2018 Market Forecast Report - Danske Maritime · Newbuilding requirements for non-cargo carriers...

64

Newbuilding Requirements 2018-2035 | SEA Market Forecast WG 2018 Market Forecast Report

Transcript of 2018 Market Forecast Report - Danske Maritime · Newbuilding requirements for non-cargo carriers...

Newbuilding Requirements 2018-2035 | SEA Market Forecast WG

2018 Market Forecast Report

3

2018 Market Forecast Report

5

Contents

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Global Economic Situation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Global Energy Consumption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Global Seaborne Trade . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Impact of Environmental Regulations . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Newbuilding Requirements: Cargo Carriers . . . . . . . . . . . . . . . . . . . . . . . 21

a . Containerships . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21b . General Cargo Ships . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24c . Bulk Carriers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27d . Oil & Chemical Tankers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30e . LNG & LPG Carriers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Newbuilding Requirements: Oil & Gas Offshore . . . . . . . . . . . . . . . . . . . . 33

Market Drivers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33The Market Cycle . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33The Effects of Shale Oil . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34Offshore Spending and Activity . . . . . . . . . . . . . . . . . . . . . . . . . . . 34The Offshore Fleet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35The Offshore Shipping Market Outlook . . . . . . . . . . . . . . . . . . . . . . 36

Offshore E&P . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36Construction & Subsea . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37Offshore Supply & Service . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41Newbuilding Requirements: Passenger Ferries . . . . . . . . . . . . . . . . . . . . . . 43

Newbuilding Requirements: Cruise Ships . . . . . . . . . . . . . . . . . . . . . . . . . 45

Newbuilding Requirements: Ro-Ro and Car Carriers . . . . . . . . . . . . . . . . . 47

Newbuilding Requirements: Other Non-Cargo Carrying Vessels (ONCCV) . . . 51

a . Fishing Vessels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51b . Research Vessels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53c . Tugs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55d . Dredgers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56e . The Arctic Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58f . Other Specialised Vessels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

7

Introduction

SEA Market Forecast exists since 1969 . The main task of this group is to conduct market forecasts and deliver regular studies on technical issues such as market forecast, newbuilding requirements, CGT coefficient and shipbuilding capacities aiming at providing best possible guidance for long-term planning . The group represents European shipyards’ and maritime equipment industry at international level and takes part at international forecasting groups .

Forecasting is a difficult business, but when it needs to be done it is good to assemble the best . That is what ISFEM is for . The International Shipbuilding Forecast Expert Meeting is the forum for discussing findings and harmonizing the methodologies to create this report together with our collaborators: SAJ, KOSHIPA and CANSI . Our partnership in this annual endeavor increases our mutual understanding of our industry and its prospect for growth . There is one certainty: reality will end up looking differently than the forecast . The forecast can nevertheless serve to give an idea of the required amount of tonnage in the future and to stimulate serious discussion on future demand for ships .

The developing global macroeconomic outlook on economic growth, production, energy con- sumption (and developing changes to the energy production mix) provide the basis for the fore-casts found inside this report . These values, in turn, inform our expectations for maritime trade volumes in dynamic global shipping routes and patterns . These volumes are further broken down into segments such as major bulk trade, oil and gas cargo, general cargo and minor bulk .

It is important to note that expectations for technological advancement are having increasingly significant impact on the forecasts . The speed of change, the convergence of sciences, advanced robotics on one hand, and on the other machine perception, intelligence and learning are deli-vering capabilities that are seamless, synchronous, and personalized . Before 2035, many ships, systems, and components will be linked to the Internet, making them accessible from any location . Maritime connectivity and semi- or full automation will advance significantly with significant impact on shipping and its supply chain . Increasingly stringent environmental rules driven by societal and policy expectations on shipping to reduce its environmental footprint in the coming years and de-cades are also taken into account as key drivers for fleet replacement investments .

This forecast is reporting on newbuilding requirements, not demand growth . Newbuilding requi-rements reflect the expected growth of the fleet and are forecasted for individual ship type and size . These estimates take into consideration the average age of the fleet-segment and the rate of vessel scrapping .

The figure below illustrates the methodology:

GLOBAL TRADE

trade patterns type of trade sea borne/land etc .

NEWBUILDNG REQUIREMENT

TO 2035

MACRO ECONOMIC

GDP demography production energy mix etc .

FLEET REQUIREMENT TO 2035

Existing fleet size & age deleted ships & replacement regulations etc .

Figure 1. Forecasting Methodology Scheme (Source: SAJ, ISFEM 2016)

Taken together, the forecast shows that newbuilding requirements are on the rise, albeit that the growth rate is relatively low . Drivers for growth include increasing demand for transport and supply-side factors: that newer, smarter, and more efficient equipment, technologies, and training are playing an even more significant role in fleet replacement . Fleet digitalization is offering new horizons of possibilities for the fleet to become more effective, transparent, responsive, and timely in their operations .

Nonetheless, with sustained overcapacity of the global shipbuilding capacity and transport capa-city, these demand prospects for growth are not enough to restore balance to the ongoing health of the overall maritime industry . In 2018, some signs of improvement are visible across several shipping segments . Much has already been done to reduce this capacity, but it still falls short and risks are still high . We applaud those who have already taken steps - you are heroic caretakers of the industry and the future of maritime business .

Jenny N . Braat - Chairwoman

Annika Poitz

Dario Bazargan

Ralph Dazert

Sandra Rand & Gijs Streppel

Elina Vähäheikkilä

Paulino Fernandez

Jesús Algarra Lois

Runar Haddal

Niels-Henrik Møller

9

Executive Summary

The shipping industry is undergoing structural changes affecting almost all segments within the industry and impacting the foreseen newbuilding requirements towards year 2035 . Apart from ongoing technological advancements and increasing regulatory pressure on the industry, the geopolitical situation, slowing pace of overall seaborne trade growth and general global econo-mic uncertainties also affect the forecasts .

Global economic growth is strengthening with data surprisingly on the upside . Global GDP growth is projected to be between 3 .5% and 3 .75% for 2018, which is close to long-run averages .

More robust and higher quality private sector investment, including in intangibles and skills, is key for long-term productivity and real wage growth . There are positive signs indicating that busi-nesses intend to invest and now the global upturn signals demand for investments . But projected investment rates remain low to sustain the acceleration of activity . As a result, the projection for global GDP for 2019 shows a tempering of growth rather than continued strengthening .

The projected growth for 2018 is to be just over 3 .5%, the fastest for seven years, with impro-ved outcomes in both advanced economies and EME . Amongst the advanced economies, policy easing is helping growth to remain stronger than anticipated . Strong infrastructure investments in China in 2016 and 2017 are the key drivers for the upturn in the EME’s, boosting external demand elsewhere and contributing to the recovery in many commodity-exporting economies .

Commodity prices have risen, partly due to industrial demand, geopolitical risk and supply con-straints . The oil prices remain below the peaks seen in 2010-11 .

Most major shipping segments are still challenged by overcapacity issues but there are signs of improvements in some segments after the record low order intake level reached in 2016 . Looking further, however, provides confidence in the industry . Despite the above mentioned structural chan-ges, being a very volatile industry, shipping has historically followed long cycles . Hence, the perspectives for sea borne trade growth, the ocean economy and maritime business potential in general are good and indisputable .

Looking at the individual segments, containership market conditions have improved in 2017, fol-lowing a severely pressurized market environment in 2016 . Overall more positive demand trends, combined with continued moderate supply growth, have helped to start to re-balance the contai-nership sector . The containership segment is forecasted to grow firmly in the medium and long term towards 2035 driven by GDP growth . While challenges and risks remain, the bulk carrier market is also starting to move on a more positive trajectory, after having picked up pace this year . Our projection to 2035 shows that due to persisting overcapacity, oil tankers’ and LNG tankers’ fleet will grow less than oil and LNG seaborne trade .

With regard to the offshore segment there is, all in all, much more optimism in 2018 than in 2017 as key drivers show a more positive development . Investors in today’s $60-70 world are now viewing situation and outlook more positively . The market will be back, but most likely not to the heights we have seen the last decade . Market development from here may be slowly upwards, but “the deeper the downturn, the sharper the rebound” is often the case (ref . to section about the market cyclein the offshore chapter ) .

