2015 full year China media scene

130

-

Upload

zenithoptimediachina -

Category

Business

-

view

4.375 -

download

1

Transcript of 2015 full year China media scene

CHINA ECONOMIC OVERVIEW

CHINA GDP AND GDP PER CAPITA

China’s GDP growth continues to slow to 6.9% - the lowest since 1990

Source: National Bureau of Statistics – Jan 2016

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

0%

5%

10%

15%

20%

25%GDP PER CAPITA (USD)

Source: National Bureau of Statistics

RMB 49,228 (USD $7,581)2014 GDP Per Capita - China

+4%YOY

VS

CHINA'S GDP GROWTH YEAR-ON-YEAR

8.1%

7.6%7.4%

7.9%7.7%

7.5%

7.8%7.7%

7.4%7.5%7.4%7.3%

5.8%7.0%6.9%6.8%

5.00%

5.50%

6.00%

6.50%

7.00%

7.50%

8.00%

8.50%

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4

2015 GDP Growth: 6.9% YOY

2

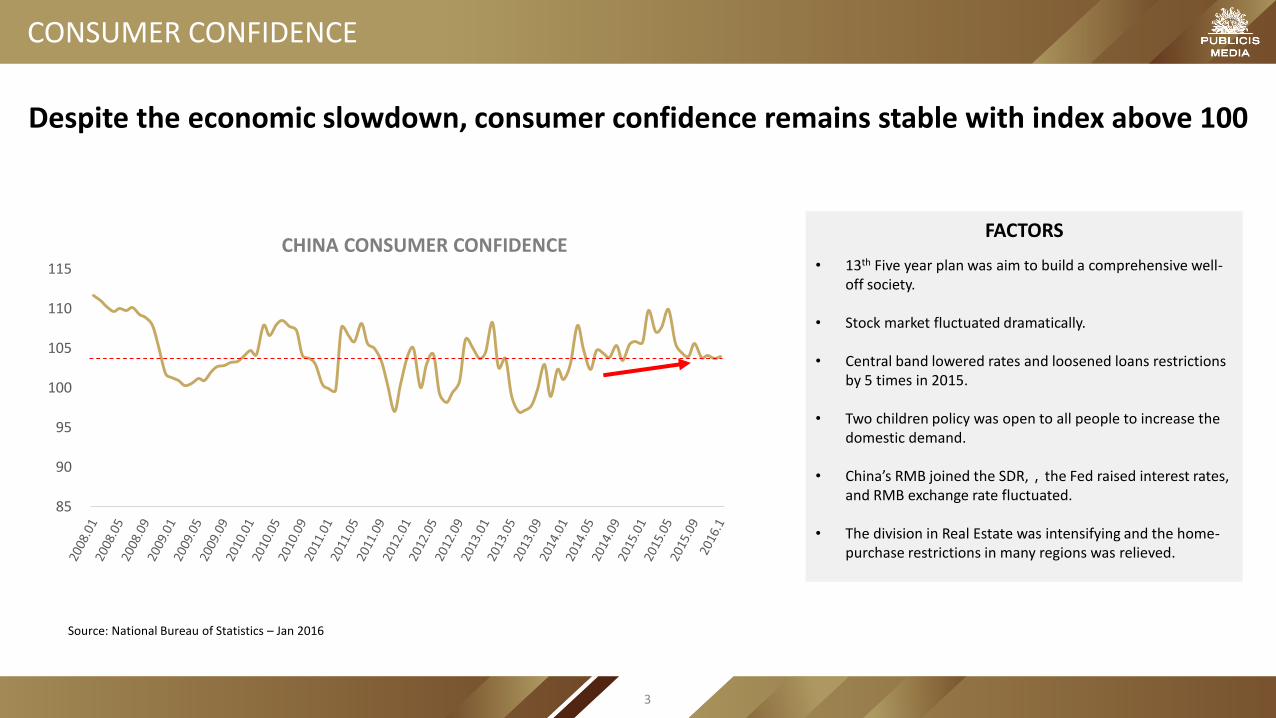

CONSUMER CONFIDENCE

Despite the economic slowdown, consumer confidence remains stable with index above 100

FACTORS

• 13th Five year plan was aim to build a comprehensive well-off society.

• Stock market fluctuated dramatically.

• Central band lowered rates and loosened loans restrictions by 5 times in 2015.

• Two children policy was open to all people to increase the domestic demand.

• China’s RMB joined the SDR,,the Fed raised interest rates, and RMB exchange rate fluctuated.

• The division in Real Estate was intensifying and the home-purchase restrictions in many regions was relieved.

CHINA CONSUMER CONFIDENCE

85

90

95

100

105

110

115

Source: National Bureau of Statistics – Jan 2016

3

CHINA ADVERTISING OVERVIEW

CHINA AD EXPENDITURE FORECAST

9.3%

26.9%

17.7%

12.6% 13.4%

10.5%8.7% 8.0% 7.5% 7.0%

0%

5%

10%

15%

20%

25%

30%

0

100,000

200,000

300,000

400,000

500,000

600,000

2009 2010 2011 2012 2013 2014 2015 2016e 2017e 2018e

Total YOY Growth

TOTAL AD INVESTMENT (2015): RMB 456 BILLION

RMB: Million

Advertising investment growth continues to slow down

Source: ZenithOptimedia Adforecast

5

MONITORED SPENDING BY INDUSTRY

0%

39%

-15%

17% 15%

50%

229%

121%

67%50%

88%

10% 13%

96% 93% 82%

-50%

0%

50%

100%

150%

200%

250%

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2014 2015 YOYRMB: Million

TOTAL MONITORED AD INVESTMENT BY SECTORS (2014 & 2015)

Food & drink still dominant category; Pharmaceuticals with significant growth taking second position while Toiletries drops into third

Media: Exclude all no-cost items & Hong Kong Media

Source: CTR AdEx Power 2015; iResearch 2015

6

CHINA AD EXPENDITURE BY MEDIA

21%

-2%

5%

-24%

2%

-14%

25%

-30%

-20%

-10%

0%

10%

20%

30%

-

50,000

100,000

150,000

200,000

250,000

300,000

Internet TV Outdoor Newspaper Radio Magazine Cinema

CHINA AD EXPENDITURE BY MEDIA (2015-2016)

2015 2016 yoy

RMB: Million

Source: ZenithOptimedia Adforecast

Internet expected to take up 50% of total ad expenditure with 21% increase in 2016

7

OVERALL MEDIA LANDSCAPE

18% 18%

72%

55%

31%27%

95% 96%

61%

74%

24%

64%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015

MEDIA PENETRATION 2012-2015

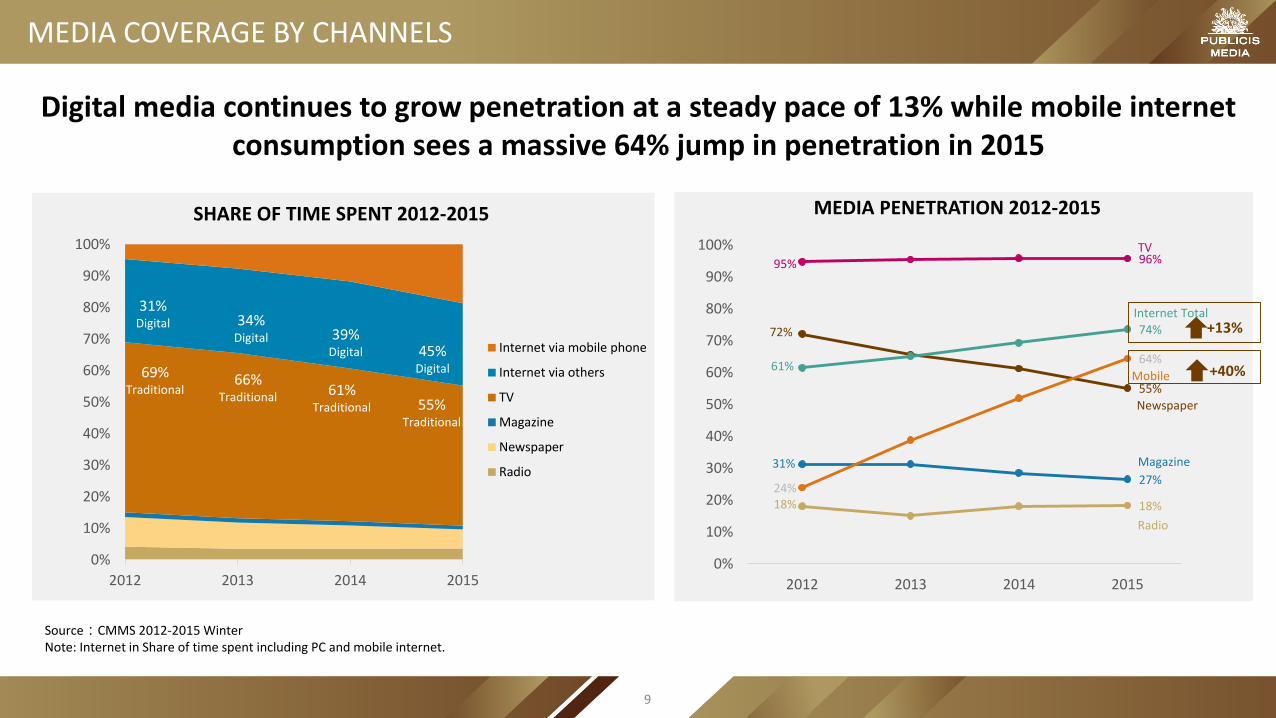

MEDIA COVERAGE BY CHANNELS

TV

Internet Total

Newspaper

Mobile

Magazine

Radio

+13%

+40%

Digital media continues to grow penetration at a steady pace of 13% while mobile internet consumption sees a massive 64% jump in penetration in 2015

Source:CMMS 2012-2015 WinterNote: Internet in Share of time spent including PC and mobile internet.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015

SHARE OF TIME SPENT 2012-2015

Internet via mobile phone

Internet via others

TV

Magazine

Newspaper

Radio

31%Digital

69%Traditional

34%Digital 39%

Digital

61%Traditional

66%Traditional

45%Digital

55%Traditional

9

0.3 0.2 0.3 0.2 0.2 0.1 0.1 0.2 0.2 0.2 0.2 0.2

0.6 0.5 0.5 0.4 0.4 0.4 0.4 0.3 0.5 0.4 0.3 0.3

0.10.1 0.1 0.1 0.0 0.0 0.0 0.0

0.1 0.1 0.1 0.1

3.13.0 2.9

2.7 2.82.5 2.4 2.4

2.52.3 2.2 2.0

1.81.8 2.0

1.91.2

1.21.3 1.2

1.11.1 1.1

0.9

0.20.3

0.61.0

0.10.3 0.5 1.0 0.4

0.5 0.71.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2012 2013Tier1

2014 2015 2012 2013Tier2

2014 2015 2012 2013Tier3

2014 2015

TIME SPENT ON MEDIA PER DAY, BY CITY TIER 2012-2015

Internet via mobile phones

Internet via others

TV

Magazine

Newspaper

Radio

CROSS TIERS MEDIA CONSUMPTION

Source:CMMS 2012-2015Winter

Tier 1 market continues to consume more media overall but digital consumption increases across all tiers

33%Digital 37%

Digital

41%Digital

29%Digital

32%Digital

42%Digital 32%

Digital 35%Digital

43%Digital

46%Digital

38%Digital 39%

Digital

10

2.4

1.81.9

2.0 2.1 2.2

2.9

1.3

1.3

1.71.8

1.8 1.60.8

1.0

1.2

1.51.5 1.3 1.2

0.4

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

all 15-19 20-24 25-29 30-34 35-39 40+

TIME SPENT ON MEDIA PER DAY, BY AGE GROUP 2015

Mobile Internet via mobile phone

Internet via others

TV

Magazine

Newspaper

Radio

MEDIA CONSUMPTION BY AGE

Young people continue to drive heavy digital consumption, in contrast to 40+ age group

Source:CMMS 2015Winter

54%Digital

58%Digital

57%Digital

53%Digital

50%Digital

25%Digital

44%Digital

11

CHINA DIGITAL LANDSCAPE

TOTAL POPULATION

28.4%71.6% OF NETIZENS

URBAN RURAL

INTERNET PENETRATION6% YOY

50% OF TOTAL POPULATION688,000,000NETIZENS

620,000,000 90% OF NETIZENS

MOBILE WEBMOBILE NETIZENS 11% YOY

Half the population has internet access with higher growth in mobile netizens of 11%

Sources: National Bureau of Statistics of China 2015; CNNIC Jan 2016

DIGITAL LANDSCAPE

1,374,620,000

13

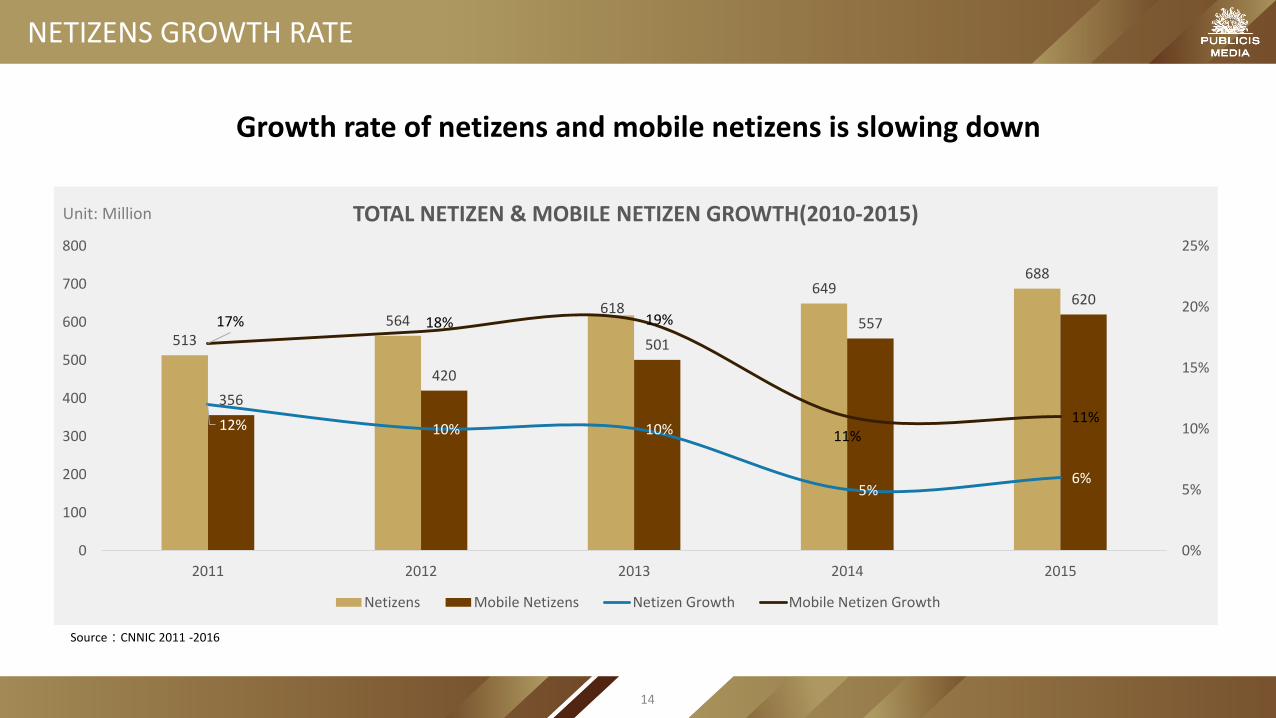

NETIZENS GROWTH RATE

Growth rate of netizens and mobile netizens is slowing down

Source:CNNIC 2011 -2016

513564

618649

688

356

420

501

557

620

12% 10% 10%

5%6%

17% 18% 19%

11%11%

0%

5%

10%

15%

20%

25%

0

100

200

300

400

500

600

700

800

2011 2012 2013 2014 2015

TOTAL NETIZEN & MOBILE NETIZEN GROWTH(2010-2015)

Netizens Mobile Netizens Netizen Growth Mobile Netizen Growth

Unit: Million

14

34% 37%

19% 17%

11% 13%

6% 5%5% 5%5% 5%5% 1%

9% 12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014.12 2015.12

SHARE OF TIME SPENT

Video IM Game Social

Search E-comment Finance News

Entertainment Others

MEDIA CONSUMPTION ON PC

User behavior remained relatively unchanged for most categories with exception of BBS

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

0

100,000

200,000

300,000

400,000

500,000

600,000

MONTHLY COVERAGE BY CATEGORY

Dec-14 Dec-15 YOY Growth

-2%

3%

Source:iUserTracker Dec 2014&2015

(‘000)

2%

15

MEDIA CONSUMPTION ON MOBILE

IM is the most used on mobile and still growing. Travel experienced massive growth in 2015

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

MONTHLY COVERAGE BY CATEGORY

Jan-2015 Dec-2015 Growth(Dec/Jan)

26% 29%

20%24%

5%

7%8%

6%5%

6%5%

4%3%

4%3%

3%

23%15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan 2016 Dec 2015

SHARE OF TIME SPEND

IM Online Video Search

Game Browser Social

News&Information E-reading Online Shopping

Others

3%

Source:mUserTracker Jan& Dec 2015,Note: not compare with Jan 2014 due to huge gap after panel change), search combine both APP and site.

