2017-04-18 Earned Income Tax Credit Due Diligence€¦ · · 2017-11-09Earned Income Tax Credit...

21

Earned Income Tax Credit Due Diligence: What Questions to Ask and What Documents to Keep Presented By: Kyle Coleman Coleman, Anastopulos & Jackson, P.C. 16250 Knoll Trail Drive, Suite 105, Dallas, TX 75248 Phone: (972) 810 – 4380 Fax: (972) 810 – 4380 Email: kyle@caj‐law.com

Transcript of 2017-04-18 Earned Income Tax Credit Due Diligence€¦ · · 2017-11-09Earned Income Tax Credit...

Earned Income Tax Credit Due Diligence: What Questions to Ask and What Documents to Keep

Presented By:

Kyle Coleman

Coleman, Anastopulos & Jackson, P.C.

16250 Knoll Trail Drive, Suite 105, Dallas, TX 75248 Phone: (972) 810 – 4380 Fax: (972) 810 – 4380

Email: kyle@caj‐law.com

1

Kyle Coleman Mr. Coleman’s practice concentrates on federal tax related controversy matters, including litigation in Federal District Court, the United States Tax Court, and the Court of Federal Claims. Mr. Coleman also represents taxpayers in Internal Revenue Service audits, appeals, and collection actions. Mr. Coleman has been admitted to the Fifth Circuit Court of Appeals Bar, the District of Columbia Circuit Bar, the Northern District of Texas, the Eastern District of Texas, the District of Colorado, and the United States Tax Court. In addition to tax controversy, Mr. Coleman also represents clients in estate and business planning as well as asset protection. His practice includes entity formation, asset transfers, and wills and trusts. Education LL.M. in Taxation, Dedman School of Law, Southern Methodist University, 1999 J.D., Oklahoma City University School of Law, 1998 B.A. in Finance, University of Central Oklahoma, 1995 Bar Admissions State Bar of Texas State Bar of Oklahoma Professional Associations and Memberships State Bar of Texas State Bar of Oklahoma Dallas Bar Association

2

Earned Income Tax Credit Due Diligence: What Questions to Ask and What Documents to Keep

