2007-2009 Crisis Lecture 5 - Brandeis...

103

2007-2009 Crisis Lecture 5 FIN254f: Financial Manias and Crises Blake LeBaron International Business School Brandeis University Spring 2010 (Readings: See last slide.)

Transcript of 2007-2009 Crisis Lecture 5 - Brandeis...

2007-2009 CrisisLecture 5"

FIN254f: Financial Manias and Crises"Blake LeBaron"

International Business School"Brandeis University"

Spring 2010"(Readings: See last slide.)

Outline" Connections to what we've done"

Bubbles, pricing and psychology" Contributing factors" History"

Pictures" Timeline"

Causes and mechanisms" Bubbles and beliefs again" Policy questions"

Historical ThoughtsMinsky/Kindleberger"

Global bubble/bust cycle" Price increases/Risk pricing decreases" Credit expands" Price crashes -> macro implications"

Behavioral Pieces" Gambler’s fallacy"

Short term data" Ambiguity aversion"

Fear of all things “securitized”" Overconfidence" Herding"

“similar strategies”""

Contributing Factors" Global real estate bubble/bust" Credit expansion/contraction" International capital flows" Classic banking crisis (U.S. repo market)" New financial products"

Asset backed securities (ratings)" New over the counter derivatives"

U.S. monetary policy"

Finance Mechanisms Specific to this Crisis"

Securitization" Risk misperceptions/ratings agencies" Knightian uncertainty"

Internal models and reserve requirements" Firesale enhancer" Amplification mechanism"

Credit default swaps / OTC derivatives" Facilitate tail risk trading and exposures"

History"

Prices" Macro variables" Timeline"

Prices"

Stock prices" Volatility/risk" Interest rate spreads"

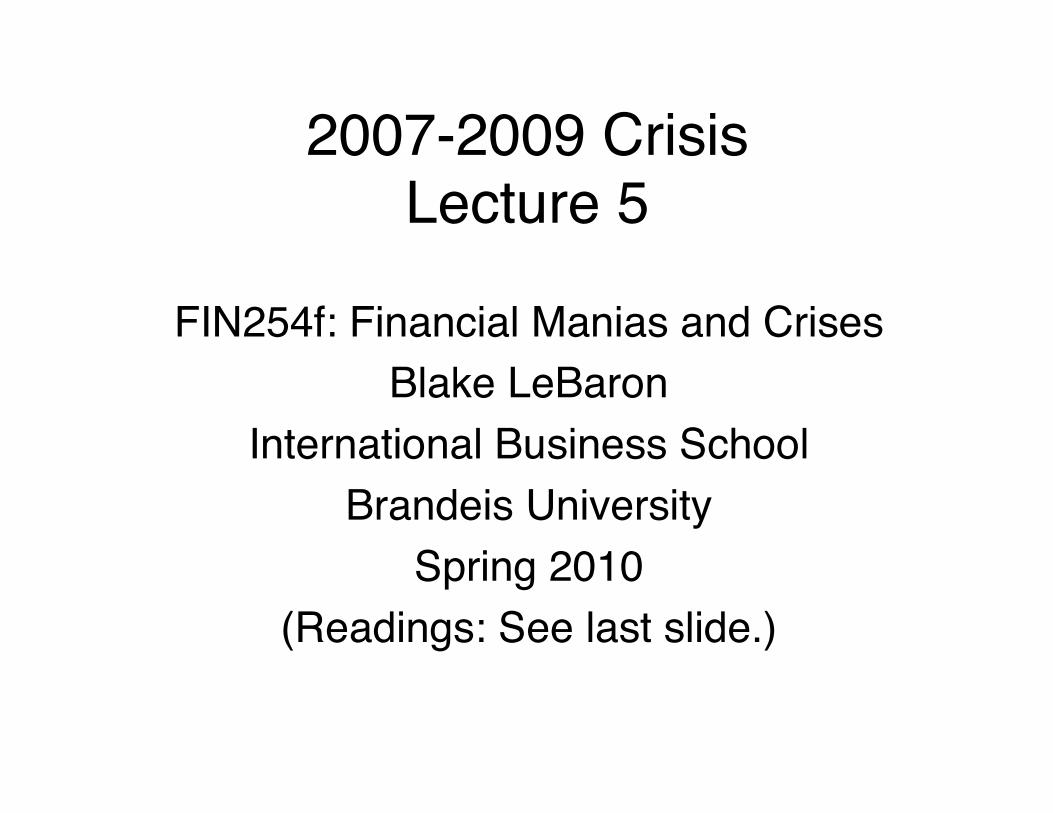

S&P 500"

Yahoo

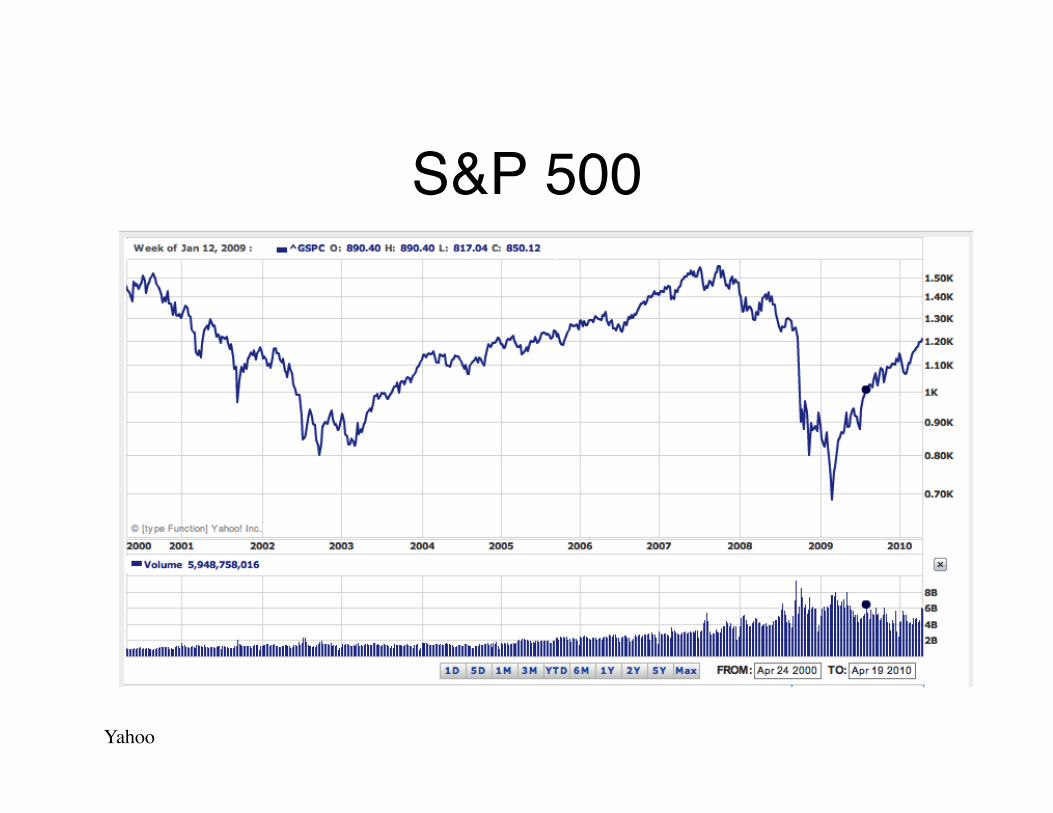

Hang Seng"

