2014 Strategy Report Bittersweet Symphony - global.com.tr · 2014 Strategy Report – Bittersweet...

30

2014 Strategy Report – Bittersweet Symphony 15 January 2014 strategic partner of Please see the last page for disclaimer Note that all data are per 9th January 2014 closing 1

Transcript of 2014 Strategy Report Bittersweet Symphony - global.com.tr · 2014 Strategy Report – Bittersweet...

2014 Strategy Report – Bittersweet Symphony

15 January 2014

strategic partner of

Please see the last page for disclaimer Note that all data are per 9th January 2014 closing

1

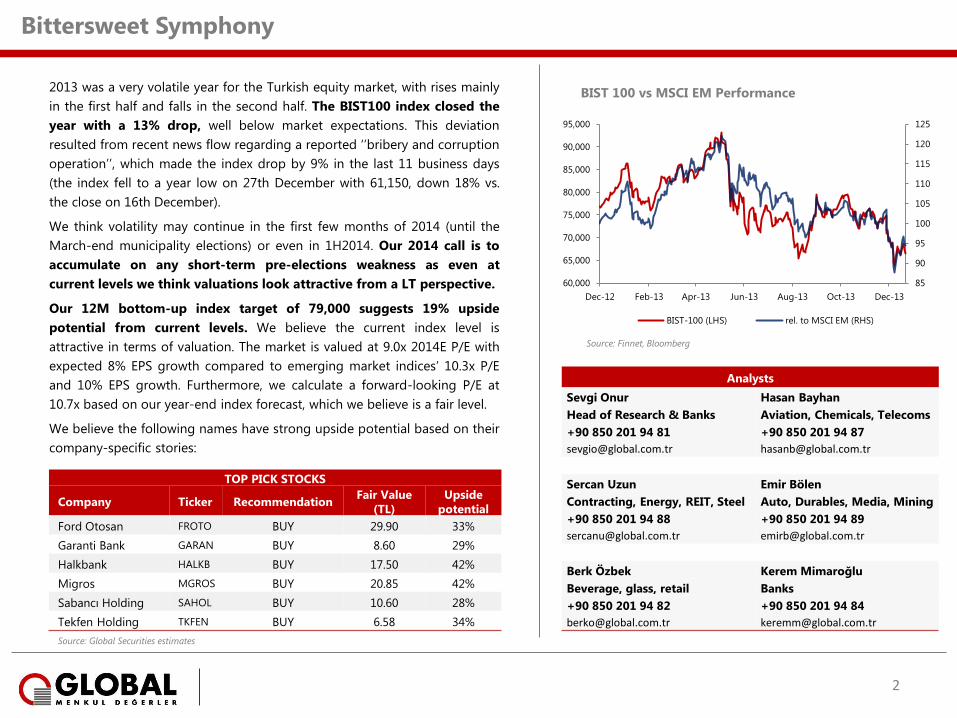

2013 was a very volatile year for the Turkish equity market, with rises mainly

in the first half and falls in the second half. The BIST100 index closed the

year with a 13% drop, well below market expectations. This deviation

resulted from recent news flow regarding a reported ‘’bribery and corruption

operation’’, which made the index drop by 9% in the last 11 business days

(the index fell to a year low on 27th December with 61,150, down 18% vs.

the close on 16th December).

We think volatility may continue in the first few months of 2014 (until the

March-end municipality elections) or even in 1H2014. Our 2014 call is to

accumulate on any short-term pre-elections weakness as even at

current levels we think valuations look attractive from a LT perspective.

Our 12M bottom-up index target of 79,000 suggests 19% upside

potential from current levels. We believe the current index level is

attractive in terms of valuation. The market is valued at 9.0x 2014E P/E with

expected 8% EPS growth compared to emerging market indices’ 10.3x P/E

and 10% EPS growth. Furthermore, we calculate a forward-looking P/E at

10.7x based on our year-end index forecast, which we believe is a fair level.

We believe the following names have strong upside potential based on their

company-specific stories:

Bittersweet Symphony

TOP PICK STOCKS

Company Ticker Recommendation Fair Value

(TL)

Upside

potential

Ford Otosan FROTO BUY 29.90 33%

Garanti Bank GARAN BUY 8.60 29%

Halkbank HALKB BUY 17.50 42%

Migros MGROS BUY 20.85 42%

Sabancı Holding SAHOL BUY 10.60 28%

Tekfen Holding TKFEN BUY 6.58 34%

Source: Global Securities estimates

Analysts

Sevgi Onur Hasan Bayhan

Head of Research & Banks Aviation, Chemicals, Telecoms

+90 850 201 94 81 +90 850 201 94 87

[email protected] [email protected]

Sercan Uzun Emir Bölen

Contracting, Energy, REIT, Steel Auto, Durables, Media, Mining

+90 850 201 94 88 +90 850 201 94 89

[email protected] [email protected]

Berk Özbek Kerem Mimaroğlu

Beverage, glass, retail Banks

+90 850 201 94 82 +90 850 201 94 84

[email protected] [email protected]

85

90

95

100

105

110

115

120

125

60,000

65,000

70,000

75,000

80,000

85,000

90,000

95,000

Dec-12 Feb-13 Apr-13 Jun-13 Aug-13 Oct-13 Dec-13

BIST 100 vs MSCI EM Performance

BIST-100 (LHS) rel. to MSCI EM (RHS)

Source: Finnet, Bloomberg

2

We believe that the market had four distinct periods of high volatility

in 2013:

i) January – the third week of May: the market was bullish (BIST100 index

gained 19%) with expectations of Turkey’s second investment grade

rating and all-time low interest rates.

ii) Third week of May – September: The BIST100 index lost 29%, affected

by the FED tapering announcement (May), Gezi protests (June) and

high tension in Syria (August).

iii) September – Mid December: BIST100 index recovered 8% thanks to no

tapering decision from the FED meeting.

iv) Mid December – year end: BIST100 index lost 9% in only 11 days. The

market was hit by the ‘bribery and corruption’ probe. The alleged

involvement of relatives of politicians, high-ranking businessmen and

bureaucrats in this corruption probe shook the Turkish market

significantly.

We have built our 2014 equity strategy on a macro environment shaped

by higher interest rates and tightened monetary policy. Accordingly, we

have increased our risk free rate from 7% to 9%, which leads to our 79,000

index target. Please see page 4 for our index sensitivity analysis.

We suggest caution in the first half 2014. The potential outcome from the

‘bribery and corruption’ probe, the likelihood of further probes and the

municipality elections at end-March all pose political risks. We are more

bullish for the second half of the year as we assume the political situation

will calm down as we explain in our base case scneario on slide 6. We also

expect FED tapering to be fully priced in with stabilizing interest rates.

Bittersweet Symphony

Valuation Multiples (2014E)*

NI growth P/E EV/EBITDA P/BV

Banks -9% 7.5 n.m. 1.1

Conglomerates 24% 6.7 n.m. 0.9

Industrial 24% 10.6 6.7 1.7

Borsa Istanbul 8% 9.0 6.7 1.3

MSCI EM 10% 10.3 6.9 1.3

65

75

85

95

105

115

125

135

Dec-12 Feb-13 Apr-13 Jun-13 Aug-13 Oct-13 Dec-13

BIST100 fin. and non-fin. rel. stock performance

Financials Non-financials

Financials underperformed non-

financials significantly in 2013;

especially after May (Fed tapering

announcement and Gezi Protests)

Source: Finnet, Bloomberg

3

Source: Bloomberg, Global Securities estimates *Coverage universe only

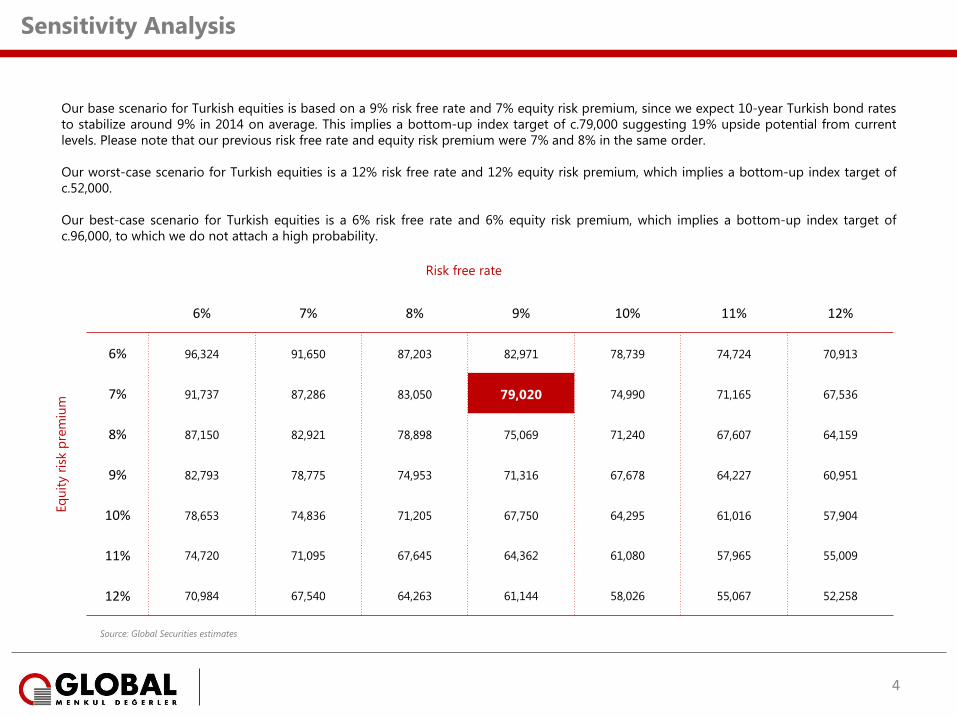

Sensitivity Analysis

Our base scenario for Turkish equities is based on a 9% risk free rate and 7% equity risk premium, since we expect 10-year Turkish bond rates

to stabilize around 9% in 2014 on average. This implies a bottom-up index target of c.79,000 suggesting 19% upside potential from current

levels. Please note that our previous risk free rate and equity risk premium were 7% and 8% in the same order.

Our worst-case scenario for Turkish equities is a 12% risk free rate and 12% equity risk premium, which implies a bottom-up index target of

c.52,000.

Our best-case scenario for Turkish equities is a 6% risk free rate and 6% equity risk premium, which implies a bottom-up index target of

c.96,000, to which we do not attach a high probability.

Risk free rate

Eq

uit

y r

isk p

rem

ium

6% 7% 8% 9% 10% 11% 12%

6% 96,324 91,650 87,203 82,971 78,739 74,724 70,913

7% 91,737 87,286 83,050 79,020 74,990 71,165 67,536

8% 87,150 82,921 78,898 75,069 71,240 67,607 64,159

9% 82,793 78,775 74,953 71,316 67,678 64,227 60,951

10% 78,653 74,836 71,205 67,750 64,295 61,016 57,904

11% 74,720 71,095 67,645 64,362 61,080 57,965 55,009

12% 70,984 67,540 64,263 61,144 58,026 55,067 52,258

4

Source: Global Securities estimates

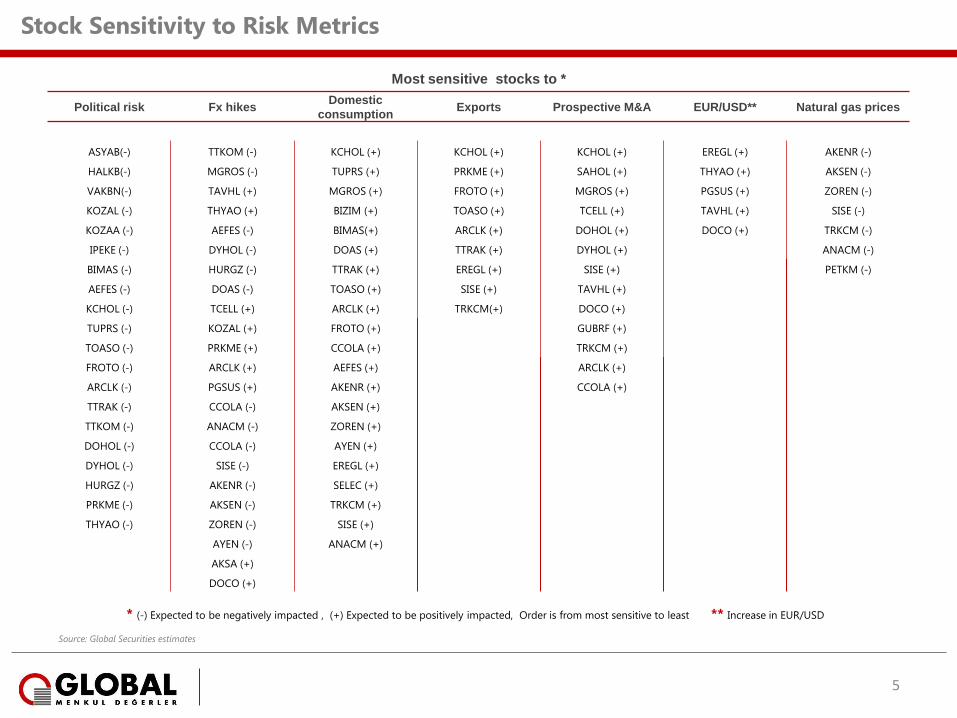

Stock Sensitivity to Risk Metrics

* (-) Expected to be negatively impacted , (+) Expected to be positively impacted, Order is from most sensitive to least

Most sensitive stocks to *

Political risk Fx hikes Domestic

consumption Exports Prospective M&A EUR/USD** Natural gas prices

ASYAB(-) TTKOM (-) KCHOL (+) KCHOL (+) KCHOL (+) EREGL (+) AKENR (-)

HALKB(-) MGROS (-) TUPRS (+) PRKME (+) SAHOL (+) THYAO (+) AKSEN (-)

VAKBN(-) TAVHL (+) MGROS (+) FROTO (+) MGROS (+) PGSUS (+) ZOREN (-)

KOZAL (-) THYAO (+) BIZIM (+) TOASO (+) TCELL (+) TAVHL (+) SISE (-)

KOZAA (-) AEFES (-) BIMAS(+) ARCLK (+) DOHOL (+) DOCO (+) TRKCM (-)

IPEKE (-) DYHOL (-) DOAS (+) TTRAK (+) DYHOL (+) ANACM (-)

BIMAS (-) HURGZ (-) TTRAK (+) EREGL (+) SISE (+) PETKM (-)

AEFES (-) DOAS (-) TOASO (+) SISE (+) TAVHL (+)

KCHOL (-) TCELL (+) ARCLK (+) TRKCM(+) DOCO (+)

TUPRS (-) KOZAL (+) FROTO (+) GUBRF (+)

TOASO (-) PRKME (+) CCOLA (+) TRKCM (+)

FROTO (-) ARCLK (+) AEFES (+) ARCLK (+)

ARCLK (-) PGSUS (+) AKENR (+) CCOLA (+)

TTRAK (-) CCOLA (-) AKSEN (+)

TTKOM (-) ANACM (-) ZOREN (+)

DOHOL (-) CCOLA (-) AYEN (+)

DYHOL (-) SISE (-) EREGL (+)

HURGZ (-) AKENR (-) SELEC (+)

