2014 the new energy consumer initiative

30

The New Energy Consumer 24 January 2014

-

Upload

kyodo-consulting-group-ceo -

Category

Business

-

view

107 -

download

2

Transcript of 2014 the new energy consumer initiative

The New Energy Consumer

24 January 2014

Agenda

The New Energy Consumer Initiative

A New Era of Change and Uncertainty

Summary Netherlands results

1. Delivering operational excellence

2. Optimizing customer interaction

3. Creating lasting customer engagement

4. Extending the value proposition

Ten Strategic Priorities for Energy Providers

2 Copyright © 2014 Accenture. All rights reserved.

NEC12

Copyright © 2014 Accenture. All rights reserved.

Accenture’s New Energy Consumer Research Program

>40,000 consumers

surveyed in 21

countries

>2,000 small and

medium businesses

in 9 countries

Survey of market

trends & priorities for

20 leading utilities

customer executives

Market insights & leading

practices from more than

50 leading energy

providers and over 30

cross industry providers

In-depth analysis of

technology adoption

in 8 major markets

3

Over 4 years of comprehensive and continuous research focused on energy users, our

research offers actionable insights into the preferences and values shaping the energy

marketplace.

Agenda

The New Energy Consumer Initiative

A New Era of Change and Uncertainty

Summary Netherlands results

1. Delivering operational excellence

2. Optimizing customer interaction

3. Creating lasting customer engagement

4. Extending the value proposition

Ten Strategic Priorities for Energy Providers

4 Copyright © 2014 Accenture. All rights reserved.

NEC12

Risks today, uncertainty tomorrow

Utilities are facing a storm of forces that are reshaping the market landscape and are

increasing uncertainty in the market.

Shifting

consumer

preferences

Government

& regulatory

shifts

Sustainability

5 Copyright © 2013 Accenture. All rights reserved.

Advancing

technology

Uncertainty is

increasing

A future of Uncertainty, Disruption and… Opportunity?

The Rise of ‘Economics

of Dissatisfaction’

In order to be successful, Utilities need to build simple, flexible organizations, while eliminating key

dissatisfiers across strategic imperatives:

The changing market place, uncertainty and disruption require Utilities to develop simple

and agile organizations

Reduce Operational

‘Cost-to-Serve’

Enhance Revenue

Potential

Drive Energy

Efficiency Goals

Sustain or Improve

Customer Value

6

Agenda

The New Energy Consumer Initiative

A New Era of Change and Uncertainty

Summary Netherlands results

1. Delivering operational excellence

2. Optimizing customer interaction

3. Creating lasting customer engagement

4. Extending the value proposition

Ten Strategic Priorities for Energy Providers

7 Copyright © 2014 Accenture. All rights reserved.

NEC12

1. Delivering operational excellence

8

Copyright © 2014 Accenture. All rights reserved.

34%

23%

22%

18%

23%

15%

8%

9%

57%

61%

61%

65%

53%

53%

50%

44%

9%

16%

17%

17%

24%

32%

42%

47%

What organizations do you trust to inform you about actions you can take to

optimize your energy consumption?

Consumer’s level of trust in their utilities/energy providers has

decreased

Base: All Netherlands respondents

Do not trust Neither trust nor distrust Trust % Trust

2012

44%

33%

23%

23%

18%

27%

17%

18%

Consumer associations

Academics/schools/scientific

Associations

Environmental associations

Government/governmental

organizations

Online service providers (e.g., Google, Microsoft)

Utilities/energy providers

Home service providers (e.g., cable television provider,

telecommunications provider, home

security company, etc.)

Retailers/equipment manufacturers

Copyright © 2014 Accenture. All rights reserved.

