2015 Refresh of DTZ 2009 Economic Viability Assessment … · 2015 Refresh of DTZ 2009 Economic...

32

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council Valuation Team: Kendal Valuation Surveyor: Matt Messenger BSocSc(Hons) DipVal MRICS (RICS Registered Valuer) Date: December 2015 Contact: [email protected] Providing Valuation Services in partnership with North-West Public Sector Clients including: Allerdale Borough Council - Barrow Borough Council - Carlisle City Council - Cumbria County Council, Eden District Council - Home Group - Hyndburn Borough Council - Lancaster City Council South Lakeland District Council - South Lakes Housing - Wyre Borough Council Yorkshire Dales National Park Authority

Transcript of 2015 Refresh of DTZ 2009 Economic Viability Assessment … · 2015 Refresh of DTZ 2009 Economic...

2015 Refresh of DTZ 2009 Economic Viability Assessment

for Eden District Council

Valuation Team: Kendal Valuation Surveyor: Matt Messenger BSocSc(Hons) DipVal MRICS (RICS Registered Valuer) Date: December 2015 Contact: [email protected]

Providing Valuation Services in partnership with North-West Public Sector Clients including:

Allerdale Borough Council - Barrow Borough Council - Carlisle City Council - Cumbria County Council, Eden District Council - Home Group - Hyndburn Borough Council - Lancaster City Council

South Lakeland District Council - South Lakes Housing - Wyre Borough Council Yorkshire Dales National Park Authority

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

1

Contents

Section 1: Context

Section 2: Method

Section 3: Commentary on Updated Assumptions

Section 4: Commentary on 2015 Site Viability Results

Section 5: Publication and other uses

Appendix 1: Economic Viability Assessment – Baseline Assumptions – NPS 2015 Update

Appendix 2: Summary results arising from NPS DCF Residual Viability Assessment (2015 Baseline Assumptions)

Appendix 3: Average house price and floor area analysis 2013

Appendix 4: Comparison of NPS 2013 and DTZ Average sale price and floor area assumptions

Appendix 5: Comparison of NPS 2015 unit prices and unit sizes and DTZ 2009 average sale price and floor area assumptions

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

2

Section 1: Context 1.1 In 2009 Eden District Council (‘EDC’) commissioned DTZ to undertake an

Affordable Housing Economic Viability Assessment (‘AHEVA’) for Eden District.

1.2 EDC’s Core Strategy was submitted to the Secretary of State for

examination in April 2009. At the Pre-Hearing meeting held in July 2009, EDC agreed with the Inspector to provide an AHEVA in support of the Council’s affordable housing policy (CS10) and reschedule the hearing session on this policy to December 2009. The aim of the AHEVA was to assess the viability of the baseline affordable housing policy as drafted within the Core Strategy, and develop an effective means of assessing an appropriate and justifiable affordable housing target in the District.

1.3 The completed DTZ study formed a key part of the Core Strategy

examination evidence base and ultimately led to approval by the Core Strategy Inspector of EDC’s affordable housing policy, which requires that in appropriate and relevant circumstances all new developments of sites within EDC’s area of planning control will include a set level of affordable housing – details of which are found within the Council’s ‘Core Strategy Development Plan Document’ 1. The relevant policy extract is re-produced below:

CS10 Affordable Housing

2. The range of circumstances in which affordable housing will be required to be provided in private sector developments is as follows:

a) The Council aspires to a target of 30% affordable share of each development above the minimum size threshold of 4 units, but recognises that this may be difficult in a recession. It also notes that the overarching target of at least 50 units per annum might partly be met through contributions lower than 30%. The Council may accordingly require a site based viability assessment to justify variance from that proportion.

1.4 As it is now six years since completion of the DTZ study EDC have

requested that NPS Property Consultants Ltd (‘NPS’) – its valuation agent – provide a professional opinion on whether the assumptions used and conclusions reached in the DTZ study remain appropriate.

1.5 Matt Messenger of NPS’s Kendal Valuation Team, who has been selected

to author this report, is an RICS Registered Valuer currently retained in a specialist planning and development viability advisory role in relation to

________________________________________________________________

1 – for further details see http://www.eden.gov.uk/planning-and-development/eden-local-development-

framework/development-plan-documents/core-strategy-dpd/

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

3

residential development sites for a range of LPA and developer clients across the UK. Tasks carried out for clients include the provision of Financial Viability Assessments (‘FVAs’) and Financial Viability Assessment Checks (’FVAC’) services in relation to individual sites, planning authority-wide ‘viability impact studies’ to inform and test planning policy and expert witness appearances at public inquiries. LPA clients within the local area include Barrow Borough Council, Carlisle City Council, Eden District Council, Lancaster City Council, South Lakeland District Council and Yorkshire Dales National Park Authority.

1.6 For the purposes of this report, ‘viability’ refers to a situation where:

the value of the site with assumed planning consent for the proposed scheme is sufficiently in excess of existing and alternative non-residential use values (if any) that a landowner, when acting reasonably, would be willing to proceed with the proposed residential development

1.7 National Planning Policy Framework (‘NPPF’) 2 paragraph 173 states that: ‘To ensure viability, the costs of any requirements likely to be applied to development, such as requirements for affordable housing, standards, infrastructure contributions or other requirements should, when taking account of the normal cost of development and mitigation, provide competitive returns to a willing land owner and willing developer to enable the development to be deliverable.’

1.8 Recently published Royal Institution of Chartered Surveyors (‘RICS’) guidance 3 (known as the 'RICS Guidance') with which this FVAC accords, has also defined ‘financial viability for planning purposes’ as being: ‘An objective financial viability test of the ability of a development project to meet its costs including the cost of planning obligations, while ensuring an appropriate Site Value for the landowner and a market risk adjusted return to the Applicant delivering the project.’

1.9 Another important source of guidance is Viability Testing in Local Plans – Advice for planning practitioners 4 (known as the 'Harman Guidance'), which states (at page 14) that:

'An individual development can be said to be viable if, after taking account of all costs, including central and local government policy and regulatory

______________________________________________________________________________________ 2 – 'National Planning Policy Framework’ - Department for Communities and Local

Government (ISBN 9781409834137), March 2012 https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/6077/2116950.pdf 3 – Financial Viability in Planning - RICS Guidance Note 1st Edition (GN 94/2012) (RICS,

August 2012): http://www.rics.org/Documents/Financial%20viability%20in%20planning.pdf 4 – Viability Testing in Local Plans – Advice for planning practitioners (LGA/HBF – Sir John

Harman, June 2012): http://www.nhbc.co.uk/NewsandComment/Documents/filedownload,47339,en.pdf

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

4

costs and the cost and availability of development finance, the scheme provides a competitive return to the developer to ensure that development takes place and generates a land value sufficient to persuade the land owner to sell the land for the development proposed. If these conditions are not met, a scheme will not be delivered.'

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

5

Section 2: Method 2.1 In order to provide a professional opinion on whether the assumptions used

and conclusions reached in the DTZ study remain appropriate NPS: (i) Itemised each of the assumptions and variables used in the DTZ 2009

study. (ii) Undertook detailed market research, relevant analysis and testing to

ascertain what the DTZ assumptions and variables would have been if their study had been undertaken in 2015, as opposed to 2009.

(iii) Agreed the updated 2015 assumptions and variables with relevant officers of EDC.

2.2 A summary of NPS’s findings arising from the actions described above (2.1)

and assumptions duly adopted are set out in Appendix 1. An accompanying commentary is provided in Section 3 of this report.

2.3 NPS went on to use the residual valuation (‘RV’) approach – which was also

used in the DTZ 2009 study – to test the effect on viability of the updated 2015 assumptions and variables, across a broad range of development scenarios representative of the type of sites that have and are likely to come forward for development within the District.

2.4 The RV approach is an accepted methodology of site evaluation and one

which is used by housebuilders when they bid for sites. The RICS Guidance 3 also advocates this approach: ‘3.2.1 In assessing the impact of planning obligations on the viability of the development process, it is accepted practice that a residual valuation model is most often used. This approach uses various inputs to establish a (Gross Development Value) GDV from which (Gross Development Cost) GDC is deducted. GDC can include a Site Value as a fixed figure resulting in the developer’s residual profit (return) becoming the output, which is then considered against a benchmark to assess viability. Alternatively, the developer’s return (profit) is an adopted input to GDC, leaving a residual land value as the output from which to benchmark viability, i.e. being greater or less than what would be considered an acceptable Site Value.’

