2015 Issue 4 aktuellThe max Planck society supports selected recipients of the Otto Hahn medal in...

16

MAX PLANCK INSTITUTE FOR TAX LAW AND PUBLIC FINANCE NOVEMBER 2016 ISSUE 05 NEWS LETTER A WARM WELCOME................................................................................. 2 OTTO HAHN GROUP ON FINANCIAL REGULATION................................ 3 THE VULNERABLE TAXPAYER .................................................................. 4 STRESS LOWERS APPETITE FOR RISK ..................................................... 5 EATLP – TAx LAw summiT...................................................................... 6 CURRENT FRONTIERS IN THE THEORY OF CONTESTS ........................... 8 THE PRICE STABILITY TARGET IN THE EUROZONE................................. 9 MISCELLANEOUS ....................................................................................11 SELECTED PUBLICATIONS ......................................................................14

Transcript of 2015 Issue 4 aktuellThe max Planck society supports selected recipients of the Otto Hahn medal in...

M a x P l a n c k I n s t I t u t e f o r t a x l a w a n d P u b l I c f I n a n c e N ov em b er 2016 I s s u e 05

N E W SLETTER

a warm welcome.................................................................................2

ot to hahN group oN fINaNcIal regulatIoN................................3

the vulNerable taxpayer..................................................................4

stress lowers appetIte for rIsk.....................................................5

EATLP – TAx LAw summiT......................................................................6

curreNt froNtIers IN the theory of coNtests...........................8

the prIce stabIlIt y target IN the eurozoNe.................................9

mIscellaNeous....................................................................................11

selected publIcatIoNs......................................................................14

2

a warM welcoMe to.

dr. Mariana lopes da fonsecasenior research fellowdepartment of public economics

raisa sherifphd student

department of public economics

fabian Pagelsphd studentdepartment of business and tax law

Christian Groeneveldphd student

department of business and tax law

Marika Öryphd student

department of business and tax law

alexander wuphd studentdepartment of public economics

Marco serenasenior research fellowdepartment of public economics

carina schwarz

phd student department of business

and tax law

dr. Mariana lopes da fonseca (pictured above) has been awarded the wicksell prize of the European Journal of Political Economy and the European Public Choice society for her paper “Candid Lame Ducks” (2016). Relying on a recent electoral reform in-troducing mayoral term limits at the municipal level in Portugal, she examined how local fiscal policy differs between re-eligible and term-limited incumbents. The results indicate that term limited officeholders pursue more conservative fiscal policies: They choose lower property tax rates and reduced levels of current expenditure relative to re-eligible incumbents. Heterogeneous effects further suggest that ineligible mayors behave more truthfully and do not engage in political business cycles, challenging pre-vious research results in this area.

wIcksell PrIze for loPes da fonseca

3

a warM welcoMe to

OttO hahn GrOup On finanCial reGulatiOn

On January 1, 2016, the Otto Hahn Group on Financial Regulation com-menced its work at the max planck institute for Tax Law and Public Fi-nance. The group currently has eight members: Corinna Coupette, andreas M. fleckner (head), Miguel Gimeno ribes, amin Kachabia, Philipp aron leimbach, Johannes liefke, daniela

pfeuffer, and zoë seiferlein. still closely affiliated with the group is irmela Sennekamp, who has successfully completed her PhD and now serves as an administrative judge in munich.

The Otto Hahn Group focuses on the foundations of financial regulation. As part of their ongoing research projects, group members scrutinise decisions by the German Federal Court of Justice using quantitative and qualitative techniques (Corinna Cou-pette, Andreas m. Fleckner), study the first historical attempts to regulate financial markets (Andreas m. Fleckner, miguel Gimeno Ribes, Philipp Aron Leimbach), and ana-lyse the legal framework of investors’ contributory negligence (Andreas m. Fleckner, Johannes Liefke). Recent publications by group members include: Andreas m. Fleck-ner, Die Börsengeschäftsbedingungen, in: Zeitschrift für das gesamte Handelsrecht und wirtschaftsrecht 180 (2016), pp. 458-521; miguel Gimeno Ribes, Caracterización jurídica de las acciones y de las participaciones. Copropiedad y derechos reales. Nego-cios sobre las propias acciones y participaciones, in: Derecho de sociedades de Capital, madrid: marcial Pons (2016), pp. 151-181; irmela sennekamp, Der Diskurs um die Abgrenzung von Kartell- und Regulierungsrecht, Tübingen: mohr siebeck (2016), xV + 214 pp.