PRKME (-) AKSEN (-) TRKCM (+)

THYAO (-) ZOREN (-) SISE (+)

AYEN (-) ANACM (+)

AKSA (+)

DOCO (+)

** Increase in EUR/USD

5

Source: Global Securities estimates

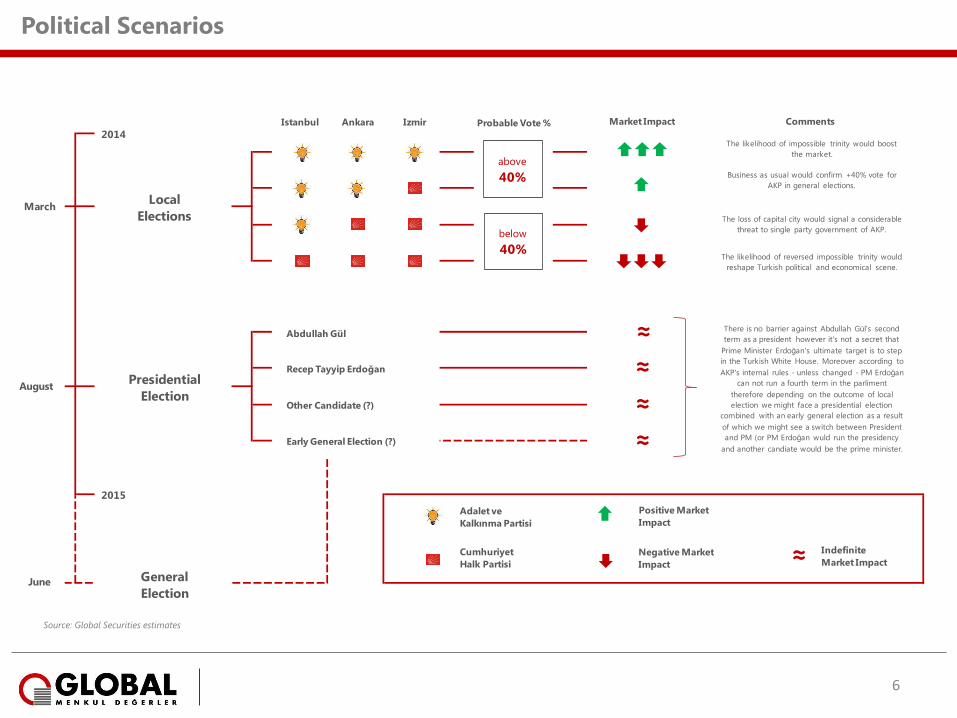

Political Scenarios

6

Presidential

Election

Local

ElectionsMarch

August

Istanbul Ankara Izmir

Abdullah Gül

Recep Tayyip Erdoğan

Other Candidate (?)

Early General Election (?)

2015

2014Probable Vote %

above

40%

below

40%

Market Impact

General

ElectionJune

Adalet ve

Kalkınma Partisi

Cumhuriyet

Halk Partisi

Positive Market

Impact

Negative Market

Impact

≈

≈

≈

Comments

The likelihood of impossible trinity would boost

the market.

Business as usual would confirm +40% vote for

AKP in general elections.

The loss of capital city would signal a considerable

threat to single party government of AKP.

The likelihood of reversed impossible trinity would

reshape Turkish political and economical scene.

There is no barrier against Abdullah Gül's second

term as a president however it's not a secret that

Prime Minister Erdoğan's ultimate target is to step

in the Turkish White House. Moreover according to

AKP's internal rules - unless changed - PM Erdoğan

can not run a fourth term in the parliment

therefore depending on the outcome of local

election we might face a presidential election

combined with an early general election as a result

of which we might see a switch between President

and PM (or PM Erdoğan wuld run the presidency

and another candiate would be the prime minister.

≈ Indefinite

Market Impact

≈

Source: Global Securities estimates

A summary of events since December 17

• On December 17, Turkey was shaken by news regarding the detention of the sons of three cabinet ministers, an AKP-affiliated mayor and several

businessmen including the CEO of Halkbank, Mr Suleyman Aslan, by the police.

• According to the various media sources, the allegations focused on illegal gold trade, money laundering, bribery and fraudulent tenders in the construction

sector. The government’s apparent response was to perceive these events as another foreign-led operation (just like the Gezi Park protests) to hurt PM

Erdogan and the ruling AKP. The tension is reported to arise from a political clash between the AKP and the Gulen Community with resultant

unsubstantiated reports of dissension within the government and with exposure of existing disagreements between both parties’ supporters.

• The Gulen Community is an Islamic Community led by Fethullah Gulen who lives in self-imposed exile in Pennsylvania. It is widely believed that the

Gulenists were natural allies of the AKP when it first came to power in 2002.

• Although initial signs of a dispute were reported in the press in early 2013, both parties rejected these allegations. However, the Gulen Community, which

has a number of representatives in parliament has aimed for more representation in both the political and economic scene. The government’s attempts to

shut down test preparation centers (dershane) in Turkey - where the Gülen Community’s centers are one of the sector drivers apparently increased the

tension between the AKP and Gulen Community.

• On December 25, the Minister of the Interior, Muammer Güler, and the Minister of the Economy, Zafer Çağlayan, whose sons had been detained, resigned

from their posts. Erdoğan Bayraktar, the Minister of Environment and Urbanization also resigned on the same day stating that PM Erdogan should also

resign for the sake of the wellbeing of the nation, as all the construction/zoning permits mentioned in the investigation were approved by PM Erdogan. He

not only resigned from his post, but also from the AKP and from his seat in parliament. Later in the day, Prime Minister Erdogan reshuffled his cabinet with

10 new faces - one of them from outside parliament.

• Following this the government reshuffled the positions of several police chief and government prosecutors as well.

Is the political situation likely to calm down?

• We think so. We believe the March 30 election results should be the key to the direction of the political tension. The AKP has a proven track record of

steering difficult situations to calmer waters. Hence our base case scenario is that the AKP should be capable of managing this situation, albeit with some

likely loss of votes at the local elections.

What happened since December 17 and what is next?

7

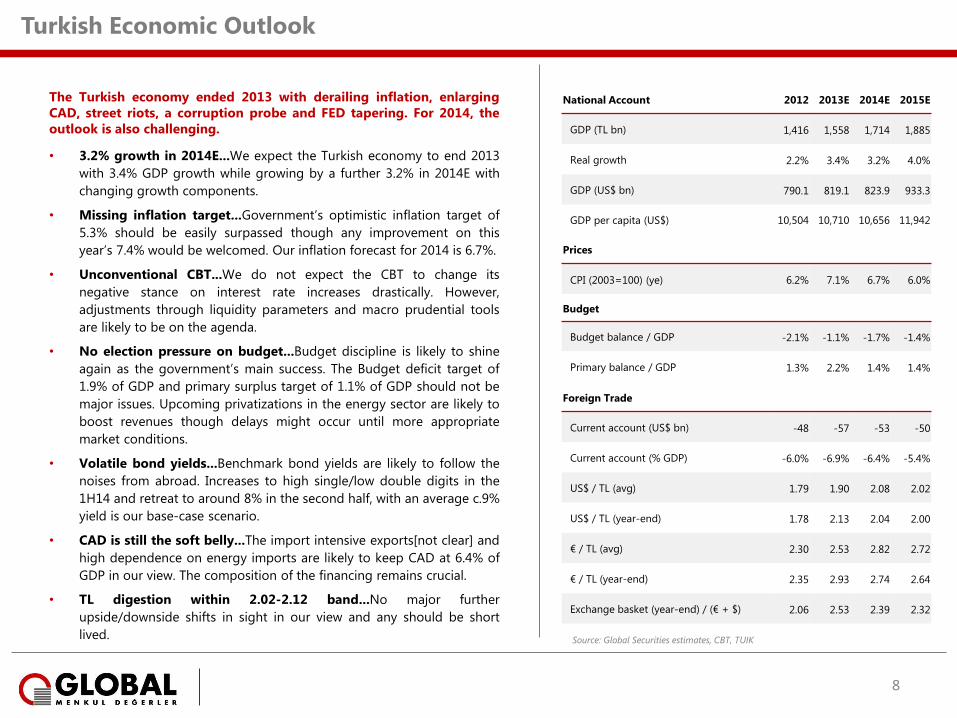

The Turkish economy ended 2013 with derailing inflation, enlarging

CAD, street riots, a corruption probe and FED tapering. For 2014, the

outlook is also challenging.

• 3.2% growth in 2014E...We expect the Turkish economy to end 2013

with 3.4% GDP growth while growing by a further 3.2% in 2014E with

changing growth components.

• Missing inflation target...Government’s optimistic inflation target of

5.3% should be easily surpassed though any improvement on this

year’s 7.4% would be welcomed. Our inflation forecast for 2014 is 6.7%.

• Unconventional CBT...We do not expect the CBT to change its

negative stance on interest rate increases drastically. However,

adjustments through liquidity parameters and macro prudential tools

are likely to be on the agenda.

• No election pressure on budget...Budget discipline is likely to shine

again as the government’s main success. The Budget deficit target of

1.9% of GDP and primary surplus target of 1.1% of GDP should not be

major issues. Upcoming privatizations in the energy sector are likely to

boost revenues though delays might occur until more appropriate

market conditions.

• Volatile bond yields...Benchmark bond yields are likely to follow the

noises from abroad. Increases to high single/low double digits in the

1H14 and retreat to around 8% in the second half, with an average c.9%

yield is our base-case scenario.

• CAD is still the soft belly...The import intensive exports[not clear] and

high dependence on energy imports are likely to keep CAD at 6.4% of

GDP in our view. The composition of the financing remains crucial.

• TL digestion within 2.02-2.12 band...No major further

upside/downside shifts in sight in our view and any should be short

lived.

Turkish Economic Outlook

National Account 2012 2013E 2014E 2015E

GDP (TL bn) 1,416 1,558 1,714 1,885

Real growth 2.2% 3.4% 3.2% 4.0%

GDP (US$ bn) 790.1 819.1 823.9 933.3

GDP per capita (US$) 10,504 10,710 10,656 11,942

Prices

CPI (2003=100) (ye) 6.2% 7.1% 6.7% 6.0%

Budget

Budget balance / GDP -2.1% -1.1% -1.7% -1.4%

Primary balance / GDP 1.3% 2.2% 1.4% 1.4%

Foreign Trade

Current account (US$ bn) -48 -57 -53 -50

Current account (% GDP) -6.0% -6.9% -6.4% -5.4%

US$ / TL (avg) 1.79 1.90 2.08 2.02

US$ / TL (year-end) 1.78 2.13 2.04 2.00

€ / TL (avg) 2.30 2.53 2.82 2.72

€ / TL (year-end) 2.35 2.93 2.74 2.64

Exchange basket (year-end) / (€ + $) 2.06 2.53 2.39 2.32

8

Source: Global Securities estimates, CBT, TUIK

Turkish Economic Outlook

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

-10%

-5%

0%

5%

10%

15%

2006 2007 2008 2009 2010 2011 2012 2013E 2014E

Growth components

Private consumption Public consumption

Gross fixed capital formation Change in inventories

Net export GDP growth (RHS)

Source: Turkstat, Global Securities

6.9%

4.7%

0.7%

-4.8%

9.2% 8.8%

2.2%

3.4% 3.2%

2006 2007 2008 2009 2010 2011 2012 2013E 2014E

Turkey GDP growth YoY

ESTIMATE

Source: Turkstat, Global Securities

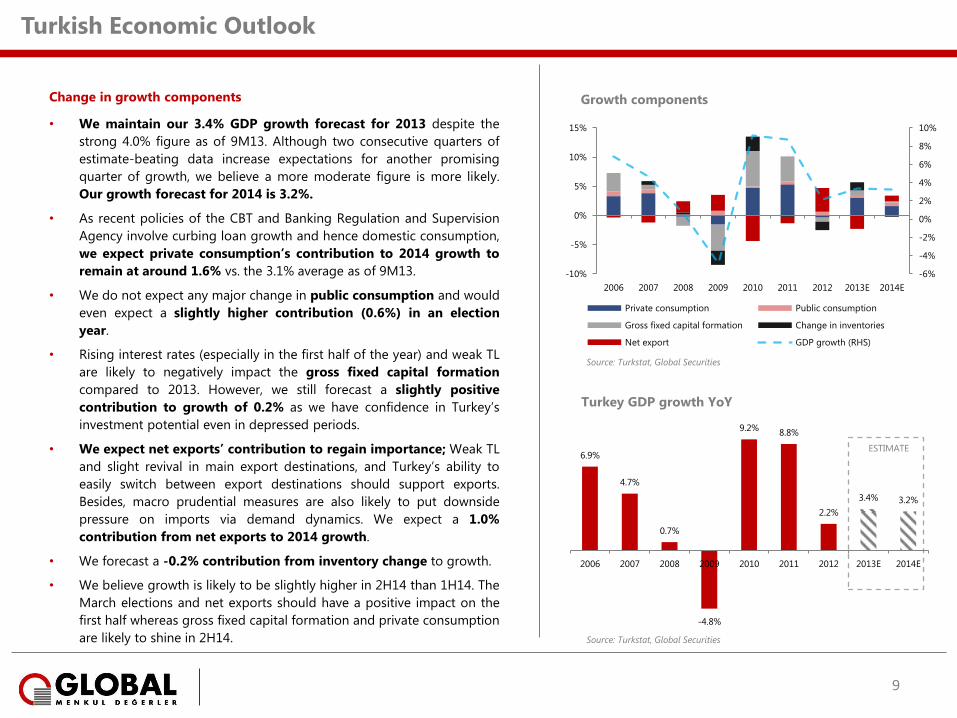

Change in growth components

• We maintain our 3.4% GDP growth forecast for 2013 despite the

strong 4.0% figure as of 9M13. Although two consecutive quarters of

estimate-beating data increase expectations for another promising

quarter of growth, we believe a more moderate figure is more likely.

Our growth forecast for 2014 is 3.2%.

• As recent policies of the CBT and Banking Regulation and Supervision

Agency involve curbing loan growth and hence domestic consumption,

we expect private consumption’s contribution to 2014 growth to

remain at around 1.6% vs. the 3.1% average as of 9M13.

• We do not expect any major change in public consumption and would

even expect a slightly higher contribution (0.6%) in an election

year.

• Rising interest rates (especially in the first half of the year) and weak TL

are likely to negatively impact the gross fixed capital formation

compared to 2013. However, we still forecast a slightly positive

contribution to growth of 0.2% as we have confidence in Turkey’s

investment potential even in depressed periods.

• We expect net exports’ contribution to regain importance; Weak TL

and slight revival in main export destinations, and Turkey’s ability to

easily switch between export destinations should support exports.

Besides, macro prudential measures are also likely to put downside

pressure on imports via demand dynamics. We expect a 1.0%

contribution from net exports to 2014 growth.

• We forecast a -0.2% contribution from inventory change to growth.

• We believe growth is likely to be slightly higher in 2H14 than 1H14. The

March elections and net exports should have a positive impact on the

first half whereas gross fixed capital formation and private consumption

are likely to shine in 2H14.

