2009 Commercial Space & Business Parks Guide

20

SPONSORED BY COMMERCIAL SPACE & BUSINESS PARKS GUIDE 2009

-

Upload

sc-biz-news -

Category

Documents

-

view

214 -

download

1

description

The 2009 Commercial Space & Business Parks Guide offers a comprehensive look at the region’s commercial real estate market.

Transcript of 2009 Commercial Space & Business Parks Guide

SPONSORED BY

COMMERCIAL SPACE &

BUSINESS PARKS GUIDE

2009

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE 3

Dear Readers,I am proud to present the 2009 Commercial Space & Business Parks Guide. Inside you’ll fi nd a wealth of

information presented in our statistics and lists, along with the featured properties, that we hope will provide

you with a useful commercial real estate decision-making tool.

We all know the real estate market ebbs and fl ows. And of late, there has been

more ebbing than fl owing. But this publication reminds me of the great opportuni-

ties for economic development that exist right here in the Charleston region. We not

only have desirable offi ce space, industrial space and available land, but we also have

competitive rates, good infrastructure, a strong business community and a wonderful

quality of life. All things one must consider when relocating an existing business or

deciding where to set up shop.

Th is publication also reminds me of the great value commercial real estate agents

bring to the table through their expertise. As our business has expanded across the

state, I have realized that the advice and representation of a commercial real estate agent are vital. One of the

overlooked assets of our region is the large number of highly knowledgeable commercial real estate agents who

reside here. All of them stay current with continuing education and many have chosen to take their skills to a

higher level by qualifying as Certifi ed Commercial Investment Managers and/or for the Society of Industrial

and Offi ce Realtors. Not only do these individuals possess a high level of knowledge, they and their companies

produce a substantial volume of high quality, accurate data upon which we rely as journalists.

As the economy turns around and real estate begins to fl ow again, we know these agents will be working

with area offi cials to help keep Charleston top-of-mind among investors and to expand the region’s economic

development base.

Enjoy,

Welcome from our

Sponsors

Contents

Grady JohnsonCEO and

Group Publisher

Th e SOCIETY OF INDUSTRIAL AND

OFFICE REALTORS® is the leading professional

commercial and industrial real estate association.

SIOR® represents today’s most knowledgeable,

experienced and successful commercial real estate

brokerage specialists. Th e designation signifi es that

an individual has achieved a high level of compe-

tence and success and adheres to high professional

standards. Many corporate executives consider

the SIOR® designation a prerequisite in choosing a

service provider.

Charleston Chapter SIOR® members hold the

prestigious SIOR® designation. Th ese real estate

professionals are recognized by corporate real

estate executives, commercial real estate brokers,

agents, lenders, and other real estate professionals

as the most capable and experienced brokerage

practitioners in the market. SIOR® designees can

hold the following specialty designations: indus-

trial, offi ce, sales manager, executive manager or

advisory service. Make a name with the only name

that matters — SIOR®.

Durlach Associates is celebrating its 30th year

of developing, leasing, and managing Class A

offi ce buildings in the Charleston area. Fift een

years ago, when Charleston Regional Business

Journal was getting started, they leased offi ce space

in a building developed and managed by Dur-

lach Associates, and we were located in adjoining

offi ces. Since its inception, Charleston Regional

Business Journal has remained a leading source for

business news and information. Durlach Associ-

ates is pleased to be a sponsor of the Commercial

Space & Business Parks Guide. We look forward

to the next 30 years and to continuing to partner

with Charleston Regional Business Journal and

other great companies in the growth of business in

Charleston.

Commercial, industrial market experts cautiously optimistic ..............4

Charleston Region Offi ce and Retail Shopping Center Space .............5

Offi ce Vacancy Rate* Second Quarter 2009 .......................................5

Offi ce Market Snapshot – Charleston – Second Quarter 2009 ......... 6

Industrial Market Snapshot – Charleston – Second Quarter 2009 .... 7

Offi ce Buildings ............................................................................ 15

