2013 Financial Review

39

www.eia.gov U.S. Energy Information Administration Independent Statistics & Analysis Markets and Financial Analysis Team May, 2015 Financial Review of the Global Oil and Natural Gas Industry 2014

-

Upload

nguyendang -

Category

Documents

-

view

217 -

download

0

Transcript of 2013 Financial Review

www.eia.gov U.S. Energy Information Administration Independent Statistics & Analysis

Markets and Financial Analysis Team

May, 2015

Financial Review of the Global Oil and

Natural Gas Industry 2014

Overview

2

• This analysis focuses on the financial and operating trends of 75 oil and natural gas

companies (“energy companies”).

• The data come from public financial statements each company submits to the U.S.

Securities and Exchange Commission, which Evaluate Energy (a data service)

aggregates for ease of data analysis.

• For consistency, companies that were later acquired by another company in the

group were kept in the prior year data. For example, ExxonMobil and XTO’s

individual numbers were kept through 2009.

• Cash flow statements list various sources and uses of cash; this analysis focuses

on three main sources (operations, net debt, and net sales of assets) and three

main uses (capital expenditure, dividends to shareholders, and net share issuance).

• Several charts show comparisons between these upstream companies and the U.S.

manufacturing industry, collected from U.S. Census Bureau’s Quarterly Financial

Report.

Brief description of terms

3

• Cash from operations is a measure of income.

• Capital expenditures represent cash used for property, plant, and equipment

(investing activities).

• Financing activities measure inflows/outflows in debt or equity markets including

dividends, share issuance or repurchases, and debt issuance or repayments.

• Return on equity is a measure of the profit a company earns on money shareholders

have invested.

• Market capitalization is the total value of all of a company’s publicly traded shares

outstanding.

• Net income or earnings represent profit after taxes and depreciation.

• Asset impairments are when a company writes down the value of a property to

reflect current market value, which may decline from loss of production potential or

price declines.

• “Upstream” refers to crude oil exploration, production, and other operations prior to

refining.

Key takeaways

4

• Price declines in the second half of 2014 contributed to reduced profitability for these

companies compared to previous years.

• Free cash flow remained low compared to previous years. Share repurchases and

dividends were met by increasing debt and sales of assets.

• Lower prices contributed to lower proved reserve additions compared to previous

years.

• Some companies increased cash balances given the volatile price environment.

• First-quarter 2015 results could show significant reductions in profits, cash flow, and

capital expenditure because of low oil prices.

• In refining, geographic differences in refining margins continued in 2014.

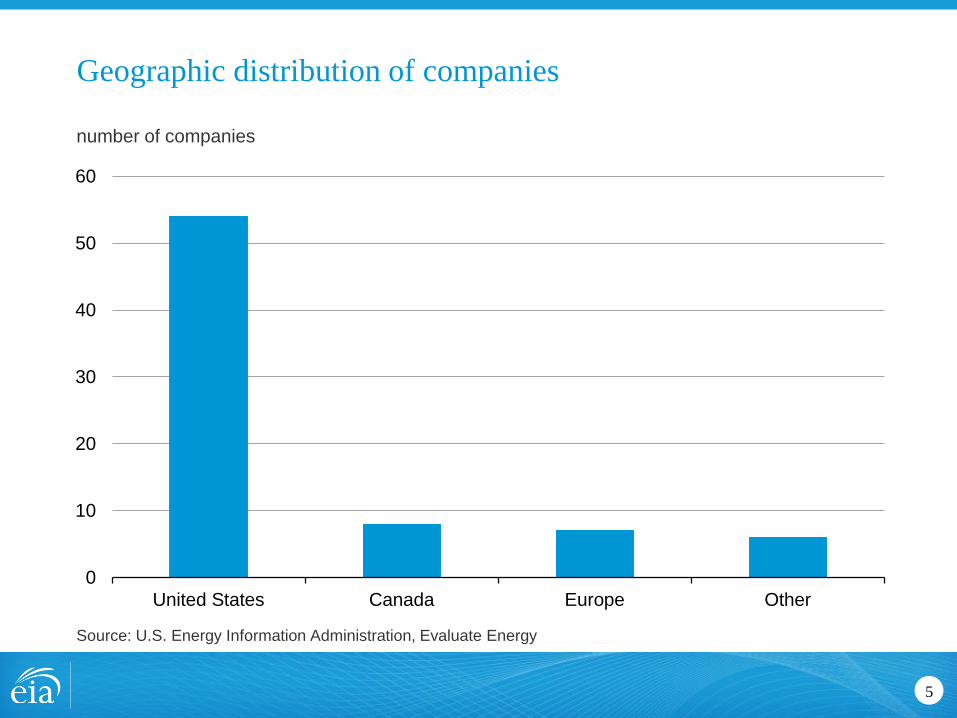

Geographic distribution of companies

5

number of companies

Source: U.S. Energy Information Administration, Evaluate Energy

0

10

20

30

40

50

60

United States Canada Europe Other

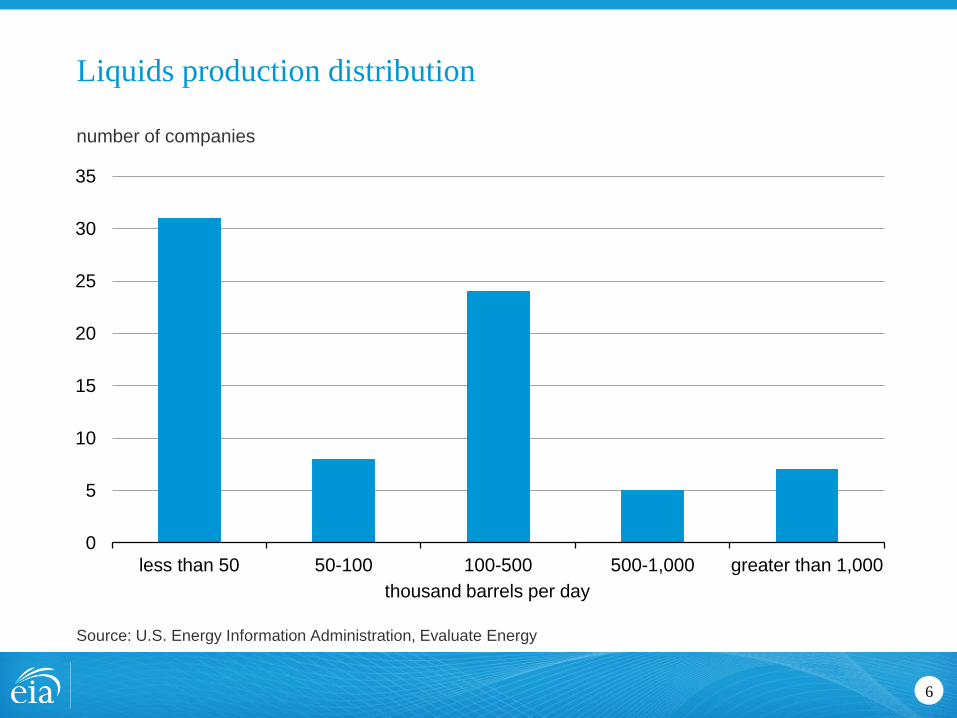

Liquids production distribution

6

number of companies

Source: U.S. Energy Information Administration, Evaluate Energy

0

5

10

15

20

25

30

35

less than 50 50-100 100-500 500-1,000 greater than 1,000

thousand barrels per day

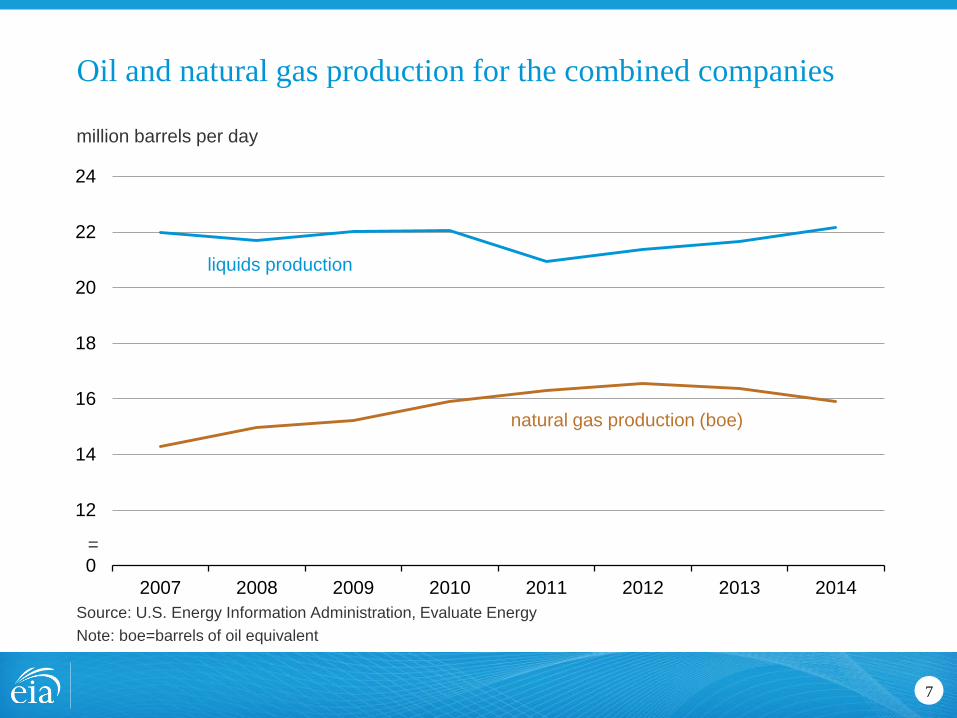

Oil and natural gas production for the combined companies

7

million barrels per day

Source: U.S. Energy Information Administration, Evaluate Energy

Note: boe=barrels of oil equivalent

10

12

14

16

18

20

22

24

2007 2008 2009 2010 2011 2012 2013 2014

liquids production

natural gas production (boe)

