2Q & 1H2021 17 Aug 2021

49

2Q & 1H2021 17 Aug 2021

Transcript of 2Q & 1H2021 17 Aug 2021

2Q & 1H2021

17 Aug 2021

Activities Highlight

Key Drivers

2Q & 1H2021 Performance

OutlookCo

nte

nts

01

02

03

04

PTT Group’s New Vision & Strategic Direction

05

1

4

Key Activities in 2Q2021

Take a big step into Future energy and Beyond

Restructured of Power Business (+12.73% stake increased)

5

Contract extension of business collaboration to operate 7-Eleven

Investment 15.38% in petrochemical producer (Olefins)in Indonesia (PT Chandra Asri,)

FID in Refinery Efficiency and Diesel Quality Improvement Project for EURO V Standards (Ultra Clean Fuel )

Award for the JV with BAFS to provide aviation fuel services at U-Tapao International Airport

1

2

3

5 7

8

6

4

2

3

1Acquired 6.66% stake in Lotus Pharmaceutical Company Limited in Taiwan

JV with Nove Foods to operate the entire supply chain of Plant-based protein business

Signed MOU with Foxconn to collaborate in setting up an open platform to support EV growth in Thailand

Establishment of EVME as digital platform to promote EV

Establishment of "AeroSky (Thailand) to provide drone-based enterprise solutions

Investment 41.6% in power project in India (Avaada: 4,560MW )

Investment 25% in offshore wind power projects in Taiwan (CI Changfang and CI Xidao : 595 MW)

Investment in High Value Business (coating resins) (the Acquisition of 100% Shares of Allnex)

2

9FID in Bioplastic project plant 2(Name plate capacity: 75,000 tons per year)

The Screening Unit and Field Hospitals (End-to-End) under PTT Group’s “Giving Breath Project”

4

➢ We aim for the fast process of screening, sorting, and treating patients. This project could potentially turn into an operation model where business sector collaborates with the public sector.

➢ The process starts with the patients’ screening section that sequentially leads into three assign-colored groups; green, yellow, and red field hospitals.

➢ This is to ensure that all COVID-19 patients get their proper treatments and not being left behind.

✓The collaboration of PTT Group , Department of Disease Control, Ministry of Public Health, The National Health Security Office, The Foundation of Bangpakok Hospital Group, and Piyavate Hospital.

✓PTT Group puts all the effort to tackle the outbreak, including manpower, innovation, technology, medical supplies and equipment as well as budget to urgently assist medical sectors to fight the COVID-19 pandemic.

The 1st section of COVID-19Screening UnitThe 2nd, 3rd and 4th section are the sections of

End-to-End Field Hospitals

3

PTT Group’s Key Activities on ESG

Activities Highlight

Key Drivers

2Q & 1H2021 Performance

OutlookCo

nte

nts

01

02

03

04

4

PTT Group’s New Vision & Strategic Direction

05

0

2

4

6

8

10

12

14

16

18

20

Jan-19 Apr-19 Jul-19 Oct-19 Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21

6.6

11.0

7.28JLC-LNG*

JKM Spot

Avg. Pooled

gas price

4.9

9.5

7.22

4.7

9.7

7.15

5.8

9.4

7.30

* JLC = Japan LNG Cocktail : Landed LNG price in Japan

3.6

9.4

7.23

3.62.1

9.1

6.79

6.20

8.48.0

5.68

6.3

5.89

6.3

10.1

1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 2Q21 Jul’21

Key Business Drivers: QoQ: Increased in most of product prices as demand improved from vaccines rollout, ease of lockdown, and production cut of OPEC+

HoH: Petroleum and petrochemical prices improved from the demand recovery while pooled gas price dropped

AVG. Petroleum Prices ($/bbl)

HDPE

PX

PP

BZ

0

20

40

60

80

100

Jan-19 Apr-19 Jul-19 Oct-19 Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21

61.2

67.4

64.1 65.1

62.163.5

62.1

43.4

Dubai

FO

(3.5%)

42.9

40.4

50.7

43.4 30.6

28.9

1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 2Q21 Jul’21

44.1

60.0

56.644.6

2019 Dubai avg.: 63.5 2020 Dubai avg.: 42.2

AVG. Petroleum Prices ($/bbl)

AVG. FX (THB/USD) Petrochemical Prices (Avg. $/ton)

29

30

31

32

33

34

6

31.8 31.8

30.9

30.5

1H20 (end. FX 31.1)End: Baht Depre.

Bt 0.7 or 2.3%

31.5

30.8

1Q21 (end FX 31.5)End: Baht Depre.

Bt 1 .3 or 4.3%

32.1

1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 2Q21 Jul’21

2Q20 (end FX 31.1)End: Baht Appre.

Bt 1.8 or 5.4%

31.5

30.4

31.5

100

400

700

1000

1300

1600

Jan-19 Apr-19 Jul-19 Oct-19 Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21

1,080

590

519

1,0931,127 1,143

1,085

Note: F igures are av erage & Naphtha (MO P’J)

1,080

909

625

541

951

813679

494

1,049

841

801

671

540

706

614

440

839986

496

371

274

760

871

546

427

397

919968

561529

408

1,000

1,142

766753

557

1,365

1,145

PP HDPE PX BZ Naphtha

QoQ 2% 4% 12% 28% 9%

YoY 53% 57% 73% >100% >100%

HoH 45% 46% 35% 74% 63%

1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 2Q21 Jul’21

Naphtha

Dubai FO 3.5%

QoQ 12% 8%

YoY >100% >100%

HoH 56% 63%

66.9

61.1

935

1,042

684

1,258

1,131

5

64.5

72.9

859

966

606

1,336

1,191

2Q21 (end FX 32.2)End: Baht Depre.

Bt 0 .7 or 2.2%

1H21 (end. FX 32.2)End: Baht Depre.

Bt 2.0 or 6.6%

32.8

6.36

10.0

8.4

14.1

2019 Avg. : 31.2 / End : 30.4 2020 Avg. : 31.5 / End : 30.2

JLC-LNG* JKM Avg. Pool

QoQ 1% 8%

YoY 8% >100% 6%

HoH 9% >100% 13%

Activities Highlight

Key Drivers

2Q & 1H2021 Performance

OutlookCo

nte

nts

01

02

03

04

6

PTT Group’s New Vision & Strategic Direction

05

QoQ: NI decreased primarily due to non - recurring items despite enhanced operating income

HoH: Robust performance as a result of petroleum & petrochemical demand recovery in line with global trend

21%

32%24%

10%

3%10%6%

14%

31%31%

15%

2%

1%

34%

20%

31%

6%5%

1%

PTT(GAS & Trading)

P&R

TEG5/

Oil &

Retail

PTT Consolidated Performance: 2Q2021 & 1H2021

REVENUE

1,011,093 MB

NI

57,166 MB

1H2021

341,325 477,837

533,256

824,892

1,011,093

2Q20 1Q21 2Q21 1H20 1H21

REVENUE 12% QoQ 23%

12,053

32,58824,578

10,499

57,166

2Q20 1Q21 2Q21 1H20 1H21

>100% YoY

54,208

102,997113,166

86,593

216,163

2Q20 1Q21 2Q21 1H20 1H21

Unit: MB

>100%NI 25% QoQEBITDA 10% QoQ >100%

EBITDA

216,163 MB

Gas1/

P&R

Oil & Retail

P&R

Trading2/

Gas1/

E & PTEG3/

Oil & Retail

TEG3/

Trading2/

3%

Unit: MB Unit: MB56% YoY >100% YoY

Others6/Others4/

Remark: 1/ PTT Gas business and affiliates

2/ PTT Trading business and affiliates3/ Technology and Engineering business mainly contributed from power business

4/ O thers business mainly contributed from coal business

Others4/

Remark: 5/ Technology and Engineering business mainly contributed from power business

6/ O thers business mainly contributed from PTT LNG, PTT NGD, PTTT and PTTGM etc.7

E & PE & P

6.37 5.61 5.596.64

5.60

28.92

56.59

63.98

40.80

60.52

34.9740.38 42.19

40.15 41.35

2Q20 1Q21 2Q21 1H20 1H21

694

(127)(9) (33)

128

282349

418

631

2Q20 1Q21 2Q21 1H20 1H21

213271

317

231294

114

112126

114

119

2Q20 1Q21 2Q21 1H20 1H21

Liquid ($/BBL)

Gas($/MMBTU)

Weighted Avg.

($/BOE)

MMUSD

Liquid

Gas

KBOED

* Includes Gain/(Loss) on FX, Deferred tax from Functional currency, Current Tax from FX

Revaluation, Gain/(Loss) from Financial Instruments, Impairment loss on assets and etc.

