2017 Tabreed presentation v2 - Brand...

37

NATIONAL CENTRAL COOLING COMPANY (PJSC) Investor Presentation National Central Cooling Company PJSC (DFM:TABR)

-

Upload

truongquynh -

Category

Documents

-

view

214 -

download

0

Transcript of 2017 Tabreed presentation v2 - Brand...

NATIONAL CENTRAL COOLING COMPANY (PJSC)

Investor PresentationNational Central Cooling Company PJSC (DFM:TABR)

Tabreed – 2017 Investor Presentation2

• These materials have been prepared by and are the sole responsibility of theNational Central Cooling Company PJSC, ‘Tabreed’ (the “Company”). Thesematerials have been prepared solely for your information and for use at thecall/presentation. By attending the meeting/call where this presentation ismade, or by reading the presentation slides, you agree to be bound by thefollowing limitations

• These materials are confidential and may not be further distributed orpassed on to any other person or published or reproduced, in whole or inpart, by any medium or in any form for any purpose. The distribution ofthese materials in other jurisdictions may be restricted by law, and personsinto whose possession this presentation comes should inform themselvesabout, and observe, any such restrictions

• These materials are for information purposes only and do not constitute aprospectus, offering memorandum or offering circularor an offer to sell any securities and are not intended to providethe basis for any credit or any third party evaluation of any securities or anyoffering of them and should not be consideredas a recommendation that any investor should subscribe for or purchase anysecurities. The information contained herein has not been verified by theCompany, its advisers or any other personand is subject to change without notice and past performance isnot indicative of future results. The Company is under no obligation toupdate or keep current the information contained herein

• No person shall have any right of action (except in case of fraud) against theCompany or any other person in relation to the accuracy or completeness ofthe information contained herein. Whilst the Company has taken allreasonable steps to ensure the accuracy of all information, the Companycannot accept liability for any inaccuracies or omissions. All the informationis provided on an “as is” basis and without warranties, representations orconditions of any kind, either express or implied, and as such warranties,representation and conditions are hereby excluded to the maximum extentpermitted by law

• The merits or suitability of any securities to any investor's particular situation should

be independently determined by such investor. Any such determination should

involve inter alia, an assessment of the legal, tax, accounting, regulatory, financial,

credit and other related aspects of any securities

• No person is authorized to give any information or to make any representation not

contained in and not consistent with these materials and, if given or made, such

information or representation must not be relied upon as having been authorized by

or on behalf of the Company

• These materials are not intended for publication or distribution to, or use by any

person or entity in any jurisdiction or country where such distribution or use would be

contrary to local law or regulation. The securities discussed in this presentation have

not been and will not be registered under the U.S. Securities Act of 1933, as amended

(the Securities Act) and may not be offered or sold except under

an exemption from, or transaction not subject to, the registration requirements of the

Securities Act. In particular, these materials are not intended for publication or

distribution, except to certain persons in offshore transactions outside the United

States in reliance on Regulation S under the Securities Act

• These materials contain information regarding the past performance of the Company

and its subsidiaries. Such performance may not be representative of the entire

performance of the Company and its subsidiaries. Past performance is neither a guide

to future returns nor to the future performance of the Company and its subsidiaries

• These materials contain, or may be deemed to contain, forward-looking statements.

By their nature, forward- looking statements involve risks and uncertainties because

they relate to events and depend on circumstances that may or may not occur in the

future. The future results of the Company may vary from the results expressed in, or

implied by, the following forward looking statements, possibly to a material degree.

Any investment in securities is subject to various risks, such risks should be carefully

considered by prospective investors before they make any investment decisions. The

directors disclaim any obligation to update their view of such risks and uncertainties

or to publicly announce the result of any revision to the forward-looking statements

made herein, except where it would be required to do so under applicable law

Disclaimer

Index

A | Overview of Tabreed

B | Business overview

D | Board of Directors and Management Team

C | Financial Performance

E | Capital Structure

F | Conclusion

Tabreed – 2017 Investor Presentation4

A GCC wide environment-friendly company delivering shareholder returnsTabreed is ..

• A provider of a part of GCC’s critical infrastructure

• Delivering and operating district cooling solutions with high reliability

• Creating sustainable value for our shareholders

• Providing uninterrupted service to our customers and maintaining the comfort of the communities we serve

We aim to be the partner of choice for Governments and Corporations across GCC in providing environmentally friendly

cooling solutions

EFFICIENT AND ENVIRONMENT FRIENDLY EFFICIENT AND ENVIRONMENT FRIENDLY EFFICIENT AND ENVIRONMENT FRIENDLY EFFICIENT AND ENVIRONMENT FRIENDLY

OPERATIONSOPERATIONSOPERATIONSOPERATIONS

We harness the most efficient technology and utilize

our extensive experience to deliver reliable and energy

efficient cooling solutions that are environmentally

friendly

SUSTAINABLE LONGSUSTAINABLE LONGSUSTAINABLE LONGSUSTAINABLE LONG----TERM SHAREHOLDER TERM SHAREHOLDER TERM SHAREHOLDER TERM SHAREHOLDER

RETURNSRETURNSRETURNSRETURNS

We generate sustainable long-term returns for our

stakeholders on the back of the utility infrastructure

business model

REGIONAL LEADERREGIONAL LEADERREGIONAL LEADERREGIONAL LEADER

As the region's preferred provider of cooling solutions,

we focus on our customers' needs and deliver

comfort, value and service to all the communities we

serve

Tabreed – 2017 Investor Presentation5

District Cooling Benefits

Overall cooling represents 70% of peak

energy consumption…

District Cooling (DC) is 50% more energy

efficient than Conventional Cooling (CC)…

DC has ~16% lower life cycle cost

than CC

KW

h/R

Th

Other

District Cooling

Conventional Cooling

Industry

Variable

Capex

Charged

Monthly

Paid

Upfront

13%

63%

7%

17%

70%

District Cooling leads to substantial energy, economic and environmental benefits

-50%

District coolingConventional

cooling

49 45

51

39

Conventional

cooling

District

cooling

-16%

A cooling plant supplies chilled water via an

underground piping network to more than one

building in a service area (or district)

What is District Cooling

Tabreed – 2017 Investor Presentation6

Tabreed at a glance

Environmentally responsible operations reducing green house gas emissions

annual reduction in energy consumption in

the GCC through Tabreed’s DC services in

2016

Enough energy to power

Serving iconic projects across the region

48,000homes in the UAE every year

=

1.4billion kWh 713,000 tons

annual elimination of CO2

emissions

=The equivalent of removing

143,000cars from our streets every year

Dubai

MetroClevelandClinic

Abu Dhabi

The Pearl

QatarJabal Omar

Project

Sheikh Zayed

Grand Mosque

Over

1m RT delivered to clients

One of the world’s largest district cooling companies

71plants in

5 countries

Equivalent to cooling

towers the size of

Burj Khalifa100

Dubai Parks

and Resorts

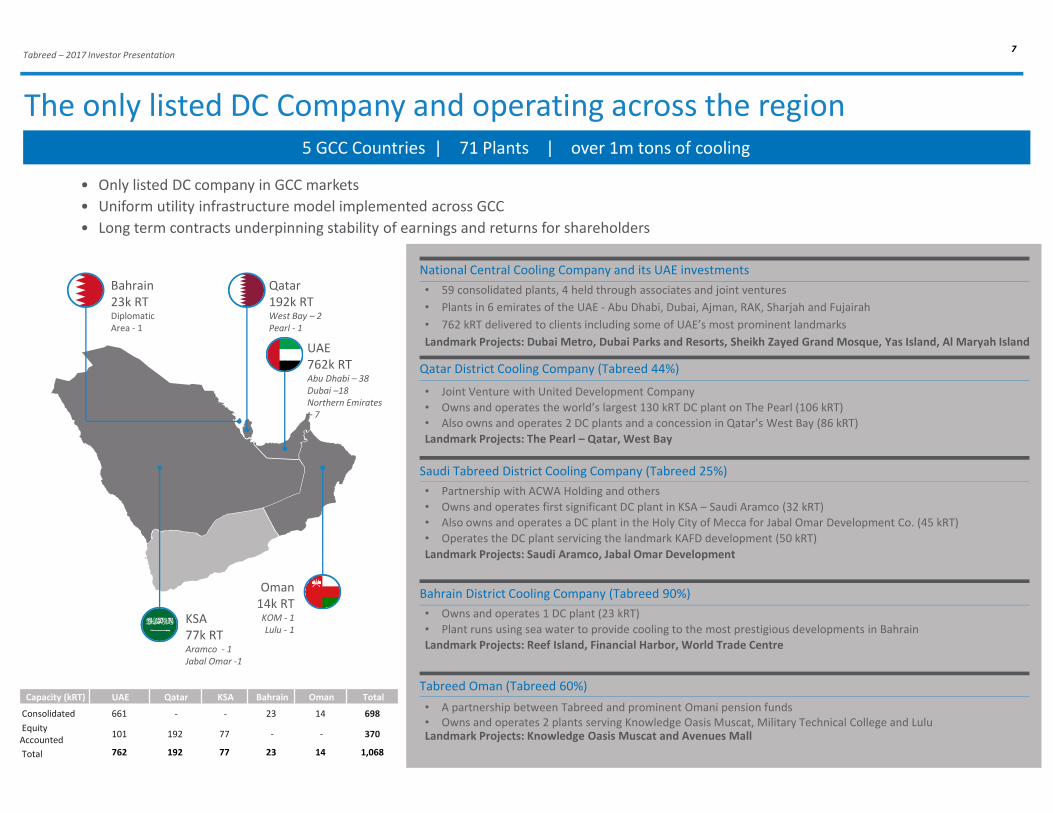

Tabreed – 2017 Investor Presentation7

The only listed DC Company and operating across the region5 GCC Countries | 71 Plants | over 1m tons of cooling

Bahrain

23k RTDiplomatic

Area - 1

Qatar

192k RTWest Bay – 2

Pearl - 1

KSA

77k RTAramco - 1

Jabal Omar -1

Oman

14k RTKOM - 1

Lulu - 1

UAE

762k RTAbu Dhabi – 38

Dubai –18

Northern Emirates

– 7

• Partnership with ACWA Holding and others

• Owns and operates first significant DC plant in KSA – Saudi Aramco (32 kRT)

• Also owns and operates a DC plant in the Holy City of Mecca for Jabal Omar Development Co. (45 kRT)

• Operates the DC plant servicing the landmark KAFD development (50 kRT)

