23 - 1 Copyright McGraw-Hill/Irwin, 2005 Four Market Models Demand as seen by a Purely Competitive...

56

23 - 1 Copyright McGraw-Hill/Irwin, 2005 Four Market Model s Demand as seen by a Purely Competi tive Seller Short-Run Profit Maximization Marginal Revenue – Marginal Cost A pproach Short-Run Competi tive Equilibrium Long-Run Supply Long-Run Equilibr ium for a Competi tive Firm Pure Competition and Efficiency Key Terms Previo us Slide Next Slid e End End Show Show Pure Competiti on 23 C H A P T E R

-

Upload

jocelyn-stevens -

Category

Documents

-

view

212 -

download

0

Transcript of 23 - 1 Copyright McGraw-Hill/Irwin, 2005 Four Market Models Demand as seen by a Purely Competitive...

23 - 1Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

Pure Competition

23C H A P T E R

23 - 2Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

Market Structure Continuum

FOUR MARKET MODELS

Pure Competition

23 - 3Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

Market Structure Continuum

PureCompetition

FOUR MARKET MODELS

Imperfect Competition

All Markets that areNot Purely Competitive

23 - 4Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

Market Structure Continuum

PureCompetition

FOUR MARKET MODELS

Pure Monopoly

23 - 5Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

Market Structure Continuum

PureCompetition

PureMonopoly

FOUR MARKET MODELS

Monopolistic Competition

23 - 6Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

Market Structure Continuum

PureCompetition

PureMonopoly

MonopolisticCompetition

FOUR MARKET MODELS

Oligopoly

23 - 7Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

Market Structure Continuum

PureCompetition

PureMonopoly

MonopolisticCompetition Oligopoly

FOUR MARKET MODELSPure Competition:• Very Large Numbers• Standardized Product• “Price Takers”• Free Entry and Exit

23 - 8Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

DEMAND AS SEEN BY APURELY COMPETITIVE SELLER

Perfectly Elastic DemandPrice Taker Role

Total RevenueAverage Revenue

Marginal Revenue

For example...

23 - 9Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

$131 0 $ 0

Product Price (P)(Average Revenue)

TotalRevenue (TR)

MarginalRevenue (MR)

QuantityDemanded (Q)

DEMAND AS SEEN BY APURELY COMPETITIVE SELLER

23 - 10Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

$131 131

0 1

$ 0131

$131

Product Price (P)(Average Revenue)

TotalRevenue (TR)

MarginalRevenue (MR)

QuantityDemanded (Q)

DEMAND AS SEEN BY APURELY COMPETITIVE SELLER

]

23 - 11Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

$131 131131

0 1 2

$ 0131262

$131131

Product Price (P)(Average Revenue)

TotalRevenue (TR)

MarginalRevenue (MR)

QuantityDemanded (Q)

DEMAND AS SEEN BY APURELY COMPETITIVE SELLER

]]

23 - 12Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

$131 131131131

0 1 23

$ 0131262393

$131131131

Product Price (P)(Average Revenue)

TotalRevenue (TR)

MarginalRevenue (MR)

QuantityDemanded (Q)

DEMAND AS SEEN BY APURELY COMPETITIVE SELLER

]]]

23 - 13Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

$131 131131131131

0 1 234

$ 0131262393524

$131131131131

Product Price (P)(Average Revenue)

TotalRevenue (TR)

MarginalRevenue (MR)

QuantityDemanded (Q)

DEMAND AS SEEN BY APURELY COMPETITIVE SELLER

]]]]

23 - 14Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

$131 131131131131131131131131131131

0 1 23456789

10

$ 0131262393524655786917

104811791310

$131131131131131131131131131131

Product Price (P)(Average Revenue)

TotalRevenue (TR)

MarginalRevenue (MR)

QuantityDemanded (Q)

DEMAND AS SEEN BY APURELY COMPETITIVE SELLER

]]]]]]]]]]

23 - 15Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

$131 131131131131131131131131131131

0 1 23456789

10

$ 0131262393524655786917

104811791310

$131131131131131131131131131131

Product Price (P)(Average Revenue)

TotalRevenue (TR)

MarginalRevenue (MR)

QuantityDemanded (Q)

DEMAND AS SEEN BY APURELY COMPETITIVE SELLER

]]]]]]]]]]

GraphicallyPresented…

23 - 16Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

DEMAND, MARGINAL REVENUE, AND TOTALREVENUE IN PURE COMPETITION

TR

D = MR

1 2 3 4 5 6 7 8 9 10

1179

1048

917

786

655

524

393

262

131

0

Pri

ce

an

d r

ev

enu

e

Quantity Demanded (sold)

23 - 17Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

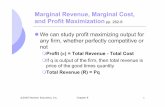

SHORT-RUN PROFIT MAXIMIZATION

Two Approaches...First:Total-Revenue -Total Cost Approach

The Decision Rule:Produce in the short-run if it can realize

1- A profit (or)2- A loss less than its fixed costs

The Decision Process:•Should the firm produce?•What quantity should be produced?•What profit or loss will be realized?

