356S

256

INTERNATIONAL TRADE CHALLENGES AND OPPORTUNITIES FOR PAKISTAN COTTON-TEXTILE AND APPAREL SECTOR By Raana Ahsan PhD. Thesis NATIONAL UNIVERSITY OF MODERN LANGUAGES ISLAMABAD June 2008

-

Upload

mian-usman -

Category

Documents

-

view

73 -

download

2

Transcript of 356S

INTERNATIONAL TRADE CHALLENGES AND OPPORTUNITIES FOR

PAKISTAN COTTON-TEXTILE AND APPAREL SECTOR

By Raana Ahsan

PhD. Thesis

NATIONAL UNIVERSITY OF MODERN LANGUAGES ISLAMABAD

June 2008

International Trade: Challenges and Opportunities for Pakistan Cotton - Textile and Apparel Sector

By

Raana Ahsan Msc Quaid-e-Azam University

A THESIS SUBMITTED TO THE

NATIONAL UNIVERSITY OF MODERN LANGUAGES ISLAMABAD

DOCTOR OF PHILOSOPHY

In Management Sciences

To

FACULTY OF ADVANCED INTEGRATED STUDIES AND RESEARCH

(MS/HRD)

NATIONAL UNIVERSITY OF MODERN LANGUAGES ISLAMABAD

JUNE 2008

© Raana Ahsan, 2008

ii

DISSERTATION AND DEFENSE APPROVAL FORM The undersigned certify that they have read the following dissertation,

examined the defense, are satisfied with the overall exam performance, and recommend the thesis to the Faculty of Advanced Integrated Studies & Research for acceptance:

Dissertation Title: International Trade: Challenges and Opportunities for Pakistan Cotton -

Textile and Apparel Sector ___

Submitted By: Raana Ahsan Registration #:130-PhD/HRD/2003

Doctor of Philosophy Management Sciences

Dr. Zafar Altaf Name of Research Supervisor Signature of Research Supervisor Prof. Dr. Shazra Munnawar Name of Dean (FAIS&R) Signature of Dean (FAIS&R) Prof. Dr. Aziz Ahmad Khan Name of Rector Signature of Rector

____June 2008 ___

Date

NATIONAL UNIVERSITY OF MODERN LANGUAGES FACULTY OF ADVANCED INTEGRATED STUDIES & RESEARCH

iii

CANDIDATE DECLARATION FORM I RAANA AHSAN

D/o: MR. ZIA MALIK

Registration No: 130-PhD/HRD/2003 Discipline: Management Sciences

Candidate of Doctor of Philosophy at the National University of

Modern Languages do hereby declare that the dissertation: International Trade: Challenges

and Opportunities for Pakistan Cotton -Textile and Apparel Sector

submitted by me in partial fulfillment of PhD degree in discipline/department Faculty of

Advanced Integrated Studies & Research is my original work, and has not been submitted or

published earlier. I also solemnly declare that it shall not, in future, be submitted by me for

obtaining any other degree from this or any other university or institution.

I also understand that if evidence of plagiarism is found in my dissertation at any stage, even

after the award of a degree, the work may be cancelled and the degree revoked.

June 2008 Signature

Date

Raana Ahsan Name

iv

ABSTRACT The purpose of this research was to provide a comprehensive analysis of international trade

in order to evaluate and determine the challenges it poses, and opportunities, it offers to Pakistan’s Cotton, Textile and Apparel Sector. The research is based on secondary data sources. World Bank, WTO, UNCTAD, and a lot of other valuable and authentic reports from the authors of repute have been consulted to understand the increasingly complex international trade relations in a globalizing world. Volumes of government reports, position papers, handouts and books have been searched to appreciate the dynamics of Pakistan Cotton, Textile and Apparel Sector.

The research thesis endeavors to capture where the challenge is. What is at stake? Who are

the players? What are the opportunities in the international market place? How these challenges can be translated in to opportunities? Brief account of recent trade development and the relationship between global and domestic trading arrangements have been discussed. Role of politics in shaping decisions and managing power both at domestic and global level, significance of international commitments, and influence of historical, cultural back grounds, shared ideas and beliefs, and individual mind set in competing interests in the domestic economy have also been dilated upon.

Analytical findings reveal that Pakistan has comparative edge on the basis of comparative

advantage, reveal comparative advantage, relative trade advantage, and trade complementarities. The estimated value of revealed comparative advantage of cotton in Pakistan is 18 which is very high than unity which implies that Pakistan has great opportunities in the export of cotton and cotton manufacturing. Moreover, the estimated values of balasa and Lafay index for all cotton and cotton products are very high which reveal that Pakistan has trade competitiveness in the cotton and cotton manufacturing. The estimated value of relative trade index for primary products, cotton seed, cake of cotton seed and cotton linter, are positive which imply that these products are highly competitive, while oil of cotton seed and cake of cotton seed are uncompetitive. Furthermore, the value of trade complementarities variable for USA, EU, Japan and Canada (trading countries) are greater than unity except SAARC countries. This means that trading with SAARC countries in cotton and cotton products is less profitable as compared to other countries where cotton trading is highly profitable. Still domestic resource cost analysis (DRC) proves that Pakistan has greater opportunities in cotton production. The values of reveal comparative advantage and relative trade advantage further suggest that Pakistan has greater opportunities and prospects for exporting cotton and cotton manufacturing. Similarly trade complementarities show and suggest that Pakistan should focus on Middle East market with highest trade complementarities, followed by Canada, USA, EU, SAARC countries and then Japan. Bt transgenic cotton is widely grown in the cotton growing areas of Sindh and Punjab.

Bt cotton can play a significant role to enhance agricultural productivity as the productivity

of cotton in Pakistan is 0.5 ton/ha as compared productivity of Bt cotton in China is 9 ton/ha which implies a huge cotton productivity gap. This gap can be narrowed down by the adoption of Bt cotton in Pakistan which will have major impact on food security efforts in the country. Urgent efforts are required to focus on cost efficiency, higher productivity with quality of cotton, export diversification of cotton products, export oriented policy and market perspective to become more competitive in the global cotton market. There is also a need to strengthen the cotton - textile value chain with back ward and forward linkages. Unique products have to be developed, and a shift from comparative advantage to competitive advantage is the way forward.