Despite a fairly mature passenger ferry market and slowing growth in passenger volumes in key markets, overall moderate demand growth is expected in the medium to long term . The cruise vessel segment has experienced tremendous growth the past years and judging from the order-books the level of growth will remain in the short to medium term . However, in the long term the newbuilding requirements will be linked to trends in international tourism, economic growth, and population growth .

Newbuilding requirements for non-cargo carriers such as fishing vessels, research vessels, tugs, dredgers and other specialized vessels are mixed . Due to an ageing fleet of fishing vessels a high level of scrapping is expected . This in turn will lead to an expected rise in newbuilding deliveries but still lower than the number of vessels scrapped resulting in a further drop of the fleet size . Despite low levels of exploration activities leading to low vessel utilization, low day rates and an increasing number of laid up vessels, recovery of exploration activities and fleet renewal are expected to restart investments in seismic research vessels . However, it remains to be seen whether the contracting levels of the past will be reached again . A similar development is expected in newbuilding requirements for oceanographic research vessels . While mature Western economies suffer from budget constraints, they still need to replace their ageing fleet . This is often achieved by replacing existing vessels with fewer but larger and more versatile vessels . Meanwhile, emer-ging economies are increasing spending on their oceanographic research fleets in their quest for energy sources and other raw materials . Taken together, these developments lead to a generally higher newbuilding requirement towards 2035 .

Compared to previous forecasts, the slowing of world seaborne trade growth, a lower level of scrapping and a generally restrained spending is expected to result in a reduced yet still increa-sing new building requirement for both tugs and dredgers . As the arctic areas of the world are opening the existing fleet of ships suited for the Arctic is exposed as ageing and insufficient . This development has spurred demand for icebreakers and ice-strengthened tonnage capable of Arctic operations in the medium to long term . The requirement for ships in the other special vessels category is expected to grow slightly below the projected annual growth rate of world seaborne trade resulting in a relatively unchanged fleet size with the potential for a gradual rise in deliveries towards 2035 .

0

10

20

30

40

50

60

Total Real deliveries Projected SEA Europe Average deliveries

Newbuilding Requirements - Actual + Forecast (in mill. CGT)

Newbuilding requirements 2018-2035. Source: SEA Europe Working Group (WG) on Market Forecast (MF), 2018

11

Global Economic Situation

Global economic growth is strengthening with data surprisingly on the upside . Global GDP growth is projected to be between 3 .5% and 3 .75% for 2018, which is close to long-run averages .

More robust and higher quality private sector investment, including in intangibles and skills, is key for long-term productivity and real wage growth . There are positive signs indicating that busi-nesses intend to invest and now the global upturn signals demand for investments . But projected investment rates remain low to sustain the acceleration of activity . As a result, the projection for global GDP for 2019 shows a tempering of growth rather than continued strengthening .

The projected growth for 2018 is to be just over 3 .5%, the fastest for seven years, with improved outcomes in both advanced economies and emerging economies (EME) . Amongst the advanced economies, policy easing is helping growth to remain stronger than anticipated . Strong infra-structure investments in China in 2016 and 2017 are the key drivers for the upturn in the EME’s, boosting external demand elsewhere and contributing to the recovery in many commodity-expor-ting economies .

Commodity prices have risen, partly due to industrial demand, geopolitical risk and supply con-straints . The oil prices remain below the peaks seen in 2010-11 .

-6,00%

-4,00%

-2,00%

0,00%

2,00%

4,00%

6,00%

8,00%

10,00%

1980

-198

9

1990

-199

9

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2017

-202

0

2021

-25

2026

-30

2030

-35

Total OECD Developing Countries Total World

GDP Growth 1980 - 2035

Source: SEA Europe WG MF 2018

Looking further ahead the world economics will change . PwC project that the world economy could more than double in size by 2050, assuming broadly growth-friendly policies (including no sustained long-term retreat into protectionism) and no major global civilization-threatening cata-strophes .

Emerging markets will continue to be the growth engine of the global economy . By 2050, the E7 economies could have increased their share of world GDP from around 35% to almost 50% . China could be the largest economy in the world, accounting for around 20% of world GDP in 2050, with India in second place and Indonesia in fourth place (based on GDP at PPPs) . These econo-mies are rapidly evolving and often relatively volatile however, so companies will need dynamic and flexible operating strategies to succeed in them . Businesses should be prepared to adjust their brand and market positions to suit differing and often more nuanced local preferences . An in-depth understanding of the local market and consumers will be crucial, which will often involve working with local partners .

Despite the above mentioned structural changes, being a very volatile industry, shipping has historically followed long cycles . Hence, the perspectives for sea borne trade growth, the ocean economy and maritime business potential in general are good and indisputable . Apart from in-creasing new-building requirements, albeit with lower growth rates than historically, SEA Europe foresees a promising potential within conversions and retrofitting of the at any time existing fleet in a quest to comply with the even tighter regulatory requirements and ensure increasing operational efficiency .

13

Global Energy Consumption

The world population is increasing, and more than one billion people are without access to electricity today . In 2040 the number is expected to be reduced to around 500 million . The world economy is projected to almost double over the next 20 years and rise in prosperity, particularly in fast-growing developing economies, drives a strong increase in energy demand even if this growth is substantially offset by rapid gains in energy efficiency .

In BP’s main scenario, global energy demand grows by around a third by 2040 – a significantly slower rate of growth than in the previous 25 years - with the industrial sector accounting for around half of the overall increase . Growth in transport demand is much slower than in the past, reflecting faster gains in energy efficiency .

Rapid deployment and falling costs of clean energy technologies, growing electrification of ener-gy, cleaner energy mix in China, and resilience of shale gas and tight oil in the United States are expected be the main large-scale shifts in the global energy system, according to IEA .

Multilateral and international energy agencies forecast that all of the growth in energy demand will come from fast-growing developing economies, driven by increasing prosperity . China, India and other emerging Asia account for around two-thirds of the growth in energy consumption while Energy demand within the OECD is flat . Africa also plays an increasingly important role in dri-ving energy demand in the long term supported by an increasing population together with some pick-up in productivity .

0

5

10

15

20 OtherAfricaOther AsiaIndiaChinaOECD

0

5

10

15

20 RenewablesHydroNuclearCoalGasOil

Primary energy demand

Region Fuel

Source: BP Statistical Review 2018

Renewable energy is the fastest growing energy source (7% p .a .), accounting for half of the in- crease in power and its share is set to reach around a quarter of total power generation by 2040 . Coal is set to remain the largest source of energy for power in 2040 but its share is forecasted to account for just 13% of the increase (compared with more than 40% over the previous 25 years) .

The transport sector continues to be dominated by oil, despite increasing penetration of alternative fuels, particularly natural gas and electricity . In the BP Scenario, oil demand accounts for around 85% of total transport fuel demand in 2040, down from 94% currently . Natural gas, electricity and a mix of ‘other’ types of fuels are each projected to account for around 5% of transport fuel by 2040 . Hence, the transition towards a lower carbon fuel mix is set to continue .

15

Global Seaborne Trade

The low transport cost of shipping compared to other means of transport is the reason that about 90% of global goods transport is by sea . Improvement in port infrastructure and logistic chains and the new generation of energy efficient vessels are meant to benefit seaborne trade and maintain the leadership in international freight transport .

Since the downturn of 2009, when it slumped by 4%, world seaborne trade has grown by 38% . While seaborne trade appears to have settled on a lower growth path since 2011, it is still growing nevertheless and in fact recorded a rebound in growth in 2017 . Crude oil and oil products account for 27% of the total, dry bulk for 44% and containers for 16% . For 2018, the indicators are also po-sitive, the world economy being projected to almost double over the next 20 years, which means that additional seaborne transport capacity will be required . However, several factors may affect the outlook of seaborne trade growth in the longer term . While world economy and trade develop-ments continue to be key drivers in the evolution of seaborne trade, the relationship between eco-nomic output and trade of goods has been shifting over the recent years, the trade to GDP growth ratio being expected to remain at 1 .4 in 2018 . Hence forecasting solely based on GDP evolution and merchandise trade may no longer be sufficient as several factors come into play in connection to seaborne trade patterns’ (re) definition and evolution . These notably include infrastructure de-velopment projects such as the Belt and Road initiative (China), geopolitical developments, and potential escalation of trade restrictive policies affecting business confidence and investment de-cisions . Protectionist tendencies in several major world economies may have the potential to limit world trade growth and hence seaborne trade recovery in the coming years .