Yahoo

Reinhart/Rogoff(2009)

Volatility (VIX)"

Yahoo

Long/Short Volatility"

Acharya et al.(2010)

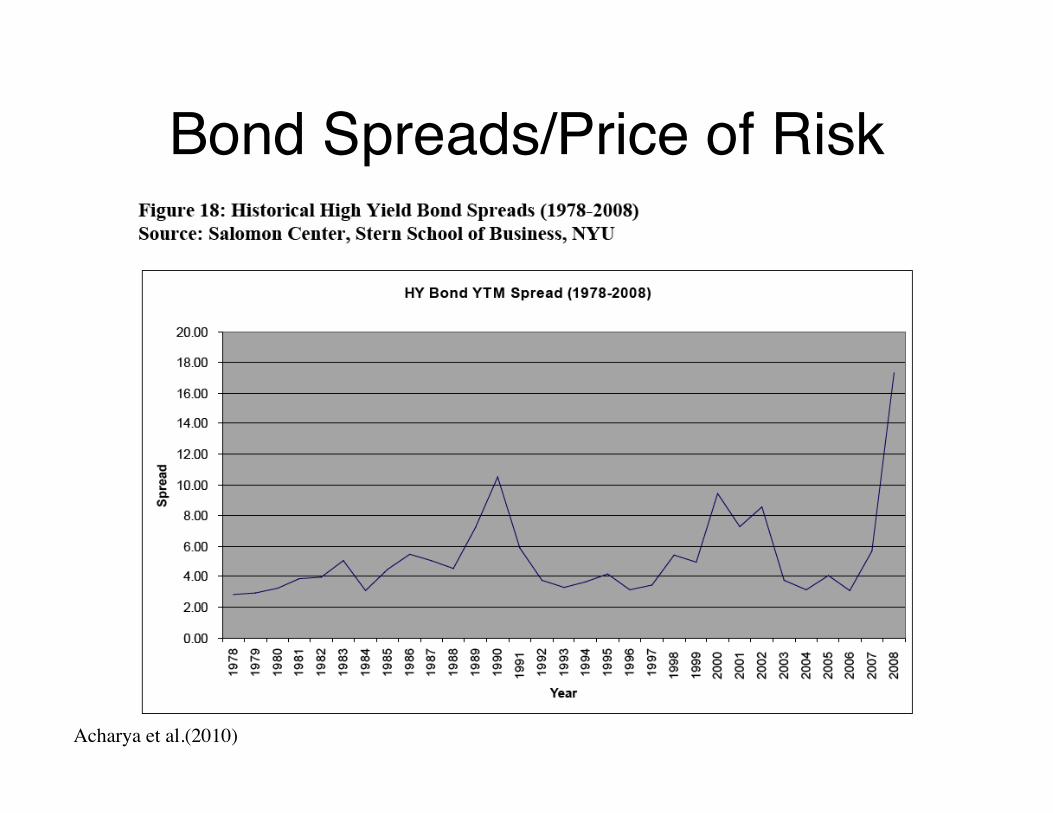

Bond Spreads/Price of Risk"

Acharya et al.(2010)

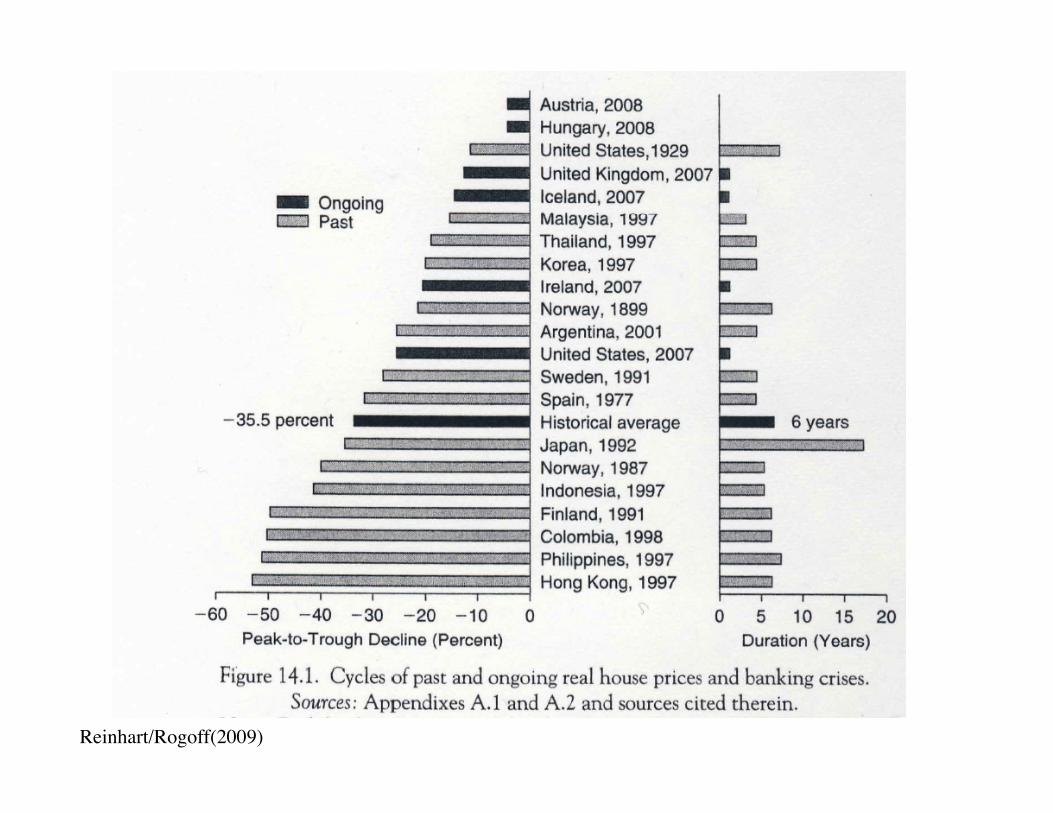

Reinhart/Rogoff(2009)

U.S. House Prices (Shiller)"

Price/Rent - Mean"

Acharya et al.(2010)"

Tiered Price Indices: Tulips??"

calculatedriskblog.com

Total U.S. Wealth Loss"

Dot Com bubble: $10 trillion" Real estate: $3 trillion"

House Prices by Country"

Loungani(2010)

