2010 monitor-john gregg-tc logistics strategy

38

Copyright © 2009 by Monitor Company Group, L.P. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means — electronic, mechanical, photocopying, recording, or otherwise — without the permission of Monitor Company Group, L.P. This document provides an outline of a presentation and is incomplete without the accompanying oral commentary and discussion. COMPANY CONFIDENTIAL SAN FRANCISCO SÃO PAULO SEOUL SINGAPORE TOKYO TORONTO ZURICH SHANGHAI BEIJING CHICAGO HONG KONG CAMBRIDGE DELHI DUBAI JOHANNESBURG PARIS LOS ANGELES MADRID MUMBAI MUNICH NEW YORK MOSCOW LONDON Temperature Controlled Logistics China Strategy - TC Development Plan John Gregg, Associate Principal & Head Monitor Emerging Markets Division Management Summary Presentation December 12 th , 2010

-

Upload

john-gregg -

Category

Business

-

view

564 -

download

1

Transcript of 2010 monitor-john gregg-tc logistics strategy

Copyright © 2009 by Monitor Company Group, L.P.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means — electronic, mechanical, photocopying,

recording, or otherwise — without the permission of Monitor Company Group, L.P.

This document provides an outline of a presentation and is incomplete without the accompanying oral commentary and discussion.

COMPANY CONFIDENTIAL

SAN FRANCISCO SÃO PAULO SEOUL SINGAPORE TOKYO TORONTO ZURICHSHANGHAI

BEIJING CHICAGO HONG KONGCAMBRIDGE DELHI DUBAI JOHANNESBURG

PARISLOS ANGELES MADRID MUMBAI MUNICH NEW YORKMOSCOWLONDON

Temperature Controlled LogisticsChina Strategy -

TC Development PlanJohn Gregg, Associate Principal & Head Monitor Emerging Markets Division

Management Summary PresentationDecember 12th, 2010

2Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Agenda

Executive Summary

China TC Market Overview & Growth Trends

Global Competitors & Local Players

TC Market Rationale & Proposed Initiatives

TC Market Breakdown & Target Industry Segments

Financial Impacts & Initiative Requirements

Implementation Plan & Risk Assessment

Next Steps & Decision Needs

3Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Executive Summary (1/2)

Temperature Controlled Logistics, also regarded as Cold Chain Logistics or Perishable logistics, is an integrated temperature-controlled system in which product quality, integrity and safety are maintained throughout the process of export, packaging, packing, transport, handling, cold storage, distribution, delivery and placement at point of sale.

It applies to all temperature sensitive products such as frozen, chilled & fresh perishable foodstuffs, pharmaceutical products, Hi-tech electronic equipments, flowers and chemicals.

As Chinese consumers’ lifestyle and buying habits evolve, more attention has been paid to food safety. In most inshore cities, cold chain logistics market emerges and begins to boom. According to reliable data from officials, TC Logistics market in 2005 reached 1.3 trillion CNY and will expand to 10.8 trillion CNY by 2015.

However, with rapid market development, we have to overcoming market challenges:

- Backward infrastructure, below-standard refrigerator vans, obsolete freezing technology

- Complicated TC-related industry segments make TC logistics a technology and capital intensive industry, high return and high risk

- Intensified competition from both experienced global competitors and emerging local players

- Out-of-date cold chain management mainly due to scarcity of skilled and qualified professionals

Notwithstanding, current cold chain logistics market is in primary stage, few players and game rules, but a more-profit bright future.

4Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Executive Summary (2/2)

The effective implementation of TC capability development plan will strengthen our existing advantage in TC-related FMCG market and make emerging TC-related Life Science market our next profit source.

Accordingly [ABC Company] ’s total revenue is expected to grow from € 68mn in 2006 to €184mn by 2010, exceeding the forecast of initial financial planning.

To achieve these financial targets, investment requirements of € 7.94mn besides of an increase of 7 indirect headcount are identified.

In a word, entry into TC market is aligned with [ABC Company] China Strategy, providing big potential to increase company’s revenue and profit in China’s intriguing and complex TC market.

5Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Agenda

Executive Summary

China TC Market Overview & Growth Trends

Global Competitors & Local Players

TC Market Rationale & Proposed Initiatives

TC Market Breakdown & Target Industry Segments

Financial Impacts & Initiative Requirements

Implementation Plan & Risk Assessment

Next Steps & Decision Needs

6Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

6

Total Logistics Market Size,

109.1

Total Logistics Market Size, 190

1.34.8

2005 2010

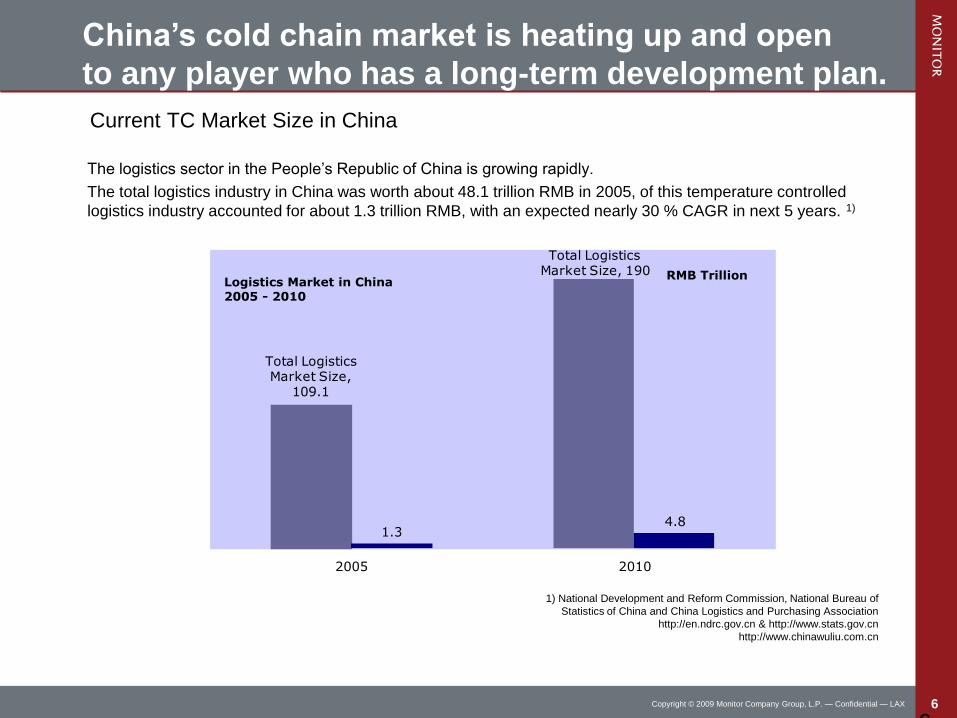

Current TC Market Size in China

ThelogisticssectorinthePeople’sRepublicofChinaisgrowingrapidly.

The total logistics industry in China was worth about 48.1 trillion RMB in 2005, of this temperature controlled

logistics industry accounted for about 1.3 trillion RMB, with an expected nearly 30 % CAGR in next 5 years. 1)

1) National Development and Reform Commission, National Bureau of

Statistics of China and China Logistics and Purchasing Association

http://en.ndrc.gov.cn & http://www.stats.gov.cn

http://www.chinawuliu.com.cn

Logistics Market in China2005 - 2010

RMB Trillion

China’s cold chain market is heating up and open

to any player who has a long-term development plan.

7Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

7

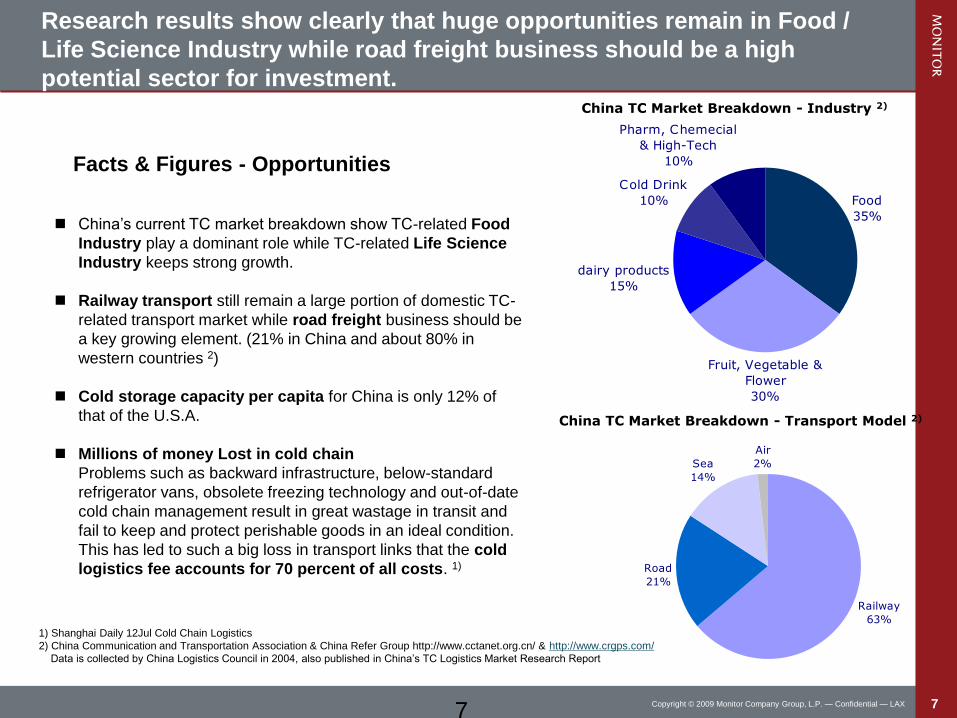

Facts & Figures - Opportunities

China’scurrentTCmarketbreakdownshowTC-related Food

Industry play a dominant role while TC-related Life Science

Industry keeps strong growth.

