2Q 2010 Private Equity Breakdown - Urish · PDF file2Q 2010 Private Equity Breakdown Presented...

8

2Q 2010 Private Equity Breakdown Presented by: P itch B ook PitchBook is the ACG Preferred Private Equity Research Provider

Transcript of 2Q 2010 Private Equity Breakdown - Urish · PDF file2Q 2010 Private Equity Breakdown Presented...

2Q 2010 Private EquityBreakdown

Presented by:

PitchBook

PitchBook is the ACG Preferred Private Equity Research Provider

[email protected] [ 2 ]

Private Equity: Data | News | Analysis

The PitchBook DifferenceBetter Data. Better decisions.

Driving Value from Due Diligence in an Uncertain Market

BDO’s Transaction Advisory Services Team supports both strategic and financial buyers in multi-million dollar domestic and international investment decisions, leveraging the deal expertise, and industry and technical specialism of senior professionals to provide focused, value driven advice.

As we head into the second quarter of 2010, many investors appear optimistic about the outlook for private equity. The middle market, in particular, seems poised to emerge as the frontrunner in the race for PE deals in 2010. Credit markets are continuing to stabilize and deal volume seems to be recovering, with more deals being completed in the first quarter of 2010 than in the trailing four quarters. But despite cautious optimism from investors, the market is still filled with uncer-tainty, heightened by potential regulatory and fiscal changes that could significantly impact the PE return model. For those attempting to source and close deals, one quarter of data may not be enough to indicate a reliable trend.

The same uncertainty in trend plagues both strategic and financial investors alike in acquisition decisions. As buyers invest precious fund resources, the due diligence process has become even more critical. At BDO, we see five critical factors emerging as true value drivers in this process.

Looking further into 2010, despite continued pricing disparity and trend uncertainty, we expect private equity volume, particularly in the middle market, to remain solid. Buyers who make informed decisions supported by a robust due diligence process likely will continue to drive attractive returns from successful transactions.

Make sure the scope fits the deal: No two deals are equal; therefore the diligence process from deal to deal should not be equal either. By spending additional time to focus the scope of the engagement, acquirers can ensure the right level of diligence is performed to address deal specific risk, avoiding a broad checklist mentality with an accompanying broad fee range. Overall investment risk in today’s market, the investment thesis, the type of investment being considered and the seller’s motivation should drive a tailored approach, using phasing to validate the key areas first and then follow-up when deal certainty is more clear.

Focus on the future: In the past, financial due diligence was historically focused; however, in today’s economic environment, historical performance may not be an accurate indicator of current, or future, value. Evaluating the sustainability of earnings remains a critical and increasingly complex part of the buy-side due diligence process; buyers should be cautious of short term, unsustainable measures taken by targets to shore up their performance metrics.

Cash is still king: Now more than ever, buyers must understand not only the cash-generating abilities of a business, but also the cash required to sustain and fund its growth. Working capital that is artificially lean, deferred-capital spending, and unexpected change-of-control outflows are areas requiring heavy scrutiny.

What the numbers don’t tell you: Financial metrics are only half of the picture. Operating efficiency, customer and supplier relationship quality and longevity, key management effectiveness and retention, strategic focus and economic responsiveness, and their collective contribution to value, merit careful and ongoing evalua-tion throughout the deal process.

Mind the GAAP1: In the wake of the economic downturn, pressures to achieve results – or to dress a company up for sale – may influence companies’ accounting decisions and judgments, causing them to consider taking items off of the balance sheet, or otherwise compromise comparability. While GAAP isn’t known for breaking a deal, its misapplication can fracture a future debt covenant and should remain in focus. Tax is another focal point; depressed deal values reduce tax attribute monetization and compliance lapses caused by operational distraction bring both risk and negotiation opportunity to the deal table.

Market Insight from

1Generally Accepted Accounting Practices

[email protected] [ 3 ]

Private Equity: Data | News | Analysis

The PitchBook DifferenceBetter Data. Better decisions.