=

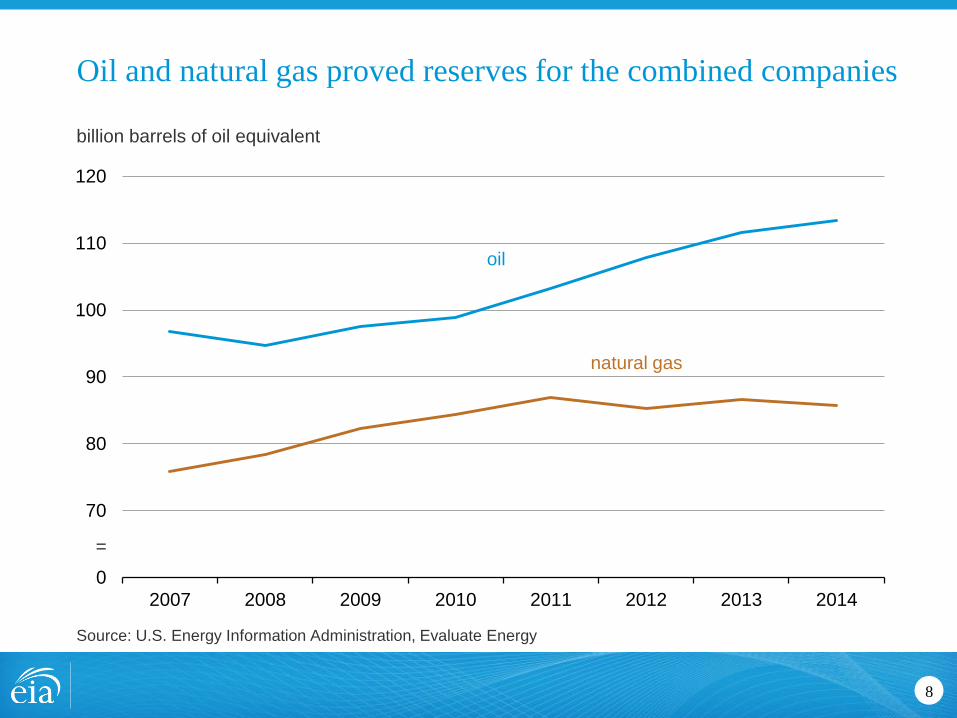

Oil and natural gas proved reserves for the combined companies

8

billion barrels of oil equivalent

Source: U.S. Energy Information Administration, Evaluate Energy

60

70

80

90

100

110

120

2007 2008 2009 2010 2011 2012 2013 2014

oil

natural gas

=

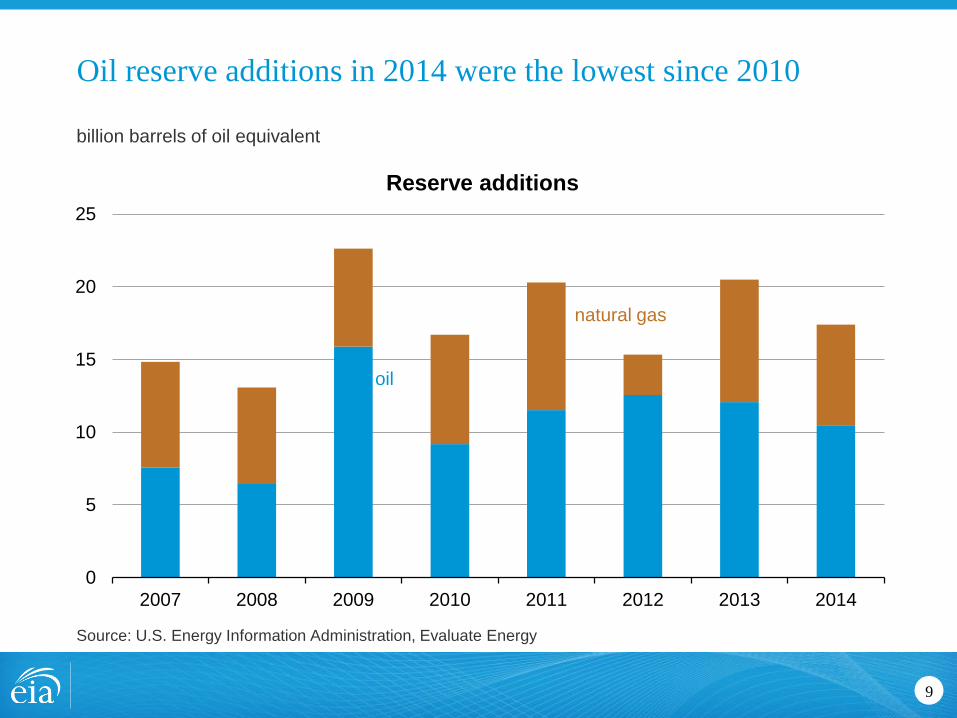

Oil reserve additions in 2014 were the lowest since 2010

9

billion barrels of oil equivalent

Source: U.S. Energy Information Administration, Evaluate Energy

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014

Reserve additions

oil

natural gas

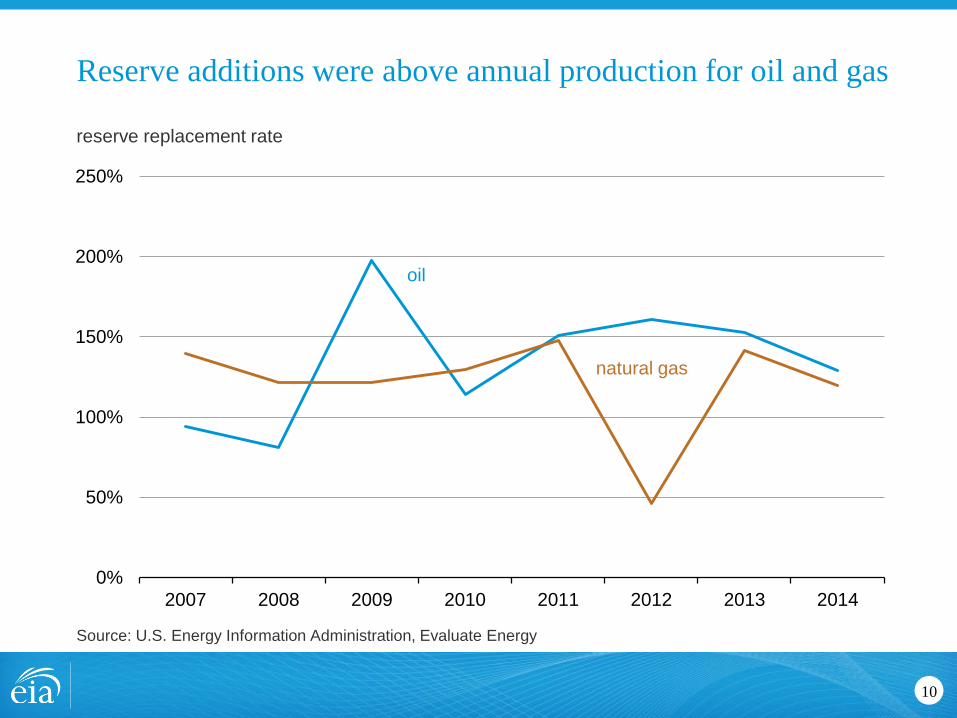

Reserve additions were above annual production for oil and gas

10

reserve replacement rate

Source: U.S. Energy Information Administration, Evaluate Energy

0%

50%

100%

150%

200%

250%

2007 2008 2009 2010 2011 2012 2013 2014

oil

natural gas

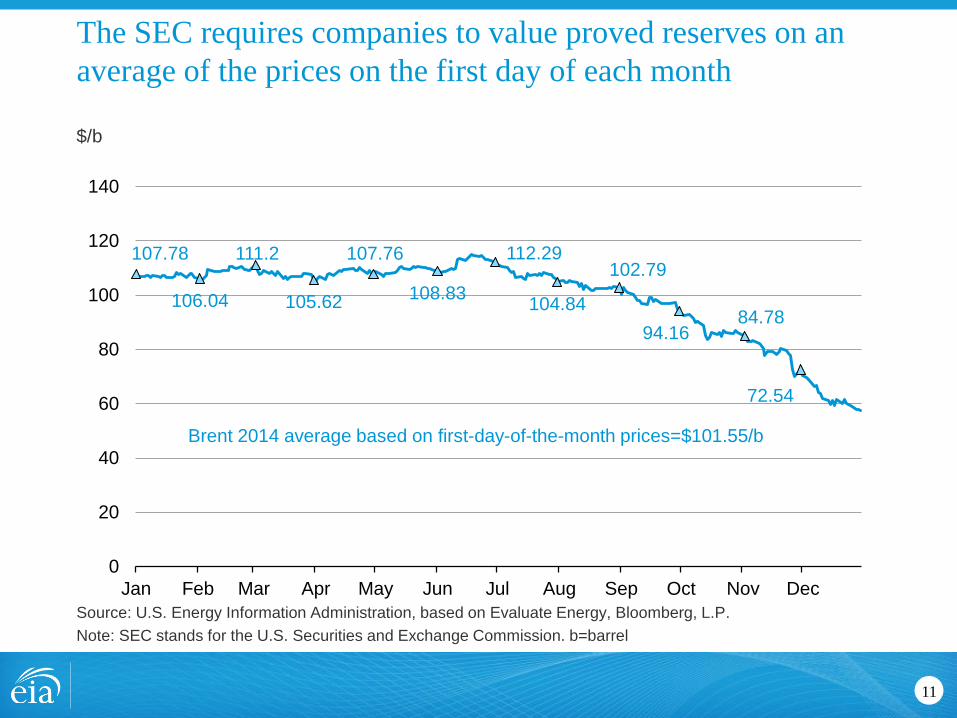

The SEC requires companies to value proved reserves on an

average of the prices on the first day of each month

11

$/b

Source: U.S. Energy Information Administration, based on Evaluate Energy, Bloomberg, L.P.

