2Q17 UNITED STATES MULTIHOUSING MARKET OVERVIEW...

25

MULTIHOUSING MARKET OVERVIEW 2Q17 UNITED STATES

Transcript of 2Q17 UNITED STATES MULTIHOUSING MARKET OVERVIEW...

MULTIHOUSING MARKET OVERVIEW

2Q17 UNITED STATES

2

3 Key Takeaways

4 Historical Sales Volume

5 Sales Volume Analysis

6 Top Markets by Sales Volume

7 Historical Pricing Trends

8 Cap Rates by Market

9 Capital Flow Allocation

10 Top Buyers and Sellers

11 Top Buyers by Region

12 Yield Spread

13 International Capital Overview

14 International Capital Distribution

15 Historical Rent Growth

16 Employment Growth

17 Technology Hubs

18 Historical Supply and Demand

19 New Supply Matrix

20 Rental Pricing And Momentum

21 Historical Occupancy Rate

22 Mortgage Maturities

23 Debt Outstanding

24 Lender Composition

TABLE OF CONTENTS

3

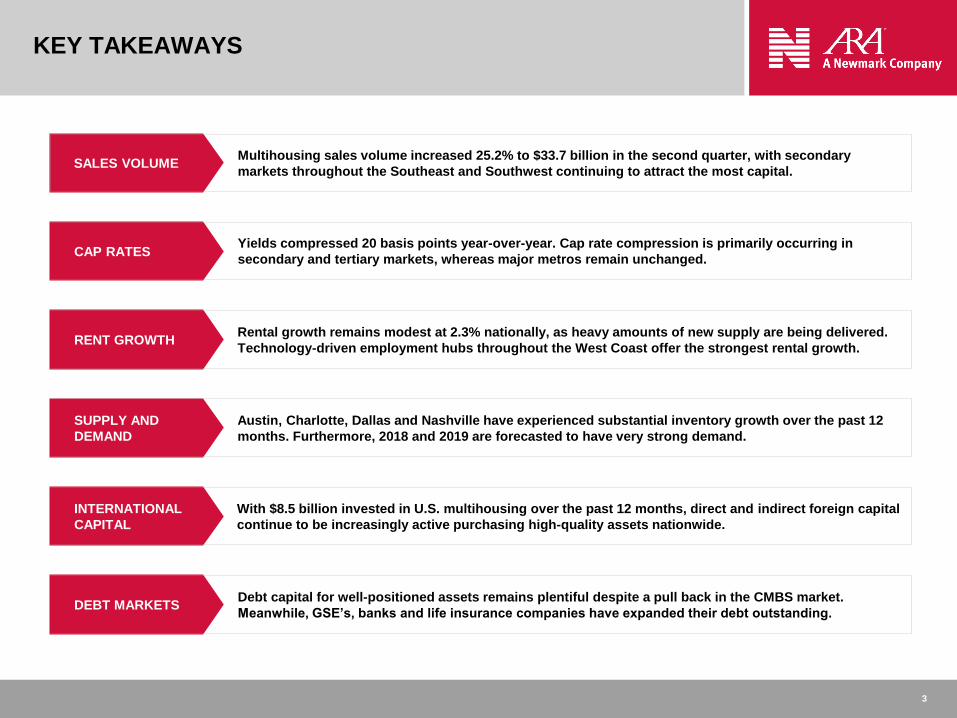

KEY TAKEAWAYS

SALES VOLUME

CAP RATES

RENT GROWTH

SUPPLY AND

DEMAND

INTERNATIONAL

CAPITAL

DEBT MARKETS

Multihousing sales volume increased 25.2% to $33.7 billion in the second quarter, with secondary

markets throughout the Southeast and Southwest continuing to attract the most capital.

Yields compressed 20 basis points year-over-year. Cap rate compression is primarily occurring in

secondary and tertiary markets, whereas major metros remain unchanged.

Rental growth remains modest at 2.3% nationally, as heavy amounts of new supply are being delivered.

