2018 Laporan Publikasi Tahunan Annual Publication Report · (tabungan). Sebagai upaya pengembangan...

154

Ciptakan Pertumbuhan Melalui Transformasi Creating Growth through Transformation Laporan Publikasi Tahunan Annual Publication Report 2018

Transcript of 2018 Laporan Publikasi Tahunan Annual Publication Report · (tabungan). Sebagai upaya pengembangan...

La

po

ran

Pu

blik

asi Ta

hu

na

n 2

01

8 A

nn

ua

l Pu

blica

tion

Re

po

rt

Ciptakan Pertumbuhan Melalui Transformasi

Creating Growth through Transformation

Laporan Publikasi TahunanAnnual Publication Report2018

Laporan Publikasi TahunanAnnual Publication Report2018

CIP

TAK

AN

PE

RT

UM

BU

HA

N M

EL

ALU

I TR

AN

SFO

RM

AS

I

Sahid Sudirman Center Lt. 56 Unit B Jl. Jend. Sudirman Kav. 86 Jakarta Pusat 10220E-mail : [email protected] :62–2127889535Fax :62–2127889533

www.okbank.co.id

PT

BA

NK

OK

E IN

DO

NE

SIA

IKHTISAR KINERJA

Ikhtisar Keuangan

Ikhtisar Kinerja

Rencana Dan Strategi Kinerja

Laporan Dewan Komisaris

Laporan Direksi

PROFIL PERUSAHAAN

Sekilas Bank Oke Indonesia

Peristiwa Penting Di Tahun 2018

Jejak Langkah

Visi & Misi

Nilai Nilai Dasar

Struktur Organisasi

Komposisi Kepemilikan Saham

Profil Pemegang Saham

Profil Dewan Komisaris

Profil Direksi

Produk Dan Layanan

Penghargaan Dan Sertifikasi

Jaringan Kantor

ANALISA DAN PEMBAHASAN MANAJEMEN

Tinjauan Keuangan

Tinjauan Usaha

Tinjauan Unit Pendukung

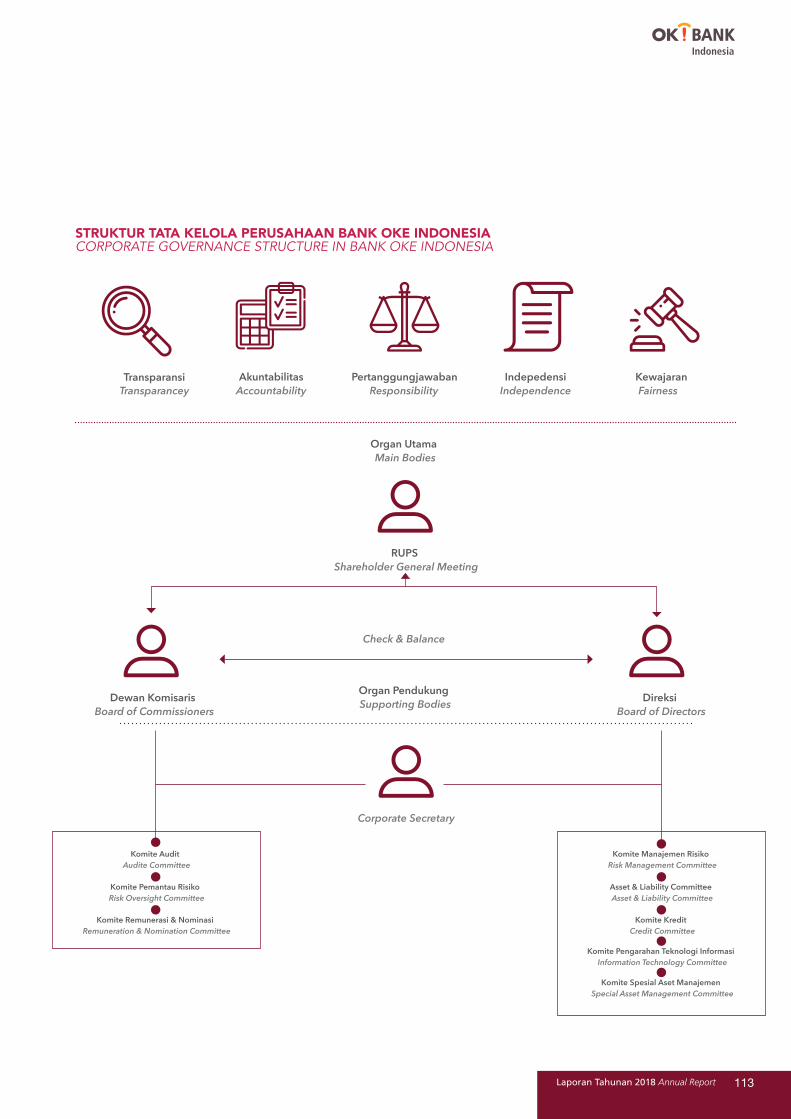

TATA KELOLA PERUSAHAAN

Tata Kelola Perusahaan

Dewan Komisaris

Dewan Direksi

Komite-Komite Dewan Komisaris

Penerapan Fungsi Kepatuhan Audit Intern dan Audit Ekstern

Kode Etik

Pengaduan Internal

Pengaduan Internal

TANGGUNG JAWAB SOSIAL PERUSAHAAN

Tanggung Jawab Sosial Perusahaan

LAPORAN KEUANGAN 2018 - AUDIT

PERFORMANCE HIGHLIGHTS

Financial Highlights

Performance Highlights

Plan And Strategy

Report From The Board Of Commissioners

Report From The Board Of Directors

COMPANY PROFILE

Bank Oke Indonesia In Brief

Important Events In 2019

Milestones

Vision & Mission Core Values

Organization Structure

Ownership Composition

Shareholders Profiles

Board of Commissioners Profiles

Board of Directors Profiles

Products and Services

Awards and Certifications

Office Network

MANAGEMENT DISCUSSION AND ANALYSIS

Financial Review

Business Review

Supporting Units

GOOD CORPORATE GOVERNANCE

Good Corporate Governance

Board of Commissioners

Board of Directors

Committees of The Board of Commissioners

Implementation of Compliance, Internal Audit and External Audit Functions

Code of Ethics

Whistle Blowing System

External Complaint Channel

CORPORATE SOCIAL RESPONSIBILITY

Corporate Social Responsibility

2018 FINANCIAL REPORT - AUDITED

4569

13

16202128293032323335384041

444750

110112116120125

141142143

146

150

DAFTAR ISITable of Content

Ciptakan Pertumbuhan Melalui TransformasiCreating Growth through Transformation

Sejalan dengan kemajuan yang dialami oleh industri perbankan di tahun 2018, Bank Oke Indonesia (OK! BANK) membukukan hasil yang positif dan mengalami kemajuan secara signifikan jika dibandingkan dengan tahun-tahun sebelumnya. Tren kemajuan tersebut dimanfaatkan dengan baik oleh OK! BANK dengan memberikan kontribusi, tidak hanya dari sektor perbankan namun juga sektor perekonomian secara umum.

Upaya kontribusi dari OK! BANK ditunjukan dengan komitmen OK! BANK dalam memperkuat lini UKM. Dalam upayanya tersebut, OK! BANK meluncurkan dua segmen bisnis baru yaitu kredit UKM, kredit ke debitur emerging market dan juga melakukan diversifikasi terhadap kredit ke BPR dan ritel.

Kinerja perbankan di tahun 2019 diprediksi mengalami kenaikan dan pertumbuhan. Namun hal tersebut tidak semerta-merta membuat OK! BANK lengah dalam mempertahankan kinerjanya. Alih-alih, OK! BANK meyakini kenaikan dan pertumbuhan yang terjadi menjadi motivasi untuk terus berupaya meningkatkan kinerja dan kontribusi yang positif.

In line with the progress experienced by the banking industry in 2018, Bank Oke Indonesia (OK! BANK) posted positive results and made significant progress compared to previous years. The progress trend is well utilized by OK! BANK by contributing, not only from the banking sector but also the economic sector in general.

The contribution of OK! BANK is shown by its commitment in strengthening the SME line. In this effort, OK! BANK launches two new business segments, namely SME loans, loans to emerging market debtors and also diversifies credit to rural banks and retail.

Banking performance in 2019 is predicted to increase and grow. However, it does not immediately make OK! BANK stall its performance. Instead, OK! BANK believes that the increase and growth that occur is what propel the Bank to strive to improve performance and positive contributions.

IkhtisarKinerjaPerformance Highlights

4 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

Dalam miliar Rupiah In billion Rupiah

IKHTISAR KEUANGANFINANCIAL HIGHLIGHTS

DATA KEUANGAN 2018 2017 2016 FINANCIAL DATA

Jumlah Aset 2.066,60 2.108,28 1.393,22 Total Assets

Jumlah Penyaluran Kredit 1.677,06 1.470,22 1.035,55 Total Loans

Jumlah Simpanan Nasabah 127,05 192,28 99,66 Deposits from Customers

Jumlah Simpanan dari Bank Lain 794,52 779,49 647,33 Deposits from Other Banks

Jumlah Ekuitas 1.116,83 1.111,22 590,01 Total Equity

Pendapatan Bunga 201,82 205,89 119,87 Interest Income

Beban Bunga (52,31) (75,06) (63,52) Interest Expense

Pendapatan Bunga – Bersih 149,51 130,83 56,34 Net Interest Income

Pendapatan Operasional Lainnya 2,21 1,41 1,63 Other Operating Income

Beban Operasional (142,55) (113,58) (77,47) Operating Expense

Laba/(Rugi) Operasional 9,17 18,67 (19,50) Operating Income

Laba (Rugi) Sebelum Pajak 10,16 19,17 (19,42) Income Before Tax

Laba (Rugi) Setelah Pajak 6,22 16,56 (18,40) Income After Tax

RASIO KEUANGAN (%) 2018 2017 2016 FINANCIAL RATIOS (%)

Imbal Hasil Aset (ROA) 0,50 0,95 (1,82) Return on Assets (ROA)

Imbal Hasil Ekuitas (ROE) 0,60 1,92 (8,98) Return on Equity (ROE)

Kredit yang Diberikan terhadap DPK 761,45 366,97 390,12 Loans to Deposits Ratio (LDR)

Kewajiban Penyediaan Modal Minimum dengan memperhitungkan risiko kredit dan operasional

72,05 98,28 77,74 CAR with credit and operational risks

Rasio Kredit Bermasalah – Kotor (termasuk BPR) 1,72 3.60 2,22 Non Performing Loan/Gross (Include BPR)

