SMEDP is rated efficient for its optimal utilization of its allocated resources despite an acceptable delay of nine months in closing the project. At appraisal, the SMEDP was designed to be disbursed in three equal annual installments over 36 months. The actual disbursement was made in 10 equal installments over 37 months despite an initial delay of 14 months from the planned date stated in the RRP for largely justified reasons. The primary reasons for this delay were a change of the implementation department and slightly ambitious scheduling. 36. The loan agreement, planned loan effectiveness date, and planned disbursement timeframe were 12 October 2009, 10 January 2010, and fourth quarter 2009, respectively. The planned timeframe appears to have not factored in the time-consuming process of legal vetting of the loan agreement and administrative agreement, and the due diligence process of selecting the PFIs. In light of these factors, it can be reasonably concluded that the project achieved its outputs and outcome efficiently with only one nine-month extension to close the project.

26

ADB. 2015. Gender Equality Results Case Study–Bangladesh: Small and Medium-Sized Enterprise Development Project. Manila. 27

BB. 2014. Women Entrepreneurs’ Conference and Products Display 2014. Dhaka.

Item 2011 2012 2013 2014

Women-led SME borrowers (number) 1,314 2,749 2,498 2,423

Loan to women-led SMEs (Tk million) 1,160 1,712 1,574 2,579

SME = small and medium-sized enterprises.

Source: Bangladesh Bank. 2014. Women Entrepreneurs' Conference and Product Display. Dhaka.

11

.

D. Preliminary Assessment of Sustainability 37. The sustainability of the SMEDP is rated likely. The project was a catalyst for enhancing sustainable access to financing. Banks and NBFIs have largely accepted SME financing as commercially feasible, and have introduced SME divisions and desks dedicated to women entrepreneurs. As a result, the country’s SME financing portfolio increased 98% during 2010–2014 against the total portfolio growth of 68% during the same period.28 Annual financing of women-led enterprises also increased 122% during 2011–2014.29 It is encouraging that a few financial institutions have begun to make SME financing their core business proposition and to provide value-added services, such as insurance, networking, and capacity development, for women entrepreneurs in addition to loans.30 The government introduced an adequate policy and institutional framework for pursing the sustainable development of SMEs in the SME Policy Strategy 2005 and the National Industrial Policy 2010. Complementing the government’s efforts, the BB introduced a number of SME-friendly regulations including the SME Credit Rating Guidelines 2013, SME Credit Program and Policy 2010, and Prudential Regulation for Small Enterprises Financing 2004. The BB is also closely monitoring disbursements by banks and NBFIs’ to SMEs and women entrepreneurs on a periodic basis. 38. Over the years, SME development has been institutionalized in Bangladesh. The government considers SME development a priority and has continuously strengthened the institutional framework supporting this. The government established an SME Cell under the Ministry of Industries responsible for SME policy formulation and strategic SME planning. The SME Foundation, established in 2006, is the primary institution for SME development and is tasked with implementing SME related policies. The BB has established a separate department, the SSPD, to formulate policies on SME development and manage refinancing schemes; it has also set up a new unit named the Women Entrepreneurs Development Unit under the SSPD that focuses on the development of women-led enterprises. In light of the government and stakeholders’ commitment and increasing interest of financial institutions in SME finance, it can reasonably be stated that the SMEDP’s sustainability is quite high. E. Impact 39. The project’s overall impact is significant. The project’s intended impact was to ensure sustained economic growth in the context of the global financial crisis of 2009–2010, which threatened Bangladesh’s economy. A vibrant SME sector was viewed as critical for investment, growth, and jobs creation in the face of a projected economic slowdown, and the project has successfully exerted its desired impact. Bangladesh’s economy continued to grow at an average rate of 6.12% during FY2010–FY2014 against the target of 5.50% noted in the DMF. The average growth of GDP during FY2010–FY2014 was slightly higher than the average growth rate during FY2006–FY2010 (6.07%). In FY2015, GDP growth increased to 6.51% compared with 6.06% in the previous financial year.31 In line with economic growth, the national poverty incidence rate also declined significantly by 5.3 percentage points from 2010 to 2013. In 2010, the percentage of the population below the national poverty line was 31.5%, declining to 26.2% in 2013, which marked significant progress in surpassing the millennium development target of

28

BB, SME and Special Programmes Department. 29

BB. 2014. Women Entrepreneurs' Conference and Product Display. Dhaka. 30

IDLC Finance Ltd. 2015. IDLC Purnota Loan. Dhaka. http://www.idlc.com/Women-Entrepreneur-Loan.php 31

Ministry of Finance. 2015. Bangladesh Economic Review, 2014. Dhaka.

12

29.0%.32 According to official estimates, the poverty incidence rate is expected to decline further to 22.7% in 2015. The project further strengthened the SME sector, which contributed to maintaining the momentum of economic growth despite a challenging global economic climate.