Non-recurring*

Recurring NI

327

383

376

134

E&P PerformanceQoQ: Soften net income without recognition of gain from Oman Block 61 acquisition despite improved operating performanceHoH: Strengthen performance from higher sales volume and prices

443

222

4%

8

Net Income (100%)

Product Prices Sales Volume

13%

35% YoY

16% QoQ

QoQ

HoH

41% QoQ

66% YoY

16%

3%

48%345

413

QoQ 20%

598 46%

409

+ Recurring NI : increased from higher sales volume and selling prices

- Non-recurring : mainly from no recognition of gain on a bargain purchase

of Oman Block 61 Project

+ Recurring NI : improved from higher sales volume and liquid prices and lower unit cost

- Non-recurring : primarily from higher loss from oil price hedging and exploration expenses from write-off of Brazil’s project offset with gain from Oman Block 61 acquisition

PTT EBITDA Breakdown by Business

GAS

S&M

TM

GSP

NGV

Others

Trading

Total

Unit: MMTHB

2Q20 1Q21 2Q21 QoQ YoY 1H20 1H21 HoH

11,028 21,775 22,134 2% >100% 25,461 43,909 72%

1,356 4,775 3,732 22% >100% 3,280 8,507 >100%

8,960 8,120 8,577 6% 4% 18,039 16,697 7%

(475) 6,220 7,384 19% >100% 1,328 13,604 >100%

(684) (221) (425) 92% 38% (1,264) (646) 49%

1,871 2,881 2,866 53% 4,078 5,747 41%

1,251 1,138 907 20% 27% 2,158 2,045 5%

12,279 22,913 23,041 1% 88% 27,619 45,954 66%

9

8%

>100%

63%

836 805 796 840 800

495 598 727 560 663

1,288 1,323 1,333 1,274 1,329

847957 958

898 958

670786 803

711794135

150 134164

142

2Q20 1Q21 2Q21 1H20 1H21

Gas Business

NG Price VS FO & Customer Breakdown NGV Price & Sales Volume

QoQ : Improved NG vol. mainly from power producers during summer while pooled price picked upHoH: Increased gas sales vol., lower pooled gas cost and higher industrial selling prices referenced to FO price

7.31 7.19 7.20 7.30 7.23 6.79 6.20 5.68 5.89

6.36

416 422 403

281 281

188

262 286

367 397

0

100

200

300

400

500

4

6

8

10

12

14

1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 2Q21

$/MMBTU

EGAT (17%)

IPP (14%)

SPP (28%)

GSP (21%)

Industry (17%)

NGV (3%)

Unit: MMSCFD

4,271

$/TON

HSFO 180 C ST 2%S

Avg. Pooled gas price

4,619

QoQ

YoYHoH

FO (2%) Pool Price8%

6%

13%

A VG.2019 = 7.25

3% QoQ

11% YoY

4,751

Fuel Oil

14.2

13.413.8

14.5

13.6

3.3 3.7 3.3 4.0

3.5

2Q20 1Q21 2Q21 1H20 1H21

Unit: K.Ton/Day

Unit: THB/KG

NGV Avg. price

NGV Sales Vol.

YoY

11% QoQ

3% QoQ

3% YoY

+ Increased overall NG sales volume mainly from power customer during summer and unplanned shutdown of domestic coal power plants

- NGV vol. reduced from impact of COVID-19 new waves

Key Highlights

NG Price

NG Vol.

QoQ

10

4,447 4,686

5%

HoH+ NG sales vol. increased from almost all customers except NGV due to the recovery of economic activities + Lower pooled gas cost benefit to overall gas business + Industrial selling prices increased according to FO price linked

13%

6%

AVG. 1H21 = 6.13AVG. 1H20 = 7.02A VG. 2020 = 6.48

1,093 1,080

951 841

839 760 919

1,000 1,145

1,191

1,046

1,067 1,008

956 955 866

979

1,239

1,533 1,540

1,037 1,017

916 838

847

754 884

983

1,185

453

490

365 430

500

307

363 418

593

528 456

457

469 472

458

446 464 425 430

423

309 314 314 334 331

328

318 281 281 297

1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 2Q21

1,146

Gas Business : Gas Separation Plant (GSP)QoQ : GSP performance enhanced from higher selling prices & volumeHoH: Outperformed GSP performance due to higher selling prices & volume together with lower feed cost

GSP Sales Vol. & U-Rate

645 748 783

127 168 161

510

582 566

200

271 275

11

11 12

2Q20 1Q21 2Q21

1,493

1,7801,797

Pentane (1%)

LPG (43%)

Propane (15%)

NGL (9%)

Ethane (32%)

81.5%

94.7% 95.9%86.8%

95.3%

1% QoQ

20% YoY

U-Rate

Unit : kTon

QoQUnit: $/Ton

LPG* 2%

*LPG Domestic ** feed cost calculation per GSP production volume

Propane 11%

LDPE 0.5%

HDPE 4%

GSP Feed Cost vs Petchem. Price

LLDPE 3%

Feed Cost** 6%

+ Higher GSP’s selling prices following referenced global petrochemical prices

+ Increased sales volume & U- Rate according to higher petrochemical demand & no planned

maintenance shutdown

- Feed gas cost increased in line with gulf gas

QoQ

Key Highlights

11

1,441 1,531

287329

1,0621,148

399

54624

23

1H20 1H21

11%

3,213

3,577

+ Increased GSP’s selling prices following global petrochemical prices

+ Higher sales volume according to higher petrochemical demand and less plants' shutdown

+ Lower feed gas cost

HoH

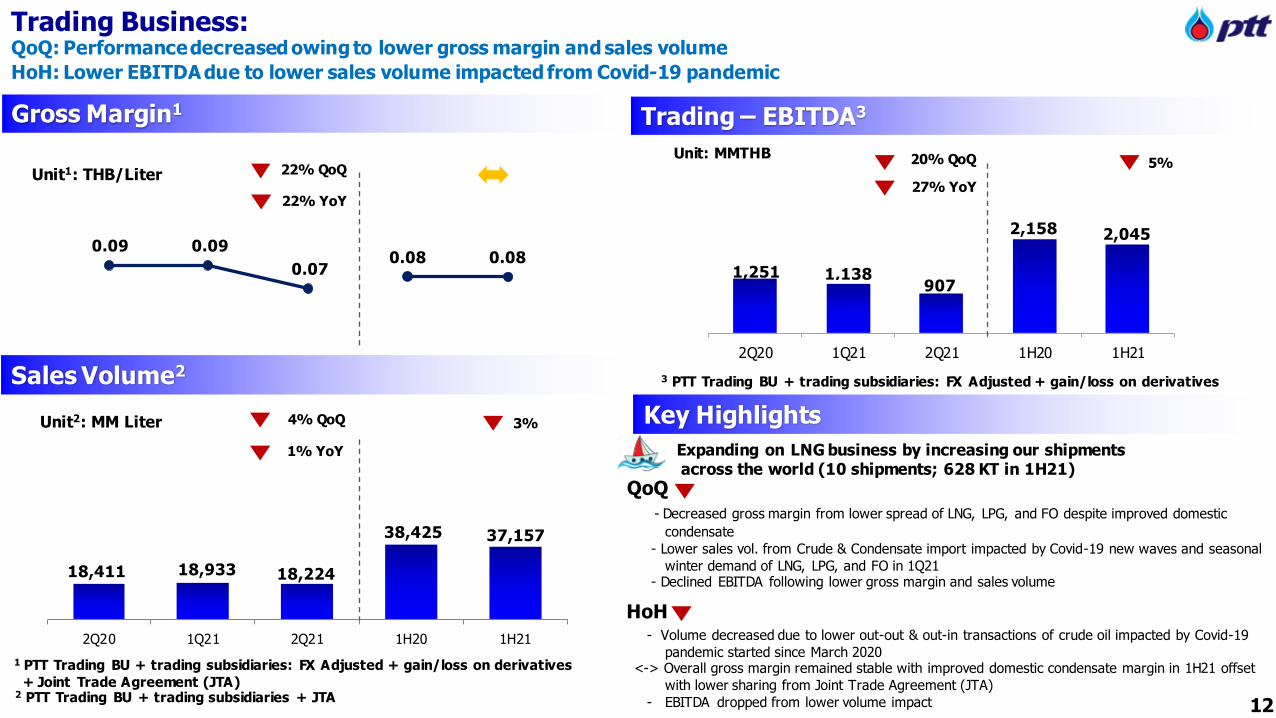

Expanding on LNG business by increasing our shipments across the world (10 shipments; 628 KT in 1H21)

- Decreased gross margin from lower spread of LNG, LPG, and FO despite improved domestic

condensate

- Lower sales vol. from Crude & Condensate import impacted by Covid-19 new waves and seasonal

winter demand of LNG, LPG, and FO in 1Q21 - Declined EBITDA following lower gross margin and sales volume

- Volume decreased due to lower out-out & out-in transactions of crude oil impacted by Covid-19

pandemic started since March 2020<-> Overall gross margin remained stable with improved domestic condensate margin in 1H21 offset

with lower sharing from Joint Trade Agreement (JTA)

- EBITDA dropped from lower volume impact 12

0.09 0.09

0.07 0.08 0.08

22% QoQ

Gross Margin1

Trading Business: QoQ: Performance decreased owing to lower gross margin and sales volume

HoH: Lower EBITDA due to lower sales volume impacted from Covid-19 pandemic

Unit1: THB/Liter

22% YoY

18,411 18,933 18,224

38,425 37,157

2Q20 1Q21 2Q21 1H20 1H21

1 PTT Trading BU + trading subsidiaries: FX Adjusted + gain/loss on derivatives

+ Joint Trade Agreement (JTA)2 PTT Trading BU + trading subsidiaries + JTA

Unit2: MM Liter 4% QoQ

1% YoY

Trading – EBITDA3

1,251 1,138 907

2,158 2,045

2Q20 1Q21 2Q21 1H20 1H21

3 PTT Trading BU + trading subsidiaries: FX Adjusted + gain/loss on derivatives

Unit: MMTHB

Key Highlights

20% QoQ

27% YoY

QoQ

HoH

5%

3%

Sales Volume2

50.7

30.6

42.9 44.6

60.0 62.9 66.3 71.6

1Q20 2Q20 3Q20 4Q20 1Q21 Apr'21 May'21 Jun'21

520

4,003 3,225 2,418

7,228

2Q20 1Q21 2Q21 1H20 1H21

Oil Business : OR GroupQoQ : NI dropped from lower oil margin and sales volume pressured by new waves of COVID-19HoH : Improved performance from higher oil margin despite decreased oil sales volume as well as non-oil expansion