v

TABLE OF CONTENTS

Chapter Page

DISSERTATION AND DEFENSE APPROVAL FORM ii

CANDIDATE DECLARATION FORM iii

ABSTRACT ……………………………………………………….. iv

TABLE OF CONTENTS ………………………………………….. v-ix

LIST OF TABLES …………………………………………………. x

LIST OF FIGURES ………………………………………………… xi

LIST OF CHARTS …………………………………………………. xii

LIST OF APPENDICES …………………………………………… xiii

LIST OF ABBREVIATIONS ……………………………………… xiv-xvii

DEDECATION ……………………………………………………… xviii

ACKNOWLEDGEMENT …………………………………………... xix

POLITICAL ECONOMY …………………………………………... xx

RESEARCH HYPOTHESIS ………………………………………... xxi

1. INTRODUCTION

1.1. Background of Study …………………………………………… 1

1.2. Economy of Pakistan …………………………………………… 2

1.2.1. Historical Perspective …………………………………….. 2

1.2.2. Recent Economic History …………………………………. 3

1.2.3. The Economy Today ………………………………………. 4

1.3. International Trade ………………………………………………. 20

1.4. Aid, Debt, Trade ………………………………………………. 22

1.4.1. Aid …………………………………………………………. 22

1.4.2. Debit …………………………………………………………. 23

1.5 Trade Not Aid ………………………………………….................... 24

1.6 Rationale of the Study ………………………………………….... 26

1.7. Limitations ………………………………………………….......... 26

vi

2. LITERATURE REVIEW

2.1 Origin of Trade …………………………………………………… 30

2.2 Evolution of Trade and Trade Theories ……………………..…… 30

2.3 Trade and Development ………………………………………….. 37

2.3.1 Why Trade ..………………………………………………… 37

2.3.2. The Benefits of Trade ………………………………………. 38

2.4 Globalization: A World without Borders…………………………. 41

2.4.1 WTO and the Agreement on Textiles and Clothing ………... 43

2.5 Regional Trading Arrangement …………………………………... 44

2.6 The Trade Policy Instruments ………………………………….. 46

2.7 Some other Important Concepts. ……………………………… 47

3. RESEARCH METHODOLOGY

3.1 Introduction ……………………………………………………… 60

3.2 Methodology and Research Design ……………………………… 61

3.2.1 Revealed Comparative Advantage ………………………… 61

3.2.2 Relative Comparative Advantage ………………………… 62

3.2.3 Opportunities for Supply Chain Integration……………… 63

3.2.4 Trade Complementarities …………..…………………… 63

3.3 Research Objectives…………… ……………………………… 64

3.4 Statement of Hypothesis………… ……………………………… 64

4. INTERNATIONAL POLITICAL ECONOMY

4.1 International Political Economy ………………………………... 67

4.2 Role of National Governments in International Political Economy…. 68

4.3 Political Economy of International Trade ………………………. 68

4.3.1 Trade Policy before World War I, 1860-1914 ……………. 68

4.3.2 International Trade from 1918 to 1939 …………………… 71

4.4 International Financial System ………………………………….. 76

4.4.1 International Monetary Fund (IMF)………………………… 77

4.4.2 Pakistan and IMF………………….………………………… 80

vii

4.4.3 The World Bank (WB)……………………………………… 80

4.5 World Trade Organization (WTO)………………………………. 82

4.5.1 Principles of Trading System ……………………………… 82

4.5.2 WTO Agreements ………………………………………… 84

4.5.3 Chronology of Key Events ………………………………... 85

4.5.4 Institutional Structure ……………………………………... 89

4.6 New Economic World Order ……………………………………. 91

4.6.1. Foreign Direct Investment (FDI)…………………………… 92

4.6.2 Multinational Corporations (MNCs)……………………… 94

4.7 Globalization …………………………………………………….. 96

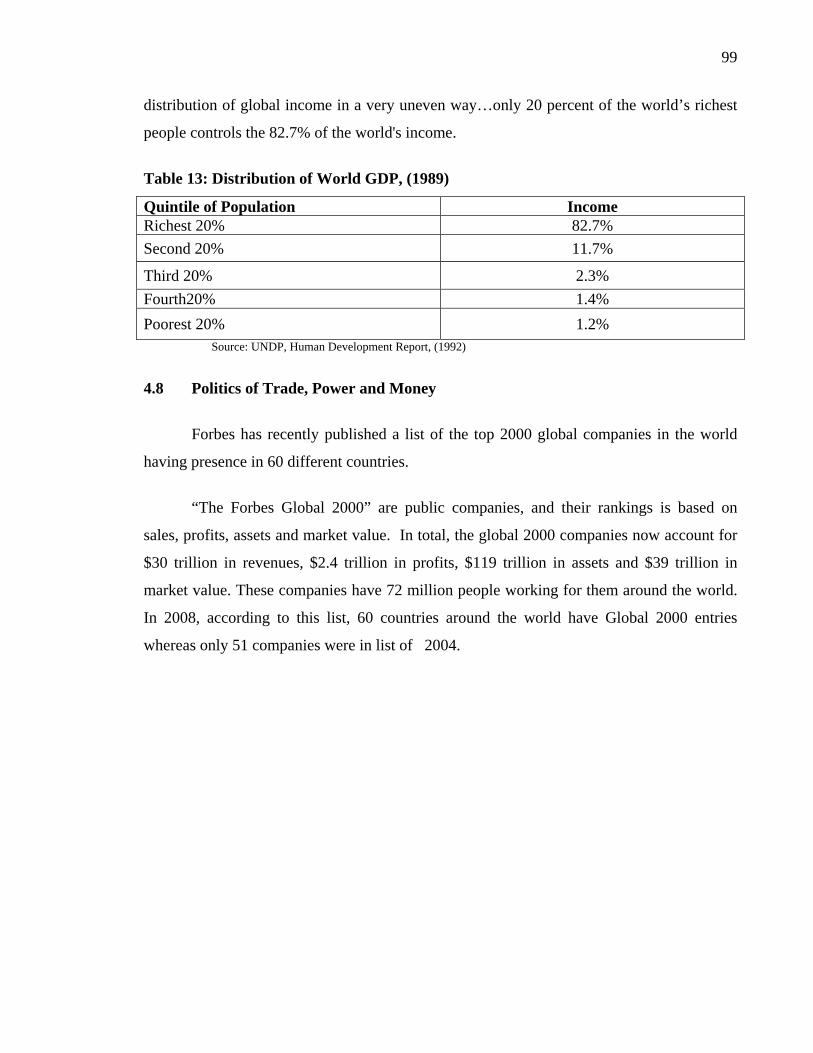

4.8 Politics of Trade, Power and Money …………………………….. 99

4.8.1. Richest People in World …………………………………… 101

4.9 Political Economy of information ……………………………… 101

5. PAKISTAN COTTON-TEXTILE AND APPAREL SECTOR

5.1. International Trade of Cotton-Textile and Apparels ……………. 107

5.1.1. Trends in Clothing and Textile International Trade ………. 108

5.2. Pakistan Trade of Textile and Clothing …………………………. 110

5.3. Global Cotton Market …………………………………………… 111

5.4. Analyzing Opportunities for Pakistan Cotton-Textile and

Apparel Sector ………………………………………………..… 113

5.4.1 Revealed Comparative Advantage……………………….. 113

5.4.2 Itemized Trade Performance of Cotton and Cotton

Manufacturing ………………………………………….. 114

5.4.3 Relative Comparative Advantage………………………... 114

5.4.4 Trade Complementarities……………………………….. 115

5.5 Pakistan Cotton-Textile and Apparel Sector- The Value Chain…. 116

5.5.1 Pakistan Cotton Situation ………………………………….. 116

5.5.2 Ginning Sector …………………………………………….. 119

5.5.3 Spinning Sector ……………………………………………. 120

5.5.4 The Textile Sector …………………………………………. 122

viii

5.5.5 Issues in Yarn Production …………………………………. 123

5.5.6 Production of Cloth and Fabric ……………………………. 123

5.5.7 Textile Made-ups ………………………………………….. 125

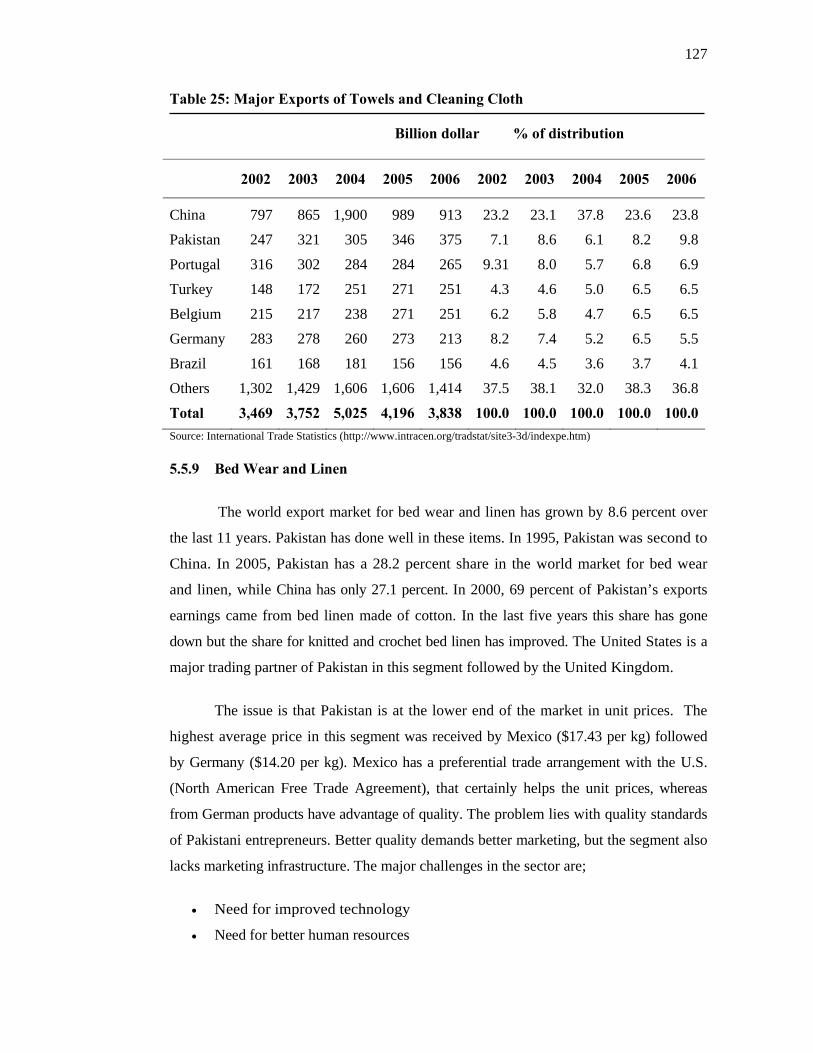

5.5.8 Towels and Cleaning Cloths ………………………………. 126

5.5.9 Bed Wear and Linen ………………………………………. 127

5.5.10 Apparels ………………………………………………….. 129

5.6 Cotton Vision 2015 ……………………………………………… 131

5.6.1 Textile Vision 2005 ………………………………………… 131

5.7 Significance of Agriculture Sector for Pakistan …………………. 133

5.8 Opinion around the World ………………………………………. 134

5.9 Challenges in the Pakistan Cotton Yarn, Textile & Apparel Sectors 137

5.10 Concessions ……………………………………………………. 139

5.11 Politics of Concessions and Rebates ……………………………. 140

5.12 Opportunities and Future ……………………………………….. 141

6. TRADE AND INDUSTRIAL REGIME OF PAKISTAN

6.1. Institutional Framework for Trade ……………………………….. 146

6.1.2. Trade Regime ………………………………………………. 148

6.1.3 Trade Policy of Pakistan …………………………………… 150

6.1.4 Trade Policy Reforms ……………………………………… 150

6.1.5 Trade Policy 2006-07 ……………………………………… 152

6.1.6 Trade Policy 2007-08: Speech by the Commerce Minister ... 153

6.2 International Trading System and Pakistan ……………………… 156

6.3 WTO and Pakistan ……………………………………………….. 158

6.3.1 Trade Policy Review ……………………………………….. 158

6.3.2 WTO Notifications …………………………………………. 162

6.4 Industrial Sector of Pakistan ……………………………………… 162

6.4.1 Ancillary Textile Industry …………………………………. 163

6.5 Small and Medium Enterprises ………………………………..….. 165

6.6 Investment Policy ………………………………………………… 166

6.7 Industrial Policy ………………………………………………….. 166

ix

6.8 Textile Policy …………………………………………………….. 168

6.9 Private Sector Stake holders ……………………………………... 168

6.10 International Trade and Developing Countries ………………… 169

6.11 Economic Structure and Economy of Income ………………….. 170

6.12 Aim of Trade …………………………………………………… 171

6.13 Trade has worked for Pakistan …………………………………. 171

7. DEVELOPMENT OF BT COTTON IN PAKISTAN

7.1 Introduction ……………………..………………………………… 174

7.2 Background of Bt Cotton in the World……….. ………………… 175

7.3 Is there a Need to Grow Bt Cotton in Pakistan?………………….. 176

7.4 Development of Bt Cotton in Pakistan…………………………….. 177

7.5 Global Adoption of Bt Cotton …………………………………... 178

7.6 Adoption of Bt Cotton in Pakistan……………. ………………… 180

7.7 Impact of Bt Cotton in the World…………… ………………….. 180

7.8 Performance of Bt Cotton in Pakistan…………………………… 184

7.9 Conclusions and Suggestions… …………………………………. 187

8. CONCLUSIONS AND RECOMMENDATIONS…………………... 192

8.1. Recommendations ………………………………………………….. 194

8.1. Future Research ………………………………………………….. 196

BIBLIOGRAPHY ……………………………………………… 198

x

LIST OF TABLES Table Page 1. Sectoral Share in Gross Domestic Product (GDP)---------------------------------- 5 2. Sectoral Contribution to the GDG growth (% Points)------------------------------ 6 3. Composition of GDP growth (Point Contribution) --------------------------------- 6 4. Structure of Exports 2007-08 --------------------------------------------------------- 8 5. Export of Textile Manufactures ------------------------------------------------------ 9 6. Major Export Markets ------------------------------------------------------------------ 10 7. Structure of Imports -------------------------------------------------------------------- 11 8. Pakistan’s Major Imports -------------------------------------------------------------- 12 9. Unit Value Indices and Term of Trade (Base year 1990-91=100)---------------- 13 10. External Debt and Foreign Exchange Liabilities ($ Billion) ---------------------- 15 11. Applied tariff rates of major traders in 1925 ---------------------------------------- 73 12. GATT and WTO Trade Rounds------------------------------------------------------- 87 13. Distribution of World GDP, 1989 ---------------------------------------------------- 99 14. Top Companies sorted by Market Value--------------------------------------------- 100 15. Imports of Textile and Clothing in to Major Markets by Origin (2006) --------- 109 16. Pakistan Export of Textile Products -------------------------------------------------- 111 17. Itemized Trade Performance of Cotton & Cotton Manufacturing (2006)-------- 114 18. Competitive advantage