2017 ANNUAL REPORT Citibank Nigeria Limited · What You Can Expect from Us and What We Expect from...

162

2017 ANNUAL REPORT Citibank Nigeria Limited

Transcript of 2017 ANNUAL REPORT Citibank Nigeria Limited · What You Can Expect from Us and What We Expect from...

© 2017 Citibank, N.A. All rights reserved. Citi and Arc Design is a trademark and service mark of Citigroup Inc., used and registered throughout the world.

GRA00000 00/00

CIT

IBA

NK

NIG

ER

IA L

IMIT

ED

| 20

17 A

nn

ua

l Re

po

rt

2017 ANNUAL REPORT Citibank Nigeria Limited

Citi’s Value Proposition: A Mission of Enabling Growth and Progress

What You Can Expect from Us and What We Expect from Ourselves

Citi’s mission is to serve as a trusted partner to its clients by responsibly providing financial services that enable growth and economic progress. Our core activities are safeguarding assets, lending money, making payments and accessing the capital markets on behalf of our clients. We have 200 years of experience in helping our clients meet the world’s toughest challenges and embrace its greatest opportunities. We are Citi, the global bank — an institution connecting millions of people across hundreds of countries and cities.

We protect people’s savings and help them make the purchases — from everyday transactions to buying a home — that improve the quality of their lives. We advise people on how to invest for future needs, such as their children’s education and their own retirement, and help them buy securities, such as stocks and bonds.

We work with companies to optimise their daily operations, whether they need working capital to make payroll or export their goods overseas. By lending to companies large and small, we help them grow, creating jobs and real economic value at home and in communities around the world. We provide financing and support to governments at all levels so they can build sustainable infrastructure, such as housing, transportation, schools and other vital public works.

These capabilities create an obligation to act responsibly, do everything possible to create the best outcomes and prudently manage risk. If we fall short, we will take decisive action and learn from our experience.

We strive to earn and maintain the public’s trust by constantly adhering to the highest ethical standards. We ask our colleagues to ensure that their decisions pass three tests: they are in our clients’ interests, create economic value and are always systemically responsible. When we do these things well, we make a positive financial and social impact in the communities we serve and show what a global bank can do.

2017 ANNUAL REPORT

1

CEO Remarks

The Nigerian economy emerged from recession during the second quarter of 2017, thus ending five consecutive quarters of

contraction. This turnaround was driven by improved foreign exchange stability, higher oil production volumes and prices as

well as an overall improvement in the security situation in the country. Citibank Nigeria Limited was able to operate successfully

within this improved operating environment by continuing to provide best-in-class solutions to customers, thus helping them

navigate the persistently fluid economic realities. The bank also continued to focus on improved service delivery as a way to

deepen existing customer relationships and build new alliances while clearly differentiating ourselves in the domestic market.

In the year ahead, we expect the economy to sustain, and even accelerate, its recovery as the government promotes policies

that maintain economic stability and continue to drive its “Ease Of Doing Business” initiative. As Nigeria navigates the volatile,

and often competing, pressures of a changing global economy and its urgent domestic economic imperatives, Citibank Nigeria

Limited will be sure to remain committed to its core objective of enabling growth and progress for our customers. This will be

done by leveraging our unique positioning to deliver innovation, upgrade our services and put the bank’s global network at the

disposal of our clients and stakeholders. Citi remain committed to our role as partners in Nigeria’s economic progress as we

continue to work with both private and public sector entities in the country to develop the market and improve its financial

infrastructure.

Here is to a successful 2018!

Akinsowon Dawodu

Chief Executive Officer,

Citibank Nigeria Limited

Akinsowon DawoduChief Executive Officer

2017 ANNUAL REPORT

2

CEO’s Remarks

Table of Contents

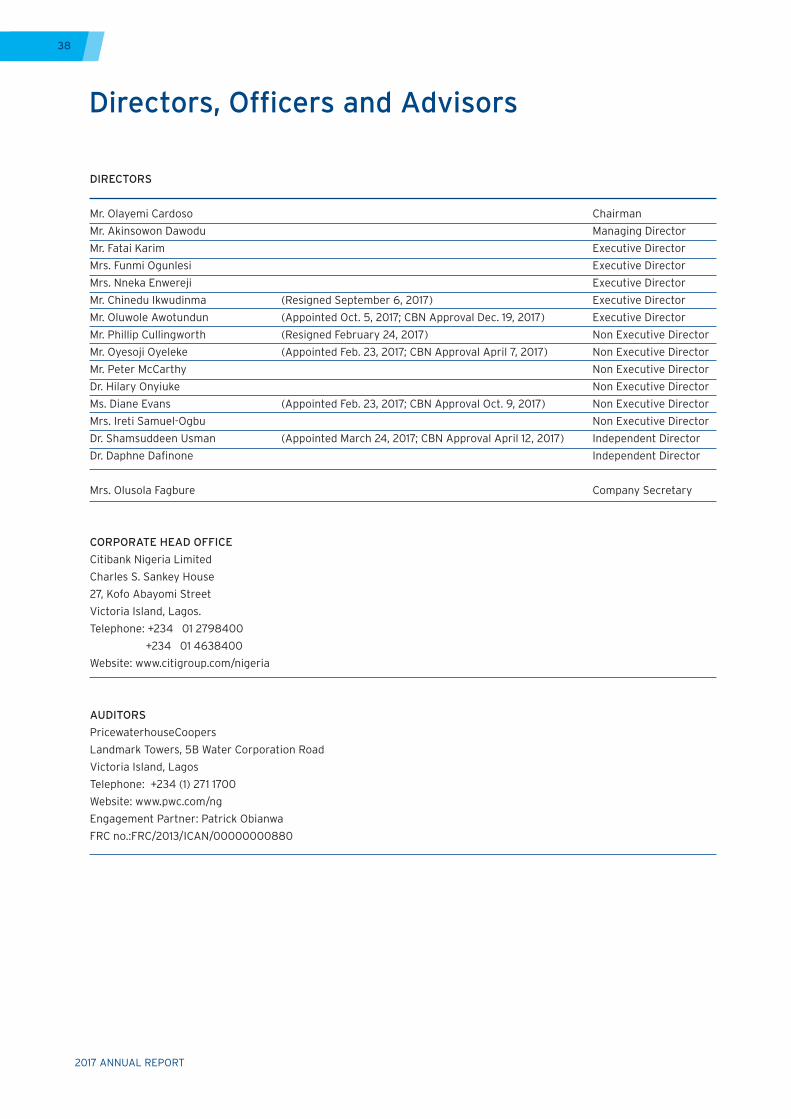

Board of Directors

Management Committee

Annual General Meeting Notice

Chairman’s Statement

Sustainability Report

Business Report

Corporate and Investment Banking

Risk Management

Treasury and Trade Solutions

Global Subsidiaries Group

Direct Custody and Clearing

Operations and Technology

Human Resources

Markets

Employee of the Year

Financial Report

2017 in Pictures

1

2

3

4

5

6

14

18

20

22

24

26

28

30

32

34

35

36

156

Contents

2017 ANNUAL REPORT

3

Olayemi CardosoChairman

Dr. Daphne Dafinone Mr. Oyesoji Oyeleke

Mr. Akin Dawodu

Mr. Peter McCarthy

Dr. Shamsudeen Usman

Mrs. Ireti Samuel-Ogbu

Ms. Diane Evans

Dr. Hilary Onyiuke

Mr. Fatai Karim Mrs. Nneka EnwerejiMrs. Funmi Ogunlesi

Mr. Oluwole Awotundun Mrs. Olusola FagbureCompany Secretaryand Legal Adviser

Board of Directors

2017 ANNUAL REPORT

3

2017 ANNUAL REPORT

4

Mr. Akin Dawodu Managing Director and CEO

Mr. Oluwole Awotundun Executive Director and Country Risk Manager, Nigeria, West and Central Africa

Mrs. Aderonke Adetoro Securities Country Manager

Mr. Gboyega Oloyede Country Human Resources Officer

Mrs. Funmi Ogunlesi Executive Director and Head of Treasury and Trade Solutions Public Sector, Africa

Mr. Segun Adaramola Head of Treasury and Trade Solutions

Mr. Sharaf Muhammed Chief Finance Officer and Head of Strategy & Sustainability

Ms. Chidinma Ohajunwa Head of Operational Risk Management

Mr. Fatai Karim Executive Director and Head of Treasury and Trade Solutions Client Operations SSA

Mr. Bayo Adeyemo Country Treasurer and Head of Markets

Mrs. Ngozi Omoke-Enyi Head of Operations and Technology

Mrs. Sola Fagbure Country Counsel and Company Secretary

Mr. Bolaji Ajao Head of Internal Audit

Mrs. Lola Oyeka Country Public Affairs Officer

Mrs. Nneka Enwereji Executive Director and Head of Global Subsidiaries Group

Mr. Mudassir Amray Head of Corporate and Investment Bank

Ms. Shola Phillips Country Compliace Officer

Management Committee

2017 ANNUAL REPORT

4

2017 ANNUAL REPORT

5

Annual General Meeting Notice

NOTICE IS HEREBY GIVEN THAT THE THIRTY FOURTH ANNUAL GENERAL MEETING OF THE MEMBERS OF CITIBANK

NIGERIA LIMITED WILL BE HELD AT CHARLES S. SANKEY HOUSE, 27, KOFO ABAYOMI STREET, VICTORIA ISLAND, LAGOS

ON THURSDAY APRIL 19 2018 AT 1.00 P.M. FOR THE TRANSACTION OF THE FOLLOWING BUSINESS:

ORDINARY BUSINESS:

1. To receive the Report of the Directors, the Balance Sheet as at 31st December, 2017 together with the Profit and Loss

Account for the year ended on that date and the Report of the Auditors thereon.

