2015 cahf yearbook-22.10.2015.compressed

256

HOUSING FINANCE IN AFRICA A review of some of Africa’s housing finance markets October 2015 Published by the Centre for Affordable Housing Finance in Africa 2015 YEARBOOK

-

Upload

maxine-ohenewaa-asiedu -

Category

Real Estate

-

view

43 -

download

0

Transcript of 2015 cahf yearbook-22.10.2015.compressed

HOUSING FINANCE IN AFRICA

A review of some of Africa’s housing finance markets

October 2015

Published by the Centre for Affordable Housing Finance in Africa

2015YEARBOOK

Copyright © Centre for Affordable Housing Finance in Africa, 2015All rights reserved.

The Centre for Affordable Housing Finance in AfricaPO Box 72624Parkview 2122South AfricaTel +27 11 447 9581Contact: Kecia RustMobile +27 83 785 4964Email [email protected] www.housingfinanceafrica.org

The Centre for Affordable Housing Finance in Africa (CAHF) is a not-for-profit company with a vision for an enabled affordable housing financesystem in countries throughout Africa, where governments, business, and advocates work together to provide a wide range of housing optionsaccessible to all. CAHF’s mission is to make Africa’s housing finance markets work, with special attention on access to housing finance for the poor.We pursue this mission through the dissemination of research and market intelligence, supporting cross-sector collaborations and a market-basedapproach. The overall goal of our work is to see an increase of investment in affordable housing and housing finance throughout Africa: moreplayers and better products, with a specific focus on the poor.

Our work covers four main areas: (1) understanding the housing asset, (2) monitoring housing sector performance, (3) exploring innovation inhousing finance, and (4) supporting housing finance market development.

Since its formation, the CAHF has come to be known as the most comprehensive and up to date source of information on housing finance inAfrica. Its research and other material is regularly used by investors, lenders, pension funds, and other financiers; legal practitioners, researchers andacademics; policy makers and other housing finance practitioners to scope and pursue the opportunities for extending access to housing financeacross Africa. As a thought leader in the sector, CAHF is a respected advocate for financial inclusion in housing finance in Africa. Our work isavailable on our website: www.housingfinanceafrica.org.

CAHF’s core funders are FSD Africa, the National Housing Finance Corporation (of South Africa), and the FinMark Trust.

Acknowledgements

This report was edited by Sireena Ramparsad. It represents the combined effort of people from all over the African continent, either as authors,reviewers, or respondents to our questionnaire. Sincere thanks are due to everyone for their contributions and insights.

Individual country and regional profiles were written and/or updated by, Josie McVitty (Algeria, Djibouti, and Libya), Shakrah Sadou (Burkino Faso,Cote d’Ivoire, Niger, Senegal, Liberia and UEMOA), Duncan Kayiira (Burundi, Uganda, South Sudan and the EAC region), Joachim Boko (Benin, Mali,and Togo), Carlson Ifughe (Cameroon and CEMAC region), Palesa Sematlane (Lesotho), Sabelo Mabuza (Swaziland), Dolapo Adejuyigbe andOlamide Udoma (Nigeria), Allan Kundu (Kenya), Zeinab Sayed (Egypt and the Northern Africa region), Azanga Katikia Henry and Joëlle Fotine(DRC), Janine Ampulire (Rwanda), Daniel Phiri (Zambia), Juana Hatfield (Mozambique, Ethiopia, The Gambia, Mauritania, Central African Republicand Eritrea), Sylvia Croese (Angola), Othata Batsetswe (Botswana), Laura Courbois - Imani Development (Malawi), Innocent Chirisa (Zimbabwe),Laverne Buya-Kamara (Sierra Leone), Ziad Sayah (Tunisia), Mounia Tagma (Morocco), Emmanual Kwaku Asamoah (Ghana), Vinson Hailulu (Namibia),Anna-Maria Shija (Tanzania), Manilall Seetohul (Mauritius, Comoros, Seychelles and Madagascar), Samuel Suttner (Chad and Cape Verde), MargaridaMoreira (Guinea-Bissau), Sireena Ramparsad and Kecia Rust (South Africa) and Sireena Ramparsad (Somalia and the SADC region). Allan Kunducollected the data for the tables in each country profile. Further thanks are extended to people who assisted in providing information or commentson the profiles: Adelaide Steedley; Kudakwashe Mativenga; Samuel Suttner; Kgomotso Tolamo; Aqualine Suliali; Oswald Urassa; Allan Cain; MohamedDubo of Datagrid Somalia; Stephen Wanjala; UN-Habitat Ethiopia; Manuela Graetz and the Housing Development and Government BuildingsBureau of the Ministry of Urban Development, Housing and Construction in Ethiopia. Kecia Rust wrote the introductory essay and SireenaRamparsad oversaw the project.

We are grateful for your insights and enthusiasm for this project, and very happy to have you all as part of our growing team of experts. TheYearbook would not have been possible without your input. The report has also drawn extensively on CAHF’s ongoing research, often undertakenby CAHF consultants, as well as on local reporting in the press. Of course, any errors of omission or interpretation remain with the Centre forAffordable Housing Finance in Africa. We welcome your comments.

Layout and production:

June Viljoen Print Consultancy cc

If cities are built the way they are financed (Renaud, 1984), then Africa’s cities areset to change.

Innovation in housing finance –in terms of products, players, and approaches, not tomention target markets – is a key feature across the continent, creating newopportunities for investment and delivery. As both local and international investorschase growth opportunities in a sluggish global economy, they are employingdiversification strategies to manage the risks of their traditional targets – and in this,residential property is increasingly becoming an option. And while establishedplayers are getting better at what they do, new players are adding to the mix andcompeting for opportunities.

Investors are faced with a paradox, however. By their very nature, they are drawnto the high income markets. It is in these markets that they can price adequatelyfor risk and realize the returns they seek. However, the real story – the scaleopportunity just waiting to be cracked – is in the lower income market segments.The arguments for investment in residential – high urbanization rates, a growingmiddle class, a shortage of supply – these are all arguments for moving down marketinto the uncharted waters of affordable housing. Can investors and developers doit? In 2015, this is a very real focus.

Five stories characterise Africa’s housing finance markets in 2015:

1. Innovation in financing 2. Growing awareness of the opportunity in residential3. The identification of niche markets and an appreciation of the affordability

challenge4. Policy & regulatory evolution to match investor interest5. Growing experience and investor sophistication

Of course, the challenges are not insignificant. But increasingly, investors anddevelopers are noting that the potential benefits outweigh the risks. And, asgovernments come to appreciate the potential that this interest offers, their effortsto streamline development processes and enable their local housing markets togrow are creating new opportunities that are beginning to change the face ofAfrican cities.

This is the sixth edition of the Housing Finance in Africa yearbook. Since last year, we have added five country profiles and one regional profile bringing thetotal to 48 country profiles and five regional profiles. We have again sought out new data sources, and rethought our approach to the affordability graphs.We have been monitoring the news so that this yearbook reflects the current situation of housing finance markets on the African continent in 2015.

The Yearbook is intended to provide housing finance practitioners, investors, developers, researchers and government officials with a current update ofpractice and developments in housing finance in Africa, reflecting the dynamic change and growth evident in the market. It is hoped that it will also highlightthe opportunities available for new initiatives, and help practitioners find one another as they strive to participate in the sector. While the general aim ofthe Yearbook is to offer a broad overview of housing finance and housing development in Africa, special emphasis is placed on the key challenge of housingaffordability, and the critical need for housing products and finance that are explicitly targeted at the income profiles of the majority.

This has been a desktop study. Using the CAHF’s research as baseline material, further information on more recent developments was accessed from mediareports, journal articles and practitioner websites. In some cases, material was shared with in-country practitioners. Of course, the yearbook is notcomprehensive, neither in the scope of countries covered nor the data provided. It is intended as an introduction, with the hope that the detail providedwill whet the appetite for more. CAHF invites readers to provide comment and share their experiences on what they are doing in housing finance in Africa.

Kecia RustCentre for Affordable Housing Finance in AfricaOctober 2015

About this publication

Overview 1Explaining the indicators 21Country profiles 25

Algeria 25Angola 29Benin 33Botswana 37Burkina Faso 41Burundi 45Cameroon 49Cabo Verde (Cape Verde) 53Central African Republic 57Chad 61Comoros 65Cote d' Ivoire 69Democratic Republic of Congo 73Djibouti 77Egypt 81Eritrea 85Ethiopia 89Gambia, The 93Ghana 97Guinea-Bissau 101Kenya 103Lesotho 107Liberia 111Libya 115Madagascar 119Malawi 123Mali 127Mauritania 131Mauritius 135Morocco 139Mozambique 143Namibia 147Niger 151Nigeria 155Rwanda 159Senegal 163Seychelles 167Sierra Leone 171Somalia 175South Africa 179South Sudan 183Swaziland 187Tanzania 191Togo 195Tunisia 199Uganda 203Zambia 207Zimbabwe 211

Regions 215CEMAC 215EAC 219North Africa Region 223SADC 225UEMOA 229

Contents

AbbreviationsAADL Lease to own programme, AlgeriaAAHDE Addis Ababa Housing Development EnterpriseACF African Capitalisation Fund, MalawiACI Agence de Cession Immobilière (Land Development Agency), Mali ACSI Amhara Credit & Savings Institution, EthiopiaADC Arrêté de Consession Definitive, Cote d’IvoireAFD Agence Française de Développement (French Development Agency)AfDB African Development BankAFRICOM Africa Command, DjiboutiAFT Agenda for Transformation, LiberiaAGETIP Agence de Gestion des Travaux d’Intérêt Public, BeninAGETU Agency for the Equipment of Urban Land