of Cotton Products Based on the RTA Index-------------115 19. Trade Complementarities -------------------------------------------------------------- 115 20. Number of Ginning Factories and Machines ---------------------------------------- 119 21. Industry Losses due to Cotton Contamination, 2004-05 --------------------------- 120 22. Installed and Working capacity in the Spinning Sector , All Pakistan Installed Capacity (000) Working Capacity (000) Capacity Utilization (%)---- 121 23. Quality of Cloth Production, Mill Sector (% distribution)------------------------- 124 24. Exports of Textile Made-ups ---------------------------------------------------------- 126 25. Major Exports of Towels and Cleaning Cloth--------------------------------------- 127 26. Composition of Pakistan’s Exports of Bed Wear ----------------------------------- 128 27. Major Country Destination of Exports of Bed Wear from Pakistan-------------- 128 28. Export of Clothing ---------------------------------------------------------------------- 130 29. Loans to Textile Sector----------------------------------------------------------------- 141 30. Main Ministries and Agencies Responsible for Trade-Related Issues ----------- 147 31. Pakistan’s Tariff Structure: 2001-02 and 2004-08---------------------------------- 160 32. Preferential Rules of Origin and Tariffs in Trade Agreements, 2007 ------------ 161 33. WTO Notifications, 2001 to end-September 2007---------------------------------- 162 34. Profile of Textile Industry ------------------------------------------------------------- 164 35. Investment Policy Matrix -------------------------------------------------------------- 167 36. The Economic structures of Low-Middle-and High-Income Countries --------- 170

xi

LIST OF FIGURES Figure Page 1. Contribution to GDP growth --------------------------------------------------------- 7 2. Major contributors to additional export economy -------------------------------- 8 3. Sources of Imports-------------------------------------------------------------------- 12 4. Current Account deficit (Month Wise)--------------------------------------------- 14 5. External Debt and Liabilities -------------------------------------------------------- 15 6. Inflation Rate by Group-------------------------------------------------------------- 17 7 & 8. Revenue and Expenditure: budget estimate 2006-07----------------------------- 18 9. Foreign Direct Investment Inflows ($ billion) ------------------------------------ 19 10. Top Investing countries -------------------------------------------------------------- 19 11. Investment Inflows by Sector ------------------------------------------------------- 20 12. Real Merchandise Trade Growth by Region 2006 ------------------------------- 21 13. Growth in the Volume of World Merchandise Trade and GDP 1996- 2006-- 21 14. Export of Textile Manufactures 2005-06 ----------------------------------------- 110 15. Share of Cotton Production---------------------------------------------------------- 112 16. Nominal Cotton Price: Cotlook A and B Indices and U.S Price---------------- 113 17. Capacity Utilization in spinning Sector -------------------------------------------- 121 18. Pakistan Major Exports 2005-06---------------------------------------------------- 149 19. Trade as Percentage of GDP -------------------------------------------------------- 149 20. Tariff Averages ----------------------------------------------------------------------- 161

xii

LIST OF CHARTS

Chart Page 1. World Merchandise Export, 1900-1950 ------------------------------------------- 74 2. World Merchandise Export Prices, 1900-1950 ----------------------------------- 75 3. Volume Growth of World Merchandise Export, 1900-1950 ------------------- 75

xiii

LIST OF APPENDICES

Appendices Page

A. Installed Capacity in the Textile Sector (For month of Dec 2007) ----------- xxii B. Dewan Salman Fiber Ltd----------------------------------------------------------- xxxv C. Nishat (Chunian) Limited---------------------------------------------------------- xxxvi D. Ibrahim Fibers (IBFL)-------------------------------------------------------------- xxxvii E. The Crescent Textile Mills Limited ---------------------------------------------- xxxviii

xiv

ABBREVIATIONS ADB : Asian Development Bank

AMIC : Agri - Marketing Integrated Centers

AOA : Agreement on Agriculture

APEC : Asia Pacific Economic Cooperation Group

APTMA : All Pakistan Textile Mills Associations

ASEAN : Association of South East Asian Nations

Association

ATC : Agreement on Textiles and Clothing

BMR : Balancing Modernization Replacement Program

CAFTA : Central American Free Trade Area

CARs : Central Asian Republics

CEC : Cotton Export Corporation, Government of Pakistan

CETP : Combined Efferent Treatment Plants

CIF : Cost Insurance and Freight

CKD : Complete Knock Down

CPI : Consumer Price Index

CPI : Consumer Price Index

DDA : Doha Development Agenda

DSU : Dispute Settlement

DTTs : Double Taxations Treaties

ECC : Economic Coordination Committee

ECO : Economic Co-operation Organization

EDL : External Debt Liabilities

EOU : Export Oriented Units

ESCAP : Economic and Social Commission for Asia and Pacific

Region

EU : European Union

FBR : Federal Board of Revenue

FDI : Foreign Direct Investment

xv

FI : Foreign Investment

FPCCI : Federation of Pakistan Chamber of Commerce and Industry

FTA : Free Trade Area/Free Trade Agreement

GATS : General Agreement on/Trade in Services

GATT : General Agreement on Tariffs and Trade

GCC : Gulf Cooperation Council

GDP : Gross Domestic Product

GNP : Gross National Product

GOP : Government of Pakistan

GSP : Generalized System of Preference

GWP : Gross World Product

IDA : International Development Association

IDBR : International Bank for Reconstruction and Development

IIAs : International Investment Agreements

ILO : International Labor Organization

IMF : International Monetary Fund

ITA : Information Technology Agreement

ITO : International Trade Organization

LCV : Light Carrier Vehicle

LDCs : Least Developed Countries

LTF-EOP : Long Term Financing of Expert Oriented Projects

M&As : Mergers and Acquisitions

MFA : Multi-Fiber Arrangement

MFN : Most Favored Nation

MMF : Man-made Fiber

MNC : Multinational Corporation

MOU : Memorandum of Understanding

MTN : Multilateral Trade Negotiations

NAFTA : North America Free Trade Agreement

NTC : National Tariff Commission

NTTFC : National Trade & Transport Facilitation Committee

xvi

NWFP : North West Frontier Province

OIC : Organization of Islamic Countries

PCFAMEA : Pakistan Cotton Fashion Apparel Manufactures and

Exporters

PHDEB : Pakistan Horticulture Development & Expert Board

PTA : Preferential Trade Agreement

QIZs : Qualified Industrial Zone

R & D : Research and Development

ROZs : Reconstruction Opportunity Zones

RTA : Registered Trade Agreements

SAARC : South Asia Association of Regional Co-operation

SAPTA : South Asian Preferential Tariff Arrangement

SME : Small & Medium Enterprise

SMEDA : Small & Medium Enterprise Development Authority

SPI : Sensitive Price Index

SPS : Sanitary and Phyto-sanity Measures

SRO : Statutory Regulatory Order

TBT : Agreement on Technical Barriers to Trade

TDAA : Trade Development Authority Pakistan

TDPA : Trade Development Pakistan Authority

TMB : Textile Monitoring Body

TNC : Trade Negotiating Committee

TNCs : Transnational Corporations

TPRB : Trade Policy Review Body

TPRM : Trade Policy Review Mechanism

TQMD : Textile Quota Management Directorate

TRB : Trade Review Body (WTO)

TRIPs : Agreements on Trade Related Aspects of Intellectual

Property Rights

TSB : Textile Surveillance Body

TTFP : Trade & Transparent Facilitation Project

xvii

UK : United Kingdom

UN : United Nations

UNCTAD : United National Conference on Trade and Development

UNICEF : United National Children’s Fund

USA : United States of America

USDA : United States Agricultural Department

WEF : World Economic Forum

WPI : Whole Sale Price Index

WTO : World Trade Organization

xviii

DEDICATION

To

DR. ZAFAR ALTAF

My Research Supervisor

His one sentence,

“Raania, prove it to yourself”

changed my mindset.

xix

ACKNOWLEDGEMENT

“All glory goes to Allah”

Thank you Ammi Jan, what ever I am today, I owe it to you. You taught me how to

face the challenges with smile and keep on struggling. Years ago you left us but your love

and care still warm my heart. I love you Ma!