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS A. Overall Assessment 40. The SMEDP is rated successful. It was relevant, accomplished the intended impact, and achieved the outcome and outputs substantially in an effective, efficient, and sustained manner. SMEs constitute more than 90% of all economic units and provide employment to at least 70% of the nonagricultural workforce. However, the growth of SMEs, specifically nonmetropolitan SMEs, has been stunted by a lack of access to medium- and long-term financing, which negatively affects economic development, employment generation, and poverty reduction. The project was relevant as it made available much-needed medium- to long-term financing for SMEs in nonmetropolitan areas with a particular focus on women entrepreneurs who are additionally disadvantaged. It was even more relevant in the context of the global financial crisis threatening the domestic economy. 41. The SMEDP was effective in achieving the primary outputs and outcome by increasing the SME credit to total credit ratio by 16.1% during 2010–2014 (target 5.0%), which was further supplemented by an increase in the SME loans to GDP ratio from 6.7% in 2010 to 8.6% in 2014. This growth in SME credit also contributed to increasing the number of SMEs and SME employment by 30% during 2007–2013 (target 8.0%) and 12.5% during 2010–2013 (target 8.0%), respectively. However, the project only disbursed 6.4% of its total credit facility to women entrepreneurs, which falls short of the allocation of 15.0%. This is not unusual as the development of entrepreneurship is a time-consuming process, and the project has built a foundation for reaping benefits in the future. The SMEDP achieved its intended results efficiently because of strong ownership by the government, implementing agency, and other stakeholders despite a nine-month delay for acceptable reasons. The impact of the SMEDP has been significant as the country maintained an average GDP growth rate of 6.1% during FY2010–FY2014 (target 5.5%), and poverty has been reduced significantly as reflected in the reduction of the national poverty index by 16.8% during 2010–2013 (target 2.0%). The project is likely sustainable as the government has been continuously improving the institutional and regulatory framework to accelerate the development of SMEs and women entrepreneurship. At project closure, SME development is still relevant to elevate economic units to the next level of excellence. B. Lessons

42. Definition of SME. The Ministry of Industries defines enterprises as cottage, micro, small, medium, and large enterprises, on the basis of ‘employment’ and ‘fixed investment’.33 As SMEs, by definition, refers to small and medium-sized enterprises, the nomenclature is frequently misunderstood and used inappropriately to address cottage and micro enterprises as well. Surveys show that cottage and micro enterprises constitute 97% of all industries by

32

General Economic Division, Bangladesh Planning Commission. 2013. Millennium Development Goals: Bangladesh Country Report, 2013. Dhaka. 33

Ministry of Industries. 2010. National Industrial Policy 2010. Dhaka.

13

.

number and employ 41% of the nonagricultural workforce.34 The SMEDP financed 13,645 enterprises having on average 6.4 employees per enterprise, indicating that a vast majority of beneficiaries are cottage and micro enterprises.35 The classification of industries, as per industrial policy, is provided in Appendix 11. 43. Data availability. There is no comprehensive, standardized, and updated database on the SME sector that also includes cottage and micro enterprises. It is challenging to acquire reliable basic statistics, such as the number of SMEs and SME employment. The Sixth Five-Year Plan, 2011–2015 recognized the lack of data as a barrier to understanding the role of SMEs. In the absence of reliable key statistics, alternative inferential methods have been used extensively to assess the SMEDP’s performance parameters. The change in the definition of SMEs, incompatible presentations of data by various agencies, and complex definitions have complicated the understanding of the SME sector and its contribution to the national economy.

44. NBFIs find the refinancing scheme more valuable. The funds disbursed through NBFIs increased to 48% of total facility for the SMEDP compared to 20% for the previous SMESDP. At the national level, banks and NBFIs disbursed SME loans at a rate of 87.8% and 2.2% in 2013.36 This disproportionate performance can be explained by the higher cost of NBFI funds as compared with banks, as the refinancing scheme provided them an opportunity to reduce their weighted average cost of capital. This indicates that NBFIs would be more interested than banks in any innovative interventions in the financial market. 45. Women entrepreneurs. The SMEDP disbursed 6.4% of the total facility to women-led SMEs, falling short of the target of 15.0%. Initial disbursements under this component were slow due to a lack of market awareness among women entrepreneurs. The target was also overly optimistic to comply with the provisions set out in the Refinance Scheme for Women Entrepreneurs of SME, given that the percentage of SME loans disbursed to women entrepreneurs was 3.4%–3.9% during 2010–2013.37 The interest rate cap at 10.0% on loans to women-led SMEs might have also eroded PFI’s motivation for such lending, as PFIs usually lend to general SMEs at a much higher rate.

46. Subloan database. The reimbursement applications made by the PFIs to the implementing agency were not standardized; the PFIs used different spellings in fields and the fields were different as well. This made analyzing the subloans for all 13,465 SMEs ( on the basis of location, industry, etc.) virtually impossible. The database would have been more effective if a standard reporting template with all required fields and their probable values had been prefixed.

C. Recommendations 1. Project–related 47. Future monitoring. The SMEDP provided refinancing facilities to 13,645 SMEs, of which 11,809 (86.5%) are in operation, 300 (2.2%) enterprises are sick, and 1,536 (11.3%) are

34

Bangladesh Bureau of Statistics. 2013. Cottage Industry Survey 2011. Dhaka; Bangladesh Bureau of Statistics. 2013. Survey of Manufacturing Industries 2012. Dhaka.

