2012 SMID-West Conference Book

28

12.12.12

-

Upload

brad-van-houte -

Category

Documents

-

view

293 -

download

0

Transcript of 2012 SMID-West Conference Book

12.12.12

CONFERENCE HOTEL MAP

7th Floor - Meeting Rooms 5th Floor - Lunch (Price Room)

Registration & Breakfast

Elevators to Lunch

SCAN with your smartphone to view

digital conference book.Also available at

lambert-edwards.com/smidwest

Room Company Room Company Room CompanyClark 1 Agnico -‐ Eagle Mines Ltd. Montrose 1 Mercantile Bank Corporation Sandburg 2 Spartan Motors, Inc.Clark 2 CTS Corporation Montrose 2 Orion Energy Systems, Inc. Sandburg 3 Summit Hotel Properties, Inc.Clark 3 Delta Apparel, Inc. Montrose 3 Perceptron, Inc. Sandburg 4 Telular CorporationClark 5 Duluth Metals Limited Montrose 4 R.G. Barry Corporation Sandburg 5 Thomas Properties Group, Inc.Clark 7 Harte -‐ Hanks, Inc. Montrose 5 Schawk, Inc. Sandburg 6 Titan International Inc.Clark 8 Kratos Defense & Security Solutions, Inc. Sandburg 7 XPO Logistics, Inc.Clark 9 Local Corporation

2012 SMID-West Investor Conference, Chicago

December 12, 2012 Welcome to the 8th Annual Lambert, Edwards & Associates SMID-West Investor Conference. We have designed this conference to introduce buyside and sellside analysts from the Midwest and beyond to the management teams of top-performing small- and mid-cap (SMID) companies. As one of the nation’s leading investor relations firms, and a specialist in the small- and mid-cap market, Lambert, Edwards & Associates (LE&A) understands the importance of building strong relationships among investment professionals and the companies they watch. To this end, we have designed this year’s conference to maximize time spent with management to further cement these relationships and provide additional insight into each company’s story. LE&A is hosting this event thanks in part to the generous support of our sponsors, including Q4 Web Systems, PR Newswire and Roadcast®. Thank you again for participating in the 2012 SMID-West Investor Conference. Should you have any questions, please look for one of us at the conference or contact any of our firm’s associates. Sincerely,

Jeff Lambert Bob Burton President & Managing Partner Managing Director, Financial Communications Lambert, Edwards & Associates Lambert, Edwards & Associates c. 616-540-8461 c. 678-576-2991 [email protected] [email protected]

www.q4websystems.com

IR WEBSITE

TEMPLATES

FOLLOW US

Q4 is the anti-template solution for your IR website - tell your investment story with no template restrictions. Q4 supports any design or interactivity and comes with all your press releases, alerts, stock quotes, charts and financial data built right in. Combined with Q4’s social media, financial and mobile app distribution, Q4 gets you in front of investors, wherever they are on the web today.

For more info visit us at www.q4websystems.com

[email protected] 1-877-426-7829 ext. 225

Tell Your Story With No Restrictions

Hundreds of companies use Q4 Web Systems for their IR Websites, Social Media and Mobile Apps

2012 SMID-West Investor Conference, Chicago

TABLE OF CONTENTS

Sponsors ...................................................................................................................... 1

SMID-West Conference Agenda .................................................................................. 2

Attending Companies .....................................................................................................

Agnico - Eagle Mines Ltd. (NYSE:AEM) ...................................................................... 3

CTS Corporation (NYSE:CTS) ..................................................................................... 4

Delta Apparel, Inc. (NYSEMKT:DLA) ........................................................................... 5

Duluth Metals Limited (TSE:DM) .................................................................................. 6

Harte - Hanks, Inc. (NYSE:HHS) ................................................................................. 7

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) ....................................... 8

Local Corporation (NASDAQ:LOCM) ........................................................................... 9

Mercantile Bank Corporation (NASDAQ:MBWM) ....................................................... 10

Orion Energy Systems, Inc. (NYSEMKT:OESX) ........................................................ 11

Perceptron, Inc. (NASDAQ:PRCP) ............................................................................ 12

R.G. Barry Corporation (NASDAQ:DFZ) .................................................................... 13

Schawk, Inc. (NYSE:SGK) ......................................................................................... 14

Spartan Motors, Inc. (NASDAQ:SPAR) ...................................................................... 15

Summit Hotel Properties, Inc. (NYSE:INN) ................................................................ 16

Telular Corporation (NASDAQ:WRLS) ....................................................................... 17

Thomas Properties Group, Inc. (NASDAQ:TPGI) ....................................................... 18

Titan International Inc. (NYSE:TWI) ........................................................................... 19

XPO Logistics, Inc. (NYSE:XPO) ............................................................................... 20

About Lambert, Edwards & Associates ..................................................................... 21

2012 SMID-West Investor Conference, Chicago

THANK YOU TO OUR SPONSORS

Q4 Web Systems (Q4) is the leader in corporate websites and social media solutions for public companies. Hundreds of investor relations’ professionals rely on Q4 for their IR website, social media and mobile applications. Using Q4, public companies of all sizes increase awareness, reduce risk and build better relationships with their investors. Through active best practice research, Q4 has earned a position at the forefront of the investor relations market, sharing knowledge through webinars, white papers and articles on http://www.q4blog.com.

PR Newswire (www.prnewswire.com) is the premier global provider of multimedia platforms that enable marketers, corporate communicators, sustainability officers, public affairs and investor relations officers to leverage content to engage with all their key audiences. Having pioneered the commercial news distribution industry 58 years ago, PR Newswire today provides end-to-end solutions to produce, optimize and target content — from rich media to online video to multimedia — and then distribute content and measure results across traditional, digital, mobile and social channels. Combining the world's largest multi-channel, multi-cultural content distribution and optimization network with comprehensive workflow tools and platforms, PR Newswire enables the world's enterprises to engage opportunity everywhere it exists. PR Newswire serves tens of thousands of clients from offices in the Americas, Europe, Middle East, Africa and the Asia-Pacific region, and is a UBM plc company.

