20101202 Master Thesis David Weiss - Ningapi.ning.com/.../20101202_MasterThesis_DavidWeiss.pdf ·...

76

Zeppelin University Department for Corporate Management & Economics Chair for Innovation Management Prof. Dr. Ellen Enkel Dipl. Ing. Annette Horváth Business Model Innovation in Venture Capital Investment Funds: Business Model Due Diligence in Venture Appraisal Master Thesis David M. Weiss [email protected] 02.12.2010

Transcript of 20101202 Master Thesis David Weiss - Ningapi.ning.com/.../20101202_MasterThesis_DavidWeiss.pdf ·...

Zeppelin University

Department for Corporate Management & Economics Chair for Innovation Management

Prof. Dr. Ellen Enkel

Dipl. Ing. Annette Horváth

Business Model Innovation in Venture Capital Investment Funds: Business Model Due Diligence in Venture Appraisal

Master Thesis

David M. Weiss [email protected]

02.12.2010

Table of Contents

I

Table of Contents

Table of Contents ........................................................................................... I

List of Figures ............................................................................................... III

List of Tables ............................................................................................... IV

List of Abbreviations .................................................................................... V

1. Introduction ............................................................................................. 61.1 Problem Outline and Relevance of Business Model Innovation and

Business Model Evaluation ................................................................... 71.2 Aim and Limitations ............................................................................... 121.3 Structure of Study and Proceedings ..................................................... 15

2. Early Stage Investment Appraisal ....................................................... 162.1 Early Stage and Venture Capital ........................................................... 162.2 Screening and Due Diligence: How Much Diligence is Due ................. 18

3. Definition of Business Model and its Context .................................... 193.1 Innovation ............................................................................................. 193.2 Business Model Innovation ................................................................... 203.3 Business Model ..................................................................................... 223.4 Business Model Typologies .................................................................. 24

4. Evaluation Approaches in Theory ....................................................... 284.1 Amit and Zott ......................................................................................... 284.1.1 Evaluation Approach ........................................................................... 284.1.2 Evaluation Approach in Theory Context .............................................. 324.1.3 Appraisal ............................................................................................. 364.2 Hamel .................................................................................................... 364.2.1 Business Model ................................................................................... 364.2.2 Evaluation Approach ........................................................................... 394.2.3 Appraisal ............................................................................................. 414.3 Morris, Schindehutte, Richardson and Allen ......................................... 414.3.1 Evaluation Approach ........................................................................... 414.3.2 Appraisal ............................................................................................. 434.4 Shi and Manning ................................................................................... 434.4.1 Evaluation Approach ........................................................................... 434.4.2 Appraisal ............................................................................................. 44

Table of Contents

II

4.5 Osterwalder et al. .................................................................................. 454.5.1 Evaluation Approach ........................................................................... 464.5.2 Appraisal ............................................................................................. 49

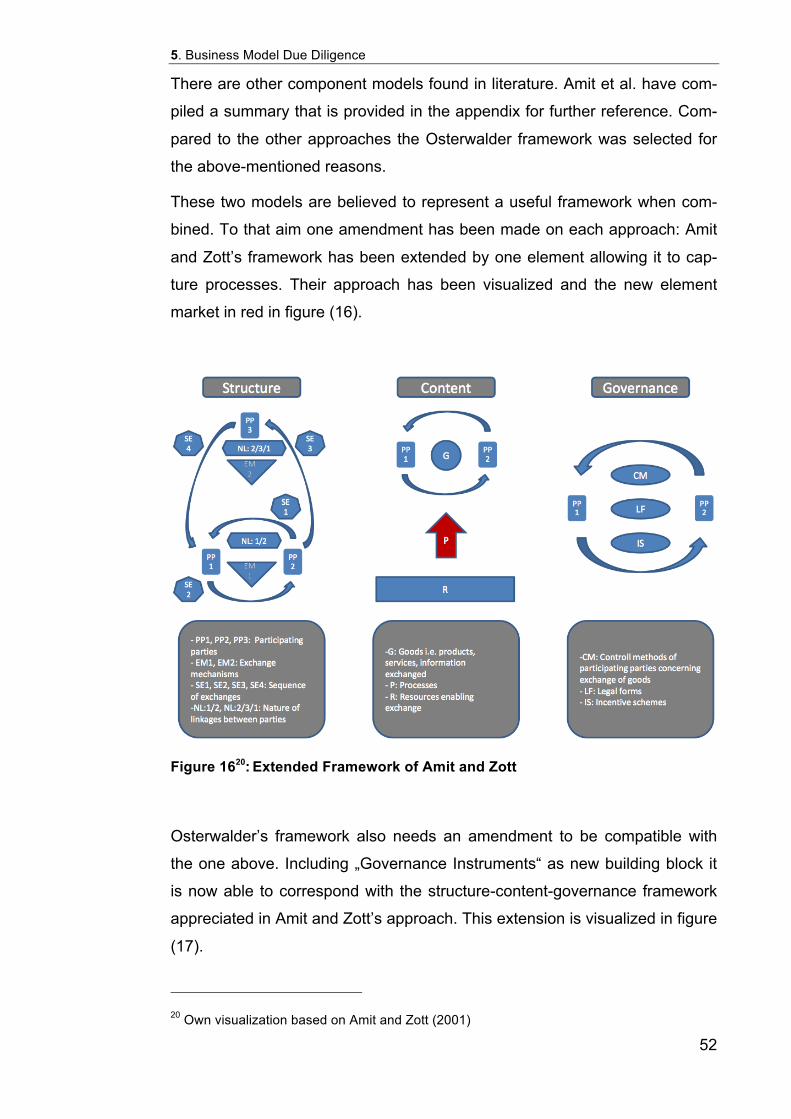

5. Business Model Due Diligence ............................................................ 505.1 Combined Evaluation Framework ......................................................... 505.2 Evaluation Criteria ................................................................................. 565.3 Evaluation Instrument Operationalized ................................................. 57

6. Survey and Methodology ..................................................................... 606.1 Research Partner .................................................................................. 606.2 Survey Results ...................................................................................... 60

7. Conclusion ............................................................................................ 65

Appendix ...................................................................................................... VI

Bibliography .................................................................................................. X

List of Figures

III

List of Figures

Figure 1: Business Model Articles in Academic and Non-Academic Literature ......................................................................................................... 7Figure 2: Operating Margin of Business Model Innovators Compared to Product and Process Innovators ................................................................... 10Figure 3: Average Premiums with Business Model Innovators Compared to Product and Process Innovators ............................................................... 11Figure 4: Types of Due Diligence .................................................................. 15Figure 5: Venture Capital Positioned in Investment Landscape .................... 17Figure 6: Venture Capital Investment Workflow ............................................ 18Figure 7: Dual Structure of Evaluation Instrument Positioned in HTGF Investments Workflow ................................................................................... 19Figure 8: Three Types on Innovation ............................................................. 20Figure 9: Three Types of Business Model Innovation ................................... 20Figure 10: Business Model Innovation Options ............................................. 22Figure 11: Strategy, Business Model and Tactics ......................................... 23Figure 12: Business Model Framework, Hamel ............................................. 37Figure 13: Big Picture Business Model Evaluation ........................................ 47Figure 14: Business Model Adaption ............................................................. 47Figure 15: Business Model Evaluation, Detailed SWOT ............................... 49Figure 16:Extended Framework of Amit and Zott .......................................... 52Figure 17: Extended Business Model Framework of Osterwalder et al. ........ 53Figure 18: New Combinded Framework: Osterwalder’s Component Framework Identified in Amit and Zott’s Framework ..................................... 54Figure 19: New Combined Framework: Amit and Zott’s Framework Identified in Osterwalder’s Component Framework ....................................... 55Figure 20: Framework Applied to Evaluation Criteria .................................... 57Figure 21: Business Model Due Diligence Tool, Long List Ratings at Level 2 ........................................................................................................... 58Figure 22: Business Model Due Diligence Tool, Caption .............................. 59Figure 23: Business Model Due Diligence Tool, Short List Ratings at Level 1 ........................................................................................................... 59

List of Tables

IV

List of Tables

Table 1: Survey Results on VC Evaluation Criteria ....................................... 14Table 2: Business Model Typologies in General ........................................... 25Table 3: Business Model Typologies in E-Business ...................................... 26Table 4: Business Model Elements and Design Themes .............................. 32Table 5: Anchoring of Design Themes in Theory .......................................... 34Table 6: Anchoring of Business Model Framework in Theory ....................... 35Table 7: Business Model Component Comparison ....................................... 42Table 8: Risk Evaluation Framework ............................................................. 44Table 9: Merging Terminology of Osterwalder et al. and Amit and Zott ........ 54Table 10: Sources of Evaluation Criteria, Short List ...................................... 56Table 11: Criteria Rating by Investment Managers ....................................... 63Table 12: Evaluation Aggregation ................................................................. 63Table 13: Criteria Ranking ............................................................................. 64

List of Abbreviations

V

List of Abbreviations

e.g. exempli gratia

et al. et alia

HTGF High-Tech Gründerfonds

i.e. id est

R&D research and development

SWOT strengths, weaknesses, opportunities threats

VC venture capital

VCs venture capitalists

1. Introduction

6

1. Introduction

Adapt or die.