Landmark Projects: Saudi Aramco, Jabal Omar Development

Saudi Tabreed District Cooling Company (Tabreed 25%)

• A partnership between Tabreed and prominent Omani pension funds

• Owns and operates 2 plants serving Knowledge Oasis Muscat, Military Technical College and LuluLandmark Projects: Knowledge Oasis Muscat and Avenues Mall

Tabreed Oman (Tabreed 60%)

• Owns and operates 1 DC plant (23 kRT)

• Plant runs using sea water to provide cooling to the most prestigious developments in Bahrain

Landmark Projects: Reef Island, Financial Harbor, World Trade Centre

Bahrain District Cooling Company (Tabreed 90%)

• Joint Venture with United Development Company

• Owns and operates the world’s largest 130 kRT DC plant on The Pearl (106 kRT)

• Also owns and operates 2 DC plants and a concession in Qatar’s West Bay (86 kRT)

Landmark Projects: The Pearl – Qatar, West Bay

Qatar District Cooling Company (Tabreed 44%)

• 59 consolidated plants, 4 held through associates and joint ventures

• Plants in 6 emirates of the UAE - Abu Dhabi, Dubai, Ajman, RAK, Sharjah and Fujairah

• 762 kRT delivered to clients including some of UAE’s most prominent landmarks

Landmark Projects: Dubai Metro, Dubai Parks and Resorts, Sheikh Zayed Grand Mosque, Yas Island, Al Maryah Island

National Central Cooling Company and its UAE investments

• Only listed DC company in GCC markets

• Uniform utility infrastructure model implemented across GCC

• Long term contracts underpinning stability of earnings and returns for shareholders

Capacity (kRT) UAE Qatar KSA Bahrain Oman Total

Consolidated 661 - - 23 14 698

Equity

Accounted 101 192 77 - - 370

Total 762 192 77 23 14 1,068

Tabreed – 2017 Investor Presentation8

Utility business model with fixed revenue providing ~92% of returns

• Capacity charges reflect the

cooling capacity reserved for the

customer

• Consumption charges recover the

cost of cooling consumed and is

billed based on metering

• Consumption billing follows a bell

curve in line with average temperatures

in the region

• Capacity bills are a fixed amount every

month

• Blended EBITDA margin is the highest

in the winter months, average 49% for

the year

• Consumption revenue covers all

variable costs of operation

• Capacity revenue covers fixed

O&M, finance and corporate costs

and provides return on capital

64%

36%

Capacity Consumption

59%

45% 43%

55%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Capacity Consumption EBITDA Margin

64%

37%

92%

36%

63%

8%

Revenue Costs and

Overheads

Total EBITDA

Capacity Consumption

Capacity ChargesCapacity ChargesCapacity ChargesCapacity Charges

Consumption ChargesConsumption ChargesConsumption ChargesConsumption Charges

Contracted cooling load (RT)

FIXEDFIXEDFIXEDFIXED

Cooling consumed (RTh)

VARIABLE (METERED)VARIABLE (METERED)VARIABLE (METERED)VARIABLE (METERED)

Majority of revenue comes

from capacity charges

Capacity revenue is fixed for the

year while consumption revenue

varies

Consumption is a pass through

and capacity provides returns

25 year contract25 year contract25 year contract25 year contract

Tabreed – 2017 Investor Presentation9

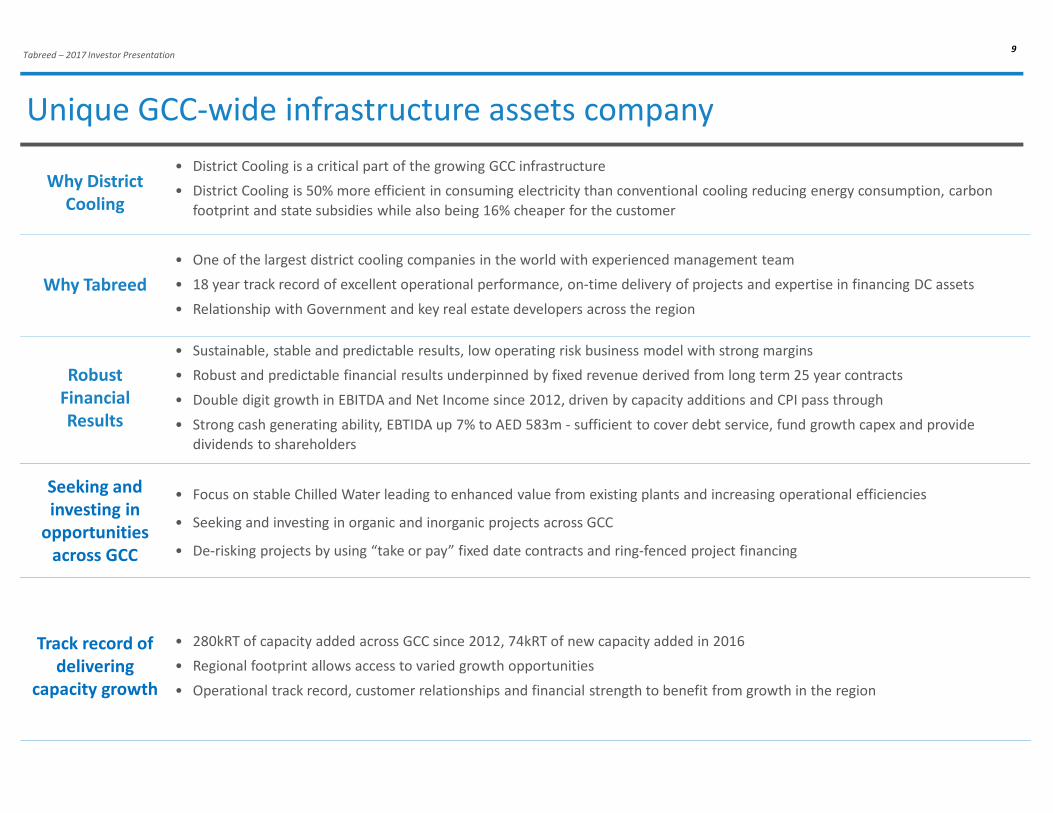

Unique GCC-wide infrastructure assets company

Why Tabreed

• One of the largest district cooling companies in the world with experienced management team

• 18 year track record of excellent operational performance, on-time delivery of projects and expertise in financing DC assets

• Relationship with Government and key real estate developers across the region

Seeking and

investing in

opportunities

across GCC

• Focus on stable Chilled Water leading to enhanced value from existing plants and increasing operational efficiencies

• Seeking and investing in organic and inorganic projects across GCC

• De-risking projects by using “take or pay” fixed date contracts and ring-fenced project financing

Robust

Financial

Results

• Sustainable, stable and predictable results, low operating risk business model with strong margins

• Robust and predictable financial results underpinned by fixed revenue derived from long term 25 year contracts

• Double digit growth in EBITDA and Net Income since 2012, driven by capacity additions and CPI pass through

• Strong cash generating ability, EBTIDA up 7% to AED 583m - sufficient to cover debt service, fund growth capex and provide

dividends to shareholders

Why District

Cooling

Track record of

delivering

capacity growth

• 280kRT of capacity added across GCC since 2012, 74kRT of new capacity added in 2016

• Regional footprint allows access to varied growth opportunities

• Operational track record, customer relationships and financial strength to benefit from growth in the region

• District Cooling is a critical part of the growing GCC infrastructure

• District Cooling is 50% more efficient in consuming electricity than conventional cooling reducing energy consumption, carbon

footprint and state subsidies while also being 16% cheaper for the customer

Index

A | Overview of Tabreed

B | Business overview

C | Board of Directors and Management Team

D | Financial Performance

E | Capital Structure

F | Conclusion

Tabreed – 2017 Investor Presentation11

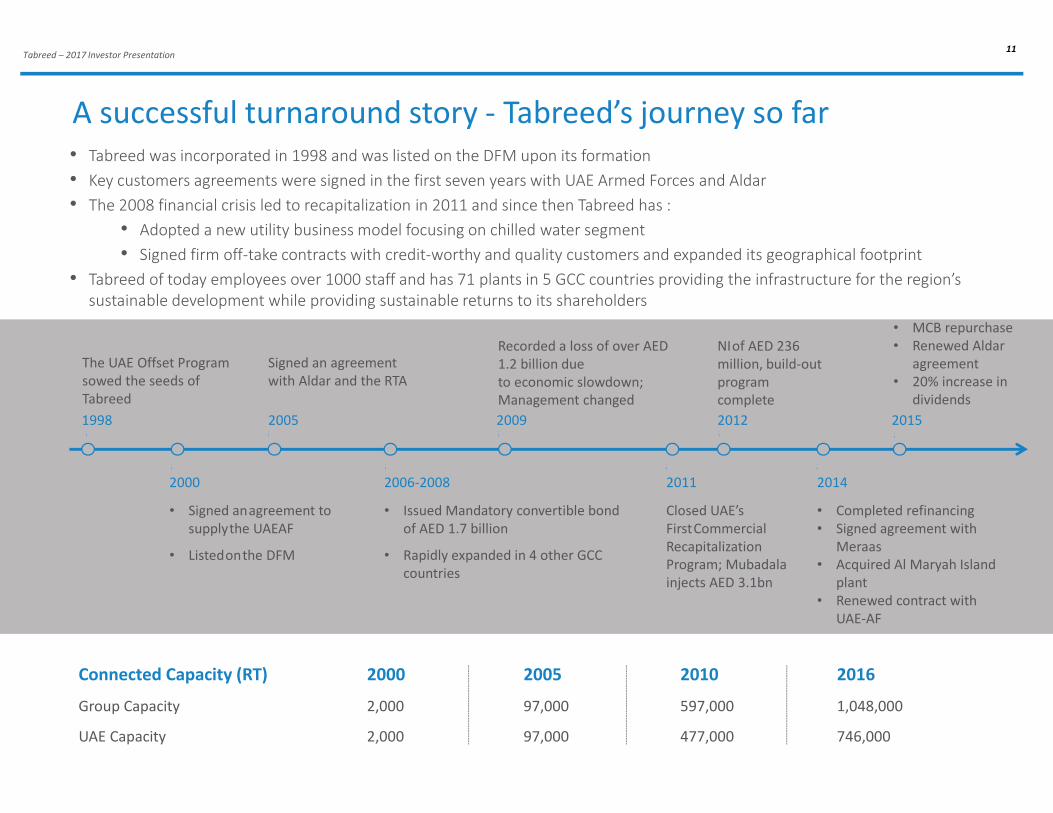

A successful turnaround story - Tabreed’s journey so far

• Tabreed was incorporated in 1998 and was listed on the DFM upon its formation

• Key customers agreements were signed in the first seven years with UAE Armed Forces and Aldar