Thank you Daddy for making me a better human being with faith, values and

principles!

I deeply appreciate my siblings for their affection, encouragement and practical help

in my efforts to produce something worth while.

My friends …. “Every time when I was down, they always come around and put my

feet back on the ground.” Thank you friends!

I am indebted to my colleagues and co – workers for their cooperation and support.

They made things easier for me.

Very humbly, I present tributes to all those economists and scholars whose vision

and knowledge; I deeply benefited from in my research endeavors.

Writing this thesis was a test of my commitment, patience and professionalism, and I

am extremely obliged to all those who directly and indirectly helped me in achieving the

target.

xx

POLITICAL ECONOMY

Of course, as in the instances of alchemy, astrology, witch- craft, and

other such popular creeds, political economy has a plausible idea at the root

of it. “The social affection,” says the economist, “are accidental and

disturbing elements in human nature; but avarice and the desire of progress

are constant elements. Let us eliminate the constants, and, considering the

human being merely as a covetous machine, examine by what laws of labor,

purchase, and sale, the greatest accumulative result in wealth is obtainable.

Those laws once determined, it will be for each individual afterwards to

introduce as much of the disturbing affectionate element as he chooses, and

to determine for himself the result on the new conditions supposed.”

JOHN RUSKIN

The Genius of John Ruskin

Editor: J. D. Reseuberg

Houston, Mifflin Company Boston, 1963

xxi

RESEARCH HYPOTHESIS

Pakistan is facing a new structure in international trade and the country should be;

• Able to work its strengths

• Develop itself from a low income country to a middle level country through its trade

in Textiles

1

CHAPTER 1

INTRODUCTION

1.1 Background of the Study The Indus Valley civilization, one of the oldest in the world and dating back at least

5,000 years, spread over much of what is presently called Pakistan (The World Fact Book,

2007). In the 21st century, Pakistan is a rapidly developing nation, strategically located, has

plenty of natural resources, and with a growing market of 160 million people.

Pakistan has a very narrow export base. The Cotton-Textile and Apparel Sector

accounts for more than 60 percent of Pakistan’s export earnings. According to Altaf (2007),

what happens to the economy of Pakistan is very much dependent on the cotton- yarn-

textile-apparel complex.

After the elimination of MFA and related quota regime, the international market

place has become aggressively competitive with challenges at one hand and on the other lots

of opportunities for smart players. The international trade of cotton-textile and apparel poses

huge challenges to this important sector of Pakistan’s economy.

This thesis aspires to establish that a vibrant and profound trade regime can give a

boast to the economy of Pakistan. The cotton-textile –apparel sector as the central pillar of

the trade regime can contribute significantly towards welfare and prosperity of the country.

It argues that macroeconomic (over all policy) and microeconomic (firm level) frameworks

have complementarities that reinforce each other for desired economic outcomes. It further

suggests that business friendly not businessmen friendly domestic trade policies can create a

business and entrepreneur’s culture that can address the supply side constrain, and can act as

a trouble shooter. It also deliberates the role of state and institutions in the international and

domestic economies, and how international political dynamics and commitments affect this

role and policies. It has also been argued that economic activities are determined by

historical norms, culture, and the political systems. Advancement of technology,

2

information, knowledge and other dimensions of globalization have deeply affected the way

of doing business.

This thesis, while giving the recount of the challenges for cotton-textile and apparel

sector of Pakistan in international trade arena, dilates upon the silver lining therein, and

suggests the way forward for positioning itself with in the global markets. “The canvass is

big and the brush should be big enough to match the canvass”.

1.2 Economy of Pakistan 1.2.1 Historical Perspective

Pakistan was a poor, resource less and predominantly agricultural economy at its

creation in 1947 (Wikipedia, 2007), after division of the sub-continent. The creation of

Pakistan, in economic terms was the break –up of a customs union that had lasted for nearly

three hundreds years, (Altaf 1983). Agriculturally, the area was the granary for the

undivided India and provided cotton and jute for the industrialized part of the sub-continent,

(Altaf, 1983). While calling Pakistan an “economic monstrosity”, he further mentions that

Pakistan inherited industrial assets worth only Rs. 580 million.

During 1950-60, this policy paid dividends but at the cost of the agriculture sector

and growth was sluggish. Attempts were made to correct the situation by an increased

inflow of aid. Further, the support price for agricultural products was increased, though still

below market prices.

The decade of 1970s witnessed the withdrawal of these economic incentives either

partially or completely. The private sector started taking capital out of the country to invest

in other third world countries, and the foreign loan commitments in the public sector swelled

up. The small entrepreneurs were burdened with the liability of repayments of these extra

loans, Altaf maintains. However, growth rates indicate, “Development was emphasized”

during this period.

Nationalization of private enterprises during late 1970s was a blow to private sector

participation in economic activities. However, in early 1980s, government began a policy of

3

greater reliance on private enterprise to achieve economic goals. This policy continued

throughout the late 1980s and early 1990s. The GDP growth rate was 6.5 percent in

the1980s, and the trade gap was $ 2.5 billion.

The government of Nawaz Sharif (1990-93) introduced a program of economic

reforms aimed at privatization, deregulation, and liberalization. Priority was given to

denationalizing. Abolishing government’s monopoly in the financial sector, and selling

utilities to private interests were the hall mark of this period. Though government made

progress in liberalizing the economy, however, it failed to control a growing budget deficit.

The government of Benazir Bhutto (1994) continued the policies of both

deregulation and liberalization, and the tighter fiscal policies. The government devoted

significant resources to health, education, and especially for women.

1.2.2 Recent Economic History

In 90s, Pakistan experienced severe fiscal imbalances, and its debt grew rapidly. The nuclear

tests of May 1998 and imposition of economic sanctions by the G-7 triggered the situation.

In early 1999 Pakistan narrowly escaped defaulting on its debt. Although the country had

been receiving IMF assistance, the government faced difficulty in meeting the

conditionalities. The IMF program was suspended in July 1999, and resumed later during

Musharraf’s government. In 2004, government announced that IMF assistance was no

longer required. Thus program ended in that year, (Daily Times, 2004). Musharraf's

economic revival agenda continued to include measures to widen the tax net, formation of

private sector assets, governance reforms, privatization, and deregulation.

Pakistan's nominal gross domestic product (GDP) in 1997 was US$ 75.3 billion.

However, in 2002, it came down to US$ 71.5 billion. During this period, the real GDP grew

by 3.0 per cent on an average. Government debt was 82 per cent of its GDP in 2002. Over

one-third of the government's revenue was being used up in servicing of the debt and

liabilities.

4

The stagnant economy showed miraculous growth in 2002 after economic sanctions

that were imposed in aftermath of the 1998 nuclear tests lifted. The economy grew at 5.1

percent in 2003, 6.4 percent in 2004 and 7.0 per cent in 2005.

The US$ 72 billion economy of 2002 turned into a US$ 108 billion economy in

2005. During 1997-2002, average export growth was 1.2 percent per year and it went up to

13 percent per year during 2003-05. In 2005, debt as a percentage of the GDP came down to

59 percent from 82 percent in 2002. Government's interest payment as a percentage of

revenue collection came down to 23 per cent in 2005, which was 35 per cent in 2002.

According to many sources, the government made substantial economic reforms

since 2000; therefore prospects for job creation and poverty reduction were the best in a

decade. Despite all this, inflation increased in 2005 because of higher food prices, rising

property prices and rentals. Inflation (consumer priced index) went up to 9.3 percent, and

transport costs also jumped due to high oil prices.

1.2.3 The Economy Today

Pakistan is one of the fastest growing economies in the region along with China,

India and Vietnam, (Economic Survey of Pakistan 2006-07). The good performance was a

combination of sound economic polices, on going structural reforms, and a benign

international economic environment.

According to the Economic Survey, (2006-07) average real GDP growth during

2003-07 was the best performance since many decades. With economic growth at 7.0 % in

2006-07, Pakistan’s real GDP has grown at an average rate of 7.0 % per annum during the

last five years and over 7.5% in the last four years (2004-07). The size of economy has

reached $145 billion with per capita income at $ 1000. All the three major sectors;

agriculture, industry and services have provided support to strong economic growth. The

commodity-producing sectors (agriculture and industry) contributed 2/5th and services

sectors contributed remaining 3/5th to GDP growth. Within the commodity-producing

sectors, the contribution of agriculture alone has been 15 percent (or 1.1 percentage point)

5

while 25 percent (or 1.8 percentage point) contribution came from industry. Services sectors

contributed almost 60 percent (or 4.2 percentage points).

Table 1: Sectoral Share in Gross Domestic Product (GDP)

Structure of Economy

The Economic Survey (2006-07) further maintains that all three sectors; agriculture,

services and industrial/ manufacture contributed to GDP. Agriculture remains the single

largest sector of the national economy, and main source of foreign exchange earnings. It

accounts for 20.9 percent of GDP, employs major share of the total work force, and supplies

raw materials to industry as well as a market for industrial products. However, the internal

composition of the agriculture sector has changed gradually.

The share of crops sub-sector in agriculture has gradually declined from 65.1% in

1990-91 to 47.9% in 2006-07, and the share of livestock in agriculture has increased from

29.8% to 49.6% in the same period. The contributions of fishing and forestry have been

insignificant with only 0.3% and 0.2% respectively.