Note: SEC stands for the U.S. Securities and Exchange Commission. b=barrel

107.78

106.04

111.2

105.62

107.76

108.83

112.29

104.84

102.79

94.16 84.78

72.54

0

20

40

60

80

100

120

140

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Brent 2014 average based on first-day-of-the-month prices=$101.55/b

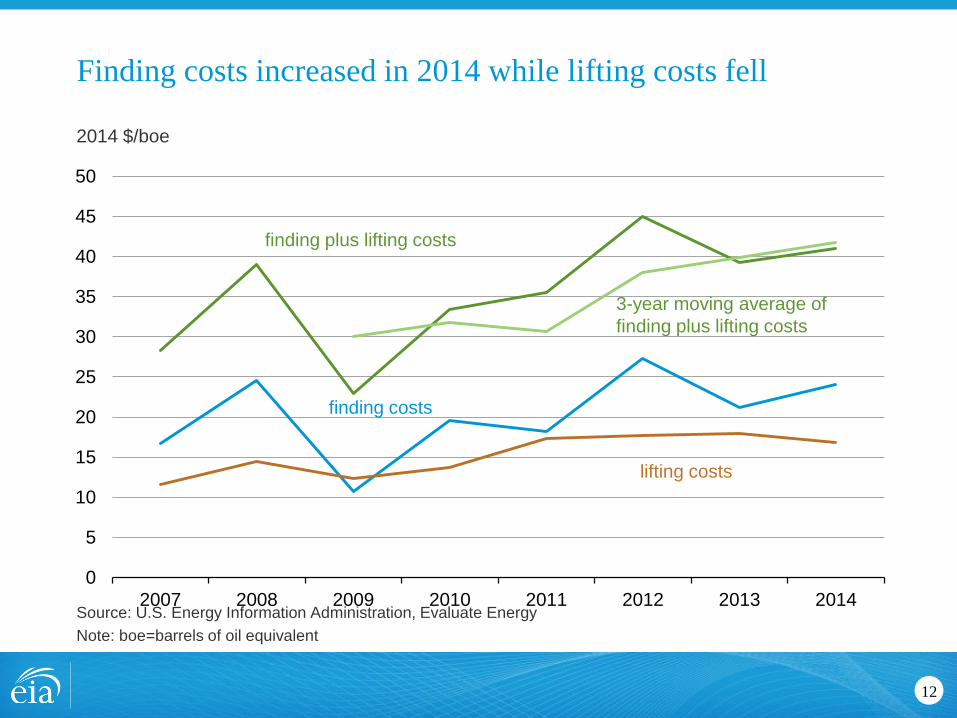

Finding costs increased in 2014 while lifting costs fell

12

2014 $/boe

Source: U.S. Energy Information Administration, Evaluate Energy

Note: boe=barrels of oil equivalent

0

5

10

15

20

25

30

35

40

45

50

2007 2008 2009 2010 2011 2012 2013 2014

finding plus lifting costs

3-year moving average of

finding plus lifting costs

finding costs

lifting costs

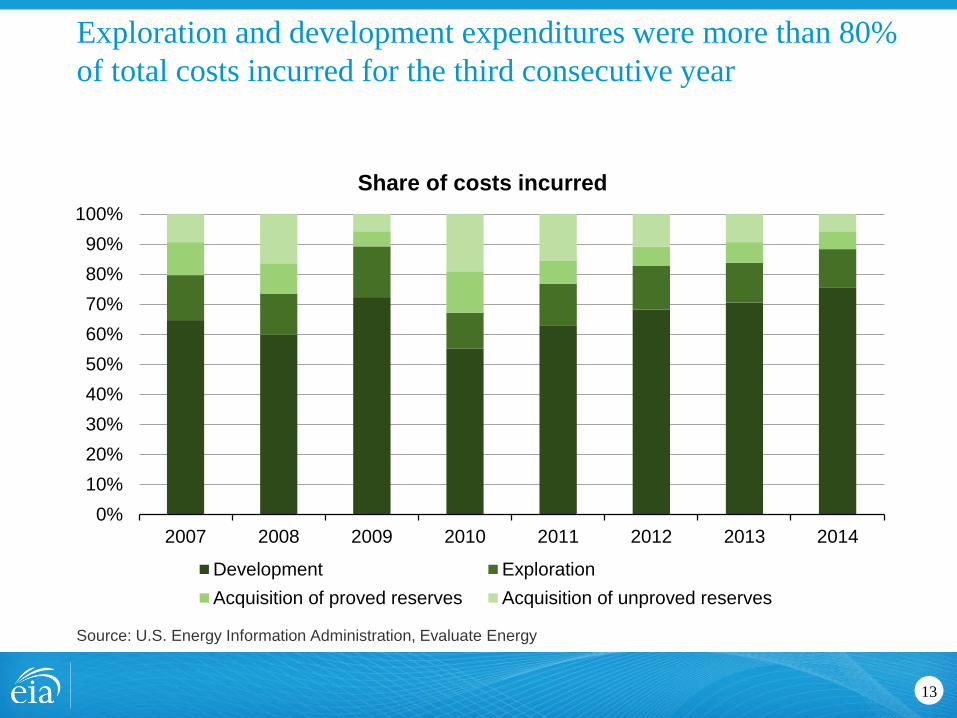

Exploration and development expenditures were more than 80%

of total costs incurred for the third consecutive year

13

Source: U.S. Energy Information Administration, Evaluate Energy

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014

Share of costs incurred

Development Exploration

Acquisition of proved reserves Acquisition of unproved reserves

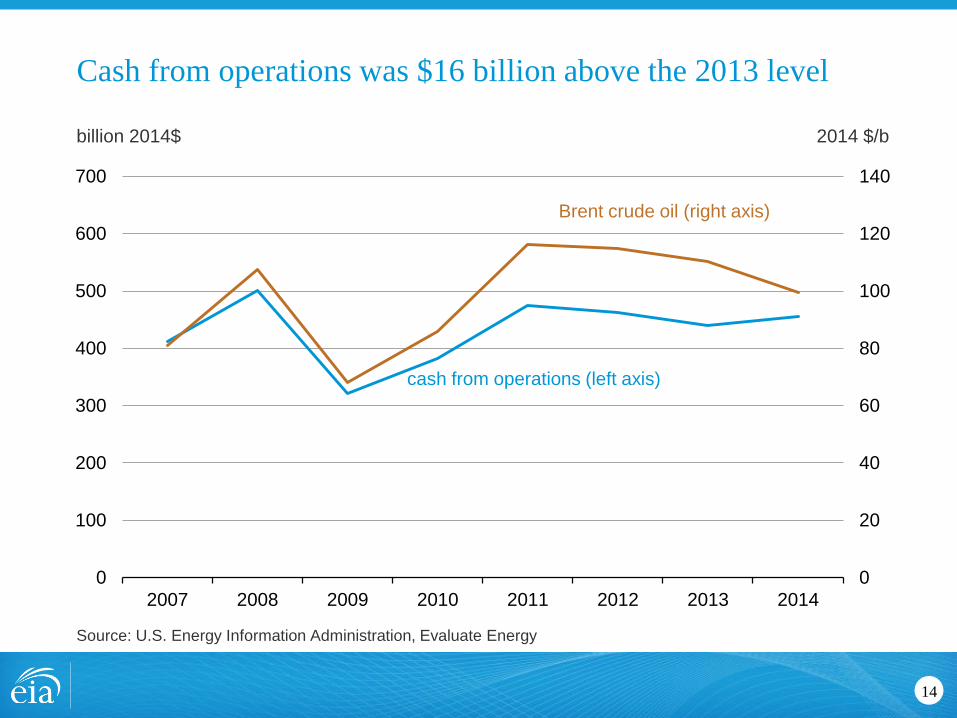

Cash from operations was $16 billion above the 2013 level

14

billion 2014$ 2014 $/b

Source: U.S. Energy Information Administration, Evaluate Energy

0

20

40

60

80

100

120

140

0

100

200

300

400

500

600

700

2007 2008 2009 2010 2011 2012 2013 2014

cash from operations (left axis)

Brent crude oil (right axis)

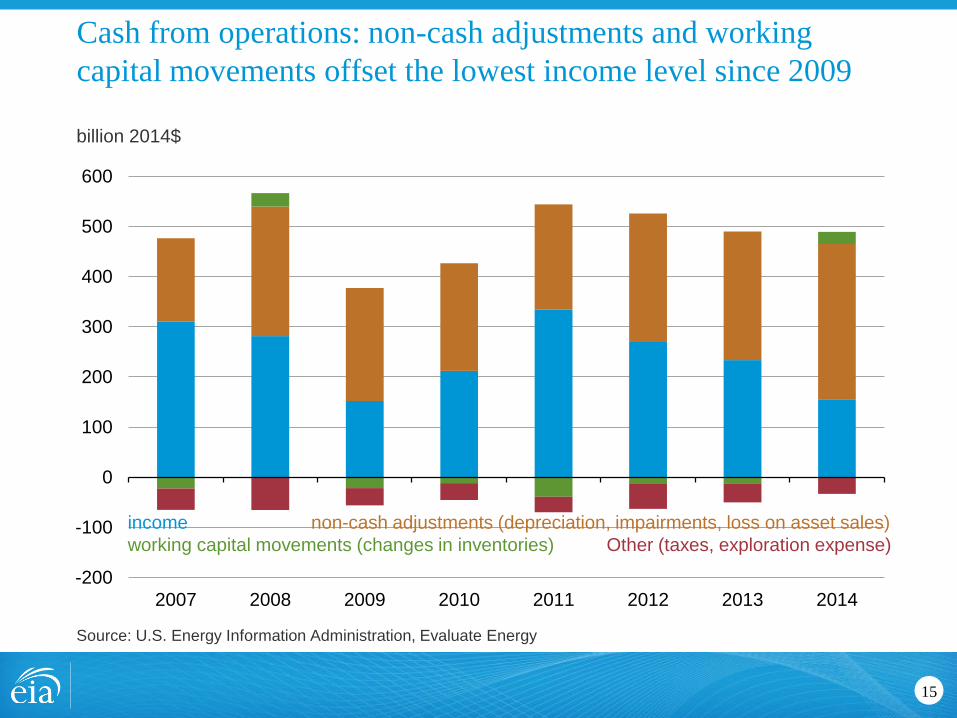

Cash from operations: non-cash adjustments and working

capital movements offset the lowest income level since 2009

15

billion 2014$

Source: U.S. Energy Information Administration, Evaluate Energy

-200

-100

0

100

200

300

400

500

600

2007 2008 2009 2010 2011 2012 2013 2014

income non-cash adjustments (depreciation, impairments, loss on asset sales)

working capital movements (changes in inventories) Other (taxes, exploration expense)