(Agence d’Equipement des Terrains Urbains), TogoAGOA African Growth and Opportunity ActAH Amiscus Horizon company, The GambiaAIB African Investment BankAMU Arab Maghreb UnionAMT Akiba Mashinani TrustANAT National Land Development Agency, MauritaniaANDF National Agency for Domain and Land

(Agence nationale du domaine et du foncierANIP The National Private Investment AgencyAPBEF Association professionnelle des banques et

établissements financiers du Mali APIM Association des promoteurs immobiliers du MaliAPIMA Angolan Association of Real Estate ProfessionalsARRU Agency for Urban Rehabilitation, TunisiaASODEV Action pour la Solidarité et le Développement, DRCASSOAL Solidarity Actions of Support to Organisations

Supporting Freedom, CameroonATM Automated teller machineBaDEx Bonds and derivatives exchangeBAI Banco Africano de Investimento BAIC Banque africaine pour l’investissement et le commerce BANCOBU Commercial Bank of BurundiBASE Banking Association of South AfricaBBCI Burundi Bank for Commerce and InvestmentBBD Benin Development BankBBS Botswana Building SocietyBCA Banco Comercial do AtlânticoBCB Bank Credit Bujumbura, BurundiBCC Central Bank of ComorosBCDC Banque Commerciale du CongoBCEAO Banque Centrale Des Etats de l’Afrique de l’OuestBCIMR Banque pour le Commerce et l'Industrie – Mer Rouge, DijoubitiBCM Central Bank of MauritaniaBCR Bank Commerciale du RwandaBCEAO Banque Centrale des États de l' Afrique de l'Ouest

(Central Bank of West African States)BCV Banco de Cabo VerdeBEA Banque El Ammane pour le Developpement de l’Habitat BEAC Banque des Etats d’Afrique Centrale

(Bank of Central African States), CameroonBESA Banco Espirito Santo AngolaBFA Banco de Fomento, AngolaBFI Banks and Financial Institutions BGF Bank Financing and Management, BurundiBHB Benin Housing BankBHBF Housing Bank of Burkina Faso (Banque de l’Habitat du Burkina Faso)BCM Central Bank of MauritaniaBCR Bank Commerciale du RwandaBCEAO Banque Centrale des États de l' Afrique de l'Ouest

(Central Bank of West African States)BCV Banco de Cabo Verde

BEA Banque El Ammane pour le Developpement de l’Habitat BEAC Banque des Etats d’Afrique Centrale

(Bank of Central African States), CameroonBESA Banco Espirito Santo AngolaBFA Banco de Fomento, AngolaBFI Banks and Financial Institutions BGF Bank Financing and Management, BurundiBHB Benin Housing BankBHBF Housing Bank of Burkina Faso (Banque de l’Habitat du Burkina Faso)BHC Botswana Housing CorporationBHM Banque de l'Habitat du Mali (Mali Housing Bank)BHR Banque de l’Habitat du Rwanda (Rwanda Housing Bank) BHS Banque de l'Habitat du SenegalBIAC Banque Internationale pour l’Afrique au CongoBIC Banco Internacional de Crédito BICIA-B Banque Internationale pour le Commerce,

l’Industire et l’Agriculture du Burkina, Burkina FasoBIM Banque Internationale du MaliBIMR Banque Indosuez Mer RougeBIAT Arab Bank of TunisiaBIP Bank for Innovation and Partnership, BIPBK Banque de Kigali (Bank of Kigali), RwandaBNDE National Bank for Economic Development, BurundiBNG Building New Ground, South African housing programmeBOA Bank of Africa BOAD Banque Ouest Africaine de Développement

(West African Development Bank)BoG Bank of GhanaBoM Bank of MauritiusBoN Bank of NamibiaBOT Build, operate and transfer modelBoT Bank of TanzaniaBoZ Bank of ZambiaBPC Banco de Poupança e CréditoBpd Barrels-per-dayBRB Bank of the Republic of BurundiBRD Banque Rwandaise de Développement (Rwanda Development Bank)BSIC Sahelo-Saharan Bank for Commerce and Investment, BeninBTCGA Banco Totta Caixa Geral AngolaBTD Togolese Development BankBTCI Banque Togolaise pour le Commerce et l’IndustrieBUCECO Burundi Cement Company BVMT Tunisian stock exchangeCABS Central African Building Society, ZimbabweCAGR Compound Annual Growth RateCAMCCUL Cameroon Cooperative Credit Union LeagueCAPEC Savings and Cooperative Union, MauritaniaCAPMAS Central Agency for Public Mobilization and StatisticsCAR Central African RepublicCBB Construction and Business Bank, EthiopiaCBE Central Bank of EgyptCBE Commercial Bank of EritreaCBE Commercial Bank of EthiopiaCBG Central Bank of The GambiaCBK Central Bank of KenyaCBL Central Bank of LesothoCBL Central Bank of LiberiaCBL Central Bank of LibyaCBR Central Bank RateCCI Centre for Community Initiatives, TanzaniaCCL Centre for Housing Construction

(Centre de la Construction et du Logement), TogoCCODE Centre for Community Organisation and Development, Malawi

Africa Housing Finance Yearbook 2015

CDMH Compte de Mobilisation pour l’Habitat, Cote d’IvoireCDN Crédit du Niger (a commercial bank in Niger)CDS City Development StrategyCEGECI Centre for the Management of Cities

(Le Centre de Gestion des Cités)CEMAC Communauté Économique et Monétaire de l'Afrique Centrale

(Economic and Monetary Community of Central Africa, EMCCA) CENFRI Centre for Financial Regulation and InclusionCEN-SAD Community of Sahelo-Saharan statesCFA Communauté Financière Africaine (currency in West Africa)CGAP Consultative Group to Assist the PoorCHF Common Humanitarian FundCIF Climate Investment Fund, MadagascarCIS Collective Investment Schemes CMA Common Monetary AreaCMCA Crédit Mutuel de CentrafriqueCMH Companhia Mocambicana de HidrocarbonetosCMP Common Market Protocol CMU Couverture Maladie Universelle (universal health coverage)CMS Credit Mutuel du SenegalCNEC Caisse Nationale d'Epargne et de Crédit de DjiboutiCNEL Savings and Loans Bank, TunisiaCNEP Caisse National d’ Épargne de Prévoyance (National Savings

and Providence Fund – one of the state-owned banks), AlgeriaCNSS National Social Security Fund, TogoCNT Confederation Nigerienne du TravailCOBAC Central African Banking CommissionCoK City of Kigali CofO Certificate of Occupancy, NigeriaCOMESA Common Market for Eastern and Southern AfricaCPA Comprehensive Peace Agreement, South Sudan CPEC Caisse Populaire d'Epargne et de Crédit, DijiboutiCPF Conservation de la Propriété FoncièreCPLP Comunidade dos Países de Língua Portuguesa

(Community of Portuguese Speaking Countries)CPIA Country Performance and Institutional Assessment, World Bank CPS Contribution Pension SchemeCRB Credit Reference Bureau, Malawi, South Sudan and ZambiaCREPMF Conseil Regional de l’epargne publique et des marches financiers

(Regional Council of Savings Public and Financial Markets)CRJE China Railway Jianchang Engineering CRI Collateral replacement indemnityCRRH Caisse Regionale de Refinancement Hypothecaire

(Regional Mortgage Refinance Fund), WAEMU CRRH-UEMOA Caisse Regional de Refinancement Hypothecaire – UEMOA CRT Togolese Pension FundCRM Retirement Fund of MaliCTA Construction technical assistanceDFI Development Finance InstitutionDID Développement International DesjardinsDNHU National Directorate for Housing and UrbanisationDRC Democratic Republic of CongoDTI Debt to Income ratio DUAT Direito de Uso de Aproveitamento da Terra

(right to use and benefit from and), MozambiqueEAC East African Community EAMU East African Community Monetary UnionEBH Elgin, Brown & Hamer, NamibiaECAM Enquête Camerounaise auprès des Ménages, or Household survey,

CameroonECF Enhanced Credit FacilityECOSAT Encadrement des Constructions sociales et aménagement des terrrains,

(Framework for social engineering and land management), BurundiECOWAS Economic Community of West African StatesEEDC Egypt Economic Development ConferenceEFSA Egyptian Financial Supervisory AuthorityEHFC Egyptian Housing Finance Company

EIU Economic Intelligence UnitEMRC Egyptian Mortgage Refinance CompanyEMSL Ecobank microfinance Institution, Sierra LeoneENDE National Strategy for DevelopmentEPS Expanded PolystyreneEU European UnionFAEU Fonds d'Amenagement et d'Equipement Urbain

(Urban Development and Equipment Fund), BurundiFDI Foreign direct investmentFECECAM Fédération des Caisses d’Epargne et de Crédit Agricole MutuelFEDEP Federal Urban PoorFFH Fundo de Fomento de Habitação

(Housing Promotion Fund), MozambiqueFGCMPI Real Estate Development Guarantee Fund, AlgeriaFGHM Fonds de Garantie Hypothecaire du Mali,

(Mali Mortgage Guarantee Fund)FHA Federal Housing Authority, NigeriaFHRL FMBN Home Renovation Loan FHSE Foundation for Rural Housing, UgandaFIP Finance and InvestmentFLISP Finance Linked Individual Subsidy Programme, South AfricaFMBN Federal Mortgage Bank of NigeriaFMO Nederlandse Financierings-Maatschappij voor Ontwikkelingslanden

(Netherlands Development Finance Company)FNB First National BankFNFI National Inclusive Finance Fund

(Fonds National de la Finance Inclusive), TogoFNM National Microfinance Fund, CongoFOGARIM Guarantee Fund for mortgages for low or

seasonal income groups, MoroccoForex Foreign exchangeFPHU Fund for the Promotion of Urban Housing, BurundiFSC Financial Sector Charter, in South Africa and NamibiaFSDH Special Fund for Housing Development