Rasio Kredit Bermasalah – Bersih (termasuk BPR) 1.40 2,11 0,05 Non Performing Loan/Net (Include BPR)

Rasio Kredit Bermasalah – Kotor (tidak termasuk BPR) 2,99 6.92 6,10 Non Performing Loan/Gross (Exclude BPR)

Rasio Kredit Bermasalah – Bersih (tidak termasuk BPR) 2,43 4.06 0,15 Non Performing Loan/Net (Exclude BPR)

Marjin Pendapatan Bunga Bersih 7,92 6,78 5,48 Net Interest Margin (NIM)

Biaya Operasional terhadap Pendapatan Operasional 95,07 90,70 116,40 Operating Expense to Operating Income

5Laporan Tahunan 2018 Annual Report

Pencairan KreditCredit Disbursement

Aset BankBank’s Assets

Jumlah Portofolio KreditLoan Portfolio

Jumlah NasabahTotal Customers

Dana Pihak KetigaThird Party Funds

Pendapatan BungaInterest Income

119.87

205.89 201,82

2016 2017 2018

IKHTISAR KINERJAPERFORMANCE HIGHLIGHTS

2016 2017 2018

983.23

1,527.26

1,673.32

2016 2017 2018

1,393.22

2,108.28 2,066,60

746.99

921.57971.78

2016 2017 2018

1,035.55

1,470.22

1,677.06

2016 2017 2018

3,726

3,914

2016 2017 2018

4,246

6 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

RENCANA DAN STRATEGI KINERJAPLAN AND STRATEGY

STRATEGI 2018 Arah Kebijakan Bank Dalam satu tahun tantangan dan perubahan, Bank Oke Indonesia memprakarsai beberapa perubahan penting dalam arah kebijakannya pada tahun 2018 untuk mewujudkan visi dan misi Bank.

Untuk mendukung pertumbuhan bisnis, mengantisipasi perubahan kondisi makro ekonomi, dan merespon kebutuhan pasar, Bank memulai proses penambahan beberapa fitur produk penting dan diversifikasi bisnisnya baik dari sisi aset dan kewajiban. Sampai akhir 2018, Bank terus mengembangkan portofolio pinjaman dan fokus ke segmen usaha SME dengan tetap memaksimalkan penyaluran pembiayaan ke selektif segmen BPR dan Multifinance. Bank juga mulai mengembangkan pembiayaan multiguna untuk memperluas portfolio pinjaman.Selain dari itu, kami akan terus memperbaiki skema suku bunga dan metode pembayaran angsuran untuk terus meningkatkan profitabilitas Bank.

Pada sisi liabilitas, Bank juga telah dan akan terus membangun dan membina kerjasama dengan bank umum lainnya untuk mendapatkan fasilitas antar bank yang diharapkan dapat meningkatkan kepercayaan kepada Bank; meningkatkan pelayanan kepada nasabah individual dan non individual dengan melakukan promosi dan beberapa alternatif bentuk simpanan (tabungan). Sebagai upaya pengembangan bisnis pendanaan, Bank mengoptimalkan aktivitas penghimpunan pendanaan adalah dengan membuat beberapa program yang menarik seperti “OK! BANK Smart Traveller”, “Staff get Customer”, dan “Customer get Customer” dengan model pengumpulan poin yang dapat ditukarkan dengan penghargaan tertentu. Selain itu juga terdapat program “Deposito & Giro Crash Program” untuk nasabah-nasabah existing utama dan Korporasi, dengan penawaran imbal hasil bunga yang menarik.

Strategi Bank yang lain dalam upaya menghimpun dana adalah dengan melakukan customer gathering, memberikan layanan tambahan perbankan melalui OK! BPR (formerly known as Andara Bersama BPR(ABB)) dan OK! Link, open booth di beberapa pameran, dan aktif mendukung kegiatan asosiasi Perbarindo Pusat dan Daerah.

Untuk mendukung pertumbuhan bisnis yang berkesinambungan, arah kebijakan Bank meliputi:1. Meluncurkan merged OK! BANK (merger Bank Oke Indonesia

dengan Bank Dinar).2. Tetap fokus memperluas jangkauan dan meningkatkan

portfolio pembiayaan pada segmen SME.3. Terus menjajaki dan membangun segmen bisnis Retail

baik pada bidang pendanaan dan pembiayaan terutama sektor produktif.

4. Melakukan pengembangan produk Personal Loan dan Commercial Loan.

5. Meningkatkan infrastruktur pelayanan melalui E-Banking channel dan sumber daya manusia yang berkualitas.

6. Membangun kapasitas operasional serta menyiapkan SOP dan kontrol internal untuk mendukung pengembangan bisnis dengan tetap menjaga kualitas yang baik.

2018 STRATEGY Bank Policy Directions In one year of challenges and changes, Bank Oke Indonesia initiated several important changes in its policy direction in 2018 to achieve the Bank’s vision and mission.

To support business growth, anticipate changes in macroeconomic conditions, and respond to market needs, the Bank began the process of adding several important product features and diversifying its business in terms of assets and liabilities. Until the end of 2018, the Bank continued to develop its loan portfolio and focus on the SME business segment and continuing to maximize financing distribution to the selective BPR and Multifinance segments. The bank also began to develop multipurpose financing to expand loan portfolio.In addition to this, we will continue to improve the interest rate scheme and the repayment methodology in order to secure profitability of the Bank.

On the liability side, the Bank has and will continue to build and foster cooperation with other commercial banks to obtain interbank facilities that are expected to increase trust in the Bank; improve services to individual and non-individual customers by conducting promotions and several alternative forms of savings. As an effort to develop the funding business, the Bank optimizes funding collection activities by making several interesting programs such “OK! BANK Smart Traveller”, “Staff get Customer”, and “Customer get Customer” with point collection models that can be exchanged for certain awards. In addition, there are also “Deposit & Current Crash Program” programs for major existing customers and corporations, with attractive interest yield offers.

Another strategy of the Bank in an effort to raise funds is by conducting customer gathering, providing additional banking services through OK! BPR (formerly known as Andara Bersama BPR(ABB)) and OK! Link, an open booth at several exhibition, and actively supports the activities of the Central and Regional Perbarindo associations.

To support sustainable business growth, the direction of Bank policy includes:1. Launch merged OK! BANK (Bank Oke Indonesia’s merger with

Bank Dinar).2. Stay focused on expanding and increasing the financing

portfolio in the SME segment.3. Keep exploring and building the Retail business segment

in the areas of funding and financing, especially the productive sector.

4. Developing Personal Loan and Commercial Loan products.

5. Improve service infrastructure through E-Banking channels and quality human resources.

6. Build operational capacity and prepare internal SOPs and controls to support business development while maintaining good quality.

7Laporan Tahunan 2018 Annual Report

Halaman ini sengaja dikosongkanThis page is intentionally left blank

8 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

TAHUN 2018 DITANDAI DENGAN LANGKAH

STRATEGIS YANG DILAKUKAN OLEH APRO FINANCIAL CO LTD, YAITU DENGAN

MELAKUKAN MERGER DENGAN BANK DINAR.

THE YEAR 2018 WAS MARKED WITH STRATEGIC LEAPS TAKEN

BY APRO FINANCIAL CO LTD BY MERGING WITH BANK

DINAR.

Moon YoungsoKomisaris Utama

President Commissioner

8 Laporan Tahunan 2018 Annual Report

9Laporan Tahunan 2018 Annual Report

LAPORAN DEWAN KOMISARIS REPORT FROM THE BOARD OF COMMISSIONERS

Merger antara Bank Dinar dan APRO melahirkan OK! BANK yang terlebih dahulu diakuisisi pada 2016 dengan penguasaan saham sebesar 99%. Setelah sukses memasuki kategori BUKU II, OK! BANK terus berupaya untuk meningkatkan modal menjadi BUKU III melalui metode organik dan anorganik. Langkah-langkah strategis ini merupakan upaya untuk menghadapi tahun depan, di mana persaingan bisnis semakin ketat di industri perbankan di Indonesia. Dalam menghadapi tantangan di tahun-tahun berikutnya, Bank memiliki rencana untuk mengembangkan portfolio yang kuat dan berbasis kolateral. Sejalan dengan rencana bisnis, Bank, melalui Direksi, melakukan perekrutan RM-RM untuk segmen UKM dengan proses seleksi yang baik untuk mendapatkan RM-RM yang berkualitas. Selain itu, OK! BANK memperkuat pengendalian internal dan manajemen risiko untuk mengantisipasi adanya debitur-debitur yang bermasalah.

Dewan Komisaris menyadari fungsinya sebagai Dewan yang senantiasa memberikan arahan untuk Bank agar tumbuh berdasarkan Tata Kelola Perusahaan yang Baik. OK! BANK mengimplementasikan 3 (tiga) prinsip Tata Kelola Perusahaan yang Baik. Pertama, OK! BANK menerapkan governance structure yang dapat memenuhi dan melengkapi komposisi Direksi sesuai ketentuan dan memperbaharui kebijakan dan prosedur operasional sesuai ketentuan perundang-undangan. Kedua, Bank menerapkan Governance Process yang direalisasikan melalui upaya dari seluruh jenjang organisasi Bank untuk melaksanakan kebijakan dan prosedur yang berlaku. Terakhir, Bank menerapkan Governance Outcome di antaranya menyediakan ketersediaan, kelengkapan, ketepatan waktu serta akurasi data terkait transparansi kondisi keuangan Bank yang disampaikan kepada stakeholders sesuai dengan ketentuan perundang-undangan.

Dalam memandang prospek bisnis Perusahaan di tahun 2019, Dewan Komisaris berpandangan bahwa Bank akan lebih berkembang di tahun 2019, salah satunya disebabkan faktor sinergi yang lebih baik dari merger. Setelah merger, Bank akan lebih mengembangkan banyak produk, khususnya untuk segmen kredit konsumen. Tidak hanya itu, Bank akan terus mengembangkan Bancassurance dan E-Channel, dan mengembangkan portfolio segmen UKM. Di samping itu, OK! BANK memprediksi tidak ada perubahan yang signifikan pada kondisi ekonomi makro di Indonesia pada tahun 2019 tang.

The merger between Bank Dinar and OK! BANK is just around the corner. Since APRO acquired OK! BANK in 2016 with 99% share ownership. OK! BANK successfully entered the BUKU II category and plans to continuously increase its capital to become BUKU III through organic and inorganic methods. This strategic leap is an effort to face future, where business competition is increasingly tight in the banking industry in Indonesia.

In facing challenges in the following years, the Bank has planned to develop a strong and collateral-based portfolio. In line with the business plan, the Bank recruits RMs for the SME segment through strict criteria. In addition, OK! BANK strengthens internal control and risk management to prevent problems with debtors.

