2019 MID-YEAR REVIEW AND OUTLOOK · 2019-06-27 · Source: Cox Automotive Industry Analysis, 12m...

41

2019 MID-YEAR REVIEW AND OUTLOOK 1

Transcript of 2019 MID-YEAR REVIEW AND OUTLOOK · 2019-06-27 · Source: Cox Automotive Industry Analysis, 12m...

2019 MID-YEAR REVIEWAND OUTLOOK

1

WELCOME!

2

3

Our Team

Shirley PowellSenior Vice President, Communications & Industry Relations

Chintan TalatiSenior Director, Public Relations

Mark SchirmerDirector, Public Relations

Dara HailesManager, Public Relations

4

Our Team

Marianne JohnsonExecutive Vice President and Chief Product Officer

Mark LuberChief Data Officer

Jonathan SmokeChief Economist

Charlie ChesbroughSenior Economist

Michelle KrebsSenior Industry Analyst

5

OUR VISION

Transform the way the world buys, sells, owns and uses cars

5

OUR PURPOSE

Empower clients to thrive in a rapidly changing marketplace

6

Schedule

10 a.m. – State of the Industry

• Economy – Jonathan Smoke• Market Conditions – Charlie Chesbrough• OEM Performance – Michelle Krebs• Curves Ahead – Jonathan Smoke

Q&A

11 a.m. – The Data Revolution

• Advanced Data & AI – Marianne Johnson

Q&A

Noon – Lunch

STATE OF THE INDUSTRY

7

JONATHAN SMOKE

8

2019 MID-YEAR REVIEWAND OUTLOOKJune 26 // TROY

C H I E F E C O N O M I S T

Overall Economy GDP Growth 1.4%(Q2 NY Fed Nowcast)

3.1% (Q1 ’19) 4.2% (Q2 ’18)

Employment Conditions

U3 UnemploymentRate

3.6%(May)

4.0% (June ’18)

Buyer Confidence UofM Consumer Sentiment

97.9(June Early)

100.0 (May ’19) 98.2 (June ’18)

Wages EarningsGrowth

3.1%(May)

3.2% (April)3.4% (March)

Buyer Ability DisposableIncome Y/Y

3.8% (April ’19)

4.9% (2018)

9Source: IRS

OUR ECONOMY: Under Pressure

Credit Availability NY Fed 1,160(Q1 ’19)

1,128(Q2 ’18)

Interest Rates Target Fed Funds Rate

2.25 -2.50%(June ’19)

1.75 -2.00% (June ’18)

Borrowing Costs Avg Rate 60m Auto Loan

6.33% (May ’19)

5.96% (Dec ’18)6.06% (May ’18)

Ownership Costs Weekly Retail Gasoline Price

$2.74 (June ’19)

$2.89(June ’18)

10Source: IRS

OUR ECONOMY: Under Pressure

CHARLIE CHESBROUGH

11

2019 MID-YEAR REVIEWAND OUTLOOKJune 26 // TROY

S E N I O R E C O N O M I S T

Source: BEA Light Vehicle SAAR, Cox Automotive Industry Analysis 12

16.0

16.2

16.4

16.6

16.8

17.0

17.2

17.4

17.6

17.8

18.0

Jan

-20

18

Feb

-20

18

Mar

-20

18

Ap

r-2

018

May

-20

18

Jun

-20

18

Jul-

20

18

Au

g-2

01

8

Sep

-20

18

Oct

-20

18

No

v-20

18

Dec

-20

18

Jan

-20

19

Feb

-20

19

Mar

-20

19

Ap

r-2

019

May

-20

19

Jun

-20

19

New Light Vehicle Seasonally Adjusted Annualized Rate (Millions)

U.S. SALES SAAR: First-Half Volatility Likely To ContinueReturn to “normal” in June forecasted – but not expected