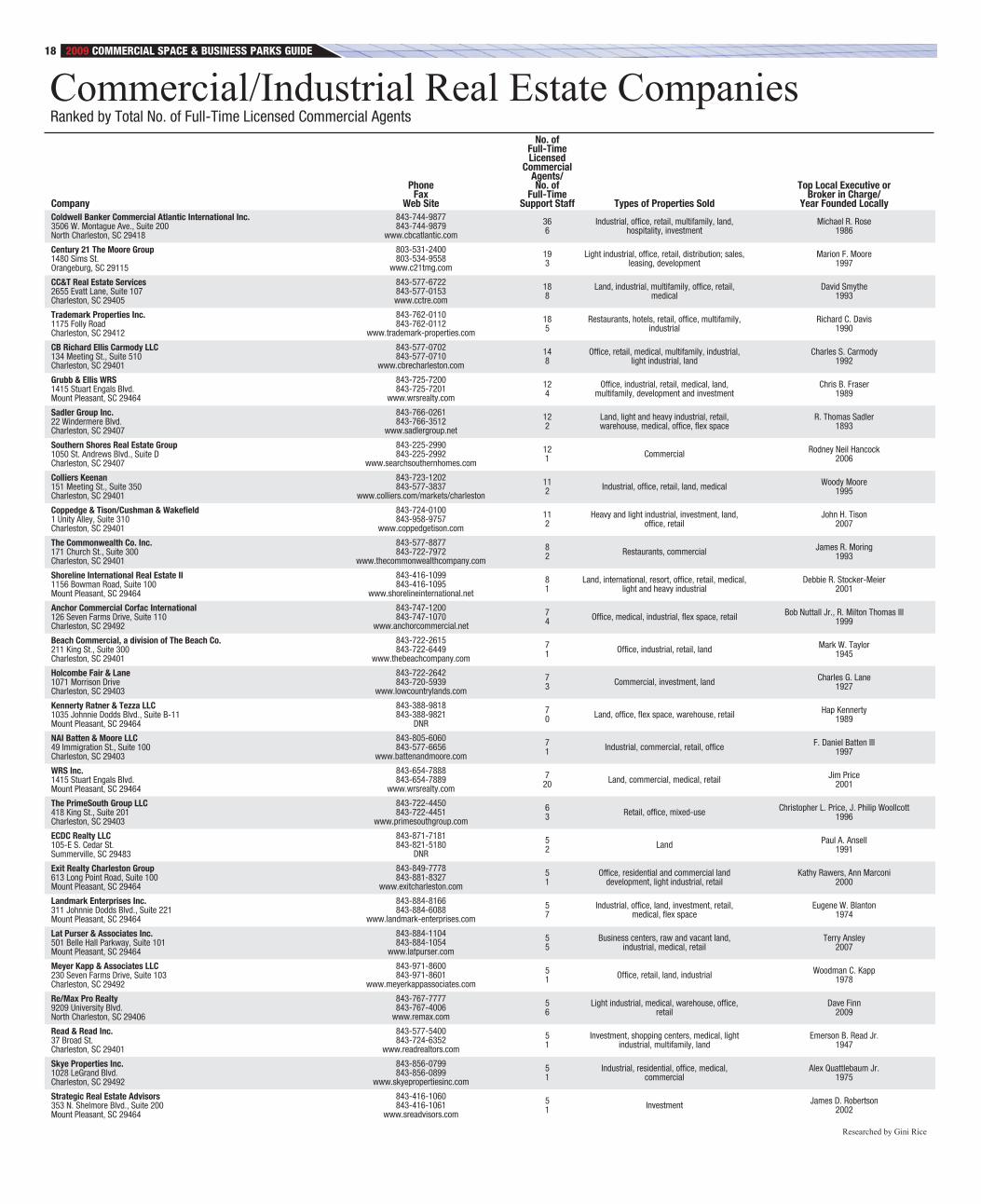

Commercial/Industrial Real Estate Companies .............................. 18

Feature PropertiesFaber Centre ....................... 8

Parkshore Centre ................ 9

SCRA Innovation Center at Charleston ......... 10

Trident Research Center ... 11

Liberty Center ................... 12

Ashley Overlook ................ 13

Two Rivers Center ............. 14

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE4

By Allison Cooke [email protected]

An increasing number of economists are saying the worst of the reces-

sion is over and the nation’s economy is on the long road to recovery.

But those in the real estate industry are still waiting to exhale.

Th ere have been signs of improvement — including a rebound in the

local housing market and a 1.4% drop in industrial property vacancies

— but the market as a whole remains uncertain, and consumers remain

cautious.