Railway transport still remain a large portion of domestic TC-

related transport market while road freight business should be

a key growing element. (21% in China and about 80% in

western countries 2)

Cold storage capacity per capita for China is only 12% of

that of the U.S.A.

Millions of money Lost in cold chain

Problems such as backward infrastructure, below-standard

refrigerator vans, obsolete freezing technology and out-of-date

cold chain management result in great wastage in transit and

fail to keep and protect perishable goods in an ideal condition.

This has led to such a big loss in transport links that the cold

logistics fee accounts for 70 percent of all costs. 1)

1) Shanghai Daily 12Jul Cold Chain Logistics

2) China Communication and Transportation Association & China Refer Group http://www.cctanet.org.cn/ & http://www.crgps.com/

DataiscollectedbyChinaLogisticsCouncilin,2004alsopublishedinChina’sTCLogisticsMarketResearchReport

Food

35%

Fruit, Vegetable &

Flower

30%

dairy products

15%

Cold Drink

10%

Pharm, Chemecial

& High-Tech

10%

China TC Market Breakdown - Industry 2)

Railway

63%

Road

21%

Sea

14%

Air

2%

China TC Market Breakdown - Transport Model 2)

Research results show clearly that huge opportunities remain in Food /

Life Science Industry while road freight business should be a high

potential sector for investment.

8Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Facts & Figures - Challenges

1) Online Article from http://www.crgps.com

2) Shanghai Daily 12Jul, Logistics road remains bumpy for domestic refrigerated deliveries

3) Standard Chartered - The Guide to Supply Chain Manegement and Logistics 2006 / 2007

Infrastructure

Railway

Rail routes are lacking in certain regions, e.g. between Guangdong and Fujian

Limited TC-related train, almost 8,000, accounting for 2%, with outmoded fresh-keeping carriage 1)

Road

Lack of a less-than-truck-load (LTL) system with broad reach

40,000 backward refrigerator vans in 2000, accounting for 0.3% of its total freight cars 2)

Facilities

Warehouse

Most of the refrigerated warehouses date from the 1950s and 1960s

Old-fashioned and full of difficulty providing different storage temperatures

Fragmented located with obsolete equipment and technology

Logistics center

Mono-functional playing role mainly as warehousing or cross docking

Inadequate management information system

Regulation Large gaps between central government policy and local practices

Food safety standards and regulations in cold chain logistics are still empty

Local protectionism and complicated licensing

Technology Some improvements in recent years but lag large behind western countries

Packing technology and standards in cold chain have not well developed

Operation &

Management

Out-of-date cold chain management and lack of TC-related training in relation to Ops

By 2010, China will need 400,000 supply chain and logistics professionals of junior

college level or above 3)

Current market condition and regulatory landscape show us

challenges in all sectors to overcome in coming years.

9Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Major Growth Trends - General Overview Rapid economic growth The Chinese economy has grown by over 9% annually in recent years. And growth rate in the logistics sector were even

higher while the infrastructure conditions, along with the lack of logistics know-how remain the very important challenges which China is facing

Increasing domestic consumption The per capita income in China is rapidly approaching USD 7500, which is the threshold for strong cold-chain demand In recent years, with the rapid growth of China’s middle class, estimated to be approaching 150 million Great potential in domestic consumption 1)

WTO entry and foreign investments After the entry of WTO in 2001, more market opened and deregulated policies attracted huge foreign investments More and more MNCs set foot in China’s market At the same time, international standard for cold chain is heating up

Rising expectation of safe and better quality products According to several recent studies, products safety is one of the hottest topic and a public concern in China’s big cities Government makes efforts to improve the situation and ensure product safety such as food and medical partly due to

upcoming events of Beijing 2008 Olympics and Shanghai exhibition in 2010

Outsourcing service remain strong and professional cold chain logistics companies emerge 60% of manufacturing companies will choose outsourcing their logistics activities in China, including temp-control

services 2)

T&L outsourcing in China is expected to grow at 22% per year to reach 178.4 billion RMB by 2008 3)

This trend provides opportunities to develop China’s local 3PLs in cold chain logistics industry

1) BNP Paribas 2) Research result from Mercer Consulting and China Logistics Alliance Network

3) AT Kearney – Outsourced Logistics Market Outlook, 1998-2008

Increasing demands and higher requirements in TC market will

make it alluring for all pioneers.

10Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

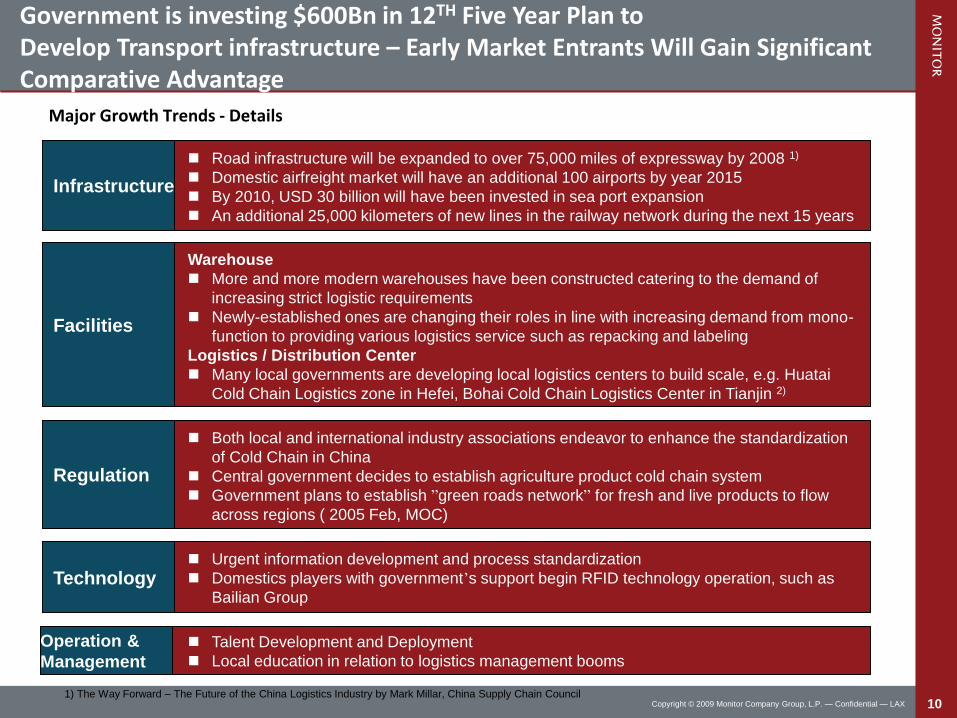

Major Growth Trends - Details

Infrastructure

Road infrastructure will be expanded to over 75,000 miles of expressway by 2008 1)

Domestic airfreight market will have an additional 100 airports by year 2015

By 2010, USD 30 billion will have been invested in sea port expansion

An additional 25,000 kilometers of new lines in the railway network during the next 15 years

Facilities

Warehouse

More and more modern warehouses have been constructed catering to the demand of

increasing strict logistic requirements

Newly-established ones are changing their roles in line with increasing demand from mono-

function to providing various logistics service such as repacking and labeling

Logistics / Distribution Center

Many local governments are developing local logistics centers to build scale, e.g. Huatai

Cold Chain Logistics zone in Hefei, Bohai Cold Chain Logistics Center in Tianjin 2)

Regulation

Both local and international industry associations endeavor to enhance the standardization

of Cold Chain in China

Central government decides to establish agriculture product cold chain system

Government plans to establish ”green roads network” for fresh and live products to flow

across regions ( 2005 Feb, MOC)

Technology Urgent information development and process standardization

Domestics players with government’s support begin RFID technology operation, such as

Bailian Group

Operation &

Management Talent Development and Deployment

Local education in relation to logistics management booms

Government is investing $600Bn in 12TH Five Year Plan to Develop Transport infrastructure – Early Market Entrants Will Gain Significant Comparative Advantage

1) The Way Forward – The Future of the China Logistics Industry by Mark Millar, China Supply Chain Council

11Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Agenda

Executive Summary

China TC Market Overview & Growth Trends

Global Competitors & Local Players

TC Market Rationale & Proposed Initiatives

TC Market Breakdown & Target Industry Segments

Financial Impacts & Initiative Requirements

Implementation Plan & Risk Assessment

Next Steps & Decision Needs

12Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

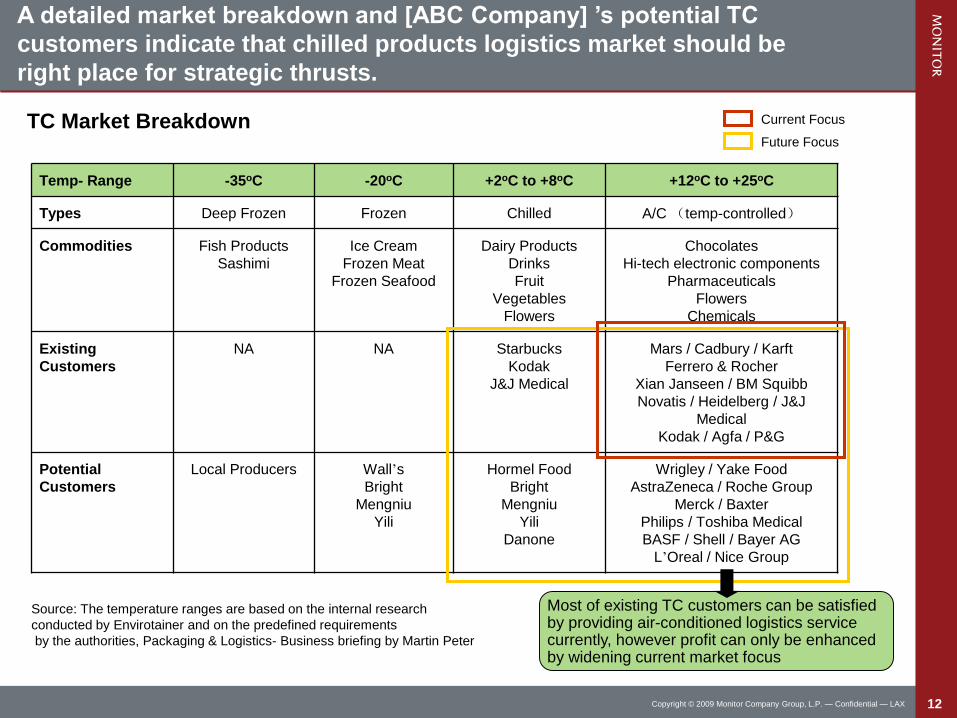

TC Market Breakdown

Temp- Range -35oC -20oC +2oC to +8oC +12oC to +25oC

Types Deep Frozen Frozen Chilled A/C (temp-controlled)

Commodities Fish Products

Sashimi

Ice Cream

Frozen Meat

Frozen Seafood

Dairy Products

Drinks

Fruit

Vegetables

Flowers

Chocolates

Hi-tech electronic components

Pharmaceuticals

Flowers

Chemicals

Existing

Customers

NA NA Starbucks

Kodak

J&J Medical

Mars / Cadbury / Karft

Ferrero & Rocher

Xian Janseen / BM Squibb

Novatis / Heidelberg / J&J

Medical

Kodak / Agfa / P&G

Potential

Customers

Local Producers Wall’s

Bright

Mengniu

Yili

Hormel Food

Bright

Mengniu

Yili

Danone

Wrigley / Yake Food

AstraZeneca / Roche Group

Merck / Baxter

Philips / Toshiba Medical

BASF / Shell / Bayer AG

L’Oreal / Nice Group

Source: The temperature ranges are based on the internal research

conducted by Envirotainer and on the predefined requirements

by the authorities, Packaging & Logistics- Business briefing by Martin Peter

Current Focus

Most of existing TC customers can be satisfied by providing air-conditioned logistics service currently, however profit can only be enhanced by widening current market focus

A detailed market breakdown and [ABC Company] ’s potential TC

customers indicate that chilled products logistics market should be

right place for strategic thrusts.

Future Focus

13Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Target Industry Sub SegmentsFood:Candy & Chocolate with 12% CAGR and Quick-frozen Product segments show good reason for [ABC Company] to invest heavily.

Source: National Bureau of Statistics of China & others refer to Appendix

Segment [ABC Company] riptionExisting Customers

Potential Customers

Meat ProductMore than 2,500 factories produce 58 million tons of meat products in 2004 with the figure increasing each year at a rate of 5%

NAYurun Food GroupHormel Food

Aquatic productAnnual output 49 million tons in 2009, 4% CAGR70% of total production provided to worldwide consumers

NA Local Producers

Cold Drink

About 4,000 cold drink producers with a 1.6 million tons output in 2003, consumption estimated to reach 2.6 million tons by 2010, 7% CAGRTurnover reached 0.9 billion CNY in 2002

Starbucks

Wall’sBrightMengniuYili

Dairy Product

More than 1,500 dairy industry factories28.3 million tons of raw milk in 2005 with an annual increase of about 25 percentTotal market value increased to RMB 85.5 billion by 2005

NA

DanoneBrightMengniuYili

Candy & Chocolate

Almost 5,000 local players remain besides limited foreign competitorOutput 1.28 million tons, turnover 20 billion CNY in 200512% CAGR

MarsCadburyKarftFerrero & Rocher

MeijiWrigleyYake Food

Fruit & Vegetable

More than 1534 million ton in 2004The 1st producer in the worldConsumption is booming in recent years

NA Local Producers

Quick-frozen Product

More than 1000 manufacturers with total sales over 10 billion An output of 8.5 million tons in 2004, 10% CAGR

NAWanzaimatouSanquanSinian

14Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

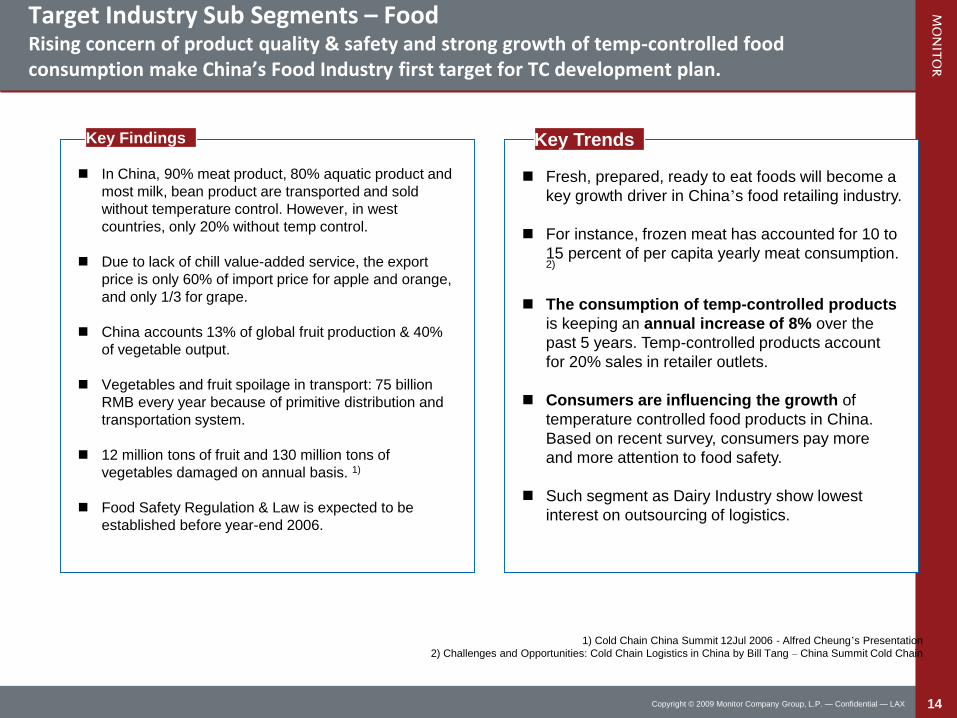

Target Industry Sub Segments – FoodRising concern of product quality & safety and strong growth of temp-controlled foodconsumption make China’s Food Industry first target for TC development plan.

In China, 90% meat product, 80% aquatic product and

most milk, bean product are transported and sold

without temperature control. However, in west

countries, only 20% without temp control.

Due to lack of chill value-added service, the export

price is only 60% of import price for apple and orange,

and only 1/3 for grape.

China accounts 13% of global fruit production & 40%

of vegetable output.

Vegetables and fruit spoilage in transport: 75 billion

RMB every year because of primitive distribution and

transportation system.

12 million tons of fruit and 130 million tons of

vegetables damaged on annual basis. 1)

Food Safety Regulation & Law is expected to be

established before year-end 2006.

Key Findings

Fresh, prepared, ready to eat foods will become a

key growth driver in China’s food retailing industry.

For instance, frozen meat has accounted for 10 to

15 percent of per capita yearly meat consumption. 2)

The consumption of temp-controlled products

is keeping an annual increase of 8% over the

past 5 years. Temp-controlled products account

for 20% sales in retailer outlets.

