2015 04-27 - Yara International ASA Q1 2015 Presentation

37

Yara International ASA First quarter results 2015 24 April 2015

-

Upload

yara-international -

Category

Investor Relations

-

view

282 -

download

2

Transcript of 2015 04-27 - Yara International ASA Q1 2015 Presentation

Yara International ASA

First quarter results 2015

24 April 2015

1

IR – 24 April 2015

Strong result driven by higher deliveries and margins

Margins benefit from lower gas prices and stronger US dollar

NOK 1.8 billion currency loss due to US dollar appreciation

Improved production reliability

Lifeco write-down of NOK 929 million

Strong Industrial result

Summary first quarter

2

IR – 24 April 2015

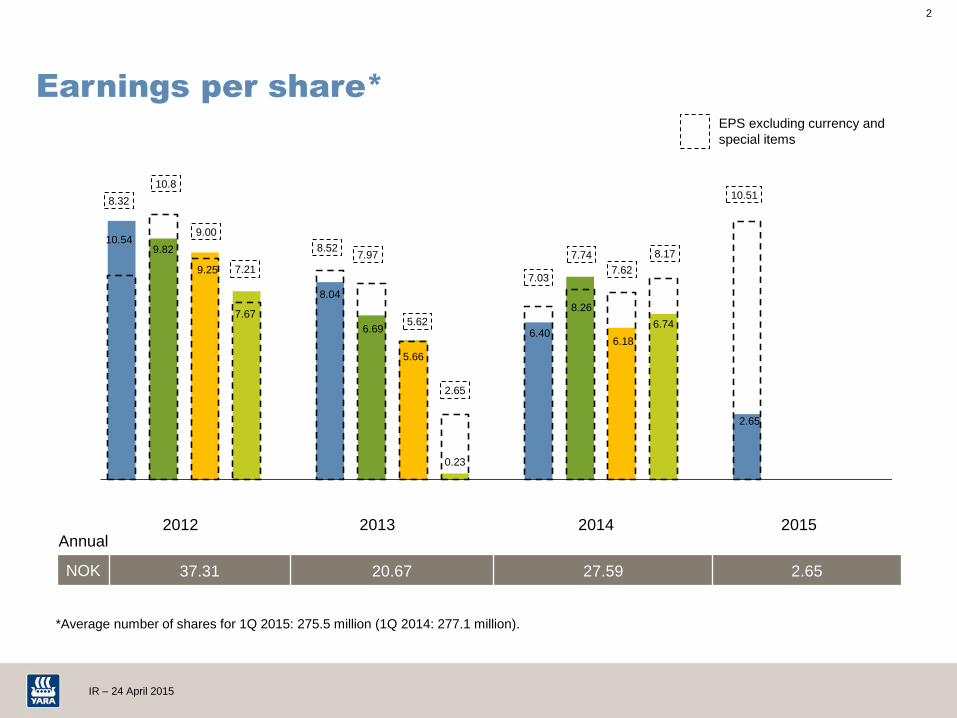

10.54 9.82

9.25

7.67

8.04

6.69

5.66

0.23

6.40

8.26

6.18

6.74

2.65

8.32

10.8

9.00

7.21

8.52 7.97

5.62

2.65

7.03

7.74

7.62

8.17

10.51

Earnings per share*

*Average number of shares for 1Q 2015: 275.5 million (1Q 2014: 277.1 million).

NOK 37.31 20.67 27.59 2.65

Annual 2012 2013 2014

EPS excluding currency and

special items

2015

3

IR – 24 April 2015

Chinese urea exports put pressure on prices

USD nitrate prices have followed the urea price development

Western Europe nitrogen fertilizer industry deliveries 3% lower; season-to-date

in line

Phosphate prices and upgrading margins similar to last year

Strong demand for value-added fertilizer products

Industrial: continued demand growth for environmental solutions but weaker

TAN market

Market development

4

IR – 24 April 2015

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

Million tons

13/144

Source: BOABC, CFMW

12/13

Chinese urea exports put pressure on prices

14/15

0

50

100

150

200

250

300

350

400

450

500

550

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

2 200

2 400Kilotons

Black Sea

USD/t

Chinese exports and urea price Chinese production

5

IR – 24 April 2015

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

10/11 11/12 12/13 13/14 14/15

Production Net imports

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

10/11 11/12 12/13 13/14 14/15

Domestic Imports

European industry deliveries similar to last

season

Source: Yara estimate for fertilizer deliveries to selected West European countries.

Total nitrogen deliveries based on TFI, US Trade Commission, Blue-Johnson and Yara estimates