Charles Darwin is quoted to have said, “It is not the strongest species that

survive nor the most intelligent, but the ones most responsive to change”.

This also holds true for companies and the way they conduct business. In

this context you may rephrase the above statement positively to read, “adapt

and outperform”.

A business model captures the logic of how companies do business. This is

why business model innovation has received increased attention over the last

decade. Companies need to understand what Business models are and how

you can design and redesign them in order to adapt to and survive in a

changing environment. Traditionally, hopes have been placed on innovative

technology as means to ensuring a comparative advantage. This no longer

holds true. There are numerous examples of companies that do not have

innovative technology and are nevertheless extremely successful simply be-

cause of a strong business model. A case in point is T-shirt producer Thread-

less. The company has integrated the customer into all major parts of the

value creation process – from designing prints to voting on which designs

should be printed ensuring that the exact demand for each print is met in

production. Like a conductor it orchestrates the players by making use of an

internet platform that is in essence quite simple and does not represent a

technological innovation. In spite of this, Threadless produces strong margins

and has been performing well.

If this company had not yet been founded and a team of entrepreneurs

showed up at a venture capital (subsequently VC) fund to present their busi-

ness idea, how could the investors know if this concept would prove to be a

success and if he should invest?

That is the ultimate question an investor needs to answer. This study identi-

fies the business model as one important source of information hardly made

use of in business practice and provides an instrument to unlock the busi-

ness model’s potential as source of information.

1. Introduction

7

1.1 Problem Outline and Relevance of Business Model Innovation and Business Model Evaluation

With the advent of the internet in the mid 1990s it became possible to con-

duct business in new ways. Information was able to flow efficiently at increas-

ing speed and volume as technology progressed and geographic regions

around the world became connected. The World Wide Web would prove to

do its part in making the world a global village.

The concept of Business models is nothing new. Every transaction since the

beginning of humankind can be reduced to some kind of model no matter

how simple, whether or not it was explicitly stated or consciously perceived

as such. The last twenty years and most notably the last decade have seen

an increase in interest in business models. The following figure shows the

numeric increase in publication in the field of business model innovation in

the past years. A clear jump can be identified in 1995.

Figure 11: Business Model Articles in Academic and Non-Academic Literature

1 Source: Amit et al. (2010)

The graph shows trends in the number of business model articles. „PnAJ“ identifies those articles Published in non-Academic Journals. „PAJ“ identifies articles Publis-

1. Introduction

8

The vast opportunities e-businesses offered and the first success stories of

the dotcom era created interest and incentives to think systematically about

how to conduct business in this newly emerging environment. Some of to-

day’s most successful businesses have emerged from this field. Not just e-

businesses have profited from systematically designing and redesigning

business models. There are numerous examples in other industries: Stihl

have shifted from selling heavy machinery to leasing; Rolls Royce does no

longer sells airplane engines but charges for the time in use. Currently Daim-

ler is rethinking their core business of selling cars by working on their “car 2

go” concept. Adopting the cost structure of the mobile phone industry cars

can be rented ad hoc for EUR 0.19 per minute in the organization’s pilot pro-

ject city of Ulm.

Apple’s success in recent years is credited to its ability to define a workable

business model for downloading music. “The combination of product innova-

tion and business model innovation (…) put Apple at the center of a market

approximately 30 times larger than its original market” (Lindgardt et al.,

2009).

Even investment funds acknowledge the importance of the business model

towards the success of a venture. This study is conducted in cooperation with

the praxis partner High-Tech Gründerfonds (subsequently HTGF). HTGF has

been traditionally focusing on investing into ventures with strong technology

USPs and has experienced that a considerable amount of portfolio compa-

nies with less interesting technology outperform technology-based firms. This

observation has lead to the idea of having a closer look at business models

and coming up with an instrument that would allow to make an ex ante

statement concerning its potential for success.

In literature there a numerous statements and findings that point to the fact

that the business model is indeed an important object of analysis and that

there is a need to expand research in this field. Chesbrough sums it up in his

hed in Academic Journals. Literature source employed: Business Source Complete EBSCOhost Database. Period: Ja-nuary 1975–December 2009.

1. Introduction

9

publication entitled “Business model innovation: it’s not just about technology

anymore” (Chesbrough, 2007). The days of focusing solely on innovative

technology as source of comparative advantage are long gone. “Today, inno-

vation must include business models, rather than just technology and R&D.

(…) A better business model often will beat a better idea or technology”

(Chesbrough, 2007). Competing on technology alone is increasingly difficult

with ever decreasing product life cycles and increasing costs of R&D. In fact

Casadeus-Masanell and Ricart (2010) point to the fact that firms compete

through their business model and that therefore the business model itself is a

source of comparative advantage. A disruptively innovative business model

can create such a comparative advantage in the same vain and become the

key asset and USP itself of the company. This does not mean that technolog-

ical innovation has become irrelevant. It means keeping pace with both these

elements: technological and business model innovation.

Rivette and Kline (2000) and Rappa (2001) point to the patentability of Busi-

ness models. It is only possible to patent Business models in the USA, how-

ever. That is a limiting factor. But to ventures operating in an industry that

cannot exclude the USA as market a patent only in the USA may present a

key asset.

Results of a study conducted by IBM in 2006 clearly show the relevance of

business model innovation. In figure (2) the right bar represents business

model innovators, the left bar product, service, market innovators and the

middle bar process innovators. Measured in cumulative annual growth rate

over five years in percent business model innovators clearly outperform

product and process innovators.

1. Introduction

10

Figure 22: Operating Margin of Business Model Innovators Compared to Prod-

uct and Process Innovators

In a similar vein, a survey conducted by The Boston Consulting Group and

BusinessWeek compare a company cluster of process and product innova-

tors with a company cluster of business model innovators. They find that a)

business innovators earn a considerable higher average premium and b) re-

turns are more sustainable so that business model innovators still outper-

formed product and process innovators even in the 10-year category.

2 Source: IBM (2006)

1. Introduction

11

Figure 33: Average Premiums with Business Model Innovators Compared to

Product and Process Innovators

Why is there a need for a business model evaluation instrument?

A standardized process is useful because it ensures that important aspects

are not overlooked. It also allows a third party to retrace the logic of an in-

vestment decision or refusal. This is especially important to VC funds that

operate according to the four-eye principle. Franke and Gruber found that on

average 55% of all investment proposals are read only by one investment

manager, before a refusal or an invitation to a personal meeting is given

(Franke and Gruber, 2004). They argue that subjective influences play a ma-

jor role. This is also supported by the argument of “similarity biases” Franke

et al find in their publication on VC funds’ investment criteria that summarizes

the message in the title: “What You Are Is What You Like” (Franke et al.,

2003).

Currently much of the decision making process is subjected to personal

judgment and the experience of the investment manager in charge. This can

work well for experienced investment managers in a majority of cases. An

inexperienced investment manager will not have these tools at his/her dis-

posal. And even experienced investors make mistakes. In light of these as-

3 Source: Lingardt et al. (2009)

1. Introduction

12

pects, a standardized process for the evaluation of business model’s can

prove to be a useful tool for all VC funds.

Besides the points of reliability and accuracy, efficiency is a further benefit of

an evaluation instrument. Larger VC funds receive between 1000-2000 in-

vestment requests per year. For these VC funds a standardized process

would save resources in the screening phase, which would allow an expan-

sion of the scope, of ventures that can be screened.

Especially in early stage investments where information is scarce, every

source of information is to be exploited to its maximum. It is argued here that

there is potential to unlock towards this aim by developing a reliable process

for business model evaluation that does not exist as of today. There are ap-

proaches towards evaluating business models in literature, however none of

them can be considered comprehensive and moreover none of them is oper-

ationalized in a way that corresponds to the logic of existing workflows, and

that is satisfactory in terms of content and user friendly in terms of applicabil-

ity.