The Board of Commissioners realizes its function that provides direction for the Bank to grow based on Good Corporate Governance. OK! BANK implements 3 (three) principles of Good Corporate Governance. Firstly, the Bank implements a governance structure that can meet the requirement of the composition of the Board of Directors in accordance with the provisions and current operational policies as well as procedures based on statutory provisions. Secondly, the Bank implements Governance Process which is actualized through efforts from all levels of the Bank’s organization to implement applicable policies and procedures. Finally, the Bank implements Governance Outcomes, including providing availability, completeness, timeliness and accuracy of data related to the transparency of the Bank’s financial condition that are conveyed to stakeholders in accordance with statutory provisions.

Regarding the Company’s business prospects in 2019, the Board of Commissioners views that the Bank will be more developed in 2019, which is due to the synergy that is much more than merger effect. After the merger, the Bank will develop many products, specifically for the consumer credit segment. Not only that, the Bank will continue developing Bancassurance and E-Channel, and developing the SME segment portfolio. In addition, OK! BANK predicts that there will be no significant changes in macroeconomic condition of Indonesia in 2019.

9Laporan Tahunan 2018 Annual Report

10 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

OK! BANK, berkoordinasi dengan Satuan Kerja Audit Intern (SKAI), melaksanakan Whistle Blowing System (WBS) dan menjamin keharasiaan dari identitas pelapor maupun informasi yang disampaikan. Sebagai upaya dukungan Manajemen/Direksi terhadap WBS, maka informasi yang diperoleh melalui WBS dijamin kerahasiaannya baik dari sisi laporan yang disampaikan maupun identitas pelapor serta tidak akan mempengaruhi Personal Appraisal dari pelapor (penilaian negatif).

Dalam menerapkan strategi pengembangan usaha, Dewan Komisaris menilai bahwa pencapaian Direksi tergolong baik. Hal tersebut dibuktikan dengan pinjaman yang diberikan mencapai 100,5% dari target RBB revisi tahun 2018 dan pencapaian NIM yang lebih besar dari target, yaitu 7,96% dari target 7,62%. Adapun, pencapaian BOPO sedikit lebih tinggi dari target, namun tidak signifikan.

Dewan Komisaris mengapresiasi kinerja Direksi yang diberikan dalam bentuk insentif dan/atau bonus yang diberikan berdasarkan penilaian yang dibuat atas dasar pencapaian KPI. Kinerja Direksi dinilai berdasarkan pencapaian parameter tertentu yang didelegasikan RUPS kepada Dewan Komisaris. Di samping itu, Dewan Komisaris menyarankan Dewan Direksi untuk mempertahankan kinerjanya agar dapat meningkatkan target pencapaian khususnya rasio BOPO dan Dewan Komisaris berharap agar jumlah laba bersih dapat ditingkatkan.

Sebagai kalimat pamungkas, saya, mewakili Dewan Komisaris, menyampaikan terima kasih kepada seluruh nasabah atas kepercayaan dan dukungan selama ini, serta kepada Dewan Direksi dan seluruh karyawan atas kontribusi kepada OK! BANK, dan kami mengucapkan terima kasih kepada pihak regulator Indonesia yang telah menciptakan iklim usaha yang kondusif dan aman.

Jakarta, 22 Maret 2018Atas nama Dewan Komisaris,

Jakarta, March 22, 2018On behalf of the Board of Commissioners,

Moon YoungsoPresiden Komisaris

President Commissioner

MOON YOUNGSOPresiden Komisaris

President Commissioner

OK! BANK, coordinating with the Internal Audit Work Unit (SKAI), implements the Whistle Blowing System (WBS) and guarantees diversity of the identity of the informant or information submitted. As an effort to support Management, the information obtained through the WBS can be well received from the side of the informant submitted and the identity of the informant and also will not negatively affect the Personal Assessment of the informant.

In executing the business development strategy, the Board of Commissioners considers the achievement of the Board of Directors as good. This is evidenced by the given loan reaching 100.5% of the revised RBB target in 2018 and the achievement of the NIM of 7.96% that is greater than the target of 7.62%. Meanwhile, the achievement of BOPO is slightly higher than the target, but not significant.

The Board of Commissioners appreciates the performance of the Board of Directors in the form of incentives and/or bonuses which are given based on the assessments made on the basis of achieving KPI. The performance of the Board of Directors is assessed based on the achievement of certain parameters delegated by the GMS to the Board of Commissioners. In addition, the Board of Commissioners advises the Board of Directors to improve its performance in order to increase achievement targets, especially the BOPO ratio and the Board of Commissioners hopes that the amount of net income can be increased.

In conclusion, I, representing the Board of Commissioners, would like to thank all customers for their trust and support, as well as the Board of Directors and all employees for their contribution to OK! BANK, and we would like to thank the Indonesian regulators for creating a conducive and safe business climate.

11Laporan Tahunan 2018 Annual Report

Halaman ini sengaja dikosongkanThis page is intentionally left blank

12 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

TAHUN 2018 MERUPAKAN TAHUN YANG STABIL DAN

SEDIKIT MENINGKAT BAGI FUNDAMENTAL

PEREKONOMIAN INDONESIA YANG TERCERMIN DARI

INFLASI YANG MASIH RENDAH, SERTA TERCAPAINYA

TARGET PERTUMBUHAN EKONOMI DI INDONESIA.

THE YEAR 2018 SAW A STABLE AND SLIGHTLY

INCREASING YEAR FOR INDONESIA’S ECONOMIC

FUNDAMENTALS, REFLECTED IN LOW INFLATION, AS WELL

AS ACHIEVING ECONOMIC GROWTH TARGETS IN

INDONESIA.

Lim Cheol JinDirektur Utama

President Director

12 Laporan Tahunan 2018 Annual Report

13Laporan Tahunan 2018 Annual Report

LAPORAN DIREKSI REPORT FROM THE BOARD OF DIRECTORS

Terdapat perubahan pada tahun 2018 dibandingkan dengan tahun 2017, di antaranya PDB Indonesia yang meningkat dari 5,1% ke 5,2%, tingkat inflasi yang menurun dari 3,6% menjadi 3,1%, Rupiah yang melemah dari 13.381 menjadi 14.250, suku bunga acuan meningkat dari 4,25% menjadi 6%, hingga tingkat pengangguran yang menurun dari 5,5% menjadi 5,3%.

Walaupun demikian, tingkat persaingan dalam dunia usaha semakin tinggi dikarenakan pemerintah mendukung berkembangnya wiraswasta di Indonesia. Karenanya Bank terus meningkatkan kualitas manajemen risiko khususnya di bidang kredit. Bank juga mewaspadai beberapa segmen industri yang sedang menurun, seperti segmen perusahaan pembiayaan (multifinance). Secara keseluruhan kondisi ekonomi di tahun 2018 yang stabil tidak memberikan dampak signifikan terhadap strategi dan kinerja bisnis OK! BANK.

Dari sisi kinerja operasional, Bank telah menambah SOP guna mengantisipasi adanya error dan/atau fraud. Dalam bidang manajemen risiko dan pengendalian internal, Bank telah melakukan berbagai penguatan seperti pengkajian ulang dan menambah prosedur-prosedur. Karyawan pun semakin meningkatkan kompetensinya dengan pemberian pelatihan dan proses seleksi yang semakin baik.

Sementara dari segi kinerja keuangan, dalam menerapkan strategi pengembangan usaha, Direksi berhasil melakukan pencapaian yang baik. Hal tersebut dibuktikan dengan pinjaman yang diberikan mencapai 100,5% dari target RBB revisi tahun 2018 dan pencapaian NIM yang lebih besar dari target, yaitu 7,96% dari target 7,62%. Adapun, pencapaian BOPO sedikit lebih tinggi dari target, namun tidak signifikan.

Sepanjang 2018, OK! BANK berupaya merekrut RM-RM untuk segmen UKM dengan proses seleksi yang baik untuk mendapatkan RM-RM yang berkualitas. Tidak hanya itu, OK! BANK juga melakukan penguatan pada pengendalian internal dan manajemen risiko guna mengantisipasi adanya debitur-debitur yang bermasalah dikarenakan kondisi industri yang menurun khususnya pada industri perusahaan pembiayaan (multifinance).

Setiap tahun berjalan, tentu akan selalu ada tantangan yang harus dihadapi. Direksi melihat bahwa tantangan OK! BANK di 2018 adalah bagaimana Bank dapat mencapai target yang telah ditetapkan, yaitu mengembangkan penyaluran kredit dengan kualitas yang baik dan meningkatkan profitabilitas di mana salah satu kendala yang ada adalah cukup tingginya kredit bermasalah. OK! BANK berkomitmen melanjutkan fokus utama OK! BANK tahun 2018 sampai dengan 2022 dengan melakukan penguatan aset secara berkesinambungan, mengembangkan infrastruktur secara berkelanjutan dan meningkatkan manajemen risiko.

There was a change in 2018 compared to 2017, including Indonesia’s GDP which increased from 5.1% to 5.2%, the inflation rate down from 3.6% to 3.1%, the weakening Rupiah from 13,381 to 14,250, the benchmark interest rate increasing from 4.25% to 6%, and the unemployment rate decreasing from 5.5% to 5.3%.

Nevertheless, the level of competition in the business world is increasingly high because the government supports the development of entrepreneurs in Indonesia. Therefore, the Bank continues improving the quality of risk management, especially in the credit sector. The Bank is also wary of several declining industrial segments, such as the multi-finance company segments. Overall, the stable economic conditions in 2018 did not have a significant impact on OK! BANK’s strategy and business performance.

In terms of operational performance, the Bank has added SOPs to anticipate errors and/or fraud. In the field of risk management and internal control, the Bank has conducted various strengthening activities such as reviewing and adding procedures. Employees increasingly improve their competence by providing training as well as having a better selection process.

In terms of financial performance, moreover, as the implementation of the business development strategy, the Board of Directors managed to score good achievements. This is evidenced by the loan reaching 100.5% of the revised Bank Business Plan target in 2018 and the achievement of the NIM, which was 7.96% of the target set for 7.62%. Meanwhile, the achievement of BOPO was not that significant, yet slightly higher than the target.

Throughout 2018, OK! BANK sought to recruit RM-RM for the SME segment with a good selection process to obtain a quality RM-RM. By the same token, OK! BANK also strengthens internal control and risk management in anticipation of troubled debtors due to declining industry conditions, especially in the finance company industry.

