2015 european business travel barometer

24

1 EUROPEAN BUSINESS TRAVEL BAROMETER 24 th edition – January 2015 Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and acknowledgment of Groupe Concomitance in its role in the preparation of this report EUROPEAN BUSINESS TRAVEL BAROMETER EVP 2015 Prepared by Concomitance Group

-

Upload

philippe-greco -

Category

Travel

-

view

91 -

download

2

Transcript of 2015 european business travel barometer

1

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

EUROPEAN BUSINESS TRAVEL BAROMETER

EVP 2015

Prepared by Concomitance Group

2

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

Contents

Executive summary .................................................................................................... 3

Methodology of the barometer .................................................................................. 4

Part 1: Economic trends and travel budget developments ..................................... 5

2014, a year of recovery ...................................................................................................................... 5

The Business Travel market back to growth ....................................................................................... 5

Business development and International expansion in Europe as market drivers ............................. 6

Air and Hotel remain the major travel expense categories ................................................................ 8

Part 2: Controlling direct costs, companies’ priority #1 ......................................... 9

Costs remain companies’ 1st concern .................................................................................................. 9

Best-buy and Online booking to control direct costs ........................................................................ 10

Part 3: Getting a complete view of expenses integrating indirect costs as companies’ next step ............................................................................................. 14

The raising issue of indirect costs ...................................................................................................... 14

Monitoring and controlling indirect costs ......................................................................................... 15

This generates new expectations towards travel agencies ............................................................... 17

Part 4: what about the traveler experience in the cost-focused context? ........... 19

Traveler security and safety, companies’ priority #2 ........................................................................ 19

Despite speeches, travelers’ level of satisfaction is little taken into account ................................... 20

The exception of the VIP traveler: towards a two-speed treatment of travelers? ........................... 22

Part 5: Forecasts 2015 .............................................................................................. 23

3

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

Executive summary

The Business Travel market back to growth

• In a context of slight recovery (overall GDP growth of +1,3% for the countries in the barometer scope) and after several years of continuously decreasing growth rates, the Business Travel market finally shows some recovery to achieve a +0,9% growth rate (vs. +0,5% in 2013).

• Business development, especially with the objective to acquire new clients/markets, and companies’ operations in Europe are the two main drivers of growth.

• This trend still needs to be confirmed in 2015, even if the international development seems to be a long-term trend.

Controlling costs is still companies’ priority #1

• Controlling costs refers to both containing and monitoring expenses. • To contain travel expenses, companies use 2 main and complementary tools: best-

buy practices (1st lever used to optimize travel budget) and corporate Online Booking Tool (current rate of OBT equipment reaches 66% vs. 50% in 2013). As a result of their previous efforts, more and more companies think that they have achieved the best expense optimization that they can achieve: nearly half of them declare that they cannot better optimize their travel expenses than what is done today.

• As for monitoring expenses, specific procedures to follow up expenditures have spread (90% of companies say they have implemented such procedures) but they still need to be automated as 78% of companies still have manual processes. In this context, companies are turning today to end-to-end solutions (OBT + Expense Management) and want to extend them to mobile tomorrow.

• This should enable them to get a complete view of expenses (companies’ priority #3 for the 3 coming years), contain indirect costs of their travel program and better integrate new suppliers such as C2C (Consumer-to-Consumer) suppliers or new kind of lodging suppliers.

• In this context, companies ask their travel agency to help them face these changes. Indeed as travel agencies are experts in the use of all these levers, they have a critical role to play in assisting companies in this transition.

Towards a 2-speed treatment of travelers?

• The level of satisfaction of travelers is still little taken into account: only 20% of companies measure it in order to bring changes to the company’s travel policy, and another 25% measure it but with no impact. Traveler’s satisfaction even declines in the ranking of companies’ travel management priorities, now listed as the 6th priority vs. 4th last year.

• On the other hand, the concept of VIP travelers seems to develop as 20% companies now purchase VIP services (vs. 12% in 2013).

• However, whoever the traveler is, he now travels in strengthened security conditions: never have so many companies taken so many measures to improve traveler safety and security. It will remain an important concern for companies which rank it as priority #2 for the next 3 years.

