2005 SOCIAL RESPONSIBILITY REPORT - UBI Banca · This is the third edition of the Social...

83

2005 SOCIAL RESPONSIBILITY REPORT

Transcript of 2005 SOCIAL RESPONSIBILITY REPORT - UBI Banca · This is the third edition of the Social...

2005SOCIAL RESPONSIBILITY REPORT

2005

SO

CIA

L R

ESP

ON

SIB

ILIT

Y R

EPO

RT

INDEX

1. INTRODUCTION 3Letter from the Chairman 5Content of the document 6Methodology 7

2. IDENTITY 9Our profile 11Our history 13Our mission 19Corporate governance 23Key values 33Activities and results 37

3. THE SOCIAL AND ENVIRONMENTAL REPORT 45Stockholders and investors 55Human resources 65Customers 87Territory 107Suppliers 117Environment 123The competitive system (compete and cooperate) 135The community (public administration) 139

4. THE ECONOMIC REPORT 143Determination and distribution of added value 145

5. IMPROVEMENT GOALS 151

6. AUDITOR’S REPORT 155Questionnaire 159

This English version is availabe for the convenience of the reader.It is a translation of the italian original version “Bilancio Sociale 2005” that takes precedence.

1. INTRODUCTION

4 5Introduction

LETTER FROM THE CHAIRMAN

CONTENT OF THE DOCUMENT

METHODOLOGY

INTRODUCTIONDear Reader,This is the third edition of the Social Responsibility Reportfor the Banca Lombarda Group, a document that supple-ments the Annual Report with a view to communicating withall stakeholders.

The topics of Social Responsibility and Business Ethics havebecome increasingly important in recent years. In this con-text, this report seeks to increase further the transparencyof the Group for those who see us as a reliable and efficientpartner, worthy of the confidence expressed by all ourstakeholders.

Compared with the past edition, this document contains even more information toexplain our activities over the past twelve months.

As in the past, the report has been audited in order to provide stronger assuranceregarding the quality of the quali/quantitative information presented.

One of the most important innovations this year is the presentation of the Group’s Codeof Ethics, as further evidence of our desire to ensure that the daily efforts made by all ouremployees comply with the rules of conduct for dealings with all parties who interactwith the Banca Lombarda Group. As stated in the Methodology, the current edition of the Group’s Social ResponsibilityReport takes account of the recommendations contained in the recent ABI volume onReporting to stakeholders, which was prepared with active input from our Bank. Thisdocument notes that the Social Responsibility or Sustainability Report should not mere-ly be a formal document, but rather a means for explaining the “Economic ValueGenerated” via a transparent and complete reconstruction of the various relationshipsand the connections between them.

In directly operational terms, key performance indicators have been prepared specifi-cally to identify, on a more timely and precise basis, the factors contributing to thebank’s competitive advantage that do not emerge from an analysis of the standardaccounting schedules.

The constant challenges that the market sets the banking system - ever more global andcompetitive - require us to become increasingly attentive and active partners of ourstockholders, customers, suppliers, employees and reference community, in order tosatisfy their economic and social expectations to the greatest possible extent.

We trust that you will find the Group’s Social Responsibility Report interesting and,therefore, a useful and effective tool for assessing the depth of our commitment thatcontributes to the ongoing process of dialog and discussion.

The ChairmanGino Trombi

7Introduction

6

CONTENT OF THE DOCUMENT

The Banca Lombarda Group hereby presents the third edition of its Social Responsibility Report.

The Social Responsibility Report comprises the following sections:

- Identity: summarises the key elements that clearly distinguish the Banca Lombarda Group

as an economic, legal and social entity within the overall context in which it operates;

- The social and environmental report: explains the nature and basis of the Banca

Lombarda Group’s interactions with its stakeholders;

- The economic report: identifies the volumes and values generated and distributed via the

activities and organization of the Group;

- Improvement goals: given the intrinsic nature of the document, oriented towards con-

stantly improving the way activities are reported to all stakeholders, the Group is commit-

ted to achieving its full economic and social potential while, at the same time, improving

the quality of its communications and the level of transparency;

- Opinion of the independent auditors: evaluates the Group’s compliance with current

reporting standards and best practice.