USA West Europe

+6%

Million tons N Million tons N

0%

6

IR – 24 April 2015

0

1 000

2 000

3 000

4 000

5 000

6 000

Kilotons

Urea Nitrates NPK CN UAN SSP - based fertilizer

2014 2011 2012 2013 2015

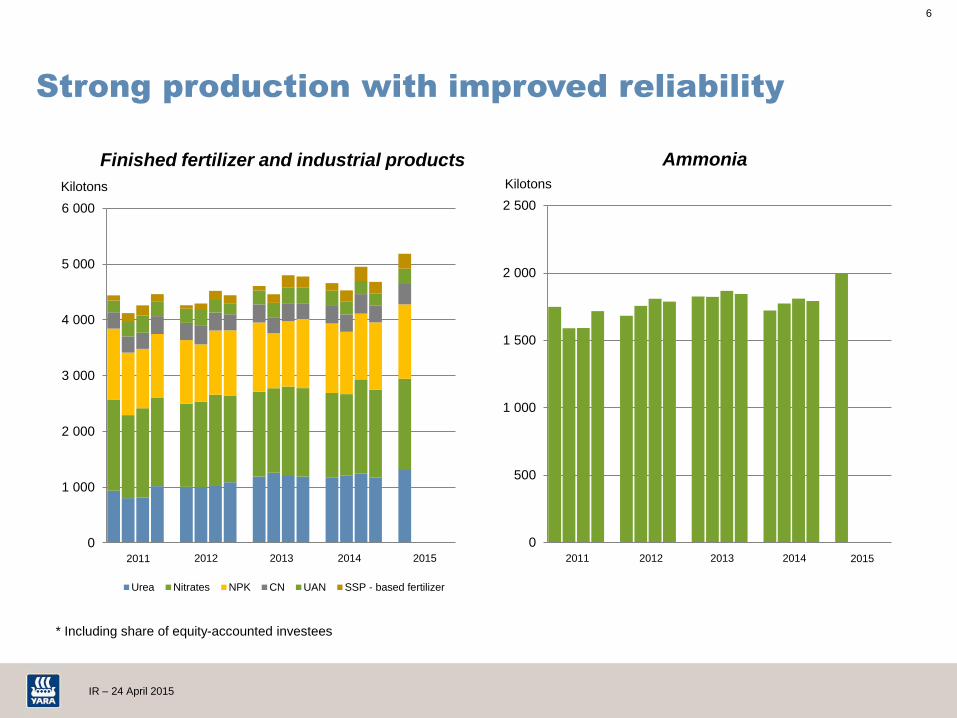

Strong production with improved reliability

0

500

1 000

1 500

2 000

2 500

Kilotons

2015

* Including share of equity-accounted investees

Finished fertilizer and industrial products Ammonia

2014 2011 2012 2013

7

IR – 24 April 2015

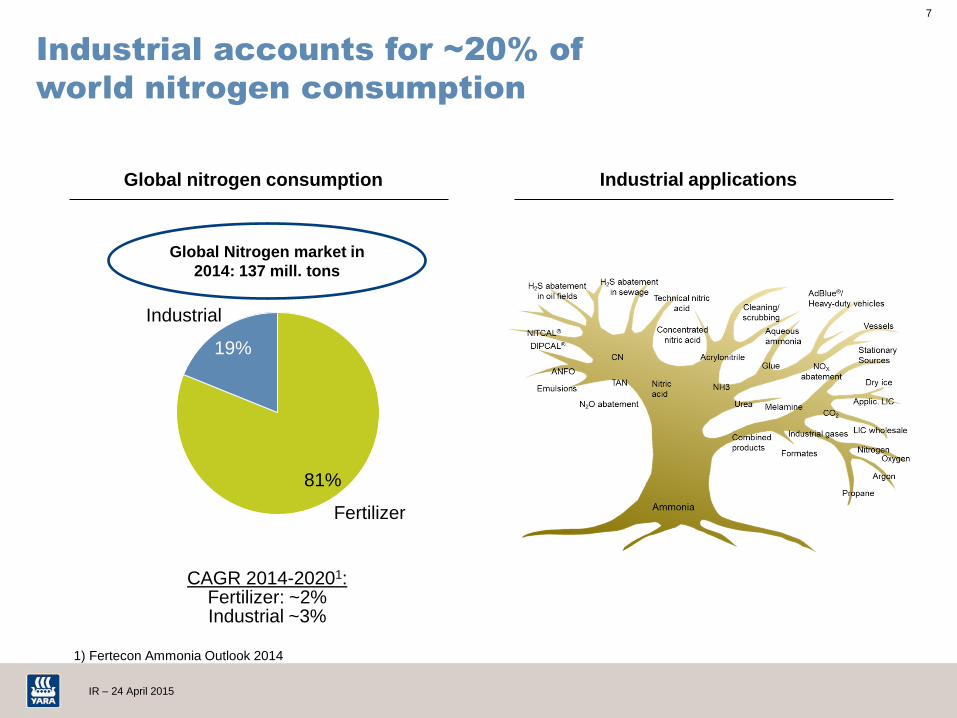

Industrial accounts for ~20% of

world nitrogen consumption

Global nitrogen consumption Industrial applications

19%

Industrial

Fertilizer

81%

Global Nitrogen market in

2014: 137 mill. tons

1) Fertecon Ammonia Outlook 2014

CAGR 2014-20201: Fertilizer: ~2% Industrial ~3%

8

IR – 24 April 2015

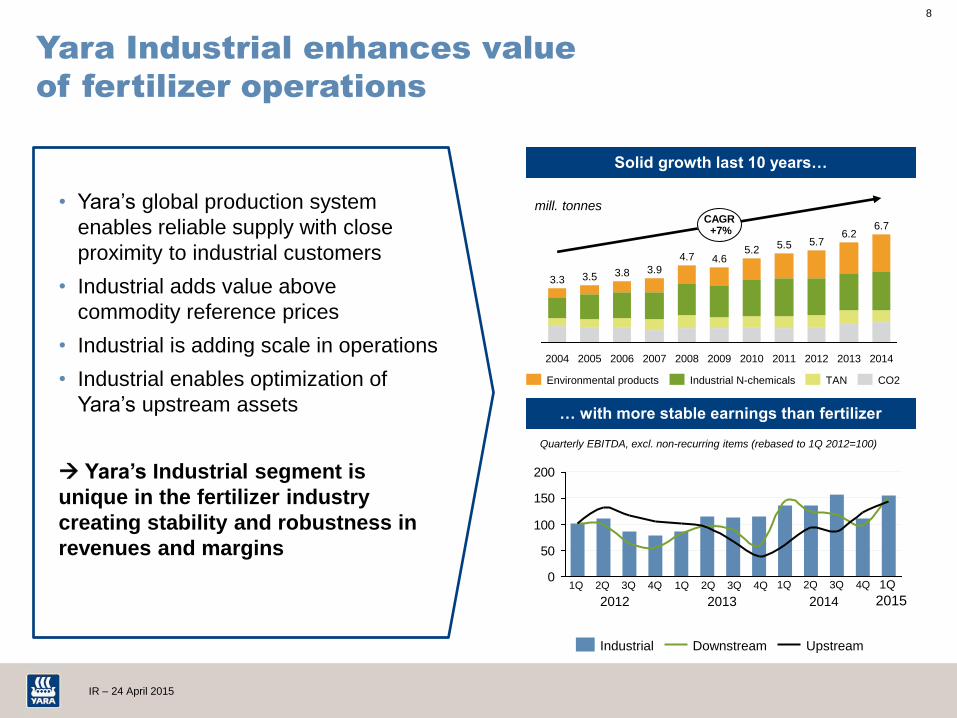

• Yara’s global production system

enables reliable supply with close

proximity to industrial customers

• Industrial adds value above

commodity reference prices

• Industrial is adding scale in operations

• Industrial enables optimization of

Yara’s upstream assets

Yara’s Industrial segment is

unique in the fertilizer industry

creating stability and robustness in

revenues and margins

Yara Industrial enhances value

of fertilizer operations

0

50

100

150

200

Quarterly EBITDA, excl. non-recurring items (rebased to 1Q 2012=100)

Downstream Industrial Upstream

2014

CAGR +7%

2013

6.2

2012

5.7

2011

5.5

2010

5.2

2009

4.6

2008

4.7

2007

3.9

2006

3.8

2005

3.5

2004

3.3

6.7

TAN CO2 Industrial N-chemicals Environmental products

mill. tonnes

1Q 2Q 3Q 4Q

2012 2013 2014

1Q

2015

Solid growth last 10 years…

… with more stable earnings than fertilizer

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

9

IR – 24 April 2015

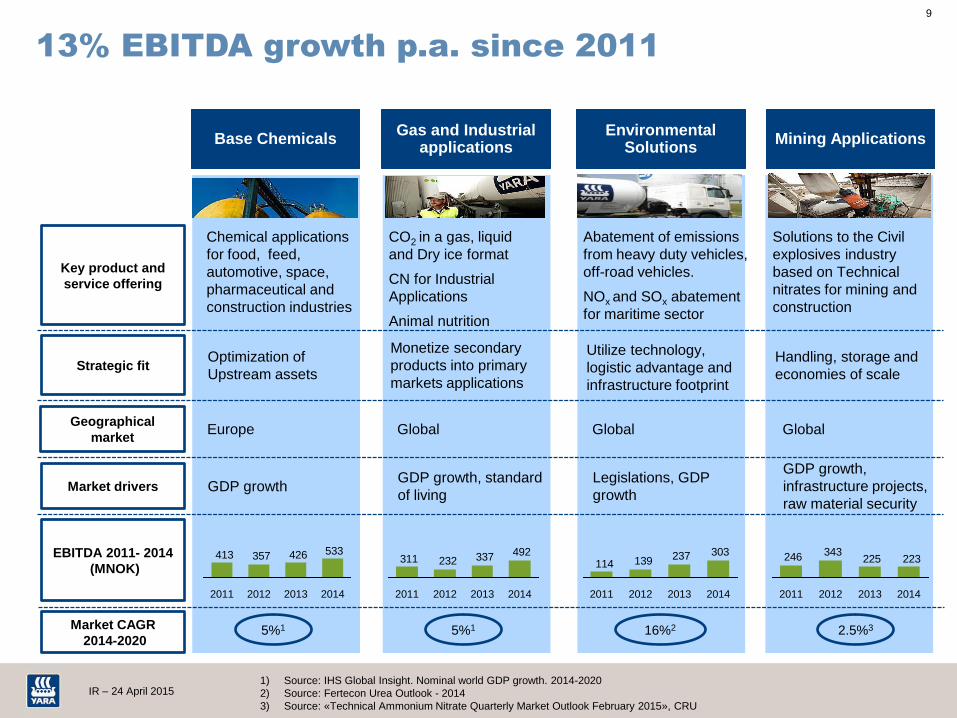

13% EBITDA growth p.a. since 2011

1) Source: IHS Global Insight. Nominal world GDP growth. 2014-2020

2) Source: Fertecon Urea Outlook - 2014

3) Source: «Technical Ammonium Nitrate Quarterly Market Outlook February 2015», CRU

Chemical applications

for food, feed,

automotive, space,

pharmaceutical and

construction industries

Base Chemicals

Abatement of emissions

from heavy duty vehicles,

off-road vehicles.

NOx and SOx abatement

for maritime sector

Environmental Solutions

Solutions to the Civil

explosives industry

based on Technical

nitrates for mining and

construction

Mining Applications

CO2 in a gas, liquid

and Dry ice format

CN for Industrial

Applications

Animal nutrition

Gas and Industrial applications

Key product and

service offering

EBITDA 2011- 2014

(MNOK)