Hunkered downMore than 125,000 square feet of offi ce space opened up in the Charles-

ton region in the second quarter, bringing the vacancy rate up to 21.5%.

According to the second-quarter offi ce market report released this summer

by Grubb & Ellis WRS, although vacancy rates have continued to increase,

they have done so at a slower rate.

“Th e pace has slowed, so I think people have hunkered down to try to

ride this out. It seems like the housing market is warming up, so I expect

it (the offi ce market) to rise slightly and hopefully level off ,” said Jeremy

Willits, senior vice president and principal of Grubb & Ellis WRS. “But I

Commercial, industrial market experts cautiously optimistic

don’t think we’ll see any dramatic improvement until the unemployment

rate improves.”

Th e central business district downtown proved to be the bright spot in

the offi ce market report, with “an astonishing 93% occupancy rate.”

Meanwhile, offi ce space in suburban areas has taken the hardest hit.

Vacancies on Daniel Island and in Mount Pleasant, North Charleston and

West Ashley range from 23.2%-27.4%.

Willits said many renters in suburban areas were largely tied to the real

estate industry, including real estate agents, homebuilders and closing

attorneys. As companies looked for ways to lower overhead this year, many

decided to consolidate offi ces and reduce their footprint.

To attract new offi ce tenants and keep current tenants, Willits said land-

lords in all areas are more willing to accept shorter lease terms or reduced

rental rates. In some cases, rent has dropped nearly 25%. Th e goal is to gen-

erate income in the short term while limiting the long-term commitment

to a lower rental rate.

When it comes to purchasing offi ce space, Willits said there are many

good opportunities, particularly for owners who intend to occupy a space.

“Th e buyers that are owner-occupants are the ones who are more likely to

get a loan,” he said. “Th ey can purchase now for a better price than they’ve

seen in years.”

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE 5

Industrial leasing strengthens“For the fi rst time since the peak of the market in 2007, the Charleston

industrial market has hard data to indicate a turnaround,” Grubb & Ellis

stated in its industrial market trends report for the second quarter.

Overall, Grubb & Ellis’ research shows vacancy rates in the second quar-

ter dropped from 13.8% to 12.4%. And while rates hover around 20% for

the Summerville, West Ashley and Clements Ferry/East Cooper areas, rates

for downtown, North Charleston and Berkeley County all have single-digit

vacancy rates.

“Leasing will be the main driver for the next 18 months or so,” said

Michael Ferrer, vice president of global logistics for Grubb & Ellis WRS.

“We are not seeing the same amount of fear people had in the fourth quarter

of last year or the fi rst quarter of this year.”

Th e report also noted that landlords continue to off er incentives, includ-

ing short-term leases, to keep properties occupied. But the real value is in

locking in a long-term lease.

“Th e silver lining is, if you are a successful company in the defense or

medical industry or other market that hasn’t been impacted, you can get a

good deal,” Ferrer said. “It’s a tenant’s market.”

With the amount of space available — about 4.6 million total square feet

— and the great desire to sell or rent, buyers and renters can fi nd a good

deal.

Th e best deals in purchasing industrial space occur when the buyer

intends to use the space purchases, rather than rent it out. Still, not too

many people have been motivated to buy, as Grubb & Ellis reports there

have been fewer than 11 transactions in the past 12 months.

Ferrer said that activity has greatly diminished as a result of a combina-

tion of more stringent lending requirements; a big disconnect between buy-

ers and sellers on property value; and diffi culty in securing fi nancing.

Cautiously optimisticLooking ahead, Ferrer is hopeful that things will really begin to turn

around by the end of next year.

“I think everyone is going to be cautiously optimistic,” he said. “It’s not

going to be red-hot like it was before.”

But Charleston is poised for a strong return, Ferrer continued.

“Charleston has very strong fundamentals, and this, too, shall pass,” he

said. “Charleston still has a lot going for it — great quality of life, good infra-

structure, great port and national developers with the ability to provide job

creation that we haven’t had in the past. Th ese things will have led Charles-

ton to a position where it is well-situated for the rebound.”

CHARLESTON REGION OFFICE AND RETAIL SHOPPING CENTER SPACE

* The Center for Business Research suspended its office and retail surveys from 2004-06.

Surveys resumed in 2007.

Note: Survey includes retail shopping centers larger than 30,000 square feet and office

buildings larger than 10,000 square feet in the tri-county area.

