2008 Tasmanian Dairy Conference 8 th October 2008 Frank Drum – NAB Agribusiness Economist...

27

008 Tasmanian Dairy Conference th October 2008 rank Drum – NAB Agribusiness Economist Tasmania’s potential for growth in a world market

-

Upload

jasmin-maxwell -

Category

Documents

-

view

215 -

download

1

Transcript of 2008 Tasmanian Dairy Conference 8 th October 2008 Frank Drum – NAB Agribusiness Economist...

2008 Tasmanian Dairy Conference8th October 2008Frank Drum – NAB Agribusiness Economist

Tasmania’s potential for growth in a world market

Discussion outline

• Macro Economic Outlook

• Potential for growth in world markets

• Summary

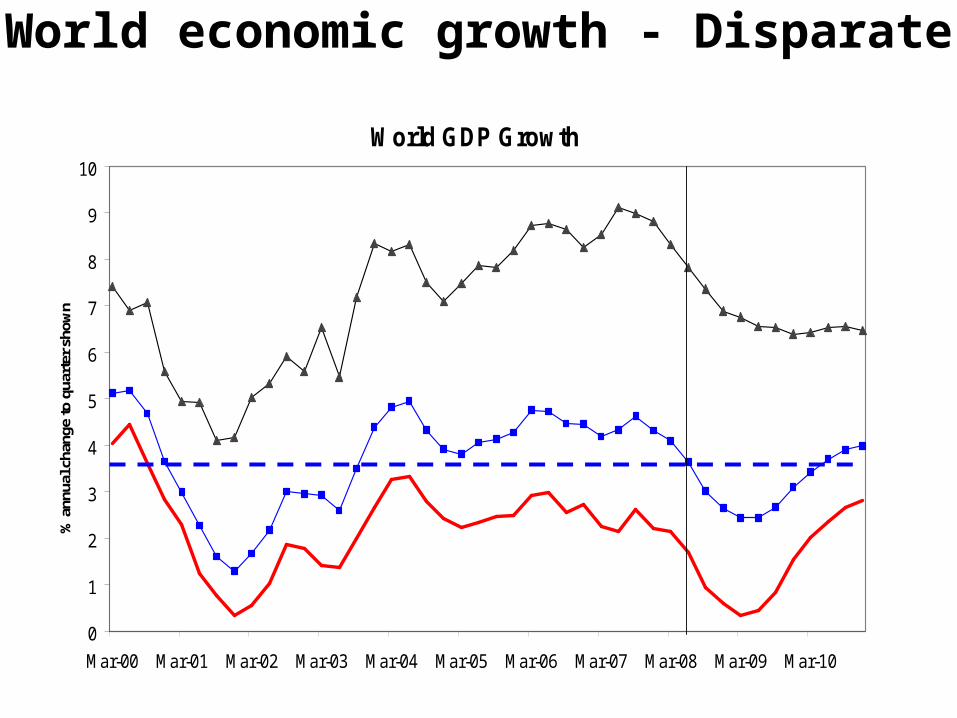

World economic growth - Disparate

World GDP Growth

0

1

2

3

4

5

6

7

8

9

10

Mar-00 Mar-01 Mar-02 Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10

% a

nnua

l cha

nge

to q

uart

er s

how

n

Forecast

Global growth

Developed economies

Emerging economies

Key drivers to global outlook

• Lagged effect of further weakness in equity markets, and high oil prices.