Roadcast® is a proprietary web-based product that enables fund managers, securities analysts and retail investors to see and hear management discuss its company’s business fundamentals in their own language. This ―virtual presentation‖ gives a qualitative insight to management and provides investors a tool to supplement their quantitative investment screening. The quality and vision of management is a key element in the investment decision. According to market studies conducted by the NYU Stern School of Business and Ernst & Young, financial analysts can explain 65% of what drives a stocks performance (i.e. tangible factors); the remaining 35% is largely dependent upon less-defined intangible factors, the most critical of which is how the Street views management, and their ability to drive shareholder value. The ability to see management’s discussion of the company’s key investment characteristics, value drivers, and strategic initiatives can have significant impact on the investment decision.

1

2012 SMID-West Investor Conference, Chicago

SMID-West 2012 Conference Agenda

7:30 – 8:20 a.m.

Welcome: Registration & Continental Breakfast

7th Floor

8:30 – 9:20 a.m.

Meeting Session 1

7th Floor

9:30 – 10:20 a.m.

Meeting Session 2

7th Floor

10:30 – 11:20 a.m.

Meeting Session 3

7th Floor

11:30 a.m. – 12:20 p.m.

Lunch

5th Floor, Price Room

12:30 – 1:20 p.m.

Meeting Session 4

7th Floor

1:30 – 2:20 p.m.

Meeting Session 5

7th Floor

2:30 – 3:20 p.m.

Meeting Session 6

7th Floor

LE&A Onsite Contact Information

Brad Van Houte 616.308.8320 [email protected] Stephanie Hwu 248.943.8214 [email protected] Mike Houston 480.270.4812 [email protected] Bob Burton 678.576.2991 [email protected] Jeff Lambert 616.540.8461 [email protected] Karen Keller 616.446.4835 [email protected]

2

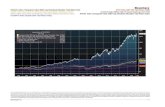

PX_TO_BOOK_RATIOPX_TO_BOOK_RATIO

AGNICO-EAGLE MINES LTD P/E P/B P/EBITDA P/S Curr Yield

#N/A 24.91 2.79 12.66 492.00 1.51

Market Cap ($MM) 9,118.3 57.35 16.74

Symbol AEM EQUITY S&P Rating NR 31.42 46.09%

Exchange New York Industry Gold Mining 171.8491M 12.43%

Beta 0.65 3.23Gross Margin 37.54 1.60

ROE (LTM) -10.49 28.73

ROA (LTM) -6.94 8.92

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 2.13 2.54 2.96

- - - - - - - 0.76 0.77 0.76

1.51 1.48 1.37 1.59 1.80 2.06 2.23 20.23 21.86 24.11

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 1,935 2,041 2,262

Operating Income 0 2 1 5 7 7 5 578 722 778

Net Income 0 1 -2 2 4 4 3 358 434 515

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

52 Week Low 2/16/2012 YTD % Change

52 Week High 11/26/2012

Price (as of 12/6/12)

53.06

YTD Change

Quick RatioCurrent Ratio

Ratios

Debt/Equity

Shares out 11/30/2012

Attending Management

SPX YTD % Chg

Agnico-Eagle is a long established, Canadian headquartered, gold producer with operations located in Canada, Finland and Mexico, and exploration and development activities in Canada,

Finland, Mexico and the United States. The Company has full exposure to higher gold prices consistent with its policy of no forward gold sales and maintains a corporate strategy based on

increasing shareholders exposure to gold, on a per share basis. It has paid a cash dividend for 30 consecutive years.

Brian Christie VP, Investor RelationsDmitry Kushnir Director, IR

Dividends

Book Value

FY

Company Description

Earnings

EBIT / Interest

$25

$35

$45

$55

0

3,000,000

6,000,000

9,000,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

3

CTS CORP P/E P/B P/EBITDA P/S Curr Yield

905 West Boulevard North Elkhart, IN 46514 United States 26.11 1.14 10.84 0.53 1.53

Market Cap ($MM) 308.8 11.22 -0.06

Symbol CTS EQUITY S&P Rating #N/A N/A 7.66 -0.65%

Exchange New York Industry Electronic Compo-Misc 33.78184M 12.43%

Beta 1.36 2.28Gross Margin 18.67 1.33

ROE (LTM) 6.16 28.26

ROA (LTM) 3.48 11.34

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 0.70 0.81 0.99

- - - - - - - - - -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 - - -

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 581 618 676

Operating Income 0 2 1 5 7 7 5 - - -

Net Income 0 1 -2 2 4 4 3 - - -

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

CTS Corporation (NYSE: CTS) was founded in 1896. CTS is an innovative designer and manufacturer of sensors, actuators, electronic components and a leading provider of value-add

electronics manufacturing services (EMS). Our sensors, actuators and electronic components serve OEMs in the automotive, communications, industrial, medical, defense and aerospace

and computer markets. Our EMS operations provide specialty solutions to customers throughout the communications, defense and aerospace, industrial and medical markets. We have

manufacturing operations located throughout North America, Asia and Europe.

Thomas Kroll Vice President & CFOMitch Walorski Director, IR

Dividends

Book Value

FY

Company Description

Debt/Equity

Earnings

EBIT / Interest

Quick RatioCurrent Ratio

Price (as of 12/6/12)