Source: Center for Business Research

Offi ce Space % Available Retail Space % Available1997 4,769,013 16.3% 11,494,631 15.0%

1998 5,130,751 12.0% 11,168,835 12.1%

1999 5,100,681 11.4% 11,354,901 10.7%

2000 5,271,948 12.5% 12,278,197 11.2%

2001 5,740,524 11.7% 12,333,817 11.8%

2002 6,548,371 16.1% 13,001,699 12.2%

2003 6,957,945 16.9% 12,683,726 10.3%

2007* 8,646,005 15.9% 14,976,315 10.0%

2008 9,881,505 17.7% 14,712,658 8.1%

OFFICE VACANCY RATE* SECOND QUARTER 2009

*All classes of space

Source: Grubb & Ellis WRS Offi ce Market Trends Charleston, Second Quarter 2009

Centra

l Bus

iness

Dist

rict

Daniel

Islan

d

Mount

Pleasa

nt

North

Charle

ston

West A

shley

25

20

15

10

5

0

6.9

27.4

24.0

25.3

23.2

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE6

2003 2004 2005 2006 2007 2008 2009

*All industrial product types

Source: Grubb & Ellis WRS Offi ce Market Trends Charleston, Second Quarter 2009

INDUSTRIAL VACANCY RATE* THROUGH SECOND QUARTER 2009

22.0%

18.0%

13.0%

9.0%8.4%

13.4% 12.4%

OFFICE MARKET SNAPSHOT – CHARLESTON – SECOND QUARTER 2009

By submarket(All classes) Total (1) SF Vacant (2) SF Vacant %

Net AbsorptionUnder Construction SF (3)

Asking Rent (4)

Current Qtr. Year-to-Date Class “A” Class “B”Downtown 1,755,436 121,538 6.9 252 263 35,000 $28.76 $23.37

CBD Total 1,755,436 121,538 6.9 252 263 35,000 $28.76 $23.37

Daniel Island 1,076,779 295,127 27.4 (49,265) (53,593) 76,120 $24.78 $22.38

Mount Pleasant 1,547,508 371,919 24 (2,633) (44,316) 22,500 $23.94 $22.75

North Charleston 3,570,318 9,047,161 25.3 (43,805) 16,100 150,000 $21.39 $20.05

West Ashley 1,096,469 254,197 23.2 (26,259) (17,816) 62,800 $23.89 $20.36

Suburban Total 7,291,074 1,825,959 25 (121,962) (99,625) 311,420 $23.20 $21.32

Totals 9,046,510 1,947,497 21.5 (121,710) (99,362) 346,420 $23.77 $21.43 (1) Inventory includes multitenant and single-tenant buildings with at least 10,000 square feet.

(2) Vacant space includes both vacant direct and vacant sublease space.

(3) Space under construction includes speculative and build-to-suit for lease projects.

(4) Asking rates are per square foot, per year, full service. Rates for each building are weighted by the size of the building.

By Class (All submarkets) Total (1) SF Vacant (2) SF Vacant %

Net AbsorptionUnder Construction SF (3)

Available for SubleaseCurrent Qtr. Year-to-Date CBD Suburban

Class A 4,422,195 1,099,122 24.9 (16,855) (1,926) 346,420 – 63,000

Class B 2,179,921 357,468 16.4 (87,340) (94,765) – – 54,790

Class C 2,444,394 490,907 20.1 (17,515) (2,671) – – 12,048

Totals 9,046,510 1,947,497 21.5 (121,710) (99,362) 346,420 – 129,838

Class “A” properties are the most prestigious buildings competing for premier offi ce users with rents above average for the area. Class “B” properties compete for a wide range of users with rents in the aver-

age range for the area. Class “C” buildings compete for tenants requiring functional space at rents below the area average.

CBD = Central Business District

Source: Grubb & Ellis WRS Offi ce Market Trends Charleston, Second Quarter 2009

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE 7

Commercial and Residential Plumbing Professionals* Unlimited License *

www.crosbyplumbing.com843.284.0286

Serving the Carolinas and Georgia

Uncompromising quality. No buts about it.

newcomers guidenewcomers guidenewcomers gug ide

Committ ed to delivering you right to South Carolina’s newcomers.

Get Th ere First! Be the fi rst to introduce your products and services!