Every year, of course there will always be challenges that must be faced. The Board of Directors sees that the OK! BANK’s challenge in 2018 was how the Bank could achieve the set targets, that is developing credit with good quality and increasing profitability, where one of the obstacles was the high level of non-performing loans. OK! BANK is committed to continue the Bank’s main focus in 2018-2022. This can be done by continuing to strengthen assets, develop infrastructure in a sustainable manner and improve risk management.

13Laporan Tahunan 2018 Annual Report

14 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

Jika dibandingkan dengan target yang dicanangkan pada 2018, Direksi menilai tidak ada capaian yang secara signifikan di bawah atau melampaui target.

Direksi menyadari bahwa implementasi Tata Kelola Perusahaan yang Baik berperan krusial bagi kelangsungan bisnis Bank. Dengan demikian, OK! BANK mengimplementasikan 3 (tiga) prinsip Tata Kelola Perusahaan yang Baik. Pertama, OK! BANK menerapkan governance structure yang dapat memenuhi dan melengkapi komposisi Direksi sesuai ketentuan dan memperbaharui kebijakan dan prosedur operasional sesuai ketentuan perundang-undangan. Kedua, Bank menerapkan Governance Process yang direalisasikan melalui upaya dari seluruh jenjang organisasi Bank untuk melaksanakan kebijakan dan prosedur yang berlaku. Terakhir, Bank menerapkan Governance Outcome di antaranya menyediakan ketersediaan, kelengkapan, dan ketepatan waktu serta akurasi data terkait transparansi kondisi keuangan Bank yang disampaikan kepada stakeholders sesuai dengan ketentuan perundang-undangan.

Dari segi pengembangan Sumber Daya Manusia, OK! BANK telah melakukan rekrutmen tenaga profesional untuk mengisi kebutuhan pemenuhan posisi-posisi untuk mencapai visi, misi objektif dan strategi Perusahaan. Bank juga melakukan penysuaian terhadap struktur organisasi secara terus menerus sesuai dengan kebutuhan dan perkembangan bisnis Bank. Sampai dengan Triwulan IV/2018 Bank telah menyelenggarakan program pelatihan secara In-house dan mengikutsertakan pegawai dalam berbagai pelatihan. Rasio biaya pendidikan dan pelatihan sampai dengan Triwulan IV 2018 adalah 2.90% (Biaya Training Rp1.712.485.350, dan Biaya Tenaga Kerja Rp59.070.839.546). Tidak hanya tenaga kerja domestik, OK! BANK juga merekrut tenaga alih daya sebanyak 39 (tiga puluh sembilan) orang untuk membantu pengembangan Bank.

OK! BANK sangat memperhatikan fungsi Teknologi Informasi yang berperan vital dalam kelangsungan bisnis Bank. Maka dari itu, sepanjang tahun 2018, OK! BANK telah melakukan optimalisasi penggunaan sistem Core Banking baru (Inoan) dan juga terus menambah fitur dan memperbaharui sistem tersebut. Bank juga telah mulai melakukan pengembangan E-Channel di tahun 2018 khususnya untuk ATM dan kartu debit.

Tidak hanya berkomitmen pada pembangunan perekonomian di Indonesia, OK! BANK menilai komitmen di bidang kegiatan sosial penting untuk dilakukan sebagai bentuk kontribusi kepada lingkungan sekitar Perusahaan. OK! BANK telah mewujudkan tanggung jawab sosial, di antaranya dengan memberikan bantuan sebesar Rp1 miliar untuk membantu pemulihan pasca bencana di Donggala, Sigi dan Palu, mengadakan acara sosial bersama Yayasan Anak Yatim Piatu Putra Nusa Benhil dengan tema “Berbagi dengan Sesama, Mencari Berkah Allah SWT di Bulan Ramadhan”, dan menyelenggarakan kegiatan Literasi dan Inklusi keuangan bersama BPR Pesisir Akbar di Bima-Dompu, Fase IV, tahun 2018, pembiayaan Rp20 miliar, terdiri dari 980 petani, dan luas lahan 2.000 Ha.

OK! BANK melihat prospek di tahun 2019 masih akan tetap terbuka. Namun, di tahun pesta politik, terdapat kemungkinan terjadi ketidakstabilan yang menyebabkan penurunan kualitas

When compared with the target set out in 2018, the Board of Directors considers that there are no achievements that are significantly below or exceed the target.

The Board of Directors realizes that the implementation of Good Corporate Governance plays a crucial role in the Bank’s business continuity. Thus, OK! BANK implements 3 (three) principles of Good Corporate Governance. First, OK! BANK implements a governance structure that can meet and complete the composition of the Board of Directors in accordance with the provisions and update operational policies and procedures in accordance with statutory provisions. Second, the Bank implements Governance Process which is realized through efforts from all levels of the Bank’s organization to implement applicable policies and procedures. Finally, the Bank implements Governance Outcomes, including providing availability, completeness, timeliness and accuracy of data related to the transparency of the Bank’s financial condition that is conveyed to stakeholders in accordance with statutory provisions.

As for the Human Resource development, OK! BANK has recruited professionals to fulfill the positions needed to achieve the Company’s vision, mission and strategy. The Bank also continuously manages the organizational structure in accordance with the needs and development of the Bank’s business. Up to Quarter IV/2018, the Bank has conducted in-house training programs and included employees in various trainings. The ratio of the cost of education and training up to Quarter IV of 2018 was 2.90% (Training Fee of Rp1,712,485,350 and Labor Costs Rp59,070,839,546). Not only domestic workers, OK! BANK also recruits labor outsourcing as many as 39 (thirty-nine) people to assist the Bank’s development.

OK! BANK is very concerned about the Information Technology function which plays a vital role in the Bank’s business continuity. Therefore, throughout 2018, OK! BANK optimized the use of the new Core Banking system (Inoan), continued adding features and updating the system. The bank also began to develop E-Channels in 2018 especially for ATMs and debit cards.

Not only is it committed to economic development in Indonesia, OK! BANK considers that commitment in the field of social activities is important to do as a contribution to the environment around the company. OK! BANK has embodied social responsibility, including providing assistance with the total of Rp1 billion to help post-disaster recovery in Donggala, Sigi and Palu, organizing social event with Putra Nusa Benhil Orphans Foundation with the theme “Sharing with Others, Seeking God’s Blessings in Ramadhan ”, and organizing financial Literacy and Inclusion activities with the BPR Pesisir Akbar in Bima-Dompu, Phase IV, 2018, financing Rp20 billion, consisting of 980 farmers, and 2,000 hectares of land area.

OK! BANK sees the prospects for 2019 will remain open. However, in the year of a political party, there is a possibility of instability which causes a decrease in credit quality and liquidity in the

15Laporan Tahunan 2018 Annual Report

Jakarta, 22 Maret 2018Atas nama Direksi,

Jakarta, March 22, 2018On behalf of the Board of Directors,

Lim Cheol Jin Direktur Utama

President Director

kredit dan likuiditas di pasar. Selain itu, OK! BANK akan tetap berfokus pada objektif, yaitu memperbesar portfolio kredit dengan seleksi yang ketat sehingga memperoleh kualitas yang baik.

Direksi berharap dapat terjadi sinergi yang baik yang akan terjadi pada kuartal II 2019 pasca merger. Dengan tambahan modal dari APRO, Direksi meyakini bahwa OK! BANK akan terus tumbuh. Tidak hanya itu, Di tahun 2019, Bank menargetkan pertumbuhan kredit sebesar 39.34% dibandingkan posisi akhir tahun 2018. Oleh karena itu, kami optimis bahwa akan ada peningkatan yang cukup baik dibandingkan dengan tahun 2018.

Sebagai penutup, Saya, atas nama Direksi dan manajemen OK! BANK, ingin memberikan apresiasi yang sebesar-besarnya kepada seluruh pemangku kepentingan (stakeholders), khususnya pada nasabah-nasabah yang sudah memberikan kepercayaan kepada OK! BANK, para karyawan yang telah bekerja baik di tahun 2018, dan kepada seluruh pemangku kepentingan lainnya yang berkontribusi untuk kemajuan OK! BANK. Saya berharap semua pihak dapat terus mempertahankan kepercayaan dan semakin meningkatkan prestasinya.

market. In addition, OK! BANK will remain focused on the objective, namely enlarging the credit portfolio with strict selection to obtain good quality.

The Board of Directors hopes that a good synergy will occur in the second quarter of 2019 after the merger. With additional capital from APRO, the Board of Directors believes that OK! BANK will continue to grow. Moreover, in 2019, the Bank targets credit growth of 39.34% compared to the position in the end of 2018. Therefore, we are optimistic that there will be a fairly good increase compared to 2018.

In conclusion, I, on behalf of the OK! BANK Directors and management, would like to give highest appreciation to all stakeholders, especially those who have given confidence to OK! BANK, employees who have worked well in 2018, and to all other stakeholders who contribute to the progress of OK! BANK. I hope all parties can continue to maintain their trust and further enhance their achievements.

Profil PerusahaanCompanyProfile

18 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

SEKILAS BANK OKE INDONESIABANK OKE INDONESIA IN BRIEF

19Laporan Tahunan 2018 Annual Report

Didirikan pada tahun 1980 dengan nama Maskapai Andil Indonesia Bank Pasar Seri Partha. Pada tahun 1989 memperoleh izin sebagai bank umum dan pada tahun 1997 berubah nama menjadi PT Bank Sri Partha yang berfokus pada pembiayaan bagi UMKM yang berada di Bali. Setelah diakuisisi oleh sekelompok pemegang saham yang memiliki reputasi internasional, baik di bidang sosial maupun perbankan, pada tahun 2009 bulan April tanggal 20 berubah nama menjadi Bank Andara setelah mendapat persetujuan dari Bank Indonesia.

Para pemegang saham memiliki beberapa kesamaan yang signifikan yang mendasari seluruh kegiatan usaha Bank dan perhatian terhadap pengembangan sektor ekonomi mikro di Indonesia. Saat itu, pemegang saham Bank Andara terdiri dari Mercy Corps (pemegang saham pengendali), DWM Fund S.C.A-SICAV SIF, International Finance Corporation (IFC), KfW, Hivos-Triodos Fund, dan I Wayan Gatha.

Pada tanggal 18 November 2016, Bank Andara beserta APRO Financial Co. sepakat untuk menandatangani akta akuisisi yang pada akhirnya menandai telah efektifnya akuisisi oleh APRO Financial Co. Ltd. Transaksi akuisisi Bank Andara dilakukan melalui pembelian saham baru Bank Andara sebesar 40% (empat puluh persen) dengan nilai pembelian Rp450miliar. APRO Financial Co. Ltd merupakan institusi keuangan besar dari Korea Selatan yang baru pertama kali berinvestasi di Indonesia. Minat yang tinggi dari investor inilah yang membuat APRO Financial Co. Ltd tertarik untuk melakukan investasi di Bank Andara.