2. To declare a dividend.

3. To re-elect Directors.

4. To authorize the Directors to fix the remuneration of the Auditors.

SPECIAL BUSINESS:

To receive the Report on the Board performance review conducted by Ernst & Young.

BY ORDER OF THE BOARD

OLUSOLA FAGBURE

Company Secretary

Dated this 15th day of March 2018

Charles S. Sankey House

27, Kofo Abayomi Street

Victoria Island, Lagos.

NOTE

A member of the Company entitled to attend and vote at the above meeting is entitled to appoint a proxy to attend and vote

instead of him and such proxy need not also be a member. A form of proxy is enclosed and if it is to be valid for the purposes

of the meeting, it must be completed and deposited at the registered office of the Company not less than 48 hours before the

time for holding the meeting.

2017 ANNUAL REPORT

6

Chairman’s Statement

Macroeconomic Overview

World EconomyThe pace of global economic growth picked up in 2017 with the world economy growing by about 3.6% compared to a growth of 3.2% in 2016. This momentum was driven by a combination of sustained growth in advanced economies and a continued recovery in emerging market economies that had previously been affected by the slump in commodity prices and various fiscal pressures.

Across advanced economies, stronger than expected domestic demand and supportive external demand led to stronger than expected growth in 2017. In the US, a weakness in consumption in the first quarter of the year proved to be temporary as consumption and business investment recovered

substantially for the rest of the year. Overall, the US economy grew by about 2.2% in 2017 compared to a growth of 1.5% in 2016. Similarly, economic growth in the Euro Area, despite Brexit negotiations, was also stronger at 2.1% in 2017. Much of this growth was led by a combination of stronger consumption and rising external demand for exports. The ongoing Quantitative Easing program and negative interest rate environment also remained vital clogs in the growth catalyst for the Euro Area. Similarly the Bank of Japan’s negative interest rate, continuing Quantitative Easing program and cap on long-term interest rates helped spur GDP growth in Japan to 1.5% in 2017 from 1.0% in 2016. Overall, advanced economies contributed significantly to the uptick in global growth in 2017.

Growth in emerging and developing economies was supported by a resilient Chinese economy and recoveries in key emerging economies including Brazil and Russia that had begun the year in recessions. China, after a slowdown in growth in 2016, grew by about 6.8% in 2017 driven by rapidly accelerating household consumption. Despite concerns about fiscal instability, high government debt and government transparency, growth in the Chinese economy remains ahead of most expectations. Meanwhile, Brazil finally came out of its longest and deepest recession on record following rising exports and growing domestic demand spurred by aggressive interest rate cuts by its central bank. The political turmoil in Brazil is however likely to weigh on more rapid growth in

Citibank Nigeria Limited and present to you its financial results and key achievements during the year 2017. Citibank Nigeria Limited continues to grow and make progress by creating sustained value for customers, employees, and shareholders of the bank.

Olayemi CardosoChairman

Fellow shareholders, members of the board of directors, distinguished ladies and gentlemen.

I am pleased to welcome you to the 34th Annual General Meeting of

2017 ANNUAL REPORT

7

2018. In Russia, higher oil prices and relative macroeconomic stabilization returned the Russian economy to growth in 2017. The Russian economy grew by about 1.8% in 2017 compared to a 0.2% contraction in 2016. The emerging economies rhetoric in 2018 will likely focus on whether the individual economic recoveries can be sustained and backed by supportive fiscal, monetary, and economic policy.

Sub-Saharan African EconomyIn Sub-Saharan Africa, growth accelerated to about 2.6% in 2017 after a slowdown to 1.5% in 2016. This growth is still under the 3.1% in growth recorded in 2015. Most of this growth was attributable to the positive response of Sub-Saharan Economies to various external pressures such as weak commodity prices, reduced capital inflows, and depreciating currencies. Favorable commodity export prices for oil, agricultural inputs and other commodities led to increased economic output and stronger currency buffers in many SSA countries. In South Africa, growth increased mildly to

about 0.7% in 2017 from 0.3% in 2016 despite an uncertain political climate; uncertainty that may weigh on growth again in 2018. In Angola, similar to Nigeria and many other oil producing Sub-Saharan economies, higher oil prices led to improved economic growth in 2017 and point to improved economic growth prospects in 2018 as well.

Global trade also picked up in 2017 reflecting a recovery in global demand and capital spending. This is a positive development for Sub-Saharan Africa due to the accompanying effect it will have on commodity prices and investment inflows as foreign capital seeks higher yield. Despite steps towards the normalization of monetary policy in advanced economies such as the US, UK, and Euro Area, yields in Sub-Saharan Africa will remain attractive to investors and investments in 2018. Furthermore, with OPEC and Russia agreeing to extend oil output cuts until the end of 2018, Sub-Saharan Africa growth will likely be sustained in 2018. However, cogent downside risks such as uncertain or inadequate government policies, rising fiscal

imbalances, and idiosyncratic factors could curtail growth prospects significantly in 2018.

Nigerian EconomyNigeria took positive steps towards full economic recovery in 2017 with the result that the economy grew by 0.8% during the year, following a contraction of 1.5% in 2016. Output was buoyed by a strong showing in the energy sector following the rise in oil prices and oil production in the second half of the year. Activity in the manufacturing and services sectors however remained weak during the year, highlighting what should be considered a very fragile recovery from the country’s recession.

The agricultural sector however continues to grow, albeit at a slowing pace. The Agricultural sector is expected to continue dominating the country’s efforts to diversify away from its dependence on Oil. Based on data from the National Bureau of Statistics, this sector now contributes about 26% to overall GDP compared to a 10% contribution by the Oil sector. The growth in agricultural

CHAIRMAN’S STATEMENT

2017 ANNUAL REPORT

2017 ANNUAL REPORT

8 CHAIRMAN’S STATEMENT

sector has been sustained by favorable government policies that have enhanced access to credit, fertilizers, and consumer markets. In addition the sector has benefited from the increasing focus on import substitution which has helped bolster agricultural production.

As at December 2017, Nigeria’s foreign currency reserves had increased by 52% to USD 38 billion from USD 25 billion in 2016. This increase in reserves was driven by the significant external borrowing undertaken in 2017 and rising oil export revenue. The Federal Government raised $4.8 billion in external debt via bonds in 2017, in line with its strategy to substitute expensive domestic borrowing for cheaper foreign debt. The increase in reserves helped enable a more stable management of foreign currency domestically for trade. This development, in combination with the introduction of the Importers and Exporters NAFEX window in April helped to stabilize the exchange rate and played a part in the eventual economic recovery. However, despite the short-term

positive effects, there are concerns about the sustainability of Nigeria’s debt profile as debt servicing costs represents an increasing proportion of government revenues.

Inflation moderated in 2017, slowing to an average of 15.8% compared to an average of 18.6% in 2016. Part of this moderation should be attributed to the already high base prices in 2016, however the slowdown is welcome overall. Despite the moderating inflation, the CBN maintained its key monetary benchmark rate at 14.0% throughout the year, retaining an asymmetric corridor of +2%/-5% around the MPR. Other monetary policy tools were also kept constant with the apex bank prioritizing a stable monetary policy environment. Looking forward, five members of the current Monetary Policy Committee are set to leave their positions at the start of 2018. These changes, amidst a general clamor for easing monetary policy in 2018, introduce further uncertainty regarding the direction of monetary policy in 2018.

In terms of regulation, the introduction of an Investors’ and Exporters’ foreign exchange Window and revised import and export documentation guidelines are some examples of regulatory changes that affected the foreign exchange and trade markets. Other key regulations introduced in 2017 include an Agri-Business/Small and Medium Enterprises Investment Scheme (AGSMEIS) into which all Banks are required to contribute 5% of their annual profits, and the ongoing implementation of IFRS 9 (Financial Instruments) for enhanced reporting. Citibank Nigeria Limited continues to comply with all relevant directives.