17.2

Source: Cox Automotive Industry Analysis 13

U.S. NEW-VEHICLE SALES: First Half Down, Second Half More

Month Jun-18 Jun-19 YOY May-19 MOM Change

Sales Millions 1.55 1.51 -2.7% 1.59 -5.0%

Quarter 2018 2019 ChangeSales Millions Q1 4.1 4.0 -3.1%

Q2 4.5 4.4F -1.3%Q3 4.3 4.2F -2.0%Q4 4.4 4.2F -4.0%

Year 17.3 16.8F -2.5%

1st Half 8.6 8.4F -2.2%

Pace of sales decline expected to increase in H2:

Higher vehicle prices, consumer budget

constraints, credit tightening slow purchases

Source: Cox Automotive Industry Analysis 14

U.S. NEW-VEHICLE MARKET: Channels Reveal Weakness

New Market FleetRetail

PurchaseRetail Lease

2018 0.5% 4.3% -0.4% -0.2%

2019F -2.4% 4.0% -3.5% -4.6%

YTD -2.2% 6.9% -5.2% -2.9%

Tax Reform

Vehicle Affordability

Residual Values

Cox Automotive Sales Forecast

2019 = 16.8 million2020 = 16.5 million

Source: Cox Automotive Industry Analysis, 12m average, KBB data 15

Average MSRP approaching $40,000 – affordability issue likely increasing

MARKET PRICING: Higher Prices Off-setting Lower Volumes

$32,711

$39,509

$30,879

$36,950

93.4%

93.6%

93.8%

94.0%

94.2%

94.4%

94.6%

$30,000$31,000$32,000$33,000$34,000$35,000$36,000$37,000$38,000$39,000$40,000

Jan-

2013

Jan-

2014

Jan-

2015

Jan-

2016

Jan-

2017

Jan-

2018

Jan-

2019

Avg MSRP Avg Price Price Strength

Average MSRP and Transaction Price Price Strength

Source: Cox Automotive Industry Analysis, 12m total, KBB data 16

Revenue at post recession peaks, but weakening prices eroding growth

MARKET REVENUE: Annual Pace Near $680 billion, Still Rising

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

$500$520$540$560$580$600$620$640$660$680$700

Jan-

2014

Jan-

2015

Jan-

2016

Jan-

2017

Jan-

2018

Jan-

2019

12m Revenue Revenue Growth

Market Revenue (12m Total, Billion $) Revenue Growth

Source: KBB MSRP data 17

Continued shift to expensive vehicles

MARKET CONDITIONS: Affordability Issues Worsening In 2019

7%

47%

24%

16%

6%

2%

30%

24%

20%

25%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

< $20,000 $20,000-29,999

$30,000-39,999

$40,000-49,999

$50,000+

2012 2013 2014 2015 2016 2017 2018 2019

Source: Cox Automotive Industry Analysis, KBB data 18

Average MSRP up 21% since 2012 but variation significant across vehicle product segments

SEGMENT PRICING: “Largest” Vehicles = Largest Price Increases

-5%

0%

5%

10%

15%

20%

25%

30%

MSRP Change: 2012-2019

Source: Cox Automotive Industry Analysis, IHS and Kelley Blue Book, Dealertrack Data 19

