2013 asia pacific-global_hotel_chain_growth_strategy

75

Development of Growth & Expansion Strategy for Client X in Asia Pacific Final Report John Gregg, Principal, Navigate Consulting Paul Davies, Director Tourism Consulting, Australia 9 June 2013

-

Upload

john-gregg -

Category

Travel

-

view

61 -

download

0

Transcript of 2013 asia pacific-global_hotel_chain_growth_strategy

Development of Growth & Expansion

Strategy for Client X in Asia Pacific

Final Report John Gregg, Principal, Navigate ConsultingPaul Davies, Director Tourism Consulting, Australia

9 June 2013

2

Agenda

1. Approach

2. Industry overview

3. Sector analysis

4. Strategic options

5. Selected strategy

6. Next steps

3

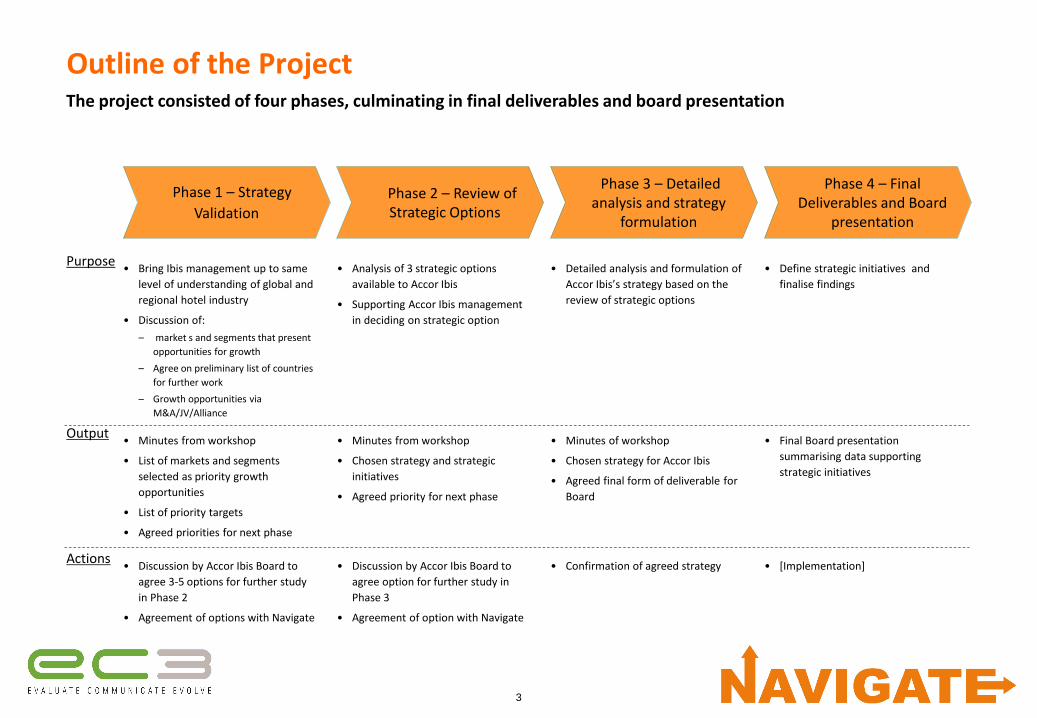

Outline of the ProjectThe project consisted of four phases, culminating in final deliverables and board presentation

Purpose

Output

Actions

Phase 1 – Strategy

ValidationPhase 2 – Review of Strategic Options

Phase 3 – Detailed analysis and strategy

formulation

Phase 4 – Final Deliverables and Board

presentation

• Bring Ibis management up to same

level of understanding of global and

regional hotel industry

• Discussion of:

– market s and segments that present

opportunities for growth

– Agree on preliminary list of countries

for further work

– Growth opportunities via

M&A/JV/Alliance

• Analysis of 3 strategic options

available to Accor Ibis

• Supporting Accor Ibis management

in deciding on strategic option

• Detailed analysis and formulation of

Accor Ibis’s strategy based on the

review of strategic options

• Define strategic initiatives and

finalise findings

• Discussion by Accor Ibis Board to

agree 3-5 options for further study

in Phase 2

• Agreement of options with Navigate

• Discussion by Accor Ibis Board to

agree option for further study in

Phase 3

• Agreement of option with Navigate

• Confirmation of agreed strategy • [Implementation]

• Minutes from workshop

• List of markets and segments

selected as priority growth

opportunities

• List of priority targets

• Agreed priorities for next phase

• Minutes from workshop

• Chosen strategy and strategic

initiatives

• Agreed priority for next phase

• Minutes of workshop

• Chosen strategy for Accor Ibis

• Agreed final form of deliverable for

Board

• Final Board presentation

summarising data supporting

strategic initiatives

4

Agenda1. Approach

2. Industry overview

• Market overview

• Key considerations

3. Sector analysis

4. Strategic options

5. Selected strategy

6. Next steps

5

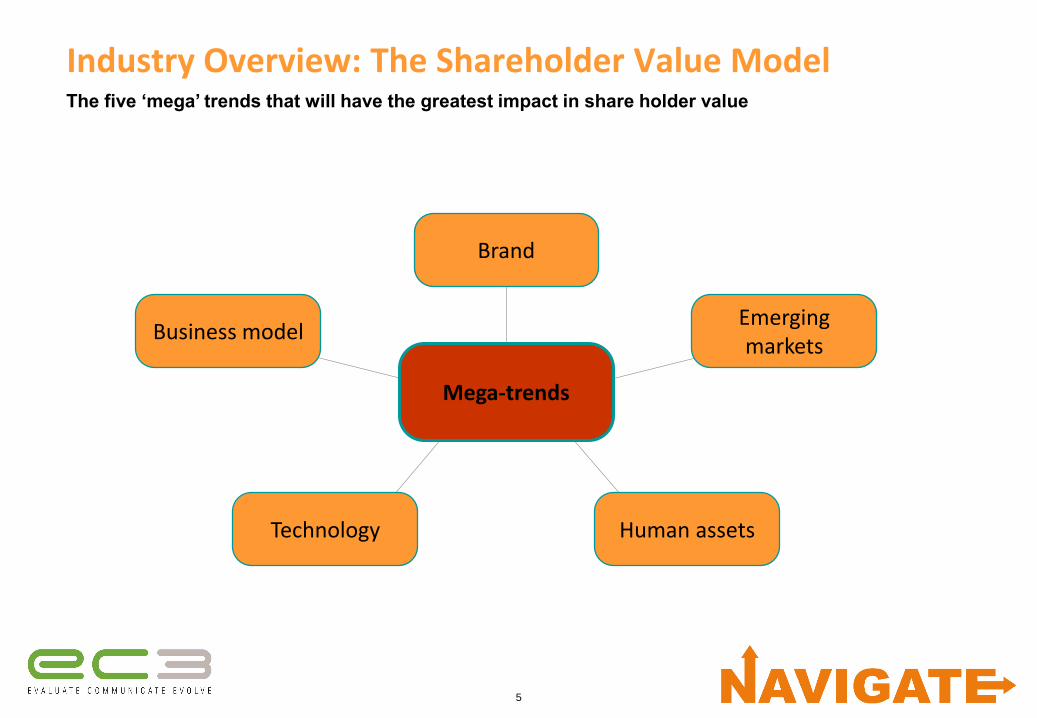

Industry Overview: The Shareholder Value Model

Brand

Human assetsTechnology

Emerging markets

Business model

Mega-trends

The five ‘mega’ trends that will have the greatest impact in share holder value

6

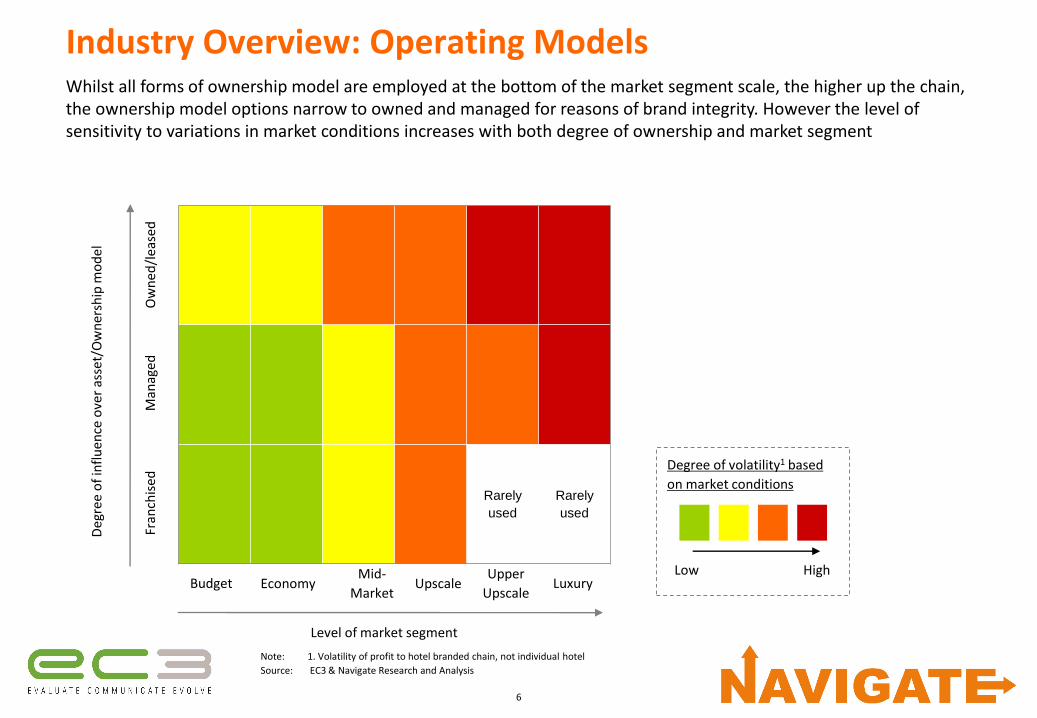

Industry Overview: Operating Models

Note: 1. Volatility of profit to hotel branded chain, not individual hotel

Source: EC3 & Navigate Research and Analysis

Whilst all forms of ownership model are employed at the bottom of the market segment scale, the higher up the chain, the ownership model options narrow to owned and managed for reasons of brand integrity. However the level of sensitivity to variations in market conditions increases with both degree of ownership and market segment

Rarely

used

Rarely

used

Budget Luxury

Ow

ned

/lea

sed

Fran

chis

ed

EconomyMid-

MarketUpscale

Upper

Upscale

Man

aged

Low High

Degree of volatility1 based

on market conditions

Deg

ree

of

infl

uen

ce o

ver

asse

t/O

wn

ersh

ip m

od

el

Level of market segment

7

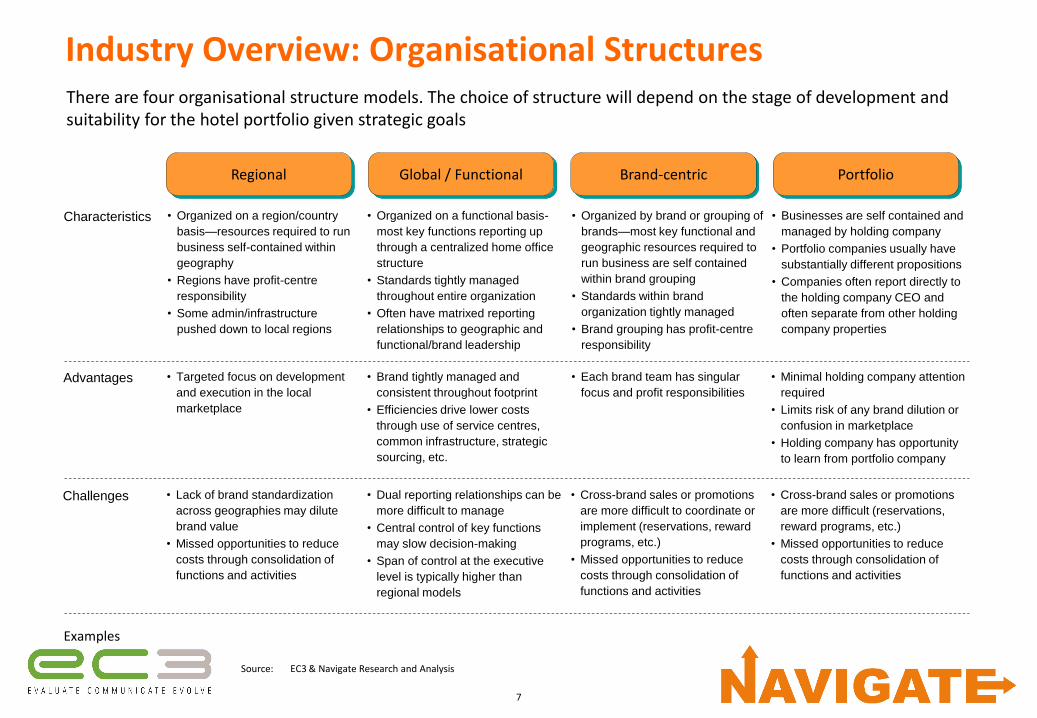

Industry Overview: Organisational Structures

Source: EC3 & Navigate Research and Analysis

There are four organisational structure models. The choice of structure will depend on the stage of development and suitability for the hotel portfolio given strategic goals

Characteristics • Organized on a region/country

basis—resources required to run

business self-contained within

geography

• Regions have profit-centre

responsibility

• Some admin/infrastructure

pushed down to local regions

• Organized on a functional basis-

most key functions reporting up

through a centralized home office

structure

• Standards tightly managed

throughout entire organization

• Often have matrixed reporting

relationships to geographic and

functional/brand leadership

• Organized by brand or grouping of

brands—most key functional and

geographic resources required to

run business are self contained

within brand grouping

• Standards within brand

organization tightly managed

• Brand grouping has profit-centre

responsibility

• Businesses are self contained and

managed by holding company

• Portfolio companies usually have

substantially different propositions

• Companies often report directly to

the holding company CEO and

often separate from other holding

company properties

Advantages • Targeted focus on development

and execution in the local

marketplace

• Brand tightly managed and

consistent throughout footprint

• Efficiencies drive lower costs

through use of service centres,

common infrastructure, strategic

sourcing, etc.

• Each brand team has singular

focus and profit responsibilities

• Minimal holding company attention

required

• Limits risk of any brand dilution or

confusion in marketplace

• Holding company has opportunity

to learn from portfolio company

Challenges • Lack of brand standardization

across geographies may dilute

brand value

• Missed opportunities to reduce

costs through consolidation of

functions and activities

• Dual reporting relationships can be

more difficult to manage

• Central control of key functions

may slow decision-making

• Span of control at the executive

level is typically higher than

regional models

• Cross-brand sales or promotions

are more difficult to coordinate or

implement (reservations, reward

programs, etc.)

• Missed opportunities to reduce

costs through consolidation of

functions and activities

• Cross-brand sales or promotions

are more difficult (reservations,

reward programs, etc.)

• Missed opportunities to reduce

costs through consolidation of

functions and activities

Examples

Regional Global / Functional PortfolioBrand-centric

8

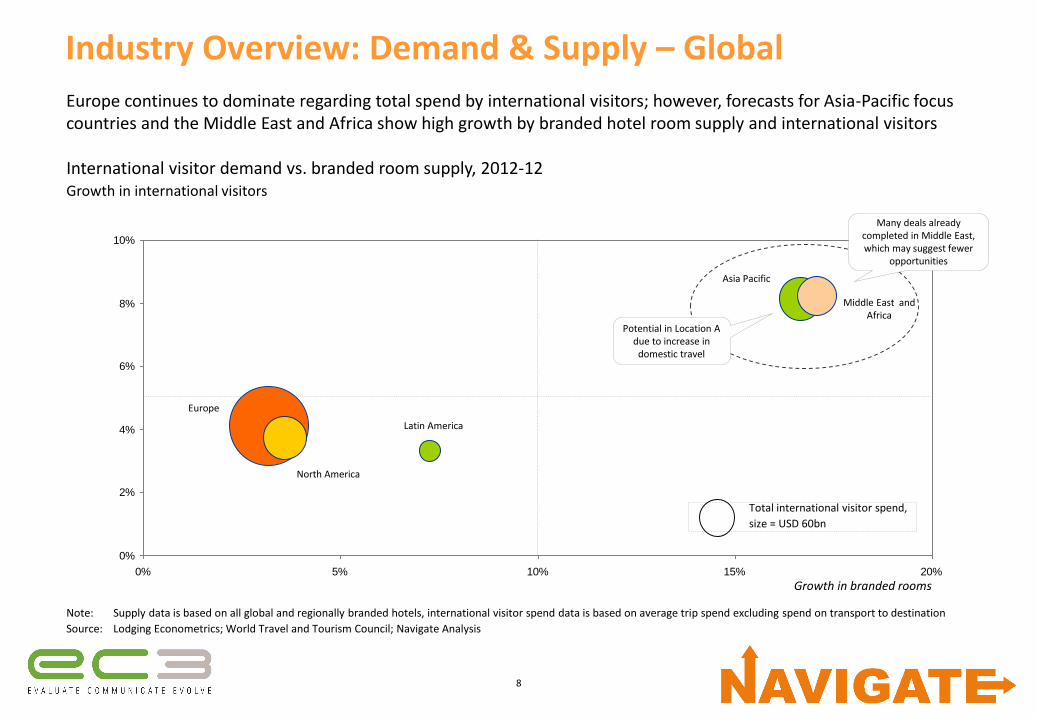

Industry Overview: Demand & Supply – Global

Europe continues to dominate regarding total spend by international visitors; however, forecasts for Asia-Pacific focus countries and the Middle East and Africa show high growth by branded hotel room supply and international visitors

0%

2%

4%

6%

8%

10%

0% 5% 10% 15% 20%

Europe

North America

Latin America

Asia Pacific

Middle East and Africa

Growth in branded rooms

Note: Supply data is based on all global and regionally branded hotels, international visitor spend data is based on average trip spend excluding spend on transport to destination

Source: Lodging Econometrics; World Travel and Tourism Council; Navigate Analysis

Total international visitor spend,

size = USD 60bn

International visitor demand vs. branded room supply, 2012-12 Growth in international visitors

Potential in Location A due to increase in

domestic travel

Many deals already completed in Middle East, which may suggest fewer

opportunities

9

China

Malaysia

Phillipines

Indonesia

Thailand

Maldives

Singapore

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0% 10% 20% 30% 40%

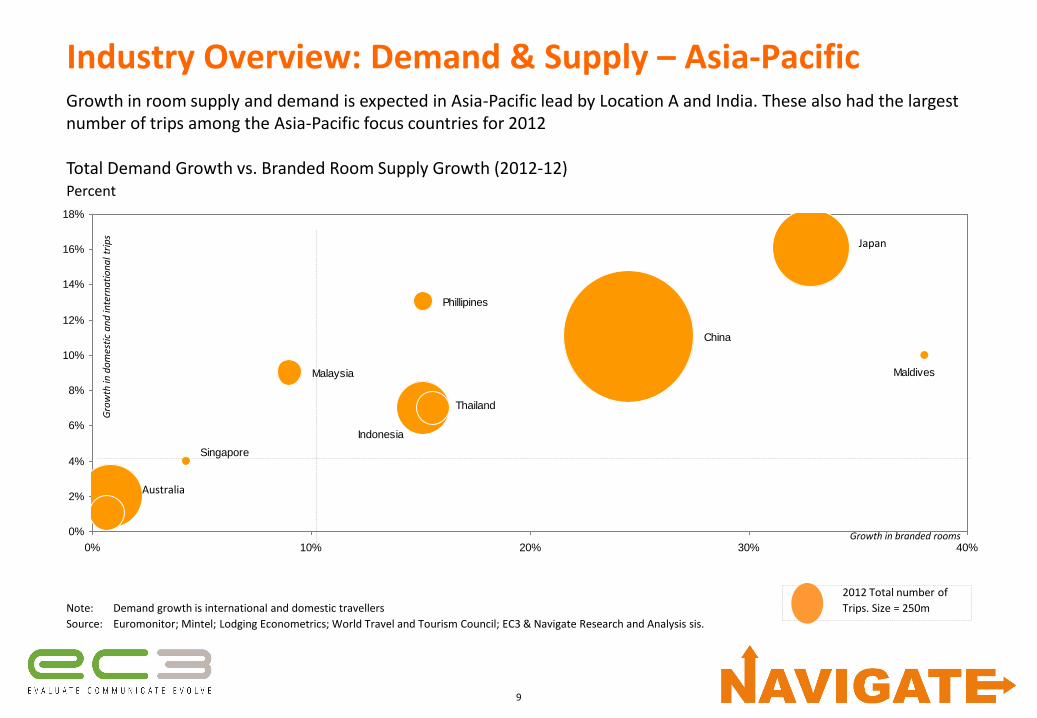

Industry Overview: Demand & Supply – Asia-PacificGrowth in room supply and demand is expected in Asia-Pacific lead by Location A and India. These also had the largest number of trips among the Asia-Pacific focus countries for 2012

Total Demand Growth vs. Branded Room Supply Growth (2012-12)Percent

Growth in branded rooms

2012 Total number of

Trips. Size = 250mNote: Demand growth is international and domestic travellers

Source: Euromonitor; Mintel; Lodging Econometrics; World Travel and Tourism Council; EC3 & Navigate Research and Analysis sis.