35 BB, SME and Special Programmes Department.

36 BB. SME and Special Programmes Department.

37 BB. 2014. Women Entrepreneurs’ Conference and Product Display 2014. Dhaka.

14

closed. Although the aggregate overdue of subloans under the SMEDP is only 5.8% compared to the national NPL rate of 11.8% (2014), the number of closed enterprises appears to be high. While political unrest has been cited as the primary reason for the closure of micro and small enterprises, a formal monitoring system should be introduced by the implementing agency for potential future projects to ascertain the specific reasons for this. 48. Covenants. The SMEDP complied with all loan covenants as stipulated in the loan agreement. The FAPAD made four minor audit observations, for which the BB provided answers and is expecting their resolution. This should be followed up with the implementing agency. 49. Recycling request. The tenor of the SMEDP loan was 40 years and there was no provision for the implementing agency to recycle repayment proceeds. This created a buildup of approximately Tk7,000 million at the BB as the typical tenor of subloans was less than five years. The implementing agency has requested the consent of the executing agency to recycle the repayment proceeds. If the proposal is approved it will increase the supply of refinancing facility by approximately $90 million. 50. Additional assistance. Although the SMEDP achievements are significant, the SME credit to total credit ratio is still low at 24.6%. As SMEs constitute more than 90% of all private sector enterprises and 70%–80% of the nonagricultural workforce, there is a pressing requirement for follow-on projects to accelerate the pace of SME development further in Bangladesh to achieve desired economic growth, employment generation, gender empowerment, and poverty reduction. 51. Timing of the project performance evaluation report. ADB could prepare the project performance evaluation report in 2017 as there are no outstanding issues that would necessitate postponement.

52. SME database. It is highly recommended for any future project to assist in developing a comprehensive SME database at the appropriate agency or agencies so that the government and stakeholders can obtain a fair view of the sector, design interventions appropriately, measure performance accurately, and take corrective actions. It is also recommended that this database should be updated and published periodically.

2. General 53. Non-performing loans. The volume of NPLs in Bangladesh’s financial sector has been growing at an alarming rate; it increased from 7.1% in 2010 to 11.6% in 2014 while the number of SME NPLs increased from 3.6% to 11.8% during the same period.38 This is a worrying development as the number of SME NPLs increased by approximately 4 percentage points in 2014 from the previous year. It is recommended that the PFIs selection criteria for any potential future assistance in the financial sector be revisited. 54. Design and Monitoring Framework. The DMF notes an 8.0% increase in SME numbers “over three years” without mentioning a base year or the SME number for this year. Similarly, benchmark numbers of women-led SMEs, the SME credit to total credit ratio, and successful applications by women entrepreneurs have not been mentioned for the base years.

38

BB, SME and Special Programmes Department.

15

.

The implementing agency called for more clarity on targets and baselines. It is recommended that the DMF should mention baseline figures specifically and set targets in line with project objectives.

55. Data sources. The RRP placed the number of SMEs in the country at 1.5 million; however, the report did not mention the year or the source of this data. It also mentions other key indicators without specifically noting any source or calculation methodology, such as “18.26 million people currently employed in the SME sector in nonmetropolitan areas,” “current total of 830,000 nonmetropolitan SMEs,” and “43% of the total SME lending portfolio of the country currently in nonmetropolitan areas” (RRP, p. 23). It is recommended that the RRP for any project should mention the data sources or calculation methodology more precisely, as far as is practical. 56. Targeted intervention. Trading enterprises have fewer difficulties in securing financing from commercial banks, which are less interested in manufacturing enterprises and longer-term credit. For any potential future assistance in the financial sector, an increased focus on the manufacturing sector and the development of industrial clusters and agro-processing industries, with a particular focus on cottage, micro, and small enterprises due to their huge contribution to employment generation and economic growth, is recommended.

57. Project management support. The implementing agency was not able to provide the required environmental monitoring report, and the performance monitoring reports did not contain the important indicators noted in the DMF. The implementing agency suggested that for any future project a dedicated project management unit should be clearly specified in the project agreement. It also suggested that funds should be allocated specifically for project management software and capacity development. A robust project management framework for implementing agencies should be established at the onset of project implementation in order to verify all reporting formats in keeping with the DMF framework, and to install appropriate systems along with a mechanism to monitor compliance with all covenants.

