2020 Poll: August 2018 - millwardbrown.com · The Economic Boom doesn’t disguise fears of...

27

2020 Poll: August 2018 for Publication on 19th August 2018 Paul Moran 19 th August 2018 41111511

Transcript of 2020 Poll: August 2018 - millwardbrown.com · The Economic Boom doesn’t disguise fears of...

2020 Poll: August 2018

for Publication on 19th August 2018

Paul Moran

19th August 2018

41111511

2

Introduction

The survey results presented here are derived from The Independent Newspaper Group/

Kantar Millward Brown Consumer Sentiment Poll. The poll was conducted among a sample of

875 adults representative of the approximate 3.57 million adults aged 18 and over - interviewed

on a face-to-face basis in-home at 64 sampling points throughout the Republic of Ireland. The

margin of error for this opinion poll is +/- 3.3%

The 875 interviews on the poll were carried out between 23rd July – 6th August 2018.

The poll was conducted in accordance with the guidelines set by ESOMAR and AIMRO (European and Irish Market and

Opinion Research governing bodies). Extracts from the report may be quoted or published on condition that due

acknowledgement is given to Kantar Millward Brown and The Sunday Independent.

© Kantar Millward Brown & The Sunday Independent 2018.

POLL

3

Introduction

This Kantar Millward Brown

Consumer Sentiment Opinion Poll was

conducted on behalf of The Sunday

Independent to be published on 19th

August and 26th August 2018.

The topics covered in this report include –

Consumer Sentiment, Personal Financial

Circumstances, how we feel about

ourselves,personal spending patterns and

attitudes towards perceived levels of

service and value received in Ireland

today.

Interviews were conducted face-to-face, in-home, with those aged 18+.

Quota controls were set on gender, age, social class and region to

mirror the 18+ population profile.

875 interviews were conducted at 64 sampling points nationwide.

Interviews were carried out between 23rd July – 6th August 2018.

Data was weighted to reflect the adult population aged 18+.

The margin of error for this opinion poll is +/- 3.3%.

The Results

5

The Economic Boom doesn’t disguise fears of Downturn

It is rather apt that today marks the zenith of a fantastic season of the showcase that is hurling. When it ends, we will all feel a little bit

deflated, as we look into the impending autumnal months, not with trepidation, but rather with a sense of looking back to what we

have seen. It is, in some respects, parallel to what we have found in our latest findings in the Sunday Independent/Kantar Millward

Brown Consumer Sentiment Opinion Poll.

As a nation, we appreciate how the economy is going, but we are beginning to have some reservations. We are becoming a little bit

more cautious in our outlook towards the future. This poll also illuminates the stark regional divide between the Haves and the Have

Nots.

First off, the headline figures. Over one in three of us (36pc) feel that we are better off than we were a year ago, compared to one in

five feeling more negatively. No change there so, compared to the last comparable poll in April 2017. Similarly, 35pc of us feel that we

will be better off this time next year. Again, no real change. Of course context is key. When we last asked this question, there was an

exuberance within the psyche of the nation. Now it has stalled, albeit still at impressively positive heights.

However, there is an undercurrent of cautiousness beneath the waves – there seems to be a nagging sense of doubt abound.

There are notable demographic rifts on this small island. Dubliners and younger people are notably more optimistic about the next

twelve months – Metropolitans are hugely more cheerful about their financial heartiness in the year ahead (over half, 52pc feel they

will be better off), with those under the age of 45 also buoyant in their outlook. Bear in mind however, that this poll seeks to

understand a feeling of financial well-being, but not quantify the value of it.

6

The Economic Boom doesn’t disguise fears of Downturn (Cont’d)

Of course, one only has to look around the capital where every available footprint of land now seems to have a crane towering over it

to understand this enthusiasm. Those in Leinster are also relatively positive (three in ten feel the future is bright). Once you step

outside the pale the feeling, whilst positive, is more muted. This regional imbalance will vex rural legislators, but more importantly,

their constituents.

In terms of where do we think we are going, two in three of us feel that the country is going in the right direction (significantly up from

52pc to 66pc), versus just one in five feeling we are on the wrong track (compared to 29pc last year). Again it is Dubliners and those

from the professional classes (ABs) who are most expectant.