4

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

Methodology of the barometer

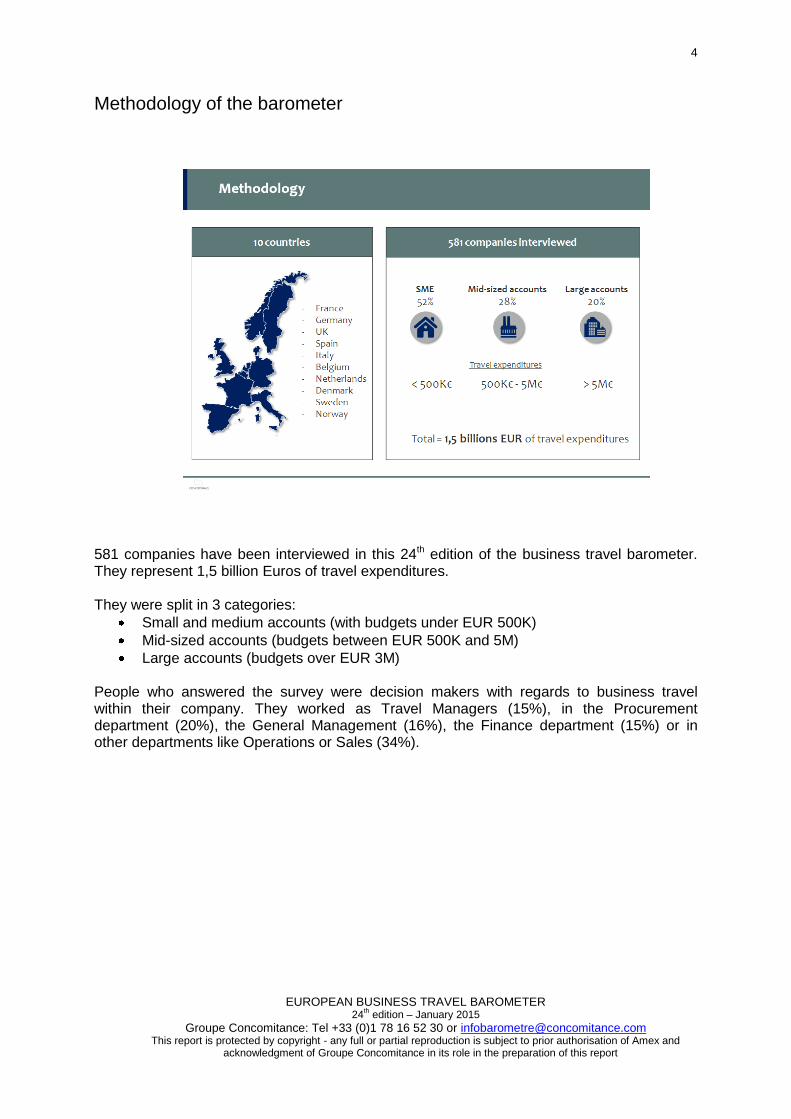

581 companies have been interviewed in this 24th edition of the business travel barometer. They represent 1,5 billion Euros of travel expenditures. They were split in 3 categories:

Small and medium accounts (with budgets under EUR 500K)

Mid-sized accounts (budgets between EUR 500K and 5M)

Large accounts (budgets over EUR 3M) People who answered the survey were decision makers with regards to business travel within their company. They worked as Travel Managers (15%), in the Procurement department (20%), the General Management (16%), the Finance department (15%) or in other departments like Operations or Sales (34%).

5

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

Part 1: Economic trends and travel budget developments

2014, a year of recovery As expected, 2014 was a better year for many economies: except Italy, all countries in the EVP scope enjoyed some recovery. Overall, the growth of the countries in the EVP scope reaches +1,3% (vs. +0,2% in 2013). Still, some disparities exist between Northern Europe and Benelux/France/Southern Europe. The United Kingdom, Sweden, Norway and Denmark are especially driving the growth within EVP countries, with GDP increases of respectively +3,2%, +2,1%, +1,8% and +1,4%. On the other hand, Belgium, the Netherlands and France hardly reach +1,0%, +0,6%, +0,4% of growth. Besides, Italy is still in recession (-0,2%) despite some improvement. The United States and China are still outdistancing the zone with respective GDP growths of +2,2% and +7,4%.

The Business Travel market back to growth After 2 years of lower and lower growth rates, the Business Travel market finally reveals an upturn: business travel expenditures grew by +0,9% in 2014. This increase is in line with the growth forecasted by companies during the 2013 barometer (growth estimated at 0,8%). Mid-sized accounts are driving the growth (+2,2%) whereas large accounts suffered a -0,9% decrease.

6

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

As a result, the market growth is slightly lower than that of GDP. This is often the case during recovery periods as the GDP and the Business Travel market growth are correlated with a small time difference – when GDP comes back to growth, a positive impact is seen on the travel market in the following year. Besides, 1 point of growth corresponds to almost 2 billion Euros at the scope of the barometer.