Reinhart/Rogoff(2009)

Reinhart/Rogoff(2009)

Macro Activity"

GDP" Exports" Credit" Public debt"

Reinhart/Rogoff(2009)

Reinhart/Rogoff(2009)

GDP"

Duration, GDP Return: Post WWII (above) versus Depression(lower)"

Reinhart/Rogoff(2009)

Reinhart/Rogoff(2009)

Unemployment"

Export Growth"

Reinhart/Rogoff(2009)

US Household Debt/GDP"

Public Debt"

Reinhart/Rogoff(2009)

Timelines"

Historical perspectives" Quick timeline" Details"

Global Crises"

Reinhart/Rogoff(2009)

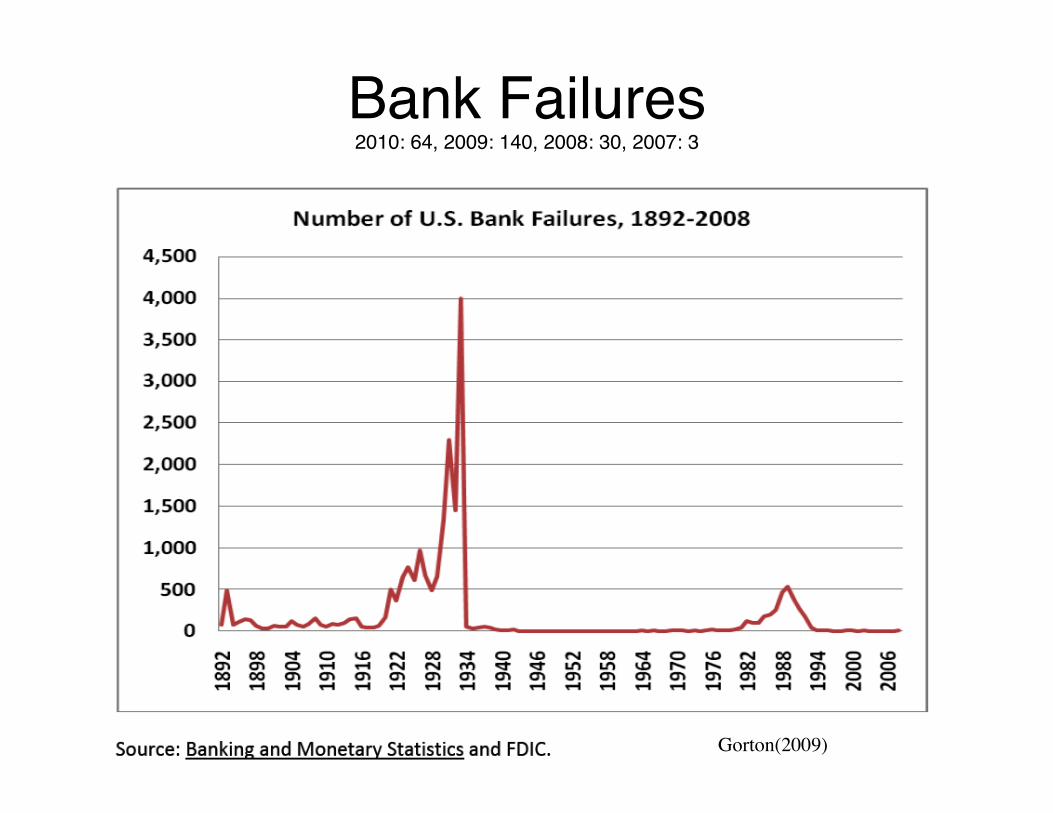

Bank Failures2010: 64, 2009: 140, 2008: 30, 2007: 3"

Gorton(2009)

U.S. Prehistory"

Bank crises of the 1800's" The Great Depression (1930's)" Latin American debt crisis (1980's)" Savings and Loan crisis (1980's-1990's)" Long Term Capital Management (1998)"

Rough Time Line" June 10th-12th, 2007: Moody's downgrades ratings

on $5 billion of RMBS (Mortgage backed securities)" June 20th, 2007: Two Bear Stearns hedge funds

invested in subprime mortgages in trouble" Aug 2007: Quant hedge fund turmoil and

deleveraging in equity markets" August 17, 2007: Run on Countrywide Bank" September 9th, 2007: Run on Northern Rock Bank

(4-5% of deposits withdrawn)"

Rough Time Line"

March 7-16, 2007: Federal Reserve increases term auction lending facility by $40 billion"

March 17: Bear Sterns bought by JP Morgan"

July 11th, 2008: IndyMac Bank seized by regulators"

Rough Time Line" September 2008: Lehman bankruptcy" September 2008: Goldman Sachs and

Morgan Stanley become banks" October/November (2008)"

Global equity markets fall drastically" Central banks taking equity stakes in banks" Buying many securities " U.S. auto bailout considered" All countries considering fiscal stimulus packages"

More Timeline" Nov 9th, Iceland collapses" Dec 11th, Madoff arrested" Feb 17th, Obama signs stimulus" March 9th, 2009, Stock market bottoms"

Dow = 6500" May 2009, Chrysler bankruptcy" June 2009, banks begin repaying bailouts" August, 2009, stocks recovering, Dow 9500,

signs of recovery"

More Timeline" November 2009, unemployment still

high, foreclosures hit record, (double dip?)"

December 14, Citibank and Wells Fargo return TARP"

Spring 2010: " Recession ending?? " Dow 11,000"

Outline" Connections to what we've done"

Bubbles, pricing and psychology" Contributing factors" History"

Pictures" Timeline"

Causes and mechanisms" Bubbles and beliefs again" Policy questions"

Causes and Mechanisms" Financial innovation"

Securitization" OTC derivatives (Credit default swaps)" Regulation changes" Size of financial services industry"

Compensation and incentives" Originate and distribute" Cash bonuses "

International capital flows" Real estate ownership, and bubbles" Bank runs, haircuts, and repo" Monetary policy"

Securitization "

Portfolios of cash flow streams" Mortgages (residential and commercial)" Student loans" Credit cards"

Form into bonds - sell to investors" Tranching"

Tranches and Ratings"

A

B

AAA

The Power of Securitization"

Large scale diversification" Concentrate losses in low rated

tranches" High rated tranches (hopefully) low risk"

Tranches and RatingsCDO^2"

A

B

AAA

AAA

Other Applications"

Commercial mortgages" Credit cards" Student loans"

Ratings"

Rating is tricky" Key parameters"

Comovements in defaults" Comovements in house price declines" Quality of mortgage pool"

Conflicts of interest" AAA rating is special"

