2013 ATM Software Trends and Analysis and published by Sponsored by 2013 ATM Software Trends and...

63

Developed and published by Sponsored by 2013 ATM Software Trends and Analysis 6th Edition ATMs and other self-service devices are changing the face of banking. In the sixth edition of the annual survey, learn what the industry thinks about current trends and future expectations of ATM software.

-

Upload

vuongxuyen -

Category

Documents

-

view

215 -

download

1

Transcript of 2013 ATM Software Trends and Analysis and published by Sponsored by 2013 ATM Software Trends and...

Developed and published by Sponsored by

2013 ATM Software Trends and Analysis

6th Edition

ATMs and other self-service devices are changing the face of banking. In the sixth edition of the annual survey, learn what the industry thinks about current trends and future expectations of ATM software.

© 2013 Networld Media Group | Sponsored by KAL 2

Page 3 About the sponsors

Page 4 Contributing organizations

Page 5 Introduction Knowing the customer Falling by the wayside

Page 8 Chapter 1 ATM survey analysis: A general overview Visa expands EMV roadmap to include ATMs The first meaningful acquirer deadlines Visa ATM upgrade dates fall later, but does it matter? Enabling ‘faster, simpler, more cost-effective implementation’ Offering free AID help for ATM transaction acquirers Repeated assurance: greater security, lower risk

Page 29 Chapter 2 A regional focus: The Americas Smartphone integration reaching critical mass

Page 40 Chapter 3 A regional focus: Europe, the Middle East and Africa Serving the unbanked

Page 51 Chapter 4 A regional focus: Asia-Pacific Preparing for the Branch of the Future The changing face of transactions Eliminating the lines

Page 63 Conclusion ATMs and self-service systems remain crucial for the future of financial retail delivery

2013 ATM Software Trends and Analysis

© 2013 Networld Media Group | Sponsored by KAL 3

Published by Networld Media Group© 2013 Networld Media GroupWritten by Richard Slawsky, contributing writer, ATMmarketplace.com.Alan Fryrear, CEOTom Harper, presidentJoseph Grove, vice president and executive editorTiffany Lauletta, custom content editor

ATMmarketplace.com, owned and operated by Louisville, Ky.-based Networld Media Group, is the world’s largest online provider of information about and for the ATM industry. The content, which is updated every business day and read by business and industry professionals throughout the world, is free.

An independent company, KAL is recognized as the world’s leading ATM software company, providing solutions to some of the world’s megabanks, such as Citi, China Construction Bank and UniCredit. KAL software is installed and supported around the world in more than 80 countries, enabling banks of all sizes to reduce costs and improve competitiveness.

© 2013 Networld Media Group | Sponsored by KAL 4

Bank of New Zealand Bendigo Bank (Australia) Diebold GE Money Bank Czech Republic) KAL (sponsor) NCR PostFinance (Switzerland) Redsys (Spain) SIBS (Portugal) Unicredt Group (Italy) Wells Fargo (USA) Westpac Bank (Australia) Wincor Nixdorf Yes Bank (India) YourCash (UK) Zijin Technology (China)

contributing organizations

© 2013 Networld Media Group | Sponsored by KAL 5

or the sixth year in a row ATMmar-ketplace.com surveyed individuals in the financial industry to compile the

“ATM Software Trends and Analysis” guide, illustrating ATM trends around the globe. Once again we take a look at what’s hap-pening in the world of ATM software and the role ATMs play in serving a financial institution’s customers. As with previous editions of the guide, the goal for the 2013 edition is to provide a tool those institu-tions can use in mapping out their plans for the future.

As with most industries, changes in the financial world are often slow to occur, with trends becoming evident only when glimpsed over the course of several years. Where appropriate, we compare survey re-sponses to those of previous years as a way to get a sense of how attitudes are shifting. In some areas, though, events such as the economic uncertainty of the past few years and the emergence of technology such as smartphones have prompted some changes to occur more quickly.

One thing has become abundantly clear in recent years, however. When it comes to physical interactions between a bank and its customers, the ATM is key.

“When you consider that your highest-value customers and the rest of your cus-tomer base as well transact with the bank almost exclusively through the ATM and the website, that tends to be their complete perception of the bank,” said Aravinda Korala, CEO of Edinburgh, Scotland-based ATM software provider KAL. “The transactions you offer are very important as is the look and feel of the application. If you’ve got green screens with black-and-

By Richard SlawskyContributing writer,ATMmarketplace.com

white text versus an up-to-date user inter-face, your customers are going to view you as outdated.”

Nearly everyone ATMMarketplace talked with regarding the topic concurred with Korala’s assessment.

“Customers who receive a technologically savvy, yet convenient service from their bank are more than likely going to be a ‘happy customer’ and creating this all im-portant customer experience is the only thing I believe banks are truly able to com-pete on in this economic climate,” said Jenny Campbell, CEO of UK-based independent ATM deployer YourCash Ltd. The company operates more than 6,000 ATMs throughout the United Kingdom and Europe.

“Face-to-face banking is in decline, mobile on the rise and Internet banking is widespread,” Campbell said. “What you have left therefore is the ATM estate providing one of the only points at which customers can physically interact with their banking provider without ever stepping in to their branch.”

Knowing the customer One of the top areas of interest regarding ATMs since the inaugural ATM Software Trends and Analysis guide in 2007-2008 is that of personalization of the user experi-ence at the ATM, particularly in terms of targeted marketing.

When it comes to physical interactions between a bank and its

customers, the ATM is key.

F

© 2013 Networld Media Group | Sponsored by KAL 6

When asked the question “What is the most critical change your organization needs to make to its ATM network in 2013” one of the top responses was “Create a better customer experience at the ATM.” And when asked “What are the most im-portant future capabilities of the ATM channel that would improve the customer experience?” one of the top responses was “Targeted 1-to-1 marketing of bank prod-ucts and services.”

“There isn’t a single bank RFP that I’ve seen in the last three years that hasn’t talked about marketing campaigns,” Korala said. “Every single bank wants that, but it’s about making sure that you do it well and you’re not going to annoy customers by putting up the same campaigns every day.”

In other words, it’s not enough to simply use the ATM screen as a delivery vehicle for advertisements. Those messages not only must be relevant to the customer but relevant to the customer’s relationship and prior interactions with the institution.

“If I’m looking for product on the bank’s website I don’t want to get a different marketing message the next time I visit the ATM,” said Thomas Daubenbuechel, spokesman for Paderborn, Germany-based ATM manufacturer Wincor Nixdorf. “If I’m looking for a mortgage I don’t want to see a message about financing a car. I would expect the bank to be intelligent enough that they only deliver to me the services that I really want.”

And because consumers are interacting with the institution across multiple chan-nels, those channels need to be able to

communicate with each other to avoid burdening them with messages in which they aren’t interested.

“If you deliver a message by one channel and the customer says “no thanks, I don’t want to take advantage of that today’ you need to immediately transfer that across multiple channels, so two hours later they don’t get the same message on another channel,” said Robert Johnston, marketing director of ATM software with Duluth, Ga.-based technology company NCR. “That doesn’t just apply to the marketing channel. It also means having the ability to, for example, take a mortgage application that someone started on the Internet chan-nel and complete it on their mobile phone or some other channel.”

It’s important to recognize, however, that customers expect their ATM transactions to be swift. Although the institution may have a few seconds to deliver targeted mes-saging to customers, it’s important to re-member that it’s the customer’s time, and any perception that they are being forced to wait for their transaction to complete so a message can be delivered will likely have a negative effect.

Not only does the ability to tailor the ATM transaction to individual customers make for a more personal experience, it offers the bank the ability to deliver targeted messages to that customer.

© 2013 Networld Media Group | Sponsored by KAL 7

“We have an opportunity where we have customers’ undivided attention for a few seconds to make them aware of new offers and services they may be eligible for, but we need to use this channel judiciously,” said Charlie Tanos, manager, ATM channels, network operations & footprint optimiza-tion at Sydney, Australia-based Westpac Bank. “Otherwise it becomes ‘white noise’ and customers will ignore those messages.”

Falling by the waysideAs technology develops and changes, the concept of offering a particular function or service occasionally holds an appeal that doesn’t quite deliver in practice. The ATM channel is no different.

A few years ago, the idea of dispensing with cards and PINs in favor of biomet-ric identification was gaining traction. In 2012, for example, more than 35 percent of survey respondents from all regions of the world indicated biometrics as one of the drivers behind considering upgrading ATM software. This year, that number fell to closer to 30 percent. In addition, bio-metric customer identification was ranked in the bottom half of future capabilities that could improve the customer experi-ence at the ATM channel.

A number of factors contributed to the waning interest in biometric capabilities. Top among those are a fear among con-sumers about banks having access to such sensitive information and the association in consumers’ minds of “fingerprints” with “criminal.” In addition, for biometrics to become widespread it would be necessary for institutions to not only agree on stan-

dards for biometrics but to share that in-formation between institutions. Otherwise, institutions would be limited to providing ATM access only to their own customers.

“Ultimately, the hardware expenditure would probably far outweigh the benefits of offering biometrics,” said Anton Marrone, manager, ATM deployment & operations at Bendigo, Australia-based Bendigo Bank.

There are scenarios where biometrics still has promise, though. In Japan, some banks are offering biometrics as an additional identification pathway for customers who wish to use the ATM to withdraw amounts above the normal transaction limits, while banks in India are looking at the govern-ment’s push to build a universal database of biometric information of its 1.2 billion citi-zens as a way to bring citizens without iden-tification papers into the banking system.

Another area that hasn’t quite gained the anticipated traction is videoconferencing. Although video interactions with offsite call centers has potential in the branch of the future (discussed later in this guide) it’s not likely to be part of the street corner ATM.

“The problem with video conferencing at the ATM is that it’s not a very private expe-rience and of course the whole transaction experience is much longer,” said KAL Di-rector of Engineering Michel Denis.

“It has to be used only in certain cases and in certain places,” Denis said. “The last thing you want when you are withdraw-ing cash is to have a line of people because someone is doing a video conference.”

© 2013 Networld Media Group | Sponsored by KAL 8

or the sixth time ATMMarketplace.com surveyed ATM executives around the world to learn what

trends they are seeing in terms of ATM software, functionality and the role ATMs will play in the future. We spoke with in-dustry leaders around the globe to gain their insights.