Share of manufacturing in the GDP has increased from 14.7 percent in 1999-2000 to

19.1% in 2006-07. Large-scale manufacturing accounting for 69.9% of overall

6

manufacturing, registered a growth of 8.8% in 2006-07. The services sector accounts for

53.3 percent in the GDP, and consists of wholesale and retail trade; transport, storage and

communications, financial and insurance services. The services sector grew by 8.5% in

2004-05, by 9.6% in 2005-06 and by 8.0% in 2006-07. Finance and insurance sectors have

been the major drivers of the growth, and showed growth of 30.8%, 33.0% and 18.2%,

respectively in these three years. The following Table will further illustrate the sectoral

contribution of these sectors to GPD.

Table 2: Sectoral Contribution to the GDP Growth (% Points)

SECTOR 2002-03 2003-04 2004-05 2005-06 2006-07 Agriculture 1.0 0.6 1.5 0.4 1.1 Industry 1.0 3.8 3.1 1.3 1.8 Manufacturing 1.1 2.3 2.7 1.8 1.6 Services 2.7 3.1 4.4 4.9 4.2 Real GDP (Fc) 4.7 7.5 9.0 6.6 7.0 Source: Economic Survey 2006-07 Consumption, investment and exports contributed to economic growth. Following illustrates

composition and contribution to GDP growth.

Table 3: Composition of GDP Growth (Point Contribution)

FLOWS 2000 2001

2001 2002 20022003 20032004 2004

2005 2005 2006

2006 2007

Avg 2003 2007

Private Consumption Public Consumption Total Consumption [C] Gross Fixed Investment Change in Stocks Total Investment [I] Exports (Goods & Serve.) [X] Imports (Goods & Serve.)[M] Net Exports [X-M] Aggregate Demand (C+I+X) Domestic Demand (C+I)

0.4 -0.5 -0.1 0.7 0.0 0.7 1.6

0.3

1.3 2.3

0.7

1.0 1.2 2.2 -0.1 0.0 0.0 1.5

0.4

1.0 3.7

2.2

0.3 0.6 0.39 0.6 0.4 1.1 4.5

1.6

2.8 6.5

2.0

7.1 0.1 7.2 -1.0 0.1 -0.9 -0.3

-1.3

1.0 6.0

6.3

8.7 0.1 8.8 1.8 0.7 2.5 1.7

5.4

-3.7 13.0

11.3

2.4 3.9 6.4 2.5 -0.5 2.0 1.8 3.2 -1.5

10.2 8.4

3.0 0.2 3.2 3.3 0.1 3.4 0.1 0.2 -0.2

6.6 6.5

5.3 1.1 6.4 1.7 0.1 1.8 0.8 1.9 -1.1

9.0 8.1

GDP MP 2.0 3.2 4.8 7.4 7.7 6.9 6.4 7.1 Source: Economic Survey 2006-07

7

Figure 1: Contribution to GDP growth

Exports

Pakistan is dependent on agriculture–based exports. Pakistan’s export is based on

commodities and not on products. Commodities tend to be more volatile in price while

products have to compete with other countries, the only exception being a unique product,

(Salicornia, Seabuckthorn). In 2005-06 exports were $ 13.46 billion, whereas in 2006-07,

export target was $ 18.6 billion, (12.9 percent higher than last year). During the first ten

months (July-April), export went up by 3.4 percent: a modest rise from $ 13.46 billion to $

13.9 billion in the same period last year. Export of textile manufacture grew by 6.2 percent:

Knitwear (13.9%) ready made garments (6.8 %) made up articles (8.9%), cotton yarn (4.6

%), towels (2.6%) and other textile material (17.2 %). However, export of raw cotton, cotton

cloth and bed wear declined. Export of food group also declined by 3.5 percent due to

decline in export of rice and fruits. Like wise, exports of petroleum products declined by 2.7

%. Engineering goods showed a growth of 6.7 % and over all exports went up by $ 452.1 in

the first ten months of 2006-07 and the textile sector contributed $ 516.1 in this increase.

8

Figure 2: Major contributors to additional export earnings (Jul-Apr 06-07)

Others, 64.8

Food Group, 13.1

Other Manufacturer,

65.6

Textile Manufacturer,

114.1

TextileManufacturer

OtherManufacturer

Others

Food Group

Source: Economic Survey (2006-07

Table 4: Structure of Exports 2007-08

9

Pakistan has a very narrow export base and exports are highly concentrated in a few

items cotton, textile manufactures, leather, rice, synthetic textiles and sports goods are the

main export commodities, and accounted for 77.2 percent of total exports during the first

nine months of 2006-07. Cotton manufacturers contributed 61.5 percent, followed by leather

(4.5%), rice (6.6%), synthetic textiles (3.0%) and sports goods (1.6%).

Table 5: Export of Textile Manufactures

ITEM 99-00 00-01 01-02 02-03 03-045 04-05 05-06 06-07* Cotton Yarn 19.2 18.7 16.1 12.9 14.0 12.7 13.7 13.3 Cotton Cloth 19.6 17.9 19.6 18.6 21.3 23.3 21.6 18.5 Knitwear 15.9 15.8 14.6 15.9 18.1 18.9 17.6 18.3 Bed war 12.7 12.9 15.9 18.4 17.2 16.4 20.8 18.1 Towels 3.5 4.2 4.6 5.2 5.0 5.9 5.8 5.5

Tents, Canvas & Tarpaulin

0.9 0.9 0.9 1.0 0.9 0.8 0.3 0.7

Readymade Garments 13.8 14.4 15.1 15.1 12.4 12.9 13.9 13.1

Synthetic Textiles Total

8.2 9.5 7.1 7.9 5.9 3.5 2.0 4.7

Made up Articles 5.5 5.7 6.1 5.0 5.2 5.5 4.3 4.1 Others 0.7 - - - - 0.1 0.1 2.9 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

*July-March (Provisional) Source: FBS & Finance Division

The structure/ composition of export have gone through changes with time. The

share of exports of primary good has declined and exports of semi- manufactured and

manufactured goods have gone up gradually.

Pakistan’s exports directions are highly concentrated in few countries. The US, UK,

Germany, Japan, Hong Kong, Dubai and Saudi Arabia are the traditional export

destinations. These countries account for one-half of Pakistan’s exports. The US alone

accounts for 28 percent of Pakistan exports.

10

Table 6: Major Export Markets

Imports

Since 2003 imports were on the rise, but in 2006-07 the import growth declined. In

2005-06 imports were $28.6 billion. In 2006-07, imports were targeted to decline by 2.1

percent. Growth in import decelerated to 8.9 percent during the first ten months (July-April)

of 2006-07 as against the increase of 40.4 percent in the same period last year. The decline

was due to pursuance of tight monetary policy, softening of international oil prices, decline

in the imports of fertilizer, and iron & steel products. Pakistan's imports are highly

concentrated in few items: machinery, petroleum & petroleum products, chemicals, transport

equipments, edible oil, iron & steel, fertilizer and tea. The eight categories accounted for

75.5 percent of total imports during 2006-07. Among these, machinery, petroleum &

petroleum products and chemicals accounted for 57.7 percent of total imports. Pakistan’s

imports sources limited, and over 40 percent of the imports come from the USA, Japan,

Kuwait, Saudi Arabia, Germany, the UK and Malaysia.

11

Table 7: Structure of Imports

12

Figure 3: Sources of import

USA, 8.1Japan, 5.7

Kuw ait, 5.4

Saudi Arabia, 11.5

Germany, 4.1U.K, 2.3

Malaysia, 3

Others, 59.9

USA

Japan

Kuw ait

Saudi Arabia

Germany

U.K

Malaysia

Others

Source: Economic Survey 2006-07 Table 8: Pakistan’s Major Imports

Trade Balance

Despite decline trend in imports, the merchandise trade deficit widen due to fall in

exports. The merchandise trade deficit widen to $11.1 billion in the first ten months (July-

13

April) of 2006-07 as against $9.5 billion in the same period last year. However, trade deficit,

as percentage of GDP is likely to be narrow down to 9.0 percent in 2006-07 as against 9.5

percent last year.

Term of Trade

With base year 1990-91 (equal to 100) the term of trade aggregated to 64.4 during

2006-07. It was 66.4 in 2005-06, thus registered a decrease of 3.4 %. The increase in unit

prices of petroleum and machinery caused this decline.

Table 9: Unit Value Indices and Term of Trade (Base Year 1990-91=100)

Current Account Balance

The current account deficit widened to $ 6.2 billion (4.3% of GDP) in the first nine

months (July-March) of the 2006-07 from $ 4.6 billion (3.6% of GDP) in the same period

last year. Despite the decline in the import growth (10.2 percent), the current account deficit

has widened due to “not satisfactory” performance of exports, and deficit in services sector.

14

Figure 4: Current account deficit (month wise)

Source: Pakistan Economic Survey 2006-07

Workers’ Remittances

Workers’ remittances are the third largest source of foreign exchange inflows after

exports and foreign investment. The inflows maintained the rising trend. Workers’

remittances totaled $ 4.45 billion in the first ten months (July-April) of the fiscal year as

against $ 3.6 billion in the same period last year, depicting an increase of 22.6 percent.

Debt and Liabilities

This includes all Government debt and liabilities denominated in foreign currency.

Pakistan’s total stock of external debt grew at an average rate of 7.4 percent per annum

during 1990-99, rising from $ 20.5 billion to $ 38.9 billion in 1999. However, there was a

slight decline in 1999-2000 ($37.9 billion.) It grew again by 1 percent in 2005, 2.9 percent

in 2006 and 4.4 percent in 2007, making the total external debt liabilities (EDLs) $ 38.86

billion at the end of March 2007.