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

6

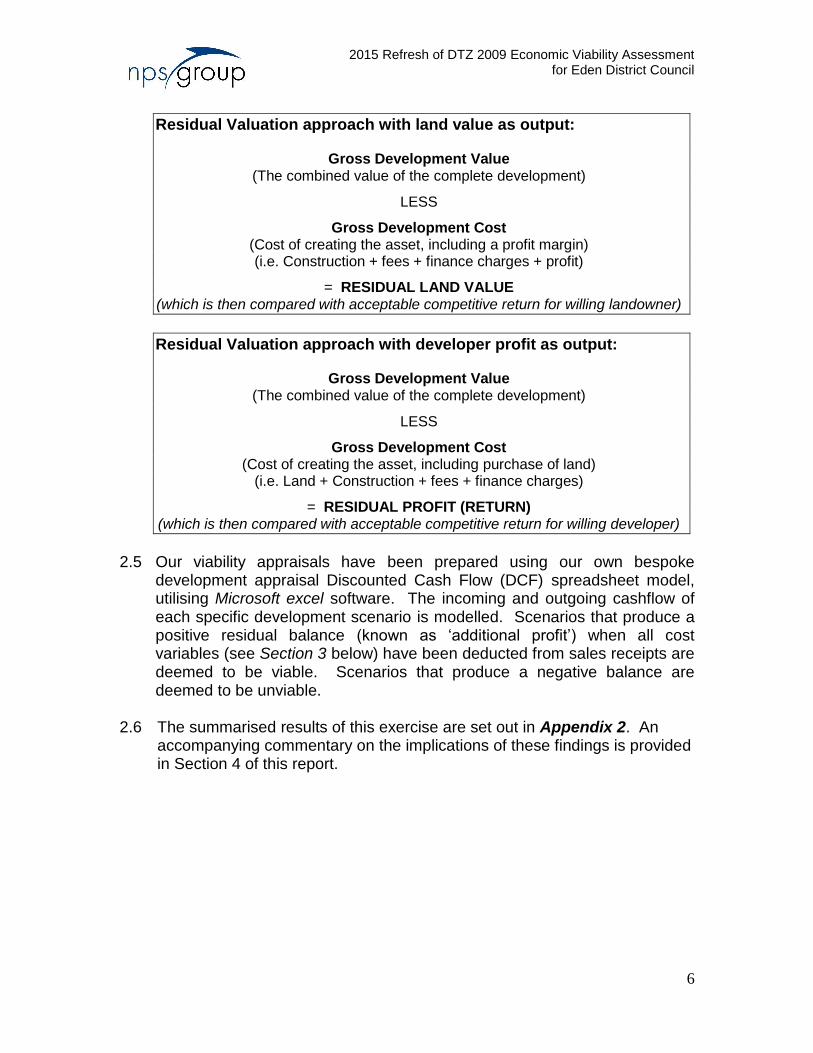

Residual Valuation approach with land value as output:

Gross Development Value (The combined value of the complete development)

LESS

Gross Development Cost (Cost of creating the asset, including a profit margin) (i.e. Construction + fees + finance charges + profit)

= RESIDUAL LAND VALUE (which is then compared with acceptable competitive return for willing landowner)

Residual Valuation approach with developer profit as output:

Gross Development Value (The combined value of the complete development)

LESS

Gross Development Cost (Cost of creating the asset, including purchase of land)

(i.e. Land + Construction + fees + finance charges)

= RESIDUAL PROFIT (RETURN) (which is then compared with acceptable competitive return for willing developer)

2.5 Our viability appraisals have been prepared using our own bespoke

development appraisal Discounted Cash Flow (DCF) spreadsheet model, utilising Microsoft excel software. The incoming and outgoing cashflow of each specific development scenario is modelled. Scenarios that produce a positive residual balance (known as ‘additional profit’) when all cost variables (see Section 3 below) have been deducted from sales receipts are deemed to be viable. Scenarios that produce a negative balance are deemed to be unviable.

2.6 The summarised results of this exercise are set out in Appendix 2. An

accompanying commentary on the implications of these findings is provided in Section 4 of this report.

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

7

Section 3: Commentary on Updated Assumptions

Valuation Date 3.1 It should be stated that NPS’s updated analysis of DTZ’s assumptions was

prepared during the second half of 2015. DTZ’s original work was carried out in June 2009. Data on land values, sales prices and number of other variables are dynamic, always changing and any study can only provide a snapshot of viability. This should remain an important consideration when reviewing the work of DTZ and the subsequent updated assumptions put forward by NPS.

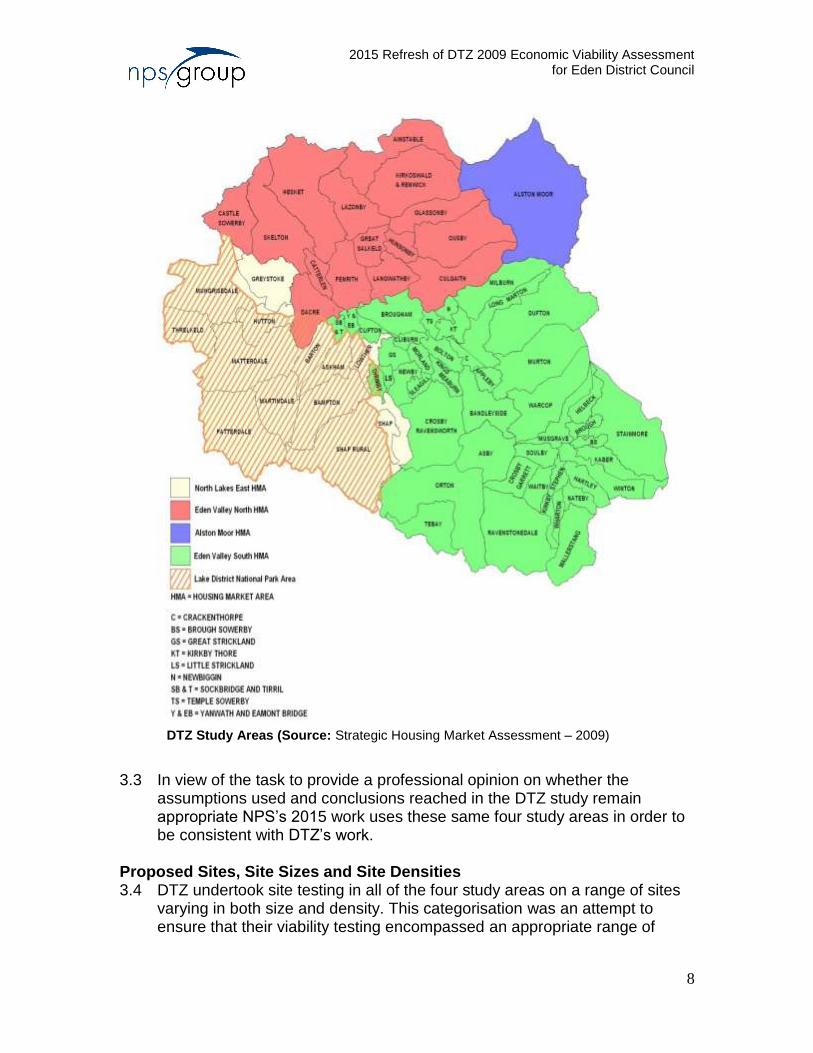

Study Areas 3.2 In order to be consistent with EDC’s Strategic Housing Market Assessment

(SHMA) 2009 DTZ tested sites within the three geographical areas identified in the SHMA, plus Penrith as a separate fourth area for testing purposes due to the anticipated proportion of development within and on the edge of Penrith in the coming years. The SHMA areas are shown on the map overleaf and were: 1. Eden Valley North – including Greystoke 2. Alston Moor 3. Eden Valley South – including Shap and Lowther 4. Penrith

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

8

DTZ Study Areas (Source: Strategic Housing Market Assessment – 2009)

3.3 In view of the task to provide a professional opinion on whether the assumptions used and conclusions reached in the DTZ study remain appropriate NPS’s 2015 work uses these same four study areas in order to be consistent with DTZ’s work.

Proposed Sites, Site Sizes and Site Densities 3.4 DTZ undertook site testing in all of the four study areas on a range of sites

varying in both size and density. This categorisation was an attempt to ensure that their viability testing encompassed an appropriate range of

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

9

sites, in respect of location, site size and development density, likely to come forward during the local plan period.

