2008 European

32

5th Value Investing Seminar A summary and overview of the ideas and topics discussed this year p. 2-3 Ciccio Azzollini, Cattolica Partecipa- zioni: Banco Popolare The founder of the Value Investing Seminar about his own investment strategy and his current investment Banco Popolare. p. 4-8 …………………………………..............…………… Whitney Tilson, T2 Partners: Fairfax The co-initiator of the seminar presented his deep analysis of the U.S. credit and housinf bubbles. His way out of the crisis: The Canadian Insurance Company Fairfax p. 9-13 Roberto Russo, Duemme SGR Parmalat p. 14-15 …………………………………..............…………… Fernando Bernad, Bestinver Asset Management Smurfit Kappa p. 16-17 …………………………………..............…………… Victor Fasciani, Sellers Capital Vulcan Materials p. 18-19 …………………………………..............…………… Guy Spier, Aquamarine Capital Ma- nagement Alaska Milk p. 20-21 …………………………………..............…………… Photo Gallery p. 22-23 …………………………………..............…………… News of the Scene p. 24-25 …………………………………..............…………… Book recommendations p. 26 …………………………………..............…………… Editorial p. 27 …………………………………..............…………… Imprint p. 28 Whitney Tilson is founder and Ma- naging Partner of T2 Partners LLC, which runs three value-oriented pri- vate investment partnerships, and the Tilson Mutual Funds, and co-initiator of the Value Investing Seminar. This year, he presented his detailed ana- lysis of the U.S. credit and housing bubbles and highlighted a way value investors might profit from the crisis: Canadian insurance company Fairfax Financial. …p. 9-13 Whitney Tilson, Founder and Managing Partner, T2 Partners LLC The founder of T2 Partners LLC co-hosted the seminar and highlighted causes and consequences of the U.S. housing and credit bubbles. »Understanding how to be a good investor makes you a better business manager and vice versa.« Charlie Munger Whitney Tilson – Ciccio Azzollini, Managing Director, Cattolica Partecipazioni S.p.A. vestors from all over the world presented their investment strategies and selected investment ideas. The idea to the Mol- fetta seminar was born in 2004, when Ciccio Azzollini invited Whitney Tilson to teach value investing to his team. All seminar fees go to charity projects for children in need. Exclusively to EVI Cic- cio Azzollini gave deep insighs into his investment approach and his investment idea Banco Popolare exclusively to the European Value Investor. …p. 4-8 The annual Value Investing Seminar in Molfetta organized by Ciccio Azzollini, Managing Director of Cattolica Parte- cipazioni, has become an established tradition for value investors in Europe and overseas. Once again top value in- Every year, Ciccio Azzolini, founder of Cattolica Partecipazioni S.p.A. organizes his Value investing seminar co-hosted with Whitney Tilson in his home region of Apulia. The world-class-event has become one of the most important European Value Conferences. Ciccio Azzollini – CONTENTS VISITOR‘S REPORT INTERVIEWS INVESTMENT IDEAS 5 th Value Investing Seminar in Bisceglie, Italy, 15 and 16 July 2008: V ALUE I NVESTOR THE EUROPEAN NO. 4 | SEPTEMBER 2008 INVESTMENT STRATEGIES BEYOND THE MAINSTREAM No. 4 – Page 1 – September 08 SPECIAL EDITION

-

Upload

vaiscapital -

Category

Documents

-

view

210 -

download

14

Transcript of 2008 European

5th Value Investing Seminar A summary and overview of the ideas and topics discussed this year p. 2-3 …………………………………..............……………

Ciccio Azzollini, Cattolica Partecipa-zioni: Banco Popolare The founder of the Value Investing Seminar about his own investment strategy and his current investment Banco Popolare. p. 4-8…………………………………..............……………Whitney Tilson, T2 Partners: Fairfax The co-initiator of the seminar presented his deep analysis of the U.S. credit and housinf bubbles. His way out of the crisis: The Canadian Insurance Company Fairfax p. 9-13

…………………………………..............……………

Roberto Russo, Duemme SGR Parmalat p. 14-15…………………………………..............……………

Fernando Bernad, Bestinver Asset ManagementSmurfit Kappa p. 16-17…………………………………..............……………

Victor Fasciani, Sellers CapitalVulcan Materials p. 18-19…………………………………..............……………

Guy Spier, Aquamarine Capital Ma-nagementAlaska Milk p. 20-21…………………………………..............…………… Photo Gallery p. 22-23 …………………………………..............……………

News of the Scene p. 24-25 …………………………………..............……………

Book recommendations p. 26 …………………………………..............……………

Editorial p. 27 …………………………………..............……………

Imprint p. 28

Whitney Tilson is founder and Ma-naging Partner of T2 Partners LLC, which runs three value-oriented pri-vate investment partnerships, and the Tilson Mutual Funds, and co-initiator of the Value Investing Seminar. This year, he presented his detailed ana-lysis of the U.S. credit and housing bubbles and highlighted a way value investors might profit from the crisis: Canadian insurance company Fairfax Financial. …p. 9-13

Whitney Tilson, Founder and Managing Partner, T2 Partners LLC

The founder of T2 Partners LLC co-hosted the seminar and highlighted causesand consequences of the U.S. housing and credit bubbles.

»Understanding how to be a good investor makes you a better business manager and vice versa.« Charlie Munger

Whitney Tilson –

Ciccio Azzollini, Managing Director,Cattolica Partecipazioni S.p.A.

vestors from all over the world presented their investment strategies and selected investment ideas. The idea to the Mol-fetta seminar was born in 2004, when Ciccio Azzollini invited Whitney Tilson to teach value investing to his team. All seminar fees go to charity projects for children in need. Exclusively to EVI Cic-cio Azzollini gave deep insighs into his investment approach and his investment idea Banco Popolare exclusively to the European Value Investor. …p.4-8

The annual Value Investing Seminar in Molfetta organized by Ciccio Azzollini, Managing Director of Cattolica Parte-cipazioni, has become an established tradition for value investors in Europe and overseas. Once again top value in-

Every year, Ciccio Azzolini, founder of Cattolica Partecipazioni S.p.A. organizes his Value investing seminar co-hosted with Whitney Tilson in his home

region of Apulia. The world-class-event has become one of the most important European Value Conferences.

Ciccio Azzollini –

CoNTENTSVISIToR‘S REPoRT

INTERVIEWS

INVESTMENT IDEAS

5th Value Investing Seminar in Bisceglie, Italy, 15 and 16 July 2008:

ValueInVestorThE EUrOPEAn

No. 4 | SEPTEMBER 2008

I N V E S T M E N T S T R A T E G I E S B E yo N d T H E M A I N S T R E A M

No. 4 – Page 1 – September 08

SPECIAL EDITIOn

5th Annual Value Investing Seminar, 15th and 16th July 2008 in Bisceglie - Visitor‘s Report

Every year Ciccio Azzollini, founder and managing director of Cattolica Partecipazioni S.p.A., invites to a two-day seminar on value investing. As every year the speakers were top value investors from the

United States and Europe who presented their views on the market, their investment approach and their best investment ideas. A visitor‘s report by Tim du Toit.

From the 15th of July I attended the two- day 5th Annual Value Investing Seminar in Bisceglie, near Molfetta (Italy). This event, as the previous four, was orga-nised and sponsored by Ciccio Azzol-lini, the founder and managing partner of Cattolica Partecipazioni S.p.A. The seminar was attended by about 80 in-vestors and investment professionals coming mainly from Europe but also from the U.S. as well as the Ukraine. As every year the speakers were top value investors from the United States and Europe who presented their views on the markets, their investment approach and their very best investment idea. Some of these ideas will be presented in detail in this issue of the european ValueInVestor.

With the following summary I want to give an overview about the ideas and topics discussed this year.

Ciccio Azzollini‘s „Italian sunshine in a stormy world“: Banco Popolare

Ciccio Azzollini – Cattolica Partecipazioni, Italy,started the conference with the theme “Italian sunshine in a stormy world”. This reflected the mood at the conference with world markets having turned down sharply (20% plus) for the second time this year as result of the credit crunch and deflating housing bubbles around the world. he presented his approach to value investing reflected in his two in-vestment ideas, Banco Popolare (ISIN: IT0004231566) and Fiat Group (ISIN IT0001976403). he sees Banco Popo-lare as attractive because the business is more franchise – than commodity-like,

solid asset quality (no subprime) and ade-quate capitalisation. After showing his previous successful investments in the Fiat Group he posed the question what next after the price declined 60% from its recent high. Based on the company’s 2007 to 2010 business plan guidance Cic-cio Azzollini built three scenarios which again using a 20% discount rate resulted in an expected share price of EUr 13.40, 40% upside from the current share price of EUr 9.58.

The credit and housing bubble - one of the main topics

One of the main topics discussed this year was the U.S. credit crisis and housing bubble, its consequences and how value investors may profit from it.

