2016 - Amazon Web Services · Android or other smartphone 46% BlackBerry 2% 3% Other 3% Cell phone...

8

The latest statistics and commentaries about the financial game-changer that is mobile payments. 2016 Mobile Payments State of the Industry Mobile Payments State of the Industry ©2016 Networld Media Group SAMPLE Mobile Payments State of the Industry ©2016 Networld Media Group SAMPLE

Transcript of 2016 - Amazon Web Services · Android or other smartphone 46% BlackBerry 2% 3% Other 3% Cell phone...

The latest statistics and commentaries about the financial game-changer that is mobile payments.

2016Mobile Payments State of the Industry

Mobile Payments

State of the Industry

©2016 Networld Media GroupSAMPLE

Mobile Payments

State of the Industry

©2016 Networld Media GroupSAMPLE

2Mobile Payments State of the Industry | © 2016 Networld Media Group

CONTENTSCONTENTS

Mobile Payments State of the Industry 2016 ©2016 Networld Media Group. 13100 Eastpoint Park Blvd., Louisville, KY 40223. (502) 241-7545. All rights reserved. No part of this publication may be reproduced without the express written approval of the publisher. Viewpoints of the contributors and editors are their own and do not necessarily represent the viewpoints of the publisher.

Page 3 Executive Summary Will Hernandez, editor, MobilePaymentsToday.com

Page 9 U.S. Consumer Survey Results

Page 19 U.K. Consumer Survey Results Page 28 Industry Survey Results

Page 40 A Snapshot of the Mobile Capture Opportunity Shirra Frost, director of product marketing, Fiserv

Page 43 Loyalty Applications and Payments: Are Consumers Ready? Stacey Finley Tappin, senior vice president of sales and marketing communications, Apriva

Page 45 The Future Is Biometric, But Privacy Fears Must Be Confronted Sirpa Nordlund, executive director, Mobey Forum

Page 47 The Merging of Social Media, Payments and Mobile Michael Hagen, corporate ID strategist and managing director, IDchecker

Page 49 What’s the Added Value in Mobile Payments? Ben Kaplan, president and CEO, CashStar

Will Hernandez, editor Mobile Payments Today

Brittany Warren, custom content [email protected]

Alan Fryrear, chairman & CEO [email protected]

Tom Harper, [email protected]