16

A

ppe

nd

ix 1

DESIGN AND MONITORING FRAMEWORK

Design Summary

Performance Targets/Indicators

Data Sources/Reporting

Mechanism Assumptions

and Risks Current Status/Remarks/Achievements

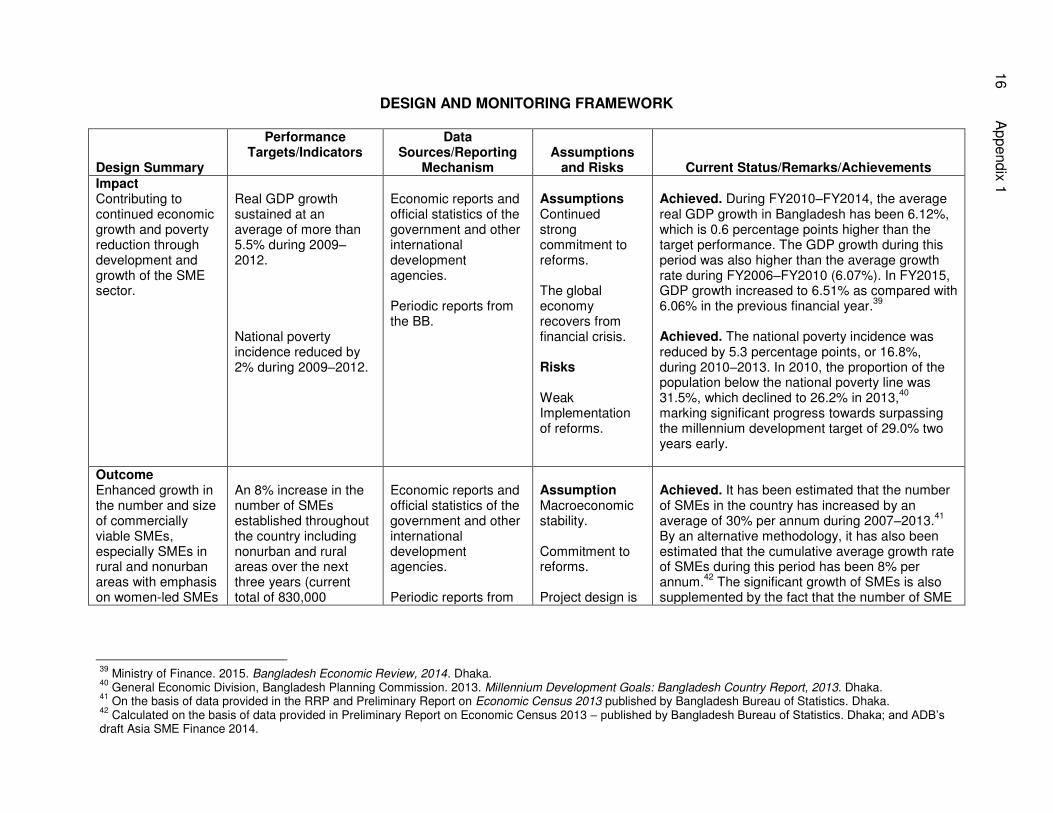

Impact Contributing to continued economic growth and poverty reduction through development and growth of the SME sector.

Real GDP growth sustained at an average of more than 5.5% during 2009–2012. National poverty incidence reduced by 2% during 2009–2012.

Economic reports and official statistics of the government and other international development agencies. Periodic reports from the BB.

Assumptions Continued strong commitment to reforms. The global economy recovers from financial crisis. Risks Weak Implementation of reforms.

Achieved. During FY2010–FY2014, the average real GDP growth in Bangladesh has been 6.12%, which is 0.6 percentage points higher than the target performance. The GDP growth during this period was also higher than the average growth rate during FY2006–FY2010 (6.07%). In FY2015, GDP growth increased to 6.51% as compared with 6.06% in the previous financial year.

39

Achieved. The national poverty incidence was reduced by 5.3 percentage points, or 16.8%, during 2010–2013. In 2010, the proportion of the population below the national poverty line was 31.5%, which declined to 26.2% in 2013,

40

marking significant progress towards surpassing the millennium development target of 29.0% two years early.

Outcome Enhanced growth in the number and size of commercially viable SMEs, especially SMEs in rural and nonurban areas with emphasis on women-led SMEs

An 8% increase in the number of SMEs established throughout the country including nonurban and rural areas over the next three years (current total of 830,000

Economic reports and official statistics of the government and other international development agencies. Periodic reports from

Assumption Macroeconomic stability. Commitment to reforms. Project design is

Achieved. It has been estimated that the number of SMEs in the country has increased by an average of 30% per annum during 2007–2013.

41

By an alternative methodology, it has also been estimated that the cumulative average growth rate of SMEs during this period has been 8% per annum.

42 The significant growth of SMEs is also

supplemented by the fact that the number of SME

39

Ministry of Finance. 2015. Bangladesh Economic Review, 2014. Dhaka. 40

General Economic Division, Bangladesh Planning Commission. 2013. Millennium Development Goals: Bangladesh Country Report, 2013. Dhaka. 41

On the basis of data provided in the RRP and Preliminary Report on Economic Census 2013 published by Bangladesh Bureau of Statistics. Dhaka. 42

Calculated on the basis of data provided in Preliminary Report on Economic Census 2013 – published by Bangladesh Bureau of Statistics. Dhaka; and ADB’s draft Asia SME Finance 2014.

.

Ap

pe

nd

ix 1

17

Design Summary

Performance Targets/Indicators

Data Sources/Reporting

Mechanism Assumptions

and Risks Current Status/Remarks/Achievements

as well as increased employment in the SME sector.

nonmetropolitan SMEs) An 8% increase in SME sector employment over the next three years (18.26 million people currently employed in the SME sector in nonmetropolitan areas) A 10% increase in women-led SMEs at three pilot sites (2009 baseline)

the BB Periodic reports from BWCCI.

able to be implemented. Risk Deteriorating security situation. Political instability.

borrowers has increased by an average rate of 15% every year during 2010–2014.

43 The

methodology has been discussed in detail in the project completion report body. Achieved. The SME sector employs around 70.0%–80.0% of the nonagricultural workforce.

44 A

labor force survey conducted by the Bangladesh Bureau of Statistics estimated the size of the nonagricultural workforce at 28.4 million in 2010.

45

Assuming that 70.0% of the workforce was employed in the SME sector, the SME workforce was estimated at 19.9 million in 2010. Pending the publication of a new survey report, SME employment has been estimated, by the same methodology, at 22.2 million in 2013, yielding a growth rate of 12.5% in three years, which exceeds the envisaged growth rate of 8.0%. The SMEDP has created 8,933 direct jobs over a period of three years with a growth rate of 10.2% as compared with the pre-finance period. Achieved. In specific pilot districts, the number of women-owned SMEs increased by over 10%.

