2nd Quarter Results - Sabesp · 2nd Quarter Results August 2012- Economic - Financial Office and...

21

2nd Quarter Results August 2012- Economic - Financial Office and Investor Relations Office

Transcript of 2nd Quarter Results - Sabesp · 2nd Quarter Results August 2012- Economic - Financial Office and...

2nd Quarter Results

August 2012- Economic - Financial Office and Investor Relations Office

This presentation may contain forward-looking statements referring to

SABESP’s business outlook, operating and financial results estimates, and growth

prospects. These are only projections, and as such, they are exclusively based on

SABESP’s management expectation in relation to the future of business and its

continuous access to capital to finance the Company’s business plan. These

forward-looking statements largely depend on changes in market conditions,

governmental rules, industry performance and the Brazilian economy, among

other factors, in addition to risks exhibited in disclosure documents filed by

SABESP. Therefore, they are subject to changes without prior notice.

Disclaimer

Agenda

Company Overview 1

Our Operations 2

Our Financial Performance 3

Sabesp is one of the largest water and sewage

service providers in the world based on the

number of Customers

Provides water to 24.0 million people and sewage

services to 20.6 million people

Also sells wholesale treated water to 7

municipalities (3.7 million people)

Natural monopoly, low operating risk

Serves the City of São Paulo and 362 out of 645

municipalities in the State

Covers 60% of State's urban population

Operations in the São Paulo Metropolitan Region*

represent 75.1% of our total revenues

(1) As of June 30, 2012

(2) Treated sewage as percentage of collected sewage

São Paulo Regional Systems

Metropolitan Region

One of the largest water and sewage service providers

in the world…

*The Metropolitan Region we consider for this estimate, includes 8

municipalities outside the legal boundaries of the São Paulo

Metropolitan Region and represent the total cities served by the

Company’s Metropolitan Division

4

Main Operational Indicators(1) Company Overview

Water Sewage

Connections (million) 7.5 6.0

Coverage (%) 100 82

Treatment (%) 100 76(²)

Billed Volume (m³ million) 1,035.1 757.1

We are a mixed capital company, majority-owned by the State of São Paulo, with significant private

ownership

State law requires the State of São Paulo to own at least 50% + 1 voting shares at all times

Currently the Government of São Paulo has 50.3% share

Listed on the “Novo Mercado” and NYSE, to the highest corporate governance standards. We are

also part of BM&FBovespa’s Sustainability Index – ISE

100% common shares

Market Cap: R$ 17,543.42 mn (as of June, 2012)

(1) As of June, 2012

…with strong corporate governance

5

Ownership Structure(1)

24.9%

24.8%

50.3%

Agenda

6

3

Our Operations 2

Our Company 1

Our Financial Performance

Diversified customer base

7

Water Volume by Type of Customer Sewage Volume by Type of Customer

Over 80% of water volume comes from

residential, commercial and industrial

customer

Over 90% of sewage volume comes from

residential, commercial and industrial

customer

Residential73%

Commercial8%

Industrial2%

Public3%

Whosale14%

Reused Water<1%

Residential82%

Commercial10%

Industrial3%

Public3%

Whosale2%

Broad coverage of municipalities

8

Nº of

municipalities

% of revenue

Renewed/Secured (Program and Service Contract) 231 69.8

Metropolitan Region Without Contract 28 13.2

Expired/Under Negotiations 66 5.8

To be expired:

Today to 2017 07 1.5

2018 to 2033 31 7.4

Total Retail 363 97.7

Wholesale 7 2.3

Total Sabesp 370 100

Concessions Contracts

30 years services agreement between Sabesp, Municipality of São Paulo and State Government

(expires in 2040)

Investment plan for the Municipality – R$ 16.9 billion for 30 years

Minimum investment of 13% of the Gross Revenues, net of Cofins and Pasep, approximately R$

500 million/year

Transfer of 7.5% of the Gross Revenues, net of Cofins and Pasep to the Municipal Environmental

Sanitation and Infrastructure Fund – to be recovered in tariff

Regulatory agency ARSESP

Agreement and Contract with the Municipality of São Paulo

9

Regulatory Framework

Discussion on Power of Concession

Obligatory creation of a Regulatory Agency Municipal or State level

Clarifies the payment conditions of non-amortized investments up to 4 years

Disbursement of federal funds conditioned to the existence of a sanitation plan Deadline 2014