Swagel (2009) The Financial Crisis: An Inside View

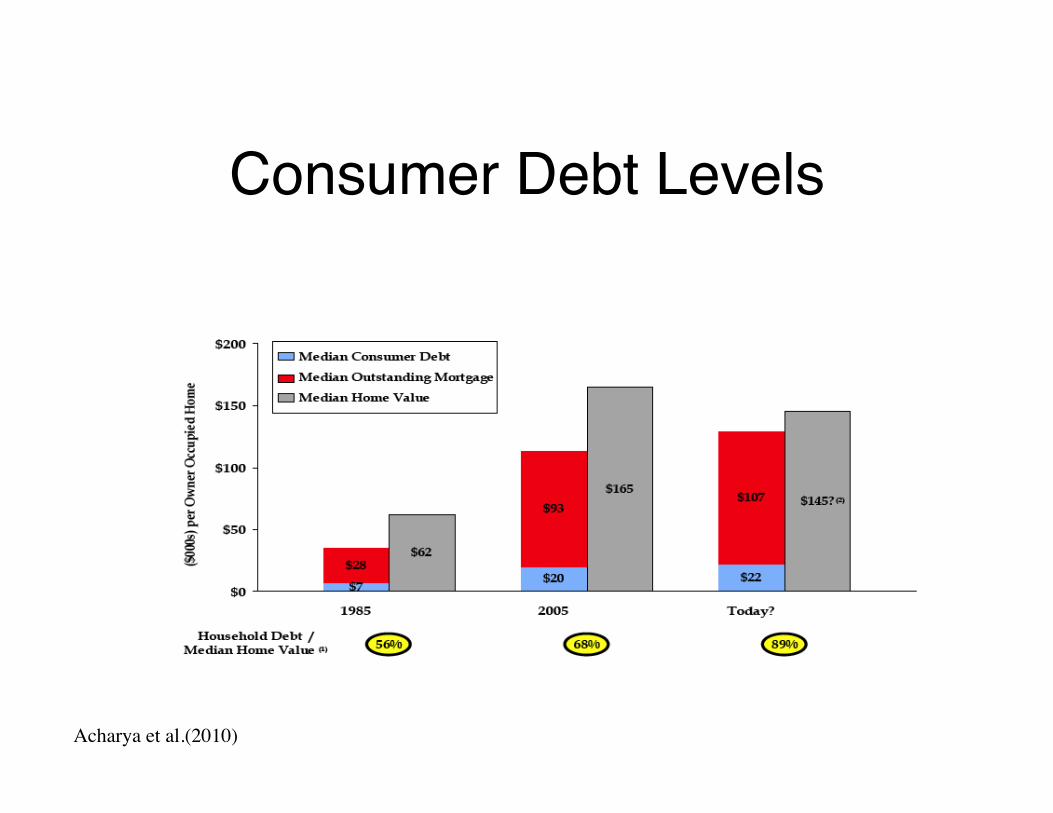

Consumer Debt Levels"

Acharya et al.(2010)

Massachusetts Foreclosures"

Gerardi et al. 2008

CDO Pricing and Implied Defaults"

Acharya et al.(2010)

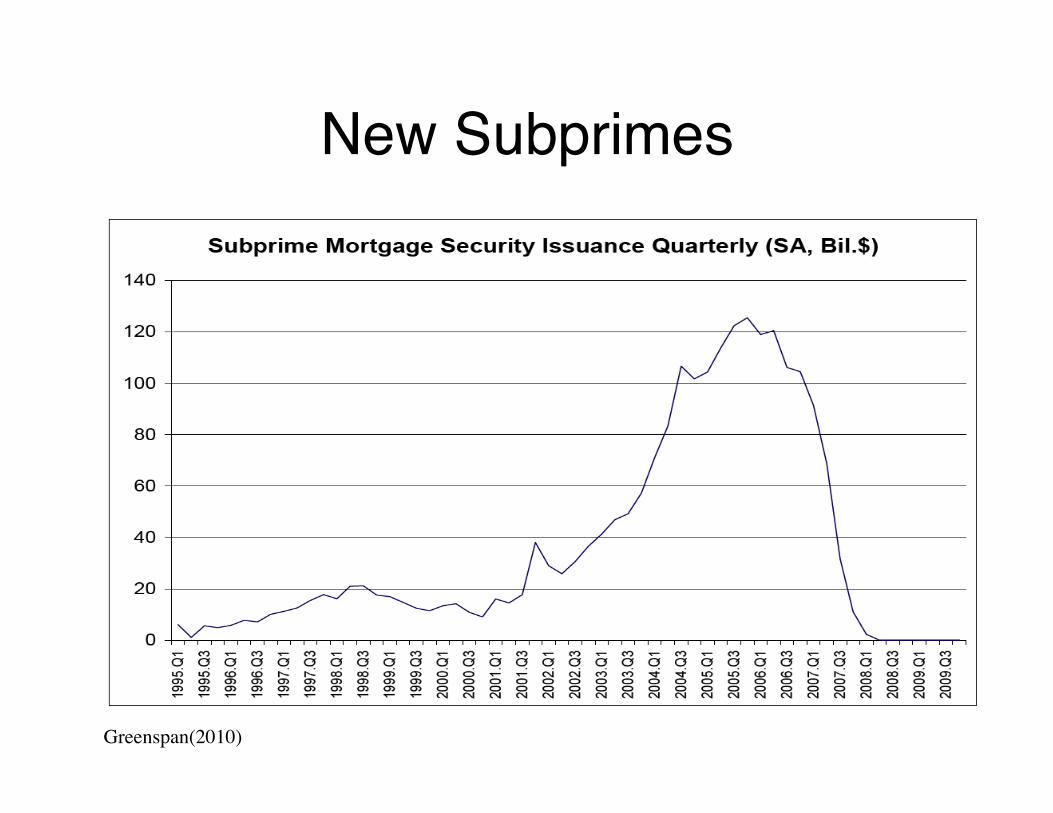

New Subprimes"

Greenspan(2010)