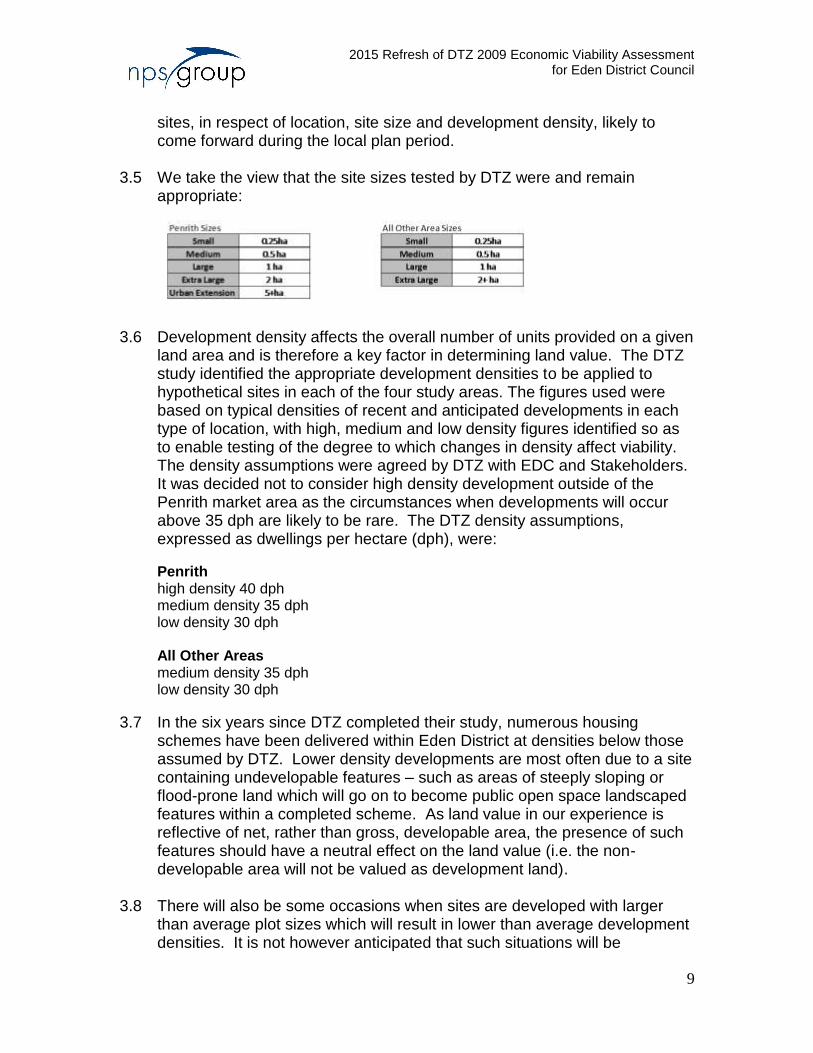

3.5 We take the view that the site sizes tested by DTZ were and remain

appropriate:

3.6 Development density affects the overall number of units provided on a given land area and is therefore a key factor in determining land value. The DTZ study identified the appropriate development densities to be applied to hypothetical sites in each of the four study areas. The figures used were based on typical densities of recent and anticipated developments in each type of location, with high, medium and low density figures identified so as to enable testing of the degree to which changes in density affect viability. The density assumptions were agreed by DTZ with EDC and Stakeholders. It was decided not to consider high density development outside of the Penrith market area as the circumstances when developments will occur above 35 dph are likely to be rare. The DTZ density assumptions, expressed as dwellings per hectare (dph), were:

Penrith high density 40 dph medium density 35 dph low density 30 dph All Other Areas medium density 35 dph low density 30 dph

3.7 In the six years since DTZ completed their study, numerous housing schemes have been delivered within Eden District at densities below those assumed by DTZ. Lower density developments are most often due to a site containing undevelopable features – such as areas of steeply sloping or flood-prone land which will go on to become public open space landscaped features within a completed scheme. As land value in our experience is reflective of net, rather than gross, developable area, the presence of such features should have a neutral effect on the land value (i.e. the non-developable area will not be valued as development land).

3.8 There will also be some occasions when sites are developed with larger

than average plot sizes which will result in lower than average development densities. It is not however anticipated that such situations will be

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

10

widespread – as EDC will always look to maximise the efficient use of development land – and therefore we do not propose to test such a scenario.

3.9 In the context of the above commentary we remain of the view that the

density assumptions adopted by DTZ remain appropriate for the vast majority potential development sites.

3.10 Within each study area DTZ also made unit mix assumptions, as set out below, which in our view remain appropriate:

Planning and Abnormal Costs 3.11 DTZ assumed that all sites have full planning permission, are clear of

contamination and structures and are ready to develop. NPS endorses this approach for a strategic district-wide viability study of this type, which is not designed to test the viability of specific sites. Clearly some sites, particularly those of a brownfield nature, will have an element of abnormal cost. NPS has assumed brownfield land values as being ‘adjusted upwards to absorb any abnormal expenditure into overall purchase expenditure’ (see 3.29 - below) as supported by analysis of relevant transactional evidence. Such studies cannot seek to encompass all the potential differences in individual site circumstances that affect viability. What they can do is adopt realistic assumptions and variables that are likely to be broadly reflective of the majority of anticipated residential development schemes coming forward in the District within the foreseeable future.

Developer Return (Profit) (Competitive return to a willing developer) 3.12 There has been much debate at appeal and through assessment of local

authority policy and guidance documents of what might be considered a competitive developer return. The following points are useful to refer to in this regard: (i) The Planning Advisory Service ‘Viability Handbook and Exercises’

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

11

(para 4.80) 5 (January 2011) advises that: 'Where a positive residual land value is achieved...Typical required

margins, depending on the developer and the risks of the development, are a 20% margin on cost and 17.5% margin on GDV.'

(ii) The accompanying guidance to the HCA’s Development Appraisal tool 6 comments as follows on Developer's Return for Risk and Profit (including developer’s overheads):

Open Market Housing The developer 'profit' (before taxation) on the open market housing as a percentage of the value of the open market housing. A typical figure currently may be in the region of 17.5-20% and overheads being deducted, but this is only a guide as it will depend on the state of the market and the size and complexity of the scheme. Flatted schemes may carry a higher risk due to the high capital employed before income is received.

Affordable Housing The developer 'profit' (before taxation) on the affordable housing as a percentage of the value of the affordable housing (excluding SHG). A typical figure may be in the region of 6% (the profit is less than that for the open market element of the scheme, as risks are reduced), but this is only a guide.

(iii) We acted as expert witness in a key appeal decision in relation to a 148 unit housing site on the urban edge of Kendal in 2013. The following extract, taken from the outline planning application Appeal Decision, (paragraphs 21 and 22) 7, sets out the Inspector’s conclusion as to developer return:

’21. The concept of a ‘competitive return’ is not further defined by the NPPF, and could be the subject of differing interpretations by the parties involved in any particular development. The assessment of a competitive return will involve an element of judgement. Clearly, however, excessively ambitious predictions must be tempered by comparison with industry norms and local circumstances. 22. In this case, it is common ground that a competitive return for the developer can be taken as a profit of 18-20% of the gross development value (‘GDV’)…I see no reason to reach a different conclusion.’

________________________________________________________________ 5– ‘Viability Handbook and Exercises’ (Planning Advisory Service, January 2011):

http://www.pas.gov.uk/c/document_library/get_file?uuid=8ab36aaf-d38e-4d45-a16f-94b9723ee4d8&groupId=332612

6 – Development Appraisal tool (Homes and Communities Agency, November 2014): https://www.gov.uk/government/collections/development-appraisal-tool

7 – Appeal Decision – Land to the west of Oxenholme Road, Kendal (Appeal Ref:

APP/M0933/A/13/2193338) (Decision date: 18 October 2013): http://www.pas.gov.uk/documents/332612/5478199/Oxenholme+Road+appeal+decision/e1c51fb3-6623-44c7-beaa-69fcee73dc04

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

12

3.13 DTZ made the generic assumption in 2009 that developers on sites generating 10 dwellings or less will require a minimum net return of 16% on GDV (net of any finance cost or central overheads) and those developing sites generating more than 10 dwellings will require a net return of 18% on GDV. DTZ reported that Stakeholder Consultation endorsed their view that these were typical minimum rates of return being sought in the market.

3.14 It is important to acknowledge that the returns sought by different

developers and how they secure this through the whole development process, can vary considerably. Developers will take into account a range of factors relating to the risk profile of the scheme, such as scheme size, time of delivery, location and other market factors, in determining what an acceptable rate of return is. Developer’s Return is often the most potentially contentious aspect of any Viability Assessment.

3.15 From experience we are aware that widely differing profit margins will be

expected by different Developers within the Cumbria area. Some smaller developers may be willing to accept profit levels of between 8 and 15% of GDV (net of central overheads) in order to keep their workforce employed. Such smaller developers will generally have low level or no funding requirements and the policies of lenders will have minimal relevance.

3.16 Other Developers have greater profit expectations of anything from 15%

and 20% of GDV. Developers falling into this bracket will generally utilise bank funding facilities and therefore the current risk-averse cautious policies of lenders will have a greater effect. In general terms ongoing reduced sales rates across the UK continue to cause lenders some concern.

3.17 In relation to the current situation in Eden District the NPS view is that whilst

some parties would no doubt make the case for an increase in assumed levels of profit, there is little robust evidence to support the necessity to significantly amend DTZ's 2009 assumptions in this regard. We believe respective minimum returns of 17% of GDV for sites of less than 11 dwellings and 18% for sites of more than ten dwellings to be appropriate. It should be noted that these assumed target rates of return are inclusive of central overhead costs.