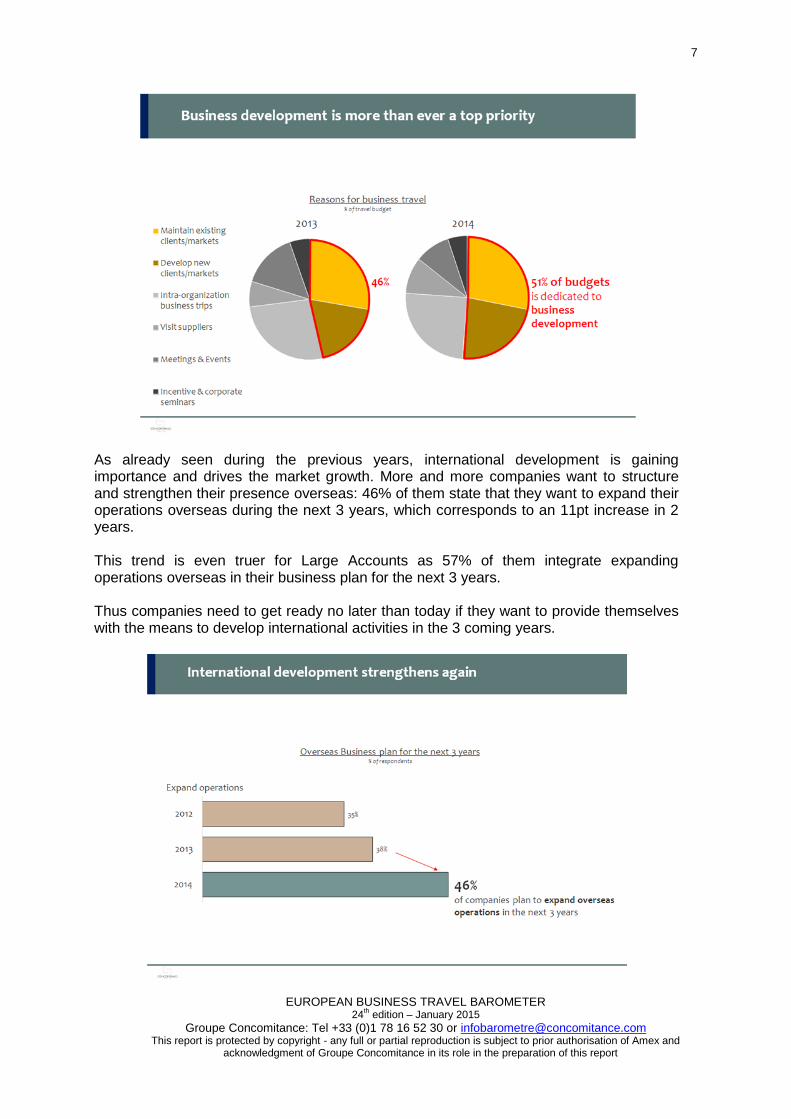

Business development and International expansion in Europe as market drivers Business development is mentioned as the first reason for travel budget increase. It now represents 51% of travel budget while it was 46% in 2013. In other words, on 10€ spent for business travel, 5€ is spent in business development. This 5-point increase is equivalent to around 9 billion Euros at the barometer scope. Developing new clients/markets especially drives business development, reaching 23% of companies’ travel budget in 2014 (+4pt vs. 2013) while maintaining existing clients/ markets remains stable at 28% of the travel budget. On the other hand, the share of companies’ travel budget dedicated to Meetings & Events was reduced. As a comparison, this business dynamism in the European EVP scope is similar to the one observed on the Chinese market, which has historically been focused on business development and which should become the 1st business travel market worldwide in 2016.

7

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

As already seen during the previous years, international development is gaining importance and drives the market growth. More and more companies want to structure and strengthen their presence overseas: 46% of them state that they want to expand their operations overseas during the next 3 years, which corresponds to an 11pt increase in 2 years. This trend is even truer for Large Accounts as 57% of them integrate expanding operations overseas in their business plan for the next 3 years. Thus companies need to get ready no later than today if they want to provide themselves with the means to develop international activities in the 3 coming years.

8

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

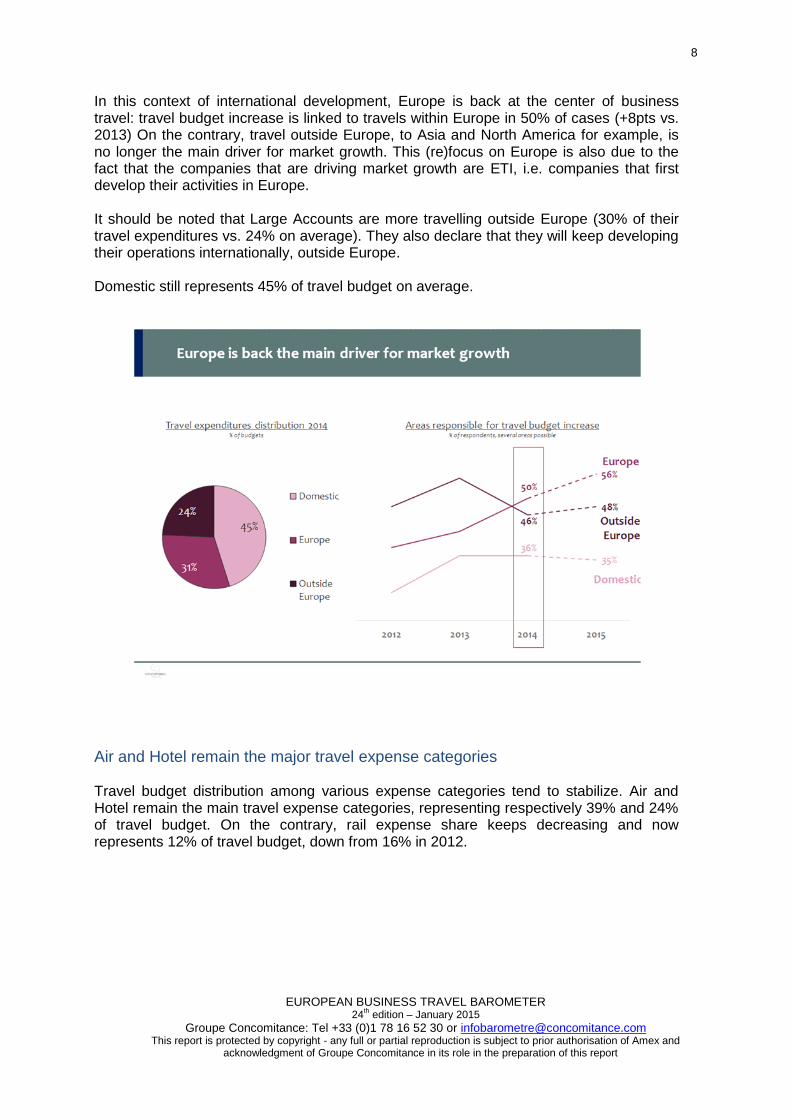

In this context of international development, Europe is back at the center of business travel: travel budget increase is linked to travels within Europe in 50% of cases (+8pts vs. 2013) On the contrary, travel outside Europe, to Asia and North America for example, is no longer the main driver for market growth. This (re)focus on Europe is also due to the fact that the companies that are driving market growth are ETI, i.e. companies that first develop their activities in Europe. It should be noted that Large Accounts are more travelling outside Europe (30% of their travel expenditures vs. 24% on average). They also declare that they will keep developing their operations internationally, outside Europe. Domestic still represents 45% of travel budget on average.

