2016 Year-End Tax Planning Considerations · 2019-12-19 · 2019 Tax Talk Year -End Planning...

79

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms. FOR INTERNAL USE ONLY YEAR-END STATE AND LOCAL TAX PLANNING FOR BUSINESSES December 4, 2019

Transcript of 2016 Year-End Tax Planning Considerations · 2019-12-19 · 2019 Tax Talk Year -End Planning...

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms.

FOR INTERNAL USE ONLY

YEAR-END STATE AND LOCAL TAX PLANNING FOR BUSINESSES

December 4, 2019

1 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

CPE and SupportCPE Participation Requirements ‒ To receive CPE credit for this webcast: You will need to actively participate throughout the program. Be responsive to at least 75% of the participation pop-ups or polling questions.

Please refer the CPE & Support Handout by clicking Handout icon for more information about group participation and CPE certificates.

Q&A: Submit all questions by clicking the Q&A icon on the bottom of your screen. The presenters will review and answer questions at the end of the session as time permits.

*Please note that questions and answers submitted/provided via the Q&A feature are visible to all presenters as well as the participants.

Technical Support: BDO Employees: Please contact technical support at 888-236-9111Alliance, International, and invited Guests: Please contact : 844-580–6963

2 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

With You Today

DOROTHY RADICEVICHPrincipal

SALTProperty Tax

(312) [email protected]

TIM SCHRAMManaging Director

SALTCredits & Incentives

(312) [email protected]

LAURA BETH CURTISExperienced Senior

SALTUnclaimed Property

(312) [email protected]

3 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

With You Today

ERIC FADERManaging Director

SALTSales Tax

(312) [email protected]

MARIANO SORI-MARINPartnerSALT

Income Tax

(312) [email protected]

4 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Credits and Incentives

5 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

2019 C&I

Trends

TRANSPARENCYMore states establish processes to regularly

and rigorously evaluate their tax incentive

programs.

TARGETED INDUSTRYData centers are taking

center stage.

TARGETED JOBSIncreased opportunities for blue collar jobs and remote

workers.

BOARDER WARSStates agree to end economic

development border wars.

Credits & Incentives

6 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Council on State Taxation2019 Credits & Incentives Trends: Transparency

MICHIGANTENNESSEE IOWA

Michigan implements new incentive

evaluation procedures, which requires an

extensive evaluation of awarded incentives by a

third party.

Tennessee introduces a new bill that would impose

a higher level of transparency and

accountability for the State’s most widely used economic development

incentives.

Iowa faces increased pressure to implement transparency policies that keep taxpayers

well-informed.

Credits & Incentives

7 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Council on State Taxation2019 Credits & Incentives Trends: Border WarsMissouri and Kansas enter into an agreement to end economic

border war -Other states now considering the same.

Credits & Incentives

8 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Council on State Taxation2019 Credits & Incentives Trends: Targeted Jobs

High Impact Business Construction Jobs Credit

Enterprise Zone Construction Jobs Credit

River Edge Construction Jobs Credit

New Construction EDGE Credit

• Must qualify under the High Impact Business Program

• Must invest at least $12 million in qualified property

• Must be located in a certified Enterprise Zone

• Must invest at least $10 million in an EZ Construction Jobs Product

• Must be certified by the Department

• Must invest at least $10 million in New Construction EDGE Project

• Must be located in a River Edge Redevelopment Zone

• Must invest at least $1 million in a qualified rehabilitation plan

Illinois passes Blue Collar Jobs Act

Credits & Incentives

9 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Council on State Taxation2019 Credits & Incentives Trends: Targeted Jobs

MANUFACTURING

25%Of manufacturers had to turn down new business in Q1 2019

2.4 millionEstimated positions unfilled between 2018 + 2028 as a result of current skills gap

Credits & Incentives

10 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Council on State Taxation2019 Credits & Incentives Trends: Targeted Industry

Program Name/State Program Description Benefit

Bluegrass State Skills CorporationKentucky

Grant-In-Aid (GIA)

• Discretionary training grant

• Provides funding reimbursements to new and expanding businesses for skills and occupational upgrade training

Skills Training Investment Credit (STIC)

• Statutory, State income tax credits

• Offsets costs associated with approved training programs provided to new and incumbent workers

Max benefits under the two programs are equal to the lesser of:

• 50% of approved costs/eligible costs

• $75,000

• GIA: $2,000 x number of trainees

• STIC: $500 x number of full-time, Kentucky resident employees paid a minimum total hourly compensation of at least $12.51, including benefits

Jobs Investment Program (VJIP)Virginia

• Discretionary cash grant available to companies creating new jobs and/or experiencing technological change

• Offsets HR costs for new and expanding companies retraining their employees

• Funding is reimbursable 90 days after the trainee is hired, or after the retraining activity has occurred

• Funding is based on a customized budget determined by an assessment of the company’s recruiting and training activities

How are states + communities helping close the skills gap?

Credits & Incentives

11 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Council on State Taxation2019 Credits & Incentives Trends: Targeted IndustryREGIONAL CENTER FOR