Land Value (Competitive return to a willing landowner) 3.18 What can be considered to be a reasonable landowner return will depend

upon the specific circumstances of the case, for example the extent of abnormal costs, and the current and future uses of the land. Clearly if a landowner does not receive what they perceive to be a reasonable return in relation to the sale of their land then it will not be made available for development.

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

13

3.19 There has been much debate at appeal and through assessment of local authority policy and guidance documents of what might be considered a ‘competitive return for a willing landowner’, for example: (i) As set out in RICS Guidance 3 on this issue ‘the issue of site valuation

is not straightforward, but it will be, by definition, at a level at which a landowner would be willing to sell’ (para 3.4.6);

(ii) ‘…the landowner holds the key to any decision as to whether development takes place…unless landowners can be persuaded that it is worth their allowing their site to be (re)developed then they will not make the decision to allow their land to be brought forward and the development land market will not function.’ (PINS Report into Barking and Dagenham EVA, para 4.7).

(iii) 'development proposals will normally need to support land values of £200,000 to £300,000 per net developable acre if the land is to come forward for development.' ('Cumulative impacts of regulations on house builders and landowners', Government Research Paper, section 3 (ii) 8)

3.20 DTZ took the cost of land to be a percentage of Gross Development Value

(GDV) for each of the schemes they tested. NPS's view is that this is a reasonable approach, subject to land value assumptions being formed from a sufficient degree of local market evidence to enable them to be meaningful and reliable. There is however, it seems, some confusion about the land value approach adopted within DTZ's 2009 study – in respect of the distinction between the treatment of greenfield, rural, brownfield and urban sites.

3.21 Appendix 6 of DTZ's study sets out slides used in a presentation to

stakeholder participants on 25 October 2009. General assumptions are set out which include 'Land Values - 5 - 10% GDV - This depends whether it will be greenfield or brownfield'.

3.22 DTZ's report (at 3.32) however states:

'Through market research and stakeholder consultation it was agreed that a value of 10% of GDV in rural areas and 20% of GDV in urban areas should be assumed as a value at which land will be brought forward and developed for residential as opposed to an alternative development use value or maintained as its existing agricultural use in areas outside of Penrith.’

3.23 NPS is not aware of any reasoned justification of evidence for land in urban

areas to command twice as much, as a percentage of GDV, than land in ________________________________________________________________ 8 – 'Cumulative impacts of regulations on house builders and landowners' - Research Paper

(Chris Hill, Turner Morum for Department for Communities and Local Government, commissioned June 2008, published June 2011) (ISBN 9781409829096):

http://webarchive.nationalarchives.gov.uk/20120919132719/http://www.communities.gov.uk/documents/corporate/pdf/1923450.pdf

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

14

rural areas. There is some logic for a distinction in value terms between greenfield and brownfield sites, as most greenfield sites will have a low-value existing agricultural use and many brownfield sites will have an existing higher value commercial use, although conversely brownfield sites are more likely to be affected by ‘abnormal’ costs. It is more difficult to make a case for such a distinction between urban and rural sites. It is clear that the majority of envisaged development in Penrith (and indeed within the District as a whole) will take place immediately outside the current developed area of the town on land currently in agricultural use. NPS would expect the land value of such sites to equate to a similar percentage of GDV as greenfield sites in small towns and large villages within the District.

3.24 This view was also reached in a recent appeal decision 7 relating to a site

on the urban fringe of Kendal in neighbouring South Lakeland, where the DTZ 2009 Eden study was referred to in evidence. The inspector observed that: ‘the study allows a wide disparity between the percentage for urban and rural sites, which seems difficult to justify in the light of high value rural sites…in desirable village(s) close to a main town.’

3.25 Appendix 1 of DTZ's study sets out 'Economic Viability Baseline Assumptions'. Within a table setting out proposed study assumptions the following comments are put forward for land value:

'These figures have been revised upwards following stakeholder consultation. Whilst stakeholders responded providing range of between 10% to 30% of GDV, the upper of these figures reflects the level of land value which would have typically been paid in the height of the market. For rural sites the impact of reality that schemes often provide less than 30 dph drives land value proportion of GDV higher than what would be calculated if schemes comprised 30 dph as a minimum. Likely brownfield sites will provide at least 30 dph hence higher land to GDV ratio is achieved. For both rural and brownfield consideration also given for deferred / staged land payments making the actual land price payable to the land owner less valuable than if payments were made up front.'

3.26 Wherever possible our preference is to undertake HM Land Registry

searches to obtain transactional evidence of relevant sites, leading to compilation of schedules of comparable evidence which can then be analysed to establish patterns of typical land values. When translated into a percentage of GDV (once abnormal costs are disregarded) the prices paid for land will typically fall into the range of 10% to 30% of GDV. As a general rule the percentage of GDV will be at the higher end of this range for smaller sites, where site infrastructure costs will be less (where for example spine roads and sub-stations are not required) and there will be more demand to purchase such sites from smaller developers and builders. Larger sites of 15 or more units will generally fall into the range of 10% to

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

15

20% of GDV. In lower value areas land value as a percentage of GDV will typically be lower than for higher value areas.

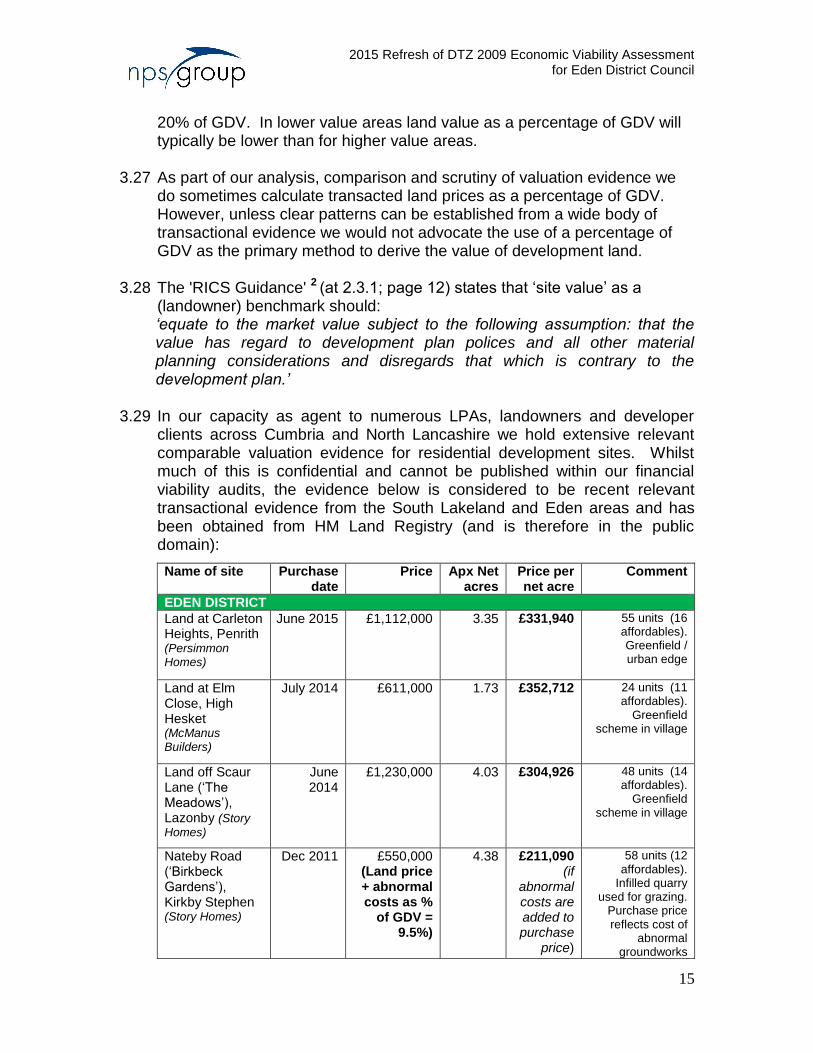

3.27 As part of our analysis, comparison and scrutiny of valuation evidence we

do sometimes calculate transacted land prices as a percentage of GDV. However, unless clear patterns can be established from a wide body of transactional evidence we would not advocate the use of a percentage of GDV as the primary method to derive the value of development land.

3.28 The 'RICS Guidance' 2 (at 2.3.1; page 12) states that ‘site value’ as a

(landowner) benchmark should: ‘equate to the market value subject to the following assumption: that the value has regard to development plan polices and all other material planning considerations and disregards that which is contrary to the development plan.’

3.29 In our capacity as agent to numerous LPAs, landowners and developer

clients across Cumbria and North Lancashire we hold extensive relevant comparable valuation evidence for residential development sites. Whilst much of this is confidential and cannot be published within our financial viability audits, the evidence below is considered to be recent relevant transactional evidence from the South Lakeland and Eden areas and has been obtained from HM Land Registry (and is therefore in the public domain):

Name of site Purchase date

Price Apx Net acres

Price per net acre

Comment

EDEN DISTRICT

Land at Carleton Heights, Penrith (Persimmon Homes)

June 2015 £1,112,000 3.35 £331,940

55 units (16 affordables). Greenfield / urban edge

Land at Elm Close, High Hesket (McManus Builders)

July 2014 £611,000 1.73 £352,712

24 units (11 affordables).