Basic discussion: sanitation services are of local interest or common interest

Still remains a discussion in the Federal level over the power of concession for sanitation services

in Metropolitan regions Law 11.445/07 does not address this matter

Two Legal proceeding under Supreme Court (STF) appraisal

Federal Law # 11,445/07 Federal Decree 7,217/10

Regulation activities and responsibilities include:

Services quality

Tariff structure and reviews

Planning is a concession holder attribution

ARSESP´s attribution

07% 08%

17%

07% 07%

04%04%

06%

05% 05%

6.87%

5.20%

13%

08%

19%

07%

09%

07%

04%

05%04% 4.05%

6.83%

5.15%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Inflation (IPCA) Tarif Increase

Tariff adjustments

10

Annual Tariffs Adjustments vs. Inflation (%) Sabesp Annual Tariffs Adjustment

Inflation (IPCA)

X

Controllable Costs

Full “Pass-Through”

of Non-Controllable Costs

Includes:

Electricity

Treatment material

Taxes

Use of water resources

Part A Part B

Tariffs revision - Sabesp formula Adjustment established by

ARSESP

New Tariff Methodology

11

BRR0 CAPEX + OPEX + Taxes + ∆ WC

BRRT = BRR0 + ∑(CAPEX+∆ WC-DEP) Volume (M3)

P0 IRR = WACC

18-May-2011 ARSESP disclosed WACC at 8.06%

16-Jan-2012 ARSESP released the Methodology for Sabesp’s Tariff Revision Process

29-Feb-2012 to

14-Mar-2012 Public hearings to discuss the Tariff Revision Process Methodology

30-Aug-2012 Sabesp presents to ARSESP the BRR – Regulatory Remuneration Basis and detailed Business Plan data

ARSESP releases final Tariff Methodology Process

21-Sep-2012 ARSESP sends the Average Tariff Proposal (P0) and Efficiency Gains Factor (X) to Sabesp, and requests Sabesp to

prepare a proposal for the Tariff Structure

01-Oct-2012 Sabesp presents proposal for the Tariff Structure

09-Oct-2012 Disclosure for public hearing of the Average Tariff (P0), Efficiency Gains Factor (X) and Tariff Structure

09-Nov-2012 Public hearing to discuss the Average Tariff (P0), Efficiency Gains Factor (X) and Tariff Structure

30-Nov-2012 Final disclosure of the Average Tariff (P0), Efficiency Gains Factor(X) and Tariff Structure

12

Water Connection Evolution (million) Water Coverage (Connections in ´000s)

Evolution of operations

Sewage Connection Evolution (million) Sewage Coverage (Connections in ´000s)