46

During 2010–2014, the number of women-led SMEs increased by 209%, yielding a cumulative average growth rate of 33%. Additionally, the number of women-led SMEs financed by refinancing schemes has increased by 84%, yielding a cumulative average growth of 23% during 2010–2013.

43

BB. SME and Special Programmes Department. 44

ADB. 2015. Asia SME Finance Monitor 2014 (Draft). Manila. 45

Bangladesh Bureau of Statistics. 2011. Report on Labor Force Survey 2010. Dhaka. 46

ADB. 2015. Gender Equality Results Case Study–Bangladesh–Small and Medium-Sized Enterprise Development Project. Manila.

18

A

ppe

nd

ix 1

Design Summary

Performance Targets/Indicators

Data Sources/Reporting

Mechanism Assumptions

and Risks Current Status/Remarks/Achievements

Output 1. Expansion of medium- to long-term credit by PFIs to SMEs located outside the metropolitan areas of Dhaka and Chittagong, with emphasis on women-led SMEs.

The SME credit to total credit ratio of PFIs increased by 5% from 2009 to 2012 (43% of the total SME lending portfolio of the country is currently in nonmetropolitan areas). A minimum of 15% of the credit facility is disbursed to women entrepreneurs in 2009–2012.

PFI compliance reports to the BB. PFI Annual Reports. BB annual reports. Information and data collected.

Assumptions. Effective functioning of SME departments of PFIs. Risks PFI lending to SMEs leads to higher nonperforming loans because of operational risks.

Achieved. The SME credit to total credit ratio of the PFIs increased from 16.9% in 2010 to 21.4% in 2014, yielding a growth rate of 26.5%.

47 At a

national level, the SME credit to total credit ratio of banks and financial institutions increased from 21.1% in 2010 to 24.5% in 2014. The growth rate was 16.1% during this period. Furthermore, the SME loans to GDP ratio also increased from 6.7% in 2010 to 8.6% in 2014, yielding a growth rate of 28.3%. Not Achieved. The SMEDP disbursed 6.4% of its total credit facility to women entrepreneurs, falling short of the target of 15.0%. On a national level, credit facility to women-led enterprises increased from 3.4% in 2010 to 3.9% in 2014. In light of this, the SMEDP has been relatively successful; however, it has not met the stipulated target. One major reason for this is that the target was very high. Prior to disbursement, development of women’s entrepreneurship is required, which is a time-consuming process. Another reason could be the capping of interest rates for subloans for women-led enterprises at 10.0% per annum by the central bank. PFIs generally charge interest rates higher than 15.0% per annum for general SMEs. The associated TA has been successful in developing women entrepreneurship, and the trend of financing women entrepreneurs will likely accelerate in the future. This is demonstrated by the fact that the growth rate of credit facility to women entrepreneurs increased by 9.0% in 2012 and by 49.0% in 2013.

48

47

BB, SME and Special Programmes Department. 48

BB. 2014. Women Entrepreneurs’ Conference and Products Display 2014. Dhaka.

.