Setahun setelah akuisisi Bank Andara oleh APRO Financial Co. Ltd tepatnya di bulan Mei 2017, APRO membeli sisa saham (saat ini menjadi 99%) yang dimiliki oleh para pemegang saham dari berbagai institusi tersebut dan menyisakan 1 pemegang saham lokal, yaitu I Wayan Gatha. Pada bulan Agustus 2017, nama Bank Andara resmi berubah menjadi Bank Oke Indonesia dan telah disetujui oleh Otoritas Jasa Keuangan.

The Company was founded in 1980 under the name Maskapai Andil Indonesia Bank Pasar Seri Partha. In 1989, it obtained a license as a commercial bank and in 1997, changed its name to PT Bank Sri Partha focusing on financing for MSMEs in Bali. On April 20, 2009, the Company changed its name to Bank Andara upon the approval from Bank Indonesia and after being acquired by a group of shareholders with international reputations, both in the social and banking fields.

The shareholders at that time shared significant common ground that served as foundations for the Bank’s business, and were aware of the development of the microeconomic sectors in Indonesia. At that time, Bank Andara shareholders comprised Mercy Corps (controlling shareholder), DWM Fund S.C.A-SICAV SIF, International Finance Corporation (IFC), KfW, Hivos-Triodos Fonds, and I Wayan Gatha.

On November 18, 2016, Bank Andara and APRO Financial Co. agreed to sign an acquisition deed which ultimately marked the effective acquisition of APRO Financial Co. Ltd. Bank Andara’s acquisition transaction was done through the purchase of Bank Andara’s 40% (forty percent) new shares with a purchase value of Rp450 billion. APRO Financial Co. Ltd is a large financial institution from South Korea that invested for the first time in Indonesia. This high interest from investors is what makes APRO Financial Co. Ltd interested in investing in Bank Andara.

A year after the acquisition of Bank Andara by APRO Financial Co. Ltd in May 2017, APRO purchased the remaining shares (bringing its current holdings to 99%) owned by shareholders of these institutions, leaving 1 local shareholder, who is I Wayan Gatha. In August 2017, the name of Bank Andara officially changed to Oke Bank Indonesia with approval of the Financial Services Authority.

20 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

PERISTIWA PENTING DI TAHUN 2018IMPORTANT EVENTS IN 2019

LITERASI DAN INKLUSI KEUANGAN

MSME CREDIT ANALYSIS TRAINING FOR RURAL BANKS IN BALI

CARES 80 ORPHANS CHILDREN’S IN THE MONTH OF RAMADHAN

OK! BANK CELEBRATES FIRST BIRTHDAY

APRO SERVICE GROUP AND BANK OKE INDONESIA CARE ABOUT EARTHQUAKES AND TSUNAMIS IN DONGGALA, SIGI AND PALU

PELATIHAN ANALISA KREDIT UMKM BAGI BPR SE-PROVINSI BALI

FINANCING LITERACY AND INCLUSION

PEDULI 80 ANAK YATIM PIATU DI BULAN RAMADHAN

OK! BANK RAYAKAN ULANG TAHUN PERTAMA

APRO SERVICE GROUP DAN BANK OKE INDONESIA PEDULI BENCANA GEMPA BUMI DAN TSUNAMI DI DONGGALA, SIGI DAN PALU

• Pada tanggal 19-20 Februari 2018 OK! BANK bersama BPR Pesisir Akbar di Bima-Dompu melakukan kegiatan Literasi dan Inklusi Keuangan, di samping itu juga melakukan evaluasi dan monitoring fase 4 pada proyek pertanian jagung.

• Atas prakarsa dari PERBARINDO Bali Bank Oke Indonesia Cabang Denpasar mendapat kesempatan memberikan Pelatihan Analisa Kredit UMKM bagi BPR se-provinsi Bali pada 13 April 2018 di Denpasar.

• Tanggal 23-30 Mei 2018 tahun Islam 1439 H, Bank Oke Indonesia dari Kantor Pusat, cabang Jakarta, Semarang, Surabaya, dan Denpasar mengadakan acara sosial bersama Anak Yatim Piatu dengan tema “Berbagi dengan Sesama, Mencari Berkah Allah SWT di Bulan Ramadhan”.

• Bank Oke Indonesia (OK! BANK) merayakan puncak acara ulang tahun pertama berbarengan dengan penutupan Asian Games 2018 di Gelora Bung Karno pada 2 September 2018. Acara ulang tahun ini dihadiri oleh seluruh karyawan OK! BANK beserta jajaran direksi dan pemegang saham Utama yaitu APRO Service Group.

• APRO Service Group bersama Bank Oke Indonesia (OK! BANK) pada 18 Oktober 2018 memberikan bantuan sebesar Rp1 miliar melalui Palang Merah Indonesia. Penyerahan bantuan ini diberikan langsung oleh Choi Yoon, Chairman APRO Service Group dan Lim Cheol Jin, CEO Bank Oke Indonesia dan diterima langsung oleh Sekretaris Jenderal PMI, dr. Ritola Tasmaya, M.P.H.

• On February 19-20, 2018, OK! BANK along with BPR Pesisir Akbar in Bima-Dompu, conducted financing literacy and inclusion and conducted evaluation and monitoring on corn farming project phase 4.

• On the initiative of PERBARINDO Bali, Bank Oke Indonesia Denpasar Branch had the opportunity to provide MSME Credit Analysis Training in Denpasar for all Rural Banks in the province of Bali on April 13, 2018.

• On May 23-30 2018 Islamic year 1439 H, Bank Oke Indonesia Head Office, along with Jakarta, Semarang, Surabaya, and Denpasar branches held a social event with Orphans with the theme “Sharing with Others, Seeking God’s Blessings in the Month of Ramadan”.

• Bank Oke Indonesia (OK! Bank) celebrated the peak of its first anniversary event in conjunction with the closing of the 2018 Asian Games at Bung Karno Stadium on September 2, 2018. This anniversary event was attended by all employees of OK! Bank along with the board of directors and Major shareholders, namely APRO Service Group.

• On October 18, 2018, APRO Service Group with Bank Oke Indonesia (OK! BANK) provided assistance of Rp1 billion through the Indonesian Red Cross. The assistance was handed over directly by Choi Yoon, Chairman of APRO Service Group and Lim Cheol Jin, CEO of Bank Oke Indonesia and received directly by the Secretary General of PMI, dr. Ritola Tasmaya, M.P.H.

21Laporan Tahunan 2018 Annual Report

JEJAK LANGKAHMILESTONES

2018 2017

• Pada 14 Agustus Bank Oke Indonesia mendapatkan penghargaan dengan predikat “SANGAT BAGUS” dari INFOBANK untuk kinerja keuangan di tahun 2017.

On August 14 Bank Oke Indonesia was awarded with the title “VERY GOOD” from INFOBANK for financial performance in 2017.

• Pada 18 Oktober 2018, APRO SERVICE GROUP bersama BANK OKE INDONESIA memberikan bantuan sebesar Rp1 miliar untuk membantu operasional pemulihan pasca bencana Tsunami di Donggala, Sigi, dan Palu.

On October 18, 2018, APRO SERVICE GROUP and BANK OKE INDONESIA provided assistance with total of Rp1 billion to assist in the operational recovery after the Tsunami disaster in Donggala, Sigi and Palu.

• Pada tanggal 6 hingga 8 Januari Bank Andara melakukan bekerjasama bersama Mercy Corps dan Syngenta dan mengadakan kegiatan Literasi keuangan di beberapa wilayah yang menjadi program Pembiayaan Jagung di Kabupaten Dompu, Bima.

On January 6-8, Bank Andara cooperated with Mercy Corps and Syngenta to conduct financial Literacy activities in several areas that became part of the program of Maize Financing in Dompu Regency, Bima.

• Pada bulan Mei, APRO Financial Co. Ltd membeli sisa saham dan total kepemilikan saham menjadi 99%.

In May, APRO Financial Co. Ltd buys the remaining shares and the total shareholding becomes 99%.

• Bank Andara, pada tanggal 24 Agustus, secara resmi berubah nama menjadi Bank Oke Indonesia setelah mendapat persetujuan dari Otoritas Jasa Keuangan (OJK).

Bank Andara on August 24 officially changed its name to Bank Oke Indonesia after obtaining approval from the Financial Services Authority (OJK).

• Pada tanggal 4 September, Bank Oke Indonesia melakukan perubahan Core Banking System dari TEMENOS ke INOAN (Inovasi Keuangan).

On September 4, Bank Oke Indonesia made a change of Core Banking System from TEMENOS to INOAN (Financial Innovation).

• Pada tanggal 4 September, Bank Oke Indonesia melakukan perubahan Core Banking System dari TEMENOS ke INOAN (Inovasi Keuangan).

On September 4, Bank Oke Indonesia made a change of Core Banking System from TEMENOS to INOAN (Financial Innovation).

• Bank Oke Indonesia cabang Denpasar mengadakan Kegiatan CSR dengan melakukan penyaluran bantuan bagi pengungsi Gunung Agung, pada tanggal 20 Desember.

Bank Oke Indonesia Denpasar branch held CSR activities by distributing aid for Gunung Agung refugees on December 20.

22 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

2016

• Penandatanganan Letter of Intent antara SAFIRA (Strengthening Agricultural Finance in Rural Areas) Project dan Bank Andara dalam Kerjasama Pendampingan Teknis untuk memperkuat institusi keuangan mikro (BPR) dalam mendukung sektor pertanian

The signing of the Letter of Intent between SAFIRA (Strengthening Agricultural Finance in Rural Areas) Project and Bank Andara in Technical Assistance Cooperation to strengthen microfinance institutions (BPR) in support of the agricultural sector.

• Pada tahun ini, Bank Andara mulai menyalurkan Pembiayaan segmen SME; dan sejak bulan Juli Bank telah berhasil membukukan laba.

In this year Bank Andara began to channeling SME segment Financing; and as of July, the Bank successfully booked its profit.

• Pada tanggal 26 Agustus, Bank Andara menjalin kerjasama dengan Asosiasi BPR Siaga Bencana (ABSIGAB). Bank Andara bertanggung jawab sebagai Bank Penampung dana (pooling of funds) yang bersumber dari simpanan anggota ABSIGAB dan lembaga keuangan dan/atau donor lainnya yang berkomitmen dalam program ILFAD (Indonesia Liquidity Facility After Disaster) di 11 provinsi yaitu; Aceh, Sumatera Utara, Sumatera Barat, Jakarta, Jawa Barat, Jawa Tengah, Yogyakarta, Jawa Timur, Nusa Tenggara Barat, Nusa Tenggara Timur, dan Maluku.