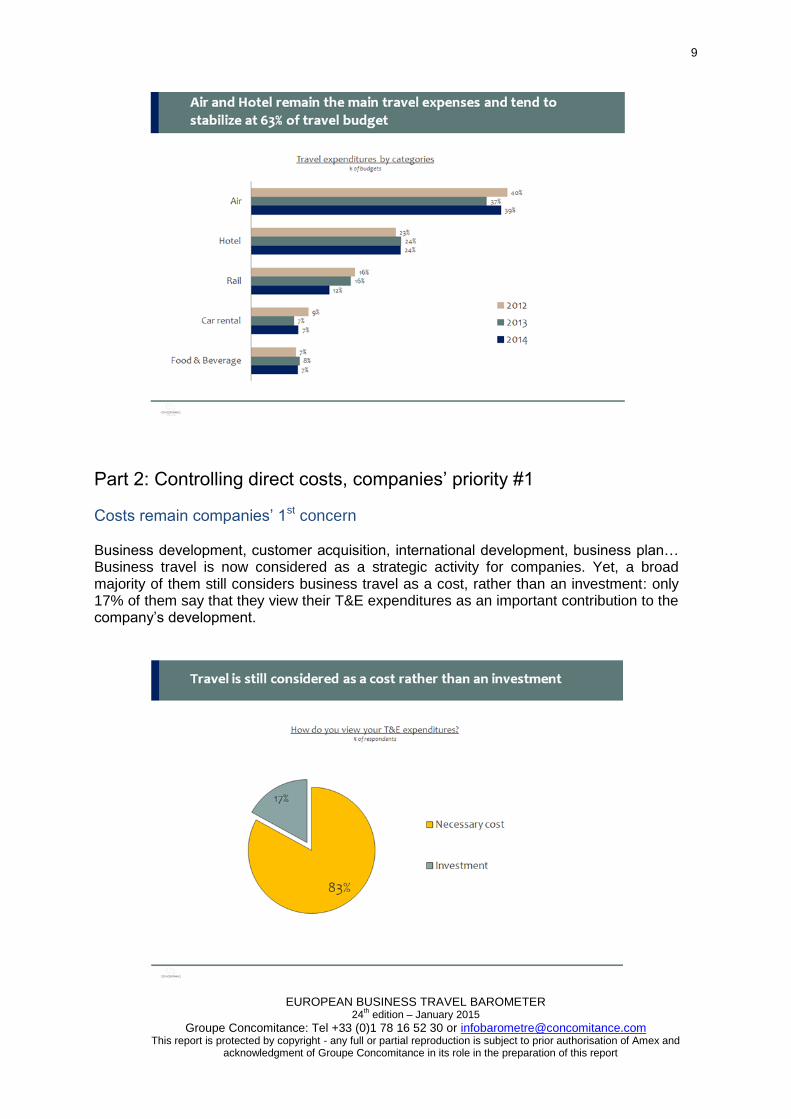

Air and Hotel remain the major travel expense categories Travel budget distribution among various expense categories tend to stabilize. Air and Hotel remain the main travel expense categories, representing respectively 39% and 24% of travel budget. On the contrary, rail expense share keeps decreasing and now represents 12% of travel budget, down from 16% in 2012.

9

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

Part 2: Controlling direct costs, companies’ priority #1

Costs remain companies’ 1st concern Business development, customer acquisition, international development, business plan… Business travel is now considered as a strategic activity for companies. Yet, a broad majority of them still considers business travel as a cost, rather than an investment: only 17% of them say that they view their T&E expenditures as an important contribution to the company’s development.