MANUFACTURING The product of industry, education,

and government working together to close the skills gap

Offsite teaching facility for Northeast State Community College

Meeting the Industrial Training/Educational Needs of Existing Industry

Building a Pipeline of Industrial Skilled Labor for the Region

A Training/Educational Resource for Economic Development

Credits & Incentives

12 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

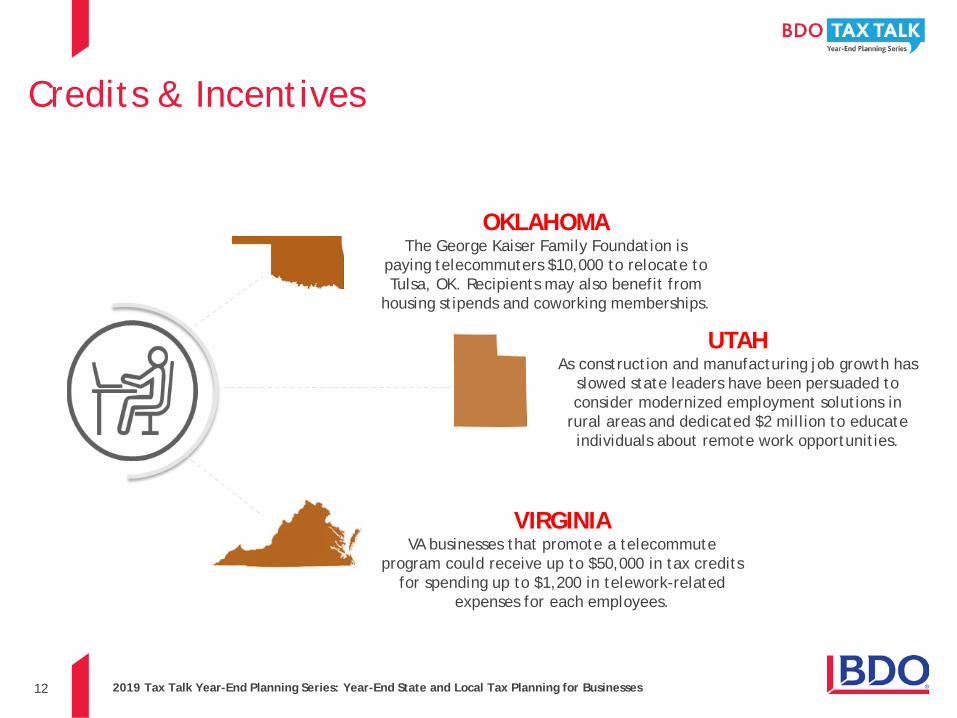

Council on State Taxation2019 Credits & Incentives Trends: Targeted Jobs

OKLAHOMAThe George Kaiser Family Foundation is

paying telecommuters $10,000 to relocate to Tulsa, OK. Recipients may also benefit from

housing stipends and coworking memberships.

UTAHAs construction and manufacturing job growth has

slowed state leaders have been persuaded to consider modernized employment solutions in

rural areas and dedicated $2 million to educate individuals about remote work opportunities.

VIRGINIAVA businesses that promote a telecommute

program could receive up to $50,000 in tax credits for spending up to $1,200 in telework-related

expenses for each employees.

Credits & Incentives

13 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Council on State Taxation2019 Credits & Incentives Trends: Targeted IndustryData Center-Specific

Incentive Opportunities

Spent on data centers in 2018 alone.

Credits & Incentives

14 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Council on State Taxation2019 Credits & Incentives Trends: Targeted Industry

Industry/State Program Description Benefit

Data CenterIllinois

• Effective January 1, 2019 new spending plan provides sales tax exemption on qualified equipment, as well as a 20% income tax break for data center operators

• Must create at least 20 net-new jobs paying wages equal to 120% or more of the county median

• Must invest at least $250 million within 5-years

• Facility must be carbon neutral or attain certification under an eligible green building program

• Existing data centers can obtain benefits retroactively if they met minimum job and capex requirements (or committed to the same) in the 5-year period immediately prior to January 1, 2020

• State and local sales tax exemption for up to 20-years

• 20% income tax credit if building in an underserved or impoverished area

Data CenterIndiana

• Effective July 1, 2019 new bill offers retroactive business personal property + sales tax exemption on eligible equipment and energy to data center projects

• Must invest at least $25 million in qualified equipment

o Eligible costs = those incurred after December 31, 2018

• Wages must be equal to 125% of county average

• Personal property + sales tax exemption for up to 25-yearso 50-years if qualified investment

is greater than $750 million

Credits & Incentives

15 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Property Tax

16 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

2019 Property Tax Updates

IL – Cook County “Data Modernization Bill” • Proposed by Cook County Assessor Kaegi- would require

commercial property owners to provide income and expense data annually

• Current Status: Re-referred to house rules committee in 2019 for next session

IL – Chicago Mayor’s 2020 budget• Budget shortfall largely addressed by increasing real

estate transfer tax and casino ownership restructuring.• As of the fall veto session, state did not approve change

to transfer tax. • Concern is need to increase property taxes to balance

budget.

CA – “Split-Roll” Reform Prop 13• Separates large Commercial/Industrial property from

Residential- basing assessment on Market Value, not Prop 13 value.

• Current Status: Qualified for November 2020 ballot as a constitutional amendment.

TX – Change in Filing Deadlines• Personal Property Renditions due 4/15 (previously 4/1).

38.0%

21.4%

8.5%

4.9%

6.2%

6.4%

4.8%3.3%

3.0% 1.6% 1.9%

Total State and Local Business Taxes, FY2018

Property Taxes onBusiness PropertyGeneral Sales Taxes onBusiness InputsCorporate Income Tax

Unemployment Insurance

Excise Taxes

Individual Income Tax onBusiness IncomeBusiness and CorporateLicensePublic Utility Taxes

Insurance Premium Taxes

Severance Taxes

Other Business TaxesFrom COST study “Total State and Local Business Taxes: State-by-State Estim

17 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Unclaimed Property

18 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Unclaimed Property IntroductionGeneral Information

All 50 states and the District of Columbia have enacted unclaimed property laws.

Examples of unclaimed property:• Uncashed or voided payroll or commission checks• Uncashed or voided payable/vendor checks• Gift certificates/gift cards• Customer merchandise credits, layaways, deposits, refunds or rebates• Overpayments/unidentified remittances• Suspense accounts• Unused/outstanding benefits (non-ERISA)• Miscellaneous income/bad debt expense accounts

19 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

UNCLAIMED PROPERTY INTRODUCTIONWhere Do I Report Unclaimed Property?

The Supreme Court of the United States in Texas v. New Jersey, established the following unclaimed property sourcing rule:• First, to the state of the rightful owner’s last known address, if known, or• Second, to the state of the holder’s incorporation (commercial domicile for

unincorporated entities).

Priority rules in Texas v. New Jersey were upheld in the subsequent cases Pennsylvania v. New York (escheat of money orders) and Delaware v. New York (unclaimed dividends and interest).

20 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

A new budget bill, A.B. 109, directs the California Controller to create an unclaimed property amnesty or voluntary disclosure program (“VDP”) within the next five months—on or before March 1, 2020

The purpose of a VDP program is to encourage compliance with state unclaimed property laws

Currently, California’s unclaimed property statue requires the controller to assess 12% interest on property from the date that the property should have been reported. While that penalty could be abated for reasonable cause, it is the holder’s burden to establish this and reasonable cause is narrowly defined

California’s prior VDP program ended in 2002 and other attempts to create a VDP program after 2002 were unsuccessful

Important State DevelopmentsProposed California Amnesty Program

21 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Important State DevelopmentsProposed California Amnesty Continued…

The proposed legislation permits the Controller to decide the specifics of the new plan

Ideally, to encourage compliance, the Controller’s plan would (1) waive interest; (2) provide release from liability for the covered years, including an audit release; and (3) limit the look-back period. Additionally, the Controller would retain some discretion to resolve disputed issues

22 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Important State DevelopmentsDelaware Compliance Review Program

Effective March 1, 2018, Delaware enacted a new compliance review program which seeks to review the annual compliance reports for reasonableness, based on:

company size Industry filing history

The reviews are expected to be completed by a combination of state employees and outside 3rd party auditing firms (reviewers). If the reviewers feel the report is inaccurate, under-reported, missing property types, etc., the reviewers can contact the company to ask questions and request records for that filing period.