89%

88%

87%

78% 75%

73% 71% 68%

63%

47% 47%

91%

85%

91%

85% 82%

77%

85%

79% 78% 76%

61%

Importance (Somewhat + very important) Performance (Good + excellent)

Consistently

gets my bill

correct

Provides me

with reliable

energy

delivery

Provides clear

and easy-to-

understand

pricing

information

Is known to

have ethical

business

practices

Is known to

work to

protect the

environment

Informs my

family or me

about efforts

we can take to

decrease

energy usage

Offers me the

latest

technology

Partners with

other

companies or

organizations

to enhance its

offerings

Is known for

treating its

employees

well

Offers a

physical

location where

I can meet with

its

representatives

Is actively

involved in my

city and

neighborhood

Base: All Netherlands respondents

How important are each of the following factors in building your trust with your

energy provider?

Based on your experience to date, how would you rate your energy provider’s

performance on each of the following factors?

Active community involvement, offering the latest technology,

treating employees well and offering physical locations are

where consumers feel their energy providers over perform

Accurate

invoice

Reliable

energy

Easy to

understand

Ethical

brand

Environmental

brand

Energy

advisor

Tech-

savvy

Partners to

create

value

Valued

employer

Face-to-

face

interaction

Community

member

2. Optimizing customer interaction

11

Copyright © 2014 Accenture. All rights reserved.

Bill payer

Spouse-partner

Other adults who live in the home

Teenagers (13 to 18 years)

Regular in-house services (e.g., nanny, child care, etc.)

Occasional in-house services (e.g., house cleaning, pool servicing, etc.)

Children (12 years and under)

Thinking about all the members of your household, please indicate the level of influence

the following have on energy usage in your home (e.g., set the temperature, turning lights on/off,

turning on/off entertainment, doing laundry, etc.)

Aside from the bill payer, others in the home have influence on

energy usage

Base: All Netherlands respondents; excludes “Not Aplicable“ responses

94%

90%

74%

72%

69%

68%

51%

Moderate to significant influence

Copyright © 2014 Accenture. All rights reserved.

Where would you be most interested in learning about energy or energy-related

products and/or services, and how much time would you be willing to dedicate to

learning about them?

14%

17%

18%

18%

25%

34%

34%

28%

35%

33%

6%

6%

7%

8%

6%

12%

14%

23%

17%

25%

<5 minutes

>5 minutes

Consumers are most interested in learning about energy or

related products and/or services during their discretionary time

and when shopping for products for the home

Base: All Netherlands respondents

20%

58%

23%

52%

25%

51%

26%

48%

31%

46%

During my free time (e.g., at home on evenings or weekends)

While shopping for appliances (e.g., washer, dryer, fridge, etc.)

While shopping for materials or products to make

major renovations to my home (e.g., insulation, furnace, windows, etc.)

While shopping for electronics (i.e., television)

While shopping for minor home improvement products (e.g., light bulbs, weather stripping, etc.)

While waiting to buy something (e.g., waiting for coffee or food, etc.)

While traveling (e.g., waiting for a train, while on a train, etc.)

At work

While shopping for groceries

At an event (e.g., concert, sporting event, etc.)

Copyright © 2014 Accenture. All rights reserved.

13%

13%

15%

18%

24%

31%

35%

38%

43%

44%

49%

79%

13%

22%

20%

35%

17%

14%

20%

22%

32%

24%

22%

26%

0% 20% 40% 60% 80% 100%

Using a mobile device

Using traditional computer

Provided you had access to a traditional computer (e.g., laptop or desktop) and a

mobile device (e.g., smartphone), which of the following features would you want

available on your energy provider’s website?

Consumers have different expectations for the features offered

on an energy provider’s website if they are accessing it via a

mobile device versus a traditional computer

Base: All Netherlands respondents

Detailed information about my energy usage

Personalized tips on actions I can take to reduce my energy bill

Personalized offers and coupons (e.g., coupon for laundry detergent, rebate for appliances)

Notifications about my energy usage (i.e., notification when higher than normal bill is forecasted)

Ability to perform self-service transactions (e.g., pay bill, update account information, view outage information, etc.)

