2014 National Survey of Technology, Policy and Strategic Issues © 2014 Technology Councils of...

32

2014 National Survey of Technology, Policy and Strategic Issues w w w . t e c h n o l o g y c o u n c i l s . o r g © 2014 Technology Councils of North America. All rights reserved. Results for: Chattanooga & Nashville Technology Councils

-

Upload

philip-cobb -

Category

Documents

-

view

214 -

download

0

Transcript of 2014 National Survey of Technology, Policy and Strategic Issues © 2014 Technology Councils of...

2014 National Survey of Technology, Policy and Strategic Issues

ww

w.t

ec

hn

olo

gy

co

un

cils

.org

© 2014 Technology Councils of North America. All rights reserved.

Results for: Chattanooga & Nashville Technology Councils

About TECNA | CompTIA | TechAmerica

About TECNAThe Technology Councils of North America (TECNA) represents almost 50+ IT and Technology trade organizations who, in turn, represent more than 22,000 technology-related companies in North America. TECNA serves its members and the industry through its strong peer-to-peer network and its regional initiatives to raise the visibility and viability of the technology industry.

About CompTIACompTIA is the voice of the world’s information technology (IT) industry. Its members are the companies at the forefront of innovation; and the professionals responsible for maximizing the benefits organizations receive from their investments in technology. CompTIA is dedicated to advancing industry growth through its educational programs, market research, networking events, professional certifications, and public policy advocacy.

TechAmerica is the public sector and public policy department of CompTIA, advocating before decision-makers at the state, federal and international levels of government. Representing technology companies of all sizes, TechAmerica is committed to expanding market opportunities and driving the competitiveness of the U.S. technology industry around the world.

About This Research

The data for this quantitative study was collected via an online survey conducted during October 2014. A total of 1,561 senior (C-level) U.S. IT and business executives belonging to one of the regional technology associations affiliated with the Technology Councils of North America (TECNA) participated in the survey.

The margin of sampling error at the 95% confidence level for the overall results is +/- 2.5 percentage points. Sampling error is larger for subgroups of the data, such as region or company size.

As with any survey, sampling error is only one source of possible error. While non-sampling error cannot be accurately calculated, precautionary steps were taken in all phases of the survey design, collection and processing of the data to minimize its influence.

The study was conducted in conjunction with the Computing Technology Industry Association (CompTIA), with data collection support from Decipher, Inc.

CompTIA is a member of the Market Research Association (MRA) and adheres to its guidelines for research best practices and ethics. Any questions about the research methodology or data collection can be directed to [email protected].

Profile of Survey RespondentsIndustry Sector of Survey Respondent

Overall Nashville/CTCIT services / Solution providers 20% 26%Enterprise Software 12% 10%Consulting 11% 6%Healthcare / Life sciences 7% 16%Finance 5% 2%Digital media / E-commerce 4% 4%Cloud service provider 4% 0%Telecommunications services / ISP 4% 8%Hardware / OEM 3% 0%Data / Analytics 2% 4%Advanced manufacturing 2% 2%Social / Web 2% 4%Energy technology / Cleantech 2% 2%Mobile apps 1% 0%Semiconductor 1% 0%Gaming 0% 0%Advanced materials 0% 0%Other 20% 16%

Firm Size by Employee Count

Overall Nashville/CTCLess than 10 23% 14%10 to 19 9% 12%20 to 49 14% 10%50 to 99 11% 14%100 to 499 17% 10%500 to 999 5% 10%1000 or more employees 22% 30%

Geographic Segmentation Categories

Northeast (n=277) Connecticut Technology Council (CTC) Greater Philadelphia Alliance for Capital & Technologies (PACT) Massachusetts Technology Leadership Council (MLTC) New Hampshire High Tech Council (NHHTC) New York Technology Council (NYTECH) Tech Collective (Rhode Island)

South (n=538) Austin Technology Council (ATC) Council for Entrepreneurial Development (CED) Chattanooga Technology Council Chesapeake Regional Tech Council (CRTC) Howard Tech Council Metroplex Technology Business Council (MTBC) Nashville Technology Council North Carolina Technology Association (NCTA) Roanoke-Blacksburg Technology Council Tampa Bay Technology Forum (TBTF) Technology Association of Georgia (TAG) Technology Association of Louisville Kentucky (TALK) Tech Birmingham

This report contains a number comparisons among geographic regions. The following groupings are based on standard U.S. Census Bureau categorizations.