Technology-driven employment hubs throughout the West Coast offer the strongest rental growth.

Austin, Charlotte, Dallas and Nashville have experienced substantial inventory growth over the past 12

months. Furthermore, 2018 and 2019 are forecasted to have very strong demand.

With $8.5 billion invested in U.S. multihousing over the past 12 months, direct and indirect foreign capital

continue to be increasingly active purchasing high-quality assets nationwide.

Debt capital for well-positioned assets remains plentiful despite a pull back in the CMBS market.

Meanwhile, GSE’s, banks and life insurance companies have expanded their debt outstanding.

4

$0

$40

$80

$120

$160

$200

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017YTD

Billi

on

s

12-Month Totals Quarterly Totals

HISTORICAL SALES VOLUMEUnited States

After a slow start to the year, sales volume accelerated 25.2% quarter-over-quarter with 12-month volume reaching $144.6 billion.

Source: Newmark Knight Frank Research, Real Capital Analytics

2Q17

$33.7B

5

Primary Markets28.7%

Secondary Markets41.9%

Tertiary Markets29.4%

Mid-Atlantic7.1%

Midwest8.0%

Northeast12.3%

Southeast25.1%

Southwest24.4%

West23.1%

Sales Volume

by Market Tier

Sales Volume

by Region

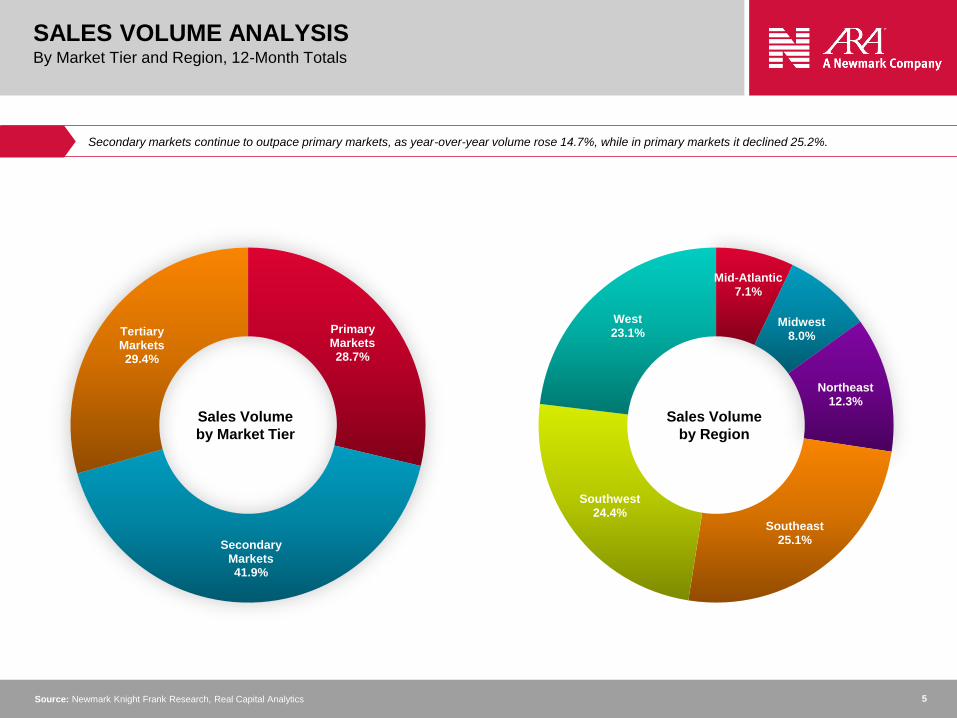

SALES VOLUME ANALYSISBy Market Tier and Region, 12-Month Totals

Secondary markets continue to outpace primary markets, as year-over-year volume rose 14.7%, while in primary markets it declined 25.2%.

