2010 North Bridge Future of Open Source Study

38

4 TH Annual Leadership Keynote

-

Upload

north-bridge -

Category

Technology

-

view

130 -

download

1

Transcript of 2010 North Bridge Future of Open Source Study

4TH Annual Leadership Keynote

Tim YeatonPresident & CEO

Larry AugustinCEO

Dries BuytaertCTO & Co-FounderJim Whitehurst

President & CEO

Michael Skok

General Partner

January 22, 2015 2

DirectionJanuary 22, 2015 3

Industry

Investment

Industry

Investment

Direction

1/22/2015 4

January 22, 2015 5

Who Took the

2010 Survey?

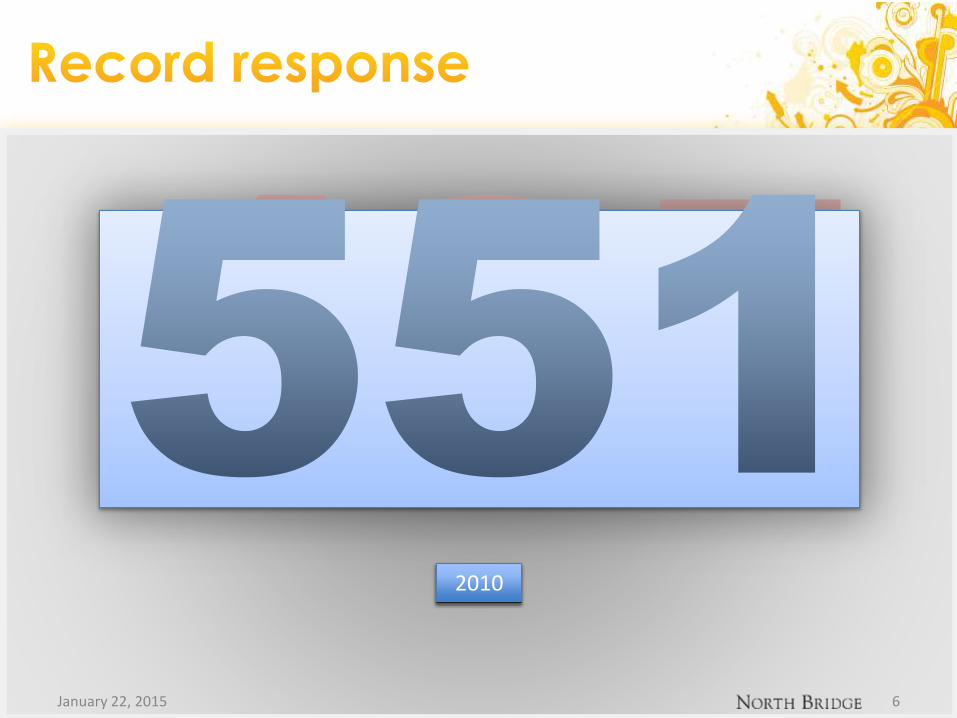

20092010

January 22, 2015 6

Vendors Non-Vendors

%%

January 22, 2015 7

Vendors Non-Vendors

January 22, 2015 8

Which sectors are susceptible to disruption?

What are the barriers for Open Source?

What business strategies create value?