Whitney Tilson – T2 Partners, USA, gave a detailed explanation why the crisis is on its second leg down due to defaulting option adjustable rate

mortgages (ArM) prime loans, home equity lines of credit and second lien loans. As investment ideas he presented Fairfax (ISIN: CA3039011026) as a long position and Washington Mutual (US9393221034) as a short. Washing-ton Mutual is in trouble due to 55% of its loan portfolio exposure to option ArM mortgages, home equity loans and subprime mortgages. he does not currently recommend shorting the stock but is not covering his short position due to the possibility of a dilutive stock issue or a run on the bank

Andrea Danese, Gianluca Galletto - Fifth Avenue Advisors, USA presented an opportunity for an insti-tutional investor to profit from New York residential property as prices are impacted by the credit crunch. They made a compelling argument in spi-te of new York property prices not having gone down much yet. Atticus Lowe and Lance Helfert – West Coast Management, USA,started out by explaining their investment approach “entrepreneurial investing” as detailed in the book „The Entrepre-

»5TH VALUE INVESTING SEMINAR«

Participants of the 5th Value Investing Seminar in Bisceglie, Hotel Salsello. In the front: Tim du Toit, Kerstin Franzisi, Roberto Russo (from left).

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 2 – September 08

neurial Investor“. Their idea was ATP Oil and Gas (ISIN: US00208J1088) a motivated (23% insider ownership), entrepreneurial oil and gas explorati-on and production company with an outstanding culture. They estimate that the company has a value of USD 122 based on an oil price of USD 90 per barrel and a natural gas price of USD 8.5 per million Btu compared to the current share price of USD 40. Poten-tial catalysts include asset sales and a master limited partnership spin off.

Consumer brands and food companies still popular in the value scene

Consumer brands and food companies stay interesting for value investors. This year we have been presented even two milk and dairy drink producing companies:

Guy Spier – Aquamarine Fund, USA, introduced the strategy of his fund and its out-performance of the DJIU S&P500 and FT 100 since its incepti-on in September 1997. his stock idea, the family owned Philippine company Alaska Milk (ISIN: PHY003281078) came from his focus on consumer brand companies.

Roberto Russo – Duemme SGR, Italy, introduced Parmalat S.p.A. (ISIN: IT0003826473), the company that emerged in 2005 from the spectacular bankruptcy scandal of its name sake predecessor.

Fernando Bernad – Bestinver Asset Management, Spain, highlighted Bestinver’s excellent 1089.4% out-performance of the Madrid stock exchange from 1993 to 25 June 2008. Bestinver’s strategy is actively trading the positions in their portfo-lios, decreasing the weighting of the company as the share price increases and increasing the weighting as the price declines. As investment oppor-tunities Fernando presented Smurfit Kappa (ISIN: IE00B1RR8406) as a “cyclical trading close to the point of maximum pessimism” and CIBA (ISIN: CH0005819724) which is perceived as a cyclical chemical com-pany with declining margins, facing a downturn.

Gabriele D’Agosta – Morgan Stanley, Italy,explained Morgan Stanley’s approach of screening for accounting criteria such as book value and cash genera-tion that cannot easily be manipula-ted by management. his idea was JD

Wetherspoon (ISIN: GB0001638955), a pub owner operator in the UK. The company is attractively valued with a 6.8% dividend yield, 23.3% FCF yield and 1.7 times book value. A margin of safety is provided by an enterprise value of GBP 692m with real estate at 1999 historical cost of GBP 793m. Gabriele sees a positive change in like-for-like sales as the catalyst for buying and revaluation of the company.

Massimo Fuggetta – Horatius, Italy, gave an interesting presentation largely focusing on probability judgement.

Victor Fasciani – Sellers Capital, USA, showed Sellers Capital‘s strategy of investing in out of favour wide moat companies and small compa-nies selling near tangible liquidati-on value. Their portfolios are very concentrated holding between five and fifteen shares. his investment idea was Vulcan Materials (ISIN: US9291601097).

For more information on the 5th Value Investing Seminar visit:

www.valueinvestingseminar.it

»5TH VALUE INVESTING SEMINAR«

The Speakers at the 5th Value Investing Seminar, Bisceglie (from left to right): Atticus Lowe, Lance Helfert, Victor Fasciani, Andrea Danese, Gabriele D‘Agosta, Ciccio Azzollini, Roberto Russo (in the back), Guy Spier, Massimo Fuggetta (in the back), Gianluca Galletto, Whitney Tilson, Fernando Bernad

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 3 – September 08

Ciccio Azzollini: Banco Popolare„Sunshine in a stormy world“ - this was the motto of this year‘s Value Investing Seminar, organized

for the fifth time in a row by Ciccio Azzollini, Managing Director of Cattolica Partecipazioni S.p.A. and devoted value investor, in his home region of Apulia, Italy. As such a „sunshine“ he presented Banco

Popolare, one of his current investments and largest holdings.

»CICCIo AzzoLLINI - BANCo PoPoLARE«

EVI: Mr. Azzollini, it’s the 5th time you have organized a two-day seminar for value investors. This event is becoming more and more popular amongst in-ternational value investors. This year there have been about 80 participants. How did you get the idea to organize such an event every year?

Azzollini: The idea to organize the Value Investing Seminar was born four years ago when I invited Whitney Tilson here to Italy to teach value investing to my team. It went so well that we decided to do it again. Each year since then more and more people have come to learn from brilliant investors from all over the world who we invite to speak, teach and share their best investment ideas. We are thrilled about the success of the seminar.

EVI: So there will be a 6th Value Inve-sting Seminar in 2009?

Azzollini: Yes, we will plan the next event soon.

EVI: How did you become a value in-vestor?

Azzollini: I bought my first stocks when I was 18 years old and, after four years of foolishly doing technical analysis, momentum investing, etc. I lost all the money my father gave me to invest. Fortunately, near the end of this period, I happened to read an article on Warren Buffett that was published in an Italian financial newspaper.

Then, in 1996, on my first trip to the U.S. and Canada with my parents, I visited a book store in Toronto and bought my first book about Warren Buffett, entitled “The Good Guy of Wall Street”1). This was how I first learned about value investing.

His own investment style is a disciplined, long-term-oriented and oportunistic value approach.

investment opportunities in other European countries.

Before he founded his own investment company Cattolica Partecipazioni S.p.A. in his hometown Molfetta, in 2003, Ciccio Azzollini had worked for three years as fund manager at Abax Bank in Milan. Cattolica Par-tecipazioni S.p.A follows the value investing philosophy by selecting undervalued companies with excel-lent businesses.

Ciccio Azzollini also is founder of the first “Value Investing Seminar” in Italy that he organized this year for the fifth time in a row in his home region of Apulia.

Ciccio Azzollini, full name Benia- mini Francesco Azzollini was born in 1974 in Molfetta. After having gra-duated at University of Bari in 1997, he obtained a diploma as “Financial Analyst” at the European Associa-tion of Financial Analysts.

Fascinated by the value investing philosophy after having read the book about Warren Buffett “The Good Guy on Wall Street”, he participated va-rious courses on value investing at Columbia Business School, taught by Joel Greenblatt, Bruce Greenwald and richard Pzena.

his own investment style is a dis-ciplined, long-term-oriented and opportunistic value approach. For his investment decisions he con-centrates on fundamental research and analysis to identify securities that are traded at far less than their intrinsic value and have a catalyst to realize that value. As Italian value investor he focuses on the Italian stock market but also looks for

Ciccio AzzolliniManaging DirectorCattolica Partecipazioni S.p.A.

1) Andrew Kilpatrick: „The Good Guy Of Wall Street“, new York, 1992

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 4 – September 08

»CICCIo AzzoLLINI - BANCo PoPoLARE«

EVI: And then, you get fascinated by the value investing philosophy…..

Azzollini: Yes. I was really impressed by that investment philosophy and wanted to know everything about it. Thanks to the internet, when I returned home I was able to learn much more about Buffett, including the fact that he attended Columbia Business School. Unfortunately my English wasn’t (and still isn’t) good enough, but I did email Joel Greenblatt. I had read his first book ”You Can Be a Stock Market Genius”2) and he was teaching a value investing course at Columbia.

he kindly said it would be OK with him if I sat in the back of his classroom. So, speaking barely any English, I moved to new York in the spring of 1999 at the peak of the internet bubble, when value investing was deeply out of fa-vour, to learn the art of value investing from one of my heroes. At the end of the course, Greenblatt suggested that I sit in on richard Pzena’s class, what I did. Later I attended Prof. Bruce Greenwald’s Executive Value Investing Program. I owe a debt of gratitude to these three great men.

EVI: Do you have any other mentor or investor who particularly influ-enced you in your own investment style?

Azzollini: My biggest educators in life are my father, mother and grandfather. As an investor, in addition to the three men who taught me at Columbia, I would cite Ben Graham, Warren Buf-fett, Charlie Munger and Seth Klarman, from whose books and shareholder’s letters I learned a great deal. Special mention goes to Whitney Tilson, who is a mentor and like a brother to me. (Full disclosure: Whitney edited my responses to these questions so that I could communicate my thoughts more clearly in English, which I’m still trying to improve.)

EVI: How would you describe your investment style? In which situations do you invest?

