30.07.2007 InVision Software AG Research Note fileVodafone, Deutsche Telekom or IKEA are testimony...

40

30.07.2007 InVision Software AG Research Note SES Research GmbH – A Member of the Warburg Group Page 1 Buy Price target: EUR 40.0 (initial coverage) The ideal time to get the show on the road InVision is a genuine pure play software provider for workforce management solutions (with royalties accounting for 57% of sales in 2006). The key strength of InVision’s solution lies in staffing requirement forecasts and the subsequent flexible optimisation of staff deployment. The software tackles mathematical optimisation issues that are extremely difficult to solve. Product specifications of this nature clearly set InVision apart from the competition and explain the com- pany’s strong growth. Over 180 clients, including top names such as Vodafone, Deutsche Telekom or IKEA are testimony to the high competitive quality of InVision’s solutions, which generally provide a return on investment within 6-12 months. InVision’s solutions allow its clients to: • cut costs by reducing instances of excess cover, • boost productivity by reducing instances of insufficient cover, • increase employee satisfaction, for example by implementing flexible schedules that employees have a say in Growth is driven primarily by: the replacement of proprietary sys- tems; a strong client pipeline; the broadening of market access to cover additional areas; the expansion of the company’s sales activi- ties and of the partner business; further internationalisation, taking the company onto the very dynamic international markets, and the planned strengthening of the company’s capital base as a growth catalyst. In financial year 2006, InVision reported growth of around 70% and an EBIT margin of 18% (EUR 1.95 m). This means that the company’s operating result was boosted by EUR 3.6 m as against the prior-year, when it still reported a loss. This highlights a key issue for pure play software providers: InVision has completed the main development work for its product and has a strong client basis that guarantees regu- lar maintenance income. Further increases in sales will have a clearly above-average impact on the EBIT margin, with even this year’s figures expected to confirm this trend (extremely high scalability). As a result, we expect the EBIT margin to increase from 18.2% to 23.0% (EUR 4.15 m) in financial year 207, with sales growth of 68%. The figures for Q1/07 support this assumption. On June 14, 2007, InVision was listed successfully at the stock exchange which will support further growth. The calculated valuation range for the share is EUR 38 to EUR 46. We initiate the coverage of InVision with the rating “BUY”. Our PT is EUR 40. Bloomberg: IVX GR Price: 32.65 Reuters: IVXG.DE Tech-All: 1091.79 ISIN DE00585969 Internet: www.InVision.de Segment: Prime Standard Sector: Software 30,5 31 31,5 32 32,5 33 33,5 34 34,5 35 35,5 06/07 07/07 07/07 InVision Software Tech-All (relativ) Share data: Bloomberg 27.07.2007 / Closing price High /Low 52 w: EUR 34.59 / 32.00 Market cap. EUR 72.97 m No. of shares: 2.24 m Shareholders: Peter Bollenbeck 17,00% Matthias Schroer 17,00% Armand Zohari 17,00% InVision Holding GmbH 6,29% Free Float 4,71% Calendar: H1/2007 14.08.2007 Figures Q3/07 14.11.2007 Analysis: SES Research Publication: 30.07.2007 Felix Ellmann (Analyst) +49-(0)40 309537-12 Institutional Client Contact: M.M.Warburg & CO +49-(0)40 3282-2636 Institutional Equity Sales Christian Alisch +49-(0)40 3282-2667 Thomas Dinges +49-(0)40 3282-2635 Matthias Fritsch +49-(0)40 3282-2696 Dr. James F. Jackson +49-(0)40 3282-2664 Oliver Jürgens +49-(0)40 3282-2666 Benjamin Kassen +49-(0)40 3282-2630 Marina Konzog +49-(0)40 3282-2669 Linn Lenné +49-(0)40 3282-2695 Dirk Rosenfelder +49-(0)40 3282-2692 Marco Schumann +49-(0)40 3282-2665 Andreas Wessel +49-(0)40 3282-2663 Sales Trading Oliver Merckel +49-(0)40 3282-2634 Thekla Struve +49-(0)40 3282-2668 Gudrun Bolsen +49-(0)40 3282-2679 Nils Carstens +49-(0)40 3282-2701 Jörg Treptow +49-(0)40 3282-2658 Patrick Schepelmann +49-(0)40 3282-2700 Sales Assistance Wiebke Möller +49-(0)40 3282-2703 Barbara C. Effler (Head of Equities) Fiscal year ending 12/05 12/06 12/07e 12/08e 12/09e Key figures per share in EUR, all other in m. EUR, Price: 32,65 EUR Sales 6.4 10.7 18.0 25.6 32.1 Gross margin 92.2% 99.2% 99.0% 99.0% 99.0% EBITDA -1.5 2.0 4.3 7.2 9.6 EBITDA-margin -24.3% 18.9% 23.8% 28.0% 29.8% EBIT -1.6 1.9 4.2 7.0 9.3 EBIT-margin -25.6% 18.2% 23.0% 27.2% 29.0% Net Income -1.2 1.4 2.6 4.6 6.4 Operating Cash Flow -0.6 0.61 1.19 2.08 2.87 DPS 0.00 0.00 0.00 0.00 0.00 Dividend Yield 0.0% 0.0% 0.0% 0.0% 0.0% EV/Sales 8.09 4.81 2.86 2.02 1.61 EV/EBITDA n.m. 25.46 12.02 7.22 5.40 EV/EBIT n.m. 26.50 12.44 7.43 5.55 PER n.m. 53.52 27.44 15.70 11.38 ROCE -877.2% 187.6% 28.9% 24.1% 26.8% Adj. Free Cash Flow Yield -2.1% 2.6% 8.2% 13.7% 18.3%

Transcript of 30.07.2007 InVision Software AG Research Note fileVodafone, Deutsche Telekom or IKEA are testimony...

30.07.2007 InVision Software AG Research Note

SES Research GmbH – A Member of the Warburg Group Page 1

Buy Price target: EUR 40.0

(initial coverage) The ideal time to get the show on the road

InVision is a genuine pure play software provider for workforce management solutions (with royalties accounting for 57% of sales in 2006). The key strength of InVision’s solution lies in staffing requirement forecasts and the subsequent flexible optimisation of staff deployment. The software tackles mathematical optimisation issues that are extremely difficult to solve. Product specifications of this nature clearly set InVision apart from the competition and explain the com-pany’s strong growth. Over 180 clients, including top names such as Vodafone, Deutsche Telekom or IKEA are testimony to the high competitive quality of InVision’s solutions, which generally provide a return on investment within 6-12 months. InVision’s solutions allow its clients to:

• cut costs by reducing instances of excess cover,

• boost productivity by reducing instances of insufficient cover,

• increase employee satisfaction, for example by implementing flexible schedules that employees have a say in

Growth is driven primarily by: the replacement of proprietary sys-tems; a strong client pipeline; the broadening of market access to cover additional areas; the expansion of the company’s sales activi-ties and of the partner business; further internationalisation, taking the company onto the very dynamic international markets, and the planned strengthening of the company’s capital base as a growth catalyst.

In financial year 2006, InVision reported growth of around 70% and an EBIT margin of 18% (EUR 1.95 m). This means that the company’s operating result was boosted by EUR 3.6 m as against the prior-year, when it still reported a loss. This highlights a key issue for pure play software providers: InVision has completed the main development work for its product and has a strong client basis that guarantees regu-lar maintenance income. Further increases in sales will have a clearly above-average impact on the EBIT margin, with even this year’s figures expected to confirm this trend (extremely high scalability). As a result, we expect the EBIT margin to increase from 18.2% to 23.0% (EUR 4.15 m) in financial year 207, with sales growth of 68%. The figures for Q1/07 support this assumption.

On June 14, 2007, InVision was listed successfully at the stock exchange which will support further growth. The calculated valuation range for the share is EUR 38 to EUR 46. We initiate the coverage of InVision with the rating “BUY”. Our PT is EUR 40.

