2015 Budget Draft

236

Budget 2 0 1 5

Transcript of 2015 Budget Draft

Budget

2 0 1 5

This page intentionally left blank.

10747 Renner Boulevard Lenexa, KS 66219

913.895.5500 www.waterone.org

Adopted December 9, 2014

by the Board of Water District No. 1 of Johnson County, Kansas

BOARD: Brenda Cherpitel, Chair

Joe Vaughan, Vice Chair Terrence D. Frederick

H. Richard "Dick" Noon Robert S. Olson Robert P. Reese James E. Vader

FINANCE COMMITTEE: Robert P. Reese, Committee Chair

Terrence D. Frederick Robert S. Olson

SENIOR STAFF:

Mike Armstrong, General Manager Ron Appletoft, Director of Finance

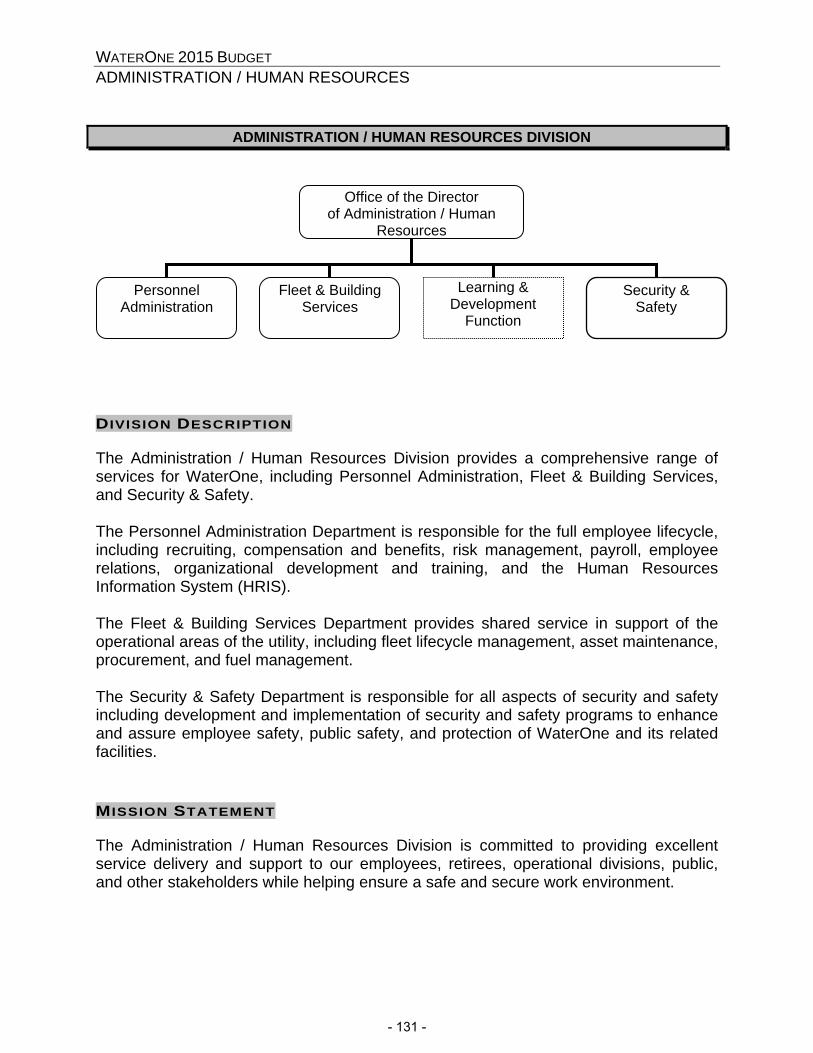

Eric Arner, Director of Legal / Auditing Colleen Browne, Director of Administration / Human Resources

C.J. George, Director of Information Technology Mandy Cawby and Dana Sargent Buhl, Acting Directors of Customer Relations

Tom Schrempp, Director of Production Dan Smith, Director of Distribution

This page intentionally left blank.

12/31/2014

EXECUTIVE SUMMARYExecutive Summary 1 - 7

OVERVIEWBudget Review and Approval Process 9Budget Process Diagram 10WaterOne Financial Overview 11Comparison of 2015 Proposed Budget to 2014 Budget 13Significant Account Summary By Category 14Explanation of Significant O&M Accounts 15 - 24Summary of Annual Capital 25

REVENUE & RATESRevenue Summary 27 - 28Water Rate Structure 29Billing Impact Comparison 30History of Water Sales By Rate Class 31Customer Growth 32History & Projection of Water Rates 33Water Rate Comparison with Neighboring Utilities 33Water Rates Compared to National Water & Sewer CPI 34History & Projection of Debt Service Coverage 34

O&MO&M By Division 35O&M By Category - All Accounts 36 - 40Comparison to Current Year Estimated Actuals 41 - 45

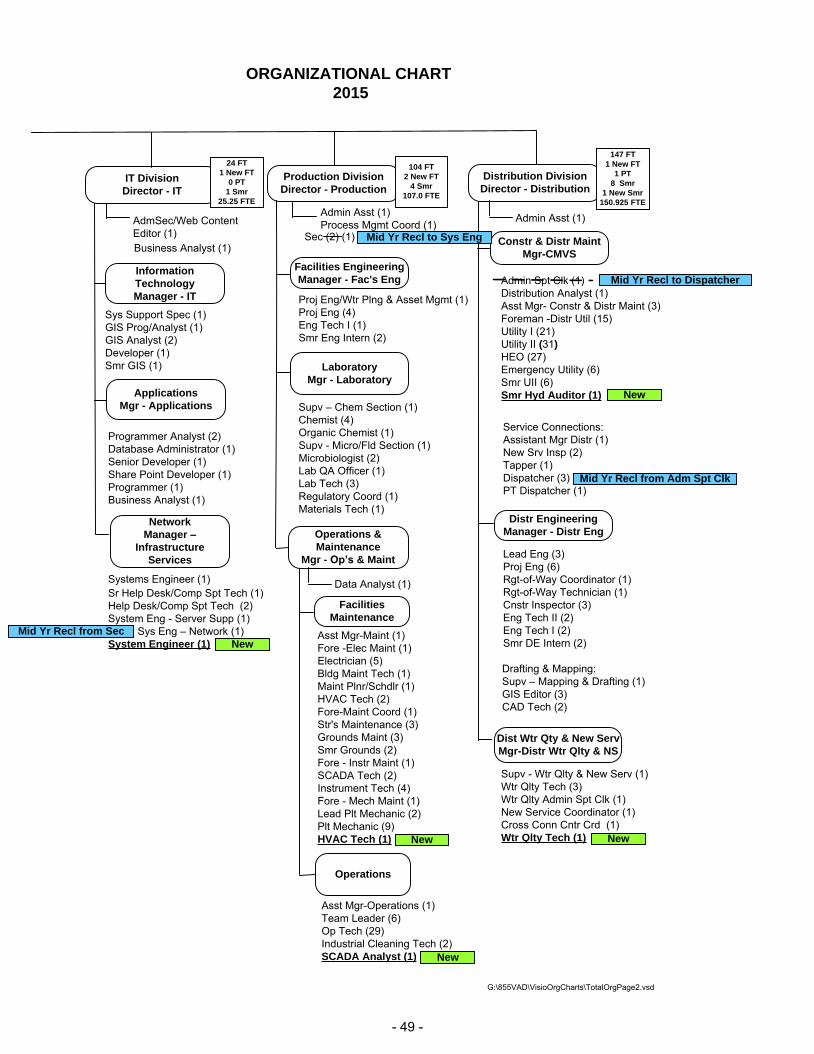

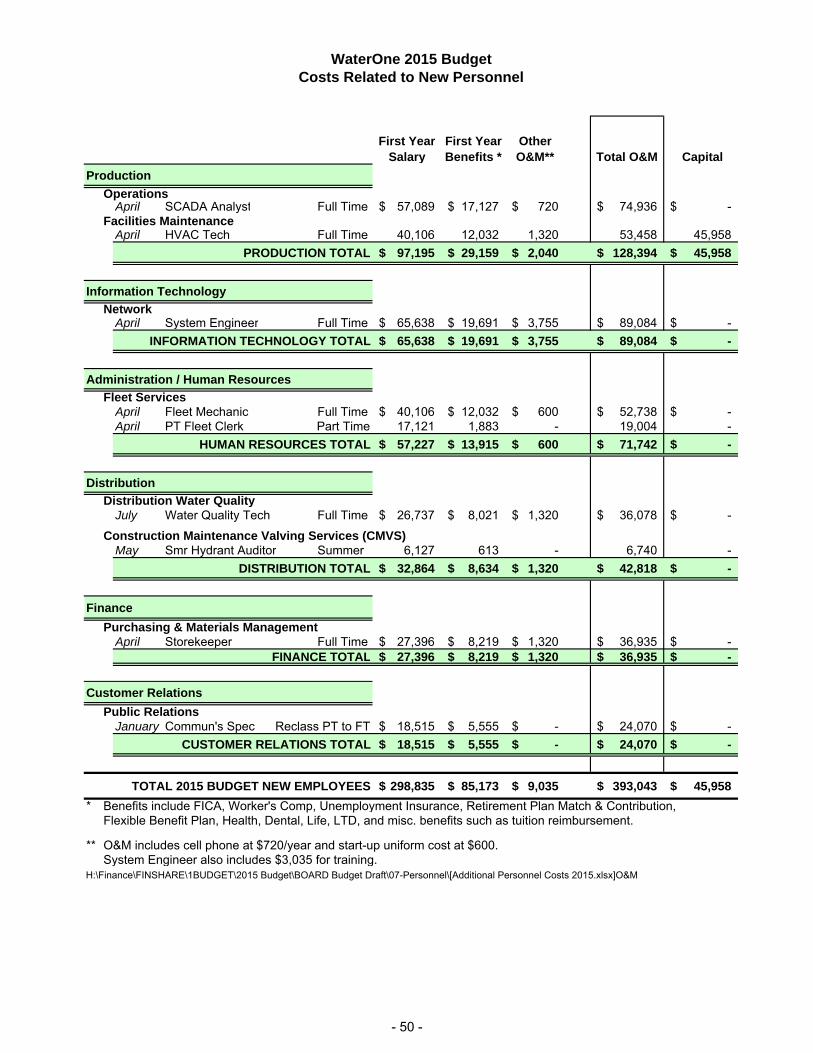

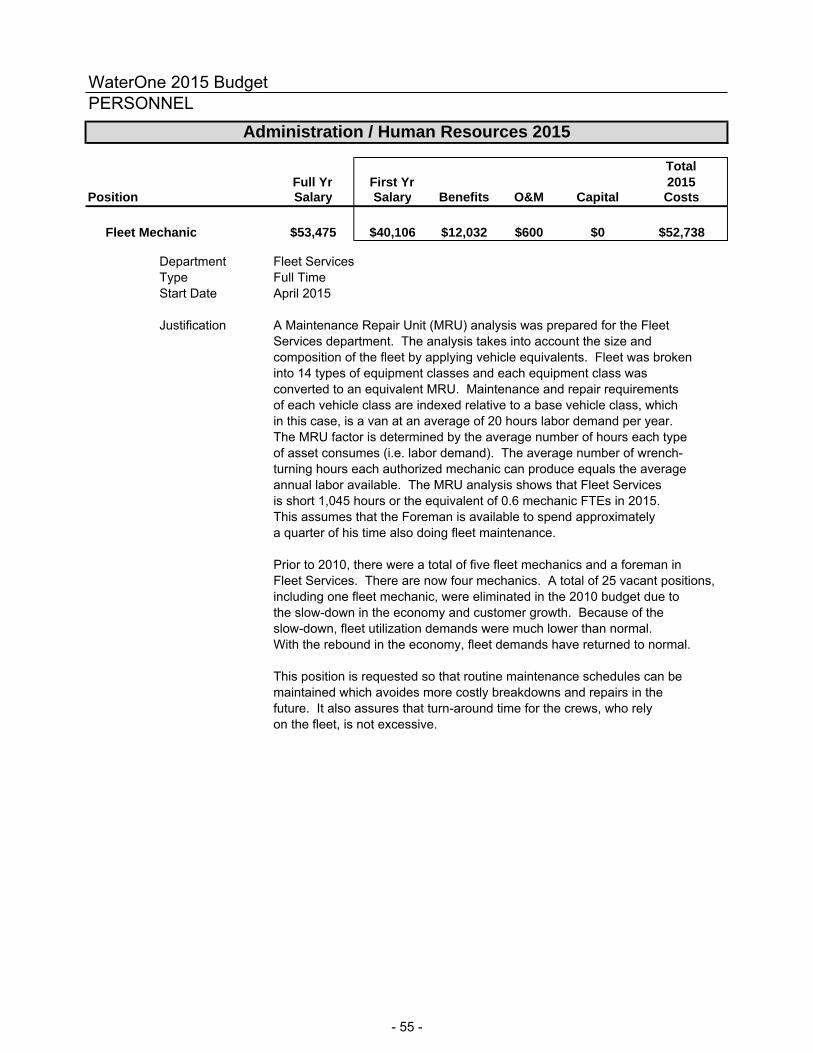

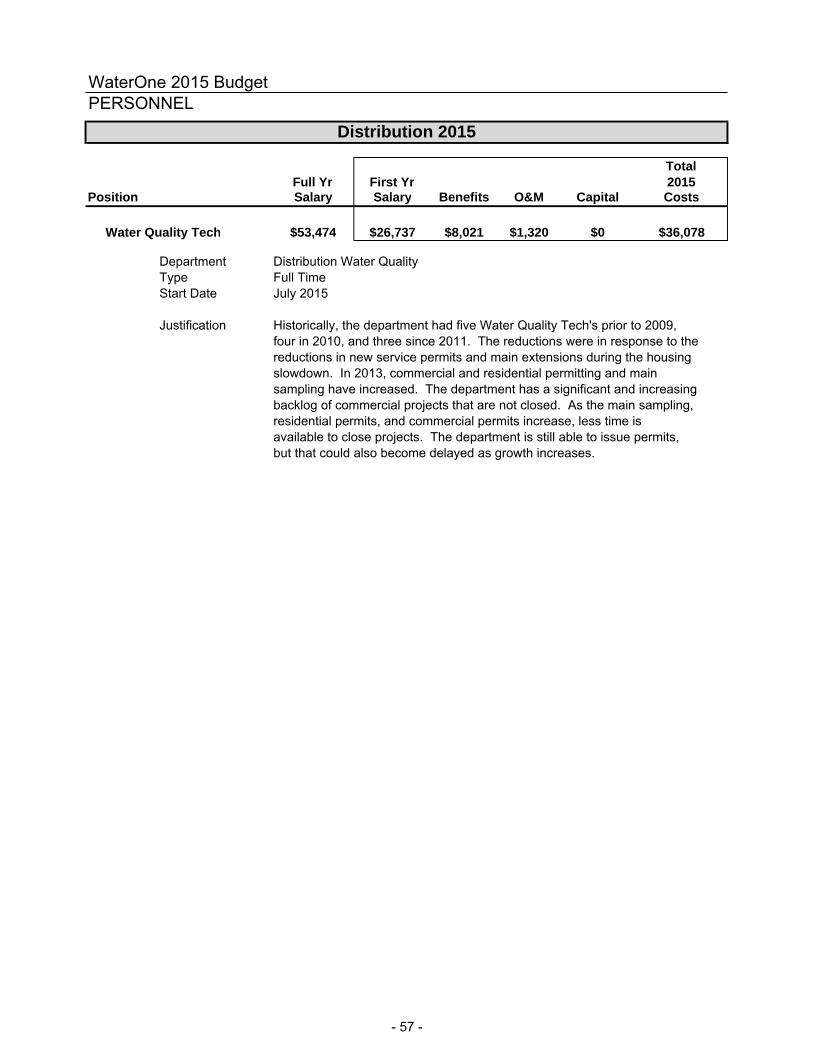

PERSONNEL Introduction 47WaterOne Organizational Chart (Detail) 48 - 49Summary of New Personnel Costs 50 - 51New Personnel Requests - Description 52 - 60Employee Benefits 61 - 6510-Year History of Full Time Equivalents 66Customers Served Per Employee 67

TABLE OF CONTENTS2015 Proposed Budget

TOC - 1

12/31/2014

TABLE OF CONTENTS2015 Proposed Budget

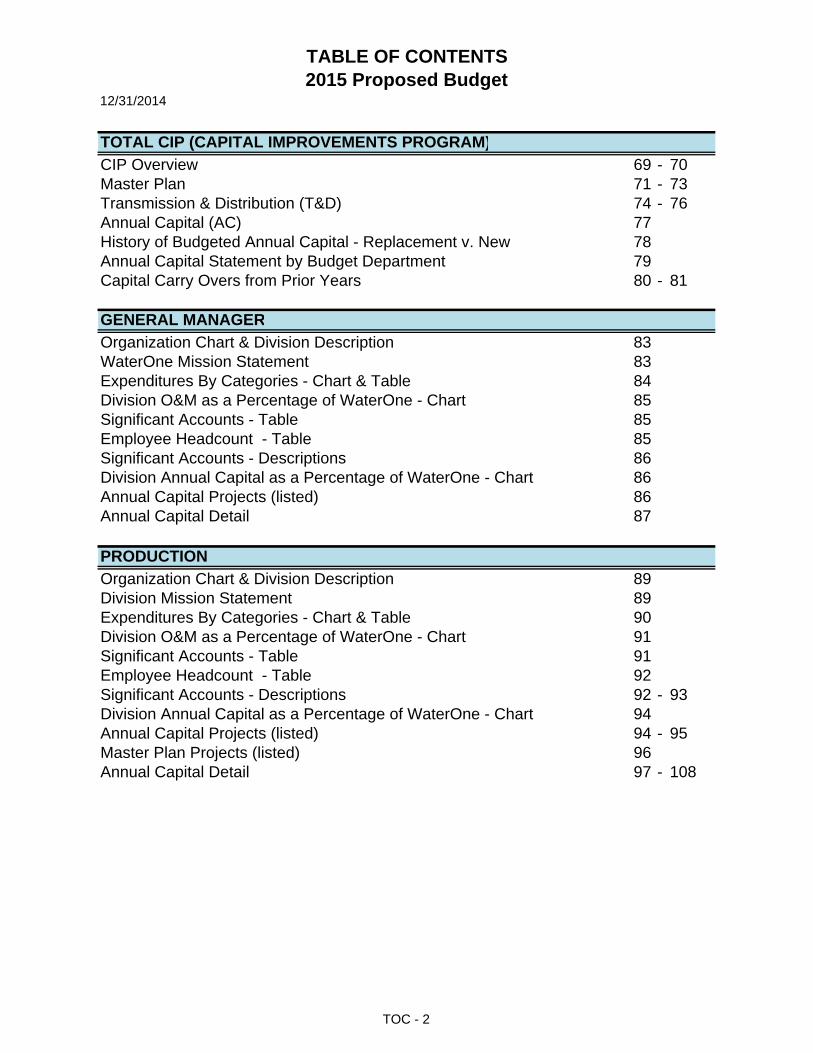

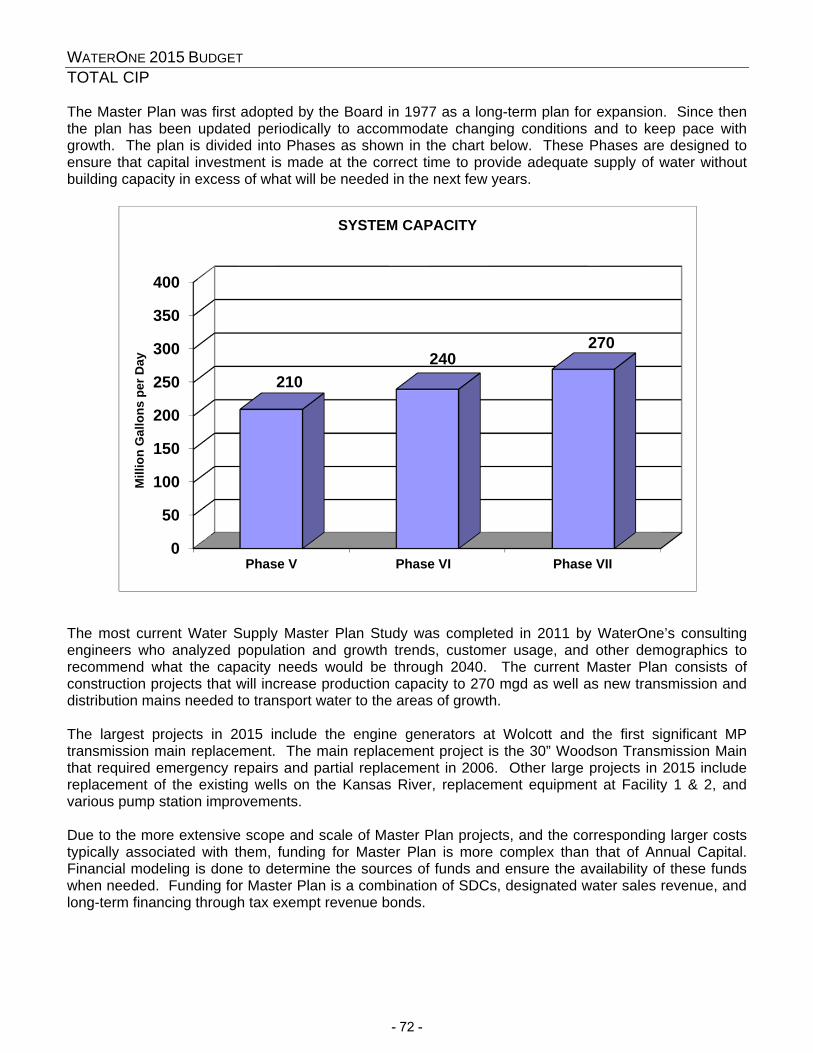

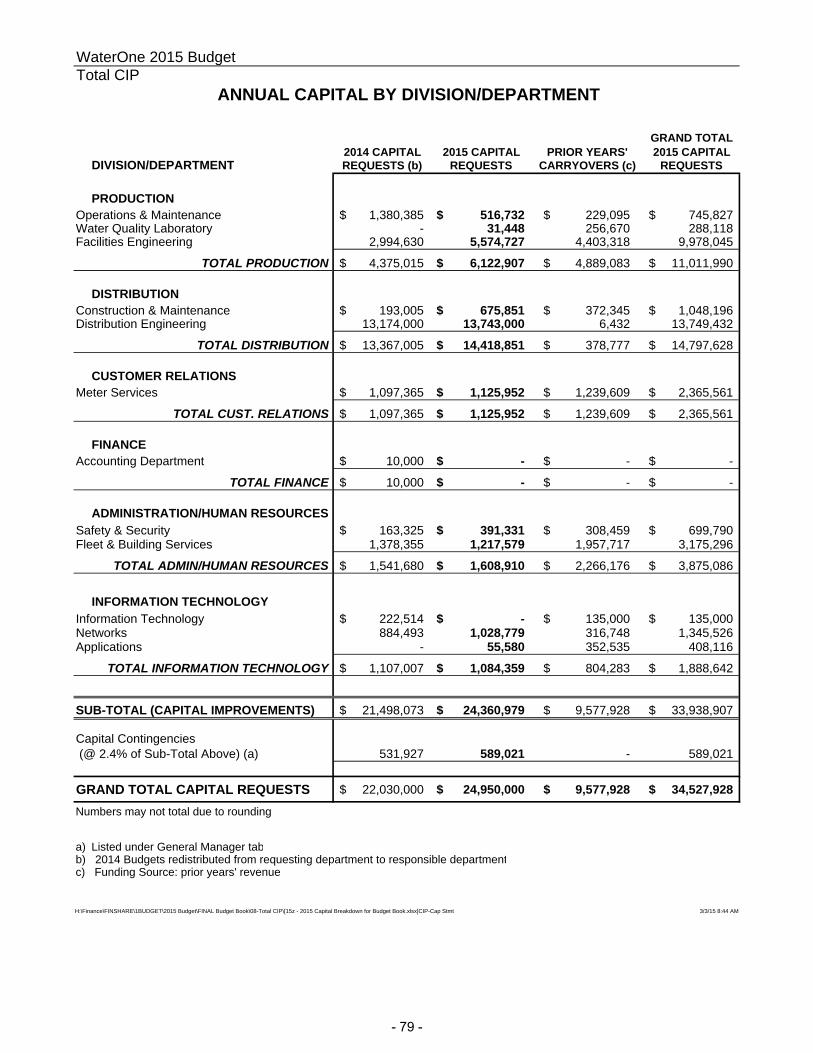

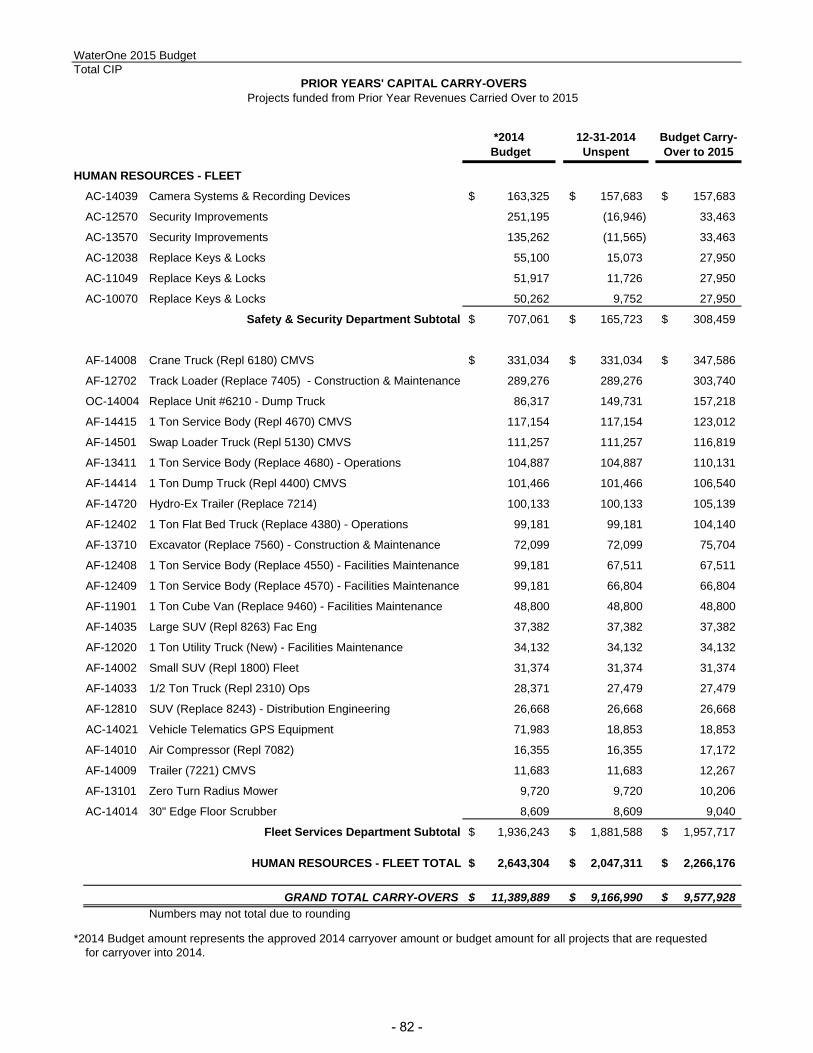

TOTAL CIP (CAPITAL IMPROVEMENTS PROGRAM)CIP Overview 69 - 70Master Plan 71 - 73Transmission & Distribution (T&D) 74 - 76Annual Capital (AC) 77History of Budgeted Annual Capital - Replacement v. New 78Annual Capital Statement by Budget Department 79Capital Carry Overs from Prior Years 80 - 81