If deficiencies are found, this could lead to other adverse consequences.

A copy of written policy and procedures will be requested by the reviewers.

23 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Important State DevelopmentsDelaware Audits/VDAs

Audit and VDA letters – Delaware is sending out batches of approximately 100 letters every 2-3 months

Expediated audits are due 12/11

SOS VDA No statutory due date Expectations of completion within 2 years

24 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Sales Tax

25 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Sales & Use Tax 2019 Update:

Nexus & Wayfair update

Who’s responsible for collecting/remitting tax?

Taxability issues

Exemptions

Planning & refund opportunities

26 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Sales & Use Tax 2019 Update:

Nexus & Wayfair Update

27 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

South Dakota v. Wayfair (June 21, 2018)

Pre-Wayfair sales tax nexus standard: Bright-line, physical-presence rule

• Quill Corp. v. North Dakota (1992)• National Bellas Hess v. Illinois (1967)

At issue in the Wayfair case: South Dakota’s economic nexus for sales/use taxes:

• $100,000 of sales delivered into South Dakota, or • 200 or more separate transactions for delivery into South Dakota

The U.S. Supreme Court held that the physical presence rule was “unsound and incorrect” and overruled Quill (1992).

The decision is not limited to

sales and use taxes.

It also removes the physical-presence rule for purposes of income,

franchise, and gross receipts taxes.

28 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

States with Sales and Use Tax Economic Nexus Laws

CA

OR

WA

NVUT

AZNM

CO

MT

WY

ID

ND

SD

KS

NE

OK

LATX

MO

AR

IA

MN

WI

IL IN

TN

KY

ALMS

FL

GA

MI

SC

NC

WVVA

PA

OH

NY

ME

NH

DE

RI

NJ

DC

HI

AK

Enacted statute, regulation, or bulletin

Statute/rule not enacted to date*

*AK, DE, MT, NH, OR have no general state imposed sales/use tax

VT

MD

CTMA

29 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

www.BDO.com/wayfair

30 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Sales/Use Tax Economic NexusLegislative Update:

Kansas Kansas law (since 2003):

• “Retailer doing business in this state” includes:“any retailer who has any other contact with this state that would allow this state to require the retailer to collect and remit tax under the provisions of the constitution and laws of the United States”

Kansas’ safe harbor legislation• Sales of $100,000 (eff. 10/1/2019) - S. 22

(vetoed 3/26/19)

8/1/19: DOR Notice 19-04 • Must collect & remit by

Oct. 1, 2019

9/30/19: AG Opinion 2019-8

• DOR’s new policy is of “no force or legal effect”

31 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Sales/Use Tax Economic NexusLegislative Update:

Missouri• Bills introduced Jan. 2019:

- All failed – adjourned

Florida• S. 1112: died in committee (5/3/19)• S. 126 (filed 8/14/19); H. 159 (filed 9/12/19)

- Remote sellers & safe harbor: 200 sales or $100,000- Proposed effective date: July 1, 2020- Both pending

32 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Proposed Federal Legislation:Sales Tax Nexus

Bills Title Proposal Status

H.R. 1933 &

S.2350

Online Sales Simplicity and Small Business Relief Act of 2019

• Small business remote sellers ($10M) immune until Congress acts Introduced

H.R. 379Protecting Businesses from Burdensome Compliance Cost Act of 2019

• Physical presence is the nexus standard until 1/1/2020 Introduced

S. 128 Stop Taxing Our Potential Act of 2019

• Physical presence is the nexus standard• Only sellers & purchasers have tax

obligationsIntroduced

33 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Sales/Use TaxPhysical Nexus

California• Issue: Amazon’s Fulfillment by Amazon (FBA):

- Inventory in warehouses in CA

• California’s Department of Tax and Fee Administration (CDTFA)- We’re seeking back taxes!

• State Treasurer Fiona Ma (D):- Urges: these remote sellers are not subject to sales tax!- Maintains that the CDTFA’s position on inventory nexus is wrong.

34 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Cookie Nexus:

Massachusetts• Blue Nile v. Massachusetts (Mass. S.Ct. 5/3/19)

- At issue: Regulation 830 CMR 64H.1.7- DOR’s motion to dismiss allowed. Retailers failed to exhaust administrative

remedies.

• Crutchfield Corp. v. Massachusetts (Va. Cir. Ct. 10/2/19)- Same issue. Held: No jurisdiction

Ohio• American Catalog Mailers Assn v. Ohio (Ohio Ct. Common Pleas 12/18/18)

- At issue: R.C. 5741.01(I)(2)(h) (substantial nexus = in-state software)- Plaintiff voluntarily dismissed case

35 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Sales Tax Compliance:A Strategic Approach

36 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Sales & Use Tax 2019 Update:

Who’s Responsible for Collecting/Remitting Sales Tax?

37 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

www.BDO.com/wayfair

38 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Who is Required to Collect & Remit?

Jefferson Parish, LA v. Wal-Mart.com USA, LLCFacts: Wal-Mart.com operates a marketplace and earns a fee commission.

Issue: Is Wal-Mart.com required to collect and remit local sales tax on all sales by third-party vendors?

Law: “Dealer” includes “every person who engages in regular or systematic solicitation of a consumer market in the taxing jurisdiction …” La. R.S. 47:301(4)(l).

Holding: La. S.Ct. (oral arguments on 10/22/19)

Fifth Cir. Ct. of Appeal (12/27/18): “dealer” (not seller) is liable

39 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Sales & Use Tax 2019 Update:

Taxability Issues

40 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

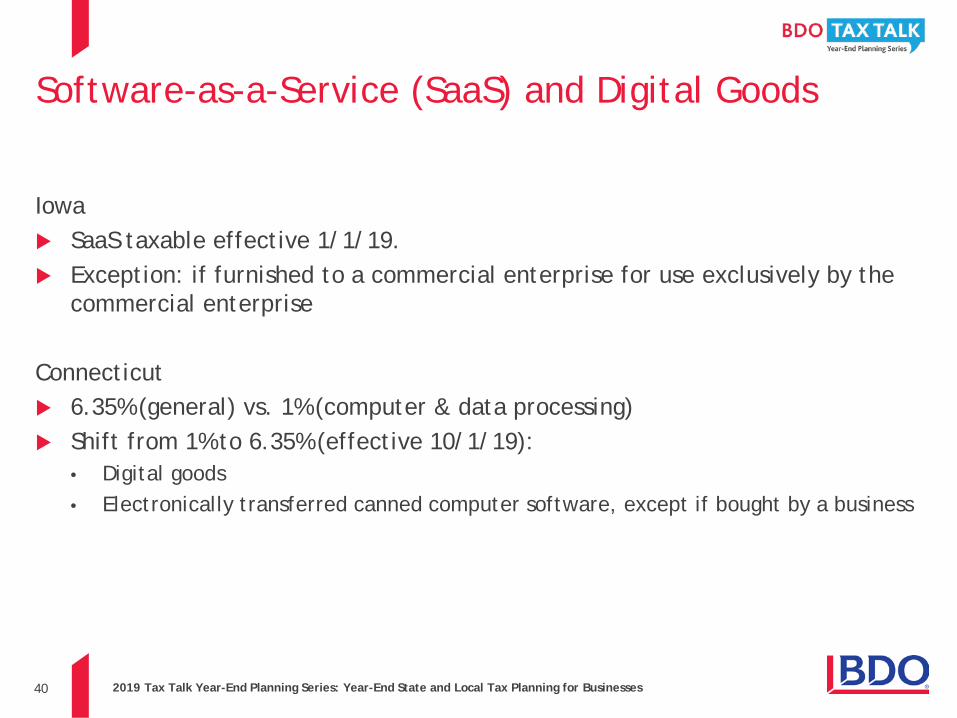

Software-as-a-Service (SaaS) and Digital Goods

Iowa SaaS taxable effective 1/1/19. Exception: if furnished to a commercial enterprise for use exclusively by the

commercial enterprise

Connecticut 6.35% (general) vs. 1% (computer & data processing) Shift from 1% to 6.35% (effective 10/1/19):

• Digital goods• Electronically transferred canned computer software, except if bought by a business

41 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Alabama Supreme Court:All software (even customized) is taxable!

Ex Parte Russell County Community Hospital, LLC (Al. S.Ct. 5/17/19) Facts: Medhost sold/installed software to a hospital

Paid ~ $18K in sales tax. Medhost filed a refund claim.

Holding: • “there is no distinction for Alabama sales-tax purposes between canned or custom

software”• “all software, including custom software created for a particular user, is ‘tangible

personal property’ for purposes of Alabama sales tax.

42 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Is taxing streaming services legal?

Labell v. City of Chicago (Ill. App. Ct. 11/21/19)• Facts: 9% tax on amusements delivered electronically (Netflix, Hulu,

Spotify, Amazon Prime)

But, automatic amusements (jukebox for music) - $150 tax yearly

• Issues: 1) sourcing

2) discrimination: Internet Tax Freedom Act (ITFA)

• Holding: Chicago’s ordinance is not facially invalid

43 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Sales & Use Tax 2019 Update:

Exemptions

44 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

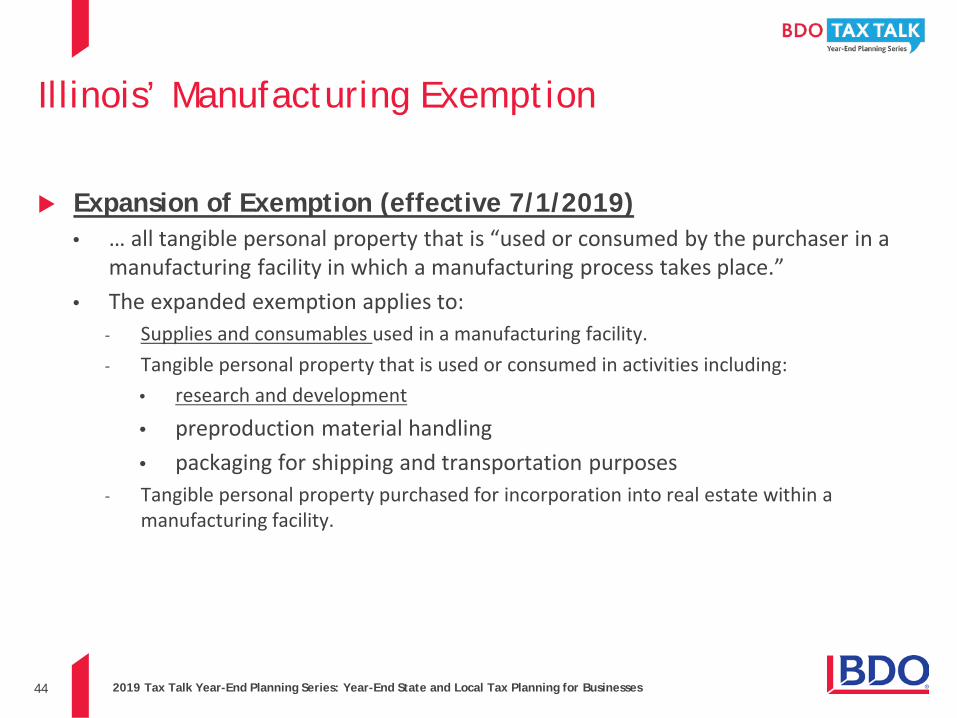

Illinois’ Manufacturing Exemption

Expansion of Exemption (effective 7/1/2019)• … all tangible personal property that is “used or consumed by the purchaser in a

manufacturing facility in which a manufacturing process takes place.”• The expanded exemption applies to:

- Supplies and consumables used in a manufacturing facility.- Tangible personal property that is used or consumed in activities including:

• research and development

• preproduction material handling• packaging for shipping and transportation purposes

- Tangible personal property purchased for incorporation into real estate within a manufacturing facility.

45 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Sales & Use Tax 2019 Update:

Planning & Refund Opportunities

46 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Refund Opportunities

State Developments

Alabama SSUT (Act 2015-448): Remote sellers may charge 8% rate; buyer may file annual refund

Texas H.B. 2153 (eff. 10/1/19) – remote sellers may use a single local use tax rate; buyers may file annual refund

Missouri SB 87 (signed 7/11/19) – extends the Missouri SOL for sales/use tax refunds from 3 years to 10 years.

