3. 22 Break-Even Analysis. 3.22 Calculating a break-even point Terminology Sales Revenue / Income...

27

3 . 22 Break-Even Analysis

-

Upload

felix-cain -

Category

Documents

-

view

221 -

download

0

Transcript of 3. 22 Break-Even Analysis. 3.22 Calculating a break-even point Terminology Sales Revenue / Income...

3.22

Break-Even Analysis

3.22 Calculating a break-even point

Terminology

Sales Revenue / Income – The amount of money a company takes from selling goods or services.

– Quantity sold x Sale price of each item

Costs / Expenditure – The money that businesses spends while they trade.

– There are fixed, variable and total costs

Profit (or loss). The amount of money a business makes (or loses) from carrying out their trade.

– Sales Revenue – Total Costs.

3.22 Calculating a break-even point

The basics of break-even analysis 1

Businesses must make a profit to survive

To make a profit, income must be higher than expenditure (or costs)

Income £50,000 Costs £40,000

Profit £10,000

Income £50,000 Costs £60,000

Loss £10,000

3.22 Calculating a break-even point

The basics of break-even analysis 2

There are two types of costs:

Variable costs increase by a step every time an extra product is sold (eg cost of ice cream cornets in ice cream shop)

Fixed costs have to be paid even if no products are sold (eg rent of ice cream shop)

3.22 Calculating a break-even point

Examples of costs

Variable: materials, labour, energy

Fixed: rent, business rates, interest on loans, insurance, staff costs (e.g. security)

These vary, depending upon the type of business. Typical costs include:

3.22 Calculating a break-even point

The break-Even Point

Variable costs + fixed costs = total costs

When total costs = sales revenue,

– This is called the break-even point,

– eg– total costs = £5,000

– total sales revenue = £5,000

At this point the business isn’t making a profit or a loss – it is simply breaking even.

3.22 Calculating a break-even point

Why calculate break-even?

Tom can hire an ice-cream van for an afternoon at a summer fete. The van hire will be £100 and the cost of cornets, ice cream etc will 50p per ice cream.

Tom thinks a sensible selling price will be £1.50.

At this price, how many ice-creams must he sell to cover his costs?

Calculating this will help Tom to decide if the idea is worthwhile.

3.22 Calculating a break-even point

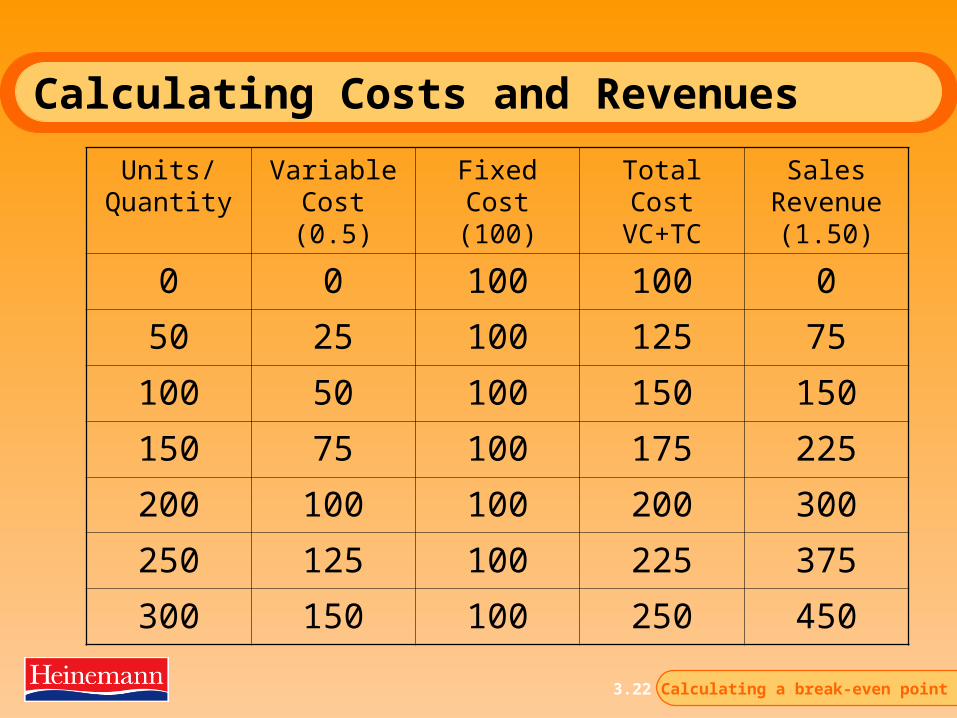

Calculating Costs and Revenues

Units/ Quantity

Variable Cost (0.5)

Fixed Cost(100)

Total CostVC+TC

Sales Revenue

(1.50)

0

50

100

150

200

250

300

3.22 Calculating a break-even point

Calculating Costs and Revenues

Units/ Quantity

Variable Cost (0.5)

Fixed Cost(100)