Midwest (n=346) Illinois Technology Association (ITA) Minnesota High Tech Association (MHTA) Northeast Ohio Software Association (NEOSA) Technology Association of Nebraska Technology Council of Greater Kansas City (KCNext)

West (n=400) Arizona Technology Council (ATC) California Technology Council Colorado Technology Association Idaho Technology Council (ITC) New Mexico Technology Council Technology Association of Oregon (TAO) Utah Technology Council (UTC) Washington Technology Industry Association (WTIA)

Assessment of Business Conditions and the Economy

Section 1

53.0

61.5

69.6 69.9

55.4

63.3

72.9 72.9

55.4

64.4

72.4 71.7

54.0

62.8

72.1 73.7

56.4

66.4

71.2 70.2

Northeast

Midwest

South

West

Nashville/CTC

Business Sentiment Segmentation: Regional Ratings

Source: TECNABase: 1,561 senior U.S. technology and business executives

Northeast=277, Midwest=346, South=538, West=400, NTC/CTC=50

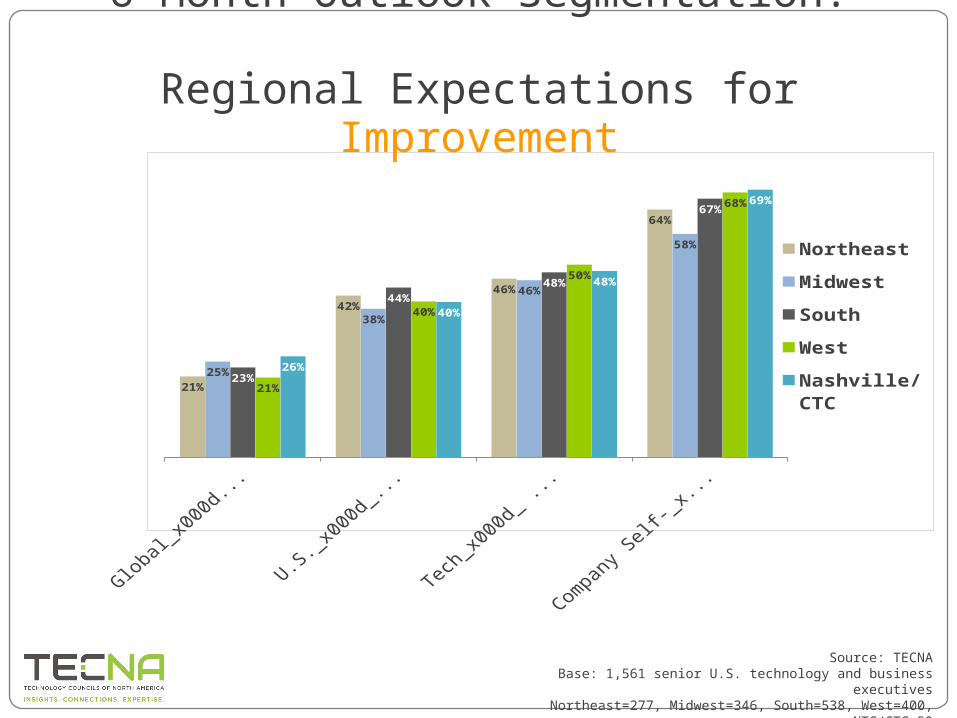

Nashville/CTC 6-Month Outlook Generally Favorable

Global Economy

U.S. Economy

Tech Sector

Company Self-Assessment

26%

44%

30%

40%

52%

8%

48%

50%

2%

69%

29%

2%

% Expecting Improvement

% Expecting Weakening

% Expecting No Change

Source: TECNABase: 50 Nashville/Chattanooga Technology Council executives

21%

42%

46%

64%

25%

38%

46%

58%

23%

44%48%

67%

21%

40%

50%

68%

26%

40%

48%

69%

Northeast

Midwest

South

West

Nashville/CTC

6-Month Outlook Segmentation: Regional Expectations for Improvement

Source: TECNABase: 1,561 senior U.S. technology and business executives

Northeast=277, Midwest=346, South=538, West=400, NTC/CTC=50