10

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

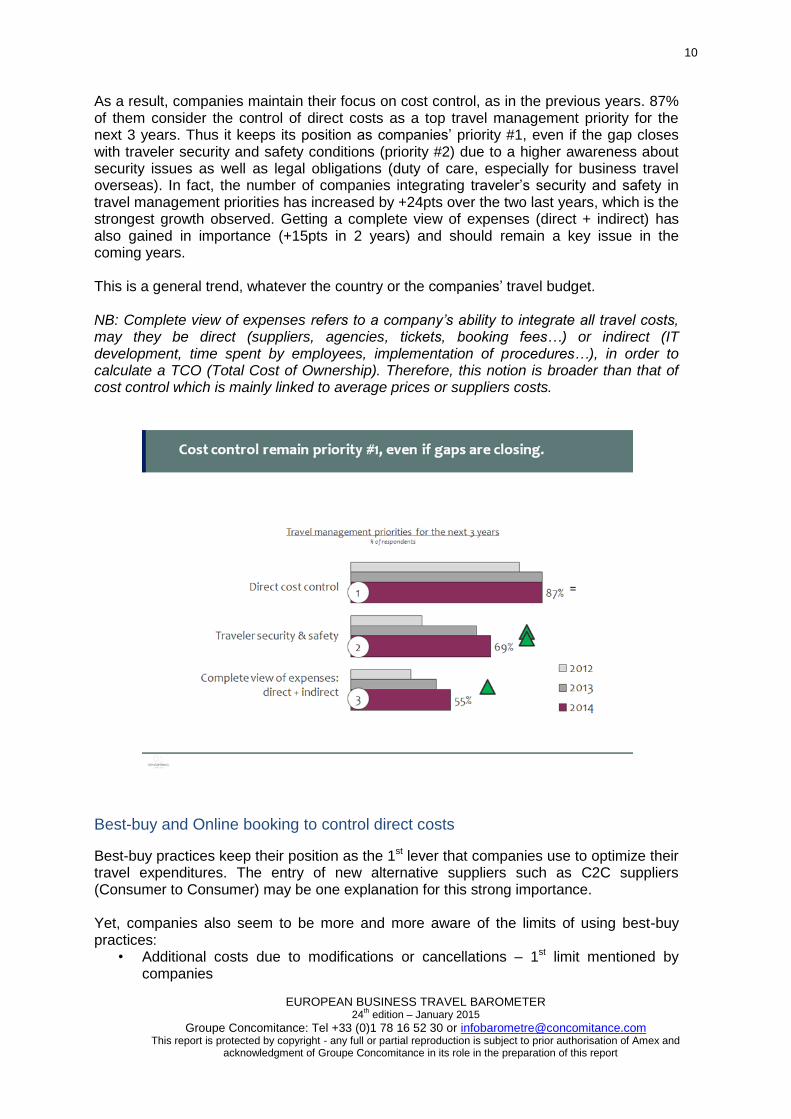

As a result, companies maintain their focus on cost control, as in the previous years. 87% of them consider the control of direct costs as a top travel management priority for the next 3 years. Thus it keeps its position as companies’ priority #1, even if the gap closes with traveler security and safety conditions (priority #2) due to a higher awareness about security issues as well as legal obligations (duty of care, especially for business travel overseas). In fact, the number of companies integrating traveler’s security and safety in travel management priorities has increased by +24pts over the two last years, which is the strongest growth observed. Getting a complete view of expenses (direct + indirect) has also gained in importance (+15pts in 2 years) and should remain a key issue in the coming years. This is a general trend, whatever the country or the companies’ travel budget. NB: Complete view of expenses refers to a company’s ability to integrate all travel costs, may they be direct (suppliers, agencies, tickets, booking fees…) or indirect (IT development, time spent by employees, implementation of procedures…), in order to calculate a TCO (Total Cost of Ownership). Therefore, this notion is broader than that of cost control which is mainly linked to average prices or suppliers costs.

Best-buy and Online booking to control direct costs

Best-buy practices keep their position as the 1st lever that companies use to optimize their travel expenditures. The entry of new alternative suppliers such as C2C suppliers (Consumer to Consumer) may be one explanation for this strong importance. Yet, companies also seem to be more and more aware of the limits of using best-buy practices:

• Additional costs due to modifications or cancellations – 1st limit mentioned by companies

11

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

• Lower back margins or other factors which can contribute to optimize companies’ travel budget indirectly or at the time of expense consolidation

• Limitation of bargaining power due to reduction of corporate rate volumes • Decline of traveler’s comfort and efficiency

As a result, the “best-buy” tends to be slightly less used as a lever to optimize travel expenditures while online booking and advanced booking are back on the list of attractive levers. Indeed, these levers have two main benefits: immediate savings and no side effect.

Besides best-buy practices, the adoption of Corporate Online Booking Tools (OBT) is increasing continuously and quickly. 66% of companies are now equipped with an OBT. This represents an increase by +16pts vs. 2013, that is to say twice as much as the increase observed between 2012 and 2013 (+8pts). Thus there is a strong acceleration of the adoption of OBTs within organizations. However, even if this may seem to be already a high equipment rate, there is still room for a higher penetration: in the US, more than 85% of companies are equipped with an OBT today. Using an OBT has two impacts on costs:

• Reduction in booking fees • Direct cost savings on travel expenses • A better travel policy compliance due to the tool configuration, guilt feelings…

Moreover, companies are not only better equipped, but they have also increased the usage of their OBT, using it for more and more bookings. 2/3 of them make almost all their bookings through their OBT. They were only 50% in 2013.

12

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

As a result, the compliance rate for the travel and expenditure policy has kept increasing for several years: 8 companies out of 10 report that their compliance rate is higher than 70%. It was only 6 out of 10 in 2012.

Besides policy compliance, companies also admit that the implementation of an OBT enabled them to make savings on their travel expenses (at constant volume). 87% of them report at least some savings and more than 1 company out of 2 speak about significant savings (higher than 10%). Large Accounts seem to have a better understanding of how they can optimize their expenses through an OBT: 75% of them report significant savings (higher than 10%). These cost savings come both from savings on booking fees (online vs. offline) and from supplier direct costs (better application of corporate rates and/or best-buy instructions). As a reminder, supplier costs account for around 95% of direct travel costs.

13

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

As a result, more and more companies declare that they cannot better optimize their current expenses: 47% of them say they do not have any more opportunities to further optimize their travel budget. Among these 47%, a large majority (76%) explain it by the fact that they have done all potential savings – only few of them (13%) declare they want to find a right balance between traveler comfort and expense optimization. The control of travel expenses comes along with the necessity to better control the chain overall, and thus to implement appropriate monitoring procedures.