9.14

Attending ManagementRatios

YTD Change

52 Week Low 10/24/2012 YTD % Change

52 Week High 4/25/2012

Shares out 10/19/2012 SPX YTD % Chg

$6

$8

$10

$12

0

50,000

100,000

150,000

200,000

250,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

4

DELTA APPAREL INC P/E P/B P/EBITDA P/S Curr Yield

322 S Main Street Greenville, SC 29601 United States 7.96 0.83 187.23 0.24 -

Market Cap ($MM) 117.9 19.74 -4.92

Symbol DLA EQUITY S&P Rating #N/A N/A 12.65 -25.77%

Exchange NYSE MKT LLC Industry Apparel Manufacturers 8.31935M 12.43%

Beta 0.85 3.81Gross Margin 17.09 1.11

ROE (LTM) -2.29 79.84

ROA (LTM) -1.03 -1.51

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 1.78 2.10 -

- - - - - - - - - -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 - - -

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 509 534 -

Operating Income 0 2 1 5 7 7 5 - - -

Net Income 0 1 -2 2 4 4 3 15 20 -

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Delta Apparel, Inc., along with its operating subsidiaries, M. J. Soffe, LLC, Junkfood Clothing Company, To The Game, LLC and Art Gun, LLC, is an international design, marketing,

manufacturing, and sourcing company that features a diverse portfolio of lifestyle branded activewear apparel and headwear, and produces high quality private label programs. The

Company specializes in selling casual and athletic products across distribution tiers and in most store types, including specialty stores, boutiques, department stores, mid-tier and mass

chains. From a niche distribution standpoint, the Company also has strong distribution at college bookstores and the U.S. military. The Company’s products are made available direct-to-

consumer on its websites at www.soffe.com, www.junkfoodclothing.com, www.saltlife.com and www.deltaapparel.com. Additional products can be viewed at www.2thegame.com and

www.thecottonexchange.com. The Company's operations are located throughout the United States, Honduras, El Salvador, and Mexico, and it employs approximately 7,200 people

worldwide. Additional information about the Company is available at www.deltaapparelinc.com.

Robert Humphreys Chairman & CEO

Dividends

Book Value

FY

Company Description

Debt/Equity

Earnings

EBIT / Interest

Quick RatioCurrent Ratio

Price (as of 12/6/12)

14.17

Attending ManagementRatios

YTD Change

52 Week Low 8/1/2012 YTD % Change

52 Week High 12/23/2011

Shares out 9/29/2012 SPX YTD % Chg

$12

$14

$16

$18

$20

0

50,000

100,000

150,000

200,000

250,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

5

DULUTH METALS LTD P/E P/B P/EBITDA P/S Curr Yield

80 Richmond Street West Suite 1500 Toronto, ON M5H 2A4 - 2.19 - - -

Market Cap ($MM) 317.4 2.74 0.44

Symbol DM CN EQUITY S&P Rating #N/A N/A 1.40 21.05%

Exchange Toronto Industry Metal-Diversified 125.4366M 1.64%

Beta 0.79 19.88Gross Margin #N/A N/A 19.57

ROE (LTM) -20.43 0.22

ROA (LTM) -16.30 #N/A N/A

Per Share Overview (CAD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 (0.27) (0.11) (0.09)

- - - - - - - - - -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 1.13 1.15 1.09

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 - - -

Operating Income 0 2 1 5 7 7 5 -13 -12 -12

Net Income 0 1 -2 2 4 4 3 -35 -20 -20

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Duluth Metals Limited (TSX:DM, DM.U in $US) is a Canadian company focused on developing a proposed underground mining development project in a joint venture which is 60% owned by Duluth and 40%

by Antofagasta known as the Twin Metals Minnesota Project. The project is located within the rapidly emerging Duluth Complex mining camp in northeastern Minnesota, U.S.A. The Twin Metals Minnesota

Project is amongst the world's largest Cu-Ni-PGM polymetallic sulphide deposits with contained metals (using a 0.3% Cu cut-off) of Indicated 8.0 Billion lbs copper, 2.5 Billion lbs nickel, and 12.1 Million ozs

palladium+platinum+gold (TPM) and Inferred 13.5 Billion lbs copper, 4.6 Billion lbs nickel, and 15.8 Million ozs TPM. In addition, Duluth Metals is currently drilling on approximately 40,000 acres of 100%

owned mineral interests on exploration properties adjacent to and nearby the joint venture. The primary exploration focus is for copper-nickel-PGM mineralization, similar to other known deposits in the

Duluth Complex. The exploration properties are situated at the junction of the Nickel Lake Macrodike and the South Kawishiwi Intrusion and represent a prime target area for Duluth Metals. Geological

modeling indicates that the property has the potential to host a "Voisey's Bay" type massive sulfide target.

Christopher Dundas Chairman & CEOMara Strazdins VP of IR & Corp. Comms

Dividends

Book Value

FY

Company Description

Earnings

EBIT / Interest

Quick RatioCurrent Ratio

Ratios

Debt/Equity

Shares out 11/30/2012 SPTSX YTD % Chg

52 Week High 12/4/2012

Price (as of 12/6/12)

2.53

Attending Management

YTD Change

52 Week Low 7/3/2012 YTD % Change

$1

$2

$3

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

6

HARTE-HANKS INC P/E P/B P/EBITDA P/S Curr Yield

9601 MC Allister Freeway Suite 610 San Antonio, TX 78216 9.14 1.00 3.88 0.42 6.31

Market Cap ($MM) 338.3 10.24 -3.70

Symbol HHS EQUITY S&P Rating #N/A N/A 5.18 -40.70%

Exchange New York Industry Direct Marketing 62.77306M 12.43%

Beta 0.98 1.34Gross Margin 61.64 1.19

ROE (LTM) -20.15 24.70

ROA (LTM) -9.94 23.29

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 0.58 0.59 0.58

- - - - - - - 0.34 0.34 0.34

1.51 1.48 1.37 1.59 1.80 2.06 2.23 - - -

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 800 776 732

Operating Income 0 2 1 5 7 7 5 - - -

Net Income 0 1 -2 2 4 4 3 36 37 36

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Price (as of 12/6/12)

5.39

Attending Management

YTD Change

52 Week Low 12/4/2012 YTD % Change

Debt/Equity

Shares out 10/15/2012 SPX YTD % Chg

52 Week High 1/31/2012

EBIT / Interest

Quick RatioCurrent Ratio

Ratios

Harte-Hanks® is a worldwide direct and targeted marketing company that provides multichannel direct and digital marketing services and shopper advertising opportunities to a wide range of local, regional,

national and international consumer and business-to-business marketers. Harte-Hanks Direct Marketing helps its clients obtain insight about their customers through database and marketing analytics. Based

on that insight Harte-Hanks Direct Marketing designs, implements and executes multichannel marketing programs on behalf of its clients using direct and digital communications. Harte-Hanks Shoppers is