Kathy Doyle, executive vice president and publisher

Mobile Payments

State of the Industry

©2016 Networld Media GroupSAMPLE

3Mobile Payments State of the Industry | © 2016 Networld Media Group

US CONSUMER SURVEY RESULTS

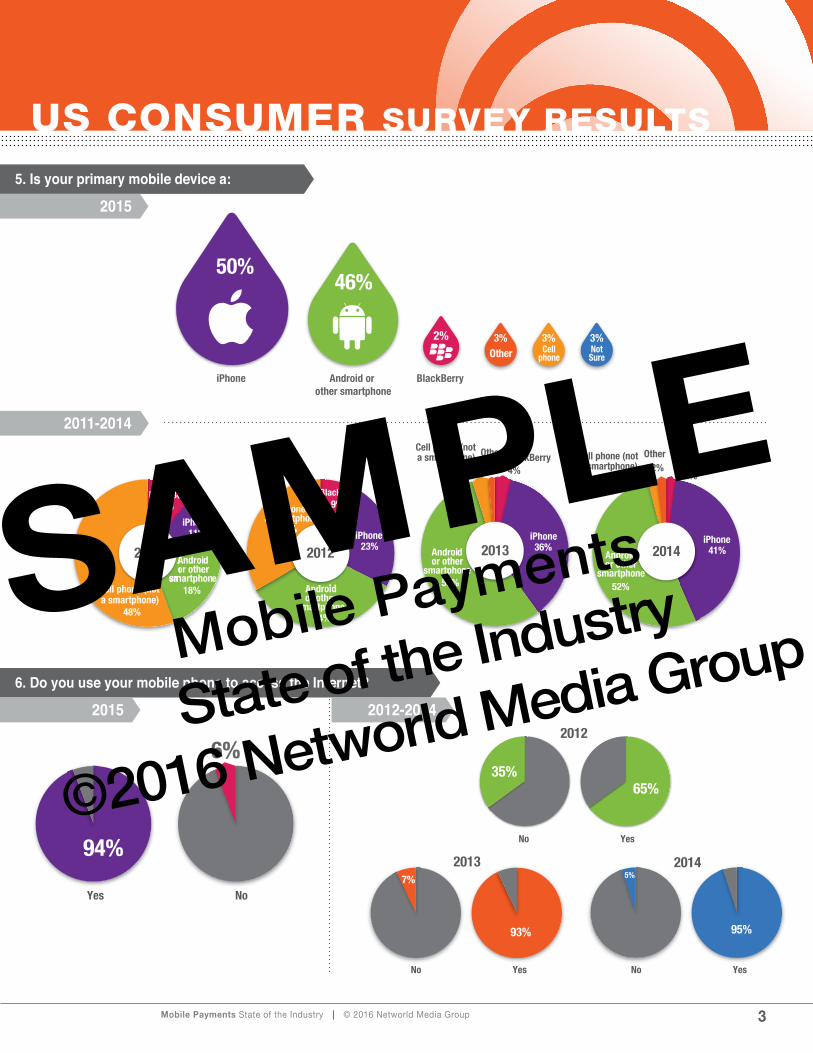

5. Is your primary mobile device a:

6. Do you use your mobile phone to access the Internet?

94%

6%

No Yes

35% 65%

2012

No Yes

7%

93%

2013

No Yes

5%

95%

2014

iPhone

50%

Android or other smartphone

46%

BlackBerry

2% 3%Other

3%Cell

phone

3%NotSure

2011-2014

BlackBerry 9% iPhone

11%

Androidor other

smartphone18% Cell phone (not

a smartphone) 48%

BlackBerry 9%

iPhone 23%

Android or other

smartphone 34%

Cell phone (not a smartphone)

33%

BlackBerry BlackBerry

4%

iPhone 36%

55%

Cell phone (not a smartphone) Cell phone (not

a smartphone) 4%

Other Other 1%

Androidor other

smartphone

2%

iPhone 41%

52%

2%

2011 2013 2014

2%

Androidor other

smartphone

2012

2015

2015

2012-2014

Mobile Payments

State of the Industry

©2016 Networld Media GroupSAMPLE

CONSUMER SURVEY RESULTS

4Mobile Payments State of the Industry | © 2016 Networld Media Group

UK CONSUMER SURVEY RESULTS

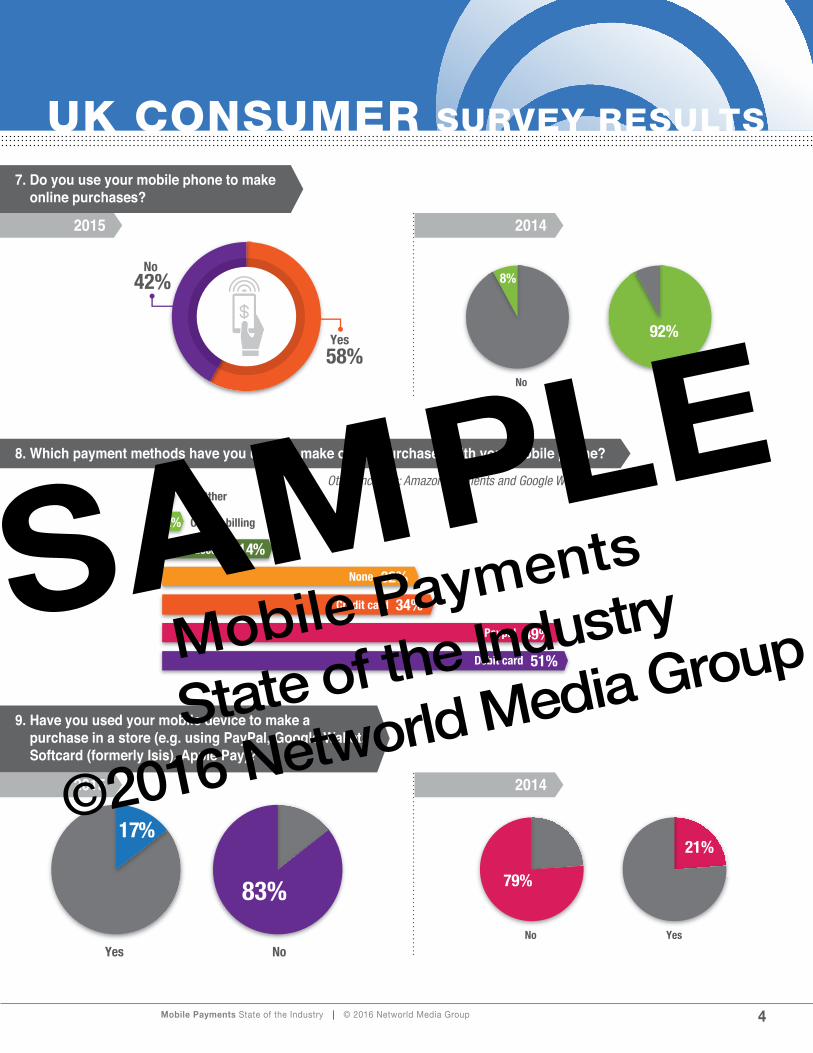

7. Do you use your mobile phone to make online purchases?

Yes 58%

No 42%

8. Which payment methods have you used to make online purchases with your mobile phone?

Other includes: Amazon Payments and Google Wallet

49%

51%

34%

32%

14%

1%

2%

Paypal

Debit card

None

Credit card

Bank account

Other

Carrier billing

2015

2015

2014

2014

No Yes

8%

92%

9. Have you used your mobile device to make a purchase in a store (e.g. using PayPal, Google Wallet, Softcard (formerly Isis), Apple Pay)?