• Further weakness in housing markets globally

• Credit availability in US and Europe

• Lower consumer and business confidence

• China…largely insulated from global problems…

Australian economic cycleSustained but slower “real” GDP growth for next couple of years

Medium term driven by the 4 P’s….Population, Participation, Productivity ….Politics/Policy

Australian GDP: Economy-wide v Excl. Farming & Mining

-2.5%

-1.5%

-0.5%

0.5%

1.5%

2.5%

3.5%

4.5%

5.5%

6.5%

Dec

-86

Dec

-87

Dec

-88

Dec

-89

Dec

-90

Dec

-91

Dec

-92

Dec

-93

Dec

-94

Dec

-95

Dec

-96

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

% c

han

ge

- 12

mo

nth

s to

-2.5%

-1.5%

-0.5%

0.5%

1.5%

2.5%

3.5%

4.5%

5.5%

6.5%

GDP GDP excl. primary resources

Key watch issues for Australia

• Further deterioration in global financial instability

• Further increase in global oil prices

• Government policy

• Sustained drought

• Brazil, Russia, India and China….

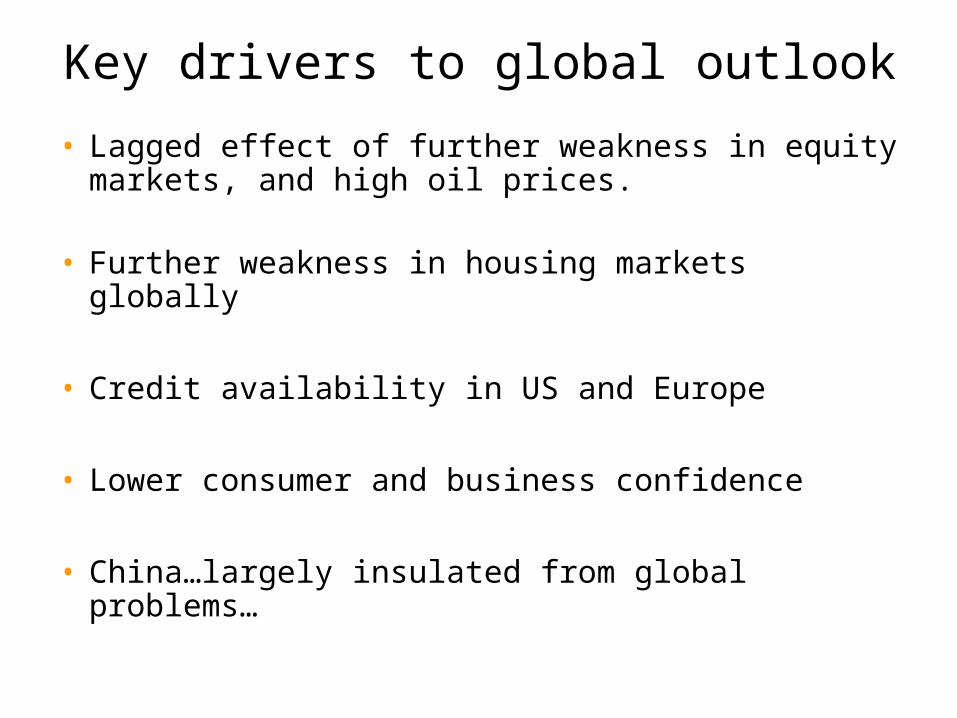

Australian cash rate forecast

1

2

3

4

5

6

7

8

9

Dec-95 Dec-97 Dec-99 Dec-01 Dec-03 Dec-05 Dec-07 Dec-09