(‘000)

4%

2%

16

33.0% 31.4% 34.1% 33.8% 33.5% 33.2% 33.1%

23.3% 27.1% 26.0% 28.2% 28.6% 29.6% 30.0%

26.2% 21.1% 17.8% 15.3% 14.7% 13.4% 12.2%

6.2%7.2% 8.0% 8.2% 8.4% 8.6% 8.7%

11.3% 13.2% 14.1% 14.5% 14.8% 15.2% 16.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016e 2017e 2018e

SHARE OF DIGITAL AD SPENDING IN CHINA BY FORMAT

Search EC ads Display Pre-roll Others

DIGITAL AD SPENDING BY FORMAT

Source: iResearch Report, March 2016

Notes: “Others” include rich media, text link, classifieds, email etc.

Digital ad investment is shifting from display banners to pre-roll and EC ads

17

INTRODUCTION TO VR MARKET AND ITS APPLICATION

450 1,350 3,150

6,300

10,980

16,830

30 75

255

1,035

3,405

8,505

-

5,000

10,000

15,000

20,000

25,000

30,000

2015e 2016e 2017e 2018e 2019e 2020e

2015-2020 Number Of Chinese VR Users

PC VR or VR Gear users(,000) Mobile VR users(,000)

VR experienced huge growth since the end of 2015 with many applications in development

VR EntertainmentVR MovieVR Game

VR TravelVR EducationVR Social

VR TrainingVR TransactionVR Live

Source:iResearch Report, March, 2016.

18

MOBILE

REACH BY DEVICE

Source:CNNIC Jan, 2010 – Jan 2016

Mobile reach now overtakes PC & laptop which have both witnessed a decline since Jan 2015

83%80% 82%

79% 78%

71%71% 70% 70% 70% 71%

68%

68%

35%40%

50% 49% 49%45% 46% 47%

44% 44% 43% 43%39%

69%72% 72% 70% 73%

72%74%

79% 81% 83%86%

89% 90%

35% 34% 32%

16% 16% 18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

INTERNET PENETRATION BY DEVICE

PC Laptop Mobile Tablet TV

20

TIME SPENT ON MOBILE PHONE VS. OTHER DIGITAL

Source:CMMS Winter, 2015

Mobile phones taking up 43% of digital consumption among all people. Teens and college-age users are the heaviest mobile consumers.

1.3 1.3 1.7 1.8 1.8 1.6

0.8

1.0 1.2

1.5 1.5 1.3

1.2

0.4

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Total Population 15-19 20-24 25-29 30-34 35-39 40+

TIME SPENT ON MOBILE INTERNET VS. DESKTOP INTERNET

Internet via others Internet via mobile phone

43% mobile phone

48% mobile phone

46% mobile phone

45% mobile phone 43%

mobile phone 42% mobile phone

37% mobile phone

Unit: Hour

21

SMARTPHONE OS

27.1%

71.4%

1.2% 0.0% 0.2%

2015 DEC. SMARTPHONE SALES

iPhone Android Windows Blackberry Others

Source:Kantar Worldpanel Dec, 2015

MEDIAN HOUSEHOLD INCOME BY OPERATING SYSTEM

Source:CMMS Winter, 2015

IOS continues to expand its market share in China, driven by higher income mobile users

Unit: Yuan

9,110

11,086 9,804

8,576 8,125

0

2000

4000

6000

8000

10000

12000

Android iPhone WindowsPhone

Blackberry Others

+5.6%

22

MOBILE ADS INVESTMENT

45

97

154

209

266

320

31%

51%

63%

70%

75%80%

12%

22%

31%

37%

43%48%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-

50

100

150

200

250

300

350

2014 2015 2016e 2017e 2018e 2019e

Mobile Internet Ad Spending in China,2014-2019

Mobile internet ad spending(Billion) % of digital ad spending %of total ad spending

Mobile ad spend surpasses PC ads in 2015 and will continue to grow in the coming years

Source:eMarketer, Sep 2015

23

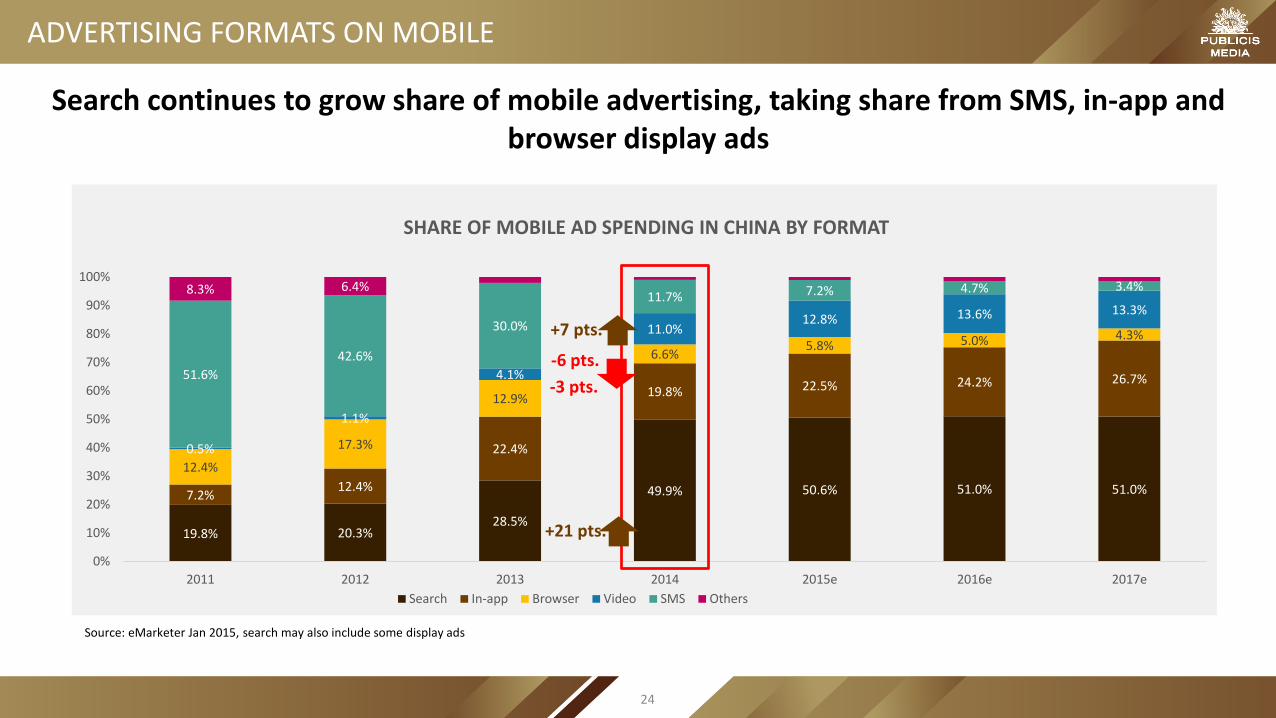

ADVERTISING FORMATS ON MOBILE

19.8% 20.3%28.5%

49.9% 50.6% 51.0% 51.0%7.2%12.4%

22.4%

19.8% 22.5% 24.2% 26.7%

12.4%

17.3%

12.9%

6.6%5.8% 5.0% 4.3%

0.5%

1.1%

4.1%

11.0%12.8% 13.6% 13.3%

51.6%

42.6%

30.0%

11.7% 7.2% 4.7% 3.4%8.3% 6.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015e 2016e 2017e

SHARE OF MOBILE AD SPENDING IN CHINA BY FORMAT

Search In-app Browser Video SMS Others

-3 pts.

+21 pts.

+7 pts.

-6 pts.

Source: eMarketer Jan 2015, search may also include some display ads

Search continues to grow share of mobile advertising, taking share from SMS, in-app and browser display ads

24

FORMATS & CASES

PANORAMIC EXPERIENCE

Uber: Play basketball with Kris Wu

Uber created an H5 page with VR to offer panoramic experience. Users can make defensive move by rotating their mobile while Kris tries to shoot. Winners get red envelops.

10 Corso Como: Panoramic Shopping

Actual instore setting is restored with 360°interaction to offer shopping experience to consumers far away, which speed up online consumption.

Shanghai E-shop

Beijing E-shop

Enhanced visual experience strengthens the sense of reality while interacting with consumers

26

2.Pro X pushes banners with different content under various AQI context1.Impression on weather forecast page to draw the attention of weather conscious females.

CONTEXTUAL MARKETING

Using real time data to understand consumer needs and target appropriately

27

Mobile will surpass all other media both in terms of penetration and time spent. Percentage of mobile investment as well as its role should be fully carefully weighted.1.

Thanks to the development of VR and AR, panoramic experience will enjoy wider implementations. User experience should not be compromised while testing technology innovations.

2.

3.

RECOMMENDATIONS ON MOBILE

Mobile video ads now share higher quality standards and innovation, plus accurate user behavior analysis. Allows for delivery of more targeted and context based content through programmatic buy.

28

TV & OTV

57% 56% 54% 56% 57% 58% 63%

43% 44% 46% 44% 43% 42% 37%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

all 15-19 20-24 25-29 30-34 35-39 40+

SHARE OF TIME SPENT ON TV/OTV – OTV VIEWERS

TV OTV

Source: CMMS 2015 Winter

58% watch OTV

97 % watch TV

TV only viewers drop by 5% as multi-screen viewing habits continue to grow

55% watch both

3% watch OTV only

OF THE TV/OTV VIEWING POPULATION:

42% watch TV only

(+4.8%)

(-5%)

(-0.4%)

(+0.4%)

(+5.2%)

TV & OTV COVERAGE

30

SMART TV OVERVIEW

201

50 46

23

77

0

50

100

150

200

250TV market sizeUnit: Million

Source:admaster,2016年1月

Although traditional TV still takes a bigger share, smart TV is catching up fast. TV time spent sees significant increase when consumers buy smart TV

46.9%

23.3%

22.4%

25.7%

13.7%

19.1%

9.1%

12.6%

6.0%

16.5%

1.9% 2.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

before they buy smart TV after they buy smart TV

TV Time Spent Share

less than 1h 1-2h 2-3h 3-4h over 4h unknown

31

SMART TV ADS FORMAT

Mainstream formats: Content based formats:

“Push content based on programs "is possible on smart TVCase study:during the World Cup, users can interact with smart TV by betting on penalty results to win prizes and collect points.

DIS

PLA

YIN

TER

AC

TIO

NEP

G

Brand zoneFull screen FrontPage/menu/portal VOD pre-roll/post-roll/pause/exit

Navigation bar ad Channel menu ad Volume bar ad

QR code

Link with other smart

devices

Mini siteCorner banner

32

NEW ADVERTISING POLICY

Banned on TV, banned on digitalSAPPRFT installs 24 hour nonstop surveillance on online series, bearing the same censor as with TV. Those already on air but failed to meet the regulations would be put off air or sent back for re-editing, such as Go, Princess go and Addiction.

Restrictions on celebrity kids showsSAPPRFT will strictly control number of reality show that have underaged kids as well as its content and time slot. Using reality shows to market kids of celebrity is especially banned. Such programs would be pulled out of evening timeslot for good, besides, program featuring celebrity kids would become history.

SAPPRFT may restore TVC during drama and 1 drama might be airedon 3 PSTVRecently, SAPPRFT made adjustments on 3 aspects of TV drama: restore TVC duringdrama with total time span of less than 18 minutes; 3 episodes or 2 episodes if eachspans 1 hour; some drama can be aired on 3 PSTV.