Certain changes have been made to this edition:

- Even more information has been provided; this includes further details about the Group’s

customers and on the training and professional development of employees; there is fur-

ther discussion of the direct environmental impact of the Group’s activities, such as paper

consumption and the generation of special waste;

- the information provided generally covers the values for all or the main Group companies,

and not just the Retail Banks;

- the Group’s Code of Ethics, which is attached to this document (available only in the italian

version).

METHODOLOGY

The Group Social Responsibility Report for 2005 has been prepared in accordance with the

guidelines drawn up by GBS (the Social and Environmental Accounting Study Group), using as

the main point of reference the “Manual for the Preparation of Social Responsibility Reports by

the Banking Sector” and the subsequent volume on “Reporting to Stakeholders - a guide for

banks” published by ABI (the Italian Banking Association). Reference was made to this last doc-

ument, in particular, for the preparation of schedules that analyze the generation and distribu-

tion of Value Added, and for the development of summary indicators for the Group.

The presentation of the topics required or recommended by the above guidelines has been

adapted to reflect the specific identity and needs of the Banca Lombarda Group.

All financial data and information have been taken from the 2005 consolidated financial state-

ments, as restated and reclassified in accordance with the guidelines.

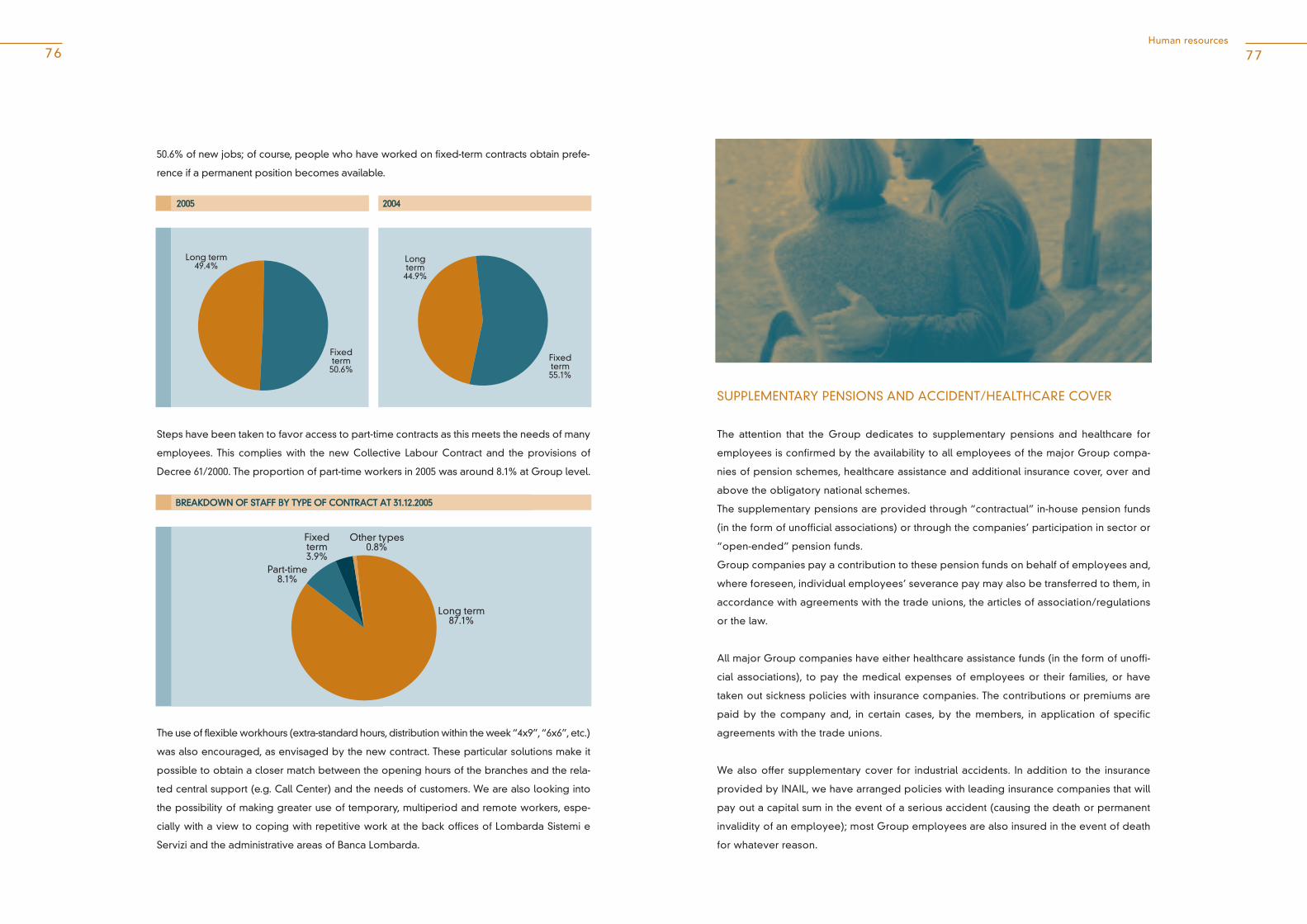

Quantitative information relating to other areas of the Group Social Responsibility Report

was identified and measured using the methodologies considered most appropriate

under the circumstances.

In particular, where phenomena can be identified in full, their parameters have been meas-

ured directly in order to maximize the reliability of the information presented in the Social

Responsibility Report.

Where this was not possible, the value of the parameters has been estimated with reference

to the best available information or to sample data.

The quantitative data and information gathered and processed were drawn from the IT sys-