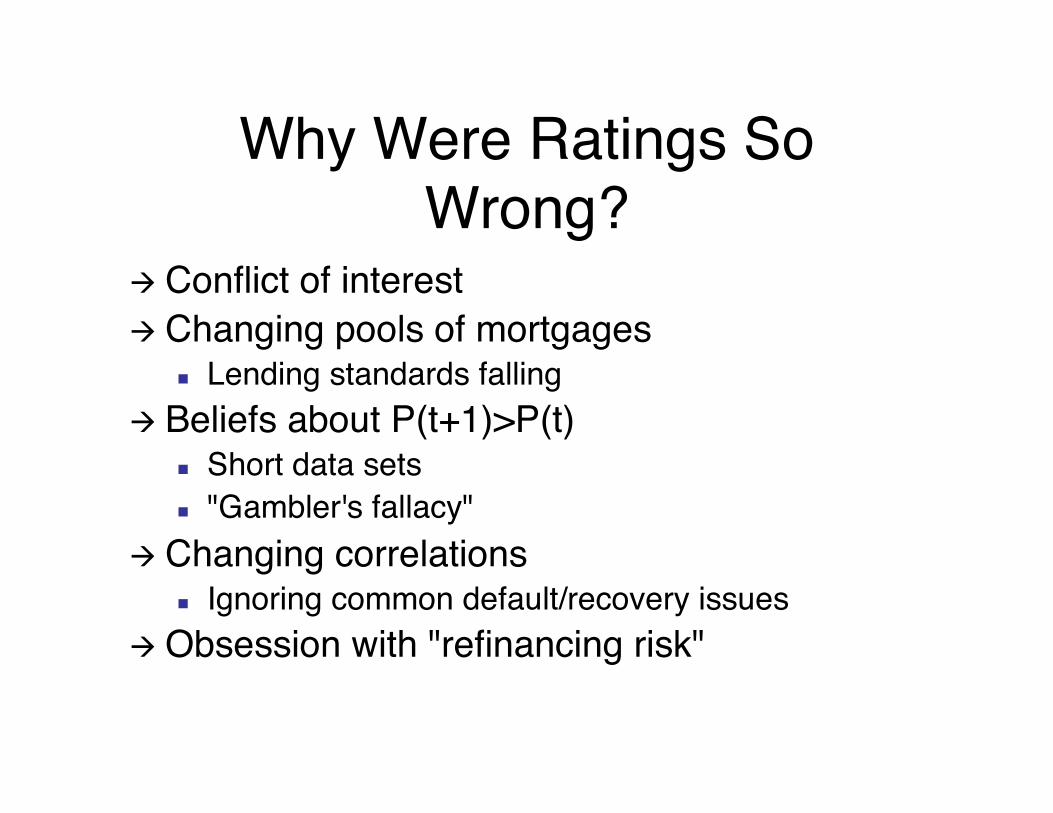

Why Were Ratings So Wrong?"

Conflict of interest " Changing pools of mortgages"

Lending standards falling" Beliefs about P(t+1)>P(t)"

Short data sets" "Gambler's fallacy""

Changing correlations " Ignoring common default/recovery issues"

Obsession with "refinancing risk""

Over the Counter Derivatives" Credit default swaps (CDS)"

Pays off when bond defaults" Insure against defaults"

Can make lower rated stuff appear like AAA if counter-party has AAA rating"

Investors write “deep out of the money” options (AIG)"

Key component in “Magnetar trade”"

OTC Markets"

What’s bad about OTC markets?" No public pricing information" No public position (open interest)

information" Counter-party risk"

Credit Default Swaps"

What’s special about CDS’s?" Ultimate tail instrument" Does this encourage the writing of naked

options?" How big a piece of the story is this?"

Selling insurance "

Financial Regulation" Glass/Steagall Act"

Depression (1933) banking regulation" Establishes FDIC" Removes risky securities trading from banks" Repealed in 1999"

Banking history" 1930-1960's: period of calm in U.S., why?"

Financial Regulation"

Basel II, and internal models" Reserve requirements set according

internal models of risk exposure" Often Value-at-Risk (VaR) based"

Impact" Volatility goes up -> required reserves

increase" Countercyclical credit "

Financial Regulation"

Leverage " SEC 15c3-1: The net capital rule" 1975-2004: Mandated capital liquidity rule

for broker dealers" Eliminated in 2004 "

Mark to market: FASB 157" Balance sheets must reflect current market

values of traded assets"

Leverage Changes?"

Lo and Mueller(2010)"

Size of Financial Services Industry"

Claim: Financial services are just too big" Recent increase in size not sustainable" Data: Increases are steady, and go back to

WWII" Possible explanation:"

Consume a greater share of income as income increases"

Reverse of food"

Size of Financial Services"

Greenspan(2010)

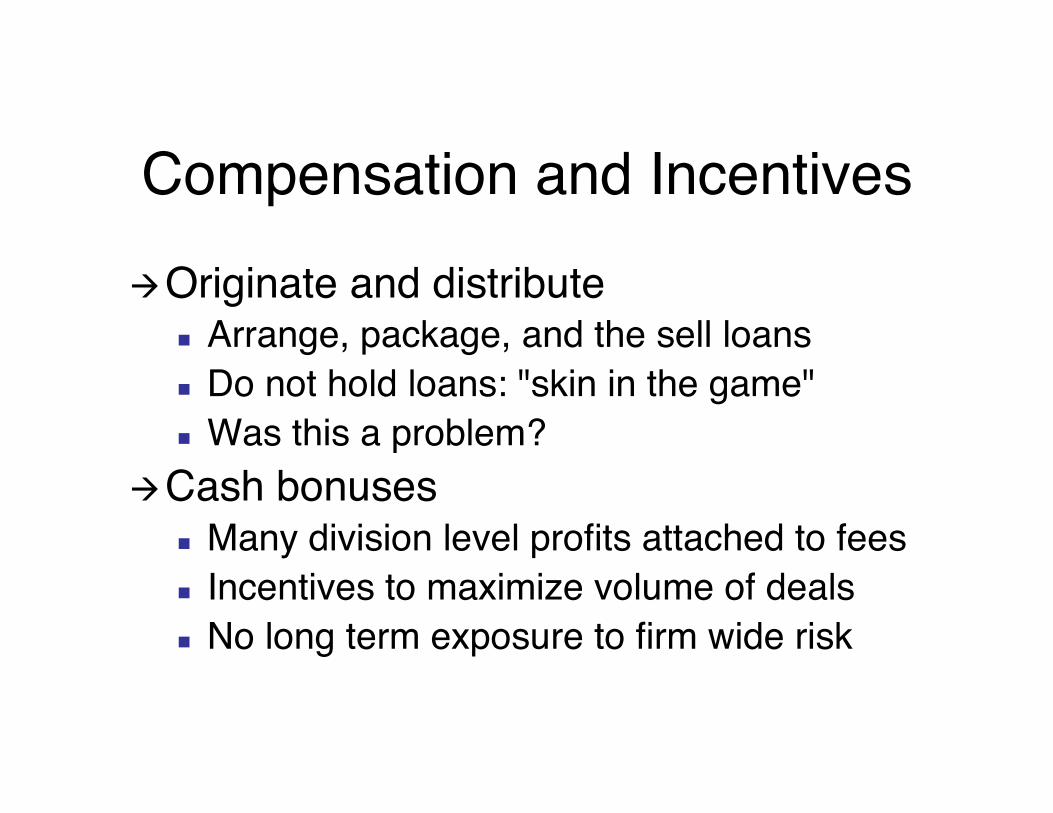

Compensation and Incentives" Originate and distribute"

Arrange, package, and the sell loans" Do not hold loans: "skin in the game"" Was this a problem?"