As with previous years many of the ques-tions we asked involved how those execu-tives plan to keep their networks competi-tive. In addition, we asked about new chal-lenges and opportunities financial institu-tions faced with their networks and how

F they planned to address those challenges and take advantage of those opportunities.

This year’s survey continued the trend of in-creasing the number of respondents. Nearly 10 percent more industry experts took part in the survey compared with last year.

We thank the industry leaders from around the globe who shared their insights via this survey. Here’s an overview of their respons-es, as well as comparisons with previous surveys where data are available. Subse-quent chapters will analyze responses on a regional basis.

Total survey respondents: 867

1: Is your company a financial institution?

No 56%

Yes 44%

© 2013 Networld Media Group | Sponsored by KAL 9

2. Respondent breakdown by region

2013 2012 2011

Asia 18% 19% 18%

Australia 5% 4% 2%

Europe 30% 28% 23%

Latin America 8% 7% 10%

Middle East/Africa 11% 13% 12%

United States and Canada 28% 29% 35%

The distribution of respondents by region has held relatively stable throughout the history of the survey, with the greatest number of respondents coming from Europe.

3. How many ATMs do you have?

1-100 25%

101-500 20%

501-2,000 20%

2,001 or more 35%

© 2013 Networld Media Group | Sponsored by KAL 10

5. Which statement best identifies your organization’s current approach to the development of ATM software?

4. Which statement best identifies your organization’s ATM software strategy?

Our ATM so*ware and hardware is from a single manufacturer

We have one standardized ATM so*ware environment on ATMs from mul;ple manufacturers (mul;-‐vendor so*ware)

We use the so*ware supplied by the manufacturer (i.e., NCR so*ware on NCR ATMs, Diebold so*ware on Diebold ATMs) and see no need to change

We have so*ware supplied by the ATM manufacturer(s) but are considering mul;-‐vendor ATM so*ware

Our ATM software and hardware is from a single

manufacturer23%

We have one standardized ATM software environment on ATMs from

multiple manufacturers (multi-vendor software)

35%

We use the software supplied by the manufacturer (i.e., NCR software on NCR ATMs, Diebold software on Diebold ATMs) and see no need to

change22%

We have software supplied by the ATM manufacturer(s) but are

considering multi-vendor ATM software

20%

Mergers and acquisitions among financial institutions as well as changing ATM models means many deployers are operating ATM fleets comprised of models from a number of manufacturers.

We develop and maintain our own proprietary ATM

application.14%

We develop and maintain our own proprietary ATM applica6on.

We rely on our ATM hardware vendor to develop and maintain our ATM so:ware.

We rely on our ATM so:ware vendor to develop and maintain our ATM so:ware.

We license ATM so:ware from a vendor, but we make ongoing changes to it.

We rely on our ATM hardware vendor to

develop and maintain our ATM software.

39%

I am not sure what we do.7%

We license ATM software from a vendor, but we make ongoing

changes to it.18%

We rely on our ATM software vendor to develop and

maintain our ATM software.22%

© 2013 Networld Media Group | Sponsored by KAL 11

6: Are there plans to replace your current ATM software?

2013 2012 2011

Yes, planned and budgeted for 2013 20% 25% 17%

Yes, planning for either 2014 or 2015 22% 23% 26%

No, we recently replaced it 18% 12% 11%

No, there are no plans to replace the existing ATM software 30% 23% 27%

Not applicable 10% 17% 19%

7. What are the primary drivers for changing ATM software? (Choose the THREE most important.)

Support for new technology (such as contactless cards, mobile phone integration, coin handling, cash recycling)

Increase security (such as EMV, 3DES, Remote Key, Biometrics)

Increase our operational productivity and efficiency

Provide an enhanced user experience

Reduce the cost of operating our ATM network

Improve customer service

Support Windows 7 or 8

Add new functionality such as deposit automation

Improve ATM availability

Be able to readily update ATM software when needed

Better promotion of new bank services

Compliance with PCI/disabled user accessibility regulations

Be able to negotiate better prices for new ATM hardware

Other

20%

6%

24%

26%

28%

12%

26%

13%

23%

18%

19%

35%

17%

2%

© 2013 Networld Media Group | Sponsored by KAL 12

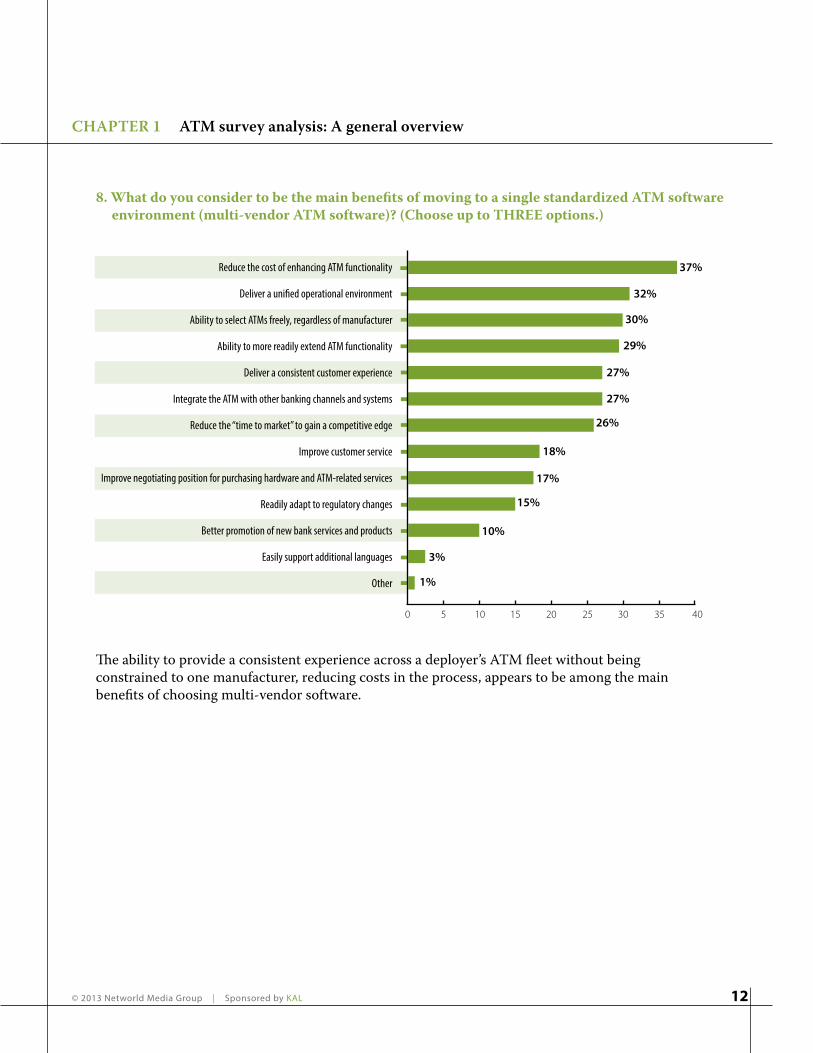

8. What do you consider to be the main benefits of moving to a single standardized ATM software environment (multi-vendor ATM software)? (Choose up to THREE options.)

The ability to provide a consistent experience across a deployer’s ATM fleet without being constrained to one manufacturer, reducing costs in the process, appears to be among the main benefits of choosing multi-vendor software.

Reduce the cost of enhancing ATM functionality

Deliver a unified operational environment

Ability to select ATMs freely, regardless of manufacturer

Ability to more readily extend ATM functionality

Deliver a consistent customer experience

Integrate the ATM with other banking channels and systems

Reduce the “time to market” to gain a competitive edge

Improve customer service

Improve negotiating position for purchasing hardware and ATM-related services

Readily adapt to regulatory changes

Better promotion of new bank services and products

Easily support additional languages

Other

30%

17%

37%

3%

15%

26%

27%

27%

29%

32%

10%

18%

1%

© 2013 Networld Media Group | Sponsored by KAL 13

Integration of the ATM with mobile phone transactions

Contactless card support

Customize user interface based on transaction history from CRM data

Targeted 1-to-1 marketing of bank products and services

Electronic receipts for ATM transaction

Touch screen / multi-touch screen capability

Display of nearest available ATM when out-of-service

Video conferencing with bank Subject Matter Experts

Biometric customer identification

Person-to-person payments

Purchase items (e.g. tickets, stamps) using cash

Support for high quality multi-media

Call customers immediately in case of card confiscation

Card escrow - allow subsequent customer retrieval of captured card

Coin handling support

Other

15%

4%

4%

4%

34%

34%

16%

16%

24%

51%

9%

10%

6%

30%

22%

3%

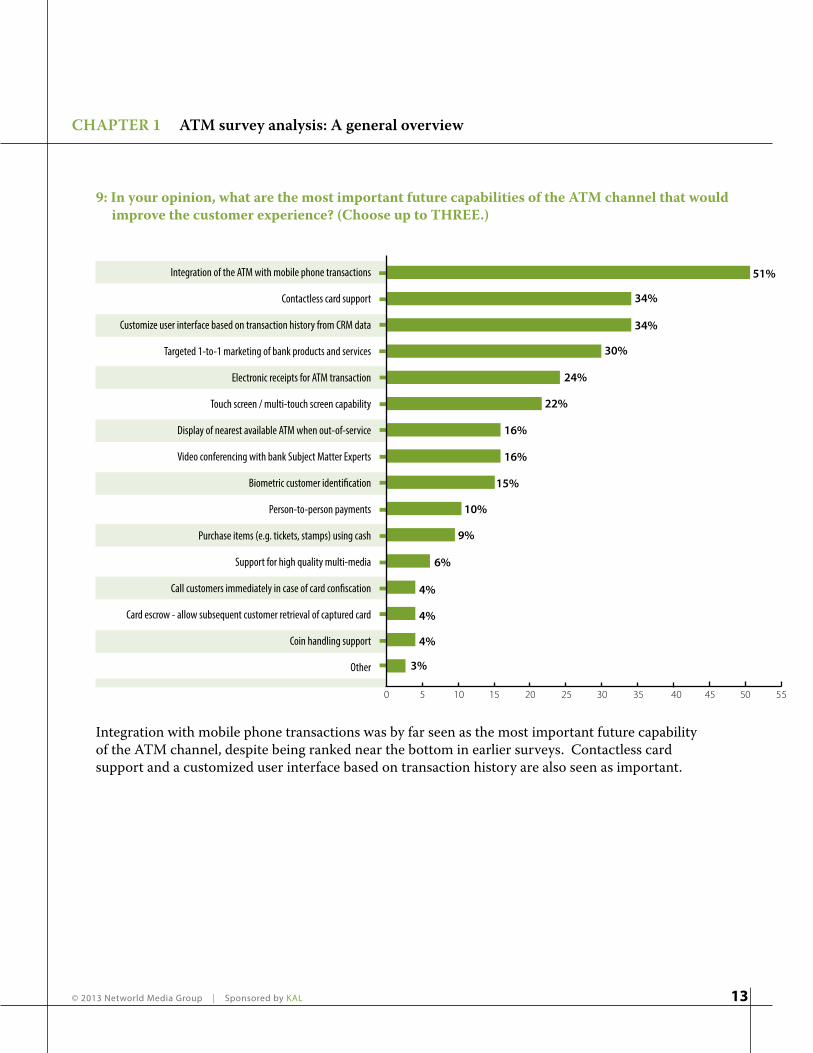

9: In your opinion, what are the most important future capabilities of the ATM channel that would improve the customer experience? (Choose up to THREE.)

