30 June 2012 Audited Financial Statements - City of …€¦ · General purpose financial...

64

2

Transcript of 30 June 2012 Audited Financial Statements - City of …€¦ · General purpose financial...

2

2

Rockdale City Council

General purpose financial statements for the year ended 30 June 2012

Contents

Page General purpose financial statements

Statement by Councillors and Management 3 Income statement 4 Statement of comprehensive income 5 Balance sheet 6 Statement of changes in equity 7 Statement of cash flows 8 Notes to the financial statements 9 Auditors’ reports 54

AASB101(46)(b),(d) These financial statements are general purpose financial statements of Rockdale City Council and are presented in the Australian currency.

AASB101(126)(a) Rockdale City Council is constituted under the Local Government Act (1993) and has its principal place of business at:

Rockdale City Council 2 Bryant Street Rockdale NSW 2216 AASB110(17) The financial statements are authorised for issue by the Council on 17 October 2012. Council has the power

to amend and reissue the financial statements.

Through the use of the internet, we have ensured that our reporting is timely, complete, and available at minimum cost. All press releases, financial statements and other information are available on our website: www.rockdale.nsw.gov.au

3

4

Rockdale City Council

Income statement for the year ended 30 June 2012

Original budget(1)

2012 $’000 Notes

Actual 2012 $’000

Actual 2011 $’000

Income from continuing operations Revenue: 50,707 Rates and annual charges 3a 50,757 48,789 4,815 User charges and fees 3b 8,697 5,260 3,109 Interest and investment revenue 3c 4,431 3,994 4,342 Other revenues 3d 4,583 4,261 5,252 Grants and contributions provided for operating purposes 3e,f 6,739 5,860 6,735 Grants and contributions provided for capital purposes 3e,f 3,422 7,090 Other Income: - Net gain from the disposal of assets 5 - 75

- Net share of interests in joint ventures and associates using the equity method 19 468 445

74,960 Total income from continuing operations 79,097 75,774 Expenses from continuing operations 29,576 Employee benefits and on-costs 4a 29,864 27,956 387 Borrowing costs 4b 354 378 18,258 Materials and contracts 4c 22,992 17,442 17,355 Depreciation and amortisation 4d 18,230 17,037 - Impairment - - 9,120 Other expenses 4e 9,947 9,422 412 Net loss from the disposal of assets 5 160 - 75,108 Total expenses from continuing operations 81,547 72,235 (148) Operating result from continuing operations (2,450) 3,539 - Operating result from discontinued operations - - (148) Net operating result for the year (2,450) 3,539 Attributable to: (148) – Council (2,450) 3,539 - – Minority interests - -

(6,883) Net operating result for the year before grants and contributions provided for capital purposes (5,872) (3,551)

Note:

(1) Original budget as approved by Council – refer Note 16.

The above Income statement should be read in conjunction with the accompanying notes.

5

Rockdale City Council

Statement of comprehensive income for the year ended 30 June 2012

Notes

Actual 2012 $’000

Actual 2011 $’000

Net operating result for the year – from Income statement (2,450) 3,539 Other comprehensive income Gain (loss) on revaluation of infrastructure, property, plant and

equipment 20(a) - 40,880 Changes in accounting policies 20(b) - (440,664) Adjustment to correct prior period errors 20(d) (4,160) (8,012) Total other comprehensive income for the year (4,160) (407,796) Total comprehensive income for the year (6,610) (404,257) Attributable to – Council (6,610) (404,257) – Minority interests - -

The above Statement of comprehensive income should be read in conjunction with the accompanying notes.

6

Rockdale City Council

Balance sheet as at 30 June 2012

Notes

Actual 2012 $’000

Actual 2011 $’000

ASSETS Current assets Cash and cash equivalents 6a 58,661 36,130 Investments 6b 6,004 5,947 Receivables 7 5,813 7,248 Inventories 8 50 56 Other 8 663 604 Non-current assets classified as held for sale - - Total current assets 71,191 49,985 Non-current assets Investments 6b 5,016 18,393 Receivables 7 445 678 Infrastructure, property, plant and equipment 9 784,876 799,976 Investments accounted for using equity method 19 1,494 1,026 Investment property 14 - - Intangible assets 21 2,335 1,954 Other 8 380 443 Total non-current assets 794,546 822,470 Total assets 865,737 872,455 LIABILITIES Current liabilities Payables 10 7,118 7,380

Borrowings 10 954 964 Provisions 10 10,194 10,268 Total current liabilities 18,266 18,612 Non-current liabilities Payables 10 - - Borrowings 10 4,909 4,989 Provisions 10 1,459 1,140 Total non-current liabilities 6,368 6,129 Total liabilities 24,634 24,741 Net assets 841,103 847,714 EQUITY Asset Revaluation Reserve 20 394,887 399,315 Retained Earnings 20 446,216 448,399 Total equity 841,103 847,714 Council equity interest 841,103 847,714 Minority equity interest - Total equity 841,103 847,714

The above Balance sheet should be read in conjunction with the accompanying notes.

7

Rockdale City Council

Statement of changes in equity for the year ended 30 June 2012

Actual 2012 $’000

Actual 2011 $’000

Notes

Retained earnings

Asset revaluation

reserve Total equity

Retained earnings

Asset revaluation

reserve Total equity

Opening balance 20 448,399 399,315 847,714 892,273 359,698 1,251,971

Correction of errors 20

267

(4,427)

(4,160)

-

-

- Restated opening

balance 20

448,666

34,887 843,553 892,273 359,698 1,251,971

Net operating result for the year 20

(2,450)

-

(2,450) 3,539 - 3,539

Other Comprehensive income 20

-

-

- (447,413) 39,617 (407,796)

Total comprehensive income 20

(2,450)

-

(2,450) (443,874) 39,617 (404,257)

Closing balance 20 446,216 394,887 841,103 448,399 399,315 847,714

The above Statement of changes in equity should be read in conjunction with the accompanying notes.

8

Rockdale City Council

Statement of cash flows for the year ended 30 June 2012

Budget 2012 $’000 Notes

Actual 2012 $’000

Actual 2011 $’000

Cash flows from operating activities Receipts: 50,482 Rates and annual charges 50,595 48,627 8,524 User charges and fees 9,732 6,193 4,058 Investment revenue and interest 4,256 2,619 10,541 Grants and contributions 11,494 12,147 1,400 Deposits and retentions received 1,443 969 4,495 Other revenue 4,274 3,417 Payments: (28,635) Employee benefits and on-costs (29,619) (27,630) (20,884) Materials and contracts (24,187) (18,362) (310) Borrowing costs (312) (378) (1,300) Deposits and retentions refunded (1,346) (1,598) (11,000) Other expenses (10,186) (7,326) 17,371 Net cash provided by operating activities 11(b) 16,144 18,678 Cash flows from investing activities Receipts: 16,935 Redemption of investments 18,351 10,361 923 Sale of infrastructure, property, plant and equipment 990 868 Payments: (4,000) Purchase of investments (4,000) (12,989) (10,000) Purchase of infrastructure, property, plant and equipment 9 (8,643) (12,773) - Purchase of intangible assets 21 (447) - 3,858 Net cash provided by (or used in) Investing activities 6,251 (14,533) Cash flows from financing activities Receipts: 1,100 Proceeds from borrowings 1,100 - Payments: (1,000) Repayment of borrowings (964) (1,090) 100 Net cash provided by (or used in) financing activities 136 (1,090) 21,329 Net increase in cash and cash equivalents 22,531 3,056

36,130 Cash and cash equivalents at beginning of reporting period 11(a) 36,130 33,074

57,459 Cash and cash equivalents at end of reporting period 11(a) 58,661 36,130

The above Statement of cash flows should be read in conjunction with the accompanying notes.

Notes to the financial statements 30 June 2012

9

Rockdale City Council

Notes to the financial statements for the year ended 30 June 2012

Contents of the notes to the financial statements Page

Note 1 Summary of significant accounting policies 10

Note 2(a) Functions or activities 19 Note 2(b) Components of functions or activities 20 Note 3 Income from continuing operations 21 Note 4 Expenses from continuing operations 25 Note 5 Gain or loss from the disposal of assets 27 Note 6(a) Cash and cash equivalents 28 Note 6(b) Investments 29 Note 6(c) Restricted cash, cash equivalents and investments 30 Note 7 Receivables 31 Note 8 Inventories and other assets 32 Note 9(a) Infrastructure, property, plant and equipment 33 Note 9(b) Restricted infrastructure, property, plant and equipment 33 Note 10(a) Payables, borrowings and provisions 35 Note 10(b) Description of and movements in provisions 36 Note 11 Reconciliation of operating result to net cash movement from operating activities37 Note 12 Commitments for expenditure 38 Note 13 Statement of performance measures – Consolidated results 39 Note 14 Investment properties 40 Note 15 Financial risk management 41 Note 16 Material budget variations 45 Note 17 Statement of developer contributions 47 Note 18 Contingencies 50 Note 19 Interests in joint ventures and associates 51 Note 20 Revaluation reserves and retained earnings 52 Note 21 Intangible assets 53

Notes to the financial statements 30 June 2012

10

MANDATORY AASB101(8)(e)

Note 1 Summary of significant accounting policies AASB101(103)(a),(b) AASB127(42)(a)

The principal accounting policies adopted in the preparation of these consolidated financial statements are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated.