Source: Newmark Knight Frank Research, Real Capital Analytics

6

$14.4

$11.3

$8.9

$8.2

$5.4

$5.4

$5.3

$5.1

$4.6

$4.6

$4.1

$3.7

$3.6

$3.2

$2.7

$2.7

$2.6

$2.4

$2.3

$2.3

$2.0

$1.9

$1.7

$1.4

$1.3

$0 $3 $6 $9 $12 $15Billions

Minneapolis

Nashville

Raleigh-Durham

Baltimore

San Antonio

Las Vegas

Charlotte

San Diego

Boston

Tampa

Portland

Orlando

South Florida Metro

Austin

Chicago

Phoenix

Houston

Washington, D.C. Metro

San Francisco Metro

Seattle

Denver

Dallas-Forth Worth

Atlanta

Los Angeles Metro

New York City Metro

South Florida Metro

Miami $1.6 B

Broward $1.2 B

Palm Beach $841.5 M

Washington, D.C. Metro

Suburban MD $2.3 B

Northern VA $2.2 B

District of Columbia $624.8 M

San Francisco Metro

Oakland $1.8 B

San Francisco $1.6 B

San Jose $1.3 B

Other $720.5 M

Los Angeles Metro

Los Angeles $6.9 B

Orange County $1.9 B

Inland Empire $1.8 B

Other $712.0 M

New York City Metro

Manhattan $6.0 B

Outer Boroughs $4.4 B

Northern NJ $2.3 B

Other $1.7 B

TOP MARKETS BY SALES VOLUME12-Month Totals

Despite a national slowdown, top-tier secondary markets such as Austin, Dallas and Orlando had record first half sales volume.

Source: Newmark Knight Frank Research, Real Capital Analytics

7

$0

$30,000

$60,000

$90,000

$120,000

$150,000

0%

2%

4%

6%

8%

10%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017YTD

Pri

ce

Pe

r U

nit

Cap

Ra

tes

Price Per Unit Cap Rates

HISTORICAL PRICING TRENDSUnited States

Cap rates compressed 20 basis points year-over-year, while price per unit increased 6.0% to an all-time high of $140,217.

Source: Newmark Knight Frank Research, Real Capital Analytics ($25M+ Transactions)