Azzollini: I have a disciplined, long-term-oriented, opportunistic value approach. At Cattolica Partecipazioni we do rigorous fundamental research and analysis to identify securities that are traded at far less than their intrin-sic value - typically at least at a 50% discount - and that, in most cases, have a catalyst to realize that value. Because I’m from Italy, I tend to in-vest quite a bit in my home country, though I also invest frequently in the U.S. market and elsewhere in Europe on occasion.

EVI: Do value investors need special characteristics to be successful?

Azzollini: Yes, absolu-tely. Most importantly, one must be able to think independently to be a sucessful value investor. In addition, an understanding of eco-nomics and finance is absolutely necessary to understand the busines-ses in which one company is operating and to be able to estimate this company’s intrinsic value. Finally, understanding psychology is also very important and helpful, because in the short term stock prices are often driven by emotional aspects of human behaviour.

EVI: Where and how do you general-ly look for investment opportunities? Looking at the portfolio of Cattolica Partecipazioni there is a concentra-tion on Italian companies. Why do you prefer this market?

Azzollini: I look for opportunities everywhere, with a focus on situations where there are motivated sellers and missing buyers. Like most value inve-stors, I try to find situations in which there is a big discrepancy between what the market is expecting and what I think the future will actually be. I focus on Italian companies for two reasons. First, there are very few value investors here, so companies’ stocks here can be very inefficiently priced. Secondly, I have many connections in the Italian business community, so I can often gain insights into certain companies that give me an investment edge.

EVI: Focusing the Italian stock mar-ket, where are you currently sear-ching for value stocks?

Azzollini: The Italian stock market has been hit hard this year, especially financial and industrial companies, so I’m finding many opportunities in these industries. Our two largest holdings are Banco Popolare (ISIN: IT0004231566), Italy’s 4th largest commercial bank, and Fiat (ISIn IT0001976403), which I both have presented at the seminar.

EVI: So, the subprime crises has also arrived the financial market in

Italy…Or are the-re other reasons for the undervaluation? Why the undervalua-tion in the industrial sector?

Azzollini: Financial stocks worldwide have been clobbe-red this year, most

justifiably so due to excessive le-verage and toxic exposures to sub-prime mortgages, structured finance products, derivatives and the like. Banco Popolare is one company that has none of these characteristics, but nevertheless, yet, its stock price is still down more than 40% this year, compared to its stock price in 2007. Like many value investors, we look for babies that have been thrown out with the bathwater.

As for industrial companies, their stocks are down because worldwide growth is slowing, many consumers and companies are hurting and costs are rising rapidly, all of which will likely compress profits. In the case of Fiat, the company will no doubt be affected by these factors,, but we think a worst-case scenario is alrea-dy built into the stock price. Doing a sum-of-the-parts analysis with very conservative assumptions, we think the expected value of the stock is around EUr 14 with a premium of 40% to today’s price of EUr 9.60.

EVI: Do macro trends influence your search?

»One must be able to think

independently to be a sucessful value investor .«

2) Joel Greenblatt: „You Can Be A Stock Market Genius“, new York, 1997

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 5 – September 08

Azzollini: not really. We are more bottom-up rather than top-down inve-stors and simply try to buy stocks at an appreciable discount from the value of underlying business. Of course,, sometimes – like in 2008 – macro factors drive stock prices much more than company-specific ones, which can cause our returns to suffer.

I’m not good at predicting macro factors, however, and I am confident that if my company-specific analysis is good, that will eventually be reco-gnized by the market.

EVI: How do you concretely form an opinion about an investment? Do you prefer one particular valuation method?

Azzollini: In investing, we focus on a few things: Understanding the business, eva-luating the people running the business, buying with large margin of safety and concentrating on our best ideas. Overall, the keys are good analysis, discipline, rationality and patience. Investing is a probabilistic exercise, so we try to figure out the risk-reward profile and expected values under different scenarios. We employ a simple approach to valuation, using standard metrics like multiples on free cash flow and asset value.

EVI: Do you also talk to management or do you concentrate exclusively on financial and industry research?

Azzollini: I usually don’t talk with management because I don’t want to

be influenced psychologically. But ana-lyzing the management is a key part of my analysis. So I dedicate special attention to how they have allocated the capital, how they’ve treated sharehol-ders and, of course, how much value they have created for them.

EVI: You already mentioned that you pay attention for the margin of safety. How important is it for you? And what do you mean by a “large margin of safety”? Is 20% like Gra-ham used it, enough for you?

Azzollini: The Margin of safety is very important for me. It’s one of the three pillars of value investing. The other two are Mr. Market and intrinsic value. But for me, the most important is margin

»CICCIo AzzoLLINI - BANCo PoPoLARE«

INVESTMENT THESISToday, the stock is at € 11.00 and the company has a market cap of about EUR 7 billion, equal to 3.2 million per branch, less than 4% of total deposits, less than 6x normalized earnings and 100% discount of private market value based on the average multiples paid over the last 10 years. The expected value in 2010 is around EUr 19.00, which would translate into an Irr of more than 30% in the next two years.

Financials: Revenue: € 3.27 b (2007)Net Margin: € 18.31% (2007)

Valuation Metrics: BP S&P mibP/E 7.88 9.39

Banco PoPolare ISIN IT0004231566

BANCo PoPoLARE SToCk PRICE

Institutional Investors:1) Franklin Mutual Advisers LLC 3.31%2) Stichting Pensioenfonds ABP 2.00%

Free Float: 94.60%

Fair Value: € 19.00

Business: Traditional banking model. Banco Popo-lare is Italy’s fourth biggest commercial bank.

Stock Information (07/30/2008):Price: € 11.5452 Week Range: € 19.54 – € 10.22Dividend Yield: 6.38% (2008e) 4.06% (2007)Market Cap: € 7.26 b

EURO

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 6 – September 08

of safety because it minimizes chan-ces of permanent capital losses. I’ve always kept Buffett’s favorite rules in mind: Rule #1: Don’t lose money. Rule #2: Don’t forget rule #1. As margin of safety we prefer to have a discount of 50%.

EVI: Are you someti-mes an activist?

Azzollini: no, though I was the lead plaintiff in one of the class action lawsuits against Parmalat (ISIN: IT0003121644). I had purchased the company’s debt after the scandal in 2003 emerged and agreed to serve as lead plaintiff in an ultimately successful attempt by bondholders to recover damages from the financial institutions that were either negligent or complicit in the scandal.

Parmalat Group is one of the major players worldwide in the production and distribution of milk, mainstream dairy products (yogurt, cream-based white sauces, desserts, cheese) and fruit-based drinks, with 2007 revenues of over EUr 3.9 bn.

EVI: How many titles do you nor-mally hold in your portfolio?

Azzollini: We are very concentrated, even among value investors, typical-ly holding five to eight positions. Our largest position can reach the 50% of our entire portfolio. In part, this ex-treme concentration is due to the fact that I manage the equity portion of a larger portfolio, but I would be very concentrated regardless – perhaps just not to such a degree.

EVI: When and how do you buy and sell?

Azzollini: When buying, we seek an expected Irr of at least 20% and a risk-reward profile whereby the reward is at least three times greater than the amount of capital that could be lost in a worst-case scenario. When I sell one stock, I do it for one of the following three reasons: The discrepancy between

our estimate of intrinsic value and market price has shrunk – hopefully because the stock has appreciated! – to

less than 10%; when I realize that I made a mistake; or when I find another invest-ment with a better Irr and risk-reward expectation.

EVI: Is your private portfolio different

from your publicly managed one?

Azzollini: no, as CEO Cattolica Par-tecipazioni S.p.A., which is a private company, a great part of my personal net worth is invested in it.

EVI: How high is your turnover? Which time horizon do you have for your investments?

Azzollini: Our turnover is typical in the single digits and our investment time horizon is 3-5 years.

EVI: Let’s talk about one of your current investment ideas. On the semi-nar you have presented Banco Popolare (ISIN: IT0004231566) as investment opportunity. For how long have you been invested in this company?

Azzollini: We started buying the stocks of Banco Popolare in november 2007. With the benefit of hindsight, I wish had waited because the share price has continued to de-cline. however, my experience is that it is really difficult to pre-dict short-term stock price performance, and I think I bought Banco Popolare, by any means, at an at-tractive price.

It has just become more attractive since then. I have continued to buy, making it our largest investment and bringing our average price to EUr 14.00 per share.

EVI: How did you become aware of Banco Popolare as an investment idea?

Azzollini: It popped up on our 52 week low screen, which is one of our sources of information. It gives us a list of the companies at 52 weeks lows.

EVI: What exactly is Banco Popolare’s business model? It is a traditional banking model? What kind of clients does the company have?

Azzollini: Yes, indeed, it’s the tradi-tional banking model. They have a big branch network to gather deposits and then lend money mostly to family-owned and small to mid-size businesses.

EVI: Why do you see upside potential in this stock right know? What are your thoughts on valuation?