Cash bonuses" Many division level profits attached to fees" Incentives to maximize volume of deals" No long term exposure to firm wide risk"

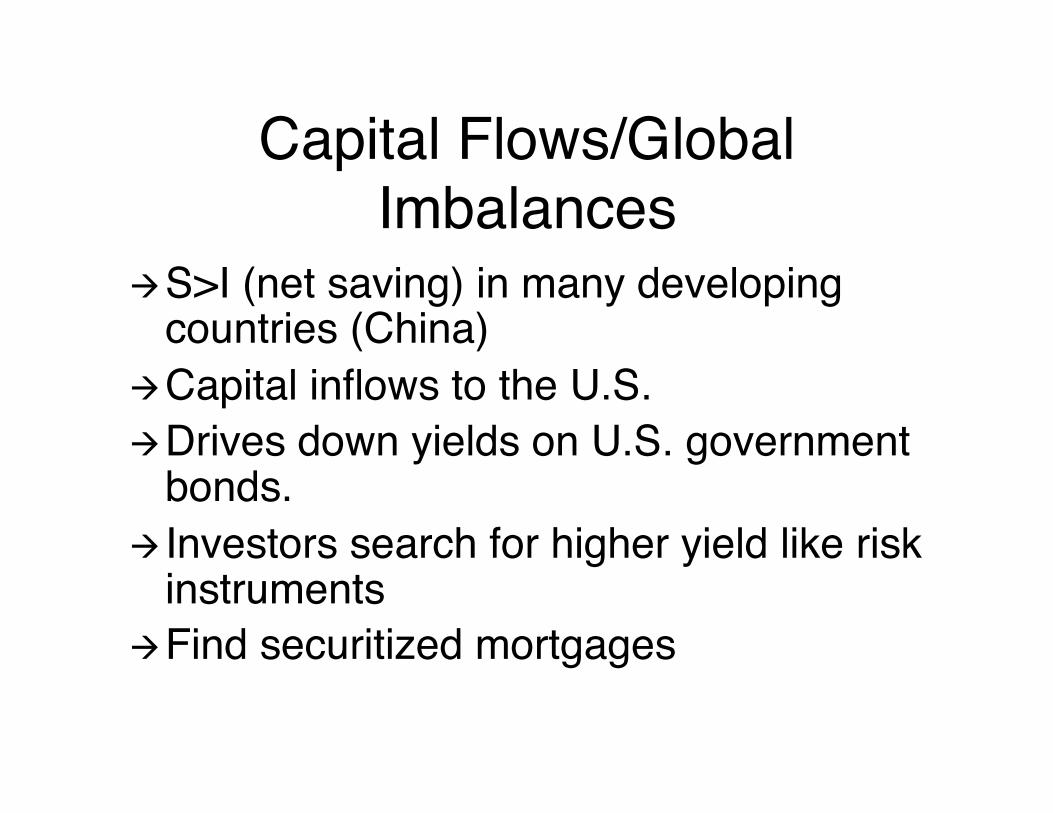

Capital Flows/Global Imbalances"

S>I (net saving) in many developing countries (China)"

Capital inflows to the U.S." Drives down yields on U.S. government

bonds." Investors search for higher yield like risk

instruments" Find securitized mortgages"

International Capital Flows"

Foreign savings feed U.S. consumption" Large demands for U.S. treasuries" Keeps U.S. interest rates low"

Problems with the Capital Flows Story"

Why did AAA bad assets stay with U.S. financials, and not with foreign governments?"

Other surplus countries hit:" Switzerland (UBS)" Netherlands (ABM Amro)" Germany (West LB, Deutsch Bank)"

Timing: Why didn’t this start earlier for the U.S.?"

Asset Backed CP/Equity"

Acharya(2010)"

Connections with House Bubbles(top countries) and CA/GDP(2006)"

Iceland, -25%" Spain, -10%" New Zealand, -9%" Australia, -7%" UK, -6%" US, -5%" Hungary, -4%"

Global Financial Networks"

The nature of global financial markets has changed" Larger global hubs" More interconnected"

Financial Networks : 1985"

Haldame(2009)

Financial Networks:2005"

Haldame(2009)

Real Estate Ownership and Bubbles"

Expansion of ownership " U.S. Department of Housing and Urban

development expands affordable housing goals"

On going from late 1980’s - 2006"

Home Ownership Rates"

58

60

62

64

66

68

70

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

Year

Ow

ne

rsh

ip R

ate

(%

)

U.S. Census and Wikipedia

Repos/Haircuts and Bank Runs"

What is the Repo market?" Shadow banking" Depositors: Institutional investors temporary cash

holding" Bank-like entities: Banks and investment banks" Mechanism: Repo"

Note: Most data on the repo market is hidden, or hard to find"

How Does Repo Market Work?"

Hedge fund deposits money with bank (investment bank, IB, and broker-dealers, BD)"

Receives collateral (1+haircut)*AAA bonds" IB/BD receives interest (6%), and pays

interest (3%) and is happy" (Note: connection to traditional banking) "

IB/BD operates with rolling short term (overnight) credit in repos"

Example: Haircut = 0" Set up repo for 100 billion"

Receive 100 billion in cash, set aside 100 billion (AAA’s) in collateral "

Take cash and purchase 100 billion of AAA’s" Receive another 100 billion in cash using these as

collateral " Repeat"

This is a kind of reserve banking with zero reserve requirements"

Reserve requirements related to haircuts"

AAA’s" Standard repo based on U.S. treasuries" Moves to CDO’s and other engineered

AAA’s" Why the change?"

Growing demand" Foreign governments (China)" Other derivative transactions"

Market working to meet this demand by engineering more AAA stuff"

Picture of Relative Shadow/Traditional Size"

Gorton(2010)

BD and IB Balance Sheets"

Assets" Mostly long term positions"

Liabilities" Mostly short term commercial paper

(overnight)" Collateral is AAA securitized debt" If lending stops, in trouble (like a bank)"