1.2 Aim and Limitations

A literature review has lead to the work of Franke, Gruber, Harhoff, and Hen-

kel (2008) who analyze investment criteria of VC funds. They find that the

team is the most important criteria and find significant differences in evalua-

tion results originating from novice or from experienced venture capitalists. In

their implications for future research they suggest “it may be fruitful to ex-tend this line of research by investigating whether experience also has a significant impact on the evaluation of other aspects of venture pro-posals. For example it may well be that the assessment of business models (e.g. Amit & Zott, 2000) could be subject to experience effects.

Whereas novice VCs [ i.e. venture capitalists] may look at simple com-

ponents of business models (…), experienced VCs may place more weight on the fit of the various components, and thus may arrive at a better understanding of the overall value creation of the proposed ven-ture.”

From this, two implications are deducted for this study. First, the business

model is a relevant unit of analysis as VC investment criterion and there is a

1. Introduction

13

need for an adequate instrument that can be used for business model evalu-

ation. Secondly an hypothesis is suggested to be tested, namely:

„Novice VCs tend to analyze single components where as experienced VCs tend to analyze the fit of linkage between the components“.

The aim of this study is to develop such an evaluation instrument for busi-

ness model evaluation and to test the proposed hypothesis. Since the first

aim poses a greater challenge it constitutes the main part of this study.

The ultimate aim for a VC is to be able to gauge ex ante whether a venture

has the potential to be successful. There are many factors that contribute to

success in the end and the business model is just one of them amongst other

objects of interest analyzed during due diligence as shown in figure (4). Of

course, the business model could be great but fail because of being imple-

mented at the wrong time, in the wrong environment or executed poorly by

the people driving it. These are important factors determining the success or

failure of a venture. However, in order to focus on the specific importance of

the business model, these other factors will not be taken into consideration.

In literature, there is not sufficient research on business models as source of

information for investment decision-making. A survey of literature conducted

by Franke, Gruber, Harhoff and Henkel sums up investment criteria that are

usually employed during the due diligence process:

1. Introduction

14

Table 14: Survey Results on VC Evaluation Criteria

They find that in essence all criteria can be „collated into four major groups,

namely criteria related to (1) the product service offering; (2) the mar-

ket/industry; (3) the start-up team; and (4) the financial returns to be ex-

pected“ (Franke et al., 2008). Striking is the fact that in none of these studies

the business model as unit of analysis is mentioned among the top three cri-

teria. This could mean that it nevertheless is a unit of analysis, however nev-

er ranks among top three or it is not seen explicitly as unit of analysis. Inter-

views with investment managers have pointed to the fact that is indeed ana-

lyzed in business practice – but not explicitly or as a structured process but

4 Source: Franke et al. (2008)

1. Introduction

15

rather in a way that overlaps with other units of analysis. In VC due diligence

you typically find six areas of the venture that are analyzed: team, technolo-

gy, market, finance, legal and tax. This study aims at contributing towards

establishing business model due diligence as new form of due diligence next

to existing forms displayed in figure 4. It is argued that the business model

contains valuable information that are currently unsufficiently exploited. This

is especially relevant for early stage investments since information is scarce

and every information source is to be made use of to maximum extent.

Figure 4: Types of Due Diligence

1.3 Structure of Study and Proceedings

Working towards these aims at first in chapter 2 relevant aspects of the VC

industry are presented to set the scene for the results this study aims at pro-

ducing. Chapter 3 defines how the term business model is used in this study

and elaborates on business model innovation and innovation as its context.

The following chapters presents the evaluation approached found as result of

a literature review. These evaluation approaches are critically appraised and

compared in order to select two approaches that would be suitable for a

combined new approach serving as underlying framework for the evaluation

TypesofDueDiligence

1)Team

2)Technology

4)Finance

5)Legal

6)Tax

7)BusinessModel

2. Early Stage Investment Appraisal

16

instrument being developed. Chapters 6 and 7 are concerned with develop-

ing the evaluation instrument. Once the underlying framework has been de-

veloped, it is filled with evaluation criteria. These have been collected from a

literature review and replenished with criteria gained from interviews with in-

vestment managers. This list of criteria is then presented to investment man-

agers asking them to rate them according to importance. The result is an

evaluation instrument that is built on a combined framework that is well an-

chored in theory and that offers high usability in business practice. It consists

of criteria collected from literature and investment managers and is opera-

tionalized as a tool for business model due diligence reflecting requirements

in VC investment processes in its dual structure.

2. Early Stage Investment Appraisal

2.1 Early Stage and Venture Capital

Early stage investment is characterized by information scarcity and high risk.

Typically you would find a team with a business idea expressed in some kind

of business plan that ranges from a chaotic PowerPoint presentation to a well

reflected, structured and elaborated business proposal and execution plan.

Some may have already passed the phase of prototyping and have first ex-

periences from field tests which allow them to verify and support the assump-

tions made in the business plan. Others have experience from operations

and may already have managed to achieve first revenues.

In contrast to this, later stage investments provide a history of revenues,

sales performance and market feedback. Therefore, during a due diligence

process there is plenty of information that can be analyzed and a valid esti-

mation of market, operational and financial risk can be made.

Since there is not much information available during early stage every source

of information needs to be exploited to its best.

It is argued here that the business model is one of the few available sources

of information in early stage. Currently it is not exploited to its best. Much of

the evaluation process pertaining to it is subject to intuitive judgment depend-

ing in its accuracy on the experience of the respective investment manager in

2. Early Stage Investment Appraisal

17

charge instead of being subject to a structured process that is objective and

well reflected. There is a need for such a process since it increases the in-

formation volume investment decisions are based on and improves the accu-

racy of this information base.

There are different opinions and definitions as to what “early stage” and “ven-

ture capital” means with regards to venture maturity and the investment

amount. Some scholars further differentiate early stage into seed, start-up,

first stage and later stage, which will not be further elaborated given the focus

of this survey. To give an overview and position the focus of this survey, the

following graph illustrates a common understanding of investment stages in

entrepreneurial finance:

Figure 5: Venture Capital Positioned in Investment Landscape

Other countries such as the USA are known to be less risk averse than the

country this survey has been conducted in which is also reflected in invest-

ment volumes and timing. You will hardly find any VC fund in Germany that

invests in an extremely early stage. Therefore founders usually start off alone

or are pre-financed by so-called friends/fools/family often followed by a busi-

ness angel round later on. However, business angels usually invest only be-

tween EUR 20.000 and EUR 200.000. Therefore any venture that needs

funding above that would need to start off with the mentioned pre-financing

stages and produce results in order to reduce investment risk, increase cred-

ibility and subsequently receive funding from a VC fund. Bank loans are not

an option unless taken privately due to conservative risk assessment. Ac-

cording to its political mandate to support start up companies, High-Tech

Gründerfonds as the leading German early stage VC fund invests into ven-

tures that are not older that 1 year with an investment of EUR 0.5 million in a

Founder(s)Friends,Fools,Family

BusinessAngels

VentureCapital

PrivateEquity

GrowthFinancingby

Banks

Exit:IPO,AqcuisiRon

2. Early Stage Investment Appraisal

18

standardized process. The total investment amount can vary upwards de-

pending on how many investors join the round pari passu.