(Fonds Special de Developpement de l’Habitat), TogoFSDP Financial Sector Development Program, RwandaFSH Fonds de Soutien à l’Habitat (Fund for housing support)FSRA Financial Services Regulatory AuthorityFTA Free Trade AreaFUCEC Faîtière des Unités Coopératives d’Epargne et de Crédit, TogoGARI Fonds Africain de Garantie des Investissements

Privés en Afrique de l’OuestGBS Gambia Bureau of StatisticsGDP Gross domestic productGHL Ghana Home LoansGIPF Government Institutions Pension FundGIZ Deutsche Gessellschaft für Internationale Zusammenarbeit

(German Society for International Cooperation)Global Findex Global Financial Inclusion DatabaseGLS Government Loan SchemeGNI Gross national incomeGNC General National Congress, LibyaGOAC Guernsey Overseas Aid CommissionGRET Groupe de Recherches et d’Échanges Technologiques, MauritaniaGREDA Ghana Real Estate Developers Association GRI Global Real Estate InstituteGSF Guarantee and Subsidy Fund, EgyptGSMA Groupe Speciale Mobile AssociationGTP Growth and Transformation Plan, EthiopiaHCBE Housing and Commerce Bank of EritreaHCF Housing Finance Company, SeychellesHDA Housing Development Agency, South AfricaHDI Human Development IndexHFB Housing Finance Bank, UgandaHFC Housing Finance Company HFC Home Finance Company of the Gambia LimitedHFCU Housing Finance Company of Uganda

HfH Habitat for HumanityHFHU Habitat for Humanity, UgandaHFP Housing Finance ProjectHIB Housing and Infrastructure Board, LibyaHMF Housing microfinanceHOFINET Housing Finance Information NetworkHSB Housing and Savings Bank, EthiopiaIAS International Accounting StandardsICF Investment Climate FacilityIDBZ Infrastructure Development Bank of ZimbabweIFAD International Fund for Agricultural DevelopmentIFC International Finance CorporationIFRS International Financial Reporting StandardsIDB Islamic Development BankIDP Internally Displaced PersonIHDP Integrated Housing Development Programme, EthiopiaIHS International Housing SolutionsIMF International Monetary FundINEP Instituto Nacional de Estudos e Pesquisa National Institute

for Studies and ResearchINPS National Institute of Social Welfare, MaliINSS National Social Security Institution, BurundiIOR-ARC Indian Ocean Rim Association for Regional CooperationIRS Integrated Resort Scheme, MauritiusISKAN National Land Development, Housing Development and

Real Estate Promotion and Management Corporation, MauritaniaKBA Kenya Bankers Association KCB Kenya Commercial BankKBRR Kenya Banks’ Reference RateKfW Kreditanstalt für Wiederaufbau

(German Reconstruction Loan Corporation)KNBS Kenya National Bureau of Statistics KoS Kingdom of Swaziland KYC Know Your Customer, South SudanLBDI Liberian Bank for Development and InvestmentLDC Least developed countryLFS Labour Force Survey, LiberiaLHLDC Lesotho Housing and Land Development CorporationLIC Low income countryLIS Lands Information systemLISGIS Institute of Statistics and Geo-Information Services, LiberiaLNG Liquefied Natural GasLOUAF Loi d’Orientation sur l’Urbanisme et l’Aménagement Foncier, NigerLPA Commercial housing, AlgeriaLPL Public rental housing, AlgeriaLPP Logement Public Promotionnel, the assisted housing programme, AlgeriaLSC Land, Services and Citizenship, GhanaLTV Loan-to-value (ratio)LUSE Lusaka Stock Exchange MCA Millennium Challenge Account, LesothoMCB Mauritius Commercial BankMCIB Public Credit Bureau, Mauritius MDG Millennium Development GoalMDI Microfinance Deposit-taking InstitutionMENA Middle East and North Africa Region MFC Mortgage Finance CompanyMFF Mortgage Finance FundMFI Microfinance InstitutionMFSDS Financial Sector Development Strategy 2013 – 2022, MozambiqueMHC Malawi Housing CorporationMHC Mauritius Housing CompanyMHDP Mass Housing Development ProgrammeMHU Ministry of Housing and Urban Development, AlgeriaMHU Ministry of Housing and Utilities, Libya

MLF Mortgage Liquid FacilityMLSP Mass Land Servicing ProgrammeMINDAF Ministry of State Property and Land Tenure, CameroonMOPH Ministério das Obras Públicas e HabitaçãoMOU Memorandum of Understanding MPD Movement for Democracy MSMEDF Micro Small and Medium Enterprises Development Fund, NigeriaMTSP Money Transfer Service ProviderNACHU National Cooperative Housing Union, KenyaNAMFISA Namibia Financial Institution Supervisory AuthorityNAPSA National Pension Scheme Authority, ZambiaNASSIT National Social Security and Insurance Trust, Sierra LeoneNASSCORP National Social Security and Welfare Corporation NBFIRA Non-Banking Financial Institution Authority, BotswanaNBBL Norwegian Federation of Co-operative Housing AssociationsNBE National Bank of EthiopiaNBS New Building Society, MalawiNDP National Development PlanNDP4 4th National Development Plan, Namibia NEF National Empowerment Foundation, MauritiusNEMA National Environmental Management Authority, KenyaNGO Non-governmental organisationNHA National Housing Agency, ZambiaNHA National Housing Authority, LiberiaNHAG Namibian Housing Action GroupNHBT National Housing Bond Trust, ZambiaNHC National Housing Corporation, Kenya and TanzaniaNHDC National Housing Development Company, MauritiusNHE National Housing Enterprise, NamibiaNHF National Housing Fund, NigeriaNHFC National Housing Finance CorporationNHP National Housing Programme, EgyptNLC National Land Commission Kenya NIESV Nigerian Institute of Estate Surveyors and Valuers NMB National Microfinance Bank, TanzaniaNMRC Nigerian Mortgage Refinance CorporationNOCAL National Oil Company of Liberia NOCIBE Nouvelle Cimenterie du Bénin – NOCIBENPL Non-performing loanNREC National Real Estate CompanyNSDP National Strategic Development Plan, Lesotho NSSA National Social Security Authority, ZimbabweNSSF National Social and Security Fund, UgandaNUCA New Urban Communities Authority, EgyptODA Official development assistanceOHADA Organisation for the Harmonisation of Business Law in AfricaOHLM Office des habitats à loyers moderesOIBM Opportunity International Bank of MalawiOMH Office Malien de l'Habitat (Mali Housing Agency)OPIC Overseas Private Investment CorporationOTC Office de Topographie et de CadastreOTR Office Togolais des RecettesPAGE Programme to Accelerate Growth and Employment, The GambiaPAMF Première Agence de MicroFinance, MadagascarPAICV African Party for the Independence of Cabo VerdePDES Economic Social Development plan, NigerPDU Urban Development Programme, MauritaniaPGE Programme Général de l’EtatPMB Primary Mortgage BanksPMC Property Management CorporationPMI Primary Mortgage InstitutionPNEI National Pact for Industrial Emergence, MoroccoPND National Development Plan, Chad

Africa Housing Finance Yearbook 2015

PNRLR National Programme for the Resorbing of Rudimentary Lodging PPC Pretoria Portland Cement PPHPZ Peoples’ Process on Housing and Poverty in ZambiaPPP Purchasing power parityPPP Public-private partnershipPRS Permanent Residence Scheme, MauritiusPSE Plan Sénégal EmergentPSI Policy support instrumentPTI Payment-to-income ratioPUIUR Programme d'Urgence d'Infrastructures Urbaines, Cote d’IvoireRCPB Réseau des Caisses Populaires du BurkinaRDP Reconstruction and Development Programme, South Africa REALL Real Equity for All (formerly Homeless International)REC Regional Economic Community RECCU Renaissance Cooperative Credit Unions, CameroonREDAN Real Estate Development Association of NigeriaREIT Real Estate Investment TrustREPI Real Estate Price Index, MoroccoRHA Rwanda Housing AuthorityRHB Rwanda Housing BankRHLF Rural Housing Loan Fund, South AfricaRISDP Regional Indicative Strategic Development Plan (SADC)RNHC National Network of Inhabitants of CameroonRNP National Postal ServiceROA Return on AssetsRSNDP Revised Sixth National Development RSSB Rwanda Social Security BoardSACCO Savings and Credit Co-operativeSACU South African Customs UnionSADC Southern African Development CommunitySALHOC Sierra Leone Housing Corporation SAPES Scheme to Attract Professionals for Emerging Sectors, MauritiusSARB South African Reserve BankSBM State Bank of MauritiusSBS Swaziland Building SocietySEC Securities and Exchange Commission, GhanaSDFN Shack Dwellers Federation of NamibiaSDI Shack / Slum Dwellers InternationalSETU Societe d’Equipement des Terrains Urbains

(Society of Urban Land Equipment), TogoSFDN Shack Dwellers Federation of NamibiaSGBB Societe Generale de Banque au BurkinaSHC State Housing Company, GhanaSHDC Seychelles Housing Development CorporationSHHA Self Help Housing Agency, BotswanaSIAB Société Inter-Africaine de Banque, TogoSIC Société Immobilière du Cameroun (Cameroon Real Estate Corporation)SID Société Immobilière de DjiboutiSIFMA-SA Societe Fonciere et Immobiliere du MaliSiHA Single Housing Agency, BotswanaSIP Société Immobilière Publique (National Real Estate Company), BurundiSIPIM Societe ivoirienne de promotion immobilièreSIPO Strategic Indicative Plan for the Organ