Reviews on energy-related products and services (i.e., reviews of energy-efficient appliances)

Ability to purchase energy-related products and services from the website (i.e., purchase an energy-efficient appliance)

Ability to purchase prepaid energy to use in the future

Ability to control heating, cooling, or appliances in my home

Online games that educate my family about energy waste-conservation

Ability to participate in social games (i.e., compete with neighbors on decreasing energy usage)

An online community hosted by my energy provider to share energy-saving

tips

3. Creating lasting customer

engagement

15

Copyright © 2014 Accenture. All rights reserved.

5% 2%

2% 1%

17%

15%

58%

61%

18% 21%

Base: All Netherlands respondents

What is your level of satisfaction with your current energy provider?

Please use a 10-point scale for which 1 means that you are extremely dissatisfied and 10 means that

you are extremely satisfied

On a year-on-year basis, consumers are less satisfied with

their energy providers

Very satisfied

Satisfied

Neutral

Not very satisfied

Not satisfied at all

2013 2012

76% 82%

Copyright © 2014 Accenture. All rights reserved.

Are you considering switching to another energy provider in the next 12 months?

Please use a 10-point scale for which 1 means that you will certainly not switch to another energy

provider in the next 12 months and 10 that you will certainly switch

Nevertheless, to date, the impact on loyalty is limited and overall

consumers’ intention to switch has decreased

6% 11%

11%

14%

20%

15%

14% 11%

49% 49%

17% 25%

2013 2012

Certainly

Probably

Neutral

Probably

not

Certainly

not

Base: All Netherlands respondents

Copyright © 2014 Accenture. All rights reserved.

Yes, could consider a provider other

than a utility/electricity provider (i.e., retailer, phone or cable provider, online site)

Retailer (e.g. Koninklijke Ahold N.V )

Phone or cable provider (e.g., Koninklijke KPN N.V)

Online site

(e.g., Amazon, Google)

You may currently, or in the future, have new companies offering you electricity, energy-efficient products

(i.e., smart thermostats), and/or related services (i.e., customized information on your electricity consumption) on top

of their traditional products and services. Would you consider purchasing electricity, energy-efficient

products, and/or related services from the following providers:

Since 2011, the interest in alternative providers for purchasing

electricity and beyond-the-meter products and services has

decreased

31%

47%

38%

60%

28%

32%

33%

46%

2013

2011

Base: All Netherlands respondents

Copyright © 2014 Accenture. All rights reserved.

57%

48%

34%

31%

29%

25%

20%

17%

9%

The provider has lower prices than my energy provider

I can bundle products and services to get a discount (e.g., Internet, phone and electricity)

I have had better experiences dealing with this provider than

with my energy provider

The provider has a store where I can talk to a representative,

see products and discuss services

The provider has better service than my energy provider

The provider has a better return or service cancellation policy

than my energy provider

I trust the provider more than my energy provider

The provider is a local company

I belong to the provider’s loyalty rewards program

Why would you consider purchasing energy or energy-related products and/or services from a provider

other than your energy provider (e.g., retailer, phone or cable provider, website)?

Better prices and convenience are the main drivers why

consumers would consider purchasing from an alternative

provider

Base: Netherlands respondents who would consider purchasing energy or energy-related products and/or services from providers

other than their energy provider

Mentioned in top three

Copyright © 2014 Accenture. All rights reserved.

23% 24% 31% 33% 36% 36% 39% 39% 40% 40% 41% 42% 42% 44% 45% 48% 48% 49% 49% 49% 51% 54%

77% 76% 69% 67% 64% 64% 61% 61% 60% 60% 59% 58% 58% 56% 55% 52% 52% 51% 51% 51% 49% 46%

CN KR IT PL ZA SG TR AU BR CA ES AVG FR JP DE SE DK UK NO BE US NL

If your energy provider offered the two following rate plans, which option would

you select?

Preferences for rate plans vary significantly across geographies

Base: All respondents

The price of energy changes throughout the day. You can

save money on your energy bill if you actively manage the

times at which you use energy (i.e., use major appliances

when energy is cheaper), if you do not, your energy bill will

increase

The price of energy is fixed and does not change throughout

the day. You do not need to pay attention to the times at

which you use energy, but you cannot save money on your

energy bill by actively managing the times at which you use

energy

Flat rate plan Variable rate plan

4. Extending the value proposition

21

I cannot afford the cost of the required

investment

14%

23%

35%

37%

46%

59%

71%

In the next 12 months, are you planning to spend money on energy-related products and/or services for your home (e.g., energy-efficient

appliances, smart thermostats, etc.)?