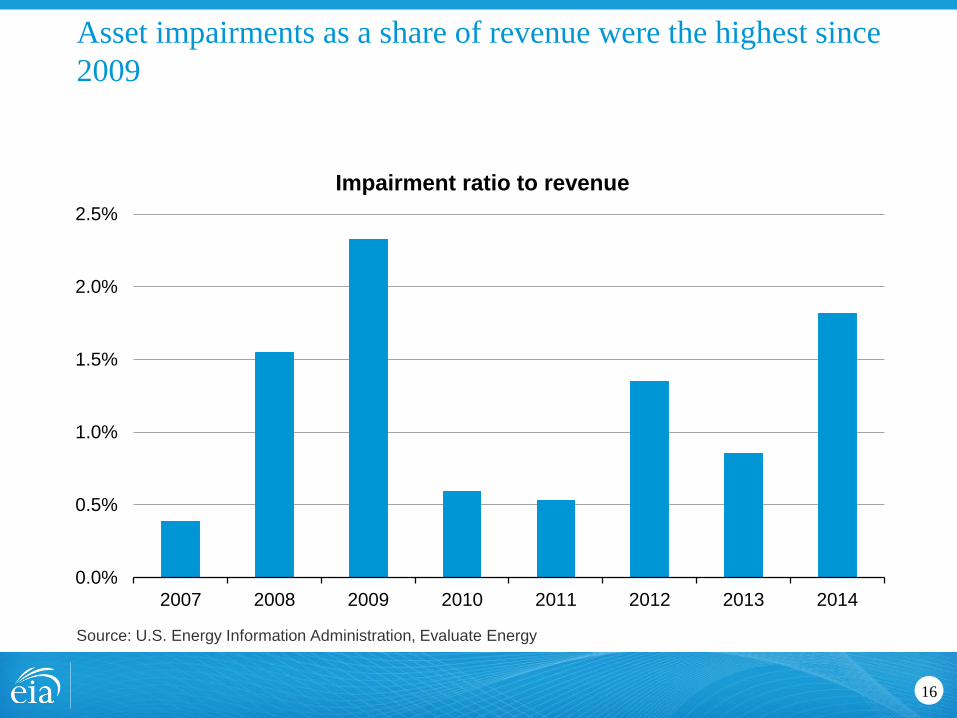

Asset impairments as a share of revenue were the highest since

2009

16

Source: U.S. Energy Information Administration, Evaluate Energy

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2007 2008 2009 2010 2011 2012 2013 2014