33

1

2

3

TV

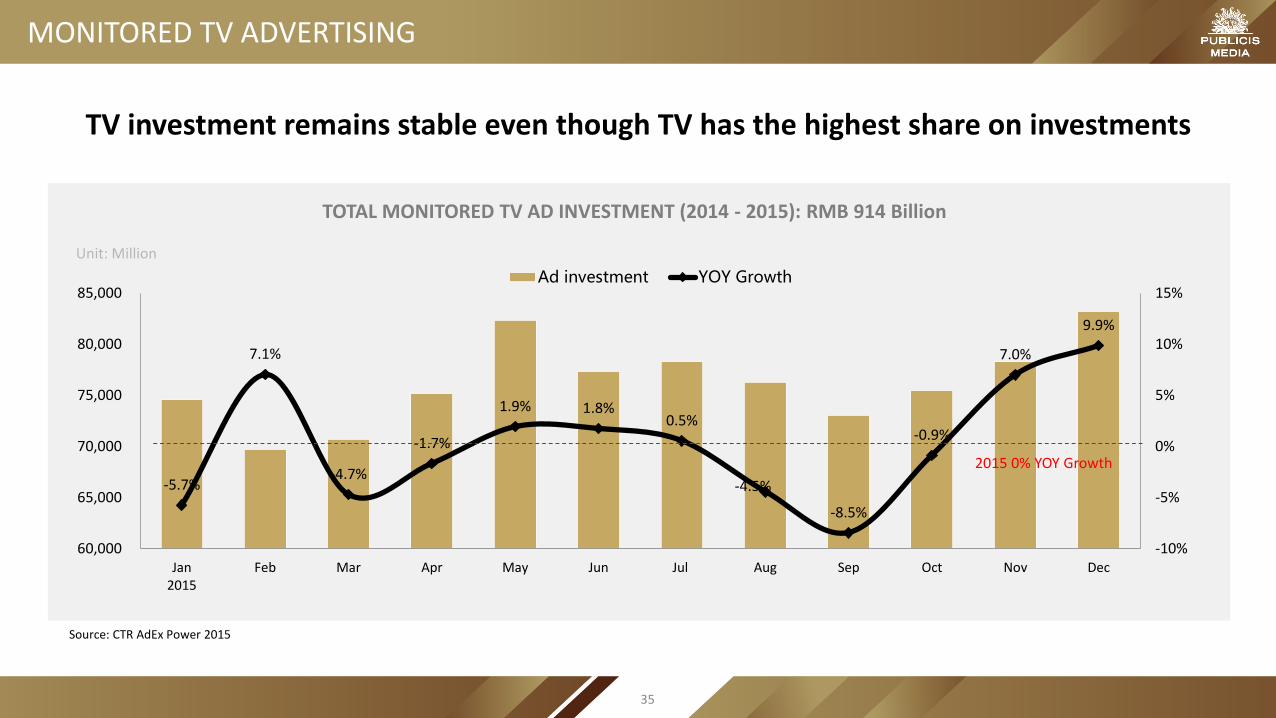

MONITORED TV ADVERTISING

Unit: Million

TOTAL MONITORED TV AD INVESTMENT (2014 - 2015): RMB 914 Billion

-5.7%

7.1%

-4.7%

-1.7%

1.9% 1.8%0.5%

-4.5%

-8.5%

-0.9%

7.0%

9.9%

-10%

-5%

0%

5%

10%

15%

60,000

65,000

70,000

75,000

80,000

85,000

Jan2015

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ad investment YOY Growth

TV investment remains stable even though TV has the highest share on investments

2015 0% YOY Growth

Source: CTR AdEx Power 2015

35

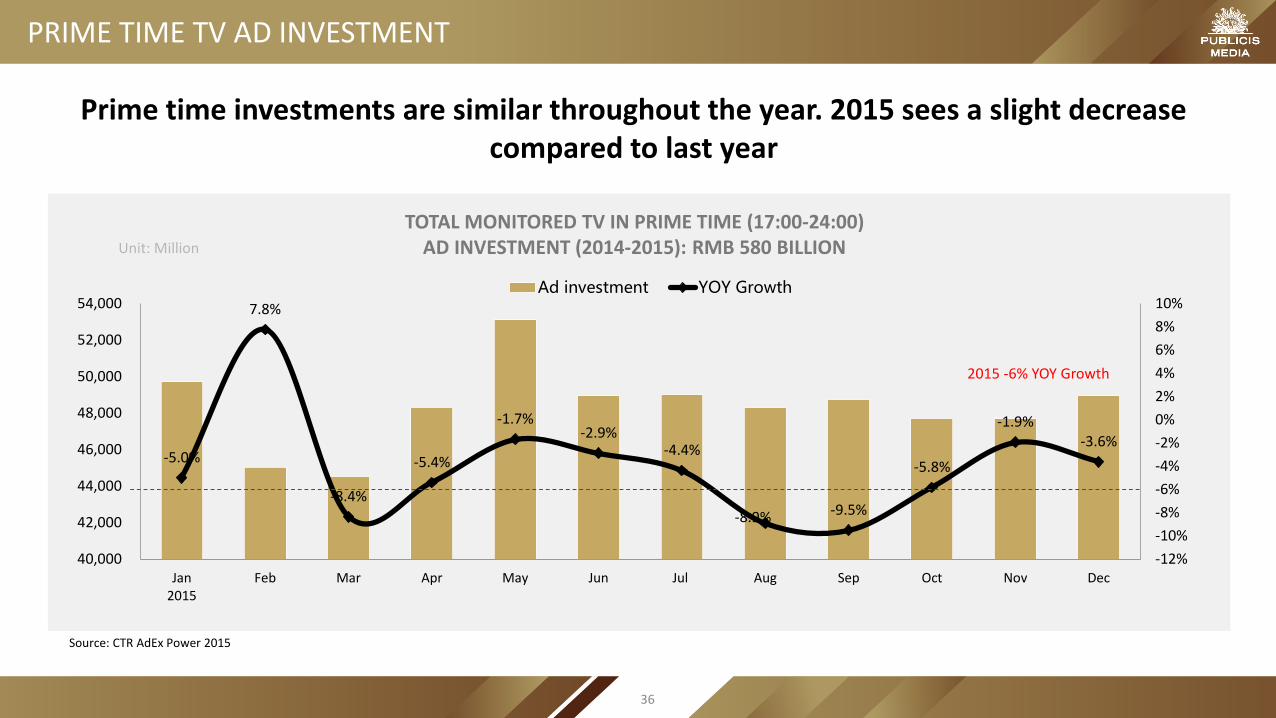

PRIME TIME TV AD INVESTMENT

Unit: Million

TOTAL MONITORED TV IN PRIME TIME (17:00-24:00)AD INVESTMENT (2014-2015): RMB 580 BILLION

-5.0%

7.8%

-8.4%

-5.4%

-1.7%-2.9%

-4.4%

-8.9% -9.5%

-5.8%

-1.9%-3.6%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

40,000

42,000

44,000

46,000

48,000

50,000

52,000

54,000

Jan2015

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ad investment YOY Growth

Prime time investments are similar throughout the year. 2015 sees a slight decrease compared to last year

2015 -6% YOY Growth

Source: CTR AdEx Power 2015

36

TV AD INVESTMENT BY CATEGORY

Unit: Million

TV MONITORED AD INVESTMENT BY SECTORS (2014-2015)

39%

-4% -4%

-22%-12%

-4% -7%-12%

33%24%

-2%

37%

11%

-12% -15%-6%

8% 10%

-11%

33%

76%

-40%

-20%

0%

20%

40%

60%

80%

100%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2014 2015 YOY Growth

Pharmaceuticals continue to strengthen investments on TV, while we see a massive drop for Toiletries and Automobile categories

Source: CTR AdEx Power 2014-2015

37

PSTV WEEKLY DRAMA

Originate from overseas, Hunan PSTV took the first attempt

• In 2011, Hunan PSTV first tried weekly aired drama but failed with unaccustomed audience and the show was cut half way.

Hunan PSTV launched 2 timeslots for weekly drama with ancient costume drama enjoying

high rating Time of Youth

(青春进行时)

Diamond Exclusive

(钻石独播剧场)

• With restrictions on entertainment shows, Hunan PSTV launched 2 timeslots for weekly drama, “Time of Youth(青春进行时)” featuring romantic and city based drama, “Diamond exclusive(钻石独播剧场)” featuring ancient costume drama.

Weekly drama shows initial popularity, PSTV compete to take advantage

• Dragon PSTV first tested with Love Me if You Dare in Oct. 2015;

• Zhejiang PSTV also launched its weekly drama strategy and name it “Drama of Magic(奇妙剧场)”

Weekly drama increased in development in 2015 and may become a priority for PSTV in 2016

38

JOINT COUNTER ATTACK OF LTV

Market Hidden Singer Chinese Idol I’m a Singer Voice of China

14 city panel 1.09 1.13 1.72 2.08

Beijing 1.13 0.521 2.028 2.135

Fuzhou 0.137 0.958 2.047 1.555

Guangzhou 1.122 0.609 2.251 1.13

Hangzhou 0.225 0.197 1.155 4.456

Jinan 0.549 0.291 1.173 2.645

Shanghai 3.483 4.423 1.2 1.664

Shenzhen 0.79 0.158 2.452 1.827

Shenyang 0.324 0.383 2.024 3.214

Suzhou 0.941 0.404 1.002 1.585

Wuxi 0.441 0.248 0.906 1.404

Wuhan 0.541 1.282 1.868 2.319

Xi’an 0.217 0.213 2.106 1.798

Changchun 0.29 0.269 1.712 2.055

Chongqing 0.552 0.718 1.549 2.106

Source: Infosys, TA: P4+

Hidden Singer was created by Shanghai Entertainment Channel, Beijing Art Channel, Guangzhou Comprehensive Channel, Shenzhen City Channel together , produced by Dragon PSTV and aired on multiple LTV.

Restricted by budget and production capability, LTV couldn’t compete with CCTV and PSTV. However, several LTV have started to join hands in creating reality shows, breaking the

dominance of CCTV and PSTVRatings

More entertainment shows jointly created by LTV will be on air soon, such as Fashion CN vs. KR and Eat, Drink, Man, Woman.

39

OTV

504MILLION USERS

73% REACHAMONG ALL NETIZENS

8 DAYS PER MONTH

60 MINUTESPER USAGE DAY

PC MOBILE

65% REACH AMONG ALL NETIZENS

15 DAYS PER MONTH

46 MINUTESPER USAGE DAY

ONLINE VIDEO OVERVIEW

Source: Total netizen number and reach rom CNNIC, days and time spent from iUserTracker & mUserTracker Dec 2015;

41

MEDIA SHARE OF TIME SPENT ON PC AND MOBILE

TIME SPENT BY VIDEO PLATFORM

PC

36%

14%8%

8%

8%

7%

4%

3%2%1%

10%

iQiyi

Baofeng

Youku

Sohu

Tencent

PPTV

Fushion

LeTV

CNTV

Tudou

Others

-4%

-9%

-5%

Source: iUserTracker & mUserTracker Dec 2014 & 2015, PC includes desktop apps.Note:iQiyi’s fast expansion is due to exclusive copyright and self produced content.

+14%

33%

23%

23%

7%

6%3%

4%0%iQiyi

Tencent

Youku

LeTV

Sohu

PPTV

Tudou

MangoTV

Funshion

Others

MOBILE

iQiyi is the only platform that grew significantly on both PC & mobile. On mobile, top 3 players take nearly 80% share of total time spent

PC Dec-2015 Mobile Dec-2015

+15%

+8%

-9%

+2%

42

VIDEO VIEWS BY DEVICE

Viewers prefer tablets and phone for online video except for Baofeng, Funshion and Kankan.com

18%28% 30% 30%

40% 42% 45%55%

76%

94%

74%65% 60% 56%

42%48% 40%

43%

22%

4%8% 7% 10% 14% 18%10% 15%

2% 2% 2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Tencent Mango TV Youku&Tudou Iqiyi& PPS PPTV LeTV Souhu 风行 Baofeng kankan.com

VIDEO VIEW % BY DEVICE

PC Mobile

Source:Claimed Publisher Data, 2016

2% 18% 21% 5% 12% 9% 12% 21%

43

ONLINE VIDEO ADVERTISING REVENUE

Source: iResearch Report, Feb, 2016

0.2 0.5 3.39.8

17.5

26.5

36.3

6.59.3

11.9

13.4

15.5

17.7

18.6

3%5%

22%

42%

53%

60%

66%

0%

10%

20%

30%

40%

50%

60%

70%

0

10

20

30

40

50

60

2012 2013 2014 2015e 2016e 2017e 2018e

2012-2018 ADVERTISING REVENUE FOR ONLINE VIDEO (MOBILE & PC)

Mobile Advertising Non-Mobile Advertising % of all OTV Advertising

RMB: Billion

Mobile video revenue is expected to take over 50% of share in 2016

44

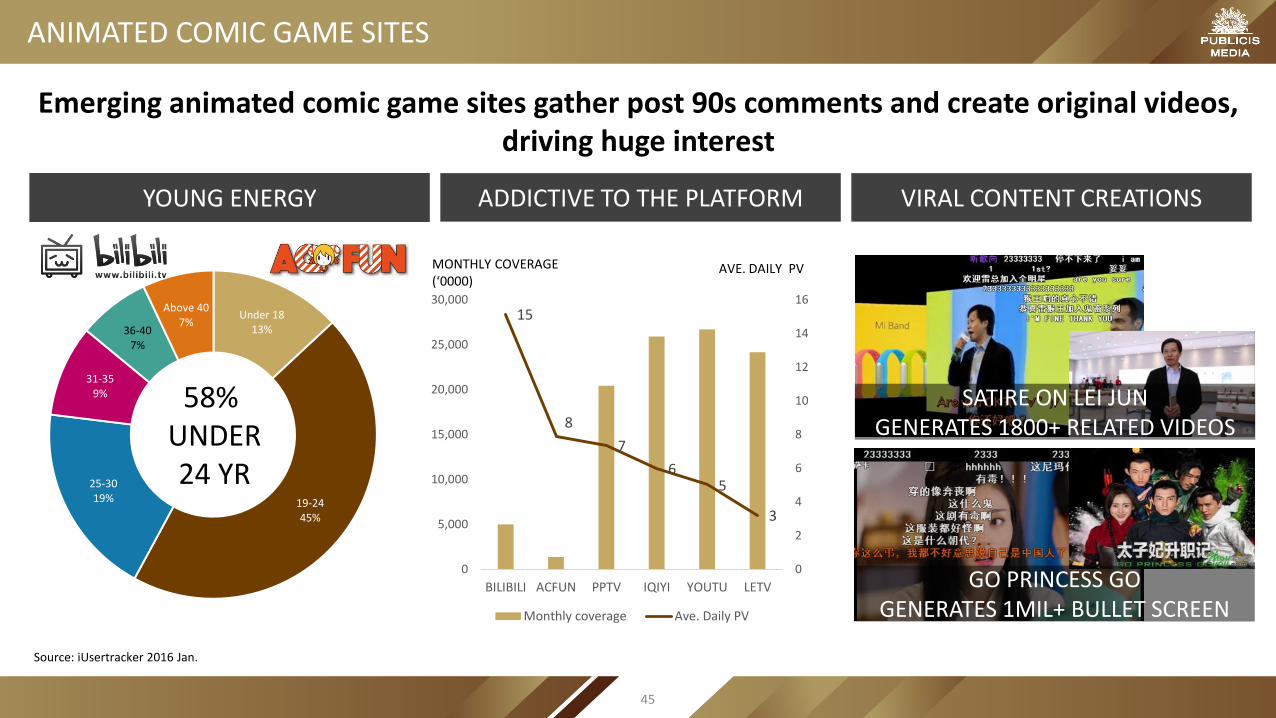

ANIMATED COMIC GAME SITES

YOUNG ENERGY ADDICTIVE TO THE PLATFORM

Under 1813%

19-2445%

25-3019%

31-359%

36-407%

Above 407%

VIRAL CONTENT CREATIONS

58% UNDER24 YR

15

8

7

65

3

0

2

4

6

8

10

12

14

16

0

5,000

10,000

15,000

20,000

25,000

30,000

BILIBILI ACFUN PPTV IQIYI YOUTU LETV

Monthly coverage Ave. Daily PV

MONTHLY COVERAGE(‘0000)

AVE. DAILY PV

Emerging animated comic game sites gather post 90s comments and create original videos, driving huge interest

SATIRE ON LEI JUN GENERATES 1800+ RELATED VIDEOS

GO PRINCESS GOGENERATES 1MIL+ BULLET SCREEN

Source: iUsertracker 2016 Jan.

45

VIDEO SITE VIP SUBSCRIPTION MODELS

iQiyi will invest more than 50% budget and resources to expend its VIP business in 2016.

iQiyi:Start the VIP subscription models

LeTV: content+ experience+ service

0.2 0.20.3

0.60.8

0.9

1.2

46%

91%

63%

171%

272%284%

256%

0%

50%

100%

150%

200%

250%

300%

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

2014Q1 2014Q2 2014Q3 2014Q4 2015Q1 2015Q2 2015Q3

VIDEO SITE VIP MARKET SCALE

Video site VIP market scale (billion) Growth

First start VIP-watch-first model First start VIP-watch-only model

Source:iQiyi《网络视频个人付费行业白皮书》

LeTV started VIP model of “content+experience+service”, and allowed the member can be engaged in more services, such as sports, music and online&offline movies.

“Go, Princess, Go” attract 2.2 million people to pay for the content.

In Jan, 2016, the VIP number has reached 20 million.

With good content and service together with convenience of online payment, VIP subscription model of video site begins booming

46

SELF-PRODUCED PROGRAM

The number of self-produced programs in online video site has doubled in 2015, and the broadcast of each episode has reached over 100 million

Souce: Media , March, 2016

3

4

4

24

21

21

30

8

9

10

30

42

42

50

PPTV

MangoTV

Souhu

Tencent

iQiyi

Letv

Youku&Tudou

The number of self-produced program (2014VS2015)

Y2015 Y2014

iQiyi-《U CAN U BB》broadcast :191,000,000/episode

iQiyi-《The Lost Tomb》broadcast:243,000,000/episode

LeTV-《Go, Princess, Go》broadcast :89,000,000/episode

47

FORMATS & CASES

UPDATED WATCH&BUY

Youku: Occasion targeting iQiyi:Facial recognition

iQiyi use the figure out technology to do the facial recognition, which can help to realize the model that the brand will be wherever the celebrity is.

Based on the content, Youku do the targeting with 6 dimensions: category, product, brand, location, scene tonality and occasion type.

Ctrip is the first tester of this techonology. In the variety show “running man”, when Dengchao shows up, Ctrip ads will pop up, which successfully transform the

celebrities fans into its own consumers.

Products:Capture the products in video and tag them to do the watch&buy.

Occasion:Define the occasion in video by tag to do the watch&buy.

49

E-COMMERCE IN VIDEO SITE

Combining with brand, KOL, content, e-commerce and social forum, Youku connects content and purchase to build a new ecosystem

Oh!8 Brand shop

Related content & video

Fans interaction area

KOL video

Shopping area

Youku mall: purchase directly

GoPro Brand shop

Social media

Brand

E-commence

Content

UPCG KOL

Experience native marketing

KOLBrand

Purchase Fans

Brands cooperate with Youku UPCG KOL to build the business ecosystem

Offer the platform to demonstrate products and

link to e-commerce platform directly.

Offer a fans interaction area to build the fans

economy.

Give the brand an opportunity to expose its products and drive sales

directly.

50

NONGFU SPRING TRUE VIEW

Now Youku and iQiyi allow users to skip pre-roll therefore advertisers only pay for the actual exposure

Exclusive displayed

1-3 minutes long

Skippable after 5

seconds

Charge after 30 seconds

Frequency cappingPC Only

Nongfu Spring 180s true view results:

The first day Whole campaign

30 s 80% 67%

180 s 70% 57%

CTR4.07%

400% higher than average

2.82%282% higher than

average

Win the word of mouth

51

LANEIGE CONTENT COOPERATION

Sponsor the drama in iQiyi and occupy the first place of the homepage

Brand/product implantation Video sites cooperation Owned media support

Watch & buy

Page decorated by brands elements+ The first pre-roll+ small video ad on the bottom right corner

Promotion in iQiyi mall in mobile App

Celebrities is using products in the drama Official wechat launched a related activity.

Official weibo interact with fans.

Official e-commence sell the same products.

Laneige partnered with the hot Korean drama “Descendants of the Sun”

52

Smart TV shows strong potential for the future with growing penetration and possibility of programmatic buying in the near future. 1.

OTV ads blocking has seen steady growth this year, therefore, advertisers need to look beyond exposure on traditional spots such as in-program.2.

OTV is incorporating E-commerce with its sales led and branding enabled content.3.

Bullet screen (弹幕) makes OTV viewing part of social experience. Advertisers can use it to build WOM.4.