%

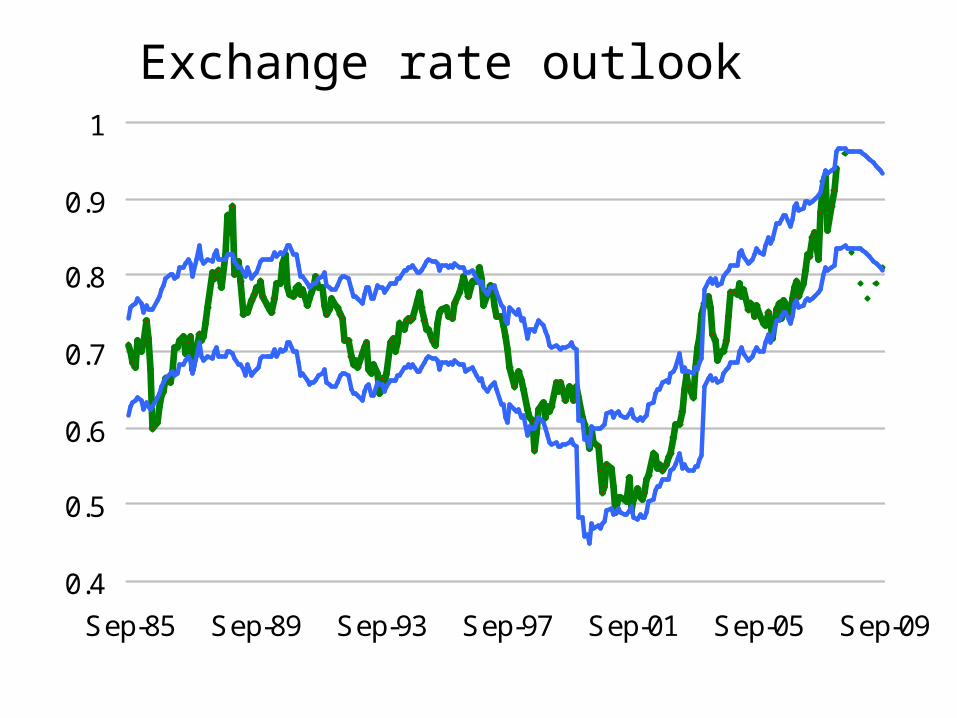

Exchange rate outlook

0.4

0.5

0.6

0.7

0.8

0.9

1

Sep-85 Sep-89 Sep-93 Sep-97 Sep-01 Sep-05 Sep-09

Macro Summary

• Global economic growth is slowing

• Growth in emerging economies to remain strong

• In Australia – slower but sustained growth

• Business – slower & a lot riskier

• Households - spending, unemployment

Growth Prospects for Tasmanian Dairy

Key growth Factors

• Developing new markets

• Production costs

• Key competitors

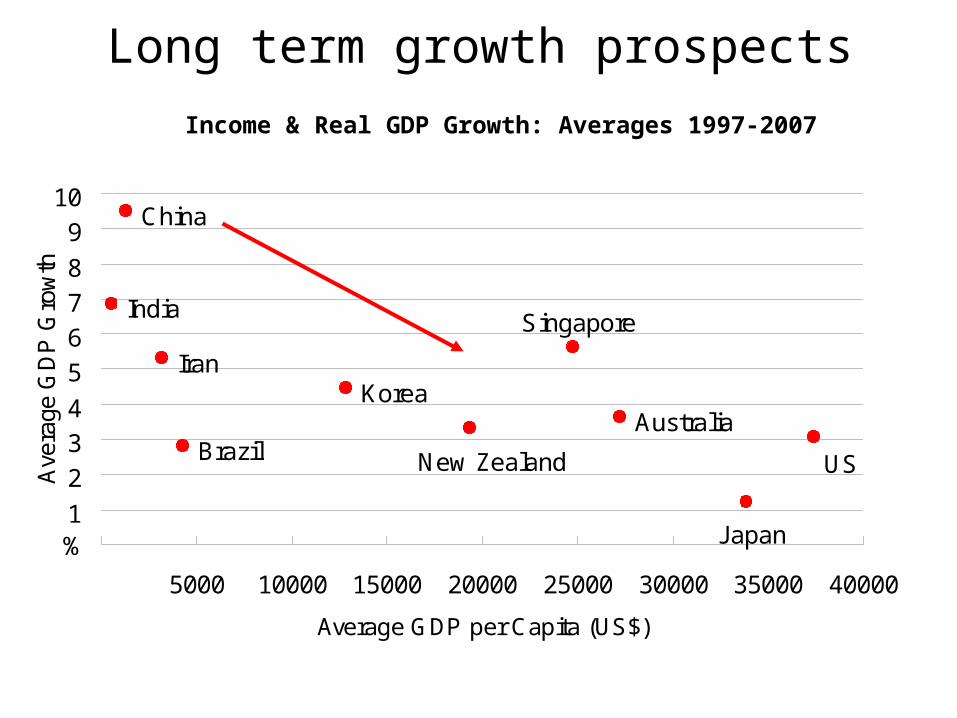

Long term growth prospects

China

India

KoreaIran

BrazilAustralia

New Zealand

Singapore

US

Japan1

2

3

4

5

6

7

8

9

10

5000 10000 15000 20000 25000 30000 35000 40000

Average GDP per Capita (US$)

Ave

rage

GD

P G

row

th

%

Income & Real GDP Growth: Averages 1997-2007

Per capita consumption of liquid milk & cheese

● China and India have low per capita consumption of milk products.

● As incomes rise and access to refrigeration increases there is scope for spectacular increases in consumption. We are already starting to see signs of that…