1/22/2015 9

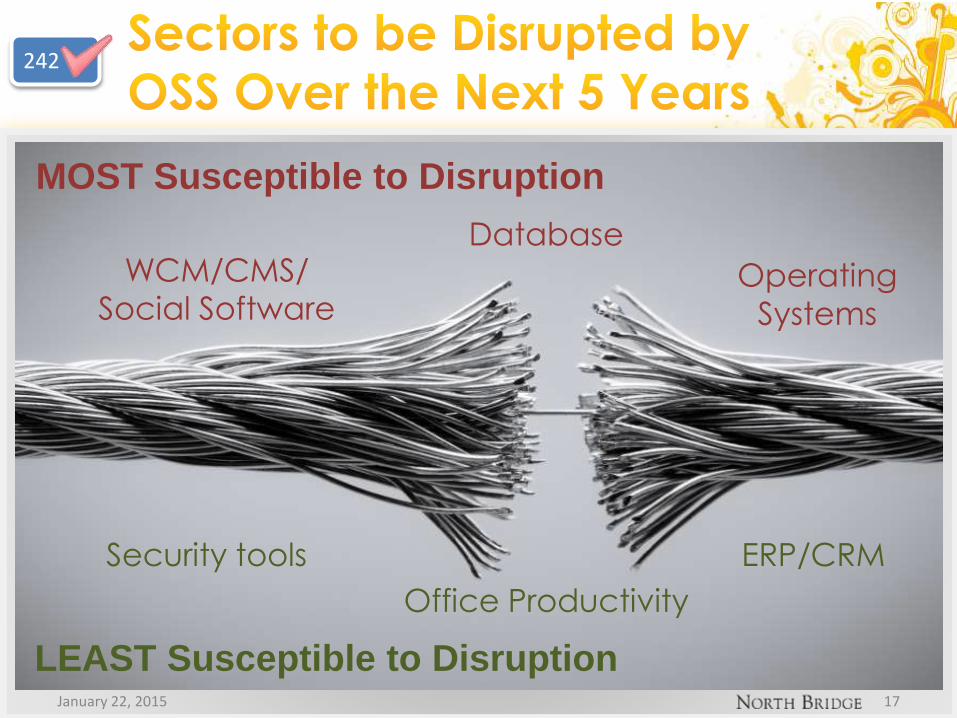

242

206

181

DirectionJanuary 22, 2015 10

Industry

Investment

Industry

Investment

Direction

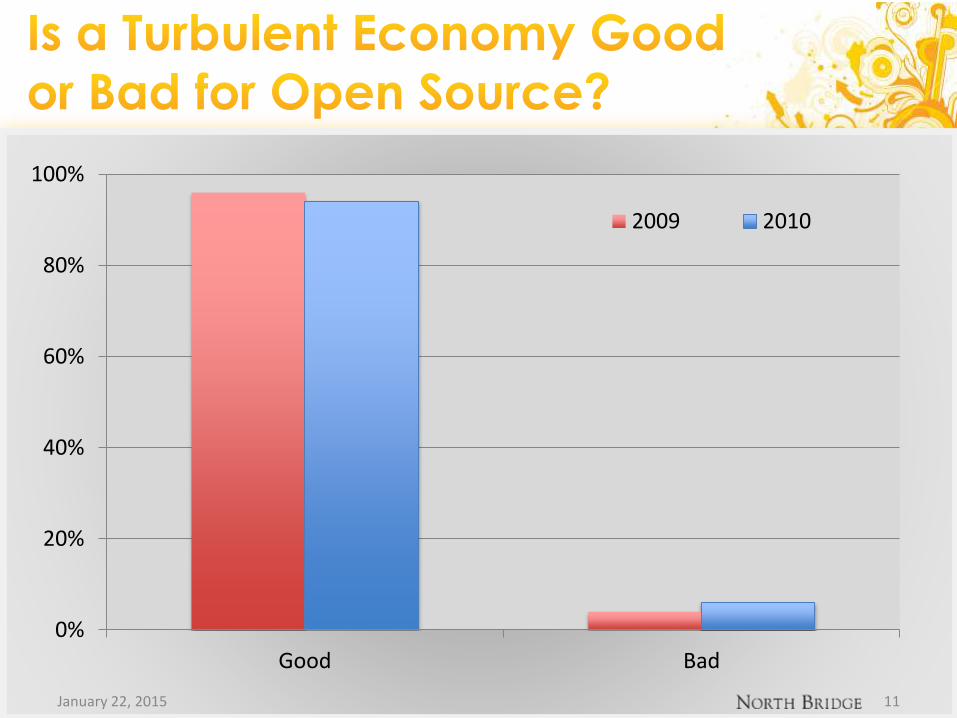

January 22, 2015 11

0%

20%

40%

60%

80%

100%

Good Bad

2009 2010

Lower costs

Superior security

Freedom of VENDOR Lock

Community support

Access to code libraries

Rapid pace of innovation

Freedom of DIY

Lower costs

Superior security

Freedom of VENDOR lock-in

Better quality software

Access to code libraries

Rapid pace of innovation

Freedom of DIY

20082009 Lower costs

Superior security

Freedom of VENDOR lock-in

Better quality software

Access to code libraries

Rapid pace of innovation

Freedom of DIY

2010

January 22, 2015 12

Economic

Downturn

Public Sector

Adoption

Private Sector

Adoption

Past

Experience

With OSS

Other

January 22, 2015 13

January 22, 2015 14

Barriers to OSS?206

Unfamiliarity with open source solutions

Lack of internal technical skills

Lack of formal commercial vendor support

January 22, 2015 15

1

2

3

January 22, 2015 16

January 22, 2015 17

ERP/CRM

Office Productivity

WCM/CMS/Social Software

Operating

Systems

Database

Security tools

MOST Susceptible to Disruption

LEAST Susceptible to Disruption

242

January 22, 2015 18

Office Productivity

MOST Susceptible to Disruption

LEAST Susceptible to Disruption

242

Office Productivity

MoreLess

Same

2009

2010

January 22, 2015 19

January 22, 2015 20

So, what ARE you

doing with OSS?