(a) Basis of preparation

AASB101(Aus15.2), (Aus15.4)

These general purpose financial statements have been prepared in accordance with Australian Accounting Standards and Interpretations issued by the Australian Accounting Standards Board, the Local Government Act (1993) and Regulation, and the Local Government Code of Accounting Practice and Financial Reporting. Rockdale City Council is a not for-profit entity for the purpose of preparing the financial statements. 1

(i) New and amended standards adopted by Council 13 AASB101(117)(a) None of the new standards and amendments to standards that are mandatory for the first time for the financial

year beginning 1 July 2011 affected any of the amounts recognised in the current period or any prior period and are not likely to affect future periods.

(ii) Early adoption of standards 15,16 AASB101(122),(125) NSW Council has not elected to apply any pronouncements before their operative date in the annual reporting

period beginning 1 July 2011.

(iii) Historical cost convention These financial statements have been prepared under the historical cost convention, as modified by the

revaluation of available for sale financial assets, financial assets and liabilities at fair value through profit or loss, certain classes of property, plant and equipment.

(iv) Critical accounting estimates and judgements The preparation of financial statements requires the use of certain critical accounting estimates. It also

requires management to exercise its judgement in the process of applying the Council's accounting policies. Estimates and judgements are continually evaluated and are based on historical experience and other factors, including expectations of future events that may have a financial impact on the entity and that are believed to be reasonable under the circumstances.

• Critical accounting estimates and assumptions Council makes estimates and assumptions concerning the future. The resulting accounting

estimates will, by definition, seldom equal the related actual results. The estimates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year is the estimated fair values of infrastructure, property, plant and equipment.

• Critical judgements in applying the entity's accounting policies (i) Impairment of Receivables Council has made a significant judgement about the impairment of a number of its receivables in

Note 7.

(ii) Projected Section 94 Commitments Council has used significant judgement in determining future Section 94 income and expenditure in

Note 17.

AASB101 (b) Revenue recognition

Council recognises revenue when the amount of revenue can be reliably measured, it is probable that future economic benefits will flow to the entity and specific criteria have been met for each of the Council’s activities as described below. Council bases its estimates on historical results, taking into consideration the type of customer, the type of transaction and the specifics of each arrangement.

AAS27 Revenue is measured at the fair value of the consideration received or receivable. Revenue is measured on major income categories as follows:

Rates, annual charges, grants and contributions Rates, annual charges, grants and contributions (including developer contributions) are recognised as

revenues when the Council obtains control over the assets comprising these receipts. Developer contributions may only be expended for the purposes for which the contributions were required but the Council may apply contributions according to the priorities established in work schedules.

Control over assets acquired from rates and annual charges is obtained at the commencement of the rating year as it is an enforceable debt linked to the rateable property or, where earlier, upon receipt of the rates.

Control over granted assets is normally obtained upon their receipt (or acquittal) or upon earlier notification that a grant has been secured, and is valued at their fair value at the date of transfer.

Revenue is recognised when the Council obtains control of the contribution or the right to receive the contribution, it is probable that the economic benefits comprising the contribution will flow to the Council and the amount of the contribution can be measured reliably.

Notes to the financial statements 30 June 2012

11

Note 1 Summary of significant accounting policies (continued) (b) Revenue recognition (continued) Where grants or contributions recognised as revenues during the financial year were obtained on condition

that they be expended in a particular manner or used over a particular period and those conditions were undischarged at balance date, the unused grant or contribution is disclosed in Note 3(g). The note also discloses the amount of unused grant or contribution from prior years that was expended on Council’s operations during the current year.

A liability is recognised in respect of revenue that is reciprocal in nature to the extent that the requisite service has not been provided at balance date.

User charges and fees User charges and fees (including parking fees and fines) are recognised as revenue when the service has

been provided, the payment is received, or when the penalty has been applied, whichever first occurs.

Sale of plant, property, infrastructure and equipment The profit or loss on sale of an asset is determined when control of the asset has irrevocably passed to the

buyer.

Interest and rents Interest and rents are recognised as revenue on a proportional basis when the payment is due, the value of

the payment is notified, or the payment is received, whichever first occurs.

AASB101(110) (c) Principles of consolidation

(i) The Consolidated Fund LGA s.409(1) In accordance with the provisions of Section 409(1) of the Local Government Act 1993, all money and

property received by Council is held in the Council’s Consolidated Fund unless it is required to be held in the Council’s Trust Fund. The consolidated fund and other entities through which the Council controls resources to carry on its functions have been included in the financial statements forming part of this report.

The following entities have been included as part of the Consolidated fund:

• General purpose operations • Rockdale Meal Services

LGA s.411 (ii) The Trust Fund In accordance with the provisions of Section 411 of the Local Government Act 1993 (as amended), a separate

and distinct Trust Fund is maintained to account for all money and property received by the Council in trust which must be applied only for the purposes of or in accordance with the trusts relating to those monies. Trust monies and property subject to Council’s control have been included in these reports.

Trust monies and property held by Council but not subject to the control of Council, have been excluded from these reports. A separate statement of monies held in the Trust Fund is available for inspection at the Council office by any person free of charge.

AASB101(110) (iii) Joint ventures Jointly controlled assets The proportionate interests in the assets, liabilities and expenses of a joint venture activity have been

incorporated in the financial statements under the appropriate headings. Details of the joint venture are set out in Note 19.

Joint venture entities The interest in a joint venture partnership is accounted for using the equity method after initially being

recognised at cost. Under the equity method, the share of the profits or losses of the partnership is recognised in profit or loss, and the share of post acquisition movements in reserves is recognised in other comprehensive income. Details relating to the partnership are set out in note 19.

Profits or losses on transactions establishing the joint venture partnership and transactions with the joint venture are eliminated to the extent of the Council's ownership interest until such time as they are realised by the joint venture partnership on consumption or sale. However, a loss on the transaction is recognised immediately if the loss provides evidence of a reduction in the net realisable value of current assets, or an impairment loss.

(d) Leases

Leases in which a significant portion of the risks and rewards of ownership are not transferred to Council as lessee are classified as operating leases. Payments made under operating leases (net of any incentives received from the lessor) are charged to the income statement on a straight-line basis over the period of the lease.

Notes to the financial statements 30 June 2012

12

Note 1 Summary of significant accounting policies (continued) (d) Leases (continued)

Lease income from operating leases where Council is a lessor is recognised in income on a straight-line basis over the lease term.

AASB101(110),(111) (e) Acquisition of assets

AASB3(14),(24),(28) AASB3(27) AASB3(31)

The purchase method of accounting is used to account for all acquisitions of assets. Cost is measured as the fair value of the assets given, plus costs directly attributable to the acquisition.

AASB101(110) (f) Impairment of assets

AASB136(9),(10) Assets that have an indefinite useful life are not subject to amortisation and are tested annually for impairment or more frequently if events or changes in circumstances indicate that they might be impaired. Other assets are tested for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs to sell and value in use.

AASB101(110) (g) Cash and cash equivalents

AASB107(6),(8),(46) For cash flow statement presentation purposes, cash and cash equivalents includes cash on hand, deposits held at call with financial institutions, other short-term, highly liquid investments with original maturities of three months or less that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value, and bank overdrafts. Bank overdrafts are shown within borrowings in current liabilities on the balance sheet.

AASB101(110) (h) Receivables

Receivables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method, less provision for impairment. Receivables are generally due for settlement within 30 days.

Collectibility of receivables is reviewed on an ongoing basis. Debts which are known to be uncollectible are written off by reducing the carrying amount directly. An allowance account (provision for doubtful debts) is used when there is objective evidence that Council will not be able to collect all amounts due according to the original terms of the receivables. Significant financial difficulties of the debtor, probability that the debtor will enter bankruptcy or financial reorganisation, and default or delinquency in payments (more than 30 days overdue) are considered indicators that the receivable is impaired. The amount of the impairment allowance is the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the original effective interest rate. Cash flows relating to short-term receivables are not discounted if the effect of discounting is immaterial.