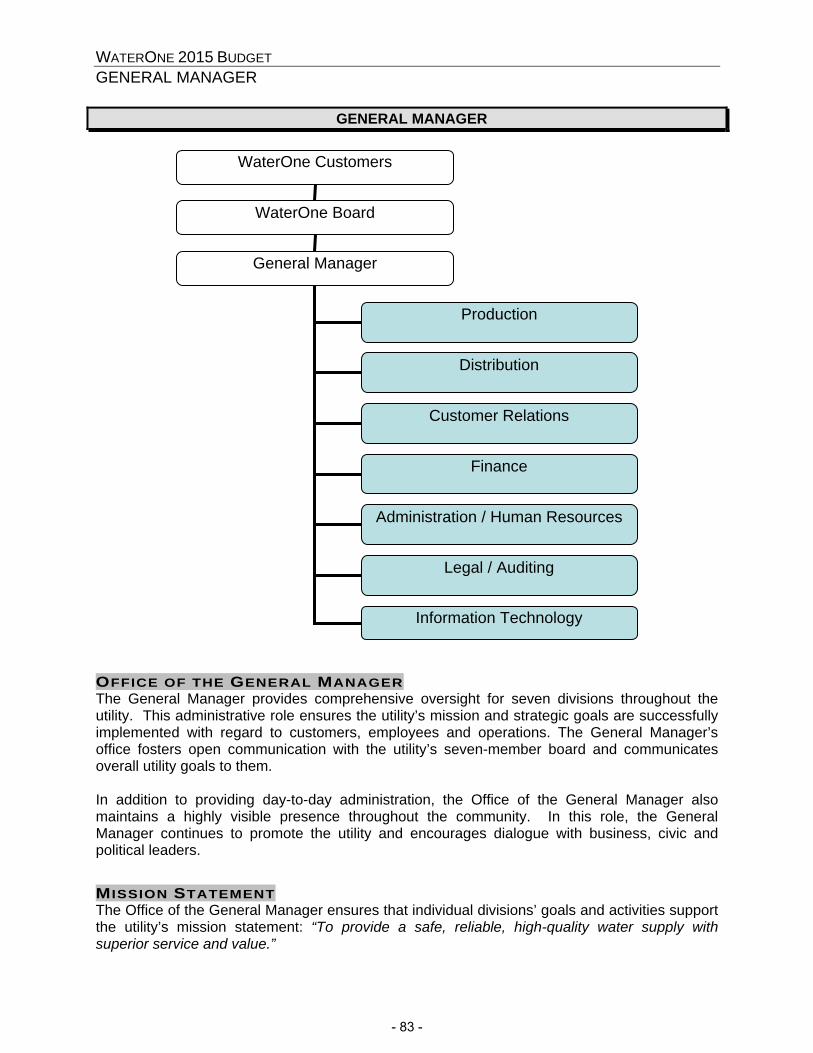

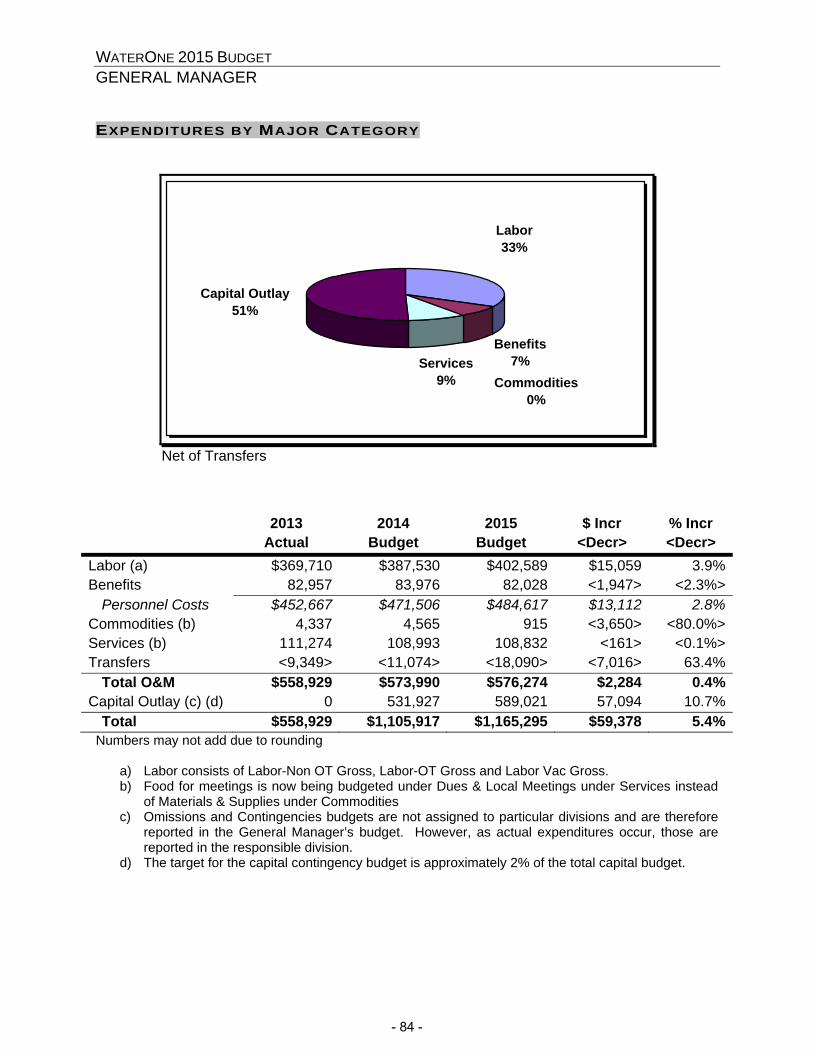

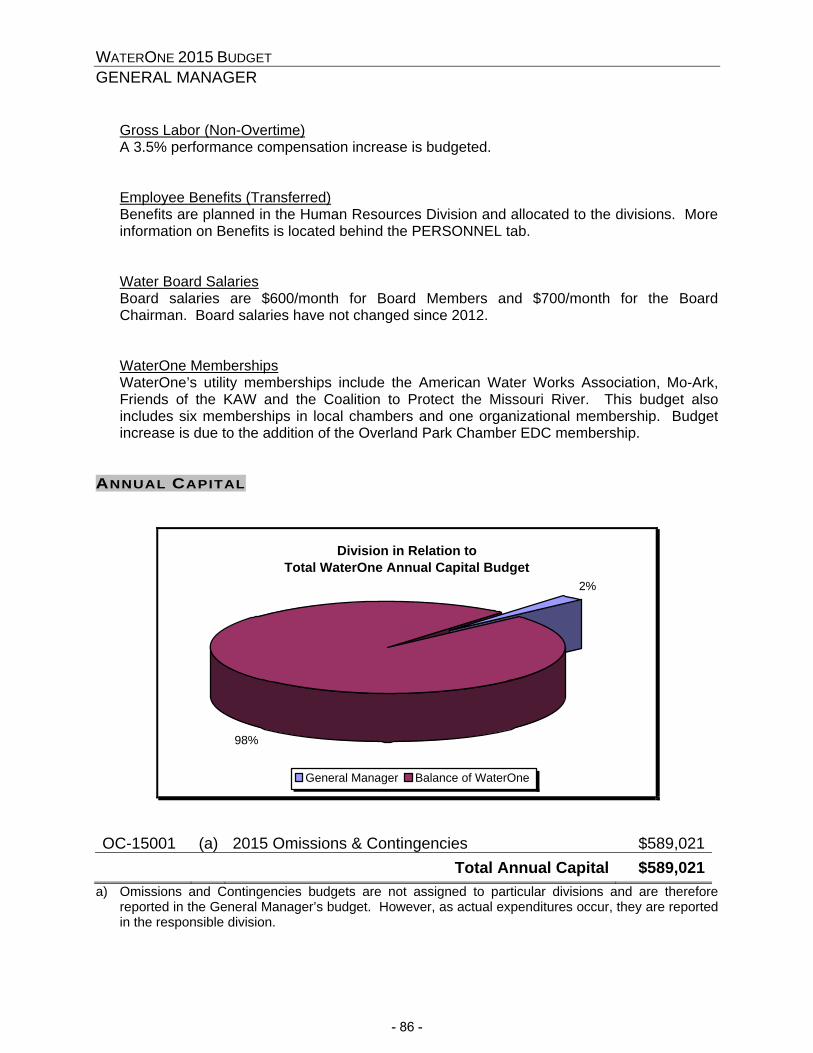

GENERAL MANAGEROrganization Chart & Division Description 83WaterOne Mission Statement 83Expenditures By Categories - Chart & Table 84Division O&M as a Percentage of WaterOne - Chart 85Significant Accounts - Table 85Employee Headcount - Table 85Significant Accounts - Descriptions 86Division Annual Capital as a Percentage of WaterOne - Chart 86Annual Capital Projects (listed) 86Annual Capital Detail 87

PRODUCTIONOrganization Chart & Division Description 89Division Mission Statement 89Expenditures By Categories - Chart & Table 90Division O&M as a Percentage of WaterOne - Chart 91Significant Accounts - Table 91Employee Headcount - Table 92Significant Accounts - Descriptions 92 - 93Division Annual Capital as a Percentage of WaterOne - Chart 94Annual Capital Projects (listed) 94 - 95Master Plan Projects (listed) 96Annual Capital Detail 97 - 108

TOC - 2

12/31/2014

TABLE OF CONTENTS2015 Proposed Budget

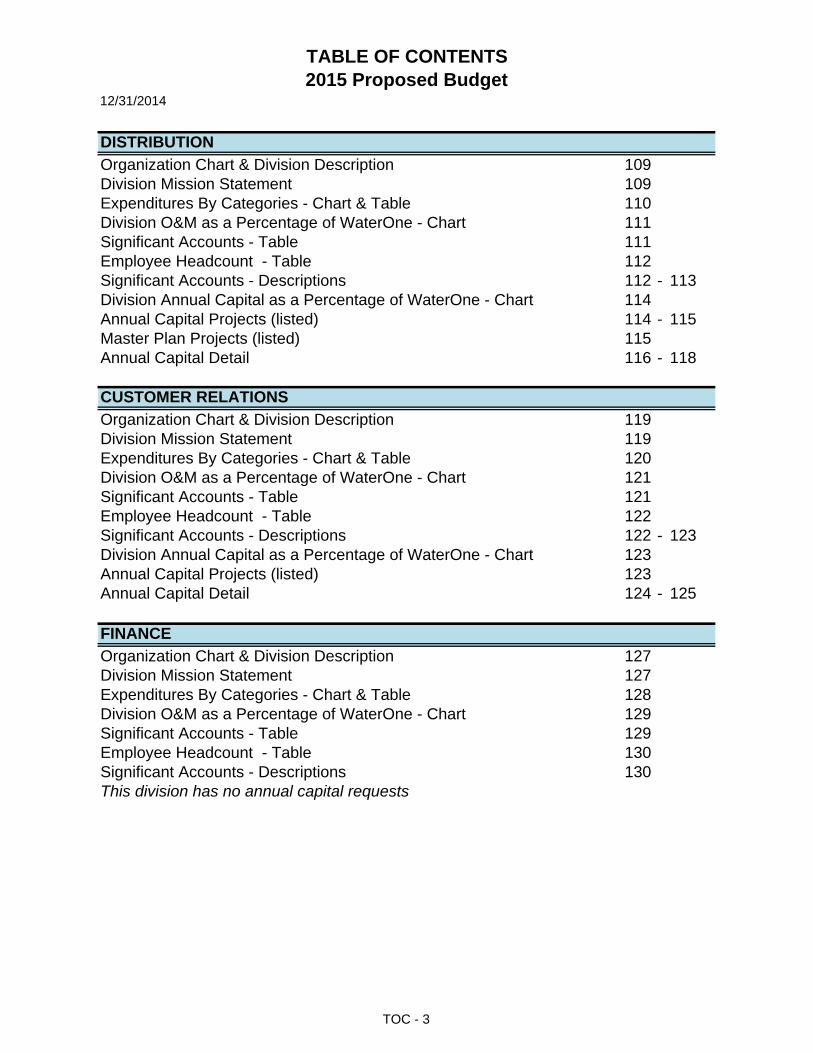

DISTRIBUTIONOrganization Chart & Division Description 109Division Mission Statement 109Expenditures By Categories - Chart & Table 110Division O&M as a Percentage of WaterOne - Chart 111Significant Accounts - Table 111Employee Headcount - Table 112Significant Accounts - Descriptions 112 - 113Division Annual Capital as a Percentage of WaterOne - Chart 114Annual Capital Projects (listed) 114 - 115Master Plan Projects (listed) 115Annual Capital Detail 116 - 118

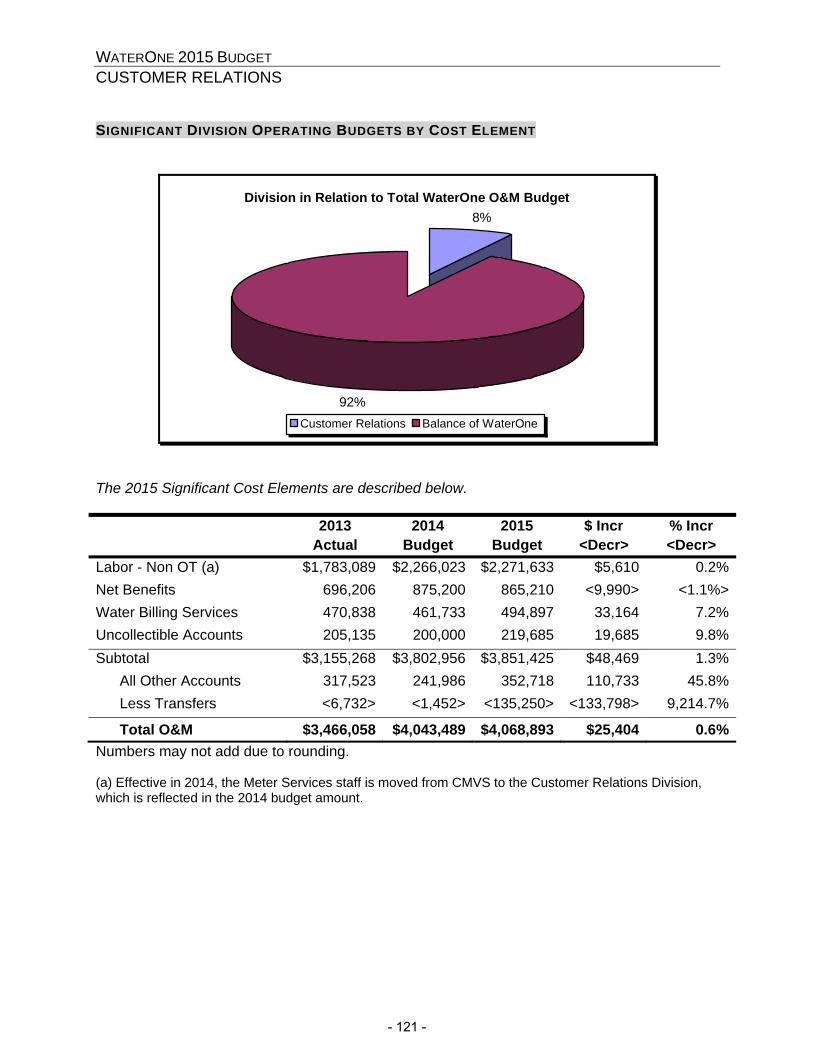

CUSTOMER RELATIONSOrganization Chart & Division Description 119Division Mission Statement 119Expenditures By Categories - Chart & Table 120Division O&M as a Percentage of WaterOne - Chart 121Significant Accounts - Table 121Employee Headcount - Table 122Significant Accounts - Descriptions 122 - 123Division Annual Capital as a Percentage of WaterOne - Chart 123Annual Capital Projects (listed) 123Annual Capital Detail 124 - 125

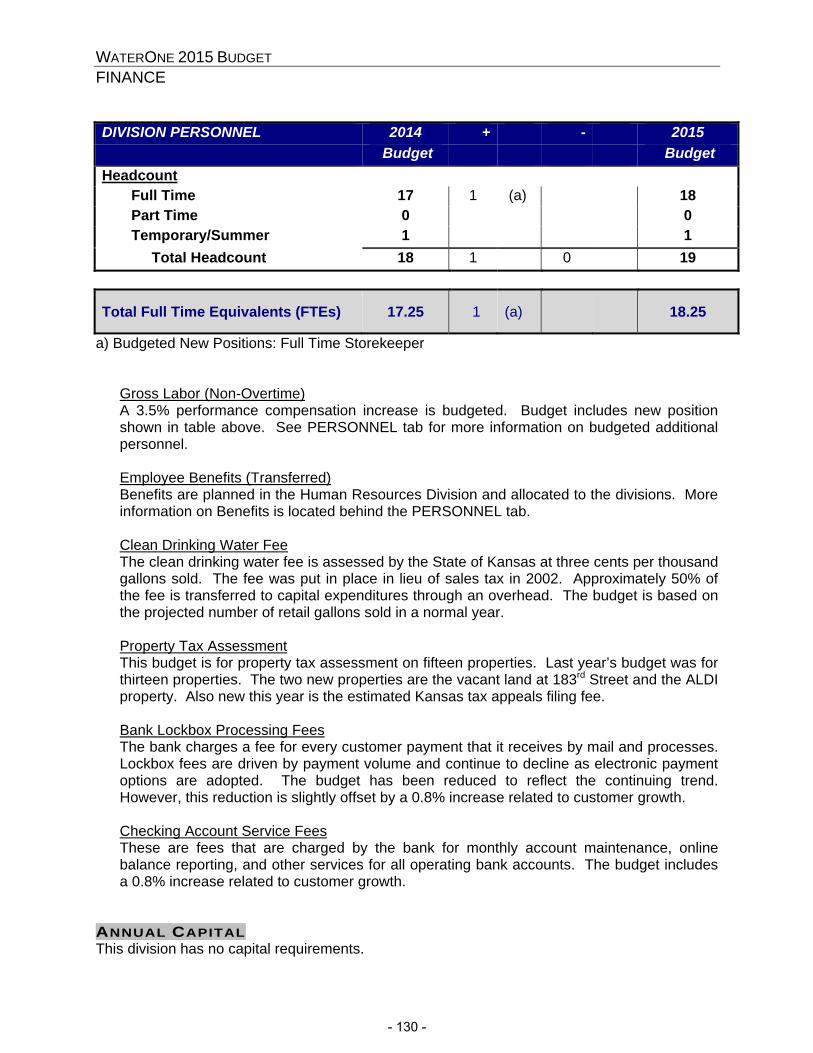

FINANCEOrganization Chart & Division Description 127Division Mission Statement 127Expenditures By Categories - Chart & Table 128Division O&M as a Percentage of WaterOne - Chart 129Significant Accounts - Table 129Employee Headcount - Table 130Significant Accounts - Descriptions 130This division has no annual capital requests