North America's largest owner, operator, and distributor of shopper products which bring buyers and sellers together at a local level through its proven multichannel offerings, including targeted print, digital

advertising, and classifieds. Its print publications are zoned into more than 950 separate editions and reach 11.2 million addresses each week in California and Florida. Shoppers also provide advertisers with

PowerSites™ to help small- and medium-size businesses establish a web presence and improve lead generation, PowerClick™ SEM services, and mobile distribution of their ads and coupons. For consumers,

PennySaverUSA.com™ and TheFlyer.com™ offer local online and mobile classifieds for garage sales, pets, used and new cars, real estate, as well as thousands of coupons and business listings.

Doug Shepard EVP & CFO

Dividends

Book Value

FY

Company Description

Earnings

$4

$6

$8

$10

$12

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

7

KRATOS DEFENSE & SECURITY P/E P/B P/EBITDA P/S Curr Yield

4810 Eastgate Mall San Diego, CA 92121 United States 9.55 0.61 1.82 0.19 -

Market Cap ($MM) 250.2 7.79 -1.55

Symbol KTOS EQUITY S&P Rating B 4.14 -25.96%

Exchange NASDAQ GS Industry Aerospace/Defense 56.604M 12.43%

Beta 1.49 1.97Gross Margin 26.58 1.50

ROE (LTM) -8.87 202.02

ROA (LTM) -2.52 0.80

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 0.46 0.41 0.75

- - - - - - - - - -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 6.40 6.95 6.88

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 971 1,019 1,058

Operating Income 0 2 1 5 7 7 5 45 64 79

Net Income 0 1 -2 2 4 4 3 -25 2 8

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Price (as of 12/6/12)

4.42

Attending Management

YTD Change

52 Week Low 11/16/2012 YTD % Change

Debt/Equity

Shares out 11/2/2012 SPX YTD % Chg

52 Week High 2/6/2012

EBIT / Interest

Quick RatioCurrent Ratio

Ratios

Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a specialized National Security technology business providing mission critical products, services and solutions for United States

National Security. Kratos’ core capabilities are sophisticated engineering, manufacturing and system integration offerings for National Security platforms and programs. Kratos’ areas of

expertise include Command, Control, Communications, Computing, Combat Systems, Intelligence, Surveillance and Reconnaissance (C5ISR), satellite communication systems, unmanned

systems, cyber warfare, cyber security, information assurance, and critical infrastructure security. Kratos has primarily an engineering and technically oriented work force of approximately

4,400. The vast majority of Kratos’ work is performed on a military base, in a secure facility or at a critical infrastructure location. Kratos’ primary end customers are National Security

related agencies.

Eric DeMarco President & CEODeanna Lund EVP & CFO

Dividends

Book Value

FY

Company Description

Earnings

$2

$3

$4

$5

$6

$7

$8

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

8

LOCAL CORP P/E P/B P/EBITDA P/S Curr Yield

7555 Irvine Center Drive Irvine, CA 92618 United States - 1.43 - 0.50 -

Market Cap ($MM) 50.9 3.21 0.18

Symbol LOCM EQUITY S&P Rating #N/A N/A 1.42 8.49%

Exchange NASDAQ CM Industry E-Marketing/Info 22.11822M 12.43%

Beta 1.17 0.97Gross Margin 37.38 0.94

ROE (LTM) -45.79 0.00

ROA (LTM) -29.80 -35.54

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 0.01 0.20 -

- - - - - - - - - -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 - - -

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 100 114 135

Operating Income 0 2 1 5 7 7 5 - - -

Net Income 0 1 -2 2 4 4 3 1 3 -

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Local Corporation (NASDAQ:LOCM) is a leading national online media company that connects merchants and consumers. Using our powerful technology platforms, we provide a host of

innovative business solutions including digital marketing products and tools such as local business and product search, mobile, SEO, web hosting, social media and daily deals—all to help

merchants grow their business. Our media services enable our partners to create rich media and other display ads that reach their target audiences with unparalleled effectiveness. Plus,

our consumer properties, including the flagship Local.com website, Spreebird.com and a network of over 1,000 regional media sites, help more than a million consumers find the products

and services they need every single a day.

Ken Cragun CFOJanine Zanelli Sr. Director, IR

Dividends

Book Value

FY

Company Description

Earnings

EBIT / Interest

Quick RatioCurrent Ratio

Ratios

Debt/Equity

Shares out 10/31/2012

Attending Management

SPX YTD % Chg

52 Week High 2/9/2012

Price (as of 12/6/12)

2.30

YTD Change

52 Week Low 9/11/2012 YTD % Change

$1

$2

$3

$4

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

9

MERCANTILE BANK CORP P/E P/B P/EBITDA P/S Curr Yield

310 Leonard Street NW Grand Rapids, MI 49504 United States 3.40 0.88 - 1.81 2.45

Market Cap ($MM) 126.7 18.69 4.92

Symbol MBWM EQUITY S&P Rating #N/A N/A 9.25 50.46%

Exchange NASDAQ GS Industry Commer Banks-Central US 8.63859M 12.43%

Beta 0.75 #N/A N/AGross Margin #N/A N/A #N/A N/A

ROE (LTM) 29.51 53.91

ROA (LTM) 2.78 #N/A N/A

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 1.28 1.36 1.40

- - - - - - - 0.06 0.35 0.24

1.51 1.48 1.37 1.59 1.80 2.06 2.23 16.98 17.85 -

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 55 55 56

Operating Income 0 2 1 5 7 7 5 - - -

Net Income 0 1 -2 2 4 4 3 9 11 10

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Mercantile Bank Corporation is the bank holding company for Mercantile Bank of Michigan. Founded in 1997 to provide banking services to businesses, individuals and governmental units,

the Bank differentiates itself on the basis of service quality and the expertise of its banking staff. Mercantile has seven full-service banking offices in Grand Rapids, Holland and Lansing,

Michigan. Mercantile Bank Corporation’s common stock is listed on the NASDAQ Global Select Market under the symbol “MBWM.”