Introduction

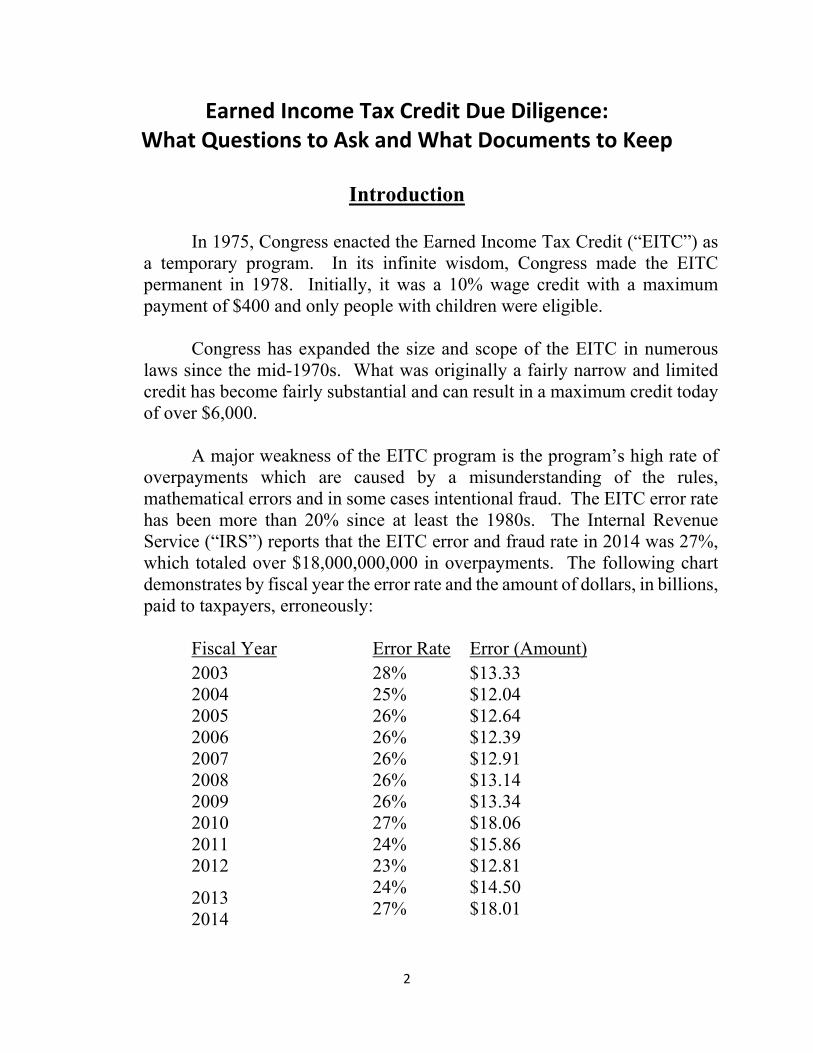

In 1975, Congress enacted the Earned Income Tax Credit (“EITC”) as a temporary program. In its infinite wisdom, Congress made the EITC permanent in 1978. Initially, it was a 10% wage credit with a maximum payment of $400 and only people with children were eligible. Congress has expanded the size and scope of the EITC in numerous laws since the mid-1970s. What was originally a fairly narrow and limited credit has become fairly substantial and can result in a maximum credit today of over $6,000. A major weakness of the EITC program is the program’s high rate of overpayments which are caused by a misunderstanding of the rules, mathematical errors and in some cases intentional fraud. The EITC error rate has been more than 20% since at least the 1980s. The Internal Revenue Service (“IRS”) reports that the EITC error and fraud rate in 2014 was 27%, which totaled over $18,000,000,000 in overpayments. The following chart demonstrates by fiscal year the error rate and the amount of dollars, in billions, paid to taxpayers, erroneously:

Fiscal Year Error Rate Error (Amount)2003 28% $13.33 2004 25% $12.04 2005 26% $12.64 2006 26% $12.39 2007 26% $12.91 2008 26% $13.14 2009 26% $13.34 2010 27% $18.06 2011 24% $15.86 2012 23% $12.81

2013 2014

24% 27%

$14.50 $18.01

3

Taxpayers are receiving excess EITC payments based on false information about such items as their income level, filing status, and qualifying children. The EITC is an easy target for dishonest filers because it is refundable, meaning that people can simply file false tax returns and wait for the IRS to issue them a refund even if they have not paid taxes into the system.

Errors and fraud are also incurred in the Child Tax Credit (“CTC”). The

improper payment rate for the CTC is more than 25%, thus costing taxpayers approximately $6,000,000,000 per year.

There are a number of ways that unscrupulous taxpayers game the EICT

system sometimes with the knowing help of the tax preparer. Typically, half of the EITC tax returns completed by paid preparers overclaim the credit. Recent IRS audit statistics show that the EITC has become so rife with fraud, 39% of all IRS audits for individual income tax filers are done on EITC filers.

The number of audits and amount of fraud and waste that results from

the EITC improper payments has attracted the attention of Congress which in turn has focused the attention of the IRS on you, tax preparers, as a first line of defense to improper payments. In a recent case, an EITC due diligence auditor personally appeared at a client’s tax preparation firm and proceeded to conduct an EITC due diligence audit on the spot. The preparers were contacted in February related to returns that were prepared in late January and early February. Without any notice, the IRS began reviewing randomly selected client files that had taken the current year’s EITC and received a refund. The Auditor selected fifty (50) files for review. There was a recurring error in document retention in each file which resulted in over $25,000 in penalties under IRC § 6695(g). If you have clients who are eligible for the EITC or the CTC, you need to be aware of the questions that you should ask and which documents you should keep. If you do not know the answer to these questions, it could be expensive. Like it or not, the IRS is making you the front line in the battle against EITC improper payment.

This outline will show the applicable Statutes, Regulations and Internal

Revenue Service Manual provisions that cover a tax preparer’s due diligence requirements in regards to the EITC. We will also show how the reporting requirements have been expanded to require return preparers to ask additional questions and retain additional documents in an attempt to reduce the error and improper payments rates related to the EITC and the CTC. Finally, we

4

will provide some examples to show what types of questions should be asked and documents that should be retained at it relates to taxpayers filing with EITC or CTC credit.