15

Figure 5: External debt and liabilities

Source: Pakistan Economic Survey 2006-07

However, EDLs as a percentage of GDP have declined from 51 percent in 2002 to

29.4 percent in 2006 and 27.1 percent in 2007. EDLs are medium and long term borrowing

from multilateral and bilateral lenders.

Table 10: External Debt and Foreign Exchange Liabilities ($ Billion)

16

Debt Servicing

The averaged debt servicing during 1999- 2000 to 2003-04 was above $ 5 billion per

annum. This came down to $ 3 billion in 2005 - 06. Whereas an amount of 2.2 billion were

paid in 2006-07 (July- March) and the rolled over amount declined from $ 4.1 billion in

1999- 2000 to $ 1.1 billion in 2006-07.

Pakistan and International Capital Markets

Pakistan participates in the global capital markets by issuance of bonds both

conventional and Islamic. In 2006 Euro bond of $ 500 million (10 year) and $ 30 million (30

year) were issued. In 2005 Islamic Bond (Sukuk) worth $ 600 million was issued, and was

successful in the Middle East markets. Euro bonds worth $ 750 million at a fixed rate of

6.875 percent were issued in 2007; the issue was “oversubscribed by 7 times”. The

international magazine “Business Week” has declared Pakistan’s KSE 100 Index the best-

performing stock market index in the world in the past few years. In 2005, the stock market

capitalization of listed companies was valued at $45,937 million by the World Bank.

Inflation

The Consumer Price Index (CPI) based inflation was 7.9%, and Sensitive Price

Index (SPI) inflation was 11.1% in 2006-07 (July–April). The food group was largest

component of the CPI and it showed an increase of 10%. The non-food prices grew at a

slower rate and showed average inflation of 6.2 %. The increase in Wholesale Price Index

(WPI) in 2006-07 was lower than of the last year.

17

Figure 6: Inflation rate by group

Foreign Exchange Reserves

At the end of April 2007, the total liquid foreign exchange reserves were $ 13.3738

billion. They were sufficient to meet over 6 months of imports. Last year’s reserves were $

13.137 billion.

Exchange Rate

Exchange rate remained quite stable during 2007. Though, rupee depreciated slightly

(0.7%) from Rs.60.2138 per dollars as at end June 2006 to Rs.60.6684 as of end April 2007.

Fiscal Budget

Fiscal year starts from 1 July and ends at 30 June.

18

Figure 7 & 8: Revenue and expenditure: budget estimate 2006-07

Total Revenues, 1163

Total Expenditure, 1536.6

Total Revenues

Total Expenditure

FBR Revenue, 835

Provincial Tax Revenues, 44.8

Others, 5.9

Non Tax Revenues, 277.3

Current Expenditure (Federal &

Provincial), 1106.5

Development Expenditure ^Net Lending, 312.3

FBR Revenue

Provincial Tax Revenues

Others

Non Tax Revenues

Current Expenditure (Federal &Provincial)Development Expenditure ^NetLending

Source: Ministry of Finance (Budget Wing)

Foreign Direct Investment (FDI)

According to different reports, Pakistan is now the most investment-friendly nation

in South Asia. The World Bank (2006) has ranked Pakistan at 74th position in the world on

ease of doing business that is much ahead of China and India, which are at 93rd and 134th

respectively. The Foreign Investment (FI) flows were US $ 8.4 billion in 2006-07. Foreign

Direct Investment (FDI) was $5.125 billion in 2006-07, with an increase of 46%.

Privatization proceeds in 2006-07 were $266.4 million. Private portfolio investment was

19

$1,820 billion in 2006-07. The USA was the largest investor in 2006-07 followed by the

UK.

Figure 9: Foreign direct investment inflows ($ billion)

1,524

3,521

5,125

237 335 306 354 442

1,102682 601 472 470 322 485

0

1,000

2,000

3,000

4,000

5,000

6,000

90/91

91/92

92/93

93/94

94/95

95/96

96/97

97/98

98/99

99/00

00/01

01/02

02/03

03/04

04/05

05/06

06/07

Source: Board of Investment

Figure 10: Top investing countries

Source: Board of Investment

0200400600800

1000120014001600

USAUAE UK

Netherl

ands

China

Switzer

land

Saudi

Arabia

2004-052005-062006-07

20

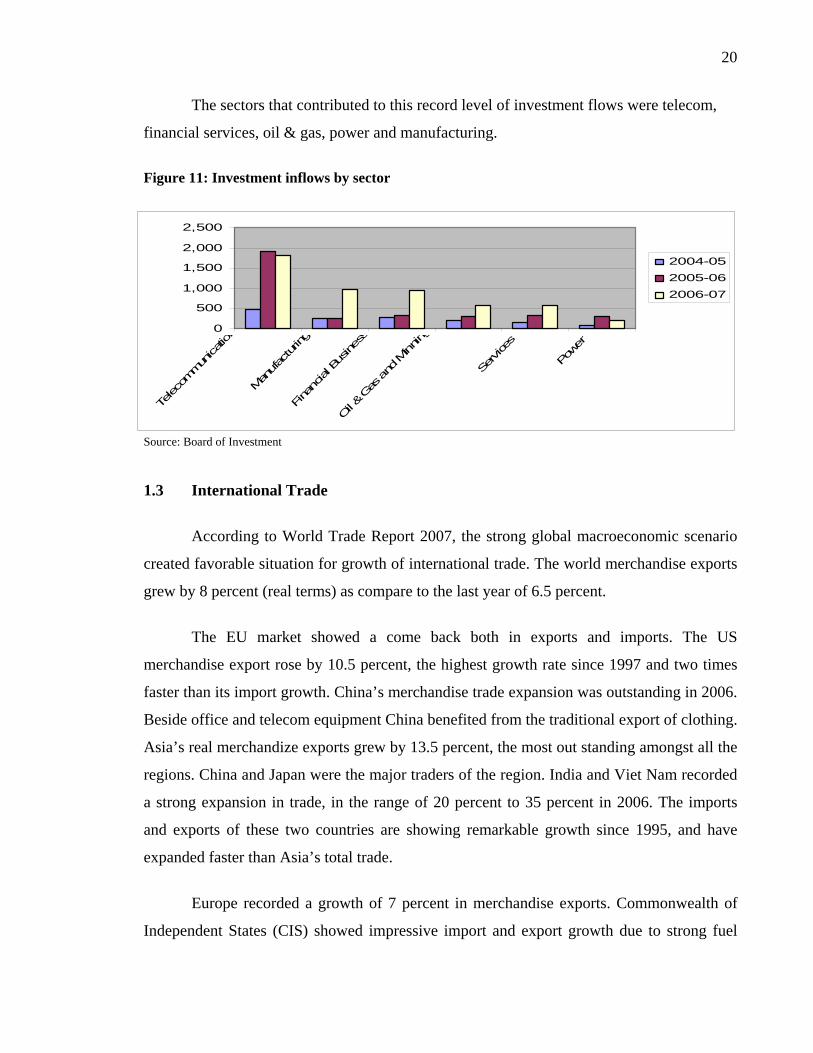

The sectors that contributed to this record level of investment flows were telecom,

financial services, oil & gas, power and manufacturing.

Figure 11: Investment inflows by sector

Source: Board of Investment

1.3 International Trade

According to World Trade Report 2007, the strong global macroeconomic scenario

created favorable situation for growth of international trade. The world merchandise exports

grew by 8 percent (real terms) as compare to the last year of 6.5 percent.

The EU market showed a come back both in exports and imports. The US

merchandise export rose by 10.5 percent, the highest growth rate since 1997 and two times

faster than its import growth. China’s merchandise trade expansion was outstanding in 2006.

Beside office and telecom equipment China benefited from the traditional export of clothing.

Asia’s real merchandize exports grew by 13.5 percent, the most out standing amongst all the

regions. China and Japan were the major traders of the region. India and Viet Nam recorded

a strong expansion in trade, in the range of 20 percent to 35 percent in 2006. The imports

and exports of these two countries are showing remarkable growth since 1995, and have

expanded faster than Asia’s total trade.

Europe recorded a growth of 7 percent in merchandise exports. Commonwealth of

Independent States (CIS) showed impressive import and export growth due to strong fuel

0

500

1,000

1,500

2,000

2,500

Telec

ommun

icatio

n

Man

ufac

turin

g

Fina

ncial Bus

iness

Oil &

Gas

and

Minn

ing

Service

s

Powe

r

2004-052005-062006-07

21

and metal prices in the world markets. Africa’s merchandise exports increased by 21

percent; faster than its imports. Middle East trade was affected by oil market development

and grew only by 19 percent. Over all exchange rate development had a moderate affect on

the dollar price level of trade goods. However, a weaker yen contributed to a weaker dollar

export prices of Japan, where as Euro and Pound balanced each other during 2005-06.

World merchandise exports in dollar terms were $11.76 trillion, and inflation factored in

about 40 percent of this value change. Commercial services exports rose by 11 percent ($

2.71trillion) in 2006.

Figure 12: Real merchandise trade growth by region 2006 (Annual Percentage Change)

Figure 13: Growth in the volume of world merchandise trade and GDP 1996-2006 (annual

percentage change)

22

Pakistan ranked 65 in global merchandize exports and 50 in imports during 2006. Its

share in global exports and imports is 0.14 and 0.24 percent in 2006, (UNCTAD, Trade

Profile 2007).

1.4 Aid, Debt, Trade

Equitable economic growth means employment and opportunity for all. It holds the

key to long-term development. However, in the prosperous world with an “up beat” growth,

poor countries face tremendous barriers to unleashing their economic potential for

development.

Burdensome debt payments, trade barriers, lack of money and balance of payments

problems are among the key obstacles to achieving sustainable development. Global poverty

will always be unresolved agenda without addressing the issues of aid, debt, and trade

according to NetAid, an initiative of Mercy Corps.