For advertising information, contact James Molnarat [email protected] or 843.849.3146

www.intronewcomersguide.com

From the publishers of

INDUSTRIAL MARKET SNAPSHOT – CHARLESTON – SECOND QUARTER 2009

By submarket(All classes) Total (1) SF Vacant (2) SF

TotalVacancy %

Net AbsorptionUnder Construction SF (3)

Asking Rent (4)

Current Qtr. Year-to-Date WH/Dist. R&D/FlexBerkeley County 6,718,590 450,215 6.7 – 129,710 – $5.74 $7.27

Downtown 2,810,406 203,860 7.3 (10,000) (10,000) – $4.22 $8.67

East Cooper 3,974,250 850,962 21.4 215,143 219,953 – $4.85 $5.50

North Charleston 17,269,400 1,626,517 9.4 241,759 95,985 39,892 $4.27 $6.52

Outside Metro AreaSummerville 5,812,077 1,373,105 23.6 81,290 70,666 60,000 $3.88 $7.20

West Ashley 764,460 139,423 18.2 – 4,000 – $4.42 $7.30

Totals 37,349,183 4,644,082 12.4 528,192 510,314 98,892 $4.41 $6.36 (1) Inventory includes multitenant and single-tenant buildings with at least 10,000 square feet.

(2) Vacant space includes both vacant direct and vacant sublease space.

(3) Space under construction includes speculative and build-to-suit for lease projects.

(4) Asking rates are per square foot, per year, triple net. Rates for each building are weighted by amount of available space within the building.

By property type Total (1) SF Vacant (2) SFTotal

Vacancy %Net Absorption

Under Construction SF (3) Asking Rent (4)Current Qtr. Year-to-DateGeneral Industrial 1,121,583 119,637 10.7 (8,000) -25,500 – $5.62

R&D/Flex 4,221,823 926,889 22 18,425 40,858 39,892 $6.36

Warehouse/Distribution 32,005,777 6,597,556 11.2 517,767 494,956 60,000 $4.41

Totals 37,349,183 4,644,082 12.4 528,192 510,314 99,892 $4.84

Industrial buildings are categorized as warehouse/distribution, general industrial and R&D/fl ex based on their physical

characteristics, including percentage of offi ce buildout, clear height, typical bay depth, typical suit size, type of loading and typical uses.

Source: Grubb & Ellis WRS Offi ce Market Trends Charleston, Second Quarter 2009

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE8

FABER CENTRE

ADDRESS: 4000 Faber Place Drive

CLASSIFICATION: Class “A+” Offi ce

PROPERTY MANAGER: Durlach Associates

AVAILABLE SQUARE FOOTAGE: Contact

Owner’s Representatives for Availabilities

YEAR DEVELOPED: 2008

DESCRIPTION: Developed by Durlach Associates and Holder Properties, Faber Centre is a modern four story Class A+ offi ce building centrally located at the intersection of I-526 and Leeds Avenue in the Executive Park at Faber Place. Faber Centre opened August 2008 and is home to lead tenants SunTrust, Centex, CIGNA, and MetLife.

TOP ASSETS: Flexible fl oor plans accommodate tenant layouts and expansion requirements up to 25,000 sq. ft. on a single fl oor. The limestone and granite lobby provides an entry appropriate for Charleston’s most successful businesses. Class A lobbies, restrooms and common areas set the tone for an exceptional business experience. Facility management by Durlach Associates.

DEVELOPER’S REPRESENTATIVE

NAME: John Durlach and Darby Siegel

PHONE: 723-2801 and 266-8601

E-MAIL: [email protected] and

WEBSITE: www.FaberCentre.com

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE 9

PARKSHORE CENTRE

ADDRESS: One Poston Road, Charleston

CLASSIFICATION: Class “A+” Offi ce

PROPERTY MANAGER: Durlach Associates

ZONING: General Offi ce

AVAILABLE SQUARE FOOTAGE: Contact

Developer’s Representative for Availabilities

PARK SIZE: 7 Acres

YEAR DEVELOPED: 1989

DESCRIPTION: Charleston’s premier offi ce environment, Parkshore Centre, offers 120,000 square feet of class A offi ces. Under 10 minutes from Charleston International Airport and downtown, Parkshore provides metropolitan convenience in a naturally wooded, beautifully landscaped setting.