Business Investment Drivers and Factors that Could Slow Growth

Section 2

Business Investment Segmentation

Planned Increase Northeast Midwest South West Nashville/CTC

Investments in new products/business lines 62% 58% 62% 65% 76%

Staffing levels in technical positions 54% 58% 59% 58% 70%

Technology expenditures 50% 47% 54% 56% 60%

Marketing/advertising expenditures 54% 46% 50% 55% 50%

Staffing levels in non technical positions 49% 42% 47% 52% 56%

Staff training or professional development 40% 45% 46% 48% 54%

Business travel 31% 34% 34% 38% 34%

Capital expenditures 32% 33% 33% 36% 40%

Cost cutting 18% 28% 26% 22% 29%

Percent indicating a planned increase in investment over next 6 months

Source: TECNABase: 1,561 senior U.S. technology and business executives

Northeast=277, Midwest=346, South=538, West=400, NTC/CTC=50

Cost cutting

Business travel

Capital expenditures

Marketing/advertising expenditures

Staff training or professional development

Staffing levels in non technical positions

Technology expenditures

Staffing levels in technical positions

Investments in new products/business lines

6%

2%

8%

4%

4%

0%

6%

0%

2%

65%

64%

52%

46%

42%

44%

34%

30%

22%

29%

34%

40%

50%

54%

56%

60%

70%

76%

Nashville/CTC Business Investment Expectations

Timeframe: over next 6 months

Planning Increases

Planning Decreases

No Change Expected

Source: TECNABase: 50 Nashville/Chattanooga Technology Council executives

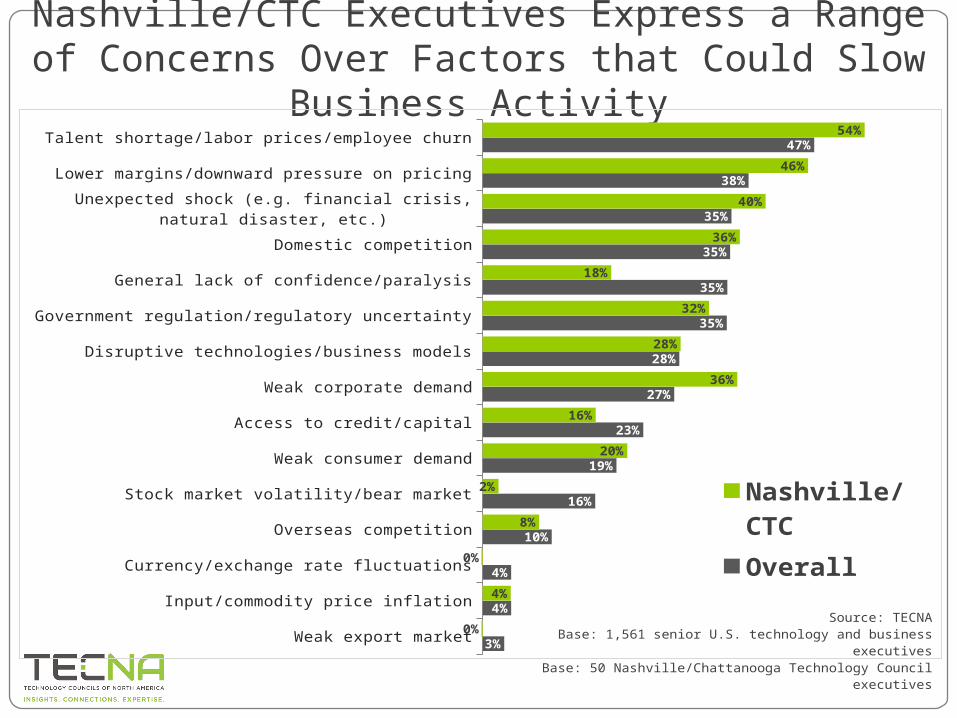

Nashville/CTC Executives Express a Range of Concerns Over Factors that Could Slow Business Activity