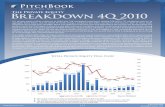

The U.S. private equity industry continues to show signs of shaking o� the credit crisis and economic recession. A strengthening deal �ow, rebounding exit market and rising valuations are all signs that the recovery in the PE industry is gaining steam. During the �rst quarter, over $14 billion was invested through 305 private equity investments in U.S. companies, an increase in deal �ow of 10% from 4Q 2009 and the third straight quarter-over-quarter increase. It is important to note, though, that deal �ow and total invested capital remain below not only the high water mark of 2007 but also 2004 and 2005 levels. The focus for many PE investors remains supporting and growing current portfolio companies as shown by the rise in add-on deals during the quarter, which accounted for 32% of the overall deal �ow. One bright spot during the �rst quarter was the 65 private equity exits, a signi�cant increase from the 31 in 1Q 2009. The continued availability of exit opportunities will be pivotal in 2010 as investors strive to provide limited partners with needed returns and build a platform for future fundraising e�orts.

An important trend that emerged in the �rst quarter and something to monitor closely over the rest of the year was the rise in valuations and deal amounts. The median U.S. private equity buyout during 1Q increased to $47.4 million from $43.7 million in 4Q 2009 and $32 million in 1Q 2009. So far in 2010, the middle market continues to make up the majority of private equity investment, accounting for 85% of the deal �ow during 1Q. Middle-market deal �ow will likely remain robust through 2010, but, as the credit crisis continues to ebb and PE investors put their $400 billion of dry powder to work, look for an increasing number of deals around the $1 billion to $2 billion mark. With the �rst quarter in the books, a number of encouraging trends have emerged for private equity that, should they continue, will mold 2010 into a much better year for the industry than 2009.

The number of deals in 1Q 2010 increased by 10% from 277 in 4Q 2009. This represented the third straight quarterly increase.The capital invested in 1Q 2010 decreased by 22% from $18 billion in 4Q 2009.The deal flow levels seen in 1Q 2010 put this year on pace to finish with over 1,200 deals; a 14% increase over 2009.

Private Equity Breakdown 2Q 2010The PitchBook

Total U.S. Private Equity Deal Flow

Source: PitchBook

[email protected] [ 4 ]

Private Equity: Data | News | Analysis

The PitchBook DifferenceBetter Data. Better decisions.

Percent of PE Transactions(Count) by Deal Size

PE Transactions (Count)by Industry Sector 1Q 2010

Percent of PE Investment (Total $ Amount) by Deal Size

Source: PitchBook

PE Transactions (Count)by Region 1Q 2010

Lower-middle market and growth equity deals under $50 million remained the most popular during the first quarter of 2010 (approximately 50% of deal flow). In a positive sign, the $50 million to $250 million range made significant gains during the quarter, a result of rising valuations and PE firms’ increasing appetites for larger deals.

Source: PitchBookSource: PitchBook

Source: PitchBook Source: PitchBook

Investment activity continued to be fairly dispersed through-out the United States. The Southeast saw a 44% rise in deal flow during 1Q 2010 compared to 4Q 2009 as activity in the Midwest and South slowed. States east of the Mississippi accounted for over half of the deal flow during 1Q with 167 deals.

Business Products & Services (B2B) continues to represent the largest portion of PE deal flow (33%). During 1Q, investors shifted more attention to the Consumer Products and Services (B2C) and Financial Services industries at the expense of the Energy and Information Technology industries. Healthcare and Materials & Resources held steady during the quarter.

In a sign of the increasing availability of debt for PE transac-tions, there were 5 deals, totaling $7.7 billion, above $500 million during the quarter. The mix of deal amounts closely resembles 2005 and will be an interesting figure to monitor as the year progresses.

Source: PitchBook Source: PitchBook

[email protected] [ 5 ]

Private Equity: Data | News | Analysis

The PitchBook Difference

Better Data. Better decisions.