83%

17%

No Yes

79%

21%

Mobile Payments

State of the Industry

©2016 Networld Media GroupSAMPLE

INDUSTRY SURVEY RESULTS

5Mobile Payments State of the Industry | © 2016 Networld Media Group

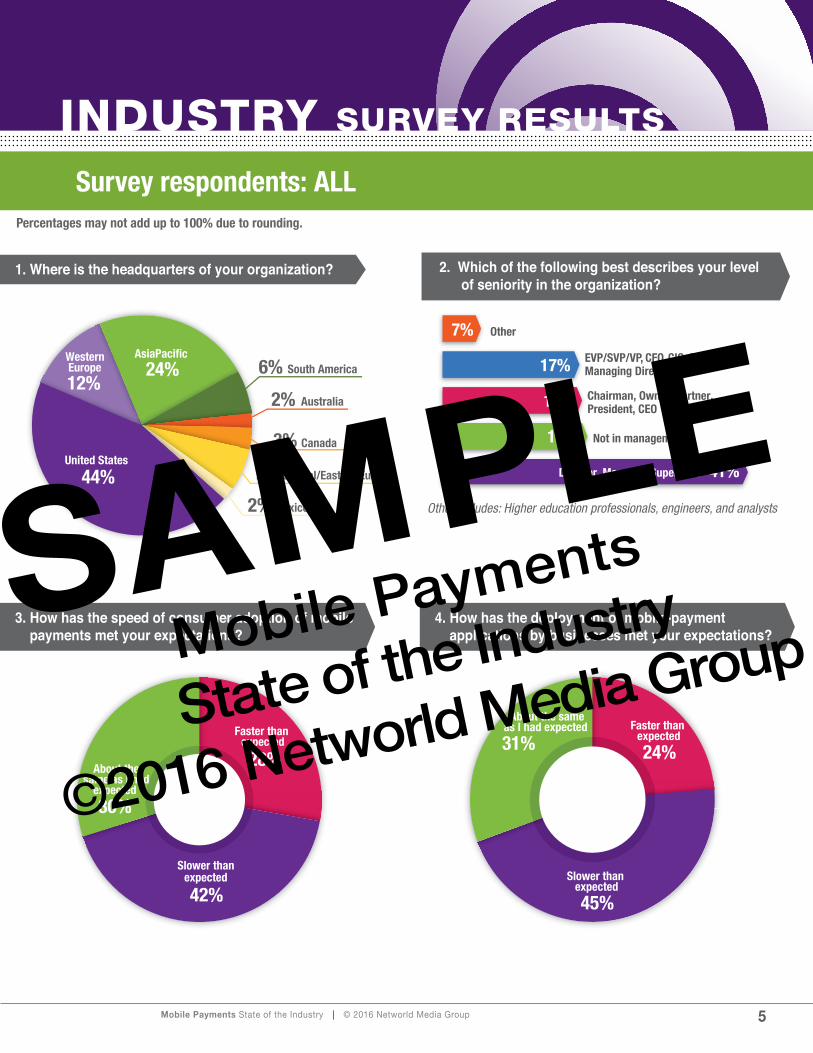

Survey respondents: ALL

1. Where is the headquarters of your organization?

3. How has the speed of consumer adoption of mobile payments met your expectations?

4. How has the deployment of mobile-payment applications by businesses met your expectations?

2. Which of the following best describes your level of seniority in the organization?

Percentages may not add up to 100% due to rounding.