Azzollini: Today, the stock is at 11 Euros and the company has a market cap of about EUr 7 billion, equal to 3.2 million per branch, less than 4% of total deposits, less than 6x nor-malized earnings and 100% discount of private market value based on the average multiples paid over the last 10 years. We have three valuation scenarios: worst case, most likely and the best case.

The expected value in 2010 from these three scenarios is around EUr 19.00, which would translate into an Irr of more than 30% in the next two years.

EVI: What are reasons for the un-dervaluation? What has the market

missed?

Azzollini: This is a question we always ask ourselves. In the case of Banco Popo-lare, the entire Italian banking system is cheap right now, ha-ving fallen more than

40% since last July, because investors are very pessimistic about financial stocks. In the U.S. and certain other markets, banks are taking big losses and being forced to deleverage, but we don’t be-lieve this will affect Italian banks.

We call this “Italian Bank sunshine in a stormy world”. Italian banks are going to deleverage too, but it’s one thing to

»CICCIo AzzoLLINI - BANCo PoPoLARE«

»The expected value for Banco Popolare

in 2010 from our three scenarios is

around EUR 19.00.«

»As margin of safety we prefer

to have a discount of 50%.«

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 7 – September 08

go from 40:1 leverage ratio to 15:1 vs. 18:1 to 15:1.

EVI: What are the competitive dy-namics in the Italian financial ser-vices market?

Azzollini: The market is wonderfully oligo-polistic with high bar-riers to entry and very loyal customers.

EVI: Does Banco Popolare have any franchises?

Azzollini: Banco Po-polare is the 4th largest Italian com-mercial bank and also the first Italian mutual bank. Its market share is about 10% in six regions of northern Italy and it has a dominating position in Italian consumer credit and leasing. It has a network of 2,200 branches across northern Italy, where per ca-pita income is the highest.

EVI: What are the risks for that investment?

Azzollini: I would say that at the current price we have almost no risk of permanent loss of capital. Banco Popolare currently earns roughly EUr 1.4 billion pretax after expen-sing more than EUr 380 million for LLP (loom loss provision)

Even in a severe business contraction, during which gross non-performing loans (now at 5%) double, Banco Popolare would still roughly break even. We rate this as a very low pro-bability and even if it did occur, it would be a temporary problem, not a permanent one.

EVI: How transparent is the asset side of the balance sheet? Is Banco Popolare influenced by the subpri-me fiasco?

Azzollini: The asset side of Banco Popolare is very clean, especially after the write-off they did two years ago. Banco Popolare has plenty of liquidity and there is no exposure to subprime or any exotic securities. The

target leverage ratio is around 15, in line with historical levels.

EVI: What were your biggest invest-ment mistakes?

Azzollini: My biggest mistakes tend to those of omission, when I fail to invest in something I should, which don’t appear as profits or losses.

I try not to let mi-stakes bother me, but rather learn from them and move on. We are in the business

of making probabilistic decisions, so some mistakes are inevitable.

My biggest investment mistake was Telecom Italia (ISIN: IT0003497168), Italy’s largest telecom company. We bought the stock back in 2005 at around EUr 2.20 per share and we thought that the intrinsic value was around EUr 3.00, based on a 12 multiple on after-tax unlevered free cash flow.

The assumption behind our investment was that the FCF would be stable in the future, so for each dollar of debt repaid, the market cap increase by the same amount. Unfortunately, the formerly oligopolistic market was opened up to competition and the company lost market share, causing margin erosion that reduced FCF and the intrinsic va-lue of the company.

We thought that this decrease in value would have been offset by the synergies with Telefonica, which bought a large stake in Telecom Italia at EUr 2.82, but they weren’t meaningful. We didn’t act promptly and the stock fell to EUr 1.40, so we lost almost 40%.

What I learned is to always think in terms of expected values under diffe-rent scenarios and that it are not the profit margins of the past but those of the future that are most important to an investor.

EVI: What have you learned from your mistakes?

Azzollini: First, beware of changes in the risk-reward calculation, espe-cially if the company is quite lever-aged. Second, don’t stray from your discipline; if you’re not finding great bargains, then, just stay in cash. Fi-nally, if you have made a mistake, act quickly to rectify it.

EVI: What do you want to do 10 years from now?

Azzollini: I considered starting a hedge fund, but decided not yet. I’m too shy to ask for money and I find that most investors don’t have my multi-year time horizon or stomach for the volatility, the inevitably results from a highly concentrated portfolio.

Thus, I plan to continue managing Cat-tolica Partecipazioni S.p.A. and conti-nue doing investing the way I do now, with the great team I’ve built, doing what I enjoy every day. At some point, I

hope to IPO Cattolica Partecipazioni S.p.A. as a holding and an investment company, sort of like Berkshire hathaway.

I also want to spend more time and ener-gy on the charity I

established called “More Love”.

EVI: Thank you very much for the open interview!

Remark: The disclaimer note published on the last page of this edition is applicable to the entire content of this article.

Contact:Ciccio AzzolliniCattolica Partecipazioni S.p.A.Piazza Garibaldi 1070056 Molfetta (BA)ItalyT: +39 080 33488-26F: +39 080 33488-32info@cattolica-partecipazioni.itwww.valueinvestingseminar.itwww.cattolica-partecipazioni.it

»CICCIo AzzoLLINI - BANCo PoPoLARE«

»In the U.S. and cer-tain other markets,

banks are taking los-ses and being forced to deleverage, but we don‘t believe this will affect Italian banks.«

»It are not the profit margins of the past

but those of the future that are most impor-tant to an investor.«

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 8 – September 08

EVI: Mr. Tilson, you have organised the Value Investing Seminar together with Ciccio Azzollini for the fifth time now. How did the idea for the conference come about?

Tilson: Ciccio read some of my arti-cles on the internet starting in 2000 and invited me to come teach a semi-nar on value investing to him and his staff in the summer of 2004.

It went so well that we decided to do it again, and he invited a couple of more speakers and more guests – and it’s just grown from there. We have both learned a lot, had fun and met many great people, so we plan to keep doing it.

EVI: Together with Mr. Glenn Ton-gue you manage three value-based private partnerships. How did you become a value investor? When did you become aware of that investment philosophy?

Tilson: I started by reading Warren Buffett’s annual letters, which really impressed me, and then I just kept on reading and started investing my own money according to those principles. And finally, on January 1st, 1999, I founded my own investment company and started my own fund.

EVI: How would you describe your investment style? In which situations do you invest?

Tilson: We are opportunistic value in-vestors, meaning we cast a wide net and invest in many types of situations – but in all cases, we are simply trying to buy a dollar for a lot less than a dollar.

EVI: Did you have a mentor or in-vestor which particularly influen-ced you?

Whitney Tilson: FairfaxWhitney Tilson is the founder and Managing Partner of T2 Partners LLC, which manages three value-oriented

private investment partnerships, and the Tilson Mutual Funds. Together with Ciccio Azzollini, he founded the annual Value Investing Seminar that last month was held for the 5th time. At the seminar, he presented his analysis

of the U.S. credit and housing bubbles and highlighted a way value investors might profit from the crisis: Canadia insurance company Fairfax Financial.

»WHITNEy TILSoN - FAIRFAx«

Together with Glenn Tongue, he manages the Tilson Mutual Funds and three value-oriented private investment partnerships, which he founded in 1999.

Chairman of the Value Investing Congress a biannual investment conference in new York City and Los Angeles. In addition he writes regular columns on value investing for several newspapers and was one of the authors of “Poor Charlie’s Al-manack” 1), a book about Berkshire hathaway Vice President Charlie Munger.

Before business school, Mr. Tilson was a founding member of Teach for America, the national teacher corps, and then spent two years as a consultant at The Boston Consulting Group.

Mr. Tilson is involved with a number of charities focused on education re-form and Africa. For his philanthropic work, he received the 2008 John C. Whitehead Social Enterprise Award from the harvard Business School Club of Greater new York. Today he lives in Manhattan with his wife and three daughters.

Whitney Tilson is the founder and Managing Partner of T2 Partners LLC and the Tilson Mutual Funds. Together With Glenn h. Tongue he manages three value-oriented private investment partnerships, T2 Accredi-ted Fund, Tilson Offshore Fund and T2 Qualified Fund, while the latter is comprised of two value-based mutual funds, Tilson Focus Fund and Tilson Dividend Fund.

Prior to starting his investment ca-reer, he studied at and graduated magna cum laude from harvard College with a bachelor‘s degree in Government. he then went on to gain an MBA with high Distinc-tion from harvard Business School in 1994 and then spent five years working with Professor Michael E. Porter studying the competitiveness of inner cities and inner-city-based companies nationwide.

Mr. Tilson also is the co-founder, Chairman and co-Editor-in-Chief of Value Investor Insight, an investment newsletter, and is the co-founder and

Whitney TilsonFounder and Managing PartnerT2 Partners LLC

1) Peter Kaufman: “Poor Charlie’s Almanack”, USA 2005

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 9 – September 08

»WHITNEy TILSoN - FAIRFAx«

FIGURE 2| THE SURGE IN BoRRoWING PoWER AND DECLINE IN LENDING STANDARDS LED To HoME PRICES SoARING FAR ABoVE TREND LINE

FIGURE 1| FRoM 2000-2006, THE BoRRoWING PoWER oF A TyPICAL HoME PURCHASER MoRE THAN TRIPLED – AND HAS NoW TUMBLED 39%

SOURCE: OFHEO, Bureau of Economic Analysis.