Oil Business

Net Income

Unit : MMTHB

2Q20 1Q21 2Q21 1H20 1H21

Dubai (USD/BBL)

Avg. 2Q21 = 66.9

19% QoQ>100% YoY

12% QoQ>100% YoY

Non-Oil Business

1/ Thailand, Japan, O man, My anmar, and Malay sia2/ Domestic, and Laos

Amazon1/

C-Store (7-11, Jiffy) 2/

60 MM Cups3,084 Outlets

73 MM Cups3,376 Outlets

70 MM Cups3,452 Outlets

128 Cups3,084 Outlets

143 Cups3,452 Outlets

1,938 Outlets 1,995 Outlets 2,018 Outlets 1,938 Outlets 2,018 Outlets

14% 14% 15%15% 14%3% 5% 5%

16% 7%51% 47% 47%

40%46%

6% 6% 6%

6%6%

24%25% 24%

21%25%

2%3%

3%

2%2%

5,433 5,910

5,542

12,056 11,452

2Q20 1Q21 2Q21 1H20 1H21

LPGAviation

Diesel

Fuel Oil

Gasoline

Others

0.83

1.31 1.23

0.81

1.27

Margin*(THB/Litre)

(MM Liter)

6% QoQ48% YoY

*Gross margin included stock gain/(loss)

Sales Volume(MM Liter)

Cups4% QoQ17% YoY

C-Store1% QoQ4% YoY

QoQ : Oil : Lower gross margin and dropped sales volume from new waves of COVID-19Non-Oil : Slightly increased margin from lower operating expenses despite reduced sales from COVID-19 impact

HoH: Oil : Better gross margin while sales volume dropped mainly from Aviation fuelNon-Oil : Improved gross margin from outlet expansion 13

5%

12%

57%

Avg. 1H20 = 40.7

>100%

4%

Avg. 1H21 = 63.5

56% HoH

Sales Volume6% QoQ2% YoY

(11,274)

5,483

(9,316)

10,155

(7,113)

34,730

129

162

2,480 3,360 2,123

(411)

5,581 4,574 1,671

9,695

25,035

57

83

79

760

1,145

1,191

800

1,168

754

1,146

1,185

800

1,165 871

1,365 1,336

929

1,351

Olefins

P&R BusinessesQoQ: Performance enhanced mainly from petrochemical business especially Aromatics despite lower stock gainHoH: Significantly improved performance from stock gain and petrochemical prices bounced back following global economic recovery

(GC ’s P lant)

100% 104% 93% 91% 98%Olefins

U-Rate

Aromatics

Refinery Net Income (100%)

95% 96% 96%99%

96%

Refinery

U-Rate

30.660.0 67.0

40.663.5

Acc.

GRM

18,719

99% 98% 102% 98% 100%BTX

U-Rate(GC ’s plant)

Unit : MMTHB

3,797

496 766

859

601812

371

753

966

493

859 Avg. Price:

$/Ton

271 253 287 263 270

146

240

393

155

317

Spread to Condensate: $/Ton

>100%70% QoQ

BZ: 28% QoQ

PX: 12% QoQ

Avg. Price:

$/Ton

Avg.

Dubai

2Q20 1Q21 2Q21 1H20 1H21

BZ: 64% QoQ

PX: 13% QoQ

31,811

PP: 2% QoQ

LLDPE: 3% QoQ

HDPE: 4% QoQ

14

2Q20 1Q21 2Q21 1H20 1H21

2Q20 1Q21 2Q21 1H20 1H21

50,530

(27,574)

PTT TANK

GC

TOPIRPC

>100% YoY

BZ: >100%

PX: 3%

PP: 45%

LLDPE: 46%

HDPE: 46%

BZ: 74%

PX: 35%

2Q20 1Q21 2Q21 1H20 1H21

1.6 1.9 1.6 1.1 1.7

(3.3)

5.1 3.2

(6.3)

4.2 0.2

(0.1) (0.4)

0.5

(0.2)

Hedging G/L

Stock G/L excl. NRV

Mkt GRM

(1.5)6.9 4.4

(4.7)5.7

31% 32% 30% 30% 31%

4,9683,381

4,9413,705

5,2513,779

10,119

6,692

10,192

7,484

2Q20 1Q21 2Q21 1H20 1H21

TEG Business: Power - GPSC QoQ: Higher NI from XPCL’s contribution, higher IPP’s gross profit, and partial insurance claim of Glow Energy Phase 5

HoH: NI increased mainly from XPCL’s contribution

Net Income

Sales Volume Gross profit & Gross profit marginUnit: Power: GWh / Steam: ‘000 Ton

Unit: MMTHB

Steam

Power

1,510 1,019 1,359 2,970 2,378

3,895 4,269 3,996

7,727 8,265 245 51 131

317 182

5,650 5,339 5,486

2Q20 1Q21 2Q21 1H20 1H21

IPP

SPP

VSPP & others

Gross profit margin

Gross profit

1,896 1,9732,302

3,476

4,276

2Q20 1Q21 2Q21 1H20 1H21

+ Higher shares of profit of XPCL due to increased water level in this year

- Lower gross profit margin from IPP due to unplanned outage of GHECO 1 despite SPP higher demand from Industrial power

QoQ

HoH

6% 2% QoQ

6% 12% YoY

Power Steam

Unit: MMTHB

+ Higher shares of profit of Xayaburi (XPCL) due to higher power sales

+ Higher gross profit + IPP: higher gross profit from higher AP due to lower plants maintenance in 2Q21

- SPP: lower gross profit due to increased natural gas and coal cost + Recognized other income from partial insurance claim of Glow Energy Ph. 5 incident

21% YoY

17% QoQ 23%

1% 12%

11,014 10,825 2%

Power Steam

3% QoQ

3% YoY

15

15,221

3,719 1,333

3,572

6,189

3,170

1,765

3,483

1Q21 Margin StockGain/(Loss)

OPEX DD&A Other Income Impairment FX &Derivatives

Int. & CIT Exp.& Other

2Q21

Margin

▲

Stock Gain/(Loss) OPEX

DD&A

Other Income

Impairment FX & Derivatives

Int. & CIT Exp. & Other

2Q21: 119,0891Q21: 103,868

2Q21: 12,1701Q21: 15,889

2Q21: (18,093)1Q21: (16,760) 2Q21: (38,608)

1Q21: (35,036)

2Q21: 9531Q21: 7,142

2Q21: (3,165)1Q21: 05 2Q21: (13,493)

1Q21: (11,728)

2Q21: (34,275)1Q21: (30,792)

7,750

3,400

8,867

3,437 739

3,521

4,874

▼

▲

1Q21: 5

▼

10,343

4,664

8,411

2,425 949

2,247

(4,461)

▼

TEG (mainly from power)

+ Higher share of profits from Xayaburi

+ IPP margin improved due to higher AP from less SD in 2Q21

Oil & Retail- Decreased in sales volume and gross margin from 3rd wave of COVID-19

Others- PTTT: Lower vol. and spread margin due to higher seasonal

demand in 1Q21

- Coal: Lower sales volume from lower production, and higher hedging loss

PTT Gas

+ GSP: Higher avg. selling prices & volume

- S&M: Adjusted gain of LNG resale booked in 1Q21, while

operating improved from sales volume increased and higher industrial customers’ selling prices linked to FO price

Trading- Lower gross margin and crude sales volume

PTTEP+ Higher avg. selling prices from liquid prices increased

+ Higher sales vol. from Oman Block 61, and Malaysia block HPTTEP

PTT

32,588

MMTHB

24,578

1Q21 2Q21

18,566

22,197

P&R

TEG/2

Extra Items

Extra Items*2Q21 : GC: Emery Oleochemicals impairment of 1,463 MB and

tax form selling stakes of GPSC 2,264 MB

1Q21 : EP: Gain on bargain purchase of Oman Block 61 7,033 MB offset write-off assets in Brazil 2,909 MB

Oil & Retails

(*PTT’s portion net tax amount)

2Q21 vs 1Q21 PTT Consolidated Performance (QoQ): NI dropped from extra items while operating margin improved

Petrochemical & Refining

Refinery

- Lower Stock gain in 2Q21

- Softer Mkt GRM due to higher crude premium

Petrochemical

+ Aromatics: Increase in BZ and PX spreads from higher

demand and tight supply

+ Olefins: Improved product prices from demand recovery

16

▲28%

▼29%

▼5%

▲37%

▼36%Others/1

▲33%

▼>100%

Remark: 1/ O thers business mainly contributed from PTT LNG, PTT NGD, PTTT and PTTGM etc.