The max Planck society supports selected recipients of the Otto Hahn medal in pursu-ing research abroad and in establishing an Otto Hahn Group upon their return. De-tailed information about the members, projects, and publications of the Otto Hahn Group on Financial Regulation can be found here:

http://www.tax.mpg.de/en/business_and_tax_law/otto_hahn_group.html

4

Taxpayers are vulnerable. states fleece their budg-ets and, by definition, don’t have to provide any-thing specific in return. To make sure that they are not stomped upon, taxpayers must be protected by the Constitution. That’s one argument, mostly advanced by tax law scholars. Taxpayers are suf-ficiently protected by the democratic principle, because parliamentarians, who design the tax law, reflect the will of the population as a whole. One has to be cautious about cutting back the freedom

of the legislator by invoking the Constitution. That’s the other argument, mostly ad-vanced by public law scholars. in a recent article, wolfgang schön, Director of the institute’s Department for Business and Tax Law, argues that tax payers are specifically vulnerable, and require special protection from the democratic tax state.

He states that the main argument that public law scholars bring to the academic debate is based on a counterfactual view of voters and parliamentarians: Law, as schön points out, is not an ideal expression of a volonté générale. According to schön, public eco-nomics has provided substantial evidence for the fact that both electors and the elected parliamentarians, instead of universal interests, pursue their own individual interests. This, according to schön, materialises especially when it comes to tax law. schön argues that tax legislation affects each and every citizen and therefore the “veil of ignorance“ that conceals the direct and personal effects of specific measures and leads to a cer-tain balance, objectivity and neutrality in other legislative processes, is missing when it comes to tax law. Against this backdrop, schön strongly argues for fundamental rights to be invoked to protect the tax payer against the taxing state. He pleads for considering taxation principles as formal constraints to coordinate the conflict between minority and majority in the governmental decision-making process. Furthermore, he consid-ers the consistency principle to be an overarching tax principle that should guide the legislator when designing an equitable taxation regime: it requires the legislator to be consistent and to impose the same rules and measurements to a multitude of causes.

Schön, W.: Grundrechtsschutz gegen den demokratischen Steuerstaat. In: Baer, S. et al. (eds.):

Jahrbuch des Öffentlichen Rechts. Tübingen, Mohr Siebeck, 2016, pp. 515-537.

research.

the vulnerable taxPayer

5

research.

stress lowers aPPetIte for rIsk

Going to a job interview without having thought about your pay expectations? That is not a good idea, especially not, if you are male. You risk ask-ing for too little. The economists Jana Cahlikova and Cingl Lubomir have found that psychosocial stress significantly increases risk-aversion for men when controlling for age and personality traits. The effect of stress on women goes in the same direction but is weaker and insignificant.

many important decisions are made under stress and they often involve risky alterna-tives. whereas there has been ample evidence that stress influences decision mak-ing, less is known about the casual relationship between stress and risk preferences. influential theories in finance, labour economics, the economics of innovation or development economics assume that risk preferences remain stable as a personality trait. Adopting an experimental approach, Cahlikova and Cingl show that this does not apply when people feel stressed. To evaluate the casual effect of psychosocial stress on risk attitudes, the economists randomly exposed participants to a highly efficient laboratory stress-induction procedure, the Trier social stress Test for Groups. Each participant was first asked to perform her best at a fictive job interview and afterwards to serially subtract 17 from a high number – all in front of an evaluation committee. A control group faced cognitively similar tasks but with no stressful aspects present. To evaluate whether people really get stressed or remain calm, the economists measured the level of a stress hormone cortisol, heart rate and the mood. Afterwards the re-searcher elicited the risk-preferences of the stressed participants and compared them to the non-stressed control group using a multiple price list format. The main result of the study, namely that risk-aversion indeed increases under stress, has important consequences: for the proper formulation of economic theories, for the explanation of puzzling economic behaviour of people who have undergone a negative shock, for the formulation of policies addressing poverty, as poverty causes stress, and for creating policy recommendations for times of stress and panic.

Cahlíková, J., Cingl, L.: Risk preferences under acute stress. In: Experimental Economics, 2016,

forthcoming. doi:10.1007/s10683-016-9482-3.