8

San Francisco

Manhattan

Boston

Washington DC

Philadelphia

Raleigh-Durham

Charlotte

Jacksonville

Orlando

South Florida

Tampa

AtlantaCharleston

Chicago

Indianapolis

Houston

Seattle

Austin

Dallas

Portland

Sacramento

Los Angeles

San Diego

San Jose

Las Vegas

Phoenix

San Antonio

Denver Kansas City

St. Louis

Oklahoma City

Wichita

Minneapolis

Nashville

MemphisTulsa

Columbus

Louisville

Detroit

BirminghamLittle Rock

Salt Lake City

5.0%

3.8%

5.5%

5.4%

5.3%

5.4%

5.5%

5.5%

5.6%

5.1%

5.5%

5.7%

6.1%

5.4%

5.9%

5.5%

5.7%6.0%

5.0%

3.0-3.9%

5.8%

5.5%

5.7%5.9%

5.7%

6.1%

5.1%

5.6%

5.4%

5.3%

5.4%

5.2%

5.5%

5.4%

5.5%

4.8%

4.9%

5.2%

4.0%

4.9%

4.7%

4.8%

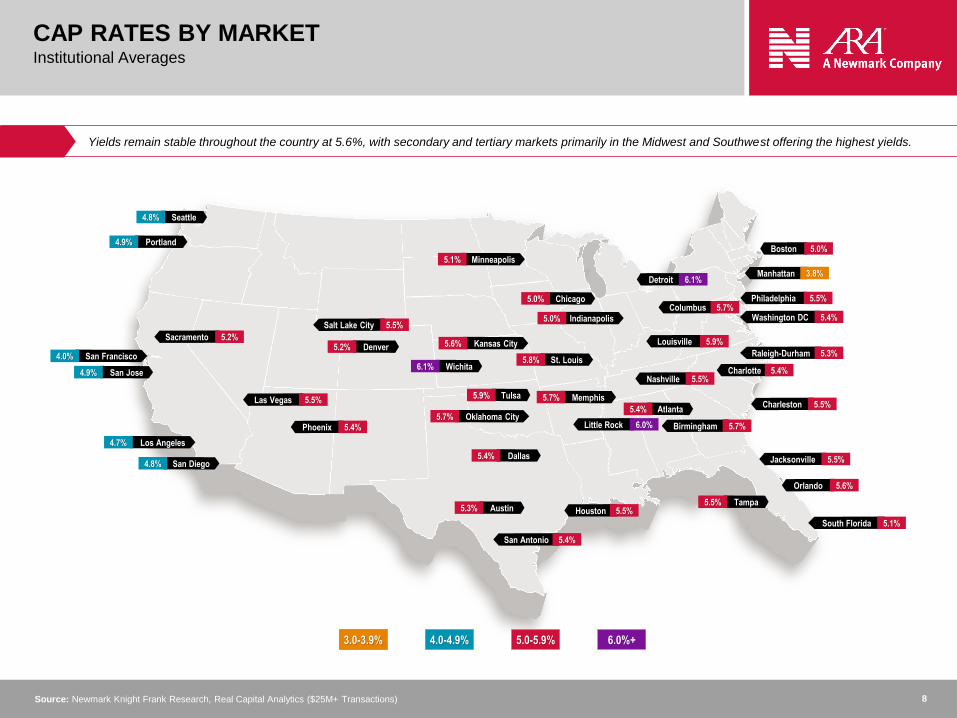

CAP RATES BY MARKETInstitutional Averages

5.0%

4.0-4.9% 5.0-5.9% 6.0%+

Yields remain stable throughout the country at 5.6%, with secondary and tertiary markets primarily in the Midwest and Southwest offering the highest yields.

Source: Newmark Knight Frank Research, Real Capital Analytics ($25M+ Transactions)

9

50%

60%

70%

80%

90%

100%

10%

15%

20%

25%

30%

35%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017-YTD

All

Pro

pe

rty T

yp

es

(e

x-M

ult

iho

us

ing

)

Mu

ltih

ou

sin

g

All Property Types (ex-Multihousing) Multihousing

CAPITAL FLOW ALLOCATIONVolume As A Percentage of Investment Sales

Since 2001, investors have increased their allocations to multihousing from 23.2% to 29.4%, growing at a quicker pace than all other property types.

Source: Newmark Knight Frank Research, Real Capital Analytics

10

$713.1

$731.1

$739.9

$739.9

$768.3

$789.6

$807.7

$822.5

$856.5

$917.3

$955.0

$955.0

$955.0

$1,035.9

$1,043.9

$1,142.7

$1,229.0

$3,242.5

$3,825.2

$4,165.3

Invesco

Strata Equity Group

TruAmerica Multifamily

Guardian Life Insurance

Investcorp

Carroll Organization

FPA Multifamily

Kennedy Wilson

BH Management

Harbor Group Int'l

GIC

Scion Group

CPP Investment Board

Cortland Partners

Mapletree Investments

Greystar

Rockpoint Group

Blackstone

Starwood Capital

MAA REIT

$831.7

$836.0

$858.7

$882.6

$890.3

$894.9

$968.0

$987.8

$1,018.9

$1,031.8

$1,061.1

$1,133.5

$1,323.0

$1,338.1

$1,415.1

$1,422.0

$1,498.9

$1,521.3

$3,028.5

$3,751.8

Trammell Crow

Lennar Corporation

AvalonBay

FPA Multifamily

Holland Partners

Alliance Residential

DRA Advisors

Ares Management

Kayne Anderson

Bascom Group

Harbor Group Int'l

Greystar

Investors Management

Starwood Capital

Blackstone

Waterton Associates

Bridge Investment

Fairfield Residential

Milestone APTS REIT

Post Properties

Top 20 Buyers$ in Millions

Top 20 Sellers$ in Millions

TOP BUYERS AND SELLERSUnited States; 12-Month Totals

Starwood Capital became the second-largest buyer of the past 12 months with its acquisition of Milestone for $3.0 billion during the second quarter.