The amount of the impairment loss is recognised in the income statement within other expenses. When a receivable for which an impairment allowance had been recognised becomes uncollectible in a subsequent period, it is written off against the allowance account. Subsequent recoveries of amounts previously written off are credited against other expenses in the income statement.

AASB101(110) (i) Inventories

Inventories are stated at the lower of cost and net realizable value. Costs are assigned on the basis of first in first out method.

AASB101(110) AASB7(21)

(j) Investments and other financial assets

Council classifies its investments as financial assets at fair value through profit or loss only. These are financial assets held for trading and are classified in this category as Council has the intention to sell them if the market conditions are favourable.

Recognition and de-recognition Regular purchases and sales of financial assets are recognised on trade-date - the date on which Council

commits to purchase or sell the asset. Investments are initially recognised at fair value plus transaction costs for all financial assets not carried at fair value through profit or loss. Financial assets carried at fair value through profit or loss are initially recognised at fair value and transaction costs are expensed in the income statement. Financial assets are derecognised when the rights to receive cash flows from the financial assets have expired or have been transferred and Council has transferred substantially all the risks and rewards of ownership.

Notes to the financial statements 30 June 2012

13

Note 1 Summary of significant accounting policies (continued) (j) Investments and other financial assets (continued)

Subsequent measurement Financial assets at fair value through profit and loss are subsequently carried at fair value. Gains or losses

arising from changes in the fair value of the ‘financial assets at fair value through profit or loss’ category are presented in the income statement within other income or other expenses in the period in which they arise. Dividend income from financial assets at fair value through profit and loss is recognised in the income statement as part of revenue from continuing operations when Council’s right to receive payments is established.

Impairment AASB139(58),(67),(68), (69),(70) AASB7(21),(B5)(f) (Revised)

Council assesses at the end of each reporting period whether there is objective evidence that a financial asset or group of financial assets is impaired. A financial asset or a group of financial assets is impaired and impairment losses are incurred only if there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition of the asset (a ‘loss event’) and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or group of financial assets that can be reliably estimated.

(i) Assets carried at amortised cost For loans and receivables, the amount of the loss is measured as the difference between the asset’s carrying

amount and the present value of estimated future cash flows (excluding future credit losses that have not been incurred) discounted at the financial asset’s original effective interest rate. The carrying amount of the asset is reduced and the amount of the loss is recognised in profit or loss. If a loan or held-to-maturity investment has a variable interest rate, the discount rate for measuring any impairment loss is the current effective interest rate determined under the contract. As a practical expedient, the group may measure impairment on the basis of an instrument’s fair value using an observable market price.

DLG Investment Policy Council has an approved investment policy complying with Section 625 of the Local Government Act and

S212 of the LG (General) Regulation 2005. Investments are placed and managed in accordance with that policy and having particular regard to authorised investments prescribed under the Ministerial Local Government Investment Order. Council maintains an investment policy that complies with the Act and ensures that it or its representatives exercise care, diligence and skill that a prudent person would exercise in investing Council funds.

Council amended its policy following revisions to the Ministerial Local Government Investment Order arising from the Cole Inquiry recommendations. Certain investments the Council holds are no longer prescribed, however they have been retained under grandfathering provisions of the Order. These will be disposed of when most financially advantageous to Council.

AASB101(110) (k) Fair value estimation

The fair value of financial assets and financial liabilities must be estimated for recognition and measurement or for disclosure purposes.

AASB132(92) The fair value of financial instruments traded in active markets is based on quoted market prices at the balance sheet date.

The fair value of financial instruments that are not traded in an active market is determined using valuation techniques. Council uses a variety of methods and makes assumptions that are based on market conditions existing at each balance date. Quoted market prices or dealer quotes for similar instruments are used for long-term debt instruments held. Other techniques, such as estimated discounted cash flows, are used to determine fair value for the remaining financial instruments.

The nominal value less estimated credit adjustments of trade receivables and payables are assumed to approximate their fair values. The fair value of financial liabilities for disclosure purposes is estimated by discounting the future contractual cash flows at the current market interest rate that is available to the Council for similar financial instruments.

AASB101(110) (l) Infrastructure, property, plant and equipment (IPPE)

Council’s assets have been progressively revalued to fair value in accordance with a staged implementation advised by the Department of Local Government. At balance date the following classes of IPPE were stated at their fair value:

• Operational land (External Valuation).

• Buildings – Specialised/Non Specialised (External Valuation).

• Plant and equipment (as approximated by depreciated historical cost).

• Road assets – roads, bridges and footpaths (Internal Valuation)

Notes to the financial statements 30 June 2012

14

Note 1 Summary of significant accounting policies (continued) (l) Infrastructure, property, plant and equipment (IPPE) (continued)

• Drainage assets – (Internal Valuation)

• Bulk earthworks - (Internal Valuation)

AASB101(110) • Community land – (Internal Valuation)

• Land Improvements – (Internal Valuation)

• Other structures – (Internal Valuation)

• Other assets (as approximated by depreciated historical cost) Council assesses at each reporting date whether there is any indication that a revalued asset’s carrying

amount may differ materially from that which would be determined if the asset were revalued at the reporting date. If any such indication exists, Council determines the asset’s fair value and revalues the asset to that amount. Full revaluations are undertaken for all assets on a 5 year cycle.

Increases in the carrying amounts arising on revaluation are credited to the asset revaluation reserve. To the extent that the increase reverses a decrease previously recognised in profit or loss, the increase is first recognised in profit or loss. Decreases that reverse previous increases of the same asset are first charged against revaluation reserves directly in equity to the extent of the remaining reserve attributable to the asset; all other decreases are charged to the Income statement.

AASB116(12) Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the item will flow to Council and the cost of the item can be measured reliably. All other repairs and maintenance are charged to the income statement during the financial period in which they are incurred.

AASB116(50),(73)(b) Land is not depreciated. Depreciation on other assets is calculated using the straight line method to allocate their cost, net of their residual values, over their estimated useful lives, as follows:

AASB116(73)(c) Office equipment and furniture 4 - 10 years Drainage - channels 30 years Vehicles,plant & equipment 7 - 8 years - pits and pipe 100 years Library resources 7 years Kerb and gutter 80 years Recycling bins 10 - 25 years Footpaths 40 - 70 years Buildings 20 - 80 years Sealed road-surface 15 years Intangible assets 10 years -pavement 110 years Park furniture and equipment 5 years Road structures 80 - 90 years Street furniture 20 - 50 years Cycleways 60 years Bulk earthworks Infinite Culverts 60 years Foreshore improvement 30 years Bridges – Concrete 120 years Open space car park 20 years

AASB116(51) The assets’ residual values and useful lives are reviewed, and adjusted if appropriate, at each balance sheet

date.

AASB136(59) An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount.

Gains and losses on disposals are determined by comparing proceeds with carrying amount. These are included in the income statement.

Land, other than land under roads, is classified as either operational or community in accordance with Part 2 of Chapter 6 of the Local Government Act (1993). This classification is made in Note 9(a).

AASB101(110) (m) Land under roads

Council has elected not to recognise land under roads acquired before 1 July 2008 in accordance with AASB 1051. Any land under roads that was recognised before 1 July 2008 was derecognised at 1 July 2008 against the opening balance of retained earnings.

AASB116(68),(71) AASB116(41)

Land under roads acquired after 1 July 2008 is recognised in accordance with AASB 116 – Property, Plant and Equipment.

Land under roads is land under roadways and road reserves including land under footpaths, nature strips and median strips.

Notes to the financial statements 30 June 2012

15

Note 1 Summary of significant accounting policies (continued) (n) Intangible assets

AASB140(75)(a), (75)(d)

IT development and software

Costs incurred in developing products or systems and costs incurred in acquiring software and licenses that will contribute to future period financial benefits through revenue generation and/or cost reduction are capitalised to software and systems. Costs capitalised include external direct costs of materials and service, direct payroll and payroll related costs of employees’ time spent on the project. Amortisation is calculated on a straight line basis over periods generally ranging from 3 to 10 years.

AASB108(28)(c) AASB140(8)(e) AASB2008-5(68)

IT development costs include only those costs directly attributable to the development phase and are only recognised following completion of technical feasibility and where Council has an intention and ability to use the asset.

AASB101(110) (o) Payables

AASB132(60)(a),(60)(b) These amounts represent liabilities for goods and services provided to the Council prior to the end of financial year which are unpaid. The amounts are unsecured and are usually paid within 30 days of recognition.

AASB101(110) AASB7(21)

(p) Borrowings and borrowing costs

AASB139(43),(47) (Revised)

Borrowings are carried at their principal amounts less amounts repaid. The liabilities are classified as current liabilities unless Council has an unconditional right to defer settlement of the liability for at least 12 months’ after the balance sheet date.