Impairment ratio to revenue

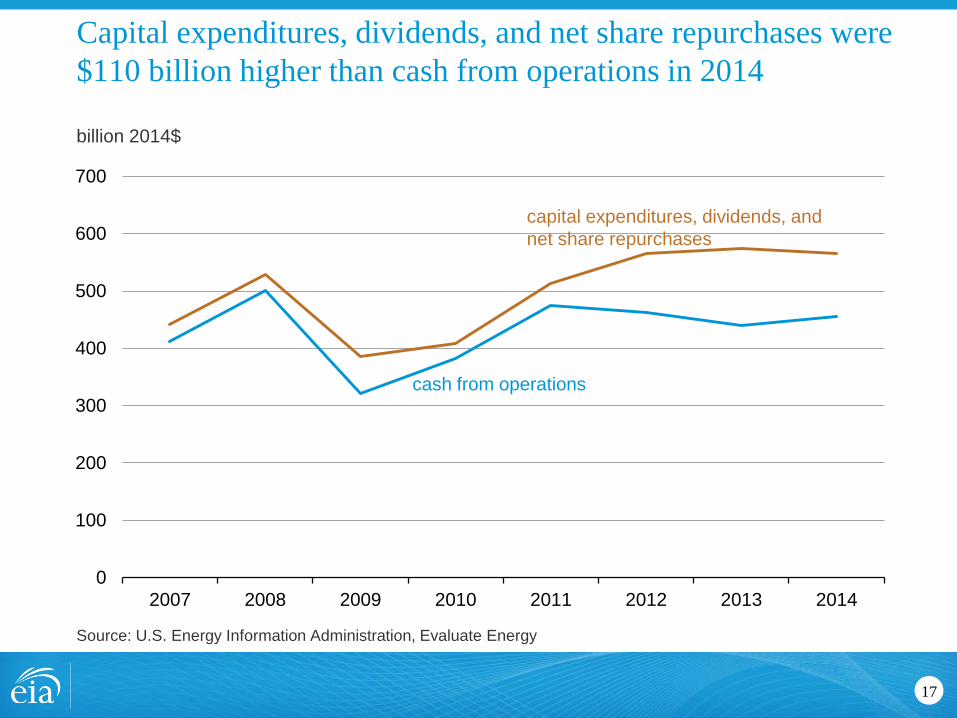

Capital expenditures, dividends, and net share repurchases were

$110 billion higher than cash from operations in 2014

17

billion 2014$

Source: U.S. Energy Information Administration, Evaluate Energy

0

100

200

300

400

500

600

700

2007 2008 2009 2010 2011 2012 2013 2014

cash from operations

capital expenditures, dividends, and

net share repurchases

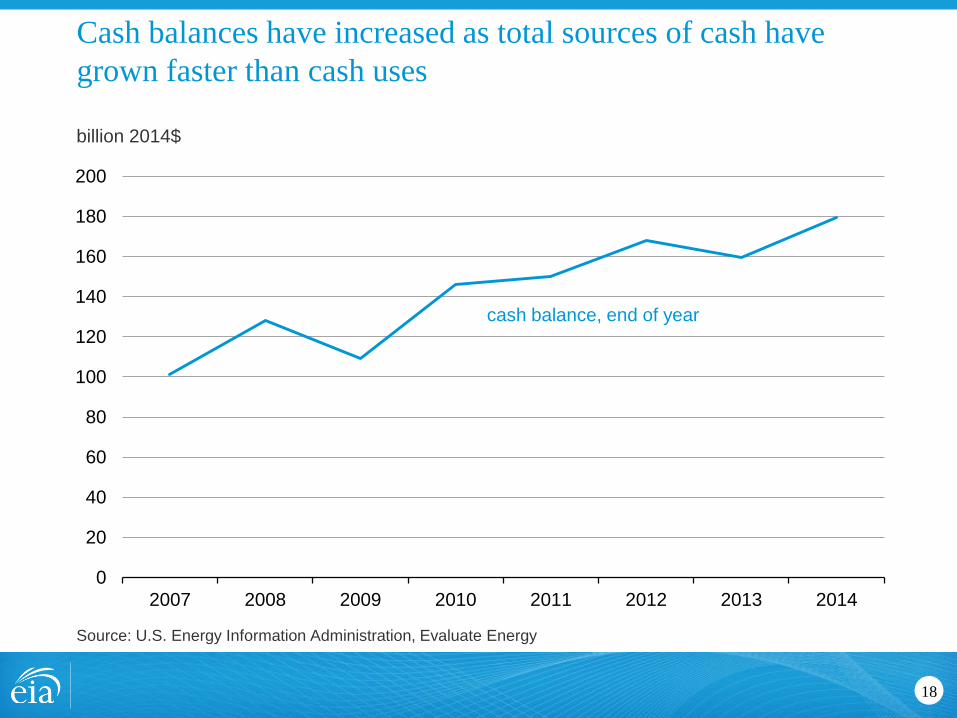

Cash balances have increased as total sources of cash have

grown faster than cash uses

18

billion 2014$

Source: U.S. Energy Information Administration, Evaluate Energy

0

20

40

60

80

100

120

140

160

180

200

2007 2008 2009 2010 2011 2012 2013 2014

cash balance, end of year

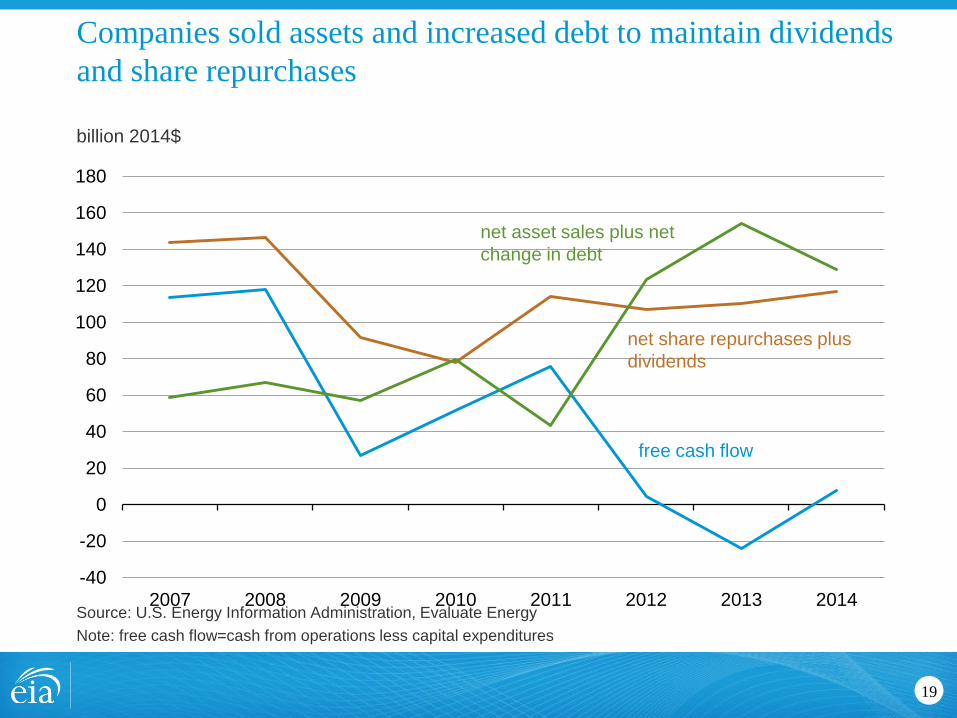

Companies sold assets and increased debt to maintain dividends

and share repurchases

19

billion 2014$

Source: U.S. Energy Information Administration, Evaluate Energy

Note: free cash flow=cash from operations less capital expenditures

-40

-20

0

20

40

60

80

100

120

140

160

180

2007 2008 2009 2010 2011 2012 2013 2014

net asset sales plus net

change in debt

net share repurchases plus

dividends

free cash flow

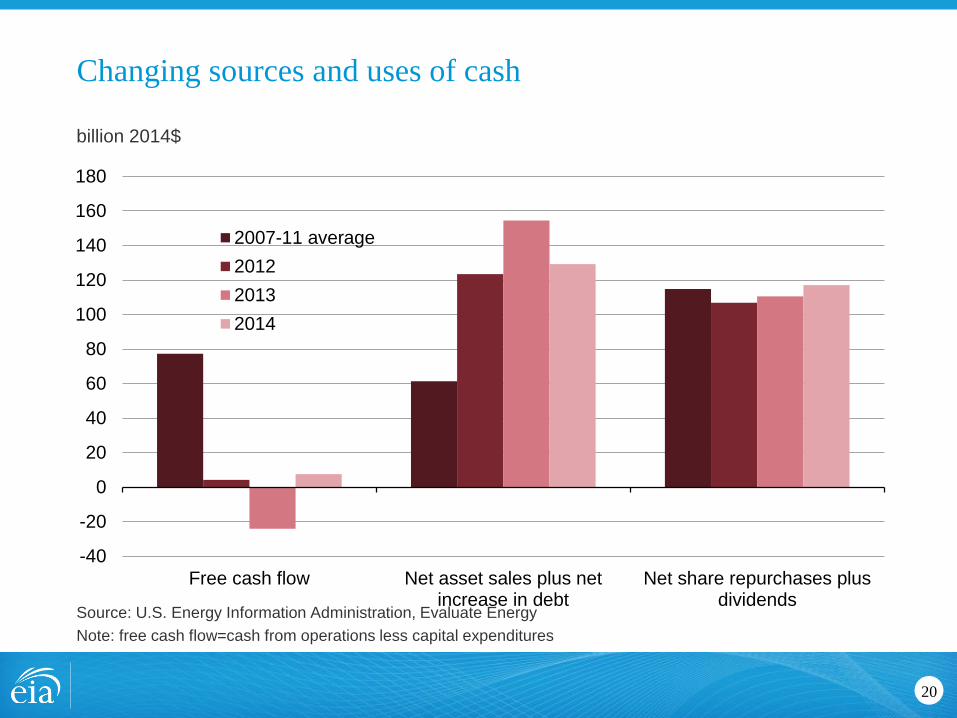

Changing sources and uses of cash

20

billion 2014$

Source: U.S. Energy Information Administration, Evaluate Energy

Note: free cash flow=cash from operations less capital expenditures

-40

-20

0

20

40

60

80

100

120

140

160

180

Free cash flow Net asset sales plus netincrease in debt

Net share repurchases plusdividends

2007-11 average

2012

2013

2014

Cash from operations made up less than 80% of cash sources

for the third consecutive year

21

Source: U.S. Energy Information Administration, Evaluate Energy

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014

Sources of cash

Operations Net asset sales Net increase in debt

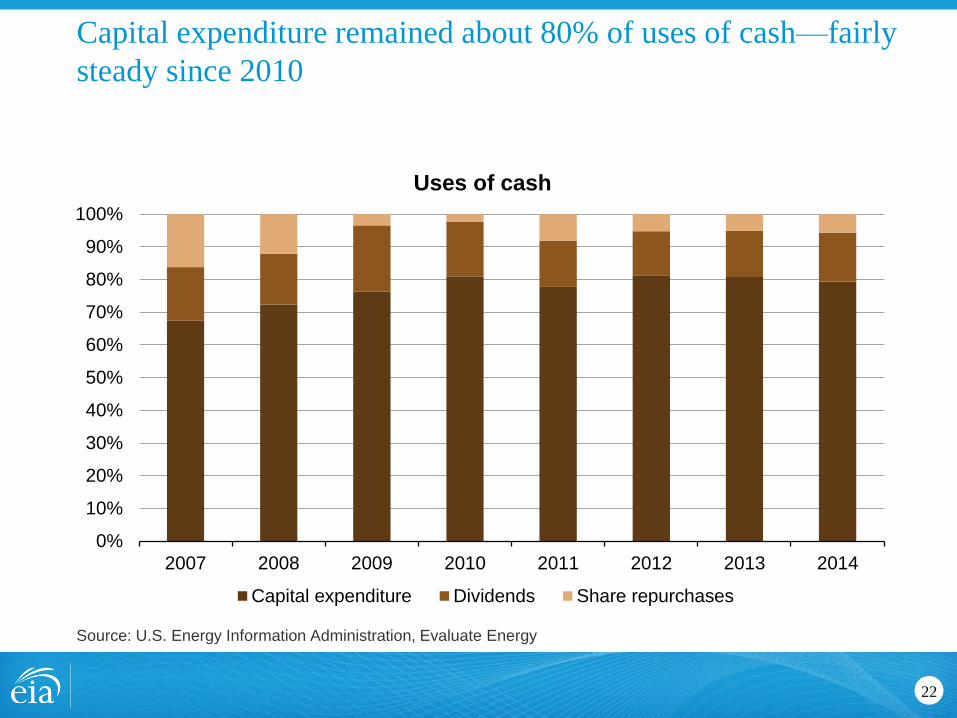

Capital expenditure remained about 80% of uses of cash—fairly

steady since 2010

22

Source: U.S. Energy Information Administration, Evaluate Energy

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014

Uses of cash

Capital expenditure Dividends Share repurchases

Energy companies’ long-term debt to shareholders’ equity ratio

increased four percentage points from the 2013 level

23

Source: U.S. Energy Information Administration, Evaluate Energy, U.S. Census Bureau

0%

10%

20%

30%

40%

50%

60%

2007 2008 2009 2010 2011 2012 2013 2014

Long-term debt to equity

energy companies

U.S. manufacturing

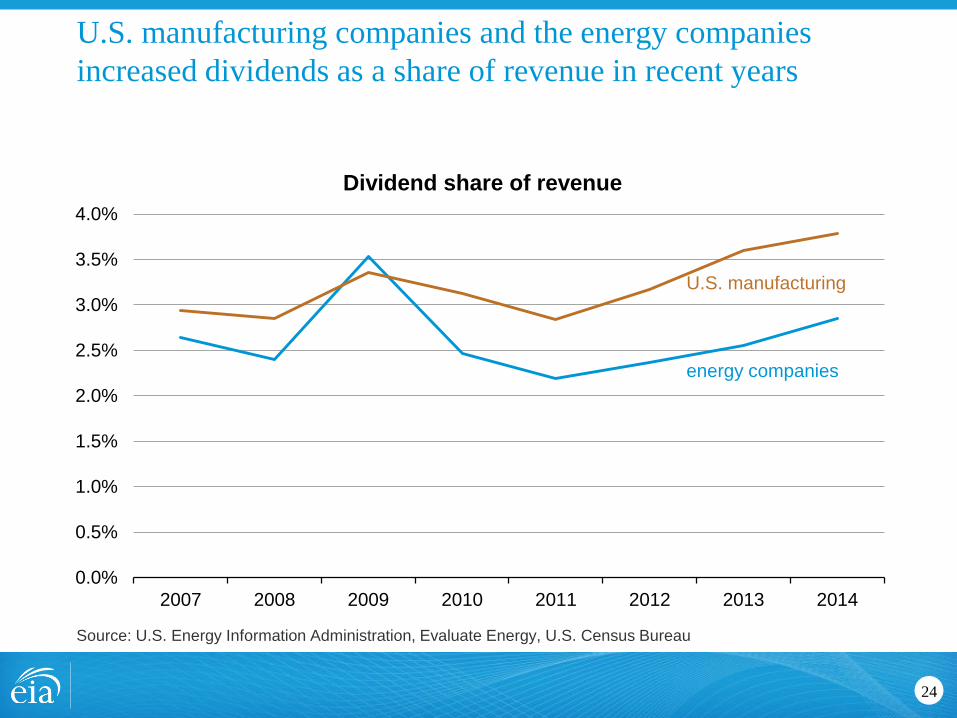

U.S. manufacturing companies and the energy companies

increased dividends as a share of revenue in recent years

24

Source: U.S. Energy Information Administration, Evaluate Energy, U.S. Census Bureau