Michael Price President & CEOCharles Christmas Senior VP, CFO & Treasurer

Dividends

Book Value

FY

Company Description

Debt/Equity

Earnings

EBIT / Interest

Quick RatioCurrent Ratio

Price (as of 12/6/12)

14.67

Attending ManagementRatios

YTD Change

52 Week Low 12/7/2011 YTD % Change

52 Week High 7/17/2012

Shares out 11/8/2012 SPX YTD % Chg

$8

$10

$12

$14

$16

$18

$20

-100,000

100,000

300,000

500,000

700,000

900,000

1,100,000

1,300,000

1,500,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

10

ORION ENERGY SYSTEMS INC P/E P/B P/EBITDA P/S Curr Yield

2210 Woodland Drive Manitowoc, WI 54220 United States - 0.38 - 0.34 -

Market Cap ($MM) 25.6 3.46 -1.68

Symbol OESX EQUITY S&P Rating #N/A N/A 1.15 -56.95%

Exchange NYSE MKT LLC Industry Lighting Products&Sys 20.13562M 12.43%

Beta 0.73 2.96Gross Margin 29.87 1.90

ROE (LTM) -13.81 7.23

ROA (LTM) -9.99 0.95

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 (0.03) 0.05 -

- - - - - - - - - -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 - - -

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 99 117 -

Operating Income 0 2 1 5 7 7 5 -6 6 -

Net Income 0 1 -2 2 4 4 3 -6 2 -

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Price (as of 12/6/12)

1.27

Attending ManagementRatios

YTD Change

52 Week Low 11/16/2012 YTD % Change

52 Week High 2/1/2012

Shares out 11/7/2012 SPX YTD % Chg

EBIT / Interest

Quick RatioCurrent Ratio

Orion is a leading power technology enterprise that designs, manufactures and deploys energy management systems – consisting primarily of high-performance, energy efficient interior

and exterior lighting platforms, intelligent wireless control systems and direct renewable solar technology for commercial and industrial customers – without compromising their quantity

or quality of light. An industry leader since 2001, Orion has retrofitted over 1.2 billion square feet of their customers’, including 144 of the Fortune 500. They have completed over 8,200

projects which have saved their customers approximately $1.6 billion in energy costs, reducing energy demand by over 700 MW since 2001. Orion’s energy management systems provide a

unique and comprehensive solution to reduce customers’ lighting–related electricity costs, while also permanently reducing base and peak load electricity demand from utilities.

John Scribante CEOScott Jensen CFO

Dividends

Book Value

FY

Company Description

Debt/Equity

Earnings

$1

$2

$3

$4

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

11

PERCEPTRON INC P/E P/B P/EBITDA P/S Curr Yield

47827 Halyard Drive Plymouth, MI 48170-2461 United States 12.41 0.94 6.47 0.77 -

Market Cap ($MM) 48.5 6.32 1.15

Symbol PRCP EQUITY S&P Rating #N/A N/A 4.08 25.12%

Exchange NASDAQ GM Industry Commercial Services 8.50058M 12.43%

Beta 0.47 3.47Gross Margin 42.12 2.69

ROE (LTM) 4.94 0.00

ROA (LTM) 3.85 #N/A N/A

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 0.38 0.44 0.45

- - - - - - - - - -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 - - -

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 - - -

Operating Income 0 2 1 5 7 7 5 - - -

Net Income 0 1 -2 2 4 4 3 - - -

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Price (as of 12/6/12)

5.71

Attending ManagementRatios

YTD Change

52 Week Low 1/12/2012 YTD % Change

52 Week High 2/9/2012

Shares out 11/7/2012 SPX YTD % Chg

EBIT / Interest

Quick RatioCurrent Ratio

Perceptron develops, produces, and sells non-contact measurement and inspection solutions for industrial applications. The Company’s products provide solutions for manufacturing

process control as well as sensor and software technologies for non-contact measurement, scanning, and inspection applications. Automotive and manufacturing companies throughout

the world rely on Perceptron’s metrology solutions to help them manage their complex manufacturing processes to improve quality, shorten product launch times and reduce overall

manufacturing costs. The Company also offers Value Added Services such as training and customer support services. Headquartered in Plymouth, Michigan, Perceptron has approximately

220 employees worldwide, with operations in the United States, Germany, France, Spain, Brazil, Japan, Singapore, China and India. For more information, please visit

www.perceptron.com.

Jack Lowry VP & CFO

Dividends

Book Value

FY

Company Description

Debt/Equity

Earnings

$3

$4

$5

$6

$7

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

12

BARRY (R.G.) P/E P/B P/EBITDA P/S Curr Yield

#N/A Requesting Data... Pickerington, OH 43147 United States 12.07 2.06 6.60 1.07 2.47

Market Cap ($MM) 164.5 15.62 2.52

Symbol DFZ EQUITY S&P Rating #N/A N/A 11.23 20.86%

Exchange NASDAQ GM Industry Footwear&Related Apparel 11.26468M 12.43%

Beta 1.04 3.48Gross Margin 43.07 2.41

ROE (LTM) 18.59 27.36

ROA (LTM) 10.65 26.12

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 1.29 1.56 -

- - - - - - - - - -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 - - -

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 - - -

Operating Income 0 2 1 5 7 7 5 - - -

Net Income 0 1 -2 2 4 4 3 - - -

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Price (as of 12/6/12)