Ap

pe

nd

ix 1

19

Design Summary

Performance Targets/Indicators

Data Sources/Reporting

Mechanism Assumptions

and Risks Current Status/Remarks/Achievements

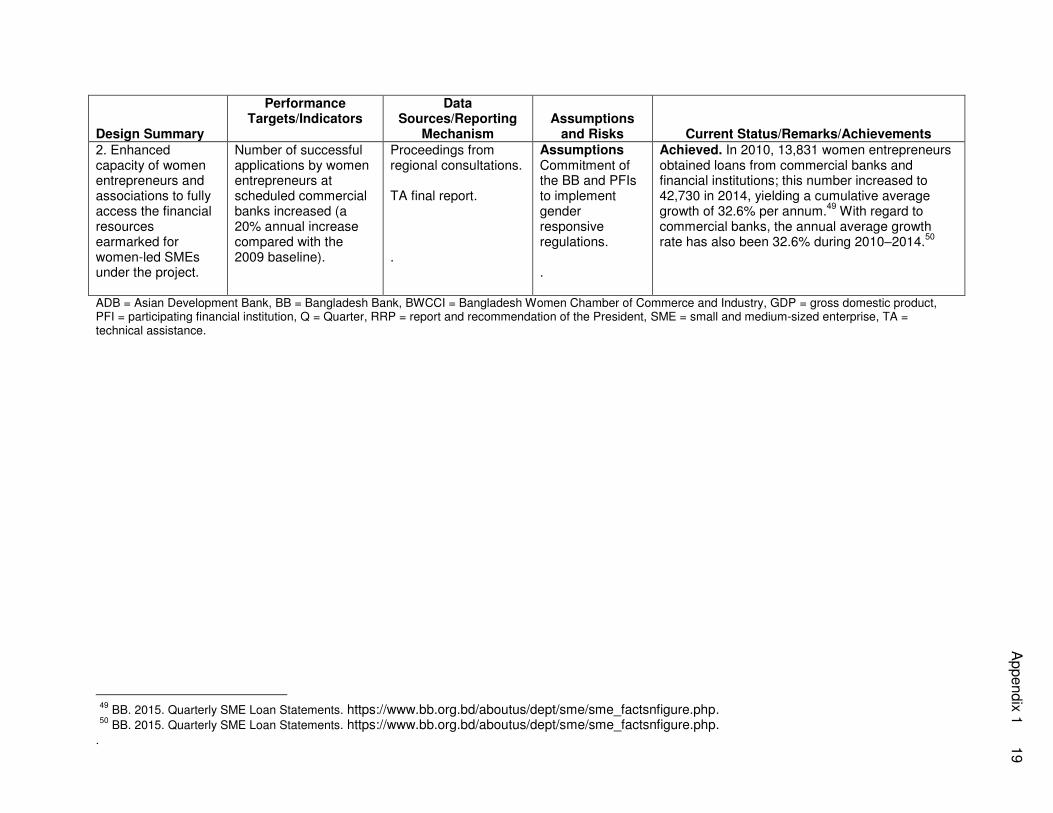

2. Enhanced capacity of women entrepreneurs and associations to fully access the financial resources earmarked for women-led SMEs under the project.

Number of successful applications by women entrepreneurs at scheduled commercial banks increased (a 20% annual increase compared with the 2009 baseline).

Proceedings from regional consultations. TA final report. .

Assumptions Commitment of the BB and PFIs to implement gender responsive regulations. .

Achieved. In 2010, 13,831 women entrepreneurs obtained loans from commercial banks and financial institutions; this number increased to 42,730 in 2014, yielding a cumulative average growth of 32.6% per annum.

49 With regard to

commercial banks, the annual average growth rate has also been 32.6% during 2010–2014.

50

ADB = Asian Development Bank, BB = Bangladesh Bank, BWCCI = Bangladesh Women Chamber of Commerce and Industry, GDP = gross domestic product, PFI = participating financial institution, Q = Quarter, RRP = report and recommendation of the President, SME = small and medium-sized enterprise, TA = technical assistance.

49

BB. 2015. Quarterly SME Loan Statements. https://www.bb.org.bd/aboutus/dept/sme/sme_factsnfigure.php. 50

BB. 2015. Quarterly SME Loan Statements. https://www.bb.org.bd/aboutus/dept/sme/sme_factsnfigure.php.

20 Appendix 2

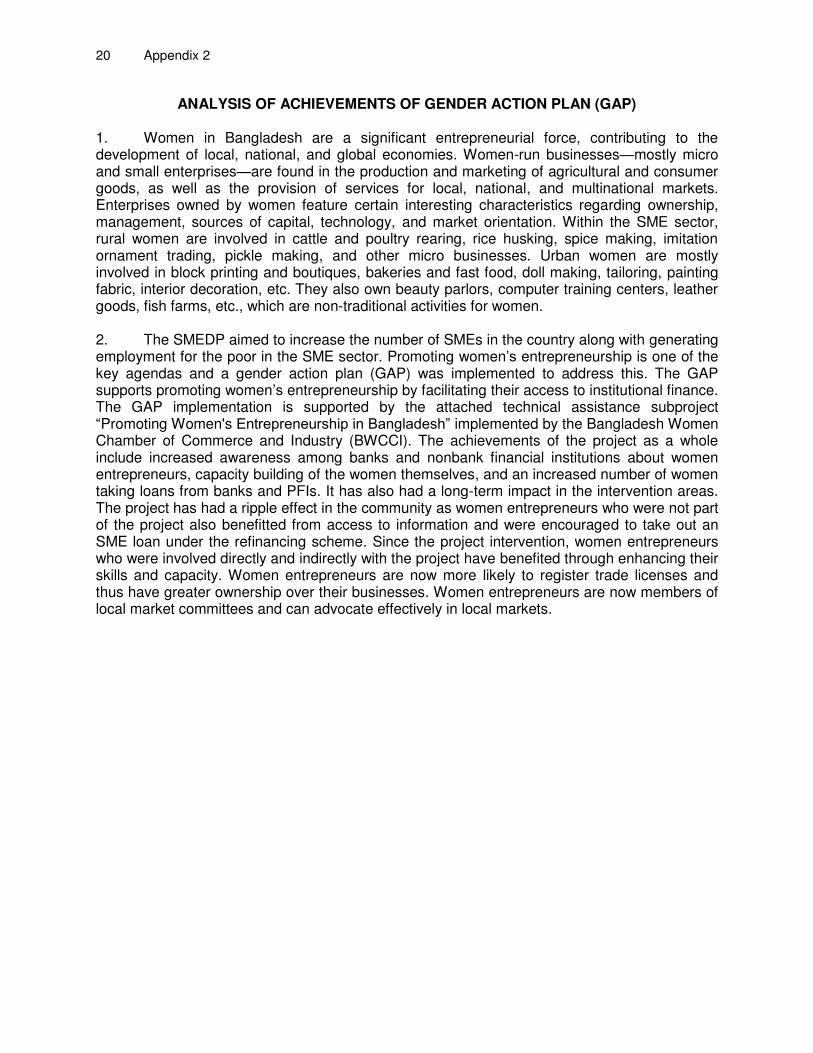

ANALYSIS OF ACHIEVEMENTS OF GENDER ACTION PLAN (GAP)