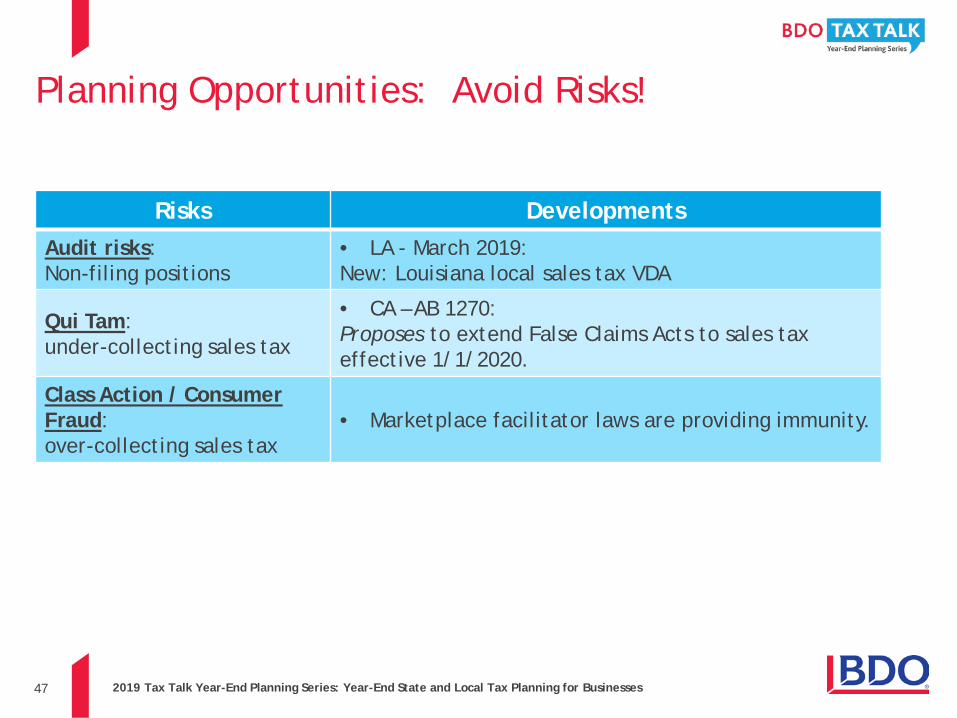

47 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Planning Opportunities: Avoid Risks!

Risks DevelopmentsAudit risks:Non-filing positions

• LA - March 2019: New: Louisiana local sales tax VDA

Qui Tam: under-collecting sales tax

• CA – AB 1270:Proposes to extend False Claims Acts to sales tax effective 1/1/2020.

Class Action / Consumer Fraud: over-collecting sales tax

• Marketplace facilitator laws are providing immunity.

48 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Income Tax

49 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

STATE INCOME & FRANCHISE TAX 2019 UPDATE

Federal Tax Reform Conformity/Decoupling Developments

State Tax Legislative Update

Apportionment Developments

Pass-Through Entities

50 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

2019 FEDERAL TAX REFORM CONFORMITY/DECOUPLING DEVELOPMENTS

51 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

CA*

OR

WA

NVUT

AZNM

CO

MT

WY

ID

ND

SD

KS

NE

OK

LATX

MO

AR*

IA(2019)

MN

WI

IL IN

TN

KY (2018)

ALMS

FL

GA

MI

SC

NC

WVVA

PA

OH

NY

ME

NH

DE

RI

NJ

DC

HI

AK

TCJA Conformity

Does Not Conform to TCJA

*Arkansas and California have conformed to a few of the TCJAamendments.

Status of State TCJA Conformity(as of 11/26/2019)

VT

MD

CT

MA

No CIT

** Most states selectively decouple from specific TCJA amendments.**

52 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

CA

OR (80%)

WA

NVUT

AZ(2019) NM

CO

MT (80%)

WY

ID (85%)

ND(70%)

SD

KS

NE

OK**

LATX

MO

AR

IA***(2019)

MN

WI

IL IN

TN**

KY

ALMS

FL

GA

MI

SC

NC

WVVA

PA

OH

NY(95%2019)

ME (50%)

NH***(2020)

DE

RI

NJ

DC

HI

AK

Full Inclusion (Gross GILTI)

Partial Subtraction (Net GILTI)*

Full Subtraction (Gross GILTI)

Partial Subtraction (Gross GILTI)

*State’s subtraction modification for GILTI explicitly applies to “net GILTI” or state requires an addition modification for the IRC 250(a)(1)(B) GILTI deduction.

**OK allocates intangible/GILTI income to a taxpayer’s state of commercial domicile. TN subtracts gross GILTI, but requires add-back of 5% of the gross GILTI amount.

***IA does not conform to IRC 951A for 2018, but conforms starting 2019. NH does not conform to IRC 951A for 2018 and 2019, but conforms starting 2020.

Also Note: AZ and NY GILTI subtractions inapplicable for 2018 tax years.

GILTI Treatment for Corporate Income Tax(as of 11/25/2019)

VT

MD

CT (95%)

MA (95%)

Full Inclusion (Net GILTI)

No IRC 951A Conformity

Full Subtraction (Net GILTI)*

Uncertainty

No CIT

NYC

53 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

CA

OR

WA

NVUT

AZNM

CO

MT

WY

ID

ND

SD

KS

NE

OK*

LATX

MO

AR

IA**(2019)

MN

WI

IL IN

TN

KY

ALMS

FL

GA

MI

SC

NC

WV VA

PA

OH

NY

ME

NH**(2020)

DE

RI

NJ

DC

HI

AK

“Line 28”

FDII Deduction Add-Back

*OK allocates deductions related to intangible income to a taxpayer’s state of commercial domicile.

**IA does not conform to IRC 250(a)(1)(A) for 2018, but conforms starting 2019. NH does not conform to IRC 250(a)(1)(A) for 2018 and 2019, but conforms starting 2020.

FDII Treatment( 11/25/2019)

VT

MD

CT

MA

No IRC 250 Conformity

FDII Deduction Allowed

Unknown

No CIT

NYC

54 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

2019 STATE TAX LEGISLATIVE UPDATE

55 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

2019 State Tax Legislative UpdateState Tax Reform

Indiana S.B. 563, enacted May 1, 2019 Indiana adopts market-based sourcing, effective for tax years beginning on or after January 1, 2019,

for sales of services and sales/licenses of intangibles. The Department of State Revenue is directed to adopt regulations implementing market-based sourcing, and to adopt the Multistate Tax Commission’s model market-based sourcing regulations.

Broadcasters and telecommunications companies will continue to use the income-producing activity/costs of performance sourcing method.

Also effective January 1, 2019, S.B. 563 adopts a provision that “income derived from Indiana shall be taxable to the fullest extent permitted by the Constitution of the United States and federal law, regardless of whether the taxpayer has a physical presence in Indiana.”

S.B. 563 also adds and addresses a number of economic development incentive provisions.-

56 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

2019 State Tax Legislative UpdateState Tax ReformKentucky H.B. 354, enacted Mar. 26, 2019 and H.B. 458, enacted Apr. 9, 2019 Among other provisions, both bills make technical corrections to Kentucky's unitary combined

reporting that became mandatory for tax years beginning on or after January 1, 2019 (enacted as part of H.B. 487, April 2018).