Bloomberg: IVX GR Price: 32.65Reuters: IVXG.DE Tech-All: 1091.79ISIN DE00585969 Internet: www.InVision.de Segment: Prime Standard Sector: Software

30,5

31

31,5

32

32,5

33

33,5

34

34,5

35

35,5

06/07 07/07 07/07

InVision Software Tech-All (relativ)

Share data: Bloomberg 27.07.2007 / Closing price High /Low 52 w: EUR 34.59 / 32.00Market cap. EUR 72.97 mNo. of shares: 2.24 m Shareholders: Peter Bollenbeck 17,00% Matthias Schroer 17,00% Armand Zohari 17,00%

InVision Holding GmbH 6,29% Free Float 4,71% Calendar: H1/2007 14.08.2007 Figures Q3/07 14.11.2007 Analysis: SES Research Publication: 30.07.2007Felix Ellmann (Analyst) +49-(0)40 309537-12 Institutional Client Contact: M.M.Warburg & CO

+49-(0)40 3282-2636Institutional Equity SalesChristian Alisch +49-(0)40 3282-2667Thomas Dinges +49-(0)40 3282-2635Matthias Fritsch +49-(0)40 3282-2696Dr. James F. Jackson +49-(0)40 3282-2664Oliver Jürgens +49-(0)40 3282-2666Benjamin Kassen +49-(0)40 3282-2630Marina Konzog +49-(0)40 3282-2669Linn Lenné +49-(0)40 3282-2695Dirk Rosenfelder +49-(0)40 3282-2692Marco Schumann +49-(0)40 3282-2665Andreas Wessel +49-(0)40 3282-2663Sales TradingOliver Merckel +49-(0)40 3282-2634Thekla Struve +49-(0)40 3282-2668Gudrun Bolsen +49-(0)40 3282-2679Nils Carstens +49-(0)40 3282-2701Jörg Treptow +49-(0)40 3282-2658Patrick Schepelmann +49-(0)40 3282-2700Sales AssistanceWiebke Möller +49-(0)40 3282-2703

Barbara C. Effler (Head of Equities)

Fiscal year ending 12/05 12/06 12/07e 12/08e 12/09e

Key figures per share in EUR, all other in m. EUR, Price: 32,65 EURSales 6.4 10.7 18.0 25.6 32.1Gross margin 92.2% 99.2% 99.0% 99.0% 99.0%EBITDA -1.5 2.0 4.3 7.2 9.6EBITDA-margin -24.3% 18.9% 23.8% 28.0% 29.8%EBIT -1.6 1.9 4.2 7.0 9.3EBIT-margin -25.6% 18.2% 23.0% 27.2% 29.0%Net Income -1.2 1.4 2.6 4.6 6.4Operating Cash Flow -0.6 0.61 1.19 2.08 2.87DPS 0.00 0.00 0.00 0.00 0.00Dividend Yield 0.0% 0.0% 0.0% 0.0% 0.0%EV/Sales 8.09 4.81 2.86 2.02 1.61EV/EBITDA n.m. 25.46 12.02 7.22 5.40EV/EBIT n.m. 26.50 12.44 7.43 5.55PER n.m. 53.52 27.44 15.70 11.38ROCE -877.2% 187.6% 28.9% 24.1% 26.8%Adj. Free Cash Flow Yield -2.1% 2.6% 8.2% 13.7% 18.3%

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 2

Company background InVision AG was formed in 1995. The two members of the company’s current Executive Board are also the company’s founders. The company is a pure play software provider with income components that are typical for this sector: royalties (57%), maintenance (22%) and services (21%). Over the past few years, the company has demonstrated strong growth, and was able to report top-line growth of around 70% in 2006 fol-lowing a year of consolidation in 2005. The EBIT margin climbed to just shy of 20%.

As a product provider, InVision offers unique technology for the optimisation of corporate staff deployment. The core ele-ment of this technology is a complex solution that can auto-matically produce rotas with a high degree of optimisation us-ing various optimisation procedures. The solutions are particu-larly valuable in sectors in which staff deployment optimisation on the basis of concrete requirements and demand forecasts is exceptionally important. As a result, InVision is active on a clear niche market that allows the company to generate high returns.

A large number of top-name clients show that InVision is a leader on this niche market. Its clients include absolute blue chips such as Deutsche Telekom, Vodafone, IKEA or freenet. In addition to attracting new clients, the expansion of the com-pany’s business with its existing clients alone offers enormous potential for InVision.

Competitive and business quality Personnel planning is a traditional field of activity in the IT sec-tor. Since this market is generally divided and the growth rates are only moderate in the industrialised nations, the only com-panies that can report strong growth are those that offer sub-stantially superior solutions for highly specific areas of applica-tion. This applies in InVision’s case.

InVision specialises in a specific personnel planning segment, namely the (mathematical) optimisation of staff development. There is considerable cost-cutting potential in this area through the implementation of optimisation solutions. Clear evidence of this potential can be provided to competitors and potential clients, because the solution to the optimisation prob-

InVision

2006 2007e 2008e 2009eFiscal year end 31.12.2006 31.12.2007 31.12.2008 31.12.2009

Sales 10,733 18,049 25,581 32,077change yoy 68.1% 68.2% 41.7% 25.4%Gross Profit 10,647 17,869 25,326 31,756in % of Sales 99.2% 99.0% 99.0% 99.0%EBITDA 2,029 4,296 7,155 9,559EBIT 1,949 4,151 6,950 9,302Net Income 1,374 2,648 4,643 6,407

Table 1; Source: SES Research

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 3

lems is a mathematical one, meaning that is very easy to jus-tify potential cost savings. Large users can generally expect a ROI within 6 to 12 months.

InVision has a leading position on the European market in terms of its core competency: optimisation. It is unlikely that the company’s US competitors will gain a stronger foothold in-ternationally and pose any real competitive threat to InVision in Europe, because they will be unable to build up comparable references in Europe in the short term, do not offer the multi-lingual service that is required within Europe and often lack fundamental, regional market knowledge.

On the whole, we believe that there is a positive market trend in the workforce management sector. The “optimisation” seg-ment is a sufficiently small niche on this market, which should allow InVision to gain market share and generate above-average growth as a result. Optimisation offers considerable and, most importantly, measurable potential for many compa-nies. We believe that more than 17 years of experience in the workforce management sector and an established, referenced solution that has allowed over 180 clients to generate a swift ROI are InVision’s main competitive strengths.

Sales and earnings growth Over the course of financial year 2006, InVision was able to demonstrate the massive earnings potential offered by the provision of pure play software for the first time. The company boosted its sales by 70% and drastically increased its net in-come for the year by more than EUR 2 m, taking it from a loss of EUR 1.25 m to a profit of EUR 1.37 m.

The sales growth seen in the previous financial year and the strong first quarter will produce a base effect in the first in-stance. Thereafter, further top-line growth will be driven by:

• solid market growth in the call centre and workforce management sector

• the replacement of proprietary systems, the majority of which only implement rudimentary optimisation measures

• a strong client pipeline, so far, only few of the possible fields of business/projects have been exploited for the ma-jority of the company’s clients.

• large pipeline of new potential clients, for which InVi-sion is participating in tenders or with which it is already running pilot projects

• broadening of market access to cover additional areas outside of the call centre business, often in cooperation with existing major clients

• expansion of sales activities and expansion of the part-ner business, which still offers considerable potential

• further internationalisation, taking the company onto the highly dynamic international markets, which increased their contribution to consolidated sales to 51% last year (+210% growth)

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 4

• the strengthening of the capital basis has the ability to act as a growth catalyst.

Earnings growth is determined primarily by the high scalabil-ity of income in the software licensing business. The following factors play a key role in explaining the bottom-line develop-ment:

• Reduction of key relative cost items (e.g. development, overheads, others). InVision’s product has already been developed. Further licence sales will now no longer be offset by development costs on a comparable scale to that seen in the past.

• Expansion of the partner business and, as a result, the realisation of higher margins due to a relatively high pro-portion of royalties

• Ongoing expansion of the installed base, and as a result, increase in maintenance income.

As a result, we have arrived at the following sales and earn-ings forecast:

Valuation The calculated valuation range of between EUR 38 m and EUR 46 m is based on the following valuation methods (under consideration of capital inflow of IPO, post-money):

• The adjusted Free Cash Flow Yield for 2008e points to-wards a fair value of EUR 41 m with substantial upside potential in subsequent years (2009e: EUR 52,20 m)

• The DCF model, based on a beta of 1.5, a risk-free rate of 4.09%, a WACC of 11.5% and a perpetual growth rate of 2% signals a value of EUR 38 m. Nevertheless, we expect

InVision - P&L

2006 2007e 2008e 2009e

Sales 10,733 18,049 25,581 32,077Change yoy 68.1% 68.2% 41.7% 25.4%

- thereof licenses 6,103 10,387 15,093 18,279- thereof maintenance 2,347 3,549 5,145 7,214- thereof services 2,283 4,113 5,343 6,584

Total Sales 10,733 18,049 25,581 32,077

Gross Profit 10,647 17,869 25,326 31,756in % of Total Sales 99.2% 99.0% 99.0% 99.0%

EBIT 1,949 4,151 6,950 9,302

Net Income 1,374 2,648 4,643 6,407Change yoy n.m. 92.7% 75.3% 38.0%in % of Total Sales 12.8% 14.7% 18.1% 20.0%

Table 2; Source: SES Research

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 5

the margin to drop in the long term and also predict a con-siderable slowdown in growth (market saturation).

This valuation approach is supported by three peer groups (comparison on EV basis, the calculated fair values include net financial item:

• The comparison with listed German pure play software providers indicates an EV of EUR 40 m (2007 EV/EBIT)

• The comparison with listed US competitors points towards an EV of EUR 42 m (2007 EV/EBIT)

• The comparison with transaction multiplies for takeovers in the sector indicates an EV of EUR 46 m (2007 EV/EBIT).

Newsflow We expect InVision to report considerable sales growth and a clearly above-average increase in earnings this year. The fourth quarter, which is traditionally strong in this sector, should provide particular momentum.

The most recent transactions executed by US peer companies have had a positive effect on the valuation. InVision should also continue to benefit from this.