Collection: From: 82% in 4Q11 to 90% in 2019

Treatment : From: 75.8% in 4Q11 to 95% in 2019

Adding 1.9 million new connections through 2019

Adding 1.2 million new connections through 2019 to

match organic population growth

6.66.8 6.9

7.17.3

7.5 7.6

2006 2007 2008 2009 2010 2011 2Q12

101.0 159.0 161.0 160.0 156.0

635.0

2012 Real 2012 2013 2014 2015 2016 - 2019

5.00 5.200

5.300 5.500

5.700 5.8770

6.00

2006 2007 2008 2009 2010 2011 2Q12

112.0 207.0 212.0 231.0 236.0

996.0

2012 Real 2.012 2.013 2.014 2.015 2016 - 2019

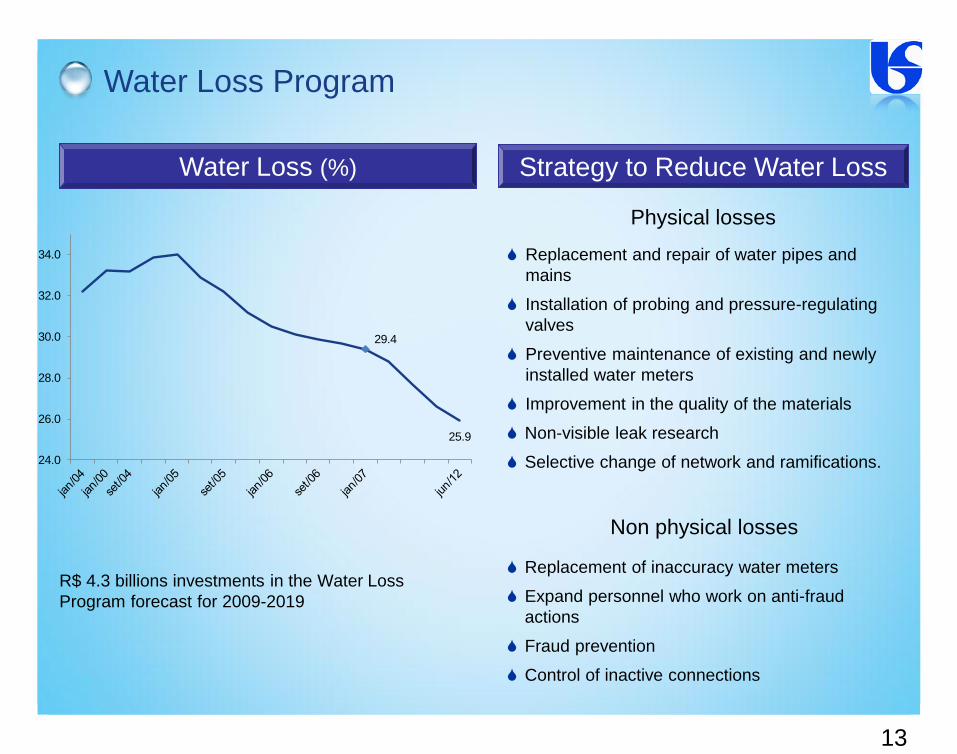

Water Loss Program

13

Replacement and repair of water pipes and

mains

Installation of probing and pressure-regulating

valves

Preventive maintenance of existing and newly

installed water meters

Improvement in the quality of the materials

Non-visible leak research

Selective change of network and ramifications.

Physical losses

Non physical losses

Replacement of inaccuracy water meters

Expand personnel who work on anti-fraud

actions

Fraud prevention

Control of inactive connections

R$ 4.3 billions investments in the Water Loss

Program forecast for 2009-2019

Water Loss (%) Strategy to Reduce Water Loss

29.4

25.9

24.0

26.0

28.0

30.0

32.0

34.0

Capex plan

14

Total Investment Plan of R$ 7.9 billion for 2012 to 2015

Metropolitan Water Program

Tietê Project

Corporate Program for Water Loss Reduction

Clean Wave Program

Coastal Water Program

Main Programs

R$ million

746 599 607 580

927991 846

368

337 395505

988

2,009 1,986 1,958 1,936

2012 2013 2014 2015

Water Suply Sewage collection Collected sewage treatment

1,124

Real.

15

CAIXA R$ 918 mn JICA R$ 716 mn IDB R$ 689 mn BNDES R$ 558 mn IBRD R$ 102 mn

CAIXA

BNDES R$ 607 mn CAIXA R$ 505 mn

Company Funds R$ 3.65 bn

46.3 %

Contracted R$ 2.9 bn

70.4%

Under contracting R$ 144.8 mn

3.4% Under negotiation

R$ 1.1 bn 26.2%

Financing R$ 4.2 bn

53.7 %

Capex financing

2012 to 2015 – R$ 7.9 billion

16

Our Company 1

Our Operations 2

Our Financial Performance 3

Agenda

JICA 12.4%

BID 9.1%

Eurobônus 12.5%

Debêntures 23.1%

BNDES 13.4%

CEF 19.4%

0 0.3%

B Brasil 8.4%

Others 1.3%

17

Long term low, cost funding

R$ million

Total Debt Breakdown Total Debt by Currency

Debt Amortization Profile

(*) Index that measures the variations of the world’s major currencies –

type of international currency (IDB 713 agreement)

Local Currency

66%

US Dollar 18%

Yen 12%

Currency Basket*

04%

0

150

300

450

600

750

900

1,050

1,200

1,350

1,500

1,650

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023+

430

1,244

750 756 773

500601 592

1,031

280 241

1,190

Local Currency

Foregin Currency

18

Net Revenues (R$ million)

EBITDA (R$ million)

Consistent performance

Net Income (R$ million)

2006 2007 2008 2009 2010 2011

Dividend

Declared 9.5* 1.32 1.30 1.73 2.00 2,54

Pay Out % 34.7 28.5 34.3 26.1 27.9 47.3

Dividends/Pay Out

* R$ / 000 shares

5,527 5,971

7,809* 8,580*9,230*

9,927*

5,053*

6,1326,541 7,099

7,703

3,924

2006 2007 2008 2009 2010 2011 2Q12

*Since 2008 calculated in accordance with CPCs / IFRS, w hich includes construction Costs