In judging the mood of the nation, from a battery of five positive and five negative words, we are generally upbeat – 26pc feel they are

happy, and 23pc feel optimistic. The net effect is that three in four of us express positive sentiments.

So why the doubts? It is instructive to note that the proportion of those who think the economy will improve over the next 12 months

is down significantly from 38pc to 30pc. It could be argued that this is a simply pragmatic vista, and that things can’t continue to rise

forever.

As such, we are not being overly flaithúlach. We feel that we are receiving worse value for money in some sectors of the economy,

notably the hospitality industry (Hotels and restaurants), although service levels are holding up. In light of the ongoing debate over

VAT rates in this sector, it is a timely reminder to all sides of the debate.

We are becoming more prudent in our discretionary spending – Just one in seven (14pc) say they are spending more on smaller

treats, compared to 19pc eighteen months ago. Instead, we are tending to hold the line; over half (52pc) remain unchanged in their

behaviour (up eight points from 44pc).

7

The Economic Boom doesn’t disguise fears of Downturn (Cont’d)

The most pertinent indicator of our financial wariness is when we ask about the future spending intentions. Across the board, the

public is retrenching in terms of their future spending habits. Most are intending not to change their outgoings over the next twelve

months, be it on bigger ticket expenditures such as household renovations, foreign and domestic holidays, or more fleeting/impulse

buys, such as restaurants, confectionary, pubs etc. Similarly, the proportion of those not intending (or able) to invest more in Savings

or Investments has increased sharply.

It paints a picture of a nation what recognises that these are relatively good times, but also are paying heed to the more negative

mood music – Mortgage rates being among the highest in the EU (at a time of record low levels from the ECB), rents at all-time highs,

homelessness and a faltering public service (health service in particular). When economically things turn sour, which they invariably

will at some stage, we seem to have learned some mistakes from the past; we are unwillingly to push the boat out too far.

It seems as if we are trudging along, neither happy or unhappy with our lot, but rather just getting on with it. We appreciate the status

quo, and the relative state of our financial platform, but are unwilling or fearful to over-indulge. It may well also be the case that the

continuing chattering about the rude health of the nation’s economic well-being is an alien place to many; between increased taxation,

and minimal pay rises for some, there is a disconnect.

From a political point of view, this will have implications. If the electorate has doubts in the middle of a “boom”, there is much to

ponder in terms of electoral strategy if things start going south. Between Brexit, Trump and other external shocks, this should weigh

heavily on the mind of all. In essence, as Fine Gael learnt at the last election, the economy is not necessarily a saviour – any

campaign could be fought on different terms; back to the ground hurling as it were.

2020 Poll:The Economy and our Personal

Financial Situation

9

Q. Taking everything into consideration would you say you are personally better off, worse off or in the

same situation as you were THIS TIME LAST YEAR?

Q. This time NEXT YEAR, do you think that you personally will be better off, worse off or in the same

situation as you are now?

Our Personal Financial Situation: Consumer sentiment towards the future remains firmly in positive

territory, although there has been some softening of future optimism compared to last year

Base: All Aged 18+ (875)

( ) = April 2017 Results

36 35

4441

2018

* 5

Comparedto last year

%

This timenext year?

%

Aug2017

(+16) (+17)

*= Better off minus worse off

Aug2019

Better off(36)

Same(43)

Don’t know(2)

Net difference(+16)

Worse off(20)

Worse off(15)

Better off(36)

Same(41)

Don’t know(8)

Net difference(+21)

10

Historical Picture: Personal Situation Compared To This Time Last Year. Trended over time

17

2724

27

11

5 6 710

4 47 6 8 8

12 13 1116 16 16 17 16

23

36 36

49

59 60

46

4329

34 33 3227

3329 31 32

2731

4340 39

48 4853 52 54

43 44

34

15 16

27

46

66

59 6057

68

61 63 6459

64

57

41 43

4035 33

28 30

21

20 20

0

10

20

30

40

50

60

70

80

90

100

Pre CelticTiger '92

Mid CelticTiger '97

Post 9/11'02

Sep '08 Jan '09 Apr '09 Sep '09 Mar '10 Sep '10 Jan '11 Mar '11 Sep '11 Jan '12 Jul'12 Mar '13 Oct '13 Jul '14 Dec '14 July '15 Oct/Nov'15