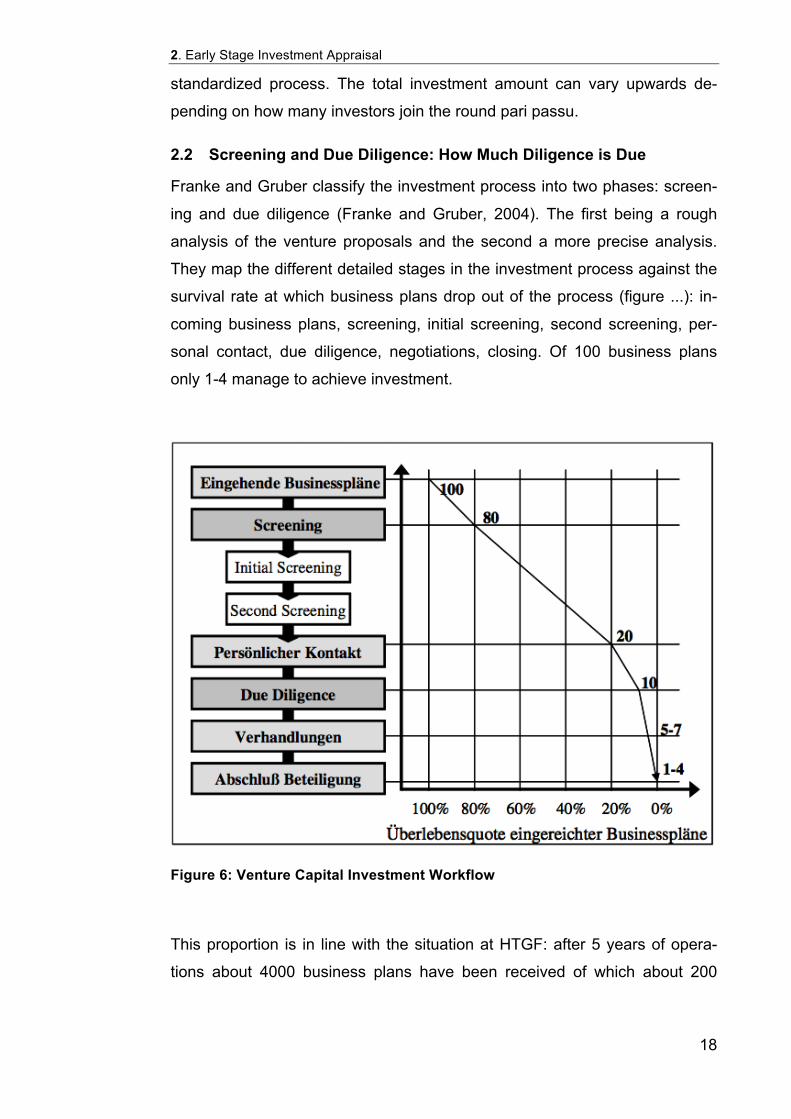

2.2 Screening and Due Diligence: How Much Diligence is Due

Franke and Gruber classify the investment process into two phases: screen-

ing and due diligence (Franke and Gruber, 2004). The first being a rough

analysis of the venture proposals and the second a more precise analysis.

They map the different detailed stages in the investment process against the

survival rate at which business plans drop out of the process (figure ...): in-

coming business plans, screening, initial screening, second screening, per-

sonal contact, due diligence, negotiations, closing. Of 100 business plans

only 1-4 manage to achieve investment.

Figure 6: Venture Capital Investment Workflow

This proportion is in line with the situation at HTGF: after 5 years of opera-

tions about 4000 business plans have been received of which about 200

3. Definition of Business Model and its Context

19

have received investments. In HTGF processes the screening phase is to be

placed before a term sheet is signed and the due diligence phase thereafter.

Figure 7: Dual Structure of Evaluation Instrument Positioned in HTGF Invest-

ments Workflow

The evaluation tool developed in this study is designed in a way that one part

is optimized for use during screening and another for use during due dili-

gence. Illustrated in form of a sieve the first part serves to sieve proposals in

search of promising ventures with a minimum of time invested into a rough

estimate that is made up of a short list of 14 criteria identified as relevant.

The second part illustrated in form of a lens serves the purpose of a detailed

analysis. A newly developed framework is operationalized in a way that it

extends these 14 criteria and gives detailed measurable statements concern-

ing different aspects of the business model. This dual structure of the instru-

ment accommodates the tradeoff between time and accuracy allowing an

adequate response to the question of how much diligence is due at a particu-

lar stage of the process.

3. Definition of Business Model and its Context

3.1 Innovation

Innovation has traditionally been understood as product and process innova-

tion. The business model concept has recently been increasingly addressed

in the domains of innovation and technology management. In these literature

3. Definition of Business Model and its Context

20

streams, „the business model represents a new dimension of

tion“ (Amit et al., 2010) that enables companies to commercialize innovative

ideas and technologies. It is seen both as a source of innovation and a vehi-

cle facilitating innovation.

Figure 8: Three Types on Innovation

3.2 Business Model Innovation

Moving on from Innovation to business model innovation, Giesen, Berman,

Bell and Biltz (2007) suggest a categorization identifying three types of busi-

ness model innovation: industry models, revenue models and enterprise

models. The first explains innovation in supply chain, the second describes

innovative ways how companies create value and the third defines the inno-

vation within the firm’s structure and its contribution to value chains.

Figure 9: Three Types of Business Model Innovation

Business model innovation needs to be distinguished from business model

invention. The first term refers to a business model that exists and has been

reshaped. The later term refers to a new business model that has not yet

been executed.

InnovaRon

ProductInnovaRon

ProcessInnovaRon

BusinessModel

InnovaRon

BusinessModel

InnovaRon

Industrymodels

Revenuemodels

Enterprisemodels

3. Definition of Business Model and its Context

21

Henderson and Clark (1990) make a distinction between a component and

architecture level pertaining to products:

"[The] distinction between the product as a whole - the system - and the

product in its parts - the components - has a long history in the design litera-

ture ( ... ) The overall architecture of the product lays out how the compo-

nents will work together ( ... ) A component is defined here as a physically

distinct portion of the product that embodies a core design concept and per-

forms a well defined function ( ... ) The distinction between the product as a

system and the product as a set of components underscores the idea that

successful product development requires two types of knowledge. First, it

requires component knowledge, or knowledge about each of the core design

concepts and the way in which they are implemented in a particular compo-

nent. Second, it requires architectural knowledge or knowledge about the

ways in which the components are integrated and linked together into a co-

herent whole“

This approach is transferred to the concept of Business models and business

model innovation by Zollenkop (2006) and summarized in figure (10). It dis-

plays three dimensions of business model innovation. The first dimension

and axis refer to business model innovation occurring on the structural level.

It ranges from principally innovated to gradually innovated. The second di-

mension and axis depicts business model innovation pertaining to the com-

ponents of a business model also ranging from principally innovated to grad-

ually innovated. Thirdly, range or number of affected elements is a dimension

and axis spanning from high to low. This results in four types of business

model innovation: architectural business model innovation (upper left quad-

rant), gradual business model innovation (lower left quadrant), principal busi-

ness model innovation (upper right quadrant) and modular business model

innovation (lower right quadrant).

3. Definition of Business Model and its Context

22

Figure 105: Business Model Innovation Options

3.3 Business Model

Moving from business model innovation to business model, it is insightful to

first clarify what a business model is not. A business model is not a business

plan, it is not strategy and it is not to be confused with typologies.

A business model is to be found in a business plan. However the business

plan stresses its execution and provides information encompassing every-

thing that pertains to the business – not just its business model.

„Today, „business model“ and „strategy“ are among the most sloppily used

terms in business; they are often stretched to mean everything – and end up

meaning nothing “ (Magretta 2002). Cassadeus-Masanell and Ricart (2010)

describe the difference between Business models, strategy and tactics using

the analogy of an automobile. Their underlying understanding of a business

model is not normative. It does not imply that a business model has to con-

sider certain aspects such as containing certain elements. It is simply a set of

choices. Based on this idea and coming back to the analogy of a car, strate-

gy is the choice what type of car you choose. A fouy-by-four will allow the

driver to move well in off-road terrain and will limit him in terms of maximum

5 Source: Zollekop (2006)

3. Definition of Business Model and its Context

23

speed, whereas a roadster will present the opposite picture of potential and

limitations. The car itself is the business model offering a certain set of op-

tions to act due to its configuration in potential and limitations. The driving of

the car is the available set of actions, or tactics as the authors call it.

Figure 116: Strategy, Business Model and Tactics

Business models should also not be confused with typologies. Typologies are

Business models that have been grouped to different clusters. Since this is

an important insight into understanding Business models an extensive list of

examples is provided in the next chapter.

But what exactly is a business model?

„At a general level the business model has been referred to as a statement

(Stewart & Zhao, 2000), a description (Applegate, 2000; Weill & Vitale,

2001), a representation (Morris, Schindehutte, & Allen, 2005; Shafer, Smith,

& Linder, 2005), an architecture (Dubosson-Torbay, Osterwalder, & Pigneur,

2002; Timmers, 1998), a conceptual tool or model (Osterwalder, 2004; Os-

terwalder, Pigneur, & Tucci, 2005; Teece, 2010), a structural template (Amit

& Zott, 2001), a method (Afuah & Tucci, 2001), a framework (Afuah, 2004), a

6 Source: Casadeus-Masanell and Ricart (2010)

3. Definition of Business Model and its Context

24

pattern (Brousseau & Penard, 2006), and as a set (Seelos & Mair, 2007).