Weak export market

Input/commodity price inflation

Currency/exchange rate fluctuations

Overseas competition

Stock market volatility/bear market

Weak consumer demand

Access to credit/capital

Weak corporate demand

Disruptive technologies/business models

Government regulation/regulatory uncertainty

General lack of confidence/paralysis

Domestic competition

Unexpected shock (e.g. financial crisis, natural disaster, etc.)

Lower margins/downward pressure on pricing

Talent shortage/labor prices/employee churn

3%

4%

4%

10%

16%

19%

23%

27%

28%

35%

35%

35%

35%

38%

47%

0%

4%

0%

8%

2%

20%

16%

36%

28%

32%

18%

36%

40%

46%

54%

Nashville/CTC

Overall

Source: TECNABase: 1,561 senior U.S. technology and business executives

Base: 50 Nashville/Chattanooga Technology Council executives

Workforce Issues

Section 3

Significant surplus

Moderate surplus

Equilibrium, supply roughly equals demand

Moderate shortage

Significant shortage

0%0%

8%

52%

38%

0%4%

8%

63%

24%

Quantity of Talent Quality of Talent

Note: don’t know responses not shown

Nashville/CTC Perceptions of Tech Talent Quantity and Quality

NET shortage of quantity of talent= 90%

Source: TECNABase: 50 Nashville/Chattanooga Technology Council executives

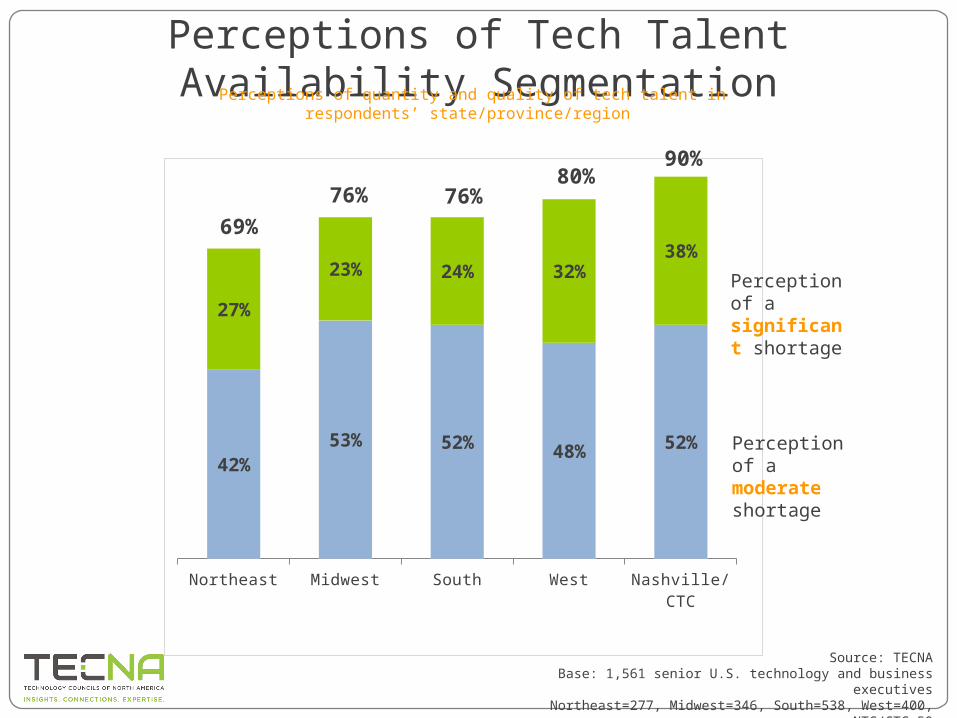

Perceptions of Tech Talent Availability Segmentation

Northeast Midwest South West Nashville/CTC

42%53% 52% 48% 52%

27%

23% 24% 32%38%

69%76% 76%

80%

Perception of a significant shortage

Perception of a moderate shortage

Perceptions of quantity and quality of tech talent in respondents’ state/province/region