Other includes: Higher education professionals, engineers, and analysts

Faster than expected

28%

Slower than expected

42%

About the same as I had

expected

30%

d

AsiaPacific

24%

Australia 2%

Canada 3%

Central/Eastern Europe 7%

Mexico 2%

United States

44%

South America 6% Western Europe

12%

Other

Not in management

EVP/SVP/VP, CFO, CIO, COO, Managing Director

Chairman, Owner, Partner, President, CEO

41%

19%

18%

17%

7%

Director, Manager, Supervisor

Faster than expected

24%

Slower than expected

45%

31%

About the same as I had expected

Mobile Payments

State of the Industry

©2016 Networld Media GroupSAMPLE

INDUSTRY SURVEY RESULTS

6Mobile Payments State of the Industry | © 2016 Networld Media Group

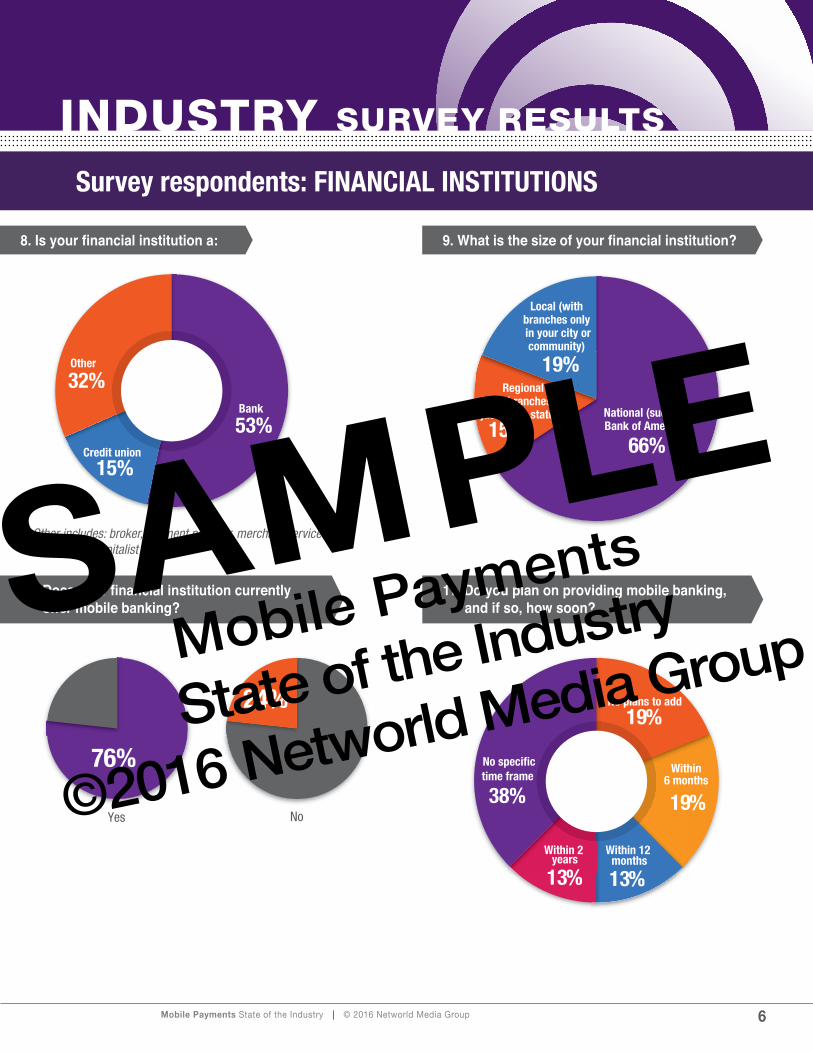

8. Is your financial institution a: 9. What is the size of your financial institution?

10. Does your financial institution currently offer mobile banking?

11. Do you plan on providing mobile banking, and if so, how soon?

Survey respondents: FINANCIAL INSTITUTIONS

Other includes: broker, payment provider, merchant services, and venture capitalist

Bank

53% Credit union

15%

Other

32% Regional(with branches in just a few states) National (such as

Bank of America)

66% 15%

Local (with branches only in your city orcommunity)

19%

No plans to add

19%

Within 6 months

19%

Within 12 months

13%

Within 2 years

13%

No specifictime frame

38%

24%

76%

Mobile Payments

State of the Industry

©2016 Networld Media GroupSAMPLE

INDUSTRY SURVEY RESULTS

7Mobile Payments State of the Industry | © 2016 Networld Media Group

37. Among the different industry stakeholders, which has the greatest chance to provide the best mobile wallet experience?

38. Will some form of consolidation/mergers happen in the future among mobile wallet providers as more companies enter this market?

Survey respondents: SOFTWARE/APPLICATION PROVIDER/DEVELOPER

Other includes: Google, Apple, Samsung, and consortiums of like compaies

Banks

28%

Retailers

14% Telcos

15%

Third-party developers

36%

Other7%

92%

8%

Mobile Payments

State of the Industry

©2016 Networld Media GroupSAMPLE

To download the rest of this report click HERE

Use coupon code MPT15 to receive 15% off this report.

© 2016 NETWORLD MEDIA GROUP

2016Mobile Payments State of the Industry