In the medium term, the company could even make a number of smaller acquisitions, which could also raise InVision’s pro-file.

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 6

IT in personnel planning

Personnel planning is a traditional field of activity in the IT sec-tor. Staff planning and time management (the recording, struc-turing and processing of personnel-relevant data) is already offered by a large number of companies (e.g. ATOSS). ERP software providers (e.g. SAP), providers of access control sys-tems (e.g. Primion) or payroll system providers (e.g. P&I) also work in the segments of this market that are relevant to per-sonnel planning, at least in part.

Since this market is generally divided and the growth rates are now only moderate in the industrialised nations, the only com-panies that can report strong growth are those that have spe-cialised in particular market segments and offer substantially superior solutions in these segments. This applies in InVi-sion’s case.

The InVision solution

InVision specialises in a highly specific segment of personnel planning, namely the optimisation of personnel deployment in certain segments that fulfil the following two core require-ments:

• Personnel requirements can be easily forecasted and, where appropriate, can be tracked via models (e.g. call centres)

• Personal deployment is considerable, meaning that rela-tively minor optimisation successes can have a relatively large impact in terms of savings (large clients)

If these two requirements are met, the use of optimisation so-lutions can produce substantial cost-cutting potential. After all, while any switch from manual to IT-based personnel deploy-ment optimisation (using solutions produced by the company’s competitors) could reduce costs in principle, InVision’s highly complex mathematical optimisation methods produce results that, according to information released by the company itself, outperform those offered by the competition.

Where it is possible to plan and forecast personnel deploy-ment as precisely as possible, InVision supplies the required methods and results. The subsequent optimisation of per-sonnel deployment is generally greater than the sort of optimi-sation that the company’s competitors could offer.

This means that there is considerable demand for InVision’s solutions, particularly among large clients. While these clients already optimise their personnel deployment, InVision allows them to further increase the extent of optimisation. The larger the systems, the higher the absolute cost savings as a result of relatively small optimisation measures. This is why there is particular demand for InVision’s solutions among large clients.

InVision’s solutions allow clients to deploy personnel in an ef-fective manner and, as a result, to achieve the following in particular:

• To cut costs but reducing instances of excess cover,

ROI value drivers

Increased operating performance

Reduction in operating costs• Fewer instances of excess coverage and surcharges

Lower personnel costs

• Automation of workflows and calculationsLower form and process costs

• Integration of employees into planning processReduced recruitment and training costs

• Fewer instances of insufficient coverageMore sales thanks to better service

Chart 1; Source: InVision

ROI value drivers

Increased operating performance

Reduction in operating costs• Fewer instances of excess coverage and surcharges

Lower personnel costs

• Automation of workflows and calculationsLower form and process costs

• Integration of employees into planning processReduced recruitment and training costs

• Fewer instances of insufficient coverageMore sales thanks to better service

Chart 1; Source: InVision

Client benefits

Company management, operations, finance and management accounting

Reduzierung der Betriebskosten

• Increased operating performance

• Lower personnel costs

• Increased productivity and motivation

• Faster and better decisions

• Lower administrative costs

Employees• Better work/life balance

• Interesting work

• More fairness

Personnel department• Standard tasks automated to a considerable degree

• Reduction of fluctuations

IT department• Lower IT costs

• Simple administration

• Comprehensive expandability

Chart 2; Source: InVision

Client benefits

Company management, operations, finance and management accounting

Reduzierung der Betriebskosten

• Increased operating performance

• Lower personnel costs

• Increased productivity and motivation

• Faster and better decisions

• Lower administrative costs

Employees• Better work/life balance

• Interesting work

• More fairness

Personnel department• Standard tasks automated to a considerable degree

• Reduction of fluctuations

IT department• Lower IT costs

• Simple administration

• Comprehensive expandability

Client benefits

Company management, operations, finance and management accounting

Reduzierung der Betriebskosten

• Increased operating performance

• Lower personnel costs

• Increased productivity and motivation

• Faster and better decisions

• Lower administrative costs

Employees• Better work/life balance

• Interesting work

• More fairness

Personnel department• Standard tasks automated to a considerable degree

• Reduction of fluctuations

IT department• Lower IT costs

• Simple administration

• Comprehensive expandability

Chart 2; Source: InVision

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 7

• To boost productivity by reducing instances of insuf-ficient cover,

• To increase employee satisfaction, for example by implementing flexible schedules that employees have a say in, the “Infothek” (info centre) principle (employ-ees can set, plan and exchange working hours them-selves).

Users can generally achieve a ROI within 6 to 12 months. The solution also offers further key advantages such as the reduc-tion of planning costs and increased employee flexibility (see box on the left).

Although the high degree of specialisation clearly limits this field of business, it nevertheless explains why InVision is growing at a considerably faster rate than its competitors.

References as a competitive advantage

In the software sector, references are a key competitive ad-vantage. They underline the quality of the solution and justify its cost-effectiveness. This is explained using a few projects as examples:

InVision has a total of more than 180 clients in 19 countries. The following table provides an overview of references (ex-cerpt):

Invision’s clients (excerpt)

Banks

• Postbank• Sparda-Bank• RBS• ABN AMRO• ...

Insurance companies

• AXA• Allianz• AOK• ...

Telecommunications

• Deutsche Telekom• Vodafone• Swisscom• ...

Energy

• Eon• Vattenfall• RheinEnergie• EnBW• ...

Other

• BMW• IKEA• NORDSEE• ...

Chart 4; Source: InVision AG

Invision’s clients (excerpt)

Banks

• Postbank• Sparda-Bank• RBS• ABN AMRO• ...

Insurance companies

• AXA• Allianz• AOK• ...

Telecommunications

• Deutsche Telekom• Vodafone• Swisscom• ...

Energy

• Eon• Vattenfall• RheinEnergie• EnBW• ...

Other

• BMW• IKEA• NORDSEE• ...

Chart 4; Source: InVision AG

Royal Automobile Club ABN AMRO Freenet customer care AG

- - -

Royal Automobile Club, UKMore than 4,500 employees24-hour service for over 6 m members 6

--

Financial services provider, NLMore than 110,000 employees worldwide

-

-

Internet and telecommunicationsproviderm GermanyOver 1 m broadband clients

InVision solution - Deployment optimisation in the following areas: road-side assistance, breakdown assistance & call centre

- Deployment optimisation and analysisand monitoring for approx. 1,200 employes in 5 service centres

- Deployment optimisation, time management and employee integration for more than 1,000 service centre employees

Client benefit -

-

16% increase in operating performance , corresponds to annual savings of GBP 1.3 mCoverage of 56 planning rules, thereof 32 fairness guidelinesPlanning input reduced by 90%

-

-

Personnel costs cut by 7.5%Planning input reduced by over 50%

-

-

-

The extent to which employee wishes are fulfilled(i.e. employees can choose their own working hours) averages between 70% and 85%Fewer employees call in sick due to unwanted working hoursLess fluctuation