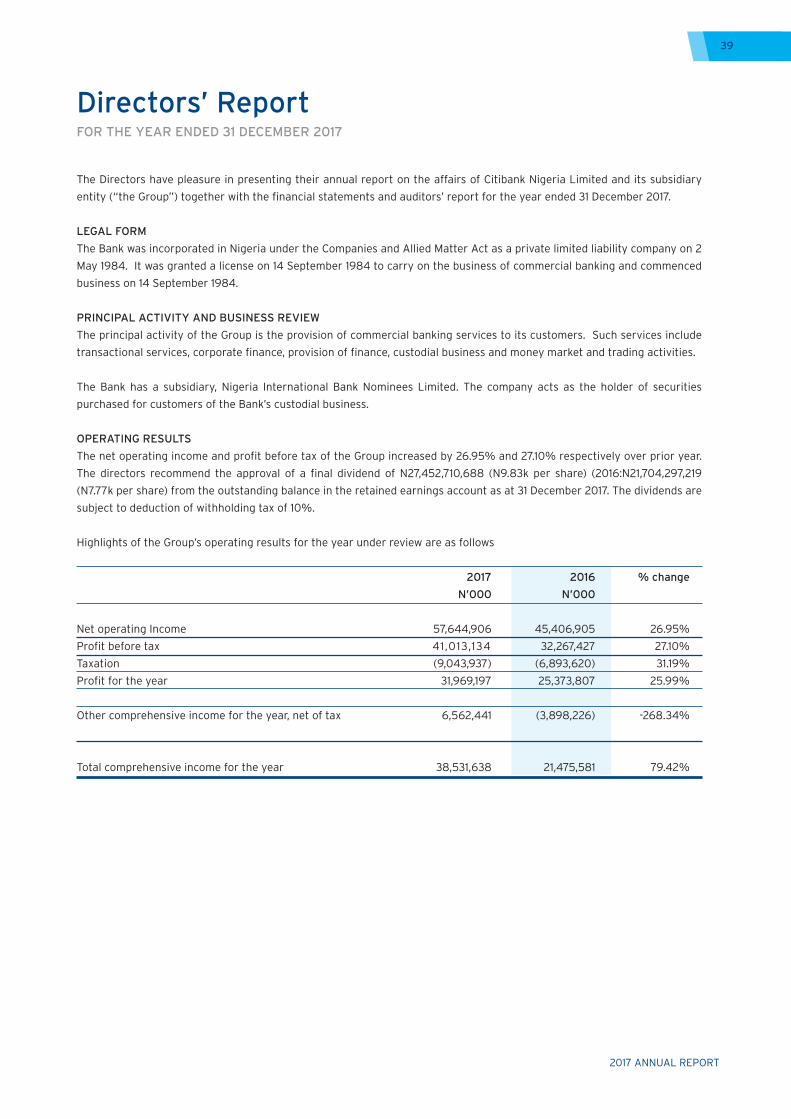

Financial Performance 2017

Maintaining its growth trajectory from the year before, Citibank Nigeria Limited, in 2017, recorded improved financial performance with gross earnings increasing by 24.9% to N66.8 billion compared to N53.5 billion in 2016. Net operating income after loan impairment charges was N57.6 billion, an

2017 ANNUAL REPORT

2017 ANNUAL REPORT

9CHAIRMAN’S STATEMENT

increase of 26.9% from N45.4 billion in 2016, while operating expenses increased by 27.3% to N16.8 billion from N13.2 billion recorded in the prior year. Overall, profit before tax for the year rose by 26.9% to N41.0 billion from N32.3 billion the prior year, while profit after tax increased by 26.0% to N32.0 billion compared to N25.4 billion in 2016. Another year of strong profit growth reflects not only our increased efforts to be the partner of choice for our clients, but also a proactive risk management focus that enabled us minimize credit impairments during a difficult economic year. The total assets on our balance sheet closed the year 2017 at N596 billion compared to N604 billion in the prior year. The Return on Assets and Return on Equity increased in 2017 to 5.4% (2016: 4.2%) and 39.7% (2015:35.2%) respectively.

Citibank Nigeria Limited is in compliance with the Central Bank of Nigeria Basel II regulatory capital guidelines of the CBN and remains well capitalized with a Capital Adequacy Ratio of 28.3%, which is

significantly above the minimum regulatory requirement of 10.0%. Our Liquidity ratio of 76.5% at the end of 2017 was also well above the CBNs minimum requirement of 30.0%.

The 2017 financial results reflect the significant dedication and efforts of all employees and stakeholders of the bank to respond in a gradually improving economic environment. These are very commendable results as Citibank Nigeria Limited has shown improvement across major business segments. Overall, Citibank Nigeria Limited is adequately capitalized and well positioned to take advantage of opportunities to support business expansion, deepen relationships and provide tailored advice for its customers in the year ahead.

Notable Events and Activities

Citi is committed to building capacity amongst its key stakeholders and taking advantage of its global resources to strengthen the knowledge base in the financial

industry through various events and/or trainings. Some of these notable evens included:

Direct Custody and Clearing (DCC) seminar – a one-day event that brought together market regulators, asset managers , financial, advisory and legal experts, custodians, stock exchange and other industry experts to discuss and explore the Nigerian asset custody ecosystem viz a viz international best practices..

Citi China Day – the second edition of Citi’s annual China Day brought together a number of high-profile industry participants. Following the growing bilateral trade and strategic co-operation between China and Nigeria and taking into consideration Citi’s focus on emerging markets, it became important and expedient for Citi Nigeria to pay the same level of special attention to this economic group of investors. The event created an enabling platform

2017 ANNUAL REPORT

2017 ANNUAL REPORT

10 CHAIRMAN’S STATEMENT

for Chinese corporations to get a better understanding of the Nigerian business environment, recent regulatory changes, macroeconomic developments and government policy direction. It also created an opportunity for the Chinese business community in Nigeria to engage with economic and banking thought leaders and imbibe best practices that Citi has deployed globally.

Cash & Trade Seminar - a week-long event for banking industry professionals. The seminar had over 45 participants from various banks in the industry. The course is designed to provide both intermediate analysis of international cash & trade policies and processes and an insight into current global developments and emerging trends. The forum also provides an excellent opportunity for interactive discussions between key operators in the local market. The primary facilitator was Mr. Parvez Todiwala a renowned Senior Trade Advisor

from Citi EMEA Trade Advisory and Trainer with experience in International trade and payments.

Accion Microfinance Bank (Accion MFB) loan - Citi Nigeria extended a loan of NGN500 million to Accion Microfinance Bank (Accion MFB) in Nigeria to drive and promote the development of the microfinance sector in Nigeria. This loan will fund Accion’s loan portfolio and support the development of approximately five thousand micro and small enterprises in the country. The agreement will also support the Central Bank of Nigeria’s National Financial Inclusion Strategy (NFIS) to reduce the proportion of excluded population by bringing them into the formal banking fold. As at 2012, according to a survey by the Enhancing Financial Innovation and Access (EFInA), about 39.7% or 34.9 million adult Nigerians were excluded from financial services.

Citi Tech for Integrity (T4I) Activation Event – T4I is a landmark effort to encourage technology innovators from around the world to create cutting-edge solutions to promote integrity, accountability and transparency in the public sector and beyond. The Activation Event in Nigeria was co-hosted by Techpreneur Africa and saw over 80 attendees, including accelerators, tech companies, and innovation hubs. T4I allies present included Techpreneur Africa, International Finance Corporation, PwC, Ventures Platform, and Startup52.

Citi Journalistic Excellence Award (CJEA) – a global Citi competition which began as a way of recognizing journalists for excellence in financial and business reporting in the markets in which Citi does business around the world. The CJEA is a unique program sponsored and co-hosted by Citi and Columbia’s Graduate School of Journalism, with

2017 ANNUAL REPORT

2017 ANNUAL REPORT

11CHAIRMAN’S STATEMENT

nominees selected by an independent panel of judges. Caleb Ojewale, Multimedia News Content Producer, BusinessDay Nigeria and winner of the 2017 award, joined other winners from across the world to participate in an 8-day business and financial seminar in New York City. The program offers participants rigorous workshops in the principles of accounting and finance, and exposure to institutions, policy makers, and other thought leaders in the United States.

Citi Financial Journalist Training (CFJT) – a capacity building initiative that was pioneered in Nigeria which provides training and a multi-party dialogue on financial concepts. Citi collaborated with the School of Media and Communication Pan-Atlantic University (PAU) in 2017 and hosted a total of 17 national business and financial journalists in the 3-Day training. Facilitators included Faculty from the School of Media

and Communication PAU, the Central Bank of Nigeria, Ms. Bunmi Lawson the former MD/CEO of Accion Microfinance Bank Nigeria Limited, Mrs. Hansatu Adegbite ED, Women in Management, Business and Public Service (WIMBIZ), and Citi Nigeria Senior Management.

Awards and Recognitions

Citi’s continued focus as trusted banking partner to its target market paid off as was evident in the numerous awards received. Some of the notable awards received in 2017 included:• GlobalFinanceMagazineAwards

2017 Best Corporate/Institutional Digital Bank in Nigeria.

• EuromoneyBestCashManagement Bank for Nigeria - for over 10 years in a row.

• LifetimeAchievementAward–African Banker Awards (2017)

• GlobalEuromoneyAwardsforExcellence 2017 - Best Digital Bank, Best Bank for Financial Inclusion, Best Bank for Markets, Best Bank for Transaction Services (2016 & 2017)

Corporate Citizenship

We continue to applaud the efforts of our non-profit partners such as Junior Achievement, Technoserve, LEAP Africa, United States African Development Foundation who, alongside Citi, continue to promote economic progress and improve the lives of people in low-income communities around Nigeria. Our combined efforts have seen an increase in financial inclusion, job opportunities for the youth and innovative approaches to building an economically vibrant nation.

Citi also celebrated its 12th annual Global Community Day as more than 1,600 Citi volunteers in Aba, Abuja, Kano, Lagos, Port-Harcourt and Warri lead sporting activities, financial literacy and entrepreneurship workshops, and donated supplies in their local communities. Various community partners joined the volunteer efforts. For the second year in a row

2017 ANNUAL REPORT

2017 ANNUAL REPORT

12

IHS Nigeria, a Citi client, Bloomberg Media Initiative Africa (BMIA) alumni and Junior Achievement Nigeria (JAN) joined the Lagos events.

Citibank Nigeria Limited hosted its Community Partner (Cheque) Presentation in Lagos to honour the 18 Community Partners in Lagos. Attendees at the Lagos event included SOS Children’s Village, Down Syndrome Association of Nigeria Atunda Olu School (For Physically Handicapped Children), Bethesda Child Support Agency, The Book Trust Wesley School 1 and 2 for the deaf, Pacelli School for the blind, Care Organization Public Enlightenment (COPE), Sickle Cell Foundation, Heart of Gold Children’s Hospice, Nigerian Red Cross Society and the Office of the United Nations High Commissioner for Refugees (UNHCR).