TOC - 3

12/31/2014

TABLE OF CONTENTS2015 Proposed Budget

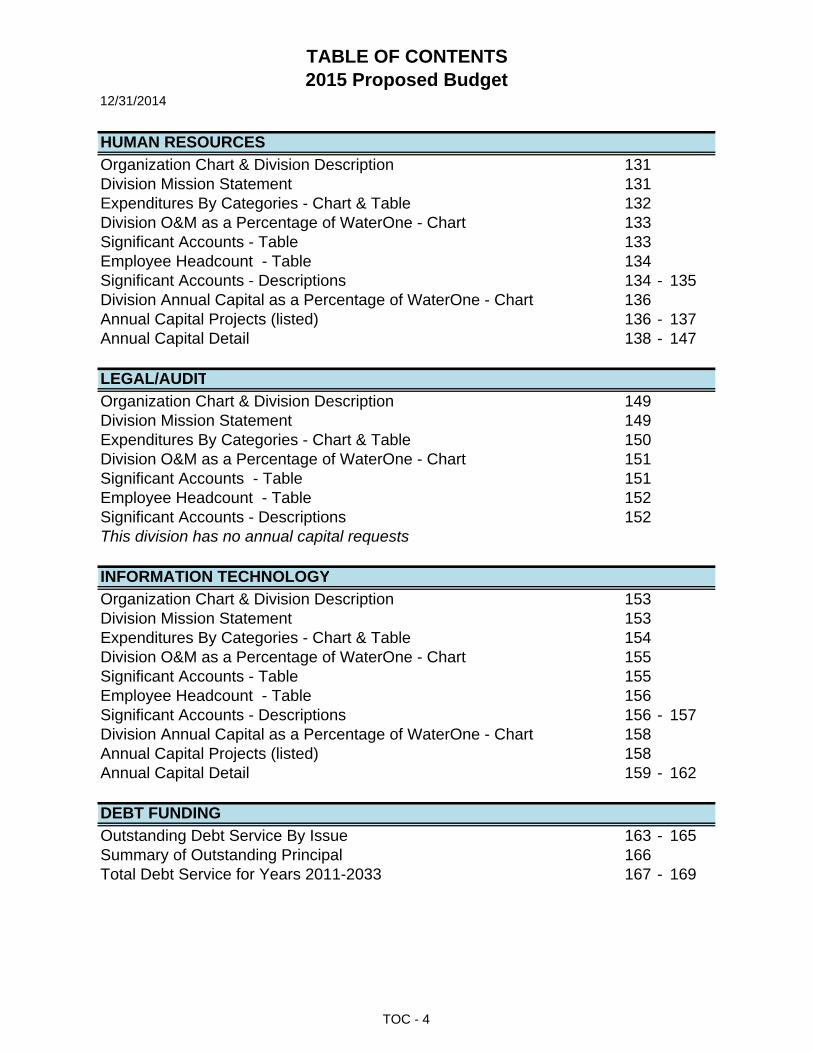

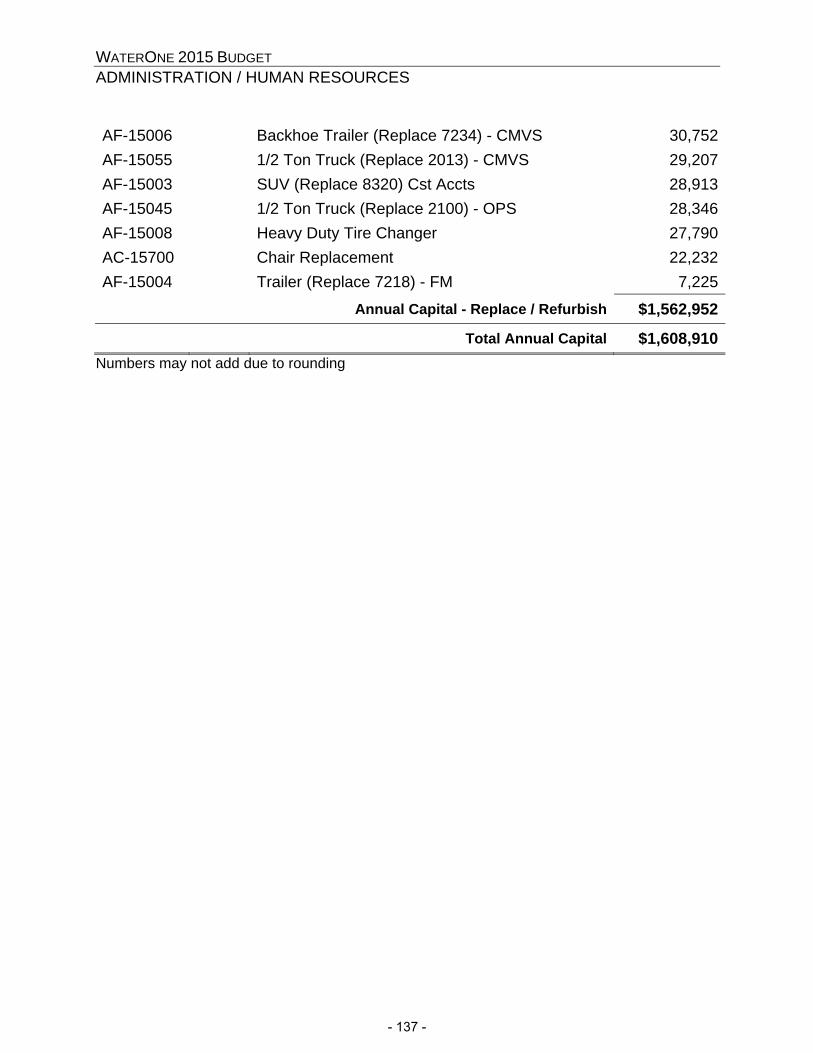

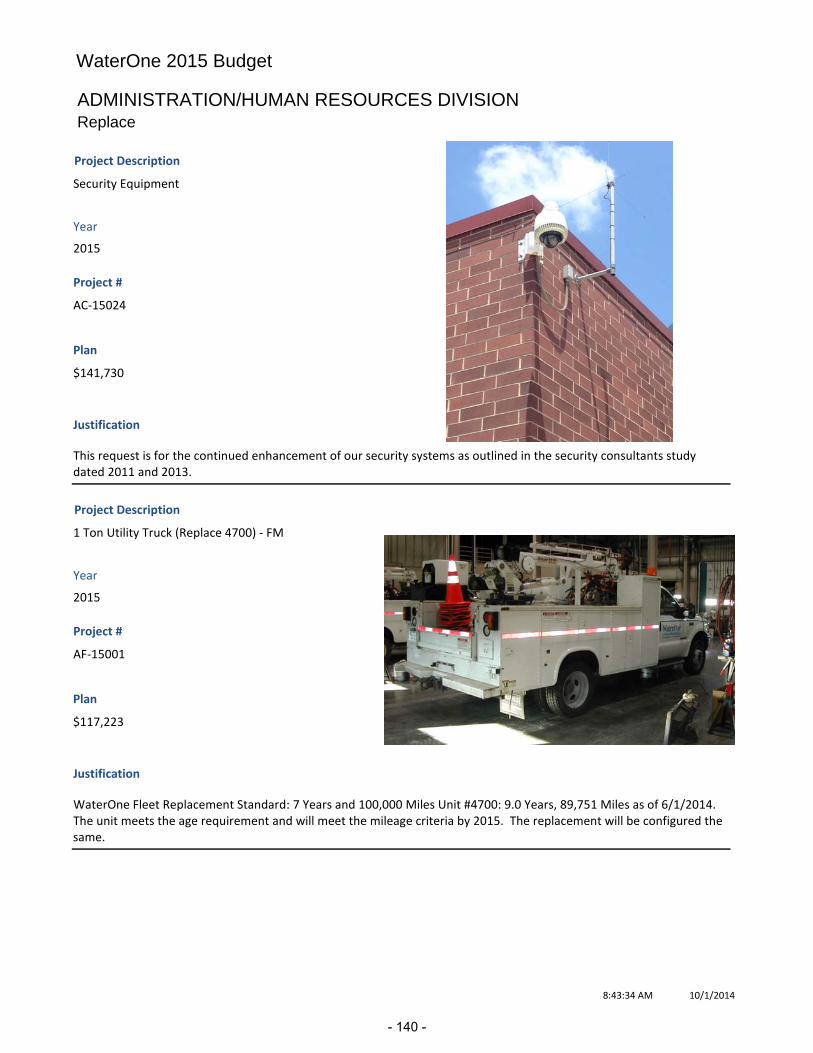

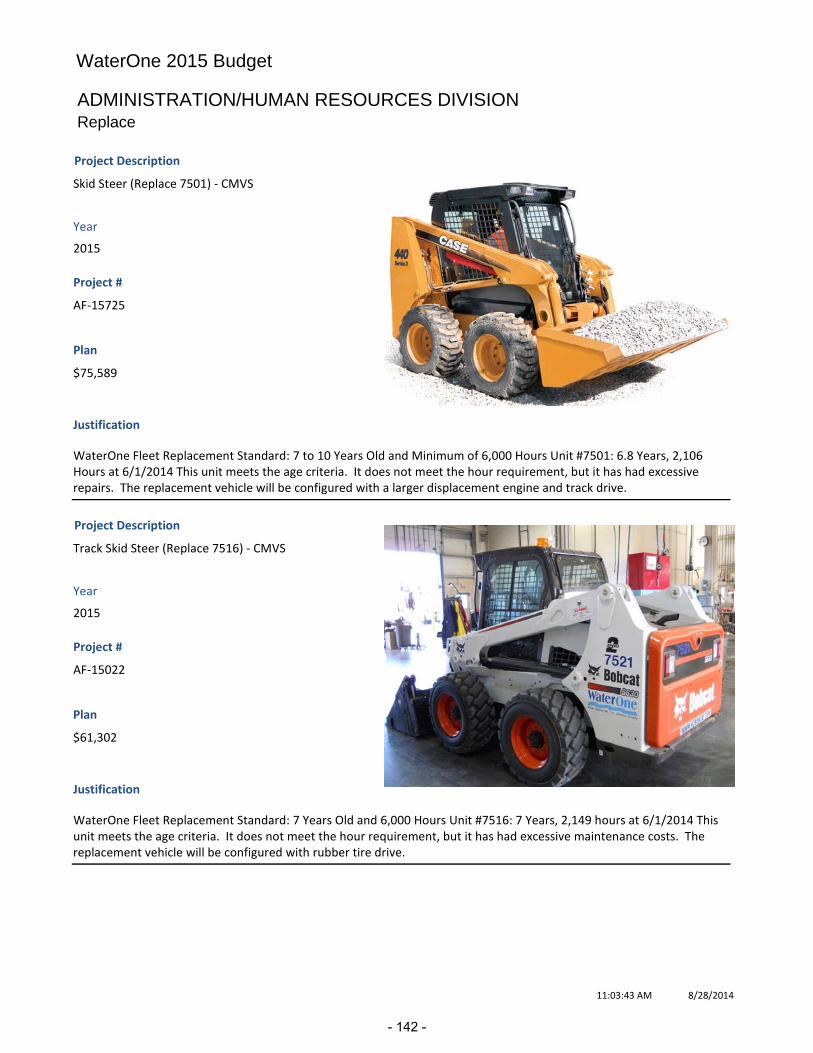

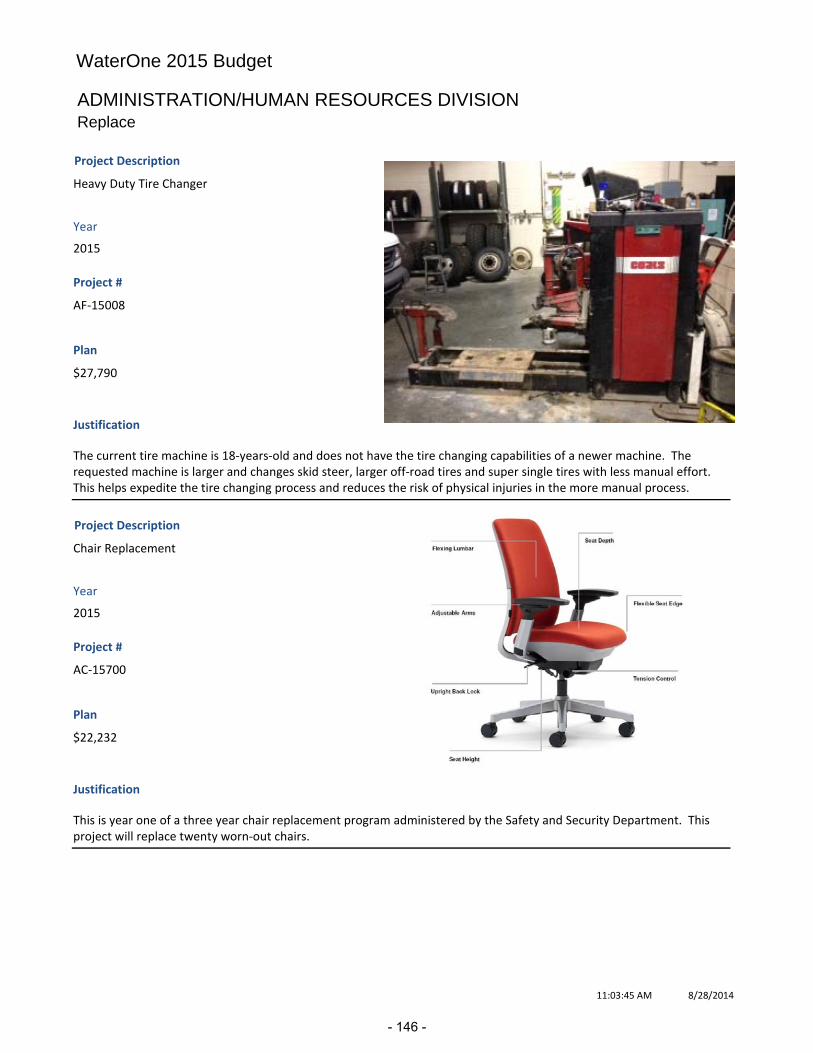

HUMAN RESOURCESOrganization Chart & Division Description 131Division Mission Statement 131Expenditures By Categories - Chart & Table 132Division O&M as a Percentage of WaterOne - Chart 133Significant Accounts - Table 133Employee Headcount - Table 134Significant Accounts - Descriptions 134 - 135Division Annual Capital as a Percentage of WaterOne - Chart 136Annual Capital Projects (listed) 136 - 137Annual Capital Detail 138 - 147

LEGAL/AUDITOrganization Chart & Division Description 149Division Mission Statement 149Expenditures By Categories - Chart & Table 150Division O&M as a Percentage of WaterOne - Chart 151Significant Accounts - Table 151Employee Headcount - Table 152Significant Accounts - Descriptions 152This division has no annual capital requests

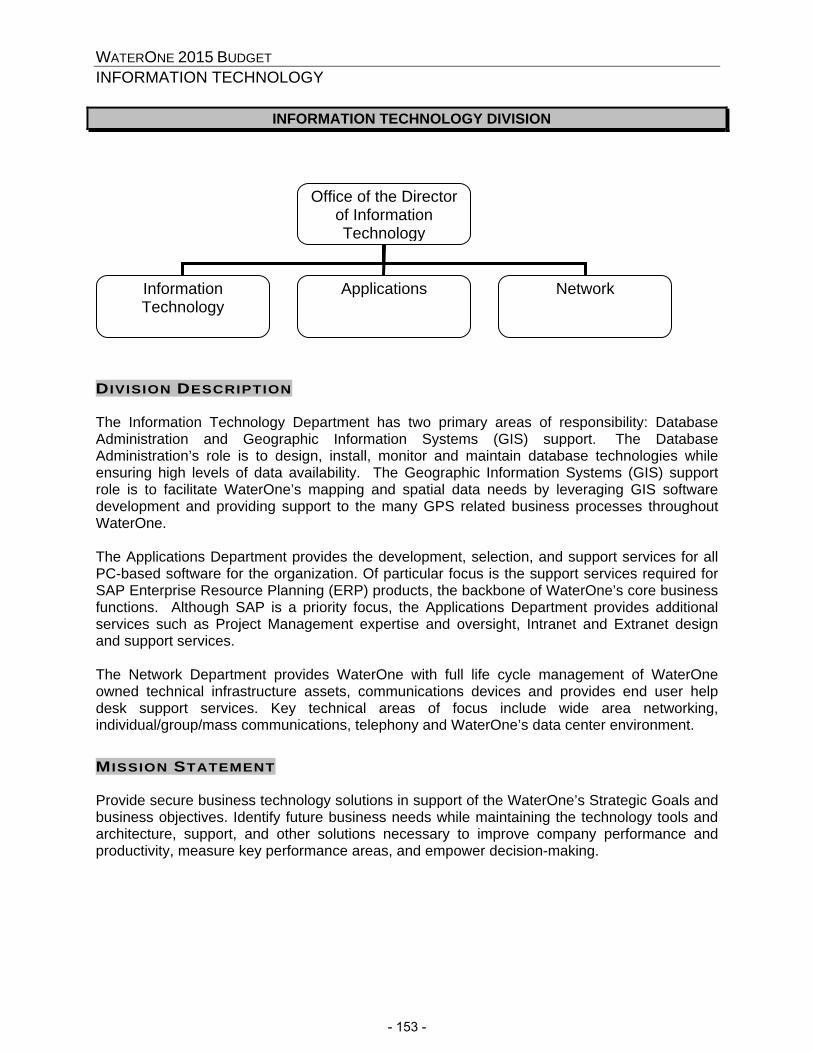

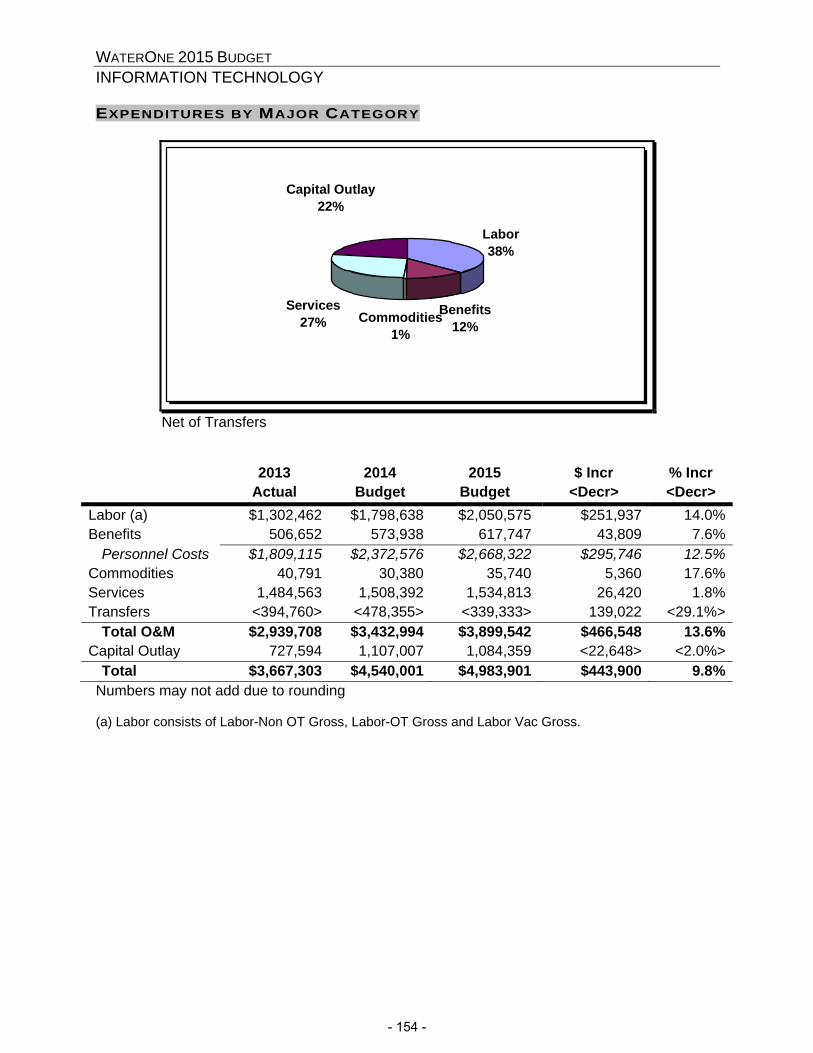

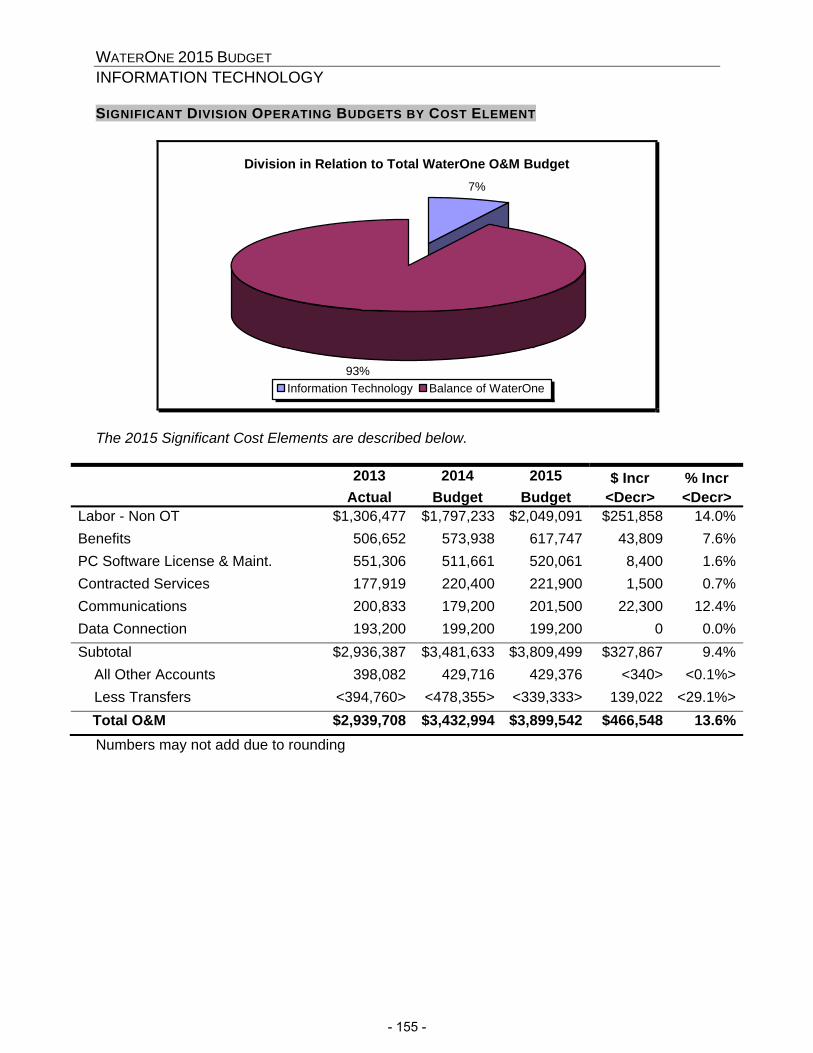

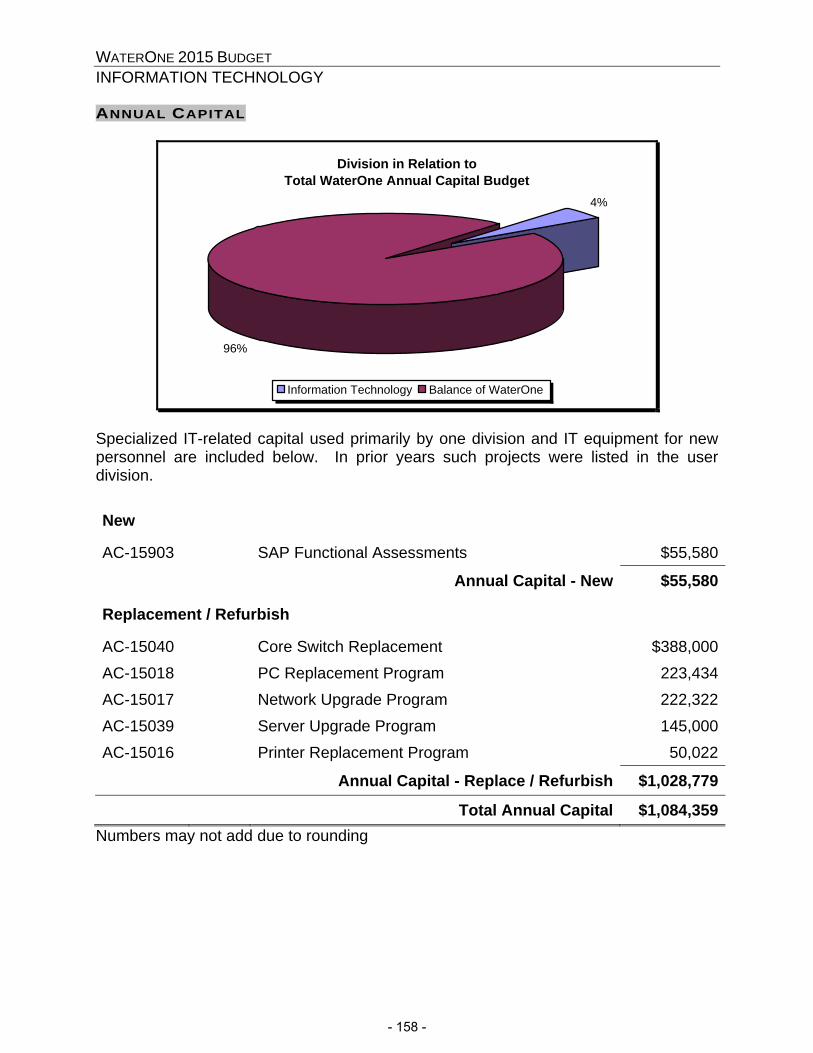

INFORMATION TECHNOLOGYOrganization Chart & Division Description 153Division Mission Statement 153Expenditures By Categories - Chart & Table 154Division O&M as a Percentage of WaterOne - Chart 155Significant Accounts - Table 155Employee Headcount - Table 156Significant Accounts - Descriptions 156 - 157Division Annual Capital as a Percentage of WaterOne - Chart 158Annual Capital Projects (listed) 158Annual Capital Detail 159 - 162

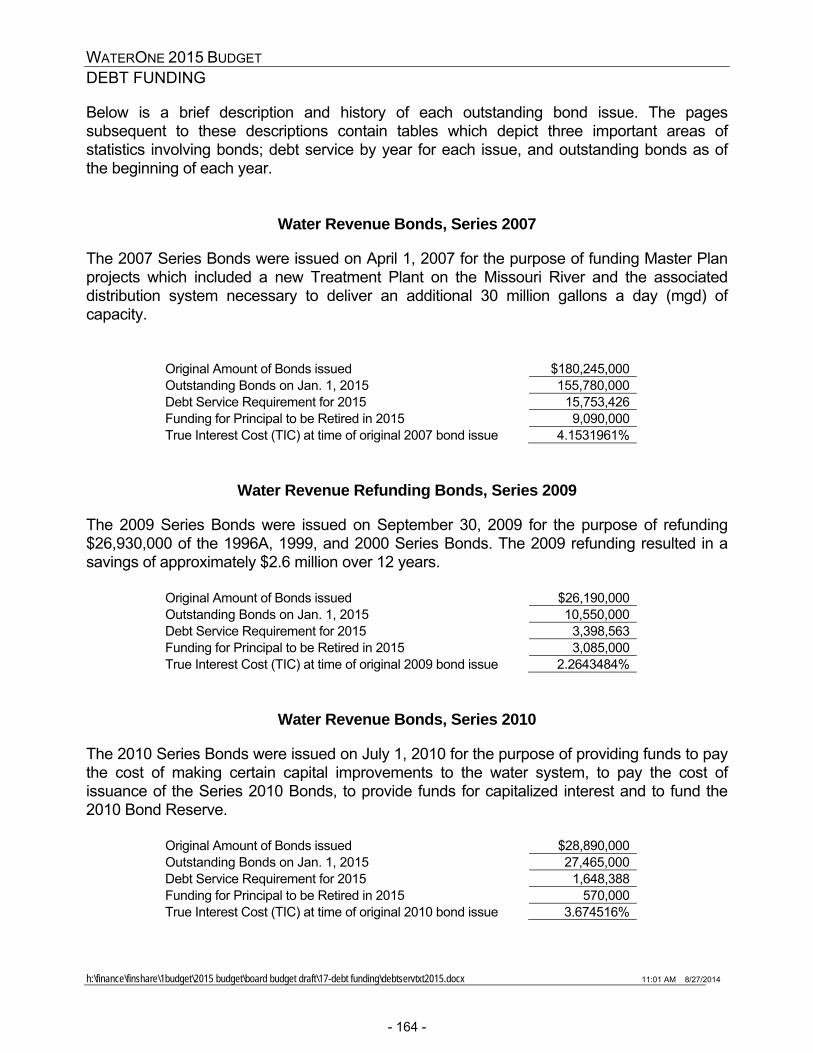

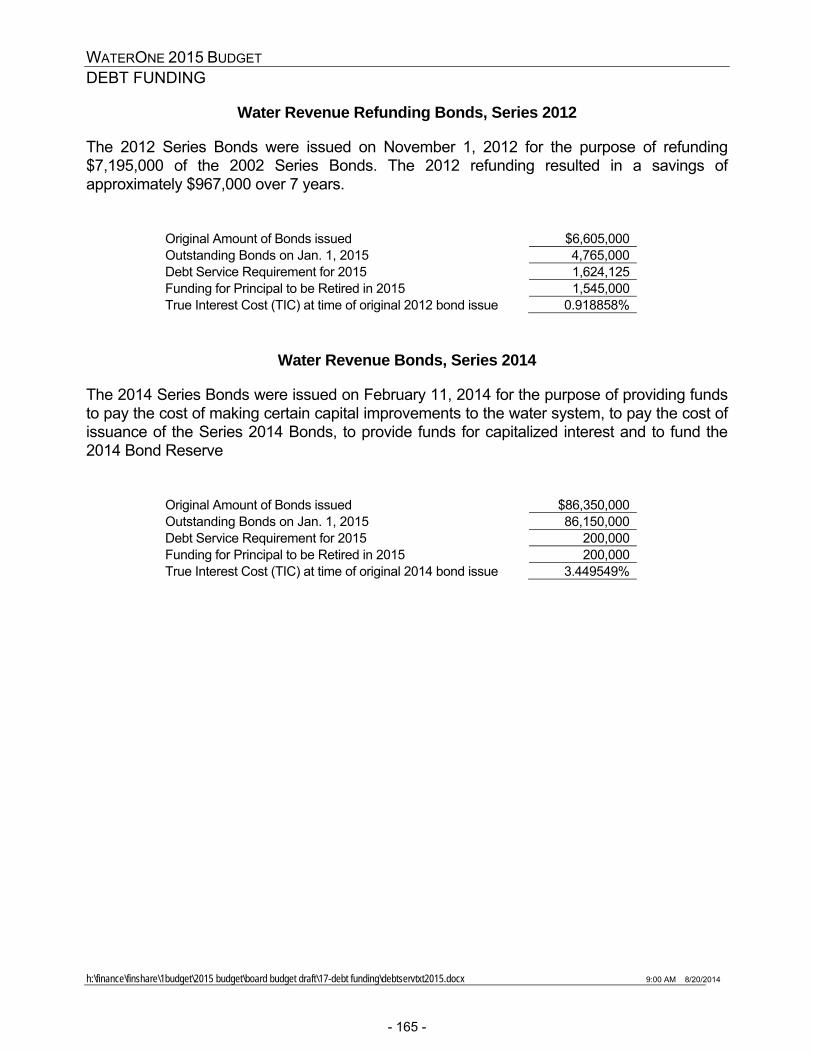

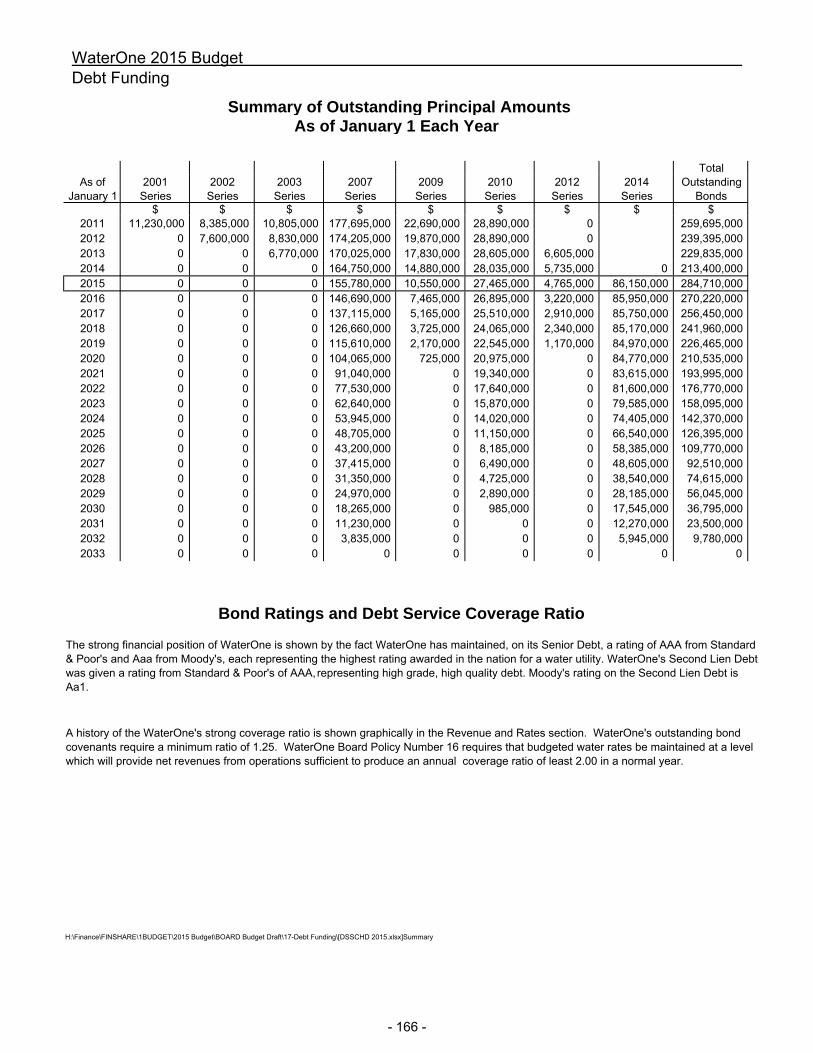

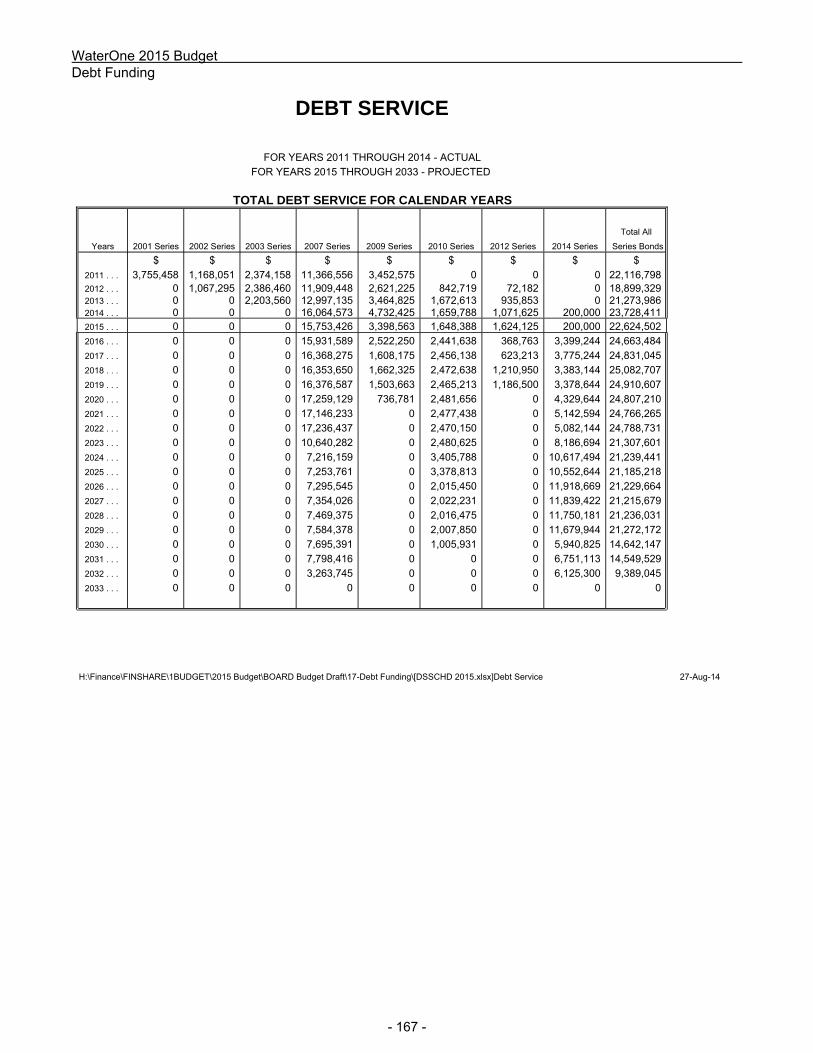

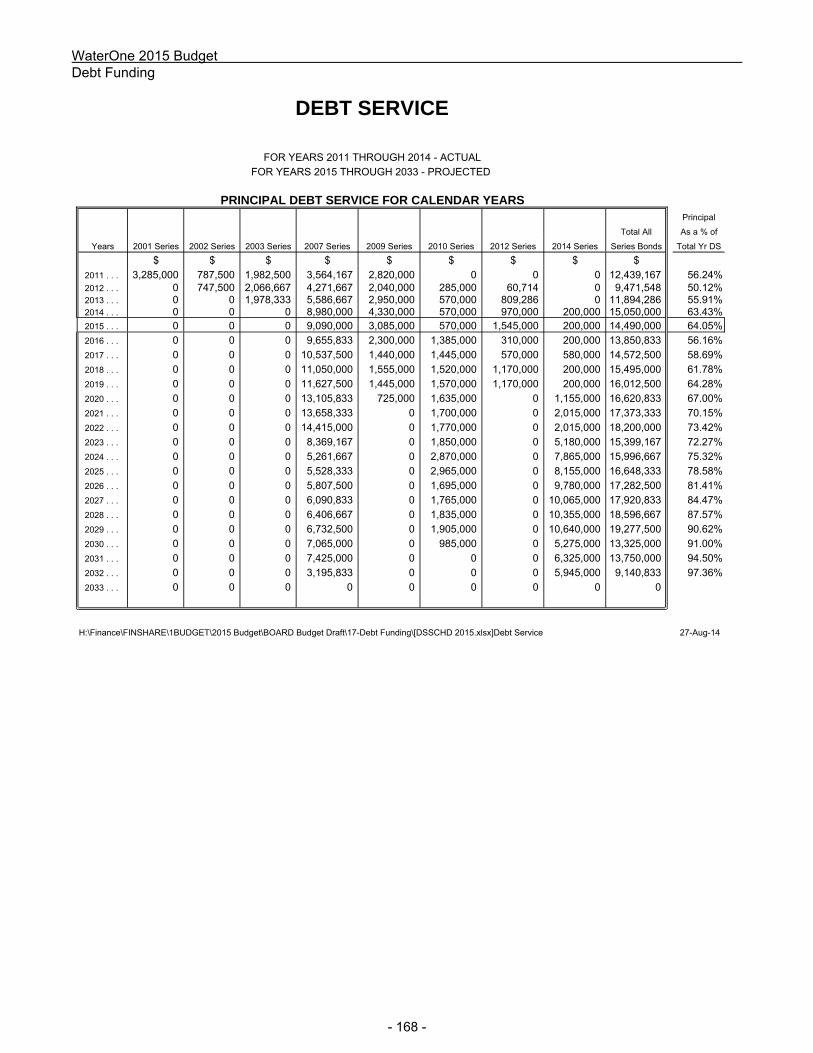

DEBT FUNDINGOutstanding Debt Service By Issue 163 - 165Summary of Outstanding Principal 166Total Debt Service for Years 2011-2033 167 - 169