Consumers are influencing the growth of

temperature controlled food products in China.

Based on recent survey, consumers pay more

and more attention to food safety.

Such segment as Dairy Industry show lowest

interest on outsourcing of logistics.

Key Trends

1) Cold Chain China Summit 12Jul 2006 - Alfred Cheung’s Presentation

2) Challenges and Opportunities: Cold Chain Logistics in China by Bill Tang – China Summit Cold Chain

15Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Target Industry Sub Segments - Life SciencePharmaceuticals and medical equipment segment remain the key growing marketin China’s TC-related landscape

Segment [ABC Company] riptionExisting

Customers

Potential

Customers

Pharmaceuticals

Total sales of pharmaceuticals in China –

excluding traditional Chinese medicine (TCM) –

reached an estimated US$19.2bn in 2005

Estimated to over $24billion by 2010, as the

5th largest pharmaceutical market in the world

Xian Janseen

BM Squibb

Novatis

GSK

AstraZeneca

Roche Group

Merck

Baxter

Invitro Diagnostics

Clinical chemistry, infectious diseases,

hematology, endocrine, blood banks, drug

abuse tests

NA MNCs

Medical equipment and

devices

The total sales revenue for medical equipment

in China stood at USD 9 billion in 2003 and

will reach USD17 billion by 2008

J&J Medical

KODAK

GE

Siemens

Philips

Toshiba

Medical

Medical/Nursing/

Surgical SuppliesIV therapy, drug delivery, syringes, garments NA MNCs

Source: Datamonitor Industry Report & GCS Industry Strategy

16Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Target Industry Sub Segments - Life ScienceRegarded as High Risk and High Rewards. Heavy investment in fundamental phase would deliver highest profit in coming years

At less than USD 15, China’s annual per-capita expenditure is one of the lowest in the world.

An estimated 97% of the drugs (excluding TCMs) produced by local companies are generics or counterfeit.

Sate Food and Drug Administration of China (SFDA) was set up in 2003 to streamline the process of drug approvals and registrations.

Implementation of a Good Manufacturing Practice(GMP) policy in July 2004 immediately forced more than 1,300 non-compliant companies to stop selling their products.

Since the 1980s, hundreds of foreign pharma companies have entered China’s highly fragmented market, where the top ten players control just 15% of total industry sales.

Today, multinationals have over 600 active joint ventures in China and most global industry giants have a China presence: Johnson & Johnson, Roche, Novartis, GlaxoSmithKline.

China’s 9,000 domestic producers of medical equipment occupy the low end of the market and present little competitive threat to MNCs.

Key Findings

A fast-growing middle-class consumer segment in size and spending power and concerns over drug safety and counterfeits will drive sales of imported pharmaceuticals.

Imported medical equipments account for significant market share and will remain key dominator for quite a long time.

More and more focus on operational quality and industry knowledge required - service failure can result in death

Global players will remain dominators in high end market while M&A will continue to play a key role in competition.

More opportunities for 3PL

-demands increase for greater transparency in the system and validated, temp-controlled logistics

-mergers and acquisitions result in unnecessary, expensive duplicate warehouses

-pharma company core competencies are in research, development and sales – not supply chain

Key Trends

Source: Datamonitor & others refer to Appendix

17Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Target Industry Sub Segments – ChemicalsMost chemicals products require long term storage and special handing procedure such as DG handing, which makes market entry a costly endeavor

1) These figures only include the 22,985 state-owned and other enterprises with annual sales of over RMB 5 million. Source: Xinhua’s China Economic Information Service,

“Petroleum and chemical industry maintains leader of China’s industrial sector,” 7 July 2006

2) Datamonitor: Chemicals in China 2004 (base, consumer, pharmaceutical and speciality chemicals)

Segment [ABC Company] riptionExisting

Customers

Potential

Customers

Chemicals

Basic, intermediate, and specialty chemicals; petrochemicals;

plastic resins and materials used in synthetic fibers; and paints

and coatings

KODAK

BASF

Shell

Bayer AG

Personal Care Skin and hair care, oral care, first aid, women’s health.P&G

Unilever

L’Oreal

Nice Group

Key Findings Key TrendsChemicals

In the first 5 months of 2006 the turnover of China’s petroleum and chemical industry stood at RMB 1.57 trillion, up 31 percent from the same period in 2005. Profits rose 27 percent to RMB 178 billion. 1)

China, currently as the 4th largest chemical producer is forecasted to become the 3rd largest chemical producing country by year-end 2006.

China is also the largest importer of chemicals globally.

The production of staple petrochemical products will remain either off-limits to foreign companies or subject to ownership restrictions.

Personal care

Market value: 109.4 billion RMB in 2008=9

Cosmetic products play a primary role, 58 billion RMB in 2008.

Chemicals

A spectacular growth rate for the next 5 to 10 years, driven by intense demand from the domestic manufacturing sector. Total value US$162.4 2008. 2)

Import dependence remains a concern and will shape government policy towards the sector.

Chinese companies are also looking for outward investments and more potential for innovative forms of cooperation both inside and outside.

Personal care

Limited profit (compared with petrochemicals and plastic chemicals, etc) and more intensified competition

18Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Agenda

Executive Summary

China TC Market Overview & Growth Trends

Global Competitors & Local Players

TC Market Rationale & Proposed Initiatives

TC Market Breakdown & Target Industry Segments

Financial Impacts & Initiative Requirements

Implementation Plan & Risk Assessment

Next Steps & Decision Needs

19Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

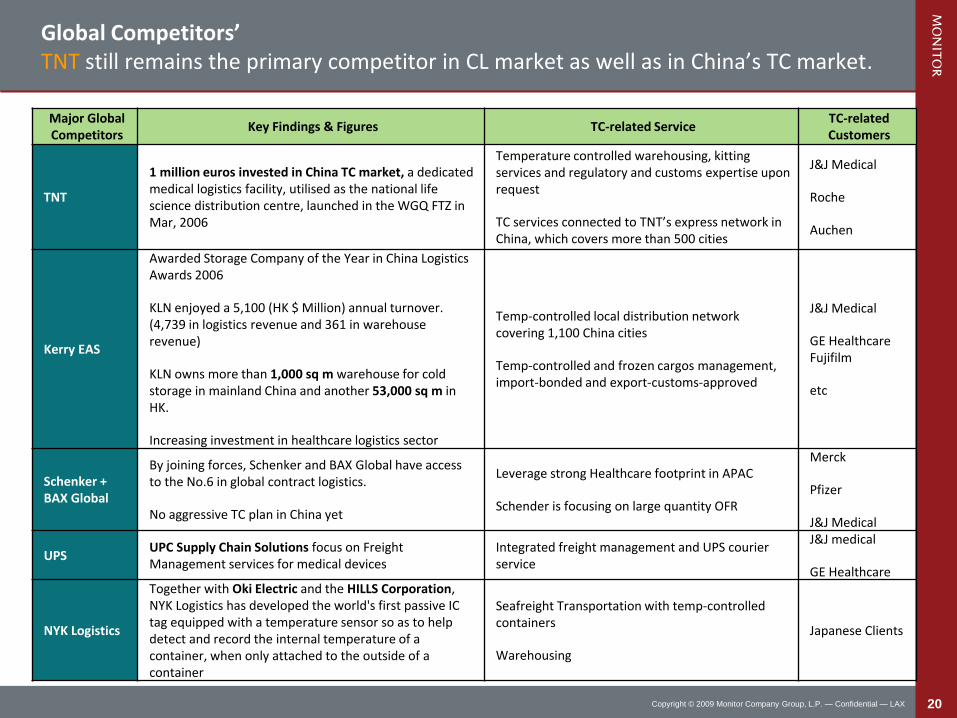

Competitor Movements - Global Players

According to our limited available data source, TNT Logistics and Kerry Logistics Network (KLN) outperform other global competitors in China TC Market nowadays.

TNT’s newly-established national life science distribution centre in SHA has turned itself into a key market player, especially in life science cold chain logistics industry.

Growing from a humble local warehouse operator in Hong Kong since 2000, KLN has grown to now a global logistics player with coverage of more than 150 cities in 16 countries and regions. Totally more than 54,000 sqm warehouse facilities for cold storage have helped KLN to widen its network even faster.

Besides, we also found some Japan-based logistics companies performed well, although their target customers limit to Japanese-related ones.

In a word, the giant players are still relatively weak in China’s local TC market with no major player staking a claim to market leadership yet. Therefore, the market is open to anyone that can develop TC capabilities despite that this takes time.

20Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Global Competitors’TNT still remains the primary competitor in CL market as well as in China’s TC market.