On August 26, Bank Andara signed an agreement with the Association of Disaster Preparedness (ABSIGAB). Bank Andara is responsible as the holder of Bank funds (pooling of funds) originating from ABSIGAB members’ savings and financial institutions and/or other donors who are committed to the ILFAD (Indonesia Liquidity Facility After Disaster) program in 11 provinces namely; Aceh, North Sumatera, West Sumatera, Jakarta, West Java, Central Java, Yogyakarta, East Java, West Nusa Tenggara, East Nusa Tenggara and Maluku.

• Bank Andara berupaya untuk terus berkomitmen menindaklanjuti program Financial Ecosystem untuk pembiayaan petani Jagung yang perdana dilakukan pada tahun 2014. Bank Andara bersama Mercy Corps Indonesia, BPR Pesisir Akbar dan PT Syngenta Indonesia berkolaborasi dengan stakeholder lain dalam pembiayaan rantai nilai (Value Chain Financing) kepada petani jagung di NTB ini yaitu PT Asuransi Central Asia untuk melindungi risiko akibat cuaca (puting beliung dan kekeringan) serta PT 8Villages Indonesia sebagai penyedia aplikasi kumpul data dan aplikasi sms petani. Sejak diluncurkannya program ini di tahun 2014, terjadi peningkatan jumlah petani dari 198 petani di tahun 2014 menjadi 640 petani di tahun 2015 dan 805 petani di tahun 2016. Wilayah jangkauan programpun meluas dari hanya 5 Kecamatan di Kabupaten Bima dan Kabupaten Dompu meluas sampai total 14 Kecamatan di Kabupaten Bima, Kabupaten Dompu, Kabupaten Sumbawa dan Kota Bima. Selama periode tersebut Bank Andara telah mengucurkan pembiayaan sebesar Rp3,2 miliar di tahun 2014, Rp9,6 miliar di tahun 2015 dan Rp12,5 miliar di tahun 2016 melalui BPR Pesisir Akbar.

Bank Andara is committed to continuing the Financial Ecosystem Program to finance maize farmers which began in 2014. Bank Andara, together with Mercy Corps Indonesia, BPR Pesisir Akbar and PT Syngenta Indonesia, collaborated with other stakeholders in this model of Value Chain Financing to maize farmers in NTB, namely PT Asuransi Central Asia to cover the risks from weather (cyclones and drought) and PT 8villages Indonesia as a provider of application programs for gathering data and applications for short message services to the farmers. Since the program’s launch in 2014, the number of farmers financed increased from 198 farmers in 2014 to 640 farmers in 2015 and 805 farmers in 2016. The area served in this program has grown from five districts in Bima and Dompu extends up to a total of 14 districts in Bima, Dompu, Sumbawa and Bima City. During this period, Bank Andara has disbursed financing of Rp3.2 billion in 2014, Rp9.6 billion in 2015 and Rp12.5 billion in 2016 through the BPR Pesisir Akbar.

• Pada tanggal 18 November 2016, Bank Andara dan APRO Financial Co. Ltd telah menyetujui penandatanganan akta akuisisi yang menandai telah efektifnya akuisisi oleh APRO Financial Co. Ltd.

On November 18, 2016, Bank Andara and APRO Financial Co. Ltd. signed a deed of acquisition to mark the effective acquisition by APRO Financial Co. Ltd.

23Laporan Tahunan 2018 Annual Report

• Bank Andara dan MercyCorps melakukan kunjungan kerja dalam rangka meninjau serapan dana Rp3,2 miliar yang telah disalurkan melalui BPR Pesisir Akbar untuk program pembiayaan tanaman jagung kepada 400 orang petani di Kabupaten Bima dan Dompu, Nusa Tenggara Barat.

Bank Andara and Mercy Corps conducted an official visit in order to review loans of Rp3.2 billion that have been disbursed through the BPR Pesisir Akbar for corn crop financing program to 400 farmers in the district of Bima and Dompu, West Nusa Tenggara.

• Bank Andara menyelenggarakan program kegiatan ‘AndaraSmart - Goes to Korea’ pada tanggal 23-27 Februari 2015 ke Seoul, Korea Selatan. Sebanyak 18 peserta dari pimpinan/pejabat BPR (Bank Perkreditan Rakyat) dan Koperasi mengikuti kegiatan tersebut dan mendapatkan kesempatan berupa pelatihan dari program AndaraSmart, program spesial dari Bank Andara untuk produk tabungan, deposito, dan giro.

Bank Andara conducted ‘AndaraSmart - Goes to Korea’ event program on February 23-27, 2015 to Seoul, South Korea. As many as participants consisting of 18 heads/officials of Rural Banks (BPR) and Cooperatives who received training from AndaraSmart program, a special program from Bank Andara for savings, fund deposits and current accounts.

• Program yang diselenggarakan oleh Literasi Keuangan didukung oleh Bank Andara seperti yang disampaikan oleh Otoritas Jasa Keungan (OJK) supaya pemanfaatkan layanan keuangan oleh masyarakat yang masih sangat minim dapat ditingkatkan lagi, salah satunya dengan memberikan edukasi kepada masyarakat. Literasi keuangan dilakukan Cabang Bank Andara Jakarta, Semarang, Surabaya, dan Denpasar.

The program organized by Financial Literacy was supported by Bank Andara as stated by the Financial Services Authority (OJK) so that the use of financial services by the community which is still very minimal can be increased again, one of which is by providing education to the public. Financial literacy is carried out by Bank Andara Jakarta, Semarang, Surabaya and Denpasar.

2015

• Bank Andara menjalin kerjasama dengan Aditama Finance yang merupakan perusahaan yang berpengalaman dalam sewa pembiayaan (finance lease) dan anjak piutang (factoring).

Bank Andara signed an agreement with Aditama Finance, a company experienced in financial leasing and factoring.

• Rencana penambahan modal Bank Andara oleh APRO, selesai pada November 2016.

Capital injection process for Bank Andara by APRO, completed November 2016.

• Sementara itu, volume transaksi Andaralink meningkat mencapai lebih dari 200.000 transaksi per bulan atau peningkatan lebih dari 140% dari awal tahun 2015 dan device, dari 112 di 2014 menjadi 232 di 2015.

Meanwhile, Andaralink’s transaction volume increased to more than 200,000 transactions per month or an increase of more than 140% from the beginning of 2015 and devices, from 112 in 2014 to 232 in 2015.

24 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

• Bank Andara bekerja sama dengan BNI dalam memperkenalkan pengiriman uang dari luar negeri melalui fasilitas BNI Wesel PIN sebagai bagian dari layanan AndaraLink.

Bank Andara collaborated with BNI in introducing remittances from abroad through the BNI Wesel PIN facility as part of AndaraLink services.

• Di tahun ini, Bank Andara membuka kantor cabang baru di Jakarta. Pembukaan cabang ini juga merupakan komitmen Bank untuk menjangkau dan melayani nasabah dan masyarakat lebih cepat dan lebih baik, serta sebagai bagian dari strategi untuk meningkatkan penetrasi pasar Bank

In this year, Bank Andara opened a new branch in Jakarta. The opening of the branch was also part of the Bank’s commitment to reach and serve customers and the community faster and better, and as part of a strategy to increase the Bank’s market penetration,

• Bekerja sama dengan Lembaga Keuangan Mikro (LKM), Bank Andara mengadakan program AndaraLink Roadshow di beberapa daerah di Sulawesi Selatan yaitu: Sengkang, Belopa, Palopo, Masamba, Sidrap, Shiva, dan Attapange.

In collaboration with Microfinance Institution (LKM), Bank Andara held the AndaraLink Roadshow program in several areas in South Sulawesi, namely: Sengkang, Belopa, Palopo, Masamba, Sidrap, Shiva, and Attapange.

• Bank Andara meluncurkan program linkage dengan BPR melalui program pembiayaan bersama yaitu Andara Pembiayaan Bersama, untuk lebih mengembangkan produk kredit dan meningkatkan pinjaman kepada usaha mikro, kecil, dan menengah (UMKM).

Bank Andara launched a linkage program with BPRs through a joint financing program, namely Andara Pembiayaan Bersama, to further develop credit products and increase lending to micro, small, and medium enterprises (MSMEs).

2014

• Bank Andara beserta Mercy Corps Indonesia dan Syngenta Indonesia mengimplementasikan model pembiayaan terintegrasi “Financial Eco-System” dengan program perdana memberikan pembiayaan untuk pengembangan tanaman jagung di Kabupaten Bima dan Dompu, Nusa Tenggara Barat.

Bank Andara with Mercy Corps Indonesia and Syngenta Indonesia implemented an integrated financing model “Financial Eco-System” with a pilot program to provide funds for the cultivation of corn crop in Bima and Dompu, West Nusa Tenggara.

25Laporan Tahunan 2018 Annual Report

• Bank Andara membuka dua kantor cabang di Semarang dan Surabaya yang merupakan bentuk komitmen dalam memperluas jangkauan layanan kepada mitra dan calon mitra.

Bank Andara opened two branches in Semarang and Surabaya, representing the Bank’s commitment to expanding its service and outreach to partners as well as potential partners.

• Untuk kedua kalinya, Bank Andara memperoleh fasilitas pinjaman dari Standard Chartered Bank Indonesia. Fasilitas pinjaman kali ini berjumlah Rp57 miliar yang digunakan untuk memperkuat pendanaan Bank dalam membiayai sektor keuangan mikro.

For the second time, Bank Andara received a loan facility from Standard Chartered Bank Indonesia. The Rp57 billion loan increased the Bank’s funding capacity to finance micro finance sector.

• Bank juga menandatangani Kerjasama Pemberian Fasilitas Kredit secara Terintegrasi dengan PT Bahana Artha Ventura (BAV). Melalui kerjasama ini Bank bersinergi dengan perusahaan modal ventura yang terafiliasi dengan BAV dalam memberikan fasilitas yang dibutuhkan.

The Bank signed an Integrated Loan Facility Agreement with PT Bahana Artha Ventura (BAV). Through this agreement the Bank established a synergy with BAV-affiliated venture capital companies to facilitate lending.

2013 2012

• Relokasi kantor pusat dari Denpasar ke Jakarta. Bank Andara meraih keuntungan bulanan untuk pertama kalinya di bulan Juli.

Relocation of the Bank’s headquarters from Denpasar to Jakarta. The Bank booked its first monthly profit in July.