Source: Newmark Knight Frank Research, Real Capital Analytics

11

$2,094 MAA

$2,161 Starwood

$1,299 Blackstone

$665 Rockpoint

Group

$734 MAA

$387 FPA Multifamily

$1,305 Starwood

$1,338 MAA

$823 Kennedy Wilson

$620 Blackstone

$503 BDMG

$380 Group Fox

$731 Strata Equity

$761 Blackstone

$702 Pacific Urban

$432 Fairstead

Capital$381

Morgan Props

$346 Strategic Props

$660 Carroll Org

$526 CortlandPartners

$602 Greystar

$432 Emerald Equity $360

Pantzer Props

$227 Monarch

$562 Blackstone

$466 BH Mgmt

$519 MG Properties

$319 A&E Real Estate $337

Quest Mgmt

$189 Campus Advantage

SO

UT

HE

AS

T

SO

UT

HW

ES

T

WE

ST

NO

RT

HE

AS

T

MID

-AT

LA

NT

IC

MID

WE

ST

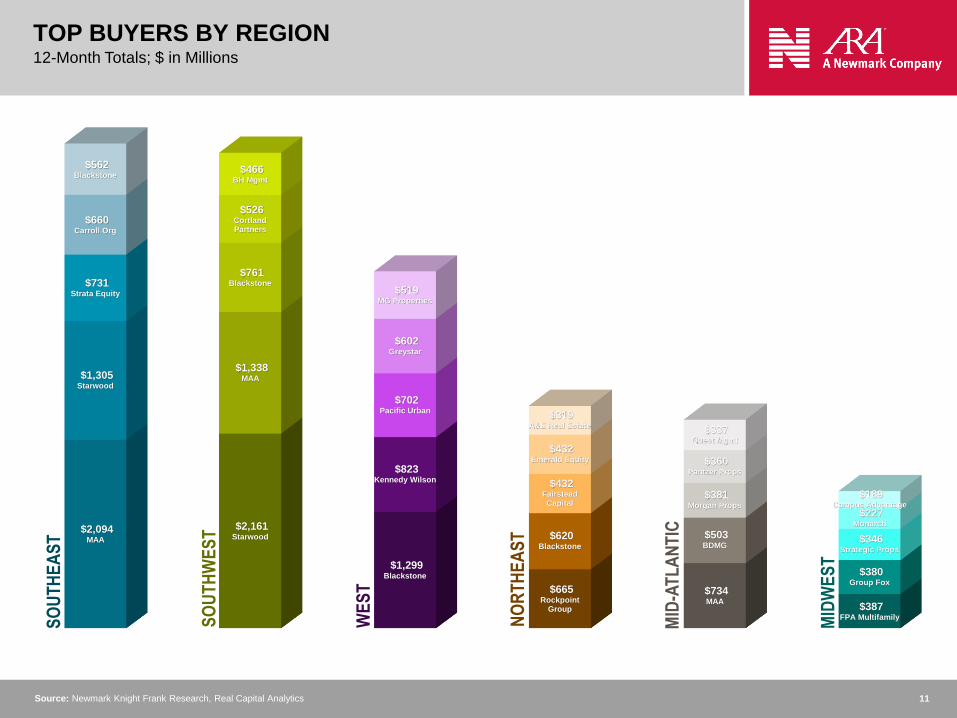

TOP BUYERS BY REGION12-Month Totals; $ in Millions

Source: Newmark Knight Frank Research, Real Capital Analytics

12

0

100

200

300

400

500

0%

2%

4%

6%

8%

10%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017YTD

Sp

rea

d (

BP

S)

Cap

Ra

tes

& T

rea

su

ry N

ote

Yield Spread Multihousing Cap Rates 10-Year Treasury Rate

YIELD SPREADMultihousing Cap Rates vs. the 10-Year Treasury Note

The 10-year Treasury note has stabilized since the election results. However, the yield spread is now at its lowest level since 2011 at 329 basis points.