2/ Technology and Engineering business mainly contributed from power business

Key Financial Ratios

1,292,717 1,387,932

530,535578,987

304,010

418,393

416,921

438,585

1,285,8451,415,903

795,503

874,316

462,835

533,678

1 2 3 4 5

11%

0.29 0.31

1.68

1.23

2020 1H21

MMTHB

Financial PositionStrong Balance Sheets maintained credit ratings

AP & Other Liabilities

PPE

Others Non-

currentAssets

AR & OtherCurrentAssets

Interest Bearing Debt (IBD)

TotalEquity

Cash & ST Invest

2,823,897

2,544,183

30 Jun 2131 Dec 20

Net Debt/EBITDA ≤ 2.0

Net Debt/Equity ≤ 1.0

PTT Ratings at Sovereign Level

Consolidated Balance Sheets

Foreign Currency Baa1 BBB+ BBB+

Local Currency Baa1 BBB+ BBB+

+ Increase in Inventories and Account Receivables from the higher product prices+ Higher PPE from PTTEP’s business acquisition of Oman Block 61 and TOP’s construction in progress of Clean Fuel Project+ Higher Interest Bearing Debt (IBD) from increase in long-term borrowing mainly from GC, GPSC, and IRPC+ Increase in Equity due to OR’s capital increase and PTT group’s net profit

17

Times

Cash Beginning Operating Investing Financing Adj & Others Cash Ending

332,032

84,889 147,171

291,414

+115,148 -203,718

+50,573 -2,621

416,921

Unit : MMTHB

*Investment in financial assets, ST/LT lending loans

Cash &Cash Equivalents

ST Investment

31 Dec 20 30 Jun 21

PTT Consolidated Cash Flows 6M21

18

Free Cash Flow

-88,570

Cash Out

-40,618

Operating 115,148 Investing (203,718) Financing 50,573

Non-Cash Adjustment 152,942 Investment (Sub. & Affiliates) (74,665) Received from Loans/Bonds 66,857

Net Income 57,166 CAPEX (64,686) Ordinary Share Issuance of Subsidiaries 53,665

Changes in Assets & Liabilities (68,046) Current Investment (61,192) Dividend Paid (33,041)

Income Tax (26,914) Others (6,656) Loan Repayment (22,829)

Dividend/Interest Received 3,481 Finance Cost Paid (14,010)

Derivatives (69)

*

438,585

Activities Highlight

Key Drivers

2Q & 1H2021 Performance

OutlookCo

nte

nts

01

02

03

04

19

PTT Group’s New Vision & Strategic Direction

05

Sources: IMF WEO (July 27, 2021), Blog by Gita Gopinath, International Industry Research and Economics Department

Global Economic Outlook: Global Economic Recovery Continues, but with Widening Gaps in Vaccine Access and Policy Support

+ Further normalization of activity in 2H2021, especially in advanced economies, as vaccine rollout proceeds and helps bring down hospitalizations

+ Sizable fiscal support in the US and new measures in other advanced economies (including France, Germany, Italy, Korea, and the UK), with associated spillovers to trading partners

+ Financial market sentiment remaining positive on balance given the expected global recovery

− Lack of access to vaccines, vaccine hesitancy, and renewed waves of COVID-19, following the emergence of highly infectious virus variants, delaying economic reopening in some countries

− Pent-up demand and supply chain bottlenecks, together with currency depreciation, putting upward pressure on prices, possibly causing some economies to begin normalizing monetary policy prematurely

IMF Forecast – 2021 GDP Growth

World: 6.0% US: 7.0% Euro area: 4.6% China: 8.1% Japan: 2.8% India: 9.5% Thailand: 2.1%

20

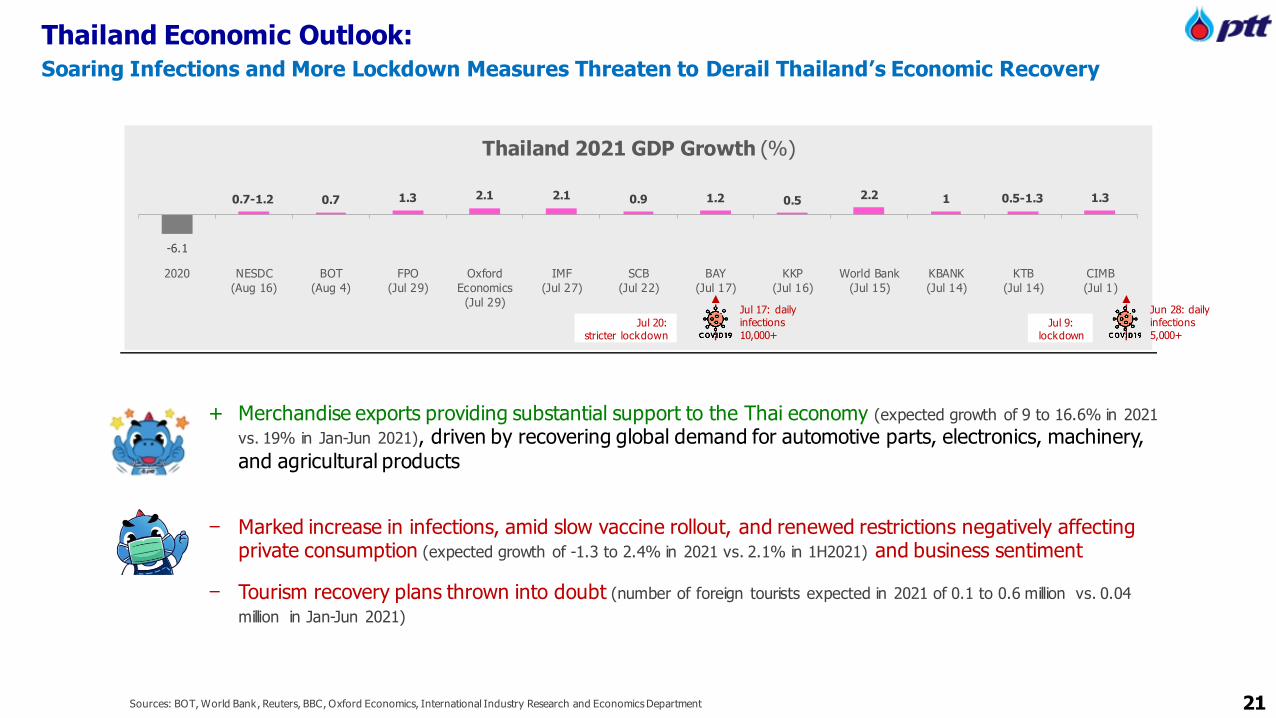

Thailand Economic Outlook: Soaring Infections and More Lockdown Measures Threaten to Derail Thailand’s Economic Recovery

21

+ Merchandise exports providing substantial support to the Thai economy (expected growth of 9 to 16.6% in 2021

vs. 19% in Jan-Jun 2021), driven by recovering global demand for automotive parts, electronics, machinery, and agricultural products

− Marked increase in infections, amid slow vaccine rollout, and renewed restrictions negatively affecting private consumption (expected growth of -1.3 to 2.4% in 2021 vs. 2.1% in 1H2021) and business sentiment

− Tourism recovery plans thrown into doubt (number of foreign tourists expected in 2021 of 0.1 to 0.6 million vs. 0.04

million in Jan-Jun 2021)

-6.1

0.7 1.3 2.1 2.1 0.9 1.2 0.5 2.2 1 1.3

2020 NESDC

(Aug 16)

BOT

(Aug 4)

FPO

(Jul 29)

Oxford

Economics

(Jul 29)

IMF

(Jul 27)

SCB

(Jul 22)

BAY

(Jul 17)

KKP

(Jul 16)

World Bank

(Jul 15)

KBANK

(Jul 14)

KTB

(Jul 14)

CIMB

(Jul 1)

Thailand 2021 GDP Growth (%)

0.5-1.3

Jun 28: daily infections 5,000+

Jul 17: daily infections 10,000+

Jul 20:stricter lockdown

Jul 9: lockdown

0.7-1.2

Sources: BOT, World Bank, Reuters, BBC, Oxford Economics, International Industry Research and Economics Department

Price 1Q21(A) 2Q21(A) 1H20(A) 1H21(A) 2020(A) 2021(E)

Dubai 60.0 66.9 40.6 63.5 42.2 63-68

Mogas 67.1 76.8 45.3 72.0 46.6 74-79

Gasoil 64.8 72.2 49.0 68.5 48.4 71-76

HSFO (3.5%S) 56.6 61.1 36.2 58.8 39.2 60-65

VLSFO (0.5%S) 67.6 71.9 50.2 69.8 49.2 70-75

Singapore GRM 1.8 2.0 0.2 1.9 0.4 2.0-2.5

23

2021 Petroleum and Gas Outlook

-5

0

5

10

15

20

0

20

40

60

80

100

1Q20 2Q20 3Q20 4Q20 1Q21 2Q21 3Q21 4Q21

Dubai Mogas Gasoil HSFO VLSFO Singapore GRM

Dubai

+ Recovered demand driven by a rise in economic activity, vaccination campaigns and mobility recovery, thus demand will gradually improve toward end of this year. However, new Delta cases will drag on near term demand

- Easing supply from OPEC+ following the increase of 2 MBD by year-end & slow supply recovery from U.S. and Iran

Gasoil

+ Demand recovery from the industrial and transportation sectors on the pace of global economic recoveries. However, subdued demand in the near term amid the COVID-19 resurgence in some Asian countries limit the upside

- Higher supply as refineries shifting Jet/Kerosene yield to produce more Gasoil

Singapore GRM

+ Improved from the recovery in light and middle distillate spreads

Fuel Oil

+ HSFO: Firm demand supported by the power demand in Middle East during summer and the upcoming utility demand in South Asia during winter