Total CostVC+TC

Sales Revenue

(1.50)

0 0 100 100 0

50 25 100 125 75

100 50 100 150 150

150 75 100 175 225

200 100 100 200 300

250 125 100 225 375

300 150 100 250 450

3.22 Calculating a break-even point

Drawing a break-even chart 1

Tom's ice creams

050

100150200250300350400450

0 100 200 300

Number sold

Co

st/

Re

ve

nu

e £

3.22 Calculating a break-even point

Drawing a break-even chart 2

Tom's ice creams

050

100150200250300350400450

0 100 200 300

Number sold

Co

st/

Re

ve

nu

e £

Fixed Cost

3.22 Calculating a break-even point

Drawing a break-even chart 3

Tom's ice creams

050

100150200250300350400450

0 100 200 300

Number sold

Co

st/

Re

ve

nu

e £

Total Cost

Fixed Cost

3.22 Calculating a break-even point

Drawing a break-even chart 4

Tom's ice creams

050

100150200250300350400450

0 100 200 300

Number sold

Co

st/R

even

ue

£

Sales Revenue

Total Cost

Fixed Cost

3.22 Calculating a break-even point

Identifying the break-even point

Tom's ice creams

050

100150200

250300350400450

0 100 200 300

Number sold

Co

st/R

even

ue

£

Sales Revenue

Total Cost

Fixed Cost

Loss

Profit

Break-even point

3.22 Calculating a break-even point

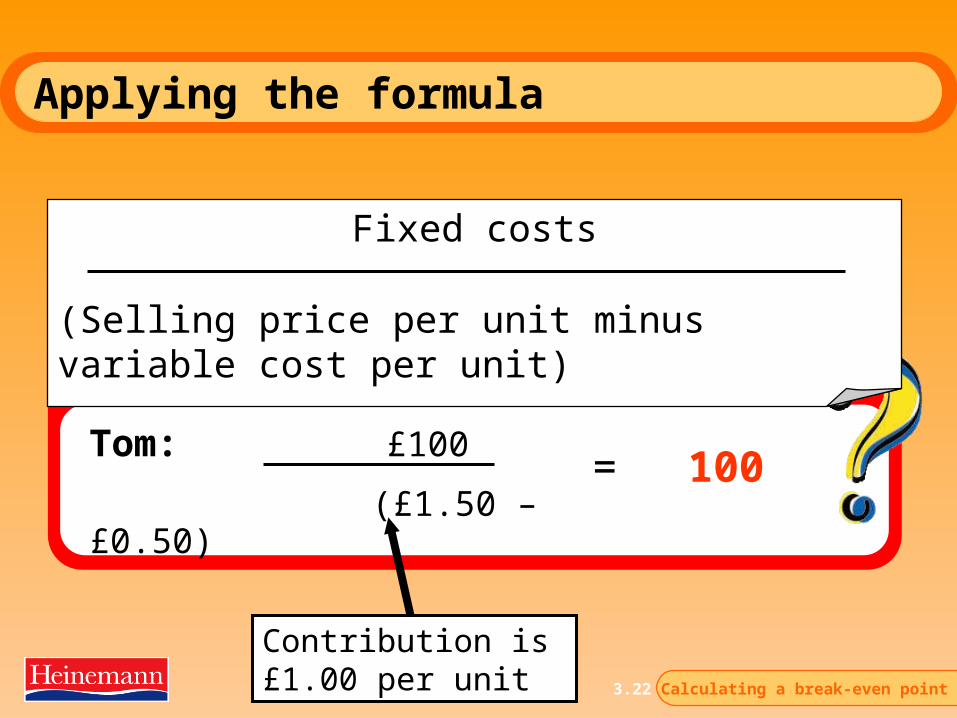

Using a formula to calculate the break-even point

The break-even point =

Fixed costs

(Selling price per unit minus variable cost per unit)

Also known as the Contribution as the amount left is what contributes to paying off the fixed costs.

3.22 Calculating a break-even point

Applying the formula

Fixed costs

(Selling price per unit minus variable cost per unit)

Tom: £100

(£1.50 – £0.50)= 100

Contribution is £1.00 per unit

3.22 Calculating a break-even point

Why the Break Even point may change

Changes in the break even point may happen if:

• Fixed Costs change

• Variable Costs change, or

• The selling price changes.

If Fixed Costs go

If Variable costs go

If Selling price go

up down up down up down

The break even point will go

up down up down down up

3.22 Calculating a break-even point

Increase in fixed costs.

Tom's ice creams

050

100150200

250300350400450

0 100 200 300

Number sold

Cost

/Rev

enue

£ Sales Revenue

Total Cost

Fixed Cost

If fixed costs go up to £120.

The B.E.P= 120

£120 .

(1.50-.50)

Original B.E.P = 100

The reverse happens if fixed costs fall.

3.22 Calculating a break-even point

Increase in variable costs.