World seaborne trade volumes are forecasted to expand across all segments, with containerized trade and major dry bulk commodities trade witnessing the fastest growth . Dry bulk trade is fore-casted to continue growing in the long term following a 4% volume expansion in 2017 (in contrast to an average growth of just 0 .8% p .a . in 2015-16) to reach 6,367 million tons in 2035 . Positive drivers for continued expansion in the short-term include rising South East Asian coal imports, growing demand for high-quality foreign iron ore in China and the positive impact of improving global economic growth on minor bulk trade . Containerised trade is also expected to continue growing to reach approximately 3,600 mln tons in 2035, driven mainly by rising intra-Asian trade volumes and improved East–West main lanes flows . Seaborne crude and oil products trade is fore-casted to continue to grow, supported to large extent by increasing energy demand coming from emerging economies and growth in Middle Eastern and US exports driven, albeit at a steadily decreasing pace .

Total oil cargo

Total five major bulk

Minor bulk

General cargo

ContainerisedLPG

LNG

Global Seaborne Trade

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

5.000

1990 1995 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2020 2025 2030 2035

million tonnes

Global Seaborne Trade forecast 2035 (mln tons). Source: SEA Europe WG MF, 2018

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

1970

1975

1980

1985

1990

1995

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2020

2025

2030

2035

Total trade in mln TONS

Total trade in mln TONS

Total trade in mln tons. Source: SEA Europe WG MF, 2018

17

Impact of Environmental Regulations

The impact of the recent and future waves of more stringent environmental regulations at global and regional level is an increasingly fundamental factor to consider when forecasting how the fleet will look like in the coming decades . Hence, the increasing, and probably overdue, environmental pressure on shipping and its potential impact on e .g . fleet replacement vs retrofitting needs or tonne-miles capacity in the bulker or container segments (resulting from slow steaming) has been incorporated in the newbuilding requirement forecasts of this report .

Shipping has come under serious pressure over the last decades due to its environmental impact: ships generate emissions of sulphur oxides (SOx), oxides of nitrogen (NOx), particulate matters (PM) and carbon dioxide (CO2) . These substances are a result of the current fuel used to power ships and especially in areas with heavy marine traffic ship generated emissions can be significant and have a negative impact on the population’s health . Moreover, the introduction of invasive ma-rine species into new environments by ships’ ballast water or attached to ships’ hulls and via other vectors has been identified as one of the greatest threats to the world’s oceans .

As a result, international and regional rules on fuel oil maximum sulphur content as loaded, bunke-red and subsequently used on board were introduced for Sulphur Emission Control Areas (SECA) and outside them with a stepwise increase in the sulphur content restrictions . The enforcement of a 0 .5% global sulphur cap on all marine bunkers from January 1, 2020 in particular is expected to be an important game changer . Similarly, NOx emission reduction regulation enforced from 2016 onwards requires newly built ships to meet the 80% Tier III criteria when operating in a NOx Emis-sion Control Area (NECA) . Increasingly stricter regulation of emissions and widening of respective control areas is expected to continue .

Shipping’s greenhouse gas (GHG) emissions and the associated climate impact were subject to intense debate within the International Maritime Organisation (IMO) . Although global regulation on mandatory energy efficiency standards in shipping was introduced in 2013, various studies projected shipping’s GHG emissions to grow if additional measures are not taken . For example, the official IMO GHG study foresees an increase of shipping’s GHG emissions of 50-250% by 2050 .

Range of exptected increase in GHG emissions from shippingMt CO2

3000

2500

2000

1500

1000

500

01990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Source: Third IMO GHG Study (2014) Transport & Environment

In April 2018, the IMO adopted an initial strategy aimed at reducing the total annual GHG emis-sions by at least 50% by 2050 compared to the 2008 level of emissions . Such decision is a key starting point towards the adoption of a revised – and hopefully more ambitious – IMO strategy in 2023 .

Finally, the IMO Ballast Water Management Convention (BMW), adopted in 2014 to prevent the spread of harmful aquatic organisms from one region to the other through the release of ships’ ballast water, entered into force on 8 September 2017 . The Convention prescribes that ships must adhere to certain discharge standards through the use of a ballast water system before the dead- line of 8 September 2024 .

Over the past recent years, the European Maritime Technology sector has helped the shipping industry with developing several technological and operational measures to enhance the sector’s environmental performance . Examples are modifications to ships’ design, development of onboard software dedicated tools to enhance energy efficiency, EEDI, alternative hull paints, conversion to alternative fuels like LNG etc . In 2018 EU shipyards and maritime technology producers are world leaders in LNG fuelled ships and alternative fuel engines and systems with a total aggregated portfolio in excess of € 15 Billion . Despite these positive developments it goes without saying that more efforts will be required to ensure that shipping really becomes environmental neutral by 2030 or 2050 .

While a rush in newbuilding activity in the short term is not to be expected in view of the upco-ming environmental regulations, there seems to be increasing speculation from various investors in Asian countries that hundreds of tankers and bulk carriers will be “removed” from the fleet by 2020 because they will become unprofitable as a result of the switch to low-sulphur fuel and associated rising costs . This would create a replacement demand for those vessels which would in turn trigger newbuild orders . For the time being, it can be observed that the increase in newbuild orders is reasonably steady but not at a high pace . IMO’s planned 50% GHG emission reduction targets may have however positive implications in the longer run for the newbuilding markets, quickening the pace of ship obsolesce and encouraging scrapping of old tonnage .

In the short term the biggest technical “disruption” will be assumably the 2020 0 .5 global sulphur cap enforcement . In the main merchant shipping segments shipowners are waiting to see what will happen in 2020, notably in relation to compliant fuel availability but it is expected that most of them will initially use fuel with low sulphur content . Given that the estimated extra cost will be about 400 dollars per fuel ton, shipowners are expected to employ slow steaming, reducing the speed by a few knots to compensate the higher fuel costs .

Installations and use of Exhaust Gas Cleaning Systems (commonly known under the name of “Scrubbers”) in combination with conventional engines running on heavy fuel oil (HFO) will conti-nue over approximately the next ten years but there is increasing awareness about the “transitio-nal” nature of such solution . Moreover, the use of open loop scrubbers in sensitive environmental areas or in ports may become limited if waste water discharge regulations become stricter .

Albeit still marginal in comparison to the total fleet size, the uptake of LNG-fuelled vessels is growing . There are currently 118 LNG fuelled vessels globally, excluding LNG carriers and inland waterway vessels, of which more than two-thirds are operating in Europe . A confirmed order book of 111 vessels will see that figure double . In addition, there are 114 vessels that are classified as LNG-ready . There is an increase in government-backed initiatives such as in Japan, Korea and China to develop LNG bunkering infrastructure as part of their commercial strategies and GHG reduction targets (DNV GL, 2017) . A quicker uptake of LNG as a fuel for shipping is thus clearly visible, also beyond short-sea ships operating in areas with developed gas bunkering infrastructu-re . As major pioneer and driver for LNG propulsion the cruise industry has stepped up ordering of clean vessels . The new orders for large LNG fuelled cruise ships already represent a quarter of all cruise tonnage on order . The multi-billion dollar investments are triggering LNG infrastructure particular in cruise destination ports . With bunkering infrastructure developing around the world, the concept is becoming increasingly appealing also to container lines, with several now giving serious consideration to LNG for their newbuild fleets as well . Lloyd’s Register Marine and the UCL Energy Institute expect that around 30% of all tankers will be fuelled by LNG by 2030 .