Major Global Competitors

Key Findings & Figures TC-related ServiceTC-related Customers

TNT

1 million euros invested in China TC market, a dedicated medical logistics facility, utilised as the national life science distribution centre, launched in the WGQ FTZ in Mar, 2006

Temperature controlled warehousing, kitting services and regulatory and customs expertise upon request

TC services connected to TNT’s express network in China, which covers more than 500 cities

J&J Medical

Roche

Auchen

Kerry EAS

Awarded Storage Company of the Year in China Logistics Awards 2006

KLN enjoyed a 5,100 (HK $ Million) annual turnover. (4,739 in logistics revenue and 361 in warehouse revenue)

KLN owns more than 1,000 sq m warehouse for cold storage in mainland China and another 53,000 sq m in HK.

Increasing investment in healthcare logistics sector

Temp-controlled local distribution network covering 1,100 China cities

Temp-controlled and frozen cargos management, import-bonded and export-customs-approved

J&J Medical

GE HealthcareFujifilm

etc

Schenker + BAX Global

By joining forces, Schenker and BAX Global have access to the No.6 in global contract logistics.

No aggressive TC plan in China yet

Leverage strong Healthcare footprint in APAC

Schender is focusing on large quantity OFR

Merck

Pfizer

J&J Medical

UPSUPC Supply Chain Solutions focus on Freight Management services for medical devices

Integrated freight management and UPS courier service

J&J medical

GE Healthcare

NYK Logistics

Together with Oki Electric and the HILLS Corporation, NYK Logistics has developed the world's first passive IC tag equipped with a temperature sensor so as to help detect and record the internal temperature of a container, when only attached to the outside of a container

Seafreight Transportation with temp-controlled containers

Warehousing

Japanese Clients

21Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Aggressive Action - Local Players

The total number of officially registered logistics service providers in China is said to be 800,000. No reliable figures for the number of unregistered carriers.

But mainly due to high-level cost and risk into cold chain logistics, there are few competitors with remarkable operation volume. Reliable data from relevant association shows that there are almost 20 local players whose cold chain storage capability is above 20,000 tons and most of the providers only possess less than 10,000 tons capabilities with old-fashioned warehouse and vans. 1)

Major Advantages of local players consist of low cost, high flexibility and adaptive to local practice.

However below-standard cold chain facilities and lack of enough talents, few domestic players have strong predominance except some state-invested cold chain logistics providers, mainly centralized in coastal cities such as SHA, BJS and CAN.

Among them, Sino-trans Yuhe Cold Chain Logistics exceeds due to its strong financial background and fast-developing players include Shanghai Xintiantian Cold Logistics Co Ltd, Shenzhen ST-Anda Logisticsand Eternal Asia Supply Chain Management Co., LTD.

Some company-owned cold chain logistics companies perform even better in TC market, such as Speed-fresh logistics under “Bright Diary” company and Shuanghui logistics under Shuanghui Group.

1) China Froze Food Network, http://www.freezefood.cn ; Shanghai Association of Refrigerated Warehouse, http://www.csarw.com

22Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Local Players’Large SOEs such as Sino-trans determined to become the leading logistics provider despite of intrinsic SOE mindset and inadequate management skills.

LocalDeveloping

PlayersKey Findings & Figures TC-related Service TC-related Customers

Sino-trans YuheCold Chain Logistics

Established in 1992More than 100 refrigerator vans ownedSino-trans will invest 3.5 billion RMB in coming 3 years so as to set up regional cold chain distribution center in SHA, BJS, CAN and other major coastal cities

Temp-controlled transportation and warehouse service

KODAKWall’sNestleDanoneAFG

Shanghai Xintiantian Cold Logistics Co Ltd,

Co-founded in 2003 by JinJiang Intl, Dazhong Transport (Group) Co Ltd and Mitsui & Co LtdAdopts the most advanced cold chain technology from JapanChina’s first professional cold logistics companyTotally more than 34,000 sqm floor area of facilities in Shanghai with a total food storage capacity of 1.38 million tons38 refrigerator vans owned

Service scope covering multi-temperature warehousingDistribution specialized in Shanghai and East ChinaValue added service as picking & packing etc

MetroASHAHI DENKAChristineMARUBNI

Shenzhen ST-Anda Logistics

Formed in 1995 as JV with Singapore-based SembCorp Logistics32 Facilities, totally 250,000 sq m located in China including limited warehouse room for cold storage

WarehousingDomestic Transportation

J&J Medical Kraft / Lianhua Supermarket Enwei PharmWyethXi’an Janssen

Eternal Asia Supply Chain Management Co., LTD

Founded in 1997 in ShenzhenLogistics network cover more than 200 cities in China8 DC owned including about 1,000 sq m refrigerated roomAmong its 400 clients, many of them are in IT industriesStrong attention to expand its service to other industries including TC market development

WarehousingDomestic Transportation

NA

Note: Local Players List includes Large SOEs, local and JV players

Source: company website & limited online news release

23Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

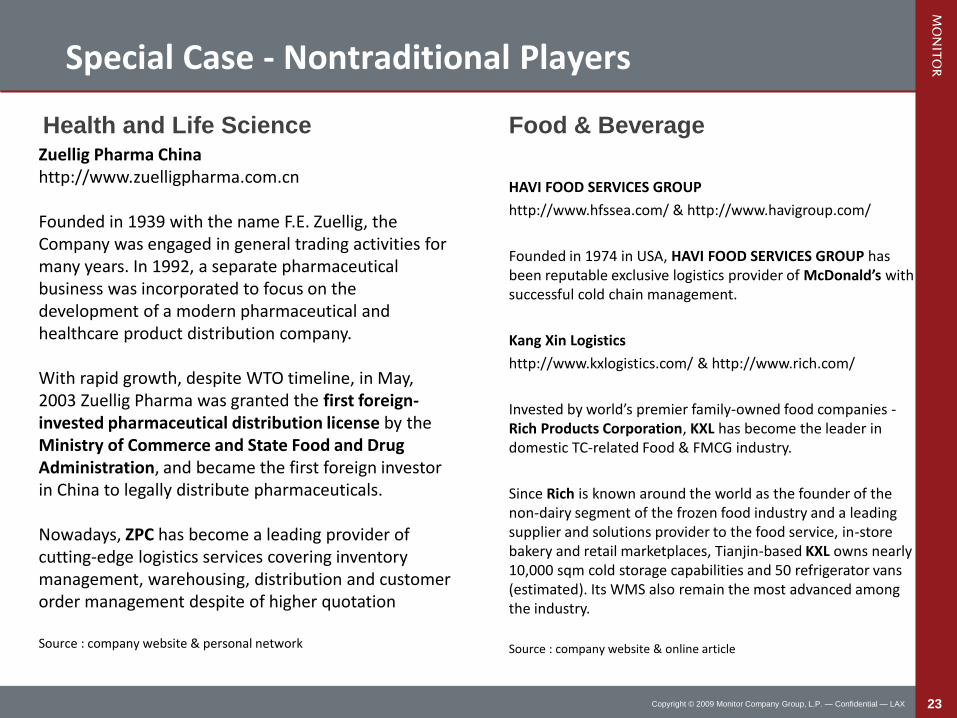

Special Case - Nontraditional Players

Zuellig Pharma Chinahttp://www.zuelligpharma.com.cn

Founded in 1939 with the name F.E. Zuellig, the Company was engaged in general trading activities for many years. In 1992, a separate pharmaceutical business was incorporated to focus on the development of a modern pharmaceutical and healthcare product distribution company.

With rapid growth, despite WTO timeline, in May, 2003 Zuellig Pharma was granted the first foreign-invested pharmaceutical distribution license by the Ministry of Commerce and State Food and Drug Administration, and became the first foreign investor in China to legally distribute pharmaceuticals.

Nowadays, ZPC has become a leading provider of cutting-edge logistics services covering inventory management, warehousing, distribution and customer order management despite of higher quotation

Source : company website & personal network

HAVI FOOD SERVICES GROUP

http://www.hfssea.com/ & http://www.havigroup.com/

Founded in 1974 in USA, HAVI FOOD SERVICES GROUP has been reputable exclusive logistics provider of McDonald’s with successful cold chain management.

Kang Xin Logistics

http://www.kxlogistics.com/ & http://www.rich.com/

Invested by world’s premier family-owned food companies -Rich Products Corporation, KXL has become the leader in domestic TC-related Food & FMCG industry.

Since Rich is known around the world as the founder of the non-dairy segment of the frozen food industry and a leading supplier and solutions provider to the food service, in-store bakery and retail marketplaces, Tianjin-based KXL owns nearly 10,000 sqm cold storage capabilities and 50 refrigerator vans (estimated). Its WMS also remain the most advanced among the industry.