Statute IRC § 6695(g)

The main statute that allows regulation of tax preparers as to EITC Due

Diligence is IRC § 6695(g). § 6695. Other assessable penalties with respect to the preparation of tax returns for other persons

… (g) Failure to be diligent in determining eligibility for child tax credit;

American opportunity tax credit; and earned income credit.--Any person who is a tax return preparer with respect to any return or claim for refund who fails to comply with due diligence requirements imposed by the Secretary by regulations with respect to determining eligibility for, or the amount of, the credit allowable by section 24, 25A(a)(1), or 32 shall pay a penalty of $500 for each such failure.

Treasury Regulation

Regulations promulgated under IRC § 6695 provide further guidance as to

your EITC Due Diligence responsibilities. The Regulation states: § 1.6695-2 Tax return preparer due diligence requirements for determining earned income credit eligibility.

(a) Penalty for failure to meet due diligence requirements. A person

who is a tax return preparer of a tax return or claim for refund under the Internal Revenue Code with respect to determining the eligibility for, or the amount of, the earned income credit (EIC) under section 32 and who fails to satisfy the due diligence requirements of paragraph (b) of this section will be subject to a penalty of $500 for each such failure.

5

(b) Due diligence requirements. A preparer must satisfy the following due diligence requirements:

(1) Completion and submission of Form 8867—(i) The tax return

preparer must complete Form 8867, “Paid Preparer’s Earned Income Credit Checklist,” or such other form and such other information as may be prescribed by the Internal Revenue Service (IRS), and—

(A) In the case of a signing tax return preparer electronically filing

the tax return or claim for refund, must electronically file the completed Form 8867 (or successor form) with the tax return or claim for refund;

(B) In the case of a signing tax return preparer not electronically filing the tax return or claim for refund, must provide the taxpayer with the completed Form 8867 (or successor form) for inclusion with the filed tax return or claim for refund; or

(C) In the case of a nonsigning tax return preparer, must provide the

signing tax return preparer with the completed Form 8867 (or successor form), in either electronic or non-electronic format, for inclusion with the filed tax return or claim for refund.

(ii) The tax return preparer’s completion of Form 8867 (or successor form)

must be based on information provided by the taxpayer to the tax return preparer or otherwise reasonably obtained by the tax return preparer.

(2) Computation of credit—(i) The tax return preparer must either—

(A) Complete the Earned Income Credit Worksheet in the Form 1040

instructions or such other form and such other information as may be prescribed by the IRS; or

(B) Otherwise record in one or more documents in the tax return

preparer’s paper or electronic files the tax return preparer’s EIC computation, including the method and information used to make the computation.

(ii) The tax return preparer’s completion of the Earned Income Credit

Worksheet (or other record of the tax return preparer’s EIC

6

computation permitted under paragraph (b)(2)(i)(B) of this section) must be based on information provided by the taxpayer to the tax return preparer or otherwise reasonably obtained by the tax return preparer.

(3) Knowledge—(i) In general. The tax return preparer must not know, or

have reason to know, that any information used by the tax return preparer in determining the taxpayer’s eligibility for, or the amount of, the EIC is incorrect. The tax return preparer may not ignore the implications of information furnished to, or known by, the tax return preparer, and must make reasonable inquiries if the information furnished to the tax return preparer appears to be incorrect, inconsistent, or incomplete. A tax return preparer must make reasonable inquiries if a reasonable and well-informed tax return preparer knowledgeable in the law would conclude that the information furnished to the tax return preparer appears to be incorrect, inconsistent, or incomplete. The tax return preparer must also contemporaneously document in the files the reasonable inquiries made and the responses to these inquiries.

(ii) Examples. The provisions of paragraph (b)(3)(i) of this section are

illustrated by the following examples:

Example 1. A 22 year-old taxpayer wants to claim two sons, ages 10 and 11, as qualifying children for purposes of the EIC. Preparer A must make additional reasonable inquiries regarding the relationship between the taxpayer and the children as the age of the taxpayer appears inconsistent with the ages of the children claimed as sons.