TOC - 4

12/31/2014

TABLE OF CONTENTS2015 Proposed Budget

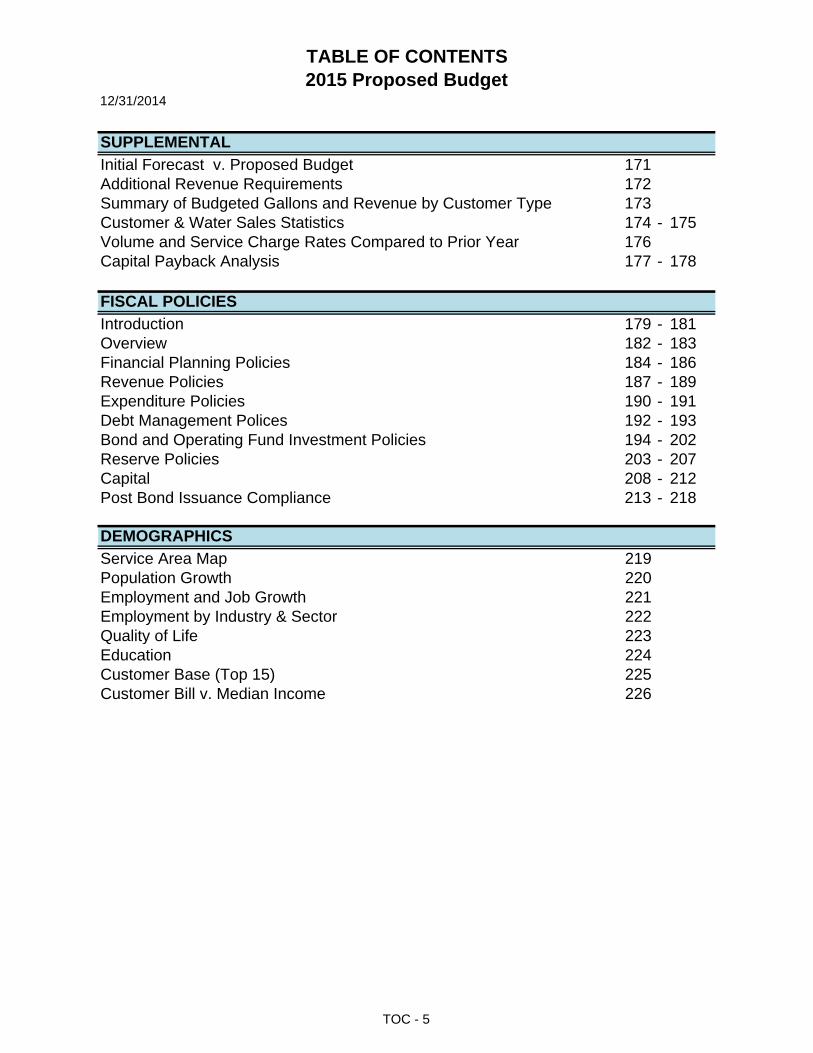

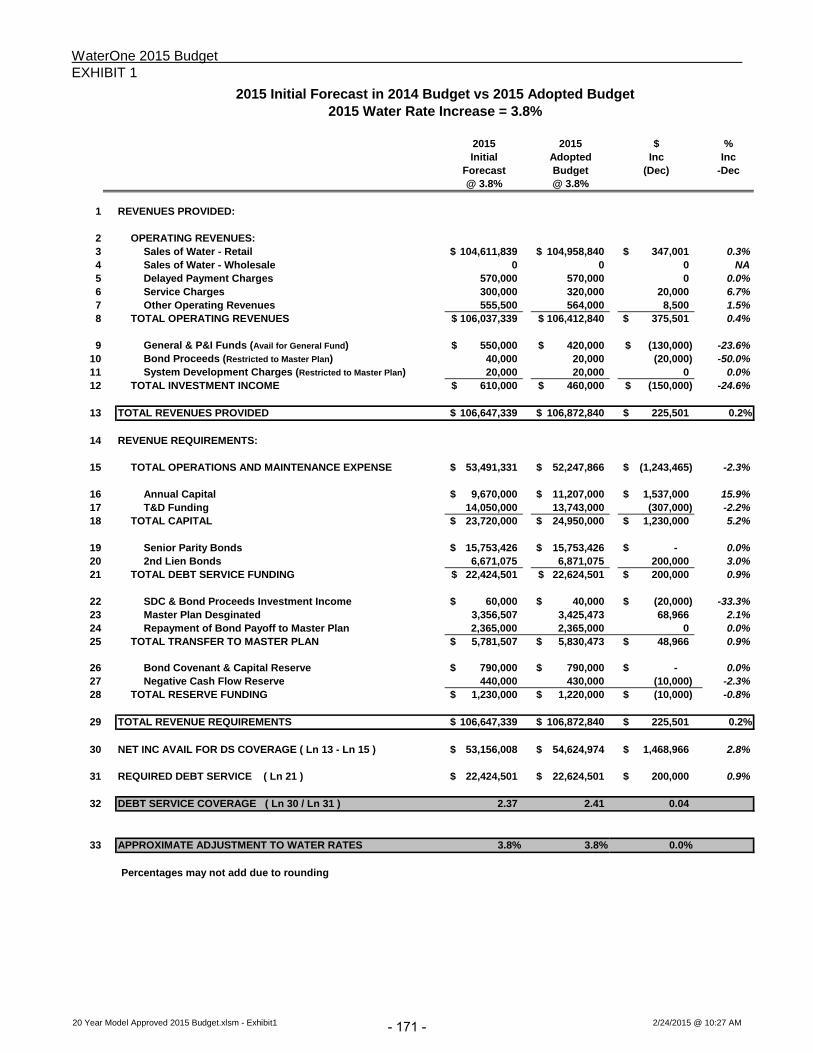

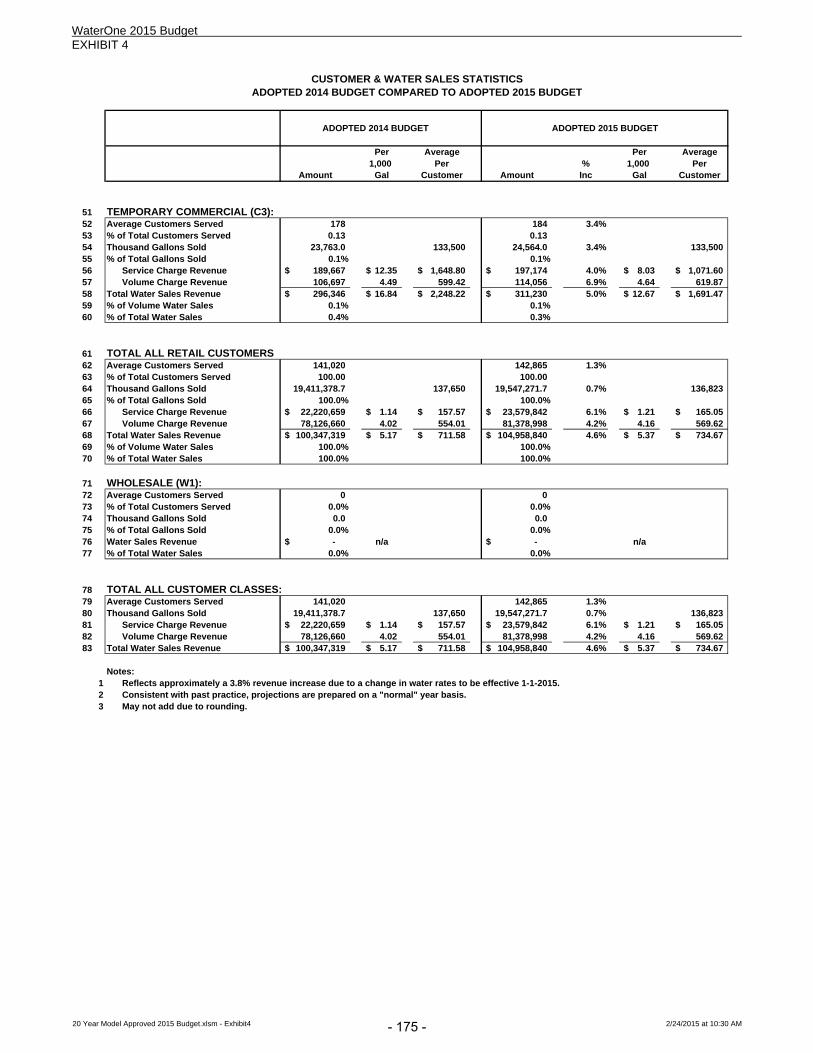

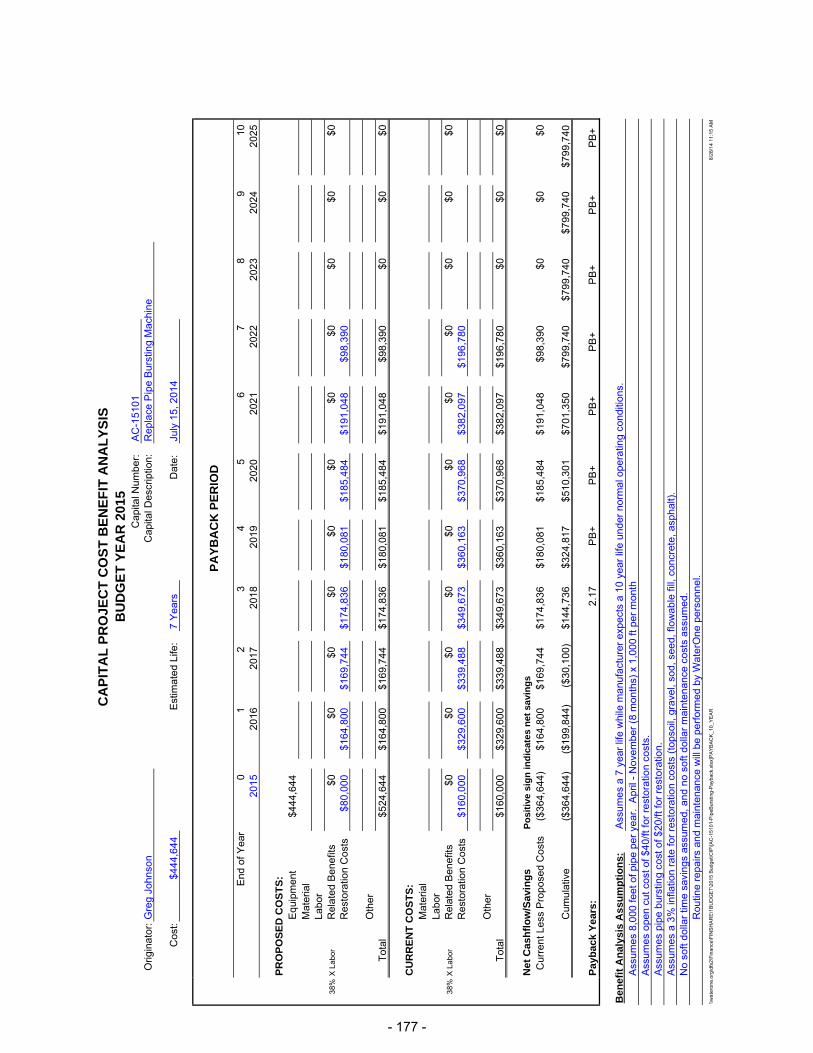

SUPPLEMENTALInitial Forecast v. Proposed Budget 171Additional Revenue Requirements 172Summary of Budgeted Gallons and Revenue by Customer Type 173Customer & Water Sales Statistics 174 - 175Volume and Service Charge Rates Compared to Prior Year 176Capital Payback Analysis 177 - 178

FISCAL POLICIESIntroduction 179 - 181Overview 182 - 183Financial Planning Policies 184 - 186Revenue Policies 187 - 189Expenditure Policies 190 - 191Debt Management Polices 192 - 193Bond and Operating Fund Investment Policies 194 - 202Reserve Policies 203 - 207Capital 208 - 212Post Bond Issuance Compliance 213 - 218

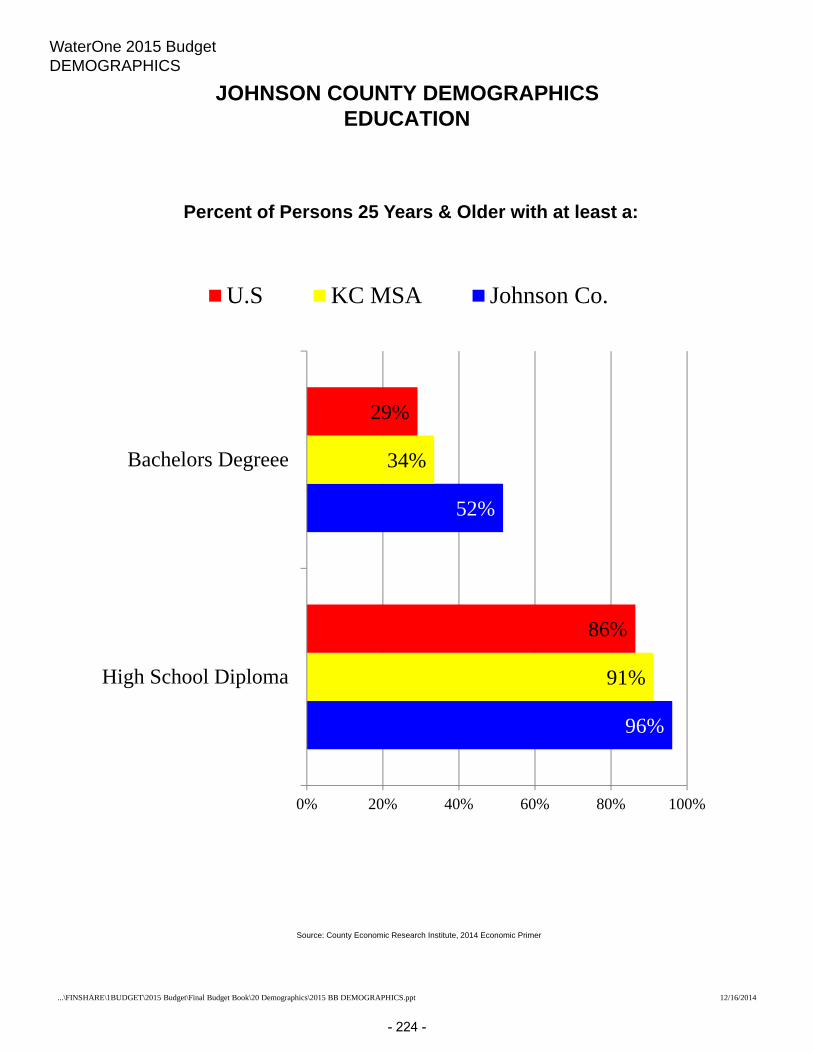

DEMOGRAPHICSService Area Map 219Population Growth 220Employment and Job Growth 221Employment by Industry & Sector 222Quality of Life 223Education 224Customer Base (Top 15) 225Customer Bill v. Median Income 226

TOC - 5

This page intentionally left blank.

EXECUTIVESUMMARY

Lookingbackat2014…The beginning of the year was fiscally challenging because the weather was wetter and cooler than average in the spring and summer. Revenues were lower than budget, but the shortfall was partially offset by expenses that were also lower than the budget. The expense savings was primarily from temporarily vacant positions, power, and chemicals. New customer growth for 2014 continued to trend higher. It was higher than 2013, and is the highest growth since 2007. Although growth remains modest compared to pre-recession levels, the increase in growth appears to be an indication that the local economy continues to rebound. Investment income was close to the amount budgeted, as short-term interest rates continue to be at historic lows.

Lookingaheadto2015…The rate increase is 3.8% which is the same as was projected in last year’s budget. The 2015 rate increase will allow the utility to sustainably manage current operations and provide for future capital investments. Why the increase? The largest increase in the budget is a 13.3% increase in capital spending. This increase in pay-go capital reflects our strategic investment in aging infrastructure which is needed to maintain a high level of service to our customers. Operations and maintenance expenses are increasing by 3.6%. The increase is primarily driven by normal increases in costs due to inflation along with the addition of new personnel which are primarily needed to accommodate the increase in customer growth. New customer growth is projected at 1,300 new customers for 2015 which is 300 more than the 2014 budget. However, domestic (winter) water use continues to decline which is reflected in the budget for gallons sold for Single Family Residential (R1), Multi-family Residential (M1), and Small Commercial (C1) customers which are all expected to use less water than the prior year. This is a trend felt nationally due to the efficiency of water-saving devices like low-flow toilets, low-flow shower heads and front-loading clothes washing machines. This reduction in usage is monitored closely, but it is expected to continue into the future and is an important factor in future projected rate increases. Costs of repaying debt are going down slightly based on a pre-determined repayment schedule while the amount set aside from current rates into the Master Plan Capital Fund is increasing. Increasing the amount designated to the Master Plan Capital Fund is part of a strategy which will help reduce the size of a future bond issue. Fortunately, some of these increasing demands are offset by savings elsewhere. Costs such as pension plan funding, property and liability insurance, and funding to the OPEB reserve for future retiree health insurance are decreasing. Reductions like these help to keep rate adjustments in check, maintaining the value of WaterOne’s service for all ratepayers.

- 1 -

WATERONE 2015 BUDGET 12/31/2014 EXECUTIVE SUMMARY

h:\finance\finshare\1budget\2015 budget\final budget book\02-exec summary\2015 exec summary.docx

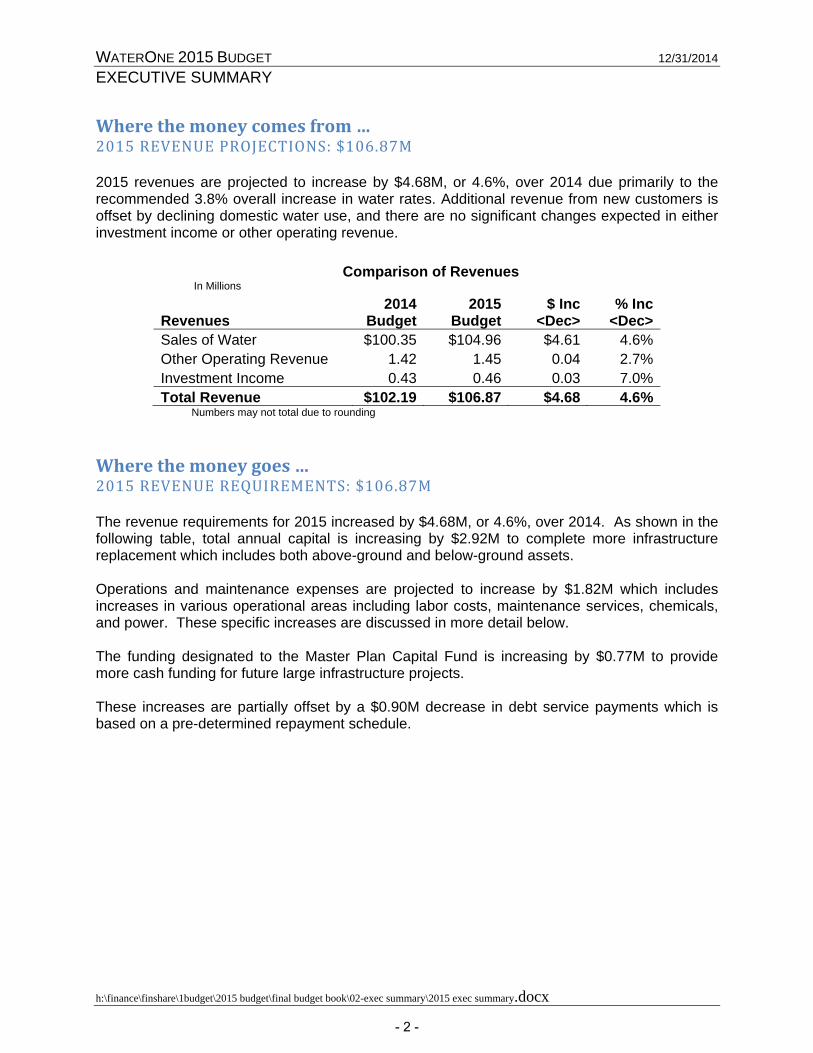

Wherethemoneycomesfrom…2015REVENUEPROJECTIONS:$106.87M 2015 revenues are projected to increase by $4.68M, or 4.6%, over 2014 due primarily to the recommended 3.8% overall increase in water rates. Additional revenue from new customers is offset by declining domestic water use, and there are no significant changes expected in either investment income or other operating revenue.

Comparison of Revenues

In Millions

Revenues 2014

Budget 2015

Budget$ Inc

<Dec> % Inc

<Dec> Sales of Water $100.35 $104.96 $4.61 4.6% Other Operating Revenue 1.42 1.45 0.04 2.7% Investment Income 0.43 0.46 0.03 7.0% Total Revenue $102.19 $106.87 $4.68 4.6%

Numbers may not total due to rounding Wherethemoneygoes…2015REVENUEREQUIREMENTS:$106.87M The revenue requirements for 2015 increased by $4.68M, or 4.6%, over 2014. As shown in the following table, total annual capital is increasing by $2.92M to complete more infrastructure replacement which includes both above-ground and below-ground assets. Operations and maintenance expenses are projected to increase by $1.82M which includes increases in various operational areas including labor costs, maintenance services, chemicals, and power. These specific increases are discussed in more detail below. The funding designated to the Master Plan Capital Fund is increasing by $0.77M to provide more cash funding for future large infrastructure projects. These increases are partially offset by a $0.90M decrease in debt service payments which is based on a pre-determined repayment schedule.

- 2 -

WATERONE 2015 BUDGET 12/31/2014 EXECUTIVE SUMMARY

h:\finance\finshare\1budget\2015 budget\final budget book\02-exec summary\2015 exec summary.docx

2015 Annual Budget - $106,872,840

Comparison of Revenue Requirements In millions

Numbers may not total due to rounding

OPERATIONS&MAINTENANCEEXPENSES:$52.25M Operations and Maintenance (O&M) expenses represent 49% of the 2015 budget. This is the same proportion as 2014 although it is an increase of $1.82M year-over-year. The table on the next page shows the breakdown of the significant O&M expenses including the difference between 2014 and 2015 followed by further discussion of the major operating costs.