• The 2008 financial crisis led to recapitalization in 2011 and since then Tabreed has :

• Adopted a new utility business model focusing on chilled water segment

• Signed firm off-take contracts with credit-worthy and quality customers and expanded its geographical footprint

• Tabreed of today employees over 1000 staff and has 71 plants in 5 GCC countries providing the infrastructure for the region’s

sustainable development while providing sustainable returns to its shareholders

1998

The UAE Offset Program

sowed the seeds of

Tabreed

• Signed anagreement to

supplythe UAEAF

• Listedonthe DFM

2000

2005

2006-2008 2011

2012

2014

Signed an agreement

with Aldar and the RTA

• Issued Mandatory convertible bond

of AED 1.7 billion

• Rapidly expanded in 4 other GCC

countries

2009

Recorded a loss of over AED

1.2 billion due

to economic slowdown;

Management changed

Closed UAE’s

FirstCommercial

Recapitalization

Program; Mubadala

injects AED 3.1bn

NIof AED 236

million, build-out

program

complete

• Completed refinancing

• Signed agreement with

Meraas

• Acquired Al Maryah Island

plant

• Renewed contract with

UAE-AF

Connected Capacity (RT) 2000 2005 2010 2016

Group Capacity 2,000 97,000 597,000 1,048,000

UAE Capacity 2,000 97,000 477,000 746,000

2015

• MCB repurchase

• Renewed Aldar

agreement

• 20% increase in

dividends

Tabreed – 2017 Investor Presentation12

Long term contracts with credit-worthy customers

• UAE Armed Forces was the first customer of the Company and continues to be an important partner

• Tabreed cools multiple military and training facilities

• Cooling agreement was renewed in 2014 for another 20 years

• Roads and Transport Authority of Dubai (RTA) is responsible for transport, roads & traffic in the Emirate of Dubai

• Tabreed has been providing cooling to all metro stations of the iconic Dubai Metro project since 2009

• Long term 27 year contract

• Aldar Properties PJSC is the leading real estate developer in Abu Dhabi and listed on ADX

• Tabreed and Aldar have been in partnership since Aldar’s incorporation in 2005

• Providing cooling to Aldar’s developments on Yas Island, Al Raha Beach, Reem Island and Abu Dhabi Island

• Cooling agreement was renewed in 2015 for another 30 years

Owned and Consolidated Plants

Joint Ventures and Associates

Tabreed’s UAE joint ventures and associates have long term contracts with key Government clients such as Mubadala,

Cleveland Clinic Abu Dhabi, Abu Dhabi Global Market Square, ZonesCorp et al while also serving reputable private

customers such as Aldar and Al Hilal Bank

Our joint ventures and associates also provide cooling to key Government clients such as Saudi Aramco, King Abdullah

Financial District and King Khalid International Airport also serve reputable private customers such as United

Development Company in Qatar and Lulu in Oman

The top 3 customers accounted for ~60% of chilled water revenues in 2016

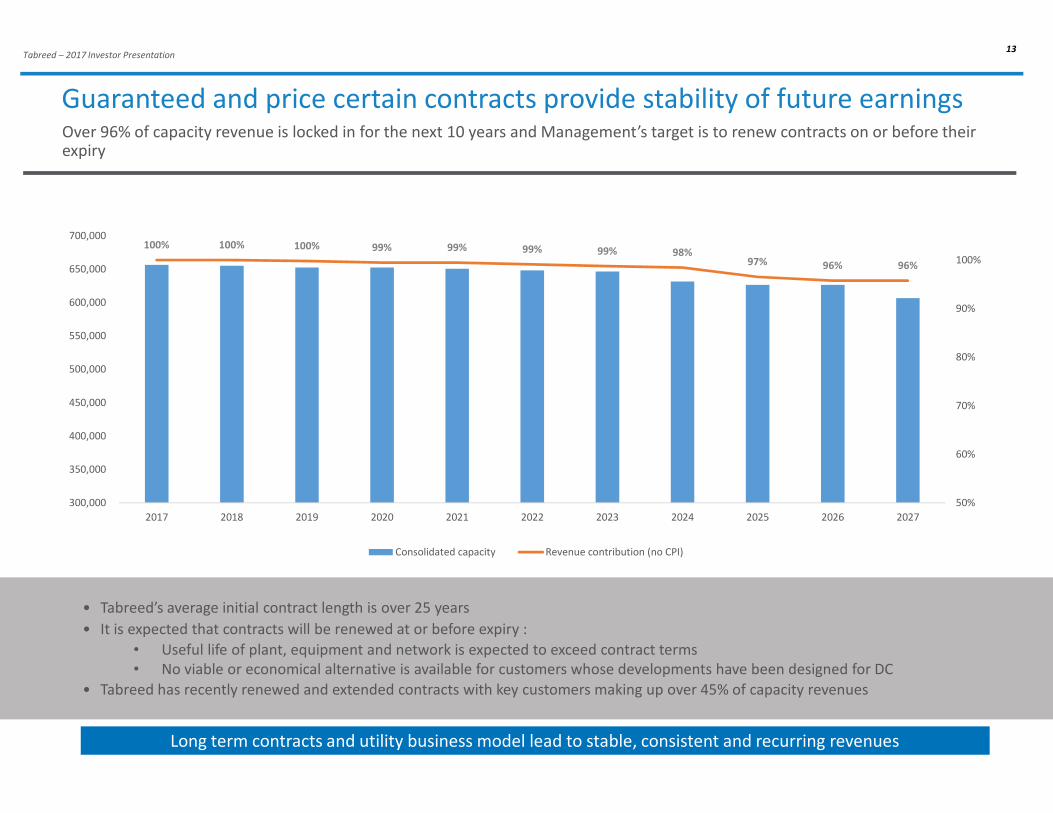

Tabreed – 2017 Investor Presentation13

Guaranteed and price certain contracts provide stability of future earnings

• Tabreed’s average initial contract length is over 25 years

• It is expected that contracts will be renewed at or before expiry :

• Useful life of plant, equipment and network is expected to exceed contract terms

• No viable or economical alternative is available for customers whose developments have been designed for DC

• Tabreed has recently renewed and extended contracts with key customers making up over 45% of capacity revenues

Long term contracts and utility business model lead to stable, consistent and recurring revenues

Over 96% of capacity revenue is locked in for the next 10 years and Management’s target is to renew contracts on or before their expiry

100% 100% 100% 99% 99% 99% 99% 98%97% 96% 96%

50%

60%

70%

80%

90%

100%

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

700,000

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Consolidated capacity Revenue contribution (no CPI)

Tabreed – 2017 Investor Presentation14

Pursuing growth opportunities across GCC

Well placed to benefit from growth opportunities in the region through a mix of existing concessions and assets and new plants

• Over 60kRT of fully contracted capacity to be connected by end of 2018 in UAE, Qatar, Saudi, Bahrain and Oman and 20kRT

added by the end of Q1

• Tabreed is also positioned to benefit from several captive concession-like arrangements with customers across the region

Concessions

Concession-like

arrangements

leading to captive

growth

New plants

New plants and

developments with

take-or-pay contracts

Existing plants

71 plants across the

region provide

opportunity for new

connections

Connections to existing plants, high margin and increasing utilization

• Tabreed has added over 50kRTto existing plants since 2011

• Usually requires no additional fixed cost and provides higher margins

• Possible additions in the future could be up to 5% of total capacity

New plants, driven by the real estate market

• 4 plants under construction in the GCC

• Major projects include King Khaled International Airport (15kRT), West Bay 3 in

Qatar (15kRT) and other projects in Oman

Concession-like arrangements, providing captive growth from key customers

• Various arrangements across the GCC providing captive growth

• UAE – Yas Island, Maryah Island, Raha Beach, Dubai Parks

• Qatar – Pearl Qatar

• KSA – Jabal Omar development

• Bahrain – Reef Island and Bahrain Financial Harbor

Tabreed – 2017 Investor Presentation15

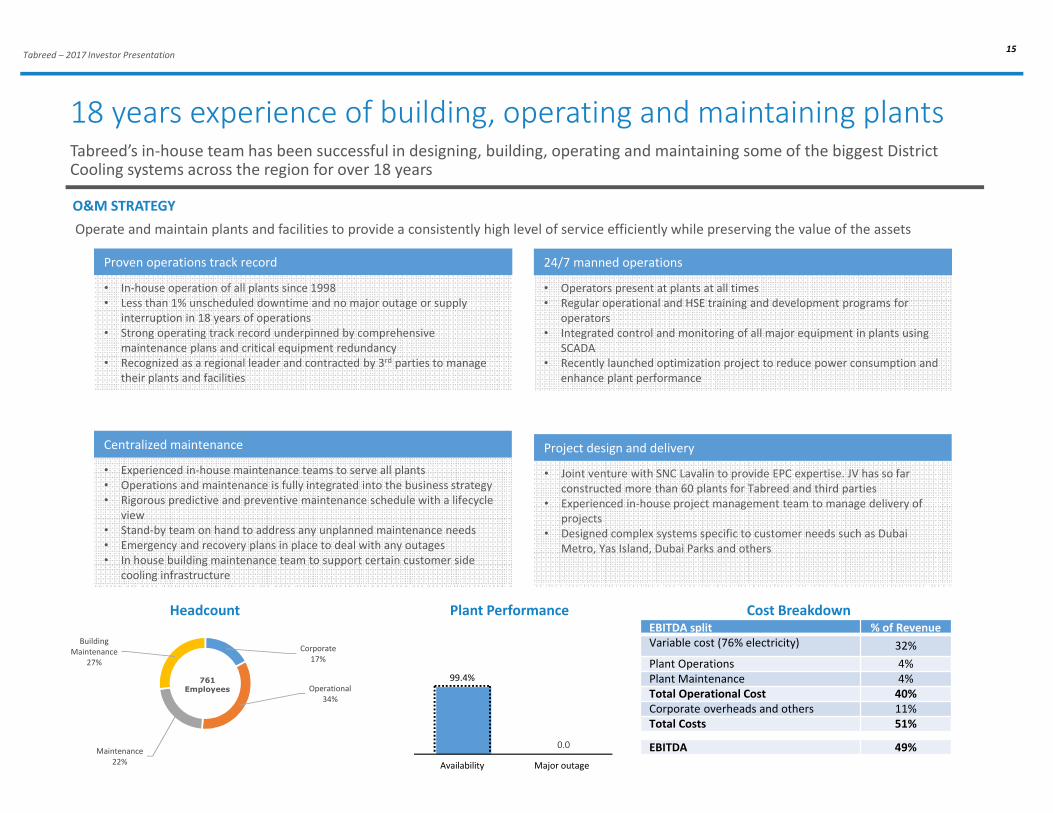

18 years experience of building, operating and maintaining plantsTabreed’s in-house team has been successful in designing, building, operating and maintaining some of the biggest District Cooling systems across the region for over 18 years

