©2015, College for Financial Planning, all rights reserved. Session 11 Fundamental & Technical...

24

©2015, College for Financial Planning, all rights reserved. Session 11 Fundamental & Technical Analysis, Ratios, Anomalies CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAM Investment Planning

-

Upload

buck-elliott -

Category

Documents

-

view

214 -

download

0

Transcript of ©2015, College for Financial Planning, all rights reserved. Session 11 Fundamental & Technical...

©2015, College for Financial Planning, all rights reserved.

Session 11Fundamental & Technical Analysis, Ratios, Anomalies

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMInvestment Planning

Session Details

Module 5

Chapter(s)

2

LOs 5-3 Explain terminology and concepts associated with fundamental and technical analysis.

5-4 Relate fundamental and technical analysis concepts to modern portfolio theory principles.

5-6 Relate the impact of financial leverage to the financial performance of a company and to the valuation of a company’s stock.

11-2

Top-Down Analysis

Economic analysis

• GDP growth

• Monetary & fiscal policy

• Political analysis

• Inflation analysis

Industry analysisCompany analysis

11-3

Industry Analysis

The growth and maturation of an industry

Output

Time to t1 t2 t3

Rapid

Growth

Dec

linin

g Gro

wth

Maturity

11-4

Bottom-Up AnalysisRatio analysis• Liquidity (current

and quick ratios)• Activity (inventory

turnover)• Profitability

(EBITDA)• Return on capital• LeverageCash flow analysis

Business analysis

11-5

Liquidity Ratios

Current ratio

Quick ratio (acid test)

sliabilitie Current

assets Current

sliabilitie Current

Inventory assets Current

11-6

Ratio ComparisonsRatios of a firm overtime, such as ROE

over the past 5 and 10

years

Ratios of firms within an industry• tend to have similar

numerical values

• differences in numerical values are reasons for further analysis

11-7

Problems for Interpretation

• Different definitions for the same ratio

• Historical data may be outmoded

• Accounting changes alter financial statements

• Non-recurring items

11-8

Financial Leverage & the Return on Equity

• The use of debt financing (financial leverage)o may increase the return on equityo also increases financial risk

• Increased risk may offset the increased return on equity

11-9

Impact of Equity vs. Debt

Two companies, each raises $100M, one all equity, the other $50M equity and $50M debt.

What is the impact of $10M in earnings on ROE?

Company A: 10/100 = 10% ROE

Company B: 10/50 = 20% ROE

Example ignores interest charges and cost of borrowing

Company A Company B

Equity - Common Stock

$100M $50M

Debt - Corporate Bond

$0 $50M

Total Capitalization $100M $100M 11-10

Technical Analysis• Focus on the stock,

not on the company

• Interprets supply and demand for the stock

• Uses graphs of stock’s price movements and volume

11-11

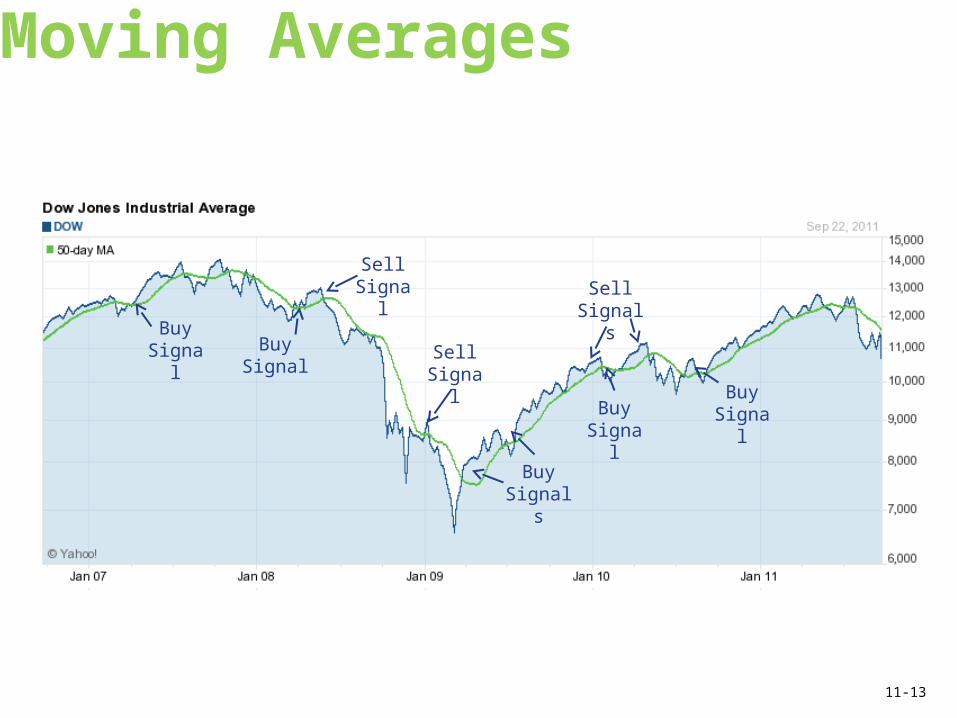

Moving Averages• Compare the stock's

current price to a moving average of the stock's price

• Moving averages may be varying amounts, such as 50, 100, or 200 days

• The moving average follows the current price

11-12

Moving Averages

Buy Signal

Sell Signals

Buy Signal

Buy Signals

Sell Signal

Buy Signal

Buy Signal Sell

Signal

11-13

Technical Trading Indicators

• Advance/decline line• Moving averages• Support and resistance levels• Mutual fund cash positions • Short sales by specialists• Short interest• Odd lot purchases• Investment advisory opinions • Put/call ratio• Barron’s Confidence Index

11-14

The Dow Theory• Emphasizes

movements in the industrial and transportation averages

• Movement in one average, confirmed by movement in the other average, indicates a trend

11-15

Dividend Growth Rate

Where: g = dividend growth rate ROE = return on equity RR = earnings retention rate

RRROEg

11-16

Constant Growth DDM

gr

DV

1

11-17

Growth Rate ExampleZarathustra Industries has assets of $300 million, and liabilities of $100 million. Zarathustra earned $25 million last year, and paid out $5 million in dividends. What is Zarathustra’s dividend growth rate?

$300M (assets) - $100M (liabilities) = $200M of equity$25M/$200M = .125 = 12.5% ROE

$25M (earnings) – $5M (dividends) = $20M in retained dividends

$20M/$25M = .80 Retention Rate (RR)

g = ROE x RR12.5 x .80 = 10%

11-18

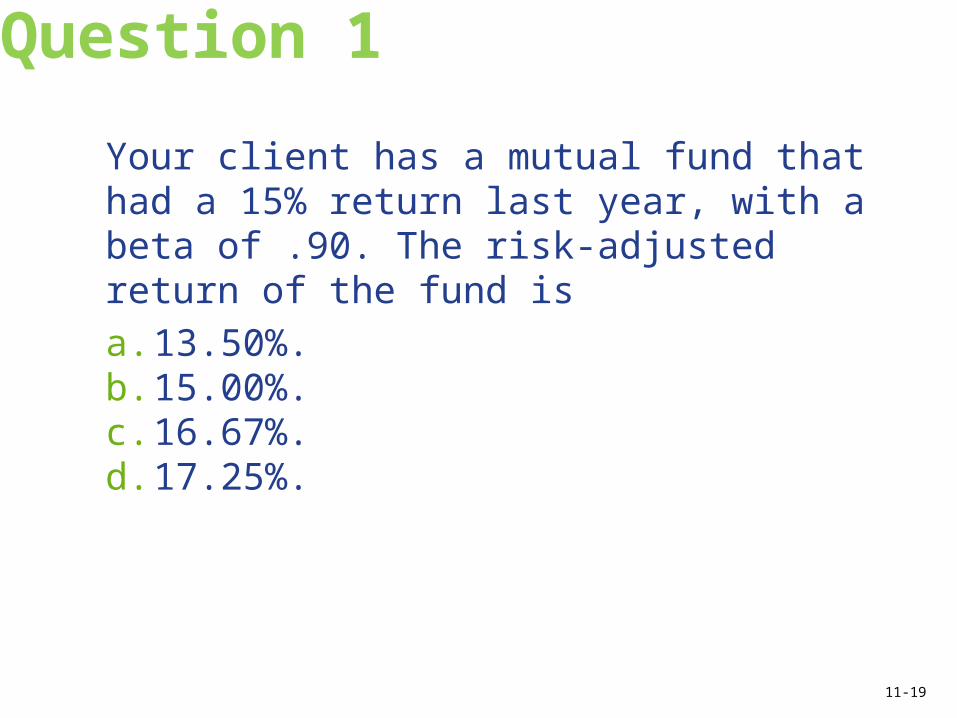

Question 1

Your client has a mutual fund that had a 15% return last year, with a beta of .90. The risk-adjusted return of the fund isa. 13.50%.b. 15.00%.c. 16.67%.d. 17.25%.

11-19

Question 2

Fundamental analysis includes which of the following?I. computation of the current ratioII. comparison of a company’s PEG ratio to its

industry’s PEG ratioIII. computation of the company’s debt-to-equity

ratioIV. comparison of a company’s daily trading

volume to its historical volumea. I and II onlyb. I and III onlyc. I, II, and III onlyd. I, III, and IV onlye. I, II, III, and IV

11-20

Question 3

In designing and implementing an investment plan for a client, a planner who believes in the strong form of the efficient market hypothesis will use which one of the following combinations of analytical techniques?a. moving average analysis, industry analysis,

and weighted average returnsb. efficient frontier, correlation coefficients, and

weighted average returnsc. efficient frontier, industry analysis, and

company analysisd. technical analysis, fundamental analysis, and

correlation coefficients

11-21

Question 4

If a company payout ratio over the past five years has gradually declined from 50% to 25%, which one of the following statements summarizes the impact on the dividend growth model?a. The payout ratio has no impact on the

dividend growth model.b. The required return (“r”) in the dividend

growth equation will rise.c. The “g” in the dividend growth model may be

difficult to determine.d. The current dollar dividend amount will be

affected, but neither “r” nor “g” will be affected.

11-22

Question 5

Kaleidoscope Inc. has assets of $600 million and liabilities of $350 million. Earnings for the current year were $50 million, and the dividend payout ratio is 25%. What is the dividend growth for Kaleidoscope Inc.?a. 10%b. 15%c. 20%d. 25%

11-23

©2015, College for Financial Planning, all rights reserved.

Session 11End of Slides

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMInvestment Planning