Source: Newmark Knight Frank Research, Federal Reserve Bank of St. Louis, Real Capital Analytics ($25M+ Transactions)

13

Canada42.7%

Singapore23.6%

Israel10.4%

France6.8%

Kuwait4.9%

Germany4.0%

Sweden2.4%

UK2.3%

Other2.9%

Land & Houses PLC

THAILAND

Stoneweg SA

Varia US Properties

SWITZERLAND

GIC

Mapletree Investments

SINGAPORE

Amitim

Electra Ltd

Menora Mivtachim

Psagot

Sage Equities

ISRAEL

AXA Group

CAPSSA

FRANCE

Jamestown

GERMANY

Wafra

KUWAIT

Akelius Residential AB

SWEDEN

Top Buyers ($100M+)Top Countries of Origin

Balfour Beatty

UK

Bentall Kennedy

Brookfield Asset Management

CPP Investment Board

Emma Capital

H&R REIT

Manulife Financial

Milestone Apartment REIT

Morguard NA Residential REIT

Pure Multi-Family REIT

Starlight Investments

Venterra Properties

Western Wealth Capital

CANADA

INTERNATIONAL CAPITAL OVERVIEWTop Buyers and Countries of Origin; 12-Month Totals

Recent portfolio transactions in the student housing market pushed Singapore to the second-largest buyer behind Canada for the past 12 months.

Source: Newmark Knight Frank Research, Real Capital Analytics

14

MAJOR MARKETS 38.3%

BY MARKET TIERAs a % of Cross-Border Capital

BY REGIONAs a % of Cross-Border Capital

SECONDARY & TERTIARY 61.7%

MID-ATLATNIC 11.1%

MIDWEST 5.8%

NORTHEAST 14.8%

SOUTHEAST 33.9%

SOUTHWEST 25.2%

WEST 9.2%

NYC$910M

ATL$630M

AUS$445M

DEN$391M

S. FL$267M

ORL$245M

TB$157M

BOS$227M

LA$195M

CHA$189M

PHX$153M

POR$127M

CHI$108M

DC$100M

SEA$82M

LV$54M

NASH$47M

DFW$350M

INTERNATIONAL CAPITAL DISTRIBUTIONTop Destinations; 12-Month Totals

With nearly $8.5 billion invested over the past 12 months, overseas investors are mainly acquiring assets in secondary markets of the Southeast and Southwest.

Source: Newmark Knight Frank Research, Real Capital Analytics

15

-10%

-6%

-2%

2%

6%

10%

$0

$300

$600

$900

$1,200

$1,500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Eff

ec

tive

Ren

t G

row

th

Eff

ec

tive

Ren

t

Effective Rent Effective Rent Growth

HISTORICAL RENT GROWTHAnnual Effective Rent

Rent growth for 2Q17 was 2.3%. While more modest than in previous years, growth remains near long-term averages and is still trending in a positive direction.

Source: Newmark Knight Frank Research, Axiometrics

16Source: Newmark Knight Frank Research, U.S. Bureau of Labor Statistics (June release)

ORL

+4.0%

LV

+3.7%

JAX

+3.6%

NASH

+3.6%

TB

+3.6%

ATL

+3.5%

DFW

+3.3%

MINN

+3.3%

MIA

+3.3%

SLC

+3.2%

IND

+3.1%

PHX

+3.0%

R-D

+3.0%

CHA

+2.9%

AUS

+2.8%

DEN

+2.6%

POR

+2.5%

SEA

+2.5%

CHI

+1.3%

STL

+1.2%

BIRM

+1.3%LA

+1.7%

SAC

+1.9%

OKC

+1.9%

HOU

+1.9%

SD

+2.0%

KC

+2.2%

DET

+2.2%

DC

+1.8%

NYC

+1.8%

BOS

+2.4%

PHI

+2.1%SF

+2.4%

SJ

+1.6% MEM

+2.1%

SA

+2.4%

COL

+2.0%

CLE

+2.0%

EMPLOYMENT GROWTHYear-over-Year Change

Employment growth remains positive nationwide with robust growth Atlanta, Florida, Las Vegas and Nashville strengthening demand for multihousing.