tems, the accounting system and paper-based records. Various functions within the Group

were involved in these phases to ensure that the data was checked and processed correctly.

The methodology used to prepare the Group Social Responsibility Report and the contents

of this Report have been approved by the Board of Directors of Banca Lombarda S.p.A., the

parent bank.

2. IDENTITY

THE PRESENCE OF A BROAD STOCKHOLDER BASE AND THE HISTORY OF

THE VARIOUS BANKS WITHIN THE BANCA LOMBARDA GROUP ARE VITAL

ASPECTS OF THE GROUP’S IDENTITY.

THE GROUP IS GUIDED BY A LONG-TERM STRATEGIC VISION WHICH

REJECTS ANY LOGIC OF A SPECULATIVE NATURE.

IT IS ORIENTED TOWARDS THE CREATION OF STABLE, LASTING VALUE FOR

ALL STOCKHOLDERS.

MANAGEMENT IS PRUDENT, BUT MOTIVATED BY GROWTH, TAKING CARE

WHEN SELECTING BUSINESS TO MEASURE AND EVALUATE THE FINANCIAL

AND OPERATIONAL RISKS AS CAREFULLY AS POSSIBLE, TO ENSURE AN

ADEQUATE AND PROPER RETURN ON INVESTMENT.

THE GROUP’S WORK ETHIC AND APPROACH TO OPERATIONS IS BASED

ON MUTUAL RESPECT AND COOPERATION, AS WELL AS ON STAFF RELIA-

BILITY, PROFESSIONALISM AND EFFICIENCY AT ALL LEVELS.

THE GROUP HAS IMPORTANT HISTORICAL ROOTS AND A WIDESPREAD

PRESENCE IN THE TERRITORIES IN WHICH IT OPERATES. THESE RELATIONS

ARE GEARED TO THE CREATION OF CUSTOMER LOYALTY THROUGH

RESPECT FOR THE CUSTOMER, PROFESSIONAL SUPPORT AND RELIABILITY,

AS REINFORCED BY CONSTANT DISCUSSIONS AND COLLABORATION

WITH LEADING OPERATORS THAT ARE PART OF THE AREA’S ECONOMIC

AND INDUSTRIAL FABRIC. THE GROUP REMAINS COMMITTED TO SUSTAIN-

ING THE DEVELOPMENT OF ITS TERRITORY WHILE, AT THE SAME TIME, PRE-

SERVING THE BANK’S POTENTIAL VIA THE CAREFUL AND EFFECTIVE SELEC-

TION OF LENDING BUSINESS.

OUR PROFILE

THE GROUP'S ROOTS ARE LINKED WITH THE

HISTORY OF THE BANKS THAT FOUNDED

AND JOINED IT ALONG A PATH OF COMMON

GROWTH

““OUR HISTORY

14 15Our history

OUR ROOTS

RECENT HISTORY

OUR HISTORY

OUR ROOTS

The Banca Lombarda Group was created at the

end of 1998 by the merger of Credito Agrario

Bresciano with Banca San Paolo di Brescia; since

then, it has grown enormously in terms of vol-

umes, scope of consolidation, range of compa-

nies, organization and distribution network.