Integration with mobile phone transactions was by far seen as the most important future capability of the ATM channel, despite being ranked near the bottom in earlier surveys. Contactless card support and a customized user interface based on transaction history are also seen as important.

© 2013 Networld Media Group | Sponsored by KAL 14

Improve the ATM functionality for the customer

Create a better customer experience at the ATM

Reduce operational costs

Integrate with other self-service channels such as mobile

Automate more branch transactions and move them to the ATM channel

Migrate to Windows 7 or 8

Better promotion of bank’s products and services

Remotely manage the ATM network

Adopt enhanced security technologies

Management reporting (availability, transaction volumes, SLAs)

Compliance with PCI/disabled user accessibility regulations

Distribute software updates and changes more frequently

Upgrade communications infrastructure

Reduce hardware purchasing costs

No changes needed

17%

24%

19%

12%

30%

9%

33%

26%

16%

22%

29%

8%

18%

9%

2%

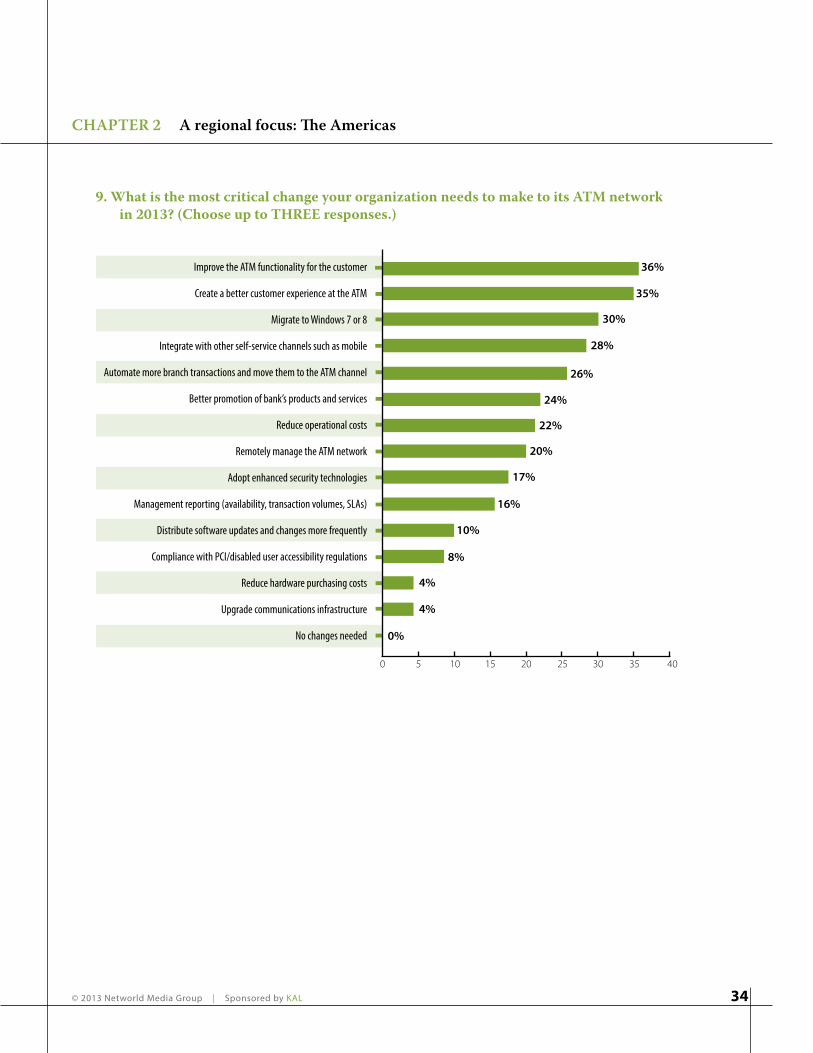

10. What is the most critical change your organization needs to make to its ATM network in 2013? (Choose up to THREE responses.)

The ATM is increasingly becoming the primary touchpoint between a bank and its customers. As such, improving that experience is becoming more and more important.

© 2013 Networld Media Group | Sponsored by KAL 15

11: Which statement best identifies your organization’s opinion regarding the future direction of the ATM operating system environment?

We will only change from Windows XP when we absolutely have to change.

We will need to begin migra:ng to Windows 7 or 8 now or within the next two years.

We will need to complete our upgrade to Windows 7 or 8 within the next two years.

We would like to have the choice of running a non-‐MicrosoB opera:ng system (e.g., Linux).

Other1%No opinion

18%

We would like to have the choice of running a

non-Microsoft operating system (e.g., Linux).

9%

We will need to complete our upgrade to Windows 7 or 8 within the next two years.

20%

We will need to begin migrating to Windows

7 or 8 now or within the next two years.

30%

We will only change from Windows XP when we

absolutely have to change.23%

© 2013 Networld Media Group | Sponsored by KAL 16

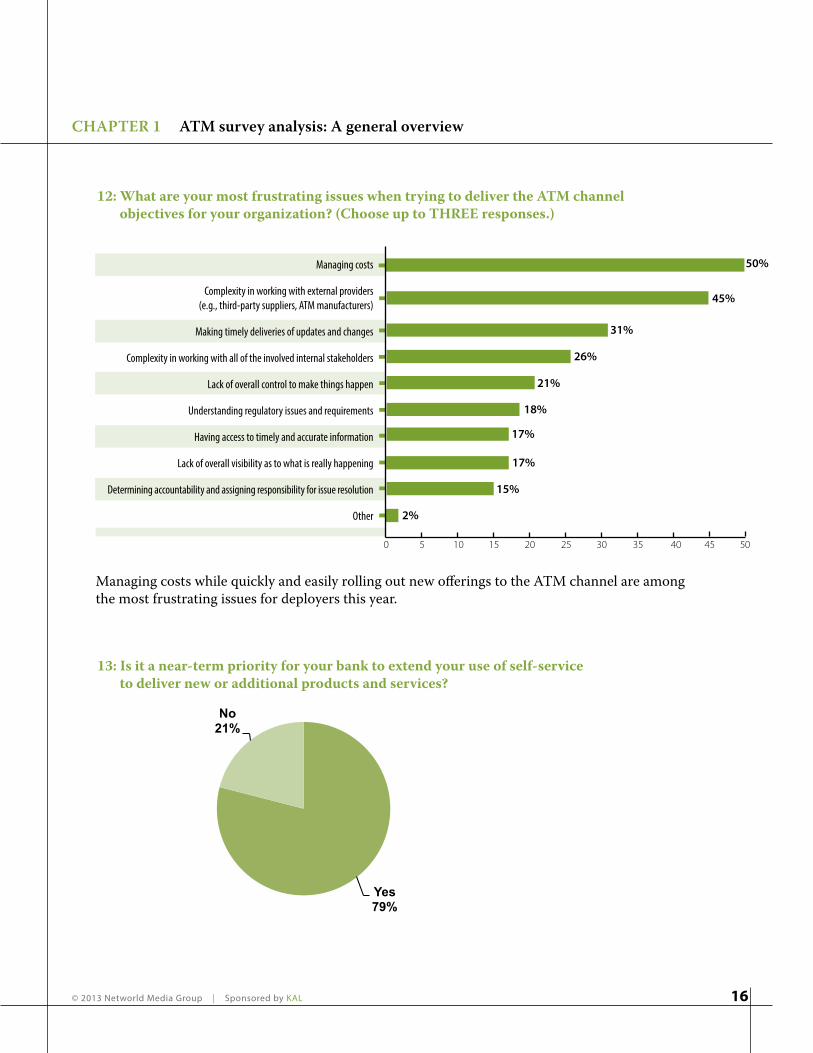

12: What are your most frustrating issues when trying to deliver the ATM channel objectives for your organization? (Choose up to THREE responses.)

Managing costs

Complexity in working with external providers (e.g., third-party suppliers, ATM manufacturers)

Making timely deliveries of updates and changes

Complexity in working with all of the involved internal stakeholders

Lack of overall control to make things happen

Understanding regulatory issues and requirements

Having access to timely and accurate information

Lack of overall visibility as to what is really happening

Determining accountability and assigning responsibility for issue resolution

Other

26%

45%

15%

21%

17%

31%

50%

17%

18%

2%

Managing costs while quickly and easily rolling out new offerings to the ATM channel are among the most frustrating issues for deployers this year.

Yes 79%

No 21%

13: Is it a near-term priority for your bank to extend your use of self-service to deliver new or additional products and services?