Why are you not planning to spend money on energy-related products and/or services in the next 12 months?

The main barriers to investing in energy-related products

and/or services are cost along with perceived lack of financial

payback

Mentioned in top three

I do not think it will result in significant

cost savings on my energy bill

I am not able to make changes

to my home (i.e., I rent it and do not own it)

I do not know what energy related

products and services are available

I do not want to spend money on

energy related products and services

I do not think it will have a significant

impact on the environment

I do not have the time to learn about

these new energy products and

services

59%

41%

Yes, I plan to

spend money

No, I do not plan to

spend money

Base: All Netherlands respondents Base: Netherlands respondents who do not plan to spend money

Copyright © 2014 Accenture. All rights reserved.

Some energy-related products (e.g., solar panels, energy efficient appliances, etc.)

can be expensive. Would any of the following motivate you to purchase energy-

related products that require a significant financial investment?

Cost savings and financing options are key to motivating

consumers to make substantial investments in energy-related

products

13%

27%

30%

37%

39%

49%

66%

Mentioned in top three

Base: All Netherlands respondents

Guaranteed reduction in your energy bill

Discounts on bundles of energy and energy-related products (e.g., bundling electricity with solar panels)

Flexible payment plans to finance my purchase (e.g., monthly payments on my bill, no payments for two years, etc.)

Renting options (e.g., rent solar panel, programmable thermostat, etc.)

Loyalty points in return for money that I spend with

my energy provider

Ability to transfer remaining payments on energy-related products if I move (e.g., transfer financing payments on my solar panels to the new owner if I sell my home)

None of these would motivate me to purchase energy-related products that

require a significant financial investment

Agenda

The New Energy Consumer Initiative

A New Era of Change and Uncertainty

Summary Netherlands results

1. Delivering operational excellence

2. Optimizing customer interaction

3. Creating lasting customer engagement

4. Extending the value proposition

Ten Strategic Priorities for Energy Providers

24 Copyright © 2014 Accenture. All rights reserved.

NEC12

Global Agenda: Ten Key Priorities for Energy Providers

The Consumer

Ecosystem

Enterprise

State of Mind

Age of Turnkey

Technologies Unconventional

Partnerships

Retail

Redefined Reinventing

Value

Workforce of

the Future

Economics of

Dissatisfaction Bridging the Digital

Divide

The Neglected

Middle

25 Copyright © 2014 Accenture. All rights reserved.

Copyright © 2014 Accenture. All rights reserved.

Growing customer preference for digital

2007 2008 2009 2010 2011 2012

100

200

300

400

500

600

700

800

Glo

bal S

mart

phone V

olu

me (

Mill

ions)

Year

119.7m 139.3m 175m

305m

494.5m

717.5m

+14% + 20%

+ 38%

+ 43%

+ 31%

Smartphone catalyzes disruptive

technology innovation

Mobile device

penetration exceeds PC

More than $100bn spent on

mobile media globally

Progressive Adoption of

Mobility Globally

“61% of

customers

would prefer

to use

digital

channels for

¾ of their

key utility

interaction

scenarios1”

Sustainable, effective digital development requires strategic value-based prioritization and

planning to deliver robust infrastructure, cumulative benefit and full integration with

existing operations and strategy.

Copyright © 2014 Accenture. All rights reserved.