A new partnership was launched between the Citi Foundation and the International Rescue Committee (IRC) that will provide young people displaced within their own countries

and vulnerable youth from the communities hosting them with support to help them generate a reliable income and contribute to their local economy. Throughout the two-year project, Rescuing Futures, young people in Yola, Nigeria, will be supported to start their own businesses.

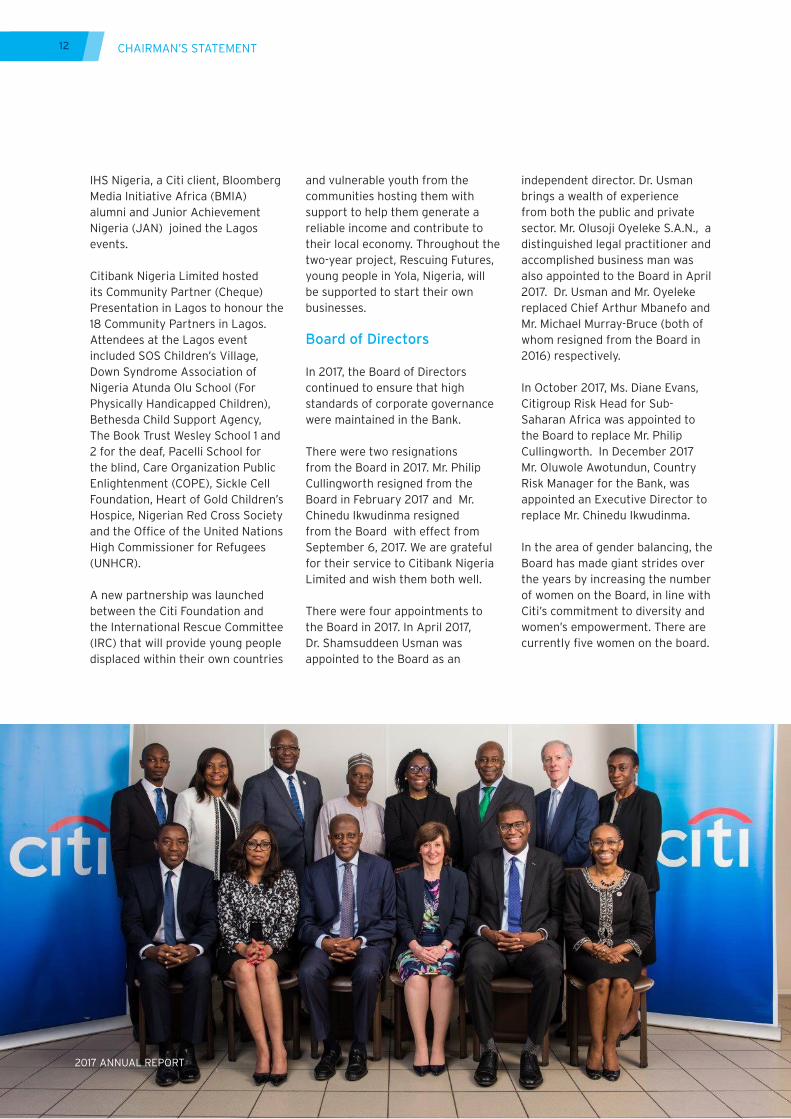

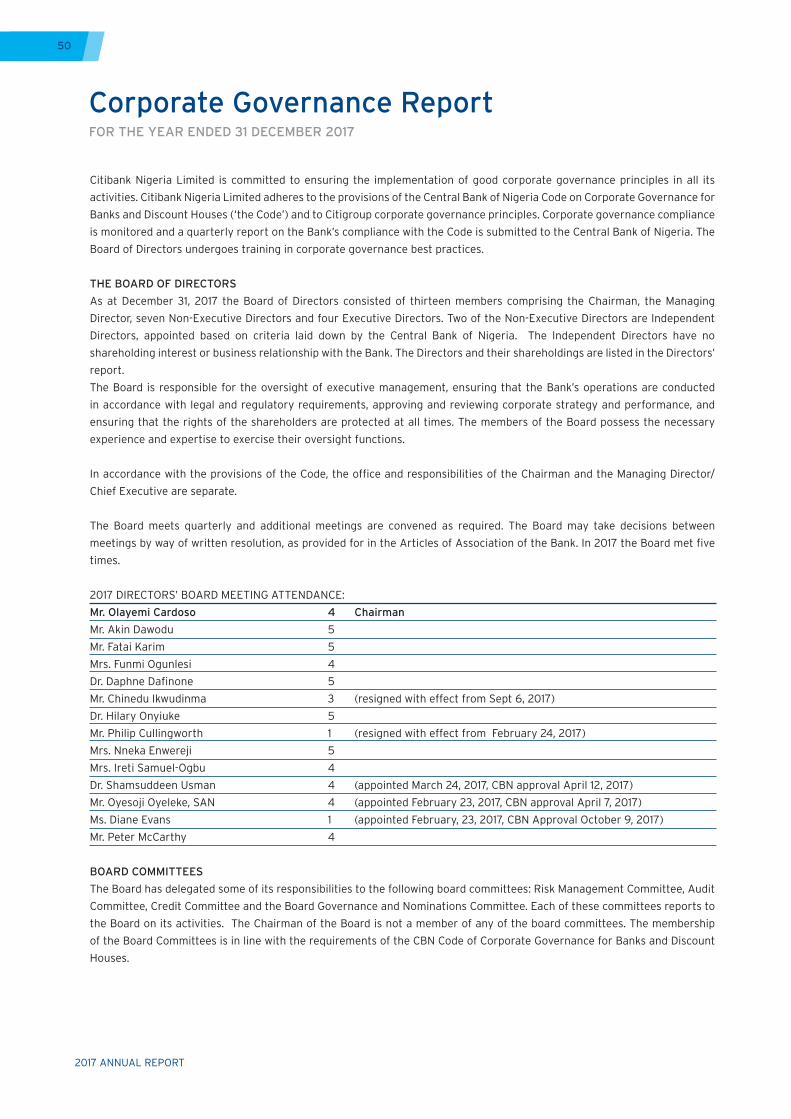

Board of Directors

In 2017, the Board of Directors continued to ensure that high standards of corporate governance were maintained in the Bank.

There were two resignations from the Board in 2017. Mr. Philip Cullingworth resigned from the Board in February 2017 and Mr. Chinedu Ikwudinma resigned from the Board with effect from September 6, 2017. We are grateful for their service to Citibank Nigeria Limited and wish them both well.

There were four appointments to the Board in 2017. In April 2017, Dr. Shamsuddeen Usman was appointed to the Board as an

independent director. Dr. Usman brings a wealth of experience from both the public and private sector. Mr. Olusoji Oyeleke S.A.N., a distinguished legal practitioner and accomplished business man was also appointed to the Board in April 2017. Dr. Usman and Mr. Oyeleke replaced Chief Arthur Mbanefo and Mr. Michael Murray-Bruce (both of whom resigned from the Board in 2016) respectively.

In October 2017, Ms. Diane Evans, Citigroup Risk Head for Sub-Saharan Africa was appointed to the Board to replace Mr. Philip Cullingworth. In December 2017 Mr. Oluwole Awotundun, Country Risk Manager for the Bank, was appointed an Executive Director to replace Mr. Chinedu Ikwudinma.

In the area of gender balancing, the Board has made giant strides over the years by increasing the number of women on the Board, in line with Citi’s commitment to diversity and women’s empowerment. There are currently five women on the board.

Arument ut apienis eos erit, illuptatem quaeper oribus sinimincim esci asitat. Sum aut ipiet, volupta sendand andaest. Musciume il magni conse corpostiores eaque

Arument ut apienis eos erit, illuptatem quaeper oribus sinimincim esci asitat. Sum aut ipiet, volupta sendand andaest. Musciume il magni conse corpostiores eaque

CHAIRMAN’S STATEMENT

2017 ANNUAL REPORT

2017 ANNUAL REPORT

13

Conclusion

Please permit me to extend, on your behalf, our heartfelt appreciation to the management and staff for their continued commitment to Citibank Nigeria Limited and for another year of growth.

I also wish to express my appreciation to the shareholders of Citibank Nigeria Limited for their constant support and encouragement over the course of the last year. Your contributions are highly valuable and have played a major role in the continued success of our bank.

In conclusion, I offer my gratitude to

my colleagues and fellow members of the Board of Directors. Your cooperation, wisdom, loyalty and hard work have immeasurably contributed to the success and continued development of Citibank Nigeria Limited. As we look to the future, I say congratulations to all of you on another excellent year.

Olayemi CardosoChairman

CHAIRMAN’S STATEMENT

2017 ANNUAL REPORT

2017 ANNUAL REPORT

14

Sustainability Report 2017

Citi Nigeria Limited has a long standing commitment to conduct business in a manner consistent with the Citigroup core principle of Responsible Finance. Citigroup has an Environmental and Social Advisory Council that provides guidance on environmental and social issues related to global business activities. This council is co-chaired by executives in our Institutional Clients Group and includes executives from Banking, Risk, Public Affairs, Operations, Corporate Sustainability, and specialists in the Environmental and Social Risk Management (ESRM) team. This council advises on Citigroup’s ambitious Sustainable Progress Strategy which aims to incorporate sustainability principles into everything we do and facilitate $100 billion in environmental finance activities globally; a goal we committed to in 2014.