26 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

• DWM bergabung sebagai pemegang saham Bank dengan kepemilikan sebesar 17,89%.

DWM became the Bank’s shareholder with 17.89% ownership.

• Peluncuran layanan AndaraLink.

AndaraLink was launched.

2011

• Bank menandatangani perjanjian implementasi ABB dengan Perbarindo Jakarta dan perjanjian penjaminan pinjaman dengan USAID.

The Bank signed the ABB Implementation Agreement with Perbarindo Jakarta and a loan guarantee agreement with USAID.

• KfW bergabung menjadi pemegang saham Bank dengan kepemilikan sebesar 13,73%.

KfW became the Bank’s shareholder with 13.73% ownership.

2010

27Laporan Tahunan 2018 Annual Report

2009

• Bank mengalami perubahan nama menjadi PT Bank Andara pada awal tahun 2009, dan memulai kegiatan operasionalnya secara penuh dengan fokus pada bisnis baru (wholesale banking) pada bulan April 2009, dengan 88 LKM menjadi debitur di tahun pertama di mana 37 di antaranya fokus pada pengentasan kemiskinan.

The Bank changed its name to Bank Andara and commenced its full operation as a wholesale bank in April 2009. During its first year of operation, the Bank successfully acquired 88 MFI borrowers, 37 of whom focused on poverty eradication.

• Bank memberikan fasilitas pemeringkatan eksternal secara gratis bagi 38 LKM bekerjasama dengan Microfinance Innovation Center for Resources and Alternatives (MICRA) serta melakukan riset pengembangan infrastruktur kerangka teknologi yang dibiayai Bill & Melinda Gates Foundation melalui hibah kepada program MAXIS dari Mercy Corps.

In collaboration with Microfinance Innovation Center for Resources and Alternatives (MICRA), the Bank facilitated free external rating service for 38 MFIs. The Bank also conducted research on the development of technology infrastructure platforms to help MFIs. This research was funded by Bill & Melinda Gates Foundation through a grant extended to Mercy Corps’ MAXIS program.

• Bank mempelopori program manajemen likuiditas secara kolektif (pooled liquidity management) dengan LKM, yang dikenal dengan nama Andara Bersama BPR (ABB). Bank juga menandatangani Nota Kesepahaman dengan Perhimpunan Bank Perkreditan Rakyat Indonesia (Perbarindo) daerah Bali untuk pembentukan ABB Bali.

Bank pioneered a pooled liquidity management program for MFIs known as Andara Bersama BPR (ABB). The Bank also signed a Memorandum of Understanding with Perhimpunan Bank Perkreditan Rakyat Indonesia (Perbarindo/ Indonesian Association of Rural Banks) of Bali region, to establish ABB Bali.

2008

• Mercy Corps, IFC, HTF, dan Catholic Organization for Relief and Development Aid (Cordaid) mengakuisisi Bank Sri Partha yang berkantor pusat di Bali.

Mercy Corps, IFC, HTF, and Catholic Organization for Relief and Development Aid (Cordaid) acquired Bank Sri Partha, headquartered in Bali, Indonesia.

28 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

28 Laporan Tahunan 2018 Annual Report

VISI & MISIVISION & MISSION

VISIVISION Untuk menjadi bank terbaik dalam mengutamakan keunggulan layanan.

To be the best bank in prioritizing service excellence

MISIMISSION Untuk memberikan kepercayaan dan kepuasan kepada nasabah serta berkontribusi bagi masyarakat dengan layanan terbaik.

To provide trust and satisfaction to costumers and contribute to society with the best service.

Creating Growth through Transformation

29Laporan Tahunan 2018 Annual Report

NILAI-NILAI DASARCORE VALUES

BUDAYA KERJA YANG BERORIENTASI PADA KEUNTUNGAN A PROFIT-ORIENTED WORKING CULTURE

PELAYANAN PELANGGAN ADALAH PRIORITAS PERTAMACUSTOMER CARE IS THE FIRST PRIORITY

PENINGKATAN KERJASAMATEAMWORK ENHANCEMENT

KODE ETIKCODE OF CONDUCT

Klien kita adalah alasan keberadaaan kita pada hari ini. PT Bank Oke Indonesia akan selalu mengutamakan kepuasan pelanggan dalam segala hal.

Our clients are the reason for our presence today. PT Bank Oke Indonesia will always put customer satisfaction in all things.

Pentingnya kerja tim di lingkungan kerja sangat penting bagi keberhasilan bank dan perkembangan setiap karyawan.

The importance of teamwork at work is vital tothe success of the bank and to the developmentof each employee.

Kode Etik dikembangkan untuk membantu kita semua menjalani nilai-nilai hidup kita dan melekat dalam segala hal yang kita lakukan.

Code of Conduct live our values and deliver our brand promise in everything we do.

Terus berusaha mengembangkan budaya kerja yang berorientasi pada profit. Strive to develop a profit oriented working culture.

30 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

Risk Management Committee

Financial Institution Div.

Multifinance

BPR Planning & Control

BPR Performance Management

MIS

Branch

BusinessDevelopment Div.

MarketingCommunication Div.

MarketingCommunication

Brand Strategy

Funding

Business Planning

SMEDivision

E-BankingDiv.

E Banking

E-Channel

SME 1

SME 2

SME 3

SME 4

SME 5

Multipurpose

SME Support

Marketing Planning & Strategy Div.

Credit Review Div.

Credit Review

ALCOLoanCommittee

IT SteeringCommittee

Audit CommitteeRisk Oversight Committee

Remuneration andNomination Committee

Director

Shareholder’s Meeting

Board of Commissioners

Board of Directors

CEO

STRUKTUR ORGANISASI 20182018 ORGANIZATION STRUCTURE

31Laporan Tahunan 2018 Annual Report

Internal Audit

Internal ControlSpecial Asset Management

Customer Care

Operation Div.Credit Control & Management Div.

Compliance Div.TreasuryDivision

Risk Management

Div.

Central OprationCredit Admin ComplianceFinanceDivision

Legal Div.

General AffairApprasial AMLIT Operation Div.

IT Planning Div.

HR Div.

Compliance Director

32 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

KOMPOSISI KEPEMILIKAN SAHAMOWNERSHIP COMPOSITION

PROFIL PEMEGANG SAHAMSHAREHOLDERS PROFILE

I WAYAN GATHA

APRO Financial Co, Ltd adalah perusahaan pembiayaan dari Korea Selatan yang berfokus pada sektor consumer loan. Perusahaan ini didirikan pada tahun 1999 sebagai A&O Financial dan diakuisisi oleh J & K Capital pada tahun 2004 dan menjadi APLO FC Group. Kemudian berubah namanya menjadi A&P Financial pada tahun 2007. Setelah itu A&P Financial diperluas ke China dan Polandia dan selanjutnya menjadi APRO Financial Co. Ltd di 2014.

I WAYAN GATHA Pengusaha swasta ini telah berkecimpung di dunia perbankan dengan spesifikasi pembiayaan pada usaha-usaha mikro selama lebih dari 30 tahun. Beliau merupakan salah satu pendiri Bank Pasar Seri Partha (BPSP) yang kemudian berubah menjadi Bank Sri Partha. I Wayan Gatha bergabung dengan pemodal lain yang memiliki visi sama untuk membantu mengentaskan kemiskinan dan mengembangkan keuangan mikro di Indonesia.

APRO Financial Co, Ltd is a finance company from South Korea that focuses on the consumer lending sector. The Company was founded in 1999 as A&O Financial and was acquired by J&K Capital in 2004 to became APLO FC Group. The company changed its name to A&P Financial in 2007. Afterwards, A&P Financial expanded to China and Poland and changed its name to APRO Financial Co. Ltd in 2014.

I WAYAN GATHA is an entrepreneur who has been actively involved in the banking industry, particularly in microfinance, for over 30 years. He was one of the founders of Bank Pasar Seri Partha (BPSP) which later became Bank Sri Partha. He joined with other shareholders who also share a common vision to fight against poverty and develop microfinance in Indonesia.

I WAYAN GATHA

APRO FINANCIAL CO, LTD.

99%

1%

33Laporan Tahunan 2018 Annual Report

PROFIL DEWAN KOMISARISBOARD OF COMMISSIONERS PROFILE

KOMISARIS UTAMA

MOON YOUNGSO

Beliau adalah warga Negara Korea Selatan, lahir di Seoul pada tanggal 30 Agustus 1963, memperoleh gelar sarjananya di Seoul National University pada tahun 1986. Salah satu jejak pendidikan beliau adalah gelar pasca sarjana yang diperolehnya di Dankook

University tahun 1989. Perjalanan karir beliau dibidang perbankan dimulai sejak 1990 di Korea Long Term Credit Bank, yang di mana

delapan tahun kemudian, bergabung dengan Long Term Credit Bank merger dengan KB Kookmin Bank yang berganti nama

menjadi KB Kookmin Bank. Setelah merger, beliau masih terus bekerja di KB Kookmin Bank dengan posisi terakhir (April 2016) sebagai General Manager KB Kookmin Bank, Human Resource Group. Setelah itu, beliau bergabung dengan APRO Financial

Co.,Ltd pada bulan Mei 2016 menjabat sebagai Managing Director Global Business Division.

He is a South Korean citizen, born in Seoul on August 30, 1963, obtained his bachelor’s degree at Seoul National University in

1986. He earned a postgraduate degree at Dankook University in 1989. His career in the banking sector began in 1990 in Korea

Long Term Credit Bank that eight years later, merged with KB Kookmin Bank and renamed KB Kookmin Bank, after merger he still

continued to work in KB Kookmin Bank with the last position (April 2016) as General Manager of KB Kookmin Bank, Human Resource Group. Joined APRO Financial Co., Ltd. in May 2016 and serves as

Managing Director of Global Business Division.

President Commissioner

33Laporan Tahunan 2018 Annual Report

34 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

ANGELINE NANGOI

Angeline Nangoi adalah lulusan Institut Teknologi Bandung (ITB), Bandung. Beliau memiliki pengalaman luas di bidang perbankan selama lebih kurang 36 tahun dengan beberapa jabatan seperti Direktur pada Bank Global International dari tahun 1997 sampai dengan tahun 2001, Direktur Kepatuhan pada Bank Societe Generale Indonesia dari tahun 2001 sampai dengan tahun 2003, Direktur Kepatuhan pada Bank OCBC Indonesia pada tahun 2003 sampai dengan tahun 2010, dan terakhir menjabat sebagai Direktur Kepatuhan PT Bank Commonwealth pada tahun 2014 sampai dengan tahun 2017. Kemudian bergabung dengan PT Bank Oke Indonesia pada bulan Maret 2018, menjabat sebagai Komisaris Independen Bank.