REAL HoME PRICE INDEx (1975=100)

A 34%decline toreturn totrend line

Housing Bubble

Trend line 1975-2000

SOURCE: Amherst Securities Group, L.P..

-39,4

Pre-Tax Income Borrowing Power

1.2.3.4.5.

1. 2. 3.

4. 5.

Slowly rising income Lenders being willing to allow much higher Debt-to-Income Ratios Falling interest ratesInterest-only mortgages (vs. full amortizing) No money down

overview of the great mortage BuBBle

Fueled by loos lending standards and a bubble mentality by all market participants, home prices nationwide from 2000-2006 rose more than 50% - and now need to fall approx. 34% from tjeir peak to return to trend line.

Historically the Ameri-can avarage houshold was able to borrow approx. 3x its pre-tax income to buy a house. At the bubbles peak from early 2006 to early 2007 the debt-to-income ratio was 9x! As of the beginning of 2008, due mainly to lenders tightenig their debt-to-income ratio limit back to historical levels around 35%, the amount that can be borrowed to by a home had fallen by 39.4% , to 5.2x income.

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 10 – September 08

»WHITNEy TILSoN - FAIRFAx«

Tilson: In addition to writings by and about Buffett, the books “The Intelligent Investor” , “Margin of Safety” and “You Can Be A Stock Market Genius” were particularly influential. In addition, like Ciccio, I sat through Joel Greenblatt’s class at Columbia Business School.

EVI: Do value investors need to have certain characteristics?

Tilson: Yes, absolutely. They need two things: the right approach and the right skills. I discussed this in depth in an article I wrote in 2001, “Traits of Successful Money Managers” .

For long-term invest-ment success, I stron-gly believe in the im-portance of thinking about investing as the purchasing of companies, rather than the trading of stocks. Value investors also have to be independent, and neither take comfort in standing with the crowd nor derive pride from standing alone. Other impor-tant characteristics are being patient and the ability to make decisions based on analysis, not emotion.

Last but not least, you only can be suc-cessful in the long run when you love what you do. Buffett has said at various times: “I’m the luckiest guy in the world in terms of what I do for a living and I wouldn’t trade my job for any job”.

EVI: Let’s have a deeper look at your strategy. Where and how do you look for opportunities?

Tilson: I try to stay flexible and look for value opportunities in many diffe-rent places, but the single best source of great ideas comes from talking to (or emailing with) other smart investors.

EVI: Where are you looking current-ly? Are there industries that currently

offer special opportunities for value investors?

Tilson: We are finding a lot of cheap stocks in sectors exposed to the U.S. consumer such as retailers like Target (ISIn US87612E1064).

EVI: Do macro trends and themes influence your search?

Tilson: not much, but more so than in the past, as macro themes have been ne-arly the sole driver of stock returns for the past year.

For example, over the past year, it hasn’t mat-tered which retailer you owned – you lost money if you didn’t see that the U.S. con-

sumer was going to get hit.

EVI: How do you form an opinion about an investment?

Tilson: We ask four questions. First: Do we (or can we) understand the company and industry (i.e., circle of competence)? Second: How much do we like the busi-ness? Third: How much do we like ma-nagement? And, last: Is the stock really, really cheap? It’s easy to find companies that meet the first three criteria, but their stocks are rarely cheap.

EVI: Do you talk to management to build your opinion about them, or concentrate exclusively on financial and industry research?

Tilson: It really de-pends, but we probably talk less to manage-ment than most in-vestors.

EVI: Which methods do you use for valu-ation? Does one me-

thod or particular methods domi-nate?

Tilson: It varies depending on the type of company and industry, but everything boils down to estimating future free cash flows, discounted back to the present. The most common metric we use is a low multiple of estimated normalized free cash flow.

EVI: Are you sometimes an „acti-vist“?

Tilson: rarely, only when we are forced to.

EVI: How many stocks do you nor-mally hold in your portfolio? How high is your level of concentration?

Tilson: About 20 stocks on the long side, of which the top 10 are typical-ly 70-80% of the long exposure. On the short side, 20-25 stocks, typically smaller positions.

EVI: When and how do you buy and sell?

Tilson: We buy when we think a stock can not possibly get any cheaper and, usually, when we see a catalyst that might cause the stock to go higher (though often a stock is really cheap precisely because there’s no catalyst – that’s OK with us too).

With lower quality businesses or small-cap stocks, we typically wait to buy until we think the stock is trading at half or less of what we think a ratio-nal buyer would pay to own the entire

company.

For better busines-ses, we’ll pay a hig-her price – perhaps a 30% discount rather than 50%. We start selling when a stock hits the low end of our estimated ran-ge of intrinsic va-

lue and finish selling when it hits the high end. We also sell if we conclude that we have made a mistake or if we need to raise cash to buy something even cheaper.

»For better businesses, we‘ll pay

a higher price - perhaps a 30% discount rather

than 50%.«

2) Benjamin Graham: „The Intelligent Investor“, 4th revised edition, New York 1973)

3) Seth A. Klarman: „Margin of Safety – Risk Avers Value Investing Strategies for the Thoughtful Investor“, New York 1991

4) Joel Greenblatt: „You Can Be A Stock Market Genius“, New York 1997

5) The complete Article of “Traits of Successful Money Managers” can be viewed at: www.fool.com/news/foth/2001/foth010717.htm

»For long-term investment success,

I believe in the impor-tance of thinking about investing as the purchasing of

companies.«

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 11 – September 08

EVI: Concerning the composition of your Mutual Fund, how does it differ from your three hedge funds?

Tilson: The Tilson Focus Fund, the mu-tual fund we manage (ticker: TILFX), is, with only a few exceptions, a long-only version of our three hedge funds (which are managed as one pool of capital). So, if we buy a 5% position in a stock, we allocate it evenly across the three hedge funds and the mutual fund. But short po-sitions only go in the hedge funds.

EVI: And how high is your turn-over?

Tilson: I’m not sure of the exact num-ber, but we tend to have 5-10 core po-sitions on the long side that we hold for a number of years.

EVI: At this year’s Value Investing Seminar, you gave a detailed overview of the US housing and credit bubbles, both the causes and consequences. Could you please summarize your take on this crisis?

Tilson: I think it is the largest financial bubble in history and its unwinding will take a long time and be very painful. There were numerous causes – many of the same ones we see in every bub-ble – but it reached a greater extreme than in any time in the past.

EVI: Do you think we have the worst behind us?

Tilson: no. I think housing prices will continue to fall for at least another 18 months and there are hundreds of billions

of dollars that still need to be written off by financial institutions.

EVI: How do you think the crisis will play out? Will banks be given the time to rebuild their balance sheets or will there be a seizure followed by nationalizations and emergency recaps?

Tilson: Probably somewhere in between. I think hundreds of small banks will fail and a few big ones as well.

EVI: Value investors are divided over whether the financial crisis presents a fertile area for finding undervalued stocks. Some are attracted to the cheap prices emerging while others caution that financials are per se unsuitable for value investors due to the high

»WHITNEy TILSoN - FAIRFAx«

INVESTMENT THESISToday, Fairfax is a very different company: its insurance businesses are growing nicely and are profitable, and its balance sheet is dramatically stronger. We think at today’s stock price, the core insurance business is undervalued and we’re getting a free call option on Fairfax’s position in credit default swaps, which we think could appreciate substantially.

Financials: Revenue: $ 7.91 bnProfit Margin: 18,65%Operating Margin: 35.84%

Valuation Metrics: Fairfax S&P 500P/E 2.92 25.75

fairfax financial ISIN CA3039011026

FAIRFAx FINANCIAL SToCk PRICE

Institutional Investors:no institutional investors > 3%

Free Float: 98.59%

Fair Value: $ 400.00

Business: Traditional Canadian Insurance Com-pany (Property & Casualty Insurances)

Stock Information (08/13/2008):Price: $ 228.6952 Week Range: $ 343.00 – $ 179.12Dividend Yield: 5.00%Market Cap: $ 4.19 bn

USD

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 12 – September 08

»WHITNEy TILSoN - FAIRFAx«

leverage and lack of transparency. Which camp are you in?

Tilson: Very much the latter – we have a large short exposure to finan-cial stocks.

EVI: You have invested in Fairfax Financial (ISIN: CA3039011026). Can you briefly describe what that company does?

Tilson: It is a diversi-fied Canadian insurance company.

EVI: How did you become aware of this stock?

Tilson: We read about Fairfax a few years ago because it was targeted by short sellers. We ended up shorting it as well (quite profitably) because its insurance businesses were losing money and its balance sheet was weak. Following hurricanes Katrina and rita, we thought another bad hurricane could put them out of business.

EVI: What is your investment thesis for Fairfax?