90%

Source: TECNABase: 1,561 senior U.S. technology and business executives

Northeast=277, Midwest=346, South=538, West=400, NTC/CTC=50

Nashville/CTC Workforce Gains / Losses Projections

None of above - expect no hiring nor layoffs

Laying-off staff - positions reduced due to downsizing,_x000d_ slow sales or other business cycle issues

Laying-off staff - positions that_x000d_ have been permanently eliminated

Hiring staff - back-fill openings_x000d_ for existing headcount

Hiring staff - positions newly_x000d_ created or additional headcount

16%

7%

5%

34%

63%

4%

8%

4%

42%

78%

Nashville/CTC

Overall

Timeframe: over next 12 months

Source: TECNABase: 1,561 senior U.S. technology and business executives

Base: 50 Nashville/Chattanooga Technology Council executives

Workforce Gains / Losses Projections Segmentation

6% 5%

33%

60%

10%6%

36%

58%

8% 7%

34%

64%

4% 3%

34%

66%

8%4%

42%

78%

Northeast

Midwest

South

West

Nashville/CTCHiring staff -

positions newly created or additional headcount

Hiring staff - back-fill openings for

existing headcount

Laying-off staff - positions that

have been permanently eliminated

Laying-off staff – positions reduced due to downsizing, slow sales or other

business cycle issues

Source: TECNABase: 1,561 senior U.S. technology and business executives

Northeast=277, Midwest=346, South=538, West=400, NTC/CTC=50

Public Policy Issues

Section 4

12%

35%

41%

12%

0%6%

14%

34%

44%

2%

Rating of Federal Government Rating of State/Local Government

Rating of How Well Government Represents the Interests of the Tech Sector

Source: TECNABase: 50 Nashville/Chattanooga Technology Council executives

Rating of How Well State/Regional Government Represents the Interests of the Tech Sector