9

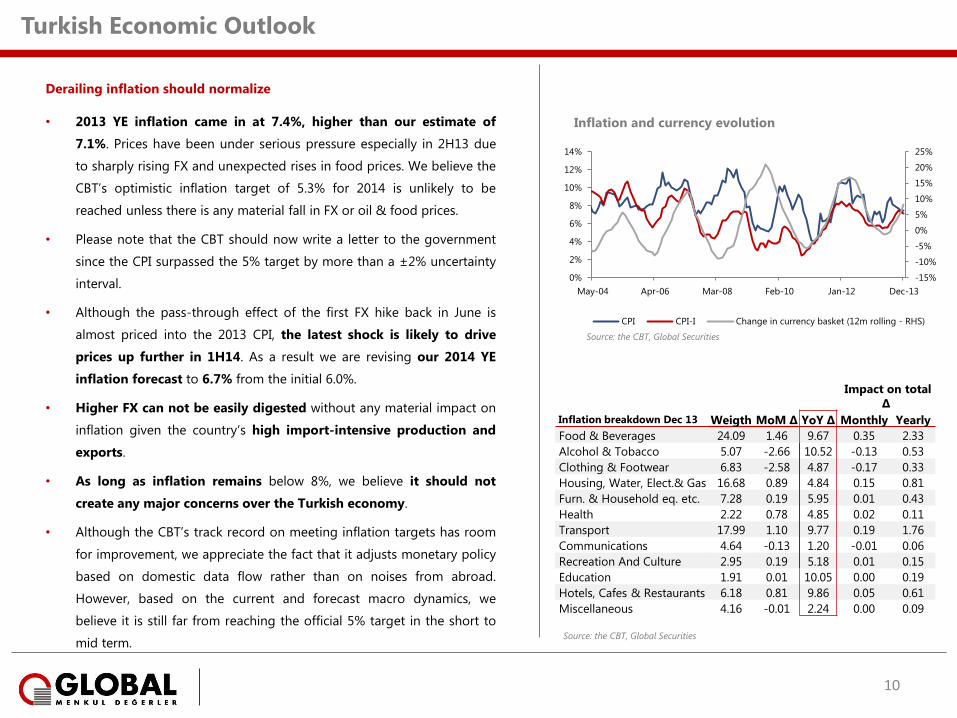

Derailing inflation should normalize

• 2013 YE inflation came in at 7.4%, higher than our estimate of

7.1%. Prices have been under serious pressure especially in 2H13 due

to sharply rising FX and unexpected rises in food prices. We believe the

CBT’s optimistic inflation target of 5.3% for 2014 is unlikely to be

reached unless there is any material fall in FX or oil & food prices.

• Please note that the CBT should now write a letter to the government

since the CPI surpassed the 5% target by more than a ±2% uncertainty

interval.

• Although the pass-through effect of the first FX hike back in June is

almost priced into the 2013 CPI, the latest shock is likely to drive

prices up further in 1H14. As a result we are revising our 2014 YE

inflation forecast to 6.7% from the initial 6.0%.

• Higher FX can not be easily digested without any material impact on

inflation given the country’s high import-intensive production and

exports.

• As long as inflation remains below 8%, we believe it should not

create any major concerns over the Turkish economy.

• Although the CBT’s track record on meeting inflation targets has room

for improvement, we appreciate the fact that it adjusts monetary policy

based on domestic data flow rather than on noises from abroad.

However, based on the current and forecast macro dynamics, we

believe it is still far from reaching the official 5% target in the short to

mid term.

Turkish Economic Outlook

Impact on total

∆

Inflation breakdown Dec 13 Weigth MoM ∆ YoY ∆ Monthly Yearly

Food & Beverages 24.09 1.46 9.67 0.35 2.33

Alcohol & Tobacco 5.07 -2.66 10.52 -0.13 0.53

Clothing & Footwear 6.83 -2.58 4.87 -0.17 0.33

Housing, Water, Elect.& Gas 16.68 0.89 4.84 0.15 0.81

Furn. & Household eq. etc. 7.28 0.19 5.95 0.01 0.43

Health 2.22 0.78 4.85 0.02 0.11

Transport 17.99 1.10 9.77 0.19 1.76

Communications 4.64 -0.13 1.20 -0.01 0.06

Recreation And Culture 2.95 0.19 5.18 0.01 0.15

Education 1.91 0.01 10.05 0.00 0.19

Hotels, Cafes & Restaurants 6.18 0.81 9.86 0.05 0.61

Miscellaneous 4.16 -0.01 2.24 0.00 0.09

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

0%

2%

4%

6%

8%

10%

12%

14%

May-04 Apr-06 Mar-08 Feb-10 Jan-12 Dec-13

Inflation and currency evolution

CPI CPI-I Change in currency basket (12m rolling - RHS)

Source: the CBT, Global Securities

10

Source: the CBT, Global Securities

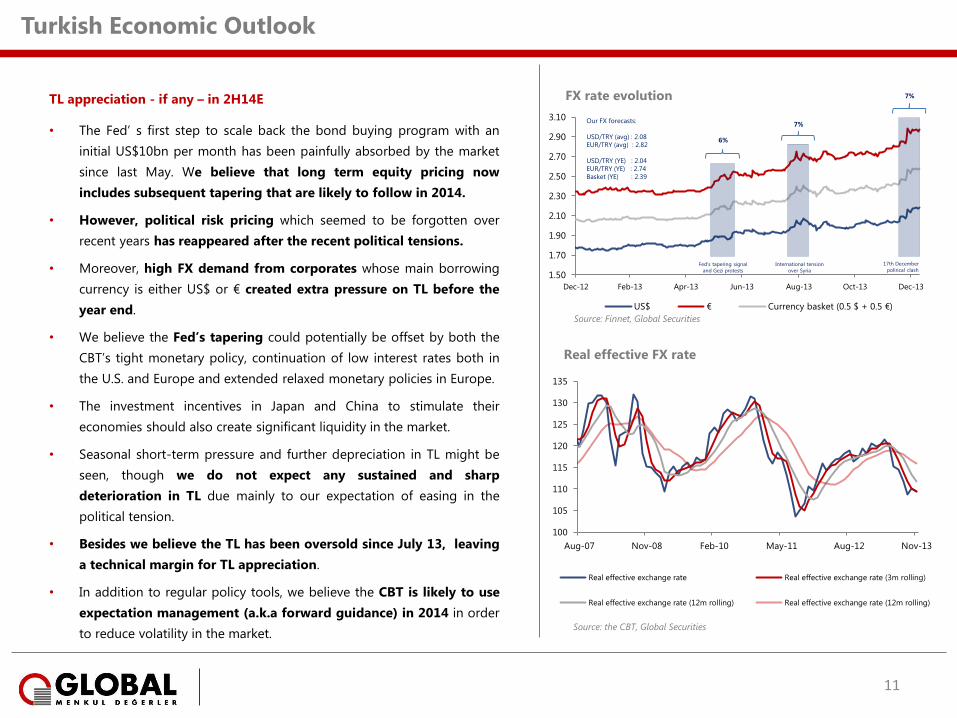

TL appreciation - if any – in 2H14E

• The Fed’ s first step to scale back the bond buying program with an

initial US$10bn per month has been painfully absorbed by the market

since last May. We believe that long term equity pricing now

includes subsequent tapering that are likely to follow in 2014.

• However, political risk pricing which seemed to be forgotten over

recent years has reappeared after the recent political tensions.

• Moreover, high FX demand from corporates whose main borrowing

currency is either US$ or € created extra pressure on TL before the

year end.

• We believe the Fed’s tapering could potentially be offset by both the

CBT’s tight monetary policy, continuation of low interest rates both in

the U.S. and Europe and extended relaxed monetary policies in Europe.

• The investment incentives in Japan and China to stimulate their

economies should also create significant liquidity in the market.

• Seasonal short-term pressure and further depreciation in TL might be

seen, though we do not expect any sustained and sharp

deterioration in TL due mainly to our expectation of easing in the

political tension.

• Besides we believe the TL has been oversold since July 13, leaving

a technical margin for TL appreciation.

• In addition to regular policy tools, we believe the CBT is likely to use

expectation management (a.k.a forward guidance) in 2014 in order

to reduce volatility in the market.

Turkish Economic Outlook

100

105

110

115

120

125

130

135

Aug-07 Nov-08 Feb-10 May-11 Aug-12 Nov-13

Real effective FX rate

Real effective exchange rate Real effective exchange rate (3m rolling)

Real effective exchange rate (12m rolling) Real effective exchange rate (12m rolling)

Source: the CBT, Global Securities

1.50

1.70

1.90

2.10

2.30

2.50

2.70

2.90

3.10

Dec-12 Feb-13 Apr-13 Jun-13 Aug-13 Oct-13 Dec-13

FX rate evolution

US$ € Currency basket (0.5 $ + 0.5 €)

6%

7%

7%

Fed's tapering signal

and Gezi protests

International tension

over Syria

17th December

polirical clash

Our FX forecasts:

USD/TRY (avg) : 2.08

EUR/TRY (avg) : 2.82

USD/TRY (YE) : 2.04

EUR/TRY (YE) : 2.74

Basket (YE) : 2.39

Source: Finnet, Global Securities

11

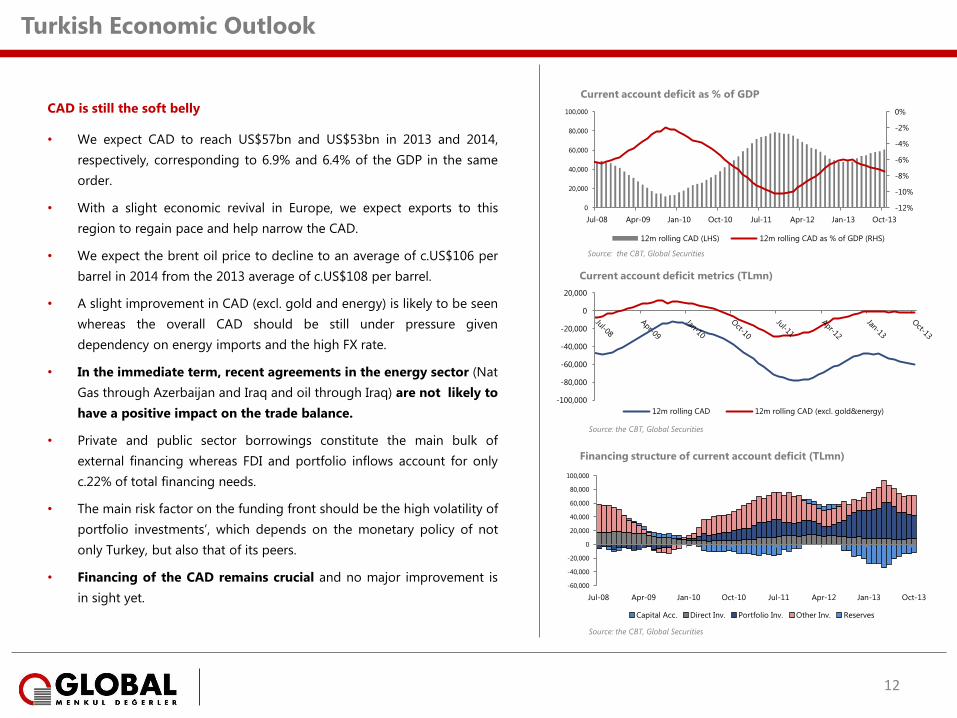

CAD is still the soft belly

• We expect CAD to reach US$57bn and US$53bn in 2013 and 2014,

respectively, corresponding to 6.9% and 6.4% of the GDP in the same

order.

• With a slight economic revival in Europe, we expect exports to this

region to regain pace and help narrow the CAD.

• We expect the brent oil price to decline to an average of c.US$106 per

barrel in 2014 from the 2013 average of c.US$108 per barrel.

• A slight improvement in CAD (excl. gold and energy) is likely to be seen

whereas the overall CAD should be still under pressure given

dependency on energy imports and the high FX rate.

• In the immediate term, recent agreements in the energy sector (Nat

Gas through Azerbaijan and Iraq and oil through Iraq) are not likely to

have a positive impact on the trade balance.

• Private and public sector borrowings constitute the main bulk of

external financing whereas FDI and portfolio inflows account for only

c.22% of total financing needs.

• The main risk factor on the funding front should be the high volatility of

portfolio investments’, which depends on the monetary policy of not

only Turkey, but also that of its peers.

• Financing of the CAD remains crucial and no major improvement is

in sight yet.

Turkish Economic Outlook

-12%

-10%

-8%

-6%

-4%

-2%

0%

0

20,000

40,000

60,000

80,000

100,000

Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12 Jan-13 Oct-13

Current account deficit as % of GDP

12m rolling CAD (LHS) 12m rolling CAD as % of GDP (RHS)

Source: the CBT, Global Securities

-100,000

-80,000

-60,000

-40,000

-20,000

0

20,000

Current account deficit metrics (TLmn)

12m rolling CAD 12m rolling CAD (excl. gold&energy)

Source: the CBT, Global Securities

-60,000

-40,000

-20,000

0

20,000

40,000

60,000

80,000

100,000

Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12 Jan-13 Oct-13

Financing structure of current account deficit (TLmn)

Capital Acc. Direct Inv. Portfolio Inv. Other Inv. Reserves

Source: the CBT, Global Securities

12

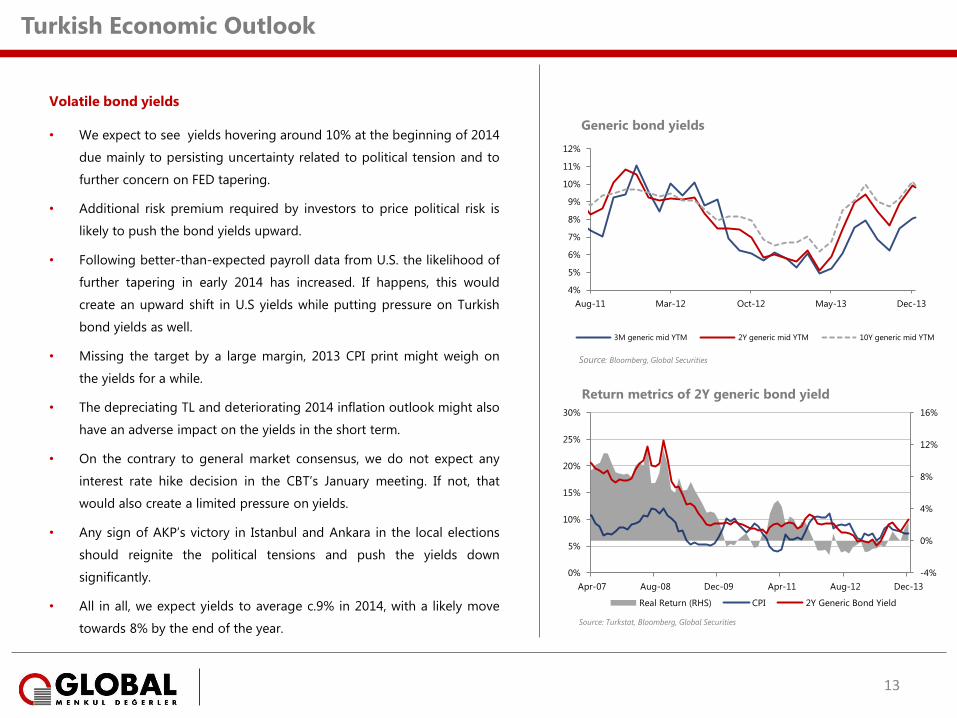

Volatile bond yields

• We expect to see yields hovering around 10% at the beginning of 2014

due mainly to persisting uncertainty related to political tension and to

further concern on FED tapering.

• Additional risk premium required by investors to price political risk is

likely to push the bond yields upward.

• Following better-than-expected payroll data from U.S. the likelihood of

further tapering in early 2014 has increased. If happens, this would

create an upward shift in U.S yields while putting pressure on Turkish

bond yields as well.

• Missing the target by a large margin, 2013 CPI print might weigh on

the yields for a while.

• The depreciating TL and deteriorating 2014 inflation outlook might also

have an adverse impact on the yields in the short term.

• On the contrary to general market consensus, we do not expect any

interest rate hike decision in the CBT’s January meeting. If not, that

would also create a limited pressure on yields.

• Any sign of AKP’s victory in Istanbul and Ankara in the local elections

should reignite the political tensions and push the yields down

significantly.

• All in all, we expect yields to average c.9% in 2014, with a likely move

towards 8% by the end of the year.

Turkish Economic Outlook

4%

5%

6%

7%

8%

9%

10%

11%

12%

Aug-11 Mar-12 Oct-12 May-13 Dec-13

Generic bond yields

3M generic mid YTM 2Y generic mid YTM 10Y generic mid YTM

Source: Bloomberg, Global Securities

-4%

0%

4%

8%

12%

16%

0%

5%

10%

15%

20%

25%

30%

Apr-07 Aug-08 Dec-09 Apr-11 Aug-12 Dec-13

Return metrics of 2Y generic bond yield

Real Return (RHS) CPI 2Y Generic Bond Yield

Source: Turkstat, Bloomberg, Global Securities

13

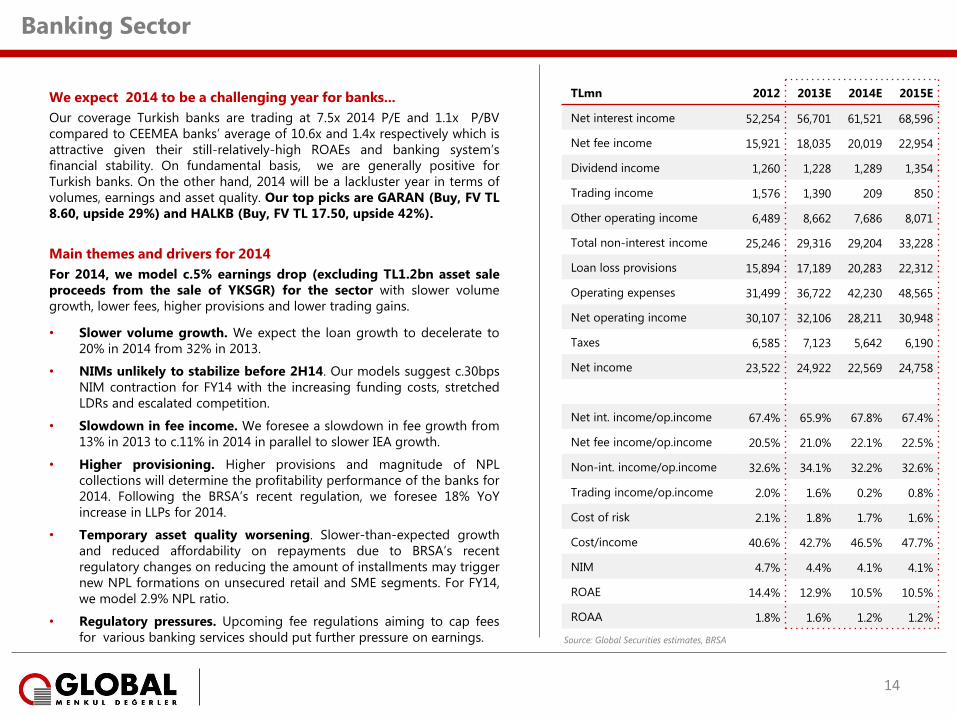

Banking Sector

TLmn 2012 2013E 2014E 2015E

Net interest income 52,254 56,701 61,521 68,596

Net fee income 15,921 18,035 20,019 22,954

Dividend income 1,260 1,228 1,289 1,354

Trading income 1,576 1,390 209 850

Other operating income 6,489 8,662 7,686 8,071

Total non-interest income 25,246 29,316 29,204 33,228

Loan loss provisions 15,894 17,189 20,283 22,312

Operating expenses 31,499 36,722 42,230 48,565

Net operating income 30,107 32,106 28,211 30,948

Taxes 6,585 7,123 5,642 6,190

Net income 23,522 24,922 22,569 24,758

Net int. income/op.income 67.4% 65.9% 67.8% 67.4%

Net fee income/op.income 20.5% 21.0% 22.1% 22.5%

Non-int. income/op.income 32.6% 34.1% 32.2% 32.6%

Trading income/op.income 2.0% 1.6% 0.2% 0.8%

Cost of risk 2.1% 1.8% 1.7% 1.6%

Cost/income 40.6% 42.7% 46.5% 47.7%

NIM 4.7% 4.4% 4.1% 4.1%

ROAE 14.4% 12.9% 10.5% 10.5%

ROAA 1.8% 1.6% 1.2% 1.2%

We expect 2014 to be a challenging year for banks...

Our coverage Turkish banks are trading at 7.5x 2014 P/E and 1.1x P/BV

compared to CEEMEA banks’ average of 10.6x and 1.4x respectively which is

attractive given their still-relatively-high ROAEs and banking system’s

financial stability. On fundamental basis, we are generally positive for

Turkish banks. On the other hand, 2014 will be a lackluster year in terms of

volumes, earnings and asset quality. Our top picks are GARAN (Buy, FV TL

8.60, upside 29%) and HALKB (Buy, FV TL 17.50, upside 42%).

Main themes and drivers for 2014

For 2014, we model c.5% earnings drop (excluding TL1.2bn asset sale

proceeds from the sale of YKSGR) for the sector with slower volume

growth, lower fees, higher provisions and lower trading gains.

• Slower volume growth. We expect the loan growth to decelerate to

20% in 2014 from 32% in 2013.

• NIMs unlikely to stabilize before 2H14. Our models suggest c.30bps

NIM contraction for FY14 with the increasing funding costs, stretched

LDRs and escalated competition.

• Slowdown in fee income. We foresee a slowdown in fee growth from

13% in 2013 to c.11% in 2014 in parallel to slower IEA growth.

• Higher provisioning. Higher provisions and magnitude of NPL

collections will determine the profitability performance of the banks for

2014. Following the BRSA’s recent regulation, we foresee 18% YoY

increase in LLPs for 2014.

• Temporary asset quality worsening. Slower-than-expected growth

and reduced affordability on repayments due to BRSA’s recent

regulatory changes on reducing the amount of installments may trigger

new NPL formations on unsecured retail and SME segments. For FY14,

we model 2.9% NPL ratio.

• Regulatory pressures. Upcoming fee regulations aiming to cap fees

for various banking services should put further pressure on earnings.

14

Source: Global Securities estimates, BRSA

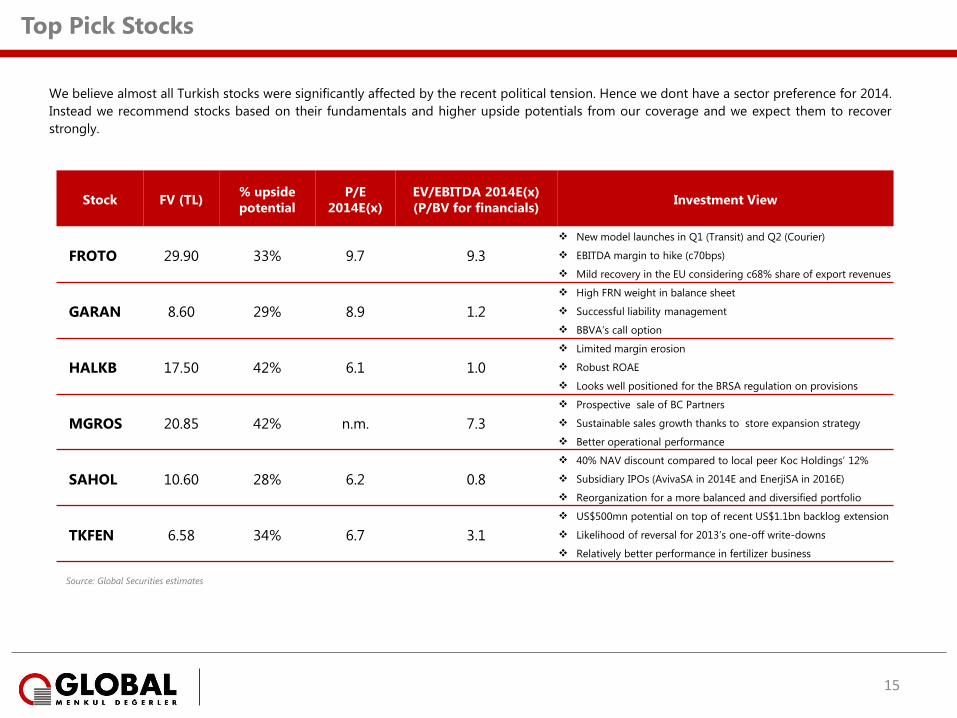

Top Pick Stocks

We believe almost all Turkish stocks were significantly affected by the recent political tension. Hence we dont have a sector preference for 2014.

Instead we recommend stocks based on their fundamentals and higher upside potentials from our coverage and we expect them to recover

strongly.

Stock FV (TL) % upside

potential

P/E

2014E(x)

EV/EBITDA 2014E(x)

(P/BV for financials) Investment View

FROTO 29.90 33% 9.7 9.3

New model launches in Q1 (Transit) and Q2 (Courier)

EBITDA margin to hike (c70bps)

Mild recovery in the EU considering c68% share of export revenues

GARAN 8.60 29% 8.9 1.2

High FRN weight in balance sheet

Successful liability management

BBVA’s call option

HALKB 17.50 42% 6.1 1.0

Limited margin erosion

Robust ROAE

Looks well positioned for the BRSA regulation on provisions

MGROS 20.85 42% n.m. 7.3

Prospective sale of BC Partners

Sustainable sales growth thanks to store expansion strategy

Better operational performance

SAHOL 10.60 28% 6.2 0.8

40% NAV discount compared to local peer Koc Holdings’ 12%

Subsidiary IPOs (AvivaSA in 2014E and EnerjiSA in 2016E)

Reorganization for a more balanced and diversified portfolio

TKFEN 6.58 34% 6.7 3.1

US$500mn potential on top of recent US$1.1bn backlog extension

Likelihood of reversal for 2013’s one-off write-downs

Relatively better performance in fertilizer business

15

Source: Global Securities estimates

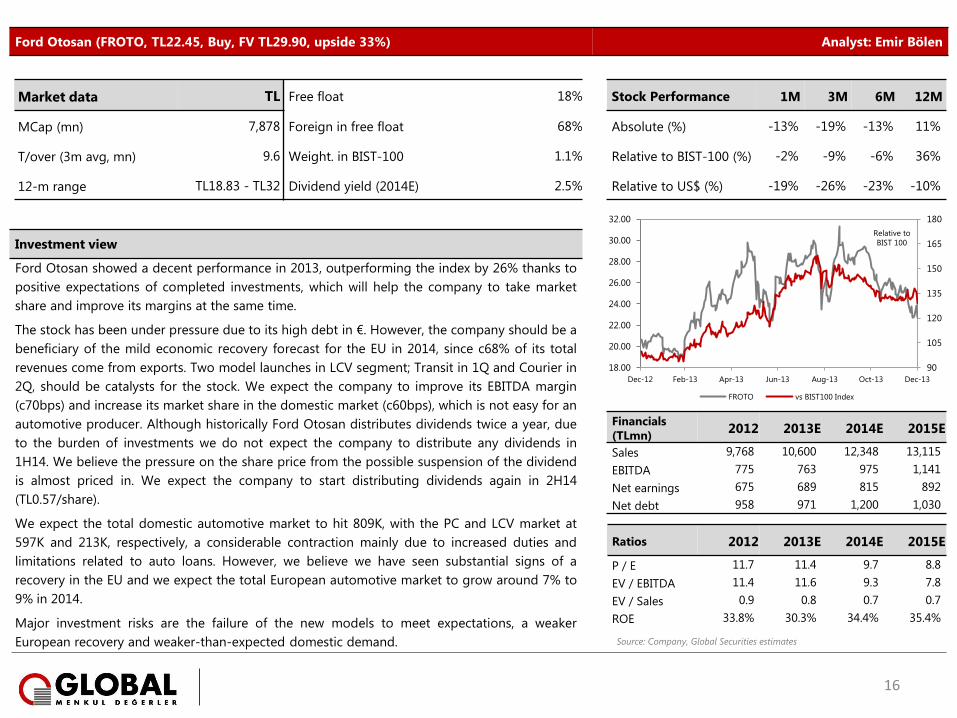

Ford Otosan (FROTO, TL22.45, Buy, FV TL29.90, upside 33%) Analyst: Emir Bölen

Investment view

Ford Otosan showed a decent performance in 2013, outperforming the index by 26% thanks to

positive expectations of completed investments, which will help the company to take market

share and improve its margins at the same time.

The stock has been under pressure due to its high debt in €. However, the company should be a

beneficiary of the mild economic recovery forecast for the EU in 2014, since c68% of its total

revenues come from exports. Two model launches in LCV segment; Transit in 1Q and Courier in

2Q, should be catalysts for the stock. We expect the company to improve its EBITDA margin

(c70bps) and increase its market share in the domestic market (c60bps), which is not easy for an

automotive producer. Although historically Ford Otosan distributes dividends twice a year, due

to the burden of investments we do not expect the company to distribute any dividends in

1H14. We believe the pressure on the share price from the possible suspension of the dividend

is almost priced in. We expect the company to start distributing dividends again in 2H14

(TL0.57/share).

We expect the total domestic automotive market to hit 809K, with the PC and LCV market at

597K and 213K, respectively, a considerable contraction mainly due to increased duties and

limitations related to auto loans. However, we believe we have seen substantial signs of a

recovery in the EU and we expect the total European automotive market to grow around 7% to

9% in 2014.

Major investment risks are the failure of the new models to meet expectations, a weaker

European recovery and weaker-than-expected domestic demand.

Financials

(TLmn) 2012 2013E 2014E 2015E

Sales 9,768 10,600 12,348 13,115

EBITDA 775 763 975 1,141

Net earnings 675 689 815 892

Net debt 958 971 1,200 1,030

Ratios 2012 2013E 2014E 2015E

P / E 11.7 11.4 9.7 8.8

EV / EBITDA 11.4 11.6 9.3 7.8

EV / Sales 0.9 0.8 0.7 0.7

ROE 33.8% 30.3% 34.4% 35.4%

Market data TL Free float 18%

Stock Performance 1M 3M 6M 12M

MCap (mn) 7,878 Foreign in free float 68% Absolute (%) -13% -19% -13% 11%

T/over (3m avg, mn) 9.6 Weight. in BIST-100 1.1% Relative to BIST-100 (%) -2% -9% -6% 36%

12-m range TL18.83 - TL32 Dividend yield (2014E) 2.5% Relative to US$ (%) -19% -26% -23% -10%

90

105

120

135

150

165

180

18.00

20.00

22.00

24.00

26.00

28.00

30.00

32.00

Dec-12 Feb-13 Apr-13 Jun-13 Aug-13 Oct-13 Dec-13

FROTO vs BIST100 Index

Relative to

BIST 100

16

Source: Company, Global Securities estimates

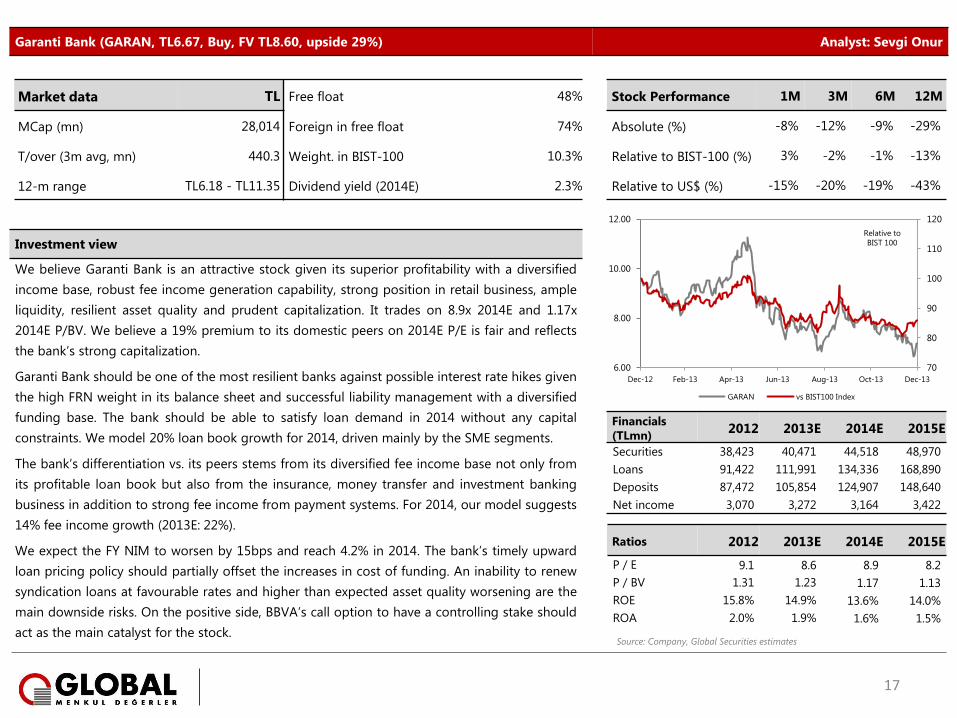

Garanti Bank (GARAN, TL6.67, Buy, FV TL8.60, upside 29%) Analyst: Sevgi Onur

Investment view

We believe Garanti Bank is an attractive stock given its superior profitability with a diversified

income base, robust fee income generation capability, strong position in retail business, ample

liquidity, resilient asset quality and prudent capitalization. It trades on 8.9x 2014E and 1.17x

2014E P/BV. We believe a 19% premium to its domestic peers on 2014E P/E is fair and reflects

the bank’s strong capitalization.

Garanti Bank should be one of the most resilient banks against possible interest rate hikes given

the high FRN weight in its balance sheet and successful liability management with a diversified

funding base. The bank should be able to satisfy loan demand in 2014 without any capital

constraints. We model 20% loan book growth for 2014, driven mainly by the SME segments.

The bank’s differentiation vs. its peers stems from its diversified fee income base not only from

its profitable loan book but also from the insurance, money transfer and investment banking

business in addition to strong fee income from payment systems. For 2014, our model suggests

14% fee income growth (2013E: 22%).

We expect the FY NIM to worsen by 15bps and reach 4.2% in 2014. The bank’s timely upward

loan pricing policy should partially offset the increases in cost of funding. An inability to renew

syndication loans at favourable rates and higher than expected asset quality worsening are the

main downside risks. On the positive side, BBVA’s call option to have a controlling stake should

act as the main catalyst for the stock.

Financials

(TLmn) 2012 2013E 2014E 2015E

Securities 38,423 40,471 44,518 48,970

Loans 91,422 111,991 134,336 168,890

Deposits 87,472 105,854 124,907 148,640

Net income 3,070 3,272 3,164 3,422

Ratios 2012 2013E 2014E 2015E

P / E 9.1 8.6 8.9 8.2

P / BV 1.31 1.23 1.17 1.13

ROE 15.8% 14.9% 13.6% 14.0%

ROA 2.0% 1.9% 1.6% 1.5%

Market data TL Free float 48% Stock Performance 1M 3M 6M 12M

MCap (mn) 28,014 Foreign in free float 74% Absolute (%) -8% -12% -9% -29%

T/over (3m avg, mn) 440.3 Weight. in BIST-100 10.3% Relative to BIST-100 (%) 3% -2% -1% -13%

12-m range TL6.18 - TL11.35 Dividend yield (2014E) 2.3% Relative to US$ (%) -15% -20% -19% -43%

70

80

90

100

110

120

6.00

8.00

10.00

12.00

Dec-12 Feb-13 Apr-13 Jun-13 Aug-13 Oct-13 Dec-13

GARAN vs BIST100 Index

Relative to

BIST 100

17

Source: Company, Global Securities estimates

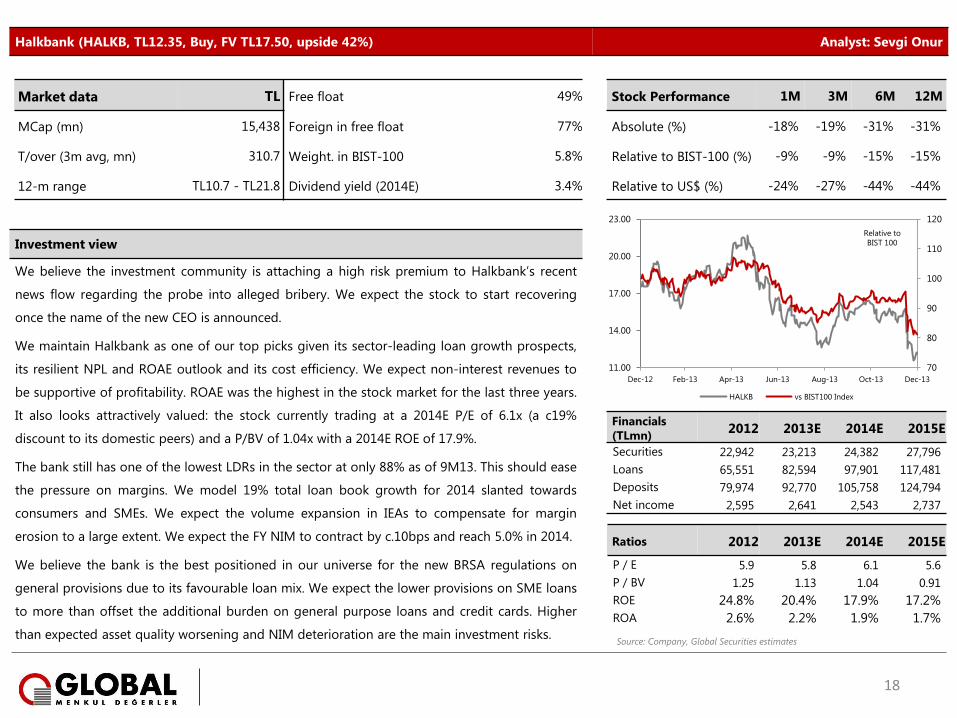

Halkbank (HALKB, TL12.35, Buy, FV TL17.50, upside 42%) Analyst: Sevgi Onur

Investment view

We believe the investment community is attaching a high risk premium to Halkbank’s recent

news flow regarding the probe into alleged bribery. We expect the stock to start recovering

once the name of the new CEO is announced.

We maintain Halkbank as one of our top picks given its sector-leading loan growth prospects,

its resilient NPL and ROAE outlook and its cost efficiency. We expect non-interest revenues to

be supportive of profitability. ROAE was the highest in the stock market for the last three years.

It also looks attractively valued: the stock currently trading at a 2014E P/E of 6.1x (a c19%

discount to its domestic peers) and a P/BV of 1.04x with a 2014E ROE of 17.9%.

The bank still has one of the lowest LDRs in the sector at only 88% as of 9M13. This should ease

the pressure on margins. We model 19% total loan book growth for 2014 slanted towards

consumers and SMEs. We expect the volume expansion in IEAs to compensate for margin

erosion to a large extent. We expect the FY NIM to contract by c.10bps and reach 5.0% in 2014.

We believe the bank is the best positioned in our universe for the new BRSA regulations on

general provisions due to its favourable loan mix. We expect the lower provisions on SME loans

to more than offset the additional burden on general purpose loans and credit cards. Higher

than expected asset quality worsening and NIM deterioration are the main investment risks.

Financials

(TLmn) 2012 2013E 2014E 2015E

Securities 22,942 23,213 24,382 27,796

Loans 65,551 82,594 97,901 117,481

Deposits 79,974 92,770 105,758 124,794

Net income 2,595 2,641 2,543 2,737

Ratios 2012 2013E 2014E 2015E

P / E 5.9 5.8 6.1 5.6

P / BV 1.25 1.13 1.04 0.91

ROE 24.8% 20.4% 17.9% 17.2%

ROA 2.6% 2.2% 1.9% 1.7%

Market data TL Free float 49% Stock Performance 1M 3M 6M 12M

MCap (mn) 15,438 Foreign in free float 77% Absolute (%) -18% -19% -31% -31%

T/over (3m avg, mn) 310.7 Weight. in BIST-100 5.8% Relative to BIST-100 (%) -9% -9% -15% -15%

12-m range TL10.7 - TL21.8 Dividend yield (2014E) 3.4% Relative to US$ (%) -24% -27% -44% -44%

70

80

90

100

110

120

11.00

14.00

17.00

20.00

23.00

Dec-12 Feb-13 Apr-13 Jun-13 Aug-13 Oct-13 Dec-13

HALKB vs BIST100 Index

Relative to

BIST 100

18

Source: Company, Global Securities estimates

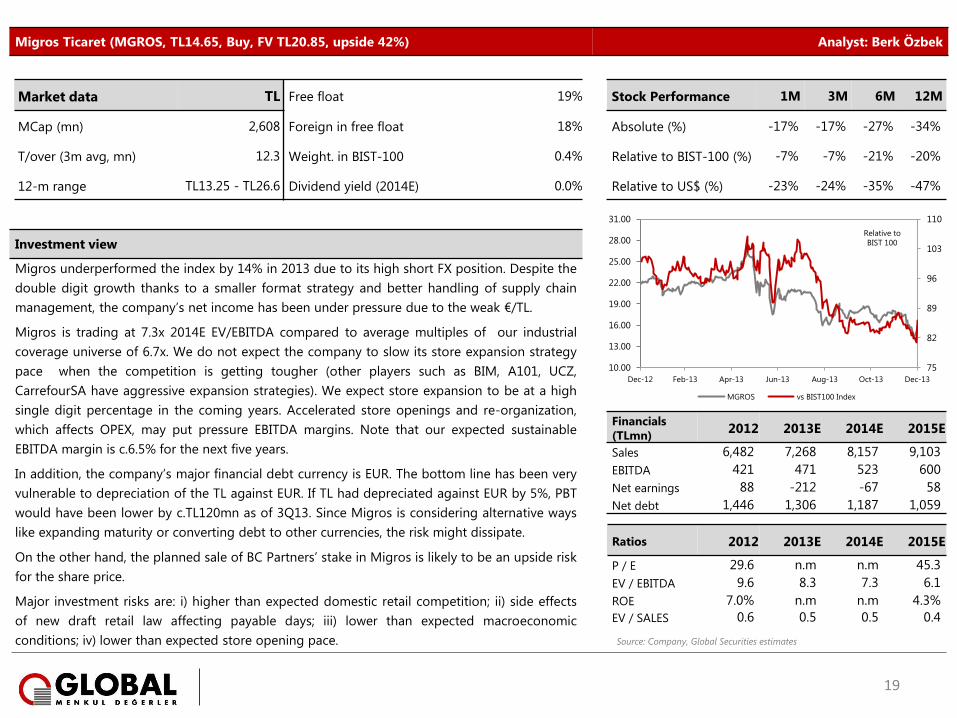

Migros Ticaret (MGROS, TL14.65, Buy, FV TL20.85, upside 42%) Analyst: Berk Özbek

Investment view

Migros underperformed the index by 14% in 2013 due to its high short FX position. Despite the

double digit growth thanks to a smaller format strategy and better handling of supply chain

management, the company’s net income has been under pressure due to the weak €/TL.

Migros is trading at 7.3x 2014E EV/EBITDA compared to average multiples of our industrial

coverage universe of 6.7x. We do not expect the company to slow its store expansion strategy

pace when the competition is getting tougher (other players such as BIM, A101, UCZ,

CarrefourSA have aggressive expansion strategies). We expect store expansion to be at a high

single digit percentage in the coming years. Accelerated store openings and re-organization,

which affects OPEX, may put pressure EBITDA margins. Note that our expected sustainable

EBITDA margin is c.6.5% for the next five years.

In addition, the company’s major financial debt currency is EUR. The bottom line has been very

vulnerable to depreciation of the TL against EUR. If TL had depreciated against EUR by 5%, PBT

would have been lower by c.TL120mn as of 3Q13. Since Migros is considering alternative ways

like expanding maturity or converting debt to other currencies, the risk might dissipate.

On the other hand, the planned sale of BC Partners’ stake in Migros is likely to be an upside risk

for the share price.

Major investment risks are: i) higher than expected domestic retail competition; ii) side effects

of new draft retail law affecting payable days; iii) lower than expected macroeconomic

conditions; iv) lower than expected store opening pace.

Financials

(TLmn) 2012 2013E 2014E 2015E

Sales 6,482 7,268 8,157 9,103

EBITDA 421 471 523 600

Net earnings 88 -212 -67 58

Net debt 1,446 1,306 1,187 1,059

Ratios 2012 2013E 2014E 2015E

P / E 29.6 n.m n.m 45.3

EV / EBITDA 9.6 8.3 7.3 6.1

ROE 7.0% n.m n.m 4.3%

EV / SALES 0.6 0.5 0.5 0.4

Market data TL Free float 19% Stock Performance 1M 3M 6M 12M

MCap (mn) 2,608 Foreign in free float 18% Absolute (%) -17% -17% -27% -34%

T/over (3m avg, mn) 12.3 Weight. in BIST-100 0.4% Relative to BIST-100 (%) -7% -7% -21% -20%

12-m range TL13.25 - TL26.6 Dividend yield (2014E) 0.0% Relative to US$ (%) -23% -24% -35% -47%

75

82

89

96

103

110

10.00

13.00

16.00

19.00

22.00

25.00

28.00

31.00

Dec-12 Feb-13 Apr-13 Jun-13 Aug-13 Oct-13 Dec-13

MGROS vs BIST100 Index

Relative to

BIST 100

19

Source: Company, Global Securities estimates

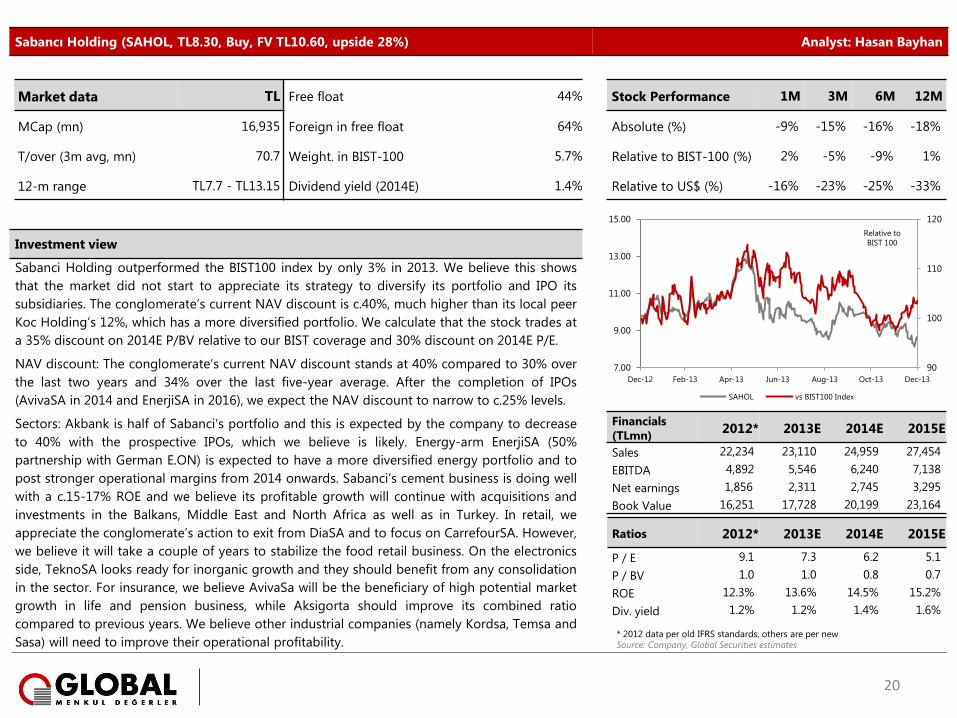

Sabancı Holding (SAHOL, TL8.30, Buy, FV TL10.60, upside 28%) Analyst: Hasan Bayhan

Investment view

Sabanci Holding outperformed the BIST100 index by only 3% in 2013. We believe this shows

that the market did not start to appreciate its strategy to diversify its portfolio and IPO its

subsidiaries. The conglomerate’s current NAV discount is c.40%, much higher than its local peer

Koc Holding’s 12%, which has a more diversified portfolio. We calculate that the stock trades at

a 35% discount on 2014E P/BV relative to our BIST coverage and 30% discount on 2014E P/E.

NAV discount: The conglomerate’s current NAV discount stands at 40% compared to 30% over

the last two years and 34% over the last five-year average. After the completion of IPOs

(AvivaSA in 2014 and EnerjiSA in 2016), we expect the NAV discount to narrow to c.25% levels.

Sectors: Akbank is half of Sabanci’s portfolio and this is expected by the company to decrease

to 40% with the prospective IPOs, which we believe is likely. Energy-arm EnerjiSA (50%

partnership with German E.ON) is expected to have a more diversified energy portfolio and to

post stronger operational margins from 2014 onwards. Sabanci’s cement business is doing well

with a c.15-17% ROE and we believe its profitable growth will continue with acquisitions and

investments in the Balkans, Middle East and North Africa as well as in Turkey. In retail, we

appreciate the conglomerate’s action to exit from DiaSA and to focus on CarrefourSA. However,

we believe it will take a couple of years to stabilize the food retail business. On the electronics

side, TeknoSA looks ready for inorganic growth and they should benefit from any consolidation

in the sector. For insurance, we believe AvivaSa will be the beneficiary of high potential market

growth in life and pension business, while Aksigorta should improve its combined ratio

compared to previous years. We believe other industrial companies (namely Kordsa, Temsa and

Sasa) will need to improve their operational profitability.

Financials

(TLmn) 2012* 2013E 2014E 2015E

Sales 22,234 23,110 24,959 27,454

EBITDA 4,892 5,546 6,240 7,138

Net earnings 1,856 2,311 2,745 3,295

Book Value 16,251 17,728 20,199 23,164

Ratios 2012* 2013E 2014E 2015E

P / E 9.1 7.3 6.2 5.1

P / BV 1.0 1.0 0.8 0.7

ROE 12.3% 13.6% 14.5% 15.2%

Div. yield 1.2% 1.2% 1.4% 1.6%

Market data TL Free float 44% Stock Performance 1M 3M 6M 12M

MCap (mn) 16,935 Foreign in free float 64% Absolute (%) -9% -15% -16% -18%

T/over (3m avg, mn) 70.7 Weight. in BIST-100 5.7% Relative to BIST-100 (%) 2% -5% -9% 1%

12-m range TL7.7 - TL13.15 Dividend yield (2014E) 1.4% Relative to US$ (%) -16% -23% -25% -33%

90

100

110

120

7.00

9.00

11.00

13.00

15.00

Dec-12 Feb-13 Apr-13 Jun-13 Aug-13 Oct-13 Dec-13

SAHOL vs BIST100 Index

Relative to

BIST 100

20

* 2012 data per old IFRS standards, others are per new Source: Company, Global Securities estimates

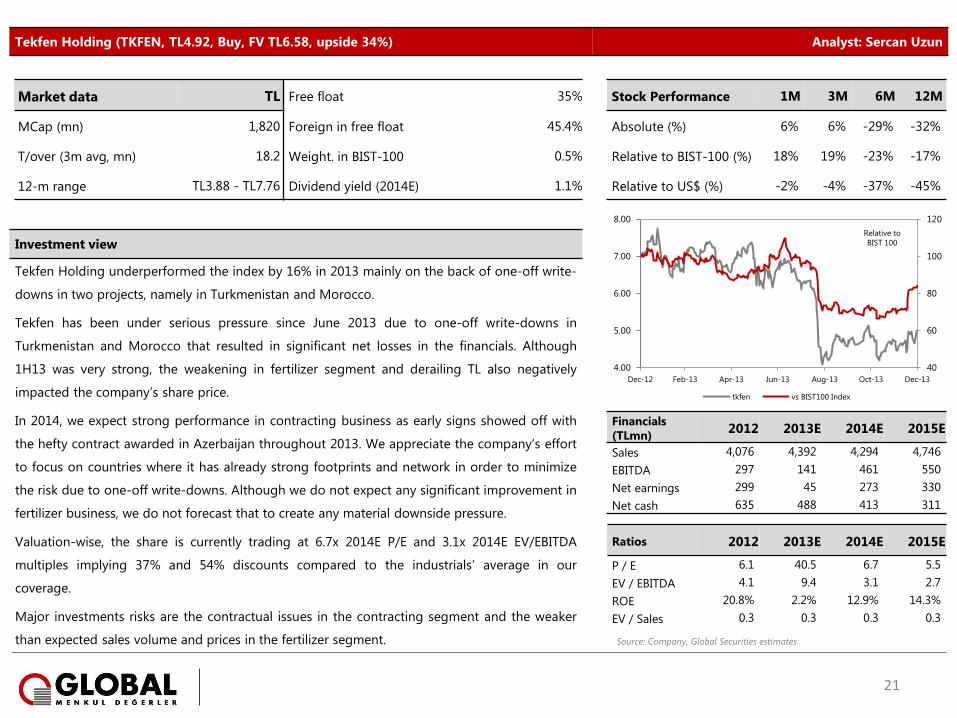

Tekfen Holding (TKFEN, TL4.92, Buy, FV TL6.58, upside 34%) Analyst: Sercan Uzun

Investment view

Tekfen Holding underperformed the index by 16% in 2013 mainly on the back of one-off write-

downs in two projects, namely in Turkmenistan and Morocco.

Tekfen has been under serious pressure since June 2013 due to one-off write-downs in

Turkmenistan and Morocco that resulted in significant net losses in the financials. Although

1H13 was very strong, the weakening in fertilizer segment and derailing TL also negatively

impacted the company’s share price.

In 2014, we expect strong performance in contracting business as early signs showed off with

the hefty contract awarded in Azerbaijan throughout 2013. We appreciate the company’s effort

to focus on countries where it has already strong footprints and network in order to minimize

the risk due to one-off write-downs. Although we do not expect any significant improvement in

fertilizer business, we do not forecast that to create any material downside pressure.

Valuation-wise, the share is currently trading at 6.7x 2014E P/E and 3.1x 2014E EV/EBITDA

multiples implying 37% and 54% discounts compared to the industrials’ average in our

coverage.

Major investments risks are the contractual issues in the contracting segment and the weaker

than expected sales volume and prices in the fertilizer segment.

Financials

(TLmn) 2012 2013E 2014E 2015E

Sales 4,076 4,392 4,294 4,746

EBITDA 297 141 461 550

Net earnings 299 45 273 330

Net cash 635 488 413 311

Ratios 2012 2013E 2014E 2015E

P / E 6.1 40.5 6.7 5.5

EV / EBITDA 4.1 9.4 3.1 2.7

ROE 20.8% 2.2% 12.9% 14.3%

EV / Sales 0.3 0.3 0.3 0.3

Market data TL Free float 35% Stock Performance 1M 3M 6M 12M

MCap (mn) 1,820 Foreign in free float 45.4% Absolute (%) 6% 6% -29% -32%

T/over (3m avg, mn) 18.2 Weight. in BIST-100 0.5% Relative to BIST-100 (%) 18% 19% -23% -17%

12-m range TL3.88 - TL7.76 Dividend yield (2014E) 1.1% Relative to US$ (%) -2% -4% -37% -45%

40

60

80

100

120

4.00

5.00

6.00

7.00

8.00

Dec-12 Feb-13 Apr-13 Jun-13 Aug-13 Oct-13 Dec-13

tkfen vs BIST100 Index

Relative to

BIST 100

21

Source: Company, Global Securities estimates

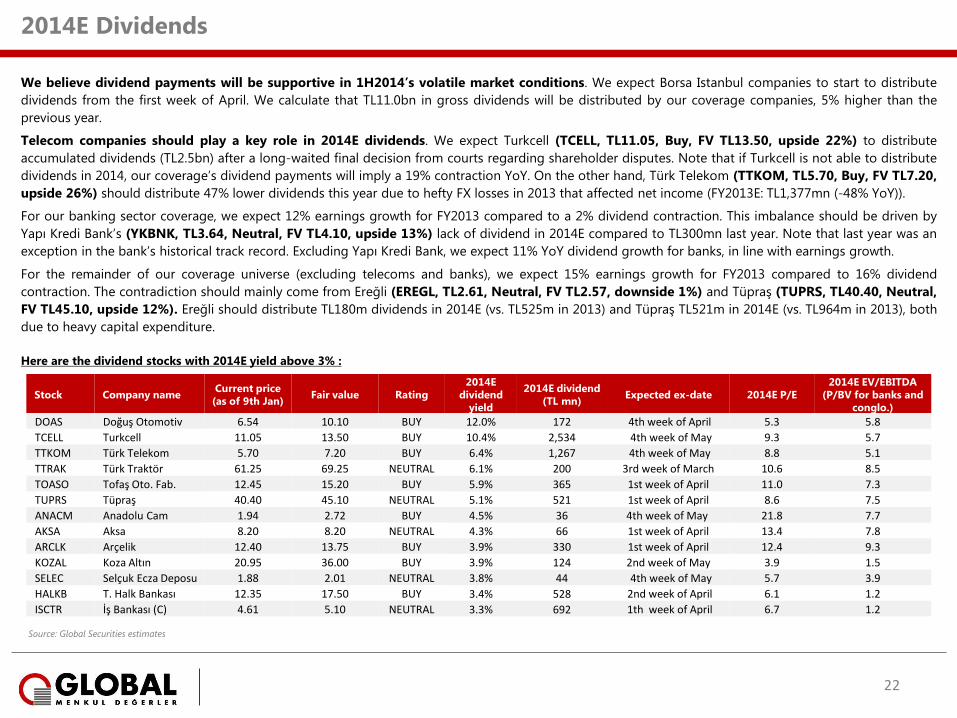

2014E Dividends

We believe dividend payments will be supportive in 1H2014’s volatile market conditions. We expect Borsa Istanbul companies to start to distribute

dividends from the first week of April. We calculate that TL11.0bn in gross dividends will be distributed by our coverage companies, 5% higher than the

previous year.

Telecom companies should play a key role in 2014E dividends. We expect Turkcell (TCELL, TL11.05, Buy, FV TL13.50, upside 22%) to distribute

accumulated dividends (TL2.5bn) after a long-waited final decision from courts regarding shareholder disputes. Note that if Turkcell is not able to distribute

dividends in 2014, our coverage’s dividend payments will imply a 19% contraction YoY. On the other hand, Türk Telekom (TTKOM, TL5.70, Buy, FV TL7.20,

upside 26%) should distribute 47% lower dividends this year due to hefty FX losses in 2013 that affected net income (FY2013E: TL1,377mn (-48% YoY)).

For our banking sector coverage, we expect 12% earnings growth for FY2013 compared to a 2% dividend contraction. This imbalance should be driven by

Yapı Kredi Bank’s (YKBNK, TL3.64, Neutral, FV TL4.10, upside 13%) lack of dividend in 2014E compared to TL300mn last year. Note that last year was an

exception in the bank’s historical track record. Excluding Yapı Kredi Bank, we expect 11% YoY dividend growth for banks, in line with earnings growth.

For the remainder of our coverage universe (excluding telecoms and banks), we expect 15% earnings growth for FY2013 compared to 16% dividend

contraction. The contradiction should mainly come from Ereğli (EREGL, TL2.61, Neutral, FV TL2.57, downside 1%) and Tüpraş (TUPRS, TL40.40, Neutral,

FV TL45.10, upside 12%). Ereğli should distribute TL180m dividends in 2014E (vs. TL525m in 2013) and Tüpraş TL521m in 2014E (vs. TL964m in 2013), both

due to heavy capital expenditure.

Here are the dividend stocks with 2014E yield above 3% :

Stock Company name Current price

(as of 9th Jan) Fair value Rating

2014E

dividend

yield

2014E dividend

(TL mn) Expected ex-date 2014E P/E

2014E EV/EBITDA

(P/BV for banks and

conglo.)

DOAS Doğuş Otomotiv 6.54 10.10 BUY 12.0% 172 4th week of April 5.3 5.8

TCELL Turkcell 11.05 13.50 BUY 10.4% 2,534 4th week of May 9.3 5.7

TTKOM Türk Telekom 5.70 7.20 BUY 6.4% 1,267 4th week of May 8.8 5.1

TTRAK Türk Traktör 61.25 69.25 NEUTRAL 6.1% 200 3rd week of March 10.6 8.5

TOASO Tofaş Oto. Fab. 12.45 15.20 BUY 5.9% 365 1st week of April 11.0 7.3

TUPRS Tüpraş 40.40 45.10 NEUTRAL 5.1% 521 1st week of April 8.6 7.5

ANACM Anadolu Cam 1.94 2.72 BUY 4.5% 36 4th week of May 21.8 7.7

AKSA Aksa 8.20 8.20 NEUTRAL 4.3% 66 1st week of April 13.4 7.8

ARCLK Arçelik 12.40 13.75 BUY 3.9% 330 1st week of April 12.4 9.3

KOZAL Koza Altın 20.95 36.00 BUY 3.9% 124 2nd week of May 3.9 1.5

SELEC Selçuk Ecza Deposu 1.88 2.01 NEUTRAL 3.8% 44 4th week of May 5.7 3.9

HALKB T. Halk Bankası 12.35 17.50 BUY 3.4% 528 2nd week of April 6.1 1.2

ISCTR İş Bankası (C) 4.61 5.10 NEUTRAL 3.3% 692 1th week of April 6.7 1.2

22

Source: Global Securities estimates

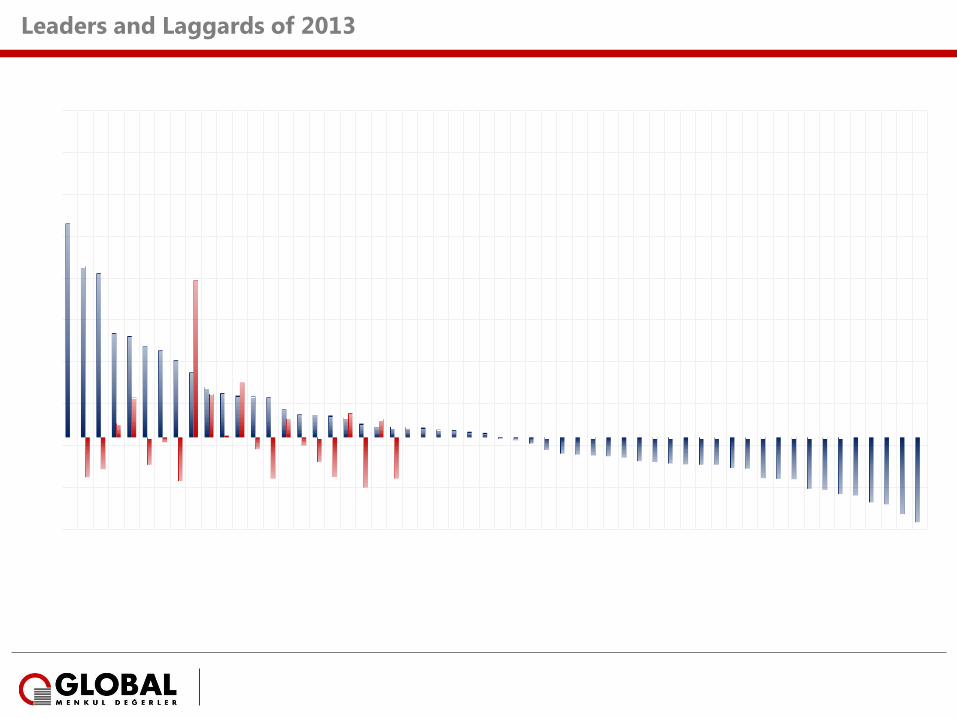

Leaders and Laggards of 2013

Leaders with above 50% relative outperformance to BIST100 index:

Pegasus Airlines’ (PGSUS, TL38.30, Neutral, FV TL35.10, downside 8%) IPO was completed in April 2013 with TL18.40/share price. The stock

closed 2013 with 97% absolute gain outperforming the BIST100 index by 128%. We believe this outperformance was driven by discounted IPO

price. The company explains the “low” price of the IPO three ways: i) an IPO at TRY20.4 was not fulfilled, hence the price was determined at

TRY18.40; ii) Turkish Airlines being the only airline company in Borsa Istanbul trades with lower multiples compared with international peers and

iii) peer LCCs have lower multiples but their growth potential is lower compared with Pegasus’.

Tav Airports (TAVHL, TL15.75,Neutral, FV TL15.60, downside 1%) outperformed the BIST100 index by 102% in 2013. We believe this was

driven by higher operational performance (2013E EBITDA margin: 33% vs. 2012A: 30%), strong €/TL parity and market’s conviction to operate

Istanbul Ataturk Airport till the concession end 2021 (due to possible cancellation or delay of Istanbul’s third airport project).

Aksa Akrilik (AKSA, TL8.20, Neutral, FV TL8.20, upside 0%) outperformed the BIST100 index by 98% in 2013. We believe this remarkable

outperformance was driven by historical high dividend distribution (with 54% pay-out ratio) , continuous acrylic world market leadership and

investors’ belief for the future of carbon fiber business.

Coca-Cola Icecek (CCOLA, TL49.50, Neutral, FV TL56.00, upside 13%) outperformed the index by 62% in 2013, which we believe was due to

solid international sales volume growth and room to increase the market shares in international markets. Solid operations especially in Pakistan

and Iraq may gain momentum in the coming years, moreover new regions may be acquired thanks to strong power of parent company Coca-

Cola that has demographic and geographic competitive advantages.

Tofaş (TOASO, TL12.45, Buy, FV TL15.20, upside 22%) outperformed the index remarkably by 60% in 2013 thanks to its flexibility as an

automotive exporter and domestic player combined with its ability to maintain operating margins in uncertain environments. We recall that

Tofaş had an old-model portfolio which is expected to be renewed in 2-3 years time.

DO & CO (DOCO, TL103, Buy, FV TL124.00, upside 20%) outperformed the BIST100 index by 54% in 2013. We believe this was achieved by

stable operating performance of the company in a competitive business environment (2013E EBITDA margin: 10% vs. 2012A: 10%) and FX hikes

especially in €/TL parity.

Enka Insaat (ENKAI, TL6.54, Neutral, FV TL6.10, downside 7%) outperformed the index by 52% in 2013 and we believe this was owing to its

long FX position, backlog extension and its relatively defensive nature in bearish markets. Enka’s very strong financials throughout 2013 in

contracting and real estate outpaced consensus estimates in each quarter. Enka was once again able to post highest EBITDA margins in

contracting among listed contractors. The company also seems well positioned to benefit from the growing and profitable real estate market in

Russia through its existing and also enlarging office blocks. The stable and predictable nature of the energy business is another positive point for

the company.

Please see page 25 for the leaders and laggards’ graph.

23

Leaders and Laggards of 2013

Laggards with below 30% relative underperformance to BIST100 index:

Koza Anadolu’s (KOZAA, TL2.60, Buy, FV TL4.44, upside 71%) 51% underperformance relative to the BIST100 index can be attributed to the

global fluctuations in the commodity prices, copper combined with gold prices due to its subsidiary Koza Altın. Note that Koza Anadolu’s

underperformance was more or less the same with its subsidiary Koza Altın in 2013.

Anel Elektrik (ANELE, TL1.00, Buy, FV TL1.56, upside 56%) underperformed the index by 46% in 2013 on the back of a weak bottom-line in

financials which we believe were a severe disappointment to investors. Moreover, we believe declining share of foreign investors in its free float

to c.12% from c.40% and lack of company support for the share price through buy-back created a lack of confidence among investors.

Ipek Enerji (IPEKE, TL3.13, Buy, FV TL4.20, upside 34%) was an underperformer in 2013 with a return of 40% below the BIST100 index despite

the heat of the news flow on oil exploration during the year. The company completed first phase of Kozluk Project with the initiation of the

production at Koza-1/K drilling site. We recall that İpek Enerji expects 350 barrels/day oil production (34 API gravity) from the Koza-1/K. Hence,

the underperformance should be related to its subsidiary Koza Anadolu.

Koza Altın (KOZAL, TL20.95, Buy, FV TL36.00, upside 72%) underperformed the BIST100 index by 39% in 2013. We believe this was mainly

due to the global fluctuations in gold prices, while gold was one of the worst performers amongst the commodities with 28% loss in value in

2013. The company initiated production in Himmetdede, a mine with 27mn proven and probable ore reserves and 0.68 g/t average gold grade.

Koza Altın’s EBITDA margin dropped to c70% from c80% as a result of deteriorated gold grades and plunged gold prices.

Aksa Enerji (AKSEN, TL2.42, Buy, FV TL4.00, upside 65%) underperformed the index by 35% in 2013 on the back of weak net earnings,

relatively weaker margins YoY and the discounted block share sale. 2013 has been a turbulent year for Aksa Enerji. The top-line and EBITDA

remained weak as profitable exports were lacking this year given the still on-going tension in Syria. Financials were also disappointing because

of weak demand in Turkey and hence prices in the spot market. Nevertheless, the company has been able to offset the worst thanks to its well

managed procurement in the spot market. However, the company was unable to offset high losses due to its short FX position.

Ayen Enerji (AYEN, TL1.16, Buy, FV TL1.65, upside 42%) underperformed the index by 34% in 2013 on the back of lack of dividends,

diminishing margins and weak bottom-line. 2013’s performance was actually signalled beginning from 4Q12 financials when the company

started to run a volume strategy while exposing itself to spot price volatility. And it did not pay off as the margins of the company declined

significantly.

Celebi Havacilik (CLEBI, TL12.05, Buy, FV TL18.10, upside 50%) underperformed the BIST100 index by 31% in 2013 after 30%

underperformance in 2012. We believe this was driven by weak operational profitability (2013E EBITDA margin: 17%, 2012A: 16% and 2011A:

18% vs. 2010A: 26%) mainly due to weak operations in India and Turkey.

Please see page 25 for the leaders and laggards’ graph.

24

Leaders and Laggards of 2013

-55%

-30%

-05%

20%

45%

70%

95%

120%

145%

170%

195%

PG

SU

S

TA

VH

L

AK

SA

CC

OLA

TO

ASO

DO

CO

EN

KA

I

ER

EG

L

TH

YA

O

TTR

AK

FR

OTO

AR

CLK

TEB

NK

TR

KC

M

BIM

AS

PETK

M

TC

ELL

SIS

E

KC

HO

L

TTK

OM

ALA

RK

AEFES

SELEC

HLG

YO

ALB

RK

ZO

REN

TU

PR

S

SA

HO

L

BIZ

IM

DO

AS

VA

KB

N

PR

KM

E

DO

HO

L

GU

BR

F

AK

BN

K

ISC

TR

GA

RA

N

MG

RO

S

SA

SA

AK

EN

R

TK

FEN

AN

AC

M

YK

BN

K

HA

LK

B

DY

HO

L

ASY

AB

HU

RG

Z

BA

GFS

SN

GY

O

CLEB

I

AY

EN

AK

SEN

KO

ZA

L

IPEK

E

AN

ELE

KO

ZA

A

2013 Relative 2012 Relative Upside to TP

25

Source: Global Securities estimates, Finnet

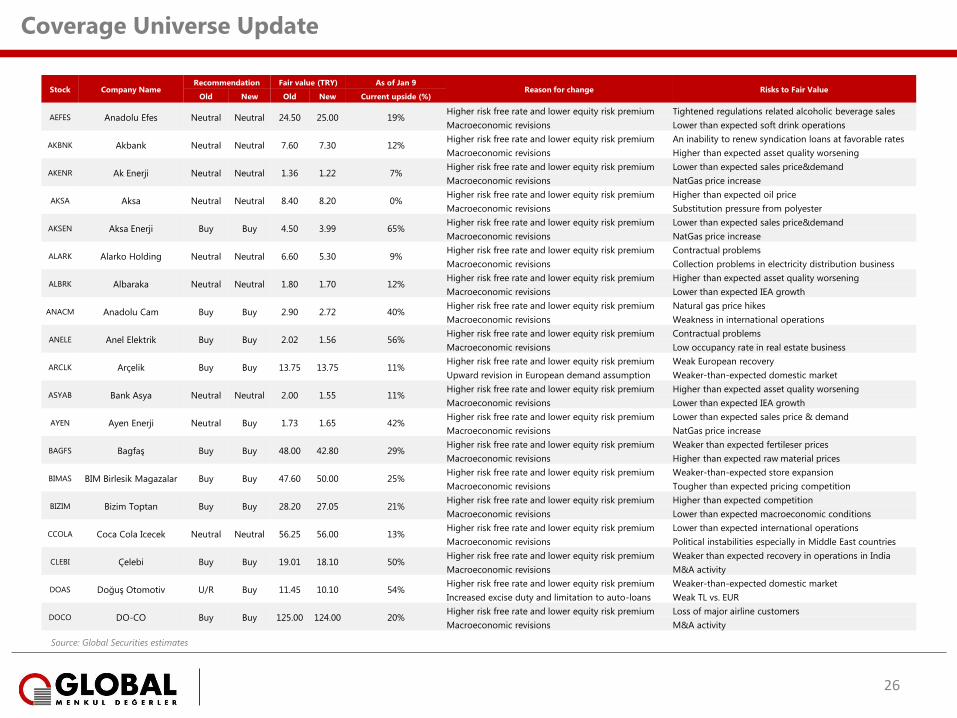

Coverage Universe Update

26

Stock Company Name Recommendation Fair value (TRY) As of Jan 9

Reason for change Risks to Fair Value Old New Old New Current upside (%)

AEFES Anadolu Efes Neutral Neutral 24.50 25.00 19% Higher risk free rate and lower equity risk premium Tightened regulations related alcoholic beverage sales

Macroeconomic revisions Lower than expected soft drink operations

AKBNK Akbank Neutral Neutral 7.60 7.30 12% Higher risk free rate and lower equity risk premium An inability to renew syndication loans at favorable rates

Macroeconomic revisions Higher than expected asset quality worsening

AKENR Ak Enerji Neutral Neutral 1.36 1.22 7% Higher risk free rate and lower equity risk premium Lower than expected sales price&demand

Macroeconomic revisions NatGas price increase

AKSA Aksa Neutral Neutral 8.40 8.20 0% Higher risk free rate and lower equity risk premium Higher than expected oil price

Macroeconomic revisions Substitution pressure from polyester

AKSEN Aksa Enerji Buy Buy 4.50 3.99 65% Higher risk free rate and lower equity risk premium Lower than expected sales price&demand

Macroeconomic revisions NatGas price increase

ALARK Alarko Holding Neutral Neutral 6.60 5.30 9% Higher risk free rate and lower equity risk premium Contractual problems

Macroeconomic revisions Collection problems in electricity distribution business

ALBRK Albaraka Neutral Neutral 1.80 1.70 12% Higher risk free rate and lower equity risk premium Higher than expected asset quality worsening

Macroeconomic revisions Lower than expected IEA growth

ANACM Anadolu Cam Buy Buy 2.90 2.72 40% Higher risk free rate and lower equity risk premium Natural gas price hikes

Macroeconomic revisions Weakness in international operations

ANELE Anel Elektrik Buy Buy 2.02 1.56 56% Higher risk free rate and lower equity risk premium Contractual problems

Macroeconomic revisions Low occupancy rate in real estate business

ARCLK Arçelik Buy Buy 13.75 13.75 11% Higher risk free rate and lower equity risk premium Weak European recovery