Corporate

17%

Operational

34%

Maintenance

22%

Building

Maintenance

27%

O&M STRATEGY

Operate and maintain plants and facilities to provide a consistently high level of service efficiently while preserving the value of the assets

Proven operations track record

• In-house operation of all plants since 1998

• Less than 1% unscheduled downtime and no major outage or supply

interruption in 18 years of operations

• Strong operating track record underpinned by comprehensive

maintenance plans and critical equipment redundancy

• Recognized as a regional leader and contracted by 3rd parties to manage

their plants and facilities

24/7 manned operations

• Operators present at plants at all times

• Regular operational and HSE training and development programs for

operators

• Integrated control and monitoring of all major equipment in plants using

SCADA

• Recently launched optimization project to reduce power consumption and

enhance plant performance

Centralized maintenance

• Experienced in-house maintenance teams to serve all plants

• Operations and maintenance is fully integrated into the business strategy

• Rigorous predictive and preventive maintenance schedule with a lifecycle

view

• Stand-by team on hand to address any unplanned maintenance needs

• Emergency and recovery plans in place to deal with any outages

• In house building maintenance team to support certain customer side

cooling infrastructure

Project design and delivery

• Joint venture with SNC Lavalin to provide EPC expertise. JV has so far

constructed more than 60 plants for Tabreed and third parties

• Experienced in-house project management team to manage delivery of

projects

• Designed complex systems specific to customer needs such as Dubai

Metro, Yas Island, Dubai Parks and others

Headcount Plant Performance

0.0

Availability

99.4%

Major outage

Cost Breakdown

761Employees

EBITDA split % of Revenue

Variable cost (76% electricity) 32%

Plant Operations 4%

Plant Maintenance 4%

Total Operational Cost 40%

Corporate overheads and others 11%

Total Costs 51%

EBITDA 49%

Tabreed – 2017 Investor Presentation16

Focus on Health, Safety and EnvironmentHealth, safety and environment is a cornerstone of our operations and an integral part of business planning and strategic goal setting.

• Integrating HSE into plant operations and processes

• Development of Tabreed’s HSE manual

• Regular HSE training and awareness programs to enhance HSE readiness

• All Tabreed and most contractor employees have been trained over the past 2 years

• Regular internal and external HSE audits to ensure compliance with UAE regulations and international standards

• HSE tracking system for effective monitoring of HSE performance and objectives

Implementation

• Recipient of International Organization for Standardization and British Standard Institute certifications

•ISO 9001 for quality management systems

•ISO 14001 for environment management systems

•OHSAS 18001 for occupational health and safety management systems

Certifications

• Top management is fully committed to HSE with direct reporting line to the CEO

• Reporting HSE performance to the Board of Directors on monthly basis

• HSE steering committee comprises HSE, Operations and Internal Audit heads

• Multiple plant and site visits performed each year by CEO and senior management

Leadership & Commitment

• Conduct business in socially responsible manner

• HSE is a key consideration in business planning and decisions

• Comply with all regulations and industry best practices

• Ensure all employees are trained and motivated to adopt and develop HSE culture

• Seek continuous improvement in HSEperformance

HSE Policy

Index

A | Overview of Tabreed

B | Business overview

C | Board of Directors and Management Team

D | Financial Performance

E | Capital Structure

F | Conclusion

Tabreed – 2017 Investor Presentation18

Khaled Abdulla Al Qubaisi

Chairman

Ahmed Saeed Al Calily

Vice Chairman, Projects Committee

Chair

Ahmed Yahia Al Idrissi

Finance Committee Chair

H.E. Dr Ahmad Abdulla Belhoul

Current Role• Chief Executive Officer, Aerospace, ICT

and Renewables• Chief Strategy & Risk Officer, Mubadala

• Chief Executive Officer, Technology,

Manufacturing and Mining

• Minister of State – Higher Education

Affairs, Abu Dhabi

Other Board Positions

• Managing Director of Abu Dhabi Racing

• Board member of Masdar, Emirates

Global Aluminum, Abu Dhabi

Motorsports Management, Mubadala

Petroleum, GLOBALFOUNDRIES, Finance

House and Cleveland Clinic Abu Dhabi

LLC

• Board member of Saudi Tabreed and

Qatar Cool

• Board Member of Mubadala Petroleum

and Masdar

• Member of Mubadala’s Investment

Committee

• Chairman of GLOBALFOUNDRIES and TM

Mining Ventures, S.L.

• Board member of Masdar, Emirates Global

Aluminium, Mubadala Petroleum and

Advanced Micro Devices, INC.

• Member of Mubadala’s Investment

Committee

• Ex-Board Member of Emirates

Development Bank

• Board member of Masdar

Board of DirectorsExperienced Board with a wide range of industry experience

Mohamed Jameel Al

Ramahi

Audit Committee Chair

Abdul Raouf Al Bitar Khaled Saleh Al Rashedi Mohammed Al Huraimel Al

Shamsi

Noms & Rems Committee

chair

Saeed Ali Khalfan Al Dhaheri

Current Role • CEO, Masdar• CEO of Al Manhal Water Factory

Co. Ltd

• Head of Government Affairs in

Mubadala

• Senior Vice President in the

Industry Unit, Mubadala

• Investments Director at Ali &

Sons, UAE

Other Board Positions

• Board Member of Shuaa Energy 2

PJSC and Abu Dhabi Carbon

Capture Company LLC

• Board member of Middle East

Specialized Cables Factory, Gulf

Insurance Group (15 Board

membership)

• Chairman of Safwa Marina

• Board member of Guinea Alumina

Corporation, AAV Limited and Abu

Dhabi Ship Building

Tabreed – 2017 Investor Presentation19

Jasim Husain Thabet

Chief Executive Officer

Management Team

Stephen Ridlington

Chief Financial Officer

Dr. Yousif Al Hammadi

Executive Vice President

of Projects and Strategic

Customer Relationship

• Joined Tabreed in August 2012

• Over 15 years of experience in the

regional energy, infrastructure and

utilities industries, including the

district cooling sector

• Prior to joining Tabreed, Jasim was

Vice-President in Mubadala

Development Company’s Industry

Unit, with responsibility for

managing several of the Unit’s key

assets

• Also held senior positions with

General Electric Power Systems,

and ZADCO, one of the region’s

leading oil producers

• Appointed Chief Financial Officer in

February 2015, a position he

previously held between 2009 –

2011

• In his first tenure, led the company

through its AED 3 billion

recapitalization

• Prior to joining Tabreed, Steve

spent over 20 years with BP in

several senior finance roles

including Deputy CFO and Group

Treasurer of TNK-BP

• Joined Tabreed’s Projects

Department in 2014

• Oversees the development of all of

the company’s projects

• Joined Tabreed from Mubadala

Development Company, where he

was instrumental in delivering a

number of key projects including

Rosewood Hotel on al Maryah

Island

• Joined Tabreed in 2011

• Over 17 years of experience in

corporate law, mergers and

acquisitions, private equity and

project finance. He has practiced

law in four countries across four

continents.

• Previously, worked for Herbert

Smith LLP where he worked on

many landmark deals in the region

Hamish Jooste

Chief Legal Counsel

Index

A | Overview of Tabreed

B | Business overview

C | Board of Directors and Management Team

D | Financial Performance

E | Capital Structure

F | Conclusion

Tabreed – 2017 Investor Presentation21

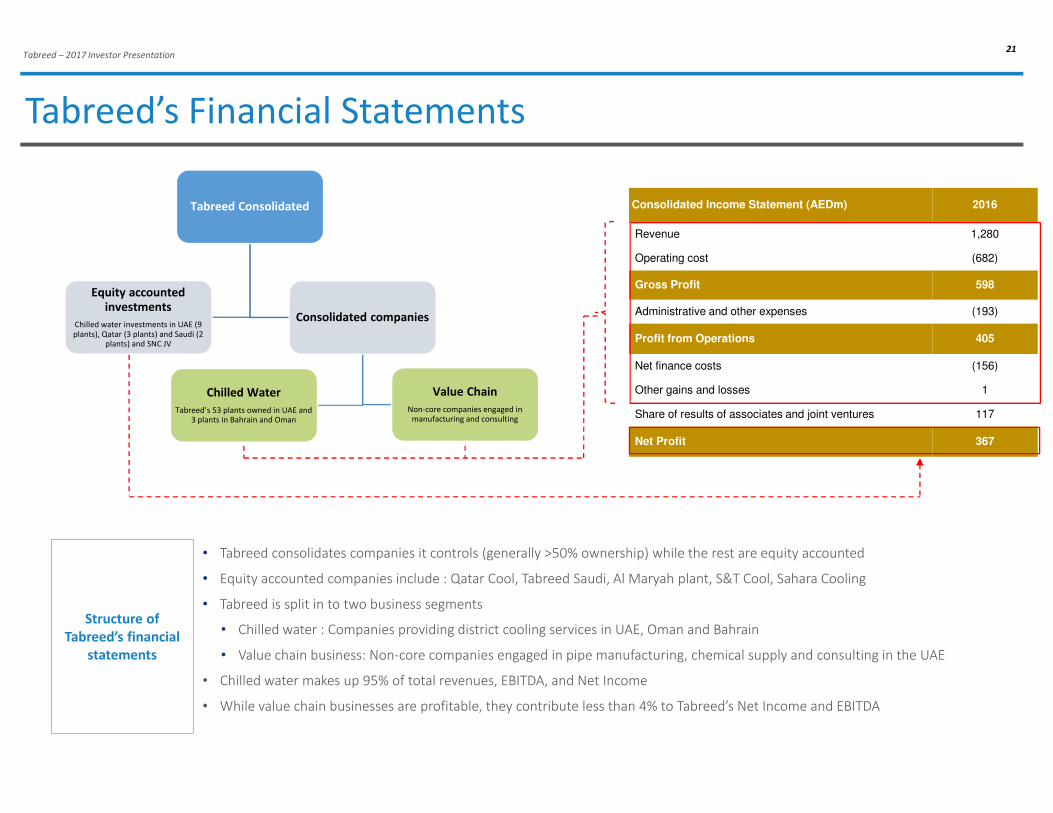

Consolidated Income Statement (AEDm) 2016

Revenue 1,280

Operating cost (682)