Annual meat consumption

20

40

60

80

100

120

140

1986 1991 1996 2001 2006 2011 2016Kg/person

US China India EU

Production Costs

Feed Costs

10 20 30 40 50 60

Tasmania

Western Australia

Western Victoria

Gipplsland

South Australia

Northern NSW and QLD

Southern & Central NSW

Northern Victoria & Riverina

%

2007-082006-07

Biofuel explosion

Production of Ethanol and Biodiesel in the US and EU

Fertiliser costs

5 10 15 20

Northern Victoria & Riverina

Southern & Central NSW

South Australia

Northern NSW and QLD

Western Victoria

Gipplsland

Tasmania

Western Australia

%

2007-082006-07

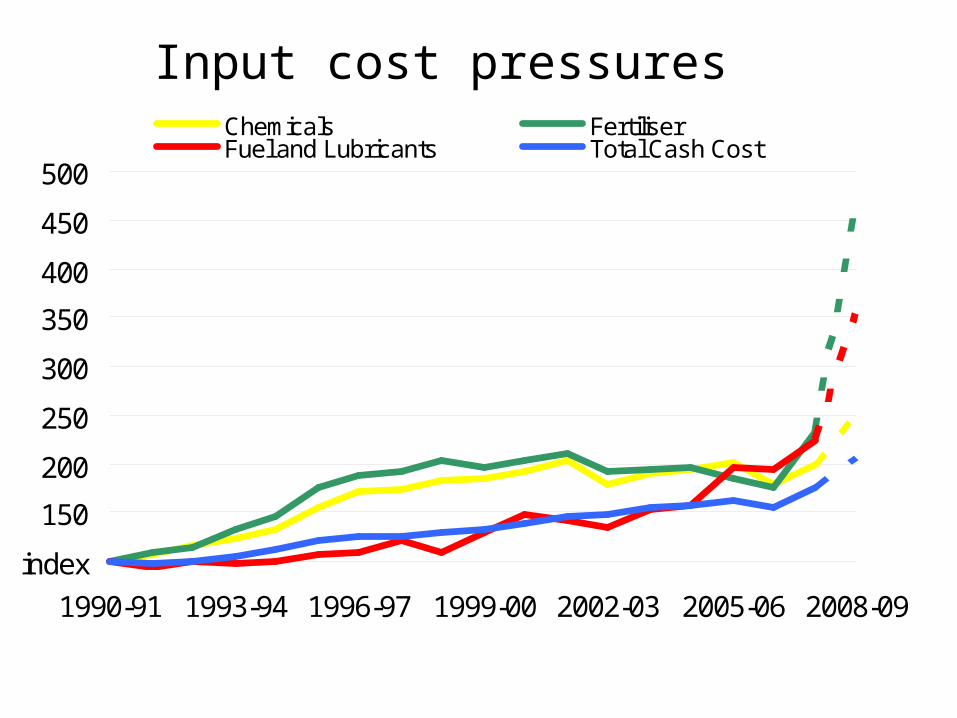

Input cost pressures

150

200

250

300

350

400

450

500

1990-91 1993-94 1996-97 1999-00 2002-03 2005-06 2008-09

index

Chemicals FertiliserFuel and Lubricants Total Cash Cost