Citi Nigeria is an inextricable part of this sustainability mission. The world is moving at a rapid pace toward cleaner, more sustainable sources of energy and businesses around the world are leading the way with new ideas, plan and projects. Citi is proud to deliver both the investments and finance required to bring these ideas, plans, and projects to reality. We recognize that sustainability issues could impact the viability of projects, ability of a potential customer to fulfill its obligations to the firm, and, ultimately, Citi’s reputation. As a result, we pro-actively assess covered transactions in line with our Sustainability Vision.

Citi Nigeria Limited’s sustainability vision entails conducting business in an environmentally and socially responsible manner. In addition to making good business sense, this is consistent with our goal of being a good corporate citizen sensitive to the communities in which we do business. This belief, reflected in our dedication to financing environmental business opportunities, actively managing

environmental and social risks, reducing our operational footprint, and managing our supply chain, is aligned with and contributes to Citi’s goal to create the best outcomes for our clients by providing financial solutions that are simple, creative and responsible.

The world is moving at a rapid pace toward cleaner, more sustainable sources of energy and businesses around the world are leading the way with new ideas, plan and projects. Citi is proud to deliver both the investments and finance required to bring these ideas, plans, and projects to reality

2017 ANNUAL REPORT

2017 ANNUAL REPORT

15

Citi Environmental and Social Policy Framework Citi Nigeria’s Environmental and Social Policy Framework includes categorization requirements and, as appropriate, environmental due diligence and elevated review and approval requirements for corporate and government loans, project finance transactions, acquisition finance, letters of credit, bid bonds, performance bonds, and project finance advisory mandates. This framework reinforces Citi’s commitment to managing environmental and social risks in a rigorous and effective manner.

In developing this framework, Citi adopted the external principles and standards listed below, which help to inform our approach to sustainability and risk management;

Equator Principles Green Bond Principles International Labour Organization’s Declaration on Fundamental Principles and Rights at Work

Natural Capital Declaration United Nations Environment

Program Finance Initiative (UNEP FI)

United Nations Global Compact United Nations Guiding Principles on Business and Human Rights

United Nations Universal declaration of Human Rights

These principles guide Citi’s Environmental and Social Policy Framework which covers all business units within the firm, with the objective of ensuring that all of Citi’s businesses effectively assess and manage the environmental and social risk associated with business. The Pillars of Citi’s Environmental and Social Policy are outlined below;

I. Environmental FinanceCiti, through its global business activities, seeks to use its skills and assets to accelerate capital markets solutions to major environmental problems. We do this through specific business units dedicated to developing environmental finance products as well as by identifying opportunities through our traditional businesses. In 2015 as part of our Sustainable Progress

Strategy, Citi announced a ten-year, $100 billion environmental finance goal to lend, invest and facilitate $100 billion to environmental and climate solutions.

II. Environmental and Social Risk ManagementCiti lends and mobilizes billions of dollars of capital towards a variety of companies and projects, including sectors that may be associated with environmental and social impacts and risks. Before making a financing decision, we carefully assess the extent of these impacts and work with our clients to apply a clearly defined set of environmentally and socially responsible policies consistent with leading international standards and good practice.

Citi’s Environmental and Social Risk Management (ESRM) Policy is outlined below;

A. Firm-Wide Prohibitions Citi does not directly or indirectly

finance the following types of projects or activities;• Production or activities

involving harmful or exploitative forms of forced labor

• Production or activities involving harmful or exploitative forms of child labor

• Illegal logging• Production or trade in any

product or activity deemed illegal under country laws or regulations

• Production or trade in wildlife or products regulated under CITES (the Convention on International Trade in Engendered Species of Wild Fauna and Flora or activity deemed illegal under country laws or regulations

2017 ANNUAL REPORT

SUSTAINABILITY REPORT 2017

2017 ANNUAL REPORT

16

• Drift net fishing in the marine environment using nets in excess of 2.5 km in length

B. Areas of High Caution and Special Focus

Consistent with the precautionary principle of “do no harm,” Citi recognizes that there are certain “areas of high caution” that require special attention, focus and respect. Utilizing the relevant International Finance Corporation (IFC) Performance Standards and national laws, Citi only proceeds with investments that impact these areas after a thorough and judicious assessment of impacts and risks, and confirmation that mitigation measures have been or will be designed to comply with Citi’s policies and standards.

C. Firm-Wide Sector Standards Citi recognizes that there are

a number of important areas that require increased attention via sector-specific policy or guidance not available through the IFC Performance Standards, IFC Environmental Health and Safety (EHS) Guidelines, or national or internationally accepted standards. To address this, Citi’s ESRM Policy incorporates several sector-specific standards for the sectors below;• Coal Mining• Forestry• Nuclear• Oil Sands• Palm Oil• Shale Oil and Gas

D. ESRM Screening and Categorization Criteria

As part of the review of a transaction’s environmental and social risks, Citi uses a system of categorization based on

IFC’s environmental and social screening criteria to characterize the magnitude of impacts understood as a result of the assessment. Categories include

• CATEGORY A – use of proceeds are likely to have potential significant adverse social or environmental impacts that are diverse, irreversible or unprecedented;

• CATEGORY B – use of proceeds is likely to have potential limited adverse social or environmental impacts that are few in number, generally site-specific, largely reversible and readily addressed through mitigation measures;

• CATEGORY C – use of proceeds expected to have minimal or no social or environmental impacts; and

• CATEGORY GR – “general review,” use of proceeds are directed to multiple projects with varying risk levels

The screening and categorization criteria above are supplemented by a focus on a number of broad, high-level issues as framed by the IFC Performance Standards. The Performance Standards include;

• PS 1 – Assessment and Management of Environmental and Social Risks and Impacts

• PS 2 – Labor and Working Conditions

• PS 3 – Resource Efficiency and Pollution Prevention

• PS 4 – Community Health, Safety and Security

• PS 5 – Land Acquisition and Involuntary Resettlement

• PS 6 – Biodiversity Conservation and Sustainable Management of Living Natural Resources

• PS 7 – Indigenous People• PS 8 – Cultural Heritage

E. Independent Review All Category A and certain

Category B Equator Principles-covered project finance transactions, and any Equator Principles-covered project related corporate loans that trigger Equator Principle 7 “high risk impacts” require review by an independent environmental and/or social expert not associated directly with the borrower. Independent review may be required of other ESRM Covered Category A transactions in “areas of high caution” (see above) or of transactions subject to certain ESRM sector standards (as described on pp. 5-7), as deemed appropriate by Citi Independent Risk.

III. Operations and Supply ChainSince 2001, Citi has been working to measure, manage and reduce the direct environmental impacts of our operations. Our efforts reduce costs, enhance work environments and productivity, and enable us to speak from a position of experience when our clients need support.

The two key elements of Citi’s Supply Chain Diversity and Sustainability Program are i) Citi’s Statement of Supplier Principles, and ii) the Corporate Responsibility Questionnaire. Citi’s Statement of Supplier Principles communicates our values related to ethics, sustainability and human rights. The principles have been circulated to our top approved suppliers and continue to be socialized and communicated internally and externally. Citi also engages suppliers through its Corporate Responsibility Questionnaire (CRQ). This tool assists the procurement

2017 ANNUAL REPORT

SUSTAINABILITY REPORT 2017

2017 ANNUAL REPORT

17

team in determining how well potential and current suppliers are managing corporate citizenship, environmental sustainability and diversity components within their business.

IV. Human RightsCiti supports the protection and preservation of human rights around the world and is guided by fundamental principles of human rights, such as those in the United Nations Universal Declaration of Human Rights and the International Labour Organization’s (ILO) Declaration on Fundamental Principles and Rights at Work (including the eight core conventions8). Citi is also a signatory to the United Nations Global Compact. Citi supports the United Nations Guiding Principles on Business and Human Rights, including the corporate responsibility to respect human rights. Our support for these fundamental principles is reflected in our policies and actions toward our employees, suppliers, clients and the countries where we do business. We work with our clients to respect human rights through application of our ESRM Policy in client engagements and through the diligence we perform related to transactions.

Activities and Initiatives

Since 2001, Citi has been working to measure, manage and reduce the direct environmental impacts of our operations. We have provided physical access to the physically challenged members of the society in our head office and most of our branches. We continue to manage our direct environmental footprint by measuring our operational environmental footprint—electricity use, fuel consumption, water use and waste. To reduce carbon emissions, we encourage the use of video and audio conference meetings rather than face-to-face meetings that require travels.

Citi is committed to sharing best practices and improving the financial literacy base of financially excluded individuals. Citi Nigeria extended a loan of NGN500 million to Accion Microfinance Bank (Accion MFB) in Nigeria to drive and promote the development of the microfinance sector in Nigeria. The

loan will fund Accion’s loan portfolio and support the development of approximately five thousand micro and small enterprises in the country. The agreement will also support the Central Bank of Nigeria’s National Financial Inclusion Strategy (NFIS) to reduce the number of excluded persons by bringing them into the formal banking fold. This loan is part of a long term business partnership between Citi Inclusive Finance, Citi’s specialized unit for microfinance and inclusive finance transactions, and the Overseas Private Investment Corporation (OPIC).

By partnering with other banks and microfinance institutions, Citi continues to explore innovative avenues to provide capital to those who otherwise would not have had access. The promotion of diversity, one of the key pillars of Citi’s operating culture, also ensures that Citi continues to provide equal opportunities for all irrespective of gender, religion or race.