AASB139(39),(41) Interest expense is accrued over the period it becomes due and is recorded as part of other creditors if unpaid at balance sheet date.

(q) Provisions

AASB137(14),(24), (63)

Provisions are recognised when Council has a present legal or constructive obligation as a result of past events, it is probable that an outflow of resources will be required to settle the obligation and the amount has been reliably estimated. Provisions are not recognised for future operating losses.

Where there are a number of similar obligations, the likelihood that an outflow will be required in settlement is determined by considering the class of obligations as a whole. A provision is recognised even if the likelihood of an outflow with respect to any one item included in the same class of obligations may be small.

Provisions are measured at the present value of management’s best estimate of the expenditure required to settle the present obligation at the reporting date. The discount rate used to determine the present value reflects current market assessments of the time value of money and the risks specific to the liability. The increase in the provision due to the passage of time is recognised as interest expense.

(r) Employee benefits

(i) Short-term obligations Liabilities for wages and salaries, including non-monetary benefits, annual leave and accumulating sick leave

expected to be settled within 12 months after the end of the period in which the employees render the related service are recognised in respect of employees' services up to the end of the reporting period and are measured at the amounts expected to be paid when the liabilities are settled. The liability for annual leave and accumulating sick leave is recognised in the provision for employee benefits. All other short-term employee benefit obligations are presented as payables.

(ii) Other long-term employee benefit obligations The liability for long service leave and annual leave which is not expected to be settled within 12 months after

the end of the period in which the employees render the related service is recognised in the provision for employee benefits and measured as the present value of expected future payments to be made in respect of services provided by employees up to the end of the reporting period using the projected unit credit method. Consideration is given to expected future wage and salary levels, experience of employee departures and periods of service. Expected future payments are discounted using market yields at the end of the reporting period on national government bonds with terms to maturity and currency that match, as closely as possible, the estimated future cash outflows.

The obligations are presented as current liabilities in the balance sheet if the entity does not have an unconditional right to defer settlement for at least twelve months after the reporting date, regardless of when the actual settlement is expected to occur.

(iii) Retirement benefit obligations All employees of the Council are entitled to benefits on retirement, disability or death. Council contributes to

various defined benefit plans and defined contribution plans on behalf of its employees. AASB137(36),(45), (47),(60)

Notes to the financial statements 30 June 2012

16

Note 1 Summary of significant accounting policies (continued) (r) Employee benefits (continued)

AASB119(54),(64) A liability or asset in respect of defined benefit superannuation plans would ordinarily be recognised in the balance sheet, and measured as the present value of the defined benefit obligation at the reporting date plus unrecognised actuarial gains (less unrecognised actuarial losses) less the fair value of the superannuation fund’s assets at that date and any unrecognised past service cost. The present value of the defined benefit obligation is based on expected future payments which arise from membership of the fund to the reporting date, calculated annually by independent actuaries using the projected unit credit method. Consideration is given to expected future wage and salary levels, experience of employee departures and periods of service. However, when this information is not reliably available, Council accounts for its obligations to defined benefit plans on the same basis as its obligations to defined contribution plans (see below).

The Local Government Superannuation Scheme has advised member councils that, as a result of the global financial crisis, it has a significant deficiency of assets over liabilities. As a result, they have asked for significant increases in contributions to recover that deficiency. Council’s share of that deficiency cannot be accurately calculated as the Scheme is a mutual arrangement where assets and liabilities are pooled together for all member councils. For this reason, no liability for the deficiency has been recognised in Council’s accounts. Council has, however, disclosed a contingent liability in note 18 to reflect the possible obligation that may arise should the Scheme require immediate payment to correct the deficiency.

AASB119(44) Contributions to defined contribution plans are recognised as an expense as they become payable. Prepaid contributions are recognised as an asset to the extent that a cash refund or a reduction in the future payments is available.

(s) Allocation between current and non-current assets and liabilities

In the determination of whether an asset or liability is current or non-current, consideration is given to the time when each asset or liability is expected to be settled. The asset or liability is classified as current if it is expected to be settled within the ensuring 12 months, being the Council’s operational cycle. In the case of liabilities where Council does not have the unconditional right to defer settlement beyond 12 months, such as vested long service leave, the liability is classified as current even if not expected to be settled within the next 12 months.

(t) Rounding of amounts

Unless otherwise indicated, amounts in the financial statements have been rounded off to the nearest thousand dollars.

(u) New accounting standards and interpretations

Certain new accounting standards and interpretations have been published that are not mandatory for 30 June 2012 reporting periods. Council's assessment of the impact of these new standards and interpretations is set out below.

(i) AASB 9 Financial Instruments, AASB 2009 11 Amendments to Australian Accounting Standards arising from AASB 9 and AASB 2010-7 Amendments to Australian Accounting Standards arising from AASB 9 (December 2010) (effective from 1 January 2013*)

AASB 9 Financial Instruments addresses the classification, measurement and derecognition of financial

assets and financial liabilities. The standard is not applicable until 1 January 2013* but is available for early adoption. When adopted, the standard will affect in particular Council’s accounting for its available-for-sale financial assets, since AASB 9 only permits the recognition of fair value gains and losses in other comprehensive income if they relate to equity investments that are not held for trading. Fair value gains and losses on available-for-sale debt investments, for example, will therefore have to be recognised directly in profit or loss.

There will be no impact on Council’s accounting for financial liabilities, as the new requirements only affect the accounting for financial liabilities that are designated at fair value through profit or loss and Council does not have any such liabilities. The derecognition rules have been transferred from AASB 139 Financial Instruments: Recognition and Measurement and have not been changed.

* In December 2011, the IASB delayed the application date of IFRS 9 to 1 January 2015. The AASB is expected to make an equivalent amendment to AASB 9 shortly.

(ii) AASB 10 Consolidated Financial Statements, AASB 11 Joint Arrangements, AASB 12 Disclosure of Interests in Other Entities, revised AASB 127 Separate Financial Statements and AASB 128 Investments in Associates and Joint Ventures and AASB 2011-7 Amendments to Australian Accounting Standards arising from the Consolidation and Joint Arrangements Standards (effective 1 January 2013)

In August 2011, the AASB issued a suite of five new and amended standards which address the accounting

for joint arrangements, consolidated financial statements and associated disclosures.

Notes to the financial statements 30 June 2012

17

Note 1 Summary of significant accounting policies (continued) (u) New accounting standards and interpretations (continued) AASB 10 replaces all of the guidance on control and consolidation in AASB 127 Consolidated and Separate

Financial Statements, and Interpretation 12 Consolidation – Special Purpose Entities. The core principle that a consolidated entity presents a parent and its subsidiaries as if they are a single economic entity remains unchanged, as do the mechanics of consolidation. However, the standard introduces a single definition of control that applies to all entities. It focuses on the need to have both power and rights or exposure to variable returns. Power is the current ability to direct the activities that significantly influence returns. Returns must vary and can be positive, negative or both. Control exists when the investor can use its power to affect the amount of its returns. There is also new guidance on participating and protective rights and on agent/principal relationships. Council does not expect the new standard to have a significant impact on its composition.

AASB 11 introduces a principles based approach to accounting for joint arrangements. The focus is no longer on the legal structure of joint arrangements, but rather on how rights and obligations are shared by the parties to the joint arrangement. Based on the assessment of rights and obligations, a joint arrangement will be classified as either a joint operation or a joint venture. Joint ventures are accounted for using the equity method, and the choice to proportionately consolidate will no longer be permitted. Parties to a joint operation will account their share of revenues, expenses, assets and liabilities in much the same way as under the previous standard. AASB 11 also provides guidance for parties that participate in joint arrangements but do not share joint control.

Council's investment in the joint venture partnership will be classified as a joint venture under the new rules. As Council already applies the equity method in accounting for this investment, AASB 11 will not have any impact on the amounts recognised in its financial statements.

AASB 12 sets out the required disclosures for entities reporting under the two new standards, AASB 10 and AASB 11, and replaces the disclosure requirements currently found in AASB 127 and AASB 128. Application of this standard by Council will not affect any of the amounts recognised in the financial statements, but will impact the type of information disclosed in relation to Council's investments.

Amendments to AASB 128 provide clarification that an entity continues to apply the equity method and does not remeasure its retained interest as part of ownership changes where a joint venture becomes an associate, and vice versa. The amendments also introduce a “partial disposal” concept. Council is still assessing the impact of these amendments.

Council does not expect to adopt the new standards before their operative date. They would therefore be first applied in the financial statements for the annual reporting period ending 30 June 2014.