Rising lease payments will lead some potential buyers to used market

MONTHLY PAYMENTS: Differences Drive Consumer Choices

$496

$563

$418

$350

$400

$450

$500

$550

$600

2014 2015 2016 2017 2018 2019

LeaseLoanUsed

$78$67

$145

$20

$40

$60

$80

$100

$120

$140

$160

2014 2015 2016 2017 2018 2019

Lease VS. Used

New Loan VS. Lease

New Loan VS. Used

Monthly Payment Payment Difference

Source: Cox Automotive Industry Analysis, IHS and Kelley Blue Book Data 20

Previous lease and fleet strategies providing growing headwind for new sales

THE POTENTIAL MARKET: New + “Gently Used” = 28 Million Vehicles

33%

34%

35%

36%

37%

38%

39%

40%

41%

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

2012 2013 2014 2015 2016 2017 2018 2019

New Vehicle Deliveries Used MY0-4 Registrations "Gently" Used Share

New and Used MY0-4 Vehicle Market Used Share

Source: Cox Automotive Industry Analysis 21

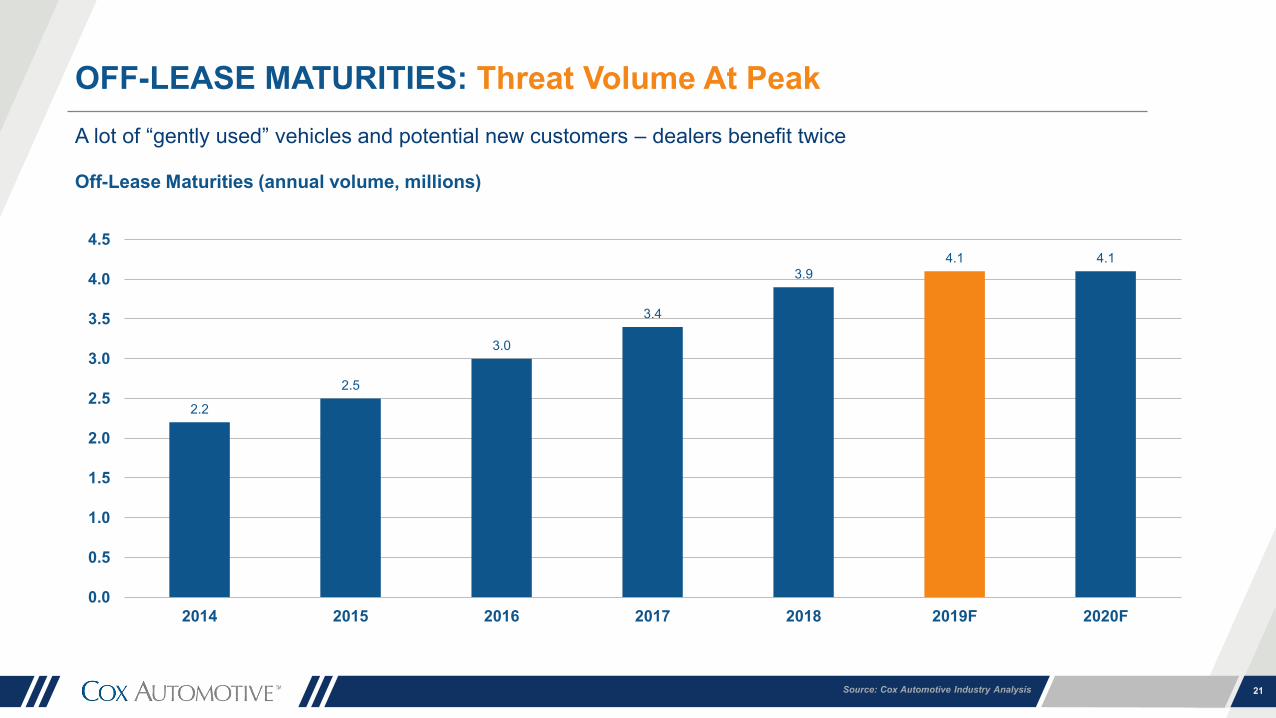

A lot of “gently used” vehicles and potential new customers – dealers benefit twice

OFF-LEASE MATURITIES: Threat Volume At Peak

2.2

2.5

3.0

3.4

3.94.1 4.1

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2014 2015 2016 2017 2018 2019F 2020F

Off-Lease Maturities (annual volume, millions)

Source: Cox Automotive Industry Analysis, IHS Data 22

High demand for off-lease vehicles and supply limitations from recession keep prices elevated

THE USED-VEHICLE MARKET: Decline Due To Supply Constraints

39.4 39.439.2 39.0

35

36

37

38

39

40

2012 2013 2014 2015 2016 2017 2018 2019F 2020F

Used Sales (annual, millions)

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

11,000,000

12,000,000

Jan-

2013

Jan-

2014

Jan-

2015

Jan-

2016

Jan-

2017

Jan-

2018

Jan-

2019

MY 0-4 MY 5-8 MY 9-12 MY 13-16 MY 17+

Total Registrations By Model Year (12m average)

Source: Cox Automotive Industry Analysis, Manheim Auction Data 23

Strong demand for affordable transportation coupled with limited supply causing tight market