Changes the definition of "tax haven" to exclude a foreign country that has entered into a comprehensive tax treaty with the U.S.

Includes a U.S. tax treaty exception from the inclusion of income of a foreign corporation that is include in a Kentucky combined report (e.g., foreign corporation included under the “20% rule”).

NOL sharing among members also enacted.

Adds a deferred tax liability deduction for publicly traded companies, including affiliates, impacted by Kentucky's mandatory unitary combined reporting. Such groups will be allowed to take a deduction over a 10 year period, beginning January 1, 2024, to take into account a decrease in a deferred tax asset, an increase in a deferred tax liability, or an aggregate change from a deferred tax asset to deferred tax liability. Taxpayers that intend to take the deduction must notify the KY DOR by filing a statement with the DOR on or before July 1, 2019.

•

57 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

2019 State Tax Legislative UpdateState Tax Reform

New JerseyA. 4202, enacted July 1, 2018 and A. 4495, enacted October 4, 2018 Mandatory water’s-edge unitary combined reporting

• Initially effective (in A. 4202) for tax years beginning after 12/31/2019 - A. 4495 accelerated the effective date to tax years ending on or after July 31, 2019.

• Water’s-edge group includes:

- U.S. corporation, except 80/20 companies (average of property and payroll).

- Any corporation if has 20% or more of its property and payroll assigned to U.S. locations.

- Any corporations if it earns 20% or more of its income from intangible property or related services activities with respect to water’s-edge group members that are deductible as expenses for those members.

• Worldwide or federal affiliated group combined reporting election is provided; binding for year of election, plus five tax years.

-

58 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

2019 State Tax Legislative UpdateState Tax Reform

New JerseyA. 4202, enacted July 1, 2018 and A. 4495, enacted October 4, 2018• Mandatory Water’s-Edge Unitary Combined Reporting (con’t)

- Joyce rule is followed for sales factor sourcing – each member of the NJ water’s-edge group is treated as a separate taxpayer.

• However, see TB-86 (1/3/2019) – Division of Taxation applies Finnigan rule for purposes of P.L. 86-272 protection.

- Net deferred tax liability deduction allowed for public companies.

• The combined group can claim 10% of the “Deferred Tax Deduction” amount for a 10-year period, starting in the 5th year after combined reporting becomes effective.

• A combined group intending to claim this deduction must file a statement with the NJ Division of Taxation before July 1 the year subsequent to the first privilege period for which a combined return is required (e.g., before July 1, 2020).

59 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

2019 State Tax Legislative UpdateState Tax Reform

New JerseyA. 4202, enacted July 1, 2018 and A. 4495, enacted October 4, 2018 The combined NOL carryforward rules apply to tax years ending on or after July 31, 2019.

• Existing NOL rules extended by A. 4495 through tax years ending before July 31, 2019.

• The transition to unitary combined reporting creates the NJ “prior net operating loss” (PNOL). A. 4495 modifies the definition of PNOL as a “net operating loss incurred in a privilege period ending prior to July 31, 2019 and converted from a pre-allocation NOL to a post-allocation NOL” (i.e., post-apportionment NOL).

An existing provision which limits the carryforward of PNOL when there is a change in ownership greater than 50 percent will not apply when the ownership change is amongst members of a New Jersey combined reporting group.

60 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

New JerseyTB-86 (Jan. 3, 2019) Defines the entities included in a New Jersey unitary combined group if they are part of a unitary

business, including U.S. and foreign corporations, casinos, banking and financial corporations, "combinable captive insurance companies," as well as federal S corporations (and QSubs) that have not made a New Jersey S corporation election, among other entity types.

The technical bulletin also clarifies when members of a New Jersey combined group are subject to the $2,000 minimum tax. Only New Jersey combined group members with New Jersey nexus are subject to the minimum tax; however, such nexus is determined based on an economic presence.

Applies “Finnigan” approach to P.L. 86-272 protection and the minimum tax.

Combined Reporting/Filing OptionsLegislative & Administrative Developments

61 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

New JerseyTB-89 (May 21, 2019) Addresses a number of NJ combined return mechanics.

New Jersey combined return defaults to a water's-edge basis unless the managerial member of the group makes an election to file a world-wide combined group return or elects to file an affiliated group return.

"Commonly owned, directly or indirectly," means that more than 50% of the voting control of each member is directly or indirectly owned by a common owner or owners.

The definition of "commonly owned" and "common ownership" include constructive and attributional ownership under IRC Section 318.

A managerial member makes the world-wide group election or the affiliated group election on a timely filed original return in the tax year it becomes effective, "not before or after."

Sourcing gross receipts for purposes of the NJ combined group's sales factor:

• Water's-edge or world-wide group - the "Joyce rule" applies.

• Affiliated group method - the "Finnigan rule" applies.

Combined Reporting/Filing OptionsLegislative & Administrative Developments

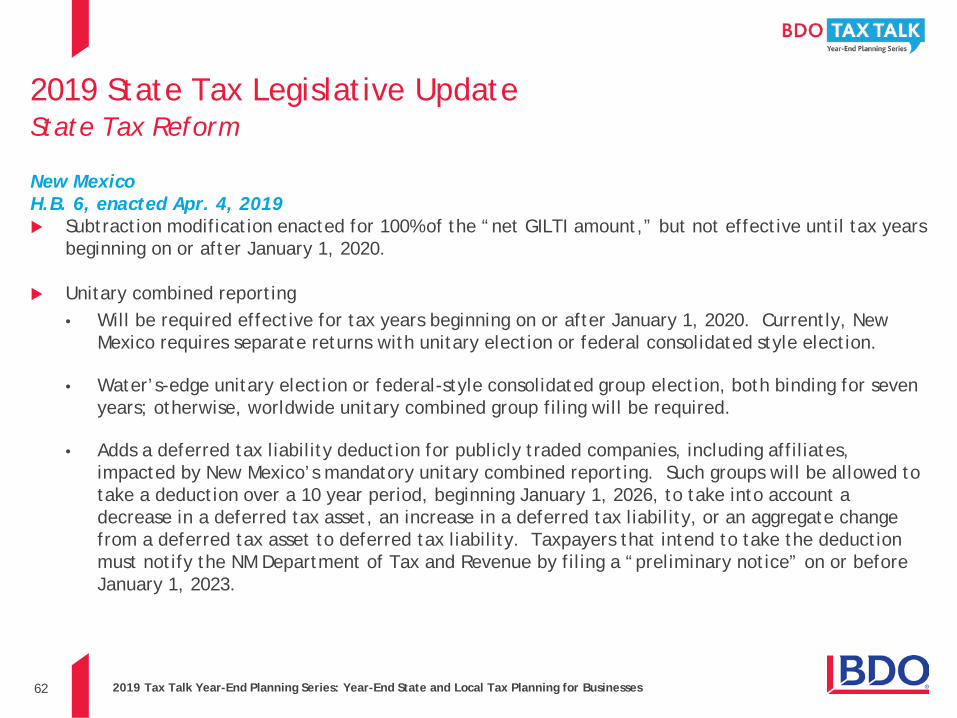

62 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

New MexicoH.B. 6, enacted Apr. 4, 2019 Subtraction modification enacted for 100% of the “net GILTI amount,” but not effective until tax years

beginning on or after January 1, 2020.