1. Women in Bangladesh are a significant entrepreneurial force, contributing to the development of local, national, and global economies. Women-run businesses—mostly micro and small enterprises—are found in the production and marketing of agricultural and consumer goods, as well as the provision of services for local, national, and multinational markets. Enterprises owned by women feature certain interesting characteristics regarding ownership, management, sources of capital, technology, and market orientation. Within the SME sector, rural women are involved in cattle and poultry rearing, rice husking, spice making, imitation ornament trading, pickle making, and other micro businesses. Urban women are mostly involved in block printing and boutiques, bakeries and fast food, doll making, tailoring, painting fabric, interior decoration, etc. They also own beauty parlors, computer training centers, leather goods, fish farms, etc., which are non-traditional activities for women. 2. The SMEDP aimed to increase the number of SMEs in the country along with generating employment for the poor in the SME sector. Promoting women’s entrepreneurship is one of the key agendas and a gender action plan (GAP) was implemented to address this. The GAP supports promoting women’s entrepreneurship by facilitating their access to institutional finance. The GAP implementation is supported by the attached technical assistance subproject “Promoting Women's Entrepreneurship in Bangladesh” implemented by the Bangladesh Women Chamber of Commerce and Industry (BWCCI). The achievements of the project as a whole include increased awareness among banks and nonbank financial institutions about women entrepreneurs, capacity building of the women themselves, and an increased number of women taking loans from banks and PFIs. It has also had a long-term impact in the intervention areas. The project has had a ripple effect in the community as women entrepreneurs who were not part of the project also benefitted from access to information and were encouraged to take out an SME loan under the refinancing scheme. Since the project intervention, women entrepreneurs who were involved directly and indirectly with the project have benefited through enhancing their skills and capacity. Women entrepreneurs are now more likely to register trade licenses and thus have greater ownership over their businesses. Women entrepreneurs are now members of local market committees and can advocate effectively in local markets.

.

Ap

pe

nd

ix 2

21

Table A2.1 Gender Action Plan

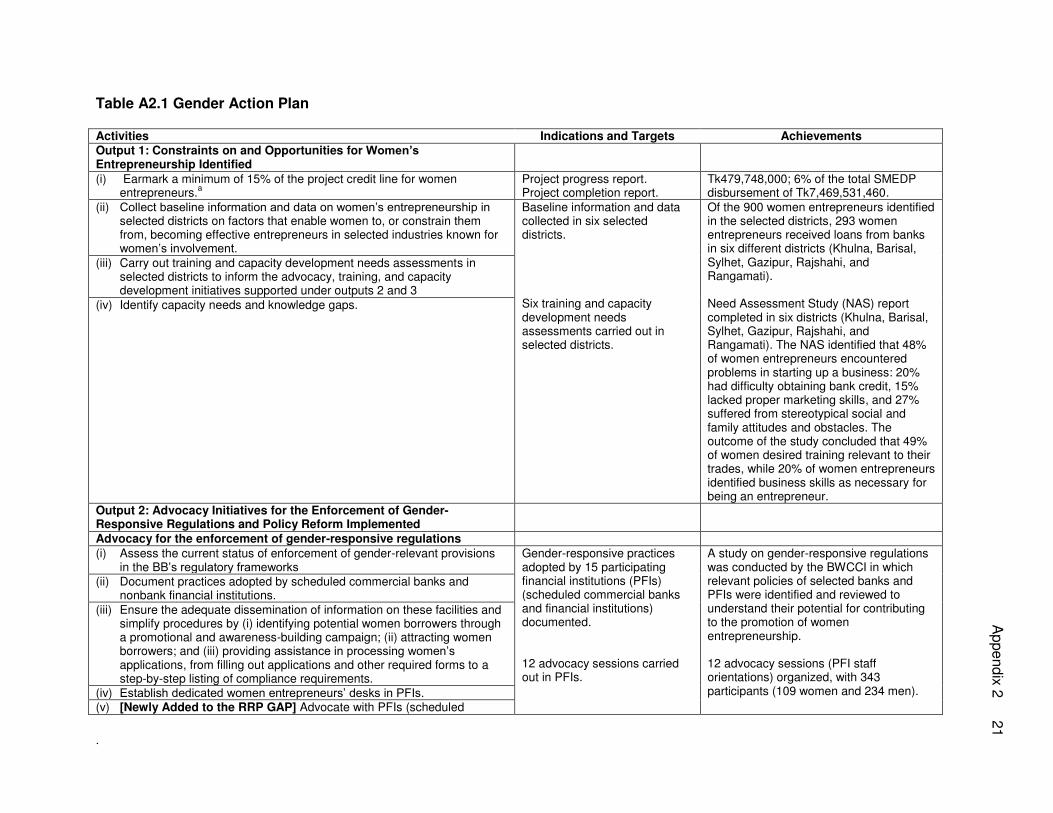

Activities Indications and Targets Achievements Output 1: Constraints on and Opportunities for Women’s Entrepreneurship Identified

(i) Earmark a minimum of 15% of the project credit line for women entrepreneurs.

a

Project progress report. Project completion report.

Tk479,748,000; 6% of the total SMEDP disbursement of Tk7,469,531,460.

(ii) Collect baseline information and data on women’s entrepreneurship in selected districts on factors that enable women to, or constrain them from, becoming effective entrepreneurs in selected industries known for women’s involvement.

Baseline information and data collected in six selected districts. Six training and capacity development needs assessments carried out in selected districts.