“This lack of definitional consistency and clarity represents a potential source

of confusion, promoting dispersion rather than convergence of perspectives,

and obstructing cumulative research progress on business models.“ (Amit et

al., 2010)

There a numerous definitions of what a business model is. Amit et al. have

compiled the most referenced to definitions in a list that is provided in the

appendix for further reference.

The definition this study is based on revolves around the idea of transactions.

It is argued in this paper that this pinpoints the core of a business model.

Cambridge online dictionary7 defines business as „the activity of buying and

selling goods, services, or a particular company that does this, or work you

do to earn money“. The idea of buying and selling is also covered by the

word trade, defined in its form as a verb as „to buy and sell goods or ser-

vices, especially between countries“. In its form as a noun it is defined as „to

exchange something, or to stop using or doing something and start using or

doing something else instead“. This definition features the notion of exchang-

ing something which is core to the idea of transaction defined as „when

someone buys or sells something, or when money is exchanged“.

Based on these considerations, the definition of Amit and Zott (2001) has

been selected to work with in this study:

“The business model depicts the content, structure, and governance of transactions designed so as to create value through the exploitation of business opportunities.”

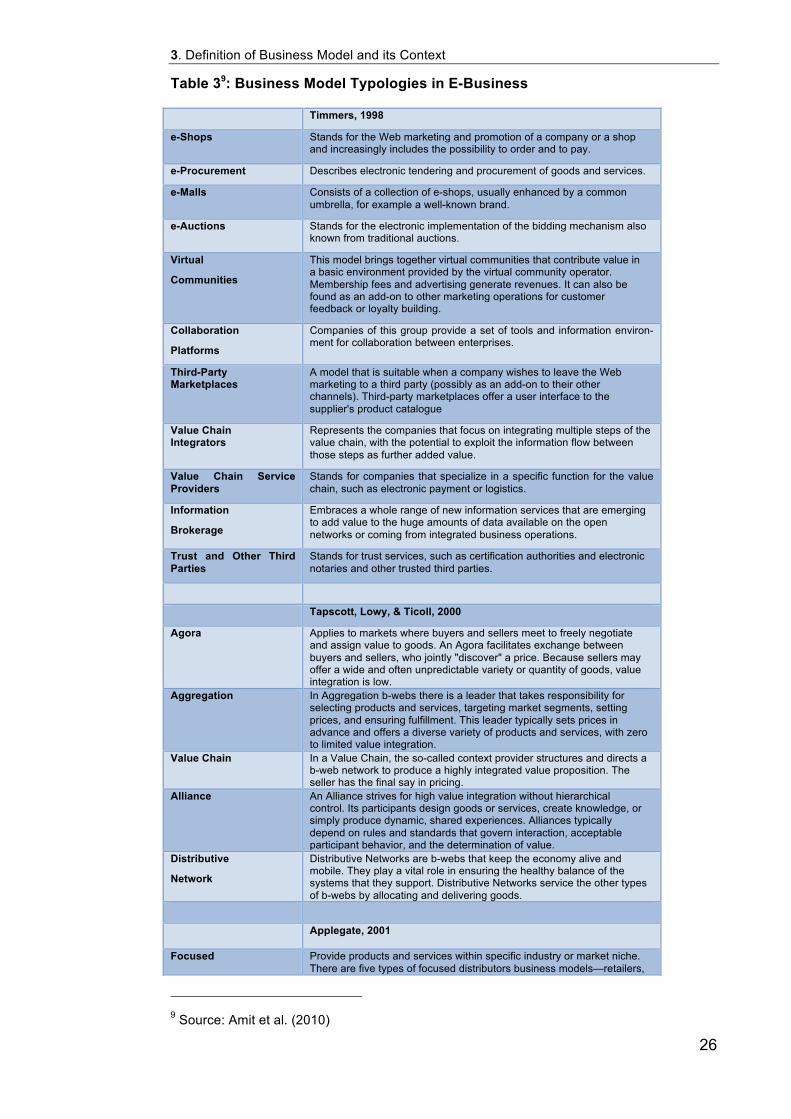

3.4 Business Model Typologies

The term business model is often confused with the term business model

typologies. Some scholars also refer to typologies as taxonomies or patterns.

To make this distinction clear, detailed examples of different typologies are

given in this chapter. Since this is a way of clustering business models into

different groups it provides a useful overview and is fruitful in gaining under-

standing about business models. Two compilations are presented that can be

7 Source: http://dictionary.cambridge.org

3. Definition of Business Model and its Context

25

found in literature. The first is taken from Johnson (2010) and is more gen-

eral. The second is taken from Amit et al. (2010) and features business mod-

el typologies from the field of e-business.

Table 28: Business Model Typologies in General

Type

Examples Description

Auction

Sotheby’s, Priceline, eBay

Customers name their own price for a product/service. Unwanted products are sold to a large customer base

Alter the usual formula

Amazon Amazon generates high profits on its positive working capital, because it holds little inventory and yet enjoys long payables like traditional booksellers do

Bricks + Clicks Home Depot, Tesco, REI

Integrate both an online (clicks) and an offline (bricks) presence to browse, order, and pick up products.

Bundle elements to-gether

iPod and iTunes, fast food value meals

Make purchasing simple and more complete by packaging related products together.

Create user communi-ties

Angie’s List Grant members access to network of quality information about services or goods; generate revenue through mem-bership fees and advertisements.

Cell phone Sprint, Better Place Give away the “cell phone” for little to no cost but gain high margins by selling the “minutes” on a per-usage fee.

Develop unique partner-ships

MinuteClinic MinuteClinic enables CVS to make money in ways other than visit fees (i.e., it gets customers into stores and ex-poses them to other CVS products).

Dial down features Motofone Target less-demanding consumers with products or ser-vices that may not be superior but are adequate and per-haps more convenient, simple, etc.

Do more to address the job

UPS Look beyond your typical offering and address other jobs your customers are trying to get done.

Disintermediation Dell Deliver your standard product or service more directly to the customer through a new, non-standard channel.

Freemium LinkedIn, Skype, Pandora

Offer basic services for free but charge for upgraded or premium services.

Lease instead of sell Xerox Allow customers the opportunity to pay for performance.

Leverage new influenc-ers

Hindustan, Unilever Identify new influencers that make the delivery of your offering more convenient, far-reaching, or affordable.

Low-touch approach Xiameter Offer standardized, low-price version of a product or ser-vice that is traditionally customized and higher priced.

Multi-level marketing Amway, Avon, NuSkin

Market and sell products or services direct to consumers, outside of retail locations.

Own the undesirable

AllLife Seek to serve segments of the market that may not appear to be immediately attractive.

Razors/blades Gillette, personal printers

Give away the “razors” for essentially no cost but make profits by selling higher-margin “blades.”

Reverse razors/blades iPod/iTunes Give away the “blades” (iTunes) for essentially no cost but make profits by selling higher-margin “razors” (iPod).

Servitzation of products IBM Provide not only a one-time product offering but also an ongoing service-offering attendant to the product.

Subscription Magazines, Netflix, BabyPlays

Consumer pays a subscription price to gain access to the product or service.

8 Source: Johnson (2010)

3. Definition of Business Model and its Context

26

Table 39: Business Model Typologies in E-Business

Timmers, 1998

e-Shops Stands for the Web marketing and promotion of a company or a shop and increasingly includes the possibility to order and to pay.

e-Procurement Describes electronic tendering and procurement of goods and services.

e-Malls Consists of a collection of e-shops, usually enhanced by a common umbrella, for example a well-known brand.

e-Auctions Stands for the electronic implementation of the bidding mechanism also known from traditional auctions.

Virtual

Communities

This model brings together virtual communities that contribute value in a basic environment provided by the virtual community operator. Membership fees and advertising generate revenues. It can also be found as an add-on to other marketing operations for customer feedback or loyalty building.

Collaboration

Platforms

Companies of this group provide a set of tools and information environ-ment for collaboration between enterprises.

Third-Party Marketplaces

A model that is suitable when a company wishes to leave the Web marketing to a third party (possibly as an add-on to their other channels). Third-party marketplaces offer a user interface to the supplier's product catalogue

Value Chain Integrators

Represents the companies that focus on integrating multiple steps of the value chain, with the potential to exploit the information flow between those steps as further added value.

Value Chain Service Providers

Stands for companies that specialize in a specific function for the value chain, such as electronic payment or logistics.

Information

Brokerage

Embraces a whole range of new information services that are emerging to add value to the huge amounts of data available on the open networks or coming from integrated business operations.