Tom's ice creams

050

100150200

250300350400450

0 100 200 300

Number sold

Cost

/Rev

enue

£ Sales Revenue

Total Cost

Fixed Cost

If variable costs go up to £0.60

The B.E.P= 112

£100 .

(1.50-.60)

Original B.E.P = 100

The reverse happens if variable cost falls.

3.22 Calculating a break-even point

Increase in Selling price.

Tom's ice creams

050

100150200

250300350400450

0 100 200 300

Number sold

Cost

/Rev

enue

£ Sales Revenue

Total Cost

Fixed Cost

If selling price goes up to £1.60

The B.E.P= 91

£100 .

(1.60-.50)

Original B.E.P = 100

The reverse happens if selling price falls.

3.22 Calculating a break-even point

Margin of Safety

If a business knows a level at which it would like to sell / produce at it can work out its Margin of Safety.

The Margin of Safety is the different between the BEP and the actual level of production / sales.

E.g. If Tom aimed to sell 200 ice creams he would have a Margin of Safety of 100 as his BEP is 100 ice creams.

3.22 Calculating a break-even point

Margin of Safety – On the BE Graph.

Tom's ice creams

050

100150200

250300350400450

0 100 200 300

Number sold

Co

st/R

even

ue

£

Sales Revenue

Total Cost

Fixed Cost

Loss

Profit

Break-even point

Margin of Safety

3.22 Calculating a break-even point

Target Profits

A business can use the break even formula to calculate the quantity needed in order to achieve a target profit.

Target profit (the profit a business wants to make) is calculated as follows:

Fixed Costs + Target Profit = Number of units

Contribution per unit

3.22 Calculating a break-even point

Benefits of Break Even Analysis

Graph easier to understand.

Helps in the decision making process.

Shows level of profit / Costs at different output / sales levels.

Can establish margin of safety.

3.22 Calculating a break-even point

Drawbacks of Break Even Analysis

Can only be used in the short term. All costs potential change.

If batch processing used cannot obtain exact BEP.

Model only viable for one type of product / service at a set price.

Assumption all output sold. Not always the case.

3.22 Calculating a break-even point

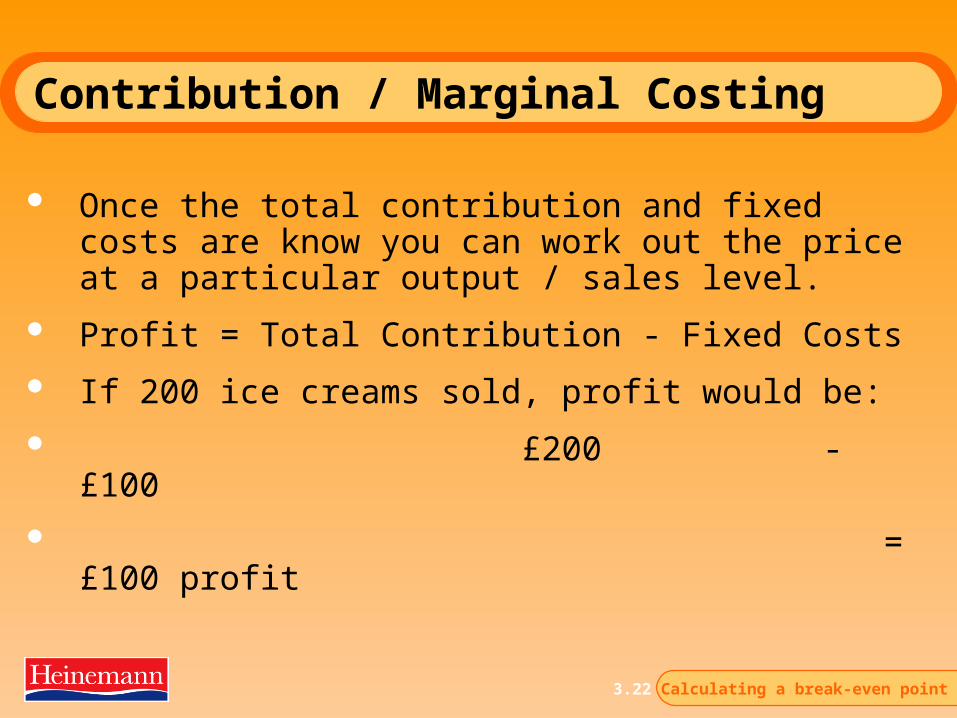

Contribution / Marginal Costing

Once the contribution per unit has been calculated you can also calculate the total contribution at various levels of output or sales.

Total Contribution =

Contribution per unit x Total Number of sales / output.

E.g. £1 x 200 ice creams = £200 total contribution

3.22 Calculating a break-even point

Contribution / Marginal Costing

Once the total contribution and fixed costs are know you can work out the price at a particular output / sales level.

Profit = Total Contribution - Fixed Costs

If 200 ice creams sold, profit would be:

£200 - £100

= £100 profit