(on Defence, Politics and Security) (SADC)SITO Société Immobilière TogolaiseSLIEPA Sierra Leone Investment and Export Promotion Agency SMB State Bank of MauritiusSMCP Savings and Micro-Credit Programme, EritreaSME Small and medium-sized enterpriseSNEC National Water Supply Company of CameroonSNC Societe Nigerienne de Cimenterie, NigerSNEN Syndicat National des Enseignants du NigerSNHB Swaziland National Housing BoardSNL Swazi Nation Land

SNPSF National Post and Financial Services Institution SOCOGIB Société de Construction et de Gestion Immobilière du BurkinaSOCOGIM Société de Construction et de Gestion Immobilière, BeninSOCOGIM Real Estate Construction and Management Company MauritaniaSOFIA Société Financière Africaine de CréditSONA State Insurance company, Democratic Republic of Congo SONIDEP Société Nigérienne Des Products PétroliersSONUCI Société Nationale d’Urbanisme et de Construction ImmobilièreSOPROFIM Land and Real Estate Promotion CorporationSPI Societé de Promotion Immobiliere, MaliSPLM South People’s Liberation Movement, South SudanSRA Swaziland Revenue Authority SREP Scaling Up Renewable Energy in Low Income

Countries Programme, MadagascarSRH Société de Refinancement Hypothécaire

(Mortgage Refinancing Company), AlgeriaSSA Sub-Saharan AfricaSSFR Social Security Fund of RwandaSSHFC Social Security and Housing Finance Corporation, GambiaSTZC Zhen Gwei Technique CongoTIPEEG Targeted Intervention Programme for Employment

and Economic Growth, Namibia TMB Trust Merchant Bank, DRCTMRC Tanzania Mortgage Refinancing CompanyPROM Togolese Sponsorship Corporation (Societe Togolaise de Promotion)UAE United Arab EmiratesUEAC Union Economique de l’Afrique Central

(Central African Economic Union)UEMOA West African Economic Monetary UnionUN United NationsUNCDF United Nations Capital Development FundUNCHS United Nations Centre for Human SettlementsUNDP United Nations Development ProgrammeUNSMIL United Nations Support Mission in LibyaUSA United States of AmericaUSAID United States Agency for International DevelopmentUSD United States DollarUTB Union Togolaise de BanqueVAT Value added taxWAEMU West African Economic Monetary UnionWAMZ West African Monetary ZoneWHPI Women’s Housing Plan Initiative, NigeriaZAMFI Zimbabwe Association of Microfinance InstitutionsZAMCO Zimbabwe Asset Management CorporationZHPPF Zimbabwe Homeless and Poor People’s FederationZIMASSET Zimbabwe Agenda for Sustainable Socio-Economic transformationZINAHCO Zimbabwe National Association of Housing CooperativesZNBS Zambia National Building SocietyZSIC Zambia State Insurance Corporation

Overview

Africa Housing Finance Yearbook 2015

If cities are built the way they are financed1 (Renaud, 1984), then Africa’s cities are set to change. Innovation in housing finance –in terms of products, players, andapproaches, not to mention target markets – is a key feature across the continent, creating new opportunities for investment and delivery. As both local andinternational investors chase growth opportunities in a sluggish global economy, they are employing diversification strategies to manage the risks of their traditionaltargets – and in this, residential property is increasingly becoming an option. And while established players are getting better at what they do, new players are addingto the mix and competing for opportunities.

Investors are faced with a paradox, however. By their very nature, they are drawn to the high income markets. It is in these markets that they can price adequatelyfor risk and realise the returns they seek. However, the real story – the scale opportunity just waiting to be cracked – is in the lower income market segments.The arguments for investment in residential – high urbanisation rates, a growing middle class, a shortage of supply – these are all arguments for moving down marketinto the uncharted waters of affordable housing. Can investors and developers do it? In 2015, this is a very real focus.

Of course, the challenges are not insignificant, and cannot be easily wished away. But increasingly, investors and developers are noting that the potential benefitsoutweigh the risks. And, as governments come to appreciate the potential that this interest offers, their efforts to streamline development processes and enabletheir local housing markets to grow are creating new opportunities that are beginning to change the face of African cities.

There are five stories that characterise Africa’s housing finance markets in 2015:

1. Innovation in financing 2. Growing awareness of the opportunity in residential3. The identification of niche markets and an appreciation of the affordability challenge4. Policy & regulatory evolution to match investor interest5. Growing experience and investor sophistication

1. Innovation in financing

A key challenge facing investors has been the inability to find investment targets in the residential real estate space that are sufficiently substantial to warrant theirattention. International and local institutional investors generally seek large investment targets where they can place their money and realise a steady return thatisn’t drained by the administrative and organisational weight of multiple projects. With the exception of South Africa, African housing markets lack the capacity toreceive big money. Developers haven’t the capacity to build housing at scale and municipalities haven’t the capacity to receive large scale housing developments.Some investors are noting a change, however: investment in large scale infrastructure – roads, energy, even telecommunications – clears the way and reduces someof the transaction costs associated with housing developments. As the African head of Real Estate Finance for Standard Bank, Gerhard Zeelie, says2 “economicgrowth and ongoing investments in infrastructure are opening up previously inaccessible markets.”

Given this, investors have been looking for innovative ways to make the connection between their capital and potential investment opportunities. The introductionof Real Estate Investment Trusts (REITs) is perhaps the most significant of these – these create a vehicle that investors understand and can trust, aggregating diversesources of funding from international and institutional investors through to households, and targeting them into a portfolio that extends beyond the limitations ofindividual projects.

REITs are new in Africa – having developed through the promulgation of legislation and issuing of regulations only in the past three years, in South Africa, Nigeria,Tanzania, Kenya, Ghana, Morocco, and Zimbabwe. Initially used for the retail and commercial real estate sectors, residential REITs are now also emerging. The firstresidential-only REIT in South Africa, Indluplace, listed on the Johannesburg Stock Exchange in June 2015. Promoted by Arrowhead Properties, which has beenbringing residential properties into its REIT portfolios since 2013, Indluplace focuses on affordable rental.

In some jurisdictions, the REIT legislation allows for a housing development focus. This was a Kenyan innovation, which allows for the Development REIT (D-REIT).Investors take some of the project risk, so the regulations limit D-REITs to professional investors. A D-REIT can be converted into an Income REIT (I-REIT) whichrealises returns through rental cash flows, when the bulk of the assets have completed the construction phase and rentals begin to flow3. In Tanzania, the CapitalMarkets and Securities Authority (CMSA) approved Watumishi Housing Company REIT in early 2015. WHC-REIT aims to mobilise funding for the developmentof low-middle income housing, both for sale and for rent, and the development of commercial properties. WHC-REIT was created explicitly to target public sectorworkers’ housing demand, and the Public Service Pension Fund, Government Employees Provident Fund, PPF Pension Fund, LAPF Pension Fund, National SecurityAuthority, National Health Insurance Fund, and National Housing Corporation are the unit holders. Over time, WHC-REIT intends to float units on the Dar esSalaam Stock Exchange to allow members of the public to also invest4.

Listed groups create a credibility on which investors can rely. As listed groups – REITs and others – explore the affordable property sector, investors can begin todevelop an understanding of this market opportunity through their arms-length relationships with developments that their investment in the REITs facilitate.

Another innovation whose practice has been evolving as its been tried in different countries, is the mortgage liquidity facility. Originally introduced in Africa withthe establishment of the Egyptian Mortgage Refinancing Company in 2007, this was soon followed by the establishment of the Tanzania Mortgage RefinanceCompany in 2010, the Caisse Regional de Refinancement Hypothecaire-UEMOA in 2012, and the Nigerian Mortgage Refinance Company in 2014. While thereare variations from one to the next, the model essentially allows for the liquidity facility to purchase mortgages from mortgage lenders, giving them the liquidity tofund further mortgages. In order to engage with multiple lenders, the facility requires standardisation of mortgages, which over time makes them more accessibleto investors. Access to funding from the liquidity facility both reduces the cost of capital and increases the loan tenor, which in turn makes the mortgages muchmore affordable to borrowers, and lower income borrowers can then also participate. An increase in effective demand on this basis encourages developers tobuild to this market, and over time, the virtuous cycle sees more housing at more affordable prices for a widening market of borrowers5.

Mortgage markets across Africa are tiny by international comparisons, but this is part of their attraction – there is space to grow. Lower interest rates, achievablein part through liquidity facilities, seem to correlate with larger mortgage markets. But it is still early days and our data collection is imprecise. The data illustrated

1

30

25

20

15

10

5

0

Mortgage to GDP vs prevailing mortgage interest rate and term

Com

oros

(201

5)

Sout

h Af

rica

(201

4)

Cape

Ver

de (2

013)

Nam

ibia

(201

1)

Mau

ritiu

s (2

011)

Tuni

sia

(Bad

ev e

t al)

Bots

wan

a (2

013)

Mor

occo

(Bad

ev e

t al)

Rwan

da (2

013)

Keny

a (2

013)

Seyc

helle

s (2

013)

Zim

babw

e (2

012)

Zam

bia

(201

2)

Buru

ndi (

2013

)

Djib

outi

(201

5)

Liby

a (2

015)

Ugan

da (2

012)

Nige

ria (2

011)

Cam

eroo

n (W

B 20

05)

Mal

awi (

2004

)

Togo

(Bad

ev e

t al)

Tanz

ania

(201

4)

Libe

ria (2

008)

Ghan

a (2

010)

Moz

ambi

que

(200

8)

Cent

ral A

frica

n Re

publ

ic (W

B 20

05)

Sene

gal (

2010

)

Mor

tgag

e to

GDP

(per

cent

)

Of course, mortgages are only feasible when they’re affordable. Mortgage rates above fifteen percent, and offered at tenors below ten years, are unhelpful. Beyondthe factors that liquidity facilities address, macro-economic factors – the pricing of Treasury Bill rates, inflation, the availability of long term capital, the strength ofcapital markets, and so on – are behind a lender’s ability to make the mortgage work. In Malawi, a borrower might as well buy their house with their credit card.It is unsurprising therefore, that mortgages comprise only 0.5 percent of GDP. Interestingly, a number of countries are offering mortgages at rates below 15 percentand for tenors over 15 years, and some now at even less than 10 percent and over 20 years.