Feb '16 Jun '16 Oct '16 Feb '17 Apr '17 Aug '18

Better Off Same Worse Off

Compared To Last Year

NET DIFFERENCE -17 +12 +8 +0 -35 -61 -53 -53 -47 -64 -57 -56 -58 -51 -56 -45 -28 -32 -24 -19 -17 -11 -14 +2 +16 +16

Base: All Aged 18+ (875)

Q. This time next year, do you think that you personally will be better off, worse off or in the same

situation as you are now?

11

Historical Picture: Personal Situation This Time Next Year. Trended over time

Q. This time next year, do you think that you personally will be better off, worse off or in the same

situation as you are now?

36

28 2622

2529 29 30

3329 31

26

32

16 1518 17 17

11 13 12 1013

10 1114

17 1815

19 2023 22 20

27

36 35

54

62 6468 68

63 6259 58

6158

63

45

3833 35

44

37

31

39

33 32 34

28 30

36

50

4144

4146

4348 49 49

41 41

10

9 8

8 7 7 9 11 9 10 11 11

23

46

52

41

3440

52

39

50 5247

5954

45

27

33 31 29

2217

22

2314 15

18

0

10

20

30

40

50

60

70

80

90

100

89 90 91 Pre CelticTiger '92

93 94 95 96 Mid CelticTiger '97

98 00 Post 9/11'02

Sept '08 Jan '09 Apr '09 Set '09 Mar '10 Sept '10 Jan '11 Mar '11 Sept '11 Jan '12 Jul'12 Dec'12 Mar '13 Oct '13 Dec '13 Jul '14 Dec '14 July '15 Oct/Nov'15

Feb '16 Jun '16 Oct '16 Feb '17 Apr '17 Aug '18

Better off Same Worse off

THIS TIME NEXT YEAR?

NET DIFFERENCE +26 +19 +18 +14 +18 +22 +20 +19 +24 +19 +20 +15 +9 -30 -37 -23 -17 -23 -41 -26 -38 -42 -34 -49 -43 -31 -10 -15 -16 -10 -2 +6 0 -3 +13 +21 +17

Base: All Aged 18+ (875)

12

Financial Situation vs. Last Year X Demographics: there are clear demographic

differences, showing that the recovery has been an uneven affair

41%

31%

44%

38%

48%

41%

29%

16%

17%

22%

12%

22%

16%

18%

18%

28%

Base: All Aged 18+ (875) Better off

Worse offGender

Male

Female

Age

18-24

25-34

35-44

45-54

55-64

65+

41%

42%

49%

20%

29%

62%

23%

27%

25%

12%

13%

13%

32%

29%

2%

25%

30%

25%

Social Class

AB

C1

C2

DE

F

Region

Dublin

Leinster

Munster

Conn/Ulster

+24

+9

+32

+16

+32

+23

No

Change

-12

+29

+29

+36

-12

No Change

+60

-2

-3

+3

Net Difference

Net Difference

Vs.Aug2017

3918

3321

3523

5216

4715

3618

2626

1524

Apr ‘17

5111

4517

4816

1827

1425

5418

3518

2321

2623

Apr ‘17

13

Financial Situation vs. Next Year X Demographics: over the next twelve months,

certain cohorts in Irish society (Under 45s and Dubliners) expect to benefit more from the buoyant economy