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

2007 2008 2009 2010 2011 2012 2013 2014

Dividend share of revenue

U.S. manufacturing

energy companies

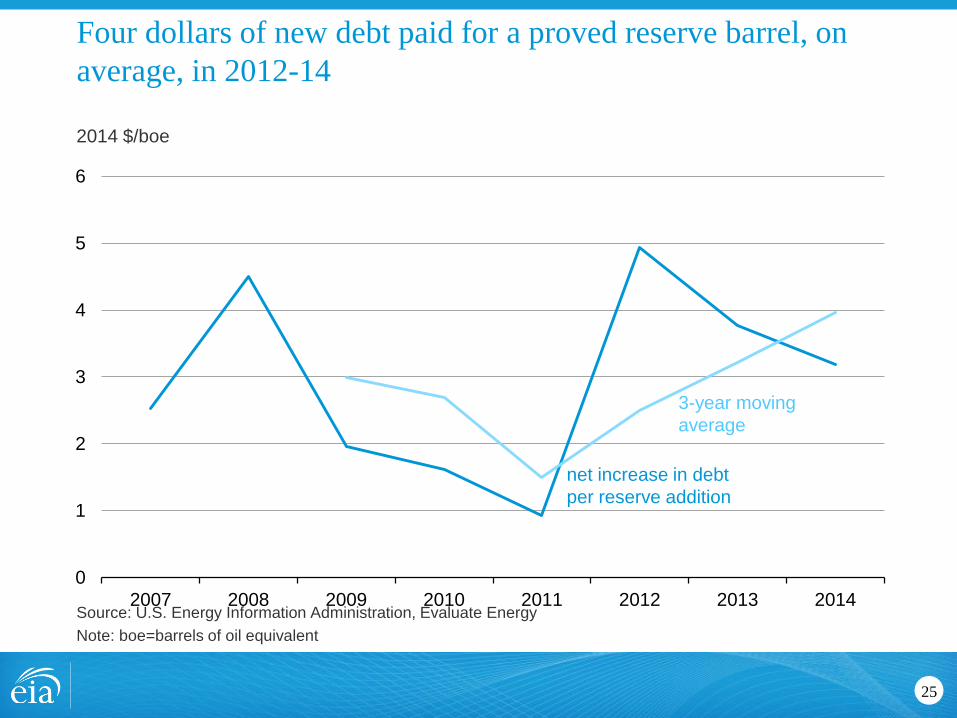

Four dollars of new debt paid for a proved reserve barrel, on

average, in 2012-14

25

2014 $/boe

Source: U.S. Energy Information Administration, Evaluate Energy

Note: boe=barrels of oil equivalent

0

1

2

3

4

5

6

2007 2008 2009 2010 2011 2012 2013 2014

net increase in debt

per reserve addition

3-year moving

average

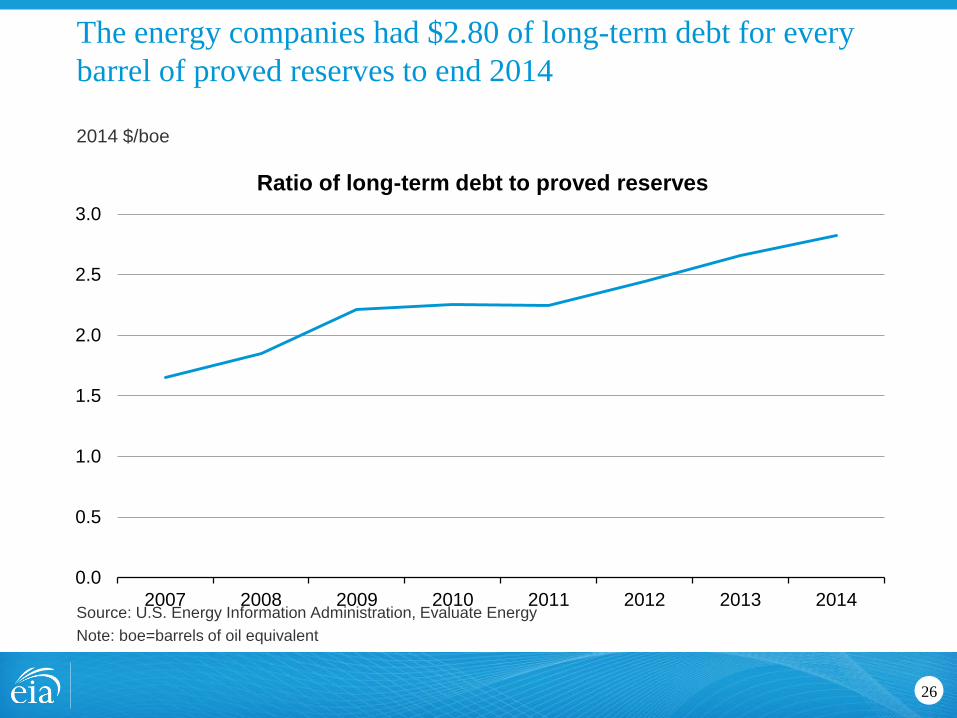

The energy companies had $2.80 of long-term debt for every

barrel of proved reserves to end 2014

26

2014 $/boe

Source: U.S. Energy Information Administration, Evaluate Energy

Note: boe=barrels of oil equivalent

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2007 2008 2009 2010 2011 2012 2013 2014

Ratio of long-term debt to proved reserves

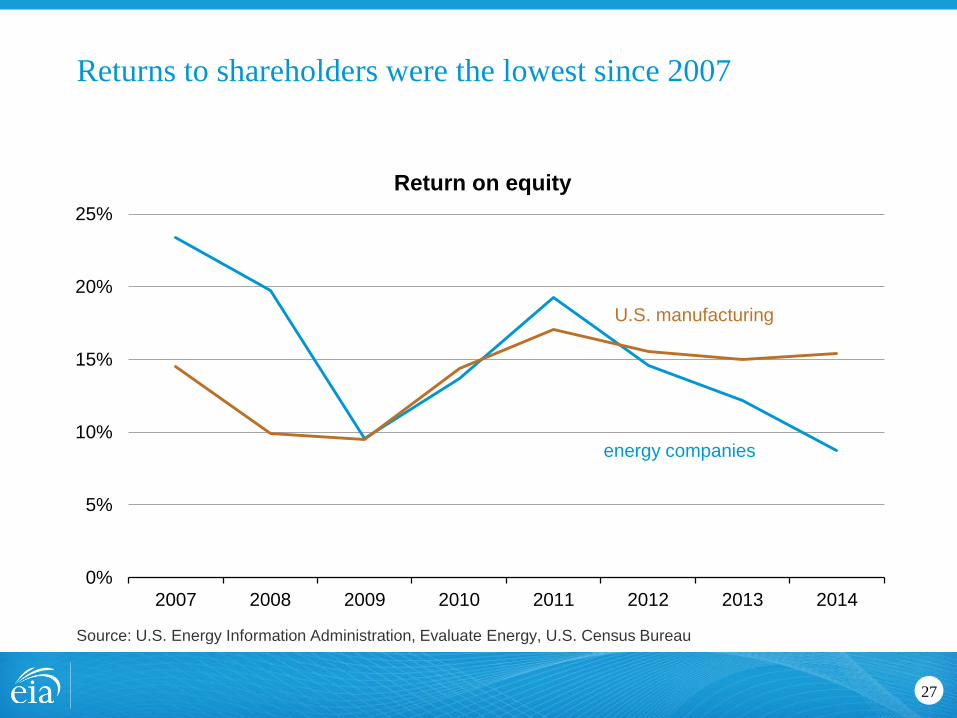

Returns to shareholders were the lowest since 2007

27

Source: U.S. Energy Information Administration, Evaluate Energy, U.S. Census Bureau

0%

5%

10%

15%

20%

25%

2007 2008 2009 2010 2011 2012 2013 2014

Return on equity

energy companies

U.S. manufacturing

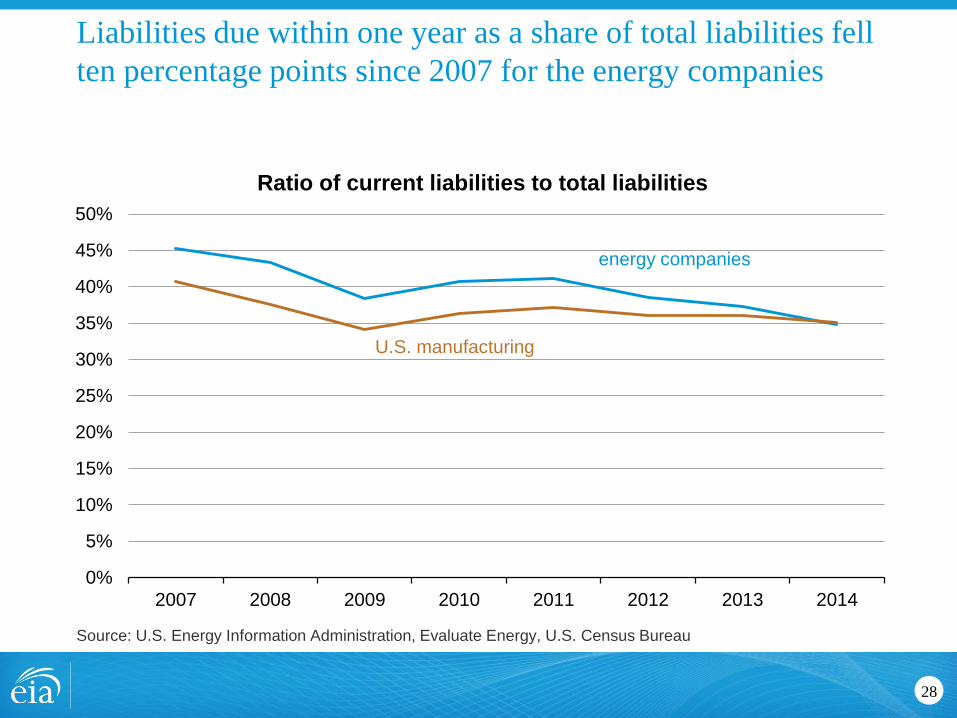

Liabilities due within one year as a share of total liabilities fell

ten percentage points since 2007 for the energy companies

28

Source: U.S. Energy Information Administration, Evaluate Energy, U.S. Census Bureau

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2007 2008 2009 2010 2011 2012 2013 2014