23 - 18Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

SHORT-RUN PROFIT MAXIMIZATION

Two Approaches...First:Total-Revenue -Total Cost Approach

The Decision Rule:Produce in the short-run if it can realize

1- A profit (or)2- A loss less than its fixed costs

The Decision Process:•Should the firm produce?•What quantity should be produced?•What profit or loss will be realized?

AppliedGraphically…

23 - 19Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

TotalCost

0 1 23456789

10

TotalProduct

TotalFixedCost

TotalVariable

CostTotal

Revenue Profit

$ 100 100 100100100100100100100100100

$ 090

170240300370450540650780930

$ 100190270340400470550640750880

1030

Price: $131

- $100- 59

- 8+ 53

+ 124+ 185+ 236+ 277+ 298+ 299+ 280

TOTAL REVENUE-TOTAL COST APPROACH

$ 0131262393524655786917

104811791310

Can you see the

profit maxim

ization?

23 - 20Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

TotalCost

0 1 23456789

10

TotalProduct

TotalFixedCost

TotalVariable

CostTotal

Revenue Profit

$ 100 100 100100100100100100100100100

$ 090

170240300370450540650780930

$ 100190270340400470550640750880

1030

Price: $131

- $100- 59

- 8+ 53

+ 124+ 185+ 236+ 277+ 298+ 299+ 280

TOTAL REVENUE-TOTAL COST APPROACH

$ 0131262393524655786917

104811791310

Graphing Total

Cost & Revenue

23 - 21Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

$1,8001,7001,6001,5001,4001,3001,2001,1001,000 900 800 700 600 500 400 300 200 100 0

To

tal r

eve

nu

e a

nd

to

tal c

ost

TotalRevenue

TotalCost

MaximumEconomic

Profits$299

Break-Even Point(Normal Profit)

Break-Even Point(Normal Profit)

1 2 3 4 5 6 7 8 9 10 11 12 13 14

TOTAL REVENUE-TOTAL COST APPROACH

23 - 22Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

SHORT-RUN PROFIT MAXIMIZATION

Two Approaches...First:Total-Revenue -Total Cost Approach

Three Characteristics of MR=MC Rule:• The rule applies only if producing

is preferred to shutting down• Rule applies to all markets• Rule can be restated P=MC

Second:Marginal-Revenue -Marginal Cost

Approach

MR = MC Rule

23 - 23Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

AverageTotalCost

0 1 23456789

10

TotalProduct

AverageFixedCost

AverageVariable

Cost

Price =MarginalRevenue

TotalEconomicProfit/Loss

$100.00

50.00 33.3325.0020.0016.6714.2912.5011.1110.00

$90.0085.0080.0075.0074.0075.0077.1481.2586.6793.00

$190.00135.00113.33100.00

94.0091.6791.4393.7597.78

103.00

- $100- 59

- 8+ 53

+ 124+ 185+ 236+ 277+ 298+ 299+ 280

MARGINAL REVENUE-MARGINAL COST APPROACH

$ 131131131131131131131131131131

MarginalCost

90807060708090

110130150

Thesame profitmaximizing

result!

23 - 24Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

AverageTotalCost

0 1 23456789

10

TotalProduct

AverageFixedCost

AverageVariable

Cost

Price =MarginalRevenue

TotalEconomicProfit/Loss

$100.00

50.00 33.3325.0020.0016.6714.2912.5011.1110.00

$90.0085.0080.0075.0074.0075.0077.1481.2586.6793.00

$190.00135.00113.33100.00

94.0091.6791.4393.7597.78

103.00

- $100- 59

- 8+ 53

+ 124+ 185+ 236+ 277+ 298+ 299+ 280

MARGINAL REVENUE-MARGINAL COST APPROACH

$ 131131131131131131131131131131

MarginalCost

90807060708090

110130150

Graphically

23 - 25Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

$200

150

100

50

0

Co

st a

nd

Rev

enu

e

1 2 3 4 5 6 7 8 9 10

MC

MR

AVCATC

Economic Profit

$131.00

$97.78

MARGINAL REVENUE-MARGINAL COST APPROACH

Profit Maximization Position

23 - 26Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

$200

150

100

50

0

Co

st a

nd

Rev

enu

e

1 2 3 4 5 6 7 8 9 10

MC

MR

AVCATC

Economic Profit

$131.00

$97.78

MARGINAL REVENUE-MARGINAL COST APPROACH

MR = MCOptimumSolution

Profit Maximization Position

23 - 27Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

the MR=MC rule still applies

If the price is lowered from $131 to $81…

…but the MR = MC point changes.