6

the mpI for tax law and Public Finance together with the Ludwig-maximili-ans-university (Lmu) in munich hosted the annual Congress of the European Association of Tax Law professors (eatlp) 2016. more than 200 tax law pro-fessors from 35 countries gathered on June 2–4 2016, to discuss the possibilities

and limitations of the international community in the fight against tax avoidance and aggressive tax planning of multinationals, to exchange ideas and to meet colleagues. The EATLP, a professional organisation of professors teaching tax law at universities in Europe, was founded in 1999 with the aim of contributing to the development of a common approach towards the study of tax issues as well as to the harmonisation of taxes within the European union, and to promote academic teaching and research on international, domestic and comparative taxation at European universities.

Wolfgang Schön, Director at the MPI for Tax Law and Public Finance and co-organiser of the congress, opened the conference in the Bavarian Academy of Sciences in beautiful downtown Munich on June 2.

The General Assembly of the European Association of Tax Law Professors welcomed new members including the first EATLP members from Latvia and from Ukraine.

conference.

eatlp – tax law SuMMit

7

Ricardo García Antón, pictured with Peter Essers from Tilburg University and Adam Zalasinski from the European Commission, was honoured with the European Academic Tax Theses Award (EATTA) 2016, awarded by the EATLP and by the European Commission.

Klaus-Dieter Drüen, hol- der of the Chair of Tax Law at the Ludwig-Maximilans-University in Munich and co-organiser of the congress, welcomed the guests at his home university.

The four Chairmen of the Board of the EATLP since its foundation in 1999 lined up for a group photo (from left to right): Manfred Mössner, Kees van Raad, Bertil Wiman and Wolfgang Schön.

Kees van Raad delivered the renowned Bertil Wiman Lecture. His presentation about the OECD‘s BEPS project was entitled “The OECD Model – Reconsidering the Structure and Operation of its Distributive Rules”.

Enjoying fruitful talks and the beautiful venue: Get-together in the classicistic hall of the Bavarian Academy of Sciences.

conference.

8

Gaining a better understanding of conflicts was the aim of the small but outstanding group of research-ers that gathered in may 2016 at the mpI for tax law and public finance in munich to discuss their latest research on decision making and the theory of contests.

workshoP.

current frontIers In the theory of contests

Sanjeev Goyal from the University of Cambridge is interested in the relationship between conflicts as a central element in human interactions, and economic, social and infrastructure networks. For instance, he studies the design and the defence of networks under threat, motivated by cybersecurity and infrastructure applications.

Robert Powell from UC Berkeley stated that many conflicts at least broadly resemble wars of attrition. In his presentation he elucidated the factors that affect a third party’s decision to take sides in a conflict and discussed how intervention affects the duration and the outcome of the conflict.

Dan Kovenock from Chapman University presented a paper that examines behaviour in a variation of the “Colonel Blotto” game. In Colonel Blotto games two players are asked to simultaneously assign a limited number of resources to several battlefields, without knowledge of their opponent’s strategy. Kovenock investigated the role of the saliency of battlefields in terms of visual cues and values, for deviations from the theoretical prediction.

9

Discussing conflicts constructively, rather than pugnaciously: (left to right) Samuel Häfner from the University of Basel, Christian Ewerhart from the University of Zurich, Robert Powell from UC Berkeley, Sanjeev Goyal from the University of Cambridge, and Brian Roberson from Purdue University.

At the conference “The Price-stability-Target in the Eurozone and the European Debt Crisis”, leading experts from academia and the financial industry as well as policy mak-ers critically discussed the European Central Bank’s unconventional monetary policies and their effects on the Eurozone. The conference was jointly organised on september 28, 2016 by the max Planck institute for Tax Law and Public Finance and the European school of management and Technology EsmT Berlin.

Otmar issing, the former Chief Economist of the ECB and the President of the Center for Financial studies at the Goethe university Frankfurt am main, warned of the great risk of overburdening the ECB with more and more responsibilities, e.g. the supervision of large banks. This may raise high expectations and could create the risk of an operational overburdening. Both of these outcomes pose threats to the credibility of the ECB, the most important asset of a central bank. further-more, the independence of the Central Bank is threatened by its increased power and the

conference.

the priCe Stability tarGet in the eurOzOne and the euroPean debt crIsIs

10

conference.

consequential political pressure on it. Contrary to many other contributions to the conference, Athanasios Orphanides, Professor at the miT sloan school of management and former Gov-ernor of the Central Bank of Cyprus, believes that the unconventional monetary policies of the ECB have not gone far enough. The uncon-ventional “Quantitative Easing“ (QE) was initi-ated too slowly and practiced too hesitantly so that inflation has remained below the ECB’s inflation target of two percent for a long period of time.