14.60

Attending Management

YTD Change

52 Week Low 4/4/2012 YTD % Change

Debt/Equity

Shares out 11/7/2012 SPX YTD % Chg

52 Week High 10/31/2012

EBIT / Interest

Quick RatioCurrent Ratio

Ratios

RG Barry Brands develop and market great accessories brands and fashionable, solution-oriented products that make life better. Our brands are sold by retailers everywhere under a growing family of

proprietary labels, including: Dearfoams®, the world’s best-known slipper brand; Foot Petals®, solution-orientated foot care and shoe care products; and baggallini® fashionable and functional handbags,

totes and travel accessories. We also supply exclusive private label products to some of the world’s finest retailers. Based upon more than 65 years of excellence in designing, sourcing and marketing

accessories products, RG Barry Brands has a reputation as an industry leader. We own approximately 30% of the North American slipper market and manage the replenishment slipper businesses for key

retailers. Our handbag and comfort insert businesses have legacies of consistent double digit growth and strong profitability. Our strengths translate into consistent top-quartile corporate performance

demonstrated as products and services that meet or beat sales and profit objectives for retailing partners; superior quality, value and function in great solution-oriented products for consumers; an exciting,

enjoyable and rewarding place for our Team Members to work; and increasing returns in the form of growing equity and cash dividends for our shareholders. For its fiscal year ended June 30, 2012, the

Company reported net earnings of $14.5 million, or $1.27 per diluted share, up 93.7% when compared to one year earlier; and a year-over-year net sales increase of 20% to $155.9 million. Additionally, cash

and short-term investments were 69.1% higher than one year prior at $41.7 million; consolidated inventory was at $21.1 million, down from $25.5 million at the end of fiscal 2011; net shareholders’ equity

rose to $74.4 million from $62.5 million one year prior; and long-term debt totaled $20.4 million, down from $24.6 million at fiscal year-end 2011. Our growth strategy is built upon the premise of investing

in and intelligently growing our existing business units both domestically and internationally, while seeking out and executing category appropriate acquisitions that meet our strict acquisition criteria. RG

Barry Brands is based in the Columbus, Ohio suburb of Pickerington. The Company has been publicly traded since 1962, and its shares are principally traded on the NASDAQ Global Market under the trading

symbol DFZ.

Jose Ibarra CFO & Sr. VP FinanceRoy Youst Director, IR

Dividends

Book Value

FY

Company Description

Earnings

$10

$12

$14

$16

$18

$20

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

13

SCHAWK INC P/E P/B P/EBITDA P/S Curr Yield

1695 South River Road Des Plaines, IL 60018 United States 25.65 1.22 8.70 0.70 2.55

Market Cap ($MM) 327.6 14.60 1.36

Symbol SGK EQUITY S&P Rating #N/A N/A 10.51 12.13%

Exchange New York Industry Data Processing/Mgmt 26.06334M 12.43%

Beta 1.74 1.53Gross Margin 35.80 1.09

ROE (LTM) 0.17 26.92

ROA (LTM) 0.10 7.64

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 0.51 0.79 1.41

- - - - - - - - - -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 - - -

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 459 483 505

Operating Income 0 2 1 5 7 7 5 - - -

Net Income 0 1 -2 2 4 4 3 - - -

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Price (as of 12/6/12)

12.57

Attending Management

YTD Change

52 Week Low 3/7/2012 YTD % Change

Debt/Equity

Shares out 10/24/2012 SPX YTD % Chg

52 Week High 10/2/2012

EBIT / Interest

Quick RatioCurrent Ratio

Ratios

Schawk, Inc. is a leading provider of brand development and deployment services, enabling companies of all sizes to connect their brands with consumers. With a global footprint of

operations in 26 countries, Schawk helps companies create compelling and consistent brand experiences by providing integrated strategic, creative and executional services across brand

touchpoints. Founded in 1953, Schawk is trusted by many of the world’s leading organizations to help them achieve global brand consistency.

Tim Cunningham EVP & CFOTim Allen Corporate VP, IR

Dividends

Book Value

FY

Company Description

Earnings

$10

$11

$12

$13

$14

$15

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

14

SPARTAN MOTORS INC P/E P/B P/EBITDA P/S Curr Yield

1541 Reynolds Road Charlotte, MI 48813 United States 29.94 0.89 8.76 0.35 2.09

Market Cap ($MM) 162.0 6.67 -0.02

Symbol SPAR EQUITY S&P Rating #N/A N/A 4.01 -0.42%

Exchange NASDAQ GS Industry Auto/Trk Prts&Equip-Orig 33.82672M 12.43%

Beta 1.24 2.96Gross Margin 14.64 1.42

ROE (LTM) 0.38 2.78

ROA (LTM) 0.28 12.69

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 0.17 0.26 0.43

- - - - - - - 0.10 0.10 -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 5.20 5.20 -

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 459 481 528

Operating Income 0 2 1 5 7 7 5 5 12 22

Net Income 0 1 -2 2 4 4 3 5 8 13

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Price (as of 12/6/12)

4.79

Attending Management

YTD Change

52 Week Low 5/23/2012 YTD % Change

Debt/Equity

Shares out 10/31/2012 SPX YTD % Chg

52 Week High 2/3/2012

EBIT / Interest

Quick RatioCurrent Ratio

Ratios

Spartan Motors (Nasdaq: SPAR) designs, engineers and manufactures specialty chassis, specialty vehicles, truck bodies and after-market parts for the outdoor recreation, emergency response, defense,

delivery and service and specialty markets. The Company employs a Customer-Centric methodology that fosters innovation, speed and agility. As a result, Spartan Motors, Inc. (Spartan Motors) products and

vehicles set the bar for excellence in every market it serves. Spartan Motors is the parent company serving multiple markets with three brands known for performance and being first to market with

innovative products. Spartan Chassis- A leader in the design and production of custom chassis for motorhomes, emergency response, defense and specialty vehicles, consistently superior performance,

exceptional safety ratings and technological innovations distinguish it in the industry. Spartan ERV- Designs and builds custom and commercial ER apparatus to offer first responders the industry’s broadest

line of pumpers, aerials, heavy-duty tankers, quick attack (urban interface / wildland) and light-duty rescue vehicles for service in urban, suburban or rural environments. Utilimaster- A leading manufacturer

of walk-in vans and commercial truck bodies offering customized delivery solutions for a broad range of industries including baking, linen, parcel delivery, snack food, uniform and utility customers.