MARGINAL REVENUE-MARGINAL COST APPROACH

Loss Minimization Position

23 - 28Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

$200

150

100

50

0

Co

st a

nd

Rev

enu

e

1 2 3 4 5 6 7 8 9 10

MC

MRAVCATC

Economic Loss

$81.00$91.67

MARGINAL REVENUE-MARGINAL COST APPROACH

Loss Minimization Position

23 - 29Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

$200

150

100

50

0

Co

st a

nd

Rev

enu

e

1 2 3 4 5 6 7 8 9 10

MC

MR

AVCATC

$71.00

MARGINAL REVENUE-MARGINAL COST APPROACH

Short-Run Shut Down Point

Minimum AVCis the Shut-Down

Point

23 - 30Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

MARGINAL REVENUE-MARGINAL COST APPROACH

Marginal Cost & Short-Run Supply

PriceQuantitySupplied

Maximum Profit (+)Or Minimum Loss (-)

Observe the impact upon profitability as price is changed

$151 131 111 91 81 71 61

10987600

$+480+299

+138 -3

-64 -100 -100

23 - 31Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

Co

st a

nd

Rev

enu

e, (

do

llar

s) MC

MR1

AVC

ATC

MARGINAL REVENUE-MARGINAL COST APPROACH

Quantity Supplied

MR2

MR3

MR4

MR5

P1

P2

P3

P4

P5

Q2 Q3 Q4 Q5

Marginal Cost & Short-Run Supply

Do notProduce –

Below AVC

Break-even(Normal Profit)Point

23 - 32Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

Co

st a

nd

Rev

enu

e, (

do

llar

s)MC

MR1

MARGINAL REVENUE-MARGINAL COST APPROACH

Quantity Supplied

MR2

MR3

MR4

MR5

P1

P2

P3

P4

P5

Q2 Q3 Q4 Q5

Marginal Cost & Short-Run SupplyYields theShort-Run

Supply Curve

Supply

NoProductionBelow AVC

23 - 33Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

MARGINAL REVENUE-MARGINAL COST APPROACH

Marginal Cost & Short-Run Supply

AVC2

MC2

Higher Costs Move theSupply Curve to the LeftC

ost

an

d R

even

ue,

(d

oll

ars)

MC1

AVC1

Quantity Supplied

S1

S2

23 - 34Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

MARGINAL REVENUE-MARGINAL COST APPROACH

Marginal Cost & Short-Run Supply

AVC2

MC2

Lower Costs Movethe Supply Curve

to the Right

Co

st a

nd

Rev

enu

e, (

do

llar

s)MC1

AVC1

Quantity Supplied

S1

S2

23 - 35Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

P

Q

S=MC

AVC

ATC

8

D

P

Q8000

D

S= MCs

IndustryFirm(price taker)

EconomicProfit

$111$111

SHORT-RUN COMPETITIVE EQUILIBRIUM

The Competitive Firm “Takes” itsPrice from the Industry Equilibrium

23 - 36Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

P

Q

S=MC

AVC

ATC

8

D

P

Q8000

D

S= MCs

IndustryFirm(price taker)

EconomicProfit

$111$111

SHORT-RUN COMPETITIVE EQUILIBRIUM

The Competitive Firm “Takes” itsPrice from the Industry Equilibrium

How about thelong-run?

23 - 37Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

PROFIT MAXIMIZATION IN THE LONG RUN

Assumptions...• Entry and Exit Only• Identical Costs• Constant-Cost IndustryGoal of the AnalysisPrice = Minimum ATCLong-Run Equilibrium - TheZero Economic Profit Model

23 - 38Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

Temporary profits and the reestablishmentof long-run equilibrium

S1

MCATC

P

Q100

P

Q100,000

IndustryFirm(price taker)

$60

50

40

$60

50

40

PROFIT MAXIMIZATION IN THE LONG RUN

MR

D1

23 - 39Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

An increase in demand increases profits…

MR

D1

MCATC

P

Q100

P

Q100,000

IndustryFirm(price taker)

$60

50

40

$60

50

40

PROFIT MAXIMIZATION IN THE LONG RUN

D2

EconomicProfits

S1

23 - 40Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

New competitors increase supply, and lowerprices decrease economic profits.