Greenfield scheme in village

Land off Scaur Lane (‘The Meadows’), Lazonby (Story

Homes)

June 2014

£1,230,000 4.03 £304,926

48 units (14 affordables).

Greenfield scheme in village

Nateby Road (‘Birkbeck Gardens’), Kirkby Stephen (Story Homes)

Dec 2011 £550,000 (Land price + abnormal costs as %

of GDV = 9.5%)

4.38 £211,090 (if

abnormal costs are added to purchase

price)

58 units (12 affordables).

Infilled quarry used for grazing.

Purchase price reflects cost of

abnormal groundworks

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

16

Clifton Hill Hotel, Clifton (Story

Homes)

2011 £1,356,000 (Land price + abnormal costs as %

of GDV = 14.6%)

3.96

£342,466 (if

abnormal costs are added to purchase

price)

48 units (6 affordables). Brownfield /

Greenfield site in village involved

redevelopment of former hotel site.

Purchase price reflects cost of

demolition of hotel and abnormal

foundations due to ground conditions

on part of site

SOUTH LAKELAND DISTRICT

Land adj Value View, Pennington, Ulverston (D & E Wood Developments)

Dec 2014 £300,000 0.75 £400,000 5 units (2 affordables).

Windfall / rural in-fill

Vicarage Dr, Kendal (Russell

Armer)

Oct 2014 £380,000 1.01 £383,800 15 units (5 affordables).

Windfall / urban in-fill

Natland Mill Beck Farm, Kendal (Story

Homes)

June 2014

£2,180,000 +

cost of building

farmhouse = say

£2,500,000

7.4 £337,800 76 units (26 affordables). Greenfield / urban edge

Dale Street Infant School, Ulverston

August 2011

£105,000 (Land price + assumed

abnormal costs as %

of GDV = 12.6%)

0.45 £344,444 (if

assumed abnormal costs are added to purchase

price)

8 units (0 affordables). Brownfield – demolition of

former school with replacement by

new build dwellings

Pengarth, Grange over Sands (Russell Armer)

Jan 2011 £620,000 (Land price + assumed

abnormal costs as %

of GDV = 27%)

1.46 £438,356 (if

assumed abnormal costs are added to purchase

price)

5 units (0 affordables). Urban in-fill - demolition of 'gentleman's

residence' with replacement by large new build

dwellings

Biggins Rd, Kirkby Lonsdale (Russell Armer)

Sept 2010 and June

2012

£1,656,860 (Land price

as % of GDV = 19.9%)

2.2 £753,118 34 units (12 affordables). Greenfield / urban edge.

Premium due to proximity to town

centre and location within

high value area.

Note: 1 Acre = 0.404686 hectares

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

17

3.30 We also successfully represented South Lakeland DC as expert witness in a key appeal decision in relation to a site on the urban edge of Kendal in 2013. The following extract, taken from the outline planning application Appeal Decision, (paragraph 51) 7, sets out the Inspector’s conclusion as to land value: ‘…I am unable to conclude that a higher benchmark value than £400,000/net developable acre should be accepted in this appeal. The evidence for the higher figure proposed by the appellants is not conclusive, being based largely on one small comparator site of a different quality and on a relatively broad brush method of checking land value against GDV. Although contested, the LADPD Viability Study suggests that not all owners have expectations in excess of the £400,000 level. The land owner in the present case appears to have started at a higher level, but the appellants themselves have significantly reduced that earlier figure. However, the expectations of one land owner are not critical in the determination of a benchmark level, which relates to the reasonable expectation of a typical owner.’

3.31 In the context of the above evidence, adopted local and national planning policy and our ongoing local knowledge and experience we take the view that a benchmark land value of around £325,000/net developable acre is appropriate for sites in and around Penrith (i.e. Penrith and Eden Valley North and South) at the present time (where sales values for new houses typically range between £1,900 and £2,400 per m2).

3.32 South Lakeland DC has an adopted Core Strategy, which was viability

tested (with evidence prepared by NPS) in 2010, which requires the provision of 35% of the total number of units as affordable units, subject to thresholds of four or ten units depending on where the site is located within the District. As part of the Local Development Framework (LDF) Land Allocations Development Plan Document (DPD) adoption process (2012 to 2013) the viability of the 35% was again examined by PINS and found to be sound. All allocated greenfield development sites (i.e. without site-specific abnormal costs) which have subsequently been the subject of specific planning applications have been able to viably provide the required 35% affordable housing contribution. Conversely, we have observed that the few brownfield development sites which have come forward in South Lakeland in recent years have made affordable housing contributions below the target level of 35% (typically 10% to 25%) as a result of site-specific abnormal costs and the higher existing use value of such sites. Such sites do not make significant contributions to overall new housing numbers.

3.33 Eden DC’s adopted Core Strategy target of 30% affordable housing was

viability tested (see 1.1 to 1.3 above) in 2009. Again, all greenfield development sites without site-specific abnormal costs subsequently granted planning consent have been able to viably make a full policy

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

18

compliant affordable housing contribution. The table below sets out details of such sites:

Name of site Planning reference

Approval date

Total Units

Total Aff’dable Units

Comment

Levens House Farm, Mellbecks, K Stephen

09/0231 07/06/2013 9 3 (33%) Greenfield SHLAA identified site

Eden Gate Farm, Warcop

11/0145 17/06/2013 12 4 (33%) Greenfield SHLAA identified site

Land adj to Castle Park, Brough

14/0305 27/08/2014 25 8 (32%) Greenfield SHLAA identified site

Land at Staynegarth, Stainton, Penrith

14/0528 07/07/2015 30 9 (30%) Greenfield SHLAA identified site

Land at Southend Rd/Castle Hill Rd (‘New Squares’), Penrith

10/0746 21/12/2010 161 48 (30%) Brownfield windfall site forming part of retail led scheme

Land to the east of Townend Croft, Clifton

14/0656 02/04/2015 61 18 (30%) Greenfield SHLAA identified site

Kirkby Thore Hall, Kirkby Thore

10/0170 17/06/2010 17 5 (29%) Greenfield windfall site

High Hesket Farm, High Hesket

14/0028 02/06/2014 17 5 (29%) Greenfield windfall site

Land off Scaur Lane, Lazonby.

13/0241 29/01/2014 48 14 (29%) Greenfield SHLAA identified site

Land off Carleton Meadows, Penrith

13/0654 21/10/2014 55 16 (29%) Greenfield SHLAA identified site

Langwathby Hall Farm, Langwathby

14/0417 08/10/2014 14 4 (29%) Greenfield windfall site

Former Mill Site and Land to North of Burthwaite Road, Calthwaite

12/0979 08/07/2015 14 4 (29%) Greenfield windfall site

Land to the North of Hackthorpe Hall

14/0655 27/03/2015 25 7 (28%) Greenfield SHLAA identified site

Land adj Coopers Close, High Hesket

13/0746 20/12/2013 11 3 (27%) Greenfield windfall site

Site adjacent to Broad Ing Syke Nateby

10/0627 10/09/2010 4 1 (25%) Greenfield windfall site

Road Head Farm, Winskill

11/0374 10/04/2013 12 3 (25%) Greenfield windfall site

Linden House, Temple Sowerby

13/0489 04/04/2014 16 4 (25%) Greenfield SHLAA identified site

Linden House, Temple Sowerby

11/1126 29/10/2012 9 2 (22%) Greenfield SHLAA identified site

Land adj to Prospect House, Kings Meaburn

13/0612 20/11/2013 9 2 (22%) Greenfield SHLAA identified site

White House Farm, Kirkby Stephen

13/0737 11/02/2015 9 2 (22%) Greenfield SHLAA / allocated site

Fell House, Shap 12/0262 20/12/2012 5 1 (20%) Brownfield (conversion of existing bedsits to flats) windfall site

Land adj Holmrooke, Drawbriggs Lane, Appleby

13/0117 20/02/2014 5 1 (20%) Greenfield windfall site

Former Yew Tree Garage, Great Strickland

13/0827 02/06/2014 5 1 (20%) Brownfield (former garage) windfall site

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

19

3.34 There have been two specific cases where planning applicants have unsuccessfully attempted to argue that they could not viably make a full affordable housing contribution on greenfield sites. Our independent scrutiny of submitted site-specific viability evidence in these instances led to the implementation by the applicants of our recommendation that the purchase price should be renegotiated to: ‘equate to the market value subject to the following assumption: that the value has regard to development plan polices and all other material planning considerations and disregards that which is contrary to the development plan.’ (see 3.28 above).