Market drivers GDP growth Legislations, GDP

growth

GDP growth,

infrastructure projects,

raw material security

GDP growth, standard

of living

Strategic fit Optimization of

Upstream assets

Utilize technology,

logistic advantage and

infrastructure footprint

Handling, storage and

economies of scale

Monetize secondary

products into primary

markets applications

Geographical

market Europe Global Global Global

533426357413

2014 2013 2011 2012

492337232311

2014 2013 2011 2012

303237139114

2011 2013 2014 2012

223225343246

2014 2013 2012 2011

Market CAGR

2014-2020 16%2 2.5%3 5%1 5%1

10

IR – 24 April 2015

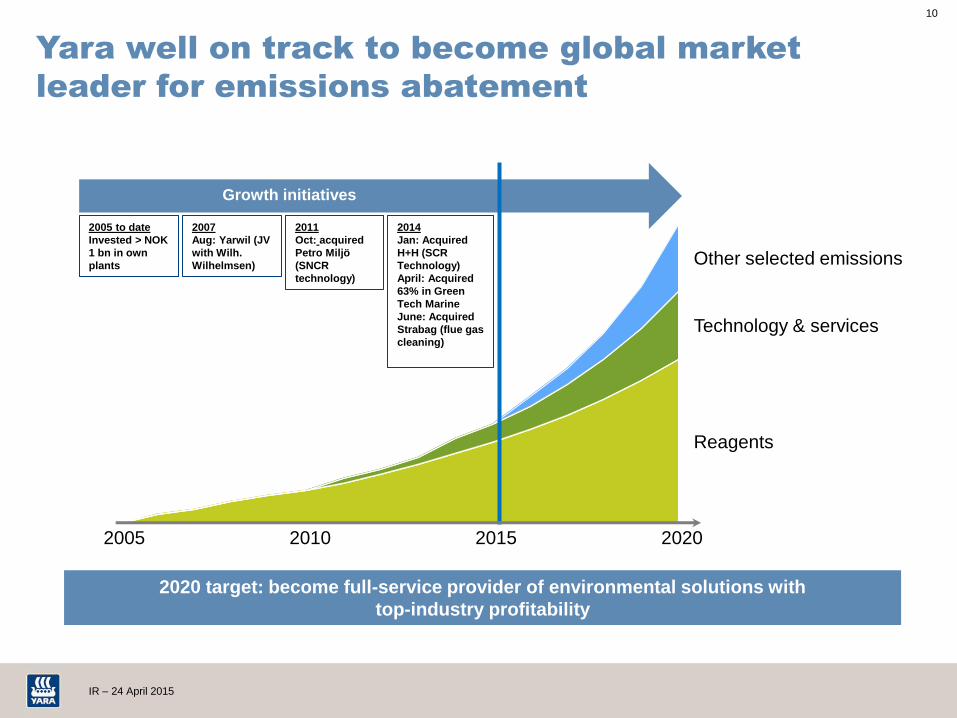

Yara well on track to become global market

leader for emissions abatement

2020 target: become full-service provider of environmental solutions with

top-industry profitability

2005

Other selected emissions

Technology & services

Reagents

2007

Aug: Yarwil (JV

with Wilh.

Wilhelmsen)

2005 to date

Invested > NOK

1 bn in own

plants

2015 2020

2011

Oct: acquired

Petro Miljö

(SNCR

technology)

2014

Jan: Acquired

H+H (SCR

Technology)

April: Acquired

63% in Green

Tech Marine

June: Acquired

Strabag (flue gas

cleaning)

2010

Growth initiatives

11

IR – 24 April 2015

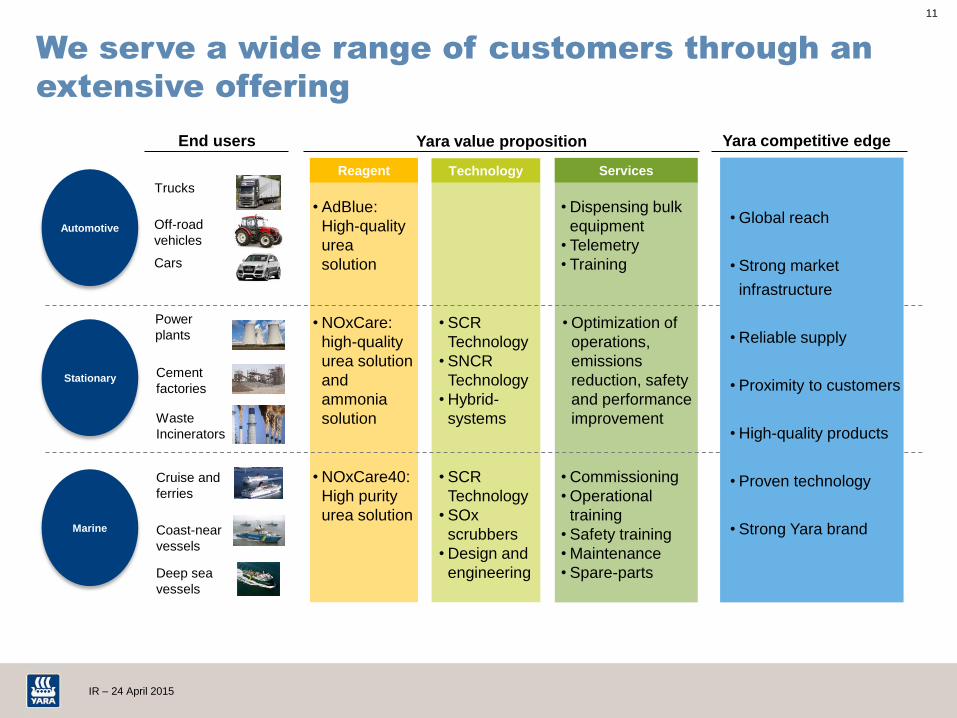

We serve a wide range of customers through an

extensive offering

Technology Services

Stationary

Marine

•Dispensing bulk

equipment

• Telemetry

• Training

• SCR

Technology

• SOx

scrubbers

•Design and

engineering

• SCR

Technology

• SNCR

Technology

•Hybrid-

systems

Automotive

•NOxCare40:

High purity

urea solution

•Optimization of

operations,

emissions

reduction, safety

and performance

improvement

•Commissioning

•Operational

training

• Safety training

•Maintenance

• Spare-parts

Cruise and

ferries

Coast-near

vessels

Deep sea

vessels

Off-road

vehicles

Cars

Trucks

• AdBlue:

High-quality

urea

solution

•NOxCare:

high-quality

urea solution

and

ammonia

solution

Yara value proposition Yara competitive edge End users

Reagent

Power

plants

Cement

factories

Waste

Incinerators

•Global reach

• Strong market

infrastructure

•Reliable supply

• Proximity to customers

•High-quality products

• Proven technology

• Strong Yara brand

12

IR – 24 April 2015

Yara Environmental Solutions grows rapidly

905

713

609619

604

2014

279

1,183

2013

NOxCare

EBITDA (MNOK)

AdBlue EBITDA (MNOK)

NOxCare volumes (kt)

AdBlue volumes (kt)

2012

245

139 4.93.2

8.3

2.2

2014

5.4

CAGR +16%1

2020

13.1

Reagent (AdBlue+NOxCare) Technology

Recent acquisitions have built Yara a solid position to capture the fast-growing Environmental

Solutions market

USDbn.

1) Per urea-equivalent (46% Nitrogen), excl. non-recurring items, source: Fertecon Urea Outlook - 2014

Yara performance Market growth 2014-2020

Yara ES 2014

sales was

USD540mill,

predominantly

reagents

13

IR – 24 April 2015

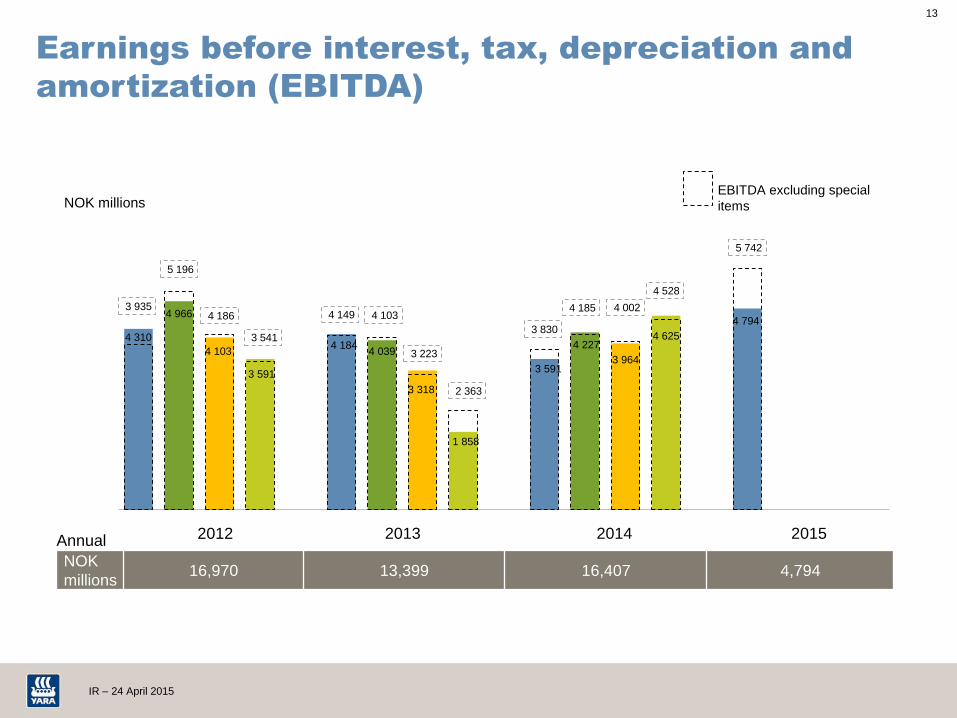

Earnings before interest, tax, depreciation and

amortization (EBITDA)