O&M49%

Debt Service21%

Repayment to Master Plan

2%

Master Plan3%

Annual Capital24%

Restricted1%

Revenue Requirements 2014

Budget2015

Budget $ Inc

<Dec> % Inc

<Dec>Operations & Maintenance Expense $50.42 $52.25 $1.82 3.6%Total Annual Capital 22.03 24.95 2.92 13.3%Debt Service 23.53 22.62 <0.90> <3.8%>Designated to Master Plan 2.66 3.43 0.77 28.8%Repayment to Master Plan 2.25 2.37 0.12 5.1%Restricted 1.30 1.26 <0.04> <3.1%>Total Revenue Requirements $102.19 $106.87 $4.68 4.6%

Labor36%

Benefits16%Power

16%

Chemicals12%

Services14%

All Other6%

2015 O&M

- 3 -

WATERONE 2015 BUDGET 12/31/2014 EXECUTIVE SUMMARY

h:\finance\finshare\1budget\2015 budget\final budget book\02-exec summary\2015 exec summary.docx

In millions O&M

2014 Budget

2015 Budget

$ Inc <Dec>

% Inc <Dec>

Labor $18.34 $19.10 $0.76 4.1% Services 7.19 7.53 0.34 4.7% Chemicals 5.83 6.07 0.24 4.2% Power 7.95 8.16 0.21 2.7% Benefits 8.44 8.43 <0.01> <0.1%> All Other 2.67 2.95 0.28 10.4% Total $50.42 $52.25 $1.82 3.6%

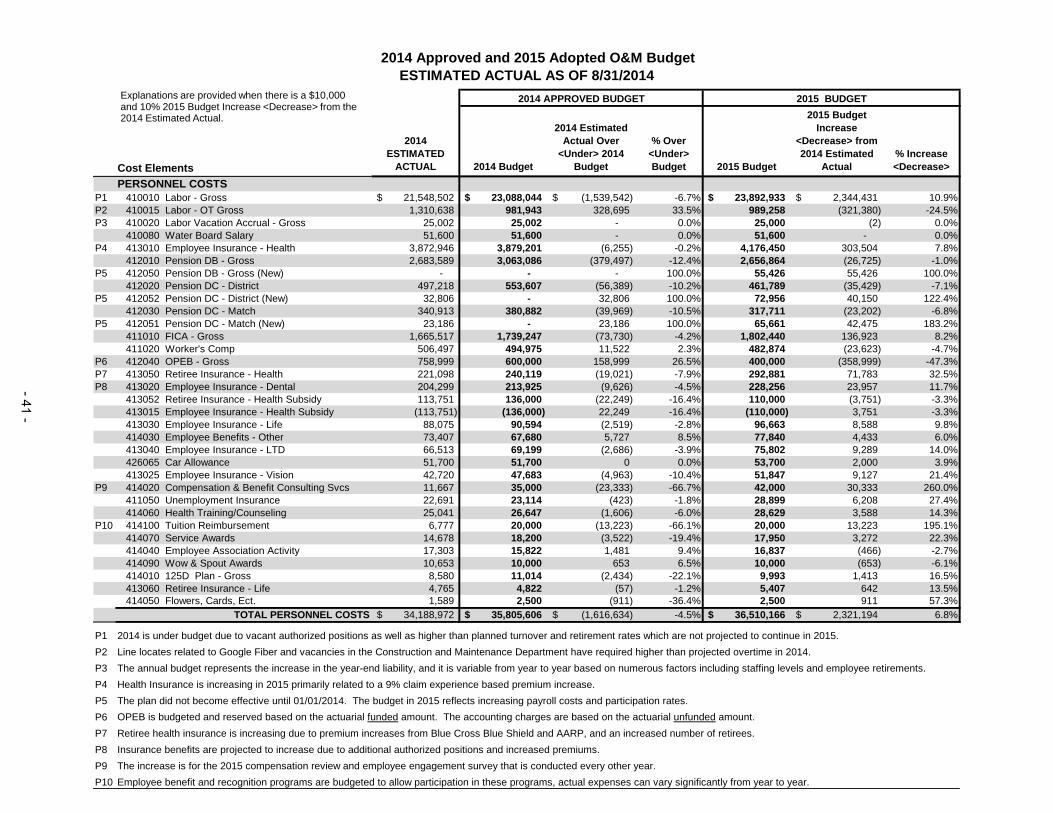

Numbers may not total due to rounding Labor Labor costs include:

The annual true-up to the 2014 base to reflect the actual outcome of payroll and benefits after turn-over, retirements and vacancies.

A 3.5% performance compensation adjustment to maintain WaterOne’s competitiveness with other employers of choice.

Overtime. Transfers of labor costs to capital projects, capturing true project costs. A net increase of 7.275 Full Time Equivalent (FTE) positions.

All positions are assessed based on operational needs including those related to continuing increases in customer growth. A number of the new positions requested for 2015 were eliminated in 2010 and 2011 as business activity slowed because of the recession.

Requested Positions SCADA Analyst - Full Time Storekeeper - Full Time HVAC Tech - Full Time Fleet Mechanic - Full Time System Engineer – Network - Full Time Fleet Clerk - Part Time Water Quality Tech - Full Time Hydrant Auditor - Summer Communication Specialist - Reclassification of Part Time to Full Time

Services All support services (net of transfers) increased $338,469 or 4.7%, in 2015. The largest increases were in maintenance services for work on the Kansas Wellfield and the Horizontal Collector Well on the Missouri River. Chemicals An increase of $243,333, or 4.2%, in the 2015 chemical budget is primarily due to an increase in the projected total water produced, a slight increase in chemical prices and a decrease to the budgeted water produced at Wolcott during January and February when the river level and temperature are likely to reduce the intake capacity of the horizontal collector well. Power The power budget increased $211,898, or 2.7%, for 2015. The budget is increasing primarily due to an increase in the projected total water produced and a decrease to the budgeted water produced at Wolcott during January and February when the river level and temperature are likely to reduce the intake capacity of the horizontal collector well. The

- 4 -

WATERONE 2015 BUDGET 12/31/2014 EXECUTIVE SUMMARY

h:\finance\finshare\1budget\2015 budget\final budget book\02-exec summary\2015 exec summary.docx

decrease to the budgeted water produced at Wolcott during January and February is effective for the 2015 budget in order to bring the budget in line with actual operating conditions over the past two winters. A 5% projected rate increase from the Board of Public Utilities is included. The rate projections are subject to change when BPU proposes and approves actual rate increases in the fall. Benefits Benefits (net of transfers to capital) decreased $7,883 or 0.1% for 2015. Following three out of the last five years of no health insurance premium increases, health insurance costs are projected to increase 7.7%. The health insurance increase is being offset by two reductions. First, there is a decrease in the required contribution to the employee pension plans which is primarily due to investment gains. Second, there is a decrease in the funding needed for the OPEB reserve which helps fund future retiree health insurance costs. The decrease is based on the funding projected in the biennial actuarial valuation.

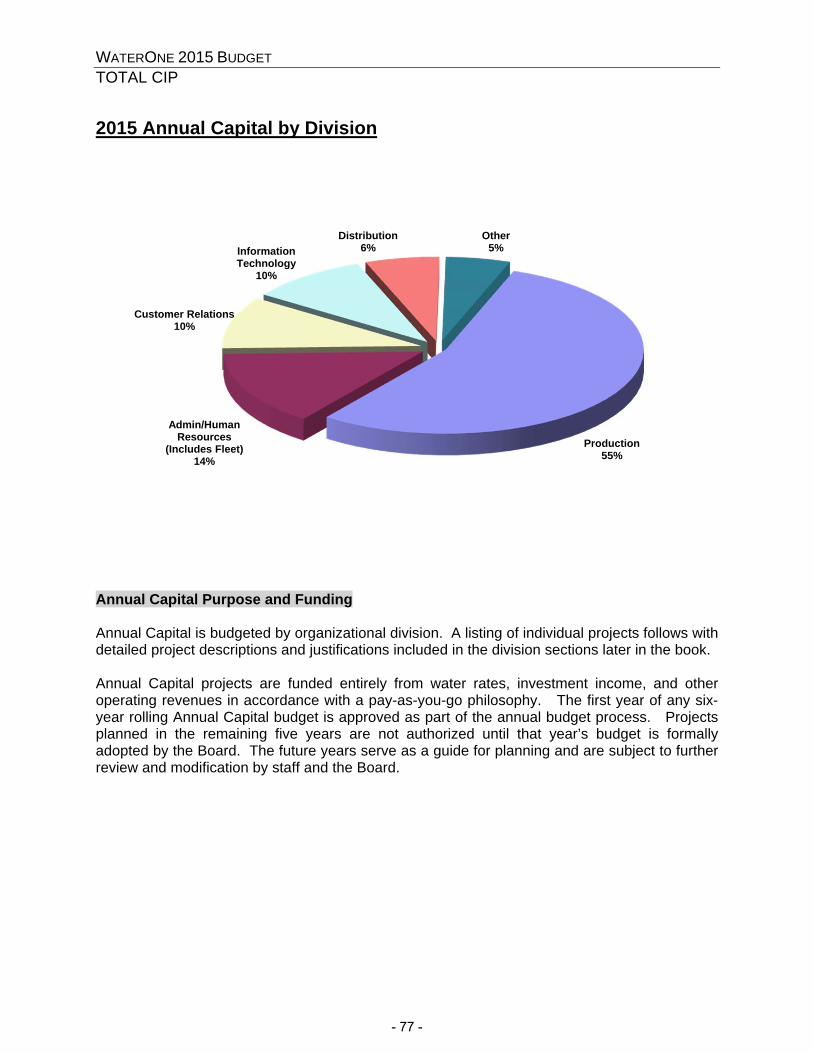

TOTALANNUALCAPITAL:$24.95M The Total Annual Capital budget for 2015 increased $2.92M, or 13.3%. Approximately 96% of the budget is used to maintain current facilities and equipment. These needs are continually being evaluated to determine the proper time to replace versus repair.

Total Annual Capital By Division

The Transmission & Distribution (T&D) budget has increased by $0.57M to $13.74M. WaterOne continues to execute its asset management strategy to target replacement of aging

- 5 -

WATERONE 2015 BUDGET 12/31/2014 EXECUTIVE SUMMARY

h:\finance\finshare\1budget\2015 budget\final budget book\02-exec summary\2015 exec summary.docx

infrastructure at the lowest life-cycle cost. The increase in 2015 is primarily for distribution main replacements and transmission main condition assessment. Annual Capital increased for 2015 by $2.35M. These capital requests are used to replace obsolete or worn-out equipment, purchase new equipment and technology, and make improvements to existing assets. Approximately $9.68M is for replacement while $0.94M is for new capital. The primary reason for the increase in 2015 is due to more Production Division replacement projects including replacing large pumps and SCADA equipment.

Total Annual Capital In millions

Total Annual Capital

2014 Budget

2015 Budget

$ Inc <Dec>

% Inc <Dec>

Transmission & Distribution $13.17 $13.74 $0.57 4.3%Production 4.38 6.12 1.75 40.0%Human Resources (incl. Fleet) 1.54 1.61 0.07 4.4%Customer Relations 1.10 1.13 0.03 2.6%Information Technology 1.11 1.08 <0.02> <2.0%>Distribution 0.19 0.68 0.48 250.2%All Other 0.54 0.59 0.05 8.7%Total Annual Capital $22.03 $24.95 $2.92 13.3%

Numbers may not total due to rounding

DEBTSERVICE:$22.62M Debt Service for 2015 decreased $0.9M, or 3.8%, from 2014 as determined by the previously scheduled bond principal and interest payments. 2015 is the second year of using capitalized interest from the 2014 bond issue which was issued for the Hedge Lane Pump Station and related transmission mains. In 2016 there will be an increase in debt service related to the 2014 bond issue.

DESIGNATEDTOMASTERPLAN:$3.43M “Designated to Master Plan” funding sets aside a portion of current revenues to help fund major capital improvements. This debt management strategy recognizes that current customers benefit from Master Plan projects and contributes a percentage of annual water sales accordingly. These funds also reduce reliance on future debt, benefitting all ratepayers. The 2015 budget of $3.43M is 3.2% of total revenue. The targeted minimum contribution is 5.0% of total revenue. The strategy is to get to the target level by 2018.

REPAYMENTTOMASTERPLAN:$2.37M The $2.37M repayment is the second of a two year repayment to the Master Plan fund for the 2013 early retirement of the Series 2003 bonds. The funds were borrowed from the OPEB reserve which is part of the Master Plan Capital Fund.

- 6 -

WATERONE 2015 BUDGET 12/31/2014 EXECUTIVE SUMMARY

h:\finance\finshare\1budget\2015 budget\final budget book\02-exec summary\2015 exec summary.docx

RESTRICTED:$1.26M Restricted funds are resources that WaterOne needs to maintain for various reasons. The budget consists of funding mandated by the bond covenants, calculated increases in the negative cash flow reserve, and changes in investment income restricted to the Master Plan Capital Fund. Interest rates and projected revenue requirements will cause the required threshold of restricted funds to fluctuate from year to year.

INSUMMARY Despite the challenges of declining domestic water consumption, below average customer growth in recent years, historically low investment yields, and an aging infrastructure, WaterOne’s financial position continues to be strong thanks to its capital investment strategy, quality staff, and ability to adapt to the variability of weather. WaterOne remains committed to its track record of steady and predictable rate adjustments which provide stability for its residential customers and the rebounding business community. The 2015 budget provides the resources needed to deliver on WaterOne’s vision of “Setting the Standard for Utility Excellence.”

- 7 -

This page intentionally left blank.

- 8 -

WATERONE 2015 BUDGET OVERVIEW Budget Review and Approval Process The Finance Division kicks off the budget planning cycle in the first quarter with an initial planning meeting to go over budget targets and challenges with managers and directors. All budget forms, instructions, standards, and schedules are then posted on WaterOne’s Unity SharePoint site. Managers and those assigned to assist them begin preparing their budget submissions. The Financial Planning Department provides specialized help to each department in preparation of their budget, including one-on-one meetings, training, and guidance as needed to ensure an organized district-wide approach to budget preparation. Each department is required to document and justify requests. For specialized requests such as computer equipment, modifications to facilities, and fleet, the department responsible for the asset’s installation and/or maintenance works with the requestor to ensure that it meets the stated needs and that the amount is appropriate. Managers prepare departmental budgets for the next fiscal year for their respective director’s approval by assessing current operating conditions, staffing needs, and program development plans. Submissions are also made for the ensuing five budget years for both capital and personnel. After the directors review and approve the requests, they are submitted to Financial Planning to be compiled, reviewed and analyzed. Financial modeling is updated with the latest budget submissions and any other revised assumptions and the water rates required to support the budget are produced. A revised 5-year projection is produced so that any longer range impacts may be reviewed as well. Each division reviews their budget requests with the General Manager and Director of Finance. The recommended budget plans are analyzed using such measures as prior year requests compared to prior year actual expenditures, trend analysis tools, current financial goals, and strategic objectives. Once final approval is received from the General Manager, the appropriate documents are prepared for Board review. The Board reviews the recommended budget in two work sessions in the fall. Once the Board has fully reviewed the recommended budget and provided direction to management, a public hearing is held in November. Additional adjustments to the recommended budget may be made at that time. The final budget is approved at the regularly scheduled December Board meeting. Water rates to support the budget become effective with water used on or after the beginning of the new fiscal year on January 1.

- 9 -

2015 BUDGET PROCESS

H:\...\2015 Budget\Board Budget Draft\dateflow.ppt

budget website launch - forms & instructions online

STRATEGY

Submissions:

•Operations & Maintenance Requests

•Fleet Requests

•Capital Requests

•Current Personnel Modifications

• Additional Personnel Requests

•5-Year Personnel & Capital

NEEDS ASSESSMENT

Decision:final budget review by G.M. & directors before submission to Board

Submission:prior year capital carry-over requests

Submission:proposed budget

to Board

Finance Committee Meetings: Board review of operating and capital budgets; Staff presentations on key budget drivers & components

Public Hearing:proposed budget and rate impact

REVIEW & DEVELOPMENT

Board Meeting:

final adoption of budget

ADOPTION

December

November

October

September

August

July

June

April

May

Budget Kick-OffMarch

Division Budget Meetings:director and managers review submissions with

G.M., Finance staff, Human Resources, and Fleet management

- 10 -

WATERONE FINANCIAL OVERVIEW4.9% 4.4% 4.9% 3.2% 3.9% 3.8% 3.6% 3.3% 3.3% 3.2% 3.2% W A T E R R A T E S

TOTAL ANNUAL OPERATING BUDGET 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 LONG TERM MODEL ACTUAL ACTUAL ACTUAL ACTUAL BUDGET ADOPTED PROJECTION PROJECTION PROJECTION PROJECTION PROJECTION PROJECTION ASSUMPTIONS

REVENUES PROVIDED: Customer Growth per YearSales Of Water 80,897,855$ 92,044,865$ 114,672,701$ 97,594,794$ 100,347,319$ 104,958,840$ 109,366,382$ 113,829,882$ 118,693,408$ 123,513,463$ 128,552,076$ 2015 2016 2017 2018 2019 2020Sales Of Water - Wholesale - - - - - - - - - - - 1,300 1,500 1,800 2,000 2,000 2,000Other Operating Revenues 1,363,021 1,235,783 1,369,535 1,273,121 1,415,500 1,454,000 1,464,000 1,474,000 1,494,000 1,524,000 1,544,000

Total Operating Revenues 82,260,876 93,280,648 116,042,236 98,867,915 101,762,819 106,412,840 110,830,382 115,303,882 120,187,408 125,037,463$ 130,096,076$ Gallons Per Customer Per Year:R1 90,300 gallons

Investment Income ( General and P&I Funds ) 309,599 277,094 228,044 197,373 270,000 420,000 530,000 1,290,000 1,930,000 2,670,000 3,150,000 M1 460,800 gallonsInvestment Income (Bond & SDC Fund) 37,213 35,339 7,266 - 160,000 40,000 - 20,000 670,000 290,000 200,000 C1 217,000 gallons

Total Investment Income 346,812 312,433 235,310 197,373 430,000 460,000 530,000 1,310,000 2,600,000 2,960,000$ 3,350,000$ C2 1,506,000 gallons

Interest % Yield on Investment IncomeTOTAL REVENUES PROVIDED 82,607,688$ 93,593,081$ 116,277,546$ 99,065,287$ 102,192,819$ 106,872,840$ 111,360,382$ 116,613,882$ 122,787,408$ 127,997,463$ 133,446,076$ 2015 2016 2017 2018 2019 2020

0.35% 0.50% 1.25% 1.75% 2.25% 2.50%REVENUE REQUIREMENTS:

Operations & Maintenance Expense 41,410,646$ 43,612,653$ 48,869,902$ 47,214,225$ 50,424,719$ 52,247,866$ 54,484,493$ 56,902,162$ 59,180,721$ 62,581,901$ 64,027,815$ O&M Assumptions (2016-2020)

Annual Capital 4,265,136 5,572,153 5,275,895 3,166,509 8,856,000 11,207,000 11,280,000 11,730,000 12,200,000 12,680,000 13,180,000 Current Year CO's to be Spent in Following Year 5,453,429 3,742,491 6,109,537 4,207,532 - - - - - - - Payroll 4.5%Transmission and Distribution (T&D) Funding 9,400,000 9,800,000 11,170,000 11,950,000 13,174,000 13,743,000 14,776,000 15,903,000 17,126,000 18,443,000 19,888,000 Power 3.0%

Total Pay as You Go Annual Capital + T&D 19,118,565 19,114,644 22,555,432 15,116,509 22,030,000 24,950,000 26,056,000 27,633,000 29,326,000 31,123,000 33,068,000 Chemicals 4.0%Health Ins. 10.0%

Debt Service Funding 21,171,389 22,116,799 18,923,282 21,273,985 23,528,410 22,624,501 24,663,482 24,831,043 25,082,706 24,910,606 28,086,660 All Other O&M 3.0%

Investment Income (Bond & SDC Fund) 37,213 35,339 10,000 - 160,000 40,000 - 20,000 670,000 290,000 200,000 Designated Master Plan 341,277 2,507,648 15,245,657 4,063,989 2,659,690 3,425,473 5,156,406 6,077,676 7,397,982 7,731,956 6,943,601 Annual Capital AssumptionsRepayment of Bond Payoff to Master Plan - - 3,754,167 3,587,500 2,250,000 2,365,000 - - - - - Inflation rate at 4%

Total Transfers to Master Plan 378,490 2,542,987 19,009,824 7,651,489 5,069,690 5,830,473 5,156,406 6,097,676 8,067,982 8,021,956 7,143,601

Bond Covenant & Capital Reserves - - - - 720,000 790,000 560,000 670,000 660,000 870,000 570,000 Negative Cash Flow Reserve 502,927 500,000 500,000 500,000 420,000 430,000 440,000 480,000 470,000 490,000 550,000

TOTAL REVENUE REQUIREMENTS 82,582,017$ 87,887,083$ 109,858,440$ 91,756,208$ 102,192,819$ 106,872,840$ 111,360,382$ 116,613,882$ 122,787,408$ 127,997,463$ 133,446,076$ Funds Available for Reservation 25,671$ 5,705,998$ 6,419,105$ 7,309,079$ -$ -$ -$ -$ -$ -$ -$

Senior Parity and 2nd Lien Debt Service Coverage 1.95 2.26 3.56 2.44 2.20 2.41 2.31 2.40 2.54 2.63 2.47

LONG RANGE MASTER PLAN BUDGET

Carryover Reserves Available for Future Awards 11,497,139$ 23,286,901$ 17,610,555$ 26,250,055$ 32,263,852$ 35,004,117$ 8,885,194$ 8,726,509$ 20,894,321$ 36,793,452$ 17,844,616$ Funding Sources:

Net Bond Proceeds 28,165,735 (2,230,875) - - 78,300,000 - - - 41,000,000 - 15,000,000 Designated Reserve for Master Plan Projects 1,232,037 2,507,648 15,245,657 8,563,989 2,659,690 3,425,473 5,156,406 6,077,676 7,397,982 7,731,956 6,943,601 SDC Revenue 4,600,000 4,900,000 6,600,000 8,700,000 6,311,500 6,311,500 7,282,500 9,001,800 10,510,000 11,040,000 11,380,000 Assumes all 5/8" SDC'sDesignated General Fund - - - - - - - - - - - Reserve Transfers (4,672,816) (2,899,271) 4,181,807 - 513,571 - - - - - - Investment Income - 31,764 40,364 - 160,000 40,000 - 20,000 670,000 290,000 200,000

Total Funding Sources 29,324,956$ 2,309,266$ 26,067,828$ 17,263,989$ 87,944,761$ 9,776,973$ 12,438,906$ 15,099,476$ 59,577,982$ 19,061,956$ 33,523,601$

TOTAL FUNDS AVAILABLE 40,822,095$ 25,596,167$ 43,678,383$ 43,514,044$ 120,208,613$ 44,781,090$ 21,324,101$ 23,825,985$ 80,472,302$ 55,855,408$ 51,368,216$ Master Plan Project Costs (Award Basis) 17,535,195$ 7,985,612$ 17,428,328$ 11,250,192$ 85,204,497$ 35,895,896$ 12,597,592$ 2,931,664$ 43,678,850$ 38,010,792$ 44,640,163$

0

Operations & Maintenance

49%

Annual Cap23%

Reserves7%

Debt Service Funding

21%

2015 REVENUE REQUIREMENTS

$34.96$37.00

$39.37$41.31

$42.80$45.50

$48.37$51.42

$54.66

$58.11$61.78

$34.96 $36.48$38.25 $39.49 $40.79 $42.37 $43.88

$45.33$46.84 $48.35 $49.88

$20

$30

$40

$50

$60

$70

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Typi

cal (

R1)

Sin

gle

Fam

ily C

usto

mer

-7,

500

Gal

/Mo

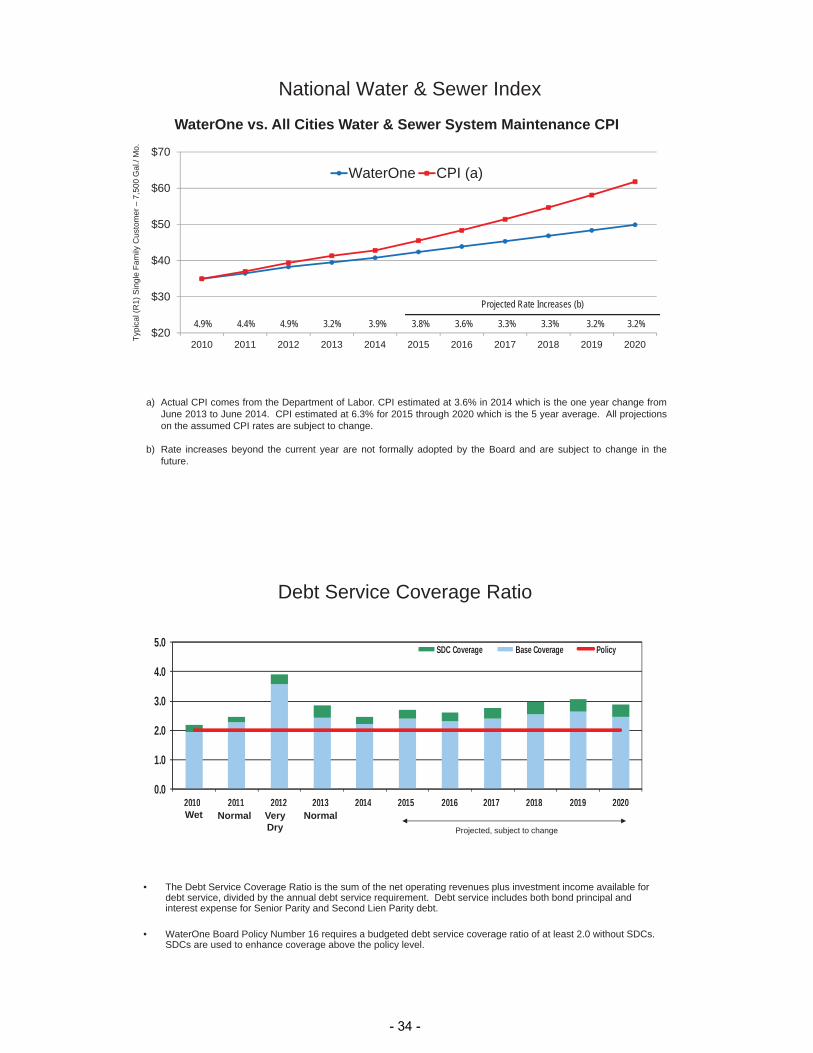

National Water & Sewer IndexWaterOne vs. All Cities Water & Sewer System Maintenance CPI

CPI WaterOne

4.9% 4.4% 4.9% 3.2% 3.9% 3.8% 3.6% 3.3% 3.3% 3.2% 3.2% Projected Rate Increases

Rate increases beyond the current year are not formally adopted by the Board and are subject

to change in the future.

$42.37

$0 $10 $20 $30 $40 $50 $60 $70

Spring Hill

Water 7

BPU

DeSoto

KCMO

Bonner Springs

Gardner

Miami RWD2

WaterOne

Olathe

2015 rates are shown when available. In instances where 2015 rates are not yet determined, current 2014 rates are shown.

Average Monthly Water Bill for Typical Customer at 7,500 Gal

Proposed

4:13 PM 2/27/2015 \\waterone.org\dfs2\Finance\FINSHARE\10YEAR\Approved Budgets\20 Year Model Approved 2015 Budget.xlsm- 11 -

This page left intentionally blank.