RECOMMENDATION ON TV & OTV

53

SOCIAL

624 MILLION USERS

91% REACHAMONG ALL NETIZENS

14 DAYS PER MONTH

17 MINUTESPER USAGE DAY

PC MOBILE

90% REACHAMONG ALL NETIZENS

19 DAYS PER MONTH

37 MINUTESPER USAGE DAY

SOCIAL OVERVIEW

Source: Total netizen number and reach number from CNNIC, days and time spent from iUserTracker & mUserTracker Jun 2015; Note PC also include social shopping here, while mobile doesn’t.

55

77%

7%

5%4%

2%QQ

Q-Zone

Sina Weibo

Aliwangwang

Baidu Tieba

Sina Blog

Real Time eXchange

Tianya

Others

46%

40%

6%2% 3%

Sina Weibo

Q-Zone

Momo

Baidu Tieba

Lamabang

Qiushibaike

Others

3%

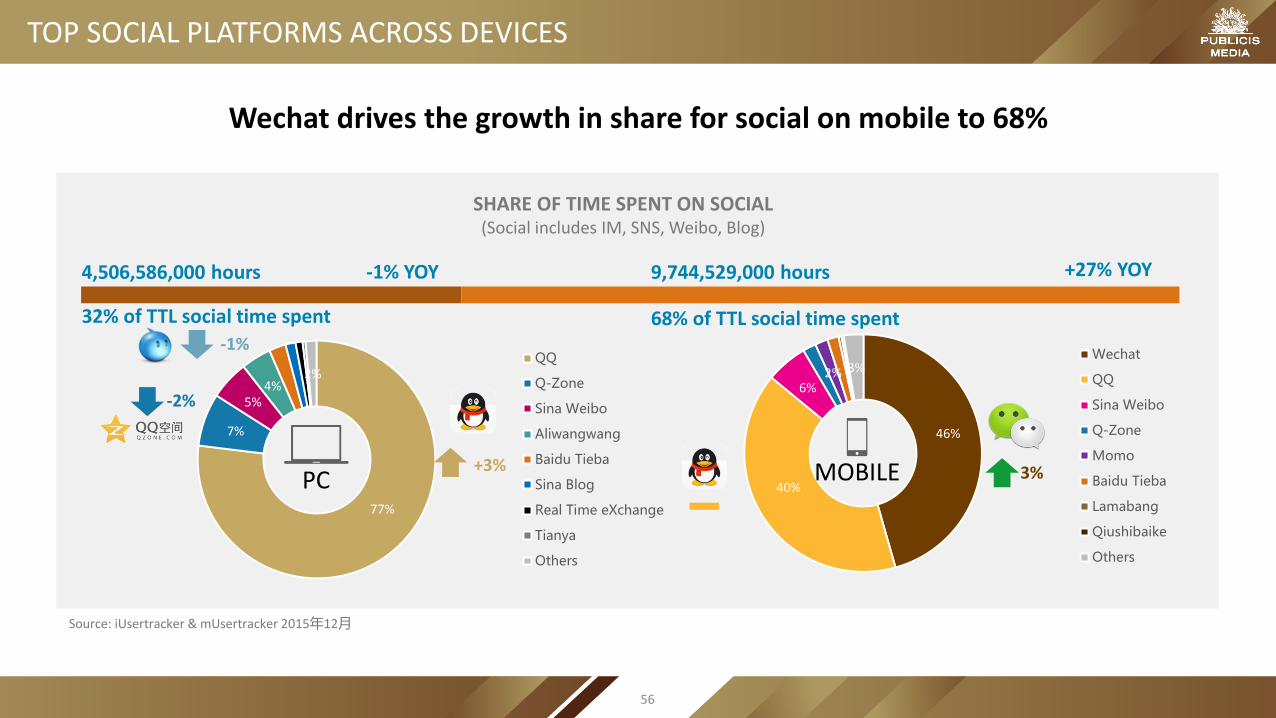

4,506,586,000 hours

32% of TTL social time spent

-1% YOY 9,744,529,000 hours

68% of TTL social time spent

+27% YOY

+3%

-2%

-1%

TOP SOCIAL PLATFORMS ACROSS DEVICES

Source: iUsertracker & mUsertracker 2015年12月

SHARE OF TIME SPENT ON SOCIAL(Social includes IM, SNS, Weibo, Blog)

PC MOBILE

Wechat drives the growth in share for social on mobile to 68%

56

MONTHLY REACH OF TOP PROGRAMS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

PC - SOCIAL REACH(%)

QQ zone

Sina Weibo

Baidu Tieba

Aliwangwang

Douban

Tianya

Source: iUsertracker & mUsertracker 2015年1-12月.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

MOBILE - SOCIAL APP REACH (%)

Sina Weibo

QQ zone

Momo

QQ mail

ChatON

Aliwangwang

On PC, the reach of QQ Zone declines sharply while others keep stable

57

AGE DISTRIBUTION OF SOCIAL MEDIA

53%

44%

33%

18%

5%

34%

72%

60%

53%

32%

10%

51%

0%

10%

20%

30%

40%

50%

60%

70%

80%

16-25 26-35 36-45 46-55 55+ Total

AGE DISTRIBUTION OF SOCIAL MEDIA

2014 2015

35%

37%64%

75%

92%

50%

Young people still the biggest users of social media, however older users have doubled in 2015

Source: Kandar-Chinese Social Media Report, Jan. 2016

58

FORMATS & CASES

VIDEO AD ON SOCIAL PLATFORMS

Wechat and Weibo both launched video ads to offer more dynamic formats

Brand feed video adsAutomatic view with Wi-Fi, shown in front-page, full screen display enabled

Weibo recommendation video adsGender, age, geographic targeting enabled, shown in second spot of Weibo video, play if slide upwards

Advertiser

Copy

6 seconds short video ( 30-90

seconds long video after clicking)

Interaction

Support to download/book activities

Support to skip to H5 page

Support to skip to public account’s news

60

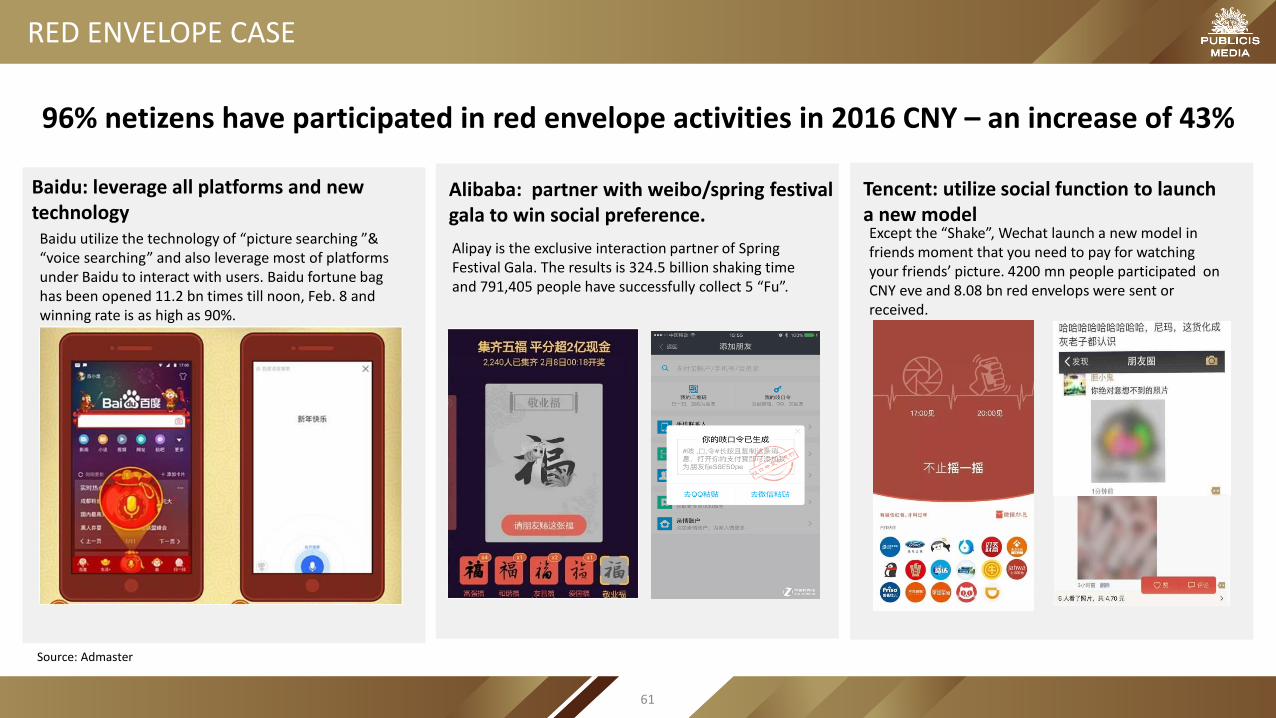

RED ENVELOPE CASE

Alibaba: partner with weibo/spring festival gala to win social preference.

Tencent: utilize social function to launch a new model

Baidu: leverage all platforms and new technology

Baidu utilize the technology of “picture searching ”& “voice searching” and also leverage most of platforms under Baidu to interact with users. Baidu fortune bag has been opened 11.2 bn times till noon, Feb. 8 and winning rate is as high as 90%.

Alipay is the exclusive interaction partner of Spring Festival Gala. The results is 324.5 billion shaking time and 791,405 people have successfully collect 5 “Fu”.

96% netizens have participated in red envelope activities in 2016 CNY – an increase of 43%

Except the “Shake”, Wechat launch a new model in friends moment that you need to pay for watching your friends’ picture. 4200 mn people participated on CNY eve and 8.08 bn red envelops were sent or received.

Source: Admaster

61

NEW SOCIAL MODEL: LIVE BROADCAST

ADVERTISMENTGAME NEWS

There’s large number of game users, and among them male with good consumption ability take the biggest account. Based on iResearch, the live game broadcast will reach to 100 million.

163 news launch the project “2016 Spring Festival Travel Live broadcast” which is a 360 hours record by video, picture and word. 22 million people in total attend this news live broadcast.

Durex launched a 3 hours video in Bilibili to promote its new product. There’re over 1 million audiences watching it and 300,000 of them watch the whole advertisement.

62

Social is becoming more diversified and can be used to reach specific targets with the right content and start conversation.1.

Social + video is attracting more and more attention, allowing advertisers to track consumer response.2.

Content which resonate with consumers tend to drive more interactions with customers.3.

RECOMMENDATIONS ON SOCIAL

63

MAGAZINE AND NEWSPAPER

33%

74%

62%

23%18%

96%

31%

66% 64%

35%

16%

95%

29%

62%

68%

49%

17%

96%

27%

55%

74%

64%

18%

96%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Magazine Reach NewspaperReach

Internet Reach Mobile InternetReach

Radio Reach TV Reach

2013-2015 REACH OF PRINT MEDIA

2012 2013 2014 2015

PRINT MEDIA OVERVIEW

Source: CMMS 2012-2015Winter

14.6 minutes on magazine 35.4 minutes on newspaper

Print readership continues to decline due to the fast rise of digital media

DAILY TIME SPENT ON PRINT

134

186

242

3283.87

7.059.43

13.84

-10

-5

0

5

10

15

0

50

100

150

200

250

300

350

2012 2013 2014 2015

No. of users (mn) Market share (bn)

2012-2015 CHINA MOBILE READING MARKET

65

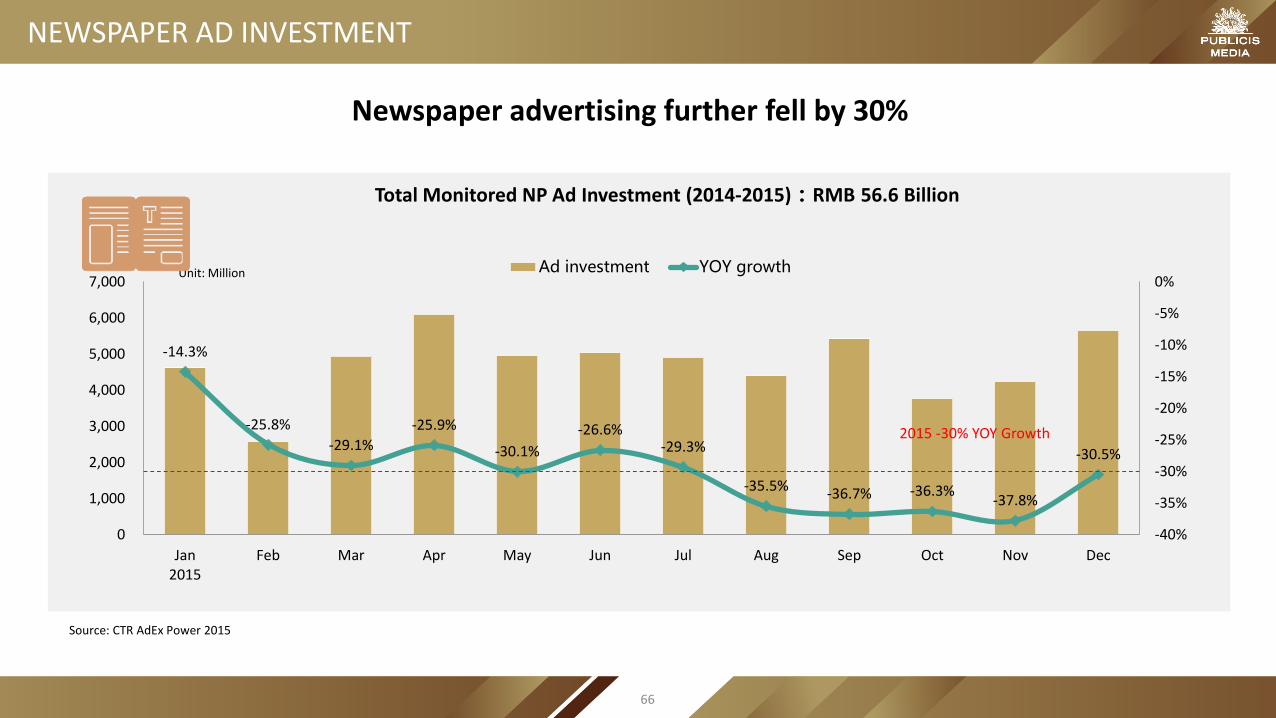

-14.3%

-25.8%

-29.1%

-25.9%

-30.1%

-26.6%-29.3%

-35.5% -36.7% -36.3%-37.8%

-30.5%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Jan2015

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ad investment YOY growth

Total Monitored NP Ad Investment (2014-2015):RMB 56.6 Billion

Unit: Million

NEWSPAPER AD INVESTMENT

2015 -30% YOY Growth

Newspaper advertising further fell by 30%

Source: CTR AdEx Power 2015

66

NP Monitored Ad Investment By Sectors (2014-2015)

Ad spend in newspapers decreased across most categories

NEWSPAPER AD INVESTMENT BY INDUSTRY

Unit: Million

-35%-44%

-16%-5%

-21%

-46%

-12%

-43%-49%

-41%

-20%

-42%-33%

-20%

-54% -56%

-21%-10% -10%

38%

-73%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

0

5,000

10,000

15,000

20,000

25,0002014 2015 YOY growth

Source: CTR AdEx Power 2014-2015

67

MAGAZINE AD INVESTMENT

Total Monitored MG Ad Investment (2014 - 2015): RMB 14.7 Billion

-10.8%

-3.8%

-14.1%

-18.7%-20.8%

-16.4%

-21.6%-23.7% -23.3%

-21.8%-19.8%

-27.7%

-30%

-25%

-20%

-15%

-10%

-5%

0%

0

200

400

600

800

1,000

1,200

1,400

1,600

Jan2015

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ad investment YOY GrowthUnit: Million

2015 -20% YOY Growth

Magazine investment dropped by 20% in 2015

Source: CTR AdEx Power 2015

68

MAGAZINE AD INVESTMENT BY INDUSTRY

MG Monitored Ad Investment By Sectors (2014 & 2015)

-22%

-13%

-21%-25%

-10%

-28% -26%

-18% -20%-17%

-32%

-20%

-29% -30%

-38% -40%

-18%

11%

-7%

1%

-39%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

0

1,000

2,000

3,000

4,000

5,000

6,0002014 2015 YOY growth

Unit: Million

As seen for newspapers, ad spend on magazines decreased across all key categories

Source: CTR AdEx Power 2014-2015

69

FORMATS & CASES

CASE: SECRET GARDEN

After the popularity of coloring book ”secret garden”, a real estate company created its secret garden in the Nanjing Newspaper.

Advertise in a newspaper by the method of coloring just like the Secret Garden

Gain a social buzz on social media Encourage consumers to finish the work and win the prize.

71

With most leading print publishers now have online versions, print buys should not be restricted to hard copy.1.

Print still can be used for local activation coupled with interactive mechanism.2.