4 310

4 966

4 103

3 591

4 184 4 039

3 318

1 858

3 591

4 227

3 964

4 625

4 794

3 935

5 196

4 186

3 541

4 149 4 103

3 223

2 363

3 830

4 185 4 002

4 528

5 742

2012 2014 2013 2015

NOK

millions 16,970 13,399 16,407 4,794

Annual

EBITDA excluding special

items NOK millions

14

IR – 24 April 2015

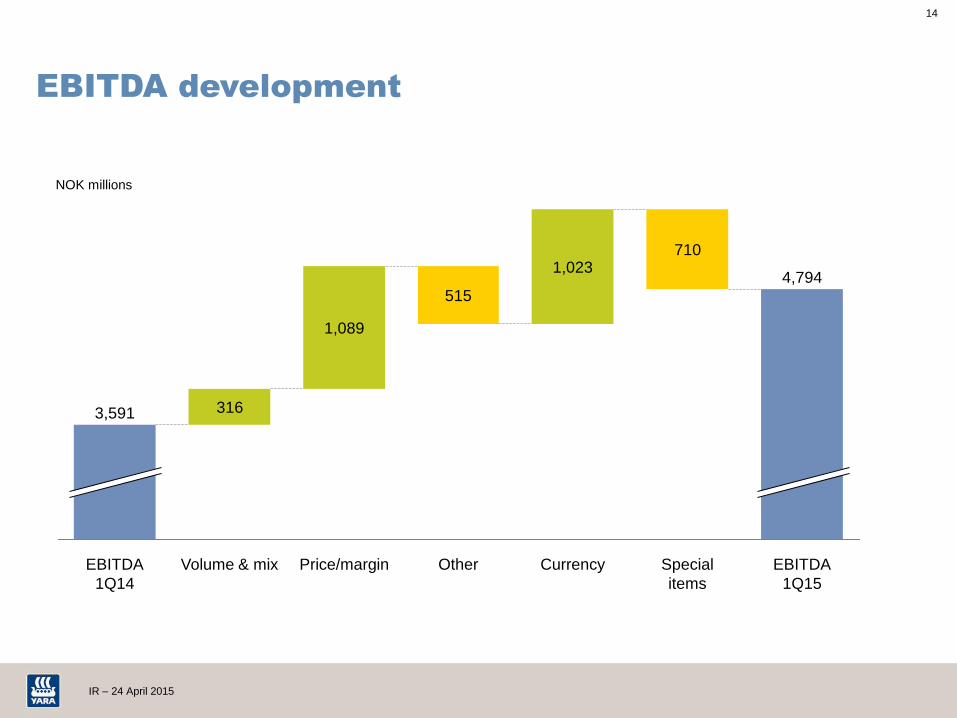

EBITDA development

316

515

710

4,794

EBITDA

1Q15

Special

items

Currency

1,023

Other Price/margin

1,089

Volume & mix EBITDA

1Q14

3,591

NOK millions

15

IR – 24 April 2015

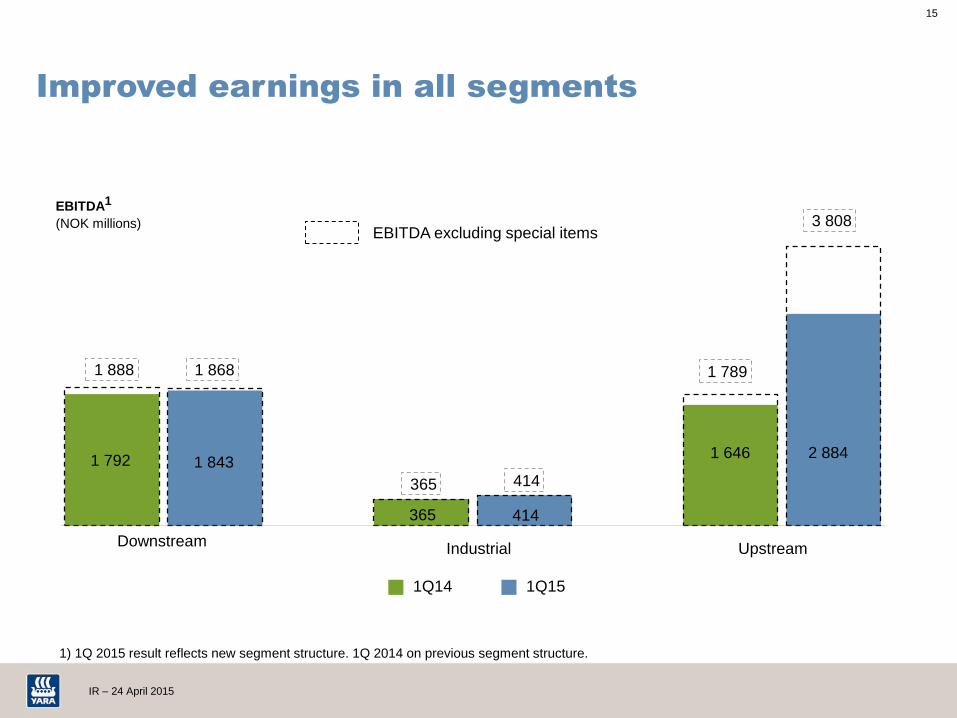

Improved earnings in all segments

1 792 1 843

365 414

1 646 2 884

1 888 1 868

365 414

1 789

3 808

Downstream Industrial Upstream

EBITDA excluding special items

1Q14 1Q15

EBITDA1 (NOK millions)

1) 1Q 2015 result reflects new segment structure. 1Q 2014 on previous segment structure.

16

IR – 24 April 2015

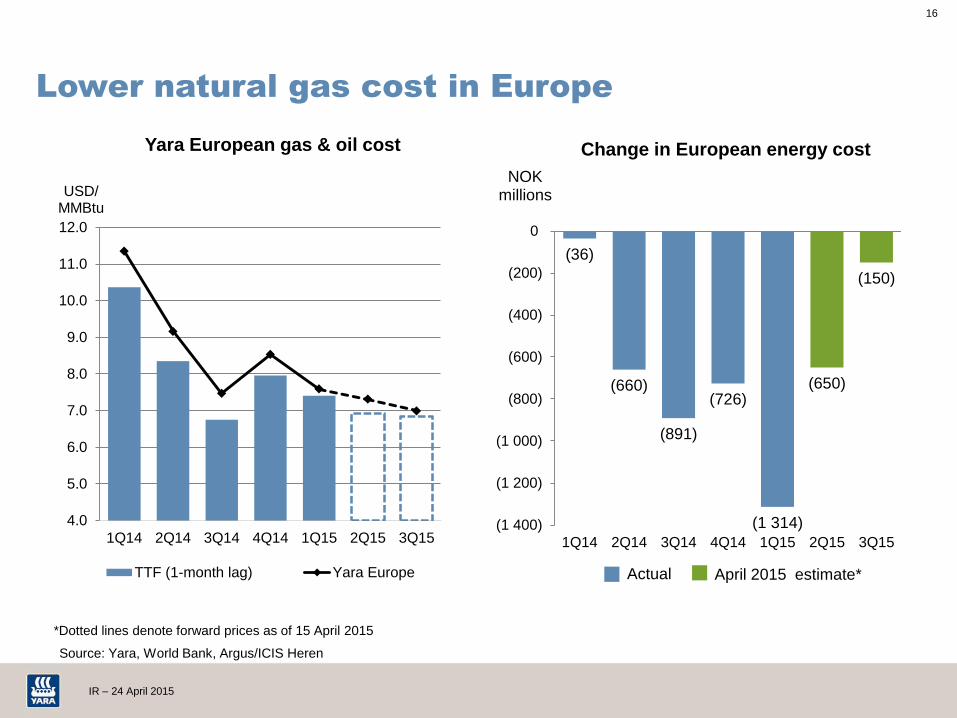

Lower natural gas cost in Europe

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15

USD/ MMBtu

TTF (1-month lag) Yara Europe

(36)

(660)

(891)

(726)

(1 314)

(650)

(150)

(1 400)

(1 200)

(1 000)

(800)

(600)

(400)

(200)

0

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15

NOK millions

April 2015 estimate*

Source: Yara, World Bank, Argus/ICIS Heren

*Dotted lines denote forward prices as of 15 April 2015

Yara European gas & oil cost

Actual

Change in European energy cost

17

IR – 24 April 2015

Stable European nitrate premium

0

100

200

300

400

500

600

700

1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15

USD/t

Nitrogen upgrading margins1 (monthly publication prices)

Urea CFR CAN (46% N) NH3 CFR (46% N)