(iii) AASB 13 Fair Value Measurement and AASB 2011-8 Amendments to Australian Accounting Standards arising from AASB 13 (effective 1 January 2013)

AASB 13 was released in September 2011. It explains how to measure fair value and aims to enhance fair

value disclosures. Council has yet to determine which, if any, of its current measurement techniques will have to change as a result of the new guidance. It is therefore not possible to state the impact, if any, of the new rules on any of the amounts recognised in the financial statements. However, application of the new standard will impact the type of information disclosed in the notes to the financial statements. Council does not intend to adopt the new standard before its operative date, which means that it would be first applied in the annual reporting period ending 30 June 2014.

(iv) Revised AASB 119 Employee Benefits, AASB 2011-10 Amendments to Australian Accounting Standards arising from AASB 119 (September 2011) and AASB 2011-11 Amendments to AASB 119 (September 2011) arising from Reduced Disclosure Requirements (effective 1 January 2013)

In September 2011, the AASB released a revised standard on accounting for employee benefits. It requires

the recognition of all remeasurements of defined benefit liabilities/assets immediately in other comprehensive income (removal of the so-called 'corridor' method) and the calculation of a net interest expense or income by applying the discount rate to the net defined benefit liability or asset. This replaces the expected return on plan assets that is currently included in profit or loss. The standard also introduces a number of additional disclosures for defined benefit liabilities/assets and could affect the timing of the recognition of termination benefits. The amendments will have to be implemented retrospectively. Council does not recognise defined benefit assets and liabilities for the reasons set out in note 1 (r)(iii) and so these changes will not have an impact on its reported results.

There are no other standards that are not yet effective and that are expected to have a material impact on the entity in the current or future reporting periods and on foreseeable future transactions.

Notes to the financial statements 30 June 2012

18

Note 1 Summary of significant accounting policies (continued) (v) Crown Reserves Crown Reserves under Council’s care and control are recognised as assets of the Council. While ownership of

the reserves remains with the Crown, Council retains operational control of the reserves and is responsible for their maintenance and use in accordance with the specific purposes to which the reserves are dedicated.

Improvements on Crown Reserves are also recorded as assets, while maintenance costs incurred by Council and revenues relating the reserves are recognised within Council’s Income Statement.

Representations from both State and Local Government are being sought to develop a consistent accounting treatment for Crown Reserves across both tiers of government.

(w) Goods and Services Tax (GST) Revenues, expenses and assets are recognised net of the amount of associated GST, unless the GST

incurred is not recoverable from the taxation authority. In this case it is recognised as part of the cost of acquisition of the asset or as part of the expense.

Receivables and payables are stated inclusive of the amount of GST receivable or payable. The net amount of GST recoverable from, or payable to, the taxation authority is included with other receivables or payables in the balance sheet.

Cash flows are presented on a gross basis. The GST components of cash flows arising from investing or financing activities which are recoverable from, or payable to the taxation authority, are presented as operating cash flows.

Notes to the financial statements 30 June 2012

19

Note 2(a) Functions or activities Income, expenses and assets have been directly attributed to the following functions or activities. Details of those functions or activities are

provided in Note 2(b).

Income from continuing operations

Expenses from continuing operations

Operating results from continuing operations

Grants included in income from

continuing operations

Total assets held (current and non-

current) Original

budget 2012 $’000

Actual 2012 $’000

Actual 2011 $’000

Original budget

2012 $’000

Actual 2012 $’000

Actual 2011 $’000

Original budget

2012 $’000

Actual 2012 $’000

Actual 2011 $’000

Actual 2012 $’000

Actual 2011 $’000

Actual 2012 $’000

Actual 2011 $’000

Functions/Activities

City Operations 18,391 22,026 18,407 33,031 36,811 31,947 (14,640) (14,785) (13,540) 978 1,801 18,410 21,141 City Planning and

Development 4,087 4,165 4,657 6,470 6,930 6,094 (2,383) (2,765) (1,437) 701 1,379 889 1,743 Corporate and

Community Services 1,391 1,448 1,407 12,465 12,863 12,992 (11,074) (11,415)

(11,585) 629 624 10,960 8,479 Governance - - - 317 295 758 (317) (295) (758) - - 252 243 General Manager 10 114 30 2,621 2,882 1,845 (2,611) (2,768) (1,815) - - 220 535 Infrastructure and

unallocated corporate costs 289 282 275 19,632 19,524 18,280 (19,343) (19,242) (18,005) 282 275 825,900 830,152

Total functions & activities 24,168 28,035 24,776 74,536 79,305 71,916 (50,368) (51,270) (47,140) 2,590 4,079 856,631 862,293

Shares of gains or (losses) in joint ventures using the equity method - 468 445 - - - - 468 445 - - 1,494 1,026

General purpose revenue (1) 44,093 46,486 43,790 572 420 319 43,521 46,066 43,471 3,916 2,767 7,612 9,136

Capital purpose revenue 6,699 4,108 6,763 - 1,822 - 6,699 2,286 6,763 1,114 2,537 - -

Net operating result for the year 74,960 79,097 75,774 75,108 81,547 72,235 (148) (2,450) 3,539 7,620 9,383 865,737 872,455

Note: (1) Rates and annual charges, interest and investment revenue.

Notes to the financial statements 30 June 2012

20

Note 2(b) Components of functions or activities

The activities relating to the Council’s functions reported in Note 2(a) are as follows:

City Operations Construction and maintenance of: • Community buildings • Playing fields and playgrounds • Parks and gardens • Beach facilities • Town centres • Road and bridges • Drainage • Footpaths Services including: • Parking and regulations • Tree services • Environmental protection • Waste services • Public health inspections • Traffic management and road safety • Asset design and inspection • Supply and fleet management City Planning and Development • Strategic asset management • Urban and environmental strategy • Town centres management • Building certification and compliance • Development assessment

Corporate and Community Services • Document management • Financial and administrative management • Information technology and information services • Youth services • Governance • Community relations • Recreation and cultural services • Library and information services • Community and customer service • Age and disability services • Multicultural services General Manager’s Department • Corporate leadership • Human resource management • City media and events Governance This unit is focused on supporting the Executive of Council, the functioning of the office of the Mayor,

operational support for councillors and the performance of their civic duties and corporate governance issues.

Infrastructure and unallocated corporate costs These costs include loan servicing, depreciation expense of infrastructure assets and contributions to

government departments including fire and rescue and state emergency services.

General purpose revenue General purpose revenue includes rates levied on residential, business, and farmland properties, general

purpose grants and interest on investments.

Capital purpose revenue Capital purpose revenue includes grants received for capital expenditure purposes and contributions from

developers under section 94 of the Environmental Planning and Assessment Act (1979).

Notes to the financial statements 30 June 2012

21

Note 3 Income from continuing operations

Actual 2012 $’000

Actual 2011 $’000

(a) Rates and annual charges Ordinary rates Residential 29,406 28,445 Business 4,541 4,405 Farmland 6 6 Total ordinary rates 33,953 32,856

Special rates Local Area Rates 434 426 Community Safety Levy 343 333 Stormwater Levy 798 798 Infrastructure Levy 1,375 1,328 Community Building Levy 1,105 1,074 Total special rates 4,055 3,959 Annual charges (pursuant to s.496, s.501 & s.502) Domestic waste management services 12,749 11,974 Total annual charges 12,749 11,974 Total rates and annual charges 50,757 48,789 Council has used 1/7/2009 valuations provided by the NSW Valuer General in calculating its rates.

(b) User charges and fees User charges (pursuant to s.502) Non-Rateable Waste Management 216 157 Non-Domestic Waste Management 636 624 Total user charges 852 781

Fees Regulatory and statutory fees Building Inspections 126 164 Building Consents and Construction Certificate 84 119 Rating Certificate Fees 135 116 Development & Planning Consent Fees 794 707 Zoning Certificate Fees (section 149) 237 188 Health Inspection & Approvals Fees 282 191 Others 21 41 Total regulatory and statutory fees 1,679 1,526 Discretionary fees Meals on Wheels Fees 195 208 Restoration & Road Opening Fee 5,067 1,743 Environmental Enforcement Fees 230 255 Engineering Inspections & Other Fees 77 89 Street Furniture Advertising Fee 63 65 Permits & Inspection Fees 187 262 Library Fees & Charges 75 85 Others 272 246

Total discretionary fees 6,166 2,953

Total user charges and fees 8,697 5,260

Notes to the financial statements 30 June 2012

22

Note 3 Income from continuing operations (continued)

Actual 2012 $’000

Actual 2011 $’000

(c) Interest and investment revenue

Interest on deposits and investments 3,192 2,689

Interest on overdue rates & charges 209 155 Fair value movements in investments 1,030 1,150

Total interest and investment revenue (losses)(1) 4,431 3,994

(d) Other revenues Fines - Car Parking Infringements 1,582 1,277 - Other 108 118 Rental Income - Residential & Commercial Property 1,271 1,169 - Halls & Community Facilities 163 192 - Parks & Sporting Facilities 424 505 Others 1,035 1,000

Total other revenue 4,583 4,261 Note:

(1) Where interest and investment revenue nets to an overall loss, this is carried to the interest and investment losses line on the Income statement.