Electricity Consumption (KwH, in Thousand)

Diesel Consumption (Litres, in Thousands)

498447

667

1052

2014 2015 2016 2017

910881

772809

2014 2015 2016 2017

66,345

274

216

186

51,900

42,389

2015 2016 2017

1861

313

169

249

1009 951

2015 2016 2017

Total Fuel Consumption by Company Fleet (Litres)

Ave. fuel use per employee

Total Air Mileage (Miles)

Total CO2 emission (Metric tons)

Since 2001, Citi has been working to measure, manage and reduce the direct environmental impacts of our operations.

2017 ANNUAL REPORT

SUSTAINABILITY REPORT 2017

2017 ANNUAL REPORT

18

2017 ANNUAL REPORT

19

Business Report

2017 ANNUAL REPORT

20

Corporate and Investment Banking

Citi’s Corporate & Investment Banking (CIB) Group’s key business objective remains to be the strategic advisor of choice to our valued clients, by providing differentiated industry advice and expertise. Citi offers a broad range of products including; Corporate Finance, Investment Banking, Transaction Services (Cash Management, Trade Products and Custody Services), Treasury services (Fixed Income, currencies and commodities) and structured solutions to meet the needs of our clients.

Citi continues to face competitive pressure with the local presence of regional and global banks such as Rand Merchant Bank (RMB), Barclays, Standard Chartered (SC) and JP Morgan, and Goldman Sachs on select transactions. With this backdrop, Citi’s CIB team has remained focused and consistent in delivering best in class product solutions and services to meet the needs of its clients.

Citi remains committed in supporting its clients to successfully navigate market volatility driven by the challenging backdrop of persistently low crude prices, providing the necessary risk

management advice and solutions, and remains confident in the country’s long term economic prospects as well as that of Citi’s rapidly growing client base.

Despite initial macro-uncertainty from the UK Brexit vote and the U.S. presidential elections, global corporates in 2017 experienced a significant recovery with equity valuations reaching a peak levels with a median forward P/E of 18x globally and 20x in the U.S. The U.S. announced a tax reform as well as a monetary policy normalization regime expected to involve higher corporate earnings, modest rate hikes and yield expansion that may have an impact on portfolio outflows, though emerging markets are expected to remain resilient.

By the third quarter of 2017, Nigeria’s economy had exited negative growth territory, demonstrating real GDP growth of 1.40%, (Q2 2017 +0.55%), a reversal of the gloomy picture at the end of 2016 - an economic recession evidenced by multiple quarters of negative growth. Real GDP growth in FY 2016 amounted to -1.5%, the worst full-year decline in twenty-five years - as both oil and non-oil GDP contracted. The improvement witnessed in 2017 was largely attributed to improved oil production and price recovery in the global markets. The real sector (trade, manufacturing, finance, insurance, information technology) is yet to recover fully, hence growth is observed as volatile and vulnerable to shocks.

The Central Bank of Nigeria (CBN) introduced an Importers & Exporters window in April 2017 which significantly impacted the FX market as the gap between the official and the parallel market exchange rate narrowed for the

first time, and has remained stable to date at c.US$/NGN360-365. Portfolio inflows have also since returned via this window, reaching over $10bn in aggregate by September 2017 and lifting the Nigerian Stock Exchange, which is at an eight-year high, with a market capitalization of over 40,000. The apex bank had earlier introduced the sale of FX forwards and futures that provided some much needed comfort to manufacturers and relieving pressure on the parallel market.

Following the decision of the Monetary Policy Committee at the fourth meeting of 2016 to raise the policy rate (MPR) by 200bps to 14% against market consensus, the Committee held the MPR constant through 2017, despite having met six times through the year, and retained the Cash Reserve Requirement (CRR) on private and public sector deposits at 22.5%, the Liquidity Ratio (LR) at 30% and the asymmetric corridor at +200bps/-500bps. Analysts believe that the overarching factor guiding the MPC’s tight regime is the quest to attract and retain foreign portfolio inflows. Going forward, the MPC may maintain its tight policy regime longer than expected as global investors monitor recent developments in the U.S. Federal Reserve’s monetary policy normalization process and its impact on capital flows to emerging markets.

Gross external reserves stood at $40.4bn by early January 2018, up from $25.84bn a year earlier, an increase attributed primarily to rising crude revenue due to a recovery in global oil prices, increased portfolio inflows, and the success of Nigeria’s Eurobond offerings. On November 7 2017, Nigerian President Muhammadu

Mudassir AmrayHead of Corporate and Investment Bank

20

2017 ANNUAL REPORT

21

Citi remains focused on being the trusted advisor to its clients, making the bank their first port of call and ensuring that Citi delivers the best possible products and services to them in a seamless manner.

Buhari presented a record budget to lawmakers to boost the nation’s spending by 18% in 2018 in a bid to further stimulate growth in an economy that had just reversed a full-year contraction for the first time in over two decades. Buhari asked lawmakers to allow his government to spend NGN8.63tn ($283bn) in 2018 in a proposal based on a projected oil price of $45.00 per barrel, and daily oil production of 2.3mn barrels. The administration is also continuing the theme of recovery through infrastructure spending, allocating 28% (NGN 2.42tn) to this, focusing on Power, Transportation, & Agriculture. Non-oil revenue of NGN4.17tn ($13.7bn) is to account for almost double oil revenue NGN2.44tn.

Citi continues to dialogue closely with its clients providing creative solutions to their businesses while financing their needs in conjunction with the bank’s product partners. Citi also leveraged on its global network to support Nigerian corporates as they expand their businesses in the region and other locations.

Global economic activity is projected to pick up pace in 2018 (3.7% growth estimate over 3.6% in 2017 according to the IMF), especially in emerging market and developing economies, with a 4.5% target according to the World Bank, relative to 2.2% in advanced economies. According to a Reuters poll, China is expected to grow at 6.4% in 2018 (down from 6.8% in 2017), while India is expected to grow at 7.3% in 2018 (up from 7% in 2017).

Capital inflows are expected to remain at sustained levels in emerging markets, due to strong

recovering economic growth in the west and sustained growth outlook in China and India, despite recent property and debt shocks. Sub-Saharan Africa continues to offer a mixed picture; whilst economies like Cote D’Ivoire and Tanzania’s have continued to grow at a pace faster than most in the continent, both have shown signs of slowing; Cote d’Ivoire due to a slump in cocoa prices, mutiny and workers’ strikes. Angola, Ghana, Nigeria and other commodity dependent economies have experienced a tepid recovery from recession largely due to the recent oil-price recovery in global markets. They seek to attract continuous offshore inflows through internal monetary policies while implementing internal reforms aimed at revenue base diversification.

The Nigerian economy is expected to witness sustained recovery in 2018 with a growth estimate of 2.5% according to the World Bank with promising prospects from the non-oil sector which remains relatively buoyant, particularly in agricultural production and infrastructure development. Crude oil prices are expected to remain at the recent levels above US$60 a barrel (Brent futures reaching $67.12, levels unprecedented since May 2015), as markets gauge the long term effects of production cuts by OPEC and Russia, and anti-government rallies in Iran.

Nigeria weathered macroeconomic headwinds in 2017 that led to a recovery of GDP growth, and has arguably begun to witness the fruit of its drive to improve non-oil revenue generation while focusing on infrastructure spending. Within this backdrop, there are some opportunities for us to create value for our clients, across equity

capital markets (rights issues and primary equity offerings within an improved valuation environment), debt capital markets (sustained interest among FIs on the back of multiple successful sovereign & FI issuances), and advisory (corporates seeking foreign strategic partnerships to bring in some much needed capital). Citi continues to be a trusted advisor to many of its clients, as we always would be side by side with our clients providing our advice, our reach and resources to support their growth plans.

Citi remains focused on being the trusted advisor to its clients, making the bank their first port of call and ensuring that Citi delivers the best possible products and services to them in a seamless manner. In this regard, the team has continued to surpass expectations, working with Citi’s product partners across electronic banking, cash, liability management, mergers & acquisitions, equity & debt capital markets, trade and treasury. Citi is committed to the continuous growth and development of talent, as this remains the key differentiator for Citi.

2017 ANNUAL REPORT

22

Risk Management

The year 2017 started on an insipid note, as the economy, which had plunged into recession in 2016 remained characterized by foreign exchange crisis cum capital controls, declining foreign exchange reserves and elevated inflation. However, there was a slight turnaround in the country’s economic metrics in the second half of the year – with positive GDP growth of 0.55% in Q2 ’17, and the country closing the year with annual positive growth of 0.44%. The growth was driven by driven by improved access to foreign exchange – occasioned by improved liquidity in the foreign exchange markets and the accretion to the foreign exchange reserves; the game changer was the introduction of Investors’ and Exporters’ (I&E) Forex Window by the Central Bank of Nigeria in April 2017.

The decision by OPEC and major non-OPEC oil producers to cut oil output in December 2016 for an initial period of 6months till June 2017 to address the glut that had characterized the markets provided the support for the turnaround in the prices of crude. The agreement by the OPEC and

non-OPEC members to extend the deal till end of 2018, along with spontaneous geopolitical tension, provided sufficient support for crude prices – with Brent crude firming above the $60pb in November 2017 – the highest level since 2014. Nigeria continues to benefit from the output cut that was agreed in December 2016 – as it was exempted from the production cap; hence, it remains one of the major beneficiaries of the price recovery, given the stability in its oil production as the ongoing engagement with the Niger Delta stakeholders has ensured limited disruptions to oil installations in the region.