Gro

wth

in d

om

esti

c a

nd

inte

rna

tio

na

l tr

ips

Australia

Japan

10

Industry Overview: Demand & Supply – Int’l Overnight and Dom. Trips

0

200

400

600

800

1,000

1,200

1,400

1,600

International 75 8.3 21 14 5.0 6.4 5.5 0.7 3.1 8.3 2.9 56 30

Domestic 1,387 346 43 92 512 105 240 - 37 1.0 19 1,199 121

Total 1,461 355 64 106 517 112 245 0.7 40 9.3 22 1,255 151

% Domestic 95% 98% 67% 86% 99% 94% 98% 0% 92% 11% 87% 96% 80%

Greater

ChinaJapan Malaysia Thailand India Korea Indonesia Maldives Philippines Singapore Vietnam

United

States

United

Kingdom

Location A leads Asia-Pacific with the largest number of both domestic and international trips

Domestic and International Trips by Country (2012)Million Trips

Note: International demand is determined by international overnight trips for 2012. Domestic trips are for 2012 and are defined as travel of 50 miles or more, each way, which includes an overnight stay. *Due to rounding of decimal places, totals might not always correspond exactly to the sum.

Source: Euromonitor; World Travel and Tourism Council; EC3 & Navigate Research and AnalysisDomestic International

*

Benchmark

11

0

200

400

600

800

1,000

1,200

1,400

1,600

Business 121 41 5.5 44 122 9.2 82 4 0.2 13 312 20

Leisure 1,265 305 37 48 390 96 158 33 0.8 6.4 887 101

Total 1,387 346 43 92 512 105 240 - 37 1 19 1,199 121

Greater

ChinaJapan Malaysia Thailand India Korea Indonesia Maldives Philippines Singapore Vietnam

United

States

United

Kingdom

Industry Overview: Demand & Supply – Domestic TripsLeisure is the main driver for domestic travellers

Domestic Business and Leisure Trips (2012)Million Trips

Leisure Business

Data not available

Note: International demand is determined by international overnight trips for 2012. Domestic trips are for 2012 and are defined as travel of 50 miles or more, each way, which includes an overnight stay.

Source: Euromonitor; World Travel and Tourism Council; Navigate Research & Analysis.

Benchmark

12

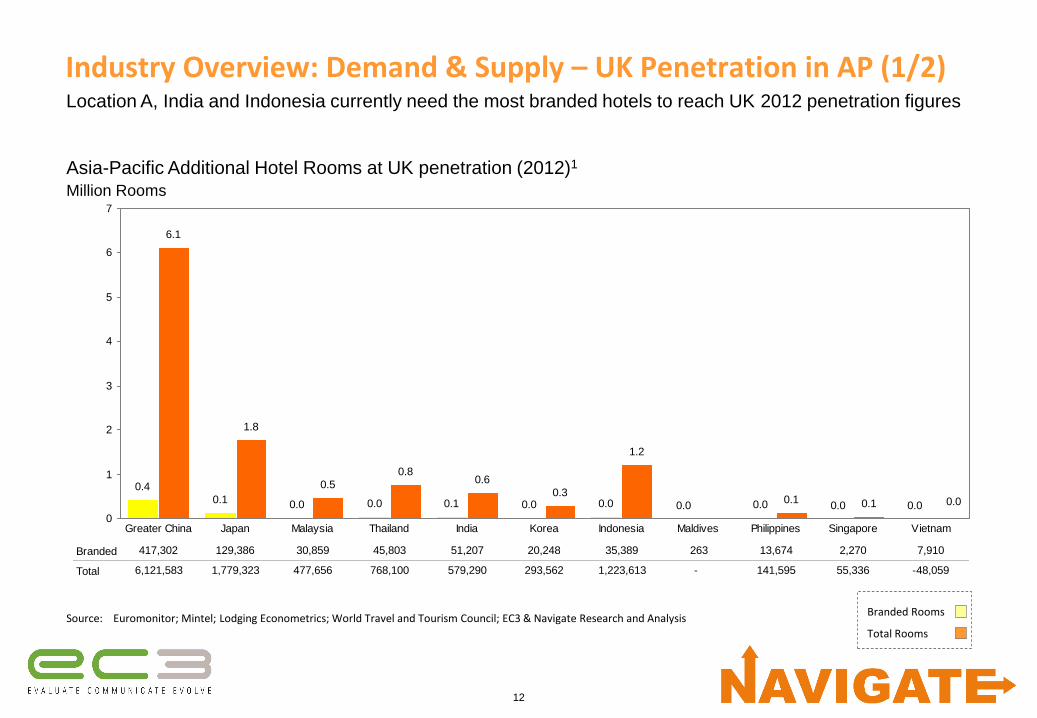

0.4

0.1 0.0 0.0 0.1 0.0 0.0 0.0 0.0 0.0 0.0

6.1

1.8

0.5

0.80.6

0.3

1.2

0.1 0.1 0.0

0

1

2

3

4

5

6

7

Branded 417,302 129,386 30,859 45,803 51,207 20,248 35,389 263 13,674 2,270 7,910

Total 6,121,583 1,779,323 477,656 768,100 579,290 293,562 1,223,613 - 141,595 55,336 -48,059

Greater China Japan Malaysia Thailand India Korea Indonesia Maldives Philippines Singapore Vietnam

Asia-Pacific Additional Hotel Rooms at UK penetration (2012)1

Million Rooms

Industry Overview: Demand & Supply – UK Penetration in AP (1/2)Location A, India and Indonesia currently need the most branded hotels to reach UK 2012 penetration figures

Source: Euromonitor; Mintel; Lodging Econometrics; World Travel and Tourism Council; EC3 & Navigate Research and AnalysisBranded Rooms

Total Rooms

13

0.5

0.1 0.0 0.1 0.1 0.0 0.0 0.0 0.0 0.0 0.0

7.2

3.0

0.6

1.2

0.60.3

1.4

0.2 0.1 0.3

0

1

2

3

4

5

6

7

8

Branded 479,411 146,249 36,856 53,652 57,420 22,554 39,631 712 16,077 7,316 9,366

Total 7,174,542 2,956,606 646,215 1,193,828 649,996 328,277 1,442,008 - 165,754 95,425 292,867

Greater China Japan Malaysia Thailand India Korea Indonesia Maldives Philippines Singapore Vietnam

Asia-Pacific Additional Hotel Rooms at UK penetration (2012)1

Million Rooms

Industry Overview: Demand & Supply – UK Penetration in AP (2/2)Looking forward to the year 2014, there is still a gap to reach UK 2013 penetration for branded rooms among

several of the Asia-Pacific countries, lead by Location A, India and Location D

Source: Euromonitor; Mintel; Lodging Econometrics; World Travel and Tourism Council; EC3 & Navigate Research and AnalysisBranded Rooms

Total Rooms

14

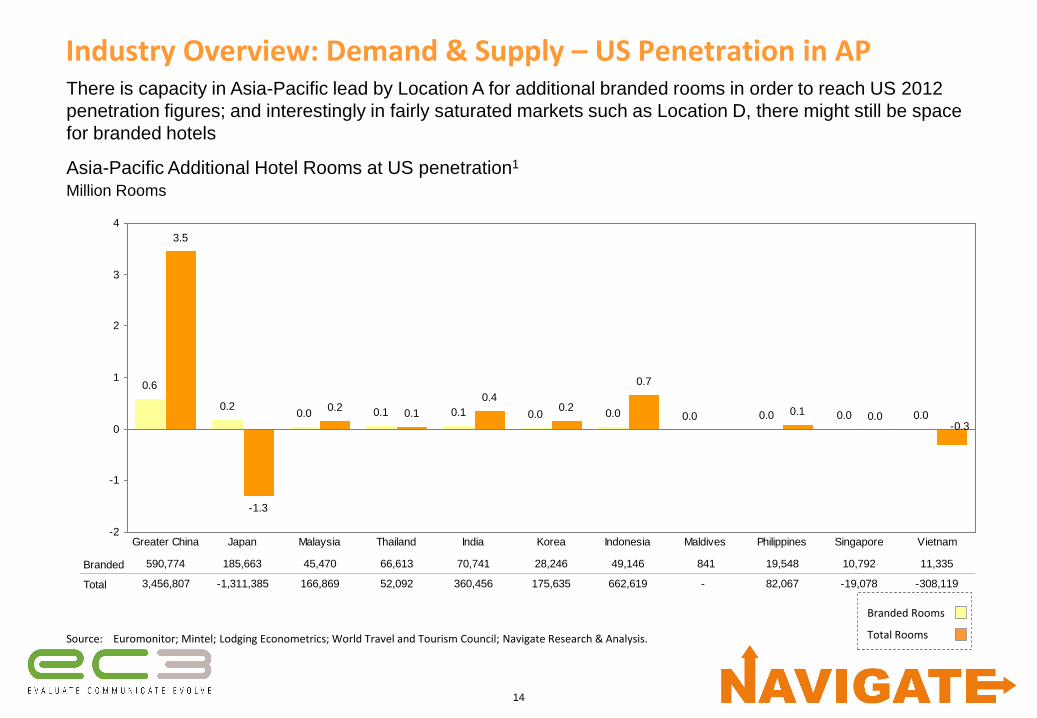

0.6

0.20.0 0.1 0.1 0.0 0.0 0.0 0.0 0.0 0.0

3.5

-1.3

0.20.1

0.40.2

0.7

0.1 0.0-0.3

-2

-1

0

1

2

3

4

Branded 590,774 185,663 45,470 66,613 70,741 28,246 49,146 841 19,548 10,792 11,335

Total 3,456,807 -1,311,385 166,869 52,092 360,456 175,635 662,619 - 82,067 -19,078 -308,119

Greater China Japan Malaysia Thailand India Korea Indonesia Maldives Philippines Singapore Vietnam

Asia-Pacific Additional Hotel Rooms at US penetration1

Million Rooms

Industry Overview: Demand & Supply – US Penetration in APThere is capacity in Asia-Pacific lead by Location A for additional branded rooms in order to reach US 2012

penetration figures; and interestingly in fairly saturated markets such as Location D, there might still be space

for branded hotels

Source: Euromonitor; Mintel; Lodging Econometrics; World Travel and Tourism Council; Navigate Research & Analysis.

Branded Rooms

Total Rooms

15

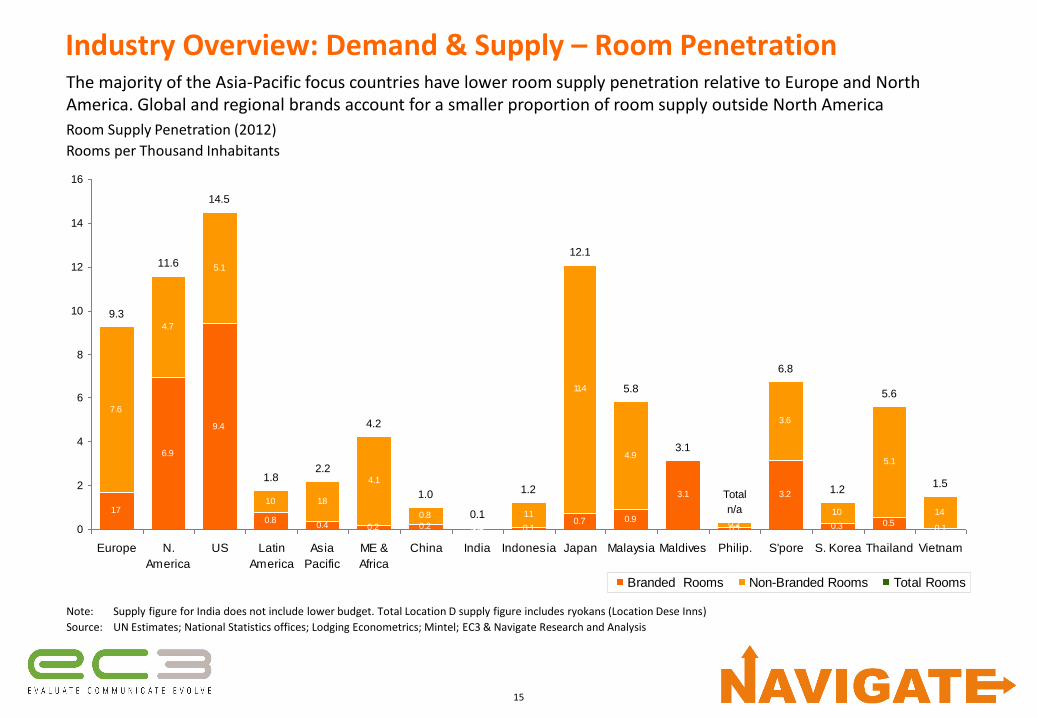

Industry Overview: Demand & Supply – Room Penetration

1.7

6.9

9.4

0.80.4 0.2 0.2 0.0 0.1

0.7 0.9

3.1

0.1

3.2

0.3 0.50.1

7.6

4.7

5.1

1.0 1.8

4.1

0.8

0.1

1.1

11.4

4.9

0.2

3.6

1.0

5.1

1.4

9.3

11.6

14.5

1.82.2

4.2

1.0

0.1

1.2

12.1

5.8

3.1

6.8

1.2

5.6

1.5Total

n/a

0

2

4

6

8

10

12

14

16

Europe N.

America

US Latin

America

Asia

Pacific

ME &

Africa

China India Indonesia Japan Malaysia Maldives Philip. S'pore S. Korea Thailand Vietnam

Branded Rooms Non-Branded Rooms Total Rooms

The majority of the Asia-Pacific focus countries have lower room supply penetration relative to Europe and North America. Global and regional brands account for a smaller proportion of room supply outside North America

Room Supply Penetration (2012)

Rooms per Thousand Inhabitants

Note: Supply figure for India does not include lower budget. Total Location D supply figure includes ryokans (Location Dese Inns)

Source: UN Estimates; National Statistics offices; Lodging Econometrics; Mintel; EC3 & Navigate Research and Analysis

16

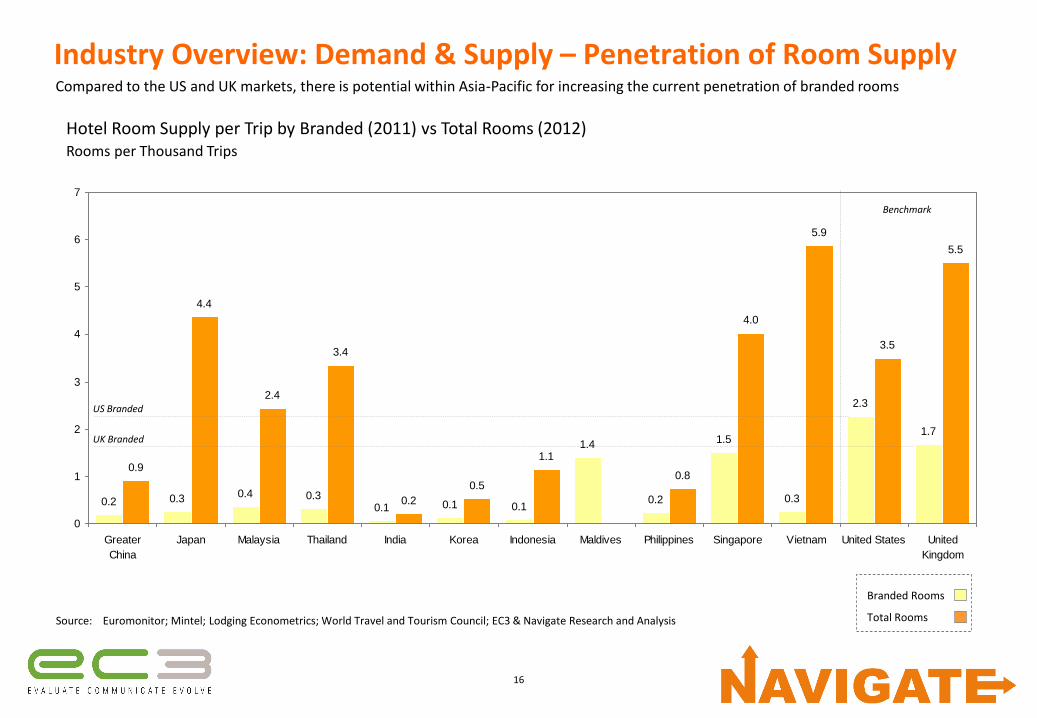

0.2 0.3 0.4 0.30.1 0.1 0.1

1.4

0.2

1.5

0.3

2.3

1.7

0.9

4.4

2.4

3.4

0.2

0.5

1.1

0.8

4.0

5.9

3.5

5.5

0

1

2

3

4

5

6

7

Greater

China

Japan Malaysia Thailand India Korea Indonesia Maldives Philippines Singapore Vietnam United States United

Kingdom

Compared to the US and UK markets, there is potential within Asia-Pacific for increasing the current penetration of branded rooms

Hotel Room Supply per Trip by Branded (2011) vs Total Rooms (2012)Rooms per Thousand Trips

Branded Rooms

Total Rooms

Industry Overview: Demand & Supply – Penetration of Room Supply

Source: Euromonitor; Mintel; Lodging Econometrics; World Travel and Tourism Council; EC3 & Navigate Research and Analysis

US Branded

UK Branded

Benchmark

17

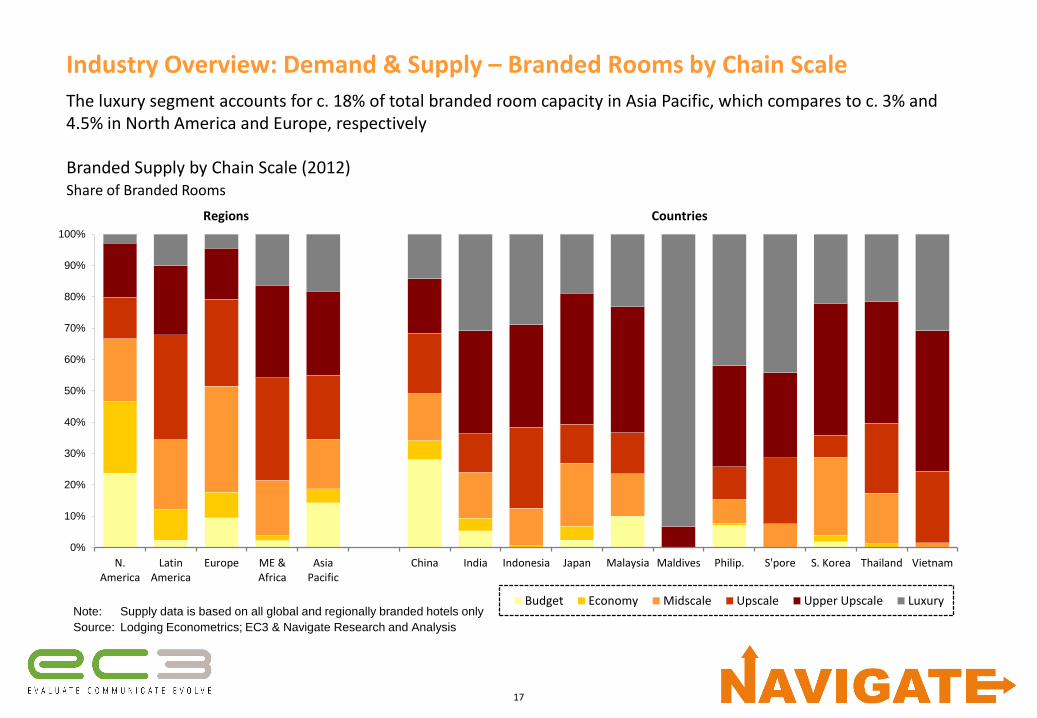

Industry Overview: Demand & Supply – Branded Rooms by Chain Scale

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

N.America

LatinAmerica

Europe ME &Africa

AsiaPacific

China India Indonesia Japan Malaysia Maldives Philip. S'pore S. Korea Thailand Vietnam