Notes to the financial statements 30 June 2012

23

Note 3 Income from continuing operations (continued) Operating Capital

Actual 2012 $’000

Actual 2011 $’000

Actual 2012 $’000

Actual 2011 $’000

(e) Grants

General Purpose (Untied) Financial Assistance 2,622 2,042 - - Pensioner’ Rates Subsidies 681 726 - - LGGC Financial Assistance – Local Road 943 727 - - 4,246 3,495 - - Special Purpose Pensioners’ Rate Subsidies (DWM) 280 279 - - RTA Roads & Traffic 383 425 330 111 Library Assistance Grant 289 253 - - Street Lighting Subsidy 282 275 - - Meals on Wheels Subsidy 230 224 - - Roads to Recovery - - 377 398 Drainage - - 20 160 Waterway & Foreshore Improvements - - - (53) Parks - - 208 1,202 Natural Disaster Mitigation Grant - - - - Federal Government Infrastructure Program - - - 1,752 Others 934 729 41 133 2,398 2,185 976 3,703 Total Grants 6,644 5,680 976 3,703 Comprising: - Commonwealth Funding 3,596 3,787 208 1,472 - State Funding 3,016 1,893 768 2,231 - Other Funding 32 - - - 6,644 5,680 976 3,703

(f) Contributions

Developer Contributions: - Open Space - - 1,057 1,941 - Community Facilities - - 124 148 - Stormwater - - 131 94 - Pollution Control - - 113 180 - Traffic Facilities - - 237 244 - Town Centre Improvements - - 124 132 - Local Infrastructure and Facilities - - 108 16 - Other Section 94 Fees - - 74 154 Other Contributions 95 180 6 101 Section 94A Levies - - 472 377 Total Contributions 95 180 2,446 3,387 Total Grants and Contributions 6,739 5,860 3,422 7,090

Notes to the financial statements 30 June 2012

24

Note 3 Income from continuing operations (continued)

Actual 2012 $’000

Actual 2011 $’000

(g) Restrictions relating to grants and contributions Certain grants and contributions are obtained by Council on the condition

they be spent in a specified manner: Grants and contributions recognised in the current period which have not

been spent 6,074 7,824 Less: Grants and contributions recognised in previous reporting periods which

have been spent in the current reporting period 3,486 3,884 Net increase in restricted grants and contributions 2,588 3,940

Notes to the financial statements 30 June 2012

25

Note 4 Expenses from continuing operations

Actual 2012 $’000

Actual 2011 $’000

(a) Employee benefits and on costs

Salaries and wages 21,652 20,489 Travelling 17 29 Employee leave entitlements 4,176 3,607 Superannuation 2,685 2,868 Workers’ Compensation Insurance 1,172 850 FBT 148 162 Training and seminars 323 299 Occupational health & safety 72 21 Others 69 153 Less: Capitalised costs (450) (522) Total employee costs expensed 29,864 27,956

Number of FTE employees 349 351

(b) Borrowing costs Interest on loans 312 378 Amortisation of premium on interest free loans 42 - Less: Capitalised costs - - Total borrowing costs expensed 354 378

(c) Materials and contracts Printing and stationery 660 853 Computer maintenance 860 772 Roads, parks and property maintenance 6,693 3,296 Recycling contract 1,228 1,186 Waste collection and disposal 9,247 7,648 Community safety, vandalism and graffiti program 104 108 Design and planning 116 11 Other contractor and consultancy 3,572 3,167 Remuneration of Auditors(1) 95 47 Legal fees: – Planning and development 27 158 – Other 390 196 Total materials and contracts 22,992 17,442

(1) During the year the following fees were paid or payable for services provided by the Council’s auditor – PricewaterhouseCoopers:

(i) Audit and other assurance services AASB1054(10)(a) Audit and review of financial statements 51 47 Total remuneration for audit and other assurance services 51 47 AASB1054(10)(b),(11) (ii) Taxation services GST advice 10 - Total remuneration for taxation services 10 - AASB1054(10)(b),(11) (iii) Other services Peer review 34 - Total remuneration for other services 34 - Total remuneration of Pricewaterhousecoopers 95 47

Notes to the financial statements 30 June 2012

26

Note 4 Expenses from continuing operations (continued)

Actual 2012 $’000

Actual 2011 $’000

(d) Depreciation, amortisation and

impairment

Plant and equipment 1,231 1,213 Computer & Office equipment 209 171 Intangibles - software 404 448 Furniture and fittings 72 66 Buildings – Non specialised 882 879 – Specialised 3,712 3,711 Depreciable land improvements 1,695 548 Other structures 593 646 Infrastructure: – roads, bridges and footpaths 8,055 7,992 – stormwater drainage 998 994 Other assets: – library books 379 369 Total depreciation, amortisation and impairment 18,230 17,037

(e) Other expenses

Other expenses for the year including the following: Food and beverages 215 231 Advertising 260 177 Bad and doubtful debts (45) 164 Communications 320 385 Mayoral fees 35 34 Councillors’ fees 237 241 Councillors’ (incl. Mayor) expenses 288 315 Donations and subsidies 161 205 Fees and charges 330 272 Property expenses 474 556 Insurance 1,425 1,373 Contributions and levies 1,435 1,442 Street lighting 1,799 1,688 Utilities/rates/charges 868 710 Postage and courier 150 104 Motor vehicle expenses 912 886 Rental contribution and subsidies 63 112 External hire charges 380 36 Others 640 491 Total other expenses from continuing operations 9,947 9,422

Notes to the financial statements 30 June 2012

27

Note 5 Gain or loss from the disposal of assets

Actual 2012 $’000

Actual 2011 $’000

Gain (or loss) on disposal of property Proceeds from disposal - - Less: carrying amount of assets sold - - Gain (or loss) on disposal - - (Loss) or gain on disposal of infrastructure, plant and equipment Proceeds from disposal 991 868 Less: carrying amount of assets sold 1,127 793 (Loss) or gain on disposal (136) 75 (Loss) or gain on disposal of intangible assets Proceeds from disposal - - Less: carrying amount of assets sold 24 - (Loss) or gain on disposal (24) - Gain (or loss) on disposal of financial assets Proceeds from disposal 3,000 10,361 Transfer to cash equivalent 15,350 - Less: carrying value of financial assets 18,350 10,361 Gain (or loss) on disposal - - Net (loss) or gain from disposal of assets (160) 75

Notes to the financial statements 30 June 2012

28

Note 6(a) Cash and cash equivalents

Actual 2012

Actual 2011

$'000 $'000 Cash at bank and on hand 3,769 5,030 Deposits at call 54,892 31,100 58,661 36,130

Notes to the financial statements 30 June 2012

29

Note 6(b) Investments The following financial assets are held as investments:

Actual 2012

Actual 2011

Current $’000

Non-current $’000

Current $’000

Non-current $’000

Financial assets at fair value through Profit and Loss(1) 6,004 5,016

5,947 18,393

Held to maturity investments - - - - Available for sale financial assets(1) - - - - Total 6,004 5,016 5,947 18,393 Financial assets at fair value through

Profit and Loss

At beginning of year 5,947 18,393 4,117 16,445 Revaluation to income statement 57 973 1,150 - Additions 3,000 1000 11,041 1,948 Disposals (3,000) - (10,361) - Transfer:current/ non-current investment 1,000 (1,000) - - Transfer to cash equivalent (1,000) (14,350) - - At end of year 6,004 5,016 5,947 18,393 Comprising of: – Notes (fixed and floating rates) 6,004 5,011 5,947 6,366 – Other - 5 - 5 – Equity linked notes - - - 12,022 6,004 5,016 5,947 18,393

Note: (1) Fair values for all investments in this Category are determined by quoted prices in active markets for

identical investments.