Angeline Nangoi is a graduate of Institut Teknologi Bandung (ITB), Bandung. She has wide experiences in Banking Industry for around 36 years with several positions such as Director of Bank Global International from 1997 until 2001, Compliance Director of Bank Societe Generale Indonesia from 2001 until 2003, Compliance Director of Bank OCBC Indonesia from 2003 until 2010, and the last held position as Compliance Director of PT Bank Commonwealth from 2014 until 2017, and then join PT Bank Oke Indonesia on March 2018, held position as Independent Commissioner of the Bank.

34 Laporan Tahunan 2018 Annual Report

KOMISARIS INDEPENDENIndependent Commissioner

35Laporan Tahunan 2018 Annual Report

PROFIL DEWAN DIREKSIBOARD OF DIRECTORS PROFILE

LIM CHEOL JIN

Lim Cheol Jin adalah Sarjana lulusan Chonbuk National University, Cheonju, Korea Selatan. Beliau memiliki pengalaman panjang di

industri perbankan. Mulai dari tahun 1982 hingga tahun 1998, beliau bergabung dengan Commercial Bank of Korea (CBK)

Kwanghwamoon Branch, Work-out Dept. Bersama perusahaan ini, beliau kemudian melebarkan karir perbankannya ke Hanvit Bank Korea pada tahun 1998 hingga akhirnya beliau pindah ke

Indonesia dan bergabung dengan Woori Bank Indonesia (dahulu Bank Hanvit Indonesia) dari 2003 hingga 2007, sebagai Direktur Utama/CEO. Beliau ditugaskan kembali di Woori Bank Indonesia sebagai Komisaris pada tahun 2010, dan 2011 sampai Mei 2017. Konsolidasi antara Bank Woori Indonesia dan Bank Saudara Tbk.

berhasil dilakukan melalui kepemimpinan beliau. Kemudian beliau bergabung dengan PT Bank Oke Indonesia pada bulan Agustus

2017, menjabat sebagai Direktur Utama Bank.

Lim Cheol Jin is a graduate of Chonbuk National University, Cheonju, South Korea. He has various experiences in banking

industry. From 1982 until 1998, he joined with the Commercial Bank of Korea (CBK) Kwanghwamoon Branch, Work-out Dept. Along with this company, he expanded his banking career by

joining Hanvit Bank Korea in 1998 until he finally moved to Indonesia and joined Woori Bank Indonesia (formerly Bank Hanvit

Indonesia) in 2003 to 2007, as President Director/CEO. He was reassigned in Woori Bank Indonesia as a Commissioner in 2010,

and 2011 to May 2017. The consolidation between Bank Woori Indonesia and Bank Saudara Tbk. is successfully carried out with his leadership. Afterwards, he joined PT. Bank Oke Indonesia in August

2017, and has been serving as the President Director of the Bank ever since.

35Laporan Tahunan 2018 Annual Report

DIREKTUR UTAMAPresident Director

36 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

36 Laporan Tahunan 2018 Annual Report

DENNY SETIAWAN HANUBRATA

Denny Setiawan Hanubrata memiliki pengalaman lebih dari 20 tahun di industri perbankan, terutama di bidang bisnis yang dimulai dari segmen konsumtif, SME, komersial, hingga corporate banking. Karir perbankan beliau dimulai dari tahun 1996 di Bank Bali, dan terus berkembang mengantarkan beliau berkarir di beberapa Bank seperti Bank Chinatrust Indonesia, PT Bank Permata, Tbk, dan Bank DBS Indonesia.

Jabatan terakhir beliau sebelum bergabung dengan Bank Oke Indonesia adalah Head of Business Banking di Bank UOB Indonesia sejak Juni 2016. Lulusan Universitas Katolik Parahyangan Bandung ini bergabung dengan Bank Oke Indonesia pada Oktober 2018, menjabat sebagai Direktur Bisnis Bank.

Denny Setiawan Hanubrata has experiences more than 20 years in Banking Industry, especially in business field starting from Consumptive Segment, SME Segment, Commercial Segment, to Corporate Banking Segment. His banking career commenced from 1996 in Bank Bali, and kept growing to help him have career in Several Banks, like Bank Chinatrust Indonesia, PT Bank Permata, Tbk, and Bank DBS Indonesia.

His last position before joining Bank Oke Indonesia was Head of Business Banking in Bank UOB Indonesia since June 2016. He graduated from University of Katolik Parahyangan Bandung and joined Bank Oke Indonesia on October 2018, as Business Director of the Bank.

DIREKTUR BISNISBusiness Director

37Laporan Tahunan 2018 Annual Report 37Laporan Tahunan 2018 Annual Report

EFDINAL ALAMSYAH

Beliau memiliki pengalaman mengemban tugas di pelbagai posisi selama lebih dari 25 tahun di industri perbankan seperti di bidang

hukum, kredit dan restrukturisasi kredit, kepatuhan, manajemen risiko, proses manajemen, branch expansion, sumber daya manusia

dan lain-lain. Beliau juga pernah terlibat dalam proses merger, akuisisi, dan restrukturisasi organisasi pada bank-bank sebelumnya.

Lulusan Universitas Padjadjaran Bandung ini, terakhir bertugas sebagai Direktur Kepatuhan, Manajemen Risiko, dan Sumber

Daya Manusia pada Bank KEB Hana Indonesia, dan sebelumnya bekerja di beberapa bank multinasional, antara lain Bank of

Tokyo Mitsubishi UFJ (BTMU), BNP Paribas, dan Korea Exchange Bank. Beliau telah bergabung ke PT Bank Oke Indonesia sebagai

Direktur Kepatuhan sejak Agustus 2016.

Efdinal Alamsyah has more than 25 years of experience in various positions in the banking industry such as law, credit and loan

restructuring, compliance, risk management, management process, branch expansion, human resources and so on so forth. He has also been involved in mergers, acquisitions, and organizational

restructuring of banks.

He graduated from University of Padjadjaran Bandung. He lastly served as Director of Compliance, Risk Management, and Human Resources at Bank KEB Hana Indonesia, and previously worked in

several multinational banks, including Bank of Tokyo Mitsubishi UFJ (BTMU), BNP Paribas, and Korea Exchange Bank. He has joined PT

Bank Oke Indonesia as Compliance Director since August 2016.

DIREKTUR KEPATUHANCompliance Director

38 Laporan Tahunan 2018 Annual Report

Creating Growth through Transformation

PRODUK DAN LAYANANPRODUCTS AND SERVICES

Pada 2018, diversifikasi dilakukan terhadap produk dan layanan Bank Oke Indonesia, di mana semula berfokus pada segmen Wholesale Banking. Pada tahun 2017, Bank Oke Indonesia melakukan ekspansi bisnis di segmen SME dan Ritel Bisnis sebagai salah satu langkah strategis dalam rangka memenuhi kebutuhan pasar.

Untuk melayani segmen pasar yang menjadi target market utama ini, Bank Oke Indonesia juga berupaya untuk menyempurnakan dan melengkapi produk dan layanannya sehingga dapat mendukung kebutuhan masyarakat umum.

PINJAMAN

Produk Pinjaman untuk segmen SME • Pinjaman Rekening Koran • Pinjaman Modal Kerja • Pinjaman Investasi

Produk lainnya yang dikembangkan tahun 2018, di antaranya:

Produk Pinjaman untuk segmen Retail Bisnis• Produk Program Kredit Potong Gaji (KPG). Merupakan

pembiayaan yang dikhususkan kepada karyawan perusahaan yang bekerjasama dengan Bank Oke Indonesia, dalam hal kebutuhan dana untuk apa saja, bagi karyawan dan keluarganya;

• Produk Program Pembiayaan Multiguna dengan Jaminan adalah pembiayaan dengan pola ke komunitas, baik itu di pasar ataupun komunitas lainnya di luar pasar tradisional. Pembiayaan ini menggunakan jaminan fix asset;

• Produk Personal Loan sedang dalam proses pengembangan. Merupakan produk kredit untuk keperluan multiguna.

SIMPANAN

Produk Dana Pihak ketiga (DPK)Bank Oke Indonesia masih terus melayani para nasabah dan masyarakat lainnya yang ingin mengembangkan dananya melalui; 1. Deposito Berjangka Deposito yang ditawarkan Bank terbagi atas tiga segmen

nasabah meliputi:• Deposito berjangka LKM, yakni deposito berjangka untuk

LKM agar nasabah dapat melakukan pengelolaan likuiditas yang lebih baik;

• Deposito berjangka korporasi yakni deposito berjangka yang ditujukan bagi korporasi yang peduli terhadap pengentasan kemiskinan melalui pemberdayaan LKM;

• Deposito berjangka individual yakni deposito berjangka yang ditujukan bagi individu.

2. Tabungan Merupakan produk dana yang menjangkau semua kalangan,

aman dan fleksibel. Saat ini produk tabungan yang sudah tersedia di antaranya;• Produk Tabungan Reguler;• Produk Tabungan Poin Jalan Jalan; dan• Produk Tabungan Qurban dan Umroh.

3. Giro Merupakan produk dana yang relatif lebih fleksibel untuk

pengaturan likuiditas dan transaksi.

In 2018, Bank Oke Indonesia began to diversify its products and services, which initially focused on the Wholesale Banking segment. In 2017, the Bank began to expand its business in the SME and Retail Business segments as strategic steps in order to grow and better serve the market.

To better serve its target customers, Bank Oke Indonesia is also working to improve and complement its products and services to support peoples’ needs.

OPERATIONS

Loan Products for SME segment• Current Account Loan• Working Capital loan • Investment Loan

Other products being developed in 2018 include:

Loan Products for the Business Retail segment• Product Salary Credit Program (KPG) is a financing program

that is devoted to employees of the company in collaboration with Bank Oke Indonesia, in terms of funding needs for anything, for employees and their families;

• Product with a Multipurpose Financing Program with Guarantees is financing program aiming the community, whether on the market or other communities outside the traditional market. This financing uses asset fix guarantees;

• Personal Loan products are in the process of being developed is a credit product for multipurpose purposes.

SAVINGS

Third Party Fund Products (TPF)Bank Oke Indonesia still continues serving customers and other communities who want to develop their funds through;1. Time Deposits The deposits offered by the Bank are divided into three

customer segments including:• MFI time deposit is time deposit for MFIs so that customers

can better manage liquidity;

• Corporate time deposit is time deposit intended for corporations that care of poverty alleviation through empowering MFIs;

• Individual time deposit is time deposit intended for individuals.