RECOMMENDATIONS ON PRINT

72

RADIO

Source:CMMS 2013-2015 Summer

1 hour 5 minutes on radio

Car Owners Non Car Owners58 minutes on radio 1 hour 11 minutes on radio

DAILY TIME SPENT ON RADIO (YESTERDAY)

15%

47%

11%

18%

52%

12%

18%

54%

11%

0%

10%

20%

30%

40%

50%

60%

Total Population Car Owners Non Car Owners

MONTHLY REACH OF RADIO 2013-2015 BY CAR OWNERSHIP

2013 2014 2015 Total Population

RADIO OVERVIEW

Radio continues to increase reach among car owners, however time spent per person declines with increase in light listeners

74

RADIO AD INVESTMENT

TOTAL MONITORED RD AD INVESTMENT (Jan- Dec 2015): 36.4 bn RMB

-2.4%

17.2%

-3.6%

7.6%6.7%

10.5%

17.3%

13.4%11.6%

12.9%

5.2%

11.9%

-5%

0%

5%

10%

15%

20%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Jan2015

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ad investment YOY GrowthUnit: Million

2015 YOY GROWTH9%

Radio investments grew at a steady pace of 9%

Source:CTR AdEx Power 2014-2015

75

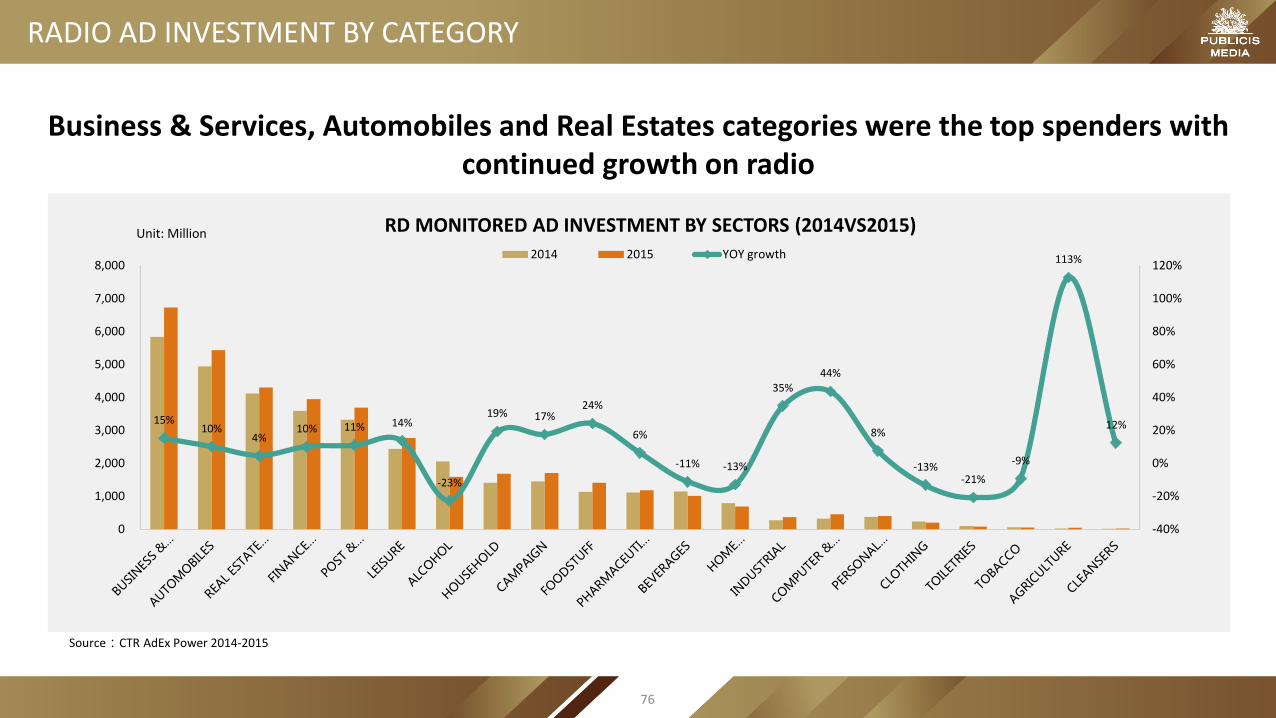

RD MONITORED AD INVESTMENT BY SECTORS (2014VS2015)

15%10%

4%10% 11% 14%

-23%

19% 17%24%

6%

-11% -13%

35%44%

8%

-13%-21%

-9%

113%

12%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,0002014 2015 YOY growth

Unit: Million

RADIO AD INVESTMENT BY CATEGORY

Business & Services, Automobiles and Real Estates categories were the top spenders with continued growth on radio

Source:CTR AdEx Power 2014-2015

76

MOBILE RADIO

65

59

66 6469 67

70 69 70 6971

74

0

10

20

30

40

50

60

70

80

3300

3400

3500

3600

3700

3800

3900

4000

4100

4200

2015 MOBILE RADIO COVERAGE

Coverage Time per person(min)

Unit:0000’

33%

23%

21%

6%

2%

2%

2% 2%

1% 1% 8%

SHARE OF TIME SPENT

Lazyaudio

Ximalaya FM

Qingting FM

Kwting

Kaola FM

Lizhi FM

ifeng FM

Douban FM

FM radio

Baidu Music

Others

Time spent on mobile radio is increasing with top 3 APP already occupying 70% of time

Source: mUsertracker, 2015

Unit:mins

77

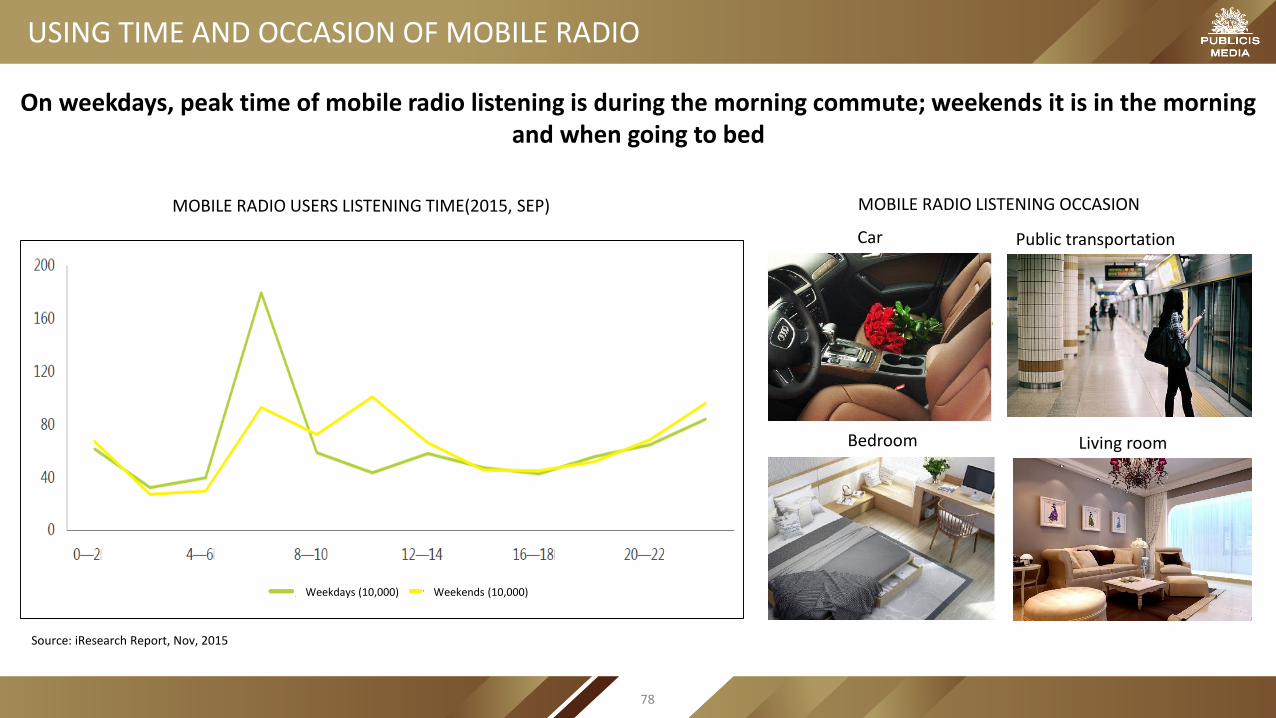

USING TIME AND OCCASION OF MOBILE RADIO

MOBILE RADIO LISTENING OCCASION

Car

Bedroom

Public transportation

Living room

MOBILE RADIO USERS LISTENING TIME(2015, SEP)

On weekdays, peak time of mobile radio listening is during the morning commute; weekends it is in the morning and when going to bed

Source: iResearch Report, Nov, 2015

Weekdays (10,000) Weekends (10,000)

78

As consumer would shift to mobile radio, it provides advertisers with newer formats and context based advertising opportunities. 1.

Car owners are still major radio listeners. Low cost radio programs can be used as part of an integrated plan targeting them.2.

RECOMMENDATIONS ON RADIO

79

OOH

OOH AD INVESTMENT

TOTAL MONITORED OOH AD INVESTMENT (Jan -Dec 2015): RMB 22.24 Billion

4.4%

14.3%

6.0%

2.0%4.7%

2.8%

-3.0%-5.1%

-8.9%

-5.2%

-7.7%

-4.3%

-15%

-10%

-5%

0%

5%

10%

15%

20%

1,650

1,700

1,750

1,800

1,850

1,900

1,950

2,000

Jan2015

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ad investment YOY Growth

Unit: Million

2015 YOY Growth:0%

OOH Investment remains stable in 2015

Source:CTR AdEx Power 2015

82

OOH AD INVESTMENT BY INDUSTRY

OOH Monitored Ad Investment By Sectors (Jan-Dec 2014 & 2015)

2.7% 1.2%

14.8%

4.1% 3.6%

-11.7% -10.0%

5.7%

-8.9%-17.8%

-5.7%

-18.9%

8.3%

-13.7%

-25.4%

7.3%

-22.7%

2.4%

19.1%

41.6%

-24.3%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

1,000

2,000

3,000

4,000

5,000

6,000

Jan-Dec,2014 Jan-Dec,2015 YOYUnit: Million

FMCG category (beverage, food, toiletries) reduce their OOH investment, while business services, real estate and telecommunications have remained stable or increased investment

Source:CTR AdEx Power 2014-2015

83

TOP 10 OOH ADVERTISER IN 2015

Internet brands join in the competition, with 5 out of top 10 are from digital roots: Tmall, Guazi.com, Tuniu.com and JD.com. KFC remains the NO.1 of OOH media investment

Source:CODC 2015年

921

924

963

1,142

1,162

1,168

1,351

1,690

1,894

2,010

0 500 1,000 1,500 2,000 2,500

Suning

XiaoTianCai

MengNiu

Nongfu Spring

JD.com

TuNiu.com

Gold JianNan

Guazi.com

Tmall

KFC

YOY Growth

5%

224%

-

26%

66%

35%

-20%

86%

1796%

-29%

Unit: Million

84

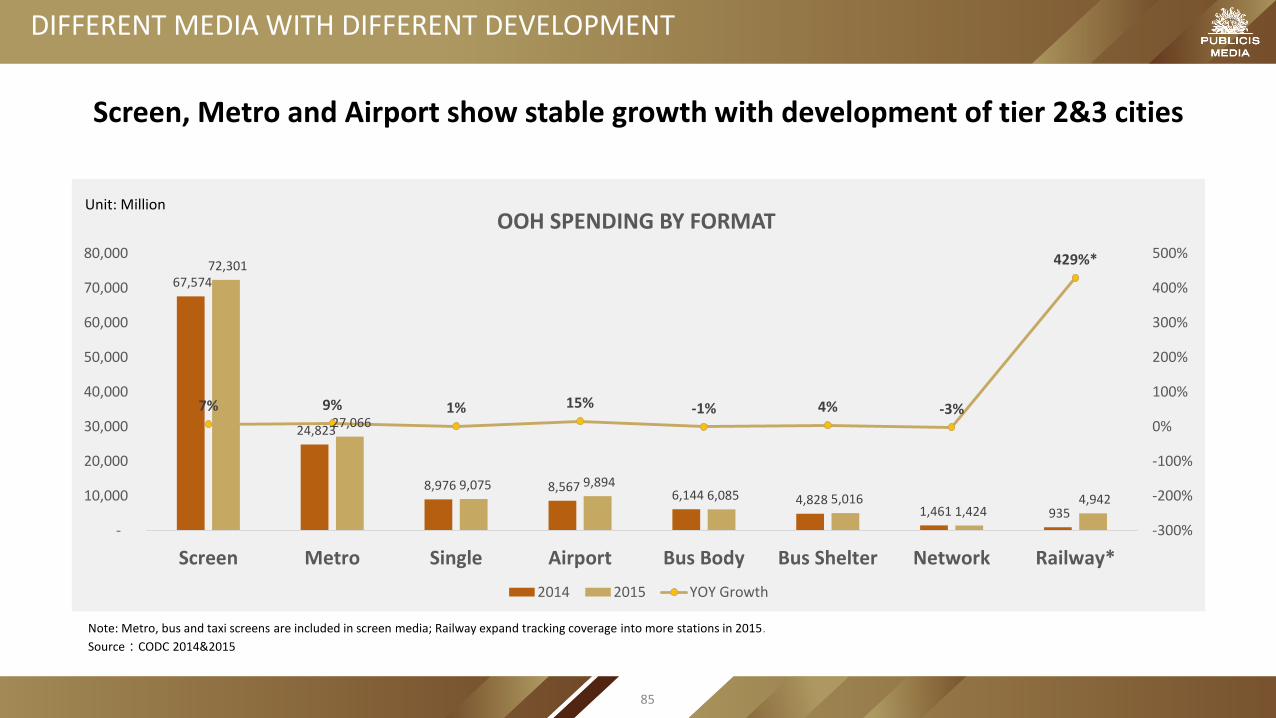

DIFFERENT MEDIA WITH DIFFERENT DEVELOPMENT

Screen, Metro and Airport show stable growth with development of tier 2&3 cities

Source:CODC 2014&2015

Note: Metro, bus and taxi screens are included in screen media; Railway expand tracking coverage into more stations in 2015.