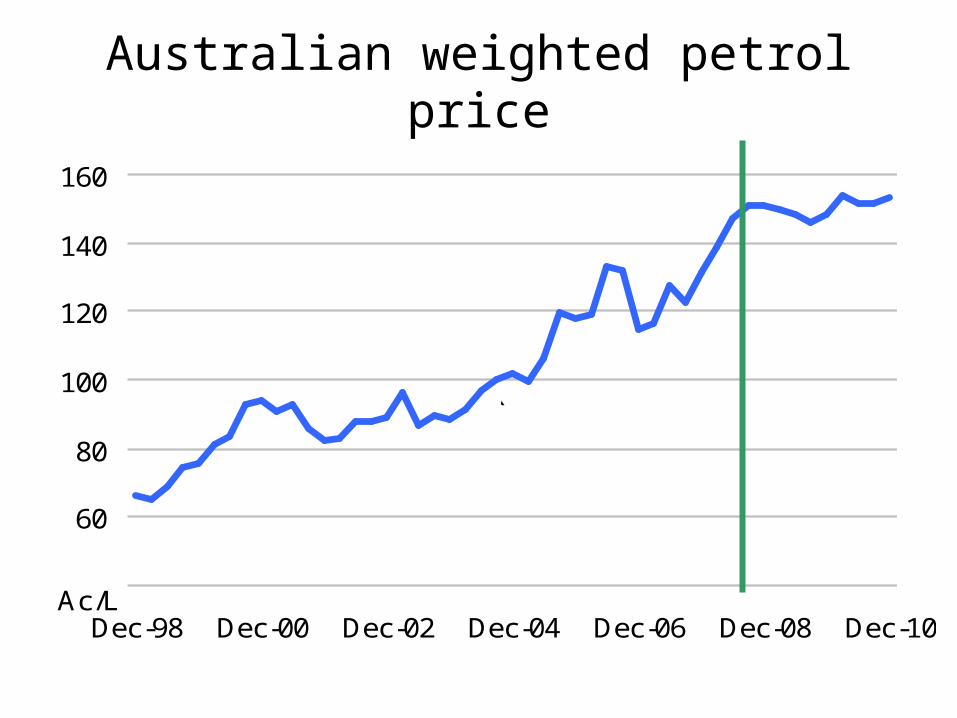

Australian weighted petrol price

60

80

100

120

140

160

Dec-98 Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10Ac/L

`

Global Players

• New Zealand

• European Union

• South America, India and China

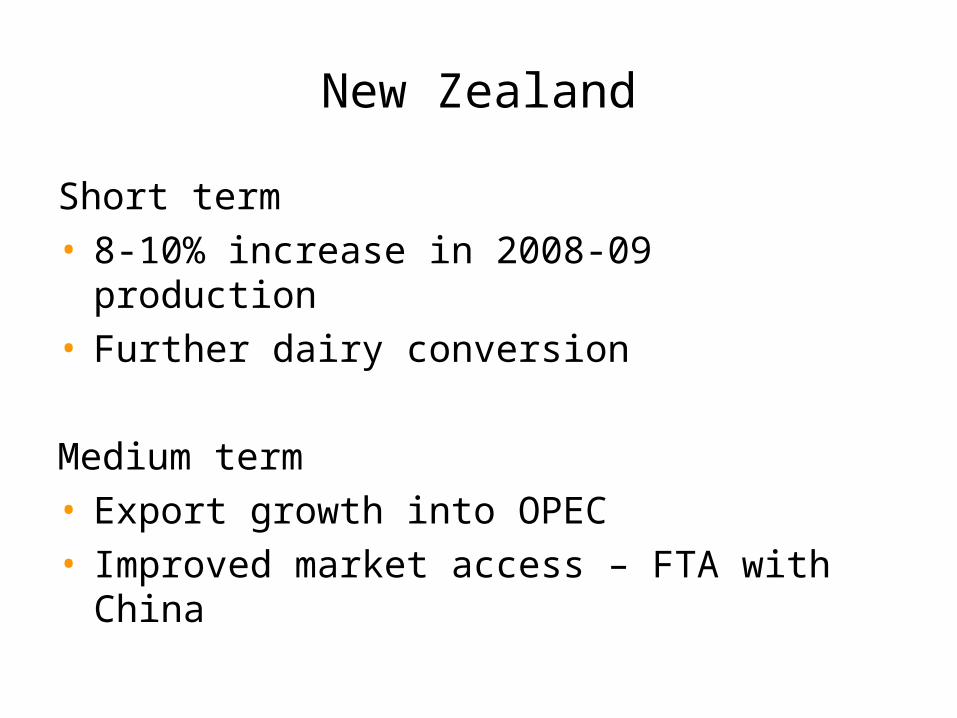

New Zealand

Short term• 8-10% increase in 2008-09 production• Further dairy conversion

Medium term• Export growth into OPEC• Improved market access – FTA with China

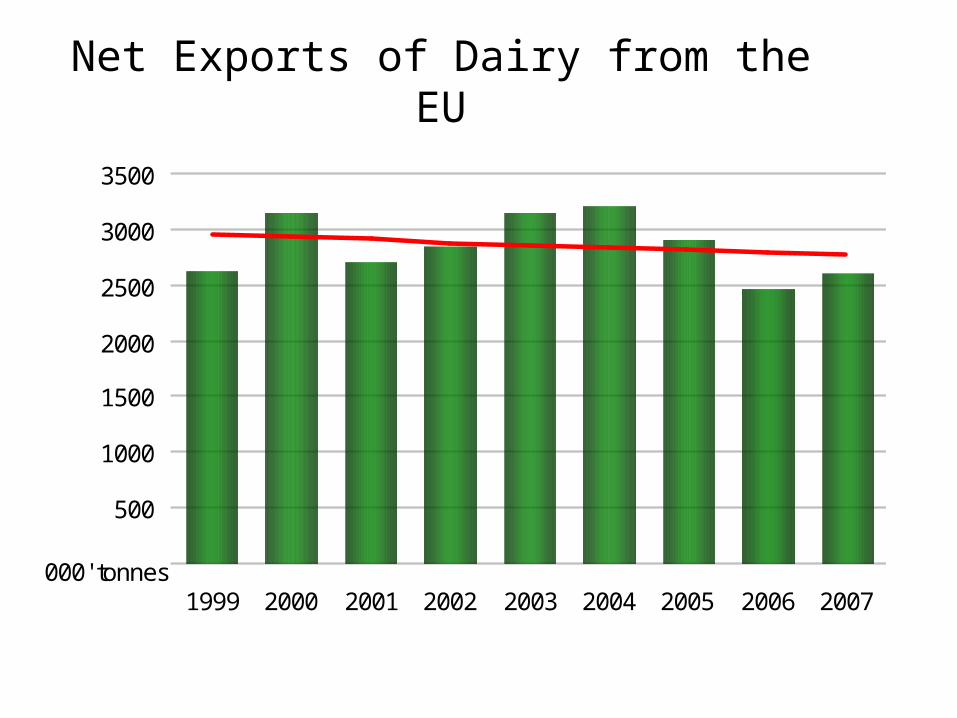

Net Exports of Dairy from the EU

500

1000

1500

2000

2500

3000

3500

1999 2000 2001 2002 2003 2004 2005 2006 2007000' tonnes

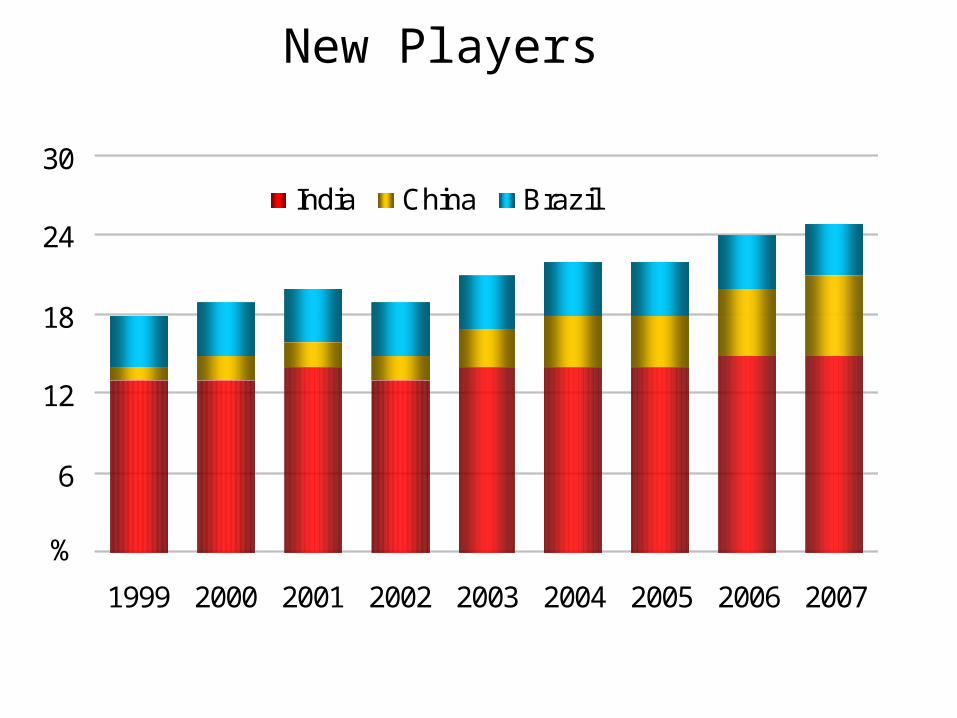

New Players

6

12

18

24

30

1999 2000 2001 2002 2003 2004 2005 2006 2007

%

India China Brazil

Summary

• Global economic environment is slowing• Increasing demand for protein remains long term

trend• Opportunities exist

• Challenges– Emerging markets– Cost competitiveness– Changing nature of global dairy environment

Important Notices

ANALYST CERTIFICATION: The person or persons named as the author's) of this report hereby certify that the views expressed in the research report accurately reflect their personal views about the subject securities and issuers and other subject matters discussed. No part of their compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in the research report. Research analysts responsible for this report receive compensation based upon, among other factors, the overall profitability of the Markets Division which is part of the Institutional Markets & Services division of National Australia Bank Limited, a member of the National Australia Bank Group (the “National”). The views of the author's) do not necessarily reflect the views of the National and are subject to change without notice. The National may receive fees for banking services provided to an issuer of securities mentioned in this report. The National, its affiliates and their respective officers, and employees, including persons involved in the preparation or issuance of this report (subject to the policies of the National), may also from time to time maintain a long or short position in, or purchase or sell a position in, hold or act as advisors, brokers or commercial bankers in relation to the securities (or related securities and financial instruments), of companies mentioned in this report. The National or its affiliates may engage in these transactions in a manner that is inconsistent with or contrary to any recommendations made in this report.