28

22.54 22.15

18.21

12.99

9.25

6.59

3.85 3.64 3.53 3.31 2.831.29 1.16 1 1 0.9 0.58 0.5 0.5 0.49 0.46 0.34 0.25 0.14 0.07 0.07

35

30

25

20

15

10

5

0

Prevailing mortgage interest rates, and term

Mor

tgag

e in

tere

st ra

te (%

) and

term

(yea

rs)

Mal

awi

Ugan

da

Sier

ra L

eone

Nige

ria

Gam

bia

Moz

ambi

que

Com

oros

Tanz

ania

Zam

bia

Sout

h Su

dan

DRC

Rwan

da

Keny

a

Buru

ndi

Cote

d' I

voire

Cent

ral A

frica

n Re

publ

ic

Ango

la

Cam

eroo

n

Beni

n

Burk

ina

Faso

Seyc

helle

s

Zim

babw

e

Eritr

ea

Mad

agas

car

Ethi

opia

Guin

ea-B

issa

u

Sene

gal

Mal

i

Nam

ibia

Leso

tho

Sout

h Af

rica

Djib

outi

Liby

a

Togo

Chad

Mau

ritiu

s

Nige

r

Som

alia

Tuni

sia

Libe

ria

Ghan

a

Alge

ria

Mor

occo

Egyp

t

n Mortgage interest rate %l Mortgage term

n Average mortgages % of GDP▲ Mortgage interest rate in 2015 (%)

n Mortgage term (years)... Linear (Mortgage interest rate in 2015%)

35

30

25

20

15

10

5

0

Mortgage interest rate (percent) and term

(years)

in the following graph comes from multiple sources – central banks, the Housing Finance Information Network (Hofinet), the World Bank, and from CAHF’s ownresearch. Aside from North African and certain markets such as South Africa and Namibia, most countries barely achieve 5 percent mortgage debt to GDP.Growing these markets will not only encourage investors to treat them more seriously, they will also encourage developers to be more targeted in their delivery,and this will support the economic development that the rest of the world knows goes with housing.

Source: Hofinet, World Bank, CAHF research, other sources.

Source: CAHF Research, September 2015.

2

Africa Housing Finance Yearbook 2015

Of course, exposure is still very limited. If booming Kenya is celebrated for its mortgage market of just over 22 013 mortgages as at the end of 2014, then weknow mortgage markets are tiny and we can suspect that there is a substantial opportunity for growth.

As mortgage markets develop further, they create exit opportunities for developers and construction financiers, supporting further investment in residentialdevelopment, greater housing supply, and the growth of cities with more formal housing. New financing approaches are changing the shape and look of African cities.

2. Growing awareness of the opportunity in residential

The investment potential in Africa is, of course, not new. Since the early “Africa rising” narrative, analysts have been citing the potential to be found in a young,growing middle class becoming economic participants in countries where the rate of urbanisation outpaces the rate of population growth. This, together with thecommodities boom, spurred investment in infrastructure, which then facilitated investment in real estate – largely commercial and retail. In 2014, foreign directinvestment into real estate was second behind coal, oil and natural gas, comprising 14 percent market share and US$12 billion6. South African retailers pushednorth into Zambia, Botswana, Mozambique, Tanzania, Kenya, Nigeria, Ghana, seeking new markets. New shopping malls were opened, and the “African real estatemarket” became a focus of more detailed analysis and investor interest. With the commodities downturn, the fall in the oil price, and the depreciation of manylocal currencies against the strengthening dollar, however, investors are being forced to diversify their strategies. Their local experience has shown them the housingbacklogs that beset virtually all African cities, and while they now have a better understanding of the target market, residential becomes a new opportunity.

Arrowhead, a REIT operating in South Africa, has a diverse portfolio, including office, retail, industrial and residential real estate. In an environment where mortgagelending is increasingly constrained, Arrowhead has positioned itself as an exit for residential property developers. It is these global forces on capital and oninvestment opportunities that are shifting a focus towards residential as a parallel investment strategy. PwC’s Global Real Estate Leader, Kees Hage, says7 that “realestate investors have a wide range of issues to consider when making investment decisions. What is clear is that they may have to approach those decisions in acompletely different way in the future. Capital allocations may need to be made to a wider range of asset types than ever before, ranging from retirement andstudent housing to data centres and self storage.”

Promoting the residential construction industry is also a diversification strategy for the public sector. In Nigeria, the emphasis on the residential real estate sectorcomes at the same time as the oil price has fallen by 40 percent. Can Nigeria shift its economic drivers away from commodities and use housing as its engine forgrowth? This must be at least in part what is behind the central government’s enabling interventions into real estate. In the past four years, Nigeria’s real estatesector has grown to become one of the main, non-oil sector contributors to the country’s rebased GDP, contributing 11 percent by 2014. It is estimated that theN6.5 trillion market will grow at an average of ten percent over the next few years. The 2015 Real Estate Review8 explicitly states that “the major growth driversin the sector have been credited to: an increased inflow of foreign investment; increased institutional investment from local companies including PFAs and MutualFunds; the growing population of High Net Worth individuals; and the targeted intervention of the Federal Government in the housing finance sector.”

3. The identification of niche markets and an appreciation of the affordability challenge

And yet, the enthusiasm with residential will be misplaced if it is only focused on the top end. The bulk of the backlog is not in the high end property market, butrather in what is being called the affordable market – home to new entrants to the middle class. Affordability is higher in urban areas, of course, where residentsare more likely to have an income stream that can support a long term mortgage obligation – but even so, less than ten percent of households across the continentare likely to afford a mortgage for even the cheapest, newly built house, built by a private developer.

CAHF has been collecting data on house prices across Africa for the past six years. We ask two simple questions: what is the price of the cheapest, newly builthouse, built by a private developer, and what is the size of that house. The answers we receive tell us nothing about scale – we have no idea if enough of thesehouses are being built annually to satisfy demand, though we suspect that in most cases they’re not. And because most countries do not collect this data in anyformal way, the information we receive cannot be taken as representative – the responses we receive are based on the opinions and experience of the respondents.However, it gives us an indication of the range of house prices, the possible relationship this may have to size, and what this means for housing affordability.

$200 000

$180 000

$160 000

$140 000

$120 000

$100 000

$80 000

$60 000

$40 000

$20 000

$0

250

200

150

100

50

0

Price of the cheapest, newly built house by a formal developer

Mor

tgag

e in

tere

st ra

te (%

) and

term

(yea

rs)

Size of that house (m2)

Ango

la

Seyc

helle

s

Guin

ea-B

issa

u

Mad

agas

car

Com

oros

Som

alia

Eritr

ea

Bots

wan

a

Zam

bia

Gam

bia

Liby

a

Cam

eroo

n

DRC

Ethi

opia

Rwan

da

Sout

h Su

dan

Alge

ria

Mau

ritiu

s

Djib

outi

Sier

ra L

eone

Sout

h Af

rica

Tuni

sia

Buru

ndi

Ghan

a

Sene

gal

Tanz

ania

Cent

ral A

frica

n Re

publ

ic

Nam

ibia

Zim

babw

e

Keny

a

Nige

ria

Beni

n

Leso

tho

Mor

occo

Mal

awi

Ugan

da

Swaz

iland

Nige

r

Burk

ina

Faso

Egyp

t

Togo

Mal

i

Moz

ambi

que

n Price of the cheapest, newly built house by a formal developer in 2015 (US$)n Price of the cheapest newly built house, by a formal developer in 2014 (US$)n Price of the cheapest newly built house, by a formal developer in 2013 (US$)n Price of the cheapest newly built house, by a formal developer in 2012 (US$)n Price of the cheapest newly built house, by a formal developer in 2011 (US$) ▲ What is the size of this house (in m2) in 2015?

Source: Annual CAHF survey of local housing practitioners

3

If we compare this data with average annual household income in urban and rural areas, we can see some countries with very serious gaps, which, in most cases,are not easily overcome with end-user finance.

Given these affordability challenges, and the very real need and obvious demand for housing, investors and developers are targeting specific niche markets that pulltogether resources in innovative ways. An important niche is the rental market. This was the focus of two recent symposia hosted by development financier ShelterAfrique this year, one of which was in Ghana. Across these two events, proponents highlighted the opportunity for regular cash flow and increasing rentals as ahedge against the long term expectation for property appreciation. The rental sector offers strong synergies with pension fund liabilities, and provides opportunitiesfor diversification. Demand is obvious: Africa’s cities are welcoming streams of new migrants, and the middle class is young and both upwardly and geographicallymobile in their pursuit of employment. This, plus the simple absence of housing for ownership, makes rental an obvious target. And critically, a growing track recordis showing impressive results.

Within the rental sector, student housing has been a critically overlooked housing niche. A key challenge in making this market segment work, has been the needfor property managers that are specialist in this market segment. As the demand for diversification shifts practitioners in the direction of residential, however, thestudent niche offers a focus that is attracting some investors.

In many countries, housing investors are targeting employers, whether public or private, as critical role players that can facilitate their workers’ access to the resourcesthey need to pay for their housing. In South Africa, Pretoria Portland Cement has embarked on a “Home Owners Support Programme”, assisting its lower gradeemployees to improve their housing circumstances9.

Certainly, a key determinant of market demand is income – both in terms of quantum and source. The graphs that follow provide an indication of the nuance ofthis demand. This sort of market segmentation can enable a more careful targeting, and changes the affordability challenge. While the majority of households cannotafford the mortgage that would buy them the cheapest, newly built house by a private developer, they may afford to buy a plot of land, servicing it collectively withmembers of their community, and then financing the incremental construction of their housing in stages, using housing microfinance.