The Group’s roots lie in the history of the originating banks and the banks that have joined

it over time.

These banks originated from economic and social initiatives that had charitable aims and

their history is intertwined with that of the local territory: ties formed by more than one hun-

dred years of collaboration and development that underpin the Group’s current identity

and structure.

- Credito Agrario Bresciano (CAB) was founded in 1883 with the mission to meet the finan-

cial needs of agriculture in the territory around Brescia. It gradually made a name for itself

in the local economy, partly via the promotion of special entities that were set up to pro-

vide assistance to farmers, carry out research into agriculture and animal husbandry, and to

finance public works.

- Banca San Paolo di Brescia was founded in 1888 and, in addition to banking, it also had

charitable aims via the provision of support for various associations and persons active in

the area. The bank was fully committed to supporting initiatives in the fields of education,

the arts and social assistance.

- Banca di Valle Camonica was founded in 1872 with the intention of creating a credit institu-

tion with programmes and purposes inspired by the Christian-Catholic ethic, thus assuring

investors that their savings would be employed in a useful and profitable way, while also

sustaining the ongoing transformation of the local economy.

- Cassa di Risparmio di Cuneo was founded in 1855 with solidarity as its inspiration, in com-

mon with many of the savings banks that arose in Italy during the 19th century, the purpose

being to manage savings for the benefit of the less well-off and to fight usury.

- Banca del Monte di Lombardia has its roots in antiquity; Banca del Monte di Lombardia

was formed in 1987 on the merger of Banca del Monte di Milano, founded in 1483 as a

pawnbroking institution, with Banca del Monte di Pavia e Bergamo which, in turn, originat-

ed from Monte di Pavia founded for humanitarian purposes in 1493 by Bernardino da Feltre,

a Franciscan monk.

- Cassa di Risparmio di Tortona was founded in 1911 to support the development of the

local economy.

- Lastly, the more recent Banco di San Giorgio was set up in 1987, initially in the form of a

cooperative bank and later transformed into a joint stock company.

17Our history

16

RECENT HISTORY

1998

CAB and Banca San Paolo di Brescia, the two Brescia banks, were merged to form Banca Lombarda.

The banking activity carried on by CAB and Banca San Paolo di Brescia was spun off into a

new company called Banco di Brescia. The equity investments previously held by Banca San

Paolo di Brescia and CAB in Banca di Valle Camonica and Banca San Giorgio, respectively,

remained under the control of Banca Lombarda.

A federal-type organizational model was selected, with a Parent Bank responsible for man-

agement policy, coordination and control, and federated Retail Banks, whose mission is

prevalently commercial, with some degree of operational autonomy designed to preserve

and develop direct links with the territory.

1999 – 2000

Control of Cassa di Risparmio di Tortona and Banca Regionale Europea was acquired during

this period: through them, Banca Lombarda now has an important presence in Piedmont and

a stronger position in Lombardy.

Banco di Brescia was also divisionalized by customer segment (retail, private banking and

corporate) to improve the service provided by creating a deeper and more specialised rela-

tionship with customers.

Together with Cattolica Assicurazioni, Lombarda Vita was formed as a captive insurance com-

pany to manage life assurance policies for the Group’s customers.

2001

Common functions were centralized and IT systems were integrated by setting up Lombarda

Sistemi e Servizi. This also helped combine the identity of a federal group with the consoli-

dation of a unified system of governance, partly with a view to achieving significant

economies of scale.

2002

Work was completed on the divisionalization by customer segment of all of the Retail Banks.

Grifogest SGR SpA was acquired, reinforcing the Group’s presence in the asset management

sector.

2003

Banca Idea, now known as Banca Lombarda Private Investment, was bought with a view to

expanding the activities of the Group’s financial consultants and its private banking business.

2004

Caboto International SA was purchased, as was the financial consultancy business of Banco

Desio.

A representative office was opened in Shanghai, to provide international support for the

Group’s corporate customers seeking to enter the Chinese market.

A joint venture was formed in China with a local company, Guodu Securities Co., in theasset

management sector, with a view to entering the Chinese retail market.