38%

33%

45%

45%

43%

42%

23%

15%

15%

21%

12%

18%

13%

16%

21%

26%

Base: All Aged 18+ (875) Better off

Worse offGender

Male

Female

Age

18-24

25-34

35-44

45-54

55-64

65+

35%

42%

44%

24%

32%

52%

30%

28%

28%

10%

10%

15%

28%

29%

6%

20%

25%

23%

Social Class

AB

C1

C2

DE

FRegion

Dublin

Leinster

Munster

Conn/Ulster

+23

+12

+33

+27

+30

+26

+12

-11

+25

+32

+29

-4

+3

+46

+10

+3

+5

Net Difference

Net Difference

3814

3416

4415

4710

4510

3320

2719

1619

Apr ‘18

488

4313

4613

2121

1416

5517

3613

2113

2420

Apr ‘18

Vs.Aug2019

14Q. Do you think that the present Economic Situation of the country is likely to improve, remain the

same or get worse over the next 12 months

How will the Economic Situation fare over the next twelve months? Three in ten believe the economic

situation will improve more over the next twelve months – significantly down compared to last year, but arguably a more

pragmatic viewpointBase: All Aged 18+ (875)

30%

6%17%

46%

Improve(38%)

Don’t know(6%)

Higher Among %

ABs 46

18-24 36

45-54 year olds 34

Munster 37

Higher Among %

Males 50

35-44 57

C2s 56

Dublin 64

Higher Among %

65+ 28

DEs 27

Farming Community 25

Conn/Ulster 25

Leinster 25

Get worse(19%)

Remainthe same

(37%)

( ) = April 2017 Results

15Q. And do you think that the present economic situation of the country is likely to IMPROVE,

REMAIN THE SAME or GET WORSE over the NEXT 12 MONTHS?

Economic Situation: Negativity towards the future is at a 20 year low

Base: All Aged 18+ (875)

30

46

17

0

20

40

60

80

100

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 2000 2002 Jan '09 Apr '09 Sept '09 Mar '10 Sept '10 Jan '11 Mar '11 Sept '11 Jan '12 Jul'12 Apr '17 Aug '18

Improve Same Get Worse

+33 +6 -12 -27 +4 +10 +19 +14 +33 +10 +1 24 -73 -56 -32 -21 -35 -42 -21 -37 -53 -32 +19 +13Net