Source : company website & online article

Health and Life Science Food & Beverage

24Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Agenda

Executive Summary

China TC Market Overview & Growth Trends

Global Competitors & Local Players

TC Market Rationale & Proposed Initiatives

TC Market Breakdown & Target Industry Segments

Financial Impacts & Initiative Requirements

Implementation Plan & Risk Assessment

Next Steps & Decision Needs

25Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

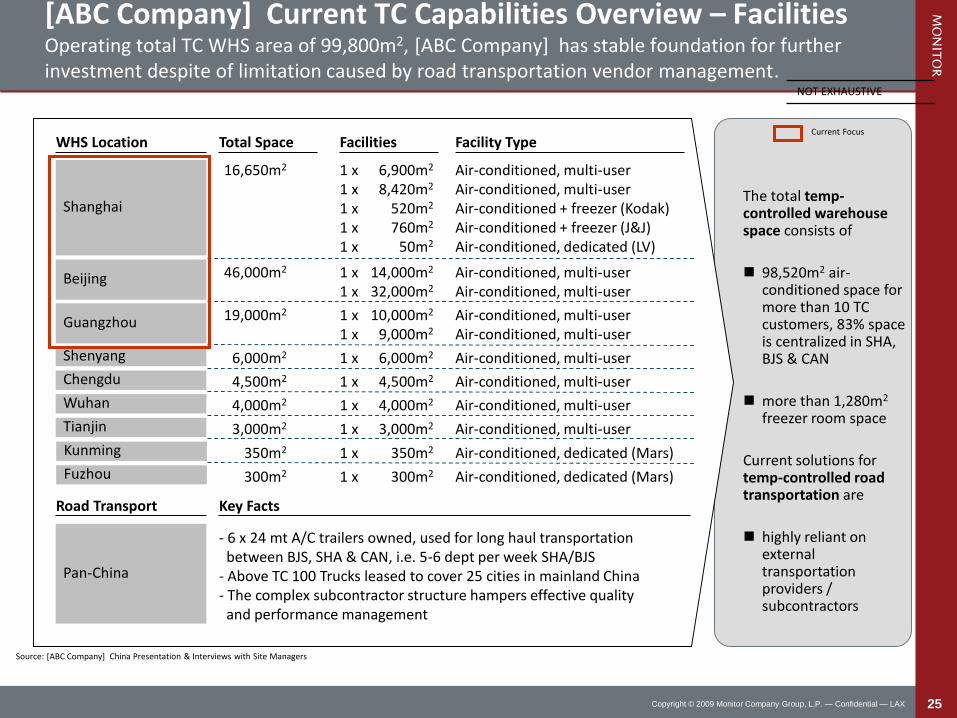

[ABC Company] Current TC Capabilities Overview – FacilitiesOperating total TC WHS area of 99,800m2, [ABC Company] has stable foundation for furtherinvestment despite of limitation caused by road transportation vendor management.

Source: [ABC Company] China Presentation & Interviews with Site Managers

Shanghai

Air-conditioned, multi-userAir-conditioned, multi-userAir-conditioned + freezer (Kodak)Air-conditioned + freezer (J&J)Air-conditioned, dedicated (LV)

Chengdu

WHS Location Total Space Facility Type

16,650m2

Facilities

1 x 6,900m2

1 x 8,420m2

1 x 520m2

1 x 760m2

1 x 50m2

46,000m2 Air-conditioned, multi-userAir-conditioned, multi-user

1 x 14,000m2

1 x 32,000m2

19,000m2 Air-conditioned, multi-userAir-conditioned, multi-user

1 x 10,000m2

1 x 9,000m2

6,000m2 Air-conditioned, multi-user1 x 6,000m2

4,500m2 Air-conditioned, multi-user1 x 4,500m2

4,000m2 Air-conditioned, multi-user1 x 4,000m2

3,000m2 Air-conditioned, multi-user1 x 3,000m2

350m2 Air-conditioned, dedicated (Mars)1 x 350m2

300m2 Air-conditioned, dedicated (Mars)1 x 300m2

Wuhan

Tianjin

Kunming

Fuzhou

Shenyang

Beijing

Guangzhou

The total temp-controlled warehouse space consists of

98,520m2 air-conditioned space for more than 10 TC customers, 83% space is centralized in SHA, BJS & CAN

more than 1,280m2

freezer room space

Current solutions for temp-controlled road transportation are

highly reliant on external transportation providers / subcontractors

NOT EXHAUSTIVE

Road Transport Key Facts

Pan-China

- 6 x 24 mt A/C trailers owned, used for long haul transportationbetween BJS, SHA & CAN, i.e. 5-6 dept per week SHA/BJS

- Above TC 100 Trucks leased to cover 25 cities in mainland China- The complex subcontractor structure hampers effective quality

and performance management

Current Focus

26Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Existing Major TC Customers Breakdown

As complete acquisition of EAC(Mars logistics) in 1994, Mars remains the largest TC customer of [ABC Company] in China until now

Customers in Life Science Industry, i.e. J&J, Novatisindicate high potential to invest heavily

By 2012, the total revenue is forecasted to double

Current key customers are Mars, Cadbury, Ferrero Rocher, Starbucks, Kraft, Xian-Janssen, BM Squibb, Novatis, J&J Medical and Kodak. Total revenue reached 144 million CNY in 2005 and is expected to exceed 300 million CNY by 2010.

85% - 90% of total TC-related revenue generated by WHS operation and road transportation in relation to customers mentioned above.

Source: [ABC Company] China Presentation and attachable financial data from ops supervisors

Kodak

J&J Medical

Novatis

BM Squibb

Xian Janseen

Karft

Cadbury

Starbucks

Mars

5.5%

13.6%

14%

14%

14%

12%

12%

7%

12%

CAGR

2005 act. 2006 . 2010 est.

[ABC Company] TC Customers’ Revenue 2005 - 2010

estimate in CNY mn]

144.4

191.5

214.3

239.9

268.6

300.1

27Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

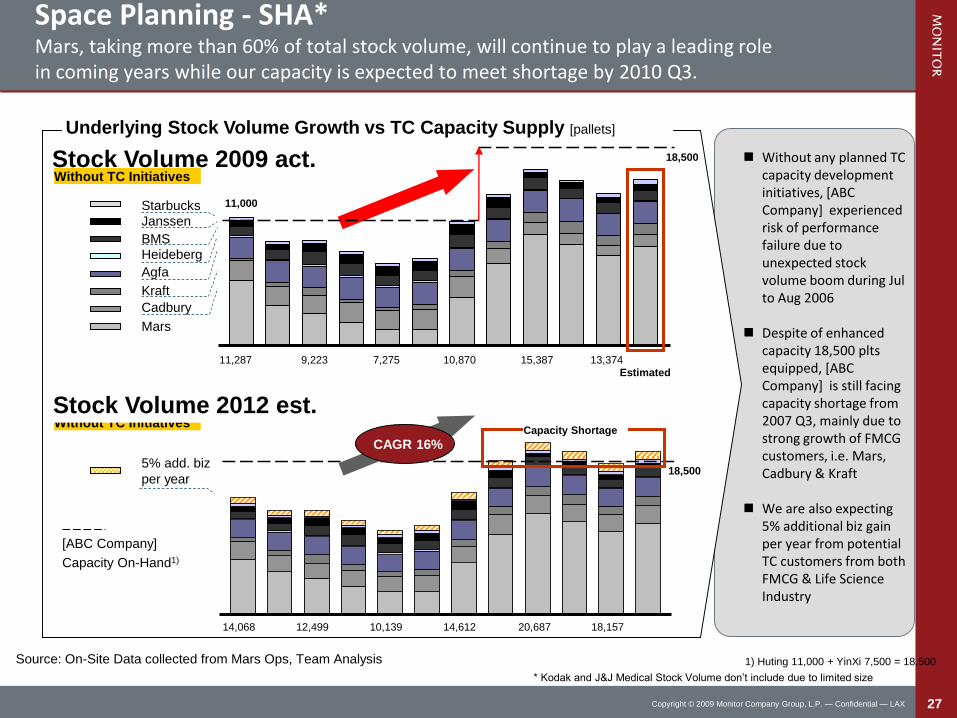

Space Planning - SHA*Mars, taking more than 60% of total stock volume, will continue to play a leading rolein coming years while our capacity is expected to meet shortage by 2010 Q3.

Without any planned TC capacity development initiatives, [ABC Company] experienced risk of performance failure due to unexpected stock volume boom during Jul to Aug 2006

Despite of enhanced capacity 18,500 pltsequipped, [ABC Company] is still facing capacity shortage from 2007 Q3, mainly due to strong growth of FMCGcustomers, i.e. Mars, Cadbury & Kraft

We are also expecting 5% additional biz gain per year from potential TC customers from both FMCG & Life Science Industry

Source: On-Site Data collected from Mars Ops, Team Analysis 1) Huting 11,000 + YinXi 7,500 = 18,500

Stock Volume 2009 act. Without TC Initiatives

Underlying Stock Volume Growth vs TC Capacity Supply [pallets]

18,500

11,000Starbucks

Janssen

BMSHeideberg

Agfa

Kraft

Cadbury

Mars

Estimated

11,287 9,223 7,275 10,870 15,387 13,374

sizelimitedtodueincludedon’tVolumeStockMedicalJ&JandKodak*

Without TC InitiativesStock Volume 2012 est.