The country’s economic metrics remained on the positive trajectory in the second half of the year – with strong traction in the key economic metrics – specifically with respect to foreign exchange markets, CPI, foreign reserves and crude output and prices. The stability in the country’s oil output, in addition to its exemption from OPEC’s production cap, and the recovery of prices at the international market resulted in strong accretion to the reserves, which provided the support for Central Bank’s spontaneous interventions in the foreign exchange markets. This, together with the sustained inflows by portfolio investors into the I&E’s FX Window, resulted in marked improvement in foreign exchange liquidity in the markets – and the contraction in past due trade obligations across the banking industry. Of particular note is that Nigeria’s exemption from OPEC’s output restriction provided a significant upside for the country’s revenues – as the crude price remained significantly above the budget benchmark.

The Federal Government’s pace at addressing the structural weakness in the economy through its Economic Recovery and Growth Plan (ERGP) remained much slower than anticipated. The government’s significant reliance on oil to drive its exports and growth remains a key challenge. Whilst the recovery of the oil price and the uptick in oil production have led to the oil revenues outperforming the government’s budget, and to an overall improvement in the country’s metrics, the damage to the economy occasioned by the oil shock of the past two years is yet to be undone, and the weakness is expected to extend into medium term.

Though the government made some progress at increasing non-oil revenues through the broadening of tax base and enforcement of compliance, the impact has been limited – with tax revenues still at less than 20% of the country’s total. The challenges on the diversification of the revenues continue to negatively impact potential growth.The relatively high non-performing loans of Nigerian banking industry on account of the macro issues that have characterized the economy between 2014 and 2016 remain a challenge for the regulators and the players. While the issue was exacerbated by the increased borrowing costs in the second half of the year, the recovery in the crude, the accretion to the foreign reserves and the return of the economy to positive growth trajectory provide some potential upside in the industry’s prognosis. Furthermore, some of the industry’s oil & gas exposure are likely to start “performing”, if the strong recovery in crude price that has

Oluwole AwotundunExecutive Director and Country Risk Manager, Nigeria, West and Central Africa

22

2017 ANNUAL REPORT

23

characterized the markets in the past few months is sustained.

Despite the slight uptick in the country’s GDP in the second half of the year, corporate performance remained constrained on account of the legacy macro issues, which was partly exacerbated by the monetary tightening – as sales were constrained by the absence of liquidity to support effective demand.

On the outlook for 2018; the expectation is that the ongoing recovery in the Nigerian economy will be sustained. However, political risks may likely depress the growth momentum in the second half of the year – as politics upstages policy implementation, in addition to potential regression in investments by local and foreign investors. Furthermore, the government’s significant reliance on oil to drive its exports and growth also presents a significant downside to the country’s prognosis.

With growths normalizing in a number of developed economies,

there are risks of potential monetary tightening by central banks as there are indications they may proceed with the unwinding of some of the financial crisis-era support – given the uptick in the key metrics and the strong growths that have been recorded in most of the economies. We expect the likely spike in interest rates to exacerbate the likely reduction in foreign flows as political risk heightens in the run-up to the 2019 general elections. Whilst we expect the positive traction that we observed in the economy in the second half of the year with respect to some of the key indicators to continue in the near term, the economy would remain vulnerable to the residual macro challenges, which continue to hunt some of the corporates and financials. Citi Nigeria’s portfolio is not immune to these challenges, as we have observed some weaknesses in the profiles of some of its obligors. However, the bank has taken measures to manage its exposure to these clients.

Overall, Citi portfolio is expected to remain relatively stable – as the bank would continue to operate in line with its target market definitions and portfolio strategy. We will continue to keep a tab on the dynamics in both the local and global politics and economics – making adjustments to our risk appetite and assets creation – as necessary.

On the outlook for 2018;

the expectation is that

the ongoing recovery in

the Nigerian economy

will be sustained.

2017 ANNUAL REPORT

2017 ANNUAL REPORT

24

Citi’s award winning e-banking platform CitiDirect, alongside its mobile tablet version (CitiDirect BE Mobile) remains Citi’s single channel for connecting and enabling clients to access payment products in the payments system.

Treasury and Trade Solutions

Cash ManagementCiti’s Liquidity Management Solutions, enhanced by Host–to-Host connectivity for improved operating efficiency, remains a defining differentiator with Citi’s clients and in the market place. Citi’s broad proposition is to enable channel innovation for clients to perform their liquidity and balance sheet management activities efficiently, supported by Citi’s global proprietary platforms. Citi is well positioned to partner with Treasurers to maximize the power of their balance sheets for improvement in profitability.

Citi continues to build on the successes of the payment system reforms in improving the risk architecture around delivery channels and products, while enhancing the capacity of the market to support bulk payments for instant delivery through the clearing system. Citi implemented the NIBSS Automated Payments System (NAPS) and completely cut-over from NIBSS Electronic Funds Transfer (NEFT), deriving the benefits of the NIBSS Instant Payment (NIP) product for the bulk / batch processing option. Citi effectively enhanced its capacity for bulk payment to near instant

delivery across the bank’s MassPay platform.

The managed liberalized FX market environment in the year 2016 which persisted till the earlier months of 2017 was not without its challenges as distortions to the flow of liquidity in the system generated significant volatilities in the pricing of liquidity at the short end of the yield curve. This further accentuated the need for a more nimble payments infrastructure for just-in-time movement of liquidity to settle obligations as well as access FX opportunities across the financial system. The achievements in the payments system from an infrastructure perspective enabled Treasurers operate in a more nimble and flexible manner to meet the exigencies of business requirements.

Citi’s award winning e-banking platform CitiDirect, alongside its mobile tablet version (CitiDirect BE Mobile) remains Citi’s single channel for connecting and enabling clients to access payment products in the payments system. The aim is to continue to draw on the strength of Citi’s infrastructure and digitization drive to develop solutions and leverage market infrastructure to maintain the bank’s competitive edge in the market.

Trade Products In 2017, Citi focused on the delivery of customized Trade Services Products - Letters of Credit, Bills for Collection and Guarantees as well as Official Agency Supported Financing. In the face of the FX challenges witnessed during the first half of 2017, Citi continued to support clients with structured products that enabled continued operations. During the year Citi arranged ECA-backed financing to support the CAPEX needs of its

client. Such loans have significant impact in developing markets such as Nigeria and provide a template for other borrowers both in Nigeria and in the African region. They also increase the visibility and credibility of Nigerian corporates in the international financing market.

Citi engaged clients to commence the initiation of Letters of Credit on Citi’s proprietary-customer Trade front-end platform - CitiDirect for Trade, putting them in the forefront of digitization. Citi’s best-in-class working capital solution - Supply Chain Finance (SCF) program enabled the bank’s clients to benefit from balance sheet optimization and increased access to alternative funding, while also accessing the efficiency benefits of Citi’s fully automated processing platform.

With relative stability in FX availability, envisaged increase in trade activity in 2018 and the backward integration focus of the Federal Government in a pre-election year, Citibank Nigeria is well positioned and adequately armed with trade solutions to ease the process for its clients, as the country

Segun AdaramolaHead of Treasury and Trade Solutions

24

2017 ANNUAL REPORT

25

moves towards import substitution and export promotion.

Solution SalesPositive macroeconomic trends helped in restoring some confidence in the Nigerian economy. This led to re-invigoration of activities and surfacing of opportunities for further investment in the country. Engagement with clients improved from prior year as the restriction on business activity, which had been imposed by the earlier FX scarcity, became more relaxed with the improved availability of FX. Citi also witnessed a number of clients centralizing their operations for efficiency.

Citi actively engaged with clients and organized a number of thought leadership events, which included a Digitization event, a Cybersecurity Roadshow for Public & Private Sector clients, a Liquidity Management seminar, a Tax event and an Electronic Banking practical workshop, among others. In 2017, Citi Nigeria won the Euromoney Cash Management Award for “Best Domestic Cash Manager in Nigeria” for the 10th consecutive year. This demonstrates Citi’s continued impact on its

clients’ banking activities. Citi also received the prestigious Adam Smith award as Highly Commended in the “Best in Class Treasury Solution in Africa” category for the solution suite implemented for Nigerian Breweries Plc.

Citi is poised to follow through on the opportunities that surfaced in 2017 and deepen engagement with its clients accordingly. The goal is to stay close to clients and ensure we remain their trusted partner for the provision of transaction banking solutions.

ImplementationsCiti’s Implementation team was able to manage the delivery of Cash, Cards and Trade products to clients using client-friendly implementation models. Onboarding experience for clients was consistently maintained, which resulted in faster and efficient solutions delivery of mandates received.

Implementation of tailored electronic solutions that provide greater efficiency were popular amongst the bank’s clients in the course of the year with increased requests for robust integration with clients’ Enterprise Resource

Planning (ERP) systems. These solutions enabled Citi clients to enhance their organizational work flow process, improve their overall productivity while aligning with various regulatory requirements.

In 2018, Citi will continue to focus on the enhancement of its service proposition to clients by deploying value-added and innovative solutions which will enable the bank’s clients to optimize their operating performance.

Citi Nigeria won the Euromoney Cash Management Award for “Best Domestic Cash Manager in Nigeria” for the 10th consecutive year.

Citi will continue to focus on the enhancement of its service proposition to clients by deploying value-added and innovative solutions which will enable the bank’s clients to optimize their operating performance.

2017 ANNUAL REPORT

2017 ANNUAL REPORT

26

Global Subsidiaries Group

Citi Nigeria’s Global Subsidiaries Group (GSG) remains part of a global client coverage force, harnessing the power of Citi’s unparalleled global network and delivering seamlessly to our clients. The team framework is designed to mirror the clients’ organizational structure and continues to create a unique alignment between the clients’ Treasury organizations and Citi’s network. Citi’s clients value the depth of Citi’s offering, universal systems, well-orchestrated global teams and extensive local market knowledge. In the last year, the bank’s clients with their global Treasury teams, especially relied on unique insights from the Citi team to interpret the rather dynamic and challenging economic environment in Nigeria, to support their business sustainability.