TOP ASSETS: Flexible fl oor plans accommodate layouts from 1,000 to 40,000 square feet on a single fl oor. Tri-county’s most central location with direct access to I-26. Class A lobby, restrooms, and common areas. Large common conference room. On site management and leasing by Durlach Associates. Abundant parking – 5 spaces per 1,000 square feet.

DEVELOPER’S REPRESENTATIVE

NAME: John Durlach

PHONE: 843-723-2801

E-MAIL: [email protected]

WEBSITE: www.durlach.com

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE10

SCRA INNOVATION CENTER AT CHARLESTON

ADDRESS: 645 Meeting St., Charleston, SC 29403

CLASSIFICATION: Class “A” offi ce/laboratory space

PROPERTY MANAGER: South Carolina Research Authority

AVAILABLE SQUARE FOOTAGE: 25,000

YEAR DEVELOPED: 2009

DESCRIPTION: The 28,400-square-foot facility will consist of fl exible-use, multi-tenant laboratory and offi ce space supporting biopharma, biomed and biotech research and commercialization.

TOP ASSETS: Parking provided. Common reception area; receptionist provided. Common meeting rooms provided. Network access including e-mail available. Administrative offi ce assistance available. Flexible modular offi ce confi gurations. 24/7 security monitoring and police substation. Business, legal and fi nancial planning assistance on site.

DEVELOPER’S REPRESENTATIVE

NAME: Mark Mattison, CCIMPHONE: 843-720-7505E-MAIL: [email protected]

NAME: Peter Fennelly, SIOR, MCRPHONE: 843-720-7500E-MAIL: [email protected]