Trust and Other Third Parties

Stands for trust services, such as certification authorities and electronic notaries and other trusted third parties.

Tapscott, Lowy, & Ticoll, 2000

Agora Applies to markets where buyers and sellers meet to freely negotiate and assign value to goods. An Agora facilitates exchange between buyers and sellers, who jointly "discover" a price. Because sellers may offer a wide and often unpredictable variety or quantity of goods, value integration is low.

Aggregation In Aggregation b-webs there is a leader that takes responsibility for selecting products and services, targeting market segments, setting prices, and ensuring fulfillment. This leader typically sets prices in advance and offers a diverse variety of products and services, with zero to limited value integration.

Value Chain In a Value Chain, the so-called context provider structures and directs a b-web network to produce a highly integrated value proposition. The seller has the final say in pricing.

Alliance An Alliance strives for high value integration without hierarchical control. Its participants design goods or services, create knowledge, or simply produce dynamic, shared experiences. Alliances typically depend on rules and standards that govern interaction, acceptable participant behavior, and the determination of value.

Distributive

Network

Distributive Networks are b-webs that keep the economy alive and mobile. They play a vital role in ensuring the healthy balance of the systems that they support. Distributive Networks service the other types of b-webs by allocating and delivering goods.

Applegate, 2001

Focused Provide products and services within specific industry or market niche. There are five types of focused distributors business models—retailers,

9 Source: Amit et al. (2010)

3. Definition of Business Model and its Context

27

Distributors marketplaces, aggregators, infomediaries, and exchanges.

Portals Not defined. They include horizontal portals, vertical portals, and affinity portals. These are differentiated on the basis of the gateway access, affinity group focus, revenues source, and costs structure.

Infrastructure

Distributors

Enable technology buyers and sellers to perform business transactions. There are three categories of focused distributors: infrastructure retailers, infrastructure marketplace, and infrastructure exchange, which are differentiated on the basis of control inventory, online selling presence, online pricing, revenues source, and costs structure.

Infrastructure Portals Enables consumers and businesses to access online services and information. They are further classified into horizontal infrastructure portals (Internet service providers, network service providers and web hosting) and vertical infrastructure portals (producers and distributor application service providers, or ASPs).

Infrastructure Producers

Design, build, market, and sell technology hardware, software, solutions, and services. Four types of infrastructure producers are: equipment component manufacturers, software firms, customer software and integration, infrastructure service firms.

Rappa, 2001

Brokerage Model They bring buyers and sellers together and facilitate transactions. Usually, a broker charges a fee or commission for each transaction it enables. Subcategories are: Marketplace Exchange, Business Trading Community, Buy/Sell Fulfillment, Demand Collection System, Auction Broker, Transaction Broker, Bounty Broker, Distributor, Search Agent, Virtual Mall.

Advertising

Model

The broadcaster, in this case a web site, provides content (usually for free) and services (like email, chat, forums) mixed with advertising messages in the form of banner ads. The banner ads may be the major or sole source of revenue for the broadcaster. The broadcaster may be a content creator or a distributor of content created elsewhere. Subcategories are: Portal, Personalized Portal, Niche Portal, Classifieds, Registered Users, Query-based Paid Placement, Contextual Advertising.

Infomediary Model Some firms function as infomediaries (information intermediaries) by either collecting data about consumers or collecting data about producers and their products and then selling it to firms which in turn can mine it for important patterns and other useful information to better serve their clients. Examples are: Advertising Networks, Audience Measurement Services, Incentive Marketing, Metamediary.

Merchant Model Wholesalers and retailers of goods and services sold over the Internet. These include: Virtual Merchant, Catalog Merchant, Click and Mortar, Bit Vendor

Manufacturer Model Manufacturers can reach buyers directly through the Internet and thereby compress the distribution channel.

Affiliate Model The affiliate model provides purchase opportunities wherever people may be surfing. It does this by offering financial incentives (in the form of a percentage of revenue) to affiliated partner sites. The affiliates provide purchase-point click-through to the merchant via their web sites.

Community Model The community model is based on user loyalty. Users have a high investment in time and emotion in the site. In some cases, users are regular contributors of content and/or money. Examples are Voluntary Contributor Models and Knowledge Networks.

Subscription Model Users are charged a periodic—daily, monthly or annual—fee to subscribe to a service. Examples are Content Services, Person-to- Person Networking Services, Trust Services, Internet Service Providers.

Utility Model The utility model is based on metering usage, or a pay-as-you-go approach. Unlike subscriber services, metered services are based on actual usage rates.

Weill & Vitale, 2001

Content Providers Provides content (information, digital products, and services) via intermediaries.

Direct to Customer Provides goods or services directly to the customer, often bypassing traditional channel members.

Full-Service Provider Provides a full range of services in one domain (e.g., financial, health,

4. Evaluation Approaches in Theory

28

industrial chemicals) directly via allies, attempting to own the primary consumer relationship.

Full-Service Provider Provides a full range of services in one domain (e.g., financial, health, industrial chemicals) directly via allies, attempting to own the primary consumer relationship.

Intermediary Brings together buyers and sellers by concentrating information.

Shared

Infrastructure

Brings together multiple competitors to cooperate by sharing common IT infrastructure.

Value Net

Integrators

Coordinate activities across the value net by gathering, synthesizing, and distributing information.

Virtual

Community

Creates and facilitates an online community of people with a common interest, enabling interaction and service provision.

Direct to Customer Provides goods or services directly to the customer, often bypassing traditional channel members.

Whole-of- Enterprise/Government

Provides a firm-wide single point of contact, consolidating all services provided by a large multi-unit organization.

4. Evaluation Approaches in Theory

Comprehensive business model innovation literature overviews already exist.

In this regard I would like to point to the review of Amit, Zott and Massa

(2010). Anders Sundelin has visualized a timeline of publications from 2000-

2010 that includes business model frameworks where provided by the au-

thors. This constitutes an excellent chronologic overview of business model

innovation literature and is referred to for means of orientation.

Given the focus of our topic this chapter on theory specifically highlights

evaluation approaches found in literature. A literature a review was conduct-

ed in search of evaluation approaches and with regards to specific evaluation

criteria that could later be used as items for evaluation. Presented to an in-

vestment manager, five of these approaches could be identified as having

potential toward informing an evaluation instrument that would be of use for

business practice. These approaches are discussed in detail in this chapter.

4.1 Amit and Zott

4.1.1 Evaluation Approach

Amit and Zott define a Business model as follows:

“The business model depicts the content, structure, and governance of

transactions designed so as to create value through the exploitation of busi-

ness opportunities.” (Amit and Zott 2001)

4. Evaluation Approaches in Theory

29

In this definition a business model at its core is all about capturing and ex-

plaining the nature of transactions that occur. The authors suggest three per-

spectives from which to approach this effort: content, structure and govern-

ance and name them business model “design elements”.

In addition they propose four sources of value: novelty, lock-in, complemen-

tarities, efficiency. They name these sources “design themes” of a business

model. Business models contain all three design elements and all four design

themes. Different businesses will focus on different themes of this cluster.

They find that novelty-centered and efficiency-centered Business models

have a positive impact on entrepreneurial firms (Amit and Zott, 2007). The

following passage summarizes these three design elements and four design

themes.

Design Elements

Content

Transaction content refers to the goods or information that are being ex-

changed, and to the resources and capabilities that are required to enable

the exchange.

Structure

Transaction structure refers to the parties that participate in the exchange

and the ways in which these parties are linked. It also includes the order in

which exchanges take place (i.e., their sequencing), and the adopted ex-

change mechanism for enabling transactions. The choice of transaction

structure influences the flexibility, adaptability, and scalability of the actual

transactions.

Governance

Transaction governance refers to the ways in which flows of information, re-

sources, and goods are controlled by the relevant parties. It also refers to the

legal form of organization, and to the incentives for the participants in trans-

actions.

In their activity system approach content refers to what activities are select-

ed, structure refers to how activities are linked and governance to who per-

4. Evaluation Approaches in Theory

30

forms activities. In addition to these design elements the authors suggest four

design themes and define them as follows:

Design Themes

Efficiency:

Efficiency refers to transaction efficiency. According to transaction theory

transaction efficiency increases as the cost per transaction decreases. Spe-

cifically, it encompasses the completeness and quality of information and the

efficiency of its flow and the efficiency of processes such as production and

distribution. A transaction is efficient if costs per transaction are considerably

lower than what you could consider as industry standard.

In short: A business model is efficient, when transactions are cheaper, faster,

of better quality and more simple than the average.