Gross Profit 598

Administrative and other expenses (193)

Profit from Operations 405

Net finance costs (156)

Other gains and losses 1

Share of results of associates and joint ventures 117

Net Profit 367

• Tabreed consolidates companies it controls (generally >50% ownership) while the rest are equity accounted

• Equity accounted companies include : Qatar Cool, Tabreed Saudi, Al Maryah plant, S&T Cool, Sahara Cooling

• Tabreed is split in to two business segments

• Chilled water : Companies providing district cooling services in UAE, Oman and Bahrain

• Value chain business: Non-core companies engaged in pipe manufacturing, chemical supply and consulting in the UAE

• Chilled water makes up 95% of total revenues, EBITDA, and Net Income

• While value chain businesses are profitable, they contribute less than 4% to Tabreed’s Net Income and EBITDA

Tabreed Consolidated

Consolidated companies

Chilled Water

Tabreed’s 53 plants owned in UAE and 3 plants in Bahrain and Oman

Value Chain

Non-core companies engaged in manufacturing and consulting

Equity accounted

investments

Chilled water investments in UAE (9 plants), Qatar (3 plants) and Saudi (2

plants) and SNC JV

Structure of

Tabreed’s financial

statements

Tabreed’s Financial Statements

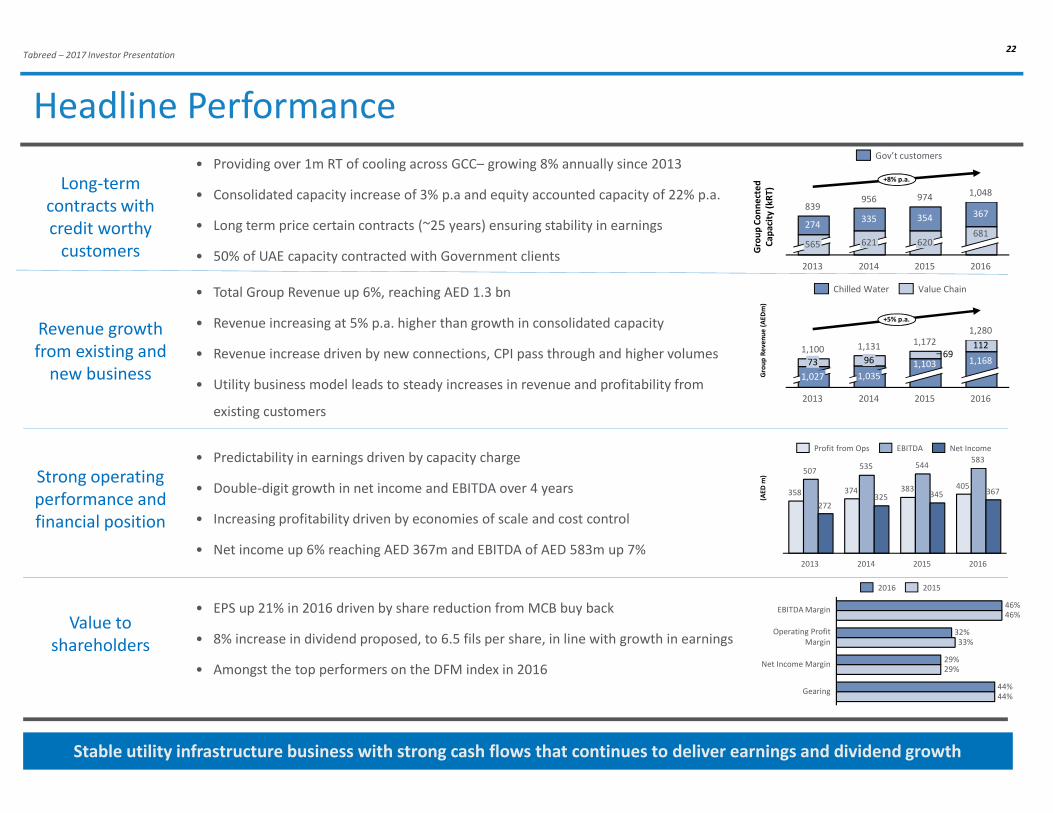

Tabreed – 2017 Investor Presentation22

1,131

2013

1,035

96 1,168

2015

+5% p.a.

1,280

1,172

2016

691,103

2014

112

73

1,027

1,100

367

681

2015

974

620

2014

1,048

354

956

621

2013

335

839

2016

274

565

+8% p.a.

Gov’t customers

Headline Performance

Revenue growth

from existing and

new business

• Total Group Revenue up 6%, reaching AED 1.3 bn

• Revenue increasing at 5% p.a. higher than growth in consolidated capacity

• Revenue increase driven by new connections, CPI pass through and higher volumes

• Utility business model leads to steady increases in revenue and profitability from

existing customers

Value to

shareholders

• EPS up 21% in 2016 driven by share reduction from MCB buy back

• 8% increase in dividend proposed, to 6.5 fils per share, in line with growth in earnings

• Amongst the top performers on the DFM index in 2016

Strong operating

performance and

financial position

• Predictability in earnings driven by capacity charge

• Double-digit growth in net income and EBITDA over 4 years

• Increasing profitability driven by economies of scale and cost control

• Net income up 6% reaching AED 367m and EBITDA of AED 583m up 7%

Long-term

contracts with

credit worthy

customers

• Providing over 1m RT of cooling across GCC– growing 8% annually since 2013

• Consolidated capacity increase of 3% p.a and equity accounted capacity of 22% p.a.

• Long term price certain contracts (~25 years) ensuring stability in earnings

• 50% of UAE capacity contracted with Government clients

(AE

D m

)G

rou

p R

ev

en

ue

(A

ED

m)

Gro

up

Co

nn

ect

ed

Ca

pa

city

(k

RT

)

Stable utility infrastructure business with strong cash flows that continues to deliver earnings and dividend growth

Chilled Water Value Chain

583

2016

383

2013

544507

345358

2014

374

535

325

2015

367405

272

Net IncomeEBITDAProfit from Ops

Gearing44%

Operating Profit

Margin 33%

32%

29%

44%

EBITDA Margin

Net Income Margin

46%46%

29%

20152016

Tabreed – 2017 Investor Presentation23

Core Chilled Water business drives performance growth

Capacity (kRT) Chilled Water Revenue and Share of results (AED m)

Chilled Water Profit From Operations (AED m)

UAE Qatar KSA Other

GCC

Total

Revenue 1,119 - - 49 1,168

Operating Costs (580) - - (37) (617)

Gross Profit 540 - - 11 551

Gross Profit Margin 48% - - 22% 47%

Profit from

Operations 382 - - 5 387

OP Margin 34% - - 10% 33%

Share of Results of

Associates 37 45 35 - 116

1,103

2014

1,035

2013

1,027

2016

1,168

+4% p.a.

2015

Equity accountedConsolidated

348 359 370387

+4% p.a.

2015

34%

2014

35%

2013

32% 33%

2016

Profit from OperationsMargin

UAE is the foundation for consistent performance with exciting opportunities in GCC beginning to materialize

Chilled Water Geographical Breakdown (AED m)

638

2014

638

2013

616

+4% p.a.

2016

683

2015

+22% p.a.

2015

336

2014

319

2013

201

2016

365

+21% p.a.

2016

117

20152014

85

2013

66

99

Share of ResultsCW Revenue

Tabreed – 2017 Investor Presentation24

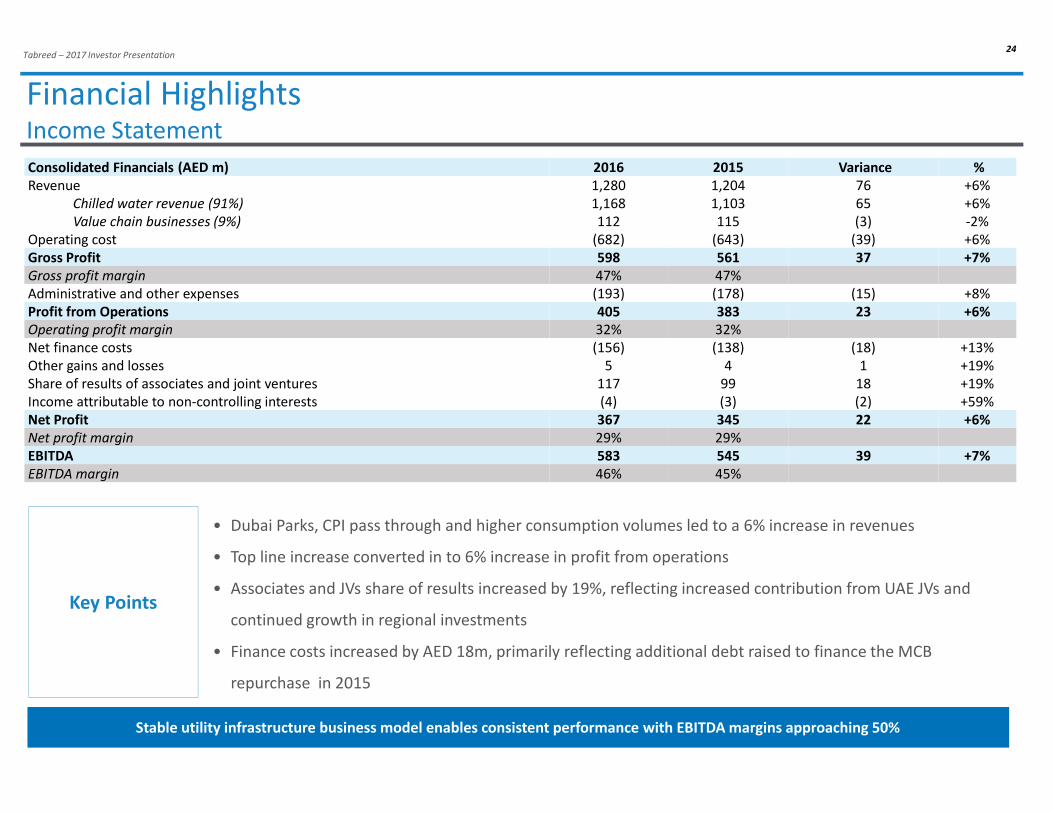

Financial HighlightsIncome Statement

Key Points

• Dubai Parks, CPI pass through and higher consumption volumes led to a 6% increase in revenues