19

LNG might see a growing uptake in the short and medium term as part of industry efforts to miti-gate CO2 emissions, in particular if LNG becomes cheaper than low-sulphur fuels . LNG fuelling is projected to account for almost 200,000 barrels of oil equivalent per day of global bunker demand in 2020 but could take until the 2040s to overtake oil-based fuels (Alphatanker analyst 2018) . Whereas LNG is currently the most promising alternative, it remains a carbon fuel and it contributes to GHG emissions also in terms of methane slip . Therefore, in the long-run the decarbo-nisation objective will require zero-GHG fuels such as renewable gases or liquids e .g . methanol . Already today, first commercial vessels operate on methanol while others gather experience with the use of fuel cells .

It is likely that what will be needed to meet future emission targets will be an intelligent mosaic of various cleaner energy sources and integrated solutions . A large number of future new-builds will be equipped with multi-fuel engines to allow for a smooth transition of main fuels, while ultra-low or zero emissions will be achieved by electric propulsion in special areas, such as ports or ECAs . Several locally operating vessels will become fully electric (small, full electric ferries are already available on the market) as large high-density battery systems will become available driving stronger market uptake, while other vessels will have hybrid propulsion systems . Ships will become wind-assisted and batteries for non-propulsion workload will be recharged by solar energy .

With regard to ballast water, to date more than 60 ballast water treatment systems have been given type approval . European maritime technology industry has up until now developed approxi-mately 70% of total ballast water system, which is a market worth around 34 billion EUR . Uptakes across mainstream shipping segments was for the moment quite limited owing to the delayed ap-plication of the new rules, but the convention deadline of 8 September 2024 is expected to lead to an acceleration in demand and supply on the market for ballast water systems in the coming years and stimulate retrofitting activity .

To conclude, the recent and future wave of increasingly stringent rules will have not only an impact on the environmental performance of the shipping sector . They will also contribute to technology developments and growth in shipbuilding, repair and marine equipment industry by creating po-tentially new business opportunities . To meet global environmental targets as well as the internatio-nal regulations, current technologies will have to undergo major modifications and new innovative solutions will have to be established . Initiatives and standards will increasingly take into account the whole life-cycle of a ship, from raw materials used in shipbuilding to final dismantling . Growing public expectations related to environmental protection will result in more non-governmental and industry-led initiatives with new and additional voluntary standards . The shipbuilding and marine equipment industries are hence expected to play a large role in mitigating adverse impacts of ship-ping and allow the sector to respond to policy and societal requests to enhance its environmental sustainability .

21

Newbuilding Requirements: Cargo carriers

a. Container Ships

Containerisation has played a crucial role in the development of global trade . It greatly reduced the cost of international trade and increased its speed, especially of consumer goods and com-modities . Standardised containers made it possible to ship increasing volumes of goods around the globe in a cost-effective way . The constant growing of containerisation’s significance reflects the changes that have occurred over time in the international system set-up of manufacturing and production . Approximately 90% of non-bulk cargo worldwide is moved by containers stacked on transport ships .

Containership market conditions have improved in 2017, following a severely pressurized market environment in 2016 . In the freight market, rates appeared to have bottomed out in 2016 on both mainlane and non-mainlane routes . Whilst rates on most trade lanes have remained volatile, and on some have lost some ground since the start of 2017, they remain considerably above the historically depressed levels seen in early 2016 . This improvement was supported by more positive fundamentals as well as strong demand by liner companies for tonnage ahead of the launch of the new alliance services structures . Subsequently, charter rates have generally moved sideways or gradually upward, although there has been variation across the size sectors . Overall more positive demand trends, combined with continued moderate supply growth, have helped to start to re-balance the containership sector . Meanwhile, second-hand boxships prices have also recorded gains in 2017, away from the historically low levels of end 2016 .

Demand

Following growth of 3 .8% in 2016, container trade expansion has accelerated further in 2017, with volumes close to 200m TEU and growth reaching 5% . The healthy performance of box trade in 2017 has received broad support across the trade lane spectrum, including strongly positive growth on the Transpacific trade and a continued return to robust levels of growth on intra-Asian trades . North-South volumes have improved beyond initial expectations, buoyed partly by a gra-dual increase in commodity prices .

For the full year of 2017, data provider CTS (Container Trades Statistics Ltd .) counted 40 .9m TEU being transported between different Asian ports (+4 .3% Y/Y) . On the most important long-haul tra-des, CTS counted 18 .5m TEU going from the Far East into North America (+7 .3% Y/Y) and 15 .8m TEU on the routes from the Far East into Europe (+3 .7% Y/Y) .

Demand also grew on the Far East to Sub-Saharan Africa trades (+5 .9% for the full year of 2017) . Another “lower volume trade” that grew strongly in 2017 was the Far East to South and Central America trade lanes, shipping 3 .6m TEU during 2017, up by 10 .7% on last year . 2017 was hence marked by strong improvement signals . However, there was still some concern over the large amount of new capacity due to enter the market in 2018 .

Supply

In full year 2017, boxship fleet capacity grew 3 .7% to 20 .8m TEU (across 5,063 ships), following 1 .2% expansion in full year 2016 . Deliveries, though up on 2016, remain down on 2015 s record levels, with 1 .2m TEU for full year 2017 and the rate of “non-delivery” of the start year order-book at around 38% . Demolition reached a record 0 .65m TEU in 2016, and although unlikely to hit that level again this year, remains elevated, with 0 .4m TEU sold for recycling in 2017, including 57 old Panamax´ units . The average age of demolition in 2017 stands at 21 years . With regard to contracting activity, 112 units of 0 .6 m TEU were ordered . At the end of December, the orderbook totalled 398 ships of 2 .8m TEU of which 235 are of feeder type under 3,000 TEU, 68 are ULCS of

12,000 TEU and more, and the rest are between 3,000 TEU and 12,000 TEU, representing 13% of the fleet . The figure shows the CGT per vessel, that has been increasing in recent years .

20.000

25.000

30.000

35.000

40.000

2003

2004

20

05

2006

2007

2008

2009

2010

20

11

2012

20

13

2014

20

15

2016

2017

Reeks1 Lineair (Reeks1)

average CGT completed

Source: SEA Europe WG MF/ IHS Fairplay 2017

Containership fleet age structure

In 2017, approximately 25% of total containers are over 15 years old . The average age for the fleet was 11 .9 years . The orderbook covers 7% of the fleet .

25%

33%

22%

13%

7%

> 15 years 10-15 years 5-9 years

<5 years Orderbook

container fleet age structure

Source: SEA Europe WG MF, 2018 / IHS Fairplay, 2017

Slow Steaming

Slow steaming started in 2007 – 2008 triggered by the financial crisis, when the market started to face an oversupply of tonnage, declining freight rates and increasing bunker prices . Through slow steaming vessels save bunker fuel, which is the largest component of operating costs structure . So, the practice of deliberately slowing down the speed of a ship was based mainly on economic reasons .

While shipowners are currently waiting to see what will happen in 2020 when the global Sulphur cap enters into force, it is expected that most of them will initially use fuel with low sulfur content . Given that the estimated extra cost will be about 400 dollars per fuel ton, shipowners will employ slow steaming, reducing the speed by a few knots to compensate the higher fuel costs . This will result in a reduction in the available containerships tonnes-mile capacity .

0

2

4

6

8

10

12

14

16

18

20

1987

19

88

1989

19

90

1991

19

92

1993

19

94

1995

19

96

1997

19

98

1999

20

00

2001

20

02

2003

20

04

2005

20

06

2007

20

08

2009

20

10

2011

20

12

2013

20

14

2015

20

16

2017

Deliveries mDWT

containerships fleet in millions DWT year delivered

23

Container Market Outlook

While freight rates appear to be sustaining more positive levels than in 2016, continued big ship deliveries suggest that further improvements in freight market conditions will be hard won by ope-rators . The charter market has made useful gains, with idle capacity much reduced (to about 2% of capacity), and supply side trends remain supportive . Although demolition has recently slightly slowed, overall expansion in containership fleet capacity is still expected to remain fairly moderate into the medium-term . Trends on the demand side are increasingly encouraging, though risks to trade growth remain . Further projected improvements in the fundamentals should support conti-nued re-balancing along with a continued focus on liner company consolidation, and the sector as a whole now appears to be starting to build on the foundations in place for gradually improved market conditions .