DISCLAIMER: So far as the law allows, National Australia Bank Limited ABN 12 004 044 937 ("the National") disclaims any warranty or representations as to the accuracy or reliability of the information and statements in this document. The National expressly advises that, to the extent permitted by the law of Victoria, Australia, by which law use and all other matters relating to this document are governed, it shall not be liable in any way whatsoever (whether in negligence or otherwise) for any loss or damage which may be suffered by any person relying upon such information or any opinion, recommendations or conclusions contained in this document or otherwise arising in connection with the contents of or any omission from this document where the liability is made non-excludable by legislation. This document has been prepared for dissemination to professional investors. The opinions expressed herein are those of the author and not necessarily those of the National. The information on which those opinions are based has been gleaned from public sources or provided by the subject on a non-confidential basis. This document does not purport to contain all relevant information and any statement as to any future matter is a present prediction of a possible future outcome, the accuracy of which cannot be guaranteed. Past performance is not a guide to future performance. Recipients should not rely upon the contents of this document, but should make their own assessment and evaluation, undertake an investigation and enquire and seek advice to enable them to make any decision concerning their own risk. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The National, its affiliates, and employees may hold a position or act as price maker in the financial instruments of any issuer discussed within this document or act as underwriter, placement agent, adviser or lender to such issuer. © Copyright National Australia Bank Limited ABN 12 004 044 937.

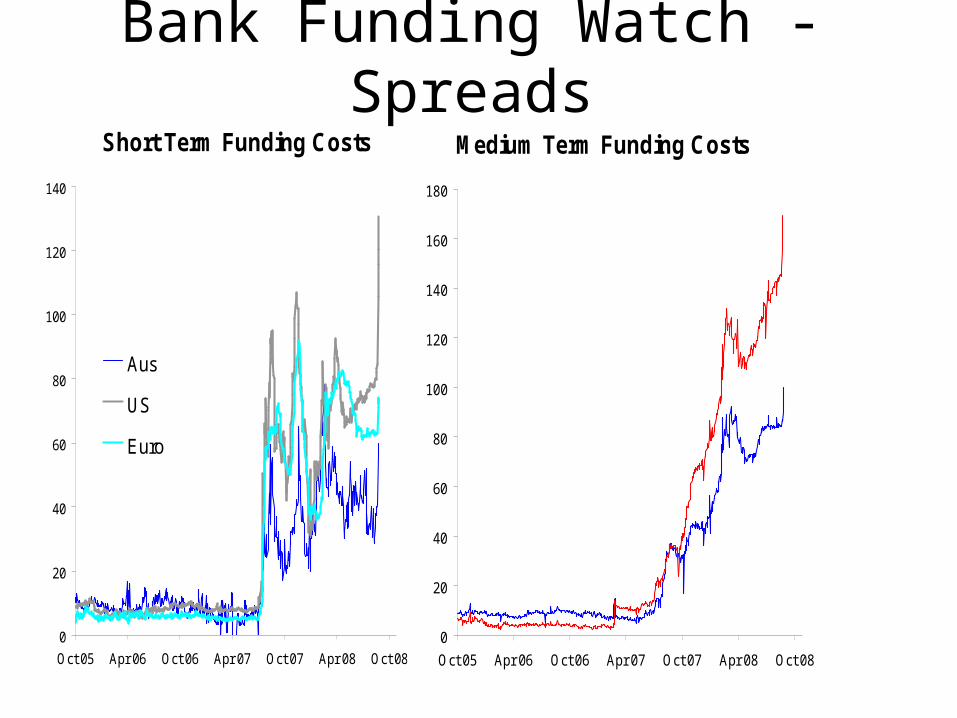

Bank Funding Watch - SpreadsShort Term Funding Costs

0

20

40

60

80

100

120

140

Oct 05 Apr 06 Oct 06 Apr 07 Oct 07 Apr 08 Oct 08

Aus

US

Euro

basis point spread between 3mth BBSW/Libor and the 3mth overight index swap

Medium Term Funding Costs

0

20

40

60

80

100

120

140

160

180

Oct 05 Apr 06 Oct 06 Apr 07 Oct 07 Apr 08 Oct 08

Bank spread to swap - 2-3 year

Domestic Banks

International Banks