MR

D1

MCATC

P

Q100

P

Q100,000

IndustryFirm(price taker)

$60

50

40

$60

50

40

PROFIT MAXIMIZATION IN THE LONG RUN

D2

Zero EconomicProfits

S1

S2

23 - 41Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

Decreases in demand, losses, and the reestablishment of long-run equilibrium

S1

MCATC

P

Q100

P

Q100,000

IndustryFirm(price taker)

$60

50

40

$60

50

40

PROFIT MAXIMIZATION IN THE LONG RUN

D1

MR

23 - 42Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

A decrease in demand creates losses…

MR

D1

MCATC

P

Q100

P

Q100,000

IndustryFirm(price taker)

$60

50

40

$60

50

40

PROFIT MAXIMIZATION IN THE LONG RUN

D2

EconomicLosses

S1

23 - 43Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

MR

D1

MCATC

P

Q100

P

Q100,000

IndustryFirm(price taker)

$60

50

40

$60

50

40

PROFIT MAXIMIZATION IN THE LONG RUN

D2

Return to ZeroEconomic Profits

S1

S3

Competitors with losses decrease supply, andprices return to zero economic profits.

23 - 44Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

LONG-RUN SUPPLY IN ACONSTANT COST INDUSTRY

Constant Cost Industry

Perfectly Elastic Long-Run Supply

Graphically...

23 - 45Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

P

Q

=$50 S

D1

Z1

Q1

D2

Z2

Q2Q3

D3

Z3

100,000 110,00090,000

LONG-RUN SUPPLY IN ACONSTANT COST INDUSTRY

P1

P2

P3

23 - 46Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

P

Q

=$50 S

D1

Z1

Q1

D2

Z2

Q2Q3

D3

Z3

100,000 110,00090,000

LONG-RUN SUPPLY IN ACONSTANT COST INDUSTRY

P1

P2

P3

How does an increasingcost industry differ?

23 - 47Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

P

Q

$555045

S

D1

Y1

Q1

D2

Y2

Q2Q3

D3

Y3

100,000 110,00090,000

LONG-RUN SUPPLY IN ANINCREASING COST INDUSTRY

P1

P2

P3

23 - 48Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

P

Q

$555045

S

D1

Y1

Q1

D2

Y2

Q2Q3

D3

Y3

100,000 110,00090,000

P1

P2

P3

How does adecreasing costindustry differ?

LONG-RUN SUPPLY IN ANINCREASING COST INDUSTRY

23 - 49Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

P

Q

$555045

S

D1

Y1

Q1

D2

Y2

Q2Q3

D3

Y3

100,000 110,00090,000

P1

P2

P3

What is the long-run competitive

equilibrium?

LONG-RUN SUPPLY IN ANINCREASING COST INDUSTRY

23 - 50Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

P MR

Q

MCATC

Quantity

Pri

ce

Price = MC = Minimum ATC(normal profit)

LONG-RUN EQUILIBRIUM FOR A COMPETITIVE FIRM

23 - 51Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

PURE COMPETITION AND EFFICIENCY

Productive EfficiencyPrice = Minimum ATC

Allocative EfficiencyPrice = MC

UnderallocationPrice > MC

OverallocationPrice < MC

23 - 52Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

PURE COMPETITION AND EFFICIENCY

Productive EfficiencyPrice = Minimum ATC

Allocative EfficiencyPrice = MC

UnderallocationPrice > MC

OverallocationPrice < MC

Resources are

efficiently allocated

under competition

23 - 53Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

PURE COMPETITION AND EFFICIENCY

Productive EfficiencyPrice = Minimum ATC

Allocative EfficiencyPrice = MC

UnderallocationPrice > MC

OverallocationPrice < MC

ConsumerSurplus

23 - 54Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

PURE COMPETITION AND EFFICIENCY

Productive EfficiencyPrice = Minimum ATC

Allocative EfficiencyPrice = MC

UnderallocationPrice > MC

OverallocationPrice < MC

pure competition

pure monopoly

monopolistic competition

oligopoly

imperfect competition

price taker

average revenue

total revenue

marginal revenue

break-even point

MR = MC rule

short-run supply curve

long-run supply curve

constant-cost industry

increasing-cost industry

decreasing-cost industry

productive efficiency

allocative efficiency

ENDBACKCopyright McGraw-Hill/Irwin, Inc. 2005

23 - 56Copyright McGraw-Hill/Irwin, 2005

Four Market Models

Demand as seen by a Purely Competitive Seller

Short-Run Profit Maximization

Marginal Revenue – Marginal Cost Approach

Short-Run Competitive Equilibrium

Long-Run Supply

Long-Run Equilibrium for a Competitive Firm

Pure Competition and Efficiency

Key Terms

PreviousSlide

NextSlide

EndEndShowShow

Coming Next...

Pure Monopoly

Chapter 24