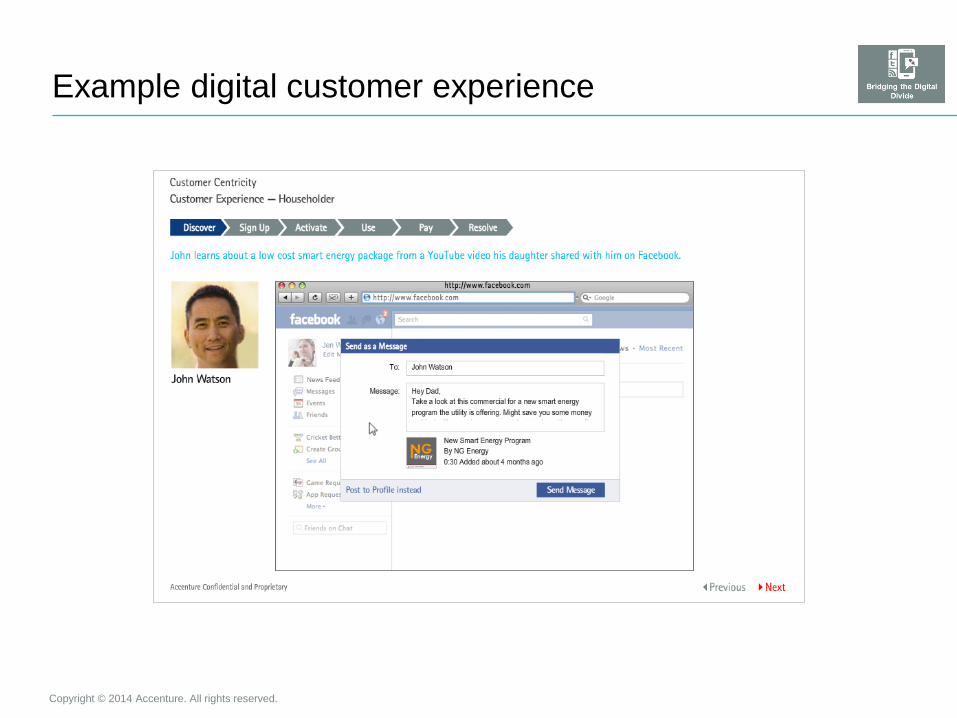

Example digital customer experience

28

Spotlight On E.On

E.On created ‘Sweden’s Largest Energy Experiment’ to drive customer energy efficiency adoption through provision of multiple digital

tools that visualized, tracked and monitored participant energy usage.

10k customers were provisioned with a smartphone app

that monitored real time power usage for their household Over 12 months the app visualized their energy

consumption in 5 ways to determine the most effective

The initiative was supported by a larger campaign

community website to facilitate comparisons and sharing

Participants on average saved 12% on their energy

consumption over the course of the year

1 2

3 4

Watch the full outcomes on YouTube here: http://www.youtube.com/watch?v=jHgZc4m1FtA&feature=youtu.be

E.On Sweden provide a leading example of how digital technology can be leveraged to

drive specific strategic outcomes, consumer behaviors and business goals in a utilities

context.

Copyright © 2014 Accenture. All rights reserved.

1. Over 5 jaar vindt 80% van het klantcontact digitaal plaats

2. Over 5 jaar wordt 80% van de producten en diensten aangeschaft, in gebruik

genomen en gefactureerd via digitale kanalen

3. Utilities kunnen alleen overleven als ze aansprekende en relevante digitale

value added services aanbieden aan hun klanten

4. Business en cultuurchange zijn grotere challenges dan IT change om een

digitale transformatie te realiseren

5. Digital = Internet

Statements

Accenture Energy Consumer Services provides

customer care solutions for competitive energy

providers globally.

We help our clients to develop and implement full value-

chain solutions that achieve three key business

imperatives: cost effectiveness, revenue assurance and

customer satisfaction. Through new energy customer

transformation, next generation customer solutions,

transformational outsourcing and asset-powered

services, we bring world-class industry-specific

management consulting, technology and business

process customer- care capabilities to our electricity, gas

and water clients.

How to increase customer satisfaction? What new value-

add products and services can be developed? How to

reduce pressure on operational costs? How the business

can be simplified? What path to define a medium- and

long-term customer care strategic vision?

We can help.

Accenture’s global New Energy Consumer program

delivers actionable insights on the trends and critical

competencies for the evolving energy marketplace. Our

New Energy Consumer research spans years of insights

into consumer needs and preferences: