2014 Predictions for Telecommunications Services in Latin America

22

2014 Predictions for Telecommunications 2014 Predictions for Telecommunications Services in Latin America Services in Latin America Regulatory, Regulatory, technological technological and competitive trends that will impact the and competitive trends that will impact the market in market in 2014 2014 Renato Pasquini, Industry Manager Information & Communication Information & Communication Technologies January 14, 2014 © 2014 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

-

Upload

frost-sullivan -

Category

Technology

-

view

1.774 -

download

1

Transcript of 2014 Predictions for Telecommunications Services in Latin America

2014 Predictions for Telecommunications 2014 Predictions for Telecommunications Services in Latin AmericaServices in Latin America

Regulatory, Regulatory, technological technological and competitive trends that will impact the and competitive trends that will impact the market in market in 2014 2014

Renato Pasquini, Industry Manager Information & Communication Information & Communication

Technologies

January 14, 2014

© 2014 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of

Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

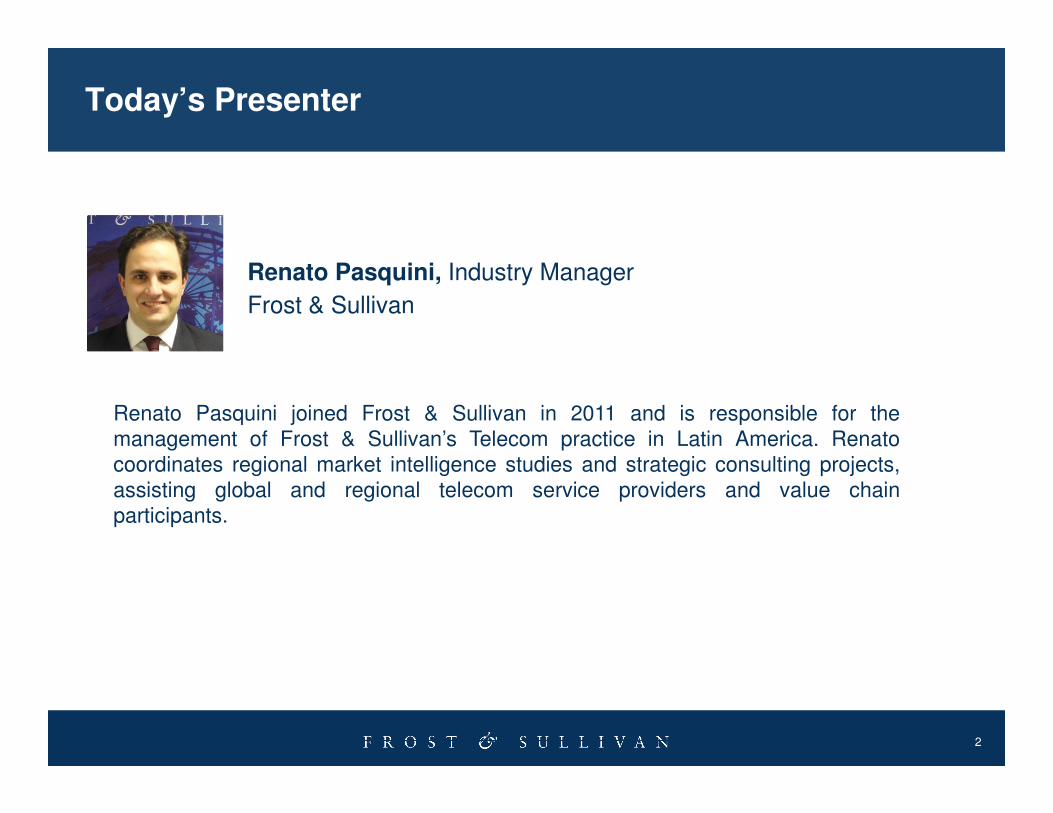

Today’s Presenter

Renato Pasquini, Industry Manager

Frost & Sullivan

Renato Pasquini joined Frost & Sullivan in 2011 and is responsible for the

2

Renato Pasquini joined Frost & Sullivan in 2011 and is responsible for the

management of Frost & Sullivan’s Telecom practice in Latin America. Renato

coordinates regional market intelligence studies and strategic consulting projects,

assisting global and regional telecom service providers and value chain

participants.

Occasion for the Analyst Briefing

• The roll-out of ultra broadband and LTE

networks in several Latin American countries in 2013 and the development of new business models by Telcos will add

value for customers and enterprises from

different verticals.

3

• This briefing will underline Frost &

Sullivan's key predictions for 2014,

focusing on the implications of the competitive landscape as companies surf

the trend of new service and application

opportunities.

2014 Predictions

• Mobile payment will become an alternative to peer-to-peer transactions and paying bills in cash and on-site, as well as payments at point-of-sale (POS) terminals. This is especially true for the lower-income population.

• For payments at POS, and also for use in public transport and other services, Latin America is likely to see in 2014 the launch of several Near-Field Communication (NFC) initiatives, as awareness of the technology begins to grow towards major adoption in the

Prediction #1: Consumers will begin to adopt mobile wallets for uses other than paying at point-of-sale

1. Mobile Payment

3. Non-linear pay TV

services

4. Carrier Wi-Fi 5. FTTH2. Satellite Broadband

6. M2M services

7. LTE2014 LATAM Telecom Trends

5

Source: Frost & Sullivan analysis

initiatives, as awareness of the technology begins to grow towards major adoption in the future.

• Adoption will be driven mainly by a member-get-member process, in addition to the marketing efforts of mobile payment companies.

• Regulations and guidelines are expected to be put in place, encouraging future investments in mobile payment.

The provision of financial services to the unbanked population, including peer-to-peer micro transactions, in a secure and convenient way for a population that uses cash frequently and/or pays bills in person, is

an opportunity for carriers and other market players to increase revenues.

Prediction #1: Consumers will begin to adopt mobile wallets for uses other than paying at point-of-sale (cont.)

1. Mobile Payment

3. Non-linear pay TV

services

4. Carrier Wi-Fi 5. FTTH2. Satellite Broadband

6. M2M services

7. LTE2014 LATAM Telecom Trends

1.6

(Mil

lio

n)

Mobile Payment Market: Registered Users Forecast, Brazil, 2012-2014

CAGR = 73.2%2014 yoy growth = 87.5%

6

Source: Frost & Sullivan analysis

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

2012 2013 2014

Registered Users 0.5 0.8 1.5

Reg

iste

red

users

(M

illi

on

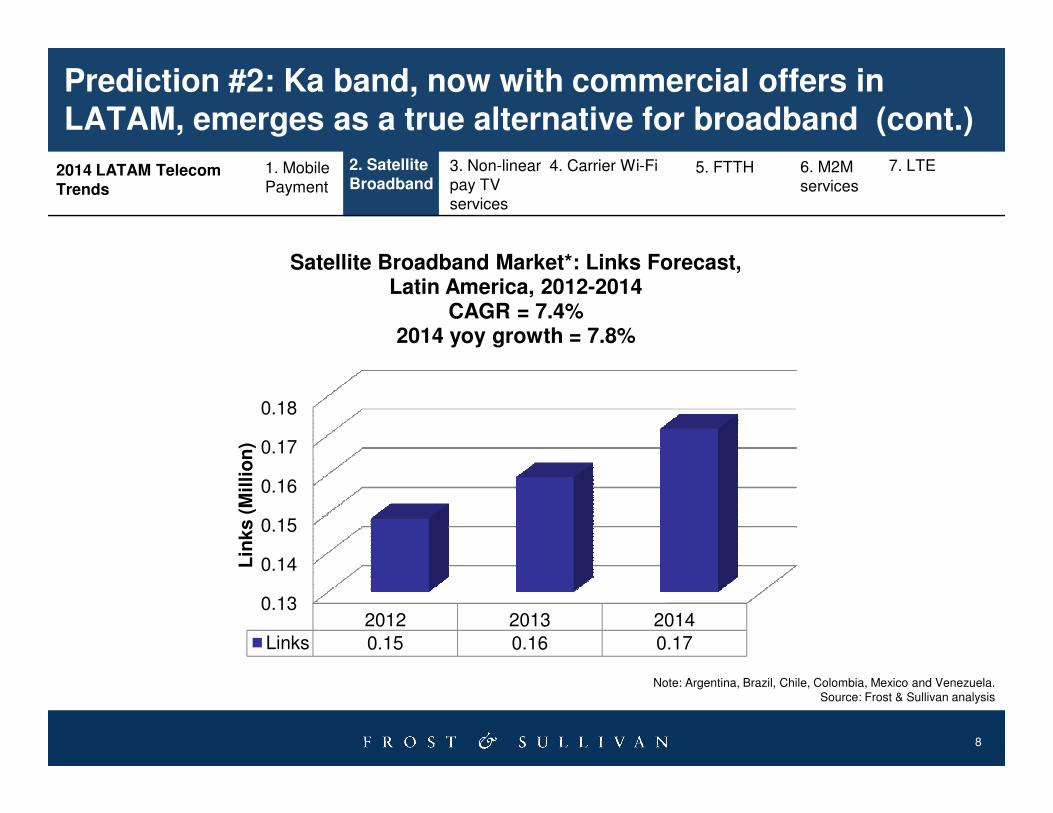

Prediction #2: Ka band, now with commercial offers in LATAM, emerges as a true alternative for broadband

2014 LATAM Telecom Trends

1. Mobile Payment

3. Non-linear pay TV services

4. Carrier Wi-FI 5. FTTH2. Satellite Broadband

6. M2M

services

7. LTE

• The launching of Hispasat’s Amazonas 3 satellite in February 2013 provided Latin America with its first Ka-band payload. The nine spot beams cover the region’s main metropolitan areas and are operated by Telefónica’s Media Networks.

• Contrary to initial speculation, operators have chosen to focus Ka-band broadband coverage on metropolitan areas as opposed to rural regions. Other applications include corporate VSAT services and airlines looking to provide in-flight Wi-Fi connectivity, as well as high-definition DTH Pay.

• Satellite M2M may also emerge in Latin America, enabling cars and other machines to connect to

7

Source: Frost & Sullivan analysis

The emergence of Ka-band services in Latin America is expected to increase the penetration of satellite technologies in the total broadband market in the region.

• Satellite M2M may also emerge in Latin America, enabling cars and other machines to connect to the Internet.

Prediction #2: Ka band, now with commercial offers in LATAM, emerges as a true alternative for broadband (cont.)

2014 LATAM Telecom Trends

1. Mobile Payment

3. Non-linear pay TV services

4. Carrier Wi-Fi 5. FTTH2. Satellite Broadband

6. M2M

services

7. LTE

0.18

Satellite Broadband Market*: Links Forecast, Latin America, 2012-2014

CAGR = 7.4%2014 yoy growth = 7.8%

8

Note: Argentina, Brazil, Chile, Colombia, Mexico and Venezuela.Source: Frost & Sullivan analysis

0.13

0.14

0.15

0.16

0.17

0.18

2012 2013 2014

Links 0.15 0.16 0.17

Lin

ks (

Mil

lio

n)

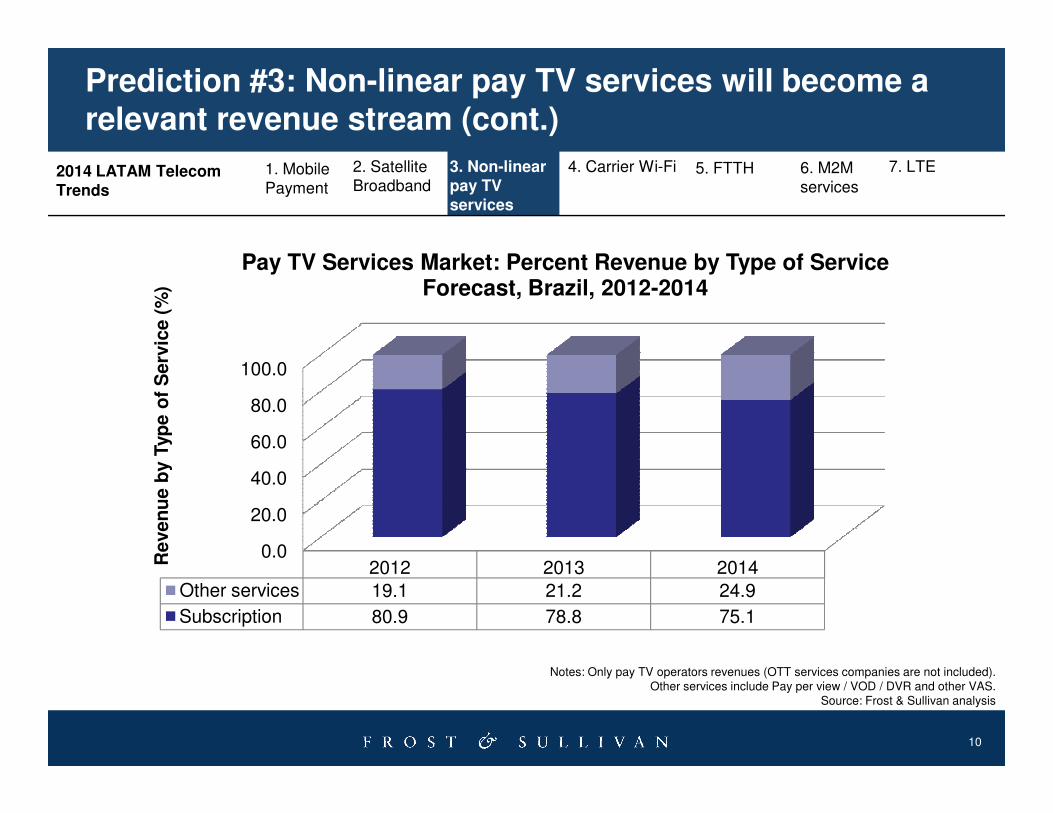

Prediction #3: Non-linear pay TV services will become a relevant revenue stream

• As smart devices grow to represent the majority of shipments, and broadband becomes widely available, the demand for Over-the-Top (OTT) services and non-linear Pay TV services increases to the highest level ever.

• OTT service providers, such as Netflix, are the ones that most benefit from this trend currently. However, traditional Pay TV service providers are also expected to benefit, as video on demand (VoD), niche content

2014 LATAM Telecom Trends

1. Mobile

Payment

3. Non-linear pay TV services

4. Carrier Wi-Fi 5. FTTH2. Satellite

Broadband6. M2M services

7. LTE

9

New customer behavior, broadband deployment and the adoption of smart devices drive the increase of non-linear Pay TV services in Latin America.

Source: Frost & Sullivan analysis

expected to benefit, as video on demand (VoD), niche content subscriptions, pay-per-view (PPV), digital video recording (DVR) and other services increase adoption. Telcos also look to include OTT applications in their set-top boxes, through revenue share agreements.

• Content Delivery Network (CDN) services in Latin America, provided by companies such as Akamai and Level 3, are expected to grow 17.4% in terms of revenues in 2014, pushed by this demand of video streaming and on demand applications.

Prediction #3: Non-linear pay TV services will become a relevant revenue stream (cont.)

2014 LATAM Telecom Trends

1. Mobile

Payment

3. Non-linear pay TV services

4. Carrier Wi-Fi 5. FTTH2. Satellite

Broadband6. M2M services

7. LTE

80.0

100.0

Reven

ue b

y T

yp

e o

f S

erv

ice (

%)

Pay TV Services Market: Percent Revenue by Type of Service Forecast, Brazil, 2012-2014

10

Notes: Only pay TV operators revenues (OTT services companies are not included). Other services include Pay per view / VOD / DVR and other VAS.

Source: Frost & Sullivan analysis

0.0

20.0

40.0

60.0

80.0

2012 2013 2014

Other services 19.1 21.2 24.9

Subscription 80.9 78.8 75.1

Reven

ue b

y T

yp

e o

f S

erv

ice (

%)

Prediction #4: The World Cup will drive Telco investments in Wi-Fi

• Since the beginning of 2012, carrier Wi-Fi deployment in Brazil has grown nearly tenfold, reaching close to 500,000 hotspots in the fourth quarter of 2013. In other Latin American markets, Wi-Fi roll-out has been slower, but is also a trend among both governments and Telcos.

• Brazil’s rapid growth was led by Oi due to its partnership with Spanish “homespot” company Fon. These Fon homespots represent 97.4% of Brazil’s 426,455 hotspots. The business model, which looks to leverage telcos’ existing broadband customers to

2014 LATAM Telecom Trends

1. Mobile Payment

3. Non-linear pay TV services

4. Carrier Wi-Fi 5. FTTH2. Satellite

Broadband6. M2M services

7. LTE

11

Source: Frost & Sullivan analysis

Mobile broadband growth pushes carriers to offloading strategies, while ISPs look to add value to fixed broadband offers.

The business model, which looks to leverage telcos’ existing broadband customers to expand their Wi-Fi footprint at a lower cost, is a growing trend globally.

• So far, carriers’ Wi-Fi strategies have focused on mobile data offloading, offering public Wi-Fi access on a freemium basis to existing mobile and fixed broadband subscribers.

• For 2014, Wi-Fi hotspot growth is expected to accelerate as Telcos prepare to boost coverage in World Cup cities and other carriers begin deploying homespots of their own.

Prediction #4: The World Cup will drive Telco investments in Wi-Fi (cont.)

2014 LATAM Telecom Trends

1. Mobile Payment

3. Non-linear pay TV services

4. Carrier Wi-Fi 5. FTTH2. Satellite

Broadband6. M2M services

7. LTE

1000

Ho

tsp

ots

(T

ho

usan

d)

Carrier Wi-Fi Market: Hotspot Forecast, Brazil, 2012–2014CAGR = 434.6%

2014 yoy growth = 93.2%

12

Source: Frost & Sullivan analysis

0

200

400

600

800

2012 2013 2014

Commercial Hotspots 6.5 12.0 17.6

Community Hotspots 28.0 497.8 967.6

Ho

tsp

ots

(T

ho

usan

d)

Prediction #5: Consumer migration to fiber networks to accelerate as carriers reduce prices

• Latin America had more than 40 projects of FTTH by 2012, with 5.2 million homes passed*.

• In 2014, it is expected that more projects will be developed by regional competitors, competing with Incumbents.

2014 LATAM Telecom Trends

1. Mobile Payment

3. Non-linear pay TV services

4. Carrier Wi-Fi 5. FTTH2. Satellite Broadband

6. M2M services

7. LTE

13

Mexico will continue to be the largest FTTH market in 2014, followed by Brazil, due to the competition of large Telecom Groups with FTTH networks

Source: Frost & Sullivan analysis

• In addition, as FTTH is decreasing the cost to deploy (resulting in price decline for end-users also), and is likely to become the main ultra broadband alternative for Incumbents and other large competitors.

• Prices are still relatively high, but competition and bundling are expected to erode them in the short term, making at least entry-level plans accessible for more people (>=20Mbps).

*Source: IDATE for FTTH Council LATAM Chapter

Prediction #5: Consumer migration to fiber networks to accelerate as carriers reduce prices (cont.)

2014 LATAM Telecom Trends

1. Mobile Payment

3. Non-linear pay TV services

4. Carrier Wi-Fi 5. FTTH2. Satellite Broadband

6. M2M services

7. LTE

1.4

Lin

es in

Serv

ice (

Mil

lio

n)

FTTH Services Market*: LIS Forecast, Latin America, 2012–2014

CAGR = 41.4%2014 yoy growth = 40.0%

14

*Argentina, Brazil, Chile and MexicoSource: Frost & Sullivan analysis

0

0.2

0.4

0.6

0.8

1

1.2

1.4

2012 2013 2014LIS 0.7 1.0 1.4

Lin

es in

Serv

ice (

Mil

lio

n)

Prediction #6: Service providers will race to position themselves in M2M services

• Telefónica and America Móvil, market leaders in Latin America, will see the emergence of stronger competitors, such as Vodafone and Verizon, expanding their global M2M capabilities to the region.

• To differentiate services and not limit themselves to mere connectivity providers, carriers look to cloud services to enhance user experience with real time management, lifecycle management, reports and alarms.

2014 LATAM Telecom Trends

1. Mobile

Payment

3. Non-linear pay TV services

4. Carrier Wi-Fi 5. FTTH2. Satellite Broadband

6. M2M services

7. LTE

15

Traditional mobile operators as well as niche M2M providers are implementing strategies aimed at capturing emerging deals as well as positioning themselves for future growth.

Source: Frost & Sullivan analysis

lifecycle management, reports and alarms.

• Another trend is a focus on specific verticals to become the pioneer/leader in practices such as m-health, transportation, security, utilities and financial services.

• Specialized providers and MVNOs working on niche M2M solutions are also expanding, such as the insurance company Porto Seguro, and new commercial operations may emerge during 2014.

Prediction #6: Service providers will race to position themselves in M2M services (cont.)

2014 LATAM Telecom Trends

1. Mobile

Payment

3. Non-linear pay TV services

4. Carrier Wi-Fi 5. FTTH2. Satellite Broadband

6. M2M services

7. LTE

16.0

(Mil

lio

n)

M2M Services Market*: LIS Forecast, Latin America, 2013-2014

2014 yoy growth = 24.0%

16

*Argentina, Brazil, Chile, Colombia, Mexico and PeruSource: Frost & Sullivan analysis

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2013 2014

LIS 12.9 16.0

Lin

es in

Serv

ice (

Mil

lio

n)

Prediction #7: LTE will gain relevance in the Latin American mobile market

• During 2012 and 2013, some of Latin America’s largest carriers launched high speed LTE mobile broadband networks, and in 2014, we expect to see 4G services gain track in Latin America’s largest economies, as more devices become available at cheaper prices.

• LTE is also expected to drive regulatory discussions as many countries are planning to auction the coveted 700 MHz spectrum frequency, considered more appropriate for

2014 LATAM Telecom Trends

1. Mobile

Payment

3. Non-linear pay Tv

services

4. Carrier Wi-Fi 5. FTTH2. Satellite Broadband

6. M2M

services7. LTE

17

The adoption of LTE is also expected to help drive the OTT market, both for telcos and independent services.

Source: Frost & Sullivan analysis

to auction the coveted 700 MHz spectrum frequency, considered more appropriate for 4G services due to its wide range and improved indoor coverage. Currently, most Latin American countries operate LTE networks on higher and less efficient frequencies.

• It’s expected that with the evolution of 4G networks and Wi-Fi hotspots, the experience with cloud services will enhance and this will allow the development of more advanced services, including video.

Prediction #7: LTE will gain relevance in the Latin American mobile market (cont.)

2014 LATAM Telecom Trends

1. Mobile

Payment

3. Non-linear pay TV services

4. Carrier Wi-Fi 5. FTTH2. Satellite Broadband

6. M2M services

8.00

LTE*: LIS Forecast, Latin America, 2012-2014

CAGR = 1081.9%2014 yoy growth = 292.0%

7. LTE6. M2M services

18

*Brazil, Chile, Colombia, Mexico and PeruSource: Frost & Sullivan analysis

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

2012 2013 2014

LIS 0.06 2.0 7.9

LIS

(M

illi

on

)

1. Innovative services will require important investments in networks and

platforms. How will companies guarantee an interesting ROI?

2. Will the consumer’s learning curve keep up to the speed of implementation

of new technologies? How to educate users in that matter?

CONCLUSION: Latin America continues with the trend of enablingconnectivity. However, there are still many challenges to be addressed:

19

4. How will governments address regulation issues with new technologies in a

transparent and effective way? How will they stimulate the national industry?

3. How will companies maintain their core business whilst expanding, exploring

and adapting to new realities and markets?

Source: Frost & Sullivan analysis

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

What would you like to see from Frost & Sullivan?

20

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation.

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

21

http://twitter.com/Frost_Latam

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

For Additional Information

Francesca Valente

Marketing & Corporate

Communications Executive

(54) 4777-5300

Renato Pasquini

Industry Manager – Latin America

Information & Communication Technologies

(55) 11-3065-8433

22

Jose Roberto Mavignier

Research Director – Latin America

Information & Communication Technologies

(55) 11-3065-8463

Antonio Carlos Tarjan

Account Executive

(55) 11-3065-8428