As we better understand the size and scope of housing affordability – even at the very general level offered by these graphs – we can better understand whatsorts of investment can be targeted where, and what sort of market will support these kinds of decisions.

$40 000

$35 000

$30 000

$25 000

$20 000

$15 000

$10 000

$5 000

$0

Average annual household income and housing affordability

Mau

ritiu

sSe

yche

lles

Bots

wan

aSw

azila

ndTu

nisi

aNa

mib

iaGa

bon

Sout

h Af

rica

Ango

laAl

geria

Mor

occo

Djib

outi

Cabo

Ver

deNi

geria

Cote

d'Iv

oire

Zim

babw

eEq

uato

rial G

uine

aEg

ypt

Liby

aSe

nega

lLe

soth

oSu

dan

Sao

Tom

e an

d Pr

inci

peM

aurit

ania

Zam

bia

Cam

eroo

nCo

mor

osGh

ana

Keny

aSi

erra

Leo

neTo

goGa

mbi

aBe

nin

Ugan

daGu

inea

-Bis

sau

Burk

ina

Faso

Moz

ambi

que

Mal

iDR

CSo

uth

Suda

nLi

beria

Rwan

daTa

nzan

iaBu

rund

iGu

inea

Mal

awi

Nige

rCh

adEt

hiop

iaSo

mal

iaCe

ntra

l Afri

can

Repu

blic

Mad

agas

car

Eritr

ea

n Average, annual HH Income (urban, 2014)n Average, annual HH Income (rural, 2014)▲ Average Annual HH Income required to afford the cheapest newly built house built by a private developer, at current mortgage rates (2015)

$65 925 $200 000 $78 567 $65 057

Source: Annual CAHF survey of local housing practitioners and C-GIDD data

4

Africa Housing Finance Yearbook 2015

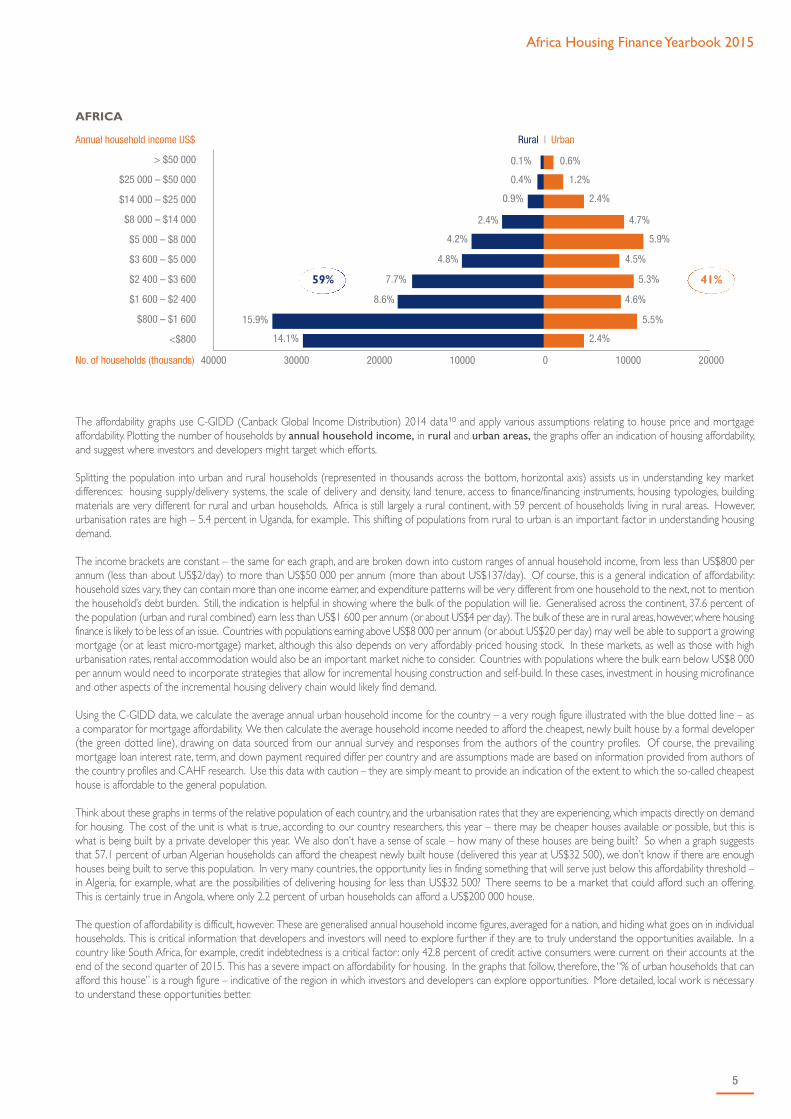

The affordability graphs use C-GIDD (Canback Global Income Distribution) 2014 data10 and apply various assumptions relating to house price and mortgageaffordability. Plotting the number of households by annual household income, in rural and urban areas, the graphs offer an indication of housing affordability,and suggest where investors and developers might target which efforts.

Splitting the population into urban and rural households (represented in thousands across the bottom, horizontal axis) assists us in understanding key marketdifferences: housing supply/delivery systems, the scale of delivery and density, land tenure, access to finance/financing instruments, housing typologies, buildingmaterials are very different for rural and urban households. Africa is still largely a rural continent, with 59 percent of households living in rural areas. However,urbanisation rates are high – 5.4 percent in Uganda, for example. This shifting of populations from rural to urban is an important factor in understanding housingdemand.

The income brackets are constant – the same for each graph, and are broken down into custom ranges of annual household income, from less than US$800 perannum (less than about US$2/day) to more than US$50 000 per annum (more than about US$137/day). Of course, this is a general indication of affordability:household sizes vary, they can contain more than one income earner, and expenditure patterns will be very different from one household to the next, not to mentionthe household’s debt burden. Still, the indication is helpful in showing where the bulk of the population will lie. Generalised across the continent, 37.6 percent ofthe population (urban and rural combined) earn less than US$1 600 per annum (or about US$4 per day). The bulk of these are in rural areas, however, where housingfinance is likely to be less of an issue. Countries with populations earning above US$8 000 per annum (or about US$20 per day) may well be able to support a growingmortgage (or at least micro-mortgage) market, although this also depends on very affordably priced housing stock. In these markets, as well as those with highurbanisation rates, rental accommodation would also be an important market niche to consider. Countries with populations where the bulk earn below US$8 000per annum would need to incorporate strategies that allow for incremental housing construction and self-build. In these cases, investment in housing microfinanceand other aspects of the incremental housing delivery chain would likely find demand.

Using the C-GIDD data, we calculate the average annual urban household income for the country – a very rough figure illustrated with the blue dotted line – asa comparator for mortgage affordability. We then calculate the average household income needed to afford the cheapest, newly built house by a formal developer(the green dotted line), drawing on data sourced from our annual survey and responses from the authors of the country profiles. Of course, the prevailingmortgage loan interest rate, term, and down payment required differ per country and are assumptions made are based on information provided from authors ofthe country profiles and CAHF research. Use this data with caution – they are simply meant to provide an indication of the extent to which the so-called cheapesthouse is affordable to the general population.

Think about these graphs in terms of the relative population of each country, and the urbanisation rates that they are experiencing, which impacts directly on demandfor housing. The cost of the unit is what is true, according to our country researchers, this year – there may be cheaper houses available or possible, but this iswhat is being built by a private developer this year. We also don’t have a sense of scale – how many of these houses are being built? So when a graph suggeststhat 57.1 percent of urban Algerian households can afford the cheapest newly built house (delivered this year at US$32 500), we don’t know if there are enoughhouses being built to serve this population. In very many countries, the opportunity lies in finding something that will serve just below this affordability threshold –in Algeria, for example, what are the possibilities of delivering housing for less than US$32 500? There seems to be a market that could afford such an offering.This is certainly true in Angola, where only 2.2 percent of urban households can afford a US$200 000 house.

The question of affordability is difficult, however. These are generalised annual household income figures, averaged for a nation, and hiding what goes on in individualhouseholds. This is critical information that developers and investors will need to explore further if they are to truly understand the opportunities available. In acountry like South Africa, for example, credit indebtedness is a critical factor : only 42.8 percent of credit active consumers were current on their accounts at theend of the second quarter of 2015. This has a severe impact on affordability for housing. In the graphs that follow, therefore, the “% of urban households that canafford this house” is a rough figure – indicative of the region in which investors and developers can explore opportunities. More detailed, local work is necessaryto understand these opportunities better.