The State of Private Equity Fundraising The fundraising environment remains extremely difficult with only 20 US private equity funds holding final closes during the first quarter, raising a total of only $17 billion, the second smallest amount of capital closed during a quarter in the last five years. The quarter presented a particularly challenging environment for funds $1 billion and above. There were only four such funds during the quarter, well off the pace from 2009 and 2008, which saw 32 and 62 funds respectively closed during the year above $1 billion. Notable fund closings during the quarter include Oaktree Capital Management’s $3.3 billion OCM Principal Opportunities Fund V and The Sterling Group’s $820 million Sterling Group Partners Fund III. The number of open funds remains high at 318, meaning that, if the fundraising market begins to turn around, fund closings could rise dramatically. Although with a $400 billion capital overhang and limited partners still recovering, private equity fundraising looks like it will remain at below-normal levels for the near future. Look for increased momentum near the end of the year as PE firms that have made a few exits and distributed returns to their LPs are able to raise new commitments.

Largest Funds Closed in 1Q 2010

Firm

Alinda Capital Partners

Oaktree Capital Management

Avista Capital Partners

Apollo Investment Management

Prudential Capital Group

The Sterling Group

LBC Credit Partners

Insight Equity

Lovell Minnick Partners

Clearlake Capital Group

4,000

3,300

1,800

1,400

965

820

645

525

455

410

Fund

Alinda Infrastructure Fund II

OCM Principal Opportunities Fund V

Avista Capital Partners II

Apollo European Principal Finance Fund

Prudential Capital Partners III

Sterling Group Partners III

LBC Credit Partners II

Insight Equity Fund II

Lovell Minnick Equity Partners III

Clearlake Capital Partners II

Size ($M)

Source: PitchBook

Fund Count by Fund Size Capital Raised by Fund Size

The number of funds raised in 1Q 2010 increased 24% compared to 17 funds closed 4Q 2009, the second straight quarter increase.Total capital raised in 1Q 2010 declined 72% compared to $61 billion raised in 1Q 2009, and declined 32% compared to $25 billion raised in 4Q 2009.

For only the second time in the last five years, no fund above $5 billion was closed during the quarter.The opportunities private equity investors are finding in the middle market are carrying over to fundraising with middle-market funds accounting for almost half of the funds closed during 1Q 2010.

Funds over $1 billion raised over half of the new PE capital in 1Q 2010.Funds between $250 million and $500 million expanded their share of total funds raised to 45% as limited partners shunned mega funds for middle-market focused funds.

Source: PitchBook

Source: PitchBook Source: PitchBook

Fundraising Activity

[email protected] [ 6 ]

Private Equity: Data | News | Analysis

By Number of Investments

Most Active Private Equity Investors 2Q 2009 - 1Q 2010

Source: PitchBook

The PitchBook DifferenceBetter Data. Better decisions.

2 by number of advisory roles in transactions

Top Investment Banks & Advisors2

Houlihan Lokey Howard & Zukin

Goldman Sachs

Jefferies & Company

JP Morgan

Imperial Capital

Moelis & Company

Lazard Middle Market

Robert W Baird

Morgan Stanley

Citigroup

Lazard

Harris Williams & Co.

3 by number of financings provided

Top Lenders in Private Equity3

Golub Capital

GE Capital

Bank of America

Wells Fargo

CIT Group

Wells Fargo Foothill

Goldman Sachs

SunTrust Banks

Fifth Third Bank

Babson Capital Management

PNC Financial Services Group

Fifth Street Finance

Wachovia Bank

1 by counsel provided on transactions

Top Law Firms in Private Equity1

Jones Day

Kirkland & Ellis

Latham & Watkins

Shearman & Sterling

Sullivan & Cromwell

Paul Weiss Rifkind Wharton & Garrison

Simpson Thacher & Bartlett

Skadden, Arps, Slate, Meagher & Flom

Proskauer Rose

Blank Rome

Weil Gotshal & Manges

Goodwin Procter

Most Active Private Equity Service Providers 2Q 2009 - 1Q 2010By Number of Deals Serviced