NET poorly Just okay NET well

41%43%

16%

43% 43%

14%

48%

40%

12%

44%

40%

16%

20%

34%

46%Northeast

Midwest

South

West

Nashville/CTC

Source: TECNABase: 1,561 senior U.S. technology and business executives

Northeast=277, Midwest=346, South=538, West=400, NTC/CTC=50

Nashville/CTC Preferences for Policy Actions in 2015

Immigration policy to restrict STEM workers

Access to public data

Tech adoption in healthcare in rural and urban areas

Opportunities for tech transfer to create new tech companies

Modernization of telecommunications laws

Immigration policy to allow more STEM skilled workers

Tech infrastructure in schools

Promotion of business between public sector and tech companies

Increased broadband deployment

Govt. efficiency through the use of technology

Access to state level funding for innovation

Access to capital for tech companies

Taxation and regulation

STEM education K-12 level

STEM education at higher ed levels

3%

11%

18%

19%

22%

25%

25%

25%

25%

26%

32%

36%

42%

43%

44%

2%

26%

42%

18%

18%

14%

30%

24%

32%

30%

28%

26%

42%

44%

48%

Nashville/CTC

Overall

Source: TECNABase: 1,561 senior U.S. technology and business executives

Base: 50 Nashville/Chattanooga Technology Council executives

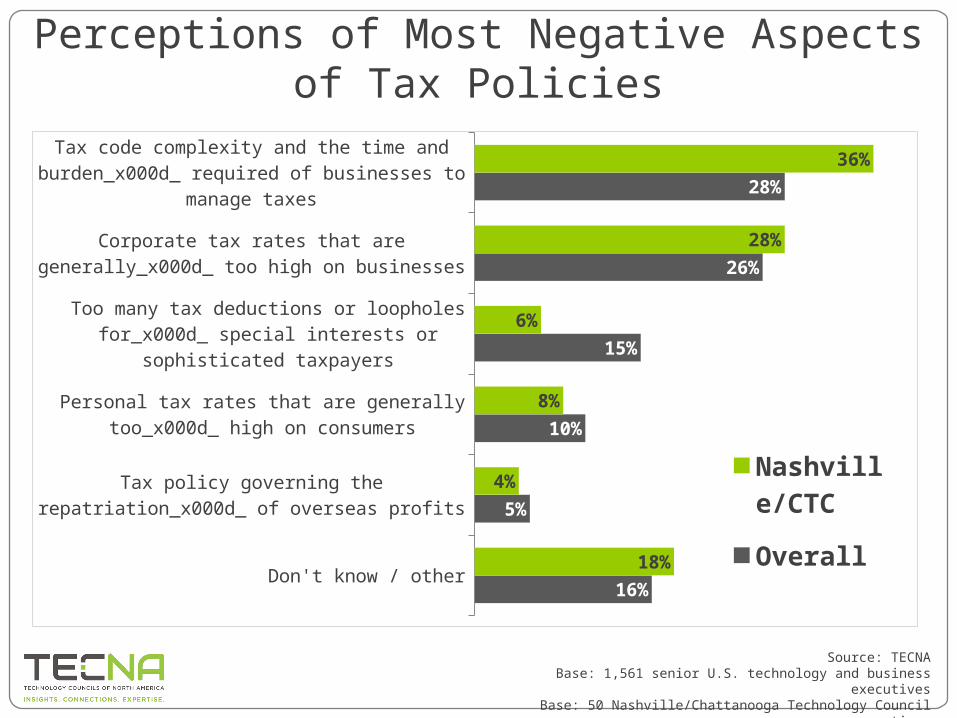

Perceptions of Most Negative Aspects of Tax Policies

Don't know / other

Tax policy governing the repatriation_x000d_ of overseas profits

Personal tax rates that are generally too_x000d_ high on consumers

Too many tax deductions or loopholes for_x000d_ special interests or sophisticated taxpayers

Corporate tax rates that are generally_x000d_ too high on businesses

Tax code complexity and the time and burden_x000d_ required of businesses to manage taxes

16%

5%

10%

15%

26%

28%

18%

4%

8%

6%

28%

36%

Nashville/CTC

Overall

Source: TECNABase: 1,561 senior U.S. technology and business executives

Base: 50 Nashville/Chattanooga Technology Council executives

Perceptions of Most Negative Aspects of Tax Policies Segmentation

Northeast Midwest South West Nashville/CTC

Tax code complexity and the time and burden required of businesses to manage taxes 26% 24% 33% 26% 36%

Corporate tax rates that are generally too high on businesses 22% 26% 28% 28% 28%

Too many tax deductions or loopholes for special interests or sophisticated taxpayers 20% 17% 10% 18% 6%