Unitary combined reporting• Will be required effective for tax years beginning on or after January 1, 2020. Currently, New

Mexico requires separate returns with unitary election or federal consolidated style election.

• Water’s-edge unitary election or federal-style consolidated group election, both binding for seven years; otherwise, worldwide unitary combined group filing will be required.

• Adds a deferred tax liability deduction for publicly traded companies, including affiliates, impacted by New Mexico’s mandatory unitary combined reporting. Such groups will be allowed to take a deduction over a 10 year period, beginning January 1, 2026, to take into account a decrease in a deferred tax asset, an increase in a deferred tax liability, or an aggregate change from a deferred tax asset to deferred tax liability. Taxpayers that intend to take the deduction must notify the NM Department of Tax and Revenue by filing a “preliminary notice” on or before January 1, 2023.

2019 State Tax Legislative UpdateState Tax Reform

63 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

OregonH.B. 3427, enacted May 16, 2019 Imposes a new Oregon “corporate activity tax” on “commercial activity” in Oregon, effective for tax

years beginning on or after January 1, 2020.

The Oregon CAT is not restricted to corporations, rather any “person” with Oregon commercial activity is subject to the tax, with some exceptions.

• Imposed at a rate of $250 plus 0.57 percent of the person’s taxable commercial activity that exceeds $1 million.

• A “person” is defined to include not only corporations, but also individuals, partnerships, limited liability companies, business trusts, trusts, estates, clubs, societies, C corporations, S corporations, qualified subchapter S subsidiaries, and entities that are disregarded for federal income tax purposes.

• Persons with less than $1 million in taxable commercial activity for the calendar year, tax-exempt organizations, governmental entities, certain hospitals, and certain other entities are exempt from the Oregon CAT.

A “unitary group of persons” will be treated as a single taxpayer for tax base, tax jurisdiction, apportionment, and the less than $ 1 million taxable commercial activity exemption.

2019 State Tax Legislative UpdateState Tax Reform

64 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

OregonH.B. 3427, enacted May 16, 2019 (con’t) Oregon CAT is imposed on any person with “substantial nexus” in Oregon, defined to include “bright-

line presence,” which means a person has either (a) $50,000 in property, (b) $50,000 in payroll, (c) $750,000 of “commercial activity” sourced to Oregon, or (d) at least 25 percent of the person’s total property, total payroll, or total “commercial activity” is in Oregon.

• The new statute also asserts that the Oregon CAT is not subject to Public Law 86-272.

The tax base is “commercial activity” sourced to Oregon, less 35 percent of the greater of the person’s “cost inputs” or “labor costs.”

• “Commercial activity” means the total amount realized by a person, arising from transactions and activity in the regular course of the person’s trade or business, without trade or business expense deductions.

• “Cost inputs” are defined as cost of goods sold under Internal Revenue Code (IRC) Section 471, and “labor costs” are defined as total compensation to employees, excluding compensation to any single employee in excess of $500,000. The deduction for cost inputs or labor costs is apportioned using the corporate income excise and income tax apportionment formula (a single sales factor formula).

• The subtraction for apportioned cost inputs or labor costs is limited to 95 percent of the person’s commercial activity sourced to Oregon.

2019 State Tax Legislative UpdateState Tax Reform

65 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

OregonH.B. 3427, enacted May 16, 2019 (con’t)

• 43 different items are excluded from the Oregon CAT tax base (i.e., excluded from the definition of “commercial activity”), including dividends, interest income, distributive share of income from pass-through entities, and intercompany receipts between unitary group members.

Commercial activity will be apportioned using market-based sourcing, which will also determine the $750,000 sales threshold for purposes of the “bright-line presence” definition of substantial nexus.

The statute does not explicitly limit the composition of a “unitary group of persons” to the “water’s-edge.”

2019 State Tax Legislative UpdateState Tax Reform

66 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

APPORTIONMENT

67 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Market-Based Sourcing – Current Status

Market-Based Sourcing

Where Benefit Received

Market-Based Sourcing

Where Service Received

Market-Based Sourcing

Where Service Delivered

Market-Based Sourcing

Where Customer Located

Arizona (election) Connecticut Alabama Georgia

California Hawaii (2020) Colorado (2019) Maryland

Iowa Illinois District of Columbia Nebraska

Michigan Maine Indiana (2019) Oklahoma

Missouri (election)* Minnesota Kentucky

New Jersey (7/1/2019) Louisiana

New York Massachusetts

New York City Montana

Rhode Island New Mexico (2020)

Utah Oregon

Wisconsin Pennsylvania

Tennessee

Vermont (2020)

*Missouri will require market-based sourcing starting 2020

68 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Single Sales Factor FormulasArizona (election) Illinois Minnesota Oregon

Arkansas (2021) Indiana Missouri (election/required 2020)

Pennsylvania

California Iowa Nebraska Rhode Island

Colorado Kentucky New Jersey South Carolina

Connecticut Louisiana New York Texas

Delaware (2020) Maine New York City Utah (elections/required2021)

District of Columbia Maryland (2022) North Carolina Wisconsin

Georgia Michigan

*States may require SSF for specific industries (e.g., financial institutions, transportation companies, etc.). MD and MA require manufacturers to use SSF. MS and VA require retailers to use SSF (and debt

buyers for VA). TN, UT, and VA provide an election to manufacturers to use SSF. TN provides asset management partnerships with a SSF election.

69 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

UtahUtah Laws 2018, H.B. 293, effective Jan. 1, 2019 H.B. 293 supersedes S.B. 72, eliminates the provisions related to “single sales factor taxpayers,” modifies provisions

related to “optional apportionment taxpayers,” and adopts provisions for “phased-in sales factor taxpayers.” Optional Apportionment Taxpayers

• A taxpayer is an optional apportionment if the average of its property and payroll factors is greater than 0.50.