Budget Economy Midscale Upscale Upper Upscale Luxury

The luxury segment accounts for c. 18% of total branded room capacity in Asia Pacific, which compares to c. 3% and 4.5% in North America and Europe, respectively

Branded Supply by Chain Scale (2012)Share of Branded Rooms

Note: Supply data is based on all global and regionally branded hotels only

Source: Lodging Econometrics; EC3 & Navigate Research and Analysis

CountriesRegions

18

Industry Overview: Demand & Supply – Upper Upscale / Luxury ValuationHotel values have increased on average nearly 6% p.a. between 2002-06, with cities in Location A, Malaysia,

Indonesia and Singapore

Tokyo

Hong Kong

Seoul Singapore

Shanghai

Beijing

BangkokPhuket Taipei

Bali Kuala Lumpur

Manila Jakarta

0

100

200

300

400

500

600

700

800

900

-2% 0% 2% 4% 6% 8% 10% 12%

Upper Upscale / Luxury Valuation per Key (2012)USD Thousands 2012 vs CAGR 2008-2012

$292k

Source: 2012 Asia Hotel Valuation Index; Navigate Research & Analysis

5.6%

19

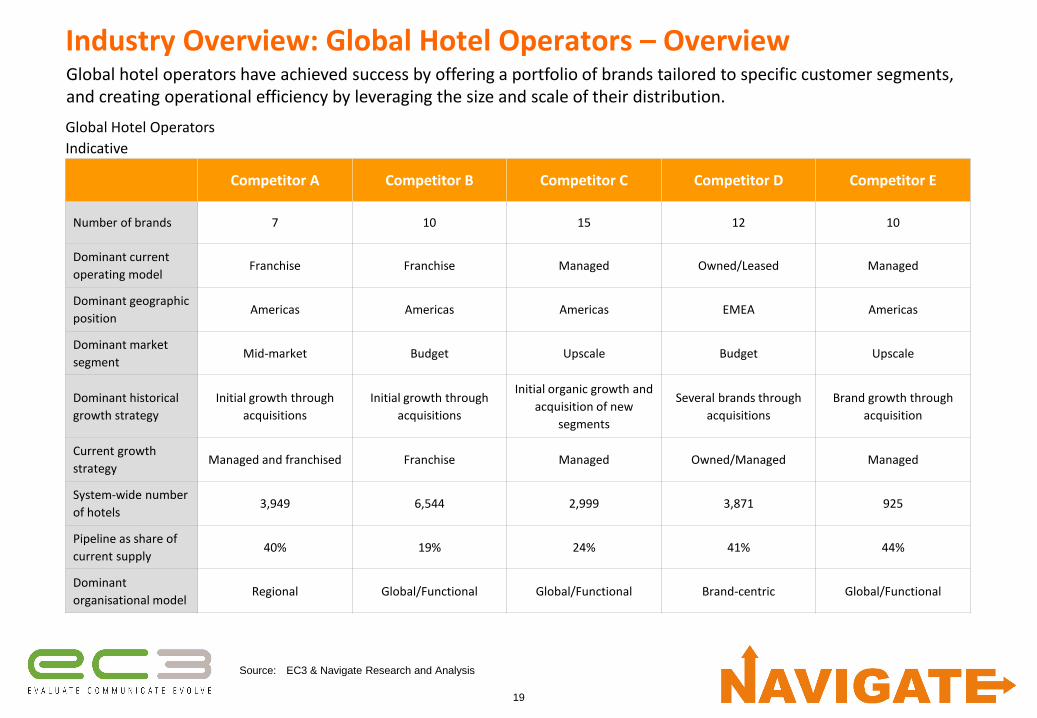

Global hotel operators have achieved success by offering a portfolio of brands tailored to specific customer segments, and creating operational efficiency by leveraging the size and scale of their distribution.

Industry Overview: Global Hotel Operators – Overview

Competitor A Competitor B Competitor C Competitor D Competitor E

Number of brands 7 10 15 12 10

Dominant current

operating modelFranchise Franchise Managed Owned/Leased Managed

Dominant geographic

positionAmericas Americas Americas EMEA Americas

Dominant market

segmentMid-market Budget Upscale Budget Upscale

Dominant historical

growth strategy

Initial growth through

acquisitions

Initial growth through

acquisitions

Initial organic growth and

acquisition of new

segments

Several brands through

acquisitions

Brand growth through

acquisition

Current growth

strategyManaged and franchised Franchise Managed Owned/Managed Managed

System-wide number

of hotels3,949 6,544 2,999 3,871 925

Pipeline as share of

current supply40% 19% 24% 41% 44%

Dominant

organisational modelRegional Global/Functional Global/Functional Brand-centric Global/Functional

Source: EC3 & Navigate Research and Analysis

Global Hotel Operators

Indicative

20

Industry Overview: Global Hotel Operators – Financial SummaryGlobal hotel operators have achieved high return on capital invested by focussing on management contracts and real-estate transformation.

Financial Results and Key Performance Indicators (2012)

Indicative

Competitor A Competitor B Competitor C Competitor Dl Competitor E

Financial Results

Total Revenue, $m 1,768 4,360 4,415 6,153 11,132

Market Cap, $m 4,470 3,864 12,777 10,469 15,837

EV / EBITDA 10.5x 5.7x 12.0x 11.4x 9.2x

P / E 12.0x 10.3x 18.8x 19.8x 11.9x

Return on capital

invested1, %17 9 25 13 13.6

Key Performance

Indicators2

RevPAR, $ 72 871 121 110 77

Occupancy, % 69.6 73.31 73.2 70.1 67.6

ADR, $ 103 1181 165 157 114

EBITDA, $m 437 892 1,385 1,164 1,905

EBITDA Margin, % 27.0 20.5 31.4 18.9 17.0

Note: 1 Due to information availability the figure is based upon the financial statements as at 2012 year end.

Source: EC3 & Navigate Research and Analysis

21

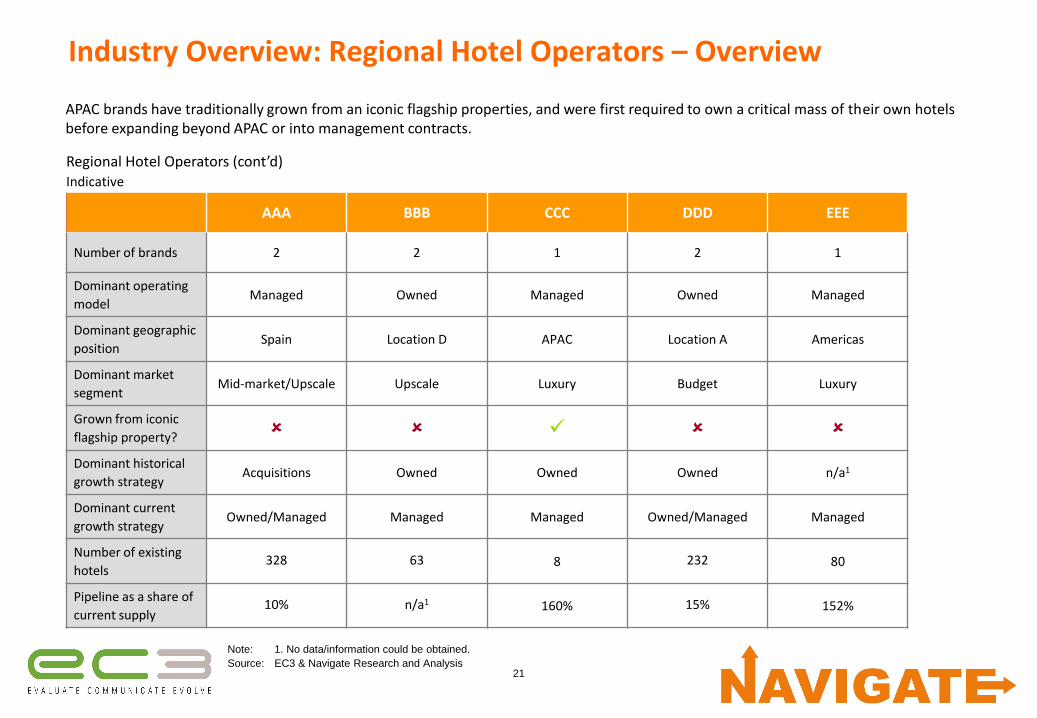

Industry Overview: Regional Hotel Operators – Overview

Note: 1. No data/information could be obtained.

Source: EC3 & Navigate Research and Analysis

APAC brands have traditionally grown from an iconic flagship properties, and were first required to own a critical mass of their own hotels before expanding beyond APAC or into management contracts.

AAA BBB CCC DDD EEE

Number of brands 2 2 1 2 1

Dominant operating

modelManaged Owned Managed Owned Managed

Dominant geographic

positionSpain Location D APAC Location A Americas

Dominant market

segmentMid-market/Upscale Upscale Luxury Budget Luxury

Grown from iconic

flagship property?

Dominant historical

growth strategyAcquisitions Owned Owned Owned n/a1

Dominant current

growth strategyOwned/Managed Managed Managed Owned/Managed Managed

Number of existing

hotels328 63 8 232 80

Pipeline as a share of

current supply10% n/a1 160% 15% 152%

Regional Hotel Operators (cont’d)Indicative

22

Industry Overview: Regional Hotel Operators – Financial SummaryAsia Pacific chains have relatively high EV/EBITDA multiples and relatively low return on capital invested as a result of their asset heavy strategies.

Financial Results and Key Performance Indicators (2012 unless otherwise stated)Indicative

AAA BBB CCC DDD EEE

Financial Results

Total Revenue, $m 1,002* 558 582 211* 430*

Market Cap, $m 8,341 1,635 2,095 696 1,873

EV / EBITDA 23.6x 12.8x 19.3x 17.9x 14.7x

P / E 22.4x 15.2x 5.1x 12.1x 38.7x

Return on capital invested1, % 7* 8 4 8* 10.1*

Key Performance Indicators2

RevPAR, $ 102* 215 316 178* 34**

Occupancy, % 70 74 68 65* 71**

ADR, $ 146* 291 465 274* 48**

EBITDA, $m 350* 190 194 70* 111

EBITDA Margin, % 34.9* 34.1 33 33* 26

Note: 1 Based on continuing operations, excluding special items; 2 Company operated; 3 Relevant data is not available for JAL, Raffles, and Four Seasons. * Figure is based on 2006 figures due to information availability. ** Jin Jiang figures are based upon their 3-Star brand. This provides a best estimate given the width of their offerings

Source: Company Data; EC3 & Navigate Research and Analysis

23

Agenda1. Approach

2. Industry overview

• Market overview

• Key considerations

3. Sector analysis

4. Strategic options

5. Selected strategy

6. Next steps

2424

Key Considerations: Strategic Framework Initial Thoughts

LocationPortfolio

Approaches

Play to your

Strengths

Most significant driver of

guest hotel choice

– Very few people choose a hotel

brand and then choose a

location

Returns first, brand fit

second

– Led to most development

approaches being more tactical

than strategic

– Organisations will have their

desired location lists but

market opportunity often

overtakes

– Organic growth focused on

locations where there is

capacity within a segment

– Can create tension between

Brand and Development

– Led to most brands having

significant range of quality and

locations

– Only strongest brands can

adopt more strategic approach

– In the absence of property

asset value increases, new

management contracts are one

of the key sources of

increasing financial return

– Development pipeline now THE

most important KPI for the

major listed hotel operators

Single segment approach

– With the exception of Four

Seasons, all luxury single

segment operators have built

growth on the foundation of

one or two iconic properties

Luxury brands

– Almost all luxury brands have

extended into resorts and

residences (both owned and

fractional)

– Resort developments are

aimed at capturing the leisure

market of their customers

– In the past 2 years the

incorporation of a residential

element has been required to

make new builds financially

viable

Multi segment approach

– Many organisations have a

luxury brand to deliver a ‘halo’

effect

– The core business is mid-

market and the luxury brand

delivers an aspiration for these

guests

– Few organisations have mid-

tier resort brands

Many hospitality

organisations have natural

strengths

– Iconic properties

– Strong brand names

– Deep heritage

– Strong cultural links

– Corporate owners

– Access to capital

Successful organisations

have developed ways of

harnessing these strengths

Operational

Excellence

A critical driver in delivering

financial return

– No value in delivering low

profitability on high occupancy

and ADR

– Poor performance can destroy

benefits of strong brand and

location

– A key consideration for owners

when selecting operators

Number 1 core competency

– Vital that have strong core

operations to support future

growth – organic or acquisition

– All successful operators have

either CEO or COO with many

years operational experience

often with same organisation

and often starting from very

low level

– Need stable central ‘system’ to

support growth to enable new

properties to be transitioned

into the organisational

smoothly

– Create pool of expertise that

can be exported to new

properties to ensure rapid

adoption of standard

processes and procedures

Growth Patterns

Home comfort

– With the exception of Four

Seasons, all the major global

and regional players have

expanded close to home

before significant global

expansion

– This is reflected in the

percentage of property

portfolios in their domestic

markets

– Second stage expansion is

often in overseas regions with

strong brand or cultural

recognition

Home advantage

– Easier to support new hotels

from a logistical perspective as

can leverage current suppliers,

staff redeployment is easier

and management can maintain

closer oversight role. There are

also obvious time zone

advantages.

– Need to build critical scale of

operations before adding

additional strains of distant

operations

– It is likely that there is stronger

brand awareness in countries

closer to home and also easier

to build this brand awareness

in weaker countries due to

cultural similarities

Talent

Global and regional

hospitality organisations

invest significantly in their

talent

– One of most significant assets

particularly since property

assets typically disposed

– At the heart of operational

efficiency

– At the heart of delivering the

branded experience

– Becomes more significant the

higher the segment

– Large, high quality talent pool

required to support growth

– Increasingly in short supply

and predicted to get more so

– Recruitment and retention

Its not just about operational

training

– Staff engagement is just as

important – feeling emotionally

connected to the organisation

– Structured career development

Source: EC3 & Navigate Research and Analysis

We have identified a range of key considerations for Client X, which fall broadly into six categories

25

Agenda1. Approach

2. Industry overview

3. Sector analysis

• Region

• Country

• City

4. Strategic options

5. Selected strategy

6. Next steps

26

Region Analysis: Summary (1/2)

Source: EC3 & Navigate Research and Analysis

Requirements Europe North AmericaMiddle East &

AfricaAsia Pacific

Ability to develop management skills, detailed operating

procedures and central shared services

Ability for Client X to oversee operations from Location X

Ability to generate efficiencies from increased scale of

operations

Summary

Ability for Client X to Enter Region in Short to Medium TermIndicative

On a regional level, the ability for Client X to enter region in the short to medium term is high only in Asia-Pacific

27

Region Analysis: Summary (2/2)

Source: EC3 & Navigate Research and Analysis

Key Drivers Europe North AmericaMiddle East &

AfricaAsia Pacific

Demand drivers

Supply drivers

Historical performance

Ability for Client X to enter region in short to medium term

Investigate further?

Summary of Key DriversIndicative

Demand and supply drivers are positive in both Asia-Pacific and the Middle East & Africa

28

55%

60%

65%

70%

75%

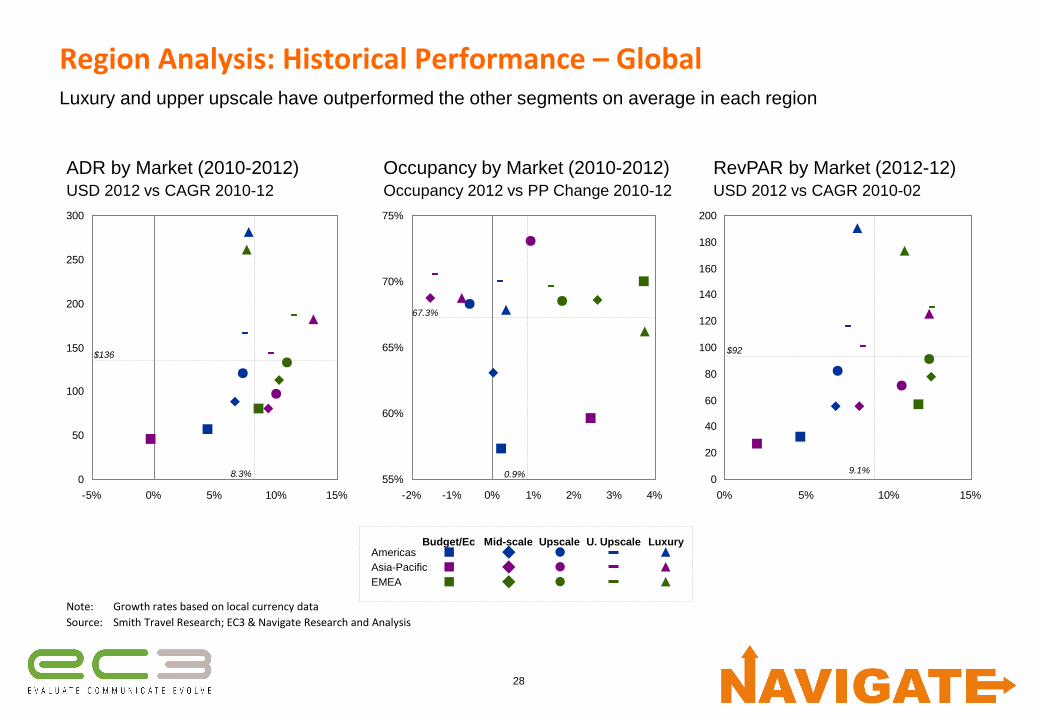

-2% -1% 0% 1% 2% 3% 4%

Region Analysis: Historical Performance – GlobalLuxury and upper upscale have outperformed the other segments on average in each region

0

50

100

150

200

250

300

-5% 0% 5% 10% 15%

ADR by Market (2010-2012)USD 2012 vs CAGR 2010-12

0.9%

67.3%

Note: Growth rates based on local currency data

Source: Smith Travel Research; EC3 & Navigate Research and Analysis

UpscaleMid-scale U. UpscaleBudget/EcAmericas

Asia-Pacific

EMEA

Luxury

RevPAR by Market (2012-12)USD 2012 vs CAGR 2010-02

Occupancy by Market (2010-2012)Occupancy 2012 vs PP Change 2010-12

8.3%

$136

0

20

40

60

80

100

120

140

160

180

200

0% 5% 10% 15%

$92

9.1%

29

Agenda1. Approach

2. Industry overview

3. Sector analysis

• Region

• Country

• City

4. Strategic options

5. Selected strategy

6. Next steps

30

Country Analysis: Overview

The key success factors for Client X to be able to enter these

countries have been identified as:

• Economic drivers

• Demand drivers

• Supply drivers

• Ability for Client X to implement

• Historical performance

• An analysis was performed determining the quantum of each

of these success factors

The focus countries have been split into the top four, middle four and bottom three through the quantification of key success

factors and subsequent ranking of these

Quantification of key success factors Ranking of countries based on key success factors

• The grouping has been determined by ranking the each

country from 1 to 11 based on the relative performance of

the key drivers, with 1 being the country with the best

performance and 11 being the country with the worst

performance

• We have primarily ranked the growth metrics in order to

identify markets where there is high potential for future

growth

• Absolute metrics are included to show relative size of metric

31

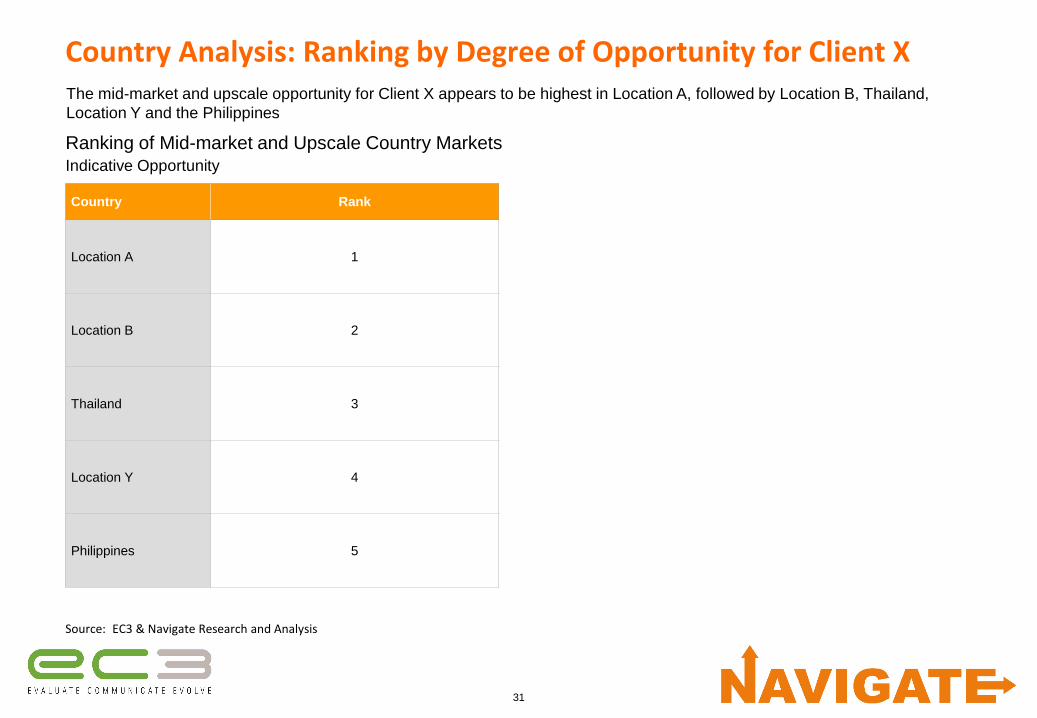

Country Analysis: Ranking by Degree of Opportunity for Client X

Source: EC3 & Navigate Research and Analysis

Country Rank

Location A 1

Location B 2

Thailand 3

Location Y 4

Philippines 5

Ranking of Mid-market and Upscale Country MarketsIndicative Opportunity

The mid-market and upscale opportunity for Client X appears to be highest in Location A, followed by Location B, Thailand,

Location Y and the Philippines

32

Country Analysis: Country Focus – Location Summary (1/2)

Country

Economy Demand DriversLocation Z

Dep.Supply Drivers

GDP Growth

2012-17

(%)

Int’l Trips

2012

(Million)

Int’l Trips

Growth

2012-17

(%)

Domestic

Trips

2012

(Million)

Domestic

Trips Growth

2011-12

(%)

Dom. Tourism

Spend1

2012

($bn)

Dom. tourism

spend growth

2012-17

(%)

Location Z

departures

2012

(Thousands)

Penetration

(Rooms per

thousand trips)

Penetration

(Rooms per

Million

Inhabitants)

Location Y 4.9% 6.4 3.0% 102 1% 19.6 5.5% n/a 0.1 1.2k

Location D 2.3% 8.3 3.2% 341 1% 216.5 4.6% 1,908 0.3 12.1k

Location A 13.3% 74.7 6.4% 1,196 10% 105.4 16.8% 361 0.2 1.0k

India 11.8% 5.0 6.7% 445 17% 22.4 10.4% n/a 0.1 0.1k

Singapore 5.5% 8.3 4.3% 906 11% 1.2 7.1% 230 1.5 6.8k

Thailand 5.9% 14.4 4.2% 85 8% 8.5 7.0% 825 0.3 5.6k

Philippines 9% 3.1 5.8% 33 15% 3.6 7.1% 485 0.3 0.3k

Location B 13.8% 2.9 8.8% 17 16% 1.5 8.5% 299 0.3 1.5k

Malaysia 6.2% 21.0 7.7% 39 6% 2.1 8.9% 111 0.4 5.8k

Indonesia 12.3% 5.5 7.5% 226 7% 7.7 12.1% 100 0.1 1.2k

Maldives n/a 0.7 4.7% n/a n/a 0.01 0% n/a 1.4 n/a

Ranked

Summary of Key Forward-looking DriversIndicative

Note: 1. Excludes business spend as data unavailable

Source: See reference pack

Key forward-looking looking drivers have been assessed for each country…

33

Country Analysis: Country Focus – Location Summary (2/2)

CountryAbility to

implement

RevPAR Performance1 RevPAR Growth in local currencies Profitability Valuation

Key Cities

2012

(USD)

Key Cities

Growth

2011-12

(%)

Luxury

2012-12

(CAGR)

Upscale /

U. Upscale

2012-12

(CAGR)

Mid-market

2012-12

(CAGR)

Budget

2012-12

(CAGR)

GOP Margin2

2012

(%)

Valuation

per Key

2012

(USD ‘000s)

Val. Growth

per Key

2008-12

(CAGR)

Location Y Very high 138 6% 3% -4% n/a n/a n/a 387 4%

Location D High 119 8% 8% -2% 2% 4% 28% 831 5%

Location A High 118 3% n/a 0% -2% n/a 44 – 50% 389 8%

India Low 207 32% 28% 30% n/a n/a 56% n/a n/a

Singapore Medium 141 22% 23% 21% 31% n/a 42% 384 10%

Thailand High 80 1% 2% 8% 14% n/a 46% 194 (0.4)%

Philippines High 79 15% 16% 11% n/a n/a n/a 96 4%

Location B High 96 35% n/a 30% n/a n/a n/a n/a n/a

Malaysia High 63 10% 11% 15% n/a n/a 30% 131 9%

Indonesia High 56 34% 16% 12% 17% n/a 26-26% 116 4%

Maldives Medium 4301 n/a n/a n/a n/a n/a n/a n/a n/a

Ranked

Summary of Key Historic DriversIndicative

Note: 1. Maldives figures for RevPAR and RevPAR growth are based upon Luxury and Upper Upscale hotels only; 2. GOP Margin is Income Before Fixed Charges based upon capital city

figures with the following exceptions: Location A (Beijing, Hong Kong and Shanghai), India (Mumbai), Indonesia (Jakarta, Bali)

Source: See reference pack

…followed by key historic drivers such as valuations, key performance indicators and profitability, and Client X’s ability to

implement

34

Country Analysis: Recap – Location Drivers Ranking (1/2)

CountryAbility to

implement

Location Z

Dep.Economy Demand Drivers Supply Drivers

Location Z

departures

2012

(Rank)

GDP

Growth

2012-17

(Rank)

Int’l Trips

2012

(Million)

Int’l Trips

Growth

2012-17

(Rank)

Domestic

Trips

2012

(Million)

Domestic

Trips Growth

2008-12

(Rank)

Dom.

Tourism

Spend1

2012

($bn)

Dom. tourism

spend growth

2012-15

(Rank)

Penetration

Rooms/Trip

(Rank)

Penetration

Rooms/Pop’n

(Rank)

Weighting Critical Very High High High High

Top 2

Location A High 4 2 74.7 5 1,1961 5 105.4 1 4 3

Location Y Very high n/a 9 6.4 11 102 10 19.6 9 2 4

Middle 5

Location B High 5 1 2.9 1 17 2 1.5 5 7 6

Philippines High 3 5 3.1 6 33 3 3.6 6 6 2

Thailand High 2 7 14.4 9 85 7 8.5 8 8 7

Indonesia High 8 3 5.5 3 226 6 7.7 2 3 5

Malaysia High 7 6 21 2 39 8 2.1 4 9 8

Bottom 4

India Low n/a 4 5 4 445 1 22.4 3 1 1

Singapore Medium 6 8 8.3 8 1 4 1.2 7 12 9

Location D High 1 10 8.3 10 341 9 216.5 10 5 10

Maldives Medium n/a n/a 0.7 7 n/a n/a 0.01 11 11 n/a

Ranking of Key Forward-looking DriversIndicative

Note: Location A figures for phase 1 based on Greater Location A; 1. Domestic trips for Location A includes mainland Location A only

Source: See reference pack

Location A and Location Y appears to provide the best opportunities for Client X

35

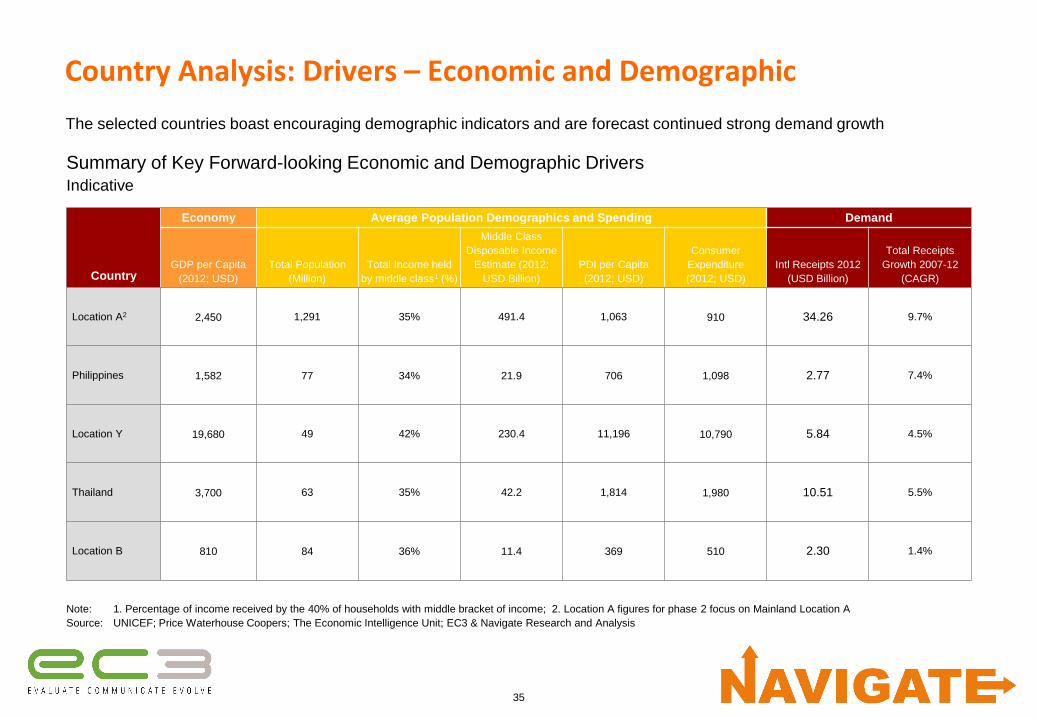

Country Analysis: Drivers – Economic and Demographic

Summary of Key Forward-looking Economic and Demographic DriversIndicative

Note: 1. Percentage of income received by the 40% of households with middle bracket of income; 2. Location A figures for phase 2 focus on Mainland Location A

Source: UNICEF; Price Waterhouse Coopers; The Economic Intelligence Unit; EC3 & Navigate Research and Analysis

Country

Economy Average Population Demographics and Spending Demand

GDP per Capita

(2012; USD)

Total Population

(Million)

Total Income held

by middle class1 (%)

Middle Class

Disposable Income

Estimate (2012;

USD Billion)

PDI per Capita

(2012; USD)

Consumer

Expenditure

(2012; USD)

Intl Receipts 2012

(USD Billion)

Total Receipts

Growth 2007-12

(CAGR)

Location A2 2,450 1,291 35% 491.4 1,063 910 34.26 9.7%

Philippines 1,582 77 34% 21.9 706 1,098 2.77 7.4%

Location Y 19,680 49 42% 230.4 11,196 10,790 5.84 4.5%

Thailand 3,700 63 35% 42.2 1,814 1,980 10.51 5.5%

Location B 810 84 36% 11.4 369 510 2.30 1.4%

The selected countries boast encouraging demographic indicators and are forecast continued strong demand growth

36

0

50

100

150

200

250

300

350

400

450

2000 2004 2008 2012 2016 2020

Country Analysis: Drivers – Investment in TourismChinese investment in travel and tourism is both significantly larger and forecast to grow more quickly than other focus countries

Note: Private capital investment includes foreign investment

Source: World Travel and Tourism Council; EC3 & Navigate Research and Analysis

Historic Forecast

CAGR

Capital Investment (2000-20)1

$ Billions

113.0

1.312.7 3.2

1.5

12.8

0.42.6 0.6

0.04

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

China Philippines South Korea Thai Vietnam

Capital Investment (2012): Public vs PrivatePercent

Private

Public2000-07 2007-20

Location A 19.0% 10.1%

Location Y 2.5% 6.4%

Thailand 4.5% 6.9%

Philippines (0.8)% 5.7%

Location B 14.0% 6.5%

125.8 1.7 15.3 3.8 1.5

37

Country Analysis: Historical Performance – RevPARRevPAR performance varies, both in absolute level and growth CAGR (2012-12), by both geography and market segment

0

50

100

150

200

250

300

-10% -5% 0% 5% 10% 15% 20% 25% 30% 35% 40%

RevPAR by Market (2010-12)USD 2012 vs CAGR 2010-12

12.1%

$123

Note: Location D Budget/Economy, Malaysia Upscale / Upper Upscale, and Philippines Upscale / Upper Upscale are all 2006-07 Percentage Change; Growth rates based on local currency data

Source: Smith Travel Research; ; EC3 & Navigate Research and Analysis

Upscale /

Upper UpscaleMid-/scale Luxury

Budget /

Economy

Indonesia

Location A

Hong Kong

India

Location D

Malaysia

Philippines

Singapore

Location Y

Thailand

Location B

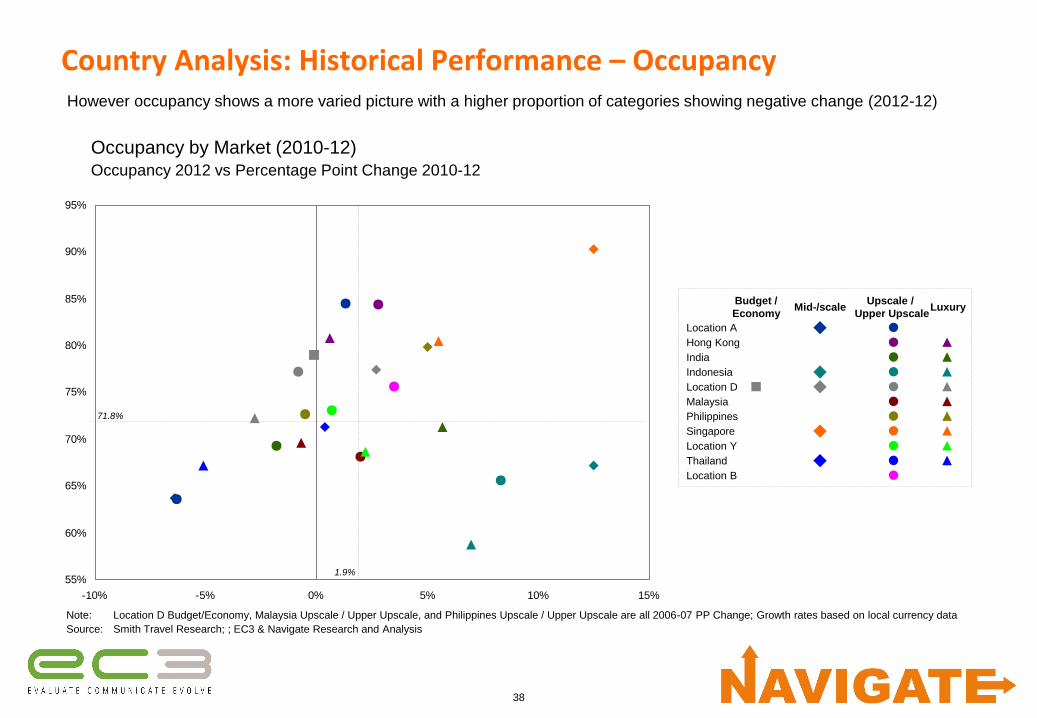

38

Country Analysis: Historical Performance – OccupancyHowever occupancy shows a more varied picture with a higher proportion of categories showing negative change (2012-12)

55%

60%

65%

70%

75%

80%

85%

90%

95%

-10% -5% 0% 5% 10% 15%

Occupancy by Market (2010-12)Occupancy 2012 vs Percentage Point Change 2010-12

1.9%

71.8%

Upscale /

Upper UpscaleMid-/scale Luxury

Budget /

Economy

Indonesia

Location A

Hong Kong

India

Location D

Malaysia

Philippines

Singapore

Location Y

Thailand

Location B

Note: Location D Budget/Economy, Malaysia Upscale / Upper Upscale, and Philippines Upscale / Upper Upscale are all 2006-07 PP Change; Growth rates based on local currency data

Source: Smith Travel Research; ; EC3 & Navigate Research and Analysis

39

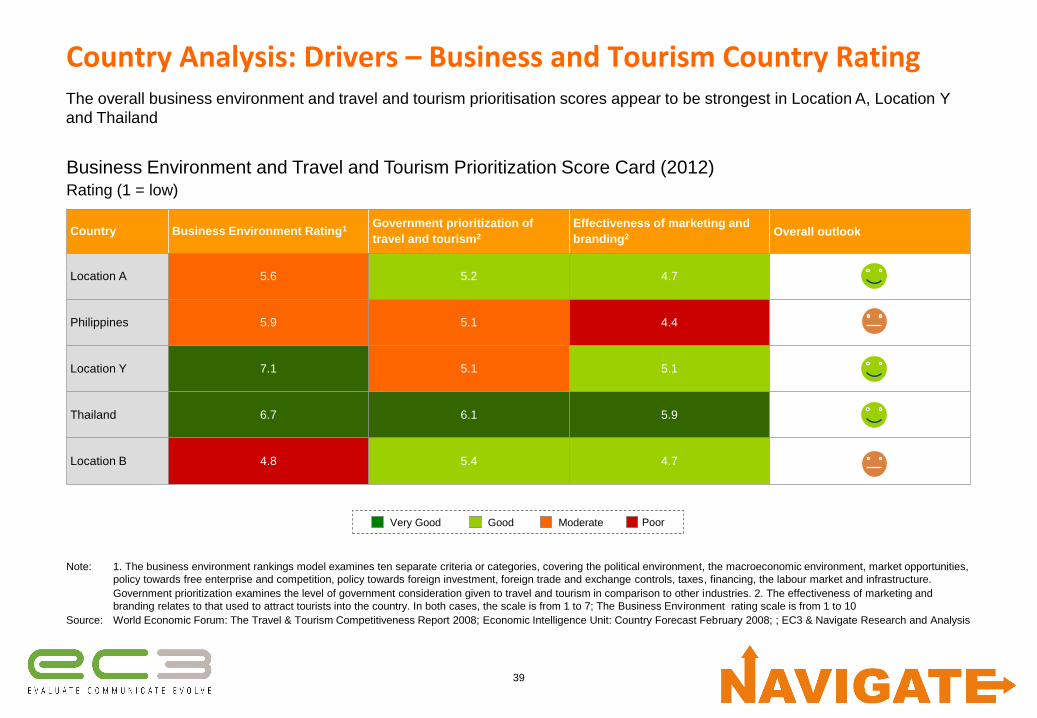

Note: 1. The business environment rankings model examines ten separate criteria or categories, covering the political environment, the macroeconomic environment, market opportunities,

policy towards free enterprise and competition, policy towards foreign investment, foreign trade and exchange controls, taxes, financing, the labour market and infrastructure.