© 2013 Networld Media Group | Sponsored by KAL 17

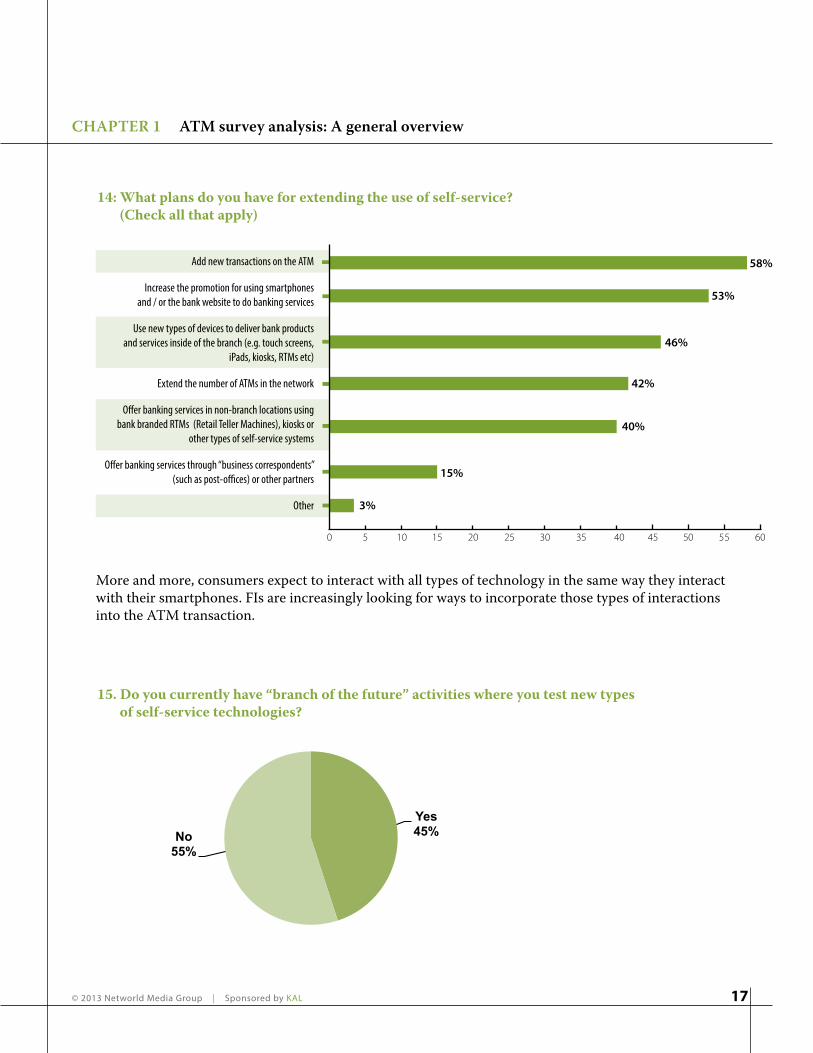

14: What plans do you have for extending the use of self-service? (Check all that apply)

Add new transactions on the ATM

Increase the promotion for using smartphones and / or the bank website to do banking services

Use new types of devices to deliver bank products and services inside of the branch (e.g. touch screens,

iPads, kiosks, RTMs etc)

Extend the number of ATMs in the network

Offer banking services in non-branch locations using bank branded RTMs (Retail Teller Machines), kiosks or

other types of self-service systems

Offer banking services through “business correspondents” (such as post-offices) or other partners

Other

42%

58%

46%

40%

15%

53%

3%

60

More and more, consumers expect to interact with all types of technology in the same way they interact with their smartphones. FIs are increasingly looking for ways to incorporate those types of interactions into the ATM transaction.

15. Do you currently have “branch of the future” activities where you test new types of self-service technologies?

Yes 45% No

55%

© 2013 Networld Media Group | Sponsored by KAL 18

Vendors/IADs/Service companies

1: Please select the category below that best identifies your organization.

ATM Manufacturer / Vendor27%

ATM Maintenance or Service Company

22%Non-bank deployer (ISO / IAD)

13%

Other28%

Processor or EFT Network

10%

ATM Manufacturer / Vendor

ATM Maintenance or Service Company

Non-‐bank deployer (ISO / IAD)

Processor or EFT Network

Other

© 2013 Networld Media Group | Sponsored by KAL 19

2: What are the most critical changes you see your customers wanting to make to their ATM networks in 2013? (Choose up to THREE responses.)

Reduce operational costs

Improve the ATM functionality for the customer

Integrate with other self-service channels such as mobile

Create a better customer experience at the ATM

Automate more branch transactions and move them to the ATM channel

Reduce hardware purchasing costs

Adopt enhanced security technologies

Remotely manage the ATM network

Better promotion of bank’s products and services

Compliance with PCI/disabled user accessibility regulations

Management reporting (availability, transaction volumes, SLAs)

Support Windows 7 or 8

Distribute software updates and changes more frequently

Upgrade communications infrastructure

No changes needed

20%

22%

14%

12%

24%

9%

22%

31%

18%

28%

10%

12%

6%

45%

2%

Cutting operational costs is by far the most critical change ATM deployers are looking to make to their ATM networks this year, with 45 percent of respondents. Improving functionality for the customer, at 31 percent, was second followed by integration with other self-service channels at 28 percent.

© 2013 Networld Media Group | Sponsored by KAL 20

3: In your opinion, what are the primary drivers for customers changing their ATM software? (Choose the THREE most important.)

Support for new technology (such as contactless cards, mobile phone integration, coin handling, cash recycling)

Reduce the cost of operating ATM network

Increase security (such as EMV, 3DES, Remote Key, Biometrics)

Add new functionality such as deposit automation

Provide an enhanced user experience

Improve ATM availability

Increase operational productivity and efficiency

Improve customer service

Better promotion of new bank services by using high-quality multi-media, real-time broadcasting

Compliance with PCI/disabled user accessibility regulations

Be able to readily update ATM software when needed

Move to Windows 7 or 8 operating system

Be able to negotiate better prices for new ATM hardware

Other

8%

35%

20%

32%

14%

22%

25%

15%

41%

19%

13%

20%

2%

10%

Support for new technology, particularly mobile phone integration, topped the list of drivers for changing ATM software, with 41 percent of respondents indicating that as primary. Reducing the cost of operating the network, at 35 percent, and increasing security, at 32 percent, were also near the top of the list.

© 2013 Networld Media Group | Sponsored by KAL 21

4: In your opinion, what are the most important future capabilities of the ATM channel that would improve the customer experience? (Choose up to THREE.)

Integration of the ATM with mobile phone transactions

Contactless card support

Touch screen / multi-touch screen capability

Customize user interface based on transaction history from CRM data

Display of nearest available ATM when out-of-service

Electronic receipts for ATM transaction

Biometric customer identification

Targeted 1-to-1 marketing of bank products and services

Person-to-person payments

Video conferencing with bank Subject Matter Experts

Purchase items (e.g. tickets, stamps) using cash

Call customers immediately in case of card confiscation

Support for high quality multi-media

Coin handling support

Other

Card escrow - allow subsequent customer retrieval of captured card

19%

11%

3%

4%

26%

23%

17%

22%

22%

6%

19%

14%

45%

24%

4%

13%

© 2013 Networld Media Group | Sponsored by KAL 22

5: Which statement best identifies your organization’s opinion regarding the future direction of the ATM operating system environment?

No opinion

We will need to begin migrating to Windows 7 or 8 now or within the next two years.

We will only change from Windows XP when we absolutely have to change.

We would like to have the choice of running a non-Microsoft operating system (e.g., Linux).

We will need to complete our upgrade to Windows 7 or 8 within the next two years.

Other

We will only change from Windows XP when we absolutely have to change.

We will need to begin migrating to Windows 7 or 8 now or within the next two years.

We will need to complete our upgrade to Windows 7 or 8 within the next two years.

We would like to have the choice of running a non-Microsoft operating system (e.g., Linux).

No opinion

Other

17%

20%

14%

17%

29%

3%

Microsoft plans to withdraw support for Windows XP in April 2014. That deadline is likely to prompt more deployers to begin considering a move to either Windows 7 or 8 or a non-Microsoft operating system.

© 2013 Networld Media Group | Sponsored by KAL 23

6: What do your customers consider to be the main benefits of moving to a single standardized ATM software environment? (Choose up to THREE options.)

Reduce the cost of enhancing ATM functionality

Ability to select ATMs freely, regardless of manufacturer

Integrate the ATM with other banking channels and systems

Deliver a consistent customer experience

Reduce the “time to market” to gain a competitive edge

Ability to more readily extend ATM functionality

Deliver a unified operational environment

Improve customer service

Improve negotiating position for purchasing hardware and ATM-related services

Readily adapt to regulatory changes

Better promotion of new bank services and products

Easily support additional languages

Other

35%

13%

24%

43%

3%

21%

12%

26%

11%

16%

31%

1%

26%

In the wake of changing technology and the number of bank mergers that have taken place over the past few years, FIs are faced with a double conundrum: Enhance ATM functionality across a variety of ATM makes and models while at the same time keeping costs in line. Part of that cost management involves being able to negotiate freely among vendors without being locked in to one particular model. The obvious way to accomplish those goals is through a single standardized ATM software environment.

© 2013 Networld Media Group | Sponsored by KAL 24

7: What are your customers’ most frustrating issues when trying to deliver their ATM channel objectives? (Choose up to THREE responses.)

Managing costs

Complexity in working with external providers (e.g., third-party suppliers, ATM manufacturers)

Making timely deliveries of updates and changes

Complexity in working with all of the involved internal stakeholders

Lack of overall control to make things happen

Understanding regulatory issues and requirements

Lack of overall visibility as to what is really happening

Determining accountability and assigning responsibility for issue resolution

Having access to timely and accurate information

Other

28%

46%

17%

24%

20%

2%

29%

49%

16%

22%

Managing costs continues to be one of the dominant themes this year, with 49 percent of respondents indicate that as their most frustrating issue when trying to deliver their ATM channel objective. AT 46 percent, complexity in working with external providers was a close second.

50

8: Is it a near-term priority for your customers to extend their use of self-service to deliver new or additional products and services?

Yes 76%

No 24%

© 2013 Networld Media Group | Sponsored by KAL 25

9: What plans do your customers have for extending their use of self-service? (Check all that apply)

Add new transactions on the ATM

Use new types of devices to deliver bank products and services inside of the branch (e.g. touch screens, iPads, kiosks, RTMs etc)

Increase the promotion for using smartphones and / or the bank website to do banking services

Offer banking services in non-branch locations using bank branded RTMs (Retail Teller Machines), Kiosks or other types of self-service systems

Extend the number of ATMs in the network

Offer banking services through “business correspondents” (such as post-offices) or other partners

Other

37%

59%

50%

43%

19%

45%

2%

Delivering new products via self-service technology is a priority for more than three fourths of survey respondents. The ATM leads the way in that regard with 59 percent of respondents indicating plans to offer new transactions at the ATM. Half of respondents plan to deploy other touchscreen devices in the branch. The Internet and smartphones, at 45 percent, also promise to serve as an extension of self service.