Difference

Height ofCeltic Tiger

BankingCrash

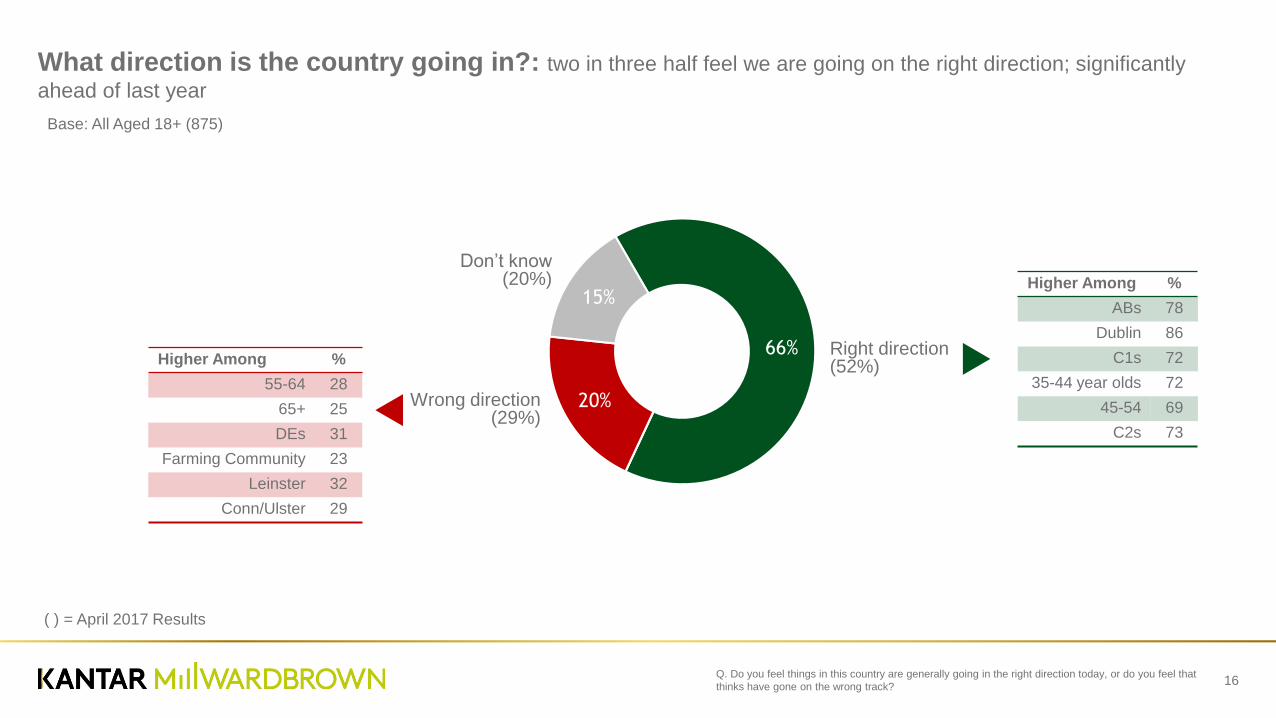

16Q. Do you feel things in this country are generally going in the right direction today, or do you feel that

thinks have gone on the wrong track?

What direction is the country going in?: two in three half feel we are going on the right direction; significantly

ahead of last year

Base: All Aged 18+ (875)

66%

20%

15%

Right direction(52%)

Don’t know(20%) Higher Among %

ABs 78

Dublin 86

C1s 72

35-44 year olds 72

45-54 69

C2s 73

Higher Among %

55-64 28

65+ 25

DEs 31

Farming Community 23

Leinster 32

Conn/Ulster 29

Wrong direction(29%)

( ) = April 2017 Results

17Q. Do you feel things in this country are generally going in the right direction today, or do you feel that

things have gone on the wrong track?

Where do we think the country is going? A focus on how our fears: how times have changed. Just one

in five believe we are on the wrong track – down from a record high of 84%

Base: All Aged 18+ (875)

66% now say that as a country are on the RIGHT TRACK

37%

34%

84%

74%

39%

55%

29%20%

0

20

40

60

80

100

2002 2005 Jan '09 Apr '09 Sept '09 Mar '10 Sept '10 Jan '11 Mar '11 Sept '11 Dec '11 Jul '12 Apr '17 Aug '18

18Q. Which ONE of the following words best describes your own personal mood about living in Ireland

nowadays?

Personal Mood 2018 versus 2017 – we are hugely more positive than were five years ago; over

three in four express upbeat sentiments

26% 23% 8% 10% 9%OptimisticHappy CalmRelaxedCheerful

PessimisticUnhappy AngryAnxiousDepressed

3% 5% 3% 11% 2%

(30%)

(3%)

(20%)

(6%)

(9%)

(4%)

(11%)

(8%)

(7%)

(3%)

25%

Negative

()=April 2017 Results

76%

Positive

(77%)

(24%)

41111511/PM

So where are we going?

A focus on Value for Money

and Perceived Service

Levels Received

21

Which sectors offer better value for money? Retail is generally holding steady, but hospitality continues to slip

back further into the bad old times – consumers feel they are getting less bang for their buck

1117

2931

1019

2522

1523

3335

1932

2931

263728

3137

504844

6343

2121

6042

3034

5034

2322

4329

2729

4234

3733

161012

15

Better value for money

%

Worse value for money

%

The same value for money

%

Grocery Shopping

Clothes Shopping

Alcohol bought to drinkat home/someone else’s home

Alcohol bought inPubs/clubs etc

Hotel Accommodation

Eating out in restaurants

Don’t Know%

16

25

29

32

18

25

30

34

28

34

33

36

35

34

37

36

29

24

28

32

33

27

26

29

Base: All Aged 18+ (875)

Q. In general, in which of these sectors do you think you are getting better or worse

value for money than you did five years ago?

May 2012

Oct 2013

April 2017

August 201810

15

21

16

12

14

15

10

7

9

11

6

4

5

6

4

3

5

7

5

14

14

15

12

22

The level of service experienced: Levels of service are holding relatively steady across most retail and hospitality

sectors

Grocery retail outlets shops

Clothes retail outlets shops

Pubs/clubs

Hotels

Restaurants

Q. And in general, in which of these sectors do you think you are getting better or worse

service than you did five years ago?