+ VLSFO: Healthy bunker demand following the global trade recovery

Mogas

+ Increasing demand restrictions are relaxed or lifted in some countries

+ Healthy summer driving demand in the US (July-August) to boost short-term gasoline price

- Concern on coronavirus Delta variant situation in some countries

- Slowdown seasonal demand during winter

Source: PTT, PRISMPetroleum Rolling as of July 2021

Pe

tro

leu

m

(GRM)$/bbl

23

02468

10121416

1Q20 2Q20 3Q20 4Q20 1Q21 2Q21 3Q21 4Q21

Asian Spot LNG

Henry Hub

Gas/LNG

Asian Spot LNG:

+ Strong fundamental gas demand growth from Chinese buyers

+ Increase gas demand in Europe as carbon and coal prices hiked

Henry Hub:

+ Increase in economic activity and easing of the COVID-19 pandemic in US

Price 1Q21(A) 2Q21(A) 1H20(A) 1H21(A) 2020(A) 2021(E)

Asian Spot LNG 10.9 10.0 2.9 10.4 4.3 12.4 – 13.8

Henry Hub (HH) 2.7 3.0 1.8 2.9 2.1 2.9 – 3.5

Ga

s/LN

G

$/MMBTU

Source: PTT, PRISM Petrochemical Rolling as of Jul 2021 22

600

800

1,000

1,200

1,400

1Q20 2Q20 3Q20 4Q20 1Q21 2Q21 3Q21 4Q21

HDPE CFR SEA

PP Yarn CFR SEA

200

400

600

800

1Q20 2Q20 3Q20 4Q20 1Q21 2Q21 3Q21 4Q21

200

400

600

800

1,000

1Q20 2Q20 3Q20 4Q20 1Q21 2Q21 3Q21 4Q21

BZ FOB Korea

PX CFR Taiwan

2021 Petrochemical Outlook

$/Ton

$/Ton

Aromatics

+ Expected more balanced BZ/PX markets from downstream capacities start-up, economic recovery, and firmer upstream crude price

+ Healthy Chinese BZ demand due to relatively low inventories

- Pressured PX price from persistent squeezed PTA and end-products margins & concerns on a sharp spike of COVID-19 infected cases and lockdown in some Asian countries in 3Q21 to affect downstream demand

- Cautious BZ/PX market direction from uncertainty on the start-up timing of China’s Zhejiang PC and Saudi Aramco in 2H21

Naphtha

+ Additional demand from new crackers startup, particularly in China and South Korea, to bolster demand

+ Seasonal demand from Petrochemical sector before New Year holidays

- Expectation on easing supply from higher refinery runs due to better COVID-19 situation

Olefins

+ Expected demand recovery due to brighter economic prospects to support olefins prices

- Easing US export supply to put pressure on Asian market sentiment

- Subdued SEA end-products demand amid rapid spreading of Delta variant COVID-19 and lockdown measures in some countries in 3Q21

- Incoming additional Asian capacities from Northeast Asia and Southeast Asia especially China in 2H21

$/Ton

Source: PTT, PRISM Petrochemical Rolling as of Jul 2021

Price 1Q21(A) 2Q21(A) 1H20(A) 1H21(A) 2020(A) 2021(E)

HDPE 1,145 1,191 800 1,168 880 1,100-1,150

PP Yarn 1,348 1,306 891 1,327 963 1,210-1,260

Price 1Q21(A) 2Q21(A) 1H20(A) 1H21(A) 2020(A) 2021(E)

Naphtha MOPJ 557 606 357 581 380 550-650

Ole

fin

sA

rom

ati

cs

Na

ph

tha

23

Price 1Q21(A) 2Q21(A) 1H20(A) 1H21(A) 2020(A) 2021(E)

BZ 753 966 493 859 485 860-910

PX 766 859 601 812 577 830-880

Upcoming projectOn 2H2021

100.0%

RA#6 : Ratchaburi -Wangnoi

COD:Sep 2021

98.3%

5th Pipeline

COD:3Q2021

84.7%

Phase III

In the process of preparing to construct :

To COD in Dec 2022

Phase I Phase II

High-quality Circular

Plastic Resin Plant

: 45 KTA

COD: Sep 2021

COD:1Q2022

Performance Recovery

PTT GroupGas Business

• Improve GSP U-Rate

GSP’s U-Rate ~ 92-94% in 2021

• Gas Volume Growth: CAGR 3.1% during 2021 -2025

E&P : + Crude oil price recovery+ Vol. rise ~16% + Unit Cost drop ~5%

OIL : - COVID-19 pandemic will suppress domestic demand+ Strong network through expanding

• Oil Stations +192 stations • EV Charging Stations +100 stations • Café Amazon + 552 outlets

P&R : + Refinery U-Rate ~95–97% + SG GRM ➔ 2.0 - 2.5$/bbl+ Petrochemical spread increase

Power : + Industrial demand increase ~4.5%

• Flat Pooled gas cost

• NG DemandIncrease ~1% vs 2020

Maintenance Schedule

2H21: Planned Major TA : Ethane Crackers3Q-4Q: HDPE2 Major TA : ~1 month

2H21

3Q: GSP#6 Major TA : 26 daysGSP#3 SD : 8 days

4Q: GSP#3 SD : 6 days GSP#6 SD : 9 days

Gas Separation Plants

Petrochemical Plants

Avaada Solar Power Platform

in India : 3,060 MW (GPSC’s portion

= 1,273 MW)COD: 2021-2022

Bakery Plant

COD: 4Q2021

24

Non-woven Fabric Plant (Innopolymed)

: 2.1 KTA COD: Dec 2021

Activities Highlight

Key Drivers

2Q & 1H2021 Performance

OutlookCo

nte

nts

01

02

03

04

PTT Group’s New Vision & Strategic Direction

05

25

PTT’s Vision has set directions for our past successes

✓ Energy self-sufficiency

✓ Petrochemical industry development

Strategic

Direction

✓ Resolved economic

crisis

✓ Fuel the Thai economy

– Market cap up by 100

bn THB on IPO✓ TAGNOC to

shift toward

Knowledge-

based

economy

2530 2540 2550 25602521 2563

Energy security for maximum benefit to

the nation

World-Class oil company with competitive edge

High performance org. & balance stakeholders

expectation?Thai Premier Multinational

Energy Company

✓ Inclusive

growth driving

sustainable

growth for all

sectors

History of PTT Vision

✓ – Big company Fortune 100 –

Strong Performance

– DJSI

Energy

security

Value

creation

Debt

restructuring

IPO

Key evolution

Economic growth led development

Economic stability & social development

• People centered development paradigm

• Participation Approach• Sufficiency Economy

Thailand 4.0 “Security, Prosperity,

Sustainability”Country direction

2551

China Japan

Korea

Philippines

Australia

Nigeria

Middle East

CrudePetroleum ProductsPetrochemical Products

CrudePetroleum ProductsPetrochemical Products

Algeria

Indonesia

Brazil

USA

India

Singapore

VietnamTaiwan

Build competitiveness in

global arena

Energy transition &

Technology disruption

Aspiration:

POWERING THAILAND’S TRANSFORMATION

2557254425402524

BIG LONG STRONG

RestartResilience

ReformReimagination

26

(B.E.)

PTT’s vision is revised to set aspirations

along with future trends

with Future Energy and Beyond

Powering Life

27

Technology & Innovation

Partnership & Platform

Positive Contribution to enhance livelihood

Low Carbon Society Growth along the way of life

to empower and better life

Deliver inclusive growth to create economic growth while

enhance quality of life – people, society, community, and environment

Powering Life with future energy and beyond Purpose

28

Powering life with

Future Energy and Beyond Strategic Positioning

Future Energy

BeyondLife

Science

Logistics & Infrastructure

Mobility & Lifestyle

High Value Business

AI, Robotics digitalization

Ready to explore…

Renewable

EV Value Chain

Hydrogen

Energy Storage & System Related

focus more on future energy trend

and new businesses that have potentials to grow

Moving toward future energy and energy technologies which are clean and environmental friendly as

well as stepping into new potential businesses that support people live and drive people well-being

29

Directing energy business in line with future trend

Reinforce Reignite new businessat speed and scaleReimagine

Focus on

Lower-carbon portfolio

▪ Collaboratively build LNG value

chain platform

▪ Accelerate LNG portfolio development through partnership

Fully integrated player in gas and LNG value chain

▪ Coal business divestment

▪ Downstream Business Portfolio

Rebalancing

▪ Resilience for Refinery Business

▪ To be Global Player with Digital

Forefront

▪ Synchronized Upstream &

Downstream Optimization

Acceleration into

LNG value chain Powering

Downstream along with Future Energy

▪ Renewable Energy

▪ Energy Storage

System

▪ EV Value Chain

▪ Energy Platform

▪ Other potential

(e.g. H2)

Expedite execution

New Energy & EV

& integrate Renewable Energy Value Chain with

PTT Group Business

30

Growing along the way of life beyond energyReignite New Business at Speed and Scale

PTT Group’s Marketing PlatformFocus on 3rd Party Logistics (3PL) segment with interest in 2nd Party Logistics (2PL)

Mobility LifestyleStrive one-stop solution for

All Lifestyle

Rail & Terminal

Modern Logistics Solution & Platform▪ Seamless logistic solution provider

▪ Rail-based intermodal logistics services provider

Strengthen energy solution for

Seamless Mobility

Oil Ecosystem

Energy

SolutionEcosystem

F&BEcosystem

One-stop

SolutionEcosystem

through M&A

Coating and Adhesive

Next HVB

▪ Accelerating growth in attractive segments(e.g. composites & UPR, coating additives)

▪ Seeking more opportunities in HPP and Composite

Pharmaceutical

Medical Technology

Nutrition

Investment in Generics / Biopharma Company

(e.g. Covid-19 Test Kit, Meltblown, MED.