17

18.1%

14.5%

23.0%

29.8%

21.5%

32.2%

16.5%

38.3%

25.3%

33.3%

18.1%

20.5%

25.4% 25.5%

28.6%

32.4%

0%

10%

20%

30%

40%

50%

2013 2014 2015 2016 2017

TECHNOLOGY HUBSRental Growth; Past 5 Years

The majority of technology-centric employment hubs have significantly outpaced the national average for rental growth of 17.5% over the past five years.

Source: Newmark Knight Frank Research, Axiometrics

18

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

0

150,000

300,000

450,000

600,000

750,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018* 2019*

Inve

nto

ry G

row

th

New

Su

pp

ly &

Ab

so

rpti

on

(U

nit

s)

New Supply Absorption Inventory Growth

HISTORICAL SUPPLY AND DEMANDUnited States

Although supply has outpaced demand for the past two years, strong absorption is anticipated with less new product coming to market in 2018 and 2019.

Source: Newmark Knight Frank Research, Axiometrics

19

SAC

SLC

SEA

ORL

SD

LV

PHX

LA

MINN

ATL

JAX

R-D

DEN CHA

DFW

MEM

IND

TBPOR

MIABOS

KC

SA

DC

SJ

NASH

SF

CHI

PHI

STL

AUS

NYC

OKC

HOU

0

5,000

10,000

15,000

20,000

25,000

30,000

0% 1% 2% 3% 4% 5%

New

Su

pp

ly (

Un

its

)

Inventory Growth

Inventory in Dallas, Austin, Nashville and Charlotte is growing at twice the pace over the trailing 12 months as the national average of 1.5%.

Source: Newmark Knight Frank Research, Axiometrics

NEW SUPPLY MATRIX12-Month Totals

20

$1.1

0

$1.3

8

$2.5

6

$1.1

0

$1.9

2

$1.3

0

$1.6

2

$1.1

8

$1.0

1

$2.6

1

$1.7

3

$1.2

2

$3.5

0

$1.2

4

$1.7

2

$1.1

3

$1.6

0

$1.0

8

$1.6

3

$2.1

8

$4.1

8

$3.1

9

$2.2

2

$1.2

0

$1.9

9

3.8%

1.0%

2.0%

2.8%

1.1%

2.4% 2.5%

-2.5%

4.1%3.6%

1.8% 1.7%

-0.8%

5.1%

1.2%

4.6%

1.9%

2.9%

9.4%

4.8%

0.5%

1.9%

5.7%

2.6%

1.5%

-4%

-1%

3%

7%

10%

14%

$0

$1

$2

$3

$4

$5

Ye

ar-

ove

r-Y

ea

r R

en

tal C

ha

ng

e

Re

nt

Pe

r S

qu

are

Fo

ot

Rent Per Square Foot Year-over-Year Change

RENTAL PRICING AND MOMENTUM Top 25 Markets

Rental rates are highest in supply-constrained coastal markets with the strongest year-over-year growth in Orlando, Sacramento and Seattle.

Source: Newmark Knight Frank Research, Axiometrics

21

95.0%

91%

92%

93%

94%

95%

96%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Occupancy Rate Long-Term Average

Long-Term Average = 94.1%

HISTORICAL OCCUPANCY RATEUnited States

Strong demand nationwide has pushed the occupancy rate to 95.0%, a 40-basis-point increase over the first quarter.