Value

above gas

Value above

ammonia

Nitrate

premium

above urea

Yara EU gas cost *20

0

20

40

60

80

100

120

140

160

180

1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15

European nitrate premium2 (quarterly Yara realized) USD/t

2) Yara European realized nitrate prices compared with urea

publication prices with one month time lag. All numbers in USD

per ton of CAN equivalents. 1) All prices in urea equivalents

18

IR – 24 April 2015

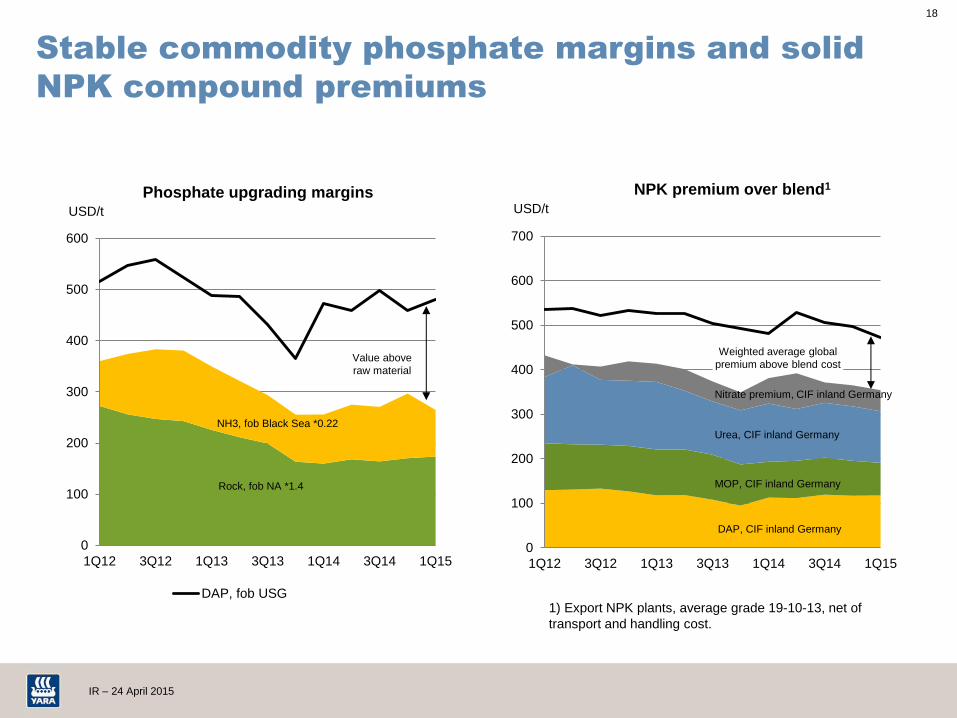

Stable commodity phosphate margins and solid

NPK compound premiums

0

100

200

300

400

500

600

700

1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15

USD/t

NPK premium over blend1

0

100

200

300

400

500

600

1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15

USD/t

Phosphate upgrading margins

DAP, fob USG

Rock, fob NA *1.4

Value above

raw material

NH3, fob Black Sea *0.22

DAP, CIF inland Germany

MOP, CIF inland Germany

Urea, CIF inland Germany

Weighted average global

premium above blend cost

1) Export NPK plants, average grade 19-10-13, net of

transport and handling cost.

Nitrate premium, CIF inland Germany

19

IR – 24 April 2015

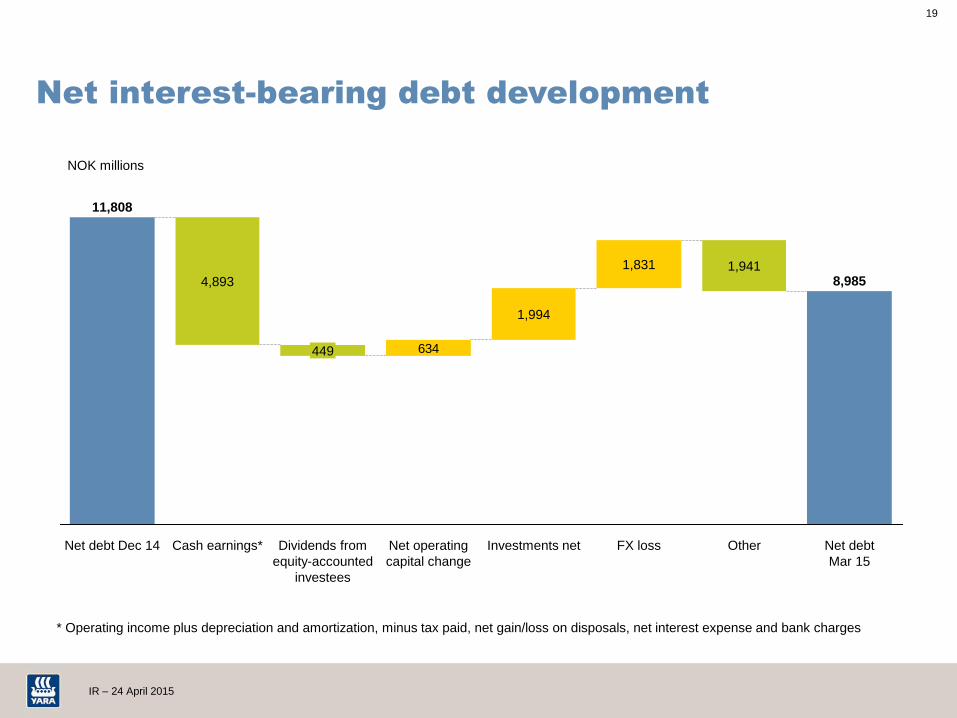

Net interest-bearing debt development

634

FX loss

1,831

Investments net

1,994

8,985

Net operating

capital change

Dividends from

equity-accounted

investees

449

Cash earnings*

4,893

Net debt Dec 14

11,808

Net debt

Mar 15

Other

1,941

* Operating income plus depreciation and amortization, minus tax paid, net gain/loss on disposals, net interest expense and bank charges

NOK millions

20

IR – 24 April 2015

Incentives for fertilizer application remain supportive

Strong US dollar improves competitiveness of European farmers and nitrogen

producers

Yara deliveries in Europe running well in April

Demand for nitrates and compound NPKs continues to grow outside Europe

China to remain swing producer – anthracite coal prices and RMB/USD

exchange rate are key for global nitrogen commodity prices

Expected further gas cost reduction of NOK 650 million in Europe in second

quarter and NOK 150 million in third quarter 2015

Prospects

Additional information

22

IR – 24 April 2015

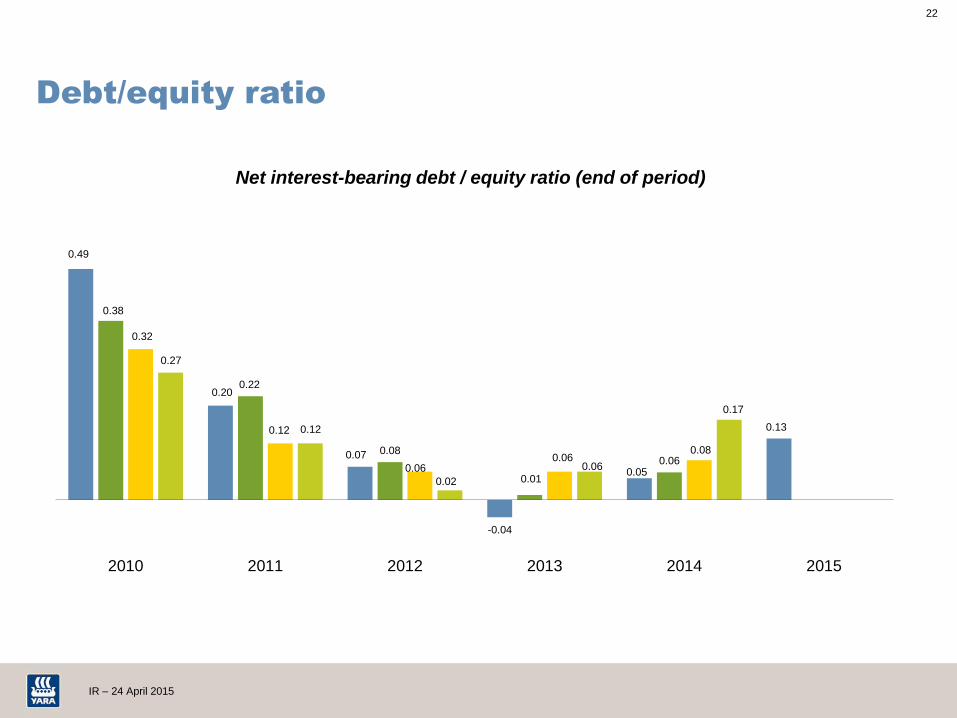

0.49

0.20

0.07

-0.04

0.05

0.13

0.38

0.22

0.08

0.01

0.06

0.32

0.12

0.06 0.06

0.08

0.27

0.12

0.02

0.06

0.17

2010 2011 2012 2013 2014 2015

Debt/equity ratio

Net interest-bearing debt / equity ratio (end of period)