Chart 3; Source SES Research

InVision - reference projects

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 8

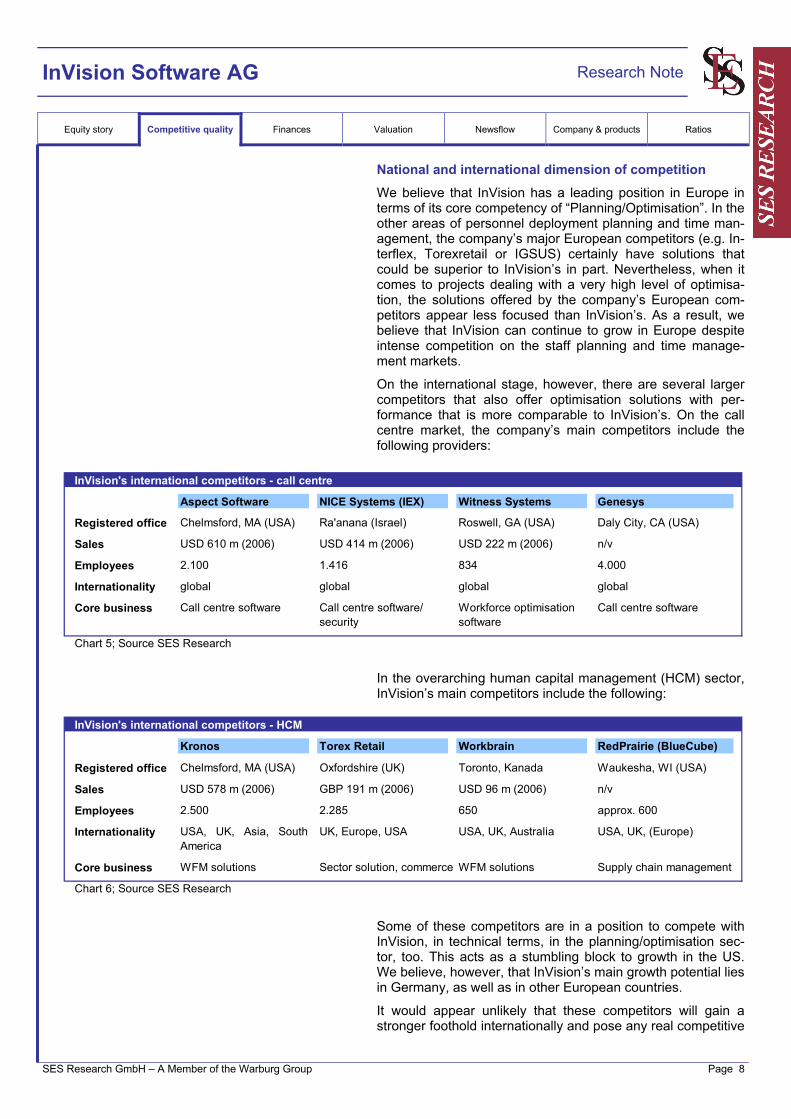

National and international dimension of competition

We believe that InVision has a leading position in Europe in terms of its core competency of “Planning/Optimisation”. In the other areas of personnel deployment planning and time man-agement, the company’s major European competitors (e.g. In-terflex, Torexretail or IGSUS) certainly have solutions that could be superior to InVision’s in part. Nevertheless, when it comes to projects dealing with a very high level of optimisa-tion, the solutions offered by the company’s European com-petitors appear less focused than InVision’s. As a result, we believe that InVision can continue to grow in Europe despite intense competition on the staff planning and time manage-ment markets.

On the international stage, however, there are several larger competitors that also offer optimisation solutions with per-formance that is more comparable to InVision’s. On the call centre market, the company’s main competitors include the following providers:

In the overarching human capital management (HCM) sector, InVision’s main competitors include the following:

Some of these competitors are in a position to compete with InVision, in technical terms, in the planning/optimisation sec-tor, too. This acts as a stumbling block to growth in the US. We believe, however, that InVision’s main growth potential lies in Germany, as well as in other European countries.

It would appear unlikely that these competitors will gain a stronger foothold internationally and pose any real competitive

InVision's international competitors - call centre

Aspect Software NICE Systems (IEX) Witness Systems Genesys

Registered office Chelmsford, MA (USA) Ra'anana (Israel) Roswell, GA (USA) Daly City, CA (USA)

Sales USD 610 m (2006) USD 414 m (2006) USD 222 m (2006) n/v

Employees 2.100 1.416 834 4.000

Internationality global global global global

Core business Call centre software Call centre software/security

Workforce optimisation software

Call centre software

Chart 5; Source SES Research

InVision's international competitors - HCM

Kronos Torex Retail Workbrain RedPrairie (BlueCube)

Registered office Chelmsford, MA (USA) Oxfordshire (UK) Toronto, Kanada Waukesha, WI (USA)

Sales USD 578 m (2006) GBP 191 m (2006) USD 96 m (2006) n/v

Employees 2.500 2.285 650 approx. 600

Internationality USA, UK, Asia, SouthAmerica

UK, Europe, USA USA, UK, Australia USA, UK, (Europe)

Core business WFM solutions Sector solution, commerce WFM solutions Supply chain management

Chart 6; Source SES Research

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 9

threat to InVision in Europe. This is because the company’s international competitors are flawed by typical weaknesses:

• They do not have any comparable references in Europe,

• They do not offer any comparable multilingual ser-vices, which are required on the European market,

• The complex and highly diverse employment law situation in Europe is often underestimated and

• The US competitors often lack fundamental under-standing of the differences in European working prac-tices, remuneration, etc.

As a result, we believe that US competitors only pose a very limited threat.

All in all, we therefore believe that InVision is well focused and that its chosen specialisation makes sense in a comparison with its competitors.

Optimisation niche market as a selling point and growth driver

We believe that there is a positive market trend in the work-force management sector on the whole. “Optimisation” is a sufficiently small niche in this sector, which should allow InVi-sion to continue to gain market share and, as a result, gener-ate above-average growth. Optimisation offers considerable and, most importantly, measurable potential for many compa-nies. We believe that InVision’s key strength in the competitive environment lies in its 17 years of experience in the workforce management sector and an established, referenced solution that has allowed over 180 clients to generate a swift ROI.

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 10

Recent performance In financial year 2006, InVision boosted its sales by 70% and drastically increased its earnings, which rose by more than EUR 2 m from EUR –1.25 m to EUR 1.37 m. This trend con-tinued in Q1.

Compared to the previous year sales almost doubled in Q1, while earnings increased by EUR 0.6 m from EUR-0.9 m to EUR-0.3 m. The fact that earnings remained in the red is nor-mal for the sector. Q2 and Q4 are normally the strong quarters for licence-driven business models. We expect InVision to generate just under 60% of its income in the fourth quarter alone.

Although the first quarter is generally of limited informational value for the year as a whole, two key points are worth noting. Sales doubled year-on-year. The assumption that this trend will continue is explained below. We expect to see sales in-crease by 68% in this financial year.

Earnings improved by EUR 0.6 m year-on-year. If we extrapo-late this improvement, our forecast of a EUR 2.2 m increase in earnings in 2007 appears absolutely justified and borders on the conservative. If we assume further, realistic economies of scale in the course of the year, our forecast would appear to be too low.

In the first two quarters, preparations for the raising of capital had a negative impact on earnings. This measure is expected to start bearing fruit in the second half of the year.

On the whole, we believe that the first quarter supports our earnings forecast.

InVision - Q1/2007Q1/07 Q1/06 change yoy 2007e 2006 change yoy

Sales 2,645 1,360 94.4% 18,049 10,733 68.2%

Total Sales 2,645 1,360 94.4% 18,049 10,733 68.2%

Gross Profit 2,614 1,331 96.5% 17,869 10,647 67.8%in % of Total Sales 98.8% 97.8% 99.0% 99.2%

EBIT -289 -846 65.91% 4,151 1,949 113.0%in % of Total Sales -10.9% -62.2% 23.0% 18.2%

Net Income -122 -958 87.2% 2,648 1,374 92.7%in % of Total Sales -4.6% -70.4% 14.7% 12.8%

Table 3; Source: SES Research

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 11

Growth in sales Any assessment of sales growth must first of all differentiate between the three types of sales:

Licence sales (one-off licence fee for unlimited use, in terms of both location and timeframe) lie at the core of any software company and should increase further in line with successful sales activities. Existing client relationships act as a catalyst in this respect (subsequent licences and expansion of sales to cover other business areas of major clients).

Service sales form the basis for the licensing business, be-cause each project has a set service requirement (mainly im-plementation and training). The fact that the company’s ser-vices are performed by its own employees means that these sales are not as scalable as the licence sales. The latter can also be boosted by strong partner business, as well as by subsequent or new licences.

Maintenance sales result directly from the licences sold (in-stalled base). They amount to 15% of the respective installed basis per year, depending on the licence amount.

Top-line growth will be supported by:

• solid market growth

• the replacement of proprietary systems

• strong client pipeline

• broadening of market access

• expansion of sales activities and expansion of the partner business

• internationalisation

• possible strengthening of the capital base as a growth catalyst

InVision - Sales per brand

2006 2007e 2008e 2009e

Sales 10,733 18,049 25,581 32,077Change yoy 68.1% 68.2% 41.7% 25.4%

Licenses 6.103 10.387 15.093 18.279Change yoy 121,0% 70,2% 45,3% 21,1%in % of Sales 56,9% 57,5% 59,0% 57,0%

Maintenance 2.347 3.549 5.145 7.214Change yoy 6,2% 51,2% 45,0% 40,2%in % of Sales 21,9% 19,7% 20,1% 22,5%

Services 2.283 4.113 5.343 6.584Change yoy 61,4% 80,2% 29,9% 23,2%in % of Sales 21,3% 22,8% 20,9% 20,5%

Table 4; Source: SES Research

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 12

Solid market growth

In principle, the market for human capital management sys-tems is believed to offer high growth potential. According to AMR, the global market is expected to grow by 10% a year, reaching a volume of USD 8.7 bn in 2010.

In the call centre systems sector, workforce management sys-tems are standard. In addition to the growth of the call centre market, growth is expected to come from system profession-alization, as many companies are still using outdated technol-ogy for optimisation purposes (e.g. EXCEL files).

Datamonitor expects the “Workforce Optimisation Technology” market to display annual growth of 12.1%, reaching a volume of USD 1.4 bn in 2009. The workforce management sub-segment is expected to chart annual growth of 10.1% and ac-count for USD 366 m in 2009.

Frost & Sullivan expects market growth in the segment for workforce management solutions for call centres totalling 13.7% annually and reaching USD 433 m in 2010. The firm expects the EMEA market share to increase to 30% of the global market, producing a significantly higher growth rate of 20.5% p.a. on this particular market. This is due to the fact that the market for solutions of this nature has yet to undergo liberalisation in Europe. InVision's main comparable competi-tors originate from the US, and we believe that the company occupies a unique position in Europe.

InVision is considerably outperforming the market in terms of growth. Over the past few years, the company has grown by around 30% p.a. Last year, sales grew by as much as almost 70%.