GLOVES and MED. DEVICE)

Explore opportunities inAI, Robotics & Digitalization▪ Robotic / AI

▪ Digital platform

▪ Cloud service provider, Data center

co-location

31

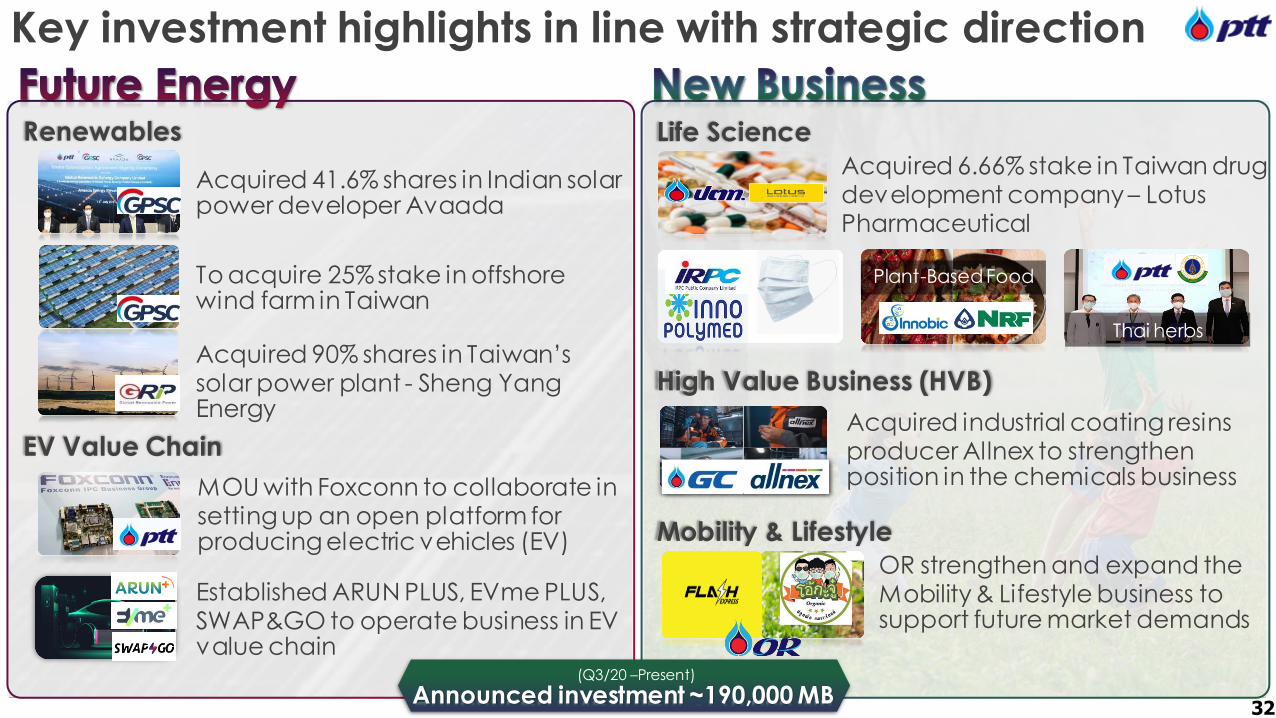

Key investment highlights in line with strategic direction

Renewables

Acquired 90% shares in Taiwan’s solar power plant - Sheng Yang Energy

Acquired 41.6% shares in Indian solar power developer Avaada

EV Value Chain

MOU with Foxconn to collaborate in setting up an open platform for producing electric vehicles (EV)

Established ARUN PLUS, EVme PLUS, SWAP&GO to operate business in EV value chain

Acquired 6.66% stake in Taiwan drug development company – Lotus Pharmaceutical

Life Science

Plant-Based Food

Thai herbs

High Value Business (HVB)

Mobility & Lifestyle

Acquired industrial coating resins producer Allnex to strengthen position in the chemicals business

OR strengthen and expand the Mobility & Lifestyle business to support future market demands

To acquire 25% stake in offshore wind farm in Taiwan

Announced investment ~190,000 MB(Q3/20 –Present)

32

Overall Strategic Direction to achieve purpose of New Vision

E&P

Gas

Oil & Retail

Power

P&R

• Build global LNG portfolio

• Expand growth for high return asset

& mainly invest in gas assets

• Accelerate growth in Thailand &

region

• Grow in retail with customer-

oriented

• Move to mobility & lifestyle

• Supply chain integration

• Move to high value business

Direction Business

Newbusiness

New Energy

• Scale up potential business e.g. life

science, logistics & infrastructure

• Expedite growth in new energy e.g.

renewable, energy storage & system

related and EV value chainFuture Energy(RE, ESS, EV)

New businessFuture

Energy

&

Beyond 32%

15%

17%

CAPEX(2021 – 2030)

PTT Group 68%

Hydrocarbon Business

(E&P, Gas, LNG, Power, P&R, Oil)

NI from Future Energy and Beyond > 30%1

New growth

Power (Conventional) 8 GW

LNG* 9 MTA

Renewable energy 12 GW

Business growth

2

315% GHG reduction from 2020

Clean growth

(Moving to net zero GHG within 2070)

* LNG Equity and controlling of portfolio v olume 33

Thank youPTT Public Company Limited

Investor Relations Department

Disclaimer

The information contained in our presentation is intended solely for your personal reference only. Please do not circulate this material. If you are not an intended recipient, you

must not read, disclose, copy, retain, distribute or take any action in reliance upon it. In addition, such information contains projections and forward-looking statements that

reflect our current views with respect to future events, financial performance and result of PTT’s activities. These views are based on assumptions subject to various risks and

uncertainties. No assurance is given that future events will occur, that projections will be achieved, or that our assumptions are correct. Actual results may differ materially from those projected.

The information contained in this presentation is subject to change without notice and PTT does not undertake any duty to update the forward-looking statements, and the

estimates and assumptions associated with them, except to the extent required by applicable laws and regulations.

35

Tel. +66 2 537-3518, Fax. +66 2 537-3948

Website: http://www.pttplc.com

E-mail: [email protected]

34

Questionnaire

PTT Gas

+ GSP: Higher avg. selling prices & volume and lower feed

gas cost

+ S&M: Higher industrial customers’ selling price linked to FO price, lower pooled gas cost, and higher sales vol.

from most of customers

Trading- Lower sales volume from Covid-19 impact

-

69,485

61,401

1,316 3,177 6,237

1,677

31,782

52,504

-

6M/2020 Margin StockGain/(Loss)

OPEX DD&A Other Income Impairment FX &Derivatives

Int. & CIT Exp.& Other

6M/2021

Margin

▲

Stock Gain/(Loss)

OPEX

DD&A

Other Income

Impairment

FX & Derivatives

Int. & CIT Exp. & Other

1H21: 222,9571H20: 153,472

1H21: 28,0591H20: (33,342)

1H21: (34,853)1H20: (33,537)

1H21: (73,644)1H20: (70,467)

1H21: 8,0951H20: 1,858

1H21: (3,160)1H20: (1,483)

1H21: (25,221)1H20: 6,561

1H21: (65,067)1H20: (12,563)

6,679

9,344

(13,304)

2,423 1,205 5,077

(925)

18,093

8,064

17,278

5,862 1,688 5,768 413

▲

▼

▲

▲

▲

PTTEP- Loss from oil price hedging from upward oil price trend

+ Higher Avg. Selling price from liquid prices increased

+ Higher Sales vol. from Oman Block 61 acquisition,

Bongkot, Contract4, and Malaysia projectPTTEP

PTT

10,499

MMTHB

57,166

1H20 1H21

29,107

40,763

P&R

Extra Items

Oil & Retails

1H21 vs 1H20 PTT Consolidated Performance (HoH): Significantly improved performance in most of PTT Group Businesses

Petrochemical & RefiningRefinery+ Higher Stock gain in 1H21

+ Higher Mkt GRM mainly from gasoline spreadPetrochemical

+ Olefins: Improved product prices and sales volume

+ Aromatics: Increased in BZ & PX spreads

35

TEG/2Others/1

▲40%▲>100%

▼14%

▲>100%

▲>100%

▲>100%▲14%

Remark: 1/ O thers business mainly contributed from PTT LNG, PTT NGD, PTTT and PTTGM etc.