Personal tax rates that are generally too high on consumers 11% 7% 10% 10% 8%

Tax policy governing the repatriation of overseas profits 4% 7% 4% 3% 4%

Source: TECNABase: 1,561 senior U.S. technology and business executives

Northeast=277, Midwest=346, South=538, West=400, NTC/CTC=50

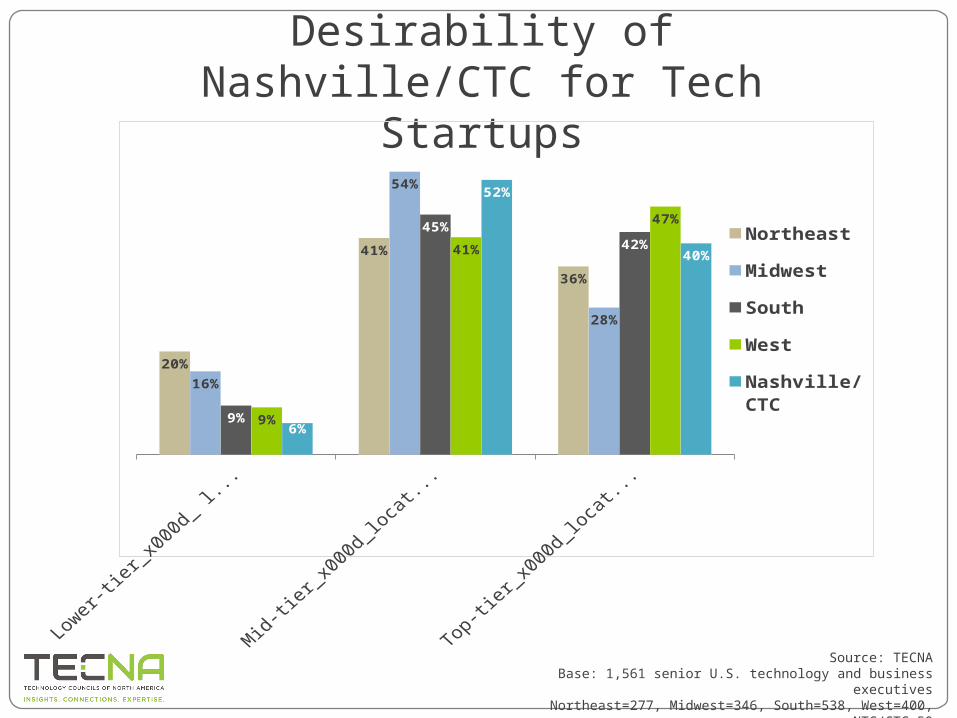

Self Assessment of Desirability of Nashville/CTC for Tech Startups

20%

41%

36%

16%

54%

28%

9%

45%42%

9%

41%

47%

6%

52%

40%Northeast

Midwest

South

West

Nashville/CTC

Source: TECNABase: 1,561 senior U.S. technology and business executives

Northeast=277, Midwest=346, South=538, West=400, NTC/CTC=50

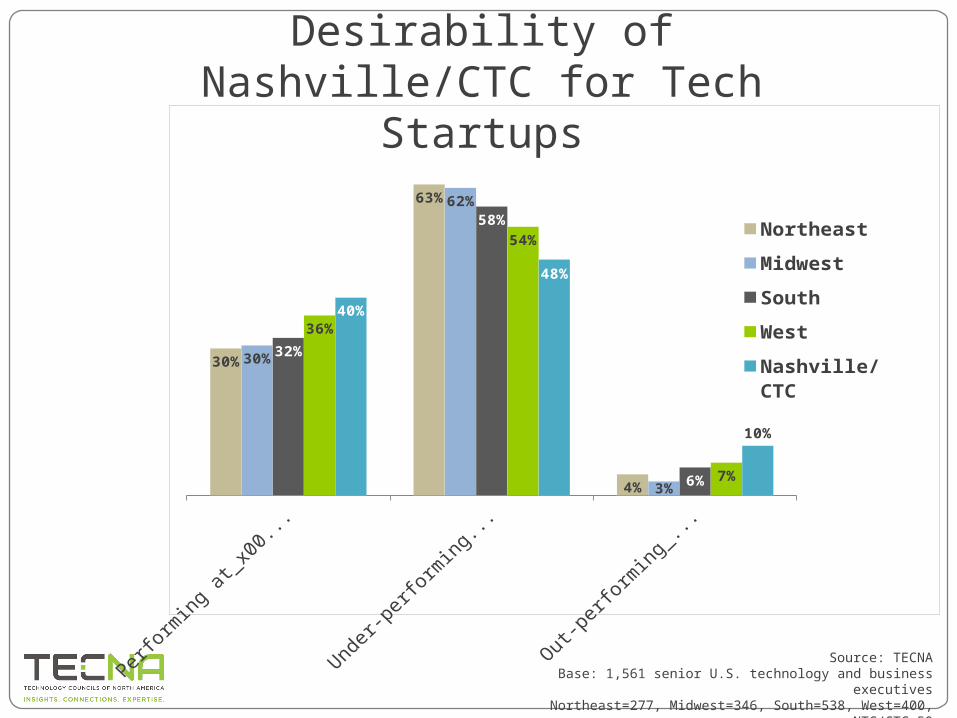

Self Assessment of Desirability of Nashville/CTC for Tech Startups

30%

63%

4%

30%

62%

3%

32%

58%

6%

36%

54%

7%

40%

48%

10%

Northeast

Midwest

South

West

Nashville/CTC

Source: TECNABase: 1,561 senior U.S. technology and business executives

Northeast=277, Midwest=346, South=538, West=400, NTC/CTC=50

Perceptions of Factors Contributing to a Healthy Tech Sector in Nashville/CTC

Other factors

K-12 education

Transportation capacity/quality

Commercial sector ecosystem

Early, mid, late-stage financing capacity

General infrastructure capacity / quality

University alignment with industry needs

Research universities

Business friendly environment

Cost advantages (e.g. land, labor, inputs, etc.)