14

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

Part 3: Getting a complete view of expenses integrating indirect costs as companies’ next step

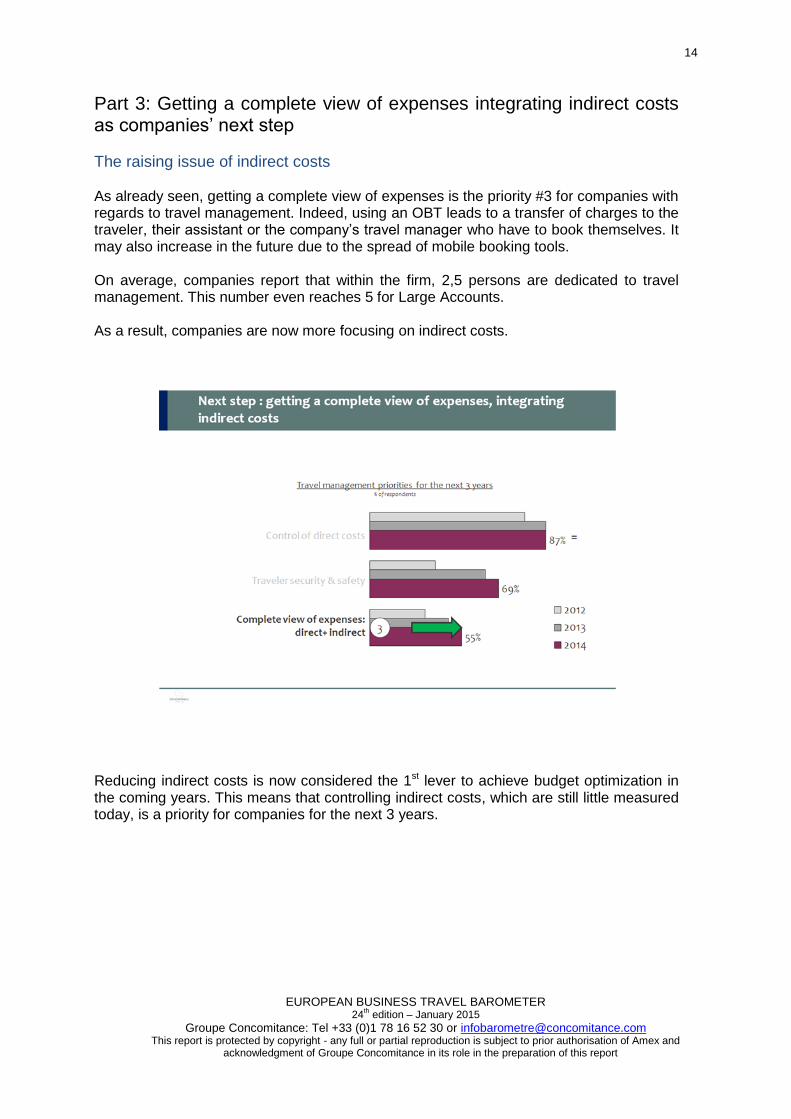

The raising issue of indirect costs As already seen, getting a complete view of expenses is the priority #3 for companies with regards to travel management. Indeed, using an OBT leads to a transfer of charges to the traveler, their assistant or the company’s travel manager who have to book themselves. It may also increase in the future due to the spread of mobile booking tools. On average, companies report that within the firm, 2,5 persons are dedicated to travel management. This number even reaches 5 for Large Accounts. As a result, companies are now more focusing on indirect costs.

Reducing indirect costs is now considered the 1st lever to achieve budget optimization in the coming years. This means that controlling indirect costs, which are still little measured today, is a priority for companies for the next 3 years.

15

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

Monitoring and controlling indirect costs To be able to monitor their expenses, more and more companies have implemented procedures dedicated to expenses follow-up. 90% of them declare they have procedures to monitor and control travel expenses. It was 80% in 2012. Procedures refer here to a structured and formalized set of rules dedicated to the monitoring and control of travel expenses, such as pre-trip approval request workflow, post-trip approval of expenses, specific reporting… This spread of monitoring and control procedures is noticeable in all European countries and for all travel budget size. Yet, these procedures are still mainly manual and 8 companies out of 10 still have procedures which are partially or even fully manual. Thus the necessity to equip with end-to-end solutions seems to be all the more urgent for them.

16

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

As a result, companies are turning to corporate end-to-end solutions. The dual equipment has kept increasing for several years to reach 43% of organizations in 2014. This growth even speeded up in the last year: +5pts between 2012 and 2013, +17pts between 2013 and 2014. Large Accounts lead the trend, with a level of dual equipment reaching 64%. Companies’ motives are clearly linked to the wish to control the complete program, hence not only to reduce costs. As a result of this dual equipment, the automation of the procedures has increased (22% of companies declare they have a 100% automated value chain vs. 15% in 2013), and has enabled them to reduce:

• Error risks • Fraud risks • Time spent to control

17

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

This generates new expectations towards travel agencies As companies are confronted with more complexity when they chose solutions and suppliers, they turn to their TMC and request assistance to manage these transitions. 29% of companies would like to develop end-to-end solutions with their travel agency, 13% would like to develop the mobile as a real alternative channel and 13% are interested in integrating new kinds of suppliers (C2C suppliers, new lodging suppliers…) supported by travelers themselves. Beside this wish to fully integrate the program with end-to-end solutions or/and equipments, the measurement of the ROI of trips appears as a second trend. Indeed, as companies are more and more equipped with end-to-end or at least expense management solutions, they are more able to measure the real investment they make in business travel (thus, the “I” of the ROI of trips). However, it is still hard to determine the true return of business travel (thus, the “R” of the ROI of trips), especially when MICE are the travel’s motive.