2005 and early 2006

Veneta Factoring was absorbed by CBI Factor during 2005, thus combining the Group’s two

Italian factoring companies in order to rationalize operations and release further synergies

with regard to costs and revenues.

Subsequently, at the end of 2005, various transactions were carried out to strengthen activities

in a number of business areas.

The network of financial consultants benefited from the purchase from Banca Popolare

dell’Etruria e del Lazio of its financial consultancy business, while banking activities were

strengthened by purchasing the residual minority interest in Banca Cassa di Risparmio di

Tortona, which was then absorbed by Banca Regionale Europea.

“ THE MAIN AIM OF THE BANCA LOMBARDA

GROUP IS TO PROVIDE FIRST-RATE BANKING

SERVICES AND CREDIT FACILITIES TO HOUSE-

HOLDS AND SMES

“OUR MISSION

21Our mission

20

RESPECT FOR THE CUSTOMER

STAFF PROFESSIONALISM

CONSTANT INNOVATION AND THE OPTIMIZATION OFPROCESSES

OUR MISSION

RESPECT FOR THE CUSTOMER

The Group aims to consolidate its relation-

ships with customers by constantly improving

service and product quality.

The creation of customer loyalty is consid-

ered a fundamental objective, considering

the huge effort needed to acquire new cus-

tomers and the size of the investment made to

ensure customer satisfaction.

STAFF PROFESSIONALISM

Motivation, a sense of belonging and profes-

sional training for all human resources are con-

sidered the best ways to increase and maintain the Group’s competitive capability.

As an entrepreneurial institution of primary importance, the Group aims to attract the

best professional profiles in the sector and retain the most talented individuals.

CONSTANT INNOVATION AND THE OPTIMIZATION OF PROCESSES

Innovation in terms of products, services, access channels and organisation is a critical success

factor for the maintenance of high levels of competitiveness. Technology is also seen as an

effective way to provide services more efficiently and to lower operating costs.

The Banca Lombarda Group’s investment decisions and operating policies are based on

selective criteria.

Banca Lombarda carries on its business in a responsible manner, complying with its Charter

of Values and Code of Ethics, in full awareness of its institutional role.

The Group has a reputation among its stakeholders as a solid and reliable bank that operates

fairly and openly in all internal and external dealings.

CORPORATE GOVERNANCE IS GENERALLY

UNDERSTOOD TO COMPRISE ALL THOSE

PROCESSES, POLICIES, PRACTICES, RULES

AND BODIES THAT INFLUENCE BOTH HOW A

COMPANY IS ADMINISTERED AND ITS TRANS-

PARENCY. THIS INCLUDES THE RELATIONS

BETWEEN THE VARIOUS STAKEHOLDERS

INVOLVED AND THE OBJECTIVES ESTAB-

LISHED FOR THE COMPANY

““CORPORATE GOVERNANCE

25Corporate Governance

STOCKHOLDERS’ MEETING

The Stockholders’ Meeting is held once a year to approve the financial statements and when-

ever needed to decide on any other matters within its sphere of competence.

THE BOARD OF DIRECTORS

The Board of Directors plays a central role in the organization, being responsible for all func-

tions involving corporate strategy and policy-making, as well as for ensuring that all necessary

and appropriate controls are in place to monitor the performance of the bank.

The Board of Directors has 21 members and currently has a majority of Independent Directors.

They are defined as Independent Directors in accordance with the Code of Conduct for Listed

Companies, namely:

1. they do not have, directly, indirectly or on behalf of third parties, nor have they had in the

recent past, economic relations with the company, its subsidiaries, the executive directors,

the stockholder or group of stockholders that controls the company, of a significance that

might condition the independence of their judgment;

2. they do not hold, directly, indirectly or on behalf of third parties, equity interests allowing

them to control or exercise significant influence over the company, nor do they participate

in stockholders’ agreements to control the company;

3. they are not close family members of the company’s executive directors or of persons who

find themselves in the situations mentioned in points 1 and 2 above.

On the other hand, given the powers granted to him by the Board, the Chief Executive Officer

is to be considered an Executive Director.

24

CORPORATE GOVERNANCE

Banca Lombarda, which is listed on the Italian

stock exchange, has always been sensitive to

questions of corporate governance. It has aligned

its organizational structure with the principles of

good management, the requirements of the arti-

cles of association and the recommendations of

the Code of Conduct for Listed Companies pre-

pared by Borsa Italiana.