Ratio of current liabilities to total liabilities

U.S. manufacturing

energy companies

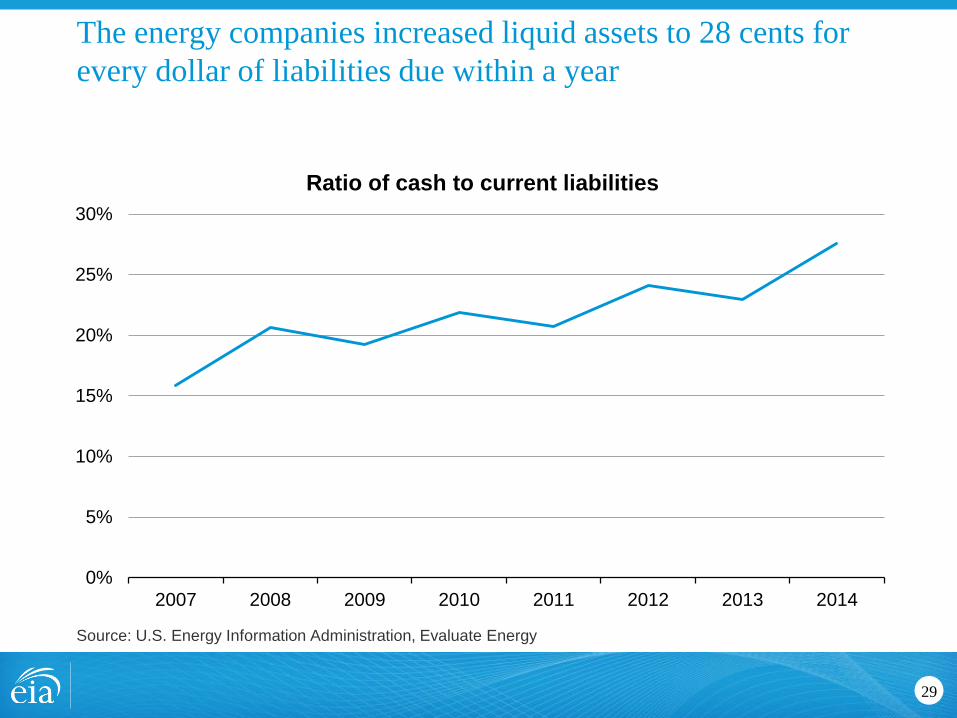

The energy companies increased liquid assets to 28 cents for

every dollar of liabilities due within a year

29

Source: U.S. Energy Information Administration, Evaluate Energy

0%

5%

10%

15%

20%

25%

30%

2007 2008 2009 2010 2011 2012 2013 2014

Ratio of cash to current liabilities

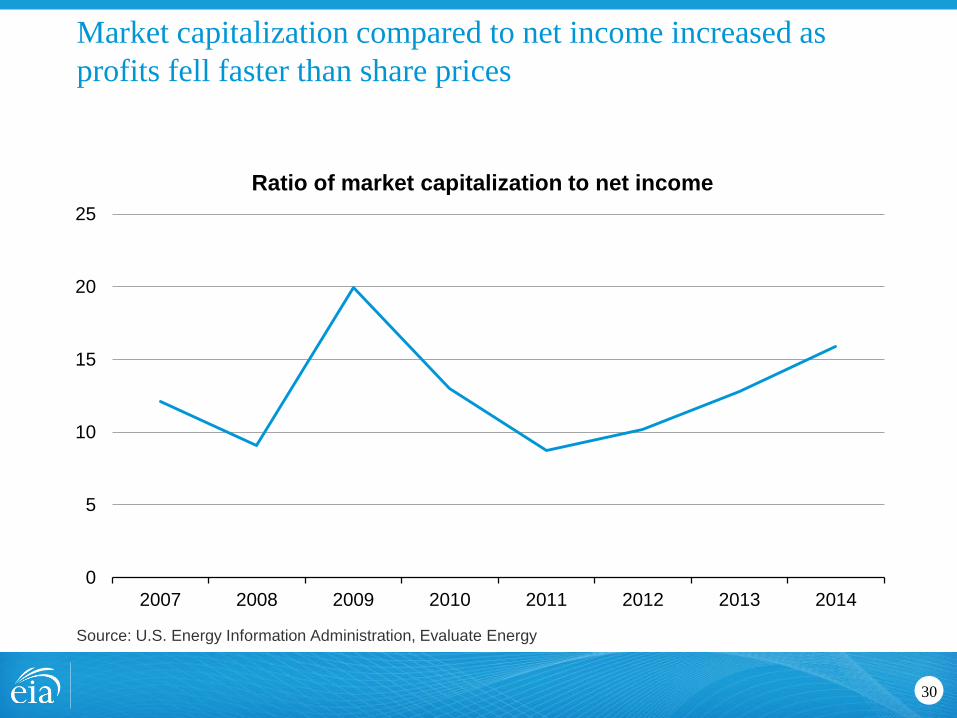

Market capitalization compared to net income increased as

profits fell faster than share prices

30

Source: U.S. Energy Information Administration, Evaluate Energy

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014

Ratio of market capitalization to net income

Appendix: list of companies

31

Source: U.S. Energy Information Administration, Evaluate Energy

Note: Some companies exist that merged or split before 2014. A total of 75 companies existed for 2014

Anadarko Petroleum Corp. EOG Resources Parsley Energy Inc.

Apache Corporation EPL Oil & Gas Inc PDC Energy

Apco Oil and Gas International Inc ExxonMobil Penn Virginia

Approach Resources Inc Forest Oil Corporation Petro-Canada

Athlon Energy Inc. Freeport-McMoRan Inc. Petrohawk Energy Corp

ATP Oil & Gas Corp. Gazprom Neft Pioneer Natural Resources Company

Berry Petroleum Co. Goodrich Petroleum Corp Plains Exploration & Production

BG Group Gulfport Energy Corporation QEP Resources Inc

BHP Billiton Halcon Resources Corporation Range Resources Corp

Bill Barrett Corporation Hess Corp Rosetta Resources Inc.

Black Hills Corp Husky Energy Inc. Royal Dutch Shell

BP Imperial Oil Limited Sanchez Energy Corp

Canacol Energy Ltd. Kodiak Oil & Gas Corp. SandRidge Energy

Carrizo Oil & Gas, Inc Laredo Petroleum Sinopec

Cenovus Energy Inc. Linn Energy SM Energy Company

Chesapeake Energy Corp. Lukoil (US GAAP) Sonde Resources Corp.

Chevron Magnum Hunter Resources Statoil ASA

Cimarex Energy Co. Marathon Oil Corp. Stone Energy

Clayton Williams Energy Mariner Energy Suncor Energy Inc.

Comstock Resources McMoRan Exploration Co. Swift Energy Co

Concho Resources Inc MDU Resources Group Synergy Resources Corporation

ConocoPhillips Murphy Oil Corporation Total

Continental Resources Newfield Exploration Company Triangle Petroleum Corporation

Denbury Resources Inc. Noble Energy Unit Corp

Devon Energy Corporation Northern Oil & Gas, Inc W & T Offshore

Encana Corporation Novatek Whiting Petroleum Corporation

Energen Corp Oasis Petroleum Inc. WPX Energy

Energy XXI Occidental XTO

Enerplus Corporation OMV YPF Sociedad Anonima

ENI Pacific Rubiales Energy Corp.

Refining

32

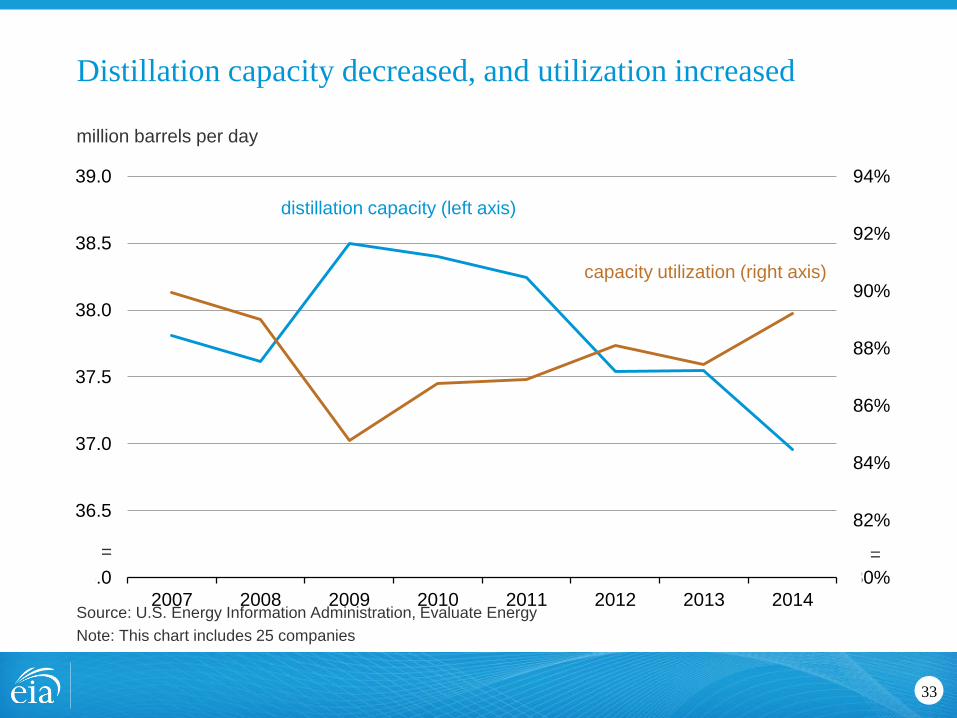

Distillation capacity decreased, and utilization increased

33

million barrels per day

Source: U.S. Energy Information Administration, Evaluate Energy

Note: This chart includes 25 companies

80%

82%

84%

86%

88%

90%

92%

94%

36.0

36.5

37.0

37.5

38.0

38.5

39.0

2007 2008 2009 2010 2011 2012 2013 2014

distillation capacity (left axis)

capacity utilization (right axis)

= =

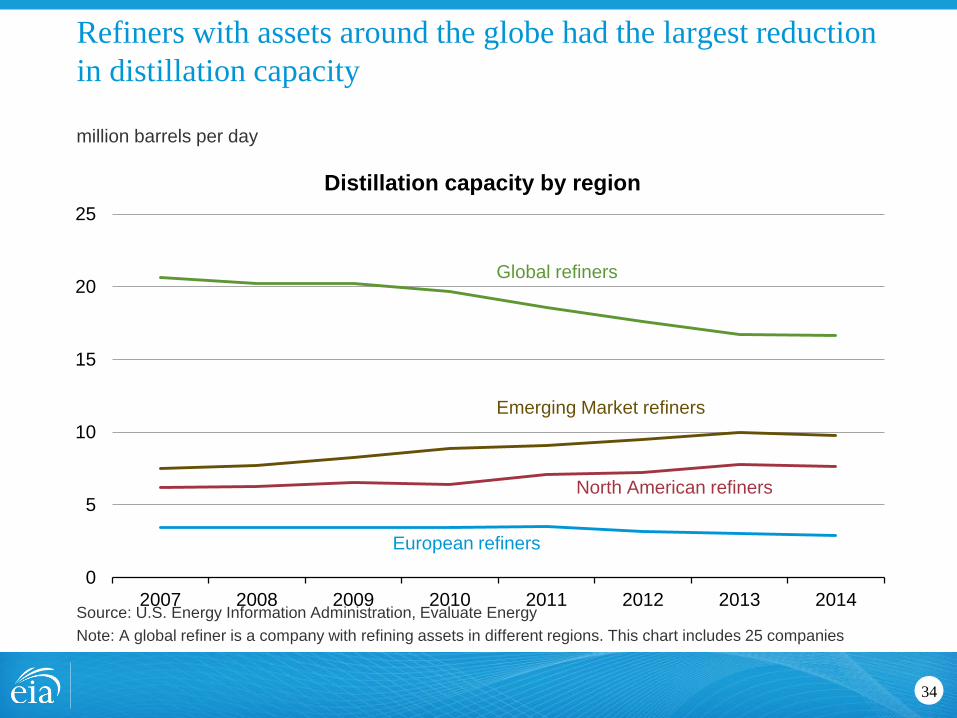

Refiners with assets around the globe had the largest reduction

in distillation capacity

34

million barrels per day

Source: U.S. Energy Information Administration, Evaluate Energy

Note: A global refiner is a company with refining assets in different regions. This chart includes 25 companies