3.35 As set out above (see 3.31), in the context of the above evidence and our

ongoing local knowledge and experience we take the view that a benchmark land value of around £325,000/net developable acre is appropriate for sites in and around Penrith (i.e. Penrith and Eden Valley North and South). For the purposes of the subject ‘Refresh’ exercise we have taken the view that a willing land owner will require a land value of at least 90% of this benchmark figure in order to reach the decision to sell a potential development site (i.e. £292,500/net developable acre or circa £725,000/net developable hectare).

3.36 It should be noted that there is very little recent transactional evidence of

land sales in the Alston area in recent years. The Zoopla house value index data suggests that based on the analysis of second-hand sales data within the different market areas in the District the Alston Moor area would achieve sales values for completed units of approximately 20% below those of the rest of the District (see 3.56). We have therefore assumed for the subject exercise that land values in Alston will be 20% below those in the rest of the District.

Sales Rates 3.37 The DTZ study assumed sales rates of one per month for small sites and

two per month for large sites. Stakeholder consultees were reported in 2009 to be broadly in agreement with this assumption. It could be argued that assumption should now be overly pessimistic, in light of the improvement in economic outlook between 2009 and 2015. However, the emergence of subsequent local evidence is not conclusive. For example the 48 completed units at Story Homes’ Clifton Hill Hotel site sold in just 13 months from March 2013 (a sales rate of 3.7 units per month). Conversely 42 units at Story Homes’ Birkbeck Gardens scheme at Kirkby Stephen sold over a 25 month period from October 2012 (a sales rate of 1.7 units per month). Meanwhile the initial 20 units at Russell Armer’s Cambridge Drive site on the northern edge of Penrith sold over a 17 month period from August 2013 (a sales rate of 1.2 units per month).

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

20

3.38 In the view of the above mixed local evidence we have taken the view to retain the assumptions of two sales per month for large sites used by DTZ in 2009. We have adopted the sale two sales a month assumption also for small sites. This assumption is backed up by representations made by the development industry in South Lakeland (an adjacent district to Eden) during the consultation process relating to the recent South Lakeland DC (SLDC) Viability Study in 2013 which led to a similar agreed assumption of a maximum delivery rate per development site of 20 market units per year.

3.39 We have assumed that any affordable or social rent properties will be

transferred to Registered Provider (‘RPs’) (formerly known as Housing Associations) upon completion of construction (see 3.64 below).

Build Costs 3.40 NPPF Planning Practice Guidance online resource on ‘Viability and decision

taking’ 9 comments on build cost assumptions as follows:

Build costs based on appropriate data, for example that of the Building Cost Information Service;

Abnormal costs, including those associated with treatment for contaminated sites or listed buildings, or historic costs associated with brownfield, phased or complex sites;

Infrastructure costs, which might include roads, sustainable drainage systems, and other green infrastructure, connection to utilities and decentralised energy and provision of social and cultural infrastructure;

3.41 The Harman Guidance 4 (at pages 34-35) provides the following advice:

Build costs

For build costs, these should be based on the BCIS or other appropriate data, adjusted only where there is good evidence for doing so based on specific local conditions and policies including low quantities of data.

Where significant proportions of development are likely to be particularly complex or high density, then adjustments should be made based on specific professional advice.

It is important to understand that BCIS costs do not include external structural and local site works and are based on Gross Internal Area (GIA)...Preliminary costs are included in the BCIS build costs figures so should not be included as a separate cost.

External works, infrastructure and site abnormals These are likely to vary significantly from site to site. The planning

________________________________________________________________ 9 – 'National Planning Policy Framework’ – Planning Practice Guidance ‘Viability and

decision taking’ (reference ID 10-016-20140306), (March 2014): http://planningguidance.planningportal.gov.uk/blog/guidance/viability-guidance/viability-and-

decision-taking/

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

21

authority should include appropriate average levels for each type of site unless more specific information is available. Local developers should provide information to assist in this area where they can, taking into account commercial sensitivity.

3.42 The DTZ 2009 study used build costs taken from Building Cost Information

Service (BCIS) data 10 – re-based using the local index for the Eden area. BCIS data is based on representative cost returns from the construction industry and as such is widely accepted as being appropriate for use in high strategic level AHEVA exercises of this kind. In this instance we have considered BCIS figures for the Eden area at the valuation date (December 2015). Based on our ongoing local experience we have decided to deduct 4% off current published BCIS rates, which at the present time are higher than the schemes in the Cumbria area for which we have recently undertaken site-specific Financial Viability Assessment Reviews (typically at the time of writing featuring basic build costs in the range of £850 to £900 per m2 for new-build housing). Therefore BCIS Median figures at 96% have been used for houses (‘Estate Housing Generally’ – £933 x 96% = £896 per m2) and flats (‘one to two storey – £1,047 x 96% = £1,005 per m2).

3.43 Whilst BCIS costs include all works to the sub-structure and super-

structure, preliminaries and site overheads, all external works within the curtilage of each plot and within the communal areas of the site (such as the installation of utilities, highways infrastructure and site landscaping) are excluded. Many of these items will depend on individual site circumstances and can only properly be estimated following a detailed assessment of each site. Clearly this is not practical within such a high level study. It is however possible to generalise. External costs are typically lower for higher density than for lower density schemes as higher density schemes will have a smaller area of external works, and services can be used more efficiently. Large greenfield sites are more likely to require substantial expenditure on bringing mains services to the site. In the light of these considerations NPS’s updated assumptions use a scale of allowances for the hypothetical residential sites, ranging from 10% of build costs for the smaller sites (0.25 hectares) to 15% for the larger greenfield schemes (of 1 hectare and above).

3.44 In respect of professional fees, we take the view, informed by our ongoing

experience of providing planning viability services to a range of clients and delivering multi-disciplinary property and design services on numerous schemes across the UK, that appropriate assumed rates would be 6% of total build costs for small sites and 7% of total build costs on large sites –

________________________________________________________________ 10 – BCIS is a reference to RICS’s (Royal Institution of Chartered Surveyors) Building Cost

Information Service - the UK property market’s leading provider of construction cost and price information

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

22

which will typically require additional input from specialist consultants.

3.45 A contingency allowance will cover unforeseen costs that arise during a

development project and will typically range between 2% and 5% of total build costs. For previously undeveloped and otherwise straightforward greenfield sites we have assumed a contingency of 2.5%. For previously developed brownfield sites we have assumed a higher figure of 5%.

3.46 The table below compares DTZ 2009 build cost assumptions (including

professional fees and contingency) for houses with those adopted in 2015 by NPS:

DTZ 2009 NPS 2013 Houses (Penrith) £839 per m2 (£78 per ft2)

£1,071 per m2 (£99.5per ft2)*

Houses (outside Penrith)

£893 per m2 (£83 per ft2)

* = Small greenfield sites featuring houses with 2.5% contingency and professional fees at 6%

3.47 It can be seen that there has been a between 20% and 28% increase in

assumed build costs since the 2009 DTZ and 2015 NPS AHEVAs. The increase would be even greater for large sites. While DTZ assumed higher build costs for the area outside Penrith, we have taken the view that the BCIS data has been re-based for the whole of the District, not just Penrith. Most of the key developers currently operating in the Eden are not based in Penrith. Some have their headquarters in Carlisle to the north, others in Kendal to the south, for example. To therefore assume that costs will be markedly lower for Penrith than the rest of the District does not in NPS’s view stand up to scrutiny.

3.48 In was noted above (see 3.41 and 3.42) that BCIS costs exclude all external

works within the curtilage of each plot and within the communal areas of the site (i.e. site infrastructure and landscaping). There is no reference in the text of the DTZ study that gives the impression that external / infrastructure costs have been reflected in their assumed build costs. The allowance of an additional 10% (for smaller sites – 0.25 hectares) to reflect externals / infrastructure costs brings NPS build cost assumptions for houses up to £985 per m2 (£91.5 per ft2). An externals / infrastructure costs 15% allowance (for larger sites – of 1 hectare and above) brings NPS build cost assumptions for houses to £1,030 per m2 (£95.7 per ft2).

Unit Values 3.49 As stated in 3.2 (above) DTZ tested sites within the three geographical

areas identified in the SHMA, plus Penrith as a separate fourth area for testing purposes (Eden Valley North – including Greystoke; Alston Moor; Eden Valley South – including Shap and Lowther; Penrith). For a high level

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

23

study of this type NPS takes the view that relatively large geographic values areas are appropriate.

3.50 The DTZ study states (at 3.29) that 'values, in terms of both sales values of

new homes and land values vary across the study area' and went on to adopt three “value bands” defined as high, medium and low value for each of these four geographic areas.

3.51 It is suspected that DTZ's floor area research may have been skewed by

the inclusion of rural 'period properties' in the areas outside Penrith, which will have larger rooms and of a greater floor area than properties with the same number of bedrooms in a nearby town (i.e. in this case within Penrith).