Government prioritization examines the level of government consideration given to travel and tourism in comparison to other industries. 2. The effectiveness of marketing and

branding relates to that used to attract tourists into the country. In both cases, the scale is from 1 to 7; The Business Environment rating scale is from 1 to 10

Source: World Economic Forum: The Travel & Tourism Competitiveness Report 2008; Economic Intelligence Unit: Country Forecast February 2008; ; EC3 & Navigate Research and Analysis

Country Analysis: Drivers – Business and Tourism Country Rating

Business Environment and Travel and Tourism Prioritization Score Card (2012)Rating (1 = low)

Good PoorModerateVery Good

Country Business Environment Rating1Government prioritization of

travel and tourism2

Effectiveness of marketing and

branding2 Overall outlook

Location A 5.6 5.2 4.7

Philippines 5.9 5.1 4.4

Location Y 7.1 5.1 5.1

Thailand 6.7 6.1 5.9

Location B 4.8 5.4 4.7

The overall business environment and travel and tourism prioritisation scores appear to be strongest in Location A, Location Y

and Thailand

40

3.5%

2.1%

5.1%

1.8%

0.2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

China Philippines South Korea Thailand Vietnam

Note: Supply data is based on all global and regionally branded hotels only

Source: Lodging Econometrics; ; EC3 & Navigate Research and Analysis

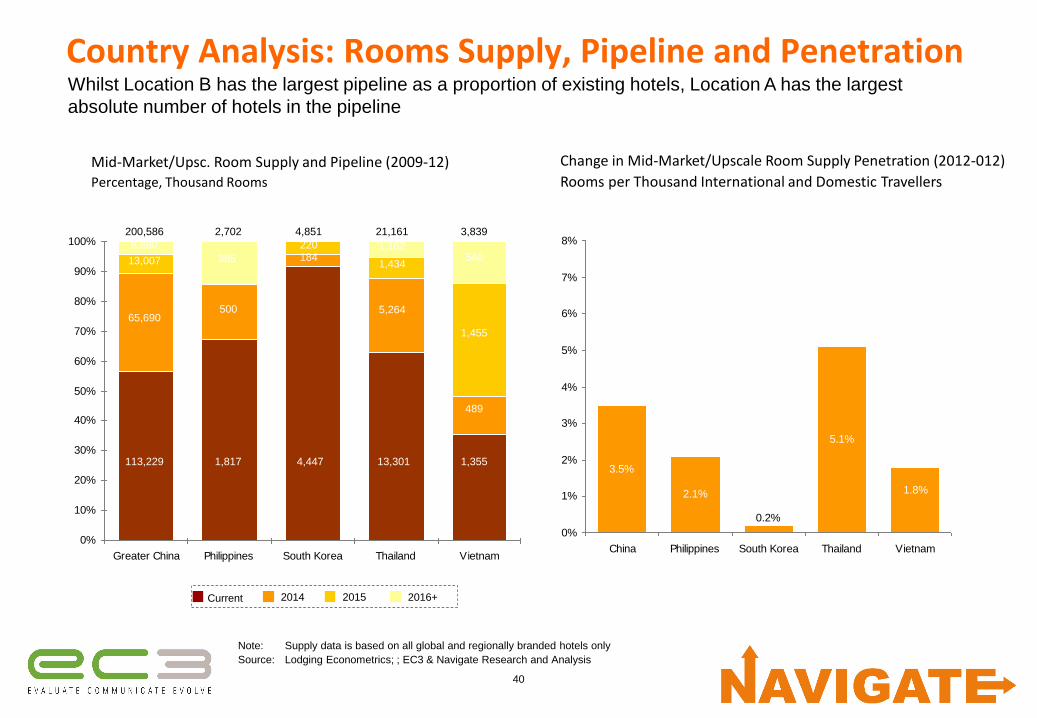

Whilst Location B has the largest pipeline as a proportion of existing hotels, Location A has the largest

absolute number of hotels in the pipeline

Mid-Market/Upsc. Room Supply and Pipeline (2009-12)Percentage, Thousand Rooms

Current 2014 2015 2016+

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Greater China Philippines South Korea Thailand Vietnam

113,229

65,690

13,007

8,660

1,817

385

4,447

184220

13,301

5,264

1,434

1,162

1,455

200,586 2,702 4,851 21,161 3,839

Country Analysis: Rooms Supply, Pipeline and Penetration

Change in Mid-Market/Upscale Room Supply Penetration (2012-012)

Rooms per Thousand International and Domestic Travellers

500

1,355

489

540

41

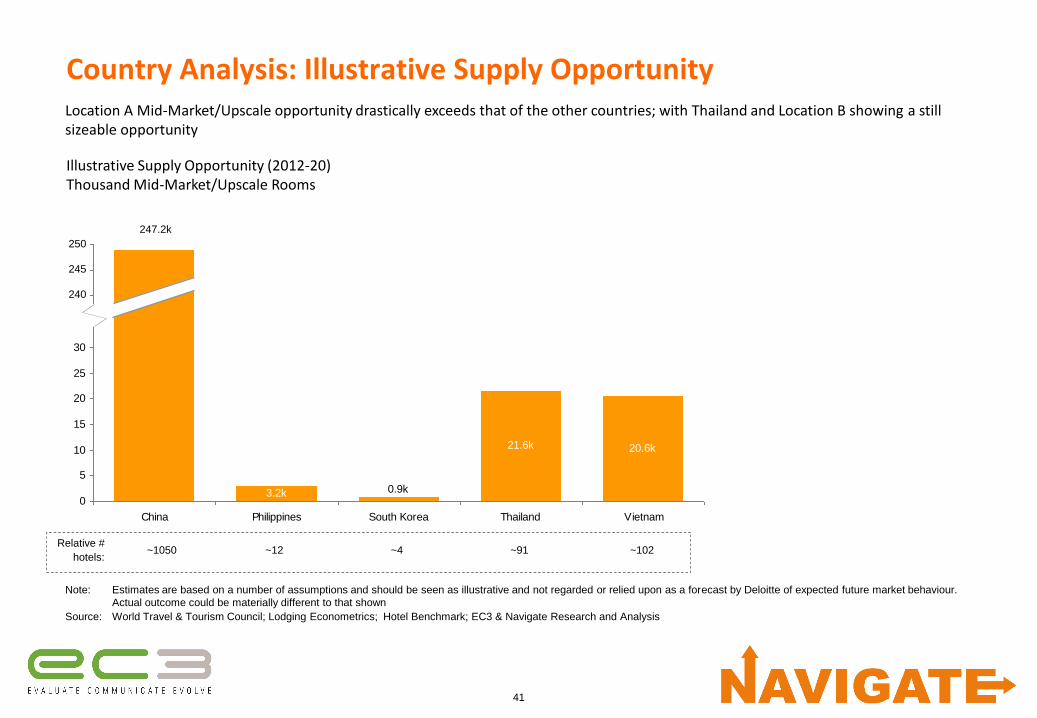

3.2k

21.6k 20.6k

0.9k0

5

10

15

20

25

30

35

40

45

50

China Philippines South Korea Thailand Vietnam

Location A Mid-Market/Upscale opportunity drastically exceeds that of the other countries; with Thailand and Location B showing a still sizeable opportunity

Illustrative Supply Opportunity (2012-20)Thousand Mid-Market/Upscale Rooms

Note: Estimates are based on a number of assumptions and should be seen as illustrative and not regarded or relied upon as a forecast by Deloitte of expected future market behaviour.

Actual outcome could be materially different to that shown

Source: World Travel & Tourism Council; Lodging Econometrics; Hotel Benchmark; EC3 & Navigate Research and Analysis

Country Analysis: Illustrative Supply Opportunity

240

245

250

247.2k

Relative #

hotels:~1050 ~12 ~4 ~91 ~102

42

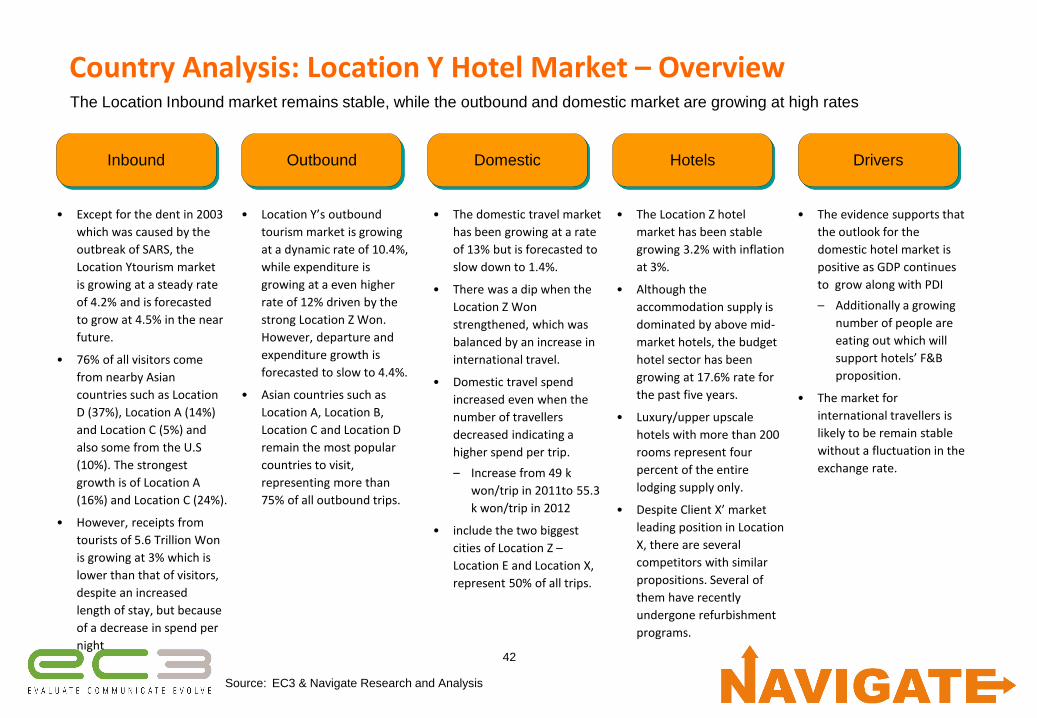

Country Analysis: Location Y Hotel Market – Overview

Source: EC3 & Navigate Research and Analysis

The Location Inbound market remains stable, while the outbound and domestic market are growing at high rates

Inbound Outbound Hotels

• Except for the dent in 2003

which was caused by the

outbreak of SARS, the

Location Ytourism market

is growing at a steady rate

of 4.2% and is forecasted

to grow at 4.5% in the near

future.

• 76% of all visitors come

from nearby Asian

countries such as Location

D (37%), Location A (14%)

and Location C (5%) and

also some from the U.S

(10%). The strongest

growth is of Location A

(16%) and Location C (24%).

• However, receipts from

tourists of 5.6 Trillion Won

is growing at 3% which is

lower than that of visitors,

despite an increased

length of stay, but because

of a decrease in spend per

night

• Location Y’s outbound

tourism market is growing

at a dynamic rate of 10.4%,

while expenditure is

growing at a even higher

rate of 12% driven by the

strong Location Z Won.

However, departure and

expenditure growth is

forecasted to slow to 4.4%.

• Asian countries such as

Location A, Location B,

Location C and Location D

remain the most popular

countries to visit,

representing more than

75% of all outbound trips.

• The Location Z hotel

market has been stable

growing 3.2% with inflation

at 3%.

• Although the

accommodation supply is

dominated by above mid-

market hotels, the budget

hotel sector has been

growing at 17.6% rate for

the past five years.

• Luxury/upper upscale

hotels with more than 200

rooms represent four

percent of the entire

lodging supply only.

• Despite Client X’ market

leading position in Location

X, there are several

competitors with similar

propositions. Several of

them have recently

undergone refurbishment

programs.

Domestic

• The domestic travel market

has been growing at a rate

of 13% but is forecasted to

slow down to 1.4%.

• There was a dip when the

Location Z Won

strengthened, which was

balanced by an increase in

international travel.

• Domestic travel spend

increased even when the

number of travellers

decreased indicating a

higher spend per trip.

– Increase from 49 k

won/trip in 2011to 55.3

k won/trip in 2012

• include the two biggest

cities of Location Z –

Location E and Location X,

represent 50% of all trips.

Drivers

• The evidence supports that

the outlook for the

domestic hotel market is

positive as GDP continues

to grow along with PDI

– Additionally a growing

number of people are

eating out which will

support hotels’ F&B

proposition.

• The market for

international travellers is

likely to be remain stable

without a fluctuation in the

exchange rate.

43

Country Analysis: Summary – Key Decision-making Drivers

Key metricsDemand

Drivers

Location Z

Arrivals

Illustrative

opportunity

Historical

Performance

(KPIs and

profitability)

Investment in

Tourism

Business

Environment

Illustrative

Yield

Ability to

implement

Weighting Medium Medium High Medium Low Low High High

Location A

Philippines

Location Y

Thailand

Location B

Summary of Key Decision-making DriversIndicative

Source: EC3 & Navigate Research and Analysis

The summary of key decision-making drivers shows medium to high results for most countries

44

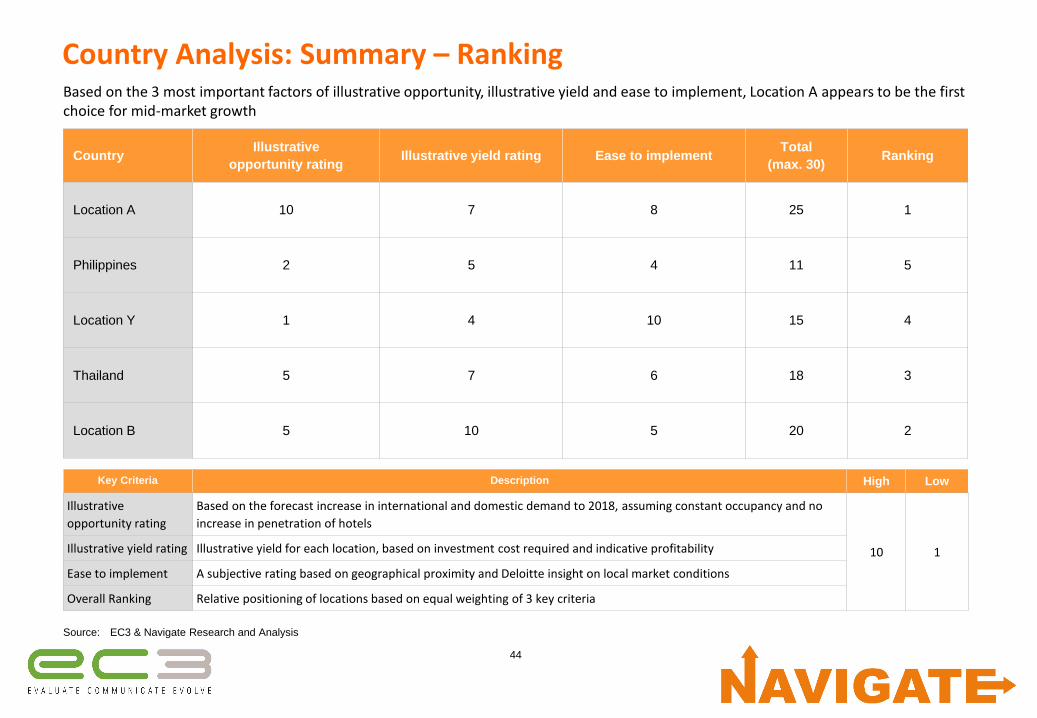

Country Analysis: Summary – RankingBased on the 3 most important factors of illustrative opportunity, illustrative yield and ease to implement, Location A appears to be the first choice for mid-market growth

CountryIllustrative

opportunity ratingIllustrative yield rating Ease to implement

Total

(max. 30)Ranking

Location A 10 7 8 25 1

Philippines 2 5 4 11 5

Location Y 1 4 10 15 4

Thailand 5 7 6 18 3

Location B 5 10 5 20 2

Source: EC3 & Navigate Research and Analysis

Key Criteria Description High Low

Illustrative

opportunity rating

Based on the forecast increase in international and domestic demand to 2018, assuming constant occupancy and no

increase in penetration of hotels

10 1Illustrative yield rating Illustrative yield for each location, based on investment cost required and indicative profitability

Ease to implement A subjective rating based on geographical proximity and Deloitte insight on local market conditions

Overall Ranking Relative positioning of locations based on equal weighting of 3 key criteria

45

Agenda1. Approach

2. Industry overview

3. Sector analysis

• Region

• Country

• City

4. Strategic options

5. Selected strategy

6. Next steps

46

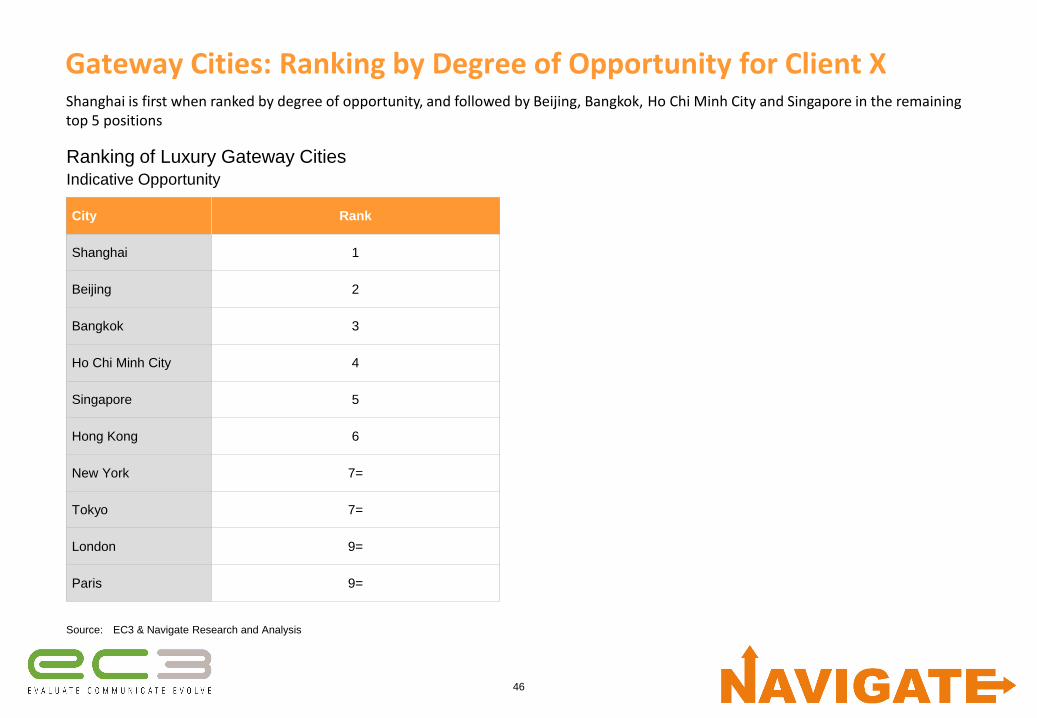

Gateway Cities: Ranking by Degree of Opportunity for Client X

City Rank

Shanghai 1

Beijing 2

Bangkok 3

Ho Chi Minh City 4

Singapore 5

Hong Kong 6

New York 7=

Tokyo 7=

London 9=

Paris 9=

Source: EC3 & Navigate Research and Analysis

Ranking of Luxury Gateway CitiesIndicative Opportunity

Shanghai is first when ranked by degree of opportunity, and followed by Beijing, Bangkok, Ho Chi Minh City and Singapore in the remaining top 5 positions