Lucrezia Reichlin, Professor at the London Business school, and Charles wyplosz, Pro-fessor at the Graduate institute in Geneva, also see in the QE an important instrument for the stimulation of inflation and economic growth. They argue that alternatives to QE are missing. stefan Homburg, Professor at the Leibniz university Hannover, coun-tered that on the one hand, the QE has not shown the hoped for effects, as infla-

tion is still very low, and on the other hand, QE entails tremendous risks and side effects. Particularly, whether the ECB can manage the necessary exit out of the QE in the event of a sudden increase in inflation remains open. Questions of how deeply the QE distorts the incentives for the necessary structural reforms in crisis countries and whether QE and low interest rates can actually stimulate economic (front row, left to right) Jörg Rocholl from

the ESMT and Kai A. Konrad from the MPI for Tax Law and Public Finance, organisors of the conference.

growth, as crisis countries may face a lack of demand for loans as a result of structural problems, were likewise valued differently.

Felix Hufeld, President of the Federal institute for Financial services (BaFin), and Dieter wemmer, Chief Financial Officer of the Allianz sE, discussed the consequences and risks that emanate from the low interest rate policy of the ECB for the insurance and bank sector. According to them, if interest rates remain low permanently, this will most probably lead to a consolidation in the bank and insurance sector.

11

Two research papers of the institute are among the top 10 of the world’s most down-loaded tax papers in 2015 on the social science Research Network (ssRN). Paul Caron, owner and publisher of the Law Professor Blogs network, reports that the most down-loaded tax paper on ssRN in 2015 is “some Reflections on the OECD and the sources on international Tax Principles” by Hugh J. Ault. The article originates in a lecture given by Prof. Hugh J. Ault on may 2, 2013 at the mPi for Tax Law and Public Finance. Hugh J. Ault, professor emeritus of law at the Boston College Law school and a former senior adviser with the OECD Centre for Tax Policy and Administration, held his lecture during a research visit at the institute. The revised text of the lecture was published in Tax Notes international 70/12. with 4620 downloads on ssRN it became the most successful tax law paper in 2015. The article “Taxing multinationals in Europe” by Prof. dr. h. c. wolfgang schön, Director of the Department of Business and Tax Law, holds seventh place in the ssRN ranking of the most downloaded tax papers in 2015.

the Most downloaded tax law PaPers

Prof. dr. dr. h. c. wolfgang schön, Direc-tor at the max Planck institute for Tax Law and Public Finance, has been honoured with the Ibfd frans vanistendael award for international Tax Law. The prize was awarded for his publication “Neutrality and Territoriality – Competing or Converg-ing Concepts in European Tax Law?”, pub-lished in iBFD’s Bulletin for international

Taxation, 2015, Volume 69, No. 4/5. “The winning publication was chosen, based on its originality, lasting impact, innovative content and outstanding research, by an inter-national jury chaired by iBFD’s Academic Chairman, Prof. Dr. Pasquale Pistone,” states the organisation’s press release. The iBFD introduced the Frans Vanistendael Award in 2015 to promote outstanding scientific research on international tax law. it is named after its previous Academic Chairman, Prof. Dr. Frans Vanistendael. The international Bureau of Fiscal Documentation (iBFD) is an independent, non-profit foundation with the goal to promote and disseminate the understanding of cross-border taxation.

MIscellaneous.

frans vanIstendael award

12

Prof. dr. kai a. konrad, Director of the department of public economics at the institute is this year’s recipient of the Richard musgrave Visiting Pro-fessorship. As part of the award, Kai a. konrad delivered the 8th richard musgrave Lecture at the Ludwig-max-imilians-university in munich in April 2016. The lecture addressed key issues of why and when alliances form, how

cooperation in alliances emerges in the shadow of conflict, and what happens once members of an alliance have achieved their common goals. The Richard musgrave Visiting Professorship – awarded by the CEsifo-Group and the international institute of Public Finance (iiPF) – honours an outstanding scholar in the area of Public Finance annually. with this award the prize winner is also named a Distinguished CEsifo Fellow.