Tilson: Today, Fairfax is a very diffe-rent company: its insurance businesses are growing nicely and are profitable, and its balance sheet is dramatically stronger. We think at today’s stock price, the core insurance business is un-dervalued and we’re getting a free call option on Fairfax’s position in credit default swaps, which we think could appreciate substantially.

Based on this, we first bought the stock last August around USD 200, saw it run up to USD 343, but since then it’s retreated to around USD 235, due prima-rily, I think, to general weakness amongst insurance stocks. We think the market is giving investors another opportunity to buy the stock at a great price.

EVI: How do you value Fairfax?

Tilson: We take book value, which was USD 252/share as of the end of Q2, add USD 20/share for the fair value of ICICI Lombard, and subtract the CDS

portfolio, which was valued at USD 679 million, or USD 37/share, as of July 25th, which yields USD 235/share of book value for the core business. Good in-surance companies like Fairfax are worth approximately 1.2-1.5x book, so that’s USD 282-USD 353. We don’t put a mul-tiple on the CDS portfolio – we simply add it to arrive at a range of intrinsic value of USD 319-USD 390.

EVI: There was con-siderable short inte-rest in Fairfax a while back. What was the short thesis?

Tilson: In addition to the reasons I cited above for our short, other shorts questio-

ned CEO Prem Watsa’s integrity and thought that the company was hiding losses in offshore entities (views we don’t share).

EVI: How strong is Fairfax’s balance sheet? Could Fairfax be hurt if the bear market continues?

Tilson: By any measure, Fairfax’s ba-lance sheet is very strong and rapidly getting stronger. For example, as of the end of Q2, Fairfax’s net debt to net total capital was a mere 10.4% vs. 36.9% as recently as the end of 2005. Prem Watsa has been very bearish for quite some time and has positioned Fairfax accordingly, so not only will the company weather any bear mar-ket, but will profit from it, thanks to the CDS portfolio.

EVI: Warren Buffett says to look for managements that have talent and integrity. Do the Fairfax managers pass the Buffett test?

Tilson: We think so. We have met with Prem Watsa, talked to people who know him well and read his annual letters for many years and he strikes us as a great businessperson with high integrity.

EVI: What were your biggest invest-ment mistakes?

Tilson: There are so many…Where do I start? We invested in Pillowtex, a textile

manufacturer coming out of bankrupt-cy and missed the fact that while in bankruptcy they had not moved their textile production offshore, so they quickly went back into bankruptcy – a so-called Chapter 22 (Chapter 11 twice). And we have lost our shirts owning retailers over the past year, thanks to not fully appreciating how the collapse of the housing market (which we predicted) would impact these companies. Fortunately, these losses have been largely offset by gains on our financial shorts.

EVI: What have you learned from these mistakes?

Tilson: Only buy stocks after they’ve finished going down – just kidding! Seriously, every mistake has a slightly different lesson. Big picture, be very careful buying low-quality businesses just because the stock looks cheap on a statistical basis. There are a lot of value traps out there.

EVI: What do you want to do 10 years from now?

Tilson: Mostly, keep doing what I’m doing now – as Buffett says, I tap dance to work every day. Still be healthy and fit enough to play pick-up basket-ball twice a week. Send my youngest daughter off to college. Make enough money to give away a lot more than I can afford to do now.

EVI: Thank you very much for the open interview!

Remark: The disclaimer note published on the last page of this edition is applicable to the entire content of this article.

Contact:Whitney R. Tilson T2 Partners LLC145 East 57th Street, Suite 1100New york, Ny 10022USAT: +1 212-386-7162F: +1 [email protected]

»We think at today‘s stock price,

the core insurance business of Fairfax

is undervalued.«

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 13 – September 08

No. 4 – Page 14 – September 08

Roberto Russo: Parmalat S.p.A. Since 2006 Roberto Russo is Chief Investment officer of Duemme SGR S.p.A., the asset

management company of Banca Esperia Group. For the 2nd time in a row he was speaker at the Value Investing Seminar in Italy. This year he presented Parmalat S.p.A. as stock idea.

Roberto Russo CIO and Portfolio ManagerDuemme SGR S.p.A.

his investment process starts with analysing three areas of market inef-ficiency: Obscure businesses (i.e. low analyst coverage), undesirable busines-ses (i.e. industry problems, subsidiary problems) and situations of motivated sellers and missing buyers.

Throughout his professional career roberto russo is regular member of AIAF and speaker on several value investing conferences, as he did for the 2nd time in a row at the Value In-vesting Seminar in Italy.

roberto russo was born in 1969 in naples. In 1995 he graduated in Eco-nomics at the University of naples with focus on finance and banking techniques. he has the Certificate AIAF (Italien Association of Financial Analysts) and the Certificate FEAAF (European Federation of Financial Analysts’ Association).

Since 2006 he is Chief Investment Of-ficer and portfolio manager of Duemme SGr S.p.A, which is the Milan based asset management company of Banca Esperia Group. Among the group, Duemme SGr is specialized in car-rying out asset management mandates from private clients and manages the Duemme Sicav portfolios.

His investment process starts with the analysis of three areas of market inefficiency: obscure businesses, undesirable businesses and situations of

motivated sellers but missing buyers.

products like yogurt, cream-based white sauces, desserts, cheeses and fruit-based drinks, with 2007 revenues of over EUr 3.8 bn. The group is present in twelve core countries, across five regions: Eu-rope, north America, Central and South America, Australia and South Africa. The company has a strong innovative tradition: the group developed leading-edge tech-nologies in the driving sectors of the food market, particularly in UhT milk, ESL (Extended Shelf Life) milk, functional milks, fresh juice-based drinks, functio-nal fruit drinks and cream-based white sauces. Today’s main Parmalat ratios are very interesting: At EUR 1.77 per share, EV/Sales 2007 is 0.51, EV/EBITDA is 5.4. (nestlé’s EV/Sales is 1.9x, EV/EBITDA is 11.3). Furthermore, Parmalat has a net cash position of EUr 1.3 bn, means 46% of its market cap. EVI: What are the company’s busi-ness prospectives?

Russo: During the first quarter of 2008 the Group profitability was affected by events and trends that were unexpected both in terms of nature and size. Increa-sing cost of raw materials and increasing prices for packaging and distribution influenced by the oil price eroded profit margins and made it necessary to adopt new price which were implemented only with difficulty and some delay. We are very confident that recent increases in milk prices gradually reflect on sales pri-ces. Strong indications about an increase in milk production seem to indicate a possible recovery of profit margins in the near future. Our worst case scenario considers an expected 3% compounded growth of sales for the next 3 years and EBITDA to be stable in 2008, with an expected 7% compounded growth in 2009 and 2010.

EVI: Parmalat’s home market and still most important market is Italy. How are the expansion opportunities in other countries?

EVI: Mr. Russo, in Bisceglie you pre-sented Parmalat (ISIN: IT0003826473) as an investment opportunity. How did you find that stock?

Russo: Screening, keyword searches in databases and reading the papers carefully are all techniques we use to identify potential ideas. Our invest-ment process starts from the analysis of three areas of market inefficiency: Obscure businesses (i.e. low analyst

coverage), undesirable businesses (i.e. industry problems, subsidiary problems) and situations of motivated sellers and missing buyers. Parmalat investment belongs to the last category.

EVI: Why do you see particular po-tential in just this stock?

Russo: Parmalat Group is one of the ma-jor players worldwide in the production and distribution of milk, mainstream dairy

»RoBERTo RUSSo - PARMALAT S.P.A.«

ThE EUrOPEAn VALUEInVESTOr

Business:One of the major players worldwide in the production and distribution of milk, main-stream dairy products and fruit-based drinks,

Stock Information (08/13/2008)Price: € 1.7752 Week Range: € 1.63 - € 2.61Dividend Yield: 8.00% (2008e) 5.98 % (2007)Market Cap: € 3.09 bn

Financials: Revenue: € 3.89 bnEBIT-Margin: 20.82 (2007)

Valuation Metrics:

Parmalat S&P mib

P/E 17.71 (2008e) 9.39 6.92 (2007) 13.62P/B 1.65 (2007) 1.26

Institutional Investors: 1) Fir Tree Inc. 3.38%2) JCD Management Corp. 3.09%3) JPMorgan Chase & Co. 3.03%

Free Float: 83.13%

Fair Value: € 2.73

Parmalat ISIN IT0003826473

INVESTMENT THESIS Parmalat has strong global and international brands what made the company to one of the major players in the production of milk and fruit-based drinks. In addition to its very important home market Italy, Parmalat is well positioned in north America, South America, Africa and Australia with potential for expansion in other countries.

Russo: As for the Parmalat Group, the Italian market accounts for 29% of total revenues and 32% of EBITDA. Further-more north America accounts for 36% of total revenues and 37% of EBITDA. Parmalat is a relevant brand also in South America, Africa and Australia. At present, thanks to its net cash position Parmalat may carefully look at business oppor-tunities for acquisitions of well-known branded companies which operate in the same markets, in order to take advantage of international synergies.

EVI: What are Parmalat’s fran-chises?