50 55 60

10: Do your customers currently have “branch of the future” activities where they test new types of self-service technologies?

One of the dominant buzz phrases of recent years is “branch of the future.” More than half of survey respondents are thinking about the changing bank branch when testing new self-service technology.

Yes 53%

No 47%

© 2013 Networld Media Group | Sponsored by KAL 26

Visa expands EMV roadmap to include ATMs

In February 2013, Visa announced new liability shift dates for its EMV roadmap — these affecting third-party acquirers of ATM transactions. And for them, the Visa dates represent a move forward from the existing MasterCard timeline.

The Visa deadlines are as follows:

• Effective April 1, 2015, U.S. third-party ATM acquirer processors and sub-pro-cessors must be able to support EMV chip data;

• Effective Oct., 1, 2015, liability will shift in Asia Pacific, excluding China, India, Japan and Thailand;

• Effective Oct. 1, 2017, liability will shift in China (excluding domestic trans-actions), India, Japan, Thailand, and the United States.

Additionally, Visa said that a liability shift will apply as of April 1, 2013, to all qualify-ing transactions taking place in Austra-lia and New Zealand.

Already, liability shifts are in effect for Eu-rope, Canada, Latin America and the Ca-ribbean, Central and Eastern Europe, and the Middle East and Africa.

According to Visa, the newly added dates ensure that by 2017, a single global liabil-ity policy will be in place that encourages chip-on-chip (EMV chip card read by an EMV chip card reader) transactions at both the POS and the ATM.

The first meaningful acquirer deadlines

Most in the industry expected that Visa, the first mover on EMV in the United

States, would eventually add ATM dead-lines to its roadmap. However, most may have thought they had until the Master-Card liability shift in October 2016 to up-grade their acquiring systems up to EMV compliance.

The MasterCard plan had set an April 1, 2013 liability shift deadline (blanketing both acquirers and deployers) for transac-tions using Maestro, the company’s Euro-pean debit card brand. Until now, this was the only announced acquirer deadline for the ATM industry.

And it was not an especially meaningful one. For acquirers, the number of Maestro transactions at ATMs was negligible, and many questioned the need for a rush to implementation.

For their part, ATM deployers dismissed the Maestro liability shift as a non-starter without a business case to support it.

In a May 2012 email Jerry McCarley, ex-ecutive vice president and CIO of USA Payments Systems, laid out the cost/ben-efit issues:

“This [Maestro transactions] represents 1/10,000 of 1 percent of our transaction volume. No ISO is going to pay someone to make his ATM EMV compatible for this. They will simply elect not to take [Maestro].

According to Visa, the newly added dates ensure that by 2017, a single global liability policy will be in place that encourages chip-on-chip (EMV

chip card read by an EMV chip card reader) transactions at both the POS and the ATM.

© 2013 Networld Media Group | Sponsored by KAL 27

“For example, an ASO with 100 ATMs would have $36 a year in revenue off all his ATMs in surcharge from these cards (part of which the ISO does not even get to keep) and it would cost him at least $20,000 to upgrade his 100 machines to EMV readers and software to support that $36 in revenue. So until there is a mandate that really affects them, no ISO will be spending any money on this.”

Visa ATM upgrade dates fall later, but does it matter?

In September 2012 Visa amended its roadmap to add a liability shift deadline for ATMs of Oct. 1, 2016 (MasterCard did not introduce a new acquirer deadline, apparently supposing that acquirers would have made their upgrades by the April 2013 deadline).

At that time of the MasterCard ATM li-ability shift announcement, Visa said that it had no intention of introducing ATM deadlines, and was focusing on EMV im-plementation at the POS. But over the last five months, Visa intentions changed — as most in the industry took for granted that they would.

Though the new Visa deadlines for ATMs do not take effect until October 2017— a full year after the MasterCard October 2016 deadline — Visa’s establishment of a truly meaningful third-party acquirer deadline effectively squeezes that sector’s upgrade calendars by six months.

ATM Industry Association executive di-rector David Tente said that even the 2017 deadline might be overly optimistic, given the complex system upgrades involved.

“ATMIA is pleased to see that Visa’s new

timetable for liability shifts in the U.S takes into account the added complexity of EMV migration at the ATM. Even though this is the latest of the announced ATM liabil-ity shift dates, larger deployers still do not expect to complete upgrades and replace-ments of their fleets until well past Oct, 2017.”

Enabling ‘faster, simpler, more cost-effective implementation’

Visa has also announced that in order to facilitate chip adoption and issuer compli-ance with U.S. debit regulations, the com-pany plans to provide some of its propri-etary EMV chip technology to the industry.

This approach will simplify EMV chip implementation for debit, reduce migra-tion costs and increase flexibility for card issuers, acquirer processors and merchants, Visa said.

“Our world is demanding greater flexibility and security when it comes to paying for goods and services,” said Jim McCarthy, global head of product at Visa Inc., in a statement about the announcement. “Visa’s expanded roadmap creates an environment in which new forms of electronic payment can flourish, offering security, convenience and flexibility to consumers, merchants, and issuers. As part of our commitment, we are offering the industry a com-mon U.S. debit solution that will streamline implementation of secure EMV chip tech-nology and advance the U.S. marketplace towards next generation payments, includ-ing mobile payments.”

Visa said it decided to support a common U.S. debit solution after “thorough con-sultation with industry stakeholders.” The company said the move will encourage

© 2013 Networld Media Group | Sponsored by KAL 28

adoption of EMV chip technology and will help to address regulations imposed by the Dodd-Frank Act, including the require-ment that debit card issuers offer at least two unaffiliated network routing options on their cards.

Offering free AID help for ATM transaction acquirers

Visa will make some of its EMV chip tech-nology available free of charge, relating to a generic, unbranded application identifier, or AID, that the company said will enable faster, simpler and more cost-effective implementation of EMV. This common approach would provide flexibility for is-suers to manage their card portfolios over time while facilitating merchant choice for transaction routing. Visa will also make its technology and generic U.S. debit AID available to support ATM transactions.

This solution means that issuers will con-tinue to have the flexibility to change debit networks without having to reissue cards. Debit networks that do not have their own EMV chip solutions will be able to sup-port debit chip card transactions quickly and will benefit from a tried and proven technology. All transactions can be routed to the appropriate network using the same methodology used in today’s magnetic stripe environment.

“Visa’s proposal enables chip technology to support debit routing from the point of sale or the ATM, providing the same capabilities the industry relies on today in the magnetic stripe environment, with a streamlined approach that minimizes complexity and time-to-market,” said Julie Conroy, research director at Aite Group, in the Visa announcement.

Repeated assurance: greater security, lower risk

Visa reiterated that EMV smart chip technology adds another layer of secu-rity, helping to reduce card-present fraud significantly. The company added that by encouraging investments in EMV chip technology, it is encouraging improved international interoperability and security, as well as helping to build a foundation for mobile payments.

It remains to be seen whether or when AmEx and Discover will follow suit with their own ATM implementation deadlines. But unless they move the deadline even earlier, the mat-ter is essentially moot, given deadlines set now by the two largest card brands.

© 2013 Networld Media Group | Sponsored by KAL 29

Total survey respondents: 322

1: Is your company a financial institution?

Yes 100%

2. How many ATMs do you have?

1-100 40%

101-500 25%

501-2,000 13%

2,001 or more 22%

© 2013 Networld Media Group | Sponsored by KAL 30

CHAPTER 2 A regional focus: The Americas

3. Which statement best identifies your organization’s ATM software strategy?Our ATM so*ware and hardware is from a single manufacturer

We have one standardized ATM so*ware environment on ATMs from mul;ple manufacturers (mul;-‐vendor so*ware)

We use the so*ware supplied by the manufacturer (i.e., NCR so*ware on NCR ATMs, Diebold so*ware on Diebold ATMs) and see no need to change

We have so*ware supplied by the ATM manufacturer(s) but are considering mul;-‐vendor ATM so*ware

Our ATM software and hardware is from a single manufacturer

29%

We have one standardized ATM software environment on ATMs from multiple

manufacturers (multi-vendor software)27%

We use the software supplied by the

manufacturer (i.e., NCR software on NCR ATMs,

Diebold software on Diebold ATMs) and see no

need to change27%

We have software supplied by the ATM manufacturer(s) but are considering

multi-vendor ATM software18%

4. Which statement best identifies your organization’s current approach to the development of ATM software?

We develop and maintain our own proprietary ATM application.

3%We develop and maintain our own proprietary ATM applica6on.

We rely on our ATM hardware vendor to develop and maintain our ATM so:ware

We rely on our ATM so:ware vendor to develop and maintain our ATM so:ware.

We license ATM so:ware from a vendor, but we make ongoing changes to it.

I am not sure what we do.

We rely on our ATM hardware vendor to develop and maintain

our ATM software.54%

We rely on our ATM software vendor to develop and maintain

our ATM software.20%

We license ATM software from a vendor, but we make ongoing

changes to it.15%

I am not sure what we do.8%

© 2013 Networld Media Group | Sponsored by KAL 31

2013 2012 2011

Yes, planned and budgeted for 2013 20% 19% 31%

Yes, planning for either 2014 or 2015. 20% 14% 22%

No, we recently replaced it 26% 37% 10%

No, there are no plans to replace the existing ATM software 27% 31% 17%

Not applicable 7% 0% 20%

5: Are there plans to replace your current ATM software?

Forty percent of respondents from the Americans indicated they planned to replace their ATM software either this year or next. For Europe, the Middle East and Africa that figure was 44 percent and in the Asia/Pacific region it was 43 percent.