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014

Distillation capacity by region

North American refiners

Global refiners

European refiners

Emerging Market refiners

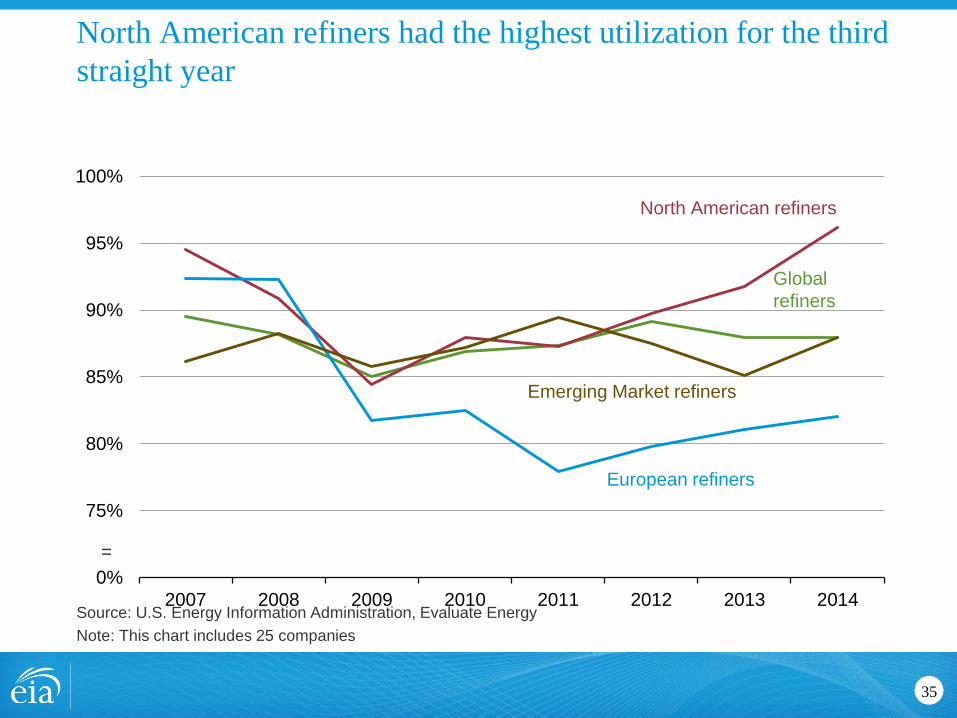

North American refiners had the highest utilization for the third

straight year

35

Source: U.S. Energy Information Administration, Evaluate Energy

Note: This chart includes 25 companies

70%

75%

80%

85%

90%

95%

100%

2007 2008 2009 2010 2011 2012 2013 2014

North American refiners

Emerging Market refiners

Global

refiners

European refiners

=

Refining capital expenditures declined, although they increased

as a share of total capital expenditures

36

billion 2014 dollars

Source: U.S. Energy Information Administration, Evaluate Energy

Note: This chart includes 31 companies

0%

4%

8%

12%

16%

20%

24%

28%

32%

36%

0

10

20

30

40

50

60

70

80

90

2007 2008 2009 2010 2011 2012 2013 2014

refining capital expenditures (left axis)

share of total capital expenditures (right axis)

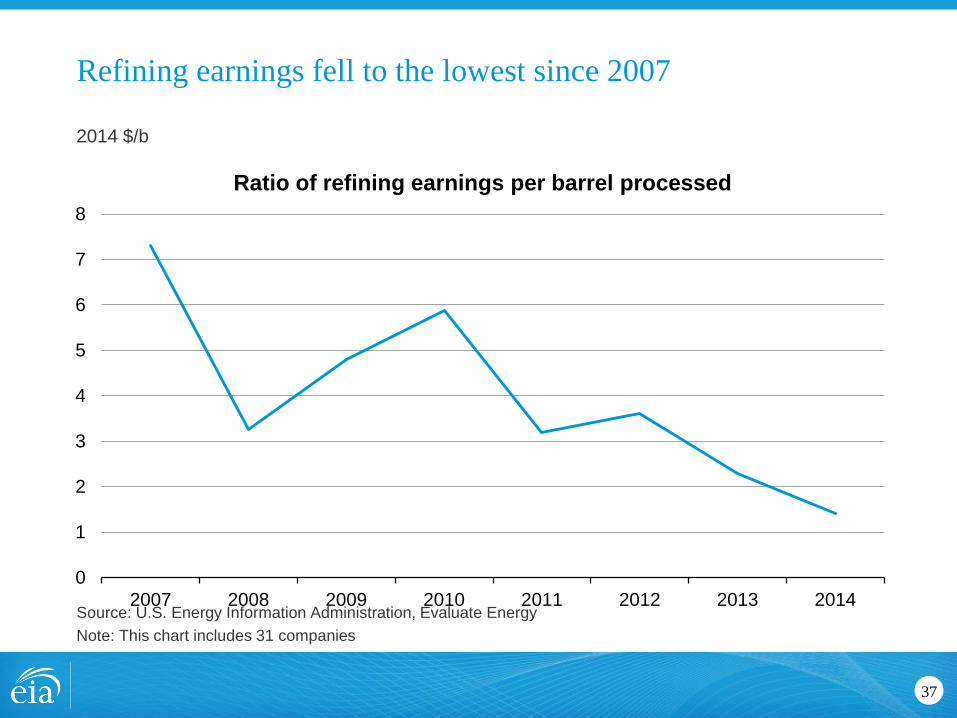

Refining earnings fell to the lowest since 2007

37

2014 $/b

Source: U.S. Energy Information Administration, Evaluate Energy

Note: This chart includes 31 companies

0

1

2

3

4

5

6

7

8

2007 2008 2009 2010 2011 2012 2013 2014

Ratio of refining earnings per barrel processed

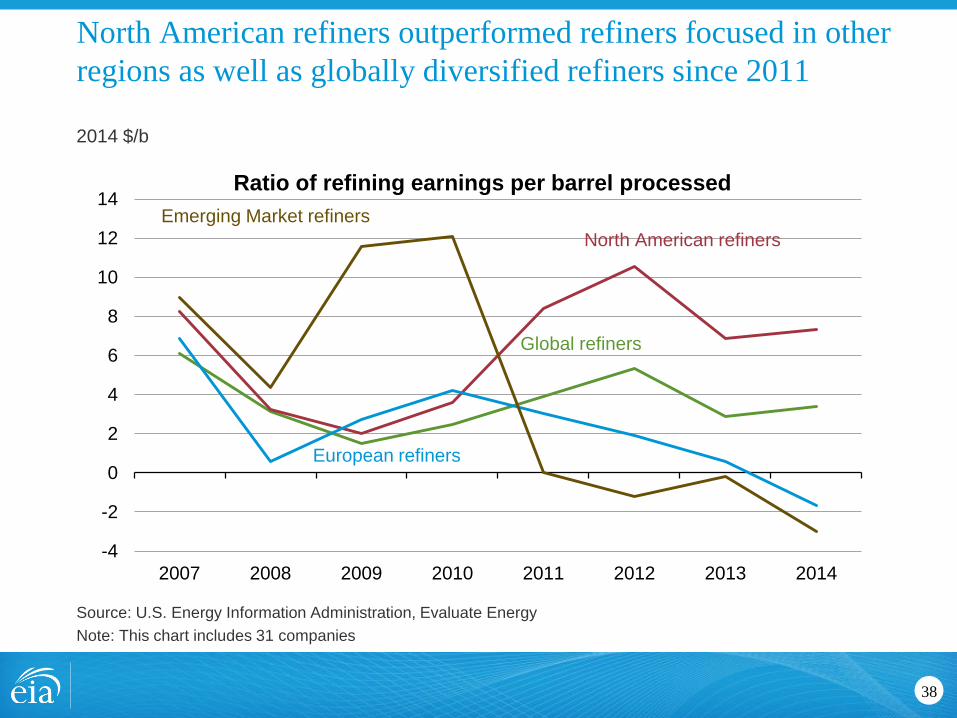

North American refiners outperformed refiners focused in other

regions as well as globally diversified refiners since 2011

38

2014 $/b

Source: U.S. Energy Information Administration, Evaluate Energy

Note: This chart includes 31 companies

-4

-2

0

2

4

6

8

10

12

14

2007 2008 2009 2010 2011 2012 2013 2014

Ratio of refining earnings per barrel processed

North American refiners

Global refiners

European refiners

Emerging Market refiners

Appendix: list of companies

39

Source: U.S. Energy Information Administration, Evaluate Energy

Note: Some companies exist that merged or split before 2014. A total of 31 companies existed for 2014

Alon USA Energy Lukoil (US GAAP) Rosneft

BP Marathon Oil Corp. Royal Dutch Shell

Chevron Marathon Petroleum Corporation Sinopec

ConocoPhillips MOL Suncor Energy Inc.

Delek US Holdings Neste Oil Tesoro Petroleum Corp.

ENI OMV TNK-BP International Ltd

ExxonMobil Petrobras (IFRS US$) Total

Grupa Lotos PetroChina TUPRAS

HollyFrontier Corp Phillips 66 Unipetrol

Husky Energy Inc. PKN Orlen Valero Energy

Imperial Oil Limited Repsol Western Refining

Indian Oil Corp.

![Financial Results & Limited Review for March 31, 2013 [Result]](https://static.fdocuments.us/doc/165x107/577ca8101a28abea748cb398/financial-results-limited-review-for-march-31-2013-result.jpg)