Unit: Million

67,574

24,823

8,976 8,567 6,144 4,828

1,461 935

72,301

27,066

9,075 9,894 6,085 5,016

1,424 4,942

7% 9% 1% 15% -1% 4% -3%

429%*

-300%

-200%

-100%

0%

100%

200%

300%

400%

500%

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Screen Metro Single Airport Bus Body Bus Shelter Network Railway*

OOH SPENDING BY FORMAT

2014 2015 YOY Growth

85

SCREEN AND METROS STILL THE KEY

Source:CODC 2014&2015

Unit: Million

Screen Media Comparison (Unit : RMB Million)

Media Type 2014 2015 Growth%

Building LCD 41,464 46,997 13%

LED Screen 12,680 13,777 9%

Metro TV 3,104 1,739 -44%

Bus LCD 3,690 4,591 24%

Metro LCD 3,104 1,739 -44%

Taxi Screen 2,403 783 -67%

Others 1,129 2,674 137%

Total 67,574 72,301 7%

Screen Media Share 55% 53%

Following the trend in 2014, screen media takes half the share of total OOH Spending, while Bus LCD and Building LCD grows the fastest

Metro20%

Single7%

Airport7%

Bus Body4%

Bus Shelter4%

Network1%

Railway Station4%

Building LCD35%

LED screen10%

Metro TV

Bus LCD 3%Metro LCD 1%

Taxi Screen1%

Others 2%

Screen Media53%

86

OOH TREND ACROSS TIERS

Source: CODC 2015

51%, Screen

24%, Metro

6%, Single

8%, Airport

4%, Bus Body

3%, Bus Shelter

1%, Network

4%, Railway

Screen

Metro

Single

Airport

Bus Body

Bus Shelter

Network

Railway

55%, Screen

19%, Metro

6%, Single

7%, Airport

5%, Bus Body

4%, Bus Shelter

3%, Railway

Screen

Metro

Single

Airport

Bus Body

Bus Shelter

Network

Railway

59%, Screen3%, Metro

13%, Single

5%, Airport

6%, Bus Body

8%, Bus Shelter

3%, Network

4%, Railway

Screen

Metro

Single

Airport

Bus Body

Bus Shelter

Network

Railway

SHARE OF OOH FORMAT INVESTMENT CROSS TIERS

Screen ads develop faster across all cities due to the improvement of infrastructure

12%7%2%

87

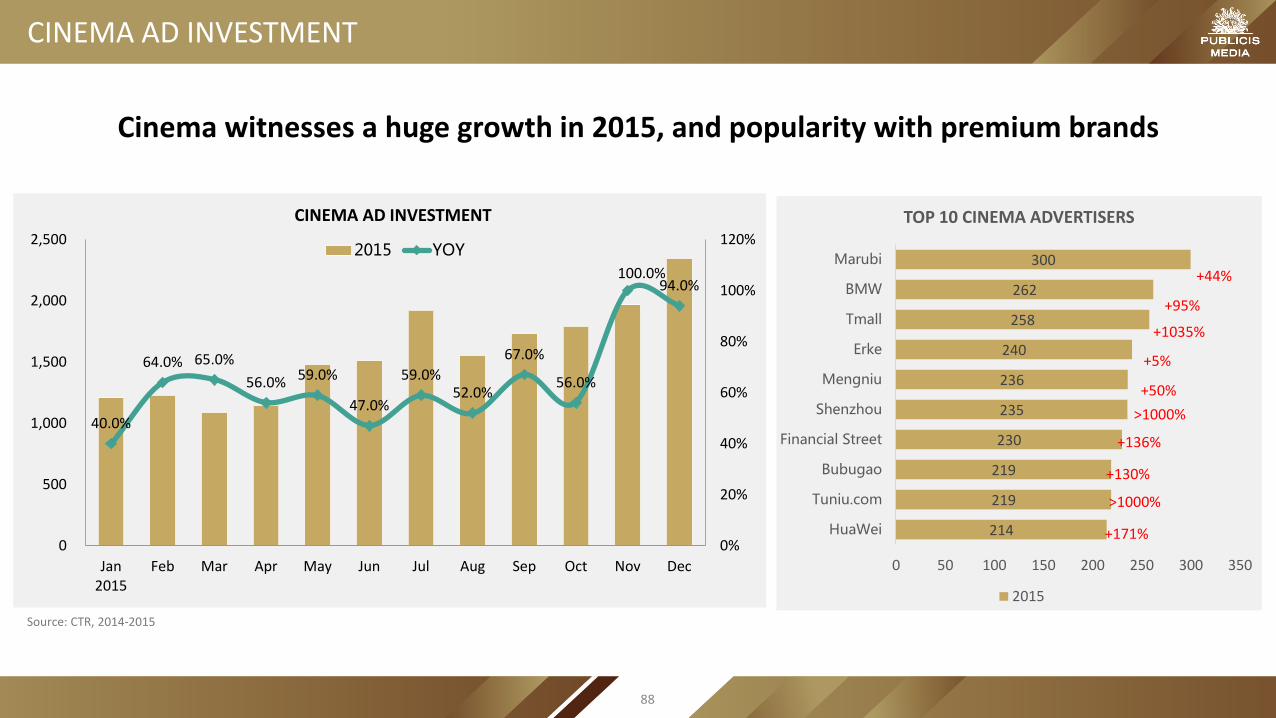

CINEMA AD INVESTMENT

40.0%

64.0% 65.0%

56.0% 59.0%

47.0%

59.0%52.0%

67.0%

56.0%

100.0%94.0%

0%

20%

40%

60%

80%

100%

120%

0

500

1,000

1,500

2,000

2,500

Jan2015

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

CINEMA AD INVESTMENT

2015 YOY

214

219

219

230

235

236

240

258

262

300

0 50 100 150 200 250 300 350

HuaWei

Tuniu.com

Bubugao

Financial Street

Shenzhou

Mengniu

Erke

Tmall

BMW

Marubi

TOP 10 CINEMA ADVERTISERS

2015

+44%

+95%

+1035%

+5%

+50%

+136%

+130%

>1000%

+171%

>1000%

Source: CTR, 2014-2015

Cinema witnesses a huge growth in 2015, and popularity with premium brands

88

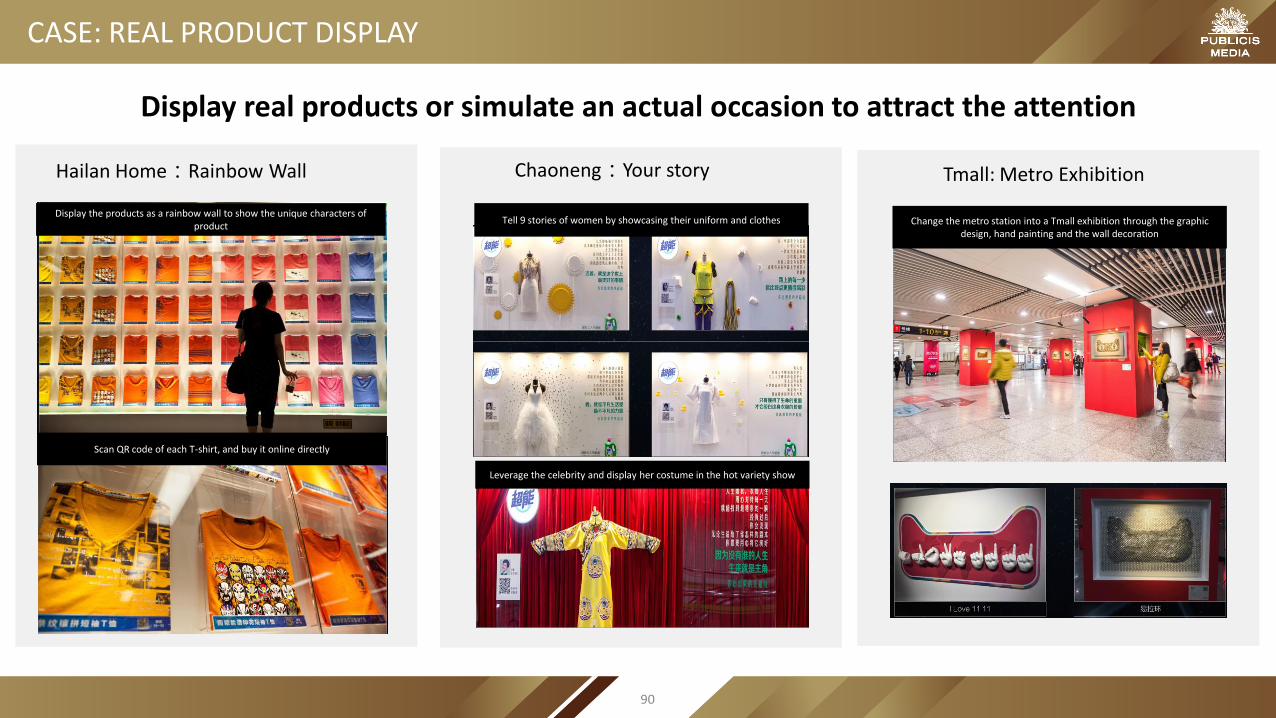

FORMATS & CASES

CASE: REAL PRODUCT DISPLAY

Hailan Home:Rainbow Wall Chaoneng:Your story Tmall: Metro Exhibition

Display the products as a rainbow wall to show the unique characters of product

Scan QR code of each T-shirt, and buy it online directly

Tell 9 stories of women by showcasing their uniform and clothes

Leverage the celebrity and display her costume in the hot variety show

Change the metro station into a Tmall exhibition through the graphic design, hand painting and the wall decoration

Display real products or simulate an actual occasion to attract the attention

90

CASE: DIRECTLY DRIVE SALES

Hailan Home: a Tin of T-shirt Georgia Coffee:The Sense of Smell Tangdaren: To be or not to be

Build up an independent space with brand elements and diffuse the coffee smell. It aims to enhance the consumer experience by combing

vision and scent.

Install an interactive devise to allow consumers to play the game by their phones, and the winners can get a free sample from the vending

machine or get a coupon.

Change the traditional light box to a interactive game machine to solve the YES OR NO problems in people’s life.

Consumers who attend the game can win a product.

Set up a t-shirt vending machine in the metro station

Scan QR code to attend the mobile game and win a tin of T-shirt

Set up a vending machine to encourage consumers to actively engage in the product experience and drive sales further.

91

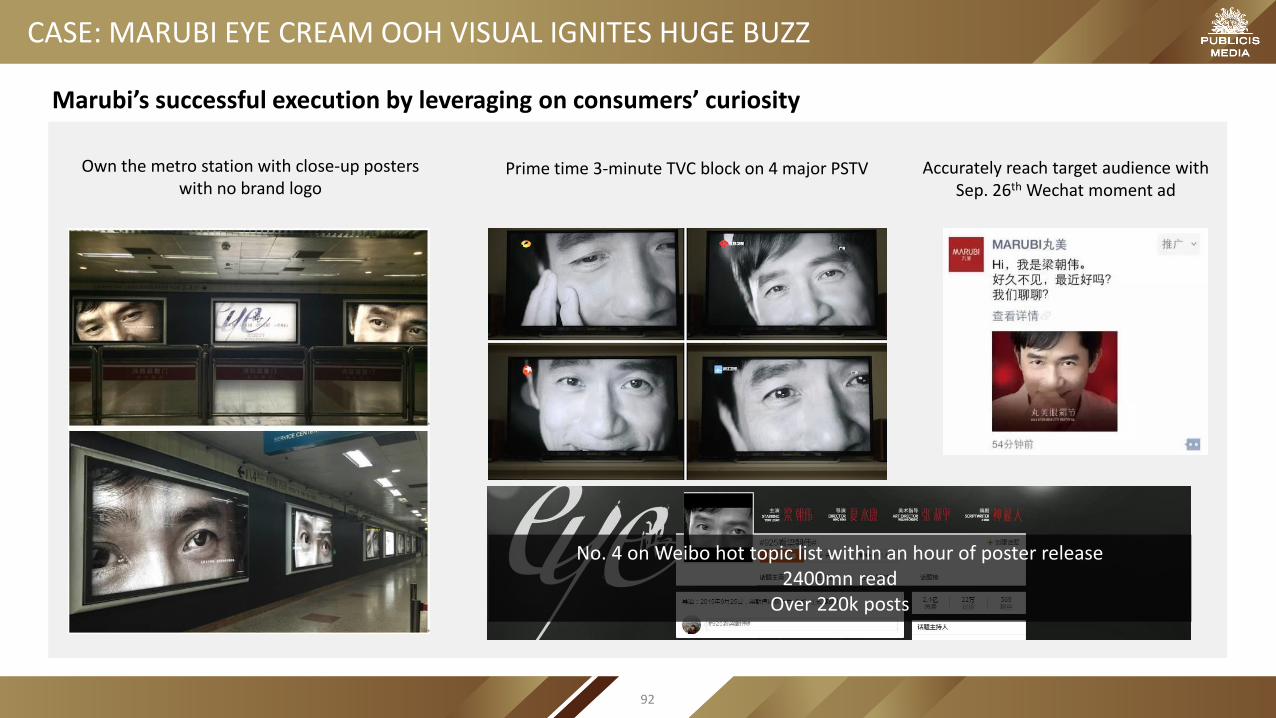

CASE: MARUBI EYE CREAM OOH VISUAL IGNITES HUGE BUZZ

Prime time 3-minute TVC block on 4 major PSTV

Marubi’s successful execution by leveraging on consumers’ curiosity

Own the metro station with close-up posters with no brand logo

Accurately reach target audience with Sep. 26th Wechat moment ad

No. 4 on Weibo hot topic list within an hour of poster release2400mn read

Over 220k posts

92

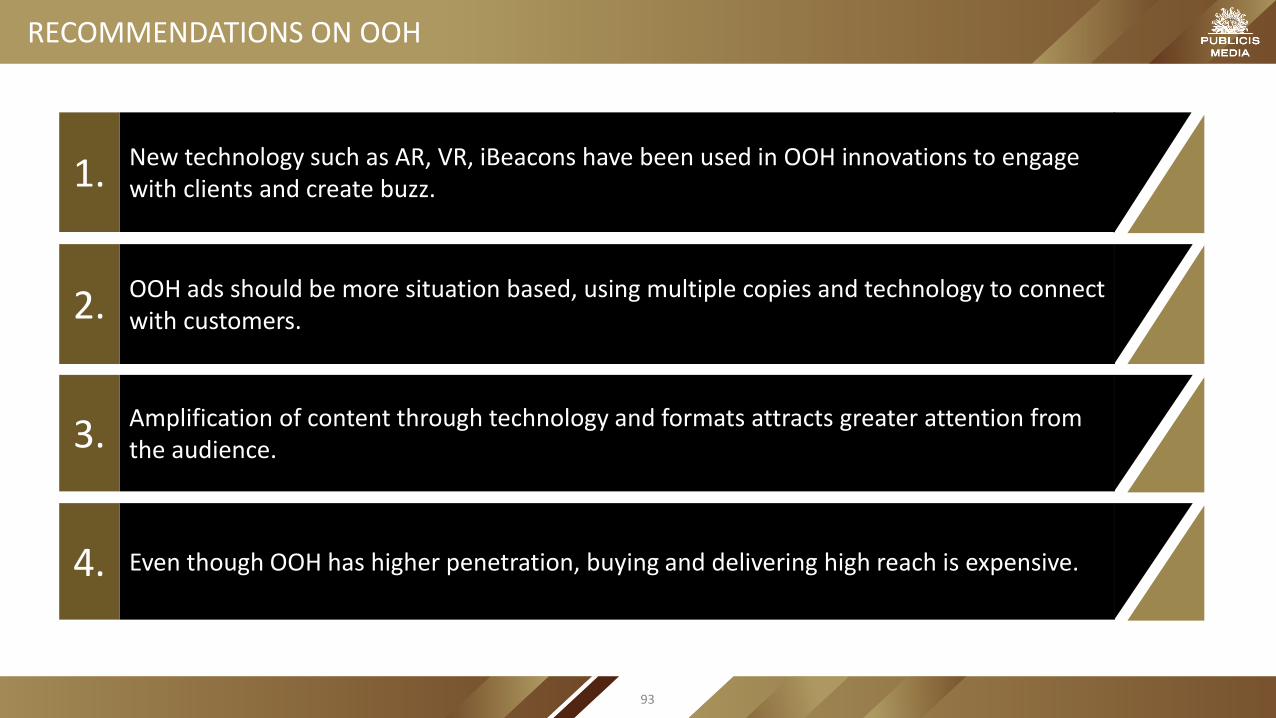

New technology such as AR, VR, iBeacons have been used in OOH innovations to engage with clients and create buzz. 1.

OOH ads should be more situation based, using multiple copies and technology to connect with customers.2.

Even though OOH has higher penetration, buying and delivering high reach is expensive.4.

RECOMMENDATIONS ON OOH

Amplification of content through technology and formats attracts greater attention from the audience. 3.