AUCTION MARKET: Prices Near Highs, Continued Growth Expected

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan-

1996

Jan-

1999

Jan-

2002

Jan-

2005

Jan-

2008

Jan-

2011

Jan-

2014

Jan-

2017

Manheim Index (annual change)

-6%

-4%

-2%

0%

2%

4%

6%

8%

ALL

CO

MPA

CT

CA

R

FULL

SIZE

CA

R

LUXU

RY

CA

R

MID

SIZE

CA

R

PIC

KU

P

SPO

RTS

CA

R

SUV

VAN

Segment Prices May (annual change)

Source: Cox Automotive Dealer Sentiment Index 24

DEALER SENTIMENT – NEW MARKET: Down From Peak

Good

Poor

57 57

61

65

5960

57

5354

57 57

61

65

5960

57

5354

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019

Overall Franchise Note: Scale 1 - 100

Franchise dealers’ outlook trending lower – reflecting

weaker new-vehicle sales environment

Source: Cox Automotive Dealer Sentiment Index 25

Good

Poor

Note: Scale 1 - 100

5557

5556

5557

5153

56

7068

6769

72 72

6866

72

50

5351

5250

52

4648

51

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019

Overall Franchise Independent

DEALER SENTIMENT – USED MARKET: Rising, Strong Market

Used-vehicle dealers enjoying robust

market – franchise especially from

off-lease opportunity, high demand

MICHELLE KREBS

26

2019 MID-YEAR REVIEWAND OUTLOOKJune 26 // TROY

S E N I O R I N D U S T R Y A N A LY S T

JUNE & FIRST-HALF FORECAST: A Slowing Industry

Monthly Forecast First Half ForecastJune ‘19 June ‘18 YOY% Jan – Jun ‘19 Jan-June ‘18 YOY%

GM 242,000 255,000* -5.2% 1,397,825 1,473,414 -5.1%Ford Motor Co 218,000 229,000* -5.0% 1,230,763 1,271,714 -3.2%Toyota Motor Co 203,000 209,602 -3.1% 1,151,353 1,189,309 -3.2%FCA Group 198,000 202,264 -2.1% 1,088,027 1,115,476 -2.5%American Honda 145,000 146,563 -1.1% 786,094 787,824 -0.2% Nissan NA 133,000 145,096 -8.3% 726,532 780,695 -6.9%Hyundai Kia 125,000 120,623 3.6% 650,289 628,612 3.4%Subaru 62,000 59,841 3.6% 340,014 322,860 5.3%VW 55,000 53,304 3.2% 314,966 310,261 1.5%Grand Total 1,512,000 1,553,200 -2.7% 8,417,457 8,615,260 -2.2%June 2019 Cox Automotive Industry Insights Forecast; all historical data from OEM sales announcementsNote: Total includes brands not shown. GM and Ford monthly sales are estimated

Cox Automotive Forecast: June Auto Sales to Slow Following Surprisingly Strong May

27

Source: Cox Automotive Industry Analysis, KBB data 28

Of Top 5 Volume Segments, three are in decline and full-size pickups are just hanging on

SEGMENT SALES YTD: Cars Continue To Drag Down Market

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Source: Cox Automotive Industry Analysis, KBB data 29

Large brands in decline – Fiat wins the bottom

BRAND SALES YTD: “Value” Imports Showing Growth

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Tesla:Up 70.2%

SEGMENT PERFORMANCE: So What About Electrics?

U.S. Luxury Share: 8.7%Beats Acura, Lincoln and Cadillac Behind Lexus, BMW, Mercedes, Audi

Brand Rep: Gold Standard Top in 7 of 12 factors luxury-vehicle shoppers consider important

Highest Interest: Top-of-mind brand for EV shoppersWithout Telsa, EV shopping would be stagnant on KBB.com

Electric VehicleMarket =

Electric VehicleMarket

< New Cox Automotive EV Study: • Consumers can see the future

Barriers Remain: • Cost of purchase vs ownership• Infrastructure • Skeptical dealers

Tools Needed: • Education & training• Incentives• Marketing

Global Impact:• China & Europe• Investments – 45% in next 5 Years• Battery supply

30

31

U.S. NEW-VEHICLE SALES: What We’re Watching

Nissan – Turmoil at the top. Relied on fleet and incentives during the good times. Now what? And Infiniti has few new products in the coming years.