1.4.1 Aid

Bilateral aid is given by a single country and multilateral aid is funded jointly by the

developed nations and is co-coordinated by many different agencies. The UN co-operates

with the independent charities in relief operations and fieldwork. Charities vary considerably

in their approaches, some concentrate in providing money to relieve suffering during

emergencies; others prefer to invest in long- term projects. Aid can be distributed either by

government bodies, or by businesses and voluntary agencies. Mostly aid is given on certain

conditions. A common condition is that the money must be spent on products or services

from the donor country. Aid or Overseas Development Assistance (ODA) is a controversial

area because aid/ grants are largely considered politically motivated.

In the article “Trade not Aid”, Anthea Spitaliotis, mentions the Brandt Report (1980)

by the former German Chancellor, Willy Brandt, which argues for an increase in aid to the

third world, “it is a moral responsibility to solve the problems of the poor countries and

remove the injustices that have prevented their development in the past. Secondly, since the

two are dependent on each other economically, the future prosperity of the developed

23

countries relies on development in the third world… It could be made to work from a

practical point of view, the crucial question though is whether the political willingness exists

to achieve these goals”, the writer argues.

“Bilateral donors, in particular, provide aid for many reasons that includes political,

strategic, commercial and humanitarian. In 1988, 41 percent of external assistance went to

middle and high income countries, largely for political reasons.” (World Development

Report, 1990).

Similar apprehensions have been expressed by James Shikwati, Director of the Inter-

Region Economic Network, Nairobi… Handouts from the rich nations too often fill the

pockets of dictators rather than the bellies of the starving. He further says that…aid gives

untrustworthy leaders the resources with which to engage in violent and repressive acts.

Mengistu (Ethiopia), Pol Pot (Cambodia) and Idi Amin (Uganda) are among the more

infamous recipients of foreign aid. By 1982 Zaire (now Democratic Republic of Congo) had

accumulated a foreign debt of $5 billion. Its president, Mobutu Sese Seko, had accumulated

a personal fortune of $4 billion.

Mr. Shikwati maintains that…aid also undermines the democratic accountability of

government. By offering governments a non-tax source of revenue, it enables them to ignore

the wishes of citizens and reduces their incentive to deliver public services efficiently and

effectively. It also exacerbates cronyism. Why not award valuable contracts to your brother-

in laws more expensive (and less efficient) building company if you know the people can't

complain”?

1.4.2 Debt

Debt retards the economic development. Poor countries with enormous amounts of

debt are deprived economically, therefore, can not meet even the basic needs of their people.

The money flows out of the country for “debt servicing” instead of invested within. One

international aid group remarked that global poverty "of which debt repayments are a major

cause" kills as many people as the tsunami every week, NetAid quotes.

24

Jones, (1989) observes that it is not just that development has been stopped or

retarded in the third world; the hope of development of a better future has been lost. In

psychological terms, it is a greater loss than some of the human tragedies.

“The debt problem which was thought to be temporary has persisted with increasing

force and perversity. It has gone deeper into the social fabric of third world countries and

has become malignant”, (Schatan, 1987).

Richard Jolly of UNICEF at the Conference “Growing out of Debt” 1988 quoted

former President of Tanzania Julius Nyrere, “must we starve our children to pay our debts”.

Jolly observed: “that question has been answered in practice and the answer has been

‘Yes’…Hundreds of thousands of children in the developing world have given their lives to

pay their countries’ debts, and many millions more are still paying the interest with their

malnourished minds and bodies”.

According to Harry L, Freeman of American Express, “Developing countries debt

has become an economic millstone around the necks of both the debtor countries and the

creditor countries to trade with them”.

In Pakistan, the component of consultants in the World Bank funded projects is

between 80 to 90 percent of the total project funding, (Economic Affairs Division).

1.5 Trade Not Aid

The current argument and debate is whether donor loans do lead to development, or

do they shift focus. “But "aid" can not stimulate development. Only trade can do that. Since

the 1960s, over $500 billion has been given to the governments of African countries in the

form of grants and soft loans. Yet the results have been less than spectacular,” Mr. Shikwati

declares. He further maintains that, “the rich world can help - by opening its markets to

textiles, agricultural goods, and other products from the poor world. Trade will lead to

production that will lift the standards of living in poor countries. It could also remove its

agricultural subsidies, which reduce world market prices of these goods, reducing the

amount poor-world producers can obtain for their goods.”

25

The case for trade as the engine for economic development is indisputable. The need

for trade has caused wars, driven colonial domination and helped to create the current

international trade system. The economic expansion of India, Japan, Thailand, Singapore

and China testifies that trade stimulates growth. These countries have developed an

industrial capacity to export that has been instrumental in producing the accelerated growth

of their economies, (Goodafrican).

Reason Magazine in the article Trade, not Aid (Marian Tupy and Christopher Preble)

quotes Uganda's President, Yoweri Museveni stating during his meeting in 2003 with

President Bush, "I don't want aid; I want trade. Aid cannot transform society." The message

has been stressed by the development economists for years!

The “subsidies plus aid” forces taxpayers to pay twice - once to sustain the

inefficient subsidies, and then again to pay for aid programs. William R. Cline, senior fellow

at the Institute for International Economics and the Center for Global Development,

estimated that global trade liberalization would save the developed nations $141 billion a

year and deliver economic benefits worth $87 billion a year to developing countries.

(Reason Magazine)

While lamenting the damage aid has done to Africans: “the poison was aid and its

consequential economic distortion and dependency”, Simon Jenkins of The Times, London,

states that the one help Africa most needs is trade. It needs Western markets open to its

primary produce.

Mary Robinson, former President of Ireland and former United Nations High

Commissioner for Human Rights emphasises the importance of trade for development and

economic growth and says that if poor countries could increase their share of world exports

by just one percent, they could lift 128 million people out of poverty. She observes that,

“We need to bring home the fact that trade is not only a key engine of development; it is also

a crucial factor in economic justice. Trade policies can directly affect people's access to

fundamental rights – to an adequate standard of living, health, food, and education.”

26

In the Doha Round, known as Doha Development Agenda, (DDA) developed

countries were urged to lower agricultural and textile subsidies. But it was politically

difficult, since many domestic farmers and workers depend on these subsidies to make a

living. To sum up, developing countries do not need aid. They need fair access to global

markets where their products are competitive, and sustain economically.

1.6 Rationale of the Study

Previous researches on the challenges and opportunities generally highlight the role

of the government in enhancing the performance of the sector, thus suggest the policy tools

and incentives for making the sector competitive. Many reports have suggested economic

parameters to up lift the sector to face the challenges of the international trade at the cost of

the other sectors.

Hardly any report has touched the dynamics working with in the sector for the last 60

years retarding the growth and expansion of the sector. There was enough room for a

research that narrates this “untold story”, with objective analysis and deep examination

keeping in view the domestic and global dimensions of the issue. Moreover, also suggests

cost effective and practical measures to over come the road blocks for competitive

positioning of the sector in international markets.

1.7 Limitations

Finding relevant and reliable material and data was very difficult. The official data

on the same subject from different sources hardly coincide. Very few reports and books are

available on cotton-textile and apparel sector’s performance after post quota. Available

material mostly is focused on the policy side of the subject, and limited information is

available on the actual performance and “behavior” of the sector and the players that

dominate the sector. More over, material on international trade mostly gives the theories and

models thus limiting the scope of its use in a research thesis for a variety of audience. Lastly,

the researchers always run against the wind in terms of time and research facilities available.

27

References

A. Gledhill, Pakistan (Stevens, London, 1957), Altaf Zafar, Dr, (1983): Pakistani

Entrepreneurs; Their Development, Characteristics and Attitudes, Croom Helm Ltd,

Provident House, Burrell Row, Beckenham, Kent BR3 1AT, Australia

Altaf Zafar, Dr, (1983) : Pakistani Entrepreneurs; Their Development,

Characteristics and Attitudes, Croom Helm Ltd, Provident House, Burrell Row, Beckenham,

Kent BR3 1AT, Australia

Board of Investment, Ministry of Investment (BOI), Government of Pakistan:

http://www.pakboi.gov.pk

CIA: The World Fact Book - Pakistan: https://www.cia.gov/library/ publications/the-

world-factbook/rankorder/2003rank.html

Concluding remarks at the Pakistan Development Forum, 2006 by John Wall, World

Bank Country Director for Pakistan: http://www.worldbank.org/html

Daily Dawn Annual Budget, 2007; June 9, 2007: http://www.dawn.com

Doing Business in 2006: South Asian Countries Pick up Reform Pace says World

Bank Group; Pakistan Among Top 10 Reformers (September12, 2005), http://worldbank.org

Economy of Pakistan: Wikipedia:http://.enwikipedia.org/wiki/ economy_of_pakistan

Good Africa: http://www.goodafrica.net/index.asp. Retrieved on 2007-03-23

Government of Pakistan, Islamabad: http://www.pakistan.gov.pk

Government of Pakistan: Ministry of Commerce: http://www.commerce.gov.pk

28

Hertz, Noreena, (2004): The Debt Threat. Harper Collins Publishers, 2004 NY.