2/ Technology and Engineering business mainly contributed from power business

Oil & Retail+ Improved oil margin, and non-oil expansion- Lower oil volume due to Covid-19 impact

TEG (mainly from power)+ Higher share of profits from XPCL due to higher water level

+ Higher contribution from increasing PTT’s direct holding in

GPSC

OthersCoal: Higher margin due to increased selling prices

following Newcastle coal price

Extra Items*1H21 : EP: Gain on bargain purchase of Oman Block 61

7,033 MB, offset write-off assets in Brazil 2,909 MB

GC: Emery Oleochemicals impairment of 1,463 MB,

and tax from selling stakes in GPSC 2,264 MB

1H20 : EP: Mariana Oil Sands impairment of 925 MB

(*PTT’s portion net tax amount)

52

6876

55

72

45 4652

47 49

55

89

109

61

99

2Q20 1Q21 2Q21 1H20 1H21

- - -

0.9

22.2

3.0

13.1

25.2

2Q20 1Q21 2Q21 1H20 1H21

Other Business : Coal business (SAR) QoQ: NI declined due to lower sales volume, and hedging loss as New Castle price spikedHoH: NI increased from higher selling prices due to referenced New Castle price surged and lower DD&A

1/ Average Calorific value ~ 5,400 kcal/kg

36

Unit: $/Ton

Avg. Selling Price

Total Cash Costs

New Castle

Unit: MMUSD

Avg. Selling Price1/ & Cash cost1/

QoQ

1,472 1,468 1,221

3,257 2,689

150 30

285

30

2Q20 1Q21 2Q21 1H20 1H21

kTon

Jembayan

Sebuku

1,622 1,4681,251

15% QoQ23% YoY

QoQ

- Lower sales volume caused by lower production plan and rainy season in Indonesia

+ Selling price increased due to rising New Castle price

- NI declined mainly from hedging loss, as New Castle price rose

HoH

+ Selling price largely improved following referenced New Castle price

- Cash cost increased from higher mining cost and gas oil price

- Sales volume dropped from lower production plan and cease operation of the Sebuku coal mine

+ NI increased mainly from higher margin from sharply increased selling prices and lower DD&A from impairment of assets in 2020

Sales Volume

Net Income (100%) Key Highlights

86% QoQ>100% YoY

3,542

2,719

23%

92%

12%

22%

13%

31%

62%

4%

7.718.75

13.43

22.40

30.57

34.1434.82

18.33

21.06

29.58

37.24 36.58

32.52

20.34

6.73

32.68

46.74

4.15

2.50 2.854.00

6.75

9.25 10.5011.50

8.008.50

10.2513.00 13.00 13.00

11.00 10.00

16.00

20.00 2.00 2.00

32.4% 32.6% 29.8% 30.1% 30.3% 30.8% 33.0%43.6%

40.4% 34.7% 34.9% 35.5%40.0%

54.1%

148.6%

49.0% 42.8% 48.2%62.5%

75.8%

-900.00%

-600.00%

-300.00%

0.00%

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

25% PTT’s min. payout ratio Policy

Baht / share

Dividend Policy & Historical Payments

Y2020 Dividend payout at 75.8%

* Spilt par value from 10 to 1 Baht/share since 24 April 2018

10-Year Avg. 59%

Avg. since IPO46%

1.00

37

Split par*

1.32

3.20

Dividend payout

EPSDPS

*Investment in financial assets, ST/LT lending loans

Cash &Cash Equivalents

ST Investment

31 Dec 20 30 Jun 21

Unit : MMTHB

PTT Only Cash Flows 6M21

38

Free Cash Flow

+27,176

Cash In

+989

Cash Beginning Operating Investing Financing Adj & Others Cash Ending

56,342

44,404 33,770

57,331

+21,594 +5,582 -26,271

+84

91,101

100,746

Operating 21,594 Investing 5,582 Financing (26,271)

Net Income 37,251 Dividend/Interest Received 20,800 Dividend Paid (23,420)

Non-Cash Adjustment 235 Current Investment 8,268 Finance Cost Paid (2,726)

Changes in Assets & Liabilities (13,018) Others 6,643 Loan Repayment (82)

Income Tax (2,874) Investment (Sub. & Affiliates) (26,093) Others (43)

CAPEX (4,036)

*

PTT Group Performance : 2Q2021 (QoQ & YoY)

1/Including PTTGE,BSA, PTT TCC and RTC

39

% PTT

holding

2Q20 1Q21 2Q21 QoQ YoY 2Q20 1Q21 2Q21 QoQ YoY

PTT Net operating Income 4,963 8,498 9,595 13% 93% 4,963 8,498 9,595 13% 93%

E&P - PTTEP 4,322 11,534 7,139 -38% 65% 65.29% 2,823 7,524 4,664 -38% 65%

Petrochemical 1,728 9,778 25,114 >100% >100% 845 4,675 1,469 -69% 74%

- GC 1,671 9,695 25,035 >100% >100% 48.42% 788 4,592 1,390 -70% 76%

- Other 57 83 79 -5% 39% 57 83 79 -5% 39%

Refining 2,069 8,941 6,697 -25% >100% 532 4,192 3,215 -23% >100%

- TOP 2,480 3,360 2,123 -37% -14% 48.03% 704 1,615 1,006 -38% 43%

- IRPC (411) 5,581 4,574 -18% >100% 48.05% (172) 2,577 2,209 -14% >100%

Oil - OR 520 4,003 3,225 -19% >100% 75.00% 559 3,439 2,439 -29% >100%

TEG - GPSC/TP/DCAP/PTTES/PTTDIGITAL/ENCO 2,568 17,037 2,702 -84% 5% 641 739 949 28% 48%

Others Business 2,132 3,485 2,824 -19% 32% 1,702 3,221 2,245 -30% 32%

Inter - PTTER/PTTGM 342 531 345 -35% 1% 100% 40 493 3 -99% -93%

Gas - PTTLNG/PTTNGD/PTTGL/TTM(T)/TTM(M) 1,465 2,255 2,282 1% 56% 1,337 2,029 2,039 0% 53%

Other - PTTT/Others1/ 325 699 197 -72% -39% 325 699 203 -71% -38%

Shared of Net Income from Affiliates 13,339 54,778 47,701 -13% >100% 7,102 23,790 14,981 -37% >100%

Tax adjustment for gain on disposal of investment and asset (12) 300 2 -99% >100% (12) 300 2 -99% >100%

PTT Conso. Net Income 18,290 63,576 57,298 -10% >100% 12,053 32,588 24,578 -25% >100%

Unit : MMTHB

Performance 100% Equity Method % PTT

PTT Group Performance : 1H21 vs 1H20 (HoH)

1/Including PTTGE,BSA, PTT TCC and RTC 40

% PTT

holding

1H20 1H21 HoH 1H20 1H21 HoH

PTT Net operating Income 6,679 18,093 >100% 6,679 18,093 >100%

E&P - PTTEP 12,935 18,673 44% 65.29% 8,419 12,188 45%

Petrochemical (6,984) 34,892 >100% (3,213) 6,144 >100%

- GC (7,113) 34,730 >100% 48.42% (3,343) 5,982 >100%

- Other 129 162 26% 130 162 25%

Refining (20,590) 15,638 >100% (10,091) 7,407 >100%

- TOP (11,274) 5,483 >100% 48.03% (5,659) 2,621 >100%

- IRPC (9,316) 10,155 >100% 48.05% (4,432) 4,786 >100%

Oil - OR 2,418 7,228 >100% 75.00% 2,423 5,878 143%

TEG - GPSC/TP/DCAP/PTTES/PTTDIGITAL/ENCO 4,802 19,739 >100% 1,205 1,688 40%

Others Business 5,672 6,309 >100% 5,491 5,466 0%

Inter - PTTER/PTTGM 448 876 96% 100% 362 496 37%

Gas - PTTLNG/PTTNGD/PTTGL/TTM(T)/TTM(M) 3,818 4,537 19% 3,723 4,068 9%

Other - PTTT/Others1/ 1,406 896 -36% 1,406 902 -36%

Shared of Net Income from Affiliates (1,747) 102,479 >100% 4,234 38,771 >100%

Tax adjustment for gain on disposal of investment and asset (414) 302 >100% (414) 302 >100%

PTT Conso. Net Income 4,518 120,874 >100% 10,499 57,166 >100%

Unit : MMTHB

Performance 100% Equity Method % PTT

Subsidiaries ConsolidatePTT Energy Resources Co., Ltd. PTTER 100.00%PTT Green Energy Pte. Ltd PTTGE 100.00%PTT Global Management Co., Ltd. PTTGM 100.00%

Subsidiaries ConsolidatePTT Oil & Retail Business Co., Ltd. OR 75.00%

Subsidiaries ConsolidatePTT Exploration & Production Plc. PTTEP 65.29% 2/

PTT Natural Gas Distribution Co., Ltd. PTTNGD 58.00%PTT LNG Co., Ltd. PTTLNG 100.00%PTT Global LNG Co., Ltd PTTGL 50.00%

Joint Ventures EquityTrans Thai-Malaysia (Thailand) Co., Ltd. TTM (T) 50.00%Trans Thai-Malaysia (Malaysia) Sdn. Bhd. TTM (M) 50.00%Map Ta Phut Air Products Company Limited MAP 49.00%

Petrochemical Subsidiaries ConsolidatePTT Global Chemical Plc. 1/ GC 48.42% 2/

PTT Tank Terminal Co., Ltd. PTTTANK 100.00%

Refining Subsidiaries ConsolidateThai Oil Plc. 1/ TOP 48.03% 2/

IRPC Plc. 1/ IRPC 48.05% 2/

Subsidiaries ConsolidateBusiness Service Alliance Co., Ltd. 1/ BSA 25.00%4/

PTT Treasury Center Co. Ltd PTT TCC 100.00%

Subsidiaries Consolidate

Global Power Synergy Co., Ltd1/ GPSC 75.23% 2/

Thai Oil Power Co., Ltd. 1/ TP 3/ 26.00%PTT Digital Solutions Co., Ltd. 1/ PTT DIGITAL 20.00%PTT Energy Solutions Co., Ltd. 1/ PTTES 40.00%Energy Complex Co., Ltd. EnCo 50.00%

Joint Ventures EquityDistrict Cooling System and Power Plant DCAP 35.00%

Remark : 1/Subsidiaries that PTT holds less than 50% but being consolidated because PTT has the power to control the financial and operating policies.