3.52 NPS's 2015 study update has simplified this approach by calculating an

average value for each of the four geographic areas. We have found in recent years that new housing sales within the three housing market areas of Penrith, Eden Valley North and Eden Valley South have achieved very similar prices when analysed on a £ per floor area basis. For example, prices achieved on the five most recent sold properties at new housing developments in Kirkby Stephen, Clifton (a village around three miles south of Penrith) and on the northern edge of Penrith are set out below:

Address Floor area

(m2)

Date of sale Sale price £ per m2

Average £ per m

2

Birkbeck Gardens, Kirkby Stephen (Story Homes)

36 Birkbeck Gardens 99 26/05/2015 £179,950 £1,818

35 Birkbeck Gardens 116 24/10/2014 £245,520 £2,117

50 Birkbeck Gardens 116 26/09/2014 £232,600 £2,005

38 Birkbeck Gardens 116 12/09/2014 £230,000 £1,983

41 Birkbeck Gardens 123 14/08/2014 £271,551 £2,208 £2,034

Clifton Hill Gardens, Clifton (Story Homes)

24 Clifton Hill Gdns 98 14/01/2014 £192,950 £1,969

47 Clifton Hill Gdns 98 18/12/2013 £195,950 £1,999

26 Clifton Hill Gdns 77 17/12/2013 £166,950 £2,168

19 Clifton Hill Gdns 108 09/12/2013 £243,950 £2,259

25 Clifton Hill Gdns 98 06/12/2013 £195,950 £1,999 £2,079

Cambridge Drive, Penrith (Russell Armer)

2 Cambridge Drive 77 25/09/2015 £167,000 £2,169

17 Cambridge Drive 87 10/04/2015 £167,500 £1,925

12 Cambridge Drive 81 30/01/2015 £165,000 £2,037

18 Cambridge Drive 87 12/12/2014 £169,950 £1,953

19 Cambridge Drive 87 31/10/2014 £169,950 £1,953 £2,003

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

24

3.53 Advertised prices for new houses currently on the market within these three housing market areas are also similar, as illustrated below:

Address Floor area

(m2)

Asking price £ per m2

Birkbeck Gardens, Kirkby Stephen (Story Homes)

19 Birkbeck Gardens 99 £219,000 £2,212

38 Birkbeck Gardens 116 £269,950 £2,327

The Meadows, Lazonby (Story Homes)

Plot 35 – The Durham 124 £273,950 £2,210

Plot 45 – The Balmoral 160 £329,950 £2,059

Carleton Manor Park, Carleton Hill Road, Penrith, (Cumbrian Homes)

The Blenheim 183 £364,000 £1,988

The Blenheim 183 £389,000 £2,125

The Marlborough 188 £372,000 £1,982

The Marlborough 188 £399,000 £2,125

3.54 The zoopla website complies a ‘zed-index’ which is the average property

value in a given area based on current zoopla estimates, which in turn are based on a range of information including sales data, asking prices, regional price trends. Zoopla estimates provide a useful starting point when considering the current price differentials between different areas. The table below shows current ‘zed-index’ figures for each postcode sub-area within Eden District:

Postcode sub-area ‘zed-index’ figure Settlements in area

CA4 £255,248 High Hesket (also includes Cumwhinton etc within Carlisle District)

CA9 £192,161 Alston, Nenthead, Garrigill

CA10 £255,981 Brougham, Clifton, Crosby Ravensworth, Culgaith, Kirkby Thore, Kirkoswald, Langwathby, Lazonby, Morland, Orton, Penrith (Carleton Hall area), Shap, Tebay, Temple Sowerby (also includes Bampton and Pooley Bridge with LDNPA planning control area)

CA11 £238,059 Dacre, Greystoke, Penrith (all except Carleton Hall) (also Glenridding, Matterdale, Mungrisedale, Patterdale with LDNPA planning control area)

CA16 £228,381 Appleby, Bolton, Great Asby, Long Marton, Warcop

CA17 £229,899 Brough, Crosby Garrett, Kirkby Stephen, Mallerstang, Ravenstonedale, Stainmore

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

25

3.55 These findings coincide with the conclusions we reached in 2013 when we undertook an exercise on behalf of EDC to calculate average values for new housing in the District. In 2013 we analysed asking prices and sale values achieved for the period between January 2011 and July 2013 for houses built within the previous twenty years. This exercise encompassed 237 properties in total. Appendix 3 sets out the information that was sourced and analysed as part of this task.

3.56 We have observed that there has been very little new development or re-

sales of recently built houses in Alston in recent years, although the second-hand sales data for comparable properties within the different market areas and the above Zoopla house value index data suggest an assumption that values for new houses in the Alston Moor area would be approximately 20% below those of the rest of the District would be appropriate. As set out above (see 3.36) we have also assumed that land values in the Alston area will be 20% below those in the rest of the District.

3.57 It is noted that DTZ had assumed that houses with the same number of

bedrooms developed in Penrith would be significantly smaller than those developed outside Penrith. NPS's 2013 research and analysis uncovered no evidence that this assumption is correct. DTZ had also assumed, primarily due their differing floor area assumptions, that houses with the same number of bedrooms developed in Penrith would be of a lower value than those developed in other parts of the District (other than Alston Moor). Again NPS's 2013 research and analysis uncovered no evidence to support this assumption. Appendix 4, compares the average sale price and floor areas calculated by NPS in 2013 to those used in the 2009 DTZ study.

3.58 Following our 2013 comprehensive review of the local housing market and

the above more recent sales evidence and asking price data (see 3.52 and 3.53) our professional view of appropriate unit prices and unit sizes to be used in this ‘Refresh’ exercise are set out in Appendix 5.

Housing Mix 3.59 Following stakeholder consultation in 2009 DTZ produced proposed

housing mix assumptions for each of the four ‘study areas’. Assumptions for the three areas outside Penrith were the same. It was assumed that no five bedroomed houses would be developed within Penrith and that developments outside the town would see 10% of the total number of units being of five bedrooms.

3.60 Whilst there is no evidence to support significantly changing the DTZ

proposed housing mix assumptions, NPS note that of 237 new and recently built homes within Eden District for which we analysed sale prices and asking prices in 2013 only one was of five bedrooms. Furthermore two recent significant developments within the District do not feature any five

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

26

bedroomed housing units. Although some developers may choose to include five bedroomed products in future proposals NPS takes the view that on current evidence it is unlikely that 10% of new houses built on sites outside Penrith will be of five bedrooms. This figure is more likely to be between 0% and 5%. Therefore for the purpose of the subject ‘Refresh’ Exercise for all densities tested (30, 35 and 40 units per hectare) we have assumed that the three ‘study areas’ outside Penrith follow DTZ’s Revised Housing Mix Assumptions for Penrith (i.e. 25% of units to be 2 bed houses; 40% of units to be 3 bed houses; 35% of units to be 4 bed houses).

Affordable Assumptions (Intermediate and Affordable Rent Homes) 3.61 The completed DTZ study formed a key part of the Core Strategy

examination evidence base and ultimately led to approval by the Core Strategy Inspector of EDCs affordable housing policy (CS10), which requires that in appropriate and relevant circumstances all new developments of sites within EDC’s area of planning control will include ‘a target of 30% affordable share of each development above the minimum size threshold of 4 units’.

3.62 NPS has been asked to provide a professional opinion on whether the

assumptions used and conclusions reached in the DTZ study remain appropriate. Consequently NPS has assumed 30% affordable housing for all hypothetical sites tested.

3.63 In their 2009 study DTZ assumed that affordable units constructed within

housing developments would be sold to RPs. This remains the usual course of action for such developments within Eden District and NPS has retained this assumption with a default position that affordable units would be split equally between intermediate and affordable rent units. In reality this default position would be subject to site specific variation based on local housing need evidence, but such detail is beyond the scope of a high level strategic study of this kind. Incidentally DTZ’s base assumption had been that 70% of the affordable housing built will be for social renting and 30% will be intermediate tenure, which was reported to be reflective of the average findings of the 2006 Eden Housing Needs Survey. The DTZ study also looked at the impact on viability of changing this proportion to 50% social rented/50% intermediate and 30% social rented /70% intermediate. NPS’s 2015 ‘Refresh’ commission does not extend to such sensitivity testing.

3.64 In 2009 DTZ assumed that intermediate housing units would be sold to

housing associations at 50% of Market Value. EDC’s Strategic Housing Team advise that in 2015 this figure should be uplifted to 60% of Market Value – which reflects the current practice of intermediate housing in the form of ‘discounted sale units’ typically sold directly to a purchaser.

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

27

3.65 In 2009 DTZ assumed that social rent units would be sold to housing associations at 35% of Market Value. By 2015 social rent units have been replaced by affordable rent units (where rent is capped at 80% of market rent). EDC’s Strategic Housing Team advise that affordable rent properties within the District are typically purchased by housing associations at between 45% and 50% of Market Value. NPS has opted for an assumption of 50% of Market Value.