Banca Lombarda’s system of corporate gover-

nance includes the following bodies:

• Stockholders’ Meeting;

• Board of Directors;

• Executive Committee;

• Chairman;

• Chief Executive Officer;

• General Manager;

• Board of Statutory Auditors.

STOCKHOLDERS’ MEETING

THE BOARD OF DIRECTORS

EXECUTIVE COMMITTEE

THE CHAIRMAN

THE CHIEF EXECUTIVE OFFICER

THE GENERAL MANAGER

THE BOARD OF STATUTORY AUDITORS

COMPENSATION COMMITTEE

INTERNAL CONTROL COMMITTEE

INTERNAL RULES FOR RELATED-PARTY TRANSACTIONS

INTERNAL DEALING

REGULATIONS FOR THE PROCESSING OF INFORMATION

THE SYSTEM OF INTERNAL CONTROLS

THE ORGANIZATIONAL MODEL PURSUANT TO DECREE 231/2001

THE GROUP’S CODE OF ETHICS

27Corporate Governance

26

The Board generally meets once a month and, on an extraordinary basis, any time the need arises.

The Board of Directors met 14 times during 2005.

The present Board of Directors, as appointed at the Stockholders’ Meeting held on 29 April

2005, comprises:

EXECUTIVE COMMITTEE

The Board of Directors has appointed an Executive Committee comprising 8 directors and

delegated its powers to this committee. In particular, it has attributed to the Executive

Committee all powers for the ordinary administration of the Bank, except for some that are

the exclusive responsibility of the Board. The Executive Committee met four times in 2005.

THE CHAIRMAN

The Chairman legally represents the Bank versus third parties and in court, with the right to

appoint attorneys and legal counsel, and, if proposed by the Chief Executive Officer, in situa-

tions of particular urgency he can take decisions that would normally be made by the Board

of Directors or the Executive Committee. Any such decisions must be reported to the Board

at its next meeting.

The Chairman allocates and distributes the amounts set aside for donations, on the basis and

in the manner decided by the Board of Directors.

THE CHIEF EXECUTIVE OFFICER

The Board of Directors has delegated to the Chief Executive Officer the power to supervise

the ordinary administration of the Bank and coordinate the activities of Banca Lombarda, the

Parent Bank, with those of its subsidiaries, in compliance with the guidelines laid down the

Board of Directors, and with the assistance of the General Manager.

THE GENERAL MANAGER

The General Manager leads the executive team and performs his duties within the scope of

the powers granted to him by the Board of Directors.

THE BOARD OF STATUTORY AUDITORS

The Board of Statutory Auditors, which comprises 3 serving members and 2 alternate mem-

bers, has responsibility for checking and ensuring that the Company is managed correctly in

accordance with the law, the Articles of Association, stockholders’ resolutions and other regulations.

COMPENSATION COMMITTEE

A Compensation committee has been set up as part of the Board, consisting primarily of non-

executive directors. The Committee makes proposals to the Board for the remuneration of

PPOOSSIITTIIOONNMMeemmbbeerr ooff tthhee

eexxeeccuuttiivvee

ccoommmmiitttteeee

MMeemmbbeerr ooff tthhee

ccoommppeennssaattiioonn

ccoommmmiitttteeee

MMeemmbbeerr ooffiinntteerrnnaattiioonnaall

ccoonnttrroollccoommmmiitttteeee

NNAAMMEE

Trombi dr. Gino

Folonari dr. Alberto

Bazoli avv. Giovanni

Faissola avv. Corrado

Cera prof. Mario

Bellini avv. Luigi

Bertolotto dr. Piero

Borlenghi dr. Sergio

Camadini dr. Giuseppe

Cattaneo prof. Mario

Fidanza Virginio

Gussalli Beretta dr. Pietro

Lucchini dr. Giuseppe

Manzoni dr. Federico

Martinelli prof. Felice

Minelli ing. Giovanni

Nocivelli cav. Luigi

Rampinelli Rota avv. Pierfrancesco

Rodella Adriano

Viglietta Matteo

Zaleski ing. Romain

Chairman

Senior Vice Chairman

Vice Chairman

Chief Executive Officer

Secretary

Director

Director

Director

Director

Director

Director

Director

Director

Director

Director

Director

Director

Director

Director

Director

Director

*****-

*-

**-

-

-

-

-

-

-

-

-

-

-

****-

-

-

-

*-

-

-

*-

-

*-

-

-

-

-

-

-

-

-

**-

-

-

*-

-

-

**-

-

-

-

-

-

29Corporate Governance

28

Directors with special duties. When the Committee makes decisions, the persons directly con-