Of the 900 women entrepreneurs identified in the selected districts, 293 women entrepreneurs received loans from banks in six different districts (Khulna, Barisal, Sylhet, Gazipur, Rajshahi, and Rangamati). Need Assessment Study (NAS) report completed in six districts (Khulna, Barisal, Sylhet, Gazipur, Rajshahi, and Rangamati). The NAS identified that 48% of women entrepreneurs encountered problems in starting up a business: 20% had difficulty obtaining bank credit, 15% lacked proper marketing skills, and 27% suffered from stereotypical social and family attitudes and obstacles. The outcome of the study concluded that 49% of women desired training relevant to their trades, while 20% of women entrepreneurs identified business skills as necessary for being an entrepreneur.

(iii) Carry out training and capacity development needs assessments in selected districts to inform the advocacy, training, and capacity development initiatives supported under outputs 2 and 3

(iv) Identify capacity needs and knowledge gaps.

Output 2: Advocacy Initiatives for the Enforcement of Gender-Responsive Regulations and Policy Reform Implemented

Advocacy for the enforcement of gender-responsive regulations (i) Assess the current status of enforcement of gender-relevant provisions

in the BB’s regulatory frameworks Gender-responsive practices adopted by 15 participating financial institutions (PFIs) (scheduled commercial banks and financial institutions) documented. 12 advocacy sessions carried out in PFIs.

A study on gender-responsive regulations was conducted by the BWCCI in which relevant policies of selected banks and PFIs were identified and reviewed to understand their potential for contributing to the promotion of women entrepreneurship. 12 advocacy sessions (PFI staff orientations) organized, with 343 participants (109 women and 234 men).

(ii) Document practices adopted by scheduled commercial banks and nonbank financial institutions.

(iii) Ensure the adequate dissemination of information on these facilities and simplify procedures by (i) identifying potential women borrowers through a promotional and awareness-building campaign; (ii) attracting women borrowers; and (iii) providing assistance in processing women’s applications, from filling out applications and other required forms to a step-by-step listing of compliance requirements.

(iv) Establish dedicated women entrepreneurs’ desks in PFIs. (v) [Newly Added to the RRP GAP] Advocate with PFIs (scheduled

22

A

pp

en

dix

2

Activities Indications and Targets Achievements

commercial banks and nonfinancial institutions) to simplify procedures to encourage women applicants.

35 dedicated women entrepreneurs’ desks open at PFIs. 6 training sessions carried out. 600 PFI desk officers trained, including BB desk officials. 36 legal, literacy, and aid initiatives carried out. 360 women entrepreneurs benefited from legal, literacy, and aid initiatives. Effective participation of women entrepreneurs (a 90% participation rate).

45 dedicated women entrepreneurs’ desks were established in six districts. The establishment of the women's desks in the PFIs was key to simplifying the process and procedure of loan applications for women entrepreneurs. The assigned PFI staff at the women's desks facilitated the processing of their loan applications. 12 training orientation sessions were organized for 343 PFI officials. 703 officials from 39 PFIs including the BB were trained to understand the issues and challenges of women entrepreneurs better. 36 legal, literacy, and aid initiatives were carried out. The project carried out advocacy meetings for 1,212 participants of whom 1,120 were women and 92 were men. Effective participation of women entrepreneurs in training and advocacy meetings (a 92% participation rate).

(vi) Ensure that PFIs (scheduled commercial banks and nonbank financial institutions) review their overall credit lending procedures and adopt simplified procedures to encourage women applicants.

(vii) Design, develop, and deliver orientation and training programs targeting PFI officials.

(viii) Women entrepreneurs commit to participate actively in training activities to be conducted under the project prior to and after disbursement.

(ix) Provide legal aid and literacy services to women entrepreneurs and associations.

Advocacy for gender-responsive policy reform (i) Support ongoing efforts to engage relevant government entities and local

government bodies, and advocate for gender-responsive policy, legal, and regulatory reforms to ensure women’s greater representation in the small and medium-sized enterprise (SME) decision-making process and structures.

(ii) Ensure women entrepreneurs’ equal access to financial resources, business opportunities, infrastructure, and services.

Three gender-responsive policy, legal, and regulatory reform initiatives supported.

The study “Gender Responsive Policies: Reform Needs” completed. The following three initiatives were supported: A recommendation for a 30% provision for women in industrial parks and economic zones submitted to the Prime Minister (industrial policy). Regarding advocacy, the National Board of Revenue issued a letter assigning a focal point for women entrepreneurs at district NBR offices (tax policy). The BWCCI advocated for a 30% quota for women entrepreneurs in international

.

Ap

pe

nd

ix 2

23

Activities Indications and Targets Achievements

trade fairs, exhibitions, and other market promotion activities (export policy). Furthermore, the BWCCI proposed a credit guarantee scheme for women entrepreneurs to the Ministry of Finance. Capacity building initiatives for women entrepreneurs have been supported by the Ministry of Finance.

Output 3: Technical capacity of Selected Women Entrepreneurs and Associations Strengthened

(i) Training programs designed, pilot-tested, and conducted on women’s entrepreneurship development under private partnership between the BWCCI and Ministry of Industry.

(ii) Gender issues integrated in the content of all training modules developed

and used in loan-supporting training programs (iii) Exposure visits and lateral learning organized. (iv) Support provided to operationalize SME helplines in selected areas.

900 women entrepreneurs trained. Five exposure visits, five trade fairs, and five lateral learning events carried out. Five SME helplines supported in selected districts.