93

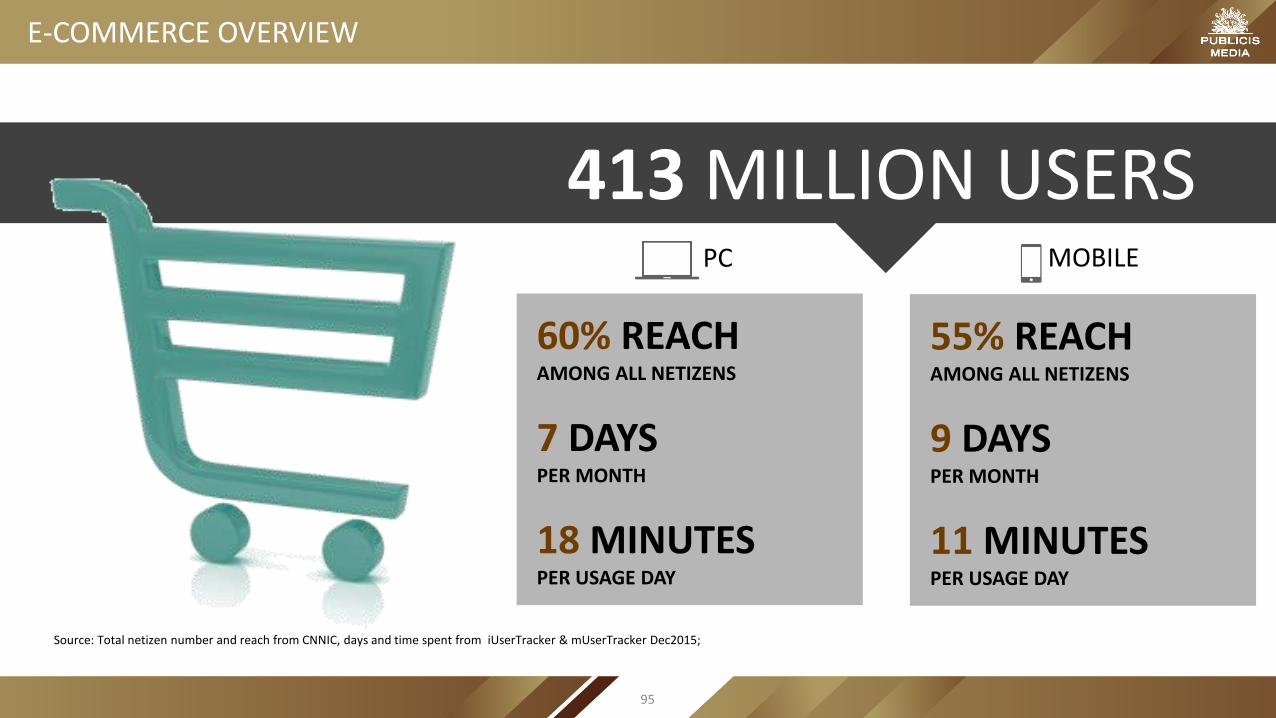

E-COMMERCE

413 MILLION USERS

60% REACH AMONG ALL NETIZENS

7 DAYS PER MONTH

18 MINUTESPER USAGE DAY

PC MOBILE

55% REACH AMONG ALL NETIZENS

9 DAYS PER MONTH

11 MINUTESPER USAGE DAY

E-COMMERCE OVERVIEW

Source: Total netizen number and reach from CNNIC, days and time spent from iUserTracker & mUserTracker Dec2015;

95

61%17%

8%

3%

Taobao

Tmall

JD.com

VIP.com

Suning

Meituan (GB)

Dangdang

Yhd.com

Amazon

Others

-1%

+2%

Source: iUserTracker & mUserTracker Dec,2015

64%7%

6%

4%

3%2%1%

Taobao

Meituan (GB)

Jindong

Tmall

VIP

Mogujie

Meilishuo

Jumei

Juhuasuan (GB)

Nuomi (GB)

Others

PCMOBILE

-1%

TOP EC PLATFORMS ACROSS DEVICES

SHARE OF TIME SPENT ON EC

-1%

+3%

Alibaba drives growth with increased share on mobile

96

B2C VS. C2C

Source: Analysys Report, Q4, 2015

B2C takes up more than half share of all transactions, dominated by TMALL and JD

25.8%36.1%

41.9%47.8% 52.5%

74.2%63.9%

58.1%52.2% 47.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015

ONLINE SHOPPING MARKET - B2C VS. C2C BY TOTAL TRANSACTIONS

B2C C2C

63.5%

20.8%

2.6%2.5%

1.5%

0.9%

0.8%0.8%

MARKET SHARE OF TOP B2C PALYERS BY TOTAL TRANSACTIONS

TMALL

JD.com

VIP.com

Suning.com

Gome.com.cn

Dangdang

yhd.com

Amazon.cn

Jumei.com

Others

97

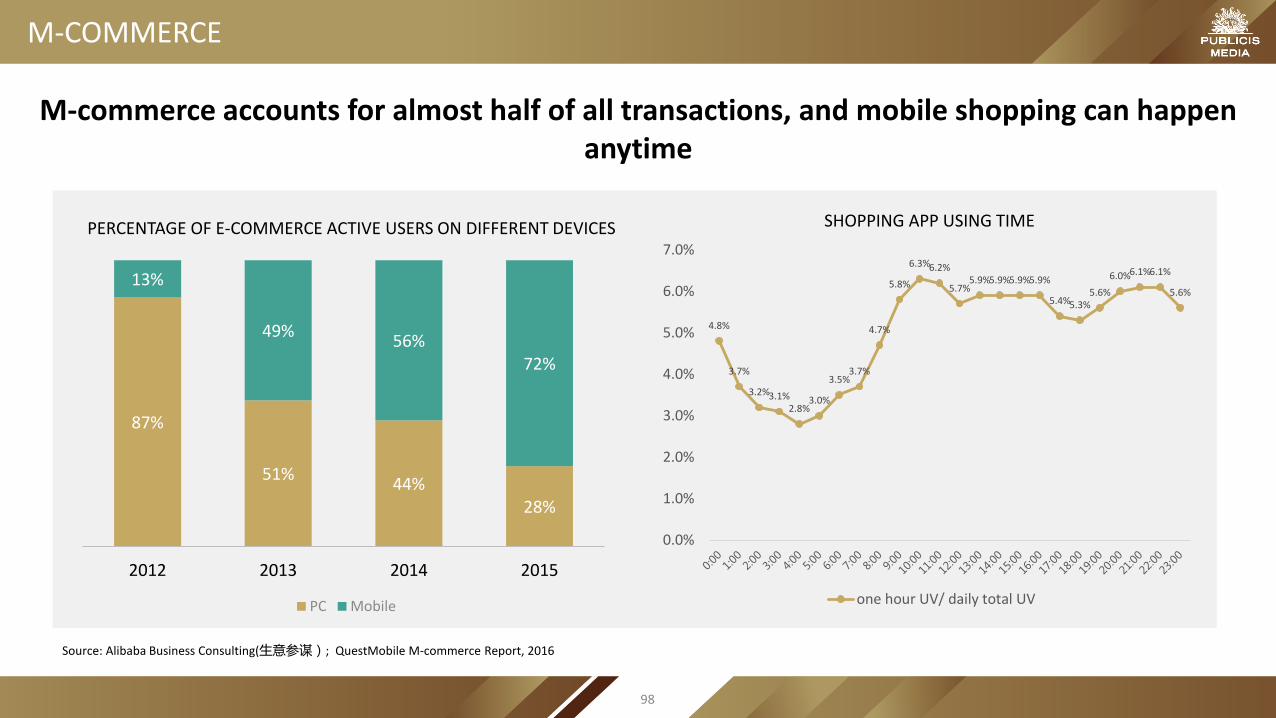

M-COMMERCE

Source: Alibaba Business Consulting(生意参谋); QuestMobile M-commerce Report, 2016

M-commerce accounts for almost half of all transactions, and mobile shopping can happen anytime

4.8%

3.7%

3.2%3.1%2.8%

3.0%

3.5%3.7%

4.7%

5.8%

6.3%6.2%

5.7%5.9%5.9%5.9%5.9%

5.4%5.3%5.6%

6.0%6.1%6.1%

5.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

SHOPPING APP USING TIME

one hour UV/ daily total UV

87%

51%44%

28%

13%

49%56%

72%

2012 2013 2014 2015

PC Mobile

PERCENTAGE OF E-COMMERCE ACTIVE USERS ON DIFFERENT DEVICES

98

CROSS-BORDER E-COMMERCE

In 2015, overseas purchase and cross-border e-commerce platform both launched a big promotion on Black Friday, with the aim of taking the market share before 11.11

56%54%

46%39%

28%27% 28%

0%

10%

20%

30%

40%

50%

60%

0

20

40

60

80

100

120

140

160

180

200

2012 2013 2014 2015 2016e 2017e 2018e

CHINA CROSS-BORDER E-COMMERCE TRANSACTION

Transcation YOY growth

Unit: Million RMB

Source: iResearch Report, March, 2016

Based on YangMatou’s data, during its Black Friday Promotion of 2015, it increased millions new users and 60% of them are the first time to do overseas purchase. The cost per customer transaction is more than 500 yuan, and the average cost of each

person is over 1500 yuan.

99

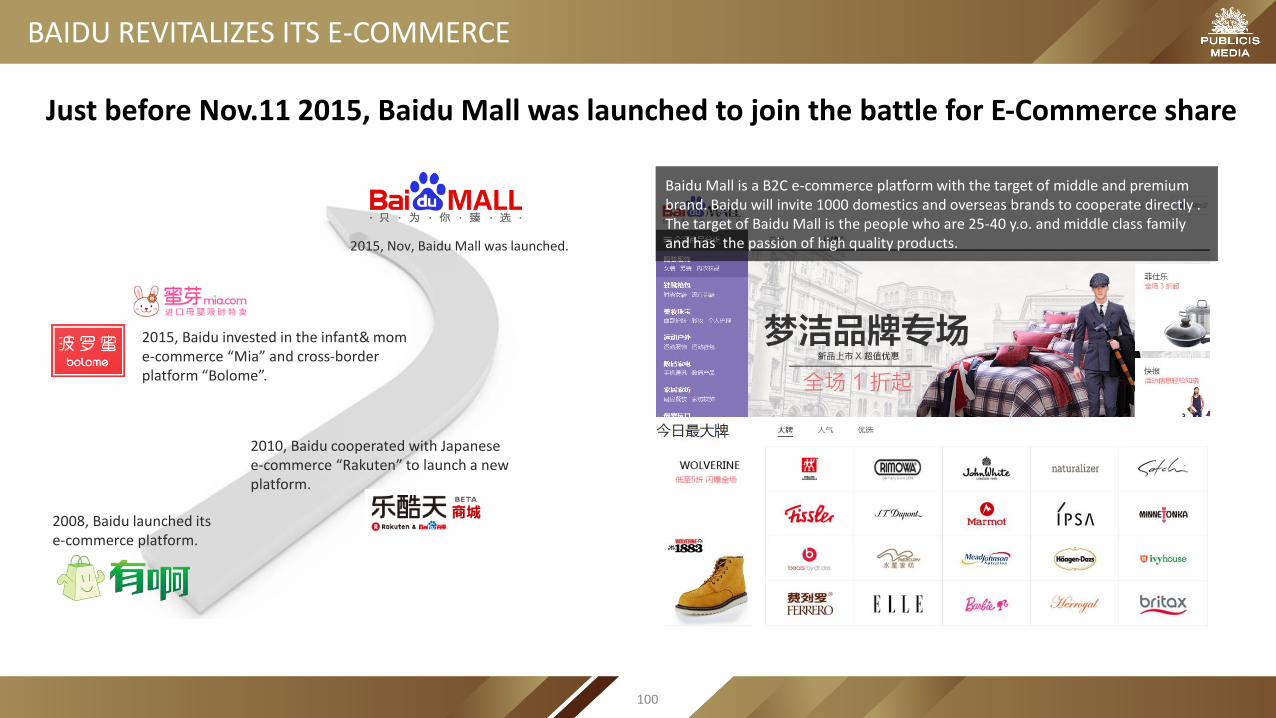

Baidu Mall is a B2C e-commerce platform with the target of middle and premium brand. Baidu will invite 1000 domestics and overseas brands to cooperate directly . The target of Baidu Mall is the people who are 25-40 y.o. and middle class family and has the passion of high quality products.

2008, Baidu launched its e-commerce platform.

2010, Baidu cooperated with Japanese e-commerce “Rakuten” to launch a new platform.

2015, Baidu invested in the infant& mom e-commerce “Mia” and cross-border platform “Bolome”.

2015, Nov, Baidu Mall was launched.

Just before Nov.11 2015, Baidu Mall was launched to join the battle for E-Commerce share

BAIDU REVITALIZES ITS E-COMMERCE

100

FORMATS & CASES

DOUBLE 11 GALA

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Rating

Hunan PSTV Zhejiang PSTV CCTV-1 CCTV-6

On the night of Nov 10th , the rating of Tmall gala is much higher than other programs, and is 2.5 times as much as that of Jingdong gala.

The 11.11 gala held by Tmall and Hunan PSTV went far beyond the previous ones. It combined TV and e-commence creating a new model of TV shopping and cross-screen interaction that allowed consumers to watch, play and buy at the

same time,

Consumers can attend interaction by shaking mobile and guessing and have a chance to win a “1 yuan” product.The total sales of double 11 is 91.2 billion. Mobile transaction accounts for 68% and one of the important reasons is the traffic from TV.

Data Source: Infosys 2015年11月10日数据;Target:P20-45;2000-2400;全国城市组

102

CASE: GO RURAL

In order to further expand the market, Tmall and JD executed significant marketing activities in rural areas

Heart wrenching series of posters and H5 story H5 game to win tickets home Two chartered trains to sent people home

103

Need to manage duplication and context as re-targeting technology allows targeting the same person behind various screens.1.

TV and OTV can drive traffic to E-commerce, therefore, should be planned together.2.

E-commerce can not only drives conversion, but can also help build band awareness and provide product information.3.

RECOMMENDATIONS ON E-COMMERCE

104

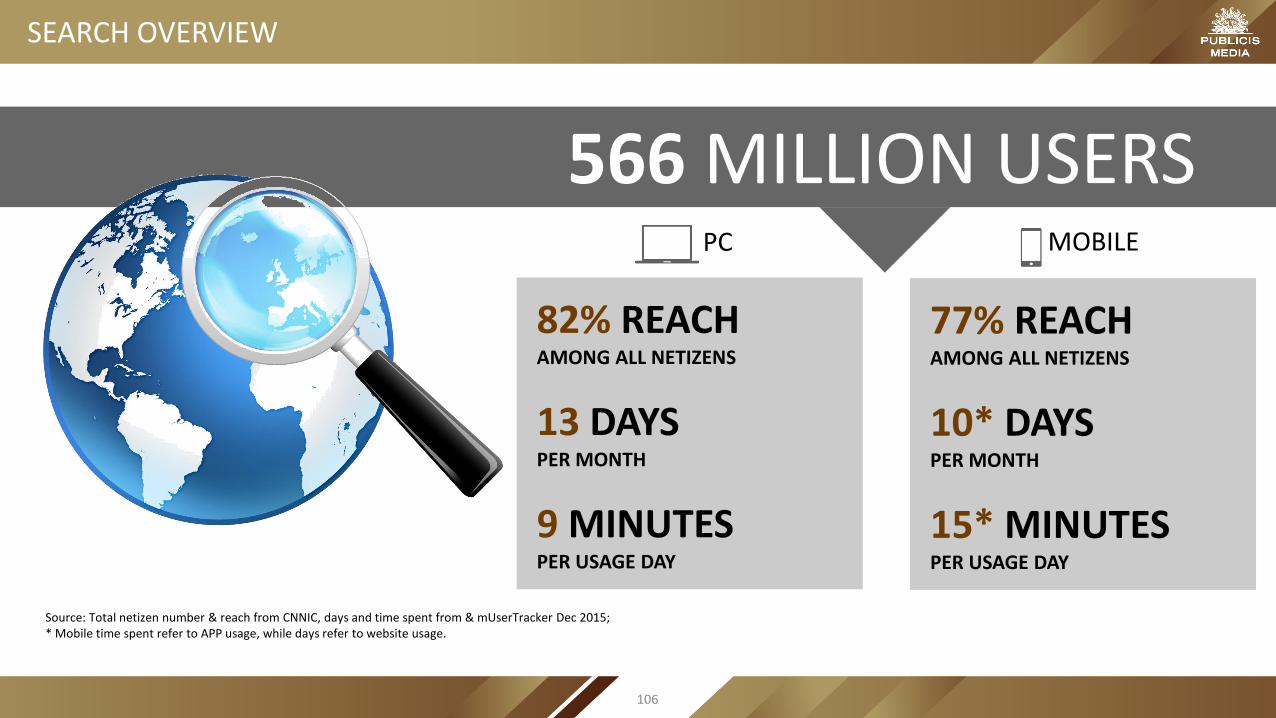

SEARCH

566 MILLION USERS

82% REACH AMONG ALL NETIZENS

13 DAYS PER MONTH

9 MINUTESPER USAGE DAY

PC MOBILE

77% REACH AMONG ALL NETIZENS

10* DAYSPER MONTH

15* MINUTESPER USAGE DAY

Source: Total netizen number & reach from CNNIC, days and time spent from & mUserTracker Dec 2015;* Mobile time spent refer to APP usage, while days refer to website usage.

SEARCH OVERVIEW

106

SEARCH RANKING BY PAGE VIEWS

0%

-4%

-3%

-1%

-32%

Source: iUsertracker & mUsertracker Jan-Dec, but Shenma is not well tracked according to the market share published by CNZZ, Mar 2015Note: PVs are within iResearch panel geography, scale may not be representative of the total online population

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-15

Sep

-15

Oct

-15

No

v-15

Dec

-15

PV OF SEARCH ENGINE ON PC (Mil)

Baidu 360 Sogou Etao

Google Soku Bing

-10,000

-

10,000

20,000

30,000

40,000

50,000

60,000

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-15

Sep

-15

Oct

-15

No

v-15

Dec

-15

PV OF SEARCH ENGINE ON MOBILE (Mil)

Baidu Easou Sogou Etao Bing

+27%

Usage of 360 search continues to grow in PV, though still dwarfed by Baidu’s dominant share of search. In mobile, Sogou surpassed Easou to be the No 2 search engine

Change in Reach

Change in Reach

Baidu, 80%

Shenma*, 13%

Sogou, 6%

MARKET SHARE OF MOBILE SEARCH

107

PC & MOBILE DIFFERENCES CROSS TIME

0 1 2 3 4 5 6 7 8 9 1 0 1 1 1 2 1 3 1 4 1 5 1 6 1 7 1 8 1 9 2 0 2 1 2 2 2 3

Monday

Tuesday

Wednesday

ThursdayFriday

Saturday

Sunday

PC MOBILE

Source: Baidu Tanxing Jul 2015

PC dominates working time (day and week days) while mobile spikes up during ‘me’ time (night and weekends)

PC VS. MOBILE SEARCH CROSS THE DAY

PCMOBILE

PC VS. MOBILE SEARCH CROSS THE WEEK

108

Trend

Queries will increasingly become more conversational and precise with specific questions.