Notes to the financial statements 30 June 2012

30

Note 6(c) Restricted cash, cash equivalents and investments

Actual 2012

Actual 2011

Current $’000

Non-current $’000

Current $’000

Non-current $’000

Total cash, cash equivalents and investments 64,665 5,016

42,077 18,393

External restrictions 42,643 5,016 24,115 18,393 Internal restrictions 21,022 - 16,962 - Unrestricted 1,000 - 1,000 - 64,665 5,016 42,077 18,393

Notes

Opening balance

01/07/2011 $’000

Transfers to restrictions

$’000

Transfers from restrictions

$’000

Closing balance

30/06/2012 $’000

External restrictions Developer Contributions (A) 17 21,739 3,941 932 24,748 Unexpended Grant Funds (B) 3,752 2,495 2,915 3,332 Domestic Waste Management (C) 4,957 316 - 5,273 Local Area Funds (C) 9,048 1,035 305 9,778 Stormwater Levy (C) 544 799 604 739 Infrastructure Levy Reserve (C) 2,358 2,483 1,213 3,628 Community Safety Levy (C) 110 334 283 161 Total external restrictions 42,508 11,403 6,252 47,659

Internal restrictions Employee Entitlements 2,919 1,278 - 4,197 Plant & Equipment 599 - - 599 Office Equipment & IT Reserve 1,197 471 - 1,668 Open Space and s94 Obligations 1,735 1,000 433 2,302 Central Library 2,274 - 199 2,075 Loan Fund Reserve 1,122 - 19 1,103 Bexley Pool Complex 763 - 129 634 Public Liability Claims 36 350 - 386 Workers Compensation 130 250 264 116 Council Election 252 142 - 394 Council Buildings 637 50 687 - Capital Works Revote 559 572 559 572 Interest Equalisation 230 1,383 - 1,613 Strategic Priorities 4,306 1,340 906 4,740 Street Lighting Hardware 112 - 40 72 Revolving Energy Fund 4 - - 4 Brighton Bath Amenities Building 87 460 - 547 Total internal restrictions 16,962 7,296 3,236 21,022 Total restrictions 59,470 18,699 9,488 68,681

A Development contributions which are not yet expended for the provision of services and amenities in accordance with contributions plans.

B Grants which are not yet expended for the purposes for which the grants were obtained. (See Note 1b) C These funds are externally restricted asset which must be applied for the purposes for which they were

raised.

Notes to the financial statements 30 June 2012

31

Note 7 Receivables

Actual 2012

Actual 2011

Purpose

Current $’000

Non-current $’000

Current $’000

Non-current $’000

Rates and annual charges - Levies 2,974 - 2,818 - - Interest 426 - 384 - Interest on investment 569 - 439 - User charges and fees 4 - 8 - Government grants and subsidies 367 - 1,700 - GST refund from ATO 443 - 280 - Sundry debtors 1,260 445 1,894 678 Total 6,043 445 7,523 678 Less: Provision for doubtful debts: – Rates and annual charges 46 - 42 - – Interest and extra charges 40 - 35 - – User charges and fees 3 - 3 - – Other doubtful debts 141 - 195 - 230 - 275 - 5,813 445 7,248 678

Restricted receivables

Externally restricted receivables Domestic waste receivable 750 - 715 - Stormwater levy receivable 44 - 43 - Local area waste receivable 24 - 35 - Total externally restricted receivables 818 - 793 - Unrestricted receivables 4,995 445 6,455 678 Total receivables 5,813 445 7,248 678

Notes to the financial statements 30 June 2012

32

Note 8 Inventories and other assets

Actual 2012

Actual 2011

Current $’000

Non-current $’000

Current $’000

Non-current $’000

Inventories Stores and materials 50 - 56 - Total inventories 50 - 56 - Inventories not expected to be realised

within the next 12 months - -

- - Other assets Prepayments 663 380 604 443 Total other assets 663 380 604 443 Externally restricted inventories and

other assets

Domestic waste management Stores and materials - - - - Prepayments - - - - Total domestic waste management - - - -

Notes to the financial statements 30 June 2012

33

Note 9(a) Infrastructure, property, plant and equipment At 30 June 2011 Movements during year At 30 June 2012

By asset type

Cost/Deemed cost $’000

Fair value $’000

Accumulated Depreciation

$’000

Written Down Value $’000

Transfers/Adjust-ments $’000

Additions $’000

WDV of Disposal

$’000

Depreciation Expenses

$’000

Accumulated Depreciation Adjustment

(Revaluation) $’000

Revaluation Increment/

(Decrement) $’000

Cost/Deemed cost $’000

Fair value $’000

Accumulated Depreciation

$’000

Written Down Value $’000

Capital Work in Progress 12,700 - - 12,700 (5,557) 5,828 - - - - 12,971 - - 12,971 Plant and Equipment - 9,781 (4,608) 5,173 153 1,833 (906) (1,231) - - - 9,502 (4,479) 5,023 Computer & Office Equipment - 3,035 (2,250) 785 11 188 (1) (209) - - - 1,358 (583) 775 Furniture and Fittings - 1,598 (1,139) 459 - - - (72) - - - 1,598 (1,211) 387 Land: – Operational Land - 126,180 - 126,180 - 430 (220) - - - - 126,389 - 126,389 – Community Land - 101,469 - 101,469 - - - - - (609) - 100,860 - 100,860 Buildings – Non specialised - 27,755 (13,698) 14,057 - - - (882) - - - 27,755 (14,580) 13,175 – Specialised - 123,231 (66,288) 56,943 398 - - (3,712) - - - 123,630 (69,999) 53,631 Depreciable Land Improvements - 74,474 (10,847) 63,627 (15,172) - - (1,695) - (3,818) - 52,290 (9,348) 42,942 Structure (non-buildings) - - - - 13,909 - - (593) - - - 16,338 (3,024) 13,314 Infrastructure: – Roads, Bridges, Footpaths - 443,560 (201,158) 242,402 4,948 - - (8,055) - - - 448,704 (209,412) 239,292

– Bulk Earthworks (non-depreciable) - 124,711 - 124,711 - - -

- - - - 124,711 - 124,711

– Stormwater Drainage - 90,923 (40,698) 50,225 948 - - (998) - - - 91,871 (41,695) 50,176 Other assets: – Library Books - 3,045 (1,800) 1,245 - 364 - (379) - - - 3,409 (2,179) 1,230 12,700 1,129,762 (342,486) 799,976 (362) 8,643 (1,127) (17,826) - (4,427) 12,971 1,128,415 (356,510) 784,876

Notes: • Exclude investment properties and non-current assets held for sale. • Additions to Buildings and Infrastructure are made up of Asset Renewals ($3,388) and New Assets ($2,861). Renewals are defined as replacements of existing assets with equivalent capacity or

performance as opposed to the acquisition of new assets. • Transfers and assets disposed of are stated in written-down values (cost/deemed costs less accumulated depreciation).

Notes to the financial statements 30 June 2012

34

Note 9(b) Restricted infrastructure, property, plant and equipment

At 30 June 2011

Movements during the year

At 30 June 2012

By asset type

Cost/ Deemed Cost $’000

Fair Value $’000

Accumulated Depreciation

$’000

WDV $’000

Transfers $’000

Additions $’000

Adjustments $’000

WDV of Disposals

$’000

Depreciation Expenses

$’000

Cost/ Deemed Cost $’000

Fair value $’000

Accumulated Depreciation

$’000

Written Down Value $’000

Domestic Waste Management Garbage and Recycling Containers

- 2,092 (1,779) 313 - 228

69 - (28)

- 467 (114) 353

Total Restrictions

- 2,092 (1,779) 313 - 228

69 - (28) - 467 (114) 353

Notes to the financial statements 30 June 2012

35

Note 10(a) Payables, borrowings and provisions

Actual 2012

Actual 2011

Current $’000

Non-current $’000

Current $’000

Non-current $’000

Payables Goods and services 1,772 - 1,228 - Payments received in advance 238 - 788 - Accrued expenses 1,260 - 1,706 - Deposits and retentions 3,727 - 3,620 - Other 121 - 38 - Total payables 7,118 - 7,380 - Current payables not expected to be

settled within the next 12 months 2,430 -

1,692 - Borrowings Loans – secured(1) 954 4,909 964 4,989 Total interest bearing liabilities 954 4,909 964 4,989 Provisions(2) Annual leave 3,375 - 3,263 - Sick leave 1,129 - 1,251 - Long service leave 5,532 922 5,460 780 Gratuities 158 241 146 212 Public liability under excess - 296 148 148 Total provisions 10,194 1,459 10,268 1,140 Current provisions not expected to be

settled within the next 12 months 6,538 -

7,615 - Liabilities relating to restricted assets Domestic waste management 728 - 1,210 - Total 728 - 1,210 - Notes:

(1) Loans are secured over the income of Council. (2) Vested ELE is all carried as a current provision.