Likewise, companies want to extend this end-to-end perspective to mobile, tool that they already use a lot in their travel program. 55% of companies have already integrated the mobile in their travel program and use it on a regular basis. Yet, the mobile is still not a real alternative to other traditional channels like OBT since all the value chain is not covered uniformly. On-trip functionalities are much more used: 87% of companies currently use the mobile channel to receive alerts from providers, 77% to check in, 74% to receive security alerts. Logically, those companies who already use mobile on regular basis want to expand their current mobile usage in the future and especially develop mobile functionalities related to booking, expense management and security:

18

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

• Currently 30% of them use the mobile channel to make their bookings, 11% for reporting and expense management, 21% for localization.

• 46% of them want to increase their use of booking functionalities, 46% their use of reporting and expense management options and 40% their use of the localization ability.

The willingness to develop mobile usage is all the more important when companies already have automated procedures. Mobile appears as a next step in their development. The required adaptation to new suppliers and the wish for a more autonomous traveler also explain the development of the mobile channel. This aligns with the practices observed on the leisure travel market. Thus travel agencies may have a role to develop the mobile channel as a real alternative to other channels.

19

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

Part 4: what about the traveler experience in the cost-focused context?

Traveler security and safety, companies’ priority #2

As said before, traveler security and safety has been ranked priority #2 for companies since 2 years. This is true for all companies, whatever their size may be. The number of companies listing this issue as a travel management priority has kept increasing in the last years, reaching 69% of companies today (+24pts vs. 2012). This continuously increasing importance that companies attach to security is to be linked to their legal obligation of “duty of care” as well as to recent events. Indeed, travelling was already risky per se, but today business travel is also taking place in a more complex and riskier environment.

The priority given to security and safety issue is also reflected in the increase in the number of companies taking measures for the employees to travel in optimal conditions: 87% of surveyed companies have the ability to contact their employees at any given moment (+6pts vs. 2013), 73% of them the ability to repatriate their employees immediately (+13pts) and 71% the ability to know all the time where their employees are. Training employees is still left behind but is also strongly increasing (32% in 2014, +9pts). Given the international development forecasted by companies, this issue will certainly remain at the heart of future concerns – and will also raise the issue of the integration of new kind of suppliers.

20

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

Despite speeches, travelers’ level of satisfaction is little taken into account

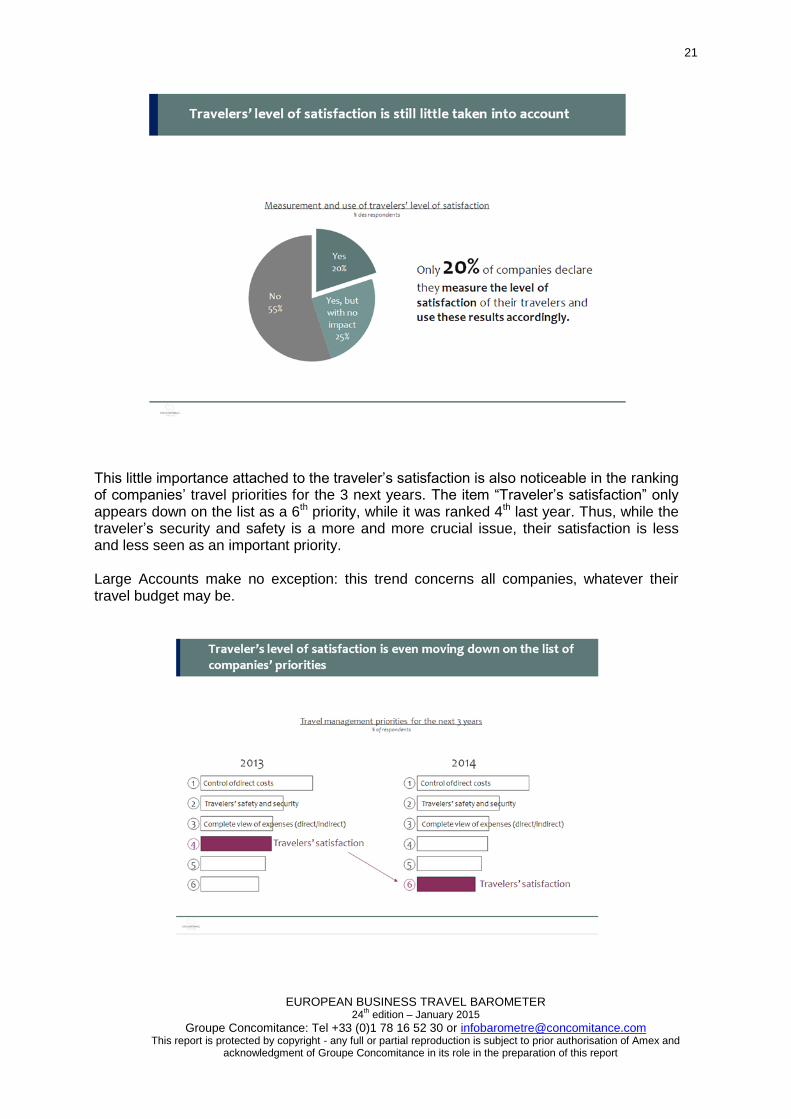

The level of satisfaction of the travelers is little measured: 55% of companies do not measure it at all. Besides, when it is measured, it is little used to bring changes to the company’s travel policy. Only 20% of companies measure it to adapt their travel policy accordingly. As a result, travel is not customized to the needs of each traveler and of each company. Yet, the traveler’s satisfaction can be the source of hidden costs which are still little known and little identified: tired traveler, longer transport times, etc. Large Accounts are more attentive to this issue: 30% of them measure the level of satisfaction of their travelers and take their remarks into account to transform their travel policy. It is also interesting to notice that the more companies are equipped with booking and/or expense management solutions, the more they measure traveler’s level of satisfaction and integrate it in their travel program.

21

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

This little importance attached to the traveler’s satisfaction is also noticeable in the ranking of companies’ travel priorities for the 3 next years. The item “Traveler’s satisfaction” only appears down on the list as a 6th priority, while it was ranked 4th last year. Thus, while the traveler’s security and safety is a more and more crucial issue, their satisfaction is less and less seen as an important priority. Large Accounts make no exception: this trend concerns all companies, whatever their travel budget may be.

22

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

The exception of the VIP traveler: towards a two-speed treatment of travelers? On the other hand, the demand for VIP services is increasing. 20% of companies are now purchasing VIP services to their travel agency, which is about twice as much as last year. The demand even reaches 37% among Large Accounts. This interest is to be linked to the appeal of the “access to concierge services” functionality on the mobile channel.

23

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

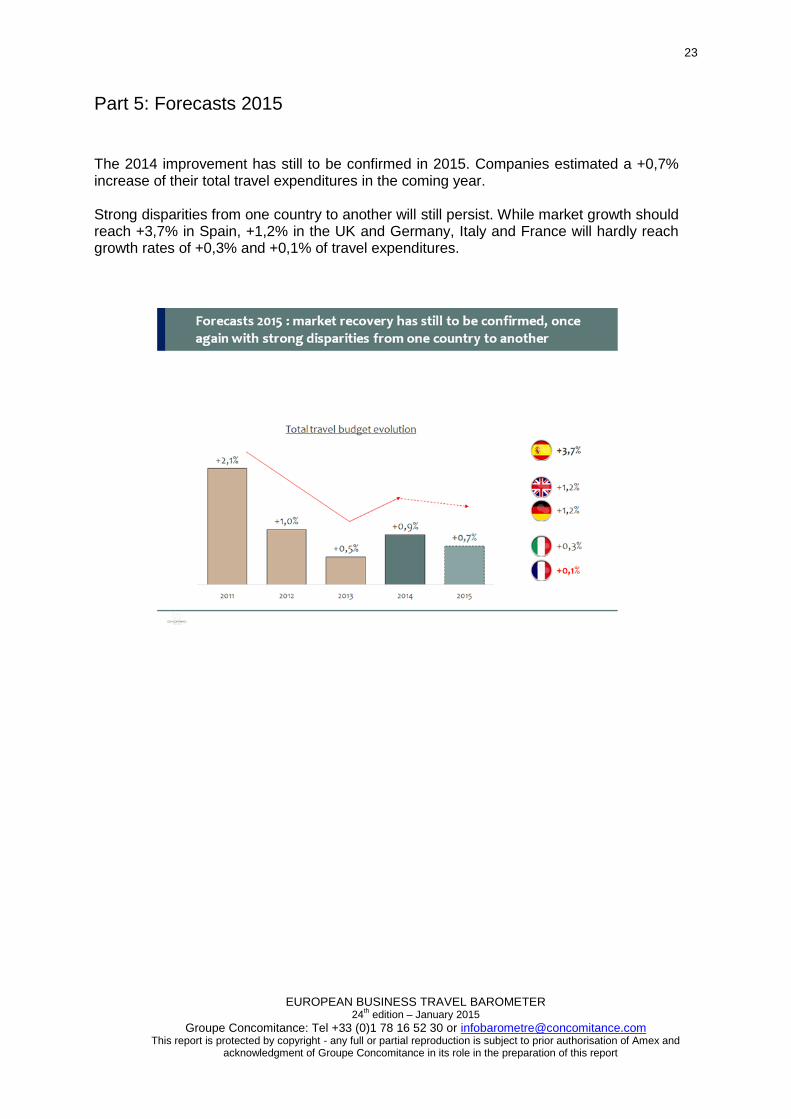

Part 5: Forecasts 2015

The 2014 improvement has still to be confirmed in 2015. Companies estimated a +0,7% increase of their total travel expenditures in the coming year. Strong disparities from one country to another will still persist. While market growth should reach +3,7% in Spain, +1,2% in the UK and Germany, Italy and France will hardly reach growth rates of +0,3% and +0,1% of travel expenditures.

24

EUROPEAN BUSINESS TRAVEL BAROMETER 24

th edition – January 2015

Groupe Concomitance: Tel +33 (0)1 78 16 52 30 or [email protected] This report is protected by copyright - any full or partial reproduction is subject to prior authorisation of Amex and

acknowledgment of Groupe Concomitance in its role in the preparation of this report

About the European Business Travel barometer, 2015 edition The 2015 barometer was prepared by Concomitance on the basis of a telephone survey conducted from November 4th to December 5th, 2014, among persons in charge of travel budgets ranging from less than €250,000 to over €50 million (Finance Directors, Purchasing Directors and Travel Managers) in 581 European companies based in 10 countries: Germany, Great Britain, France, Belgium, Luxembourg, the Netherlands, Spain, Italy, Denmark, Sweden and Norway. About Concomitance Concomitance is a service company specialized since 2001 in marketing, commercial, sales and client relations research, consultancy and performance development. Concomitance has teams specialized in several activity sectors such as telecommunications, travel and business travel, banking, distribution, etc. Since its establishment, Concomitance has stood out in terms of its capacity to transpose commercial and marketing issues into action plans which are immediately effective and comprehensible to all players. This capacity is a direct result of Concomitance's DNA: the prior business experience of our consultants allows us to formulate recommendations and share them with our clients in line with the maturity of their organization.