The container shipping business is also changing, and operators are forming new alliances to in-crease operational efficiency . The alliances formed in the market limit the amount of port calls due to the large vessels for the main routes, which results in an increased number of feeders especially for small ports and shorter shipping routes . We can also notice a predilection for eco-friendly designs .

The phase-in of the new large containerships in 2018-2020 together with the scrapping of the oldest feeder fleet have produced a feeder vessel shortage . Therefore this will create a need to order and deliver a high number of feeder units until 2020 to maintain the same relative structure of the fleet .

Overall demand growth is expected to be lower than in 2017, but still high enough to potentially improve the fundamental market balance . BIMCO forecasts demand to grow by 4 .0-4 .5% against a fleet growth of 3 .9% in 2018 . The IMF January update of its World Economic Outlook signifi-cantly lifted expected GDP growth in advanced economies for 2018 and 2019, and growth in advanced economies is generally good for container shipping demand .

0

50

100

150

200

250

300

350

0

2.000.000

4.000.000

6.000.000

8.000.000

10.000.000

12.000.000

2011 2012 2013 2014 2015 2016 2017 2018 2020 2025 2030 2035

Containerships Completions, Actual and Forecast CGT Vessels

Source: SEA Europe WG MF , December 2017 / IHS Fairplay, 2018.Note: the bars represent CGT, while the line represents number of vessels

B. General Cargo ships

Background and fleet profile

For a century, the general cargo ship was the workhorse of global seaborne trade . This started to change with the advent of the container ship in the late 1960s . By the mid-80s, classic general cargo vessels were being sent off to the scrapping beaches in droves, as containerships pushed these ships out of more and more trades . As the classic general cargo ship left the scene, the com-position of the general cargo tilted more and more towards short sea cargo ships below 10,000 dwt carrying capacity on the one hand and multipurpose and heavy lift tonnage on the other hand . Despite these changes to the composition of the general cargo fleet, the decline in size and market share of this fleet continued . Of course there were certain periods of revival (as seen in the graph below), but overall the general cargo fleet has declined quite sharply in size, from 116 million dwt in 1980 to 75 million dwt as of the beginning of 2017 . Because the total merchant fleet expanded sharply in the same timeframe, the general cargo fleet’s share of the world merchant fleet has declined much more severely, from 17 .0% in 1980 to 4 .0% at the beginning of 20171 .

116 106 103

104 101

92

108

78 74 75 75

0

20

40

60

80

100

120

140

1980 1985 1990 1995 2000 2005 2010 2014 2015 2016 2017 0

2

4

6

8

10

12

14

16

18

General Cargo fleet development, 1980-2016, in size and share of world fleet

Million DWT %

General Cargo fleet development, 1980-2017, in size and share of world fleet. NOTE : bars indicate fleet size, while the line indicates market share (Source : UNCTAD review of maritime transport, issues 2012, 2015 & 2017). This graph is meant as an indication and is based on Clarksons data. The numbers may not match those used in the SEA Europe forecast, which is based on IHS Fairplay data.

While general cargo vessels have been replaced by container ships in many trades, there are some regions where volumes and port infrastructure do not (yet) allow replacement by container ships . General cargo ships with their own gear have the advantage of flexibility and can call at small ports with no ship-to-shore cargo handling equipment, while the ever-larger container ships require container cranes on the quays2 . More importantly, there are several trades for which con-tainer vessels are not suitable . Examples are short sea shipping and heavy lift shipping . These two shipping segments enjoyed a strong revival during the economic boom prior to the Lehmann crisis of 2008 . Short sea shipping, in Europe in particular, benefited from strong economic growth in various EU economies and plentiful financing, especially in Germany and the Netherlands, where the KG3 and CV4 capital structures attracted many new investors . Heavy lift shipping rode the wave of demand for project cargoes to China, as that country rapidly became the world’s factory . Heavy lift and multipurpose tonnage is very suited for the transport of outsized or breakbulk cargo which does not fit well in a container .

1) UNCTAD, Review of Maritime Transport 2017, pg . 242) UNCTAD, Review of Maritime Transport 2017, pg . 233) KG=Germany Limited Partnership4) sCV=Dutch Limited Partnership

25

The economic boom of the mid-00’s led to a sharp recovery of the size of the general cargo fleet, from 92 million DWT in 2005 to 109 million DWT in 2009 and 20115 . Unfortunately, the reco-very was shortlived as the general cargo fleet saw a very sharp decline in the years from 2011 onwards: in the space of four years (2011-2015) the fleet declined from 109 million DWT to 74 million DWT: a decrease of 32 percent and the worst decrease on record since 1980 .

As of December 31, 2017 the General Cargo fleet, as per the registers of IHS Fairplay, consisted of 15,189 ships . These are all vessels carrying an IMO number and they are classed by IHS either as “In service/commission”, “Laid up”, “In casualty or repair” or “Converting/rebuilding” . Of this total, 13,588 vessels are classed as “General Cargo Ships” . Heavy lift and multipurpose ships account for another 479 ships . The remainder of the category is made up by niche tonnage such as deck cargo ships, livestock carriers, semisubmersible heavy lift ships and the lone yacht carrier .

A large part of the fleet is very old: some 6,829 vessels or 45 percent of the fleet is at least 25 years old . At the same time, 3,635 vessels or 24 percent of the fleet is at most ten years old . The high proportion of old vessels indicates significant fleet renewal potential in the years ahead . Un-fortunately, trends in recent years have shown that the amount of vessels scrapped ever year quite often exceeds yearly newbuild deliveries . As newbuilds tend to be larger than the vessels they replace, the decline in terms of tonnage is less pronounced than the decline in numbers of vessels .

•Recent Market Developments and Market Drivers

With the European short sea shipping industry currently in the doldrums, ordering of newbuilds for this segment has slowed down significantly in recent years . Low freight rates, lack of finances on the shipowners’ side and reluctance of banks to finance newbuilds have left only a few European owners able to order newbuilds . When these owners do order newbuilds, the new ships tend to be much more efficient than the ships they are replacing, in order to reduce fuel consumption, harmful emissions and to comply with the EEDI6 design criteria of the IMO7 . Hulls are being opti-mised and installed engine power is being reduced, compared to older vessels . The large Dutch short sea shipowner, Royal Wagenborg, has indicated that its latest 22,000 dwt newbuildings of the R-BORG class burn two thirds less fuel than the 8,400 dwt ships from the late 90s they are replacing . Despite being almost three times larger, the R-BORG series has 15 percent lower instal-led engine power than its late 90s fleetmates8 . Short sea vessels with Open Top notation, able to sail without hatchcovers, are also on the rise . These vessels are particulary suited to ferry windmill parts to offshore windfarm installation projects . The very latest generation of these open top ves-sels has been adapted further to include a Dynamic Positioning system, increasing suitability for the offshore windfarm market . In recent years, many heavy lift vessels for project cargoes have been built as well, but this segment is currently also suffering from overcapacity and low rates, resulting in an early withdrawal of vessels with lower lifting capacities . Last but not least, the issue of sulphur emissions is firmly on the cards for short sea vessels, as many trade in present or future Sulphur Emission Control Areas, coupled with the global sulphur cap for shipping of 0 .5% per 20209 . While some ships have been retrofitted with sulphur scrubbers, these installations are pro-ving too large or too expensive for most short sea ships . Also many of the smaller short sea ships are either running on marine diesel, which is already compliant with the upcoming sulphur cap or their fuel consumption when running on Heavy Fuel Oil (HFO) is so low that the business case for a scrubber is not viable . Meanwhile, yards in Europe and China are starting to deliver the first short sea ships fuelled by LNG-burning dual fuel engines . Further on the horizon, issues like remote monitoring, autonomous ships and battery-powered ships are coming up .