Similarly, in addition to base effects due to InVision’s small size, there are a number of key growth drivers that have fos-tered, and will continue to foster substantial growth at InVi-sion:

Replacement of proprietary systems

Particularly in Europe, the workforce management market is characterised to a considerable degree by proprietary or very straightforward systems. Often, smaller call centres still per-form manual optimisation. Furthermore, optimisation is still seen as being less important than advanced time manage-ment and personnel planning systems. This means that there is still considerable potential for optimisation using profes-sional solutions as far as the replacement of sub-optimum systems is concerned. This market structure, which is advan-tageous for InVision, represents a key growth driver which, in our view, is actually more important to the company than mar-ket growth itself. This is because InVision’s systems are usu-ally employed during a later investment cycle, namely when the company in question has already set up the infrastructure, when the latter is up and running, and when the company starts asking questions with respect to improved optimisation.

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 13

Strong client pipeline

As mentioned above, InVision has over 180 clients. Follow-up business is a key pillar of InVision’s business model. This is highlighted in the following examples:

These projects show how much potential still lies in InVision’s client base. The company should be able to exploit this poten-tial at a relatively low marketing cost. In this respect, one fac-tor that is particularly important is that InVision has been fo-cusing on large clients for several years now and is expending the business areas with these clients from merely call centres, to cover other areas with similar requirements. This is particu-larly relevant with respect to a client like IKEA. This issue will be examined in further detail in the next section.

Broadening of market access

In principle, workforce management solutions can be em-ployed in a whole range of sectors and business areas, pro-vided that the necessary conditions for planning and optimisa-tion (see above) are met. Although InVision has its roots in the call centre market, the relative proportion of sales attributable to this segment has fallen over the past few years (although the proportion is on the rise in absolute terms). This shows that the solution can obviously also work well in sectors out-side of the call centre industry. The chart below shows the ar-eas which could act as potential business areas for InVision (the areas in boxes have been localised as target markets):

Share of call centre projects in total sales

in %

0

10

20

30

40

50

60

70

80

90

100

2004 2005 2006 2007e

Call Center Projekte Andere Projekte

Chart 8; Source: InVision

Deutsche Telekom (T-Mobile) Mannesmann Mobilfunk IKEA

The German mobile telephony provider uses an InVision solution for 1,500 call centre employees

The German mobile telephony provider uses an InVision solution for 2,500 call centre employees

IKEA Germany uses anInVision solution for 100 call centre employees.

Follow-up business Follow-up business Follow-up businesswith international group subsidiariesand equity interests

- New areas: T-Com VC, T-Com TK - Vodafone Omnitel (Italy) - IKEA International- Upgrades to release 4 ar T-Mobile, T-Com - SFR/Cegetel (France) - 50,000+ employees- International group subsidiaries: T-Mobile AT,

HT Telecom, Htmobile--

Swisscom Mobile (Switzerland)Safaricom (Kenya)

--

100+ home furnishings stores in 11 countriesVarious international call centres

- Domestic group subsidiaries: Vivento Customer Services

--

Various international logistics centresFunctional scope: requirement forecasting,

- Expansion of area of application: back office deployment optimisation, time management- Functional expansion:

Capacitor, TrainingPlannerand analysis and monitoring

- Client-specific developments: SAP integration, data warehouseinterface, among others

- Increase in benefits due to various subsequent user licence purchases

Chart 7; Source: InVision

InVision's reference clients

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 14

We believe that the expansion of market access also consti-tutes a key top-line growth driver. In the first instance, this re-lates to the commerce, transport and logistics.

Expansion of sales activities and the partner business

One key factor for pure play software providers is whether or not they can manage to focus on licence sales without having to provide the associated, low-margin services themselves, meaning that they can focus on further developing their solu-tions. Implementation partners that can perform this work within the framework of the company’s projects are merely supplied with software licences, which is very attractive for In-Vision from a margin point of view.

At present, the company works with the following partners:

Business model

Other

Transport & logistics

Wholesale & retail

Supply & waste management

Telecommunications

Financial services providers

Sector

External salesProductionLogistics

Sales organisationBack officeCall centres

Area of application

Sales focus “call centres“ and “back office”

Sales focus “retail”

Sales focus “transport & logistics”

Chart 9; Source: InVision

Ideal conditions for deployment optimisation Good conditions for deployment optimisation

Business model

Other

Transport & logistics

Wholesale & retail

Supply & waste management

Telecommunications

Financial services providers

Sector

External salesProductionLogistics

Sales organisationBack officeCall centres

Area of application

Sales focus “call centres“ and “back office”

Sales focus “retail”

Sales focus “transport & logistics”

Chart 9; Source: InVision

Ideal conditions for deployment optimisation Good conditions for deployment optimisation

Business model

Other

Transport & logistics

Wholesale & retail

Supply & waste management

Telecommunications

Financial services providers

Sector

External salesProductionLogistics

Sales organisationBack officeCall centres

Area of application

Sales focus “call centres“ and “back office”

Sales focus “retail”

Sales focus “transport & logistics”

Chart 9; Source: InVision

Ideal conditions for deployment optimisation Good conditions for deployment optimisation

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 15

Sales by region in million EUR

0

2

4

6

8

10

12

2004

2005

2006

DACH ROW

Chart 11; Source: InVision

These partners are involved in InVision’s projects, which ex-plains the high contribution made by licence sales and the relatively low service sales. InVision has already stated that expanding its partner business is one of its objectives, be-cause at present, its partners still do not generate their own leads (client acquisitions) and InVision does not pur-sue any active partner management policy. This offers considerable potential. This issue is to be tackled and should result in additional sales growth, along with above-average margins.

Internationalisation

The reorientation of the company’s sales activities in 2004/05 to focus on major international clients, company-wide work-force management and management restructuring (account managers were entrusted with managerial duties) reduced the company’s sales activities in the Germany/Austria/Switzerland (GAS) region (decline in sales in 2005: –12%). The strategic shift, as well as the establishment of increased sales capacity considerably boosted sales in 2006, particularly abroad. In the GAS region, sales grew by 12%, while they increased by 210% in the rest of the world (ROW). Foreign markets (ROW) now account for 51% of consolidated sales.

The fact that the market momentum for the company’s foreign business is far higher than in Germany and that the contribu-tion made to total sales already stands at above 50% following spectacular growth rates shows the enormous potential that internationalisation offers for top-line growth.

Implementation partners

Type of resources

• Application consultants

• Software developers

• Application consultants

• IT consultants

• Application consultants

• Application consultants

• Application consultants

• Application consultants

Deployment regions

FR, IT, NL, NO, SE, ES,

PL, RU, UK, US

UK, FR, MA

FR, DE, PL

IT

South America

Chart 10; Source: InVision

Implementation partners

Type of resources

• Application consultants

• Software developers

• Application consultants

• IT consultants

• Application consultants

• Application consultants

• Application consultants

• Application consultants

Deployment regions

FR, IT, NL, NO, SE, ES,

PL, RU, UK, US

UK, FR, MA

FR, DE, PL

IT

South America

Chart 10; Source: InVision

Implementation partners

Type of resources

• Application consultants

• Software developers

• Application consultants

• IT consultants

• Application consultants

• Application consultants

• Application consultants

• Application consultants

Deployment regions

FR, IT, NL, NO, SE, ES,

PL, RU, UK, US

UK, FR, MA

FR, DE, PL

IT

South America

Chart 10; Source: InVision

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 16

Possible strengthening of the capital base as a growth catalyst

We believe that the strengthening of InVision’s capital base should have an above-average impact on the company’s suc-cess:

• The technology is developed and established, any moves to step up the company’s sales activities should have a very clear impact on earnings (scaling). To put things simply: once the technology has been developed, each additional licence sold = profit.

• The same applies to the rapid adaptation of the prod-uct to suit other segments. Here, too, the company can enter into new fields of activity at a low adaptation cost and the situation set out above applies by means of analogy.

• In the medium term, we could also see the company acquiring implementation competence. This would also produce considerable up-selling potential.

• The improvement of the company’s balance sheet quality is also advantageous in terms of its external image.

Strong sales growth justified

The factors set out above highlight the fact that InVision should be able to display strong sales growth in the future.

Earnings growth With average annual top-line growth for the period 2006-2009 of 44%, we expect to see an above-average increase in the operating result. The above-average nature of this increase is due, in our view, to the company’s licence-driven business model.

The following factors largely explain the bottom-line develop-ment:

• Below-average development in key cost positions (e.g. development, overheads, other), i.e. these fall in relation to sales

• The expansion of the partner business and the asso-ciated increase in margins due to a higher proportion of licence sales in relative terms

• The ongoing expansion of the installed base and, as a result, of the high-margin recurring maintenance in-come

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 17

Personnel expenses in million EUR, as a % of sales

0

2

4

6

8

10

12

14

2004

2005

2006

2007

e

2008

e

2009

e

30,0%

40,0%

50,0%

60,0%

70,0%

80,0%

Chart 12; Source: InVision

Other operating expenses in million EUR, as a % of sales

0

2

4

6

8

10

2004

2005

2006

2007

e

2008

e

2009

e

20,0%

30,0%

40,0%

50,0%

Chart 13; Source: InVision

Maintenance fees in million EUR, as a % of sales

0

2

4

6

8

2004

2005

2006

2007

e

2008

e

2009

e

10,0%

20,0%

30,0%

40,0%

50,0%

Chart 14; Source: InVision

Below-average increase in cost items vis-à-vis sales

Personnel expenses and other operating expenses are by far InVision’s main cost items. This means that both of these items have the greatest impact on the bottom line.