Support for new technology (such as contactless cards, mobile phone integration, coin handling, cash recycling)

Increase security (such as EMV, 3DES, Remote Key, Biometrics)

Provide an enhanced user experience

Support Windows 7 or 8

Add new functionality such as deposit automation

Increase our operational productivity and efficiency

Be able to readily update ATM software when needed

Improve customer service

Compliance with PCI/disabled user accessibility regulations

Improve ATM availability

Reduce the cost of operating our ATM network

Better promotion of new bank services

Be able to negotiate better prices for new ATM hardware

Other

26%

4%

11%

23%

32%

12%

17%

30%

24%

38%

11%

22%

2%

18%

6. What are the primary drivers for changing ATM software? (Choose the THREE most important.)

© 2013 Networld Media Group | Sponsored by KAL 32

Support for new technology was ranked as the primary driver for changing ATM software by respondents in the Americas at 38 percent, followed by increase security at 32 percent and providing an enhanced user experience at 30 percent. In Europe, the Middle East and Africa the primary driver was reducing costs at 36 percent, support for new technology at 35 percent and providing an enhanced user experience at 29 percent. In the Asia/Pacific region enhanced security was the top driver at 38 percent, with support for new technology second at 29 percent followed by a tie between improving customer service and improving ATM availability at 23 percent.

Deliver a consistent customer experience

Deliver a unified operational environment

Integrate the ATM with other banking channels and systems

Ability to more readily extend ATM functionality

Reduce the cost of enhancing ATM functionality

Ability to select ATMs freely, regardless of manufacturer

Reduce the “time to market” to gain a competitive edge

Readily adapt to regulatory changes

Improve negotiating position for purchasing hardware and ATM-related services

Better promotion of new bank services and products

Improve customer service

Other

Easily support additional languages

24%

15%

33%

26%

1%

38%

38%

18%

24%

13%

10%

36%

2%

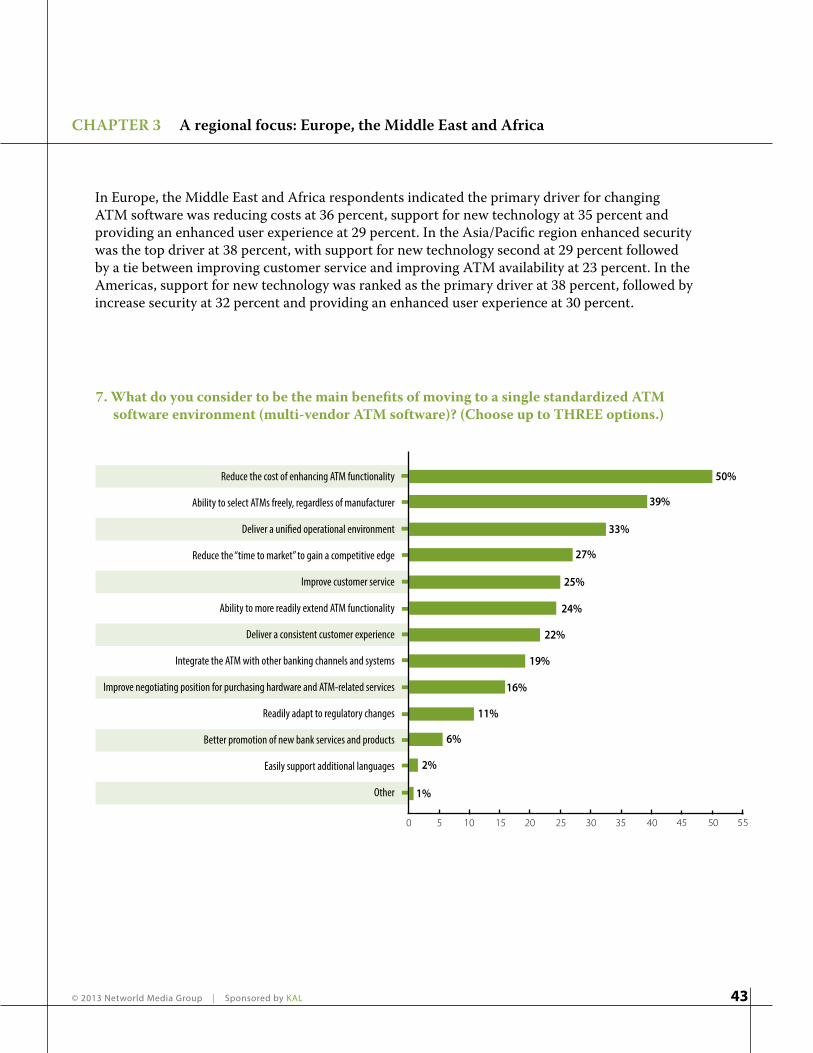

7. What do you consider to be the main benefits of moving to a single standardized ATM software environment (multi-vendor ATM software)? (Choose up to THREE options.)

© 2013 Networld Media Group | Sponsored by KAL 33

8: In your opinion, what are the most important future capabilities of the ATM channel that would improve the customer experience? (Choose up to THREE.)

At 51 percent, integration of mobile phone transactions with the ATM was by far indicated as the most important future capability of the ATM channel in the Americas, followed by a tie between electronic receipts and targeted 1-to-1 marketing at 35 percent. Mobile phone integration was also listed as a top driver in Europe, the Middle East and Africa at 50 percent, followed by contactless card support at 39 percent and a customized user interface based on transaction history from CRM data at 38 percent. In the Asia/Pacific region integration of mobile phone transactions with the ATM was the top driver at 55 percent followed by a customized user interface based on transaction history from CRM data at 33 percent and touch screen / multi-touch screen capability at 29 percent.

Integration of the ATM with mobile phone transaction

Electronic receipts for ATM transaction

Targeted 1-to-1 marketing of bank products and services

Contactless card support

Customize user interface based on transaction history from CRM data

Video conferencing with bank Subject Matter Experts

Biometric customer identification

Touch screen / multi-touch screen capability

Display of nearest available ATM when out-of-service

Purchase items (e.g. tickets, stamps) using cash

Person-to-person payments

Support for high quality multi-media

Other

Coin handling support

Call customers immediately in case of card confiscation

Card escrow - allow subsequent customer retrieval of captured card

17%

1%

1%

2%

33%

32%

13%

35%

35%

51%

11%

7%

7%

15%

19%

4%

© 2013 Networld Media Group | Sponsored by KAL 34

Improve the ATM functionality for the customer

Create a better customer experience at the ATM

Migrate to Windows 7 or 8

Integrate with other self-service channels such as mobile

Automate more branch transactions and move them to the ATM channel

Better promotion of bank’s products and services

Reduce operational costs

Remotely manage the ATM network

Adopt enhanced security technologies

Management reporting (availability, transaction volumes, SLAs)

Distribute software updates and changes more frequently

Compliance with PCI/disabled user accessibility regulations

Reduce hardware purchasing costs

Upgrade communications infrastructure

No changes needed

17%

26%

24%

8%

35%

10%

36%

28%

16%

30%

22%

4%

20%

4%

0%

9. What is the most critical change your organization needs to make to its ATM network in 2013? (Choose up to THREE responses.)

© 2013 Networld Media Group | Sponsored by KAL 35

10: Which statement best identifies your organization’s opinion regarding the future direction of the ATM operating system environment?

No opinion18%

We would like to have the choice of running a

non-Microsoft operating system (e.g., Linux).

5%

We will need to complete our upgrade to Windows 7 or 8 within the next two years.

27%

We will need to begin migrating to Windows

7 or 8 now or within the next two years.

31%

We will only change from Windows XP when we

absolutely have to change.18%

We will only change from Windows XP when we absolutely have to change.

We will need to begin migra:ng to Windows 7 or 8 now or within the next two years.

We will need to complete our upgrade to Windows 7 or 8 within the next two years.

We would like to have the choice of running a non-‐MicrosoB opera:ng system (e.g., Linux).

No opinion

11: What are your most frustrating issues when trying to deliver the ATM channel objectives for your organization? (Choose up to THREE responses.)

Complexity in working with external providers (e.g., third-party suppliers, ATM manufacturers)

Managing costs

Making timely deliveries of updates and changes

Complexity in working with all of the involved internal stakeholders

Having access to timely and accurate information

Lack of overall control to make things happen

Understanding regulatory issues and requirements

Determining accountability and assigning responsibility for issue resolution

Lack of overall visibility as to what is really happening

Other

27%

53%

14%

19%

12%

39%

50%

20%

15%

4%

© 2013 Networld Media Group | Sponsored by KAL 36

In the Americas, 53 percent of respondents listed complexity in working with external providers as their most frustrating issue when trying to deliver their ATM channel objectives followed by managing costs at 50 percent and making timely deliveries of updates and changes at 39 percent. Fifty-two percent of respondents from Europe, the Middle East and Africa listed managing costs as their most frustrating issue when trying to deliver their ATM channel objectives, followed by complexity in working with external providers at 36 percent and complexity on working with internal stakeholders at 32 percent. In the Asia/Pacific region managing costs was also top at 45 percent, followed by complexity in working with external providers at 43 percent and making timely deliveries of updates and changes at 29 percent.

12: Is it a near-term priority for your bank to extend your use of self-service to deliver new or additional products and services?

Yes 80%

No 20%

© 2013 Networld Media Group | Sponsored by KAL 37

Increasing the promotion for using smartphones and / or the bank website to do banking services was listed as a plan for extending the use of self-service by 64 percent of survey respondents in the Americas followed by a tie between adding new transactions at the ATM and the use of new devices at the branch to deliver bank products and services. Adding new transactions on the ATM was listed as a plan for extending the use of self service by 64 percent of respondents in Europe, the Middle East and Africa, followed by increasing the promotion for using smartphones and / or the bank website to do banking services at 44 percent. Using new types of devices to deliver bank products and services was listed by 39 percent of respondents from Europe, the Middle East and Africa. Sixty percent of respondents from the Asia/Pacific region listed adding new transactions at the ATM as a plan for extending the use of self-service followed by use new types of de-vices to deliver bank products and services inside of the branch at 55 percent and extending the number of ATMs in the network at 50 percent.

14. Do you currently have “branch of the future” activities where you test new types of self-service technologies?

Yes 31%

No 69%

13: What plans do you have for extending the use of self-service? (Check all that apply)

Increase the promotion for using smartphones and / or the bank website to do banking services

Add new transactions on the ATM

Use new types of devices to deliver bank products and services inside of the branch (e.g. touch screens, iPads, kiosks, RTMs etc)

Extend the number of ATMs in the network

Offer banking services in non-branch locations using bank branded RTMs (Retail Teller Machines), Kiosks or other types of self-service systems

Offer banking services through “business correspondents” (such as post-offices) or other partners

Other

46%

50%

50%

44%

13%

64%

4%

50 55 60 65

© 2013 Networld Media Group | Sponsored by KAL 38

Smartphone integration reaching critical mass

In the 2012 ATM Software Trends & Analy-sis guide, when asked about the importance of mobile and smartphone technology as a customer touchpoint, respondents by far ranked it near the bottom of their concerns.