In June 2016 Prof. dr. kai a. konrad delivered a keynote lecture on the strategic aspects of alliance forma-tion at the 15th Journées Louis-André-Gérard-Varet. The conference is considered to be one of, if not the, most important annual conferences in public economics in Europe. According to the organisers, it aims to promote and diffuse high-quality research, with a special emphasis on articles that shed light on “real world” public decision-making. Alongside Kai A. Konrad, keynote speakers at the Journées Louis-André Gérard-Varet included Kaushik Basu, Chief Economist and senior Vice President of the world Bank, François Bourguignon, Emeritus Professor of Economics at the Paris school of Economics, and Pierre-André Chiappori, Professor of Economics at Columbia university. The latter, after entering the stage as a keynote speaker, performed as a pianist.

MIscellaneous.

riChard MuSGrave prOfeSSOrShip

kaI a. konrad delIvers keynote lecture

13

MIscellaneous.

diStinGuiShed prOfeSSOrShip at eSMt

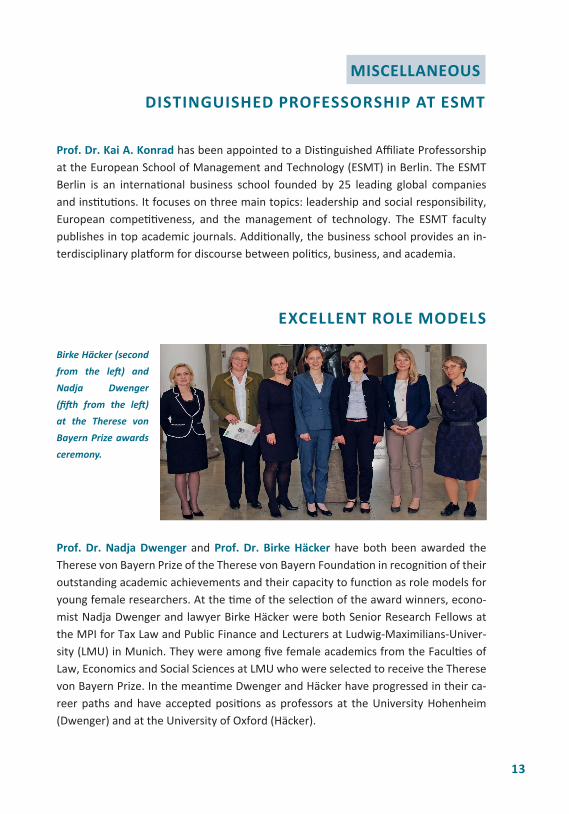

Prof. dr. nadja dwenger and Prof. dr. birke häcker have both been awarded the Therese von Bayern Prize of the Therese von Bayern Foundation in recognition of their outstanding academic achievements and their capacity to function as role models for young female researchers. At the time of the selection of the award winners, econo-mist Nadja Dwenger and lawyer Birke Häcker were both senior Research Fellows at the mPi for Tax Law and Public Finance and Lecturers at Ludwig-maximilians-univer-sity (Lmu) in munich. They were among five female academics from the Faculties of Law, Economics and social sciences at Lmu who were selected to receive the Therese von Bayern Prize. in the meantime Dwenger and Häcker have progressed in their ca-reer paths and have accepted positions as professors at the university Hohenheim (Dwenger) and at the university of Oxford (Häcker).

Birke Häcker (second from the left) and Nadja Dwenger (fifth from the left) at the Therese von Bayern Prize awards ceremony.

Prof. dr. kai a. konrad has been appointed to a Distinguished Affiliate Professorship at the European school of management and Technology (EsmT) in Berlin. The EsmT Berlin is an international business school founded by 25 leading global companies and institutions. it focuses on three main topics: leadership and social responsibility, European competitiveness, and the management of technology. The EsmT faculty publishes in top academic journals. Additionally, the business school provides an in-terdisciplinary platform for discourse between politics, business, and academia.

excellent role Models

14

Coordination and the fight against tax havenskai a. konrad and tim b.M. Stolper Journal of international economics, 2016, no. 103, pp. 96-107.

why would a country ever comply with international standards of transparency de-spite the sizeable returns in the tax haven business? in a recent publication, Kai A. Konrad and Tim stolper highlight fundamental coordination problems in the fight against tax havens and what this implies for whether the fight will be successful or not. A country’s decision as to whether or not to operate as a tax haven depends on the decisions of many single investors. Each investor’s decision, however, depends on the anticipated decision of the haven country and the decisions of the other inves-tors. The haven country will trade-off costs—e.g. arising from international political pressure—and benefits such as financial sector profits, which create tax revenues, jobs and other economic spillovers and are proportional to the amount of capital at-tracted by being a tax haven. Each individual investor, when deciding whether or not to use this haven country to conceal capital and evade taxation, assesses how likely it is that the country will provide a secrecy regime, which also depends on how many other investors deposit their capital there. This feedback loop creates a coordination problem among many players. A coordination failure can induce compliance, although the costs from international pressure may not exceed the potential gains from the tax haven business. The analysis offers a possible explanation for recent concessions by some haven countries as well as the large profits for those countries that persist as tax havens. Furthermore, it connects previously unrelated policy issues – the fight against tax havens and the level of taxation as well as the degree of punishment for revealed tax evaders.