Example 2. An 18 year-old female taxpayer with an infant has $3,000 in

earned income and states that she lives with her parents. Taxpayer wants to claim the infant as a qualifying child for the EIC. This information appears incomplete and inconsistent because the taxpayer lives with her parents and earns very little income. Preparer B must make additional reasonable inquires to determine if the taxpayer is the qualifying child of her parents and, therefore, ineligible to claim the EIC.

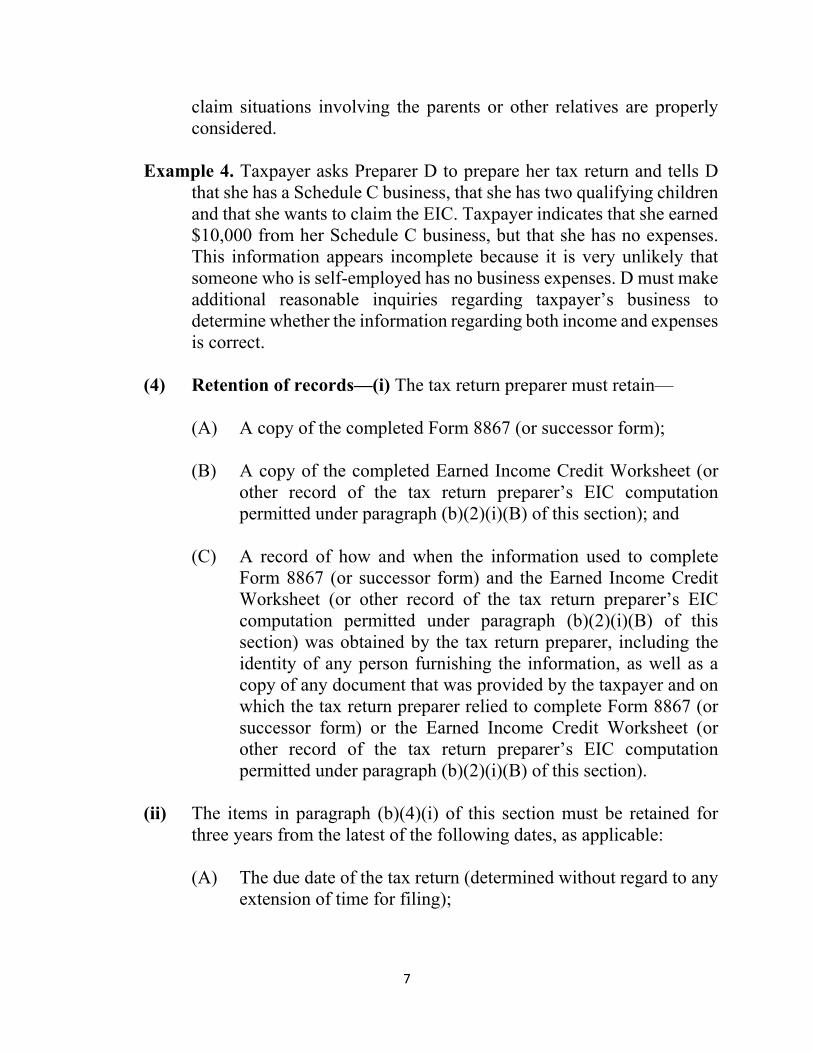

Example 3. Taxpayer asks Preparer C to prepare his tax return and wants to

claim his niece and nephew as qualifying children for the EIC. Preparer C should make reasonable inquiries to determine whether the children meet EIC qualifying child requirements and ensure possible duplicate

7

claim situations involving the parents or other relatives are properly considered.

Example 4. Taxpayer asks Preparer D to prepare her tax return and tells D

that she has a Schedule C business, that she has two qualifying children and that she wants to claim the EIC. Taxpayer indicates that she earned $10,000 from her Schedule C business, but that she has no expenses. This information appears incomplete because it is very unlikely that someone who is self-employed has no business expenses. D must make additional reasonable inquiries regarding taxpayer’s business to determine whether the information regarding both income and expenses is correct.