Upward revision in European demand assumption Weaker-than-expected domestic market

ASYAB Bank Asya Neutral Neutral 2.00 1.55 11% Higher risk free rate and lower equity risk premium Higher than expected asset quality worsening

Macroeconomic revisions Lower than expected IEA growth

AYEN Ayen Enerji Neutral Buy 1.73 1.65 42% Higher risk free rate and lower equity risk premium Lower than expected sales price & demand

Macroeconomic revisions NatGas price increase

BAGFS Bagfaş Buy Buy 48.00 42.80 29% Higher risk free rate and lower equity risk premium Weaker than expected fertileser prices

Macroeconomic revisions Higher than expected raw material prices

BIMAS BIM Birlesik Magazalar Buy Buy 47.60 50.00 25% Higher risk free rate and lower equity risk premium Weaker-than-expected store expansion

Macroeconomic revisions Tougher than expected pricing competition

BIZIM Bizim Toptan Buy Buy 28.20 27.05 21% Higher risk free rate and lower equity risk premium Higher than expected competition

Macroeconomic revisions Lower than expected macroeconomic conditions

CCOLA Coca Cola Icecek Neutral Neutral 56.25 56.00 13% Higher risk free rate and lower equity risk premium Lower than expected international operations

Macroeconomic revisions Political instabilities especially in Middle East countries

CLEBI Çelebi Buy Buy 19.01 18.10 50% Higher risk free rate and lower equity risk premium Weaker than expected recovery in operations in India

Macroeconomic revisions M&A activity

DOAS Doğuş Otomotiv U/R Buy 11.45 10.10 54% Higher risk free rate and lower equity risk premium Weaker-than-expected domestic market

Increased excise duty and limitation to auto-loans Weak TL vs. EUR

DOCO DO-CO Buy Buy 125.00 124.00 20% Higher risk free rate and lower equity risk premium Loss of major airline customers

Macroeconomic revisions M&A activity

Source: Global Securities estimates

Coverage Universe Update

27

Stock Company Name Recommendation Fair value (TRY) As of Jan 9

Reason for change Risks to Fair Value Old New Old New Current upside (%)

DOHOL Doğan Holding Buy Buy 1.05 1.05 40% Higher risk free rate and lower equity risk premium Fail to grow inorganically

Aslancık HEPP to be operational in coming quarters Failure of energy investments to generate cash

DYHOL Doğan Yayın Holding Neutral Neutral 0.74 0.74 32% Higher risk free rate and lower equity risk premium Weak TL vs. USD

Cash injection from the parent to pay the debt Weaker-than-expected D-Smart growth

ENKAI Enka İnşaat Neutral Neutral 6.04 6.10 -7% Higher risk free rate and lower equity risk premium Contractual problems

Macroeconomic revisions Weak Russian real estate market

EREGL Ereğli Demir Çelik Neutral Neutral 2.90 2.57 -1% Higher risk free rate and lower equity risk premium Higher raw material & weak finished product prices

Macroeconomic revisions Weak demand from main export markets

FROTO Ford Otosan U/R Buy 23.00 29.90 33% Higher risk free rate and lower equity risk premium Weak European recovery

Upward revision in European demand assumption Weaker-than-expected domestic market

GARAN Garanti bank Buy Buy 9.50 8.60 29% Higher risk free rate and lower equity risk premium An inability to renew syndication loans at favorable rates

Macroeconomic revisions Higher than expected asset quality worsening

GUBRF Gübre Fabrik. Buy Buy 4.63 4.20 46% Higher risk free rate and lower equity risk premium Weaker than expected fertilizer prices

Macroeconomic revisions Higher than expected raw material prices

HALKB Halk Bank Buy Buy 20.10 17.50 42% Higher risk free rate and lower equity risk premium Higher than expected asset quality worsening

Macroeconomic revisions Higher than expected NIM worsening

HLGYO Halk GMYO Buy Buy 1.81 1.81 51% Higher risk free rate and lower equity risk premium Lower than expected sales price & demand

Macroeconomic revisions Delay in investments

HURGZ Hürriyet Gazetecilik Neutral Neutral 0.80 0.80 33% Higher risk free rate and lower equity risk premium Lower-than-expected growth in online segment

Decent performance of online segment Slowdown in Russia to continue

IPEKE İpek Doğal Enerji U/R Buy 4.20 4.20 34% Higher risk free rate and lower equity risk premium Disappointments from the oil exploration

Initiation of oil production Legal challenges

ISCTR İşbank Neutral Neutral 5.50 5.10 11% Higher risk free rate and lower equity risk premium An inability to renew syndication loans at favorable rates

Macroeconomic revisions Higher than expected asset quality worsening

KCHOL Koç Holding Neutral Neutral 9.70 9.60 12% Higher risk free rate and lower equity risk premium Lower than expected Turkish GDP growth

Changes in subsidiaries FV Lower than expected recovery in Europe

KOZAA Koza Anadolu Buy Buy 4.44 4.44 71% Higher risk free rate and lower equity risk premium Poor copper prices

Upward revision in copper grade Lower copper grade production

KOZAL Koza Altın U/R Buy 35.00 36.00 72% Higher risk free rate and lower equity risk premium Poor gold prices

Upward revision in gold grade Lower gold grade production

MGROS Migros Ticaret Buy Buy 21.50 20.85 42% Higher risk free rate and lower equity risk premium Weaker-than-expected store expansion

Macroeconomic revisions Higher than expected competition

PETKM Petkim Neutral Neutral 3.15 3.10 17% Higher risk free rate and lower equity risk premium Higher than expected oil prices

Macroeconomic revisions Lower than expected petrochemical prices

PGSUS Pegasus Sell Neutral 35.10 35.10 -8% Higher risk free rate and lower equity risk premium Higher than expected oil prices

Macroeconomic revisions Lower than expected Turkish aviation growth

PRKME Park Elektrik Buy Buy 7.50 6.40 26% Higher risk free rate and lower equity risk premium Poor copper prices

Transfer of asphaltite shares Lower copper grade levels due to the open-pit transition

Source: Global Securities estimates

Coverage Universe Update

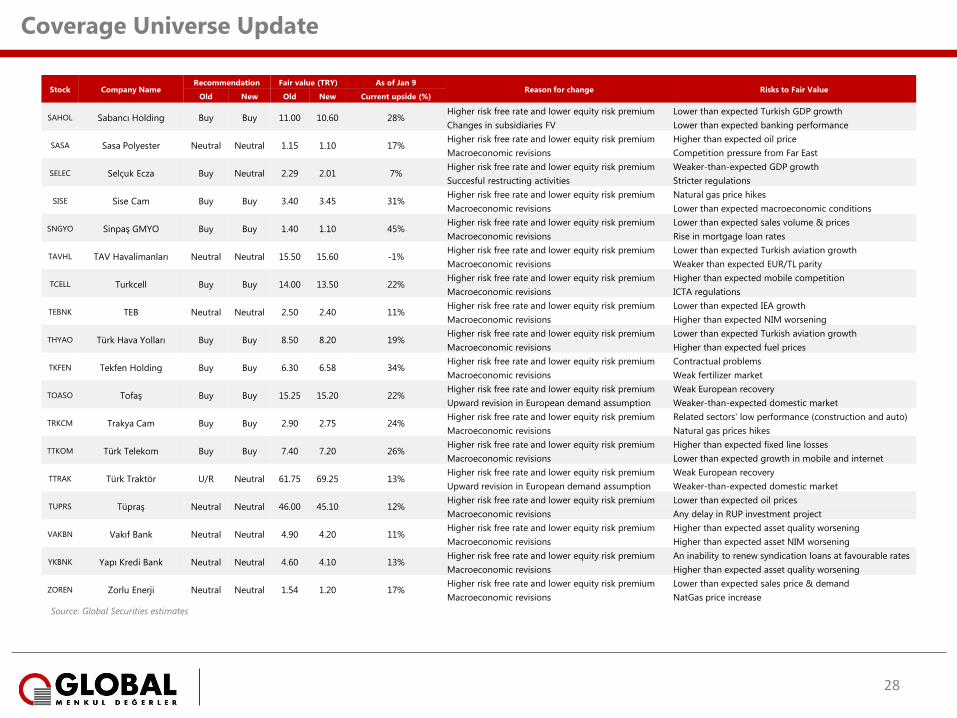

28

Stock Company Name Recommendation Fair value (TRY) As of Jan 9

Reason for change Risks to Fair Value Old New Old New Current upside (%)

SAHOL Sabancı Holding Buy Buy 11.00 10.60 28% Higher risk free rate and lower equity risk premium Lower than expected Turkish GDP growth

Changes in subsidiaries FV Lower than expected banking performance

SASA Sasa Polyester Neutral Neutral 1.15 1.10 17% Higher risk free rate and lower equity risk premium Higher than expected oil price

Macroeconomic revisions Competition pressure from Far East

SELEC Selçuk Ecza Buy Neutral 2.29 2.01 7% Higher risk free rate and lower equity risk premium Weaker-than-expected GDP growth

Succesful restructing activities Stricter regulations

SISE Sise Cam Buy Buy 3.40 3.45 31% Higher risk free rate and lower equity risk premium Natural gas price hikes

Macroeconomic revisions Lower than expected macroeconomic conditions

SNGYO Sinpaş GMYO Buy Buy 1.40 1.10 45% Higher risk free rate and lower equity risk premium Lower than expected sales volume & prices

Macroeconomic revisions Rise in mortgage loan rates

TAVHL TAV Havalimanları Neutral Neutral 15.50 15.60 -1% Higher risk free rate and lower equity risk premium Lower than expected Turkish aviation growth

Macroeconomic revisions Weaker than expected EUR/TL parity

TCELL Turkcell Buy Buy 14.00 13.50 22% Higher risk free rate and lower equity risk premium Higher than expected mobile competition

Macroeconomic revisions ICTA regulations

TEBNK TEB Neutral Neutral 2.50 2.40 11% Higher risk free rate and lower equity risk premium Lower than expected IEA growth

Macroeconomic revisions Higher than expected NIM worsening

THYAO Türk Hava Yolları Buy Buy 8.50 8.20 19% Higher risk free rate and lower equity risk premium Lower than expected Turkish aviation growth

Macroeconomic revisions Higher than expected fuel prices

TKFEN Tekfen Holding Buy Buy 6.30 6.58 34% Higher risk free rate and lower equity risk premium Contractual problems

Macroeconomic revisions Weak fertilizer market

TOASO Tofaş Buy Buy 15.25 15.20 22% Higher risk free rate and lower equity risk premium Weak European recovery

Upward revision in European demand assumption Weaker-than-expected domestic market

TRKCM Trakya Cam Buy Buy 2.90 2.75 24% Higher risk free rate and lower equity risk premium Related sectors' low performance (construction and auto)

Macroeconomic revisions Natural gas prices hikes

TTKOM Türk Telekom Buy Buy 7.40 7.20 26% Higher risk free rate and lower equity risk premium Higher than expected fixed line losses

Macroeconomic revisions Lower than expected growth in mobile and internet

TTRAK Türk Traktör U/R Neutral 61.75 69.25 13% Higher risk free rate and lower equity risk premium Weak European recovery

Upward revision in European demand assumption Weaker-than-expected domestic market

TUPRS Tüpraş Neutral Neutral 46.00 45.10 12% Higher risk free rate and lower equity risk premium Lower than expected oil prices

Macroeconomic revisions Any delay in RUP investment project

VAKBN Vakıf Bank Neutral Neutral 4.90 4.20 11% Higher risk free rate and lower equity risk premium Higher than expected asset quality worsening

Macroeconomic revisions Higher than expected asset NIM worsening

YKBNK Yapı Kredi Bank Neutral Neutral 4.60 4.10 13% Higher risk free rate and lower equity risk premium An inability to renew syndication loans at favourable rates

Macroeconomic revisions Higher than expected asset quality worsening

ZOREN Zorlu Enerji Neutral Neutral 1.54 1.20 17% Higher risk free rate and lower equity risk premium Lower than expected sales price & demand

Macroeconomic revisions NatGas price increase

Source: Global Securities estimates

BASIS FOR RECOMMENDATIONS

12-MONTH RATING DEFINITION

BUY: Analyst expects at least 10% upside potential to fair value, which should be realized in

the next 12 months

NEUTRAL: Analyst expects upside/downside potential of between +10% and -10% to fair

value, which should be realized in the next 12 months

SELL: Analyst expects at least 10% downside potential to fair value, which should be

realized in the next 12 months

TRADING RATING DEFINITION

TRADING BUY: Analyst expects a positive short-term movement in the share price (max

duration 2 months from the time Trading Buy is announced) and may move out of line with

the fair value estimate during that period.

TRADING SELL: Analyst expects a negative short-term movement in the share price (max

duration 2 months from time Trading Sell is announced) and may move out of line with the

fair value estimate during that period.

ANALYST CERTIFICATION

We, Global research team, hereby certify that the views expressed in this research report

accurately reflect my personal views about the subject securities and issuers. I also certify

that no part of my compensation was, is, or will be, directly or indirectly, related to the

specific recommendations or view expressed in this research report.

IMPORTANT DISCLOSURE INFORMATION

This material was produced by Global Menkul Değerler A.Ş. (“GMD”) or its Affiliates, solely

for information purposes and for the use of the recipient. It is not to be reproduced under

any circumstances and is not to be copied or made available to any person other than the

recipient. It is distributed in the world by GMD or an authorised affiliate of GMD (such

entities and any other entity, directly or indirectly, controlled by GMD, the “Affiliates”). This

document does not constitute an offer of, or an invitation by or on behalf of GMD or its

Affiliates or any other company to any person, to buy or sell any security. The information

contained herein has been obtained from published information and other sources which

GMD or its Affiliates consider to be reliable.

None of GMD or its Affiliates accepts any liability or responsibility whatsoever for the

accuracy or completeness of any such information. All estimates, expressions of opinion and

other subjective judgments contained herein are made as of the date of this document.

Emerging securities markets may be subject to risks significantly higher than more

established markets. In particular, the political and economic environment, company

practices and market prices and volumes may be subject to significant variations. The ability

to assess such risks may also be limited due to significantly lower information quantity and

quality. By accepting this document, you agree to be bound by all the foregoing provisions.

GMD or its Affiliates have not recently been the beneficial owners of 1% or more of the

securities mentioned in this report; GMD or its affiliates have not managed or co-managed a

public offering of these securities, or received compensation for investment banking services

from the issuer of these securities in the past 12 months and do not expect to receive

compensation for investment banking services from the issuer of these securities within the

next three months. However, one or more of GMD or its Affiliates may, from time to time,

have a long or short position in any of the securities mentioned herein and may buy or sell

those securities or options thereon either on their own account or on behalf of their clients.

GMD or its Affiliates may, to the extent permitted by law, act upon or use the above material

or the conclusions stated above or the research or analysis on which they are based before

the material is published to recipients and from time to time provide investment banking,

investment management or other services for or solicit to seek to obtain investment

banking, or other securities business from, any entity referred to in this report.

© 2014 Global Menkul Degerler A.Ş.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval

system, or transmitted in any form or by any means, electronic, mechanical, photocopying,

recording, or otherwise, without the prior consent of Global Menkul Değerler A.Ş.

strategic partner of