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

AFRICA

Rural | UrbanAnnual household income US$

No. of households (thousands) 40000 30000 20000 10000 0 10000 20000

0.1% 0.6%

0.4% 1.2%

0.9% 2.4%

2.4% 4.7%

4.2% 5.9%

4.8% 4.5%

7.7% 5.3%

8.6% 4.6%

15.9% 5.5%

14.1% 2.4%

59% 41%

5

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

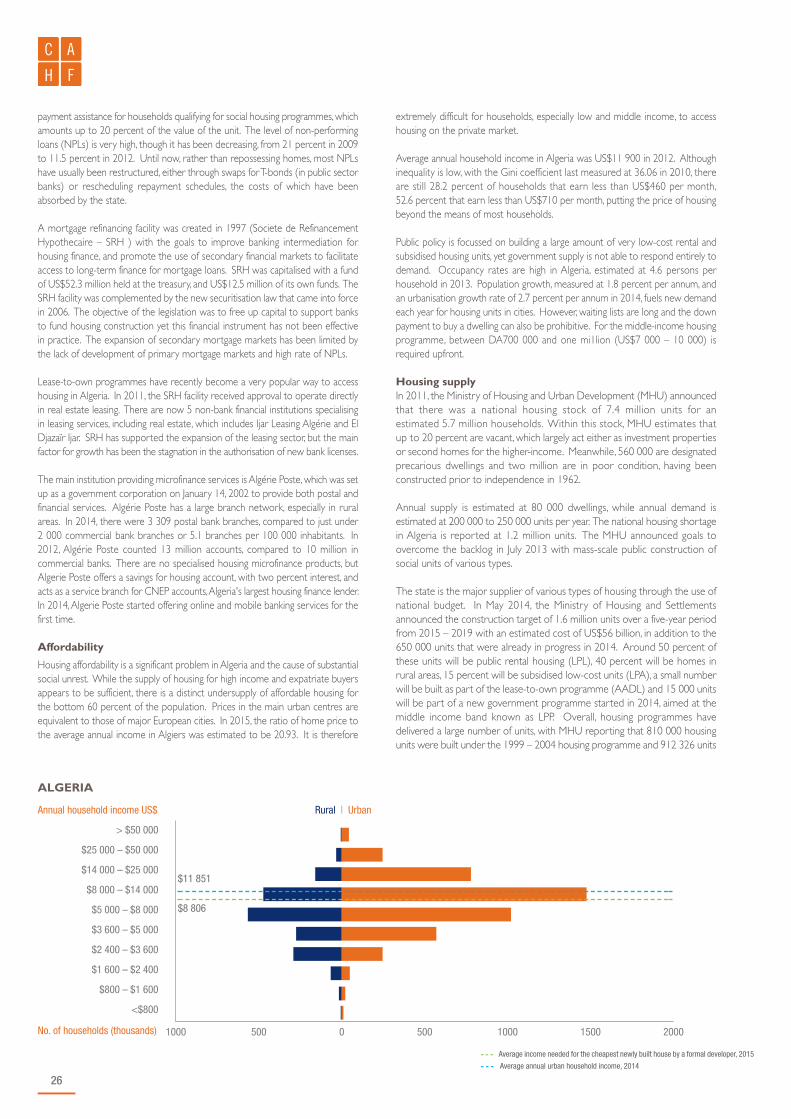

ALGERIA

$11 851

$8 806

Rural | UrbanAnnual household income US$

No. of households (thousands) 1000 500 0 500 1000 1500 2000

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

BENIN

$10 351

$3 514

Rural | UrbanAnnual household income US$

No. of households (thousands) 500 400 300 200 100 0 100 200 300

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

ANGOLA

$108 638

$12 408

Rural | UrbanAnnual household income US$

No. of households (thousands) 800 400 200 0 200 400 600

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

BOTSWANA

$26 564

$16 194

Rural | UrbanAnnual household income US$

No. of households (thousands) 60 40 20 0 20 40 60 80

Population:24 400 000

Urbanisation rate:4.88

Cost of Unit (US$):200 000

% of urban households that can afford this house:

2.2%

Population:10 599 510

Urbanisation rate:3.63

Cost of Unit (US$):15 188

% of urban households that can afford this house:

6.8%

Population:20 38 587

Urbanisation rate:1.3

Cost of Unit (US$):69 640

% of urban households that can afford this house:

19.0%

Population:39 928 947

Urbanisation rate:2.71

Cost of Unit (US$):32 500

% of urban households that can afford this house:

57.1%

6

Africa Housing Finance Yearbook 2015

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015- - - Average annual urban household income, 2014

BURKINA FASO

$2 761

$2 991

Rural | UrbanAnnual household income US$

No. of households (thousands) 1000 800 600 400 200 0 200 400

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

BURUNDI

$18 325

$2 210

Rural | UrbanAnnual household income US$

No. of households (thousands) 800 700 600 500 400 300 200 100 0 100 200

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2013- - - Average annual urban household income, 2014

CAMEROON

$24 084

$4 853

Rural | UrbanAnnual household income US$

No. of households (thousands) 800 600 400 200 0 200 400 600 800

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015- - - Average annual urban household income, 2014

CABO VERDE

$9 239

$12 052

Rural | UrbanAnnual household income US$

No. of households (thousands) 10 5 0 5 10 15 20

Population:17 419 615

Urbanisation rate:5.75

Cost of Unit (US$):8 429

% of urban households that can afford this house:

41.7%

Population:10 482 752

Urbanisation rate:5.59

Cost of Unit (US$):25 000

% of urban households that can afford this house:

0.4%

Population:22 818 632

Urbanisation rate:3.57

Cost of Unit (US$):42 163

% of urban households that can afford this house:

3.7%

Population:503 637

Urbanisation rate:2.05

Cost of Unit (US$):28 000

% of urban households that can afford this house:

36.5%

7

8

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015- - - Average annual urban household income, 2014

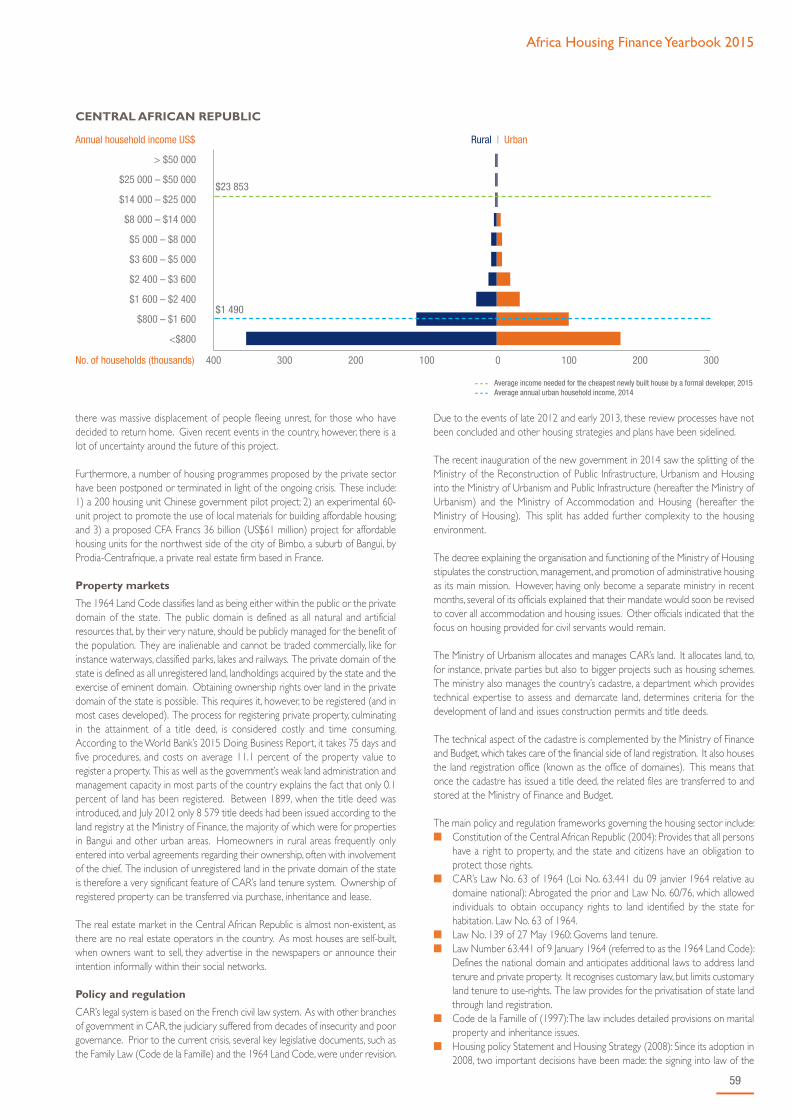

CENTRAL AFRICAN REPUBLIC

$23 853

$1 490

Rural | UrbanAnnual household income US$

No. of households (thousands) 400 300 200 100 0 100 200 300

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

CHAD

$15 582

$1 853

Rural | UrbanAnnual household income US$

No. of households (thousands) 1400 1200 1000 800 600 400 200 0 200 400

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average Income needed to purchase cheapest 3 bedroom semi-detached house, 2015

- - - Average annual urban household income, 2014

COMOROS

$78 567

$4 584

Rural | UrbanAnnual household income US$

No. of households (thousands) 30 25 20 15 10 5 0 5 10 15

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

CÔTE D'IVOIRE

$8 863

$6 718

Rural | UrbanAnnual household income US$

No. of households (thousands) 300 200 100 0 100 200 300 400

Population:4 709 203

Urbanisation rate:2.64

Cost of Unit (US$):20 229

% of urban households that can afford this house:

0.9%

Population:13 211 146

Urbanisation rate:3.48

Cost of Unit (US$):25 000

% of urban households that can afford this house:

0.4%

Population:752 438

Urbanisation rate:2.67

Cost of Unit (US$):131 000

% of urban households that can afford this house:

1.4%

Population:20 804 774

Urbanisation rate:3.72

Cost of Unit (US$):16 858

% of urban households that can afford this house:

59.1%

Africa Housing Finance Yearbook 2015

9

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

DEMOCRATIC REPUBLIC OF CONGO

$35 621

$2 551

Rural | UrbanAnnual household income US$

No. of households (thousands) 5000 4000 3000 2000 1000 0 1000 2000

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2013

- - - Average annual urban household income, 2014

DJIBOUTI

$12 621

$9 351

Rural | UrbanAnnual household income US$

No. of households (thousands) 10 5 0 5 10 15 20 25 30 35

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

EGYPT, ARAB REP.