For the 2013 guide, respondents ranked the ability to perform banking services via smartphone at or near the top of their concerns. In addition, many in the industry see the smartphone becoming an integral component of the ATM channel.

“Smartphones will serve as the link be-tween the different banking channels such as Internet banking and ATMs,” said Armando Bordel, smart cards manager at Madrid, Spain-based card payments net-work processing operator Redsys.

Driving that is the ability of the smart-phone to take the place of paper in many transactions. Wells Fargo, for example, said in 2012 that just two years after intro-ducing an e-receipt feature at their ATMs, customers had used the service more than 100 million times. Another driver is the increasing number of mobile payment so-lutions in the marketplace.

“We see a convergence of services through-out the various channels,” said Wincor’s Daubenbuechel.

“For instance in Africa, a lot of money transactions are carried out by phone, from one phone to another phone,” he said. “That is quite common, but the system only works if at some point in the process you have a

defined way of how money gets into that circle and money leaves the circle.”

Consider, for example, a student who wants to send someone cash via PayPal, but they don’t have a credit card. With the integration of the ATM channel and smart-phone technology, that student could sim-ply go to an ATM, deposit cash, and pick up that transaction with their phone.

“Mobile payments will enable a different customer interaction that could quickly enhance new ways to access the ATM,” said Mattia Ghidoni, head of cards client support and fraud management at Verona, Italy-based UniCredit Business Integrated Solutions.

In addition, the mobile phone holds tre-mendous potential as a way to “pre-stage” a transaction, allowing customers to begin a transaction on the smartphone and com-plete it at the ATM. For example, a cus-tomer can begin the process of making a deposit at home or at the office, then com-plete the process quickly at the ATM.

“I think there is some mileage in using that in areas like business deposits when the of-fice staff is sent to go deposit the day’s tak-ings,” said NCR’s Johnston. “I think we’re going to see that having a significant influ-ence over the next 3 to 5 years.”

Johnston point out, though, that there is still work that needs to be done in terms of adopting standards for technology such as near-field communication.

“Interestingly however, NFC mobile integration with the ATM opens up a

© 2013 Networld Media Group | Sponsored by KAL 39

whole host of alternative opportunities to simply withdrawing your money,” said YourCash’s Campbell.

“With banks now moving to the branchless banking model whereby they solely rely on ATMs to perform almost all standard teller operations, NFC becomes an enabler,” she said. “NFC can be an informatics tool used in conjunction with existing ATM functionality for the transfer of money and communicating with the ATM. You could preload far more significant pieces of data on to your phone that would have taken tens of minutes to plug in to the ATM key-pad and simply transfer that data across to the ATM which is, in essence, that con-sumers banking provider.”

Although QR codes are another area where some standardization still needs to occur, the fact that just about every smartphone today incorporates a camera holds promise of ATM/smartphone integration.

NCR, for example, is pilot-testing a Mobile Cash Withdrawal system that allows users to launch a smartphone app and scan a QR code on an ATM to withdraw cash. The process eliminates the need for both cards and PINs.

And just as QR codes are being used in retail settings to deliver information about products to shoppers’ phones, QR codes at the ATM or in the branch can serve as a way to quickly pass along information about a bank’s products, eliminating print-ing costs in the process. “As smartphone use has increased among the general public, a communication link to users have been implemented in ways such as QR codes on the ATMs,” said Alice Skyvarova, senior manager of distribution channels at GE Money Bank in the Czech Republic. “This speeds up the volume of valuable information transferred to the customers.

© 2013 Networld Media Group | Sponsored by KAL 40

Total survey respondents: 355

1: Is your company a financial institution?

No1%

Yes99%

Yes

No

2. How many ATMs do you have?

1-100 12%

101-500 17%

501-2,000 27%

2,001 or more 44%

© 2013 Networld Media Group | Sponsored by KAL 41

Our ATM software and hardware is from a single manufacturer

19%

We have one standardized ATM software environment on ATMs from multiple

manufacturers (multi-vendor software)43%

We use the software supplied by the

manufacturer (i.e., NCR software on NCR ATMs,

Diebold software on Diebold ATMs) and see no

need to change16%

We have software supplied by the ATM manufacturer(s) but are considering

multi-vendor ATM software22%

3. Which statement best identifies your organization’s ATM software strategy?

Our ATM so*ware and hardware is from a single manufacturer

We have one standardized ATM so*ware environment on ATMs from mul;ple manufacturers (mul;-‐vendor so*ware)

We use the so*ware supplied by the manufacturer (i.e., NCR so*ware on NCR ATMs, Diebold so*ware on Diebold ATMs) and see no need to change

We have so*ware supplied by the ATM manufacturer(s) but are considering mul;-‐vendor ATM so*ware

We develop and maintain our own proprietary ATM application.

23%

We rely on our ATM hardware vendor to develop and

maintain our ATM software.26%

We rely on our ATM software vendor to develop and maintain

our ATM software.24%

We license ATM software from a vendor, but we make ongoing

changes to it.20%

I am not sure what we do.7%

4. Which statement best identifies your organization’s current approach to the development of ATM software?

We develop and maintain our own proprietary ATM applica6on.

We rely on our ATM hardware vendor to develop and maintain our ATM so:ware.

We rely on our ATM so:ware vendor to develop and maintain our ATM so:ware.

We license ATM so:ware from a vendor, but we make ongoing changes to it.

I am not sure what we do.

© 2013 Networld Media Group | Sponsored by KAL 42

Forty-four percent of respondents from Europe, the Middle East and Africa indicated they planned to replace their ATM software either this year or next. For the Americas that figure was 40 percent and for the Asia/Pacific region it was 43 percent.

2012 2012 2011

Yes, planned and budgeted for 2013 18% 18% 19%

Yes, planning for either 2014 or 2015 26% 27% 20%

No, we recently replaced it 13% 14% 16%

No, there are no plans to replace the existing ATM software 29% 41% 29%

Not applicable 14% 0% 16%

5: Are there plans to replace your current ATM software?

6. What are the primary drivers for changing ATM software? (Choose the THREE most important.)

Reduce the cost of operating our ATM network

Support for new technology (such as contactless cards, mobile phone integration, coin handling, cash recycling)

Increase our operational productivity and efficiency

Improve customer service

Provide an enhanced user experience

Improve ATM availability

Increase security (such as EMV, 3DES, Remote Key, Biometrics)

Add new functionality such as deposit automation

Better promotion of new bank services

Support Windows 7 or 8

Be able to readily update ATM software when needed

Compliance with PCI/disabled user accessibility regulations

Be able to negotiate better prices for new ATM hardware

Other

15%

10%

36%

29%

21%

11%

24%

16%

28%

22%

19%

35%

11%

2%

© 2013 Networld Media Group | Sponsored by KAL 43

In Europe, the Middle East and Africa respondents indicated the primary driver for changing ATM software was reducing costs at 36 percent, support for new technology at 35 percent and providing an enhanced user experience at 29 percent. In the Asia/Pacific region enhanced security was the top driver at 38 percent, with support for new technology second at 29 percent followed by a tie between improving customer service and improving ATM availability at 23 percent. In the Americas, support for new technology was ranked as the primary driver at 38 percent, followed by increase security at 32 percent and providing an enhanced user experience at 30 percent.

Reduce the cost of enhancing ATM functionality

Ability to select ATMs freely, regardless of manufacturer

Deliver a unified operational environment

Reduce the “time to market” to gain a competitive edge

Improve customer service

Ability to more readily extend ATM functionality

Deliver a consistent customer experience

Integrate the ATM with other banking channels and systems

Improve negotiating position for purchasing hardware and ATM-related services

Readily adapt to regulatory changes

Better promotion of new bank services and products

Easily support additional languages

Other

39%

16%

24%

50%

2%

33%

22%

11%

27%

6%

25%

19%

1%

7. What do you consider to be the main benefits of moving to a single standardized ATM software environment (multi-vendor ATM software)? (Choose up to THREE options.)