Joe Nowicki CFOGreg Salchow Director, IR & Treasury

Dividends

Book Value

FY

Company Description

Earnings

$3

$4

$5

$6

$7

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

15

SUMMIT HOTEL PROPERTIES INC P/E P/B P/EBITDA P/S Curr Yield

2701 South Minnesota Avenue Suite 6 Sioux Falls, SD 57105 - 1.06 6.21 1.48 5.14

Market Cap ($MM) 492.3 10.16 -0.69

Symbol INN EQUITY S&P Rating #N/A N/A 7.40 -7.31%

Exchange New York Industry REITS-Hotels 46.15965M 12.43%

Beta 1.21 #N/A N/AGross Margin #N/A N/A #N/A N/A

ROE (LTM) -2.19 78.05

ROA (LTM) -0.26 -0.69

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 (0.20) 0.19 0.36

- - - - - - - 0.45 0.47 0.57

1.51 1.48 1.37 1.59 1.80 2.06 2.23 6.79 6.39 6.13

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 187 241 268

Operating Income 0 2 1 5 7 7 5 - - -

Net Income 0 1 -2 2 4 4 3 -7 10 21

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Price (as of 12/6/12)

8.75

Attending Management

YTD Change

52 Week Low 3/16/2012 YTD % Change

Debt/Equity

Shares out 11/1/2012 SPX YTD % Chg

52 Week High 2/24/2012

EBIT / Interest

Quick RatioCurrent Ratio

Ratios

Summit Hotel Properties, Inc. is a self-managed hotel investment company organized to continue and expand the existing hotel investment business of the company's predecessor, Summit Hotel Properties,

LLC., a leading U.S. hotel owner. The company focuses primarily on acquiring and owning premium-branded, select-service hotels in the upscale and upper midscale segments of the U.S. lodging industry. The

company's current portfolio consists of 73 hotels with a total of 7,533 guestrooms located in 20 states. The hotels are located in markets in which the company has extensive experience and that exhibit

multiple demand generators, such as business and corporate headquarters, retail centers, airports and tourist attractions. Based on total number of rooms, approximately 57% of the portfolio is positioned in

the top 50 metropolitan statistical areas, or MSAs, and approximately 78% is located within the top 100 MSAs. Nearly 90% of the hotels operate under premium franchise brands owned by Marriott

International, Inc. (Courtyard by Marriott, Residence Inn by Marriott, SpringHill Suites by Marriott, Fairfield Inn by Marriott and TownePlace Suites by Marriott), Hilton Worldwide (DoubleTree, Hampton Inn,

Hampton Inn & Suites and Hilton Garden Inn), IHG (Holiday Inn Express and Staybridge Suites) and an affiliate of Hyatt Hotels Corporation (Hyatt Place).

Dan Hansen President & CEOStuart Becker EVP & CFO

Dan Boyum

Dividends

Book Value

FY

Company Description

VP, IR

Earnings

$6

$8

$10

$12

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

16

TELULAR CORP P/E P/B P/EBITDA P/S Curr Yield

311 South Wacker Drive Suite 4300 Chicago, IL 60606 29.47 2.36 9.95 2.04 4.79

Market Cap ($MM) 167.1 11.36 2.52

Symbol WRLS EQUITY S&P Rating #N/A N/A 7.05 33.60%

Exchange NASDAQ GM Industry Wireless Equipment 16.67982M 12.43%

Beta 0.59 1.96Gross Margin 53.34 1.44

ROE (LTM) 8.97 0.00

ROA (LTM) 6.50 #N/A N/A

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 0.48 0.60 -

- - - - - - - - - -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 - - -

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 97 110 -

Operating Income 0 2 1 5 7 7 5 - - -

Net Income 0 1 -2 2 4 4 3 8 11 -

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Price (as of 12/6/12)

10.02

Attending Management

YTD Change

52 Week Low 5/24/2012 YTD % Change

Debt/Equity

Shares out 7/27/2012 SPX YTD % Chg

52 Week High 11/13/2012

EBIT / Interest

Quick RatioCurrent Ratio

Ratios

Telular Corporation (NASDAQ: WRLS) provides remote monitoring and asset tracking solutions for business and residential customers, enabling security systems and industrial applications

to exchange actionable information wirelessly, typically through cellular and satellite technology. With over 25 years of experience in the wireless industry, Telular Corporation has

developed solutions to deliver remote access for voice and data without significant network investment. Headquartered in Chicago, Telular Corporation has additional offices in Atlanta,

Washington, D.C., and Miami. For more information, please visit www.telular.com.

Jonathan Charack CFO

Dividends

Book Value

FY

Company Description

Earnings

$6

$8

$10

$12

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

17

THOMAS PROPERTIES GROUP P/E P/B P/EBITDA P/S Curr Yield

515 South Flower Street Sixth Floor Los Angeles, CA 90071 27.95 1.63 12.97 2.42 1.51

Market Cap ($MM) 310.2 6.15 1.98

Symbol TPGI EQUITY S&P Rating #N/A N/A 3.05 59.46%

Exchange NASDAQ GM Industry Real Estate Oper/Develop 46.11315M 12.43%

Beta 1.10 #N/A N/AGross Margin #N/A N/A #N/A N/A

ROE (LTM) -1.16 188.64

ROA (LTM) -0.34 -0.43

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 0.13 0.22 -

- - - - - - - - - -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 - - -

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 112 160 -

Operating Income 0 2 1 5 7 7 5 - - -

Net Income 0 1 -2 2 4 4 3 -11 0 -

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Thomas Properties Group, Inc., based in Los Angeles, is a full-service real estate company that owns, acquires, develops and manages primarily office, as well as mixed-use and residential

properties on a nationwide basis. The company's primary areas of focus are the acquisition and ownership of premier properties, both on a consolidated basis and through its strategic

joint ventures, property development and redevelopment, and property management and leasing activities.