CAGR 16%

[ABC Company]

Capacity On-Hand1)

5% add. biz

per year

14,068 12,499 10,139 14,612 20,687 18,157

18,500

Capacity Shortage

28Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

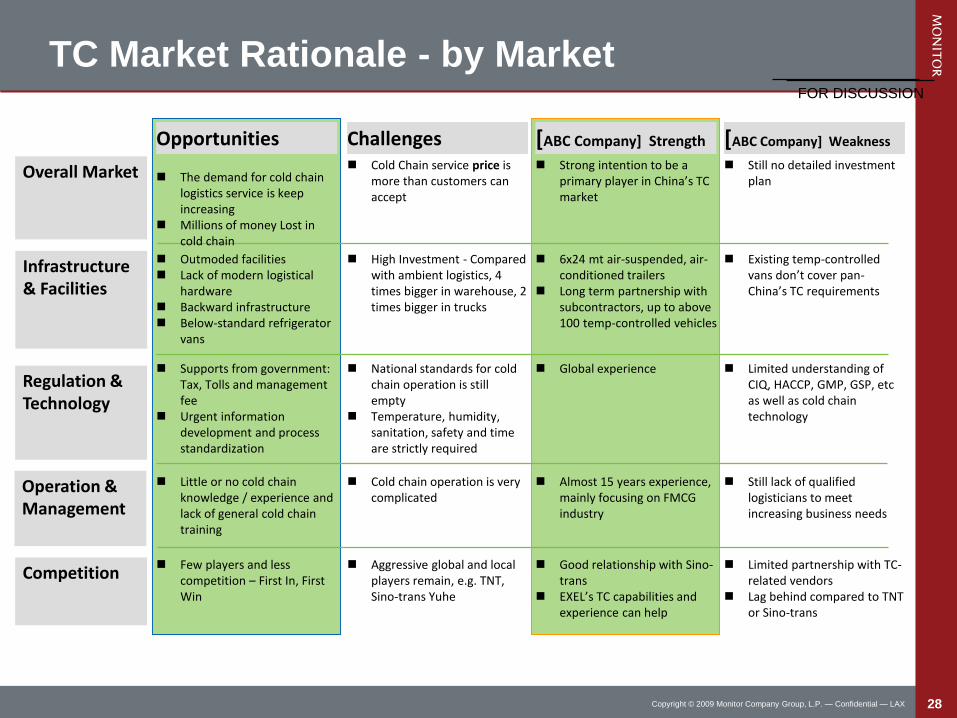

TC Market Rationale - by Market FOR DISCUSSION

Opportunities [ABC Company] Strength [ABC Company] Weakness

Overall Market

Regulation & Technology

Competition

Infrastructure & Facilities

Operation & Management

Challenges

The demand for cold chain logistics service is keep increasing

Millions of money Lost in cold chain

Cold Chain service price is more than customers can accept

Strong intention to be a primary player in China’s TC market

Still no detailed investment plan

Outmoded facilities Lack of modern logistical

hardware Backward infrastructure Below-standard refrigerator

vans

High Investment - Compared with ambient logistics, 4 times bigger in warehouse, 2 times bigger in trucks

6x24 mt air-suspended, air-conditioned trailers

Long term partnership with subcontractors, up to above 100 temp-controlled vehicles

Existing temp-controlled vans don’t cover pan-China’s TC requirements

Supports from government: Tax, Tolls and management fee

Urgent information development and process standardization

National standards for cold chain operation is still empty

Temperature, humidity, sanitation, safety and time are strictly required

Global experience Limited understanding of CIQ, HACCP, GMP, GSP, etc as well as cold chain technology

Little or no cold chain knowledge / experience and lack of general cold chain training

Cold chain operation is very complicated

Almost 15 years experience, mainly focusing on FMCG industry

Still lack of qualified logisticians to meet increasing business needs

Few players and less competition – First In, First Win

Aggressive global and local players remain, e.g. TNT, Sino-trans Yuhe

Good relationship with Sino-trans

EXEL’s TC capabilities and experience can help

Limited partnership with TC-related vendors

Lag behind compared to TNT or Sino-trans

29Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

TC Market RationalFocus on Life Science and keep primary advantage in TC-related Food Industry;Develop chemicals sub segment strategy and domestic cut flower logistics market.

FOR DISCUSSION

Opportunities [Strength Weakness

Food

Chemicals

Life Science

Flower

Challenges

Booming domestic consumption and urgent need to improve food safety and quality

Such segment as Dairy Industry show low interest on outsourcing of logistics

Local players with lower price play a primary role currently

Almost 15 years experience

Especially in candy & chocolate segment industry

Good relationship with local partners

Limited capabilities and validated, temp-controlled WHS facilities restrict us from strengthening our services to existing customers as well as developing new business

Booming domestic and global consumption

Global industry giants play a key role, while most of them are GCS customers

Strong intention to outsource logistics ops

Strict regulatory requirements from GMPand SFDA

Huge competition from global and local players

Almost 10 years experience commenced from relationship with Xian Janseen

Ditto

Booming domestic and global consumption

Dangerous goodshandling are strictly required as well as time and temperature sensitive products

Global experience in relation to handling low-DG and chemical goods

segment, i.e. P&G

Ditto

Booming domestic and global consumption

Pre-cooling services and transportation monitoring services are required

No qualified freight cars for flowers transportation until now

EXEL’s strong presence in perishables logistics handling focusing on air export biz

Ditto

30Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Proposed Initiatives - BTS temp-controlled facility (1/2)

No. DeveloperProposed

Site Location

Rental RateProperty

Management Fee

Lease Commencement Date

Lease Term

(Fixed + Optional)

Rental ReviewBuilding Standard

Comments from Property

1

Macquarie Goodman

Kangqiao, Current BTS facility

RMB 1.54/sqm.day( equivalent rate for 9m height building, or RMB1.72/sqm.day for a 12.5m high building same as current BTS facility)

To be agreed on open book format

Practical completion date of Aug 31st, 2007

10 + 10 years

3.5% fixed annual increase.

Steel portal frame + metal cladding.

Good solution, but the rental is higher than our expectation.

2Kangqiao, Phase II Land

RMB 1.2 ~ 1.4/sqm.day

Ditto Ditto Ditto Ditto Ditto

The location is just next to current Kangqiao BTS, which is only couple of kilometers away from A20 (outer ring road). Transportation to PVG, Hongqiao airport, Waigaoqiao, Yangshan etc is convenient (no toll gate except to Linggang). Rental is cheaper.

3 AMBShining, Fengxian

RMB1.625/sqm.day

RMB 1.80/sqm.mth(RMB 0.06/sqm.day)

Oct. 1st, 2007

10 + 5 Years

In an upward only direction to 'open market rental value'.

Steel portal frame + metal cladding.

It is located in the current Shining RDC, which is good for synergy of operations. Transportation is good, but the toll gate fee of the high way (A4) to the facility might be a concern. The rental is relatively higher.

Source: Proposals Summary for TC Facility by Jack Yang

31Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Proposed Initiatives - BTS temp-controlled facility (2/2)

No. DeveloperProposed

Site LocationRental Rate

Property

Manageme

nt Fee

Lease Commencement Date

Lease Term(Fixed +

Optional)Rental Review Building Standard

Comments from Property

5

Prologis

Prologis Park, Songjiang

Year 1 ~ 3, RMB1.388/sqm.day;Year 4 ~ 6, RMB1.483/sqm.day;Year 7 ~ 9, RMB1.588/sqm.day;Year 10, RMB1.702/sqm.day

RMB 2.13/sqm.mth (RMB 0.07/sqm.day)

10 months following signing off lease agreement

10 years

10% escalation every 3 years, as shown in 'rental rate'.

Ditto Location is not ideal.

6Prologis Park, Jiading

Year 1 ~ 3, RMB 1.381/sqm.day;Year 4 ~ 6, RMB 1.475/sqm.day;Year 7 ~ 9, RMB 1.577/sqm.day;Year 10, RMB 1.690/sqm.day

Ditto Ditto Ditto Ditto Ditto Ditto

7 GazeleyJunchoLogistics Park, Jiading

RMB 2.05/sqm.day

NA

Base building completion in 20 weeks after planning permission.

10 yearsFixed rate for 10 years.

Steel portal frame + metal cladding.

Location is not ideal. Rental is high.