47

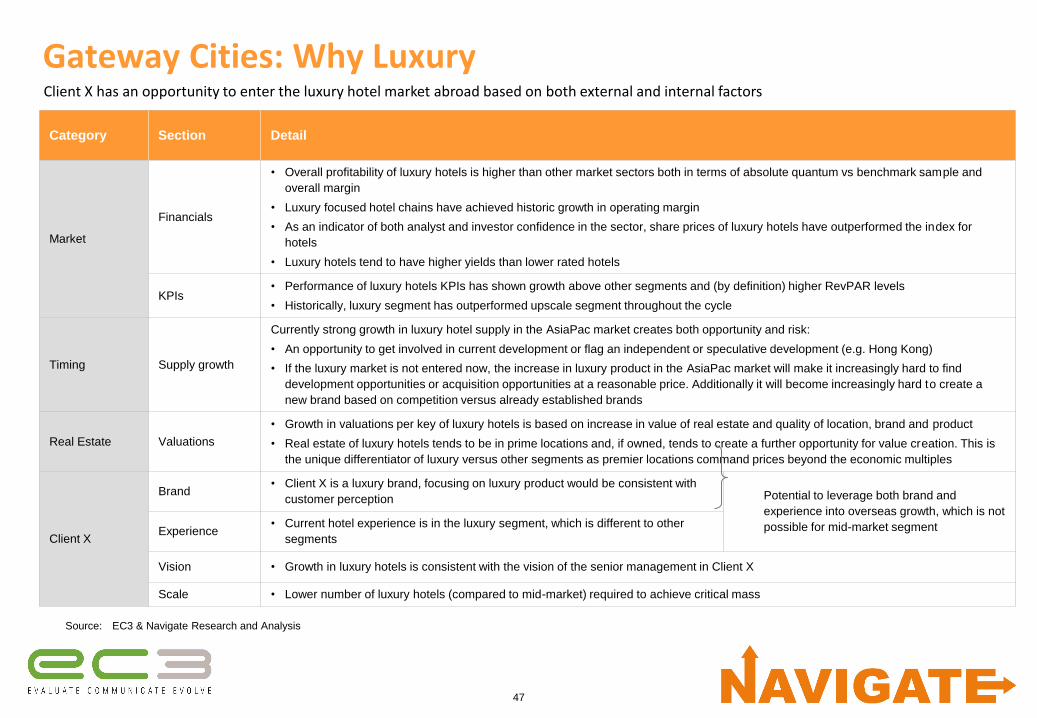

Gateway Cities: Why Luxury

Category Section Detail

Market

Financials

• Overall profitability of luxury hotels is higher than other market sectors both in terms of absolute quantum vs benchmark sample and

overall margin

• Luxury focused hotel chains have achieved historic growth in operating margin

• As an indicator of both analyst and investor confidence in the sector, share prices of luxury hotels have outperformed the index for

hotels

• Luxury hotels tend to have higher yields than lower rated hotels

KPIs• Performance of luxury hotels KPIs has shown growth above other segments and (by definition) higher RevPAR levels

• Historically, luxury segment has outperformed upscale segment throughout the cycle

Timing Supply growth

Currently strong growth in luxury hotel supply in the AsiaPac market creates both opportunity and risk:

• An opportunity to get involved in current development or flag an independent or speculative development (e.g. Hong Kong)

• If the luxury market is not entered now, the increase in luxury product in the AsiaPac market will make it increasingly hard to find

development opportunities or acquisition opportunities at a reasonable price. Additionally it will become increasingly hard to create a

new brand based on competition versus already established brands

Real Estate Valuations

• Growth in valuations per key of luxury hotels is based on increase in value of real estate and quality of location, brand and product

• Real estate of luxury hotels tends to be in prime locations and, if owned, tends to create a further opportunity for value creation. This is

the unique differentiator of luxury versus other segments as premier locations command prices beyond the economic multiples

Client X

Brand• Client X is a luxury brand, focusing on luxury product would be consistent with

customer perception Potential to leverage both brand and

experience into overseas growth, which is not

possible for mid-market segmentExperience• Current hotel experience is in the luxury segment, which is different to other

segments

Vision • Growth in luxury hotels is consistent with the vision of the senior management in Client X

Scale • Lower number of luxury hotels (compared to mid-market) required to achieve critical mass

Client X has an opportunity to enter the luxury hotel market abroad based on both external and internal factors

Source: EC3 & Navigate Research and Analysis

48

Gateway Cities: Current and Pipeline Supply

Source: Lodging Econometrics; EC3 & Navigate Research and Analysis

The largest pipelines – both in terms of total rooms and as share of current supply – are found in the Chinese cities

29.1k

51.1k

4.5k

23.2k

29.5k

54.6k

19.3k

35.9k

12.7k

26.7k

2.5k

8.1k

7.8k

6.2k

8.7k

0.2k

0.3k

0.5k

1.6k

0.6k

0

10

20

30

40

50

60

70

Bangkok Beijing Ho Chi Minh City Hong Kong London New York Paris Shanghai Singapore Tokyo

Current (2012) and Pipeline (c. 2012-20) Upper Upscale / Luxury Supply by City

Thousand Rooms

Current Supply Pipeline

Pipeline: 8.7% 15.9% 12.8% 33.6% 5.5% 11.3% 2.8% 24.1% 2.1% 0.8%

Predominantly

independents

49

Paris

Ho Chi Minh City

Hong Kong

0

50

100

150

200

250

300

350

400

450

0% 5% 10% 15% 20% 25% 30% 35% 40%

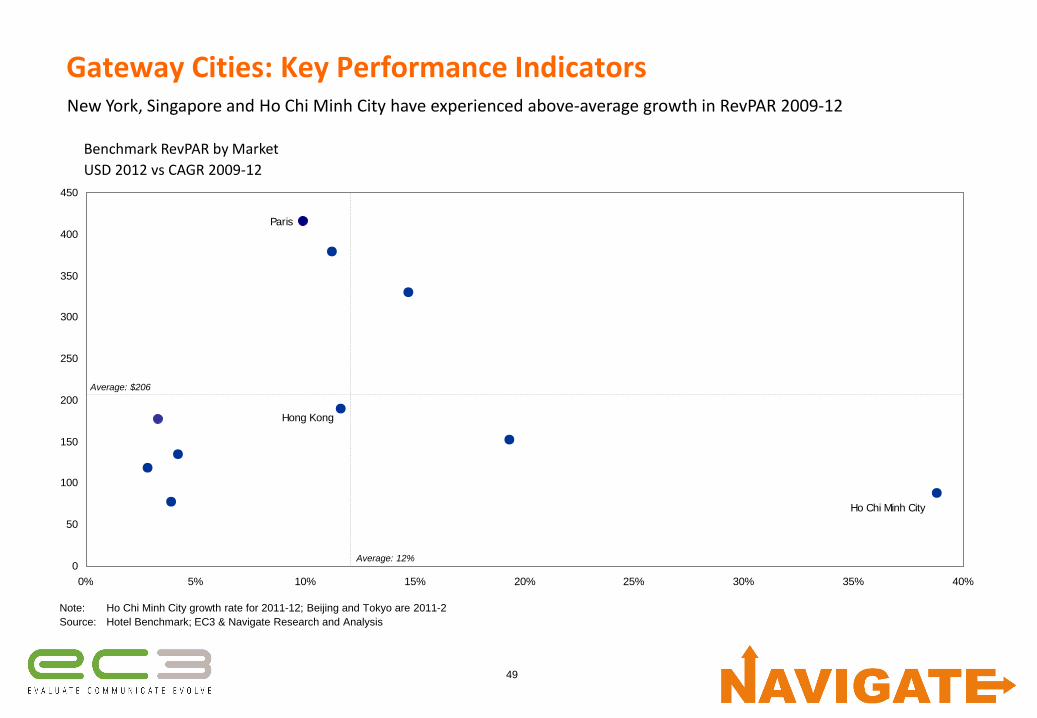

Gateway Cities: Key Performance IndicatorsNew York, Singapore and Ho Chi Minh City have experienced above-average growth in RevPAR 2009-12

Benchmark RevPAR by Market

USD 2012 vs CAGR 2009-12

Note: Ho Chi Minh City growth rate for 2011-12; Beijing and Tokyo are 2011-2

Source: Hotel Benchmark; EC3 & Navigate Research and Analysis

Average: 12%

Average: $206

50

0

50

100

150

200

250

300

350

400

450

500

25% 30% 35% 40% 45% 50% 55%

Singapore

Hong Kong

Bangkok

Shanghai

Beijing

Ho Chi Minh City

Tokyo

Paris

London

New York

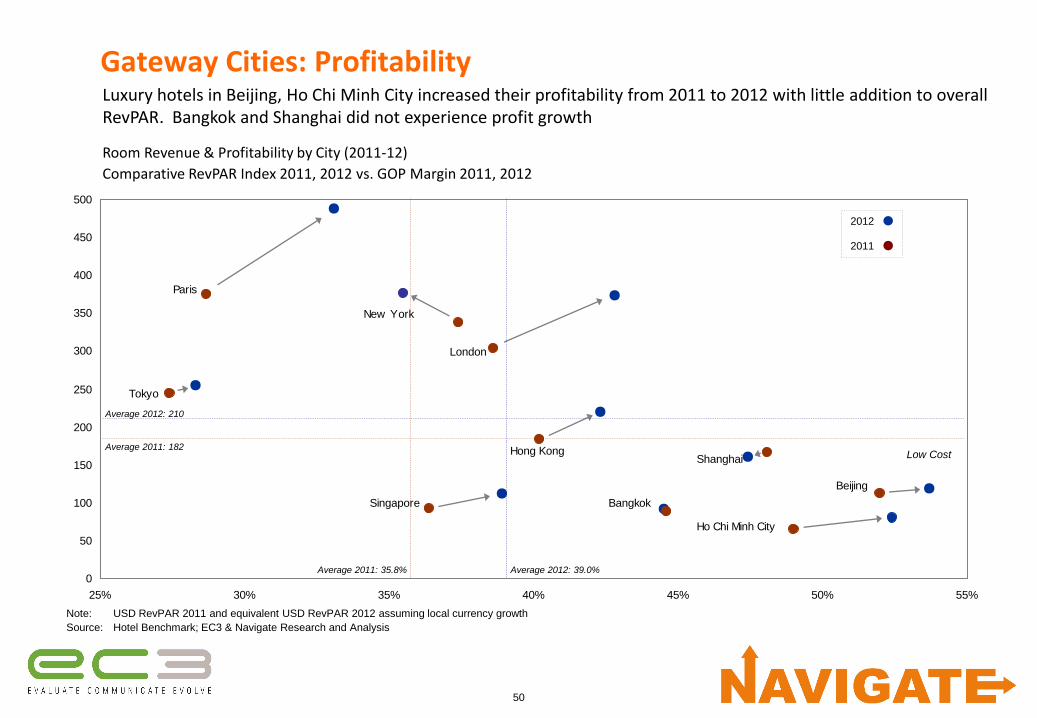

Gateway Cities: ProfitabilityLuxury hotels in Beijing, Ho Chi Minh City increased their profitability from 2011 to 2012 with little addition to overall RevPAR. Bangkok and Shanghai did not experience profit growth

Room Revenue & Profitability by City (2011-12)

Comparative RevPAR Index 2011, 2012 vs. GOP Margin 2011, 2012

Average 2012: 210

Note: USD RevPAR 2011 and equivalent USD RevPAR 2012 assuming local currency growth

Source: Hotel Benchmark; EC3 & Navigate Research and Analysis

Average 2012: 39.0%

2012

2011

Average 2011: 182

Average 2011: 35.8%

Low Cost

51

Gateway Cities: Illustrative Supply OpportunityThe Chinese gateways appear to have the largest opportunity, driven by growth in demand

43.2k

4.0k

19.7k

9.2k

19.2k

6.5k

32.5k

6.5k9.1k

17.3k

0

5

10

15

20

25

30

35

40

45

50

Bangkok Beijing HCMC Hong Kong London New York Paris Shanghai Singapore Tokyo

Illustrative Supply Opportunity (2012-20)Thousand Upper Upscale / Luxury Rooms

Note: Estimates are based on a number of assumptions and should be seen as illustrative and not regarded or relied upon as a forecast by Navigate of expected future market behaviour.

Actual outcome could be materially different to that shown

Source: World Travel & Tourism Council; Lodging Econometrics; Hotel Benchmark; EC3 & Navigate Research and Analysis

Relative #

hotels:~53 ~123 ~15 ~46 ~58 ~62 ~44 ~115 ~14 ~20

52

New York

New York 2010-12

0

100

200

300

400

500

600

700

800

900

0% 1% 2% 3% 4% 5% 6% 7% 8%

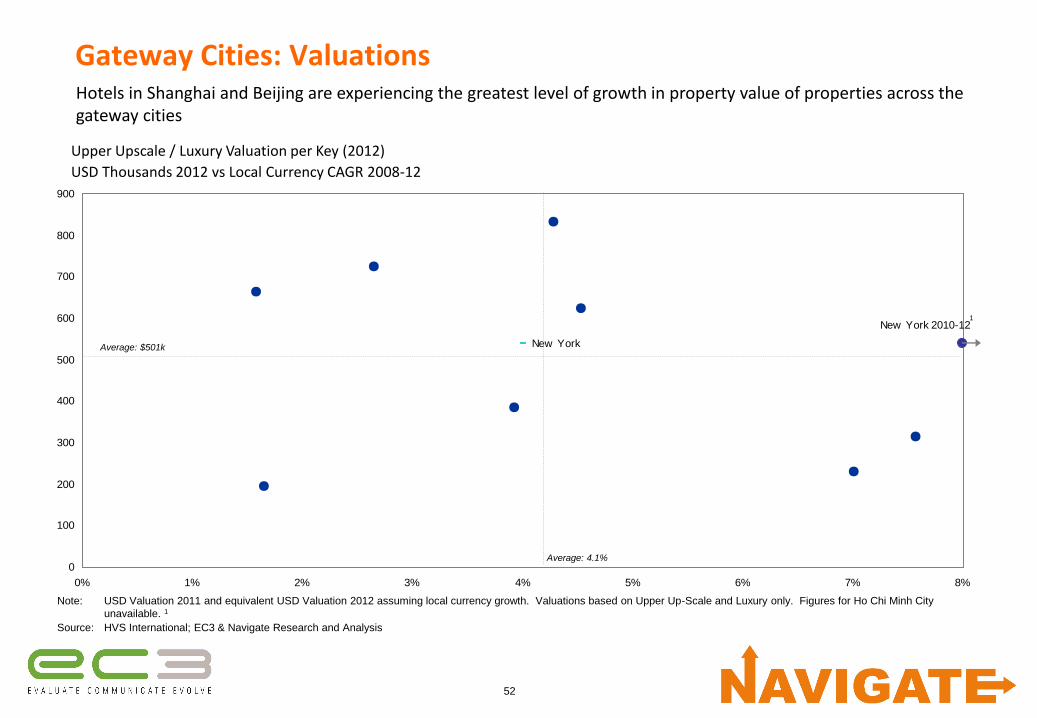

Gateway Cities: ValuationsHotels in Shanghai and Beijing are experiencing the greatest level of growth in property value of properties across the gateway cities

Upper Upscale / Luxury Valuation per Key (2012)

USD Thousands 2012 vs Local Currency CAGR 2008-12

Note: USD Valuation 2011 and equivalent USD Valuation 2012 assuming local currency growth. Valuations based on Upper Up-Scale and Luxury only. Figures for Ho Chi Minh City

unavailable. 1

Source: HVS International; EC3 & Navigate Research and Analysis

Average: 4.1%

Average: $501k

1

53

2012

2011

Singapore

Bangkok

Shanghai

Beijing

Tokyo

New York

Relatively high return and low investment costs

Gateway Cities: Yields – AcquisitionThailand and Chinese cities offer the highest yields at relatively low investment levels

Illustrative Acquisition Upper Upscale / Luxury Yield by City (2011-12)

Valuation Thousand USD vs. Benchmark Percentage Return per Annum

Note: Valuation figures not available for Ho Chi Minh City; IBFC excludes ownership costs (rates, insurance, rent, interest,

management fees, depreciation and taxes). Relative yield equals IBFC per key divided by valuation per key

Source: Hotel Benchmark; HVS International; ; EC3 & Navigate Research and Analysis

Annual Income before Fixed Charges per available room,

expressed as a percentage of valuation per Room

Locati

on X

0

100

200

300

400

500

600

700

800

900

5% 7% 9% 11% 13% 15% 17% 19% 21%

Market valuations increasing faster

than increases in hotel IBFC

Market valuations increasing less

than increases in hotel IBFC

Hong Kong

Paris

54

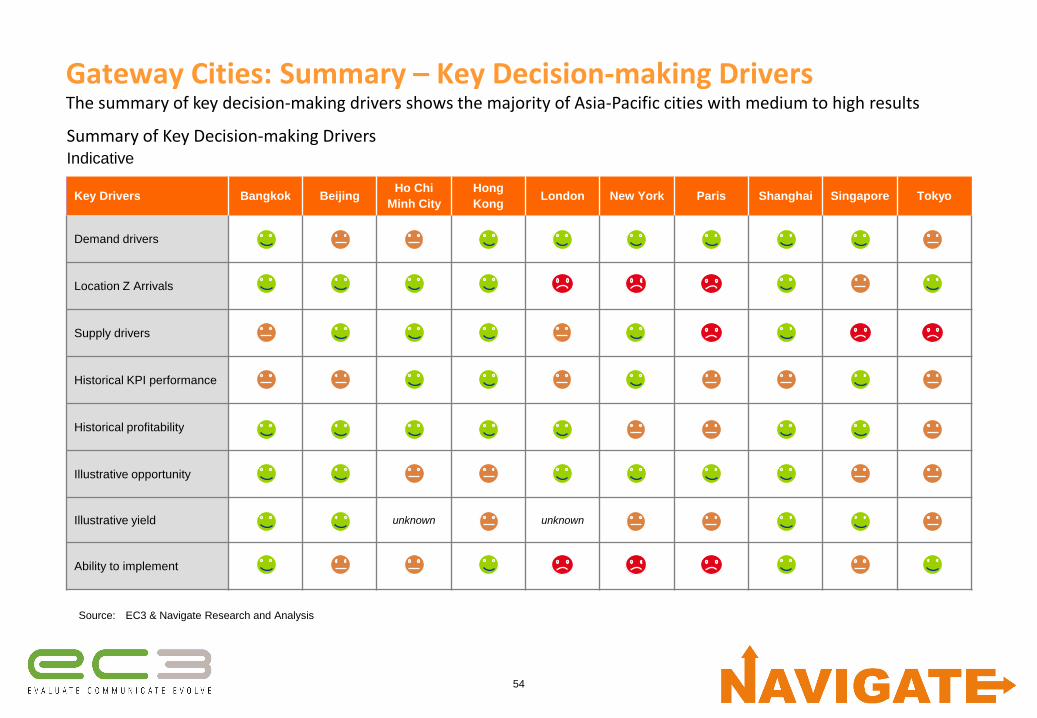

Gateway Cities: Summary – Key Decision-making Drivers

Source: EC3 & Navigate Research and Analysis

Key Drivers Bangkok BeijingHo Chi

Minh City

Hong

KongLondon New York Paris Shanghai Singapore Tokyo

Demand drivers

Location Z Arrivals

Supply drivers

Historical KPI performance

Historical profitability

Illustrative opportunity

Illustrative yield unknown unknown

Ability to implement

Summary of Key Decision-making DriversIndicative

The summary of key decision-making drivers shows the majority of Asia-Pacific cities with medium to high results