5) UNCTAD review of maritime transport 2010, pg .30 & UNCTAD review of maritime transport 2012, pg .316) Energy Efficiency Design Index7) International Maritime Organisation, a United Nations agency8) Presentation by Albert Engelsman, Royal Wagenborg, 10/9/’159) IMO .org, 15/11/’16

•demand and supply

As indicated before, there is significant overcapacity as well as a severe lack of financing for newbuilds in the European short sea sector . Dutch short sea expert Johan Wagelaar only sees a balancing of demand and supply in the European short sea market by 2020, providing demand growth remains at 2 percent per year and newbuild contracting remains low10 . Contracting of ge-neral cargo newbuilds worldwide is in fact currently very low, resulting in a sharp drop in expected newbuild deliveries, from over 1 .05 million CGT for 2017, via 1 .87 million CGT in 2018 to a mere 660,000 CGT in 2019 . Deliveries for 2018 will probably end lower than expected due to delays on newbuilds, resulting in slightly higher final numbers for 2019 . Upon closer examination, over 300,000 CGT of the current general cargo orderbook was contracted before 2013, raising doubts whether this tonnage will be delivered at all .11 On the upside, some new contracting for 2019 deliveries is still to be expected, as general cargo ships generally have fairly short lead times . Nevertheless, the outlook for the next few years for yards specialising in general cargo tonnage is challenging . An improvement of newbuild contracting towards the end of the current decade (2018-2020) would seem likely though, given the significant scrapping potential of the existing fleet, exacerbated by upcoming new environmental regulations as detailed before . In addition, the orderbook-to-fleet ratio for the general cargo fleet at the end of 2017 was low at approximately 3 .3% in CGT terms .

In his very latest update, Mr Wagelaar notes that the financial situation of publicly listed European short sea operators is rapidly improving and specialised shipyards are starting to see a recovery of ordering for short sea tonnage as of May 2018 .12

•Uncertainties and Possible Future Demand Drivers

Of course, there are many developments and circumstances which are hard to predict in a de-mand requirement forecast . Perhaps intra-Asian trade will grow so fast that there will be a sharp increase in Asian demand for short sea vessels . Alternatively, a lot of this new intra-Asian traffic could be containerised immediately . Another interesting potential development could be that of unmanned ships, which might generate so many savings that wholesale replacement of existing manned ships by newly built unmanned short sea ships turns out to have a solid business case .

In the heavy lift and project cargo sector, a continuous push for larger and more capable ships (mainly in terms of lifting capacity) could generate a premature fleet replacement of the exi-sting ships . With the Chinese economy reaching maturity, the “Belt and Road’ (BRI) initiative or “Maritime Silk Road” of the Chinese government might generate renewed intense demand for heavy lifters . Also, a continued growth of several energy- and resource-rich African countries could spur heavy lift demand . At the time of writing however, the fate of many of these sub-Saharan “boom” economies is hanging in the balance .

General Cargo market outlook

SEA Europe predicts a relatively modest demand requirement for on average 138 General Cargo vessel deliveries or 1 .05 million CGT per year for the period 2018-2020 . For the period 2021-2025, the demand recovery for General Cargo is expected to peak at an average of 218 vessel deliveries per year or 1 .77 million CGT . In the longer run, however, we expect the world’s gene-ral cargo fleet to resume the declining trend it has exhibited over the years . Our forecast for the period 2031-2035 is therefore decidedly bearish, at an average 67 newbuild deliveries per year or 616,000 CGT per year . Demolition numbers are expected to remain firm throughout the entire forecasting period, oscillating between 277 and 284 ships per year or 1 .42 to 1 .46 million CGT per year . There are simply that many elderly ships in the general cargo fleet .

10) Johan Wagelaar, Tristan Beumer; The European Short Sea market in perspective, Volume III, 2015, pg .2611) Data source: IHS Fairplay, updated to end August 201612) Johan Wagelaar, presentation for Netherlands Maritime Technology, 24 May 2018

27

0

100

200

300

400

500

600

700

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

3.000.000

3.500.000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018-20 average

2020-25 average

2025-30 average

2030-35 average

General Cargo Vessels Completions, Actual and Forecast

CGT VESSELS

Source: SEA Europe WG MF, 2018 / IHS Fairplay, 2017 Note: the bars represent CGT, while the line represents number of vessels

C. Bulk Carriers

Background and Fleet Profile

Bulk carrier market conditions have shown clear improvement in 2017, compared to the historically depressed market environment seen in 2016 . The bulk carrier segment as a whole has seen last year much more positive sentiment amongst owners and stronger investor interest than in the past years . Second-hand prices recorded strong gains in early 2017, while sale and purchase activity has remained high . The improved balance in the bulk carrier sector this year has largely been driven by positive developments on the demand side . While recycling has slowed this year, in line with higher earnings, overall fleet growth has remained relatively moderate allowing faster dry bulk trade growth to start to erode some of the surplus capacity .

Furthermore, there is more room for demolitions, particularly given costly regulations on ballast water treatment systems and low sulphur emissions that are coming into play, which may sway retirement decisions .

•Demand

Expansion in seaborne dry bulk trade accelerated to around 4% in 2017, following average growth of just 0 .8% p .a . in 2015-16 . Strong Chinese demand has remained a key driver of volume growth .

Chinese seaborne imports of iron ore, coal and crude oil have all grown strongly throughout 2017 . Both seaborne imports of crude oil and iron ore have reached the highest level ever recorded, while coal reached the highest level in three years .

Imports of crude oil and coal have benefited the shipping industry to the greatest extent as both volumes and distances have increased .

China continues to ramp up its imports of iron ore with seaborne imports growing 4 .7% in 2017 compared to 2016 . This amounts to a total seaborne import of 1,054 million tonnes of iron ore breaking the record of 1,006 million tonnes from the year before . Total Chinese imports of Iron ore by all modes of transportation was 1,075 million tonnes in 2017, compared to 1,023 million tonnes in 2016 .

•supply

Expansion in bulk carrier fleet capacity picked up slightly in 2017 to around 2 .9%, following mu-ted growth of 1 .4% in 2016 . Bulk carrier demolition has slowed in 2017, with 14 .5m dwt sold for recycling in 2017, compared to close to 30m dwt in full year 2016 . Meanwhile “non-delivery” of the scheduled orderbook has decreased slightly this year, but remains significant with 34% in dwt terms and 37 .4m dwt being delivered, down almost 20% compared to 2016 . Following a period of extremely subdued contracting, the orderbook has dwindled to total 733 vessels of 76 .8m dwt at the end of December 2017, equivalent to 9% fleet capacity . Newbuilding interest has picked up strongly in the bulk carrier market this year with 286 units ordered in January-December 2017 (54 in 2016) .

15%

22%

29%

25%

9% Capesize

Panamax

Handymax

Handysize

Rest

BulkcarriersNumber (Fleet end 2017)

Source: SEA Europe WG MF, 2018 / IHS Fairplay, 2017

Capesize spot earnings averaged in 2017 reached USD 13,475 per day, up to 125% from the full year 2016 average, and in late September reached the highest level for almost three years (with USD 24,018 per day) . The improved market conditions have been supported by strong demolition over the last few years (although recycling has slowed more recently) and the continued firm pace of growth in iron ore trade, which has helped to gradually absorb surplus capacity .

The Panamax market has also seen an improvement in 2017 reaching up to 57 .5% from the 2016 average . While lower recycling led to a faster rate of growth in the Panamax fleet this year (2 .8%) than in the previous year (0 .5%), firm growth in coal and grain trade has supported a more po-sitive market environment, although earnings this year are still 45% below the ten year historical average .

16.000

16.500

17.000

17.500

18.000

18.500

19.000

19.500

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Reeks1 Lineair (Reeks1)

bulkcarriers average CGT completed

Source: SEA Europe WG MF, 2018 / IHS Fairplay, 2017

Capesize

Panamax

Handymax

Handysize

Rest

Bulkcarriersdwt (Fleet end 2017)

23%

25%

11%

0%

41%

29

The high growth trend in the average vessel size continues, as can be seen in the above graph .