Russo: Parmalat offers milk products and fruit based drinks in several markets across the world, primarily under strong brand names.The brands portfolio inclu-des “Parmalat” and “Santàl” as global brands and many very strong internatio-nals brands. In order to understand the importance of Parmalat’s brands, you should consider that, on a yearly ave-rage, Parmalat products are used by 17 million Italian families and 200 million families in the world. And did you know that every year in the world 12 billion glasses of Parmalat milk and 1.5 billion glasses of Parmalat fruit-based drinks are consumed? This really means com-petitive advantages!

EVI: What are reasons for the cur-rent undervaluation?

Russo: The current world crisis, caused by the combination of subprime insol-vencies and the oil & commodities bubble provoked an irrational distrust of most investors in all assets, which were sold irrespectively of their fun-damentals (a so-called “motivated sel-lers and missing buyers” phase.) This situation is considered ideal for value investors, who constantly monitor risk/reward profiles and the “margin of safety” (the difference between the intrinsic value of the shares and the price at which they are able to buy them). We believe that buying with a large margin of safety (30% at least) is the best way to mitigate risk. Only after having concluded that our downside is well protected we consider the upside potential for most of our investments.One useful representation of such panic

waves is Graham‘s favorite allegory of “Mr. Market”. Today’s Mr. Market is extremely depressed and Parmalat is one of the shares he’s selling strongly below its intrinsic value….

EVI: Where do you see the fair va-lue?

Russo: With a valuation of 7.5x EBITDA (versus at least 10x of the main competi-tors) or 10x Pretax Free cash flow (versus at least 18x of the main competitors) we have a current valuation of EUr 2.23 per share plus a potential upside of EUr 0.5 per share, due to undisclosed claw-back and damage claims, assuming a 10%

recovery ratio on claw-backs and 5% on damages.

EVI: Thank you for the interview!

Contact:Roberto Russo Duemmes SGR S.p.A.Piazzetta M. Bossi 120121 MilanoItalyT: +39 02 88219-1F: +39 02 [email protected]

»RoBERTo RUSSo - PARMALAT S.P.A.«

PARMALAT SToCk PRICE

EUR

Remark: The disclaimer note published on the last page of this edition is applicable to the entire content of this article.

No. 4 – Page 15 – September 08

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 16 – September 08

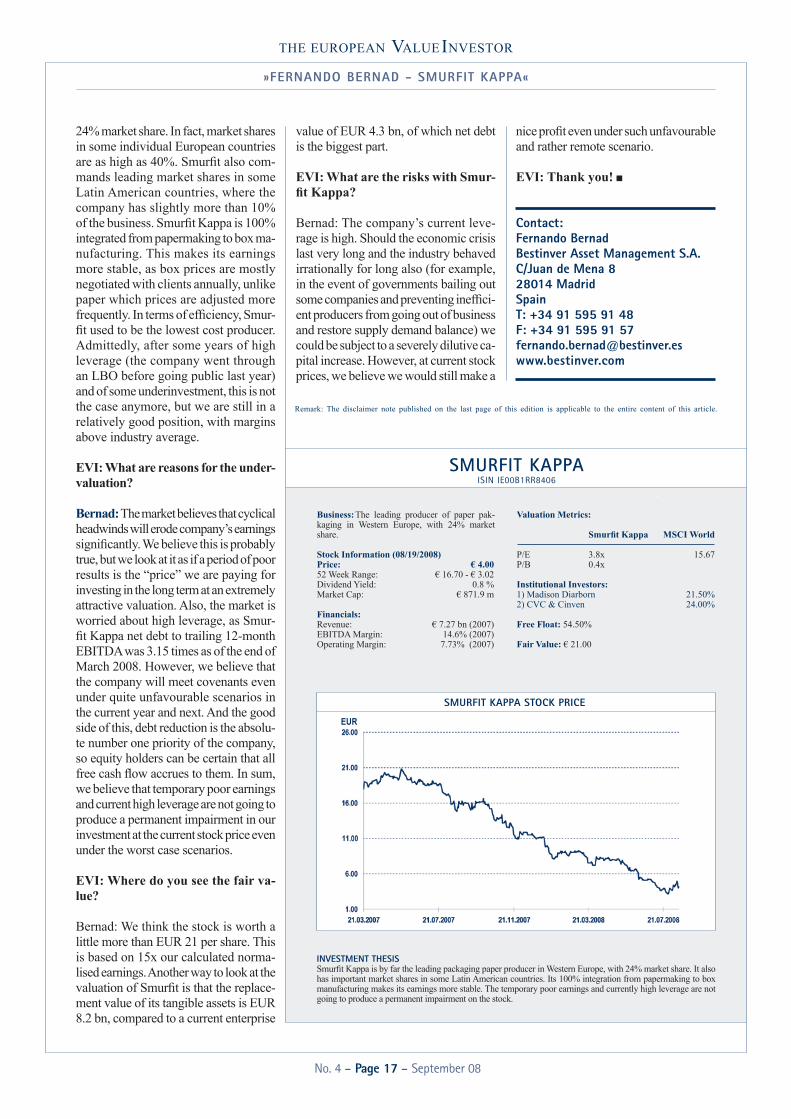

Fernando Bernad: Smurfit Kappa Fernando Bernad is fund manager with Bestinver Asset Management S.A. As one of Bestinver’s current

stock ideas he presented Smurfit kappa, the leading producer of packaging paper in Western Europe. knowing the packaging paper sector for years, the IPo of Smurfit kappa caught Bestinver’s eyes.

Fernando Bernad Fund ManagerBestinver Asset Management

ideas based on the theory of value. In 2005 he joined the Vetusta Group as investment director, leading a three-per-son team specialising in the value-style management of portfolios and funds. In his two years in charge at Vetusta he achieved average annual returns of around 30% on equities, always beating benchmark indices. he joined Bestinver in February 2007 along with Francisco García Paramés and Álvaro Guzmán, whom he considered the leading lights in the Spanish value school.

he has a Bachelor in Business Admi-nistration (summa cum laude, awarded jointly by ICADE, Madrid and northea-stern University, Boston) and is a CFA charter holder. He is fluent in English and reads German and French.

Following full-time internships at Pri-ce Waterhouse (Madrid, 1994), BBVA (Madrid, 1996), and DG Bank (Frank-furt, 1997), he started his professional career in 1998 in Frankfurt, where he worked alongside Álvaro Guzmán de Lazaro at the same asset management company, Value Management & re-search. It was here that he began to gain in-depth knowledge of the theories of value investing.

he then worked in the Spanish private equity sector as an Associate at BnP Paribas Leveraged Finance. Subse-quently he joined the analysis team at Banesto as a cyclicals analyst (steel and oil sectors) and later formed and led the analysis team at Interdin, who-se strategy was focused on investment

Fernando Bernad joined the team of Bestinver along Francisco García Paramés and Álvaro Guzmán de Lazaro in February 2007

– a particular packaging paper made out of wood, as opposed to using recycled paper - gives a return below the cost of capital of the marginal producer. This has been the case for long, due to endemic overcapacity in the US and, lately, very unfavourable exchange rate in Europe. Should this situation change to impro-ve, this would increase our fair value of Smurfit Kappa. At EUR 4.2 per share, the stock is trading below 3 times our estimated normalised earnings.

EVI: How do you see the market situa-tion and the competion situation?

Bernad: We are facing a challenging situation going forward, as demand is weakening precisely at a time when se-veral capacity expansion projects are under way to be commissioned by end 2008 and 2009. This will exert strong pressure on paper prices. In our view, however, capacity additions will be par-tially compensated with shut-downs of inefficient sites. This is even more li-kely in a scenario of paper prices being (temporarily) low. We believe in ratio-nal business behaviour, and expect that producers will not invest in those as-sets under-earning its cost of capital. The industry, today still fragmented, is gradually consolidating, and leading producers like Smurfit Kappa, Mondi (ISIN: GB00B1CRLC47), DS Smith (ISIN: GB0008220112), SCA (ISIN: DE0006889801) and International Paper (ISIN: US4601461035) already account for more than 50% share of the Western European market. These companies have undertaken permanent closure of sites in the past few years, and we expect will continue to manage their capacity plans prudently for the shake of overall industry profitability.

EVI: What competitive advantages does Smurfit Kappa have?

Bernad: Smurfit Kappa is by far the lea-ding producer in Western Europe, with

EVI: Mr. Bernad, how did you come aware of Smurfit Kappa (ISIN: IE00B1RR8406)?

Bernad: We know the packaging paper sector for years already, and looked at Smurfit Kappa soon after the IPO in March 2007. We became interested in the company as we saw the stock price fall from an IPO price of EUr 16.5 per share and a peak in May 07 of EUr 20 per share to just above EUr 10 per

share by the end of last year.

EVI: Why do you see potential in just this stock

Bernad: We value cyclical stocks based on normalised (“mid-cycle”) earnings. We normalise earnings based on the estimated per ton profit at which the marginal pro-ducer makes a modest return on capital employed. In case of Smurfit Kappa we assume that profit per ton of Kraftliner

»FERNANDo BERNAD - SMURFIT kAPPA«

ThE EUrOPEAn VALUEInVESTOr

Business:The leading producer of paper pak-kaging in Western Europe, with 24% market share.