- 12 -

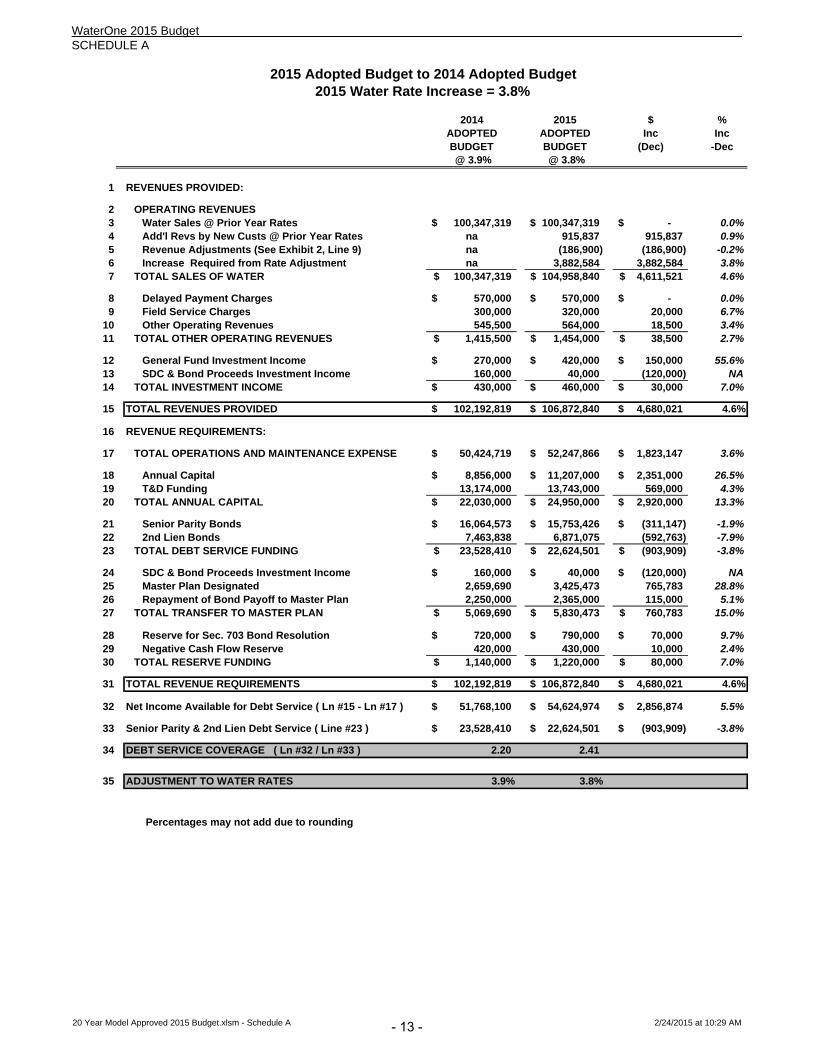

WaterOne 2015 Budget SCHEDULE A

2014 2015 $ %ADOPTED ADOPTED Inc IncBUDGET BUDGET (Dec) -Dec @ 3.9% @ 3.8%

1 REVENUES PROVIDED:

2 OPERATING REVENUES3 Water Sales @ Prior Year Rates 100,347,319$ 100,347,319$ -$ 0.0%4 Add'l Revs by New Custs @ Prior Year Rates na 915,837 915,837 0.9%5 Revenue Adjustments (See Exhibit 2, Line 9) na (186,900) (186,900) -0.2%6 Increase Required from Rate Adjustment na 3,882,584 3,882,584 3.8%7 TOTAL SALES OF WATER 100,347,319$ 104,958,840$ 4,611,521$ 4.6%

8 Delayed Payment Charges 570,000$ 570,000$ -$ 0.0%9 Field Service Charges 300,000 320,000 20,000 6.7%

10 Other Operating Revenues 545,500 564,000 18,500 3.4%11 TOTAL OTHER OPERATING REVENUES 1,415,500$ 1,454,000$ 38,500$ 2.7%

12 General Fund Investment Income 270,000$ 420,000$ 150,000$ 55.6%13 SDC & Bond Proceeds Investment Income 160,000 40,000 (120,000) NA14 TOTAL INVESTMENT INCOME 430,000$ 460,000$ 30,000$ 7.0%

15 TOTAL REVENUES PROVIDED 102,192,819$ 106,872,840$ 4,680,021$ 4.6%

16 REVENUE REQUIREMENTS:

17 TOTAL OPERATIONS AND MAINTENANCE EXPENSE 50,424,719$ 52,247,866$ 1,823,147$ 3.6%

18 Annual Capital 8,856,000$ 11,207,000$ 2,351,000$ 26.5%19 T&D Funding 13,174,000 13,743,000 569,000 4.3%20 TOTAL ANNUAL CAPITAL 22,030,000$ 24,950,000$ 2,920,000$ 13.3%

21 Senior Parity Bonds 16,064,573$ 15,753,426$ (311,147)$ -1.9%22 2nd Lien Bonds 7,463,838 6,871,075 (592,763) -7.9%23 TOTAL DEBT SERVICE FUNDING 23,528,410$ 22,624,501$ (903,909)$ -3.8%

24 SDC & Bond Proceeds Investment Income 160,000$ 40,000$ (120,000)$ NA25 Master Plan Designated 2,659,690 3,425,473 765,783 28.8%26 Repayment of Bond Payoff to Master Plan 2,250,000 2,365,000 115,000 5.1%27 TOTAL TRANSFER TO MASTER PLAN 5,069,690$ 5,830,473$ 760,783$ 15.0%

28 Reserve for Sec. 703 Bond Resolution 720,000$ 790,000$ 70,000$ 9.7%29 Negative Cash Flow Reserve 420,000 430,000 10,000 2.4%30 TOTAL RESERVE FUNDING 1,140,000$ 1,220,000$ 80,000$ 7.0%

31 TOTAL REVENUE REQUIREMENTS 102,192,819$ 106,872,840$ 4,680,021$ 4.6%

32 Net Income Available for Debt Service ( Ln #15 - Ln #17 ) 51,768,100$ 54,624,974$ 2,856,874$ 5.5%

33 Senior Parity & 2nd Lien Debt Service ( Line #23 ) 23,528,410$ 22,624,501$ (903,909)$ -3.8%

34 DEBT SERVICE COVERAGE ( Ln #32 / Ln #33 ) 2.20 2.41

35 ADJUSTMENT TO WATER RATES 3.9% 3.8%

Percentages may not add due to rounding

2015 Adopted Budget to 2014 Adopted Budget2015 Water Rate Increase = 3.8%

20 Year Model Approved 2015 Budget.xlsm - Schedule A 2/24/2015 at 10:29 AM- 13 -

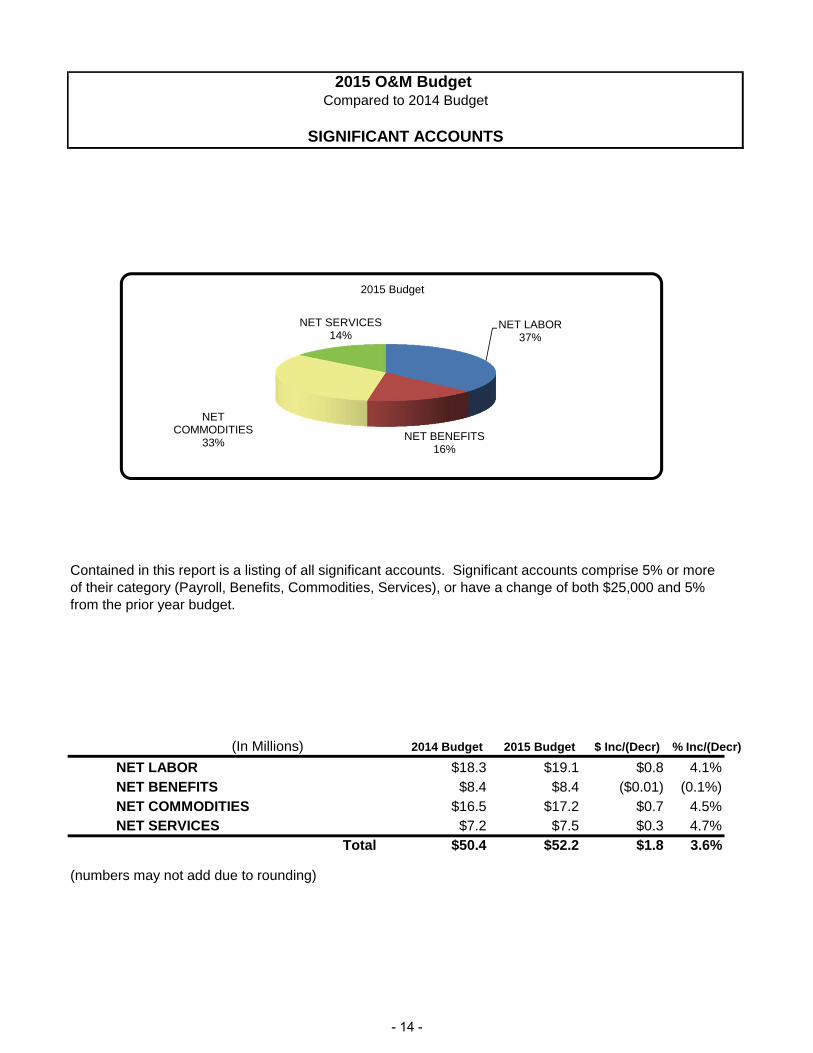

2015 O&M Budget Compared to 2014 Budget

SIGNIFICANT ACCOUNTS

(In Millions) 2014 Budget 2015 Budget $ Inc/(Decr) % Inc/(Decr)

NET LABOR $18.3 $19.1 $0.8 4.1%NET BENEFITS $8.4 $8.4 ($0.01) (0.1%)NET COMMODITIES $16.5 $17.2 $0.7 4.5%NET SERVICES $7.2 $7.5 $0.3 4.7%

Total $50.4 $52.2 $1.8 3.6%

(numbers may not add due to rounding)

Contained in this report is a listing of all significant accounts. Significant accounts comprise 5% or more of their category (Payroll, Benefits, Commodities, Services), or have a change of both $25,000 and 5% from the prior year budget.

NET LABOR37%

NET BENEFITS16%

NET COMMODITIES

33%

NET SERVICES14%

2015 Budget

- 14 -

2015 Budget Compared to 2014 Budget

By Category

ACCOUNTS ‐ BY CATEGORY

12/12/2014

2014 2015 $ DIF % DIF

PAYROLL

Labor ‐ Non OT 410010 23,088,044 23,892,933 804,889 3.5%

% Chg

2015 from 2014

Budget Budget

2014 Budget Gross Payroll 23,088,044$

Annual True‐Up of 2014 Base (291,814) ‐1.3%

2015 Beginning Base 22,796,230

New Authorizations 298,835 1.3%

23,095,065

Performance Compensation (a)

797,868 3.5%

Total Projected 2015 Labor Budget 23,892,933$ 3.5%

Percentages may not add due to rounding.

(a) Performance Compensation is calculated as a percent of Beginning Base Pay.

Labor‐Non OT Gross includes projected payroll costs for all authorized WaterOne

employees. In projecting labor, it is assumed that all current authorized positions are

filled as of January 1, 2015. Budgeted salaries have a reduction of 1% for slippage.

The 2015 Labor Budget is increasing a total of $804,889 or 3.5% over the 2014 Budget.

After the annual true‐up to reflect the actual outcome of payroll and benefits after

turn‐over, retirements and vacancies, the beginning base is $22,796,230.

- 15 -

12/12/2014

2014 2015 $ DIF % DIF

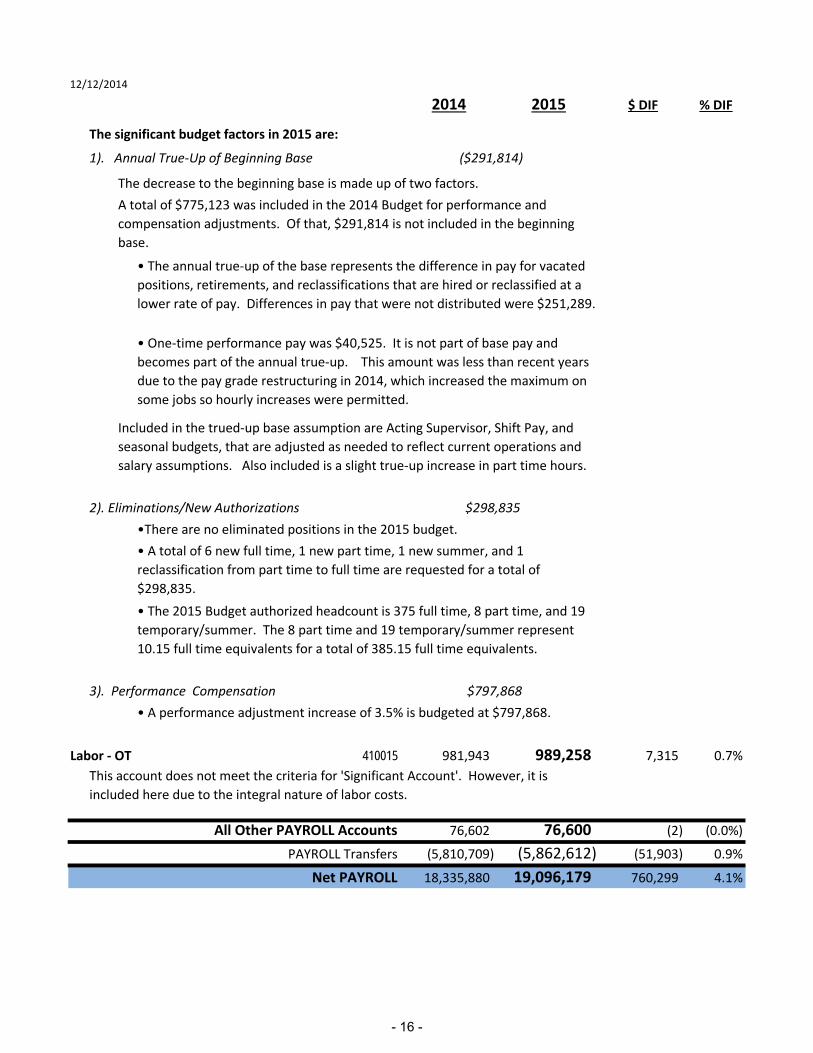

Labor ‐ OT 410015 981,943 989,258 7,315 0.7%

All Other PAYROLL Accounts 76,602 76,600 (2) (0.0%)

PAYROLL Transfers (5,810,709) (5,862,612) (51,903) 0.9%

Net PAYROLL 18,335,880 19,096,179 760,299 4.1%

1). Annual True‐Up of Beginning Base ($291,814)

The significant budget factors in 2015 are:

The decrease to the beginning base is made up of two factors.

A total of $775,123 was included in the 2014 Budget for performance and

compensation adjustments. Of that, $291,814 is not included in the beginning

base.

This account does not meet the criteria for 'Significant Account'. However, it is

included here due to the integral nature of labor costs.

Included in the trued‐up base assumption are Acting Supervisor, Shift Pay, and

seasonal budgets, that are adjusted as needed to reflect current operations and

salary assumptions. Also included is a slight true‐up increase in part time hours.

2). Eliminations/New Authorizations $298,835

3). Performance Compensation $797,868

• A performance adjustment increase of 3.5% is budgeted at $797,868.

•There are no eliminated positions in the 2015 budget.

• A total of 6 new full time, 1 new part time, 1 new summer, and 1

reclassification from part time to full time are requested for a total of

$298,835.

• The 2015 Budget authorized headcount is 375 full time, 8 part time, and 19

temporary/summer. The 8 part time and 19 temporary/summer represent

10.15 full time equivalents for a total of 385.15 full time equivalents.

• One‐time performance pay was $40,525. It is not part of base pay and

becomes part of the annual true‐up. This amount was less than recent years

due to the pay grade restructuring in 2014, which increased the maximum on

some jobs so hourly increases were permitted.

• The annual true‐up of the base represents the difference in pay for vacated

positions, retirements, and reclassifications that are hired or reclassified at a

lower rate of pay. Differences in pay that were not distributed were $251,289.

- 16 -

12/12/2014

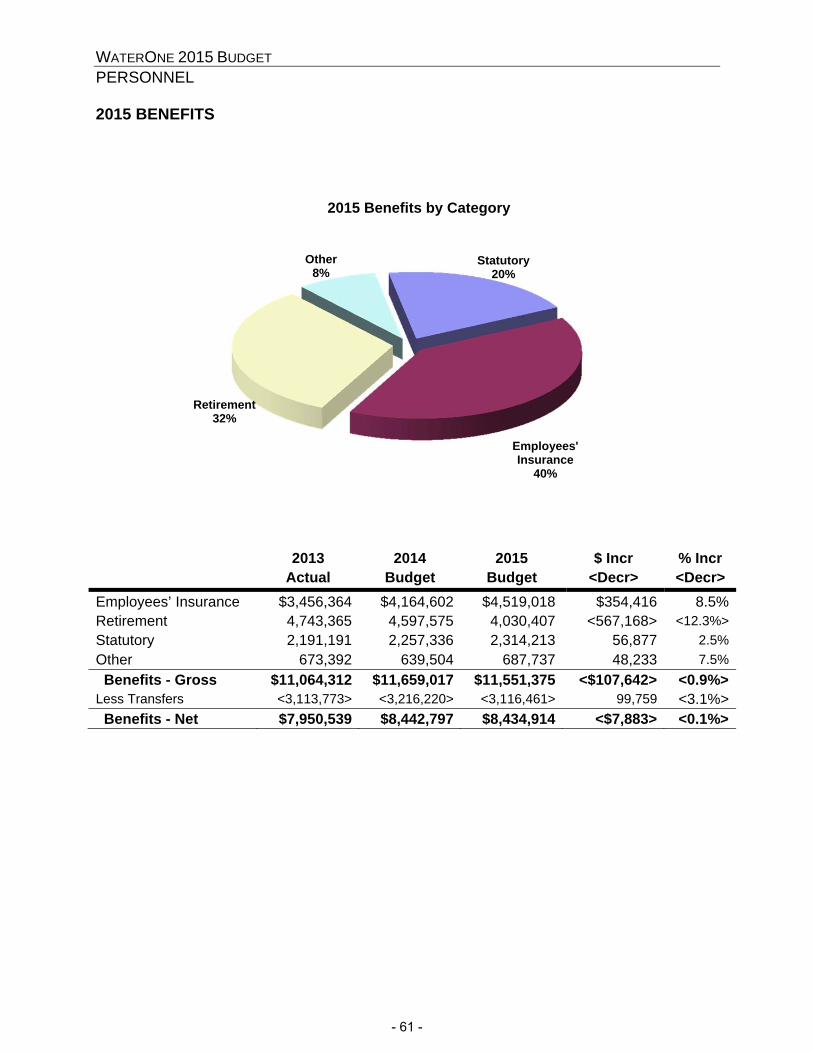

2014 2015 $ DIF % DIF

BENEFITS

Employee Insurance ‐ Health 413010 3,879,201 4,176,450 297,249 7.7%

Total Pension Accounts 3,997,575 3,630,407 (367,168) (9.2%)

% Change

from 2014

2015 Budget Budget

Defined Benefit (DB) Plans

412010 ‐ Defined Benefit 2,656,864 (13.3%)

412050 ‐ Cash Balance (New Plan) 55,426 NA (a)

Total DB Plans 2,712,290

Defined Contribution (DC) Plans

412020 ‐ Base 461,789 (16.6%)

412052 ‐ Base (New Plan) 72,956 NA (a)

Total DC ‐ Base 534,745

412030 ‐ Match 317,711 (16.6%)

412051 ‐ Match (New Plan) 65,661 NA (a)

Total DC ‐ Match 383,372

Grand Total Pension 3,630,407 (9.2%)

The budgeted components of the increase in health insurance are a 4.9% experience

premium increase, a 1% increase for the Affordable Care Act (ACA), and a 1.8%

increase for six additional full time personnel plus a reclassification from part time to

full time. Changes in the employee coverage mix are included in the 4.9% premium

increase.

The Total Pension budget is comprised of both Defined Benefit Plans and Defined

Contribution Plans, which include plans for employees hired prior to 1/1/2014 and

employees hired 1/1/2014 and after (the "new" plan). The total projected pension

cost has decreased, and the majority of the projected reduction is due to the addition

of a 2013 gain and the expiration of a 2004 loss in the pre‐2014 Defined Benefit Plan.

(a) The 2014 budget for these accounts was zero. The plans did not become effective

until 01/01/2014

- 17 -

12/12/2014

2014 2015 $ DIF % DIF

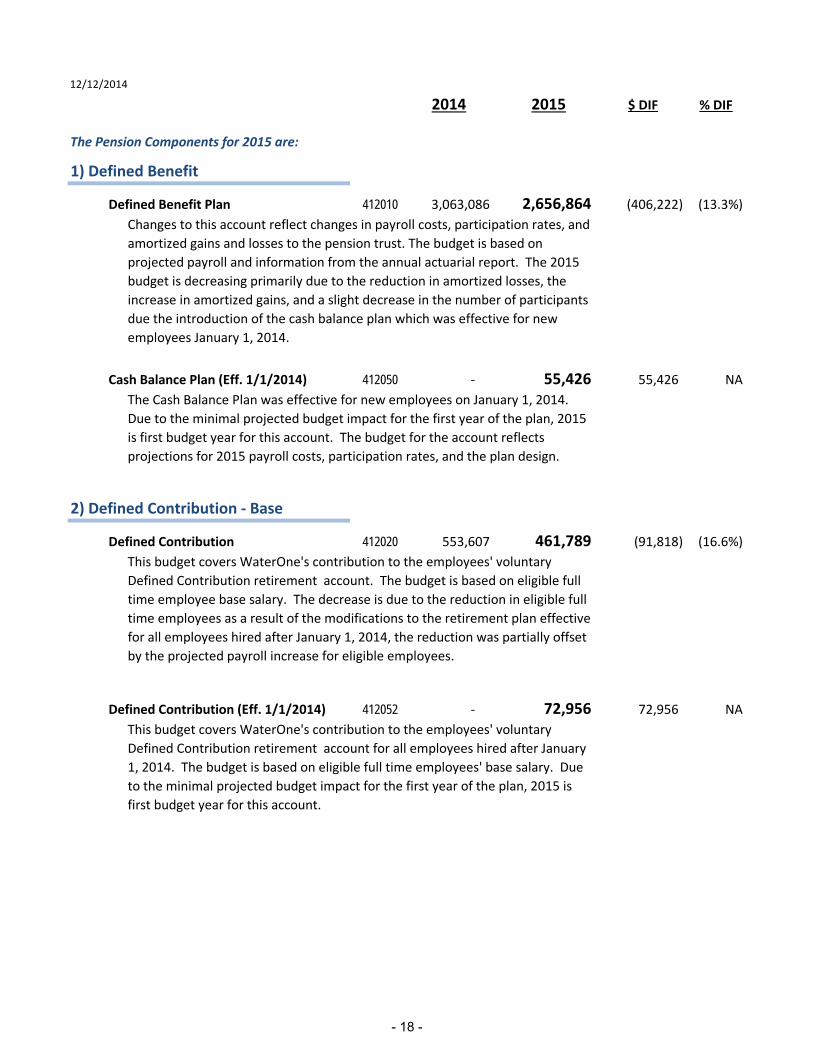

The Pension Components for 2015 are:

1) Defined Benefit

Defined Benefit Plan 412010 3,063,086 2,656,864 (406,222) (13.3%)

Cash Balance Plan (Eff. 1/1/2014) 412050 ‐ 55,426 55,426 NA

2) Defined Contribution ‐ Base

Defined Contribution 412020 553,607 461,789 (91,818) (16.6%)

Defined Contribution (Eff. 1/1/2014) 412052 ‐ 72,956 72,956 NA

The Cash Balance Plan was effective for new employees on January 1, 2014.

Due to the minimal projected budget impact for the first year of the plan, 2015

is first budget year for this account. The budget for the account reflects

projections for 2015 payroll costs, participation rates, and the plan design.

This budget covers WaterOne's contribution to the employees' voluntary

Defined Contribution retirement account. The budget is based on eligible full

time employee base salary. The decrease is due to the reduction in eligible full

time employees as a result of the modifications to the retirement plan effective

for all employees hired after January 1, 2014, the reduction was partially offset

by the projected payroll increase for eligible employees.

This budget covers WaterOne's contribution to the employees' voluntary

Defined Contribution retirement account for all employees hired after January

1, 2014. The budget is based on eligible full time employees' base salary. Due

to the minimal projected budget impact for the first year of the plan, 2015 is

first budget year for this account.

Changes to this account reflect changes in payroll costs, participation rates, and

amortized gains and losses to the pension trust. The budget is based on

projected payroll and information from the annual actuarial report. The 2015

budget is decreasing primarily due to the reduction in amortized losses, the

increase in amortized gains, and a slight decrease in the number of participants

due the introduction of the cash balance plan which was effective for new

employees January 1, 2014.

- 18 -

12/12/2014

2014 2015 $ DIF % DIF

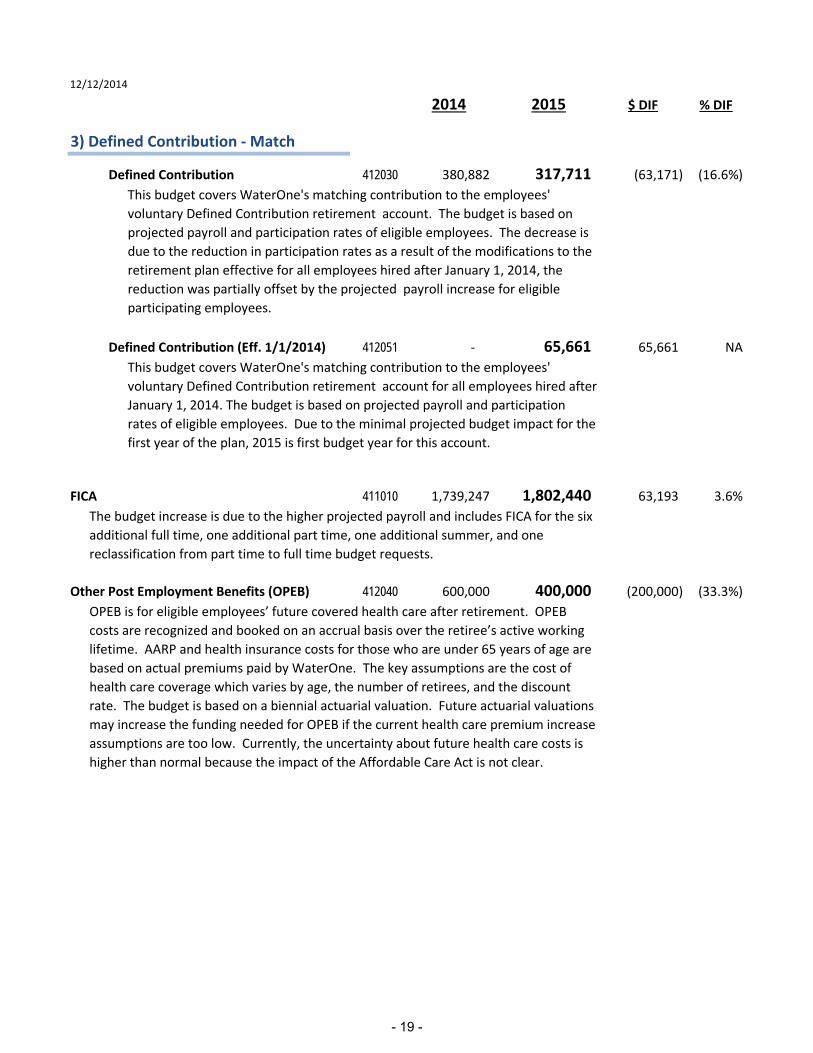

3) Defined Contribution ‐ Match

Defined Contribution 412030 380,882 317,711 (63,171) (16.6%)

Defined Contribution (Eff. 1/1/2014) 412051 ‐ 65,661 65,661 NA

FICA 411010 1,739,247 1,802,440 63,193 3.6%

Other Post Employment Benefits (OPEB) 412040 600,000 400,000 (200,000) (33.3%)

OPEB is for eligible employees’ future covered health care after retirement. OPEB

costs are recognized and booked on an accrual basis over the retiree’s active working

lifetime. AARP and health insurance costs for those who are under 65 years of age are

based on actual premiums paid by WaterOne. The key assumptions are the cost of

health care coverage which varies by age, the number of retirees, and the discount

rate. The budget is based on a biennial actuarial valuation. Future actuarial valuations

may increase the funding needed for OPEB if the current health care premium increase

assumptions are too low. Currently, the uncertainty about future health care costs is

higher than normal because the impact of the Affordable Care Act is not clear.

This budget covers WaterOne's matching contribution to the employees'

voluntary Defined Contribution retirement account for all employees hired after

January 1, 2014. The budget is based on projected payroll and participation

rates of eligible employees. Due to the minimal projected budget impact for the

first year of the plan, 2015 is first budget year for this account.

This budget covers WaterOne's matching contribution to the employees'

voluntary Defined Contribution retirement account. The budget is based on

projected payroll and participation rates of eligible employees. The decrease is

due to the reduction in participation rates as a result of the modifications to the

retirement plan effective for all employees hired after January 1, 2014, the

reduction was partially offset by the projected payroll increase for eligible

participating employees.