© 2013 Networld Media Group | Sponsored by KAL 44

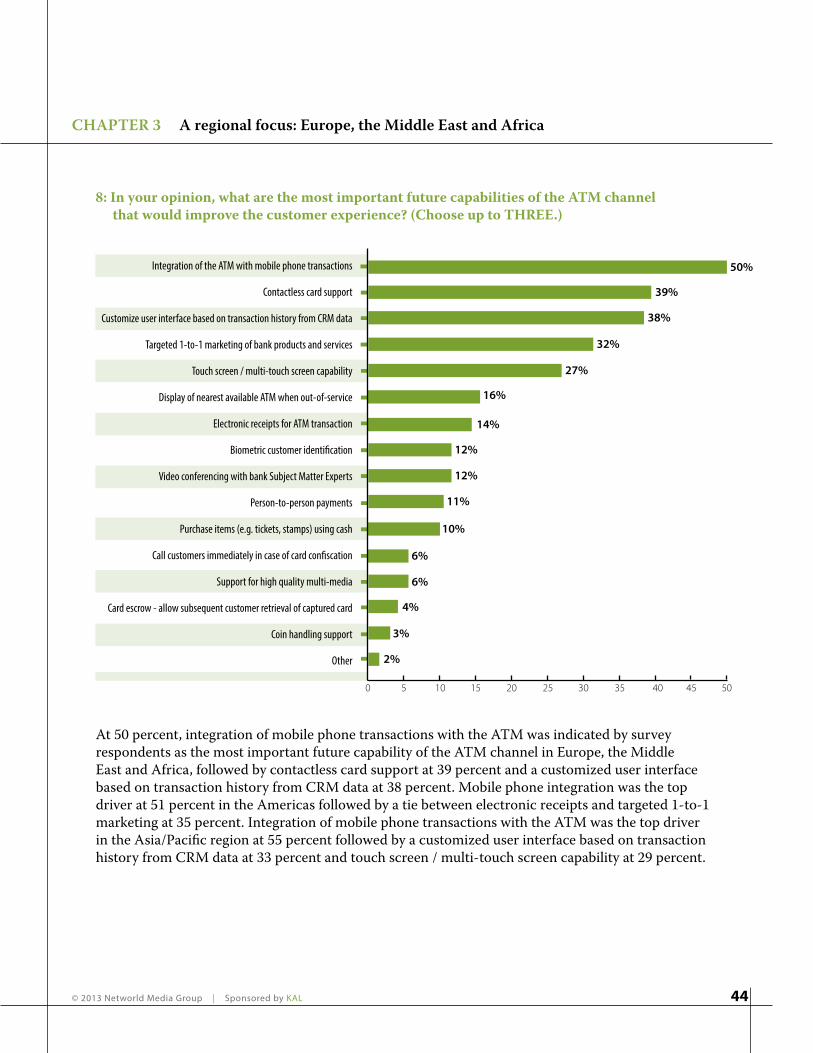

Integration of the ATM with mobile phone transactions

Contactless card support

Customize user interface based on transaction history from CRM data

Targeted 1-to-1 marketing of bank products and services

Touch screen / multi-touch screen capability

Display of nearest available ATM when out-of-service

Electronic receipts for ATM transaction

Biometric customer identification

Video conferencing with bank Subject Matter Experts

Person-to-person payments

Purchase items (e.g. tickets, stamps) using cash

Call customers immediately in case of card confiscation

Support for high quality multi-media

Card escrow - allow subsequent customer retrieval of captured card

Coin handling support

Other

6%

4%

3%

39%

38%

16%

14%

50%

10%

11%

6%

32%

27%

12%

12%

2%

8: In your opinion, what are the most important future capabilities of the ATM channel that would improve the customer experience? (Choose up to THREE.)

At 50 percent, integration of mobile phone transactions with the ATM was indicated by survey respondents as the most important future capability of the ATM channel in Europe, the Middle East and Africa, followed by contactless card support at 39 percent and a customized user interface based on transaction history from CRM data at 38 percent. Mobile phone integration was the top driver at 51 percent in the Americas followed by a tie between electronic receipts and targeted 1-to-1 marketing at 35 percent. Integration of mobile phone transactions with the ATM was the top driver in the Asia/Pacific region at 55 percent followed by a customized user interface based on transaction history from CRM data at 33 percent and touch screen / multi-touch screen capability at 29 percent.

© 2013 Networld Media Group | Sponsored by KAL 45

9. What is the most critical change your organization needs to make to its ATM network in 2013? (Choose up to THREE responses.)

Reduce operational costs

Improve the ATM functionality for the customer

Create a better customer experience at the ATM

Integrate with other self-service channels such as mobile

Migrate to Windows 7 or 8

Automate more branch transactions and move them to the ATM channel

Better promotion of bank’s products and services

Management reporting (availability, transaction volumes, SLAs)

Compliance with PCI/disabled user accessibility regulations

Remotely manage the ATM network

Adopt enhanced security technologies

Reduce hardware purchasing costs

Upgrade communications infrastructure

Distribute software updates and changes more frequently

No changes needed

11%

22%

16%

27%

7%

31%

25%

17%

17%

23%

34%

11%

12%

11%

4%

© 2013 Networld Media Group | Sponsored by KAL 46

10: Which statement best identifies your organization’s opinion regarding the future direction of the ATM operating system environment?

No opinion17%

We would like to have the choice of running a

non-Microsoft operating system (e.g., Linux).

7%

We will need to complete our upgrade to Windows 7 or 8 within the next two years.

16%

We will need to begin migrating to Windows

7 or 8 now or within the next two years.

36%

We will only change from Windows XP when we

absolutely have to change.24%

We will only change from Windows XP when we absolutely have to change.

We will need to begin migra:ng to Windows 7 or 8 now or within the next two years.

We will need to complete our upgrade to Windows 7 or 8 within the next two years.

We would like to have the choice of running a non-‐MicrosoB opera:ng system (e.g., Linux).

No opinion

Other

11: What are your most frustrating issues when trying to deliver the ATM channel objectives for your organization? (Choose up to THREE responses.)

Managing costs

Complexity in working with external providers (e.g., third-party suppliers, ATM manufacturers)

Complexity in working with all of the involved internal stakeholders

Understanding regulatory issues and requirements

Lack of overall visibility as to what is really happening

Making timely deliveries of updates and changes

Lack of overall control to make things happen

Determining accountability and assigning responsibility for issue resolution

Having access to timely and accurate information

Other

32%

36%

14%

20%

23%

23%

52%

13%

24%

1%

© 2013 Networld Media Group | Sponsored by KAL 47

Fifty-two percent of respondents from Europe, the Middle East and Africa listed managing costs as their most frustrating issue when trying to deliver their ATM channel objectives, followed by complexity in working with external providers at 36 percent and complexity on working with internal stakeholders at 32 percent. In the Asia/Pacific region managing costs was also top at 45 percent, followed by complexity in working with external providers at 43 percent and making timely deliveries of updates and changes at 29 percent. In the Americas, 53 percent of respondents listed complexity in working with external providers as their most frustrating issue when trying to deliver their ATM channel objectives followed by managing costs at 50 percent and making timely deliveries of updates and changes at 39 percent.

12: Is it a near-term priority for your bank to extend your use of self-service to deliver new or additional products and services?

Yes 74%

No 26%

© 2013 Networld Media Group | Sponsored by KAL 48

Add new transactions on the ATM

Increase the promotion for using smartphones and / or the bank website to do banking services

Use new types of devices to deliver bank products and services inside of the branch (e.g. touch screens, iPads, kiosks, RTMs etc)

Offer banking services in non-branch locations using bank branded RTMs (Retail Teller Machines), Kiosks or other types of self-service systems

Extend the number of ATMs in the network

Offer banking services through “business correspondents” (such as post-offices) or other partners

Other

34%

67%

39%

38%

15%

44%

2%

50 55 60 65 70

13: What plans do you have for extending the use of self-service? (Check all that apply)

Adding new transactions on the ATM was listed as a plan for extending the use of self service by 64 percent of respondents in Europe, the Middle East and Africa, followed by increasing the promotion for using smartphones and / or the bank website to do banking services at 44 percent. Using new types of devices to deliver bank products and services as listed by 39 percent of respondents. In the Americas, increasing the promotion for using smartphones and / or the bank website to do banking services was listed as a plan for extending the use of self-service by 64 percent of survey respondents followed by a tie between adding new transactions at the ATM and the use of new devices at the branch to deliver bank products and services. Sixty percent of respondents from the Asia/Pacific region listed adding new transactions at the ATM as a plan for extending the use of self-service followed by use new types of devices to deliver bank products and services inside of the branch at 55 percent and extending the number of ATMs in the network at 50 percent.

14. Do you currently have “branch of the future” activities where you test new types of self-service technologies?

Yes 52%

No 48%

© 2013 Networld Media Group | Sponsored by KAL 49

Serving the underbanked

The tremendous growth of online billpay, retailers such as Amazon.com and on-line gaming platforms such as World of Warcraft have sparked a secondary boom among the unbanked and underbanked: the prepaid card.

In addition, many employers now offer un-banked employees a reloadable debit card on which their wages can be loaded each pay period, while government benefits such as Social Security and unemployment com-pensation increasingly come in the form of a plastic card as opposed to a paper check.

ATMMarketplace blogger Mark D. Smith, vice president of financial solutions at Kahuna ATM solutions, defines the un-derbanked community as those who use a bank for limited services but don’t have an account or don’t engage with other tradi-tional banking programs.

In June 2011, the FDIC sponsored the second National Survey of Unbanked and Underbanked Households to collect data on the number of U.S. households that are unbanked and underbanked, their demo-graphic characteristics, and their reasons for being unbanked and underbanked.

Some of the key overall findings from the 2011 include: • 8.2 percent of US households are un-

banked. This represents 1 in 12 house-holds in the nation, or nearly 10 million in total.

• The proportion of unbanked households increased slightly since the 2009 survey.

The estimated 0.6 percentage point in-crease represents an additional 821,000 unbanked households.

• 20.1 percent of US households are un-derbanked. This represents one in five households, or 24 million households. The 20.1 underbanked rate in 2011 is higher than the 2009 rate of 18.2 per-cent, although the proportions are not directly comparable because of differ-ences in the two surveys.

• 29.3 percent of households do not have a savings account, while about 10 percent do not have a checking account. About two-thirds of households have both checking and savings accounts.

• One-quarter of households have used at least one AFS product in the last year, and almost one in ten households have used two or more AFS. In all, 12 percent of households used an AFS product in the last 30 days, including four in ten unbanked and underbanked households.

Still, 63 percent of the underbanked popu-lation has access to broadband Internet and 68 percent of underbanked consumers own a mobile phone.

Despite the criticism over high fees, pre-paid cards are an increasingly popular fixture in the financial landscape. The Mercator Advisory Group expected $552 billion to be loaded onto network-branded prepaids cards.

An interesting pattern became clear since banks and credit unions began offering prepaid card services to the underbanked community, Smith said.

© 2013 Networld Media Group | Sponsored by KAL 50

“The majority of customers participating in these programs have chosen to remain underbanked; they did not become fully banked customers as many financial insti-tutions had predicted,” Smith said. “Instead of converting to standard banking services, many of the recipients remained satisfied with this type of prepaid program.”

The trend toward prepaid cards is not only popular in the United States, but in emerging countries as well. Last year in India, for ex-ample, the government launched a program to extend ATM availability to Indians nation-wide and has added prepaid cards to the mix. All Indian citizens who have registered for India’s biometrics-based identity program will also be eligible for a prepaid card issued by one of five national banks participating in the new Saral Money program.

Saral Money will allow the government to transfer social welfare benefits directly to the cardholder. The card can then be used to obtain cash, make purchases from mer-

chants that accept Visa and MasterCard, pay bills and transfer money. The participat-ing banks will use “micro-ATMs” — hand-held devices equipped with a biometric fingerprint reader to verify the cardholder’s identity in order to disburse cash.

Clearly, that trend illustrates a tremendous opportunity for banks and ATM deployers.

“Pre-paid cards have now been developed to be directly dispensed from the ATM from the standard cash cassette,” said YourCash’s Campbell.