(4) Retention of records—(i) The tax return preparer must retain—

(A) A copy of the completed Form 8867 (or successor form); (B) A copy of the completed Earned Income Credit Worksheet (or

other record of the tax return preparer’s EIC computation permitted under paragraph (b)(2)(i)(B) of this section); and

(C) A record of how and when the information used to complete

Form 8867 (or successor form) and the Earned Income Credit Worksheet (or other record of the tax return preparer’s EIC computation permitted under paragraph (b)(2)(i)(B) of this section) was obtained by the tax return preparer, including the identity of any person furnishing the information, as well as a copy of any document that was provided by the taxpayer and on which the tax return preparer relied to complete Form 8867 (or successor form) or the Earned Income Credit Worksheet (or other record of the tax return preparer’s EIC computation permitted under paragraph (b)(2)(i)(B) of this section).

(ii) The items in paragraph (b)(4)(i) of this section must be retained for

three years from the latest of the following dates, as applicable:

(A) The due date of the tax return (determined without regard to any extension of time for filing);

8

(B) In the case of a signing tax return preparer electronically filing the tax return or claim for refund, the date the tax return or claim for refund was filed;

(C) In the case of a signing tax return preparer not electronically filing the tax return or claim for refund, the date the tax return or claim for refund was presented to the taxpayer for signature; or

(D) In the case of a nonsigning tax return preparer, the date the

nonsigning tax return preparer submitted to the signing tax return preparer that portion of the tax return or claim for refund for which the nonsigning tax return preparer was responsible.

(iii) The items in paragraph (b)(4)(i) of this section may be retained on paper

or electronically in the manner prescribed in applicable regulations, revenue rulings, revenue procedures, or other appropriate guidance (see § 601.601(d)(2) of this chapter).

(c) Special rule for firms. A firm that employs a tax return preparer

subject to a penalty under section 6695(g) is also subject to penalty if, and only if—

(1) One or more members of the principal management (or principal

officers) of the firm or a branch office participated in or, prior to the time the return was filed, knew of the failure to comply with the due diligence requirements of this section;

(2) The firm failed to establish reasonable and appropriate

procedures to ensure compliance with the due diligence requirements of this section; or

(3) The firm disregarded its reasonable and appropriate compliance

procedures through willfulness, recklessness, or gross indifference (including ignoring facts that would lead a person of reasonable prudence and competence to investigate or ascertain) in the preparation of the tax return or claim for refund with respect to which the penalty is imposed.

(d) Exception to penalty. The section 6695(g) penalty will not be applied

with respect to a particular tax return or claim for refund if the tax return preparer can demonstrate to the satisfaction of the IRS that,

9

considering all the facts and circumstances, the tax return preparer’s normal office procedures are reasonably designed and routinely followed to ensure compliance with the due diligence requirements of paragraph (b) of this section, and the failure to meet the due diligence requirements of paragraph (b) of this section with respect to the particular tax return or claim for refund was isolated and inadvertent. The preceding sentence does not apply to a firm that is subject to the penalty as a result of paragraph (c) of this section.

(e) Effective/applicability date. This section applies to tax returns and

claims for refund for tax years ending on or after December 31, 2011.

Internal Revenue Manual

The IRM very closely tracks the Regulations. The Manual states as follows: 20.1.6.5.7.1 - Failure to Be Diligent in Determining Eligibility for Earned Income Tax Credit—IRC 6695(g) for Tax Returns or Claims for Refund for Tax Years Ending on or After December 31, 2011 (05-16-2012)

(1) The IRC 6695(g) penalty applies if tax return preparer fails to comply with due diligence requirements with respect to determining eligibility for, or the amount of, the EIC.

(2) Compliance visits with preparers to determine the due diligence

requirement for the earned income credit are not third party contacts. (3) Under Treas. Reg. 1.6695-2(b), the preparer must comply with the

following due diligence requirements for tax returns or claims for refund for tax years ending on or after December 31, 2011.

(a.) The tax return preparer must complete Form 8867 or such other

form and such other information as may be required by the IRS to be submitted in the manner required by forms, instructions, or other appropriate guidance.