Personnel expenses

Personnel expenses have increased considerably over the past few years. In the restructuring year, 2005, which saw key structural changes within the company (see above) the ratio increased considera-bly. In 2006, personnel expenses returned to a normal ratio of 53% and are expected to decrease further (2009e: 44%).

51% of personnel expenses are attributable to devel-opment, 26% to services, 16% to sales and 7% to other areas. The high development expense, in par-ticular, is expected to fall in relation to sales. The pro-portion of expenses relating to services is likely to re-main constant on the back of a steady project flow. The fact that the only 16% of the company’s person-nel expenses are attributable to sales, and that it is nevertheless reporting strong growth, shows just how much potential is offered by the expansion of this area. We therefore expect sales and marketing costs to increase slightly in relation to sales, which means a considerable increase in absolute terms.

The personnel expense ratio on the whole, however, is likely to fall due to the expectations of high top-line growth.

Other operating expenses

Other operating expenses consist primarily of rental, marketing, travel and vehicle costs. In this case, too, we expect to see a decline in costs in relation to sales.

Both cost items are impacted by a key effect. It is estimated that InVision can already generate around 50% of its business with its existing clients. Only 20% of the company’s sales po-tential has been exploited for 80% of its clients (estimates).

Expansion of the partner business

The section above (top line growth) mentioned that the partner business should have a positive impact on sales. The impact on earnings, however, is much greater. This is because a functional partner business means:

• Lead generation by the partner (hardly any sales ex-pense for InVision)

• Services provided by the partner (no personnel ex-penses relating to services for InVision)

• Considerable increase in royalties, which has a direct impact on earnings.

At present, only 30-45% of projects are implemented with the help of partners, which still do not generate leads. The im-provement of its partner business is one of InVision’s strategic

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 18

EBIT in million EUR, as a % of sales

-4,00

-2,00

0,00

2,00

4,00

6,00

8,00

10,00

12,00

2004

2005

2006

2007

e

2008

e

2009

e

-30,0%

-20,0%

-10,0%

0,0%

10,0%

20,0%

30,0%

Chart 15; Source: InVision

objectives. We believe that this strategy offers considerable earnings potential (this has not yet been explicitly accounted for in our pre-money scenario).

Ongoing expansion of the installed base and, as a result, maintenance income

Maintenance income continues to rise at InVision. In the first instance, this income charts slower growth than licence sales, because it follows the latter. 15% of the installed base/licences can be booked as annual maintenance income. We believe that in as early as 2009, maintenance income alone will cover the company’s development costs in full. In principle, the installed base can be seen as a hidden re-serve at software companies.

Earnings situation

In financial year 2006, InVision was able to demonstrate the massive earnings potential offered by a pure play software provider for the first time. The company boosted its sales by 70% and drastically increased its earnings, which rose by more than EUR 2 m from EUR-1.25 m to EUR 1.37m. Accord-ing to our estimates and on the basis of these factors, the earnings situation is as follows:

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 19

The balance sheet InVision’s balance sheet (Q1/2007) can be explained quickly and briefly. Its assets consist more or less exclusively of re-ceivables (trade receivables, 60% of total assets) and de-ferred tax assets (30% of total assets). InVision has not

InVision - P&L

2006 2007e 2008e 2009e

Sales 10,733 18,049 25,581 32,077Change yoy 68.1% 68.2% 41.7% 25.4%

- thereof licenses 6,103 10,387 15,093 18,279- thereof maintenance 2,347 3,549 5,145 7,214- thereof services 2,283 4,113 5,343 6,584

Changes in Inventory / Other 0 0 0 0

Total Sales 10,733 18,049 25,581 32,077Change yoy 68.1% 68.2% 41.7% 25.4%

Material Expenses 86 180 256 321Change yoy -82.8% 110.7% 41.7% 25.4%in % of Total Sales 0.8% 1.0% 1.0% 1.0%

Gross Profit 10,647 17,869 25,326 31,756in % of Total Sales 99.2% 99.0% 99.0% 99.0%

Other Operating Income 138.5 361.0 511.6 641.5Change yoy -59.9% 160.6% 41.7% 25.4%in % of Total Sales 1.3% 2.0% 2.0% 2.0%

Personnel Expenses 5,742 8,700 11,519 14,178Change yoy 15.3% 51.5% 32.4% 23.1%in % of Total Sales 53.5% 48.2% 45.0% 44.2%

Depreciation 80 144 205 257Change yoy -3.1% 80.2% 41.7% 25.4%in % of Total Sales 0.7% 0.8% 0.8% 0.8%

Other Operating Expenses 3,014 5,234 7,163 8,661Change yoy 7.6% 73.7% 36.8% 20.9%in % of Total Sales 28.1% 29.0% 28.0% 27.0%

EBIT 1,949 4,151 6,950 9,302Change yoy n.m. 113.0% 67.4% 33.8%in % of Total Sales 18.2% 23.0% 27.2% 29.0%

Financial Result -68 -620 -760 -760

EBT 1,881 3,531 6,190 8,542Change yoy n.m. 87.7% 75.3% 38.0%in % of Total Sales 17.5% 19.6% 24.2% 26.6%

Taxes 454 883 1,548 2,136Tax Rate 24.1% 25.0% 25.0% 25.0%

Net Income 1,374 2,648 4,643 6,407Change yoy n.m. 92.7% 75.3% 38.0%in % of Total Sales 12.8% 14.7% 18.1% 20.0%

Table 5; Source: SES Research

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 20

capitalised its own software, which produces a massive hidden reserve.

90% of the liabilities side of the balance sheet comprises cur-rent liabilities. The majority of these liabilities are deferred charges and prepaid expenses (maintenance) and trade pay-ables.

Equity is low at only EUR 174,000 and the current liabilities to banks of EUR 0.8 m considerably exceed the company’s cash and cash equivalents. At present, this means that the balance sheet is in a critical state and it would certainly make sense for the company to raise further capital.

We believe that this is the mark left by the high growth that InVision generated in 2006. Furthermore, InVision has spent a lot of capital on software development over the past few years. A certain amount of debt financing has proven to have made sense from a strategic point of view and is bound to have been more valuable to InVision than the superficial ap-pearance of its balance sheet.

On June 14, 2007 InVision was listed successfully at the stock exchange. The InVision share is allocated at EUR 32.00. The 1.077.000 InVision shares were placed successfully. Including greenshoe the issue volume was EUR 34.5 m. The company accrued gros roughly EUR 22.9 m. Thus, the company is ab-solutely adequate capitalised and the mentioned weakness is eliminated.

Balance sheet InVision

Balance sheet (in EUR m) 2005 2006 2007e 2008e 2009e

ASSETS

Long-Term Assets 0.1 0.1 0.2 0.2 0.2

Current Assets 2.3 5.6 30.0 35.3 42.5

Total Assets 2.4 5.7 30.1 35.5 42.7

LIABILITIES AND SHAREHOLDERS' EQUITY

Total Equity -1.1 0.2 24.0 28.6 35.0

Minority Interest 0.0 0.0 0.0 0.0 0.0

Provisions 0.4 1.3 1.5 1.8 2.2

Total Liabilities 3.5 5.5 6.2 6.9 7.7

Total Liabilites and Shareholders' Equity 2.4 5.7 30.1 35.5 42.7

Table 6; Sources: InVision (reported data), SES Research (estimates)

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 21

Balance sheet InVision

Balance sheet (in % of Balance Sheet Total) 2005 2006 2007e 2008e 2009e

ASSETS

Long-Term Assets 6.2% 2.5% 0.5% 0.5% 0.5%

Current Assets 93.8% 97.5% 99.5% 99.5% 99.5%

Total Assets 100.0% 100.0% 100.0% 100.0% 100.0%

LIABILITIES AND SHAREHOLDERS' EQUITY

Total Equity -46.8% 4.2% 79.5% 80.5% 82.0%

Minority Interest 0.0% 0.2% 0.0% 0.0% 0.0%

Provisions 15.5% 22.2% 5.0% 5.1% 5.1%

Total Liabilities 146.8% 95.7% 20.4% 19.4% 18.0%

Total Liabilites and Shareholders' Equity 100.0% 100.0% 100.0% 100.0% 100.0%

Table 6; Sources: InVision (reported data), SES Research (estimates)

The cash flow statement Our basic scenario assumes that additional working capital will be required to generate further growth. The expected cash flow shows that it would make sense for the company to raise additional capital (as set out above)

Statement of Cash Flows InVision

Statement of Cash Flows (in EUR m) 2005 2006 2007e 2008e 2009e

Cash Flow -1.7 1.9 3.0 5.2 7.0

Cash Flow from Operating Activities -0.3 -0.3 1.0 3.0 5.2

Cash Flow from Investing Activities -0.1 -0.1 -0.2 -0.2 -0.3

Cash Flow from Financing Activities 0.4 0.4 21.1 0.0 0.0

Net Changes of Cash and Cash Equivalents 0.0 0.0 21.9 2.8 4.9

Cash and Cash Equivalents, end of period 0.1 0.1 22.0 24.8 29.7

Table 7; Sources: InVision (reported data), SES Research (estimates)

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 22

Valuation range The range of EUR 38 m to EUR 46 m is based on the follow-ing valuation methods (under consideration of capital inflow of IPO, post-money):

• The adjusted free cash flow yield 2008e points towards a fair value of EUR 41 m with substantial upside potential in subsequent years (2009e: EUR 52.20 m)

• The DCF model, based on a beta of 1.5, a risk-free rate of 4.09%, WACC of 11.5% and a perpetual growth rate of 2%, points towards a value of EUR 38 m. Here, however, we expect to see a drop in the margin in the long term and a very substantial growth slowdown (market saturation).