Fleet growth in the Handymax sector remained the fastest of all the bulkcarrier segments this year at 4%, but improved growth in seaborne coal, grain and minor bulk trade have still helped to ti-ghten the market . An improvement in minor bulk trade volumes has helped to support fundamentals in the Handysize market despite a slight acceleration in fleet growth . Average Handysize trip rates reached up to 46% compared to the 2016 average .

Bulk Carrier Market Outlook

Momentum in the bulk carrier market appears to have picked up pace this year, and with seasonal factors also playing a role, earning rose to the highest level in almost four years . The faster pace of growth in dry bulk trade has been a key factor behind the improved market environment in 2017, and there remain positive drivers for continued expansion in the short-term, including rising South East Asian coal imports, rising demand for high-quality foreign iron ore in China, and the positive impact of improving global economic growth on minor bulk trade . However, there remain risks to the demand outlook, including from the potential impact of environment inspections on Chinese industrial activity, and from further displacement of Indian coal imports from rising domestic coal output . Nevertheless, even if demand growth moderates slightly in the short-term, the expected sharp slowdown in deliveries in 2018 looks like to limit fleet growth to a very subdued level of 1% in short term .

One of the uncertainties is on the issue of sulphur gas emissions . Shipowners are waiting to see what will happen in 2020, so they will initially use fuel with low sulfur content (assuming that in 2020 there will be enough low-sulphur fuel to meet all the demand) . Given that the estimated extra cost is about 400 dollars per fuel ton, shipowners will employ slow steaming, reducing the speed by a few knots to compensate the higher fuel costs . It is estimated that this may results in a 16 .7% reduction in the available bulk carriers tonnes-mile capacity . On the other hand, the rise of new technologies will make the productivity of the fleet greater . Another factor to consider is that by 2020 there will be almost 20% of existing fleet that would be over 15 years of age and become likely scrapping candidates due to expensive regulatory environment, the evolution of BDI and higher scrap prices .

While challenges and risks remain, it appears that the bulk carrier market is starting to move on a more positive trajectory .

0

50

100

150

200

250

300

350

400

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2020 2025 2030 2035

Bulkcarriers completions, actual and forecast

Capesize Panamax Handymax Handysize Rest

Num

ber

Source: SEA Europe WG MF, 2018

Bulkcarriers completions, actual and forecast

0

5.000.000

10.000.000

15.000.000

20.000.000

25.000.000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2020 2025 2030 2035

Capesize Panamax Handymax Handysize Rest

CGT

Source: SEA Europe WG MF, 2018

D. Oil & Chemical Tankers

Background and Fleet Profile

In the long term, the pace of growth in oil consumption slows down globally, albeit in absolute terms, going from growth of more than 3% per year to below 2% in 2030 and 2035 .

On the other hand, in the past decade the tanker fleet grew more than oil seaborne trade, gene-rating fleet overcapacity . The projection to 2035 shows that due to this overcapacity, the tanker fleet will grow less than oil seaborne trade .

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

1.000

2.000

3.000

4.000

5.000

6.000

1990

1995

2000

2005

2010

2016

2020

2025

2030

2035

2040

mill

ion

tons

(Oil

equi

vale

nt)

World Oil Consumption million tons (Oil equivalent)

Non-OCDE OCDE Annual increase % - Right Axis

Source: SEA Europe WG MF, 2018

31

Tanker Fleet Requirement and Newbuilding Forecast

-5%

0%

5%

10%

15%

20%

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2020

2025

2030

2035

Ann

ual G

row

th

Oil Seaborne Trade Growth and Tanker Fleet Growth

Oil Seaborne Trade Growth (mill. Tons) Tanker Fleet Growth (dwt)

Source: SEA Europe WG MF, 2018

We expect the oil tankers fleet requirement to expand at a rate of 1 .7% per year in terms of dwt . In contrast to the previous decade, tanker fleet grew at a rate close to 5% per year in terms of dwt . In the period 2018-2035, oil tankers new building requirements, according to our forecasts, have a mean of 300 units per year, 33 dwt pa, and 9 .4 CGT p .a .

E. LNG & LPG Carriers

Background and Fleet Profile

Between 2001 and 2014, the strong growth in LNG transport demand and high gas prices led to an increase in the contracting of LNG and LPG vessels . However, as of 2015, as a result of the fall in the price of natural gas and oil reduced freight prices, contracts fell sharply to the lowest levels of the last 10 years . In 2017 only 17 units of LNG were contracted and only 9 units in 2016, com-pared to 70 LNG contracts in 2014 and 37 in 2015 . 2035 forecasts estimate growth of seaborne trade in LNG of 5,1% pa .

0

1000

2000

3000

4000

5000

6000

7000

0

100

200

300

400

500

600

700

800

900

1.000

198

5 1

986

199

0 1

995

200

0 2

001

200

2 2

003

200

4 2

005

200

6 2

007

200

8 2

009

201

0 2

011

201

2 2

013

201

4 2

015

201

6 2

017

202

0 2

025

203

0 2

035

Aver

age

dista

nce

mill

ion

tons

(Oil

equi

vale

nt)

Seaborne Trade in LNG million tons (Oil equivalent)

LPG LNG

Average distance, n. miles LNG Average distance, n. miles LPG

Source: SEA Europe WG MF, 2018

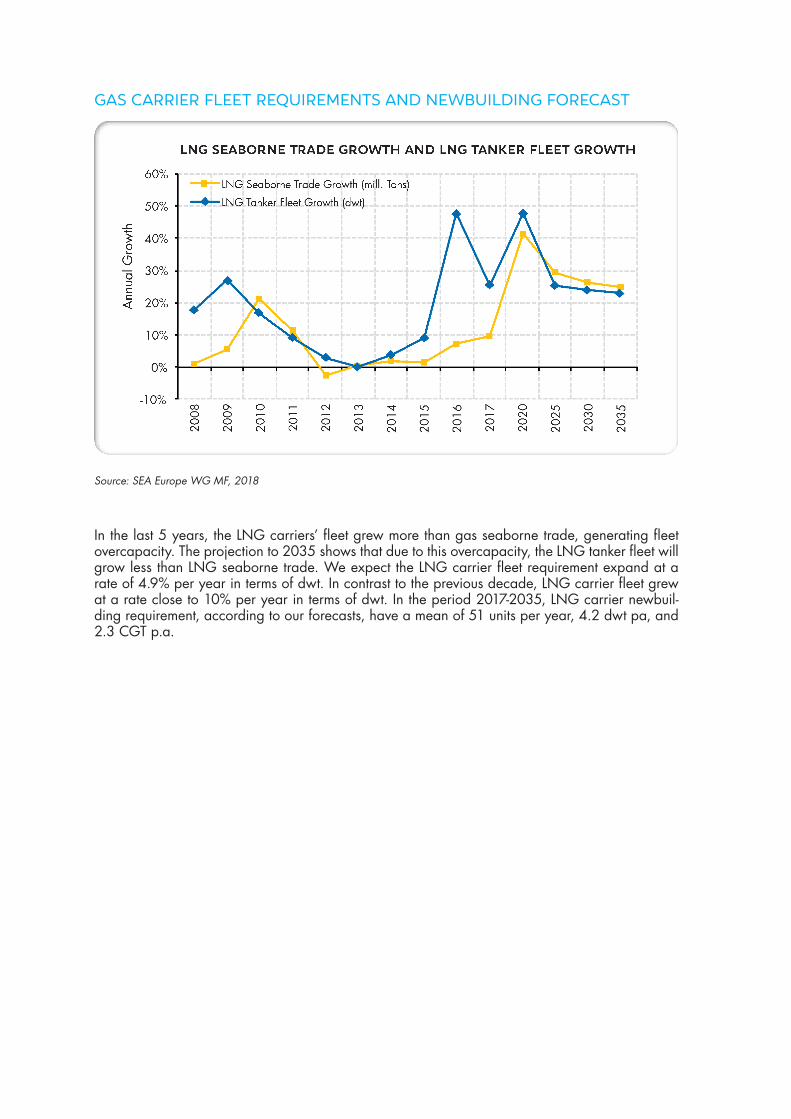

Gas Carrier Fleet Requirements and Newbuilding Forecast

-10%

0%

10%

20%

30%

40%

50%

60% 20

08

2009

2010

2011

2012

2013

2014

2015

2016

2017

2020

2025

2030

2035

Ann

ual G

row

th

LNG Seaborne Trade Growth and LNG Tanker Fleet Growth

LNG Seaborne Trade Growth (mill. Tons)

LNG Tanker Fleet Growth (dwt)

Source: SEA Europe WG MF, 2018

In the last 5 years, the LNG carriers’ fleet grew more than gas seaborne trade, generating fleet overcapacity . The projection to 2035 shows that due to this overcapacity, the LNG tanker fleet will grow less than LNG seaborne trade . We expect the LNG carrier fleet requirement expand at a rate of 4 .9% per year in terms of dwt . In contrast to the previous decade, LNG carrier fleet grew at a rate close to 10% per year in terms of dwt . In the period 2017-2035, LNG carrier newbuil-ding requirement, according to our forecasts, have a mean of 51 units per year, 4 .2 dwt pa, and 2 .3 CGT p .a .