cerned abstain. With input from the Chief Executive Officer, the Committee also makes pro-

posals regarding the remuneration of senior management.

INTERNAL CONTROL COMMITTEE

An Internal Control Committee has been set up as part of the Board. It is responsible for

checking that all internal functions are carried on properly, so that the system of internal

controls is as effectively as possible.

As part of its checks, the Internal Control Committee met 9 times during 2005 and paid par-

ticular attention to evaluating the Group’s system of internal controls, especially with

regard to the management of credit risk and the system for measuring and monitoring

operating risk. The Committee also assessed matters regarding the preparation of the

financial statements, including the effects of Decree 37 of 6 February 2004 and certain

aspects regarding the Bank’s regulatory structure.

INTERNAL RULES FOR RELATED-PARTY TRANSACTIONS

In accordance with Borsa Italiana’s recommendations contained in the Code of Conduct

for Listed Companies, Banca Lombarda has approved its own “Internal Rules for Related-

Party Transactions”.

This regulation lays down guidelines and criteria for identifying related-party transactions,

which must be approved by the Board of Directors. Such transactions also include those

carried out between Group companies, if they are material from an economic, capital or

financial point of view. If they are not conducted in the ordinary course of business and on

standard market terms, the related-party transactions carried out by subsidiaries must be

authorized by the Board of Directors of the subsidiary concerned and communicated

immediately to the Parent Bank.

The regulation also defines behavioural guidelines for such transactions to ensure that they

are correct in substance and in line with procedures.

INTERNAL DEALING

In order to adopt the rules issued by Borsa Italiana, which became effective on 1 January

2003, Banca Lombarda prepared a code of conduct which was approved by the Board of

Directors during the meeting held on 11/12/2002.

Following Italy’s implementation of the Market Abuse Directive 2004/72/EC and Consob’s

adoption of the corresponding enabling regulations, the law introduced an obligation to

communicate to the market all transactions in the company’s financial instruments carried

out by “relevant persons” and by those closely associated with them.

As a result, as confirmed by Borsa Italiana, its internal dealing rules were abrogated from

the date the new provisions became effective, which was 1 April 2006.

In order to adopt the new rules, on 22 March 2006 the Board of Directors approved, with

effect from 1 April 2006, the new “Regulations for transactions carried out by relevant per-

sons and persons closely associated with them” in accordance with current law.

The new regulations more or less reiterate Borsa Italiana’s rules on internal dealing.

The “relevant persons” required to report their activities have been identified as the direc-

tors, statutory auditors, members of senior management and the head of the finance

department of Banca Lombarda e Piemontese S.p.A. and the persons closely associated

with them.

The following transactions do not have to be disclosed:

a) transactions totalling less than 5,000 euro in any one year; if derivatives are involved,

the amount is calculated with reference to the underlying shares;

b) transactions between relevant persons and those closely associated with them;

c) transactions carried out by the listed issuer and by its subsidiaries.

REGULATIONS FOR THE PROCESSING OF INFORMATION

For the purpose of ensuring proper control over confidential information relating to Banca

Lombarda e Piemontese S.p.A. and its subsidiaries, the Board of Directors has also

approved a set of new regulations called: “Internal Regulations for managing and han-

dling confidential information and communicating documents and information externally”.

These Regulations identify the persons in charge of managing this information and define

the rules of conduct to be adopted by directors, statutory auditors and employees of

Banca Lombarda and its subsidiaries, as well as the procedures for communicating docu-

ments and information externally, with particular reference to price-sensitive information.