Source: Newmark Knight Frank Research, Axiometrics

22

17.2 19.8 21.7 24.728.9 32.5 33.1 33.0 31.9 29.0 26.6 23.9 27.3

34.141.6

49.0

3.04.3

5.2

10.49.3

8.1 8.6 10.2 10.4 12.8 14.915.7

21.2 5.9

5.4

3.5

2.72.7

2.9

3.13.3

3.4 3.7 4.0 4.0 3.8 3.9 4.4

4.5

4.4

4.2

4.6

24.3

27.331.2

35.038.3

40.144.4

49.5 53.2 54.7 54.8 57.9

61.7

65.9

66.0

68.0

$0

$30

$60

$90

$120

$150

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Billi

on

s

Banks CMBS Life Insurance Other

MORTGAGE MATURITIESBy Lender Type

Mortgage maturities are set to rise to $114.7 billion in 2017, up 12.6% from 2016, when mortgage maturities totaled $101.9 billion.

Source: Newmark Knight Frank Research, Federal Reserve Bank, Trepp

23

$0

$250

$500

$750

$1,000

$1,250

$1,500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017YTD

Mil

lio

ns

$1,213.7

Banks 35.7%

CMBS4.1%

Life Co5.6%

Others1.5%

Agency & GSE42.9%

Gov't8.6%

DEBT OUTSTANDINGUnited States

Year-over-year CMBS declined 19.7%, while agency and GSEs increased their debt outstanding 14.3%, banks by 11.4% and life insurance companies by 9.7%.

Source: Newmark Knight Frank Research, Federal Reserve Bank of St. Louis, Mortgage Bankers Associates

24

1.2% 2.1% 3.0% 1.0% 2.5% 1.0% 2.0% 3.6% 1.4%

7.2% 6.1% 3.3% 8.5% 5.1% 7.9% 5.7%6.0%

4.9%

37.3%

66.0% 71.9% 64.6%

60.9%

28.4%

72.3% 67.8%

50.0%

8.4%

7.8%3.3%

7.2%

9.0%

8.5%

6.6%7.4%

6.6%

3.5%

1.5% 0.6% 1.4%

1.3%

4.7%

1.4%1.1%

2.2%16.8%

7.9%5.3%

7.4%

7.1%

12.9%

5.5%5.8%

19.1%

24.1%

7.1%11.2%

9.1%13.4%

35.2%

4.7% 6.7%

14.2%

1.5% 1.5% 1.4% 0.8% 0.7% 1.4% 1.8% 1.6% 1.7%

0%

20%

40%

60%

80%

100%

Major Metros Secondary Markets Tertiary Markets Mid-Atlantic Midwest Northeast Southeast Southwest West

CMBS Financial Gov't Agency Insurance Int'l Bank Na'l Bank Regl/Local Bank Private/Other

LENDER COMPOSITIONUnited States; 12-Month Totals

Lending in major metros has benefitted from regional banks expanding their real estate balance sheets, while larger national banks remain more risk averse.

Source: Newmark Knight Frank Research, Real Capital Analytics

www.aranewmark.com

New York City

HEADQUARTERS

125 Park Avenue

New York, NY 10017

212.372.2000

Blake Okland

Vice Chairman, Head of US Multifamily

704.379.1987

Jonathan Mazur

Managing Director, Research

212.372.2154

Michael Wolfson

Senior Capital Markets Research Analyst

212.372.2453

Newmark Knight Frank Research Reports are also available at www.ngkf.com/research

All information contained in this publication is derived from sources that are deemed to be reliable. However, Newmark Knight Frank (NKF) has not verified any such information, and the same constitutes the statements and representations only of the source thereof, and not of NKF. Any recipient of this publication should independently verify such information and all other information that may be material to any decision that recipient may make in response to this publication, and should consult with professionals of the recipient’s choice with regard to all

aspects of that decision, including its legal, financial, and tax aspects and implications.

Any recipient of this publication may not, without the prior written approval of NKF, distribute, disseminate, publish, transmit, copy, broadcast, upload, download, or in any other way reproduce

this publication or any of the information it contains.