23

IR – 24 April 2015

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

5 500

6 000

6 500

7 000

Europe Outside Europe

Fertilizer deliveries

Kilotons

2011 2008 2009 2010 2012 2013 2014 2015

24

IR – 24 April 2015

Yara 1Q fertilizer sales by market and product

3 110

1 585

926

482 285

3 008

1 852

901

420 385

Europe Latin America North America Asia Africa

1Q14 1Q15

1 463

858

1 570

1 246

556 418

279

1 416

763

1 595 1 378

717

418 278

NPK compounds NPK blends Nitrate Urea Other products UAN CN

Kilotons

25

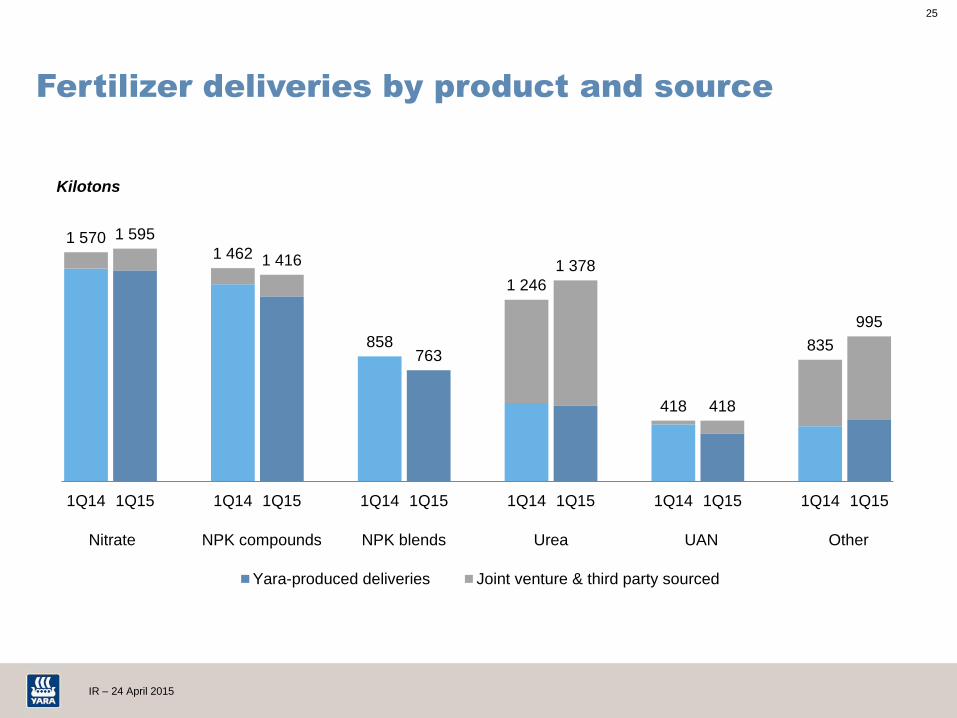

IR – 24 April 2015

1 570 1 595

1 462 1 416

858 763

1 246

1 378

418 418

835

995

1Q14 1Q15 1Q14 1Q15 1Q14 1Q15 1Q14 1Q15 1Q14 1Q15 1Q14 1Q15

Yara-produced deliveries Joint venture & third party sourced

Fertilizer deliveries by product and source

Nitrate NPK compounds NPK blends Urea UAN

Kilotons

Other

26

IR – 24 April 2015

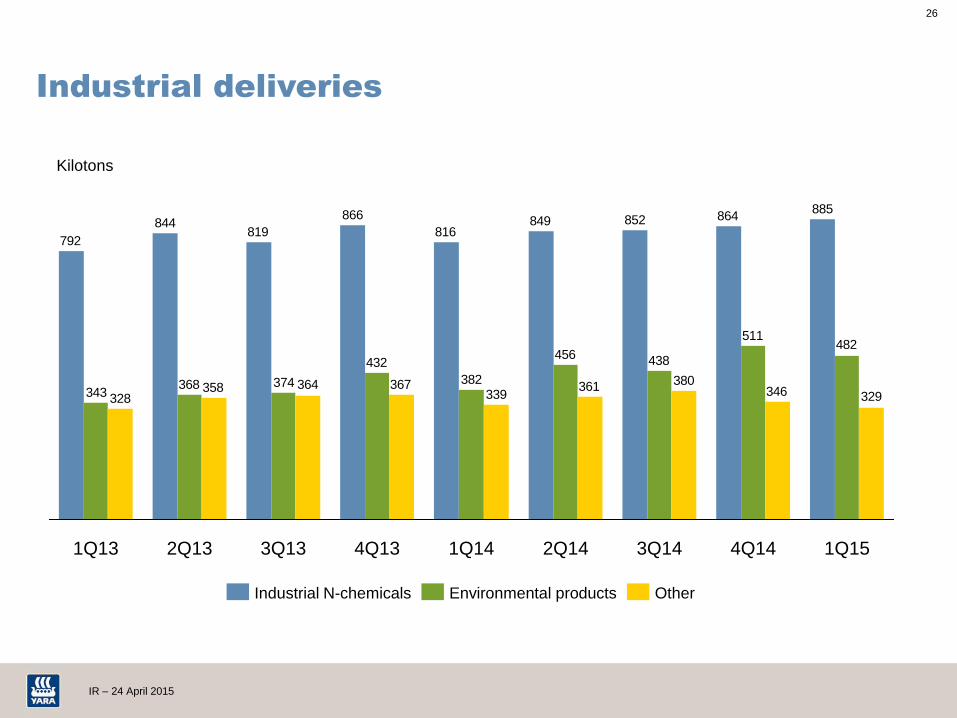

Industrial deliveries

885864852849

816

866

819844

792

482511

438456

382

432

374368343 329346

380361339

367364358328

1Q15 4Q14 3Q14 2Q14 1Q14 4Q13 3Q13 2Q13 1Q13

Industrial N-chemicals Environmental products Other

Kilotons

27

IR – 24 April 2015

0

50

100

150

200

250

300

350

400

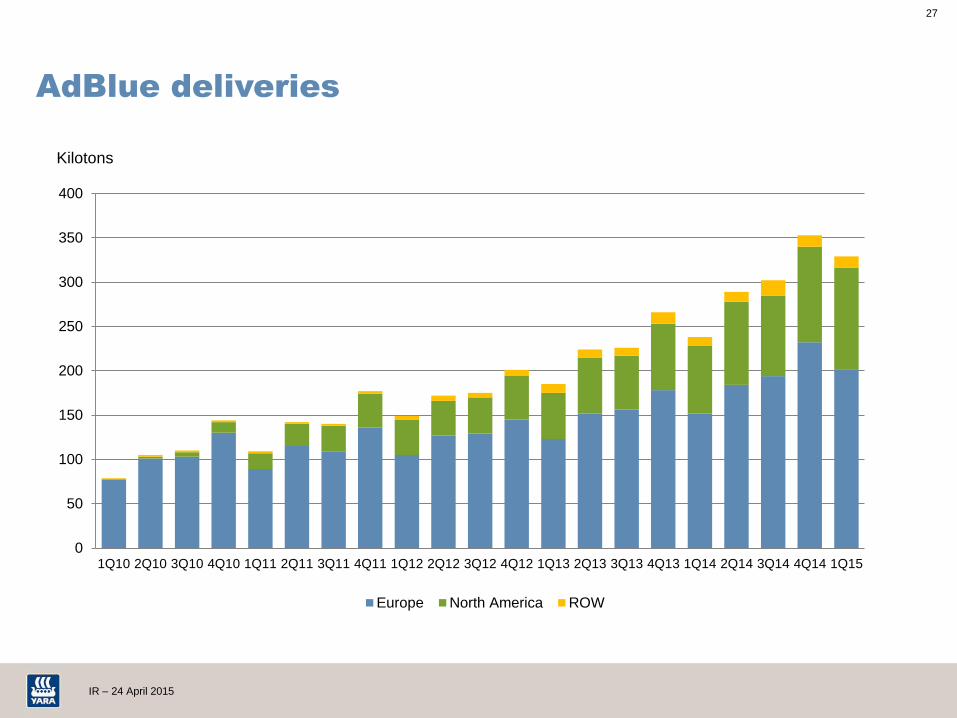

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

Europe North America ROW

AdBlue deliveries

Kilotons

28

IR – 24 April 2015

500

600

700

800

900

1 000

1 100

1 200

1 300

1 400

1Q11 1Q12 1Q13 1Q14 1Q15

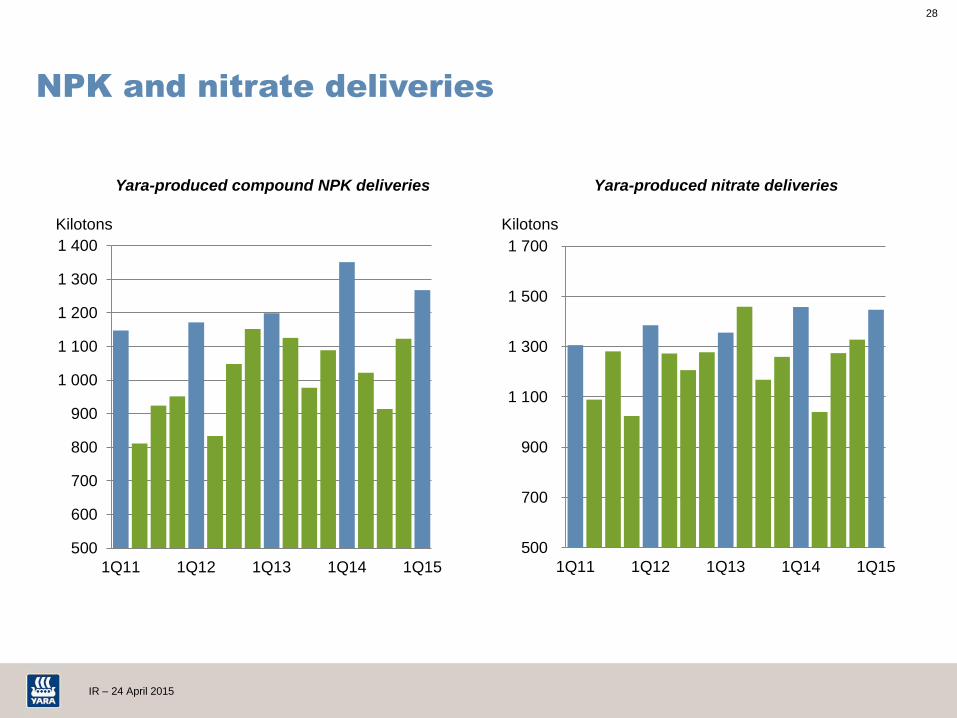

NPK and nitrate deliveries

Kilotons

500

700

900

1 100

1 300

1 500

1 700

1Q11 1Q12 1Q13 1Q14 1Q15

Yara-produced nitrate deliveries