• Top line increase converted in to 6% increase in profit from operations

• Associates and JVs share of results increased by 19%, reflecting increased contribution from UAE JVs and

continued growth in regional investments

• Finance costs increased by AED 18m, primarily reflecting additional debt raised to finance the MCB

repurchase in 2015

Stable utility infrastructure business model enables consistent performance with EBITDA margins approaching 50%

Consolidated Financials (AED m) 2016 2015 Variance %

Revenue 1,280 1,204 76 +6%

Chilled water revenue (91%) 1,168 1,103 65 +6%

Value chain businesses (9%) 112 115 (3) -2%

Operating cost (682) (643) (39) +6%

Gross Profit 598 561 37 +7%

Gross profit margin 47% 47%

Administrative and other expenses (193) (178) (15) +8%

Profit from Operations 405 383 23 +6%

Operating profit margin 32% 32%

Net finance costs (156) (138) (18) +13%

Other gains and losses 5 4 1 +19%

Share of results of associates and joint ventures 117 99 18 +19%

Income attributable to non-controlling interests (4) (3) (2) +59%

Net Profit 367 345 22 +6%

Net profit margin 29% 29%

EBITDA 583 545 39 +7%

EBITDA margin 46% 45%

Tabreed – 2017 Investor Presentation25

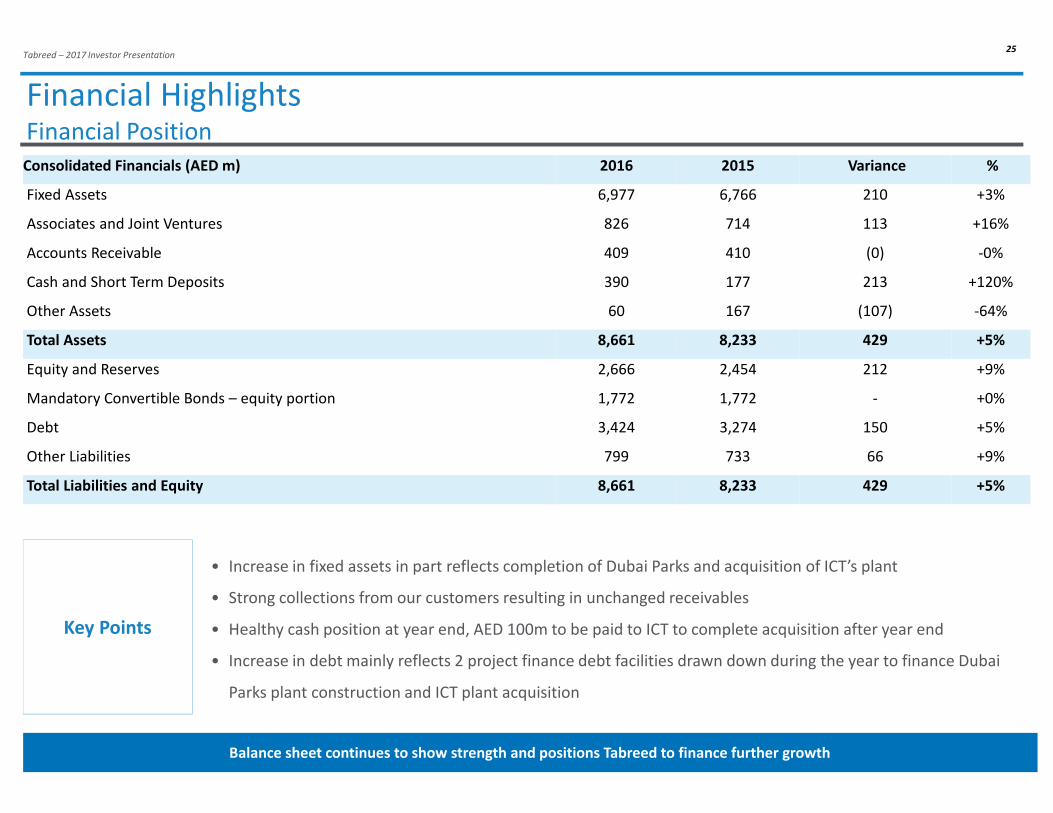

Financial HighlightsFinancial Position

Key Points

• Increase in fixed assets in part reflects completion of Dubai Parks and acquisition of ICT’s plant

• Strong collections from our customers resulting in unchanged receivables

• Healthy cash position at year end, AED 100m to be paid to ICT to complete acquisition after year end

• Increase in debt mainly reflects 2 project finance debt facilities drawn down during the year to finance Dubai

Parks plant construction and ICT plant acquisition

Balance sheet continues to show strength and positions Tabreed to finance further growth

Consolidated Financials (AED m) 2016 2015 Variance %

Fixed Assets 6,977 6,766 210 +3%

Associates and Joint Ventures 826 714 113 +16%

Accounts Receivable 409 410 (0) -0%

Cash and Short Term Deposits 390 177 213 +120%

Other Assets 60 167 (107) -64%

Total Assets 8,661 8,233 429 +5%

Equity and Reserves 2,666 2,454 212 +9%

Mandatory Convertible Bonds – equity portion 1,772 1,772 - +0%

Debt 3,424 3,274 150 +5%

Other Liabilities 799 733 66 +9%

Total Liabilities and Equity 8,661 8,233 429 +5%

Tabreed – 2017 Investor Presentation26

Financial HighlightsCash flow Statement

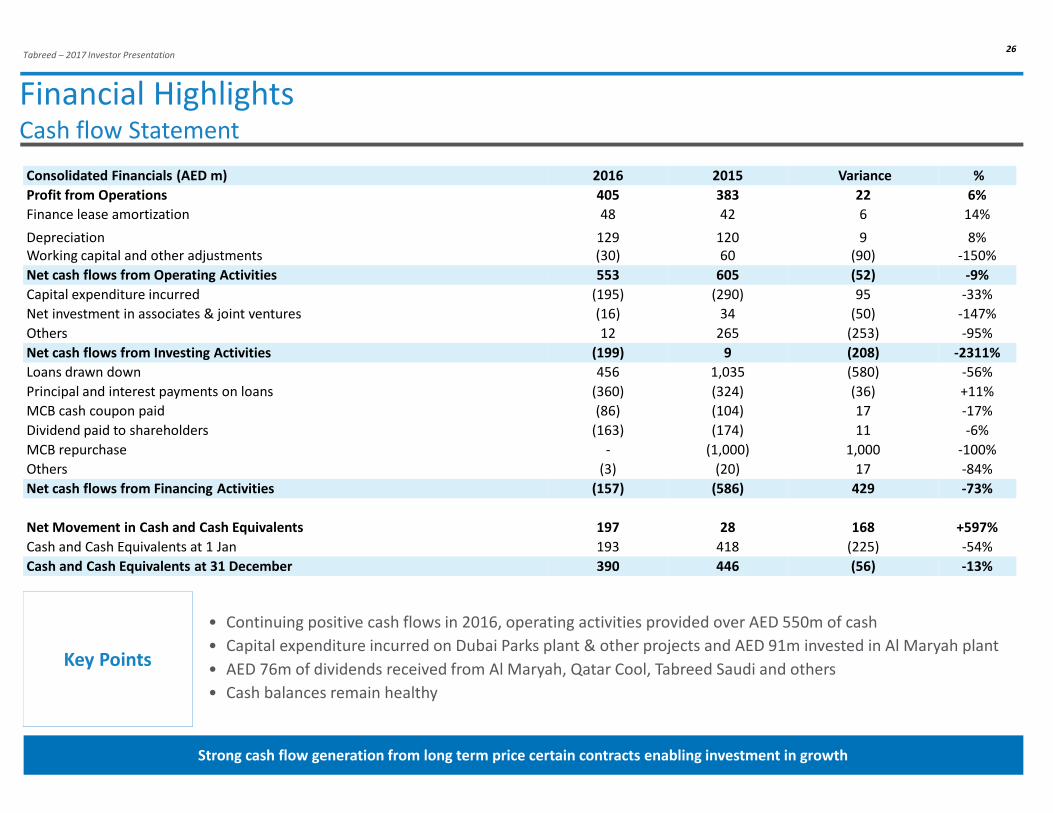

Key Points

• Continuing positive cash flows in 2016, operating activities provided over AED 550m of cash

• Capital expenditure incurred on Dubai Parks plant & other projects and AED 91m invested in Al Maryah plant

• AED 76m of dividends received from Al Maryah, Qatar Cool, Tabreed Saudi and others

• Cash balances remain healthy

Strong cash flow generation from long term price certain contracts enabling investment in growth