WEB SITE: www.scra.org/scra_innovationacenters.shtml

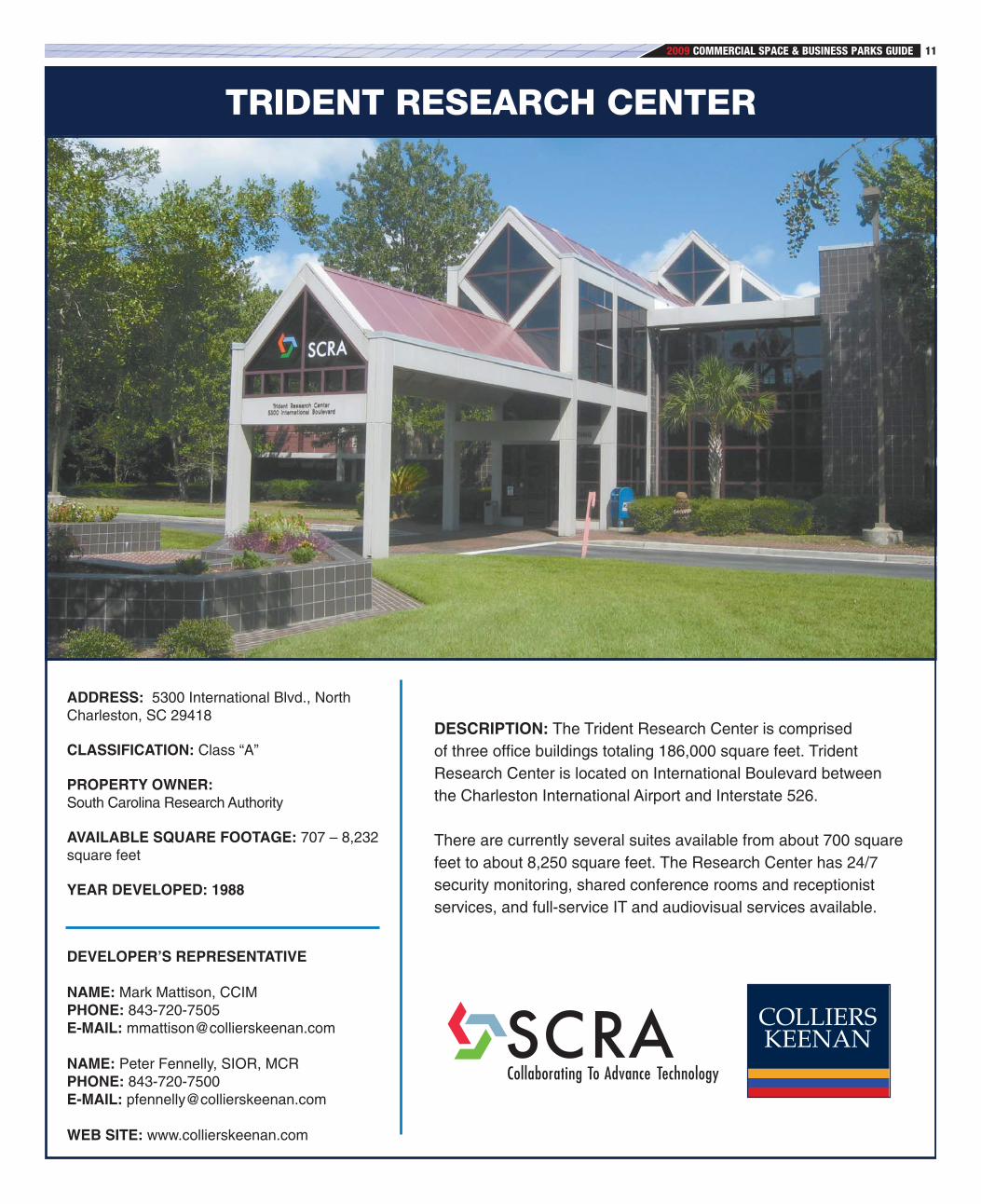

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE 11

TRIDENT RESEARCH CENTER

ADDRESS: 5300 International Blvd., North Charleston, SC 29418

CLASSIFICATION: Class “A”

PROPERTY OWNER:South Carolina Research Authority

AVAILABLE SQUARE FOOTAGE: 707 – 8,232 square feet

YEAR DEVELOPED: 1988

DESCRIPTION: The Trident Research Center is comprised of three offi ce buildings totaling 186,000 square feet. Trident Research Center is located on International Boulevard between the Charleston International Airport and Interstate 526.

There are currently several suites available from about 700 square feet to about 8,250 square feet. The Research Center has 24/7 security monitoring, shared conference rooms and receptionist services, and full-service IT and audiovisual services available.

DEVELOPER’S REPRESENTATIVE

NAME: Mark Mattison, CCIMPHONE: 843-720-7505E-MAIL: [email protected]

NAME: Peter Fennelly, SIOR, MCRPHONE: 843-720-7500E-MAIL: [email protected]

WEB SITE: www.collierskeenan.com

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE12

LIBERTY CENTER

ADDRESS: 151 Meeting StreetCharleston, SC 29401

CLASSIFICATION: “A+” offi ce space

AVAILABLE SQUARE FOOTAGE: 14,100

YEAR DEVELOPED: 1981

DESCRIPTION: The Class “A” offi ce space is a sublease opportunity of approximately 14,100 square feet located on the 4th fl oor of Liberty Center at 151 Meeting St. in the Central Business District. The space may be subdivided to suites as small as 3,000 square feet.

TOP ASSETS: Liberty Center has true Class “A” fi nishes within the common areas. The 4th fl oor lobby entrance has marble fl oors and the interior of Suite 400 has many private offi ces with side lights and a 12-person conference room, break area, storage areas and work rooms.

DEVELOPER’S REPRESENTATIVE

NAME: Mark Mattison, CCIMPHONE: 843-720-7505E-MAIL: [email protected]

NAME: Colin DunnPHONE: 843-720-1202E-MAIL: [email protected]

WEB SITE: www.collierskeenan.com

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE 13

ASHLEY OVERLOOK

ADDRESS: 4390 Belle Oaks Dr., North Charleston, SC 29405

CLASSIFICATION: Class A Offi ce

PROPERTY OWNER: Grubb & Ellis Realty Investors

PROPERTY MANAGER: Holder Properties

AVAILABLE SQUARE FOOTAGE: 11,078 rentable square feet

YEAR DEVELOPED: 2006

DESCRIPTION: Located in only Class A offi ce park in Charleston. With close proximity to Interstates 526 and 26, downtown, the Charleston Airport and a variety of restaurants and shopping all make Ashley Overlook a great location.

TOP ASSETS: Built in 2006. First generation space still available. Professionally managed by Holder Properties.