Net Renevues Net Renevues Without Construction

2,4462,699

2,865* 2,727*

3,222* 3,213*

1,687*44% 45%

37% 32% 35% 32%

33%

47%42% 45%

41% 41%

2006 2007 2008 2009 2010 2011 2Q12

Since 2008 calculated in accordance with CPCs / IFRS, w hich includes construction Costs

EBITDA Margin EBITDA Margin EBITDA Without Constrution

789

1,055863*

1,508* 1,630*

1,223*

785*

2006 2007 2008 2009 2010 2011 2Q12

*Since 2008 calculated in accordance with CPCs / IFRS, which includes construction Costs

19

* EBITDA – LTM

Calculated in accordance with CPCs/IFRS

Capital structure has remained consistent with operating cash generation and

capitalization

Historical leverage metrics

Net Debt vs. EBITDA* (R$ million) Net Debt vs. Shareholders’ Equity (R$ million)

5,2205,787

6,220 6,2816,643

2,865 2,7273,222 3,213

3,470

1.8x

2.1x1.9x

2.0x

1.9x

2008 2009 2010 2011 2Q12

Net Debt EBITDA Net Debt/EBITDA

5,220 5,7876,220 6,281

6,6436,758

8,4399,682

10,54611,043

0.8x 0.7x

0.5x 0.6x 0.5x

2008 2009 2010 2011 2Q12

Net Debt Shareholders' Equity Net Debt/SE

Financial Highlights

20

* In accordance with CPCs / IFRS, which includes construction Costs.

(In R$ million)

** R$ / 000 shares

2002 2003 2004 2005 2006 2007 2008* 2009* 2010* 2011* 2Q12

Net Revenues (R$) 3.767,1 4.130,8 4.397,1 4.953,4 5.527,3 5.970,8 7.809,3 8.579,5 9.230,4 9.927,4 5.052,7

EBITDA (R$) 1.860,0 2.076,5 1.927,0 2.285,6 2.446,1 2.698,9 2.865,1 2.727,3 3.222,5 3.213,4 1.686,7

EBITDA Margin (%) 49,4 50,3 43,8 46,1 44,3 45,2 36,7 31,8 34,9 32,4 33,4

Net Income (R$) (651,0) 833,3 513,1 865,6 789,4 1.055,3 862,9 1.507,7 1.630,4 1.223,4 784,7

Net Margin (%) 20,2 11,7 17,5 14,3 17,7 11,0 17,6 17,7 12,3 15,5

Total Assets (R$) 16.331,9 16.590,1 16.783,8 17.431,1 17.999,9 18.659,9 17.206,0 20.242,9 23.293,1 25.018,6 25.149,8

Total Debt (R$) 7.925,1 7.264,3 7.050,7 6.664,2 6.326,7 5.685,2 6.865,0 6.557,9 8.264,6 7.892,4 8.386,5

Short-term Debt (R$) 1.132,4 997,0 1.496,8 759,0 852,5 742,1 1.449,0 1.009,9 1.242,1 1.629,2 1.323,6

Long-Term Debt (R$) 6.592,6 6.267,3 5.553,8 5.905,2 5.474,2 4.943,1 5.416,0 5.548,0 7.022,5 6.794,1 7.062,9

Foreign Currency Debt (R$) 3.708,0 3.012,7 2.680,9 1.575,9 1.472,2 1.242,3 2.281,0 1.745,6 2.249,9 3.053,4 3.189,1

Shareholders' Equity (R$) 4.217,1 7.576,9 7.951,6 8.482,5 9.018,5 9.780,5 6.758,2 8.438,6 9.681,8 10.545,9 11.042,5

Total Debt/Total Cap. (%) 65,3 48,9 47,0 44,0 41,2 36,8 50,4 43,7 46,1 42,8 43,2

Investments (R$) 619 594 601 678 905 921 1.734 2.059 2.194 2.440 1.124

Dividend Declared (R$/ share) 17,7 5,4 12,2 9,5 1,3 1,3 1,7 2,0 2,5 -

Pay Out (%) 60,5 29,8 40,2 34,7 28,5 34,3 26,1 27,9 47,3 -

Dividend Yield (%) 10,8 3,4 7,8 3,2 3,2 4,7 5,0 4,7 4,9 -

Outstanding shares - 227,836,623

www.sabesp.com.br

IR Contacts

Mario Azevedo de Arruda Sampaio Angela Beatriz Airoldi [email protected] [email protected] (55 11) 3388 8664 (55 11) 3388 8793