Diana Liang CFORandy Scott EVP

Dividends

Book Value

FY

Company Description

Debt/Equity

Earnings

EBIT / Interest

Quick RatioCurrent Ratio

Price (as of 12/6/12)

5.31

Attending ManagementRatios

YTD Change

52 Week Low 12/9/2011 YTD % Change

52 Week High 9/11/2012

Shares out 11/7/2012 SPX YTD % Chg

$3

$4

$5

$6

$7

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

18

TITAN INTERNATIONAL INC P/E P/B P/EBITDA P/S Curr Yield

2701 Spruce Street Quincy, IL 62301 United States 9.90 1.81 3.67 0.52 0.09

Market Cap ($MM) 1,011.2 29.95 1.72

Symbol TWI EQUITY S&P Rating B+ 16.86 8.84%

Exchange New York Industry Auto/Trk Prts&Equip-Orig 47.74108M 12.43%

Beta 2.02 3.21Gross Margin 15.61 1.81

ROE (LTM) 25.66 80.43

ROA (LTM) 10.47 2.61

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 2.23 2.72 3.60

- - - - - - - - - -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 - - -

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 1,847 2,326 3,165

Operating Income 0 2 1 5 7 7 5 214 308 362

Net Income 0 1 -2 2 4 4 3 119 151 210

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Titan International (NYSE: TWI) owns subsidiaries that manufacture wheels, tires and assemblies primarily for off-highway equipment used in agricultural, earthmoving/construction and

consumer (including all terrain vehicles) applications. Titan has become the leading manufacturer in the off-highway industry. The Company produces a broad range of unique products

that meet the specifications of original equipment manufacturers (OEM) and aftermarket customers in these markets.

Paul Reitz CFOKrista Gray IR & Treasury Manager

Dividends

Book Value

FY

Company Description

Debt/Equity

Earnings

EBIT / Interest

Quick RatioCurrent Ratio

Price (as of 12/6/12)

21.18

Attending ManagementRatios

YTD Change

52 Week Low 9/26/2012 YTD % Change

52 Week High 5/3/2012

Shares out 10/22/2012 SPX YTD % Chg

$10

$15

$20

$25

$30

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

19

XPO LOGISTICS INC P/E P/B P/EBITDA P/S Curr Yield

5 Greenwich Office Park Greenwich, CT 06831 United States - 1.33 - 0.92 -

Market Cap ($MM) 281.6 19.40 3.36

Symbol XPO EQUITY S&P Rating #N/A N/A 11.06 27.21%

Exchange New York Industry Transport-Services 17.92179M 12.43%

Beta 1.43 6.17Gross Margin 16.82 6.00

ROE (LTM) -11.21 0.69

ROA (LTM) -4.84 9.03

Per Share Overview (USD) Consensus Estimates2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.01 0.06 (0.08) 0.13 0.21 0.25 0.16 (1.34) (0.75) 0.47

- - - - - - - - - -

1.51 1.48 1.37 1.59 1.80 2.06 2.23 13.54 11.34 8.21

Financials Consensus Estimates

in millions, except per share amounts 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 75 70 91 113 121 134 162 280 779 1,550

Operating Income 0 2 1 5 7 7 5 -26 -6 41

Net Income 0 1 -2 2 4 4 3 -20 -12 20

EPS excluding Extraordinary Items (Fully Diluted) 0.01 0.06 -0.08 0.13 0.21 0.24 0.15

Average Shares Outstanding (Primary) 19.76 19.83 19.21 18.74 17.96 17.92 18.11

Notes

*Data provided by Bloomberg and Lambert, Edwards & Associates

Price (as of 12/6/12)

15.71

Attending Management

YTD Change

52 Week Low 12/20/2011 YTD % Change

Debt/Equity

Shares out 11/6/2012 SPX YTD % Chg

52 Week High 6/19/2012

EBIT / Interest

Quick RatioCurrent Ratio

Ratios

XPO Logistics, Inc. is a non-asset based, third-party logistics provider of freight transportation services that uses a network of relationships with ground, sea and air carriers to find the best

transportation solutions for its customers. The company offers its services through three distinct business units: freight brokerage; expedited transportation (Express-1, Inc.); freight

forwarding (Concert Group Logistics, Inc.). XPO Logistics serves more than 7,000 retail, commercial, manufacturing and industrial customers through 30 U.S. branches and 23 agent

locations.

Scott Malat Chief Strategy Officer

Dividends

Book Value

FY

Company Description

Earnings

$10

$12

$14

$16

$18

$20

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

1/3/2012 2/3/2012 3/3/2012 4/3/2012 5/3/2012 6/3/2012 7/3/2012 8/3/2012 9/3/2012 10/3/2012 11/3/2012 12/3/2012

YTD Performance

Volume Price

20

2012 SMID-West Investor Conference, Chicago

About Lambert, Edwards & Associates Established in 1998, Lambert, Edwards & Associates (LE&A) has a CAGR of 21.32% and now serves more than 100 clients in 20 states and five countries. We have achieved this with a team of national caliber talent who are continually focused on positively impacting clients and their businesses, the communities we serve and the individuals we counsel. With this commitment firmly in place, we’ve emerged as a top-20 investor relations agency nationally and a leader in small- and mid-cap IR. LE&A is a strategic advisory practice specializing in investor relations (IR), corporate communications, public relations (PR) and market research. Our approach to investor relations emphasizes solutions for the unique needs of each client – our custom IR programs are designed with the long-term strategic objectives of the company in mind. In addition to securing results for its clients, LE&A has also earned national recognition for its efforts, including the 2007 Silver Anvil – the “Oscar” of the industry – for Small-Cap IR Program of the Year and the 2011 Bulldog “Best Integration of IR and PR” award. Equipped with a team of seasoned industry professionals from a variety of Wall Street, corporate and agency backgrounds, our clients receive informed counsel from individuals with first-hand expertise and a broad array of industry experience. Our team includes senior staff with decades of experience who are actively involved in the daily activities and project execution for all clients. For more information: www.lambert-edwards.com

21