2/ Holding portion of PTT Group (direct & indirect)

Data as of 30 Jun 2021

Subsidiaries Consolidate PTT International Trading Pte. PTTT 100.00%PTT International Trading London Ltd PTTT LDN 100.00%PTT International Trading USA Inc. PTTT USA 100.00%

PTT Group Accounting Structure

Others Fair valueBaania (Thailand) Company Ltd. Baania 2.73%HG Robotics Plc. HG Robotics 9.49%Innospace (Thailand) Innospace 15.75%Sunfolding, Inc. Sunfolding 5.59%Luminar Technologies, Inc. Luminar Technologies 0.06%

Others Fair valueSarn Palung Social Enterprise Company Ltd. SPSE 20.00%Dhipaya Insurance Plc. TIP 13.33%

Joint Ventures EquitySuez Environmental Services Co.,Ltd. SES 40.00%

41

E&P and Gas Business Group International Trading Business GroupPetrochemicals &

Refining Business Group

Oil Business Group

Technology and Engineering Business Group International Investment Business Group

Others

3/ Entire business transfer to TOP on 1 Feb. 20214/ PTT holds 100.00% of BSA’s ordinary shares, PTT’s ownership interest in BSA is 100%

14,200

2,000

12,000

24,354

3,000

13,000

2,00012,236

7,0004,000

3,884

3,222

6,346

18,38622,555

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000USD (LHS)

THB (LHS)

PTT Debt Outstanding (RHS)

84,702 92,487 91,451

369,409449,943 443,644

32,67953,946 57,092

236,049

288,567345,610

117,381 146,433 148,543

605,458

738,510789,254

31 Dec 19 31 Dec 20 30 Jun 21 31 Dec 19 31 Dec 20 30 Jun 21

USD&Others THB

Debt Profile : Control Cost & Manage Risk

Debt Portfolio

Managed debt according to financial risk and policy

ConsolidatedPTT OnlyUnit : MMTHB : Cost of debts ~ 4.60%

: % fixed-rate ~ 77.66%: Avg. debt life ~ 17.38 years

: Cost of debts ~ 3.56%

: % fixed-rate ~ 73.59%: Avg. debt life ~ 11.42 years

(38%)

(62%)

(37%)

(63%)

(44%)

(56%)

(39%)

(61%)

(28%)

(72%)

(39%)

(61%)

Note : 1. PTT Data as of 30 Jun 21 (THB/USD = 32.2219 THB/JPY = 0.2940) excluding liabilities from finance leases.

3. Cost of debts, % fixed rate, and avg. debt life took into account the derivative transactions, including withholding tax (update as of 30 Jun 21).

2. Debt Outstanding represents amount and portion before derivative swaps, and reconciled with accounting.

FX: 32.2219

As of 30 Jun 21

*PTTC10DA (C entury Bonds) is due on 2 Dec 2110

Unit : MMTHB

Note: 1. Debt O utstanding for Repayment Profile represents financial data and portion after derivative swaps

2. Bond repayment amounting 3,884 MB in 2022 is THB swaps to USD and amounting 6,236 MB in 2035 is USD swaps to THB

5,884

15,458

PTT Only : Debt Outstanding and Repayment Profile

42

Gas Business RoadmapShort term Gas Demand growth be maintained

Thailand Gas Demand Outlook (Short Term – 5 year plan)

LNG Terminal 2

+7.5 MTA

New SupplyAdditional capacity

(mmscfd)

Major Project : COD & Capacity/

Accumulate Pipeline distance

5th pipeline

RA#6 Pipeline

4,702 KM

Bongkot Erawan

700 800

GSP#7*

460 mmscfd

BPK-SB** pipeline

4,776 KM

43

*Replace GSP#1 **Bang Pakong–South Bangkok Power Plant

4545

Natural Gas Price Structure : As of Jun 2021

CustomersSales Price Structure

Gas Pool Price Supply Margins Pipeline Tariffs+ +

Average Purchased Gas Price

1.75%

1.75%

9.33%

21.7 Bt/MMBtu

Charged at the same price structure of power producers

Reference to a bi-weekly average of Platt’s FOB Arub Gulf price

Charged at prices comparable to fuel oil

Gas prices are mostly agreed under long term contracts and volatility pass-through to ensure stable returns

Profit-sharing mechanism based on market prices of petrochemicals

Reference to Naphtha market price

At GSPs cost (adjusted every 3 months)

*

*

*

* EGAT IPP and SPP Supply Margins not more than 2.1525 and 11.4759 bt/mmbtu respectively

44

GSP 21%

Petrochemicals Feedstocks

Industry 17%

Ethane, Propane, LPG

NGL

Local Cooking Gas

Export Cooking Gas

Power Producers 59%

: EGAT 17%

: IPP 14%

: SPP 28%

Charged at Avg. gas cost + Operating cost (3.892 bt/kg) for both Public & Private vehiclesNGV’s selling price reflects the natural gas cost and operating cost* (including gas quality adjustment) * The allowed operating cost is still regulated and not fully cover PTT’s operating cost

A s of 16 Jul 2021 = 14.55 Baht/Kg.

Public transportation vehicles : regulated and capped to minimize the impact from the rising global crude prices on end-users• Since 16 May 2018 : Allowance to adjust NGV public price from 10.62 Baht/Kg. to 13.62 Baht/Kg. by every 4 month (16 May 19, 16 Sep 19 and 16 Jan 20)• Since 1 Jan 2021 : Use the same pricing as private vehiclesPrivate vehicles: reflect the natural gas cost, gas quality adjustment and operating cost (not fully cover PTT’s operating cost)• Since 16 Jul 2016 : The retail price is set to reflect the natural gas cost but operating cost is still regulated• Since 5 Sep 2017 : Allowance to adjusted +0.46 Baht/Kg. to 3.8920 Baht/Kg. for gas quality improvement cost

NGV 3%

Gas Business Generates Stable Returns

Sole owner and operator of entire

gas transmission pipelines in

Thailand (~ 4,000 km), a regulated

business

• IRROE ranges between

12.5% - 18% for transmission

pipeline investment

Supply & marketing of natural gas

provides fixed margin with long-term

contracts of 25-30 years

6 Gas Separation Plants; Total

production 6.7 MTA; are on

petrochemical market price-linked

profit sharing basis

Overview Gas transmission pipeline capacity

Gas Separation Plant Capacity

Unit 1 420 MMcf/d

Unit 2 and 3 820 MMcf/d

Unit 4 170 MMcf/d

Unit 5 580 MMcf/d

Unit 6 880 MMcf/d

45

PTT Group Clean & Green Strategic Execution

2030 GOAL

Aim to achieve Carbon Neutrality By 2065-2070 (align with "National Energy Plan")

Aim to reduce GHG emission15% from 2020

Continue execution in GHG reductionand initiate carbon price application to enable green investment

2012

Base year

2018 2021 2030

Financial & investment Mechanism

Carbon Exchange Platform

EnablerCarbon Neutral Framework

Scope 3 (Other Indirect Greenhouse Gas Emission)

Scope 1+2

Carbon Credit Offset

Reforestation & Community GHG Project

Biofuel / Low Carbon Product Electric Mobility

Renewable Energy in Operations

Process Optimization & Energy Efficiency (All facilities)

(All facilities)

CO2 Utilization and Storage (PTTEP, PTT)

Renewable/New Energy Investment(PTT, GPSC)

(PTT)(OR, GC, IRPC, TOP, INI)

(CSR)

R&D Partnership

As Hidden Price in Feasibility Study

Review and adjust price to ensure meeting GHG reduction target

Apply Carbon Price in Investment Decision Process

per ton CO2e

STRATEGIC DIRECTION

to achieve GHG reduction

and manage carbon intensity

Circular Economy(GC, IRPC)

(Direct and Indirect

Greenhouse Gas Emissions)

46

PTT Suggestion for Thailand moving toward low carbon society

Economic tools

Business expansion

Regulationestablishment

& revision

Provide incentives for GHG reduction activities

e.g. tax exemption, low interest loan

Develop clear rules and regulation for carbon

taxes, if imposed

Establish carbon credit platform and support for

transparent trade

Support the potential businesses in GHG

reduction technology

Improve regulations tosupport

CCUS and related technology

Promote wider participation in ‘Low Carbon Business’ among SMEs

Promote ‘Ecotourism’ to offset with the loss from fuel tax income as well as cope with the trends

Energy efficiency in public/private sector

the participation of public sector in reforestation

47

PTT Sustainability Strategic Direction

Sufficiency Economy ESG

Reasonableness Prudence Social Governance & Economics

Environmental

DJSI SDGs

Sufficiency Economy

SUSTAINABILITY as Business Goal

Operate with Integrity (GRC)

Economic Drive by creating ‘Next Growth’

Circular Economy

Low Carbon Society

Social Shared Value

Workforce for

New Growth

PTT’s Sustainability DNA

Sustainable Production and Consumption

ENVIRONMENTAL GOVERNANCE

Good Governance and Performance Excellence

SOCIALPeople’s

Well-being

Safety and Human Rights

VirtuesKnowledge

Moderation

โลกเราตอ้งรกัษ์ สงัคมไทยเราตอ้งอุม้ชู ผลด าเนนิงานเราตอ้งเลศิ

48