Kilotons

Yara-produced compound NPK deliveries

29

IR – 24 April 2015

-

1 000

2 000

3 000

4 000

5 000

6 000

7 000

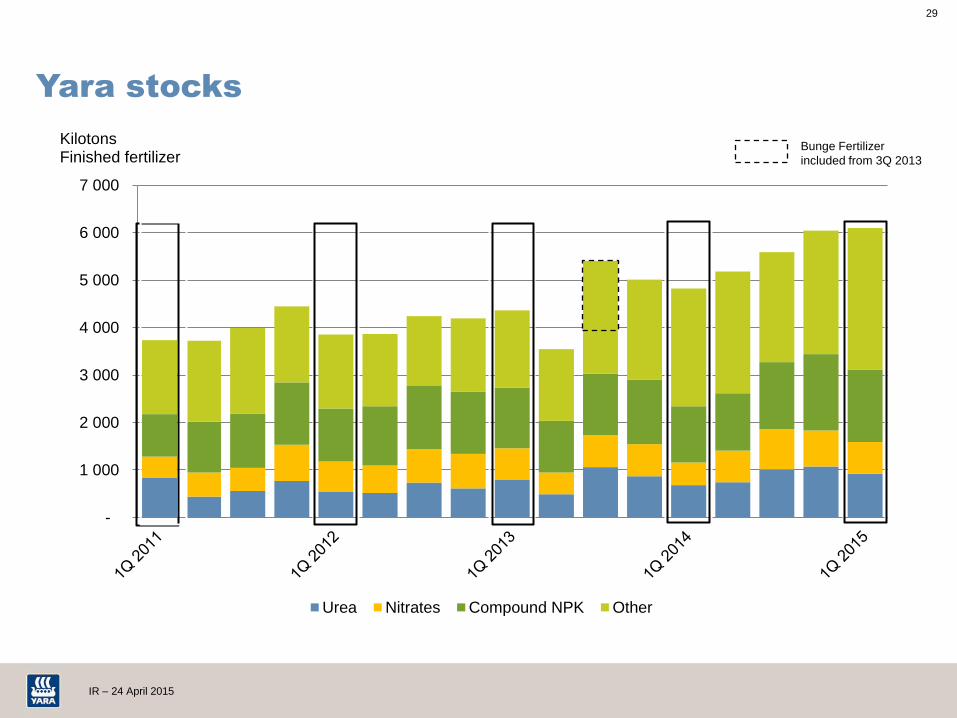

Kilotons Finished fertilizer

Urea Nitrates Compound NPK Other

Yara stocks

Bunge Fertilizer

included from 3Q 2013

30

IR – 24 April 2015

4.0 4.4

4.0

2.8

3.7

5.2

4.6

3.9 3.8

2.9 2.9 2.6 2.7

4.8

5.7

8.2 8.0 8.0 8.1

6.9

6.1 6.5

6.0 6.0 5.7 5.5 4.7

6.6

9.2 9.4

10.5

9.8

7.6

7.0

8.1

7.0 6.9 6.8

6.6

7.6

10.7 11.0 11.4 11.3

9.2

7.5

8.5

7.6 7.3 7.0

2009 2010 2011 2012 2013 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15

US gas price (Henry Hub) Yara Global TTF day ahead (Zeebrugge 2009-2012) Yara Europe

Energy cost

USD per MMBtu

Source: Yara, World Bank, Platts/Argus/ICIS Heren

Yearly averages 2009 – 2013, quarterly averages for 2014-15 with forward prices* for 2Q15 and 3Q15.

*Dotted lines denote forward prices as of 15 April 2015

31

IR – 24 April 2015

Net income from equity-accounted investees

24

-90

53

204

17

-955

129169

Other Lifeco GrowHow UK Qafco

NOK millions

1Q15

1Q14

32

IR – 24 April 2015

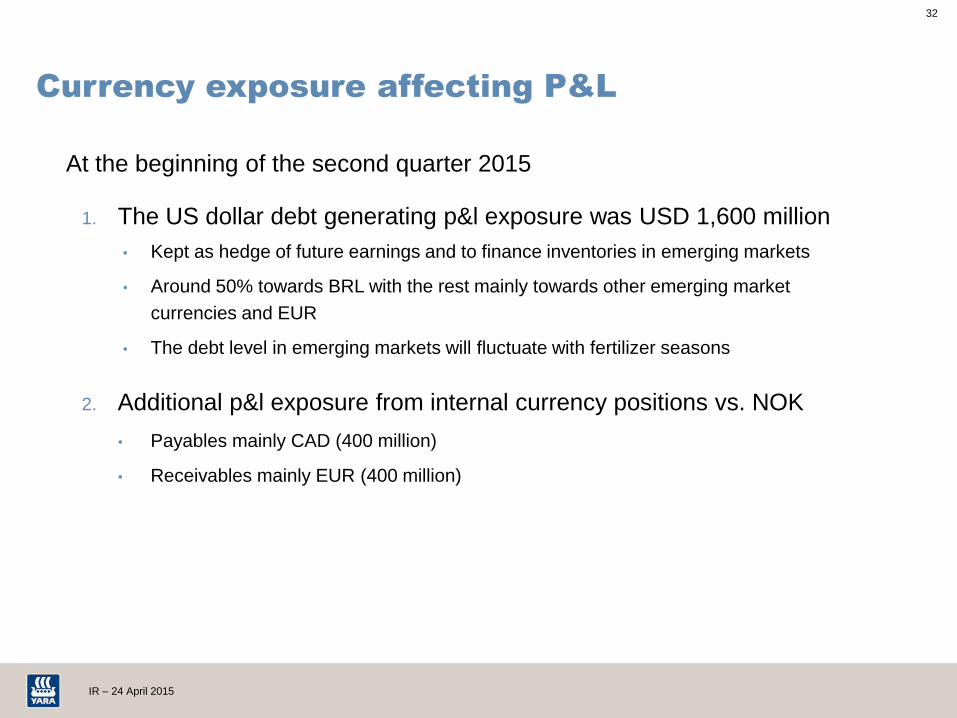

Currency exposure affecting P&L

At the beginning of the second quarter 2015

1. The US dollar debt generating p&l exposure was USD 1,600 million

• Kept as hedge of future earnings and to finance inventories in emerging markets

• Around 50% towards BRL with the rest mainly towards other emerging market

currencies and EUR

• The debt level in emerging markets will fluctuate with fertilizer seasons

2. Additional p&l exposure from internal currency positions vs. NOK

• Payables mainly CAD (400 million)

• Receivables mainly EUR (400 million)