Other Developer Contributions 3.66 Planning policy and statutory consultees will typically seek a range of

‘developer contributions’ from residential developments in addition to affordable housing, through Section 106 and Section 278 Agreements. Other such costs imposed by the public sector on developments, include highway works, provision of community facilities and education payments. These represent an additional development cost imposed on the development and, therefore, need to be taken into account in site-specific and strategic viability testing exercises. At present developments within Eden District are not subject to Community Infrastructure Levy (‘CIL’).

3.67 EDC seeks payments from developers to mitigate the impact of each

development, as appropriate, through improvements to the local infrastructure. In 2013 Cumbria County Council adopted its Planning Obligation Policy setting out in detail the contributions that developers may be asked to provide. NPS are aware that a number of aspects of the Cumbria County Council document (such as education and highways contribution) remain 'under discussion' between relevant stakeholders and are likely to vary in different parts of the District dependent on local circumstances. At this point in time it is difficult to sensibly come up with a 'one size fits all' per unit contribution allowance applicable across the District, or even a specific Housing Market Area within the District. Past trends in neighbouring South Lakeland District show that around £1,500 residential unit is an approximate average amount that has been collected. The future application of the Cumbria County Council Planning Obligation Policy and the 2014 proposed restriction to the ability of local authorities to pool s106 payments is likely to lead to changes to typical levels of s106 contributions across the lives. Against this context NPS takes the view that it would be appropriate to continue with the DTZ approach of testing the viability effect of a range of s106 contributions (£1,000; £2,500; £5,000 and £7,500 per unit). Where appropriate, for some site-type scenarios, we have also tested an additional assumed s106 contribution of £10,000 per unit.

Local Occupancy Housing 3.68 When DTZ undertook its 2009 study EDC anticipated that Local Occupancy

Units would form part of its approved Core Strategy. Consequently DTZ were asked to look at the impact of the Local Occupancy requirement on scheme delivery and its impact on affordable housing viability. Following

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

28

consultation with stakeholders DTZ felt that a figure of 15% reduction in value was appropriate - this incidentally mirrors the result of similar previous consultation and analysis carried out by NPS in South Lakleland. Whist we have not been commissioned to test the viability of local occupancy housing within this ‘Refresh’ exercise we can confirm that in our professional opinion the proposed ‘cascade’ framework set out in Appendix 6 of the emerging Local Plan document (i.e. Policy HS1 – “locality” refers to the parish and surrounding parishes in the first instance, and if after a reasonable period of active marketing an occupier cannot be found the definition would cascade out to include the County. Following a further reasonable period of marketing if no reasonable offers have been received from qualifying potential occupiers the property may be marketed on the open market’ and Policy HS2 -“Locality” refers to the parish and surrounding parishes in the first instance. It will generally be expected that a dwelling is actively marketed for at least 6 months before the definition of locality will be extended to cover Eden District.’) is likely to be acceptable to lenders. We would also expect landowners of affected sites to typically adjust land value expectations to enable the viable development of the limited number of small-scale schemes we would expect to come forward under the relevant proposed policy. It should be recognised that such sites are expected to provide a very small proportion of overall development within the District anticipated within the emerging plan period.

Other Assumptions 3.69 The DTZ 2009 study incorporated a number of other assumptions which

were held as constant for all aspects of the viability testing exercise. NPS has reviewed these and amended as necessary. Details are set out below:

DTZ 2009 Assumed Rate NPS 2015 Assumed Rate

Cost of finance 7.55% per annum 7% per annum

Disposal costs including marketing and sales expenses

3% of gross development value (sales receipts) (for private units only)

2.5% of gross development value (sales receipts) (for all units)

Site acquisition costs (including Stamp Duty)

5.75% of land value Stamp Duty (0 to 5% of land value dependent upon transaction figure) + 1.5% of land value (for legal and acquisition costs)

Section 4: Commentary on 2015 Site Viability Results 4.1 NPS fed the updated 2015 assumptions and variables (as detailed in

Section 2) into a standard development appraisal Discounted Cash Flow (DCF) model – commonplace in the development industry and mirroring the approach used in the DTZ 2009 study – in order to ascertain the viability of

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

29

a range of hypothetical new build development scenarios representative of the type of sites that have and are likely to come forward for development within the District. The results of this exercise are set out in Appendix 2.

4.2 As set out above (3.35 and 3.36), based on current evidence a benchmark

land value of around £325,000/net developable acre is appropriate for sites in Penrith and Eden Valley North and South. We have taken the view that willing land owner will require a land value of at least 90% of this figure to reach decision to sell (i.e. £292,500/net developable acre or circa £725,000/net developable hectare). Land values in Alston Moor have been taken to be 80% of this figure (i.e. £234,000/net developable acre).

4.3 Schemes that produce a positive residual balance when all variables

(including site value / land price) have been deducted from sales receipts are deemed to be viable (see ‘residual’ figures highlighted in green on Appendix 2). Schemes that produce a marginally negative balance are deemed to be potentially viable, subject to some flexibility from all parties (landowner, developer and local authority) (see ‘residual’ figures highlighted in amber on Appendix 2). Schemes that produce a significantly negative balance are deemed to be unviable (see ‘residual’ figures highlighted in deep pink on Appendix 2).

4.4 It can be seen that for the three ‘study areas’, other than Alston Moor,

greenfield sites of low and medium densities with low to moderate ‘developer contribution’ requirements (£1,000, £2,500 and £5,000 per unit) are viable. We have not tested high density sites with these levels of ‘developer contribution’ as all would clearly produce even more favourable residual figures than low and medium density sites, so can be assumed to be viable.

4.5 In these three areas greenfield sites of low and medium densities with

moderate to high ‘developer contribution’ requirements (£7,500 and £5,000 per unit) are viable or marginally viable for small and medium-sized sites (0.25 and 0.5 hectares). For larger sites viability issues are experienced for some scenarios where the ‘developer contribution’ reaches £10,000 per unit.

4.6 In the Alston Moor area, with land and sales values assumed to be 20%

lower, even greenfield sites with the lowest ‘developer contribution’ requirements (£1,000 per unit) are unviable.

4.7 We have not tested brownfield site scenarios within the subject ‘Refresh’

exercise as in our view such schemes will form the minority of sites coming forward for development within the District. Furthermore in our experience with the District and beyond virtually every such site brings with it site-specific abnormal costs which have to be reviewed and have a resultant

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

30

effect of the site value. It is safe to assume that unless such a development scenario can be cross-subsidised by a retail scheme (e.g. Penrith New Squares) then we would not expect to see the provision of the full policy requirement of 30% affordable housing (see Nateby Road and Clifton Hill Hotel sites detailed at 3.29 above).

4.8 It is NPS’s view that the results of the DCF development appraisal site

modelling exercise are a fair reflection of what has actually happened in reality within Eden District over the past four years since the Core Strategy examination (see 3.33 above). Developers are willing to develop greenfield sites with no abnormal constraints with a full quota of 30% affordable housing and landowners are generally willing to sell at a level of price which facilitates such development scenarios to viably proceed.

4.9 This mirrors the situation in South Lakeland, where we are also retained by

the District Council in a planning viability advisory role. Again a number of greenfield sites, with no or minimal abnormal constraints, have been developed or it has been indicated that they can be developed with a full quota of 35% affordable housing (the adopted South Lakeland policy). In both Districts it is envisaged that such unconstrained greenfield, as opposed to brownfield, sites will continue to form the majority of Housing Land Supply in years to come.

4.10 In conclusion this document provides a professional opinion on whether the

assumptions used and conclusions reached in the DTZ 2009 study remain appropriate. NPS has gone on to test the viability of the updated 2015 assumptions and variables across a broad range of development scenarios representative of the type of sites likely to come forward for development within the District. It has been established that unconstrained greenfield sites in all areas other than Alston Moor can in theory potentially be developed viability – as long as developer contributions are kept below £8,000 per unit. As developer contributions are increased above this level the amount of affordable housing that can viability be provided is likely to decrease from the 30% policy target proposed within in policy HS1of the draft Eden Local Plan.

2015 Refresh of DTZ 2009 Economic Viability Assessment for Eden District Council

31

Section 5: Publication and other use 5.1 Neither the whole nor any part of this report or any reference hereto may

be included in any published document, circular or statement, or published in any way without the Valuer’s written approval of the form and context in which it may appear. In any event, such publication of, or reference to, this Report will not be permitted unless it contains a sufficient contemporaneous reference to the departures from the Practice Statements in RICS Valuation - Professional Standards January 2014

5.2 This report is provided for the stated purpose only and for the use of EDC.

It is confidential to the parties concerned and their professional advisers. No responsibility whatsoever is accepted to any other person or organisation and no benefit is conferred or purported to be conferred on any other party.

Signed… Date… 4 April 2016 Matt Messenger MRICS (Registered Valuer) Estates and Valuation Surveyor / Planning Viability Consultant For and on behalf of NPS Group