H.I.G. CapitalThe Blackstone GroupWarburg PincusParthenon Capital PartnersGTCR Golder RaunerMetalmark CapitalPlatinum EquitySun Capital PartnersAmerican Industrial PartnersGolden Gate CapitalSterling PartnersThe Carlyle GroupThe Riverside CompanyVeronis Suhler StevensonApollo Investment ManagementBlackEagle PartnersGeneral AtlanticOaktree Capital ManagementSummit PartnersBanc of America Capital InvestorsFrancisco PartnersGraham PartnersGridiron CapitalMarlin Equity PartnersMillennium Technology VenturesNavigation Capital PartnersThoma BravoTPG CapitalAdvent InternationalAmerican Securities Capital PartnersAudax GroupBain CapitalClearview CapitalCortec GroupEnCap InvestmentsEnergy Capital PartnersFalcon Investment AdvisorsGreat Point PartnersHellman & FriedmanHuntington CapitalJ.F. Lehman & CompanyLightyear CapitalMilestone PartnersProvidence Equity PartnersRiverside PartnersStone Point CapitalWelsh, Carson, Anderson & StoweWind Point Partners

Deal Count12121110

99998888887777766666666655555555555555555555

Investor Name

Source: PitchBook

[email protected] [ 7 ]

Private Equity: Data | News | Analysis

Your Single Source for Quality Private Equity DataOnly PitchBook tracks the entire private equity lifecycle and every party involved: limited partners, �inancial sponsors & investors, target companies, service providers and key professionals. By dynamically linking these parties, PitchBook makes it easy to identify relationships and networks. Additionally, it actively researches target companies the entire time they are in an investor’s portfolio so you’ll always be up-to-date on the crucial details of a transaction and the company’s progress.

Broadest Private Equity Coverage

The PitchBook Platform contains information on over 25,000 private equity-backed companies, investors, and service providers across every industry segment, every deal size and every private equity deal type from announcement to exit.Deepest Level of DetailPitchBook’s mission is to provide hard-to-�ind information on private equity: the details you can only �ind through direct contact with key players and painstaking background research.

PitchBook researches deal amounts and valuations, target company �inancials and price multiples, capitalization structures, deal terms, investor information and service provider contact information. It also tracks deal stakeholders and participants – not just �inancial sponsors and investors, but also the many other �inancial, legal, and advisory �irms associated with taking a deal through to completion.

Deal monitoring and research through the entire lifecycle. Without exception, PitchBook actively researches and reports on companies from announcement to �inal exit. PitchBook captures the full �inancing story, much more than just a snapshot of the deal’s announcement.Full spectrum coverage. PitchBook covers the full spectrum of private equity deals: all sizes, all industries, and all types.

No shortcuts. It takes meticulous research to produce complete, consistent, timely, and accurate information, and we devote the manpower and resources necessary to make this happen.

What Makes PitchBook Different

The Pitchook Platform Places Powerful Intelligence at Your Fingertips:

The PitchBook DifferenceBetter Data. Better decisions.

Detailed Reports

Sortable Results

Excel Downloads

Customizable Dashboard

Advanced Searches*

*Advanced Searches allow selecting criteria from more than 130 search options

Visit us at www.pitchbook.com

Request a Demo

Come visit the PitchBook table and ask about

special pricing for ACG members

ACG InterGrowth Participants:

“I know exactly who you should call.”

For 100 years…People who know private equity, know BDO.

www.bdo.com/privateequity

© 2010 BDO Seidman, LLP. All rights reserved.

The Private Equity Practice at BDO.

Strategically focused. Remarkably responsive. A century of experience. The multi-disciplinary partners and directors of BDO’s Private Equity Practice provide integrated, value-added assurance, tax and consulting services across the fund cycle; from investment origination, acquisition and closure, ownership support and compliance, to exit.

To speak with a Private Equity Practice leader, please contact: LEE DURAN / 858-431-3410 / [email protected] HENDON / 214-665-0750 / [email protected] KINNEY / 212-885-7485 / [email protected] WOOD / 415-490-3290 / [email protected]

BDO Seidman, LLP, a New York limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms. BDO is the brand name for the BDO network and for each of the BDO Member Firms.

![[PPT]PowerPoint Presentationc.ymcdn.com/.../Dublin_Presentation_1_-_B_M.pptx · Web viewSources: Euromonitor International, IMF, Asia Private Equity Review, EMPEA, EVCA and PitchBook.](https://static.fdocuments.us/doc/165x107/5b2684ad7f8b9a53228b4672/pptpowerpoint-web-viewsources-euromonitor-international-imf-asia-private.jpg)