The valuation approach is underlined by three peer groups (comparisons based on EV, the calculated fair values include net financial items):

• The comparison with German pure play software provid-ers points towards an EV of EUR 40 m (2007 EV/EBIT)

• The comparison with US competitors suggests an EV of EUR 42 m (2007 EV/EBIT)

• The comparison with transaction multiples for takeovers in the sector indicates an EV of EUR 46 m (2007 EV/EBIT)

We believe that a post-money valuation of EUR 40 m is ap-propriate for InVision, because this valuation takes account of the fact that earnings visibility remains low at present.

Free cash flow yield Our adjusted free cash flow yield is based on the assumption that investors buy an asset (in this case, the enterprise value) at a price that means that the free cash flow return (free cash flow = net income for the year + depreciation and amortisation - maintenance capex + taxes - (1-t) interest) on the EV ex-ceeds the opportunity costs. In order to simplify matters, we have based our assumptions on a value of 10%.

In as early as the current 2007 financial year, the adjusted free cash flow doubles due to the dynamic top-line and above-average bottom-line growth. For 2008e, this corresponds to a fair value of EUR 70 m, and a value of EUR 93 m for 2009e.

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 23

DCF model In order to calculate a value for InVision on the basis of the expected medium to long-term business success, we have applied a DCF model.

In the years leading up to 2009, we expect further sales growth at a high level, in particular in 2007. Due to the ex-tremely high scalability of the business, we expect to see a considerable increase in earnings, because the main devel-opment work on the software has already been performed. It is possible for InVision to expand into further areas of activity and the company has already started to do so.

Sales and, in particular, earnings growth will be supported by the further expansion of the partner business and ongoing growth in maintenance income, which we estimate will cover the company’s development costs in full by as early as 2009.

It is particularly worth mentioning that InVision already has an extremely renowned client base and that the potential has not yet been anywhere near exploited for individual clients.

We expect sales to increase by 42% a year in the period lead-ing up to 2009, with the EBIT margin likely to increase from 18% to 29%.

From 2011 onwards, we expect sales growth to decline con-siderably to 5% and also expect the EBIT margin to gradually fall to 20%. This assumption is designed to take account of the fact that no long-term forecast can be made for the dy-namic markets for software solutions.

We have assumed a perpetual growth rate of 2%.

2005 2006 2007e 2008e 2009e 2010e

Net Income -1,241.1 1,374.3 2,648.5 4,642.9 6,406.7 7,625.6+ Depreciation + Amortisation 83.0 80.0 144.4 204.7 256.6 282.9- Net Interest Income -19.0 -67.7 -620.0 -760.0 -760.0 -760.0+ Taxes -409.7 454.0 882.8 1,547.6 2,135.6 2,541.9- Maintenance Capex 23.1 32.9 53.9 81.9 102.7 113.2

+/- Others 0.0 0.0 0.0 0.0 0.0 0.0= Adjusted Free Cash Flow -1,571.8 1,943.1 4,241.8 7,073.3 9,456.2 11,097.3

Adjusted Free Cash Flow Yield -2.1% 2.6% 8.2% 13.7% 18.3% 21.5%Fair Free Cash Flow Yield 10.0% 10.0% 10.0% 10.0% 10.0% 10.0%

= Actual Enterprise Value 73,337.8 73,709.8 51,651.8 51,651.8 51,651.8 51,651.8

= Fair Enterprise Value -15,718.2 19,431.4 42,418.0 70,732.5 94,561.9 110,972.6

- Net Debt (Cash) 365.0 737.0 -21,321.0 -21,321.0 -21,321.0 -21,321.0- Pension Liabilities 0.0 0.0 0.0 0.0 0.0 0.0- Off Balance Sheet 0.0 0.0 0.0 0.0 0.0 0.0= Fair Market Capitalisation -16,083.2 18,694.4 63,739.0 92,053.5 115,882.9 132,293.6

Table 8; Source: SES Research

Free Cash Flow Yield

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 24

We have assumed a beta of 1.5 and a risk-free rate of 4.09%. Our assumed market yield stands at 9%. Based on these fig-ures, and assuming full self-financing in the long term, this produces a WACC of 11.5%.

Peer group comparison InVision’s valuation on the basis of a peer group comparison uses three peer groups.

• Comparable US companies

• Listed German pure play software providers (product business of over 60% with top-line growth of over 20%)

• Multiplier comparison based on previous transactions

We believe that the EV/EBIT multiplier for financial year 2007 is of primary importance with respect to the valuation. Al-though financial year 2008 produces considerably higher val-ues, we have discarded these due to the low earnings visibility for 2008. It is worth taking into account that InVision is likely to grow at a far faster rate than its peer group, which is what makes the company particularly interesting from a valuation point of view (see below).

We have based our comparative analysis on the following companies:

DCF Model2007e 2008e 2009e 2010e 2011e 2012e 2013e 2014e 2015e 2016e 2017e 2018e 2019e 2020e

Sales 18.0 25.6 32.1 35.4 37.1 39.0 40.9 43.0 45.1 47.4 49.8 52.2 54.9 57.6Change 68.2% 41.7% 25.4% 10.2% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0%

EBIT 4.2 7.0 9.3 10.9 10.4 10.9 11.5 12.0 9.0 9.5 10.0 10.4 11.0 11.5EBIT-Margin 23.0% 27.2% 29.0% 30.9% 28.0% 28.0% 28.0% 28.0% 20.0% 20.0% 20.0% 20.0% 20.0% 20.0%

Tax rate 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0%

Depreciation 0.1 0.2 0.3 0.3 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.3 0.3 0.3in % of Sales 0.8% 0.8% 0.8% 0.8% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5%

Change in Liquidity from- Working Capital -2.0 -2.1 -1.8 -0.9 2.6 -0.4 -0.4 -0.4 -0.4 -0.5 -0.5 -0.5 -0.5 -0.5- Capex -0.2 -0.2 -0.3 -0.3 -0.2 -0.2 -0.2 -0.2 -0.2 -0.2 -0.2 -0.3 -0.3 -0.3Capex in % of Sales 0.9% 0.9% 0.9% 0.9% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5%

Other 0.0 0.0 0.0 0.0 -1.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Free Cash Flow 1.0 3.1 5.1 7.2 9.4 7.8 8.2 8.6 6.3 6.7 7.0 7.3 7.7 8.1(WACC-Model)

Valuation (EUR mln) Model parameter Sensitivity Value per Share (EUR) Terminal Growth

Present values 2020e 43.8 Debt ratio 0.00% WACC 1.25% 1.50% 1.75% 2.00% 2.25% 2.50% 2.75%

Terminal Value 20.0 Costs of Debt n.a. 12.46% 34.78 34.93 35.09 35.26 35.44 35.62 35.82

Liabilities -0.9 Market return 9.00% 11.96% 36.05 36.23 36.41 36.61 36.81 37.03 37.26

Liquidity 22.2 Risk free rate 4.09% 11.71% 36.73 36.92 37.12 37.33 37.56 37.79 38.04

Equity Value 85.1 11.46% 37.44 37.65 37.87 38.10 38.34 38.59 38.87

Beta 1.50 11.21% 38.19 38.41 38.65 38.90 39.16 39.44 39.74

WACC 11.46% 10.96% 38.97 39.22 39.48 39.75 40.04 40.34 40.66

Terminal Growth 2.00% 10.46% 40.68 40.97 41.27 41.60 41.94 42.30 42.69

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 25

Comparable US companies

Genesys

The US company based in Daly City employs a global work-force of around 4000 and its core business concentrates on call centre software. The company is globally active.

NICE Systems

NICE Systems has its headquarters in Ra’anana in Israel and currently employs a global workforce of 1,416. In its core business area, the company focuses on call centre software and security.