Notes to the financial statements 30 June 2012

36

Note 10(b) Description of and movements in provisions

Class of provision

Opening balance

$’000

Increases in provision

$’000 Payments

$’000

Re-measurement

$’000

Closing balance

$’000

Annual leave 3,263 2,068 1,955 - 3,376 Sick leave 1,251 12 135 - 1,128 Long service leave 6,240 1,584 1,370 - 6,454 Gratuities 358 41 - - 399 Public liability under

excess 296 - - - 296 Total 11,408 3,705 3,460 - 11,653

Notes to the financial statements 30 June 2012

37

Note 11 Reconciliation of operating result to net cash movement from operating activities

Notes

Actual 2012 $’000

Actual 2011 ’000

(a) Reconciliation of cash assets

Total cash and cash equivalents 6a 58,661 36,130 Less: Bank overdraft - - Balances as per cash flow statement 58,661 36,130 (b) Reconciliation of net operating result to cash

provided from operating activities

Net operating (loss) profit from income statement (2,450) 3,539 Add: Depreciation and impairment 18,230 17,037 Decrease in receivables 1,669 - Decrease in inventories 6 9 Decrease in other assets 4 - Increase in payables - 1,580 Increase in provisions 243 325 Loss on disposal of assets 160 - Amortisation of premium recongnised on interest free loans 42 - Less: Increase in receivables - 2,021 Increase in other assets - 121 Decrease in payables 262 - Share of profit in joint ventures 468 445 Gain on disposal of assets - 75 Investment revaluation increment 1,030 1,149 Net cash provided from operating activities (from cash

flow statement)

16,144 18,679 (c) Non-cash financing and investing activities

Acquisition of plant and equipment by means of finance

leases

- - S.94 contributions in kind - - Dedications - - - - (d) Financing arrangements

Unrestricted access was available at balance date to the

following:

Bank overdraft facility(1) 350 350 Corporate credit cards 60 60 410 410

Notes: (1) The Bank overdraft facility may be drawn at any time and may be terminated by the bank without notice. (2) Interest rates on overdrafts are variable while the rates for loans are set for the period of the loan.

Notes to the financial statements 30 June 2012

38

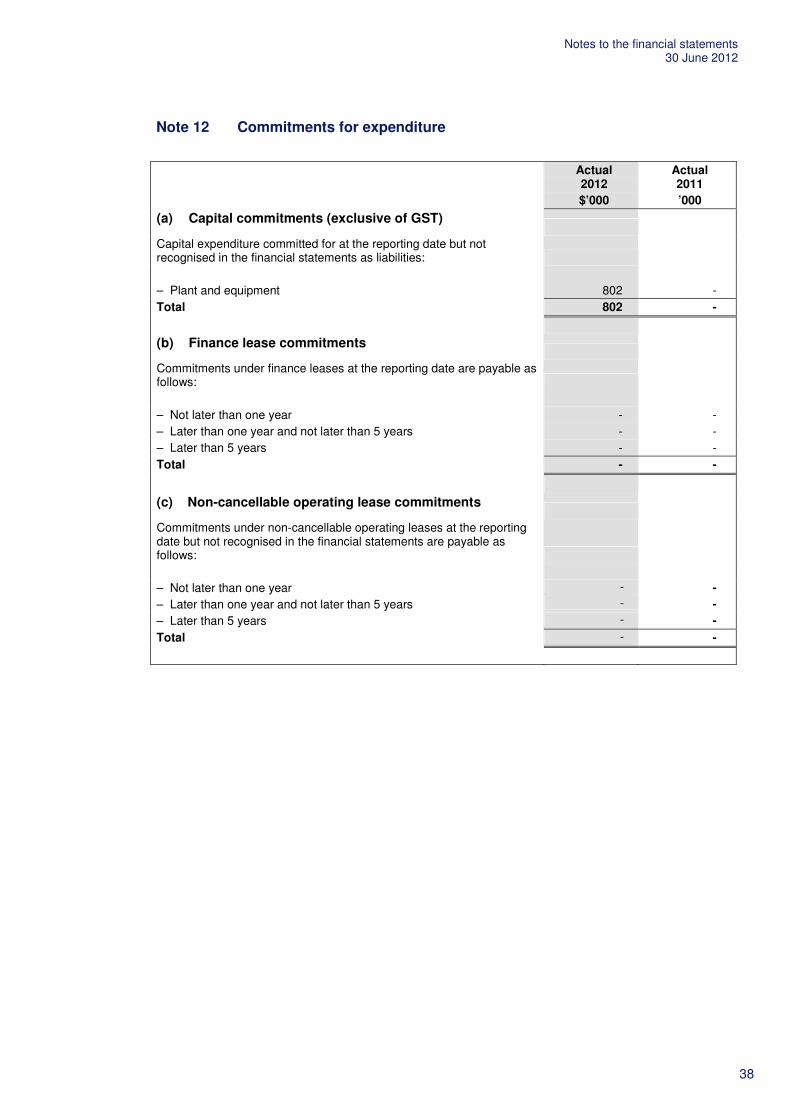

Note 12 Commitments for expenditure

Actual 2012 $’000

Actual 2011 ’000

(a) Capital commitments (exclusive of GST)

Capital expenditure committed for at the reporting date but not recognised in the financial statements as liabilities:

– Plant and equipment 802 - Total 802 - (b) Finance lease commitments

Commitments under finance leases at the reporting date are payable as

follows: – Not later than one year - - – Later than one year and not later than 5 years - - – Later than 5 years - - Total - - (c) Non-cancellable operating lease commitments

Commitments under non-cancellable operating leases at the reporting

date but not recognised in the financial statements are payable as follows:

– Not later than one year - - – Later than one year and not later than 5 years - - – Later than 5 years - - Total - -

Notes to the financial statements 30 June 2012

39

Note 13 Statement of performance measures – Consolidated results

2012 Amounts

$’000

Current year

indicators 2011 2010 1. Unrestricted current ratio Current assets less all external restrictions(1) $ 27,731 3.24 3.10 4.31 Current liabilities less specific purpose

liabilities(2), (3), (4) $ 8,568

2. Debt service ratio Debt service cost $ 1,276 0.02 0.02 0.02 Income from continuing operations

excluding capital items and specific purpose grants/contributions

$ 73,181

3. Rate coverage ratio Rates and annual charges $ 50,756 0.64 0.64 0.62 Income from continuing operations $ 79,096 4. Rates and annual charges

outstanding percentage

Rates and annual charges outstanding $ 3,314 6.13%

6.05% 5.63% Rates and annual charges collectible $ 54,082 5. Building and infrastructure renewals

ratio(5)

Asset renewals (building and infrastructure) $ 3,388 0.21 0.17 0.36 Depreciation, amortisation and impairment

(building and infrastructure) $ 15,934

Notes:

(1) Refer to Notes 6-8 inclusive. (2) Refer to Note 10(a). (3) $6.5 million provisions not expected to be settled deducted. (4) $2.4 million payables not expected to be settled deducted. (5) Refer Note 9(a) – Notes.

Notes to the financial statements 30 June 2012

40

Note 14 Investment properties

Actual 2012 $’000

Actual 2011 $’000

At fair value AASB140(76) Opening balance at 1 July 2011 - - AASB140(76)(a) Acquisitions - - AASB140(76)(a) Capitalised subsequent expenditure - - AASB140(76)(c) Classified as held for sale or disposals - - AASB140(76)(d) Net gain (loss) from fair value adjustment - - AASB140(76)(f) Transfer (to) from inventories and owner occupied property - - AASB140(76) Closing balance at 30 June 2012 - -

AASB140(75)(f)

(a) Amounts recognised in profit and loss for investment property AASB140(75)(f)(i) Rental income - - Net gain (loss) from fair value adjustment - - AASB140(75)(f)(ii) Direct operating expenses from property that generated rental income - - AASB140(75)(f)(iii) Direct operating expenses from property that did not generate rental income - - - -

(b) Valuation basis AASB140(75)(a),(d),(e) N/A

AASB140(75)(h) (c) Contractual obligations

N/A

AASB117(56)(c) (d) Leasing arrangements

N/A

Notes to the financial statements 30 June 2012

41

Revised Note 15 Financial risk management

Risk management

Council’s activities expose it to a variety of financial risks including price risk, credit risk, liquidity risk and interest rate risk. The Council's overall risk management program focuses on the unpredictability of financial markets and seeks to minimise potential adverse effects on the financial performance of the Council.

Council does not engage in transactions expressed in foreign currencies and is therefore not subject to foreign currency risk.

Financial risk management is carried out by the Finance Section under policies approved by the Council.

Council held the following financial instruments at balance date:

Carrying value Fair value

2012 $’000

2011 $’000

2012 $’000

2011 $’000

Financial assets Cash and cash equivalents 58,661 36,130 58,661 36,130 Receivables 6,258 7,926 6,258 7,926 Financial assets at fair value through profit

or loss 11,020 24,340

11,020 24,340 Available-for-sale financial assets - - - - Held-to-maturity investments - - - - 75,939 68,396 75,939 68,396

Financial liabilities Payables 7,118 7,380 7,118 7,380 Borrowings 5,863 5,953 5,863 5,657 12,981 13,333 12,981 13,037 Fair value is determined as follows:

• Cash and Cash Equivalents, Receivables, Payables – estimated to be the carrying value which approximates net market value.