Conversational questions will expect conversational answers, inviting new styles of copywriting.

Implications for brands

For brands, it will imply a clear identification of the question and connecting it to precise and to the point results, in order to avoid frustration

It will also require the creation of assets that can be read out loud by AI assistants, making AI compatible assets a crucial part of the content production expertise.

Better

Voice vs. key in10 times faster

Can hear and understand your needs

With better communication

Always improving user experience

Faster

Smarter

50% MILLENNIALS and 100% POST 90’Shave used voice search

VOICE SEARCH WILL TRANSFORM THE WAY BRANDS RESPOND

109

FORMATS & CASES

CASE: L’OREAL PLAY WITH BRAND ZONE

• Search the key word “玻尿酸”or “范冰冰”, an creative animation will pop up;• Adopt the customized floating ads and tailor-made brand zone to demonstrate the news product.

Version 1 Version 2

L'Oréal worked with Baidu mobile platform with a creative animation appearing when certain key words are searched

111

1.

2.

3.

4.

RECOMMENDATIONS ON SEARCH

360 is threatening Baidu’s dominance with the second largest market share on PC. Baidu still secures its absolute leading position when combined with their mobile search offering.

Baidu releases a very robust voice search functionality, efficiency and ease of voice based searching means this is expected to gain popularity very quickly.

Shema gaining popularity on mobile. This is Alibaba’s mobile search engine and particularly important for ecommerce players.

Baidu increasingly offers highly tailored, interactive and rich advertising formats to advertisers.

112

PROGRAMMATIC BUYING

PROGRAMMATIC INVESTMENT USA VS. CHINA

3%

8%

15%

23%

29%

35%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

0

5

10

15

20

25

30

35

40

45

50

2013 2014 2015 2016e 2017e 2018e

PROGRAMMATIC DISPLAY INVESTMENT IN CHINA

Programmatic digital display ad spending

% of total China digital display ad spending

10.32

15.43

21.55

26.78

49%

59%

67%72%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

5

10

15

20

25

30

2014 2015e 2016e 2017e

PROGRAMMATIC DISPLAY INVESTMENT IN USA

Programmatic digital display ad spending

% of total US digital display ad spending

China witnesses a rapid growth in programmatic investment however way behind USA

Source: USA data from eMarketer, Oct 2015O; China data from iResearch Report, Mar 2016.

Unit: Billion (USD) Unit: Billion (RMB)

114

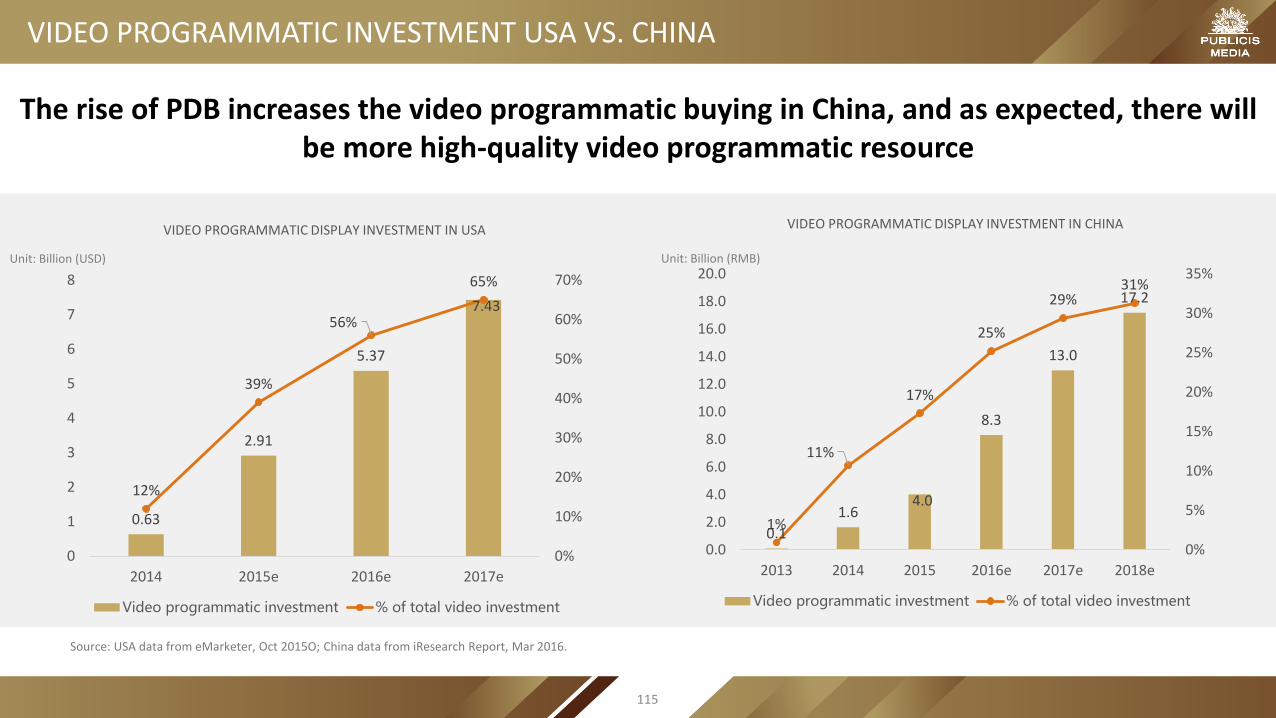

VIDEO PROGRAMMATIC INVESTMENT USA VS. CHINA

0.63

2.91

5.37

7.43

12%

39%

56%

65%

0%

10%

20%

30%

40%

50%

60%

70%

0

1

2

3

4

5

6

7

8

2014 2015e 2016e 2017e

VIDEO PROGRAMMATIC DISPLAY INVESTMENT IN USA

Video programmatic investment % of total video investment

0.1

1.64.0

8.3

13.0

17.2

1%

11%

17%

25%

29%31%

0%

5%

10%

15%

20%

25%

30%

35%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2013 2014 2015 2016e 2017e 2018e

VIDEO PROGRAMMATIC DISPLAY INVESTMENT IN CHINA

Video programmatic investment % of total video investment

The rise of PDB increases the video programmatic buying in China, and as expected, there will be more high-quality video programmatic resource

Source: USA data from eMarketer, Oct 2015O; China data from iResearch Report, Mar 2016.

Unit: Billion (USD) Unit: Billion (RMB)

115

CHINA MOBILE PROGRAMMATIC INVESTMENT

China saw a huge growth of mobile programmatic buying, and mobile resource has tripled in the RTB market

5% 8%29%

40%47%

54%

100% 95% 92%

71%60%

53%47%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016e 2017e 2018e

2012-2018 CHINA PROGRAMMATIC INVESTMENT IN DIFFERENT DEVICES

MOBILE PC

PC Mobile

2014-2015 CHINA PROGRAMMATIC SOURCE

2014 2015

~80bn PV/day

~10bn PV/day

~1bn PV/day

~3bn PV/day

Source: iResearch Report, March, 2016

116

SEMANTIC TARGETING

• The semantic targeting strategy could better reach audience with recent purchase intention and influence their consumption. It is suitable for advertiser’s on-hand promotion.

• The conventional DSP + semantic targeting strategy is suitable for the campaign during holidays and special media environment. It could improve the ads efficiency and help brands stand out from the exploding ads.

Semantic targeting better reach audience with recent purchase intension

Conventional DSP reached more TA with demographic labels

45 41

3458

Converional DSP Semantic Targeting

When do you plan to go to the market?

in a week in 1-2 days

+20%

98%

2%

Conventional DSP

TA Non-TA

75%

25%

Semantic DSP

TA Non-TA

Source: VivaKi 2015 Programmatic Ads Research White Paper

117

CONSUMPTION TARGETING

• The consumption targeting strategy could effectively grab audiences with special consumption characteristics and make up for the conventional DSP targeting’s weakness on premium consumer targeting.

• The consumption targeting strategy is suitable for luxury goods, automobiles, and other premium categories that require participation of high consumption level audiences. It will effectively improve conversion rate of premium brand’s campaign.

Consumption Targeting Largely Improved the Campaign Efficiency

KPI Actual

CPC

in a week

-18%

Source: VivaKi 2015 Programmatic Ads Research White Paper

Leads

X4 times than planned

DMP

DSP

Conduct special group from multiple data sources:• Live in 5-stars hotel• Bought premium brand• ……

Deliver ads to TA:• Luxury consumers• Real estate consumers• ….

118

CONTEXTUAL TARGETING

• The contextual targeting strategy could effectively facilitate the conversion of the audiences who have positive attitude toward the brands.

• For new brand or new product, the campaign should focus on those who have positive brand impression to improve the brand preference and facilitate purchase conversion. For those matured brands, the campaign should on the one hand deliver promotion ads to those positive audiences. On the other hand, it will also deliver branding ads to those negative audiences to improve the brand images.

Trigger Ads on 2nd And 3rd Screens Based on TV Ads

Contextual Targeting Could Deliver Different Ads Based on the Social Buzz

Contextual Targeting Effectively Improved Audience’s Brand Image and Largely Increased the Brand Favorability

24%20%

28%

46%

35%

54%

44% 46% 48% 46%

BrandFavorability

PurchaseIntention

ComprehensiveComposition

Blanced Nutrition Professional

The Target Brand Index (%)

Control Contextual Targeting

Source: VivaKi 2015 Programmatic Ads Research White Paper

119

OTV PROGRAMMATIC BUYING:DSP+REGULAR BUY

• Comparing to regular buy, DSP can make better cross-platform frequency control and effectively utilize inventory to precisely reach TA.

• Supplying DSP ads on the basis of regular buy can take full advantage of UGC/PGC inventory. Combining DSP with regular buy as an integral solution will largely enhance TA accuracy, brand impression, and drive audience’s consumption.

• In terms of exposure environment, there can be 6-8 pre-rolls before the hero videos, which will largely distract audiences’ attention and memory. On the contrast, there are only 1-2 pre-rolls before the UGC/PGC. The exclusiveness will ensure the audience’s attention and long-term memory.

DSP Inventory Resulted in Higher Visual Attention and long-term memory

DSP+ Regular Buy Improved Brand Favorability & Purchase Intention

0.03 0.01

Regular Buy DSP

0.59 0.67

25.7 28.8

Emotion

Visual Attention

Long-term memory

Source: VivaKi 2015 Programmatic Ads Research White Paper

Control Regular Buy DSP only Combo

Brand Favorability

10%

Control Regular Buy DSP only Combo

Purchase Intention

30%

120

OTV PROGRAMMATIC BUYING:RTB+PDB

• PDB can target a large number of active audiences and achieve large coverage through premium inventory. RTB inventory can be more accurate and more flexible to reach TA. PDB + RTB strategy can effectively achieve frequency capping cross media, reduce the campaign cost, and effectively reach the target audiences.

• PDB + RTB strategy should be widely used in the video programmatic buying. Advertisers should allocate budget on PDB and RTB wisely based on campaign spending and goal.

PDB Could Reached Broader Group, while RTB more precisely reached the TA with Demographic Labels

Source: VivaKi 2015 Programmatic Ads Research White Paper

Inventory Pricing InventoryCost

Effeciency

PDB Reserved Fixed ☆☆☆ ☆

RTB Open Bidding ☆ ☆☆☆

34.3%24.4%

PMI over 5000 RMB:

Most likely to buy the brand:

27.5% 21.2%

RTB+ PDB Largely lifted the Brand Performance

(RTB) (PDB)

(PDB)(RTB)

Unaided Brand Awareness:

Purchase Intention:

Brand Recommendation:

7.6%

10.1%

8.9%

121

OTV PDB ADVANTAGES

Media Buying VivaKi Inventory ManagerSelected Inventory

Unselected Inventory

Client Platform

VivaKi DMP

Other Advertisers

Experienced top video

media negotiation

Competitive media price

under PUBLICIS Group

All PDB tech supported

Successfully served many

industry-leading clients

VivaKi DMP empower DSP to know more about the audience.

Returnable media has no extra charge.

Frequency Capping & High-Quality inventory to increase TA

coverage. With the help of VivaKi DMP data, AOD covers

potential target efficiently.

Inventory returnable model

122

0.8B

Daily active users

90%

Social market share

Cross screens

Unique technic

85%

Mobile socialmarket share

6B PV

Daily volume

Purchasing behavior, app behavior, ’like’

behavior、SNS search behavior

Blog, Weibo, album, video, shuoshuo,

wenwen

Birthday,Anniversary, gift,

LBS…

Gender, Age,location, education, profession, school…

OnlineBehavior

Data

ContentData

SituationData

DemographicData

Friends' Feed

Friend interactionFriends’ sharingFriends’ commentFriends’ game……

Relationship chain

Friend recommendation

SocialChannel

Targeting accurate TA by Tencent big data – Users’ real QQ personal information, location, Qzone blog content, QQ group etc..

Social Data System

SOCIAL DATA MAKING MORE POSSIBILITIES

123

THE IMPORTANCE OF VIEWABILITY

• Viewability is an important index besides regular KPIs to measure campaign performances. High viewability will directly improve the brand message delivery and campaign performance. On the contrary, low viewability will weaken the value of ads.

• Content that can drive audiences’ attention will have higher viewability. In addition to the optimization on technology and inventory, advertisers should further focus on improve the quality of the ads to better attract the audiences’ attention.

50% above1s

above2s

At least

of advertisement is seen

Display ads

Video ads

An Effective Advertising:

High Viewability ads could improved Brand image, especially the brand information delivery

35.3

19.1

13.9

20.9

29

44.4

28.4

22.2 21

33.3

Aided BrandAwareness

Online AdsAwareness

InformationDelivery

BrandFavorability

PurchaseIntention

Low Viewability High Viewability

60%

Source: VivaKi 2015 Programmatic Ads Research White Paper

124

FORMATS & CASES

FMCG CASE SHARING: CLOSED ECO FROM BRANDING TO PERFORMANCE

0.75%

53.4%

0.11%

Landing Rate 53.4%

Click Ads

Visit Site

Impression

Click

Visit

Conversion ROI 0.9

Challenge

• Build brand awareness- Maximize TA Reach (F25-45)

• Drive Quality traffic To Boost Conversion- Increase Online sales & Sample Redeem

Solution

• Arose TA Awareness in Tier 1 City• Boosting EC Sales National Wide

Result

• 2x More TA Accuracy to Internet Ave.

• 60%+ TA Improvement comparing with Regular Buy

• 1.6x Effective on EC Sales On Programmatic Retargeting &

Audience Targeting Brings appx. 1:0.9 ROI

Bounce Rate 75.2% Nearly ¼ viewed 2nd page

ROI Performance- An international cosmetics advertiser

126

An health product adviser

Challenge

• 4 different Landing Pages

• Find The Right People + Push The Right Message

Solution• Audience interest labels; based on four product lines, SEM search

Intention, Shop geo-targeting• Machine allocate budget by time/hours performance & Geo

performance • Various creative concepts in 1 product line to stimulate the landing

site engagements

Result

• CTR/clicks over achieved at both PC & Mobile; esp. Mobile CTR is

2x better than est.

• PC Engagement- Landing Rate

Is 1.25x better than Drama Buy

Is 1.5x better than Regular Buy

0.6%

0.3%

0.2%

AOD Direct Buy Drama Buy

CTR

60%

41%48%

AOD Direct Buy Drama Buy

Landing Rate

85%86%

85%

AOD Direct Buy Drama Buy

Bounce Rate

PHARMACEUTICAL CASE SHARING: FIND THE RIGHT PEOPLE + PUSH THE RIGHT MESSAGE

127

Besides performance and efficiency, inventory quality and media environment are also important criteria. Therefore, PDB+RTB is becoming the mainstream for programatic buy.1.

Each targeting method has its own strength. Careful selection or mix is required according to the communication purpose.2.

Social big data can be used to target certain TA, but be careful with privacy issue.3.

RECOMMENDATION ON PROGRAMATIC BUY

128

BERTILLA TEO PUBLICIS MEDIA GREATER CHINA CEO MYKIM CHIKLI PUBLICIS MEDIA GREATER CHINA COO