33

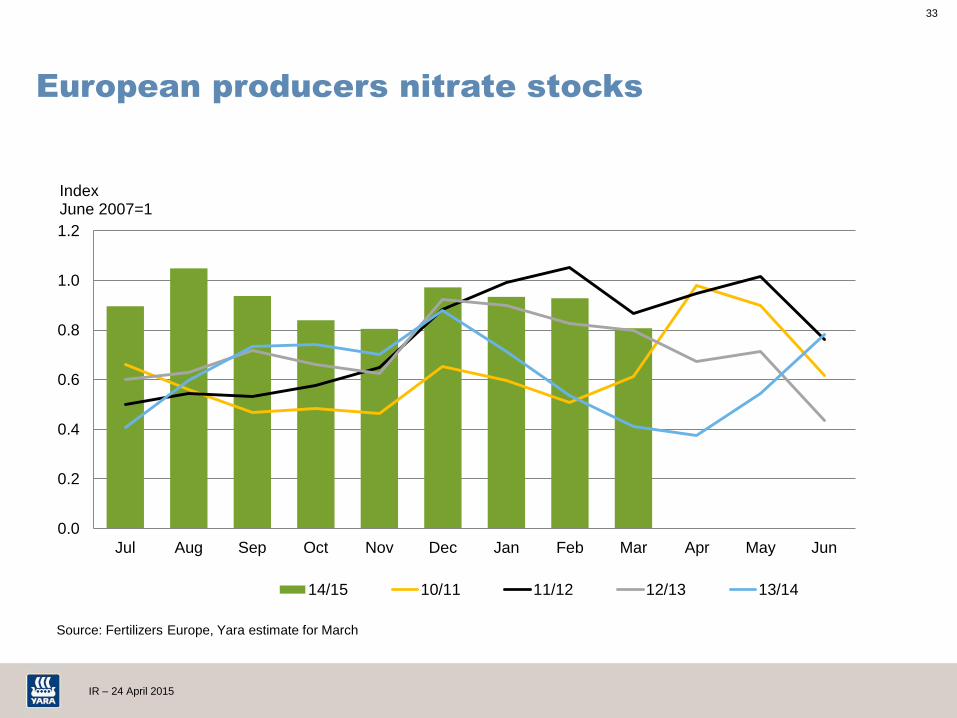

IR – 24 April 2015

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

Index June 2007=1

14/15 10/11 11/12 12/13 13/14

Source: Fertilizers Europe, Yara estimate for March

European producers nitrate stocks

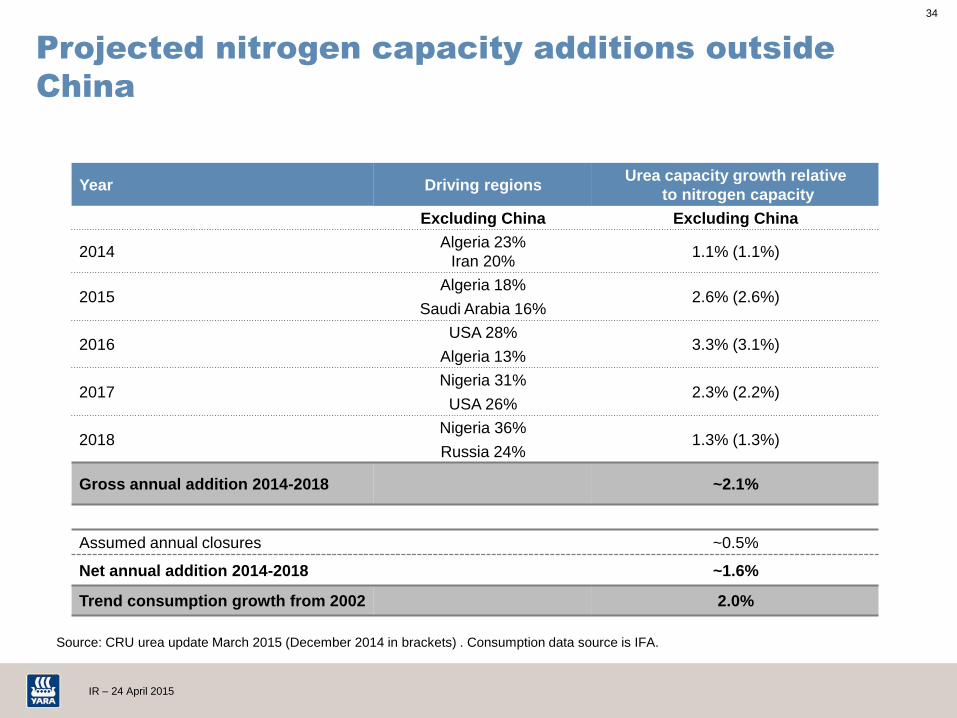

34

IR – 24 April 2015

Source: CRU urea update March 2015 (December 2014 in brackets) . Consumption data source is IFA.

Year Driving regions Urea capacity growth relative

to nitrogen capacity

Excluding China Excluding China

2014 Algeria 23%

Iran 20% 1.1% (1.1%)

2015 Algeria 18%

Saudi Arabia 16% 2.6% (2.6%)

2016 USA 28%

Algeria 13% 3.3% (3.1%)

2017 Nigeria 31%

USA 26% 2.3% (2.2%)

2018 Nigeria 36%

Russia 24% 1.3% (1.3%)

Gross annual addition 2014-2018 ~2.1%

Assumed annual closures ~0.5%

Net annual addition 2014-2018 ~1.6%

Trend consumption growth from 2002 2.0%

Projected nitrogen capacity additions outside

China

35

IR – 24 April 2015

Key value drivers – quarterly averages

338 299

320 315 295

414

358 358 355 337

1Q14 2Q14 3Q14 4Q14 1Q15

Urea prilled fob Black Sea (USD/t)/Urea granular fob Egypt (dotted line, USD/t)

345 354

309 310 295

1Q14 2Q14 3Q14 4Q14 1Q15

CAN cif Germany (USD/t)

5.2

4.6

3.9 3.8

2.9

1Q14 2Q14 3Q14 4Q14 1Q15

US gas price Henry Hub (USD/MMBtu)

9.8

7.6 7.0

8.1 7.0

1Q14 2Q14 3Q14 4Q14 1Q15

TTF day ahead (USD/MMBtu)

6.1 6.0 6.3 6.9

7.7

1Q14 2Q14 3Q14 4Q14 1Q15

NOK/USD exchange rate

438 485 488

572

413

1Q14 2Q14 3Q14 4Q14 1Q15

Ammonia fob Black Sea (USD/t)

Source: Fertilizer Market Publications, CERA, World Bank, Norges Bank

36

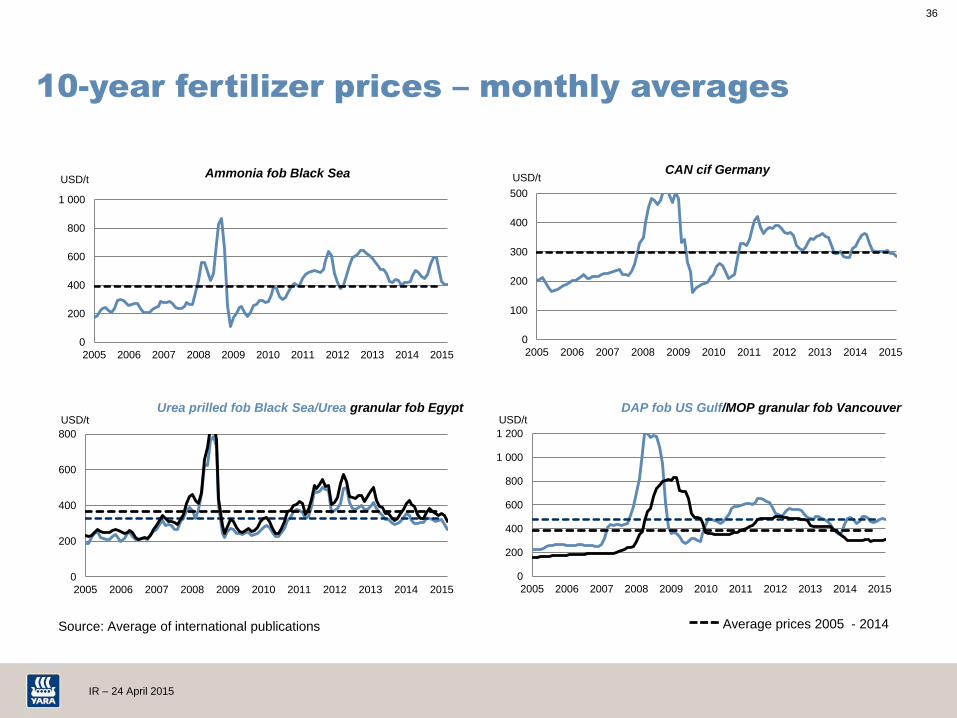

IR – 24 April 2015

10-year fertilizer prices – monthly averages

Source: Average of international publications

0

200

400

600

800

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

USD/t Urea prilled fob Black Sea/Urea granular fob Egypt

Average prices 2005 - 2014

0

200

400

600

800

1 000

1 200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

USD/t DAP fob US Gulf/MOP granular fob Vancouver

0

100

200

300

400

500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

USD/t CAN cif Germany

0

200

400

600

800

1 000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

USD/t Ammonia fob Black Sea