55

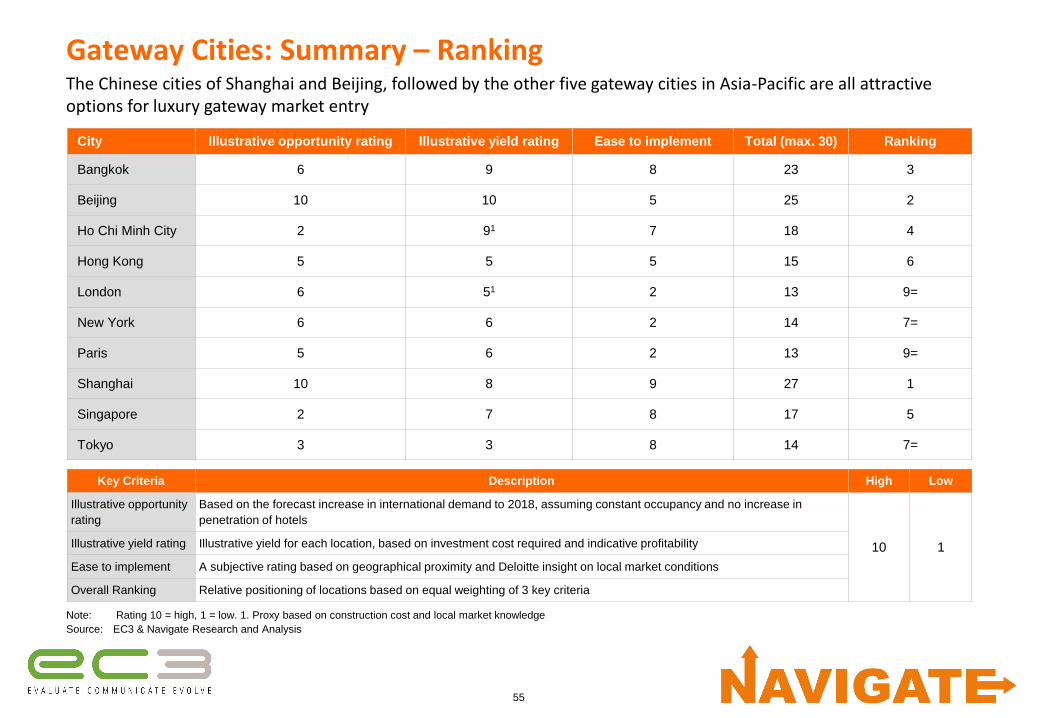

Gateway Cities: Summary – RankingThe Chinese cities of Shanghai and Beijing, followed by the other five gateway cities in Asia-Pacific are all attractive options for luxury gateway market entry

City Illustrative opportunity rating Illustrative yield rating Ease to implement Total (max. 30) Ranking

Bangkok 6 9 8 23 3

Beijing 10 10 5 25 2

Ho Chi Minh City 2 91 7 18 4

Hong Kong 5 5 5 15 6

London 6 51 2 13 9=

New York 6 6 2 14 7=

Paris 5 6 2 13 9=

Shanghai 10 8 9 27 1

Singapore 2 7 8 17 5

Tokyo 3 3 8 14 7=

Note: Rating 10 = high, 1 = low. 1. Proxy based on construction cost and local market knowledge

Source: EC3 & Navigate Research and Analysis

Key Criteria Description High Low

Illustrative opportunity

rating

Based on the forecast increase in international demand to 2018, assuming constant occupancy and no increase in

penetration of hotels

10 1Illustrative yield rating Illustrative yield for each location, based on investment cost required and indicative profitability

Ease to implement A subjective rating based on geographical proximity and Deloitte insight on local market conditions

Overall Ranking Relative positioning of locations based on equal weighting of 3 key criteria

56

Agenda1. Approach

2. Industry overview

3. Sector analysis

4. Strategic options

• Overview

• Organic

• M&A

5. Selected strategy

6. Next steps

57

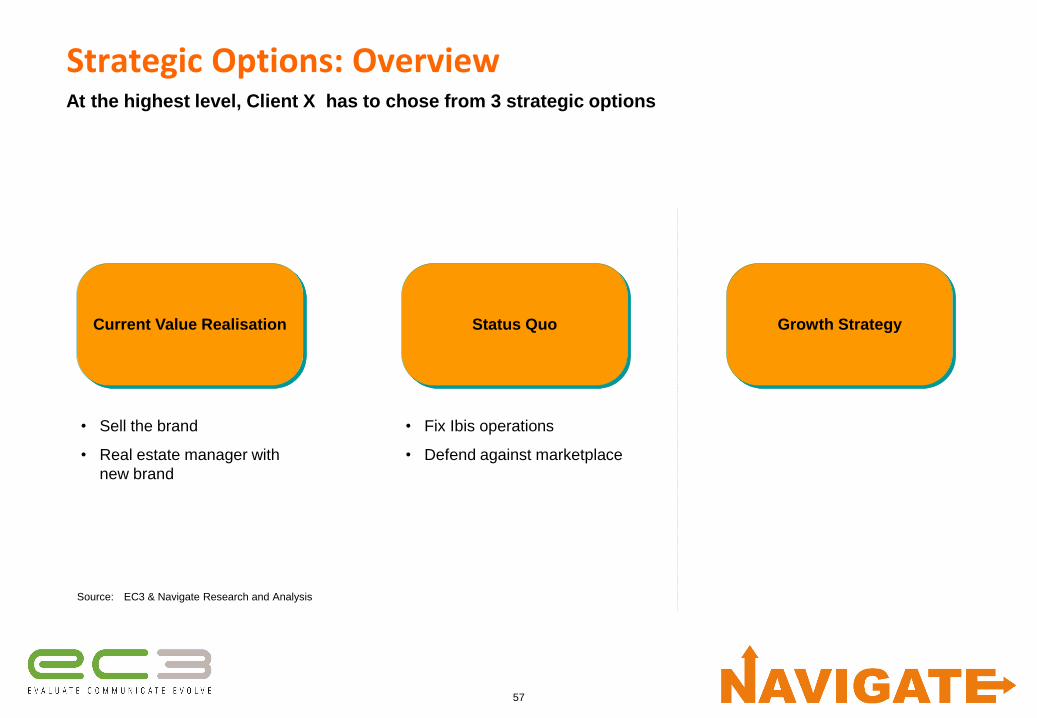

Strategic Options: Overview

Current Value Realisation Status Quo Growth Strategy

At the highest level, Client X has to chose from 3 strategic options

Source: EC3 & Navigate Research and Analysis

• Sell the brand

• Real estate manager with

new brand

• Fix Ibis operations

• Defend against marketplace

58

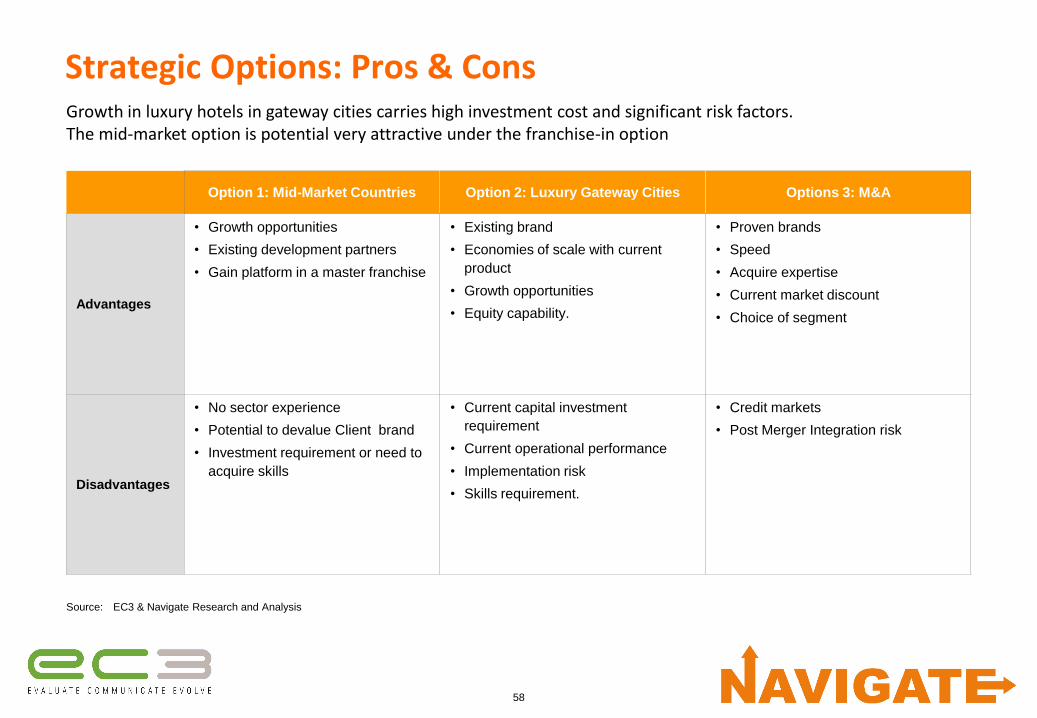

Strategic Options: Pros & ConsGrowth in luxury hotels in gateway cities carries high investment cost and significant risk factors.The mid-market option is potential very attractive under the franchise-in option

Option 1: Mid-Market Countries Option 2: Luxury Gateway Cities Options 3: M&A

Advantages

• Growth opportunities

• Existing development partners

• Gain platform in a master franchise

• Existing brand

• Economies of scale with current

product

• Growth opportunities

• Equity capability.

• Proven brands

• Speed

• Acquire expertise

• Current market discount

• Choice of segment

Disadvantages

• No sector experience

• Potential to devalue Client brand

• Investment requirement or need to

acquire skills

• Current capital investment

requirement

• Current operational performance

• Implementation risk

• Skills requirement.

• Credit markets

• Post Merger Integration risk

Source: EC3 & Navigate Research and Analysis

59

Strategic Options: Organic Growth – Available Operating ModelsClient X will need to follow an owned/leased operating model in both the mid-market and luxury sector in the short to medium term, until it is able to prove its ability to operate hotels profitably to owners

Owned/Leased

under Client X Brand

or Client X Brand

Family

Entering the mid-market with a Client X brand would

be high risk due to the lack of an existing brand, and

lack of experience and skills in the mid-market.

If Client X is willing to commit significant investment

capital into owned/leased hotels, it will be able to

enter gateway cities in the luxury sector

Managed

under Client X Brand

or Client X Brand

Family

For the above reasons it would be highly risky to

attempt to manage hotels under a Client X mid-

market brand. Furthermore, returns are likely to be

higher under a franchised in brand.

Client X will only be able to secure management

contracts in the luxury sector in gateway cities (other

than potentially in Location X) once it has a proven

track record. This will be in the medium to long term.

Owned/Leased

under franchised in

brand

Depending availability within each country, Client X

has the potential to franchise in a global brand and

capitalise on their brand, operational experience and

procedures, sales and marketing platform, etc.

Not applicable as luxury operators do not franchise

out their brands.

Managed

under franchised in

brand

Not applicable in short to medium term until Client X

can prove to owners that it can operate effectively.

Not applicable as luxury operators do not franchise

out their brands.

Mid-market in focus countries Luxury in gateway cities

= Operating models available to Client X in the short to medium term

Source: EC3 & Navigate Research and Analysis

60

Strategic Options: Key Components of a Platform for Profitable Growth

Sales and marketing

• Global or regional sales and marketing team driving reservations

• Participation in global marketing strategies and programmes (e.g. promotions, yield management)

• Access to a globally recognised guest loyalty program (driving 30% - 50% of paid room nights)

• Strong cost effective distribution systems including website and GDS

• Standard operating procedures

• Improving hotel operating margins through procurement savings

• Providing shared services

• Providing access to training

• Brand standards

• Architecture and construction services

• Providing local development expertise

• Financial modelling

• Expertise in maximising real estate values

Operations

Development

Source: EC3 & Navigate Research and Analysis

Real estate

61

Strategic Options: Focus Country International ArrivalsBased on number of international arrivals (line width) and historical growth (%), Location A and Location B appear to be the most attractive country options. However, this will depend on risk/reward aptitude

Note: Reflects major population flows between focus countries only

Source: Euromonitor; EC3 & Navigate Research and Analysis

Location ALocation B

ThailandPhilippines

Rep. of

Location Z 30%15%

16%

18%

16%

22%

3%

51%

20%

4%

13%

11%

12%

Suggested countries of focus

3%Historical growth &

International Arrivals

2008-12

Approx. # Int’l Arrivals

3.0m

1.0m

0.5m

62

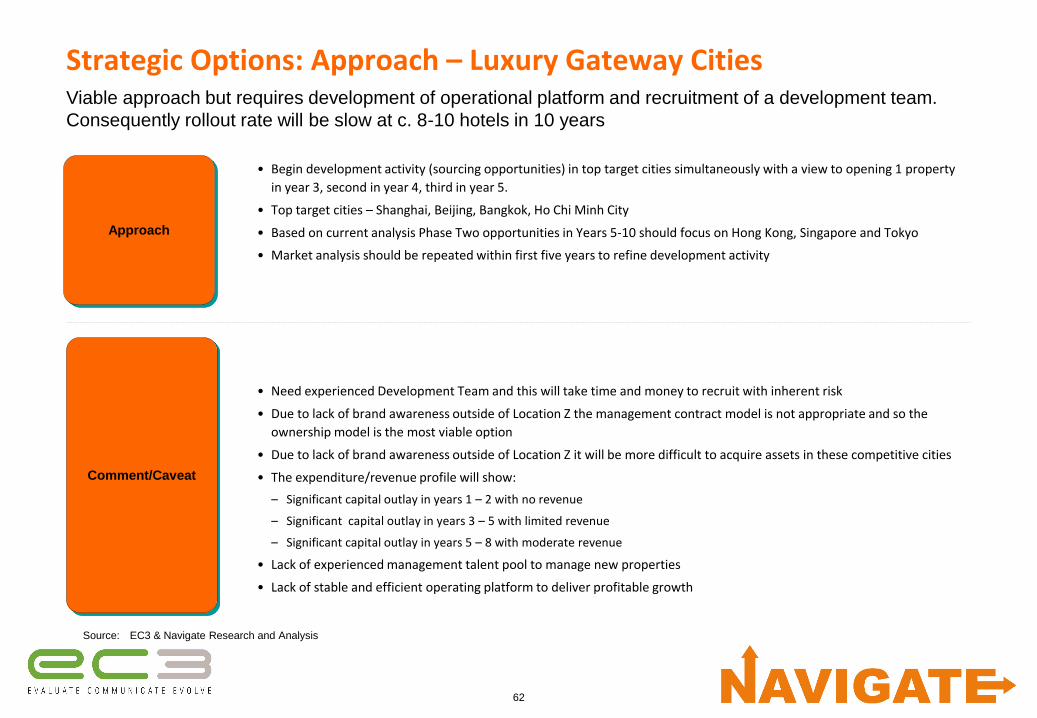

Strategic Options: Approach – Luxury Gateway CitiesViable approach but requires development of operational platform and recruitment of a development team.

Consequently rollout rate will be slow at c. 8-10 hotels in 10 years

Approach

• Begin development activity (sourcing opportunities) in top target cities simultaneously with a view to opening 1 property

in year 3, second in year 4, third in year 5.

• Top target cities – Shanghai, Beijing, Bangkok, Ho Chi Minh City

• Based on current analysis Phase Two opportunities in Years 5-10 should focus on Hong Kong, Singapore and Tokyo

• Market analysis should be repeated within first five years to refine development activity

• Need experienced Development Team and this will take time and money to recruit with inherent risk

• Due to lack of brand awareness outside of Location Z the management contract model is not appropriate and so the

ownership model is the most viable option

• Due to lack of brand awareness outside of Location Z it will be more difficult to acquire assets in these competitive cities

• The expenditure/revenue profile will show:

– Significant capital outlay in years 1 – 2 with no revenue

– Significant capital outlay in years 3 – 5 with limited revenue

– Significant capital outlay in years 5 – 8 with moderate revenue

• Lack of experienced management talent pool to manage new properties

• Lack of stable and efficient operating platform to deliver profitable growth

Comment/Caveat

Source: EC3 & Navigate Research and Analysis

63

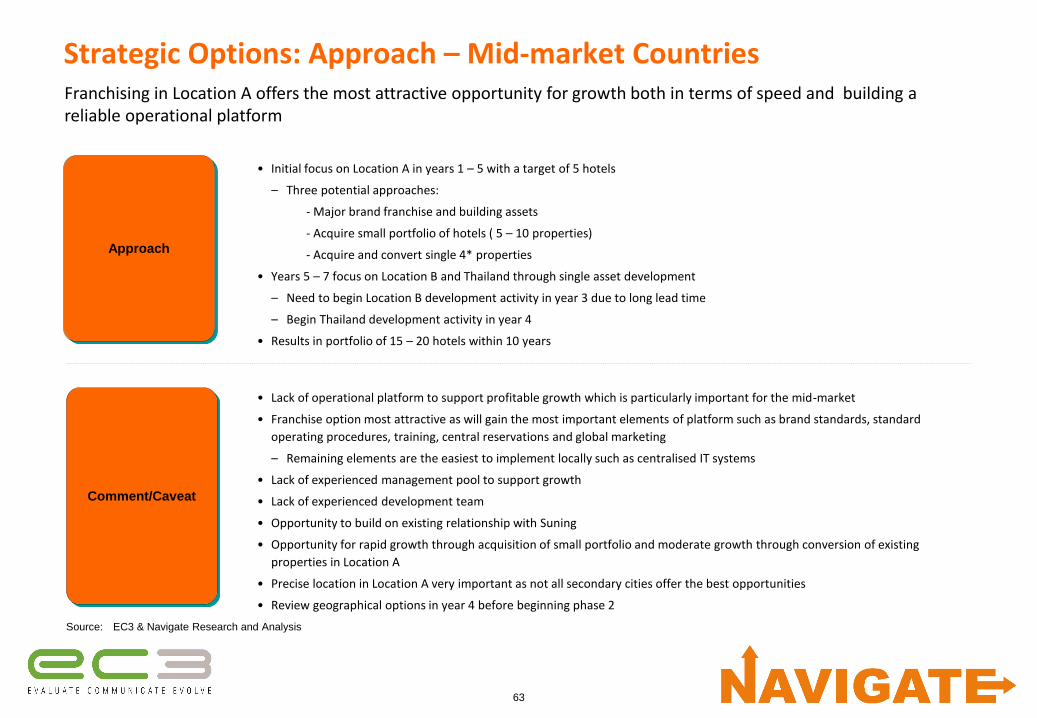

Strategic Options: Approach – Mid-market CountriesFranchising in Location A offers the most attractive opportunity for growth both in terms of speed and building a reliable operational platform

Approach

• Initial focus on Location A in years 1 – 5 with a target of 5 hotels

– Three potential approaches:

- Major brand franchise and building assets

- Acquire small portfolio of hotels ( 5 – 10 properties)

- Acquire and convert single 4* properties

• Years 5 – 7 focus on Location B and Thailand through single asset development

– Need to begin Location B development activity in year 3 due to long lead time

– Begin Thailand development activity in year 4

• Results in portfolio of 15 – 20 hotels within 10 years

• Lack of operational platform to support profitable growth which is particularly important for the mid-market

• Franchise option most attractive as will gain the most important elements of platform such as brand standards, standard

operating procedures, training, central reservations and global marketing

– Remaining elements are the easiest to implement locally such as centralised IT systems

• Lack of experienced management pool to support growth

• Lack of experienced development team

• Opportunity to build on existing relationship with Suning

• Opportunity for rapid growth through acquisition of small portfolio and moderate growth through conversion of existing

properties in Location A

• Precise location in Location A very important as not all secondary cities offer the best opportunities