• Allows an optional apportionment taxpayer to choose between a single sales factor apportionment formula (previously a double-weighted sales factor formula) or an evenly weighted three-factor formula

Phased-In Sales Factor Weighted Taxpayers• For taxable years beginning before January 1, 2020, a taxpayer is a phased in sales factor

weighted taxpayer if it is not a “sales factor weighted taxpayer” and does not meet the definition of an optional apportionment taxpayer.

• For taxable years beginning on or after January 1, 2020, a taxpayer is a phased-in sales factor weighted taxpayer if it meets the definition of an optional apportionment taxpayer and apportioned income as a phased-in sales factor weighted taxpayer during the previous taxable year.

• A “sales factor weighted taxpayer” means a taxpayer that generates greater than 50% of its total sales in activities classified under NAICS codes other than 21 – Mining, 2212 – Natural Gas Distribution, 31-33 – Manufacturing, 48-49 – Transportation and Warehousing, or 51 – Information and 52 – Finance and Insurance.

Single Sales Factor FormulaLegislative Developments

70 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

UtahUtah Laws 2018, H.B. 293, effective Jan. 1, 2019 (cont’d) A phased-in sales factor weighted taxpayer apportions income as follows:

• 2019 – Three-factor formula, with the sales factor multiplied by four

• 2020 – Three-factor formula, with the sales factor multiplied by eight

• 2021 – Single sales factor

Single Sales Factor FormulaLegislative Developments

71 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

PASS-THROUGH ENTITIES

72 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Pass-Through Entities – “PTE Taxes”Louisiana S.B. 223, enacted June 22, 2019 Provides an election for a pass-through entity (partnership, LLC, S corporation) to pay a “PTE income

tax.” Election is binding until revoked.

Effective for tax years beginning on or after January 1, 2019.

Graduated rates:

• 2% on first $25,000 of PTE’s taxable income.• 4% on the next $75,000.• 6% on taxable income above $75,000.

PTE allowed the C corporation federal income tax deduction, as if it had filed a federal 1120.

Shareholder, partner, member excludes their distributive share of PTE income or loss.

Election must be made either:

• Any time during the preceding tax year; or• Any time during the tax year and on or before the 15th day of the fourth month after close.

Termination: more than 50% of interests consent to revocation. DOR may terminate upon material change in circumstances, including significant change in federal tax law.

73 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Pass-Through Entities – “PTE Taxes”

Oklahoma H.B. 2665, enacted Apr. 29, 2019 Provides an election for a pass-through entity (partnership, LLC, S corporation) to pay a “PTE income

tax.” Election is binding until revoked.

Effective for tax years beginning on or after January 1, 2019.

Partners/members whose only Oklahoma source income is from the electing PTE are relieved of obligation to file Oklahoma tax returns.

Distributive shares of income to partners/members that are individuals, trusts or estates are aggregated and subject to 5% tax rate (highest marginal individual rate). Distributive shares of income to corporations, financial institutions, or another PTE are aggregated and subject to 6% tax rate.

If PTE has a net loss, it is eligible to be carried back two years or forward 20 years.

74 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

Pass-Through Entities – “PTE Taxes”

Wisconsin S.B. 883, enacted Dec. 14, 2018 Persons owning more than 50% of the capital and profits interests in a partnership (or LLC taxed as a

partnership) or owning more than 50% of the shares of an S corporation may make an annual electionfor the PTE to be taxed at the entity level.

Effective for S corporations starting with the 2018 tax year and for partnerships/LLCs starting with the 2019 tax year.

The PTE will be taxed at the Wisconsin corporate rate of 7.9%.

The PTE may not carry forward losses.

The only tax credits that the PTE may claim are for PTE-level taxes paid to other states, including for composite returns.

75 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

ENTITY LEVEL TAXESMost States Also Follow Federal Pass-through Treatment No tax on the PTE, but tax on the partners

• Alabama (Business Privilege Tax)• California (LLC Fee and Minimum Tax)• Connecticut (Effective 2018)• District of Columbia• Illinois (Replacement Tax)• Kentucky (LLET)• Minnesota (Fee based on MN Appt. Factors)• New Hampshire (BET and BPT)• New Jersey (Fee based on # of partners;

Minimum fee for S Corps)• New York (Fee based on NYS Gross Receipts)• Nevada (Commerce Tax)

• Ohio (CAT)• Oklahoma (Effective 2019)• Oregon (CAT enacted 5/16/19)• Rhode Island (Minimum Fee)• Tennessee (Excise and Franchise Tax)• Texas (Franchise Tax)• Vermont (Minimum Fee)• Washington (B&O Tax)• Wisconsin (Eff. 2018 for S Corps, 2019 for Partnerships)• City taxes: Philadelphia (BIRT, NPT), NYC (UBT), KY, MI,

OH

Some Noteworthy Exceptions and Variations:

76 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

General Disclaimer:

These materials do not constitute tax or legal advice, and cannot be relied upon for purposes of avoiding penalties under the Internal Revenue Code. These materials may omit discussion of exceptions, qualification, definitions, effective dates, jurisdictional differences, and other relevant authorities and considerations. In no event should a reader rely on these materials in planning a specific transaction. BDO will not be responsible for any error, omission, or inaccuracy in these materials.

Questions?

Tim Schram – [email protected] Dorothy Radicevich – [email protected] Laura Beth Curtis – [email protected] Eric Fader - [email protected] Mariano Sori-Marin – [email protected]

77 2019 Tax Talk Year-End Planning Series: Year-End State and Local Tax Planning for Businesses

ConclusionThank you for your participation!

Certificate Availability – If you logged in and participated the entire time and responded to at least 75% of the pop-ups or polling questions, your certificate will be emailed to you within 48 hours of the webinar.

After 48 hours your certificate will also be available under your profile on BDO.com*.

More information is available by clicking the handouts icon on the screen.

Please exit the interface by clicking the “X” button in the upper right hand corner of your screen.

*If you are participating as part of group, please allow additional time for CPE processing.

78

BDO is the brand name for BDO USA, LLP, a U.S. professional services firm providing assurance, tax, and advisory services to a wide range of publicly traded and privately held companies. For more than 100 years, BDO has provided quality service through the active involvement of experienced and committed professionals. The firm serves clients through more than 60 offices and over 650 independent alliance firm locations nationwide. As an independent Member Firm of BDO International Limited, BDO serves multi-national clients through a global network of more than 73,800 people working out of nearly 1,500 offices across 162countries.

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms. BDO is the brand name for the BDO network and for each of the BDO Member Firms. For more information please visit: www.bdo.com.

Material discussed is meant to provide general information and should not be acted on without professional advice tailored to your needs.

© 2019 BDO USA, LLP. All rights reserved.