Verint Systems

This US company is based in Melville, New York and focuses on the provision of business and security software. Verint Sys-tems is globally active.

German pure play software providers

SAF

The Swiss company SAF AG has its headquarters in Täger-wilen and concentrates on scheduling and planning software. In addition to Switzerland and Germany, the company also has locations in the US and Slovakia.

Update software

Update is a listed company with its registered office in Vienna. At present, the leading European provider of CRM software employs a workforce of around 186.

Utimaco Safeware

Ultimaco a global manufacturer of professional data protection solutions. The company is based in Oberursel near Frankfurt am Main and currently employs around 270 people.

Recent transactions in the sector (company takeovers)

Kronos Inc

The US-firm Kronos Inc is based in Chelmsford and employs a workforce of around 2,500. The company is active in the US, the UK, Asia and South America and markets WFM solutions.

Witness Systems Inc

The US-company based in Roswell deals with workforce op-timisation software. It employs a global workforce of 834.

Workbrain Corp.

Workbrain Corp. is based in Canada and employs around 650 people. The company focuses on workforce management so-lutions and its products are marketed in the US, the UK and Australia.

The following table sets out the consensus estimates for the listed peer groups:

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 26

Company LC Price MC EVin LC in LC m in LC m 06e 07e 08e 06e 07e 08e 06e 07e 08e 06e 07e 08e

Workforce ManagementGenesys EUR 1.35 94.3 121.9 13.50 n.a. n.a. 0.86 0.86 0.86 n.a. n.a. n.a. 5.19 5.86 5.67NICE Systems ILs 14,970.00 7,745.9 7,068.4 30.27 25.15 21.76 4.04 3.36 2.98 n.a. n.a. n.a. 26.04 17.58 13.85Verint Systems USD 31.35 1,009.1 744.8 25.32 24.70 21.74 2.12 1.71 1.24 23.13 17.71 12.28 15.50 13.21 7.43

Average 23.03 21.12 19.00 2.34 1.98 1.69 23.13 17.71 12.28 15.58 12.22 8.98

German Pure Play SoftwareanbieterSAF EUR 25.01 138.5 135.0 30.17 19.54 12.99 10.05 6.63 4.73 28.66 20.10 12.81 27.13 18.55 11.87Update software EUR 4.58 52.2 44.0 15.27 13.47 10.90 1.86 1.40 1.20 16.28 11.57 8.45 13.32 10.47 6.98Utimaco EUR 13.20 194.6 161.8 22.72 23.53 19.67 3.87 3.26 2.71 18.17 17.30 13.40 16.42 14.28 11.27

Average 22.72 18.85 14.52 5.26 3.76 2.88 21.04 16.32 11.55 18.96 14.43 10.04

Average Total 22.87 19.98 16.76 3.80 2.87 2.29 21.56 16.67 11.73 17.27 13.33 9.51

Median Total 24.02 21.53 16.59 3.00 2.48 1.97 20.65 17.51 12.54 15.96 13.74 9.35

Invision EUR 32.65 72.97 51.65 53.52 27.44 15.70 4.81 2.86 2.02 26.50 12.44 7.43 25.46 12.02 7.22

Fair Value (EV) Peer Group Workforce Management 25.12 35.69 43.30 45.08 73.53 85.36 31.60 52.48 64.28

Fair Value (EV) Peer Group German Software 56.48 67.90 73.75 41.01 67.76 80.30 38.47 62.01 71.84

Table 10; Sources: SES Research, Bloomberg

Peer Group Fair Value (EV) Peer Group Workforce ManagementP/E EV/Sales EV/EBIT EV/EBITDA

This produces the following multiples:

If we apply the EV/EBIT multiples in the peer group for 2007, we arrive at appropriate valuations (EV) of between EUR 68 m and EUR 74 m (EUR 40-42 per share), depending on the peer group. For 2008, the values already stand at around EUR 80-85 m (EUR 45-48 per share). The value per share are to be understood as a total value (incl. financial funds).

Valuation of comparable transactions

The valuation of comparable transactions includes three transactions among competitors that were all executed in Feb-ruary/March of this year. As a result, there is substantial scope for comparability:

Company LC Price Buyer EVper share in LC in LC m 06e 07e 08e 06e 07e 08e 06e 07e 08e

Kronos Inc USD 55.00 Hellman & Friedman 1,777.4 578.20 655.69 706.00 82.59 90.72 101.36 113.57 126.22 136.96Witness Systems Inc USD 27.50 Verint Systems 880.1 214.35 252.82 292.13 22.22 52.60 66.75 59.48 59.40 74.32Workbrain Corp. USD 12.50 Infor 168.1 93.63 106.30 119.18 -1.14 4.27 6.67 1.83 6.39 9.45

Invision EUR 10.73 18.05 25.58 1.95 4.15 6.95 2.03 4.30 7.16Table 11; Sources: SES Research, Bloomberg

Peer Group InVision - Acquisitions Workforce Management

Company LC Price MC EVin LC in LC m in LC m 06e 07e 08e 06e 07e 08e 06e 07e 08e 06e 07e 08e

Workforce ManagementGenesys EUR 1.35 94.3 121.9 0.10 n.a. n.a. 141.90 141.00 141.80 n.a. n.a. n.a. 23.50 20.80 21.50NICE Systems ILs 14,970.00 7,745.9 7,068.4 4.95 5.95 6.88 1,750.47 2,106.73 2,371.44 #WERT! #WERT! #WERT! 271.49 402.03 510.26Verint Systems USD 31.35 1,009.1 744.8 1.24 1.27 1.44 350.57 435.15 601.69 32.20 42.05 60.65 48.05 56.40 100.26

German Pure Play SoftwareanbieterSAF EUR 25.01 138.5 135.0 0.83 1.28 1.93 13.43 20.35 28.52 4.71 6.72 10.54 4.98 7.28 11.37Update software EUR 4.58 52.2 44.0 0.30 0.34 0.42 23.60 31.50 36.50 2.70 3.80 5.20 3.30 4.20 6.30Utimaco EUR 13.20 194.6 161.8 0.58 0.56 0.67 41.80 49.68 59.68 8.90 9.35 12.08 9.85 11.33 14.35

Invision EUR 10.73 18.05 25.58 1.95 4.15 6.95 2.03 4.30 7.16

Table 9; Sources: SES Research, Bloomberg

Peer Group InVisionEPS Sales EBIT EBITDA

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 27

Company LC Price Buyer EVper share in LC in LC m 06e 07e 08e 06e 07e 08e 06e 07e 08e

Kronos Inc USD 55.00 Hellman & Friedman 1,777.4 3.07 2.71 2.52 21.52 19.59 17.54 15.65 14.08 12.98Witness Systems Inc USD 27.50 Verint Systems 880.1 4.11 3.48 3.01 39.62 16.73 13.19 14.80 14.82 11.84Workbrain Corp. USD 12.50 Infor 168.1 1.80 1.58 1.41 n.a. 39.41 25.19 91.82 26.30 17.80

Average 2.99 2.59 2.31 30.57 25.24 18.64 40.75 18.40 14.21

Median 3.07 2.71 2.52 30.57 19.59 17.54 15.65 14.82 12.98

Fair Value (EV) by multiples EUR 32.11 46.77 59.19 59.58 81.33 129.53 82.70 79.04 101.65

(median)

Table 12; Sources: SES Research, Bloomberg

Peer Group InVision - Acquisitions Workforce Management

The takeover prices paid produce the following multiples:

The EV/EBIT multiples (2007/08) produce enterprise values of EUR 81 m and EUR 103 m respectively for InVision. This means that the scenario here is similar to that produced by the previous peer group comparison.

Conclusion We believe that the InVision post-money valuation of EUR 40 m is fair, although the peer group analyses and the FCF model point towards higher values. The DCF model should be viewed as the central valuation method in this case, because it values the company-specific factors and allows reasonable consideration to be given to the relatively low visibility for earnings from 2008 onwards on the risk side (BETA of 1.5).

InVision grew by around 70% in the previous financial year and achieved an EBIT margin of 18% (EUR 1.95 m). This means that earnings increased by EUR 3.6 m as against the prior year, when the company still generated a loss. This high-lights something that is key to pure play software providers: InVision has performed the main development work on its product and has a strong client base that ensures regular maintenance income. Further increases in sales will have a significantly above-average impact on the EBIT margin.

The raising of capital has to the potential to act as a growth driver for InVision. Capital that is currently being ploughed into the development of the company and measures to attract fur-ther clients should pay off several times over in the current situation, given that the main development work has been completed.

InVision Software AG Research Note

Equity story Competitive quality Finances Valuation Newsflow Company & products Ratios

SES Research GmbH – A Member of the Warburg Group Page 28

The company’s recent newsflow has been positive and was characterised by the figures for Q1 2007 (as at 31 March 2007) and the 2006 annual report:

We expect the high top-line growth to continue and predict that InVision will drastically increase its sales and earnings this year. This should become evident in as early as the first half of the year. Due to the IPO, however, the second half and, in particular, the fourth quarter, which is traditionally strong in this sector, will provide the main impetus.