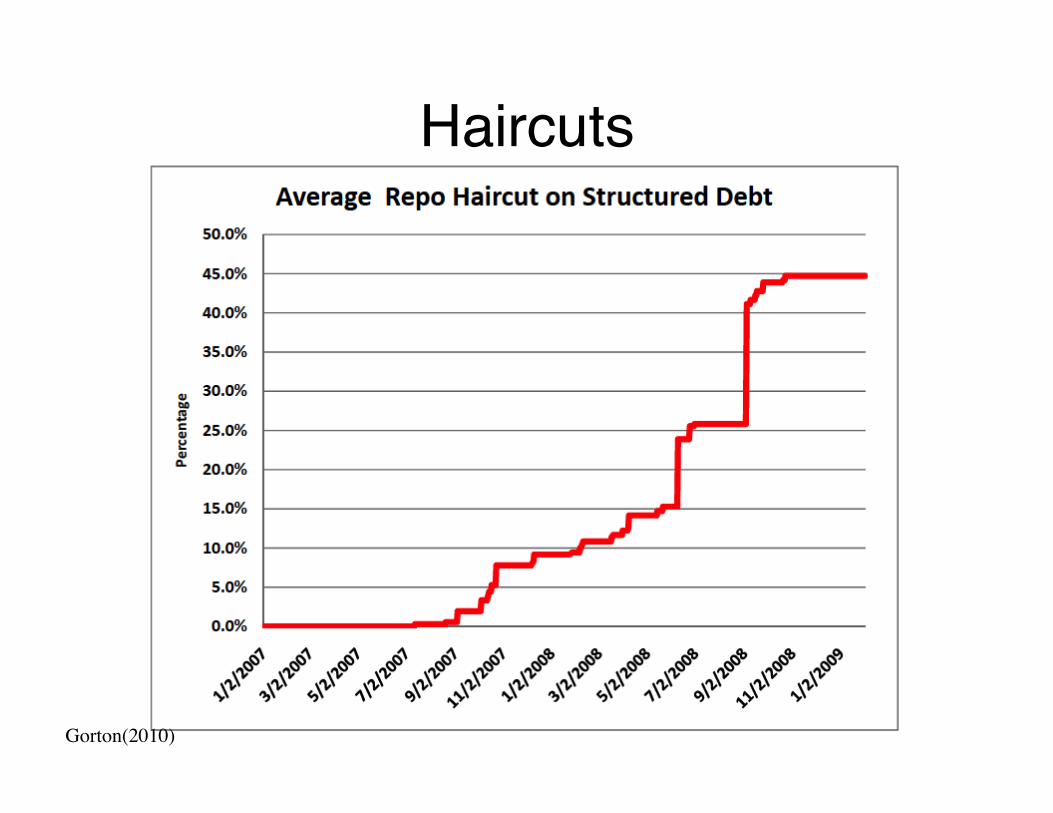

What Happened to Haircuts?"

Firms worried about " AAA securitized debt" Counter-party risk"

Haircuts increase (!!!)"

Haircuts"

Gorton(2010)

IB and BD’s Reaction"

Can no longer maintain leverage" Need to raise cash"

Selling stock difficult" Unwind portfolio, sell highest quality assets" This was usually AAA corp bonds"

“Firesale”"

Institutional Bank Run"

Institutions withdraw short term funds" Run on the repo money market" IB and BD’s need to raise even more

money" Continue emergency liquidations" This is a classic bank run"

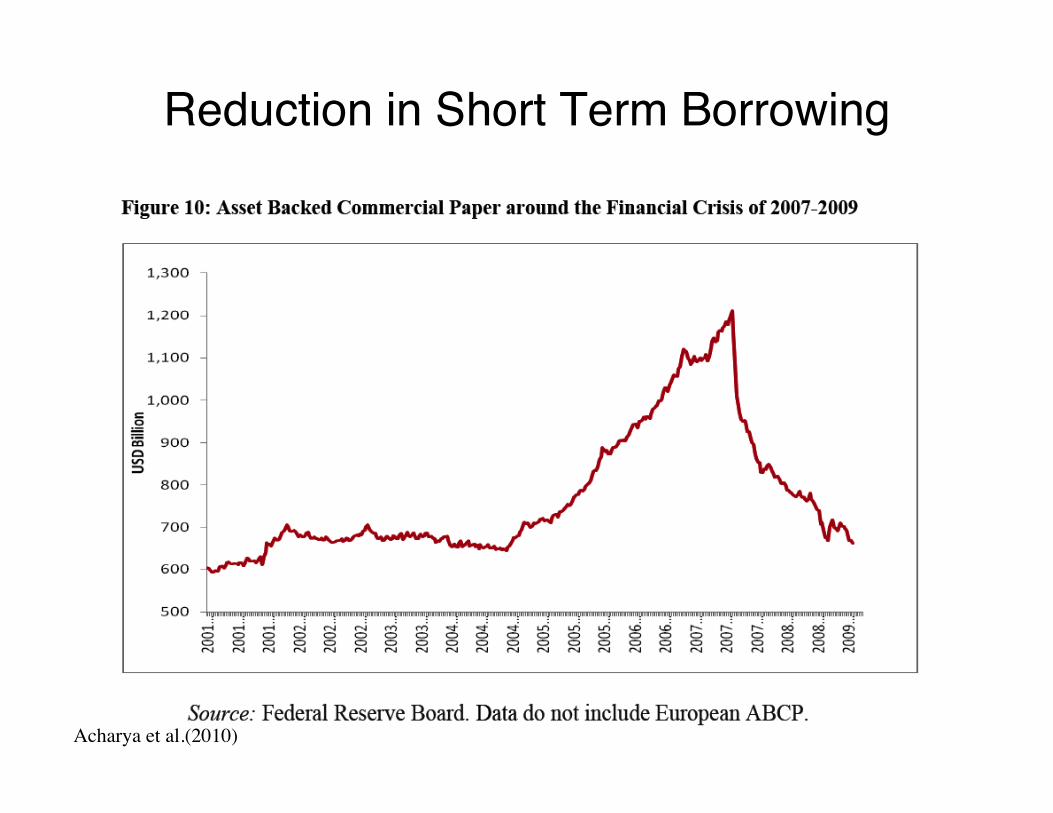

Reduction in Short Term Borrowing"

Acharya et al.(2010)