Complementarities:

Complementarities refer to the bundles of goods that provide more value

than the total separate value of each single good. You want to serve custom-

er needs and wants as good as possible thinking in a job-to-be-done mentali-

ty. You thus integrate products and services from partners to create that all-

encompassing solution. Combination of online and offline (click-and-mortar),

vertical and horizontal complementarities and cross-selling are core themes.

In resource based view theory complementarities are considered strategic

assets and a source of value creation. Network theory emphasizes the im-

portance of complementarities among network participants. Complementari-

ties increase value by enabling revenue increase. Complementarities are

given when product value is enhanced and additional products or services

are provides in a way the works towards providing a solution to a customer’s

needs and wants.

In short a business model performs well in terms of complementarities when

products and/or services are complementarily combined (alone or with part-

nering companies) to bundles in a "job-to-be-done" mentality, meeting needs

and wants of customers extremely well.

4. Evaluation Approaches in Theory

31

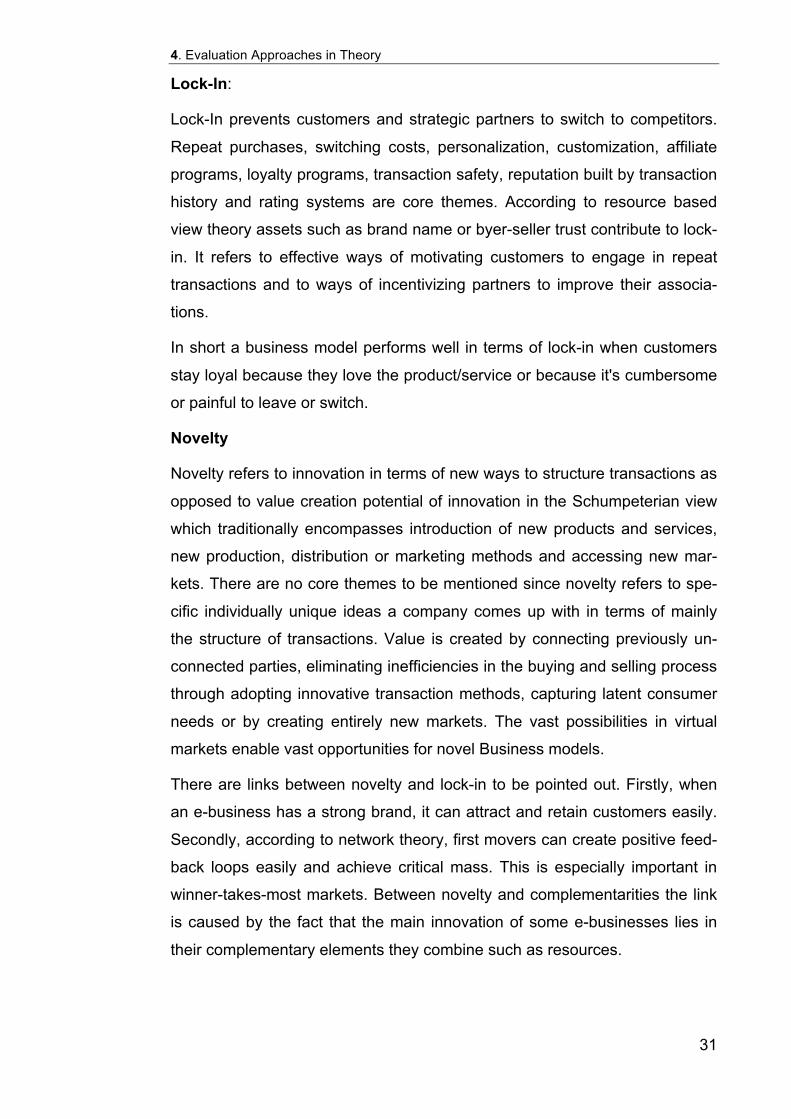

Lock-In:

Lock-In prevents customers and strategic partners to switch to competitors.

Repeat purchases, switching costs, personalization, customization, affiliate

programs, loyalty programs, transaction safety, reputation built by transaction

history and rating systems are core themes. According to resource based

view theory assets such as brand name or byer-seller trust contribute to lock-

in. It refers to effective ways of motivating customers to engage in repeat

transactions and to ways of incentivizing partners to improve their associa-

tions.

In short a business model performs well in terms of lock-in when customers

stay loyal because they love the product/service or because it's cumbersome

or painful to leave or switch.

Novelty

Novelty refers to innovation in terms of new ways to structure transactions as

opposed to value creation potential of innovation in the Schumpeterian view

which traditionally encompasses introduction of new products and services,

new production, distribution or marketing methods and accessing new mar-

kets. There are no core themes to be mentioned since novelty refers to spe-

cific individually unique ideas a company comes up with in terms of mainly

the structure of transactions. Value is created by connecting previously un-

connected parties, eliminating inefficiencies in the buying and selling process

through adopting innovative transaction methods, capturing latent consumer

needs or by creating entirely new markets. The vast possibilities in virtual

markets enable vast opportunities for novel Business models.

There are links between novelty and lock-in to be pointed out. Firstly, when

an e-business has a strong brand, it can attract and retain customers easily.

Secondly, according to network theory, first movers can create positive feed-

back loops easily and achieve critical mass. This is especially important in

winner-takes-most markets. Between novelty and complementarities the link

is caused by the fact that the main innovation of some e-businesses lies in

their complementary elements they combine such as resources.

4. Evaluation Approaches in Theory

32

In short, a business model is novel when something in the business model is

new, be it components or connections or innovatively new combinations

thereof.

Amit and Zott sum up all four design themes at their three elementary levels

of content, structure and governance as follows:

Table 410: Business Model Elements and Design Themes

4.1.2 Evaluation Approach in Theory Context

Amit and Zott review contributions of several theories to the notion of busi-

ness models including value chain analysis, Schumpeterian innovation, re-

source-based view, theory of strategic networks and transaction cost eco-

nomics. While none of them completely explain the notion of the business

model and its function of value creation, they argue that each theoretical

framework contributes elements towards that aim and is reflected in each

design theme to a different degree as summarized in the table below. Their

10 Source: Amit and Zott (2001)

4. Evaluation Approaches in Theory

33

proof of theoretical anchoring is summarized in this chapter and in detail in

their 2001 publication for further reference.

Value chain analysis contributes to the notion of Business models since it

describes value creation at the firm level as suggested by Porter (1985). All

four aspects of this analysis are relevant to a comprehensive business mod-

el: defining the strategic business unit, identifying critical activities, defining

products, and determining the value of an activity. Central to this theory is the

idea of value creation by differentiation along every step oft he value chain.

Schumpeterian innovation revolves around the idea that innovation is the

source of value. Sources for innovation in turn can be new goods, new mar-

kets, new production methods, new supply sources, and reorganization of

industries. This is why this value source „novelty“ is mainly traced back to this

theory line. Schumpeter coined the term „creative destruction“ describing a

technological innovation that changes practices in economic life and enables

the entrepreneur to achieve so-called Schumpeterian rents until this technol-

ogy becomes established in the market. This change caused by technologi-

cal innovation is also referred to as disruption or Schumpeterian shock.

Resource based view of the firm ascribes the firm’s value creation to its

unique bundle of resources and capabilities. It states that uniquely combining

a set of resources and capabilities creates value especially if they are com-

plementary, specialized, heterogeneous within an industry, durable, scarce,

not easily imitated and not easily traded. Stressing the idea of resource com-

binations, especially the value source „complementarities“ is rooted in this

theory line.

Strategic network theory is especially relevant for e-businesses in the virtual

market space. The Internet enhances transaction efficiency, reduces asym-

metries of information and thereby improves coordination between the parties

involved in the transaction. Value creation by lock-in draws mainly on these

aspects in terms of theoretical background.

Transaction cost economics identifies transaction efficiency as a major

source of value creation. Efficiency is understood in a sense that costs are

reduces for participating parties in the transaction. Therefore efficiency as a

source of value is derived mainly from transaction cost theory.

4. Evaluation Approaches in Theory

34

Theoretical anchoring of sources of value (design themes) in e-businesses

are summarized by the authors in the following table:

Table 511: Anchoring of Design Themes in Theory

The above stated business model definition by Amit and Zott contains the

business model elements content, structure and governance. He authors

claim that „this definition of a business model is consistent with the im-

portance of transaction efficiency (emphasized by transaction cost econom-

ics), novelty in transaction content, structure and governance (Schumpeteri-

an innovation), complementarities among resources and capabilities (advo-

cated by resource-based view theory), and network effects (inherent in stra-

tegic networks). It captures the sources of value in e-businesses identified in

this paper and is hence applicable in virtual markets in general“ (Amit and

Zott, 2001). They support this model with five arguments.