Stock Information (08/19/2008)Price: € 4.0052 Week Range: € 16.70 - € 3.02Dividend Yield: 0.8 %Market Cap: € 871.9 m

Financials: Revenue: € 7.27 bn (2007)EBITDA Margin: 14.6% (2007)Operating Margin: 7.73% (2007)

Valuation Metrics:

Smurfit Kappa MSCI World

P/E 3.8x 15.67P/B 0.4x

Institutional Investors: 1) Madison Diarborn 21.50%2) CVC & Cinven 24.00%

Free Float: 54.50%

Fair Value: € 21.00

smurfit kaPPa ISIN IE00B1RR8406

INVESTMENT THESIS Smurfit Kappa is by far the leading packaging paper producer in Western Europe, with 24% market share. It also has important market shares in some Latin American countries. Its 100% integration from papermaking to box manufacturing makes its earnings more stable. The temporary poor earnings and currently high leverage are not going to produce a permanent impairment on the stock.

EUR

24% market share. In fact, market shares in some individual European countries are as high as 40%. Smurfit also com-mands leading market shares in some Latin American countries, where the company has slightly more than 10% of the business. Smurfit Kappa is 100% integrated from papermaking to box ma-nufacturing. This makes its earnings more stable, as box prices are mostly negotiated with clients annually, unlike paper which prices are adjusted more frequently. In terms of efficiency, Smur-fit used to be the lowest cost producer. Admittedly, after some years of high leverage (the company went through an LBO before going public last year) and of some underinvestment, this is not the case anymore, but we are still in a relatively good position, with margins above industry average.

EVI: What are reasons for the under-valuation?

Bernad: The market believes that cyclical headwinds will erode company’s earnings significantly. We believe this is probably true, but we look at it as if a period of poor results is the “price” we are paying for investing in the long term at an extremely attractive valuation. Also, the market is worried about high leverage, as Smur-fit Kappa net debt to trailing 12-month EBITDA was 3.15 times as of the end of March 2008. however, we believe that the company will meet covenants even under quite unfavourable scenarios in the current year and next. And the good side of this, debt reduction is the absolu-te number one priority of the company, so equity holders can be certain that all free cash flow accrues to them. In sum, we believe that temporary poor earnings and current high leverage are not going to produce a permanent impairment in our investment at the current stock price even under the worst case scenarios.

EVI: Where do you see the fair va-lue?

Bernad: We think the stock is worth a little more than EUr 21 per share. This is based on 15x our calculated norma-lised earnings. Another way to look at the valuation of Smurfit is that the replace-ment value of its tangible assets is EUr 8.2 bn, compared to a current enterprise

value of EUr 4.3 bn, of which net debt is the biggest part.

EVI: What are the risks with Smur-fit Kappa?

Bernad: The company’s current leve-rage is high. Should the economic crisis last very long and the industry behaved irrationally for long also (for example, in the event of governments bailing out some companies and preventing ineffici-ent producers from going out of business and restore supply demand balance) we could be subject to a severely dilutive ca-pital increase. however, at current stock prices, we believe we would still make a

nice profit even under such unfavourable and rather remote scenario.

EVI: Thank you!

Contact:Fernando Bernad Bestinver Asset Management S.A.C/Juan de Mena 828014 MadridSpainT: +34 91 595 91 48F: +34 91 595 91 [email protected]

»FERNANDo BERNAD - SMURFIT kAPPA«

SMURFIT kAPPA SToCk PRICE

Remark: The disclaimer note published on the last page of this edition is applicable to the entire content of this article.

No. 4 – Page 17 – September 08

ThE EUrOPEAn VALUEInVESTOr

No. 4 – Page 18 – September 08

Victor Fasciani: Vulcan Materials Victor Fasciani is Senior Securities Analyst at Sellers Capital LLC, where he also manages the

Praetorian Value Fund, launched by him in 2004 Currently he sees potential in aggregate producing companies like Vulcan Materials, which he presented in Bisceglie.

Victor FascianiSenior Securities AnalystSellers Capital, LLC

Before the foundation of Praetorian he spent several years in merchant banking and consulting in Eastern Europe. From May 1993 through June 1994 he was a Senior Consultant with East West resources Corpora-tion in Potomac, Maryland. In that capacity Mr. Fasciani, who is fluent in russian, led consulting projects in Moscow with a consortium of firms. In June 1994 he co-founded novacor, Inc. in McLean, Virginia, serving as its President.

he lead projects in the telecommu-nications, manufacturing, and com-mercial construction industries with various corporate partners including Deutsche Telecom, haliburton, and Joy Global.

Victor Fasciani received his B.A. in Economics in 1987 from Villanova University and completed graduate studies in International relations and Economics at the Johns hopkins School of Advanced International Studies in Washington, DC.

In 1999, Mr. Fasciani founded Prae-torian Investments, LLC, managing separate accounts with a value ap-proach for five years before launching Praetorian Value Fund, a value orien-ted hedge fund. he was asked to join Sellers Capital, LLC by Fund Manger Mark Sellers in late 2007 as a Senior Securities Analyst and continues to manage Praetorian Value Fund, LLC as an affiliated Fund of Sellers Capital, LLC.

In 2007, Victor Fasciani joined the team of Mark Sellers as Senior Securities Analyst, where he continues to manage the Praetorian

Value Fund, launched by him in 2004.

Fasciani: I became interested in Vul-can Materials early in 2007, when they acquired one of the companies in my portfolio, Florida rock Indu-stries. Vulcan Materials possesses what we look for in larger companies: wide moat characteristics. The most attractive companies in the industry own mines or quarries closest to the point of consumption.

Vulcan Materials is one of those com-panies in the U.S. at the top of the heap. Furthermore the U.S. infrastructure is in great need of repair and expan-sion. The American Society of Civil Engineers gives U.S. infrastructure extremely low grades, and has war-ned of the need for very substantial investment in infrastructure for the health of the economy.

EVI: Are there expansion possibi-lities for Vulcan Materials in other countries?

Fasciani: Vulcan’s operations are all within the U.S., primarily the hig-her growth areas of the Southeast, Southwest, and California; we do not expect the company to expand outside of the U.S.

EVI: How is the competitive situati-on? Will there be a consolidation in the market?

Fasciani: The aggregate industry is what we call a “globally local busi-ness”. Each mine or quarry operates within its limited geographic area since aggregate is so expensive to transport economically, even short distances. Thus the company with the most strategically located operation in its local market has a major advan-tage. The larger companies replicate this throughout several markets. We believe there will be consolidation in the industry. In fact, Vulcan’s purchase of Florida rock has been viewed as a

EVI: Mr. Fasciani, you presented aggregate producing companies as investment opportunities. What‘s your background for this?

Fasciani: Aggregate is a broad cate-gory of materials describing crushed stone, gravel, and sand. They have been used for thousands of years, at least since ancient roman times, for the construction of roads, building, bridges, and other structures. Aggre-

gates are key components of concrete, asphalt concrete, and substrate.

In the United States alone, over 2.5 Billion tons of aggregate is produced annually, with a market value of ap-proximately USD 6 bn.

EVI: As stock idea you have introduced Vulcan Materials (ISIN: US9291601097). When and how did you come aware of that company?

»VICToR FASCIANI - VULCAN MATERIALS«

ThE EUrOPEAn VALUEInVESTOr

Business:Vulcan Materials Company provides essential infrastructure materials required by the U.S. economy. Vulcan is the nation‘s leading pro-ducer of construction aggregates.

Stock Information (08/19/2008)Price: $ 72.6452 Week Range: $ 49.39 - $ 96.07Dividend Yield: 2.62% (2008e) 2.33% (207) Market Cap: $ 7.85 bn

Financials: Revenue: $ 3.09 bn (2007)EBIT-Margin: 22.85% (2007)Net Margin: 21.91% (2007)

Valuation Metrics:

Vulcan Materials S&P 500

P/E 19.31 25.75

Institutional Investors: none above 5%

Fair Value: $ 90.00

vulcan materials ISIN US9291601097

INVESTMENT THESIS Vulcan Materials is the leading producer of aggregates in the U.S. The company owns some of the best strategi-cally located mines and quarries in each of the regional markets in which they operate. Through the acquisition of Florida rock Industries in 2007 Vulcan could expand its strong position. We believe the current undervalua-tion is a function of the overall environment for equities coupled with a slowdown in the U.S. housing market. There are signs that the commercial construction market is slowing also, and this should not be ignored, but we believe that Vulcan is attractively valued and should perform well over a three to five year period

USD

defensive move to stave off acquisiti-on by larger rivals. We do not believe they can prevent this from happening if shareholder value is maximized through an attractive offer.

The larger cement and aggregate companies in the world seeking a strong strategic presence in the U.S. market would be the most logical buyers, including Holcim (ISIN: CH0012214059), CEMEX (ISIN: MXP225611567), and Hanson PLC (ISIN: GB0033516088).

EVI: Which are Vulcan Materials’ franchises?