8

15

9

11

11

14

9

11

13

17

10

9

12

19

10

8

14

18

9

12

44

33

27

30

38

32

30

32

33

26

36

33

31

26

30

32

21

17

23

26

Better Service%

Worse Service%

The same level of Service

%

Don’t Know%

38

40

49

49

45

47

51

52

52

53

49

56

52

51

54

57

51

53

53

54

Base: All Aged 18+ (875) May 2012

Oct 2013

April 2017

August 201810

12

15

9

6

7

9

5

2

3

5

2

4

3

6

3

14

12

14

9

How our Discretionary

Spending behaviour is

changing

24Q. Which ONE of these statements BEST describes your behaviour regarding the purchase of smaller

treat items such as take-away coffees, lottery tickets, confectionery, magazines, cosmetics etc.?

Discretionary Spending compared to the two years ago – just over half are holding their discretionary

spending steady – one in seven are spending more

Base: All Aged 18+ (875)

Higher Among %

18-24 59

65+ year olds 59

Dublin Residents 57

Farming Community 60

“Which ONE of these statements BEST describes your behaviour regarding the purchase of smaller treat items such as take-away

coffees, lottery tickets, confectionery, magazines, cosmetics etc?”

%

JULY2012

%

APR2017

%

AUG2018

719

14

30

44 52

62

2829

29 5

More

No change

Less

Don’t know

Higher Among %

18-24 year olds 19

25-34 year olds 20

35-44 year olds 18

ABs 24

Leinster Residents 19

Higher Among %

Females 32

55-64 38

DEs 33

Dublin 57

25

Projected Spending over the next twelve months (I): Again there is evidence that many are adopting a

cautious approach to the future, and are consolidating what they have

ForeignHolidays

49

15 14

50

1611

37

12 9

56

19 17

39

14 12

58

19 17

55

20 18

40

5973

40

59 70

49

66 70

36

5968

53

6665

39

6361

39

60 68

7

19

10 5

1714

1216 16

4

1510

5

14 19

2

14 19

3

139

5 6 4 5 7 6 2 5 4 4 7 4 3 6 4 1 5 3 3 6 5

House decorations/renovations

WeeklyGrocery shopping

Clothesshopping

Savings orInvestmentaccounts

Entertainingat home

Weekendbreaks in

Ireland

Q. Over the next 12 months do you think you will reduce, increase or not change the amount you

spend on each of the following?

Base: All aged 18+ (n=875)

Will reduce

Will not change

Will increase

Don’t know

Apr ’17%

Jul ’12%

Apr ’18%

Apr ’17%

Jul ’12%

Apr ’18%

Apr ’17%

Jul ’12%

Apr ’18%

Apr ’17%

Jul ’12%

Apr ’18%

Apr ’17%

Jul ’12%

Apr ’18%

Apr ’17%

Jul ’12%

Apr ’18%

Apr ’17%

Jul ’12%

Apr ’18%

26

Going to restaurants

Mobiletelephone

bills

Impulse purchase of sweets and

soft drinksGoing to

pubs Alcohol

Q. Over the next 12 months do you think you will reduce, increase or not change the amount you

spend on each of the following?

Projected Spending over the next twelve months (II): Impulse purchases also see signs of this cautious approach.

We are not intending to become too flaithúlach

57

21 19

44

15 17

57

32 25

55

24 22

45

2519

39

62 66

52

71 68

39

55 62

39

63 66

47

6470

2

1213

3

9 12

2

169

17 8

24 7

2 6 3 27 3 2 5 4 5 6 4 3 7 5

Will reduce

Will not change

Will increaseDon’t know

Apr ’17%

Jul ’12%

Apr ’18%

Apr ’17%

Jul ’12%

Apr ’18%

Apr ’17%

Jul ’12%

Apr ’18%

Apr ’17%

Jul ’12%

Apr ’18%

Apr ’17%

Jul ’12%

Apr ’18%

Base: All aged 18+ (n=875)

Thank you…

For Further details contact

Kantar Millward Brown | 6 Ely Place, Dublin 2 | T. +353 (1) 297 4500

Paul [email protected]

087 286 0773