Vendors

Non-Vendors

January 22, 2015 21

Build & Sell OSS

Exclusively

Build & Sell OSS &

Proprietary

Build Solutions on OSS

Limited OSS Use

Substantial OSS Use

Exclusive OSS Use

Other

January 22, 2015 22

Services

Support

Custom

software for

clients

Traditional

license sales

SaaS

Cloud

computing

Other

Appliance

sales

12%

29%

27%

9%

31%

38%

Dual Licensing

Pro-Serv & Consulting

Subscription-based Support

2009

2010

January 22, 2015 23

Which business strategies will create

the most value for OSS Vendors ?

181

0% 20% 40% 60%

2010

2009

2008

January 22, 2015 24

SaaS

Virtualized

Infrastructure

Cloud

Computing

January 22, 2015 25

January 22, 2015 26

2009

2010

DirectionJanuary 22, 2015 27

Industry

Investment

Industry

Investment

Direction

1/22/2015 28

37%

$375M

Dollars

Invested

20%

66

Deals

Done

12

12

M&A $4.3B

Overall

Exists

1.2

DirectionJanuary 22, 2015 29

Industry

Investment

Industry

Investment

Direction

1/22/2015 30

OPEN

142

111119

155

% of IT Deployment which is OSSJanuary 22, 2015 31

75%-100%50%-75%

25%

-50%

0%-

25%

January 22, 2015 32

2009-2014

2010-2015

2008-2013

50% or more on OSS

DirectionJanuary 22, 2015 33

Industry

Investment

Industry

Investment

Direction

Tipping point

New sectors

Innovation

But…

1/22/2015 34

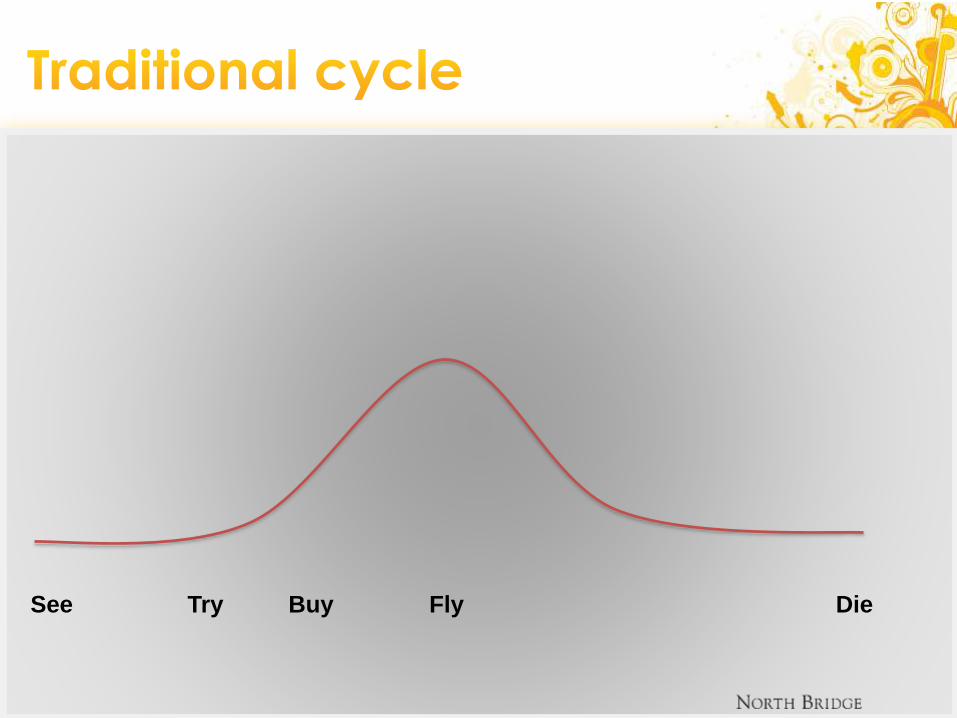

See Try Buy Fly Die

See Try Buy Fly Die

Open Source barriers:

Skills?Visibility?

Unfamiliarity

Value add? Solo?

Vendor support

Free?

DeveloperUser

See Try Buy Fly Die

Live OpenCommercial Open Source v2.0:

Open Source barriers:

Marketplace

Friction free

Self service

On demand

… as a Service

Supported

Skills?Visibility?

Unfamiliarity

Value add? Solo?

Vendor support

Free?

Managed

January 22, 2015 38

tinyurl.com/FOOS2010