Source: Proposals Summary for TC Facility by Jack Yang

32Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

32

Agenda

Executive Summary

China TC Market Overview & Growth Trends

Global Competitors & Local Players

TC Market Rationale & Proposed Initiatives

TC Market Breakdown & Target Industry Segments

Financial Impacts & Initiative Requirements

Implementation Plan & Risk Assessment

Next Steps & Decision Needs

33Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

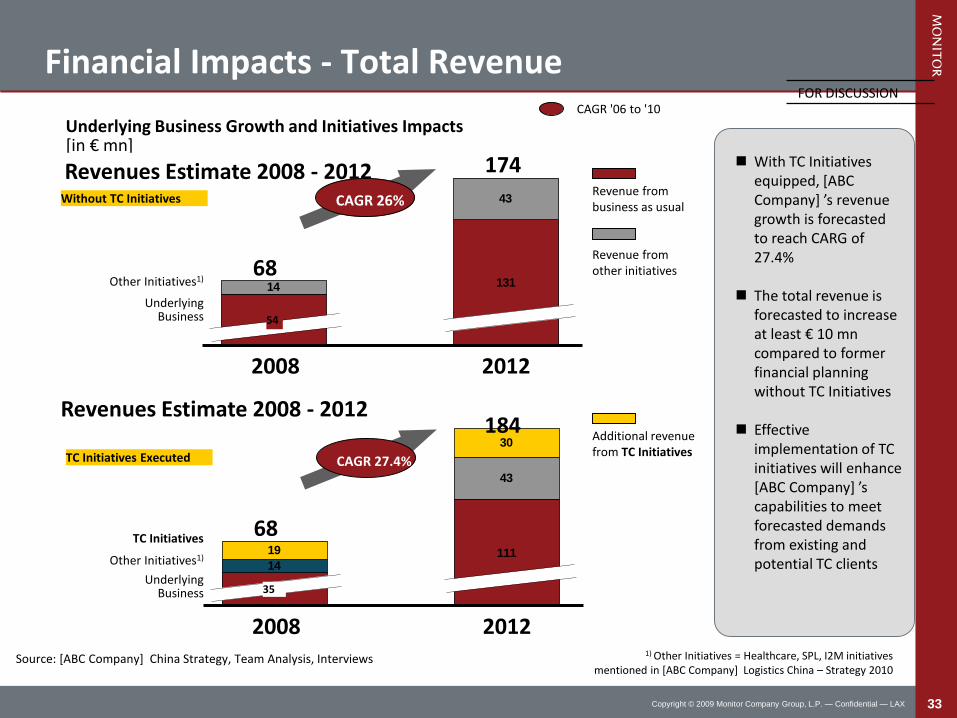

Financial Impacts - Total Revenue

With TC Initiatives equipped, [ABC Company] ’s revenue growth is forecasted to reach CARG of 27.4%

The total revenue is forecasted to increase at least € 10 mncompared to former financial planning without TC Initiatives

Effective implementation of TC initiatives will enhance [ABC Company] ’s capabilities to meet forecasted demands from existing and potential TC clients

Source: [ABC Company] China Strategy, Team Analysis, Interviews

Underlying Business Growth and Initiatives Impacts[in € mn]

Revenues Estimate 2008 - 2012

54

13114

43

2012

UnderlyingBusiness

Other Initiatives1)68

2008

174

CAGR 26%

54

Without TC Initiatives

35

11114

43

19

30

2012

UnderlyingBusiness

Other Initiatives1)

TC Initiatives68

2008

184

CAGR 27.4%

35

TC Initiatives Executed

Revenues Estimate 2008 - 2012

CAGR '06 to '10

Revenue from business as usual

Additional revenue from TC Initiatives

Revenue from other initiatives

FOR DISCUSSION

1) Other Initiatives = Healthcare, SPL, I2M initiativesmentioned in [ABC Company] Logistics China – Strategy 2010

34Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

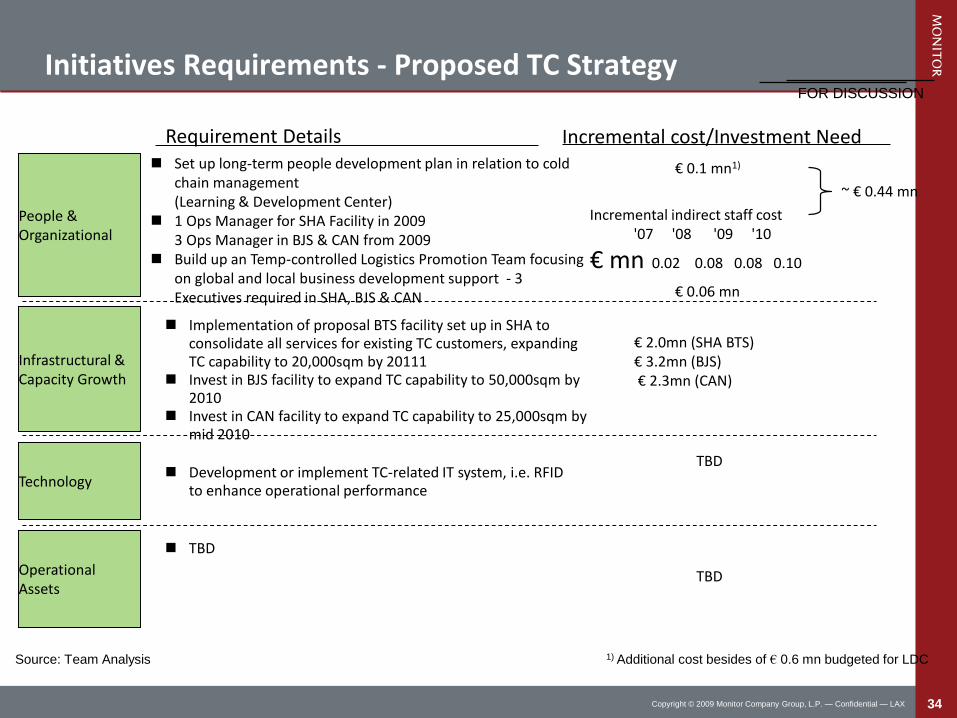

Initiatives Requirements - Proposed TC Strategy

People &Organizational

Infrastructural &Capacity Growth

Set up long-term people development plan in relation to cold chain management (Learning & Development Center)

1 Ops Manager for SHA Facility in 20093 Ops Manager in BJS & CAN from 2009

Build up an Temp-controlled Logistics Promotion Team focusing on global and local business development support - 3 Executives required in SHA, BJS & CAN

Technology Development or implement TC-related IT system, i.e. RFID

to enhance operational performance

OperationalAssets

TBD

€ 2.0mn (SHA BTS)€ 3.2mn (BJS)€ 2.3mn (CAN)

Requirement Details Incremental cost/Investment Need

€ 0.1 mn1)

€ 0.06 mn

Source: Team Analysis 1) Additional cost besides of € 0.6 mn budgeted for LDC

Implementation of proposal BTS facility set up in SHA to consolidate all services for existing TC customers, expanding TC capability to 20,000sqm by 20111

Invest in BJS facility to expand TC capability to 50,000sqm by 2010

Invest in CAN facility to expand TC capability to 25,000sqm by mid 2010

FOR DISCUSSION

TBD

TBD

Incremental indirect staff cost'07 '08 '09 '10

€ mn 0.02 0.08 0.08 0.10

~ € 0.44 mn

35Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

35

Agenda

Executive Summary

China TC Market Overview & Growth Trends

Global Competitors & Local Players

TC Market Rationale & Proposed Initiatives

TC Market Breakdown & Target Industry Segments

Financial Impacts & Initiative Requirements

Implementation Plan & Risk Assessment

Next Steps & Decision Needs

36Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Implementation Plan & Potential Risks - TC InitiativesLaunching of multi-user TC Facilities and recruitment of local talents who are experienced in TC market are our upcoming main focus.

2010 2011 2012 2013

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2014

Q1 Q2 Q3 Q4

Mu

lti-

us

er

TC

Fa

cil

itie

sP

eo

ple

& O

rga

niz

ati

on

TB

D

TBD

Responsible

TBD

TBD

TBD

Action

Roll-out TC facility - SHA

Roll-out TC facility - BJS

Roll-out TC facility - CAN

DG1)/WW1)

DG/WW

DG/WW

Recruitment& Training Team Development, Knowledge Improvement

Go-Live

Go-Live

Go-LiveID Planning Implementation

Risk Slowdown in business outsourcing and/or loss of minor accounts Delay in construction of multi-user TC Facility Operational problems due to lack of qualified ops managers and knowledge in relation

to cold chain management High operating cost due to regulatory alteration, especially in FMCG industry

Approval

Source: Team Analysis 1) DG: Desmond Gay, WW: Windy Wu

Approval

Planning

PlanningID

Approval

Implementation

Implementation

ID

Develop detailed learning & development plan

Build up Temp-controlled Logistics Promotion Team

Planning

Roll-out Cold Chain Management Knowledge ChampionID

37Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

37

Agenda

Executive Summary

China TC Market Overview & Growth Trends

Global Competitors & Local Players

TC Market Rationale & Proposed Initiatives

TC Market Breakdown & Target Industry Segments

Financial Impacts & Initiative Requirements

Implementation Plan & Risk Assessment

Next Steps & Decision Needs

38Copyright © 2009 Monitor Company Group, L.P. — Confidential — LAX

Decision Needs & Next Steps

Action Plan Responsibility Due date

Develop implementation organisation TBD TBD

Develop detailed implementation plan TBD TBD

Next Steps

Confirm China TC Development Plan

Sign-off of investment needs

Approval of headcount increase

I

II

Decisions