The budget increase is due to the higher projected payroll and includes FICA for the six

additional full time, one additional part time, one additional summer, and one

reclassification from part time to full time budget requests.

- 19 -

12/12/2014

2014 2015 $ DIF % DIF

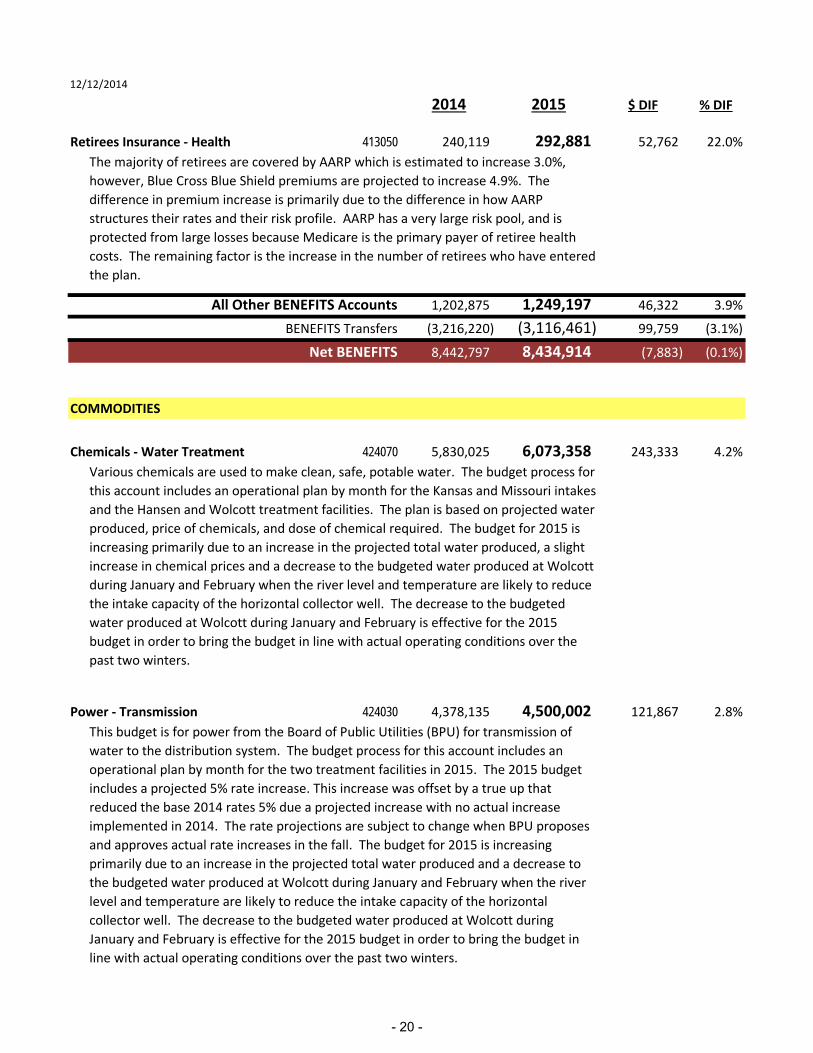

Retirees Insurance ‐ Health 413050 240,119 292,881 52,762 22.0%

All Other BENEFITS Accounts 1,202,875 1,249,197 46,322 3.9%

BENEFITS Transfers (3,216,220) (3,116,461) 99,759 (3.1%)

Net BENEFITS 8,442,797 8,434,914 (7,883) (0.1%)

COMMODITIES

Chemicals ‐ Water Treatment 424070 5,830,025 6,073,358 243,333 4.2%

Power ‐ Transmission 424030 4,378,135 4,500,002 121,867 2.8%

This budget is for power from the Board of Public Utilities (BPU) for transmission of

water to the distribution system. The budget process for this account includes an

operational plan by month for the two treatment facilities in 2015. The 2015 budget

includes a projected 5% rate increase. This increase was offset by a true up that

reduced the base 2014 rates 5% due a projected increase with no actual increase

implemented in 2014. The rate projections are subject to change when BPU proposes

and approves actual rate increases in the fall. The budget for 2015 is increasing

primarily due to an increase in the projected total water produced and a decrease to

the budgeted water produced at Wolcott during January and February when the river

level and temperature are likely to reduce the intake capacity of the horizontal

collector well. The decrease to the budgeted water produced at Wolcott during

January and February is effective for the 2015 budget in order to bring the budget in

line with actual operating conditions over the past two winters.

Various chemicals are used to make clean, safe, potable water. The budget process for

this account includes an operational plan by month for the Kansas and Missouri intakes

and the Hansen and Wolcott treatment facilities. The plan is based on projected water

produced, price of chemicals, and dose of chemical required. The budget for 2015 is

increasing primarily due to an increase in the projected total water produced, a slight

increase in chemical prices and a decrease to the budgeted water produced at Wolcott

during January and February when the river level and temperature are likely to reduce

the intake capacity of the horizontal collector well. The decrease to the budgeted

water produced at Wolcott during January and February is effective for the 2015

budget in order to bring the budget in line with actual operating conditions over the

past two winters.

The majority of retirees are covered by AARP which is estimated to increase 3.0%,

however, Blue Cross Blue Shield premiums are projected to increase 4.9%. The

difference in premium increase is primarily due to the difference in how AARP

structures their rates and their risk profile. AARP has a very large risk pool, and is

protected from large losses because Medicare is the primary payer of retiree health

costs. The remaining factor is the increase in the number of retirees who have entered

the plan.

- 20 -

12/12/2014

2014 2015 $ DIF % DIF

Power ‐ Source 424020 2,255,041 2,309,315 54,274 2.4%

Power ‐ Distribution 424010 1,316,665 1,352,422 35,757 2.7%

Inventory Withdrawals 421010 1,164,627 1,246,233 81,606 7.0%

Material & Supplies 421070 1,124,596 1,361,185 236,589 21.0%

Material and supplies are non‐inventory items that are necessary to operate and

maintain WaterOne facilities. The budget increase in 2015 reflects trends and also

includes non‐inventory parts previously budgeted in 'Vehicle Repair Services'. Not

including the transferred budget, the increase is $41k or 3.6%.

This budget is for power from the Board of Public Utilities (BPU) at source or intake

facilities. The budget process for this account includes an operational plan by month

for the four sources in 2015. The 2015 budget includes a projected 5% rate increase.

This increase was offset by a true up that reduced the base 2014 rates 5% due a

projected increase with no actual increase implemented in 2014. The rate projections

are subject to change when BPU proposes and approves actual rate increases in the

fall. The budget for 2015 is increasing primarily due to an increase in the projected

total water produced and a decrease to the budgeted water produced at Wolcott

during January and February when the river level and temperature are likely to reduce

the intake capacity of the horizontal collector well. The decrease to the budgeted

water produced at Wolcott during January and February is effective for the 2015

budget in order to bring the budget in line with actual operating conditions over the

past two winters.

This budget is for power primarily from Kansas City Power & Light (KCP&L) at the pump

stations throughout the distribution system. The budget process for this account

includes an analysis of the historical trends for power use at each of the large pump

stations. The budget is increased primarily due to an adopted 2.3% KCP&L rate

increase as well as increased projected power usage at pump stations in the southern

areas of the distribution system.

This budget covers stock material, parts and commodities, including fuel for the fleet,

used from inventory. The price per gallon is $3.48 for 2015 vs $3.54 in 2014. Fuel is

budgeted based on a seven year average of price increases applied to the current price

and average gallons used. Fuel makes up approximately 70% of this budget. The

increase in this account is primarily for non‐fuel inventory in Construction and

Maintenance associated with the average number of main breaks trending up.

- 21 -

12/12/2014

2014 2015 $ DIF % DIF

Safety Equipment & Supplies 421110 62,269 88,051 25,782 41.4%

All Other COMMODITIES Accounts 941,244 927,780 (13,464) (1.4%)

COMMODITIES Transfers (619,924) (673,406) (53,482) 8.6%

Net COMMODITIES 16,452,678 17,184,940 732,262 4.5%

SERVICES

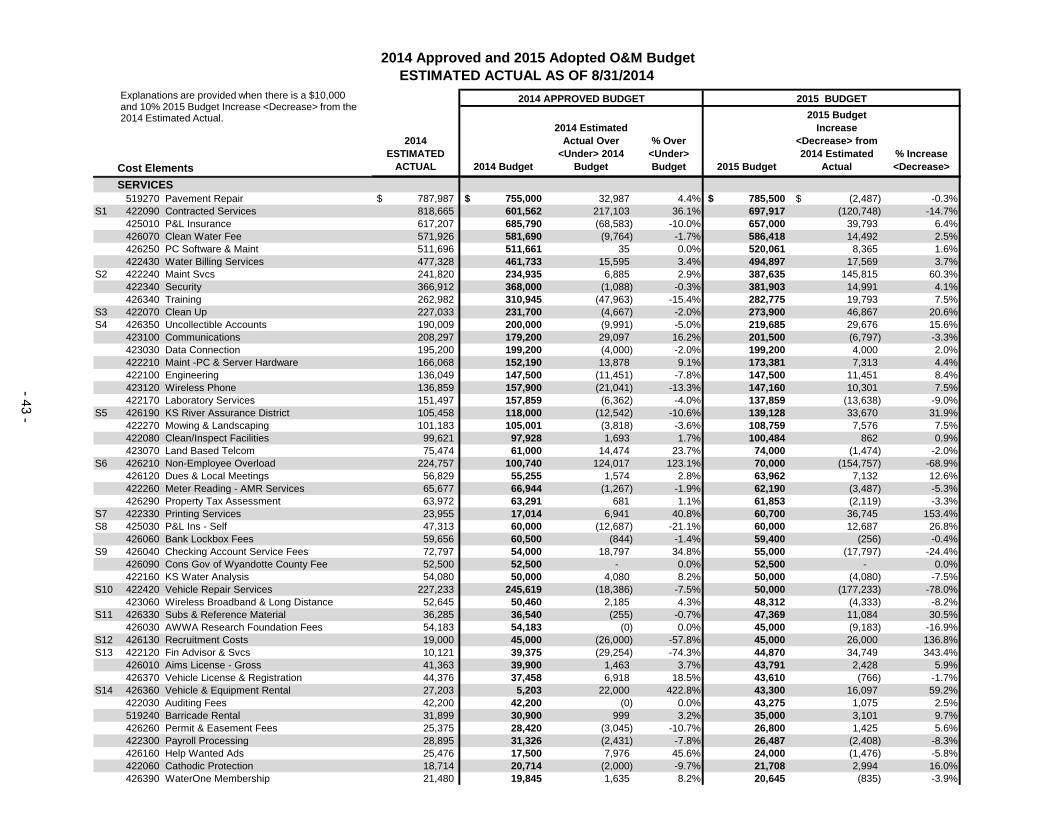

Pavement Repair 422290 755,000 785,500 30,500 4.0%

Property & Liability Insurance 425010 690,790 657,000 (33,790) (4.9%)

Contracted Services 422090 601,562 700,809 99,247 16.5%

Clean Drinking Water Fee 426070 581,690 586,418 4,728 0.8%

The budget includes insurance premiums for General Liability, Property, Pollution,

Umbrella, Crime, Licenses, and Fiduciary Insurance. The budget is based on the actual

7/1/2014 renewals. The decrease was mostly due to a reduction in costs for Property

coverage.

These are services that are not cost‐effective to complete in‐house. Budgets for

building services for the administrative headquarters and fire hydrant painting were

both increased to reflect historical spending. The increase also includes additional

services to support goals set in the Communications Plan.

The clean drinking water fee is assessed by the State of Kansas at three cents per

thousand gallons sold. The fee was put in place in lieu of sales tax in 2002.

Approximately 50% of the fee is transferred to capital expenditures through an

overhead. The budget is based on the projected number of retail gallons sold in a

normal year.

The increase to this account includes additional safety equipment in facilities

maintenance ‐ ventilated arc flash hoods, safety harnesses, and other fall protection

equipment. Other increases are for the purchase of additional automated external

defibrillator (AED) and the related maintenance.

Pavement Repair consists of the restoration of pavement, curbs, and sidewalks

damaged because of transmission and distribution construction repairs. The budget is

based on historical analysis, which includes a trended number of main breaks and a

trended cost per break. The budget for 2015 is higher than 2014 based on main

breaks trending higher.

- 22 -

12/12/2014

2014 2015 $ DIF % DIF

PC Software License & Maintenance 426250 511,661 520,061 8,400 1.6%

Water Billing Services 422430 461,733 494,897 33,164 7.2%

Vehicle Repair Services 422420 245,619 50,000 (195,619) (79.6%)

Maintenance Services 422240 234,935 387,635 152,700 65.0%

The budget is for outsourced maintenance services that are not cost‐effective to

complete in‐house. The budget is increasing due to the higher costs of the Kansas

River wells rehab and the first required maintenance contract for the Missouri River

horizontal collector well. The horizontal collector well maintenance work will be

completed by the end of 2014 and the charges will begin amortization during 2015.

Other increases include repairs at the administrative headquarters and additional lab

equipment maintenance.

This category is for outside services for vehicle repair. The more difficult and time

consuming projects are outsourced when in‐house experienced staff is not available.

In previous years this account has included material and supplies utilized during in‐

house vehicle maintenance. The budget for 2015 has been reduced in order to move

those expenses into the material and supplies budget.

The printing and mailing of water bills is outsourced. There are two items in this

budget. The first is water bills, which includes regular, corrected, and final bills. The

budget is developed using actual bills and customer counts. There is a a savings from

the increase in the ebill adoption rate, but this savings is offset by an increase the

number of billing inserts and the corresponding increase in postage and paper costs.

The second part of the budget is for dunning notices, which are budgeted based on

actual history.

1. PC and Application software: SAP, Microsoft, document management system, virus

protection, and miscellaneous software. This portion of the budget has increased

primarily due increases in the annual maintenance contracts for SAP and Microsoft.

2. GIS software: GIS, computer aided design, hydraulic modeling, and SCADA software.

This account decreased slightly in 2015 primarily due to a reduction in the budgeted

annual ESRI contract.

This account covers the District’s software licenses and maintenance on that software.

It is divided into two areas. One area experienced a budget increase while the other

decreased in 2015 which is described below.

- 23 -

12/12/2014

2014 2015 $ DIF % DIF

Training 426340 310,945 282,775 (28,170) (9.1%)

Clean Up 422070 231,700 273,900 42,200 18.2%

Non‐Employee Overload 426210 100,740 70,000 (30,740) (30.5%)

Printing Services 422330 17,014 60,700 43,686 256.8%

Vehicle & Equipment Rental 426360 5,203 43,300 38,097 732.2%

All Other SERVICES Accounts 3,112,605 3,205,781 93,176 3.0%

SERVICES Transfers (667,833) (586,943) 80,890 (12.1%)

Net SERVICES 7,193,364 7,531,833 338,469 4.7%

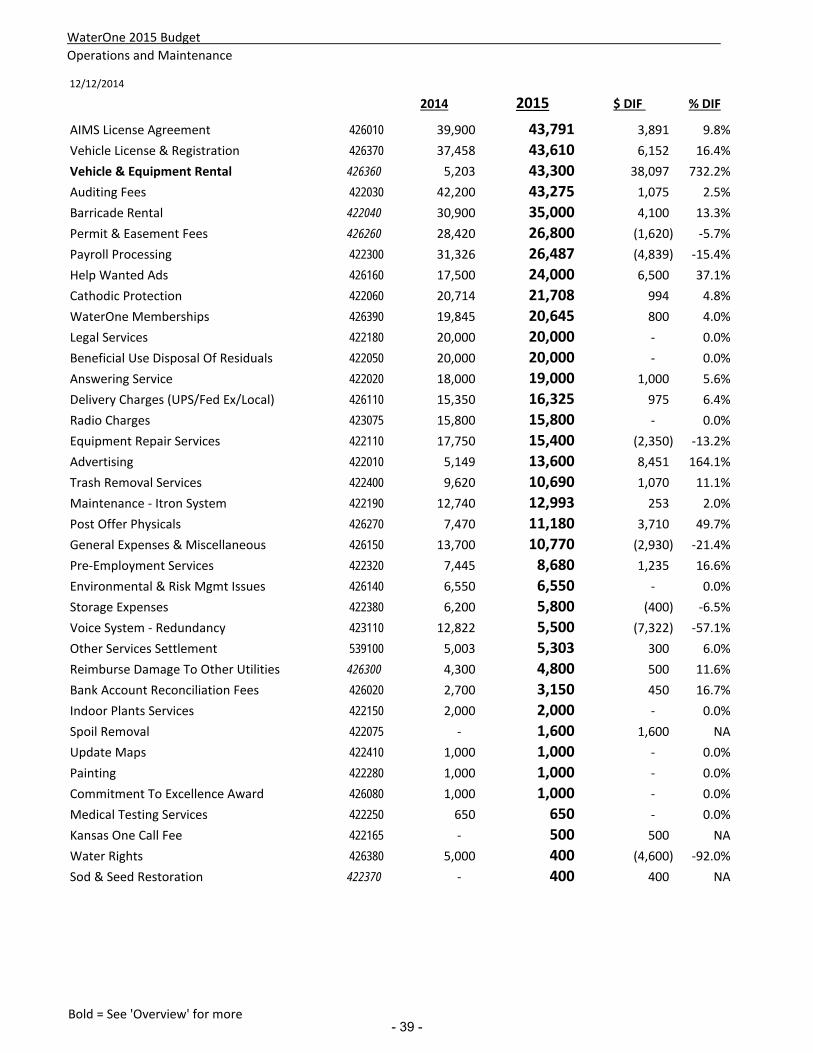

GRAND TOTAL 50,424,719 52,247,866 1,823,147 3.6%

Numbers may not add due to rounding

H:\Finance\FINSHARE\1BUDGET\2015 Budget\OandM\[District Level O_M Comparison‐15Z.xlsx]By Category‐SIGNIF

This account is used for rental of equipment when WaterOne assets are under repair

and for special equipment needed on an irregular basis. The 2015 budget includes an

increase for the rental of vehicles for summer hydrant auditors. With the rebound in

the economy, fleet utilization has increased and vehicles are no longer available for

summer staff to use. It is more efficient to rent vehicles for the summer months than

it is to add vehicles to the fleet. The remainder of the increase is based on the actual

historical trend which is higher than the 2014 budget.

Increases to this account are primarily due to the following programs: a $25,300

increase to printed materials for the Smart Watering Campaign, $6,800 in materials for

the new Pro Tap campaign, and an increase of $6,000 of printed material for Notify

JoCo.

Non‐Employee overload for Mapping and Drafting was increased from half time to full

time. All other non‐employee overload from 2014 has been eliminated including fleet

clerical, a lab chemist, and records center clerical.

Clean Up includes the removal of construction debris, addition of topsoil, site grading

as well as reseeding or sod replacement. It is the second largest component of main

break costs after pavement repair. The budget is based on average actual history and

the increase is associated with the average number of main breaks trending up.

Training is reduced based on actual trends.

- 24 -

WaterOne 2015 BudgetOVERVIEW

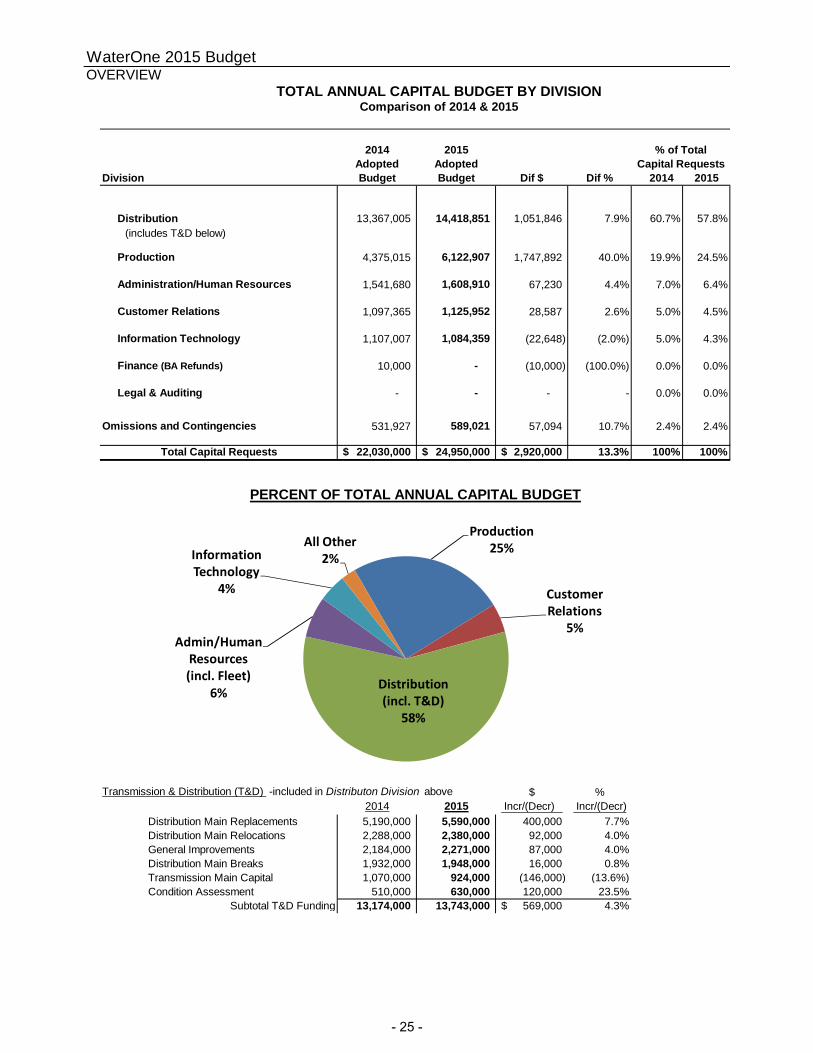

TOTAL ANNUAL CAPITAL BUDGET BY DIVISIONComparison of 2014 & 2015

2014 2015Adopted Adopted

Division Budget Budget Dif $ Dif % 2014 2015

Distribution 13,367,005 14,418,851 1,051,846 7.9% 60.7% 57.8%(includes T&D below)

Production 4,375,015 6,122,907 1,747,892 40.0% 19.9% 24.5%

Administration/Human Resources 1,541,680 1,608,910 67,230 4.4% 7.0% 6.4%

Customer Relations 1,097,365 1,125,952 28,587 2.6% 5.0% 4.5%

Information Technology 1,107,007 1,084,359 (22,648) (2.0%) 5.0% 4.3%

Finance (BA Refunds) 10,000 - (10,000) (100.0%) 0.0% 0.0%

Legal & Auditing - - - - 0.0% 0.0%

Omissions and Contingencies 531,927 589,021 57,094 10.7% 2.4% 2.4%

Total Capital Requests 22,030,000$ 24,950,000$ 2,920,000$ 13.3% 100% 100%

Transmission & Distribution (T&D) -included in Distributon Division above $ %2014 2015 Incr/(Decr) Incr/(Decr)

Distribution Main Replacements 5,190,000 5,590,000 400,000 7.7%Distribution Main Relocations 2,288,000 2,380,000 92,000 4.0%General Improvements 2,184,000 2,271,000 87,000 4.0%Distribution Main Breaks 1,932,000 1,948,000 16,000 0.8%Transmission Main Capital 1,070,000 924,000 (146,000) (13.6%)Condition Assessment 510,000 630,000 120,000 23.5%

Subtotal T&D Funding 13,174,000 13,743,000 569,000$ 4.3%

% of TotalCapital Requests

PERCENT OF TOTAL ANNUAL CAPITAL BUDGET

Production25%

Customer Relations

5%

Distribution (incl. T&D)

58%

Admin/Human Resources (incl. Fleet)

6%

Information Technology

4%

All Other2%

- 25 -

This page intentionally left blank.

- 26 -

WATERONE 2015 BUDGET REVENUES & RATES

2015 REVENUE SUMMARY

OPERATING REVENUE ASSUMPTIONS Comparison of Revenues Revenue Type 2014 Budget 2015 Budget $ Inc<Dec> % Inc<Dec> Sales of Water $100,347,319 $104,958,840 $ 4,611,521 4.6%Other Operating Revenues 1,415,500 1,454,000 38,500 2.7%Investment Income 430,000 460,000 30,000 7.0%Total $102,192,819 $106,872,840 $4,680,021 4.6% Sales of Water Sales of Water in 2015 is projected to increase 4.6% or $4,611,521

An overall 3.8% rate increase is proposed, which will produce $3,882,584 additional water sales revenue.

1,300 new customers will provide additional revenue of $915,837. WaterOne projects new customer growth by analyzing the long term historical average as well as the recent growth trends.

The true-up of 2013 actual and 2014 estimated actual for customer growth caused a revenue increase of $468,395. The 2014 budget for customer growth is 1,000 and the estimated actual is 1,300.

A 1% budgeted reduction in single family residential (R1) gallons per customer caused revenues to decrease by $448,529. A reduction in multi-family residential (M1) and small commercial (C1) gallons per customer caused revenue to decrease $102,885. Trends in residential usage are declining due to more efficient appliances and plumbing fixtures.

The water sales budget is developed assuming “normal” weather which means that average temperature, rainfall, and rain frequency are assumed.

- 27 -

WATERONE 2015 BUDGET REVENUES & RATES

Other Operating Revenues Delayed Payment Charges Delayed Payment Charges are applied to water bills paid after the due date. Budgeted revenues from this source are $570,000 which is no change from the 2014 budget. Field Service Charges Field Service Charges are assessed when service is restored after being shut off for delinquent payment or other rule violations. This category also includes charges assessed for returned checks. Field Service Charges for 2015 are budgeted to be $320,000, which is a 6.7% increase from the 2014 budget. This account is budgeted based on trends which have been increasing. Miscellaneous Revenue Miscellaneous Revenue includes revenue sources from interest income on WaterOne checking accounts, rental income from farm land and wireless phone antennas, sale of miscellaneous equipment, purchasing card revenue sharing, reimbursements from Johnson County Wastewater for WaterOne’s IT time, and HomeServe commissions. It is budgeted that these revenues will total $564,000, an increase of $18,500 or 3.4% when compared to the 2014 budget. This increase is due to increased checking account interest and antenna rental income. The antenna rental income budget is based on scheduled increases agreed upon in the rental contracts . Five of the seven contracts are scheduled to increase in 2015. INVESTMENT INCOME Investment income is earned on invested balances in the General Fund and on Master Plan funds. Investment income in 2015 is budgeted to be $460,000. This is an increase of $30,000 or 7.0% relative to the 2014 budget. The increase is primarily due to a higher projected General Fund balance. NON-OPERATING REVENUE (not a funding source for the Annual Budget) System Development Charges (SDCs) SDCs are paid by new customers when they apply for a service connection permit. They cannot be used for operating expenses and therefore the revenue is not included as a funding source for the annual budget. SDCs are used exclusively at this time to fund Master Plan, though they could be utilized for retirement of debt should the right opportunity arise. For 2015, SDC income is budgeted at $6,311,500 compared to the 2014 budget of $4,855,000. SDCs are conservatively budgeted by assuming that all of the budgeted customer growth will be 5/8” service connections.