DEVELOPER’S REPRESENTATIVE

FOR LEASING INFO: Darby Siegel, Director, Holder Properties

PHONE: 843-266-8601

E-MAIL: [email protected]

WEBSITE: www.ashleyoverlook.com

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE14

TWO RIVERS CENTER

ADDRESS: 1190 Clements Ferry Road

CLASSIFICATION: Offi ce park

PROPERTY OWNER: Maritime Construction and Development LLC

PROPERTY MANAGER: W. Jason Stewart

ZONING: Commercial

AVAILABLE SQUARE FOOTAGE: Units vary in size from 1,241 sq ft to 4,849 sq ft.

NUMBER OF BAYS: 14 units available.

Additional land is available for build-to-suit.

PARK SIZE: 5.32 acres

YEAR DEVELOPED: 2004

TRANSPORTATION ACCESS: Property is ½ mile to Highway 41 and 6 miles to I- 526.

DESCRIPTION: Condo offi ce park. Units are for sale or lease. Please call for a brochure or for additional information.

TOP ASSETS: Class A, offi ce/fl ex space, brick veneer, one-story complex, two existing buildings. Public water and sewer. Property fronts on Clements Ferry Road at the intersection of Clements Ferry and Cainhoy Road. This property is located in Berkeley County.

IMPROVEMENTS PLANNED: Two additional buildings on site, one to be 15,000 square feet and one to be 5,000 square feet or build-to-suit.

DEVELOPER’S REPRESENTATIVE

NAME: Rick Kay, Agent

PHONE: 843-860-2131

E-MAIL: [email protected]

WEB SITE: CharlestonMLS.com, loopnet.com

MARITIME CONSTRUCTION AND DEVELOPMENT,LLC

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE 15

These industry-specifi c lists appear in each issue of the Charleston Regional Business Journal. To update your

company information or to be added to the list, call Gini Rice at 843-849-3114 or update online at

www.charlestonbusiness.com/update_lists/.

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE16

Why use SCJobMarket.com?SCJobMarket.com is an Internet recruiting Web site based in

South Carolina, devoted to connecting local candidates with local employers. Currently, we have over 135,000 unique site visitors a

month and over 18,000 active job seekers registered.

Connect with the Best Local Job Candidates.

From the publishers ofFor more information, call 843.849.3126 or visit our web site at www.SCJobMarket.com

These industry-specifi c lists appear in each issue of the Charleston Regional Business Journal. To update your

company information or to be added to the list, call Gini Rice at 843-849-3114 or update online at

www.charlestonbusiness.com/update_lists/.

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE 17

These industry-specifi c lists appear in each issue of the Charleston Regional Business Journal. To update your

company information or to be added to the list, call Gini Rice at 843-849-3114 or update online at

www.charlestonbusiness.com/update_lists/.

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE18

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE 19

2009 COMMERCIAL SPACE & BUSINESS PARKS GUIDE20

EXPECT MORE!

More space lease/sold

More transactions closed

More transaction dollar volume

Make a name with the only name that matters—SIOR®

The ociety of ndustrial and f ce EALTORS®pecialists in ndustrial and f ce eal Estate

Thomas G. Buist, JrSIOR

Grubb & Ellis/Barkley Fraser

725-7200

Robert A. CaldwellSIOR

Caldwell Commercial Real Estate Services

566-1888

Charles S. Carmody SIOR, CCIM

CB Richard Ellis Carmody, LLC

577-0702

Kristie S. RoeSIOR, CCIM

The Beach Company722-2615

Peter S. Fennelly SIOR, MCR

Colliers Keenan 723-1202

Michael G. McFallSIOR, CCIM

Maybank Properties740-9202

Charles L. Moore, JrSIOR, CCIMNAI Batten

& Moore, LLC805-6060

Frank W. NorvellSIOR

Norvell Real Estate Group, LLC 579-0055

Robert H. Nuttall, JrSIOR

Anchor Commercial CORFAC International

747-2333

Robert L. PrattSIOR, CCIM

RE/MAX Professional Realty

576-2705

R. Milton Thomas IIISIOR, CCIM

Anchor CommercialCORFAC International

747-3999

Hagood MorrisonSIOR, CCIM

Colliers Keenan723-1202

Reid P. DavisSIOR, CCIM

Anchor Commercial CORFAC International

277-4326

W. Scott RogersSIOR, CCIM

Sperry Van Ness290-9948

Eric V. CooperSIOR, CCIMBond Street

Investment Properties469-5455