Consolidated Financials (AED m) 2016 2015 Variance %

Profit from Operations 405 383 22 6%

Finance lease amortization 48 42 6 14%

Depreciation 129 120 9 8%

Working capital and other adjustments (30) 60 (90) -150%

Net cash flows from Operating Activities 553 605 (52) -9%

Capital expenditure incurred (195) (290) 95 -33%

Net investment in associates & joint ventures (16) 34 (50) -147%

Others 12 265 (253) -95%

Net cash flows from Investing Activities (199) 9 (208) -2311%

Loans drawn down 456 1,035 (580) -56%

Principal and interest payments on loans (360) (324) (36) +11%

MCB cash coupon paid (86) (104) 17 -17%

Dividend paid to shareholders (163) (174) 11 -6%

MCB repurchase - (1,000) 1,000 -100%

Others (3) (20) 17 -84%

Net cash flows from Financing Activities (157) (586) 429 -73%

Net Movement in Cash and Cash Equivalents 197 28 168 +597%

Cash and Cash Equivalents at 1 Jan 193 418 (225) -54%

Cash and Cash Equivalents at 31 December 390 446 (56) -13%

Tabreed – 2017 Investor Presentation27

Index

A | Overview of Tabreed

B | Business overview

C | Board of Directors and Management Team

D | Financial Performance

E | Capital Structure

F | Conclusion

Tabreed – 2017 Investor Presentation28

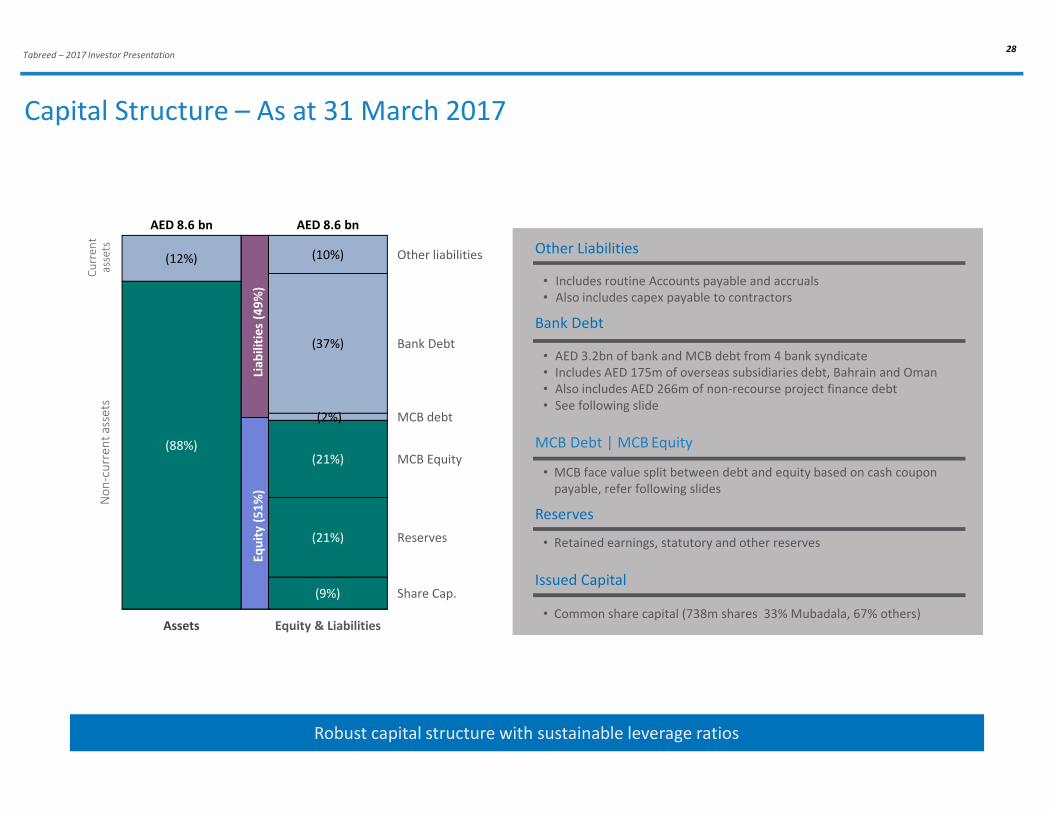

Capital Structure – As at 31 March 2017

(88%)

(9%)

(21%)

(21%)

(10%)

Share Cap.

Reserves

MCB Equity

MCB debt(2%)

(37%)

Assets

AED 8.6 bn

Bank Debt

Other liabilities

Equity & Liabilities

AED 8.6 bn

(12%)

• AED 3.2bn of bank and MCB debt from 4 bank syndicate

• Includes AED 175m of overseas subsidiaries debt, Bahrain and Oman

• Also includes AED 266m of non-recourse project finance debt

• See following slide

• MCB face value split between debt and equity based on cash coupon

payable, refer following slides

• Retained earnings, statutory and other reserves

• Common share capital (738m shares 33% Mubadala, 67% others)

• Includes routine Accounts payable and accruals

• Also includes capex payable to contractors

Eq

uit

y (

51

%)

Lia

bil

itie

s (4

9%

)

Robust capital structure with sustainable leverage ratios

Other Liabilities

Bank Debt

MCB Debt | MCB Equity

Reserves

Issued Capital

Cu

rre

nt

ass

ets

No

n-c

urr

en

t a

sse

ts

Tabreed – 2017 Investor Presentation29

• Tabreed’s current gearing is 44% (debt: debt + equity), approaching global utility peers

• 95% of debt is denominated in AED, with the balance in USD and OR, in line with cash flow generation profile

• Majority of the debt is floating rate with 60% of total debt hedged into fixed rates

• Weighted average loan life is ~5 years, with ~AED 2bn of debt maturing in 2021

Debt position as at 31 March 2017 (AED in millions)

Debt portfolio adequately hedged against interest rate increases

Borrower Type Amount (AED m)Undrawn amount

(AED m)Currency Interest Hedging (%) Maturity

Tabreed Term loan 2,702 - AED EIBOR + margin 63 2021

Tabreed Revolver 105 345 AED EIBOR + margin - 2021

Dubai Parks SPV Project

Finance

185 - AED EIBOR + margin 62 2032

ICT SPV Project

Finance

76 - AED EIBOR + margin 77 2028

Bahrain DC

Company

Term loan 125 - USD LIBOR + margin - 2019

Tabreed Oman Term loan 63 5 OR Fixed margin 100 2024

Total 3,255 350 60

Tabreed – 2017 Investor Presentation30

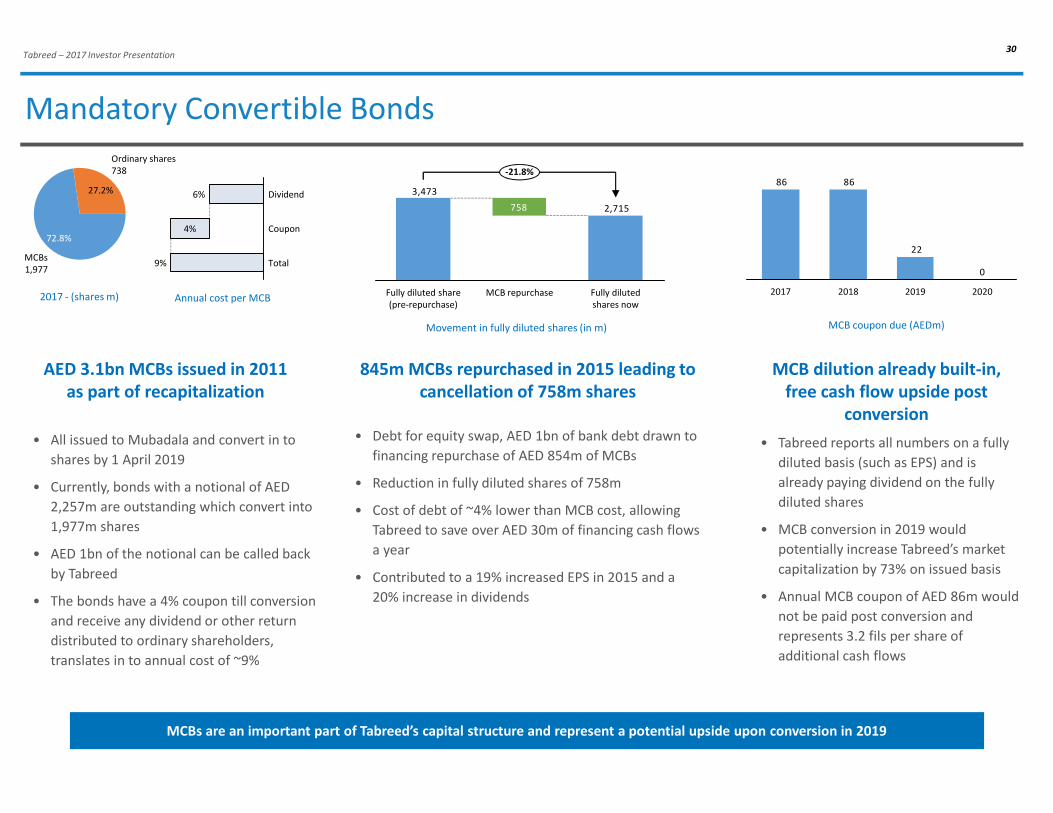

Mandatory Convertible Bonds

AED 3.1bn MCBs issued in 2011

as part of recapitalization

845m MCBs repurchased in 2015 leading to

cancellation of 758m shares

MCB dilution already built-in,

free cash flow upside post

conversion

MCBs

1,977

72.8%

Ordinary shares

738

27.2%

9%

Coupon

Total

6%

4%

Dividend

2,715

3,473

758

MCB repurchase Fully diluted

shares now

Fully diluted share

(pre-repurchase)

-21.8%

2017 - (shares m) Annual cost per MCB

Movement in fully diluted shares (in m)

• All issued to Mubadala and convert in to

shares by 1 April 2019

• Currently, bonds with a notional of AED

2,257m are outstanding which convert into

1,977m shares

• AED 1bn of the notional can be called back

by Tabreed

• The bonds have a 4% coupon till conversion

and receive any dividend or other return

distributed to ordinary shareholders,

translates in to annual cost of ~9%

• Debt for equity swap, AED 1bn of bank debt drawn to

financing repurchase of AED 854m of MCBs

• Reduction in fully diluted shares of 758m

• Cost of debt of ~4% lower than MCB cost, allowing

Tabreed to save over AED 30m of financing cash flows

a year

• Contributed to a 19% increased EPS in 2015 and a

20% increase in dividends

• Tabreed reports all numbers on a fully

diluted basis (such as EPS) and is

already paying dividend on the fully

diluted shares

• MCB conversion in 2019 would

potentially increase Tabreed’s market

capitalization by 73% on issued basis

• Annual MCB coupon of AED 86m would

not be paid post conversion and

represents 3.2 fils per share of

additional cash flows

0

22

8686

2017 20202018 2019

MCB coupon due (AEDm)

MCBs are an important part of Tabreed’s capital structure and represent a potential upside upon conversion in 2019