- 28 -

WATERONE 2015 BUDGET REVENUES & RATES

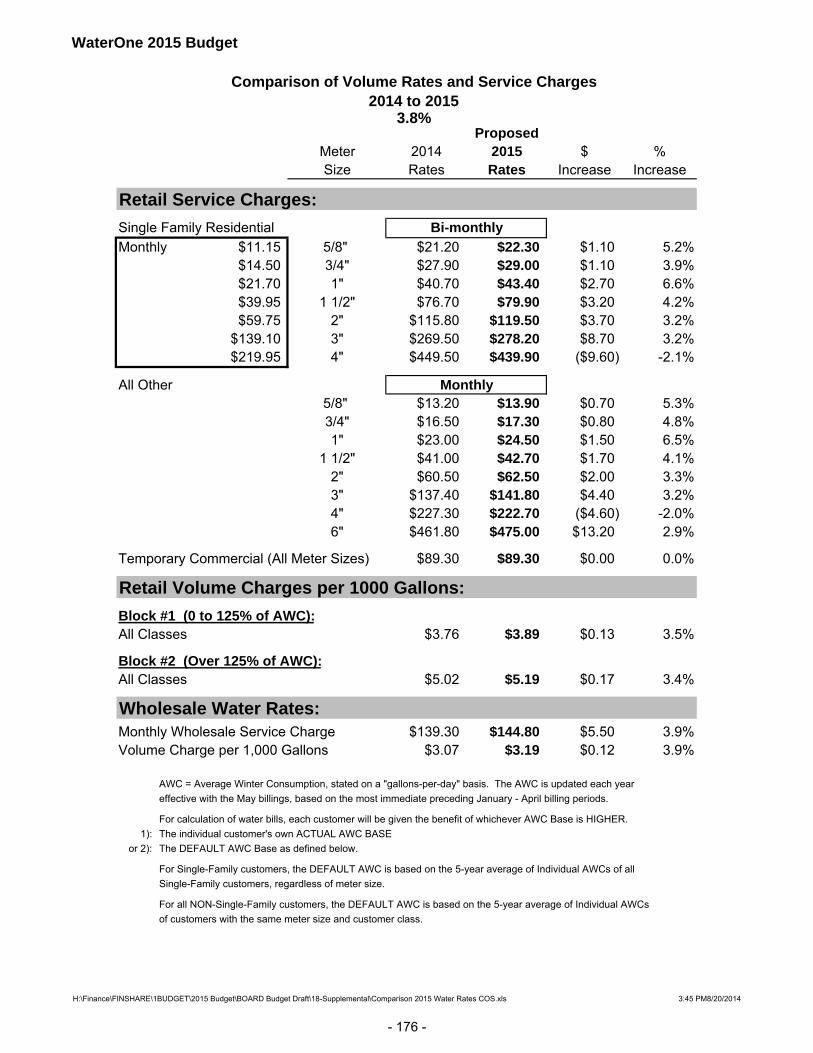

WATER RATE STRUCTURE WaterOne uses a Peak Management Rate (PMR) fee structure for water rates. This is an inclining rate structure designed to encourage customers to reduce peak usage. This delays the need for additional capacity and/or recovers costs more equitably from those customers who choose to have peak water usage. PMR rates are designed to charge a higher amount for water usage above the customer’s base usage. Block 1 rates are for volumes up to 125% of the customer’s Average Winter Consumption (AWC). Block 2 rates are for those gallons used in excess of 125% of the customer’s AWC. Each customer’s AWC is calculated individually based on their actual consumption over the prior winter. There is also a Default AWC for each customer class and the customer is given the benefit of whichever is higher. The Default AWC is used when no individual customer AWC is set, such as for new customers. The typical customer is defined by a usage pattern of 7,500 gallons per month. This number of gallons is the benchmark for the American Water Works Association (AWWA). The typical customer’s bill is calculated as follows:

Block Gallons 2015 Rates per 1,000 gallons Total 1 5,930 $3.89 $23.07 2 1,570 $5.19 $8.15

Service Charge NA $11.15 $11.15 7,500 $42.37 The 2015 rate increase requires the typical customer to pay an additional $1.58 per month. The schedule on the following page provides the monthly bill impact for a variety of customers.

- 29 -

Rate Class Meter Monthly Block 1 2014 2015 % Monthly

Size Consumption (In Gallons)

Gallon % Avg Bill Avg Bill Increase/

(Decrease)

Increase/

(Decrease)

AWWA Typical Customer 5/8" 7,500 79% 40.79$ 42.37$ 3.9% 1.58$

Single Family Residential

Low Usage 5/8" 3,662 98% 24.46$ 25.49$ 4.2% 1.03$

Moderate Usage 5/8" 7,212 86% 38.99$ 40.52$ 3.9% 1.53$

High Usage 5/8" 12,061 64% 61.42$ 63.71$ 3.7% 2.29$

Low Usage 1" 4,014 93% 35.80$ 37.68$ 5.3% 1.88$

Moderate Usage 1" 9,597 71% 59.94$ 62.65$ 4.5% 2.71$

High Usage 1" 27,324 40% 143.74$ 149.30$ 3.9% 5.56$

Multi‐Family Residential

Low Usage 1" 10,087 99% 61.05$ 63.87$ 4.6% 2.82$

Moderate Usage 1" 20,463 97% 100.71$ 104.90$ 4.2% 4.19$

High Usage 1" 44,901 76% 205.40$ 213.17$ 3.8% 7.77$

Low Usage 1 1/2" 22,503 99% 125.90$ 130.53$ 3.7% 4.63$

Moderate Usage 1 1/2" 40,447 98% 194.10$ 201.09$ 3.6% 6.99$

High Usage 1 1/2" 91,255 74% 414.01$ 428.53$ 3.5% 14.52$

Low Usage 2" 26,213 99% 159.39$ 164.81$ 3.4% 5.42$

Moderate Usage 2" 51,055 97% 254.40$ 263.10$ 3.4% 8.70$

High Usage 2" 143,952 67% 661.61$ 684.23$ 3.4% 22.62$

Small Commercial

Low Usage 5/8" 631 99% 15.58$ 16.36$ 5.0% 0.78$

Moderate Usage 5/8" 2,666 93% 23.46$ 24.51$ 4.5% 1.05$

High Usage 5/8" 17,979 63% 89.18$ 92.49$ 3.7% 3.31$

Low Usage 3/4" 1,546 97% 22.47$ 23.38$ 4.0% 0.91$

Moderate Usage 3/4" 7,929 73% 49.11$ 50.93$ 3.7% 1.82$

High Usage 3/4" 37,045 42% 182.96$ 189.34$ 3.5% 6.38$

Low Usage 1" 2,630 98% 32.95$ 34.80$ 5.6% 1.85$

Moderate Usage 1" 12,543 80% 73.32$ 76.55$ 4.4% 3.23$

High Usage 1" 51,618 51% 248.95$ 258.17$ 3.7% 9.22$

Large Commercial

Low Usage 1 1/2" 13,793 89% 94.77$ 98.33$ 3.8% 3.56$

High Usage 1 1/2" 104,689 59% 488.71$ 505.74$ 3.5% 17.03$

Low Usage 2" 25,028 92% 157.13$ 162.46$ 3.4% 5.33$

High Usage 2" 175,355 65% 797.17$ 824.42$ 3.4% 27.25$

Low Usage 3" 100,277 90% 527.08$ 544.91$ 3.4% 17.83$

High Usage 3" 522,029 69% 2,304.14$ 2,382.87$ 3.4% 78.73$

Low Usage 4" 327,298 96% 1,474.43$ 1,512.91$ 2.6% 38.48$

High Usage 4" 2,872,859 77% 11,861.81$ 12,257.11$ 3.3% 395.30$

Proposed

Monthly Bill Impact

By Rate Class and Meter Size

- 30 -

HISTORY OF WATER SALES BY RATE CLASS

Wet Normal Very Dry Normal Normal Normal

In Million $'s 2010 2011 2012 20132014

Budget2015

BudgetR1 52.0$ 59.4$ 74.3$ 63.0$ 64.0$ 66.8$ M1 7.7$ 8.3$ 9.5$ 9.0$ 9.7$ 10.2$ C1 4.4$ 5.1$ 6.4$ 5.3$ 5.4$ 5.8$ C2 16.4$ 18.9$ 24.0$ 19.9$ 20.9$ 22.0$ C3 0.3$ 0.3$ 0.5$ 0.4$ 0.4$ 0.3$ W1 -$ -$ -$ -$ -$ -$

Total 80.9$ 92.0$ 114.7$ 97.6$ 100.3$ 105.0$

R1 = Single Family Residential C2 = Large CommercialM1 = Multi-Family Residential C3 = Temporary CommercialC1 = Small Commercial W1 = Wholesale

H:\Finance\FINSHARE\1BUDGET\2015 Budget\BOARD Budget Draft\05-Revenues and Rates\[2015 Summary Charts.xls]SalesHistory 2015 8/27/14 9:25 AM

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

2010 2011 2012 2013 2014Budget

2015Budget

W1

C3

C2

C1

M1

R1

Millions

- 31 -

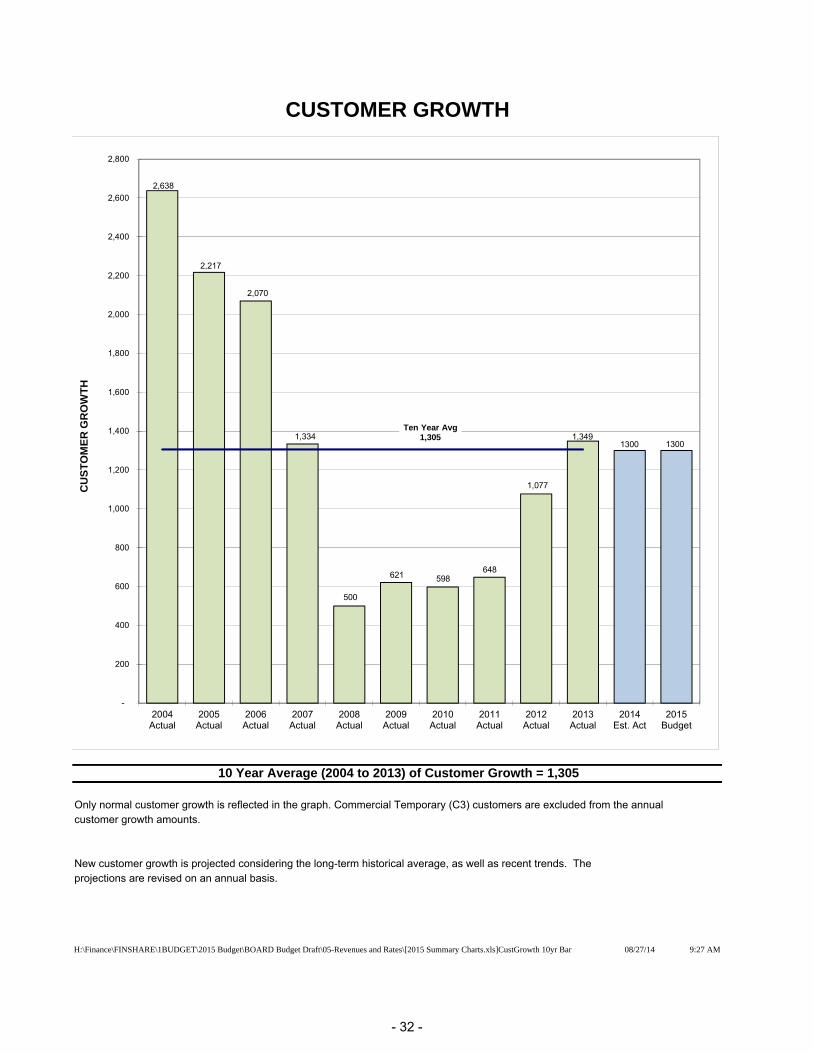

CUSTOMER GROWTH

Only normal customer growth is reflected in the graph. Commercial Temporary (C3) customers are excluded from the annualcustomer growth amounts.

New customer growth is projected considering the long-term historical average, as well as recent trends. Theprojections are revised on an annual basis.

H:\Finance\FINSHARE\1BUDGET\2015 Budget\BOARD Budget Draft\05-Revenues and Rates\[2015 Summary Charts.xls]CustGrowth 10yr Bar 08/27/14 9:27 AM

10 Year Average (2004 to 2013) of Customer Growth = 1,305

2,638

2,217

2,070

1,334

500

621 598 648

1,077

1,349 1300 1300

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2,800

2004Actual

2005Actual

2006Actual

2007Actual

2008Actual

2009Actual

2010Actual

2011Actual

2012Actual

2013Actual

2014Est. Act

2015Budget

CU

ST

OM

ER

GR

OW

TH

Ten Year Avg 1,305

- 32 -

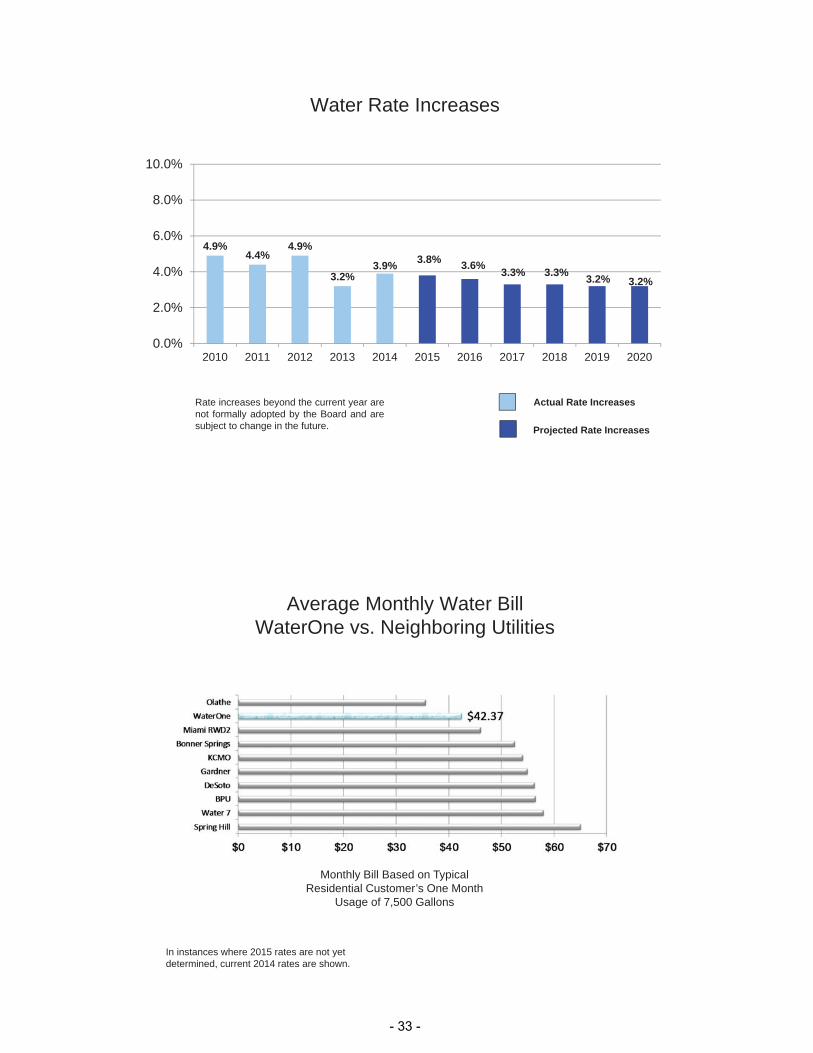

Water Rate Increases

Actual Rate Increases

Projected Rate Increases

Rate increases beyond the current year arenot formally adopted by the Board and aresubject to change in the future.

4.9%4.4%

4.9%

3.2%3.9% 3.8% 3.6% 3.3% 3.3% 3.2% 3.2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Monthly Bill Based on Typical Residential Customer’s One Month

Usage of 7,500 Gallons

Average Monthly Water BillWaterOne vs. Neighboring Utilities

In instances where 2015 rates are not yet determined, current 2014 rates are shown.

- 33 -

$20

$30

$40

$50

$60

$70

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

WaterOne CPI (a)

4.9% 4.4% 4.9% 3.2% 3.9% 3.8% 3.6% 3.3% 3.3% 3.2% 3.2%

National Water & Sewer Index

Typi

cal (

R1)

Sin

gle

Fam

ily C

usto

mer

–7,

500

Gal

./ M

o.WaterOne vs. All Cities Water & Sewer System Maintenance CPI

Projected Rate Increases (b)

a) Actual CPI comes from the Department of Labor. CPI estimated at 3.6% in 2014 which is the one year change fromJune 2013 to June 2014. CPI estimated at 6.3% for 2015 through 2020 which is the 5 year average. All projectionson the assumed CPI rates are subject to change.

b) Rate increases beyond the current year are not formally adopted by the Board and are subject to change in thefuture.

0.0

1.0

2.0

3.0

4.0

5.0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

SDC Coverage Base Coverage Policy

• The Debt Service Coverage Ratio is the sum of the net operating revenues plus investment income available for debt service, divided by the annual debt service requirement. Debt service includes both bond principal and interest expense for Senior Parity and Second Lien Parity debt.

• WaterOne Board Policy Number 16 requires a budgeted debt service coverage ratio of at least 2.0 without SDCs. SDCs are used to enhance coverage above the policy level.

Projected, subject to change

Debt Service Coverage Ratio

Wet Normal Very Dry

Normal

- 34 -

WaterOne 2015 BudgetO&M

OPERATIONS & MAINTENANCE BUDGET BY DIVISIONComparison of 2014 & 2015

2014 2015Division Budget Budget $ Dif % Dif 2014 2015

Production 24,728,594$ 25,363,183$ 634,589$ 2.6% 49.0% 48.5%

Distribution 9,621,095 10,156,992 535,896 5.6% 19.1% 19.4%

Admin/Human Resources 4,670,131 4,727,708 57,577 1.2% 9.3% 9.0%

Customer Relations 4,043,489 4,068,893 25,404 0.6% 8.0% 7.8%

Information Technology 3,432,994 3,899,542 466,548 13.6% 6.8% 7.5%

Finance 1,852,854 1,964,957 112,103 6.1% 3.7% 3.8%

Legal & Auditing 1,501,571 1,490,317 (11,254) (0.7%) 3.0% 2.9%

General Manager 573,990 576,274 2,284 0.4% 1.1% 1.1%

TOTAL 50,424,719$ 52,247,866$ 1,823,147$ 3.6% 100% 100%(totals may not add due to rounding)

PERCENT OF TOTAL BUDGET BY DIVISION

H:\Finance\FINSHARE\1BUDGET\2015 Budget\OandM\[District Level O_M Comparison-15Z.xlsx]CY vs. PY by div

% of TotalO&M Requests

Production 48.5%

Distribution 19.4% Information

Technology 7.5%

Customer Relations 7.8%

Finance 3.8%

Admin/Human Resources

9.0%

Legal & Auditing 2.9%

General Manager 1.1%

- 35 -

WaterOne 2015 Budget

Operations and Maintenance

2015 Budget Compared to 2014 Budget

O&M ACCOUNTS BY CATEGORY

H:\Finance\FINSHARE\1BUDGET\2015 Budget\OandM\[District Level O_M Comparison‐15Z.xlsx]By Category‐ALL ACCTS

12/12/2014

2014 2015 $ DIF % DIF

PAYROLL

Labor ‐ Non OT 410010 23,088,044 23,892,933 804,889 3.5%

Labor ‐ OT 410015 981,943 989,258 7,315 0.7%

Water Board Salaries 410080 51,600 51,600 ‐ 0.0%

Labor ‐ Vacation Earned 410020 25,002 25,000 (2) 0.0%

TOTAL PAYROLL BEFORE TRANSFERS 24,146,589 24,958,791 812,202 3.4%

PAYROLL Transfers (5,810,709) (5,862,612) (51,903) 0.9%

Net PAYROLL 18,335,880 19,096,179 760,299 4.1%

BENEFITS

Employee Insurance ‐ Health 413010 3,879,201 4,176,450 297,249 7.7%

Pension ‐ Defined Benefit 412010 3,063,086 2,656,864 (406,222) ‐13.3%

Pension ‐ Cash Balance Plan 412050 ‐ 55,426 55,426 NA

Pension ‐ Defined Contribution (Old) District 412020 553,607 461,789 (91,818) ‐16.6%

Pension ‐ Defined Contribution (New) District 412052 ‐ 72,956 72,956 NA

Pension ‐ Defined Contribution (Old) Match 412030 380,882 317,711 (63,171) ‐16.6%

Pension ‐ Defined Contribution (New) Match 412051 ‐ 65,661 65,661 NA

FICA 411010 1,739,247 1,802,440 63,193 3.6%

Worker's Compensation 411020 554,975 542,874 (12,101) ‐2.2%

Other Post Employment Benefits (OPEB) 412040 600,000 400,000 (200,000) ‐33.3%

Retirees Insurance ‐ Health 413050 240,119 292,881 52,762 22.0%

Employee Insurance ‐ Dental 413020 213,925 228,256 14,331 6.7%

Retirees Insurance ‐ Health Subsidy 413052 136,000 110,000 (26,000) ‐19.1%

Employee Health ‐ Retiree Subsidy 413015 (136,000) (110,000) 26,000 ‐19.1%

Employee Insurance ‐ Life 413030 90,594 96,663 6,069 6.7%

Other Tangible Employee Benefits 414030 67,680 77,840 10,160 15.0%

Employee Insurance ‐ Long Term Disability 413040 69,199 75,802 6,603 9.5%

Car Allowance ‐ Employees 426065 51,700 53,700 2,000 3.9%

Employee Insurance ‐ Vision 413025 47,683 51,847 4,164 8.7%

Compensation & Benefits Consulting Services 414020 35,000 42,000 7,000 20.0%

Unemployment Insurance 411050 23,114 28,899 5,785 25.0%

Health Related Training & Counseling 414060 26,647 28,629 1,982 7.4%

Employees Association Activity 414040 19,422 20,437 1,015 5.2%

Tuition Reimbursement 414100 20,000 20,000 ‐ 0.0%

Service Awards 414070 18,200 17,950 (250) ‐1.4%

WOW & Water Spout Awards 414090 10,000 10,000 ‐ 0.0%

Bold = See 'Overview' for more- 36 -

WaterOne 2015 Budget

Operations and Maintenance

12/12/2014

2014 2015 $ DIF % DIF

125D Flexible Benefit Plan 414010 11,014 9,993 (1,021) ‐9.3%

Retirees Insurance ‐ Life 413060 4,822 5,407 585 12.1%

Flowers, Cards, Memorials 414050 2,500 2,500 ‐ 0.0%

Vending Costs & Revenues 414080 (3,600) (3,600) ‐ 0.0%

Worker's Comp ‐ Returns Of Premium/Divid 411030 (60,000) (60,000) ‐ 0.0%

TOTAL BENEFITS BEFORE TRANSFERS 11,659,017 11,551,375 (107,642) ‐0.9%

BENEFITS Transfers (3,216,220) (3,116,461) 99,759 ‐3.1%

Net BENEFITS 8,442,797 8,434,914 (7,883) ‐0.1%

COMMODITIES

Chemicals ‐ Water Treatment 424070 5,830,025 6,073,358 243,333 4.2%

Power ‐ Transmission 424030 4,378,135 4,500,002 121,867 2.8%

Power ‐ Source 424020 2,255,041 2,309,315 54,274 2.4%

Material & Supplies 421070 1,124,596 1,361,185 236,589 21.0%

Power ‐ Distribution 424010 1,316,665 1,352,422 35,757 2.7%

Inventory Withdrawals 421010 1,164,627 1,246,233 81,606 7.0%

Electricity 424040 204,910 203,500 (1,410) ‐0.7%

Natural Gas 424050 182,600 172,000 (10,600) ‐5.8%

BPU Water Purchased In‐House 424065 178,000 166,518 (11,482) ‐6.5%

Safety Equipment & Supplies 421110 62,269 88,051 25,782 41.4%

Uniforms 421160 84,688 87,860 3,172 3.7%

Small Tools & Equip 421130 49,227 72,452 23,225 47.2%

On‐Line Analyzer Supplies 421090 60,000 60,000 ‐ 0.0%

Office Supplies 421080 37,920 37,885 (35) ‐0.1%

Kitchen Supplies 421040 35,000 35,000 ‐ 0.0%

Other General Settlement 599000 24,329 27,900 3,571 14.7%

Crushed Rock 421020 26,000 27,200 1,200 4.6%

Postage 426280 22,520 22,500 (20) ‐0.1%

Paper & Print Shop Supplies 421100 10,000 10,000 ‐ 0.0%

OT Meals 426230 5,950 5,410 (540) ‐9.1%

Medical & First Aid Supplies 421060 4,100 4,100 ‐ 0.0%

Software ‐ Misc Small Purchases 421140 10,000 4,000 (6,000) ‐60.0%

Proactive Safety Recognition 421120 3,000 4,000 1,000 33.3%

Envelopes 421030 3,500 3,500 ‐ 0.0%

Topsoil 421150 1,500 1,750 250 16.7%

Warm Water For Ice Control 424080 4,000 ‐ (4,000) ‐100.0%

Hardware ‐ Misc Small Purchases 421035 5,000 ‐ (5,000) ‐100.0%

Cash Discount Taken 426560 (11,000) (17,795) (6,795) 61.8%

TOTAL COMMODITIES BEFORE TRANSFERS 17,072,602 17,858,346 785,744 4.6%

COMMODITIES Transfers (619,924) (673,406) (53,482) 8.6%

Net COMMODITIES 16,452,678 17,184,940 732,262 4.5%

Bold = See 'Overview' for more- 37 -

WaterOne 2015 Budget

Operations and Maintenance

12/12/2014

2014 2015 $ DIF % DIF

SERVICES

Pavement Repair 422290 755,000 785,500 30,500 4.0%

Contracted Services 422090 601,562 700,809 99,247 16.5%

Property & Liability Insurance 425010 690,790 657,000 (33,790) ‐4.9%

Clean Drinking Water Fee 426070 581,690 586,418 4,728 0.8%

PC Software License & Maintenance 426250 511,661 520,061 8,400 1.6%

Water Billing Services 422430 461,733 494,897 33,164 7.2%

Maintenance Services 422240 234,935 387,635 152,700 65.0%

Security and/or Security Guards 422340 368,000 381,903 13,903 3.8%

Training 426340 310,945 282,775 (28,170) ‐9.1%

Clean Up 422070 231,700 273,900 42,200 18.2%

Uncollectible Accounts 426350 200,000 219,685 19,685 9.8%

Communications 423100 179,200 201,500 22,300 12.4%

Data Connection 423030 199,200 199,200 ‐ 0.0%

Maintenance ‐ PC & Server Hardware 422210 152,190 173,381 21,191 13.9%

Engineering 422100 147,500 147,500 ‐ 0.0%

Wireless Phone 423120 157,900 147,160 (10,740) ‐6.8%

Kansas River Water Assurance Dist. (KRWAD) 426190 118,000 139,128 21,128 17.9%

Laboratory Services 422170 157,859 137,859 (20,000) ‐12.7%

Mowing & Landscaping 422270 105,001 108,759 3,758 3.6%

Cleaning & Inspecting Facilities 422080 97,928 100,484 2,555 2.6%

Land Based Telecommunications 423070 61,000 74,000 13,000 21.3%

Non‐Employee Overload 426210 100,740 70,000 (30,740) ‐30.5%

Dues & Local Meetings 426120 55,255 63,962 8,707 15.8%

Meter Reading ‐ AMR Services 422260 66,944 62,190 (4,754) ‐7.1%

Property Tax Assessment 426290 63,291 61,853 (1,438) ‐2.3%

Printing Services 422330 17,014 60,700 43,686 256.8%

Property & Liability Insurance ‐ Self Ins. 425030 60,000 60,000 ‐ 0.0%

Bank Lockbox Processing Fees 426060 60,500 59,400 (1,100) ‐1.8%

Checking Account Service Fees 426040 54,000 55,000 1,000 1.9%

Contractual Fee To Consol. Gov. Wy'dot. 426090 52,500 52,500 ‐ 0.0%