selected PublIcatIons.

häcker, b. Divergence and Convergence in the Common Law – Lessons from the Ius Commune. Law Quarterly Review (LQR), 2015, Volume 131, pp. 424-453.

Konrad, K. a., Morath, f. Bargaining with incomplete information: Evolutionary stabil-ity in finite populations. Journal of mathematical Economics , 2016, 65(C), pp. 118 -131.

15

Market infrastructure regulation and the financial transaction tax

caroline heber and Christian Sternbergworld tax Journal, 2016, volume 8, no 1, pp. 3-35.

Based on the fragility of the European financial markets highlighted by the last financial crisis, the European union is pushing for reforms of the existing regulatory framework and has also proposed a financial transaction tax. until now, the European union has already adopted a Regulation on short selling and certain aspects of credit default swaps and a European market infrastructure Regulation aiming at regulating over-the-counter derivatives markets. The Directive on markets in Financial instruments was subject to major reforms and Regulations on markets in Financial

instruments and on Central securities Depositories were enacted. This strand of finan-cial market regulation shall be complemented by a Financial Transaction Tax pushed forward through the enhanced cooperation mechanism. in “market infrastructure Regulation and the Financial Transaction Tax” Caroline Heber and Christian sternberg analyse the interplay between the financial market regulation and the proposed fi-nancial transaction tax. The authors conclude that both ways of regulating financial markets are not sufficiently coordinated.

IMPrInt Publisher: max Planck institute for Tax Law and Public Finance

Prof. Dr. Kai A. Konrad and Prof. Dr. Dr. h. c. wolfgang schön

marstallplatz 1, 80539 munich, Germany

website: www.tax.mpg.de

Editor / Layout: Christa manta

Photo Credits: istockphoto (p. 3,4,5), mPi (2,6,7,8,9), Bettina Ausserhofer (p. 9, 10), iBFD (11),

CEsifo (p. 12), Journées Louis-André-Gérard-Varet (p. 12), Lmu (p. 13).

Contributors and proof-readers: Andreas m. Fleckner, Caroline Heber, Adelphia Nierhoff-King,

Harald Lang, Christa manta, Erik Röder, Jenny Rontganger, sven Arne simon, Christian stern-

berg, Tim stolper, Anna wilson.

Email: [email protected]

Print: Flyeralarm GmbH, issN: 2192-3108

16

interested in more scientific research results?

read the discussion papers of the research fellows of the max Planck institute for Tax Law and Public Finance on:

http://www.ssrn.com/link/tax-MpG-reS.html

Steuerliche bedingungen von Kapitalbildung und Kapitalbeschaffungerik röderSieker, S. (ed.): Steuerrecht und wirtschaftspolitik (dStJG vol. 39), Köln (ottoschmidt), 2016, pp. 307-360.

The way in which capital is taxed influences business financing decisions. whether a company funds a new project out of re-tained profits or whether it raises external equity or debt capital, is in turn relevant for its economic performance. so, for instance, the traditional debt bias of corporate income tax systems has been blamed for deepening the global financial crisis by render-ing companies more vulnerable to economic shocks. in his arti-cle, Röder first observes that Germany does not have a coherent tax policy in place when it comes to the taxation of income from

capital. in the context of the last major overhaul of business taxation in 2008, the draftsmen paid lip-service to neutrality, but the reform left the tax system heavily til- ted in favour of debt. it is not evident, which ideal tax policy should pursue. main-stream public finance literature still suggests that the normal return on capital should not be taxed at all, but this policy recommendation has become more contested in recent years. if income from capital is taxed, there is a strong case for neutrality and against favouring one source of capital over the other. Finally, the article examines different options for reforming the taxation of income from capital, including inno-vative concepts such as a comprehensive business income tax and an allowance for corporate equity, and arrives at the conclusion that a dual income tax would be the best way to reduce distortions without causing major disruptions to the tax system.

This newsletter is a free service. To subscribe or unsubscribe, or if you would like to receive the electronic version write an email to [email protected].