• Review geographical options in year 4 before beginning phase 2

Comment/Caveat

Source: EC3 & Navigate Research and Analysis

64

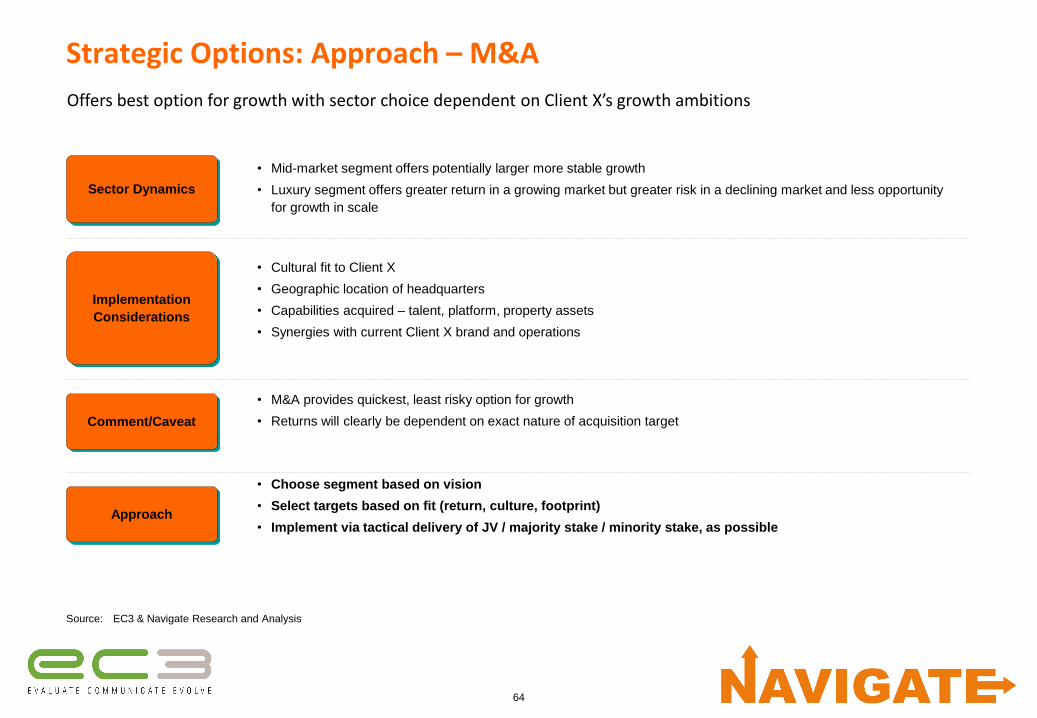

Strategic Options: Approach – M&A

Offers best option for growth with sector choice dependent on Client X’s growth ambitions

Sector Dynamics

• Mid-market segment offers potentially larger more stable growth

• Luxury segment offers greater return in a growing market but greater risk in a declining market and less opportunity

for growth in scale

• Cultural fit to Client X

• Geographic location of headquarters

• Capabilities acquired – talent, platform, property assets

• Synergies with current Client X brand and operations

• M&A provides quickest, least risky option for growth

• Returns will clearly be dependent on exact nature of acquisition target

• Choose segment based on vision

• Select targets based on fit (return, culture, footprint)

• Implement via tactical delivery of JV / majority stake / minority stake, as possible

Implementation

Considerations

Comment/Caveat

Source: EC3 & Navigate Research and Analysis

Approach

65

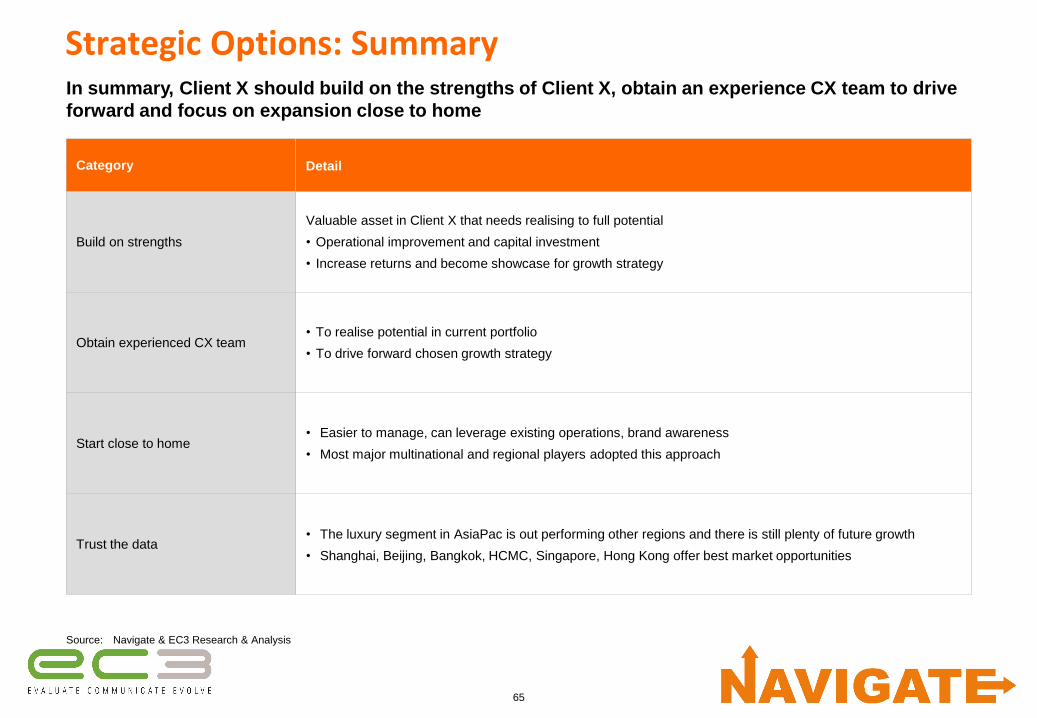

Strategic Options: Summary

Category Detail

Build on strengths

Valuable asset in Client X that needs realising to full potential

• Operational improvement and capital investment

• Increase returns and become showcase for growth strategy

Obtain experienced CX team• To realise potential in current portfolio

• To drive forward chosen growth strategy

Start close to home• Easier to manage, can leverage existing operations, brand awareness

• Most major multinational and regional players adopted this approach

Trust the data• The luxury segment in AsiaPac is out performing other regions and there is still plenty of future growth

• Shanghai, Beijing, Bangkok, HCMC, Singapore, Hong Kong offer best market opportunities

Source: Navigate & EC3 Research & Analysis

In summary, Client X should build on the strengths of Client X, obtain an experience CX team to drive

forward and focus on expansion close to home

66

Agenda

1. Approach

2. Industry overview

3. Sector analysis

4. Strategic options

5. Selected strategy

• Foundation stage

• Growth stage

• Financial implications

6. Next steps

67

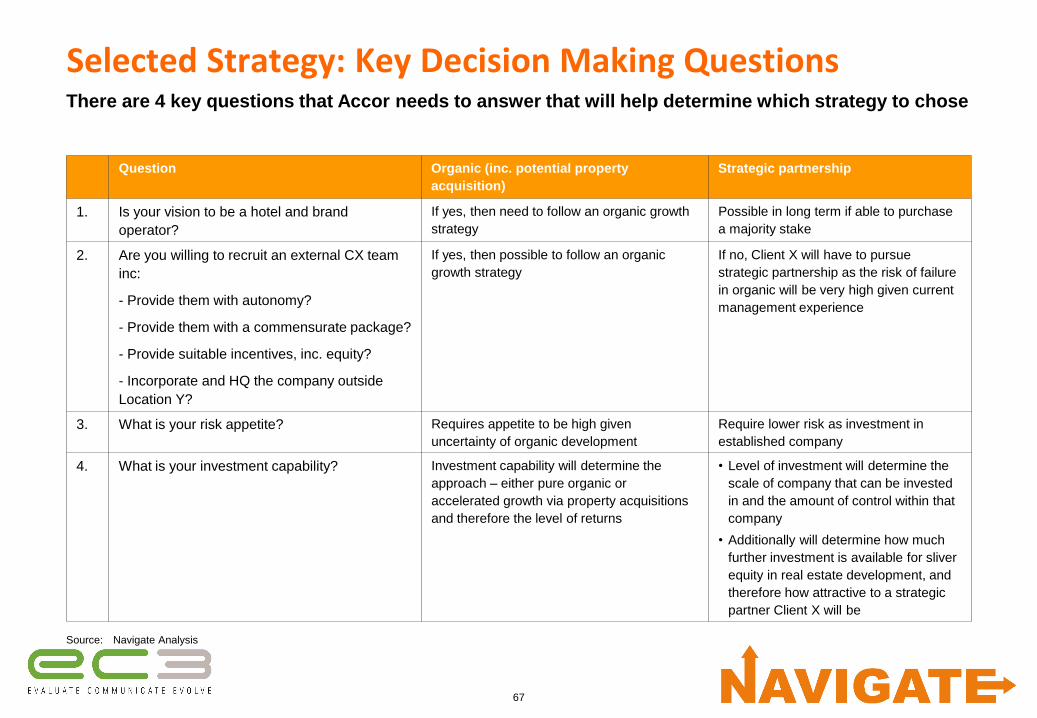

Selected Strategy: Key Decision Making QuestionsThere are 4 key questions that Accor needs to answer that will help determine which strategy to chose

Source: Navigate Analysis

Question Organic (inc. potential property

acquisition)

Strategic partnership

1. Is your vision to be a hotel and brand

operator?

If yes, then need to follow an organic growth

strategy

Possible in long term if able to purchase

a majority stake

2. Are you willing to recruit an external CX team

inc:

- Provide them with autonomy?

- Provide them with a commensurate package?

- Provide suitable incentives, inc. equity?

- Incorporate and HQ the company outside

Location Y?

If yes, then possible to follow an organic

growth strategy

If no, Client X will have to pursue

strategic partnership as the risk of failure

in organic will be very high given current

management experience

3. What is your risk appetite? Requires appetite to be high given

uncertainty of organic development

Require lower risk as investment in

established company

4. What is your investment capability? Investment capability will determine the

approach – either pure organic or

accelerated growth via property acquisitions

and therefore the level of returns

• Level of investment will determine the

scale of company that can be invested

in and the amount of control within that

company

• Additionally will determine how much

further investment is available for sliver

equity in real estate development, and

therefore how attractive to a strategic

partner Client X will be

68

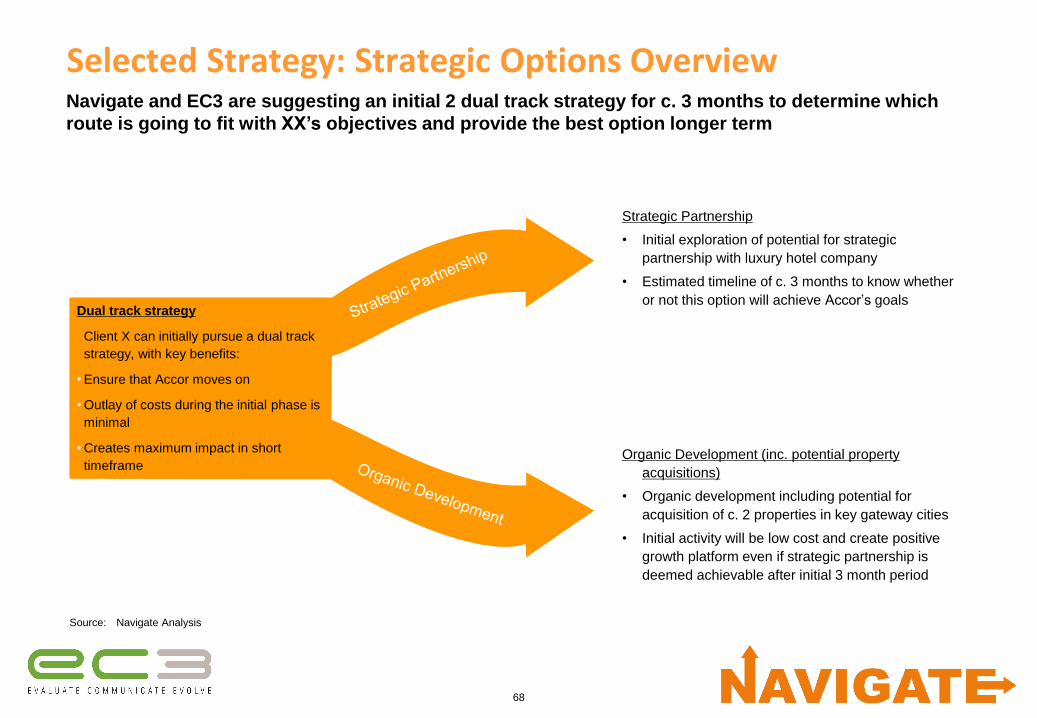

Selected Strategy: Strategic Options OverviewNavigate and EC3 are suggesting an initial 2 dual track strategy for c. 3 months to determine which

route is going to fit with XX’s objectives and provide the best option longer term

Source: Navigate Analysis

Dual track strategy

Client X can initially pursue a dual track

strategy, with key benefits:

• Ensure that Accor moves on

• Outlay of costs during the initial phase is

minimal

• Creates maximum impact in short

timeframe

Strategic Partnership

• Initial exploration of potential for strategic

partnership with luxury hotel company

• Estimated timeline of c. 3 months to know whether

or not this option will achieve Accor’s goals

Organic Development (inc. potential property

acquisitions)

• Organic development including potential for

acquisition of c. 2 properties in key gateway cities

• Initial activity will be low cost and create positive

growth platform even if strategic partnership is

deemed achievable after initial 3 month period

69

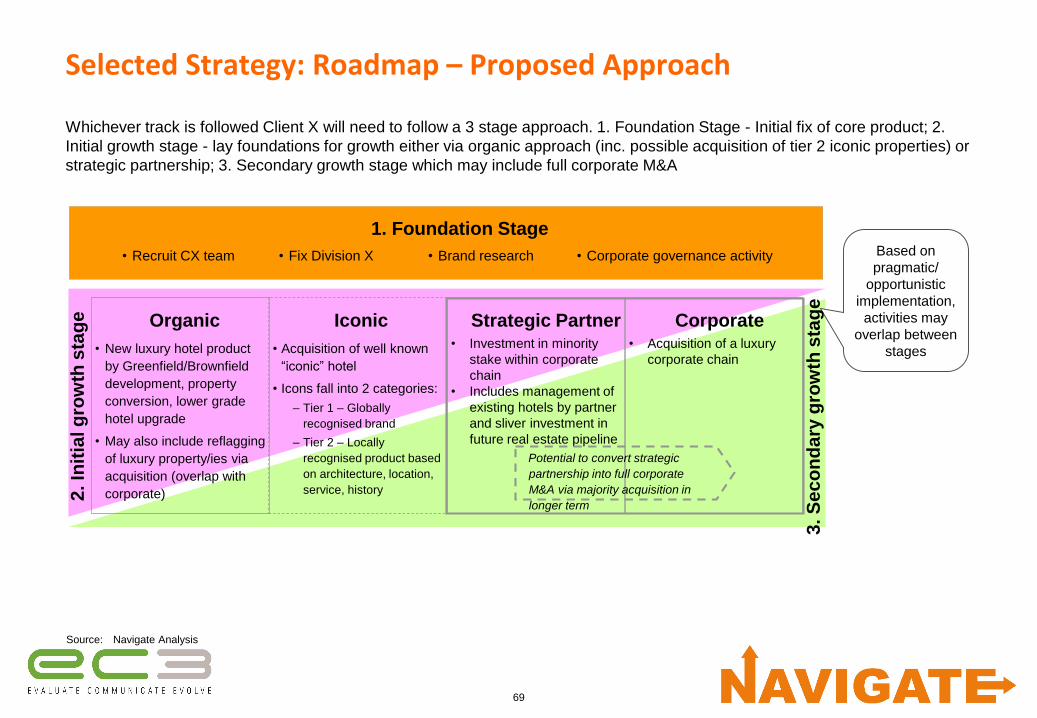

Selected Strategy: Roadmap – Proposed Approach

Whichever track is followed Client X will need to follow a 3 stage approach. 1. Foundation Stage - Initial fix of core product; 2.

Initial growth stage - lay foundations for growth either via organic approach (inc. possible acquisition of tier 2 iconic properties) or

strategic partnership; 3. Secondary growth stage which may include full corporate M&A

Organic Iconic Corporate

1. Foundation Stage

• Recruit CX team • Fix Division X • Brand research • Corporate governance activity Based on

pragmatic/

opportunistic

implementation,

activities may

overlap between

stages

2. In

itia

l g

row

th s

tag

e

3. S

ec

on

da

ry g

row

th s

tag

e

Source: Navigate Analysis

• New luxury hotel product

by Greenfield/Brownfield

development, property

conversion, lower grade

hotel upgrade

• May also include reflagging

of luxury property/ies via

acquisition (overlap with

corporate)

• Acquisition of well known

“iconic” hotel

• Icons fall into 2 categories:

– Tier 1 – Globally

recognised brand

– Tier 2 – Locally

recognised product based

on architecture, location,

service, history

• Acquisition of a luxury

corporate chain

• Investment in minority

stake within corporate

chain

• Includes management of

existing hotels by partner

and sliver investment in

future real estate pipeline

Strategic Partner

Potential to convert strategic

partnership into full corporate

M&A via majority acquisition in

longer term

70

Agenda

1. Approach

2. Industry overview

3. Sector analysis

4. Strategic options

5. Selected strategy

• Foundation stage

• Growth stage

• Financial implications

6. Next steps

71

Agenda

1. Approach

2. Industry overview

3. Sector analysis

4. Strategic options

5. Selected strategy

• Foundation stage

• Growth stage

• Financial implications

6. Next steps

72

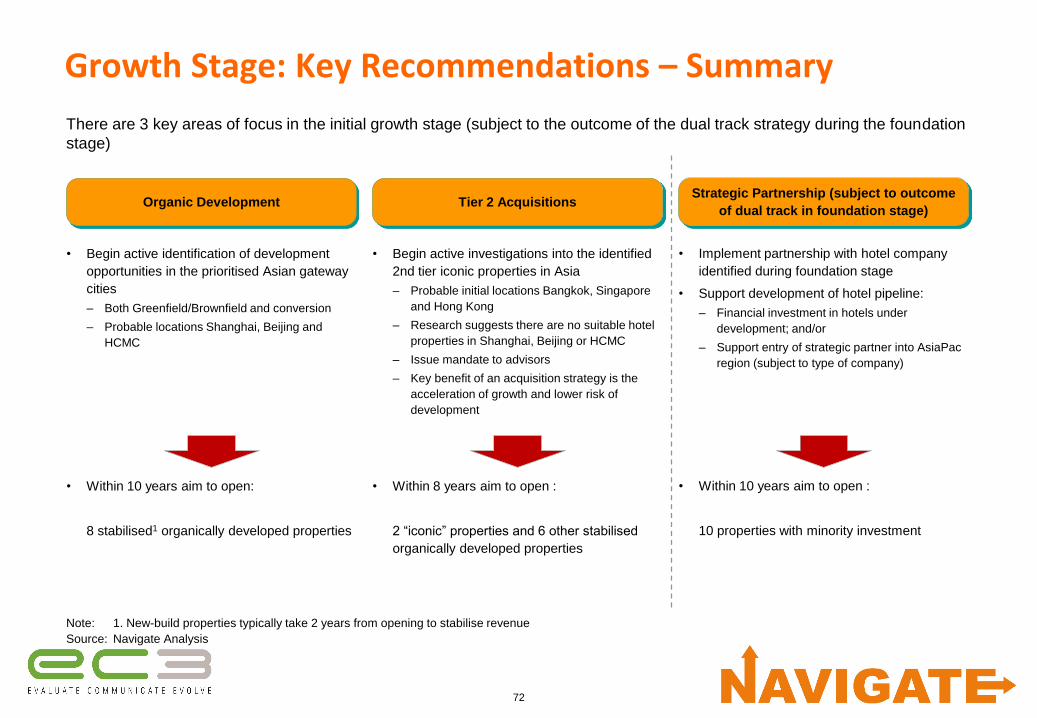

Growth Stage: Key Recommendations – Summary

There are 3 key areas of focus in the initial growth stage (subject to the outcome of the dual track strategy during the foundation

stage)

Organic Development Tier 2 Acquisitions

Note: 1. New-build properties typically take 2 years from opening to stabilise revenue

Source: Navigate Analysis

Strategic Partnership (subject to outcome

of dual track in foundation stage)

• Begin active investigations into the identified

2nd tier iconic properties in Asia