Tesla – Everyone is watching, always. Every quarter is new adventure, as the bulls and shorts fight it out on Twitter. The real question: Is demand softening?

Ford – Will Ford execute critically-important launches of the high-volume, high-profit Explorer and Escape?

Fiat & Mini – Limited, small-vehicle portfolios and no U.S. production capacity may spell trouble for these brands as the market slows.

European Luxury – There are new bosses at all the luxury houses from Germany. With tariff threats and a push for

electric, will they hold share?

JONATHAN SMOKE

32

2019 MID-YEAR REVIEWAND OUTLOOKJune 26 // TROY

C H I E F E C O N O M I S T

33

FIVE TAKEAWAYS: First Half 2019

THE SEASONOF VOLATILITY

AFFORDABILITY WORSENS

CREDIT CRUNCH

ALL PATHS LEAD TO USED

FLEET – THENEW NORMAL

Lo/Hi— Black Keys

La La Land—Bryce Vine

featuring YG

Easier—5 Seconds of

Summer

Jump—Armin van

Buuren Remix

Don’t Stop Me Now—

First Ladies of Disco

34

Curves Ahead“The first half of the year was marked by volatility. The second half will be worse.”

CURVES AHEAD: Geopolitical Risks / Trade & Tariff

Ratification of USMCA (ITC Report Delivered)

Immigration Related Tariffs on Mexico (for now)

Section 232 Tariff on Imported Autos and Parts / Action on EU and Japan Postponed to Nov. 18

China Trade Deal (March 1; tbd)

EU Trade Deal

Japan Trade Deal

UK Trade Deal Post Brexit?

35

Source: Cox Automotive industry insight 36

CURVES AHEAD: Tariff Exposure

100% 99%

88%

80%

73%

61% 60% 59% 59%

53% 51% 51% 51% 50% 49%

38%34%

32% 31% 30% 29%

15% 14%

1% 0% 0% 0%1%4%

10% 9%

2%

18%14%

26%

51%

62%

54%

21%

70%

5%

59%

99%

79%

100%

0%

20%

40%

60%

80%

100%

Domestic Share Import Share Riskiest Imports

ALFA ROMEO

ASTON MARTIN

AUDI

BENTLEY

FERRARI

FIAT

GENESIS

JAGUAR

LAMBORGHINI

LAND ROVER

LOTUS

MASERATI

MCLAREN

MINI

MITSUBISHI

PORSCHE

ROLLS ROYCE

SMART

37Source: Cox Automotive estimates based on IHS Markit Registrations

0%

5%

10%

15%

20%

25%

30%

35%

COMPACT CAR LUXURY CUV VAN PICKUP MIDSIZE CAR SUV

Composition of New Vehicles Sold Retail in 2018 in the US by Major Segments and Major Regions of Origin

USA MEXICO+CANADA JAPAN SOUTH KOREA EUROPE

CURVES AHEAD: Tariff Exposure

UAW Negotiations

• Contracts Expire Sept. 14, 2019• Issues: Health Care, Plant Closing,

Tiered Job Structure• Likely Target: GM

CURVES AHEAD: Industry Risks

Fuel Economy Standards

• CARB vs. the 50 State Solution• Safer Affordable Fuel-Efficient

(SAFE) Vehicles Rule proposal• MY2021 - 2026

Credit Steve Carmody

38

Copyright @ Free Vector Maps

CURVES AHEAD: Economic / Financial Risk

U.S. Economy China

Slowdown / Showdown

Brexit

39

The Middle East

Q&A

40

2019 MID-YEAR REVIEWAND OUTLOOKJune 26 // TROY

THANK YOU!

FOR MORE NEWS:www.coxautoinc.com/newsroom

TO DOWNLOAD PRESENTATION:www.coxautoinc.com/newsroom/market-insights/ 2019-mid-year-review

53