(b.) The tax return preparer’s completion of Form 8867 (or successor

form) must be based on information provided to the tax return preparer or otherwise reasonably obtained by the tax return

10

preparer. (c.) The tax return preparer must either complete the earned income

credit worksheet in the Form 1040 instructions or such other form and such other information as may be prescribed by the IRS or otherwise record in one or more documents in the tax preparer’s paper or electronic files the EIC computation, including the method and information used to make the computation.

(d.) The completion of the earned income credit worksheet or other

permitted record must be based on information provided by the taxpayer to the tax return preparer or otherwise reasonably obtained by the tax return preparer.

(e.) The tax return preparer must not know, or have reason to know,

that any information used by the tax return preparer in determining the taxpayer’s eligibility for, or the amount of, the EIC is incorrect. The tax return preparer may not ignore the implications of information furnished to, or known by, the tax return preparer, and must make reasonable inquiries if the information furnished to the tax return preparer appears to be incorrect, inconsistent, or incomplete. A tax return preparer must make reasonable inquiries if a reasonable and well-informed tax return preparer knowledgeable in the law would conclude that the information furnished to the tax return preparer appears to be incorrect, inconsistent, or incomplete. The tax return preparer must also contemporaneously document in the files the reasonable inquiries made and the responses to these inquiries.

(4) See IRM 20.1.6.5.7 (4) above which list the four examples from Treas.

Reg. 1.6695-2(b)(3)(ii). (5) See Treas. Reg. 1.6695-2(b)(4) regarding record retention. (6) See Treas. Reg. 1.6695-2(c) regarding special rule for firms. (7) See Treas. Reg 1.6695-2(d) regarding exceptions to the penalty.

11

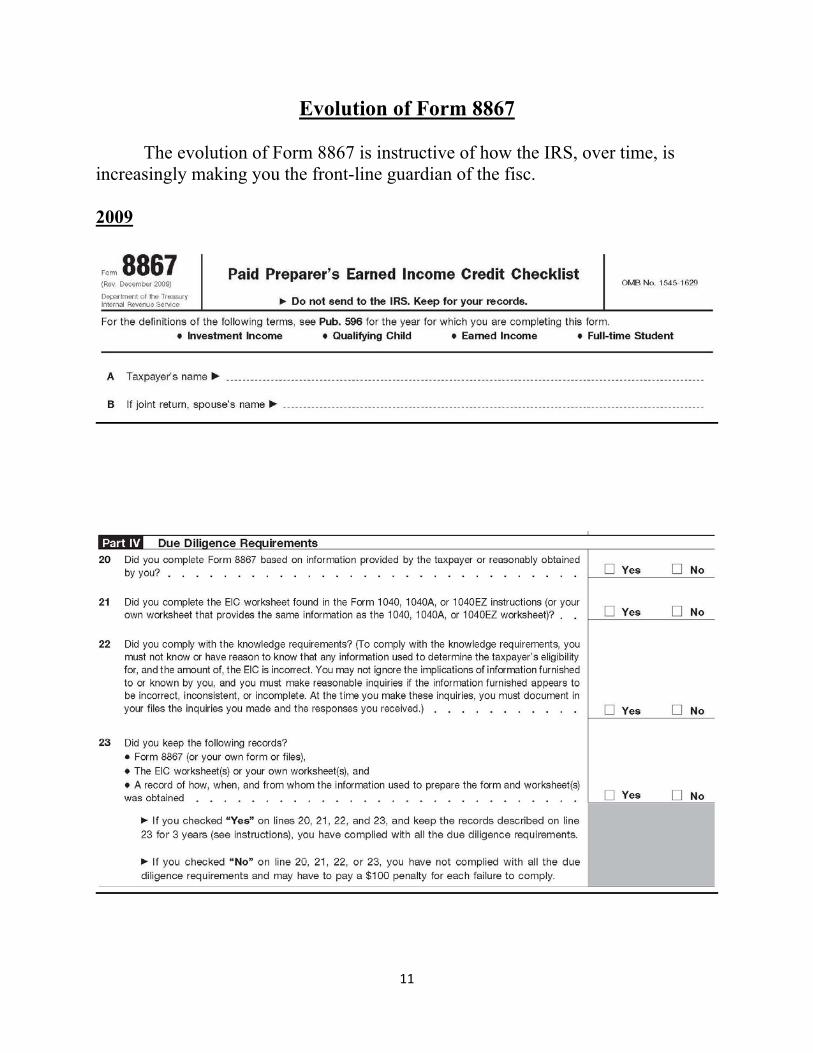

Evolution of Form 8867

The evolution of Form 8867 is instructive of how the IRS, over time, is increasingly making you the front-line guardian of the fisc. 2009