The year 2016 was quite historic in the Nigeria economic landscape, with negative growth recorded for four consecutive quarters and the country ultimately recording its first recession in over two decades. Many factors were contributory but severe Foreign Exchange shortages

considerably dampened the business environment.

Citi played quite a pivotal role in supporting clients’ needs during this crucial period, leveraging its diversified foreign investor footprint and cross-border Trade Finance capacity. In particular, Citi deployed import and Foreign Exchange solutions which enabled our clients secure the much needed production inputs to remain in business. The critical supply chain partners of Citi’s client base were also integrated into the bank’s trade solution suite.

The Central Bank of Nigeria (CBN) Foreign Exchange reforms in June 2016 were laudable and provided some of the much needed flexibility. In particular, the new Foreign Exchange policy enabled hedging opportunities and the bank worked with several clients to improve their cost certainties. The ensuing naira devaluation increased Citi clients’ input costs, coupled with a change in the fuel price regime which led to a sharp increase in the pump price of fuel. Also most market operators had foreign currency liabilities, which resulted in exchange losses when the exchange rate moved adversely. The CBN tightened the monetary policy rate by 200bps during the year to control inflationary pressures and interest costs increased, further aggravating business costs.

All of these cost escalations squeezed out business margins for most companies and inevitably led to outright losses in several others. While some market operators had sufficient capacity and financial flexibility to withstand the market

stresses, others were more vulnerable. Citi worked closely with its clients to lower their financial risks. Citi’s rich credit culture, advanced credit monitoring techniques and proactive screening of the credit portfolio against key stress factors, ensured that Citi continued to maintain a healthy portfolio of credit clients, and defend shareholder value.

While credit availability generally reduced in the market due to cautious lending appetite in the bank market, Citi continued to provide competitively priced loans to clients in its target market. Citi’s scalable supply chain financing solution further deepened Citi’s reach, to provide financing options to its clients’ supply chain. Where some companies increased the number of their banking providers, ostensibly to improve access to Foreign Exchange, Citi’s multi-banking technology platforms/systems proved invaluable to optimizing liquidity across banking system applications and enhancing overall operating efficiency.

Citi remained key banking providers to strategic Industry segments. Citi especially dominated the wallets of a number of clients during the year, on the strength of the bank’s product innovation and dynamic response to clients’ key business imperatives. Notably, Citi won landmark client mandates for Capital Raising and debt restructuring.

In Citi’s annual Client feedback survey, most clients defined their relationship with the Citi team as Trusted Advisor relationships, underscoring the strength of

Nneka EnwerejiExecutive Director and Head of Global Subsidiaries Group

26

2017 ANNUAL REPORT

27

Citi played quite a pivotal role in supporting clients’ needs during this crucial period, leveraging its diversified foreign investor footprint and cross-border Trade Finance capacity.

our partnerships. The quality of Citi’s client engagement was also validated in the KPMG 2016 Banking Industry Customer Satisfaction survey which for the third consecutive year voted Citibank Nigeria as the Most Customer Focused Bank in the wholesale banking category.

During the year, Citi continued to invest in its GSG team, which remains fundamental to the bank’s business aspirations. Citi deployed various talent intervention programs, including training courses and short-term assignments with other businesses. In-house partnerships were crucial to the bank’s achievements during the year and GSG collaborated very effectively with the various product, risk and control functions, to drive our business agenda. The bank’s network connectivity remains a key advantage and Citi continued to optimally exploit this.

Overall, while it was a tough year, it was a very accomplished one for

Citi’s business, as Citi differentiated itself as a trusted partner to its esteemed client base.

2017 OutlookThe Nigeria economic growth forecasts for 2017 signal some growth, albeit marginal. This would be driven by higher or at least more stable oil prices, continued containment of the Niger Delta militancy and better traction on economic policy implementation. Foreign Exchange availability would no doubt be a key enabler for the anticipated growth momentum and it is a good sign that the CBN have significantly boosted market supply in the first couple of months.

Citi’s continued insights on the business terrain, strong knowledge of our clients’ business dynamics, strategic client partnerships, innovative and proactive solutions should once again serve the bank well to steer the business to another record performance amidst the market uncertainties.

2017 ANNUAL REPORT

2017 ANNUAL REPORT

28

Citi organized a client seminar themed Charting Industry Progress in Nigeria, designed to bring together market regulators, participants and other industry experts to discuss and explore the Nigerian asset custody ecosystem vis-à-vis global developments

Aderonke AdetoroSecurities CountryManager

Direct Custody and Clearing

2017 Overview

2017 began with quite some optimism against the recessionary back drop of 2016. Gross Domestic Product (GDP) turning positive in the second quarter of 2017 – progressively increasing from -0.52 per cent in quarter one to 0.72 per cent in quarter two to 1.40 per cent in quarter three of 2017, with the economy steadily clawing its way out of recession (2016 GDP -1.58 per cent). Foreign exchange (FX) reserves have continued to grow, with a foreign reserve balance of USD 37.7 billion as at 21 December 2017. The FX reforms implemented by the Central Bank of Nigeria (CBN) have supported the improved performance in the financial markets.

A number of policies geared towards the FX environment were implemented by the CBN in 2017. Some of these policies include the establishment of the Investors’ and Exporters’ (I&E) FX Window which took effect in April 2017; this was predicated on a willing buyer and willing seller transaction execution, with the aim of boosting liquidity in the FX market and ensuring the

timely execution and settlement of eligible transactions. The Nigerian Autonomous Foreign Exchange (NAFEX) fixing was also introduced. This is the reference rate for FX activities in the I&E FX window representing the spot FX market rate in the window.

On the capital market front, there was a notable resurgence in the equity market in 2017, especially following the commencement of the I&E FX window. According to the Nigerian Bureau of Statistics (NBS), Foreign Portfolio Investment (FPI) remained the largest component of capital importation into Nigeria in the third quarter of 2017, at 67 per cent, with this component exhibiting the highest growth of the three capital importation categories (FPI, Foreign Direct Investment (FDI) and Other Investments) with a 200 per cent year-on-year growth. The Nigerian Stock Exchange (NSE) market capitalisation grew by about 48.25 per cent on a year-to date basis as at 22 December 2017; a reflection of increased investor confidence and improved FPI flows into the Nigerian equities market. The NSE All Share Index as at 22 December 2017 stood at 38,522.14; close to the year high of 39,534.14 set on 7 December 2017. A low of 24,581.99 was seen on 6 March 2017 before the FX reforms began.

Fixed income yields on the other hand, closed the fourth quarter of the year at a low. At the final primary T-Bill auction for the year, the 182 day T-Bill was issued at 15 per cent, compared with 17.50 per cent during the first week of 2017. Yields on the 1 year note also fell from 18.685 percent to 15.75 percent. The benchmark 10 year government bonds has decreased by approximately 300 bps from January 2017 levels.

Within Direct Custody and Clearing (DCC), we continued to leverage Citi’s custody-related technology platforms and broad knowledge pool to support our domestic and foreign clients in 2017. Following the FX policy changes in 2017, there was an increase in Assets under Custody (AUC) compared to 2016. The overall year-on-year AUC growth is 68 per cent – with a growth of 62 per cent for FPI clients and 73 per cent for domestic clients. New client mandates were won during the year, and incremental deals from existing clients all led to a steady growth. In 2017, Citi organized a client seminar themed Charting Industry Progress in Nigeria, designed to bring together market regulators, participants and other industry experts to discuss and explore the Nigerian asset custody ecosystem vis-à-vis global developments while identifying opportunities for success transfer to help meet the needs of investors in the Nigerian capital market sector. The seminar

28

2017 ANNUAL REPORT

29

also provided informative sessions on the Nigerian economy and capital market through various presentations from the Securities and Exchange Commission (SEC), Central Securities and Clearing Systems PLC (CSCS), and NSE. The participants at the seminar were from various sectors including Asset Management, Financial Services and Advisory and Legal Services.

Throughout 2017 Citi also hosted a number of FPI clients as part of their sub-custodian annual due diligence visits. Through this medium, Citi provided the clients with in-depth discussions on the Nigerian economy, capital market developments as well as Citi’s custody service offering, its strengths and differentiating factors. Some capital market developments that occurred in 2017 include the market-wide implementation of the Electronic Certificate of Capital Importation System (eCCIS) by the CBN, Financial Markets Dealers Association (FMDA) and Association of Asset Custodians of Nigeria

(AACN) – to dematerialise the existing CCI process and provide increased efficiency in the issuance, tracking and transfer of CCIs as well as the launch of the fully SWIFT enabled system, TCS BaNCS, by the CSCS to improve efficiency in the depository and settlement services provided by the CSCS. The CSCS also issued a directive requiring all corporate and institutional investors to provide their Legal Entity Identifier (LEI) code which facilitates the identification of parties involved in any financial transaction – this takes effect on 1 January 2018.

2018 Outlook

Citi is optimistic about 2018, and expects GDP growth to continue its recovery. Oil production and the FX reserves will remain stable, giving foreign investors the confidence to put money into the Nigerian market. As a business, Citi will continue to provide global perspectives on best practices, working closely with the market infrastructure and regulators, on improving efficiency

As a business, Citi will continue to provide global perspectives on best practices, working closely with the market infrastructure and regulators, on improving efficiency in the Nigerian capital market.