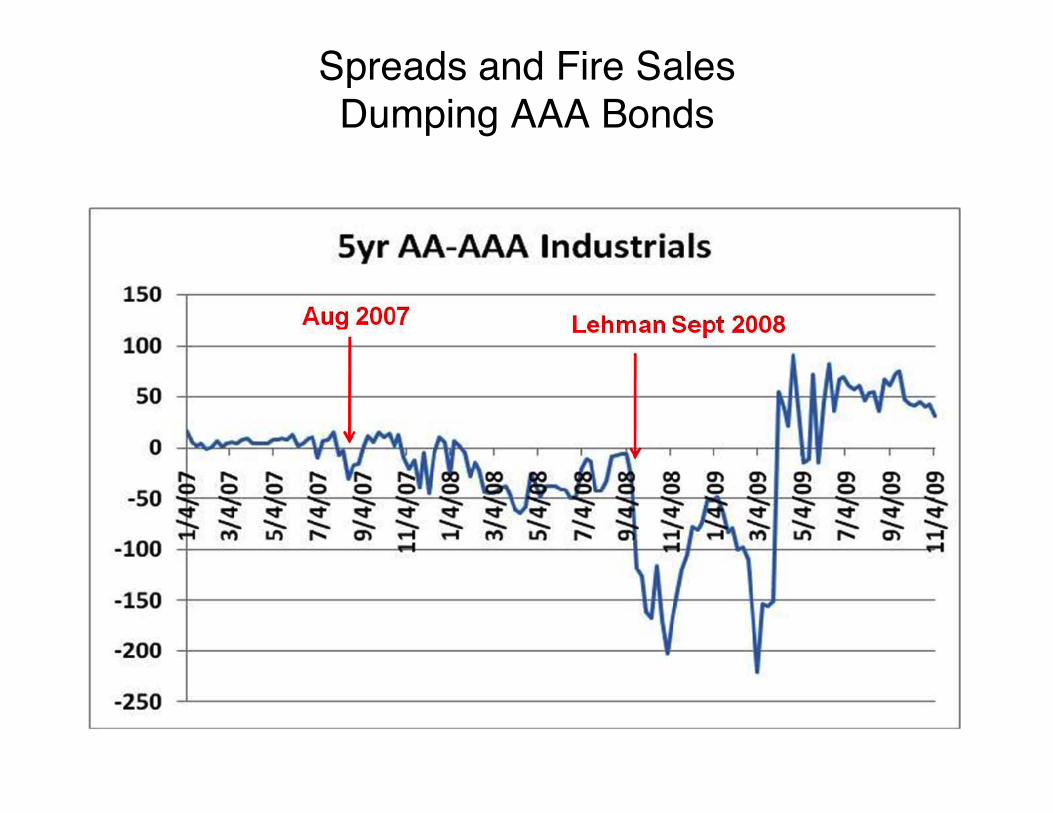

Spreads and Fire SalesDumping AAA Bonds

"

General Nervousness" All spreads over risk free increase" Indicates"

Counter-party risk" Uncertainty about any securitization" Ratings questions"

General uncertainty" “Knightian uncertainty”" “E-coli”"

Spreads"

Swagel(2009)

More Spreads"

Gorton(2010)

Monetary Policy"

After dot.com bubble bursts," U.S. eases monetary policy" Interest rates are low" Were they too low?" Should the Federal have seen real estate

bubble building and raised rates" Classic question??"

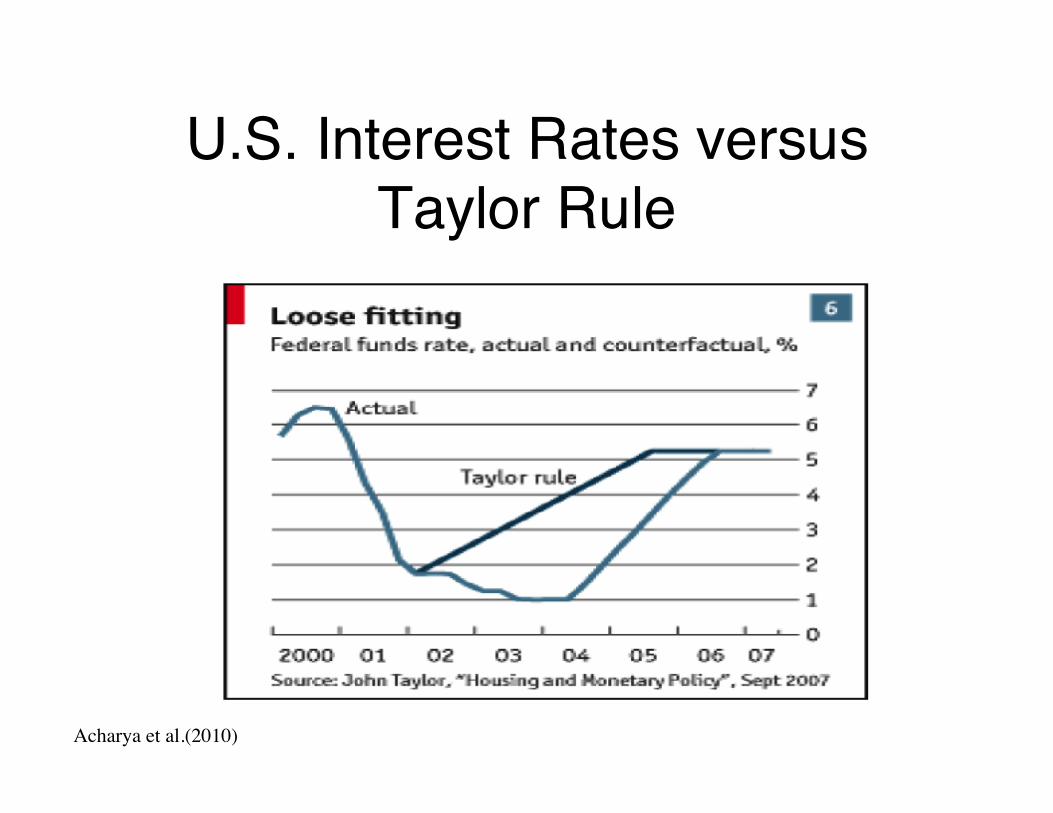

U.S. Interest Rates versusTaylor Rule"

Acharya et al.(2010)

Problems With This"

Is it right?" Do we really know the counterfactual?" Was the climate right for raising rates?"

Deflation fears" Bursting bubbles not general policy"

Outline" Connections to what we've done"

Bubbles, pricing and psychology" Contributing factors" History"

Pictures" Timeline"

Causes and mechanisms" Bubbles and beliefs again" Policy questions"

Summary"

Classic bubble: housing and credit" Other factors"

Security creation" Writing deep out of the money options" Capital flows"

Bubbles"

Returns and prices" P(t+1)>P(t)" Ratings" Shaky lending"

Risk" Risk under estimated and classified" Expands credit"

Bubbles"

Can the "popping" of the risk side be much worse?"

Asset returns outside anyone's belief distributions"

Models of the world completely wrong" Knightian uncertainty"

Policy Questions" Ratings agencies" Over the counter derivatives (exchange)" Bank (and Bank like) regulation"

Capital requirements (leverage restrictions)" Repo markets" Separations (Glass/Steagall)" Consumer lending practices" Convertible securities"

Security design (simplicity)" Systemic risk department" Capital flows"

Policy Philosophy"

Top down/discretionary " Low level/micro/automatic"

Historical/Theory View"

Bubbles are ubiquitous" Policy"

Don't try to eliminate bubbles" Build systems to impede their spread" Fire breaks"

Stop Here"

Readings" Acharya, Cooley, Richardson, and Walter,

Manufacturing tail risk, 2010." Gerardi et al., Making sense of the subprime crisis,

2009." Gorton, Questions and answers about the financial

Crisis, 2010." Gorton, Slapped in the Face by The Invisible Hand,

2009." Gjerstat and Smith, From Bubble to Depression,

WSJ, April 6, 2009. " Greenspan, The Crisis, 2010." Haldame, Rethinking the financial network, 2009."

More Readings" Jagannathan, Kapoor, and Schaumburg, Why are we

in a recession? The financial crisis is the symptom, not the disease, 2009. "

Lo and Mueller, Warning: Physics envy may be hazardous to your wealth, 2010."

Loungani, Housing prices: More room to fall?, Finance and Development, IMF, March 2010."

Reinhart and Rogoff, This Time is Different, 2009." Swagel, The financial crisis: An inside view,

Brookings Paper on Economic Activity, 2009."

Extra Figures"

The following slides are supplementary data figures."

Reinhart/Rogoff(2009)