Tabreed – 2017 Investor Presentation31

Index

A | Overview of Tabreed

B | Business overview

C | Board of Directors and Management Team

D | Financial Performance

E | Capital Structure

F | Conclusion

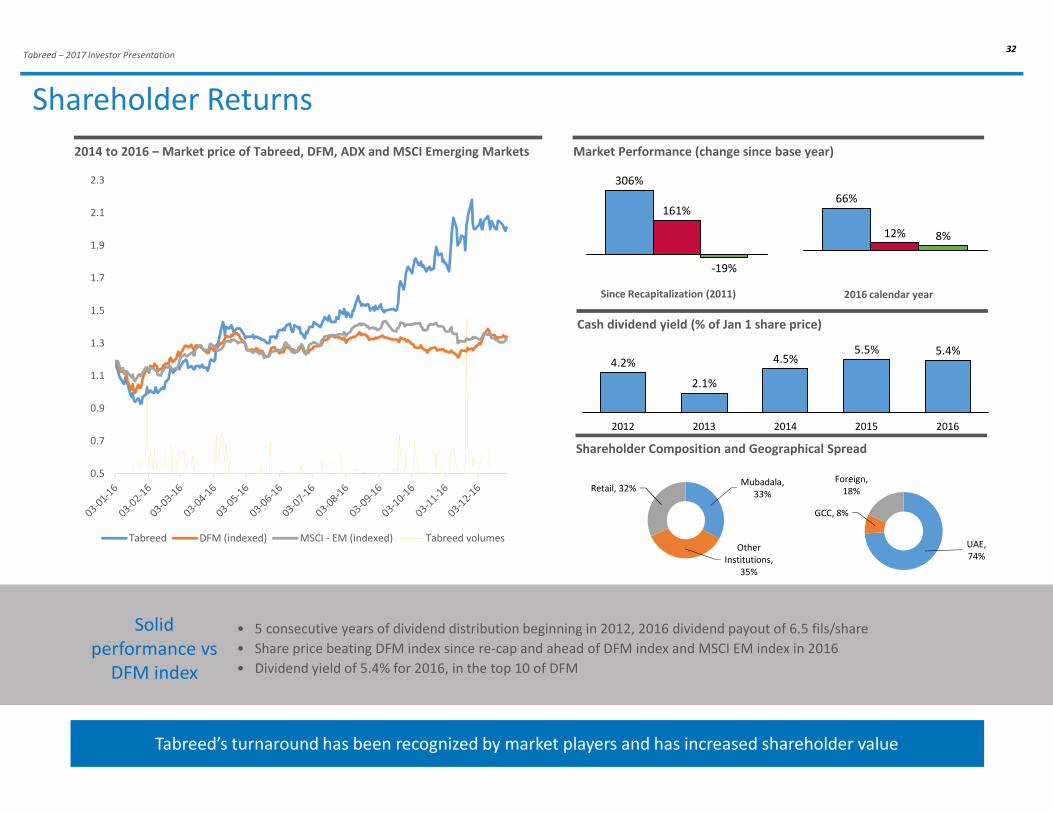

Tabreed – 2017 Investor Presentation32

-19%

161%

306%

Tabreed’s turnaround has been recognized by market players and has increased shareholder value

Shareholder Returns

• 5 consecutive years of dividend distribution beginning in 2012, 2016 dividend payout of 6.5 fils/share

• Share price beating DFM index since re-cap and ahead of DFM index and MSCI EM index in 2016

• Dividend yield of 5.4% for 2016, in the top 10 of DFM

Solid

performance vs

DFM index

4.5%

20162015

5.5%

2013 2014

2.1%

5.4%

2012

4.2%

Market Performance (change since base year)

Cash dividend yield (% of Jan 1 share price)

2014 to 2016 – Market price of Tabreed, DFM, ADX and MSCI Emerging Markets

Mubadala,

33%

Other

Institutions,

35%

Retail, 32%

UAE,

74%

GCC, 8%

Foreign,

18%

Shareholder Composition and Geographical Spread

8%12%

66%

Since Recapitalization (2011) 2016 calendar year

-

80,000,000

160,000,000

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

Tabreed DFM (indexed) MSCI - EM (indexed) Tabreed volumes

NATIONAL CENTRAL COOLING COMPANY (PJSC)

Contact usFaisal Tahir BhattiInvestor Relations

Ahmed Al NowaisCommunications

Tel: +971 2 2020336

Email: [email protected]

Tel: +971 2 2020333

Email: [email protected]

Management looks forward to engaging with shareholders and investors at the following 2017 events

SecondSecondSecondSecond quarter earnings callquarter earnings callquarter earnings callquarter earnings call End of July 2017

EFG MENA & Frontier conference, London Early September

Arqaam Investors conference,Arqaam Investors conference,Arqaam Investors conference,Arqaam Investors conference, Abu Dhabi 18 – 19 September 2017

Third quarter earnings callThird quarter earnings callThird quarter earnings callThird quarter earnings call End of October 2017

BAMLBAMLBAMLBAML MENA conference, MENA conference, MENA conference, MENA conference, Dubai 15 – 16 November 2017

YearYearYearYear end earnings callend earnings callend earnings callend earnings call End of January 2018

Tabreed – 2017 Investor Presentation34

APPENDICES

34

Tabreed – 2017 Investor Presentation35

Stable core business model delivering consistent performance

Capacity (fixed) Consumption

(variable)

Total

Revenue, net of amortization 64 36 100

Utility Costs - (32) (32)

Plant operation & maintenance (9) - (9)

Depreciation (11) - (11)

Gross Profit 44 4 48

Corporate overheads (16) - (16)

Profit from Operations 28 4 32

Add back: depreciation & amortisation 16 - 16

EBITDA 44 4 48

68% 12% 48%

Profit Statement (% of revenue) – based on 2016 results

64% of the revenue is

fixed

Stable and predictable earnings - 91% of EBITDA arises from capacity charges

• Tabreed bills customers for capacity (fixed) charges and consumption (variable) charges

• Capacity charges reflect the cooling capacity (in RT) reserved for the customer and are

generally fixed, subject to escalation based on country CPI every year

• Consumption charges recover the cost of cooling consumed. Contractually, any change in

variable cost is generally passed through to the customers

• Tabreed’s EBITDA is driven by capacity charges allowing recovery of plant operation cost,

corporate overheads and providing a strong return on capital invested

Billing structure and profitability

36%64%

ConsumptionCapacity

61%39%

9%91%

Only 39% of the cost is

against fixed revenue,

rest is passed through

Hence, 91% of the

EBITDA is from capacity

revenue

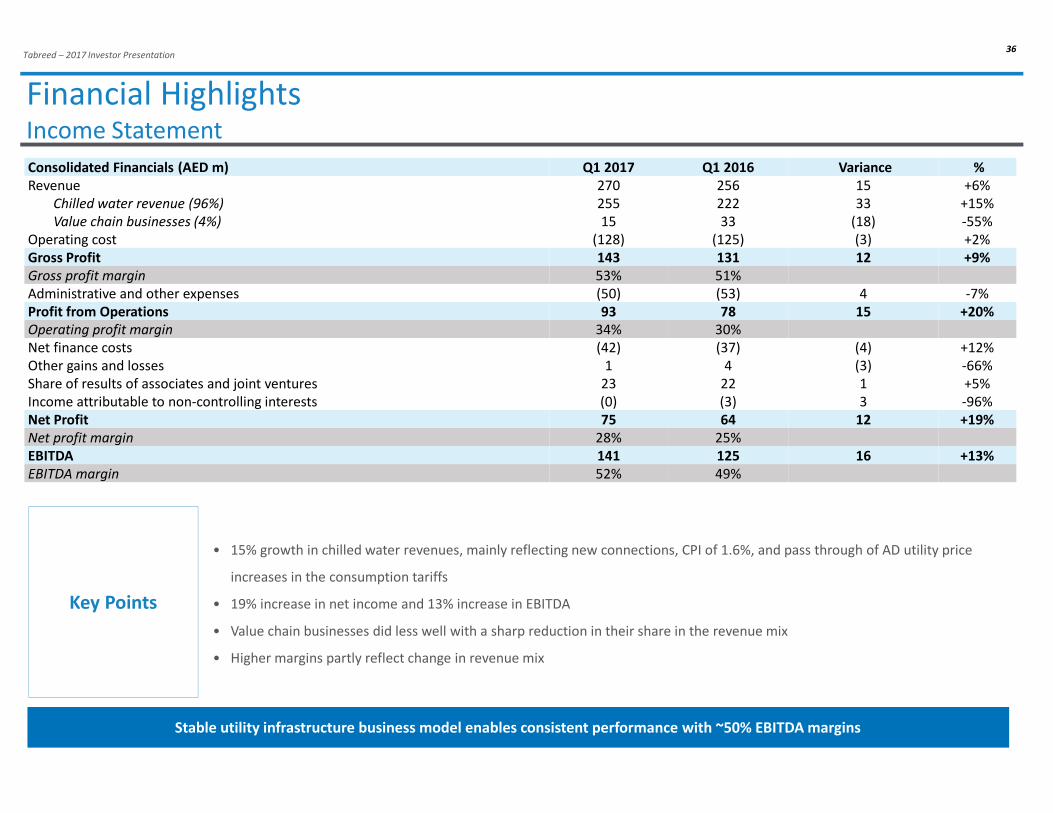

Tabreed – 2017 Investor Presentation36

Financial HighlightsIncome Statement

Key Points

• 15% growth in chilled water revenues, mainly reflecting new connections, CPI of 1.6%, and pass through of AD utility price

increases in the consumption tariffs

• 19% increase in net income and 13% increase in EBITDA

• Value chain businesses did less well with a sharp reduction in their share in the revenue mix

• Higher margins partly reflect change in revenue mix

Stable utility infrastructure business model enables consistent performance with ~50% EBITDA margins

Consolidated Financials (AED m) Q1 2017 Q1 2016 Variance %

Revenue 270 256 15 +6%

Chilled water revenue (96%) 255 222 33 +15%

Value chain businesses (4%) 15 33 (18) -55%

Operating cost (128) (125) (3) +2%

Gross Profit 143 131 12 +9%

Gross profit margin 53% 51%

Administrative and other expenses (50) (53) 4 -7%

Profit from Operations 93 78 15 +20%

Operating profit margin 34% 30%

Net finance costs (42) (37) (4) +12%

Other gains and losses 1 4 (3) -66%

Share of results of associates and joint ventures 23 22 1 +5%

Income attributable to non-controlling interests (0) (3) 3 -96%

Net Profit 75 64 12 +19%

Net profit margin 28% 25%

EBITDA 141 125 16 +13%

EBITDA margin 52% 49%

Tabreed – 2017 Investor Presentation37

Financial HighlightsFinancial Position

Key Points

• Accounts receivables have increased due to short-term timing delays in customer collections

• Reduction in cash primarily reflects payment made to ICT to complete acquisition of Nation Towers plant

• Increase in liability balances reflect recording of 2017 dividend of 6.5 fils

Balance sheet continues to show strength and positions Tabreed to finance further growth

Consolidated Financials (AED m) 2017 2016 Variance %

Fixed Assets 6,954 6,977 (22) -0%

Associates and Joint Ventures 836 826 10 +1%

Accounts Receivable 478 409 69 +17%

Cash and Short Term Deposits 258 390 (132) -34%

Other Assets 62 60 2 +4%

Total Assets 8,588 8,661 (73) -1%

Equity and Reserves 2,566 2,666 (100) -4%

Mandatory Convertible Bonds – equity portion 1,773 1,773 - +0%

Debt 3,383 3,424 (41) -1%

Other Liabilities 867 799 68 +9%

Total Liabilities and Equity 8,588 8,661 (73) -1%