33

Newbuilding requirements: Oil & Gas Offshore

Market drivers

The key driver for offshore newbuilding demand is the prevailing oil price and the perception of future oil price development vs . actual and expected cost development . Higher oil price results in a higher number of profitable offshore fields, increase in exploration activity and thus higher spending and a higher demand for rigs and ships .

However, there are significant differences in recognised oil analyst’s prognosis on future oil price development . As it is a challenge to predict future oil price it is equally challenging to predict the future level of offshore vessel demand or timing of the next peak .

New significant discoveries in one region will usually affect the sentiment to oil companies . New discoveries and high hit rates in areas previously regarded as not promising will be key drivers for increased interest and further exploration activity .

In emerging regions, the infrastructure is often limited, distances may be longer and the rig density is low . Thus, a higher number of support vessels per rig will be needed . Operation in arctic areas will drive this number even further .

Mature regions with predicted lower future production are often interpreted as declining offshore markets . However, lower production is also an important driver for higher exploration activity when there is a sufficient focus on replacing reserves . In addition, there will be higher focus on increasing the production rate per field or well (well intervention) . Development of marginal fields and tiebacks will also require subsea vessels . A mature installed base of subsea wells and pipeli-nes will require vessels for inspection, maintenance and repair . Then at some point there will be a need for decommissioning and specialist vessels accordingly . Activity in mature areas is often key for driving innovation with the North Sea as a good example .

Countries’ aiming to get less dependent on oil or gas import is also an important activity driver . For national oil companies (NOC) there will often be less attention on short-term profitability and more attention on long-term growth of reserves and production . This will depend on government policy . Still, as NOCs usually share production licences with international companies the challenge will be to make licences and projects as attractive as possible .

The mix of shallow water, deep water, ultra-deep water activity and effects of increased activity in remote areas is also key . Distances from shore are increasing leading to higher demand for more efficient vessels . With this there are new requirements and a need for more rigs and ships capable of operating in these areas in the most efficient and safe way .

More cost-efficient vessel designs and systems are also important drivers for newbuild demand as vessels then will have a competitive advantage, obtain higher utilisation and thus be preferred in the market .

The market cycle

Offshore shipping markets are normally very volatile . Oil price development has always been one reason for this, but other reasons are sometimes low market visibility, speculative orders, lack of discipline, the fight for market shares and overreaction from too many of the market players .

The market balance is sensitive with trigger effects . When fleet utilization is increasing above a certain level, the charter rates are sky rocketing with an order boom as a result . However, what is often the case is an order book containing too many vessels at the time when day rates start to drop again . The consequence may be several years with a low number of offshore orders .

Thus, the peaks may get higher and downturns deeper than what is possible to predict in a newbu-ilding prognosis .

Demolitions increase

Fleet shrinks

Lay-ups decreasing

Fright rates recover

Demand for newbuildings

increase

Yards reopened

or new yards

created

Excess of shipbuilding

capacity

Ship price drop

Cancellations

Lay-ups increase

Demand for newbuilding

drop

Fright rates drop

Over ordering by speculators/

bargain hunters

Oversupply

Shipping market cycle

The effects of shale oil

One main advantage of shale oil versus offshore is a far shorter lead-time from development to production start, reducing the time until a project turns cash positive . A disadvantage of shale oil wells is the higher decline rates compared to offshore, where the typical shale oil well declines 80% in production within the first three years . However, this becomes less of a concern when ta-king into account the lead times and costs .

According to several market observers, shale companies will struggle to keep growth rates up as they deplete the most profitable wells and have to move to higher-cost locations . Shale producers are also starting to face pressure from investors to stop growing at all costs, but rather to look at increasing cash flows instead .

With higher oil price and activity in the short and medium term, marginal costs for shale oil is expected to increase faster than for offshore . This is bringing offshore projects back to a compe-titive position .

Supply from offshore will be needed for decades . Shale will not be able to close the gap .

Offshore spending and activity

For E&P spending there was a trend shift in 2013, moving from double to single digit growth . The key reason for this was the stable oil price vs . very strong growth in costs . On the top of growth in costs there was a severe oil price slide resulting in aggressive spending cuts . It was a matter of survival . It was the first time in history that we saw reductions in E&P spending for three consecutive years .

However, after over three very lean years, companies are feeling the turn . After a prolonged effort to cut its cost base, there are clear positive signs in the industry . Investors in today’s $60-70 world are now viewing situation and outlook more positively . Oil demand has increased, not just becau-se of economic growth, but also due to the low oil price itself .

35

According to a report from DNV GL, confidence in industry growth has risen from 32% in 2017 to 63% in 2018 . In a survey from 2017, seven out of ten business leaders in the Norwegian oil and gas industry will hire more people in 2018 . The number of UK offshore fields set to get the go-ahead in 2018 alone represents a burst of 225% over the past two years combined, according to Rystad Energy . Shell says it has made one of its largest US Gulf of Mexico discoveries in the past decade at the deep-water Whale well . Brazil’s Petrobras is preparing a new wave of multi-billion dollar investments to help develop its massive pre-salt resources .

An offshore recovery is also needed to prevent an oil supply deficit emerging in the 2020s . The level of discoveries has been very low in recent years . A massive underinvestment could disturb the global supply system and trigger a new growth cycle, with shale production likely to prevent any drastic fluctuations in price .

A significant share of the growth in offshore spending that we saw before the oil price slide in 2014 was due to cost inflation, not increased activity . Now offshore is becoming much more cost efficient .

A significant reduction in costs - including improved project design, increased standardization, reduced complexity, increased drilling speed etc . - will help foster growth in offshore production . Field projects with sub-$40 break-even prices are matured to final investment decisions . For the giant Johan Sverdrup offshore field in the North Sea, break-even oil price in phase one is reduced to below USD 15 per barrel . The arctic offshore field Johan Castberg was originally not commer-cially viable with a break-even oil price of $80/bbl . Now the break-even oil price is $35/bbl . In 2013, the actual oil price was around $112/bbl . Still, Statoil’s cash flow was negative . Today, Statoil’s portfolio as a whole is said to have a break-even price of $27/bbl . According to Statoil, 80-90% of the cost improvements they have achieved are related to efficiency, doing things diffe-rently, not market effects nor deferring activities .

In general, oil companies and offshore operators have pushed down costs significantly in the past two years because of simpler concepts, cheaper equipment and more efficient drilling . This is af-fecting the number of profitable projects .

Offshore final investment decisions, subsea tree awards and general global upstream spending are set to rise further in 2018 . From a low base in 2016, offshore sanctioned capital expenditure was up 40% in 2017 . Project sanctions are set to further increase this year, but the timing of spen-ding will of course be spread out over several years .

Most market observers see higher oil prices in 2018-2019 and an increase in offshore E&P spen-ding from 2018 and onwards, perhaps with a significant increase in 2019 .

However, despite the above, several key questions remain; what happens if the OPEC cuts end, what will Russia do, to what extent an increase in US shale production will continue to impact the market, will there be a significant increase in onshore production in Iraq, the economic and politi-cal development in Venezuela etc .

The offshore fleet