12

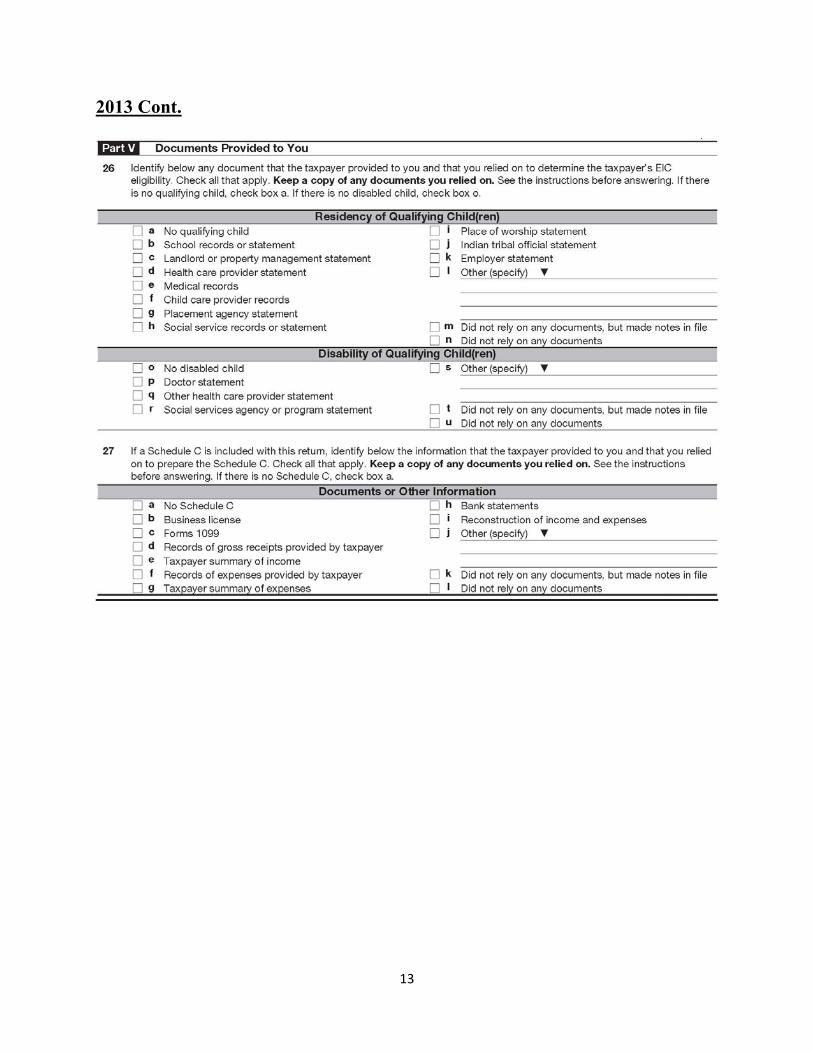

2013

13

2013 Cont.

14

2016

15

2016 Cont.

16

IRS Website

The IRS has also devoted significant resources to update, educate and provide sample materials to return prepares as to the Due Diligence Requirements for the EITC and CTC. There are literally dozens of pages devoted to EITC compliance including video on-line CPE and handout materials. The following page is an example.

17

18

19

20

Conclusion

Since the 1980’s, 1 in 5 returns claiming the EITC have errors either by mistake or outright fraud. The solution is becoming apparent. You, as the tax preparers, are now, like it or not, EITC auditors. And if you do not document asking your clients the right questions, or keep the right documents in your file, it could cost you $500 per mistake.