Skilled workforce

Entrepreneurship/innovation ecosystem

Quality of life

2%

4%

7%

9%

9%

14%

24%

26%

26%

27%

36%

44%

57%

2%

6%

6%

6%

14%

16%

14%

6%

44%

36%

14%

60%

64%

Nashville/CTC

Overall

Source: TECNABase: 1,561 senior U.S. technology and business executives

Base: 50 Nashville/Chattanooga Technology Council executives

Perceptions of Factors Contributing to a Healthy Tech Sector in Nashville/CTC Segmentation

Northeast Midwest South West Nashville/CTC

Quality of life 49% 55% 55% 69% 64%

Entrepreneurship/innovation ecosystem 45% 42% 41% 50% 60%

Skilled workforce 42% 39% 32% 37% 14%

Cost advantages 11% 23% 34% 32% 36%

Business friendly environment 11% 20% 33% 33% 44%

Research universities 37% 20% 30% 19% 6%

University alignment with industry needs 29% 25% 28% 17% 14%

General infrastructure capacity 11% 20% 14% 13% 16%

Early, mid, late-stage financing capacity 18% 8% 6% 9% 14%

Commercial sector ecosystem 9% 14% 7% 7% 6%

Transportation capacity/quality 10% 12% 5% 3% 6%

K-12 education 4% 8% 3% 1% 6%

Source: TECNABase: 1,561 senior U.S. technology and business executives

Northeast=277, Midwest=346, South=538, West=400, NTC/CTC=50

Perceptions of Factors that can Inhibit Nashville/CTC Tech Sector Growth / Performance

Quality of life

Research universities / R&D capacity

Commercial sector ecosystem

General infrastructure capacity / quality

Entrepreneurship/innovation ecosystem

University/college alignment with industry needs

Business environment

K-12 education

Transportation capacity/quality

Workforce

Costs (e.g. land, labor, inputs, etc.)

Early, mid, late stage financing capacity

0%

22%

4%

14%

4%

41%

6%

39%

27%

59%

2%

37%

Source: TECNABase: 2014 – 50 Nashville/Chattanooga Technology Council executives

Expectations of Sectors that Will Drive Innovation / Startups / Job Growth

Advanced materials

Defense / military technology

Telecommunications

Broadcasting / Digital media / entertainment technology

Advanced manufacturing

Energy technology / Cleantech

IT services

Data center / cloud computing infrastructure

Cybersecurity

Data / analytics

Software / apps

Life sciences or healthcare technology

1%

4%

3%

2%

3%

3%

8%

8%

6%

9%

30%

22%

0%

2%

2%

2%

0%

0%

2%

6%

2%

17%

21%

46%

Nashville/CTC

Overall

Source: TECNABase: 1,561 senior U.S. technology and business executives

Base: 50 Nashville/Chattanooga Technology Council executives

2-Year Outlook for Sectors that Will Drive Innovation / Startups / Job Growth

Advanced materials

Defense / military technology

Telecommunications

Broadcasting / Digital media / entertainment technology

Advanced manufacturing

Energy technology / Cleantech

IT services

Data center / cloud computing infrastructure

Cybersecurity

Data / analytics

Software / apps

Life sciences or healthcare technology

1%

2%

6%

2%

4%

1%

10%

8%

6%

14%

24%

22%

0%

0%

2%

4%

4%

2%

2%

8%

4%

31%

12%

31%

Nashville/CTC

Overall

Source: TECNABase: 1,561 senior U.S. technology and business executives

Base: 50 Nashville/Chattanooga Technology Council executives