Ishrat Husnain - Economy of Pakistan. Article by the Governor of State Bank of

Pakistan; http://www.bis.org/review/r050217g.pdf

James Shikwati, (2002): http://www.smh.com.au

Jones, S. Griffith, (1988): “Debt Crisis Management in the Early 1980s: Can Lesson

be Learnt”? Development Policy review, Vol.6. 1988

Jones, S. Griffith, (1989): Growing out of Debt: A Conference organized by the

British All parliamentary Group on Overseas Development

Mary Robinson, former President of Ireland: Africa needs friar Trade, not Charity:

Yale Global Online: http://yaleglobal.yale.edu

Net Aid: http://www.mercycorps.org: retrieved on 22- 02-2007

Nicholas Louise, (2007): Comparative Prospects for Growth of Real GDP:2000-

2015:

World Economic Prospects 2007 http://www.euromonitor.com/: Retrieved in 2007

Pakistan – The Economy; Retrieved on 2008-04-12. http://www.mongabay.

com/reference/country_studies/pakistan/ECONOMY.html

Pakistan Economic Survey, (2006-07), Finance Division, Government of Pakistan,

Islamabad

Pakistan Economy Profile 2007: Retrieved on: 2007-12-20: http://www.

indexmundi.com/pakistan/economy_profile.html

29

Pakistan ends 15-year ties with IMF; Daily Times, 7 September 2004, Pakistani

Newspaper Article, 2004. http://www.daliytimes.com.pk

Reason Magazine: Trade, not Aid; http://www.reason.com Retrieved on 2008- 02-25

Richard Jolly, (1988); UNICEF: Growing out of Debt: A Conference organized by

the British All parliamentary Group on Overseas Development.

Schatan, J (1987), World Debt- Who is to pay? English edition, Zed books, London

Simon Jenkins: Do not patronize Africa: give Trade, not Aid:

http://www.thirdworldtraveler.com: Retrieved on 2007-01-28

Telegraph Daily; (newspaper): http://www.telegraph.co.uk: Retrieved on 2007-04-23

Trade not Aid: Time Magazine: http://www.time.com

Trade, not aid, is what Africa needs: the Financial Express; (newspaper): Retrieved

on 2007-12-28: http://www.financialexpress.com

USA History; Trade not aid, (Anthea Spitaliotis): http://www.usahistory.com

World Economy: Wikipedia, the free encyclopedia; http://wikipedia.org: Retrieved

on 2008-03-22

World Development Report, (1990): World Trade Organization, Switzerland, United

Nations Conference on Trade and Development, Publication. New York and Geneva,

World Trade Report, (2007): World Trade Organization, Switzerland, United

Nations Conference on Trade and Development, Publication. New York and Geneva,

WTO 2007: Trade Profiles, (2007): World Trade Organization, Switzerland

30

CHAPTER 2

LITERATURE REVIEW 2.1 Origin of Trade

“The study of international trade and finance is the oldest among the specialties of

economics, conceived in the sixteenth century, a child of Europe’s passion for Spanish gold,

and grew to maturity in the turbulent years that witnessed the emergence of modern nation

states”, (Kenen, 1994).

2.2 Evolution of Trade and Trade Theories

Trade started with the beginning of communication in prehistoric times. Trading was

common between prehistoric people, who bartered goods and services before the innovation

of the modern day currency. Watson, (2005) argues that the history of long-distance trade

and commerce started from circa 150,000 years ago.

It is believed that trade has taken place throughout the human history, and the

exchange of obsidian and flint during the Stone Age was common. Since 3000 BC materials

used for making jewelry were traded with Egypt. There are evidence of long-distance trade

routes in the 3rd millennium BC, which supports that Sumerians in Mesopotamia traded

with the Harappan of the Indus Valley. The Phoenicians were sea traders, and traveled

across the Mediterranean Sea, and as far north as Britain, and established trade colonies the

Greeks called emporia. In the 5th century, trade brought spice to Europe from the Far East,

including China. Trade strengthened the Roman Empire, and Romans established a stable

and secure transportation system that enabled the shipment of trade goods without fear of

piracy.

31

The fall of the Roman Empire brought instability to Western Europe and the trade

network almost collapsed. Some trade did occur. Radhanites and Jewish merchants traded

with the Christians in Europe and the Muslims of the Near East.

The caravan merchants of Central Asia dominated the East-West trade route known

as the Silk Road from the 4th century AD up to the 8th century AD. From the 8th to the

11th century, the trade was dominated by Vikings and Varangians as they sailed from and

to Scandinavia and Russia. Between the 13th and 17th centuries, the Hanseatic League an

alliance of trading cities maintained a trade monopoly over most of Northern Europe and the

Baltic.

In 1498, Vasco da Gama restarted the European spice trade. The spice trade with

Europe was controlled by Islamic powers especially Egypt, prior to his sailing around

Africa. Holland was the centre of free trade and free movement of goods in the 16th century.

Trade in the East Indies was dominated by Portugal in the 16th century. The 17th and 18th

century’s trade was dominated by the Netherlands and the British respectively. The Spanish

Empire established regular and organized trade links across the Atlantic and the Pacific

Oceans.

Around the 16th century trade became part of national policy. During this period,

European countries gained wealth and precious metals from their colonies and trading

partners. This system of international trade, called “mercantilism”, remained active from the

16th to the 18th centuries. Mercantilism was a sixteenth-century economic philosophy that

upheld that a country's wealth was measured by its assets of gold and silver, (Mahoney,

Trigg, Griffin, & Pustay, 1998).

The philosophy of mercantilist was that one country's gain through international

trade was another country's loss. Hence, mercantilist’s belief was that international

commerce and trade always had a loser. During this period the European empires tried to

increase and maintain the power by gathering gold and silver and simultaneously imposed a

number of trade restrictions and introduced protectionist policies to ensure that they export

32

more than they import to maintain a positive and favorable balance of trade. Mercantilism

was popular with manufactures and their workers. Export-oriented manufacturers favored

mercantilist trade policies, and grant of subsidies and tax rebates, because it stimulated their

sales to foreigners. In the same vein the domestic manufacturers threatened by imports

support mercantilist trade policies, such as imposing tariffs or quotas, because it protected

them from foreign competition, (Mahoney, Trigg, Griffin, & Pustay, 1998).

In the 17th and 18th centuries, the development of nation-states facilitated

international trade to evolve towards its present state. It was realized by the leaders that by

promoting and facilitating trade, they could not only increase their wealth and power, but

also strengthen the power and stability of their respective nations. During this period,

economists began formulating theories of international trade and conceiving of liberalized

trade policies.

Adam Smith (1723-1790) is considered as the founder of theoretical study of

international trade. Smith developed the theory of "absolute advantage” based on doctrines

of the French economist François Quesnay (1694-1774). He argued that with in their limited

natural resources, countries should produce only those products which can be manufactured

more cheaply and efficiently than their trading partners. In other words, the theory of

absolute advantage, suggests that a country should export only those goods and services for

which it is more productive and efficient than other countries, and import those goods and

services for which other countries are better than it is, (Mahoney, Trigg, Griffin, & Pustay,

1998).

Smith attacked the philosophy of mercantilism, and expressed that mercantilism

actually weakens a country. In An Inquiry into the Nature and Causes of the Wealth of

Nations, (1776), Smith argued that a country’s true wealth is measured by the wealth of its

citizens, not just that of its monarch, (Mahoney, Trigg, Griffin, & Pustay, 1998). Smith was

of the view point that a greater division of labor could bring more productivity to

international trade, and therefore, the workers should be allowed to specialize in production

of specific goods.

33

According to Gans, King, & Mankiw (1999), the term absolute advantage is used by

the economists to compare the productivity of one person, firm or nation with that of

another. It means that a producer who requires a smaller quantity of inputs to produce a

good has an absolute advantage in producing that good.

In 1815 English economists Robert Torrens (1780-1864) and David Ricardo (1772-

1823) suggested that countries import and export goods according to the principle of

"comparative advantage." According to this theory no trade would take place if one country

has an absolute advantage over both products. The difference between absolute and

comparative advantage theories is delicate. It suggests that “absolute advantage looks at

absolute productivity differences, comparative advantage looks at relative productivity

differences”, (Mahoney, Trigg, Griffin, & Pustay, 1998).

In 1817, David Ricardo, James Mill and Robert Torrens in the theroy of comparative

advantage demonstrated that free trade would benefit both weak as well as the strong

countries industrially. In Principles of Political Economy and Taxation, Ricardo pointed

out…When an inefficient producer sends the merchandise it produces best to a country able

to produce it more efficiently, both countries benefit. In other words, a country can still

produce and export a product even though it cannot produce the product as cheaply as some

other country, on the premise that this more expensively produced product can fetch more

revenues in a foreign market than in the domestic market.

In the mid 19th century the rise of free trade was essentially based on national

advantage. The rise of “national” economist was a key step in the development of

contemporary international trade. These economists proposed theories aimed at the interests

and benefits of their respective nations. These theories received further acceptance on the

ideas of American politician Alexander Hamilton (1755-1804) and others in the late 18th

and early 19th centuries. Hamilton in a way facilitated the concept of political economy to

develop, which implies active government involvement in economics including international

trade. Hamilton argued that to avoid reliance on importing essential goods, resources and

34

equipments, Congress should enact such policies that would make the United States self-

sufficient.

John Stuart Mill (1806-1873) suggested that in international market a country with

monopoly pricing power could influence the terms of trade through maintaining tariffs, and

getting reciprocity in trade policy. This theory was given by David Ricardo and others

earlier. It was believed that trade surplus would grow following reciprocal, rather than free

trade policies. This was against the philosophy of free trade. Within a few years the infant

industry scenario was presented by Mill. The theory promoted that government had the

"duty" to protect young industry, and to facilitate it to develop to full capacity. The policy

was attractive to many countries on the way to industrialization. Milton Freidman also

supported this thought, and demonstrated that under certain circumstances tariffs might be

beneficial to the host country but not for the world at large.

Keynesianism and Keynesian theory is based on the ideas of 20th century British

economist, John Maynard Keynes. According to this theory actions of individuals and firms

at micro level can affect aggregate macroeconomic out comes, and the economy operates

below its potential in output and growth. Many classical economists had supported Say’s

Law, that supply creates its own demand; however, Keynes maintained that aggregate