$8 126

$4 178

Rural | UrbanAnnual household income US$

No. of households (thousands) 5000 4000 3000 2000 1000 0 1000 2000 3000 4000

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

ERITREA

$34 770

$1 074

Rural | UrbanAnnual household income US$

No. of households (thousands) 1000 800 600 400 200 0 200

Population:69 360 118

Urbanisation rate:3.93

Cost of Unit (US$):25 000

% of urban households that can afford this house:

0.3%

Population:886 313

Urbanisation rate:1.62

Cost of Unit (US$):30 000

% of urban households that can afford this house:

39.3%

Population:83 386 739

Urbanisation rate:1.71

Cost of Unit (US$):9 102

% of urban households that can afford this house:

86.3%

Population:6 536 176

Urbanisation rate:5.10

Cost of Unit (US$):90 901

% of urban households that can afford this house:

0.0%

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

ETHIOPIA

$17 152

$1 743

Rural | UrbanAnnual household income US$

No. of households (thousands) 8000 6000 4000 2000 0 2000 4000

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

GAMBIA, THE

$29 943

$3 582

Rural | UrbanAnnual household income US$

No. of households (thousands) 40 30 20 10 0 10 20 30 40 50

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

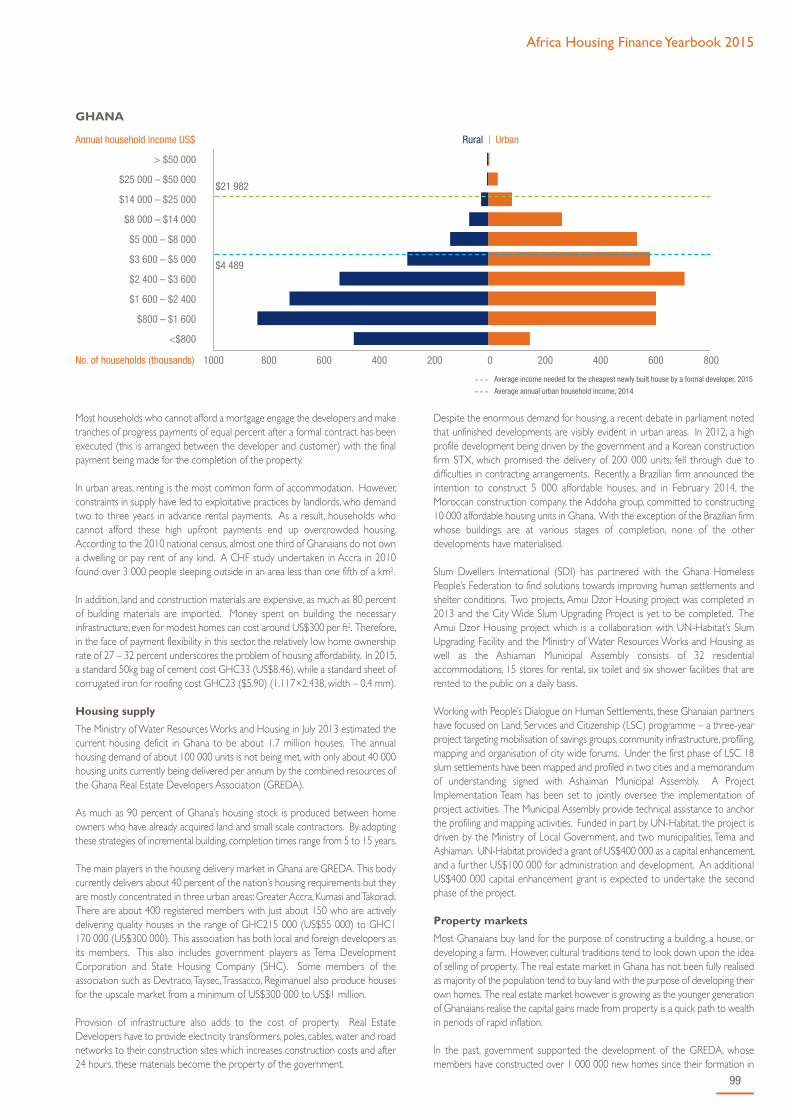

GHANA

$21 982

$4 489

Rural | UrbanAnnual household income US$

No. of households (thousands) 1000 800 600 400 200 0 200 400 600 800

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

GUINEA BISSAU

$89 892

$3 343

Rural | UrbanAnnual household income US$

No. of households (thousands) 50 40 30 20 10 0 10 20 30 40

Population:96 506 031

Urbanisation rate:4.85

Cost of Unit (US$):34 515

% of urban households that can afford this house:

0.1%

Population:1 908 954

Urbanisation rate:4.27

Cost of Unit (US$):50 000

% of urban households that can afford this house:

0.8%

Population:26 442 178

Urbanisation rate:3.29

Cost of Unit (US$):24 359

% of urban households that can afford this house:

3.4%

Population:1 745 798

Urbanisation rate:4.08

Cost of Unit (US$):153 429

% of urban households that can afford this house:

0.0%

10

Africa Housing Finance Yearbook 2015

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

KENYA

$8 821

$4 140

Rural | UrbanAnnual household income US$

No. of households (thousands) 3000 2500 2000 1500 1000 500 0 500 1000

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

LESOTHO

$6 578

$6 286

Rural | UrbanAnnual household income US$

No. of households (thousands) 80 70 60 50 40 30 20 10 0 10 20 30

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

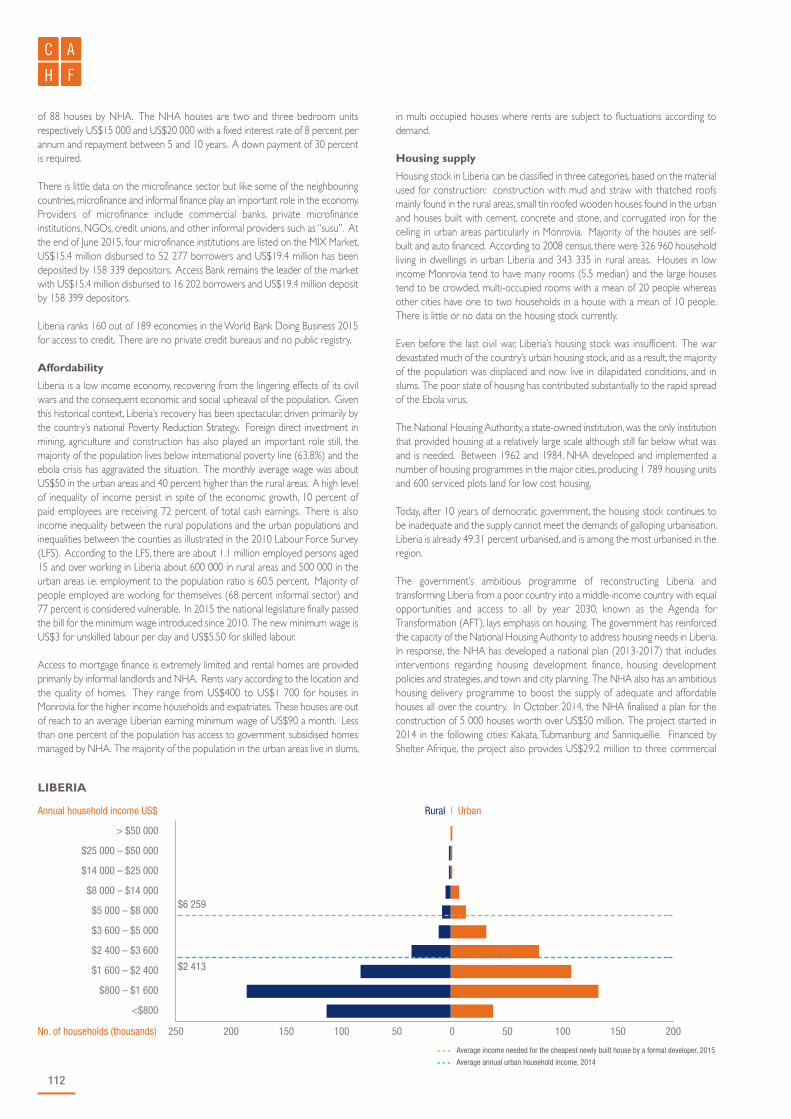

LIBERIA

$6 259

$2 413

Rural | UrbanAnnual household income US$

No. of households (thousands) 250 200 150 100 50 0 50 100 150 200

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2013

- - - Average annual urban household income, 2014

LIBYA

$18 013

$7 989

Rural | UrbanAnnual household income US$

No. of households (thousands) 100 50 0 50 100 150 200 250 300

Population:45 545 980

Urbanisation rate:4.32

Cost of Unit (US$):17 000

% of urban households that can afford this house:

10.2%

Population:2 097 511

Urbanisation rate:3.06

Cost of Unit (US$):14 615

% of urban households that can afford this house:

39.0%

Population:4 396 873

Urbanisation rate:3.15

Cost of Unit (US$):15 000

% of urban households that can afford this house:

5.9%

Population:6 253 452

Urbanisation rate:1.08

Cost of Unit (US$):50 000

% of urban households that can afford this house:

9.3%

11

12

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

MADAGASCAR

$65 057

$1 291

Rural | UrbanAnnual household income US$

No. of households (thousands) 3000 2500 2000 1 500 1000 500 0 500 1000

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

MALAWI

$14 666

$2 103

Rural | UrbanAnnual household income US$

No. of households (thousands) 2500 2000 1500 1000 500 0 500

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average income needed for the cheapest newly built house by a formal developer, 2015

- - - Average annual urban household income, 2014

MALI

$2 669

$2 259

Rural | UrbanAnnual household income US$

No. of households (thousands) 800 600 400 200 0 200 400

> $50 000

$25 000 – $50 000

$14 000 – $25 000

$8 000 – $14 000

$5 000 – $8 000

$3 600 – $5 000

$2 400 – $3 600

$1 600 – $2 400

$800 – $1 600

<$800

- - - Average annual urban household income, 2014

MAURITANIA

$5 167

Rural | UrbanAnnual household income US$

No. of households (thousands) 100 80 60 40 20 0 20 40 60 80 100

Population:23 571 962

Urbanisation rate:4.65

Cost of Unit (US$):138 000