1) Innovation in the context of business model not only refers to products

and, processes, distribution channels and markets but also to ex-

change mechanisms and transaction architectures. Therefore this

business model definition is consistent with Schumpeter’s idea of in-

novation being an act of „creative destruction“.

2) The definition’s consistency with the value chain framework is justified

by highlighting the fact that elements such as processes and sources

of value are core to this theory. A higher level of consistency is

achieved if the idea of value chain is extended to a process that ena-

11 Source: Amit and Zott (2001)

Table entries describe the degree to which the identified sources of value in e-businesses are viewed, directly or indirectly by different theoretical frameworks in strategic and ent-repreneurship as important for value creation.

4. Evaluation Approaches in Theory

35

bles transaction instead of following a flow of goods from creation to

sale.

3) The value oft he business model increases as the bundle of products

and services become „more difficult to imitate, less transferrable, less

substitutable, more complementary and more productive with

use“ (Amit and Zott 2001). With resources and their combinations at

the core of this notion the definition is consistent with resource based

view theory.

4) Consistency with network theory is derived from the link between net-

work configuration and value creation and the fact that the locus of

value creation is seen as the network and not necessarily the firm.

5) Rooted in Williamson’s (1975) focus on the efficiency of alternative

governance structures mediating transaction it is argued that in addi-

tion to efficiency enhancements there are other factors that contribute

to value creation, namely novelty, lock-in and complementarities.

Business model elements content, structure and governance are argued

to be rooted in strategic network theory. Therefore the business model

construct can be seen as extension of strategic network theory. The au-

thors support this finding with the following table.

Table 612: Anchoring of Business Model Framework in Theory

12 Source: Amit and Zott (2001)

4. Evaluation Approaches in Theory

36

4.1.3 Appraisal

According to journal rank and references in literature the approach of Amit

and Zott can be considered the most accepted in this field. They have con-

tinuously published well-accepted papers in this field for almost 10 years. It

was decided to significantly build this study on their approach because it is

simply the best approach to be found. It is theoretically well grounded and

applicable to business practice. The fact that the business model definition

focuses on transaction allows enough flexibility to apply it to different indus-

tries and stages of venture maturity. Since innovation is something that dis-

rupts existing structures it is necessary to work with concepts that are open

enough to incorporate innovative elements. This points to a shortcoming of

the widely accepted component models. While they have a wide range of

uses and portray simplicity, they lack an openness of concept that would al-

low for innovation.

The focus of Amit and Zott on e-business is limiting on the one hand. On the

other hand it allows accurate results in this field while all-encompassing ap-

proaches tend to be blurry and too unspecific when applied to the task at

hand.

According to my opinion, their approach lacks especially one important as-

pect: process. My suggestion, as elaborated in Chapter 5.1 is to extend the

approach with this element. Having worked with the detailed level of the ap-

proach, I find that hardly any items presented on “sequence” as part of struc-

ture and “legal forms” as part of governance are suggested. Furthermore it is

not so clear what is meant by “exchange mechanisms” and what the differ-

ence is to “nature of linkages”. It is also unclear how to handle the financial

model, since it is unclear where it fits into content-structure-governance-

framework.

Nevertheless this approach is by far the best I could find in literature.

4.2 Hamel

4.2.1 Business Model

To understand the evaluation approach of Hamel one needs to grasp the

business model it is based on. It consists of four key elements (customer in-

4. Evaluation Approaches in Theory

37

terface, core strategy, strategic resources and value network) that are linked

by three bridges (customer benefit, configurations and company boundaries).

The quality of this business model can be measured by four criteria, namely

efficiency, uniqueness, fit and profit boosters.

Figure 1213: Business Model Framework, Hamel

Core strategy consists of three elements: business mission, product and

market scope and basis for differentiation.

Business Mission captures the overall objective of the strategy and encom-

passes value proposition, strategic intent, “big, hairy, audacious goals” (Ha-

mel 2000), purpose, and overall performance objectives. Product and market

scope describe the essence of where the firm competes: which customers,

which locations, what product segments, and where it doesn’t compete. Ba-

sis for differentiation depicts the essence of how the firm competes and in

specific how it competes differently from its competitors.

Strategic resources comprise core competencies, strategic assets and core

processes.

Core competencies means what the firm knows. It encompasses skills and

unique capabilities. Strategic assets are what the firm owns and include:

brands, patents, infrastructure, proprietary standards, customer data, and

anything else that is both rare and valuable. Core processes are what people

13 Source: Hamel (2000)

4. Evaluation Approaches in Theory

38

in the firm actually do. It refers to methodologies and routines used in trans-

forming inputs into outputs. Core processes are activities, rather than assets

or skills that are used in translating competencies, assets, and other inputs

into value for customers.

Configuration refers to the unique way in which competencies, assets and

processes are combined and interrelated in support of a particular strategy. It

explains the linkages between competencies, assets and processes and how

these linkages are managed. To be successful strategies and business mod-

els need to rest on a unique blending of competencies, assets and process-

es.

Customer interface includes the four elements fulfillment & support, infor-

mation & insight, relationship dynamics and pricing structure.

Fulfillment & support describes how the firm reaches customers – which

channels it uses, what kind of customer support it offers, and what level of

service it provides. Information & insight is knowledge collected from and uti-

lized on behalf of customers. It is the information content of the customer in-

terface. It also refers to the ability to extract insights from this information that

can help the firm to do novel things for customers. Furthermore, it covers the

information that is made available to customers before and after purchase.

Relationship dynamics, describes the nature of the interaction between pro-

ducer and customer. It can be face-to-face or indirect, sporadic or continu-

ous. Relevant aspects are how the customer can interact with the producer

and what feelings these interactions invoke on the part of the customer. It

enables ways to create a sense of loyalty by the pattern of interactions. And

finally the pricing structure describes if you charge for a product or for a ser-

vice, if you charge directly or indirectly via a third party, if you can bundle

components or price them separately, if you charge a flat rate or charge for

time or distance and if you have set prices or market-based prices.

Customer benefits refer to a customer-derived definition of the basic needs

and wants that are being satisfied. They link the core strategy to the needs of

the customer. It is important to decide what benefits are going to be included.

Value network includes suppliers, partners and coalitions.

4. Evaluation Approaches in Theory

39

Suppliers are to be found at the top of the producer’s value chain. Privileged

access to or a good relationship with suppliers can be a key element of a

novel business model. Partners supply curtail complements to a product or

solution. Where relationships with suppliers are vertical relationship with pro-

ducers are more horizontal. A creative configuration of partners can be the

key to a successful business model. Coalitions with like-minded competitors

can be of advantage where investment or technology hurdles are high or

where there is a high risk of ending up on the losing side of a winner-take-all

market. Coalition members are more than partners; they share directly in the

risk and rewards of industry revolution.

Company boundaries describe the link between strategic resources and the

value network. They are decisions that have been made about what the firm

does in-house and what it outsources out to the value network.

4.2.2 Evaluation Approach

Hamel offers an approach to evaluate the performance of the above de-

scribed business model. Four evaluation criteria are proposed toward that

aim: efficiency, uniqueness, fit and profit boosters.

Efficiency the way Hamel understands it means that the value customers

place on the benefits delivered must exceed the costs of producing those

benefits. This differs from Amit and Zott’s definition of efficiency that aims at

transaction efficiency measured in the costs that are reduced for participating

parties.

Uniqueness is given when above average profits can be realized because

the business model differentiates itself from others in the market. The aim is

to create a business model that is unique in its conception and execution. A

business model must be unique in ways that are valued by customers.

Fit between business model elements allows a firm to generate healthy prof-

its. This is the case when all its elements are mutually reinforcing and the

business model can be considers internally consistent because all its parts

work together for the same end goal.

Profit boosters is a criterion well elaborated by Hamel and supported by

subcategories, namely network effects, positive feedback effects, learning

4. Evaluation Approaches in Theory

40

effects, pre-emption, choke points, customer lock-in, scale, focus, scope,

portfolio breadth, operating agility and lower breakeven.

Network effects: the value of a network increases with increasing amount of

network members. Positive feedback effects refer to the way the firm makes

use of market feedback to turn an initial lead into an „unbridgeable