As a suitable tool for the identification of persons with access to privileged information, as

envisaged by art. 115 bis of Decree 58/98 and the related enabling regulations, a “Register

of persons with access to privileged information about Banca Lombarda and its finan-

cial instruments” has been set up at Group level to record the following information:

1. the identity of the persons who have access to privileged information because of their

job or profession, or in view of their activities on behalf of the entity required to maintain

the Register;

31Corporate Governance

30

2. the reason for which the person is listed in the Register;

3. the registration date of each update.

The person concerned is promptly informed that this information has been recorded.

THE SYSTEM OF INTERNAL CONTROLS

Banca Lombarda has adequate internal control and risk management systems, which com-

ply with the supervisory instructions issued by the Bank of Italy.

The system of internal controls is designed to ensure the correctness and propriety of all

corporate processes, safeguard asset values, and ensure the reliability and completeness

of accounting and operational information.

The Internal Auditing department is responsible for checking that the activities of the

organization are carried out on a proper basis and for assessing the functioning of the sys-

tem of internal controls.

THE ORGANIZATIONAL MODEL PURSUANT TO DECREE 231/2001

At the meeting held on 12 May 2004, the Board of Directors approved the structure of the

organisation, management and control model required by Decree 231/2001 (on the admin-

istrative responsibilities of companies), appointing in Banca Lombarda a “collegiate

body” comprising the heads of the Corporate and Legal Secretariat, Human Resources

and Group Auditing Departments, coordinated by an independent Director.

This step was taken in the conviction that adoption of this Model - quite apart from the

Decree, which says that it is voluntary and not obligatory - represents a valid tool for rais-

ing the awareness of everyone working at the Parent Bank and at Group companies, so

that they will always performing their duties properly and in a manner that prevents the

crimes envisaged in the decree.

In accordance with the corporate governance principles and guidelines adopted by the

Group, Banca Lombarda has taken steps to make this Model known to Group companies,

proposing that they should implement it and make any adjustments needed to reflect local

circumstances.

During 2005, to ensure that Model is constantly updated and effectively implemented fol-

lowing legislative changes, particularly with reference to the question of market abuse and

the protection of small investors, the Parent Bank’s Control Unit initiated a project to verify

and update the Model with support from external consultants, partly to obtain an inde-

pendent opinion on the work carried out.

In particular, the mapping of activities at risk of abuse and their related supervision has

been reviewed and updated. Risk areas have been recognised, internal controls and pro-

cedures evaluated, and action plans identified and classified on a priority basis.

Consequently, a plan has been prepared to extend the organisational model by means of

specific rules for conduct and controls within each sensitive process and activity, in order

to strengthen organisational supervision.

In this context, the Organisational Model has been updated with regard to the rules by

which the Control Unit functions, together with the related information flows, the discipli-

nary system and the system for reporting violations and training/information. The revised

Model was reviewed by the Board of Directors on 14 March 2006.

THE GROUP’S CODE OF ETHICS

The Board also discussed the adoption of the Group’s Code of Ethics, which forms an inte-

gral part of the organisational model.

Particular attention was paid to the provision of training/information on this matter. Training

sessions involving the entire management of Banca Lombarda were held during the fourth

quarter of 2005, supplementing the IT support already available as part of the corporate

regulatory system.

KEY VALUES

35Key values

34

SENSE OF RESPONSABILITY

THE ABILITY TO LISTEN AND RESPECT FOR CUSTOMERS

INNOVATION

RESPECT FOR LEGAL RIGHTS AND EQUAL OPPORTUNTY

TRADITION AND TERRITORIAL ROOTS

KEY VALUES

The Group’s Charter of Values approved by the

Board of Directors of Banca Lombarda, the Parent

Bank, consists of the following principles.

SENSE OF RESPONSIBILITY

The Banca Lombarda Group bases all its efforts

on the serious acceptance of responsibility at

all levels within the organization. In concrete

terms, this translates into fair dealing, openness

and continuity of relationships. Continuity is

considered the cornerstone of the relationship

of trust that exists between the Bank and its

customers, stockholders, employees and the

entire community.

Fair dealing versus all stakeholders is the basis

of all actions and initiatives; indeed, it must

inspire everything that the Bank does: there is

no economic objective, however interesting

and attractive, that can be pursued without paying proper attention to the rules and reg-

ulations that govern how we operate; there can be no lasting success if we ignore the

rules and the respect that lie at the basis of community life and preservation of the envi-

ronment. Openness is pursued not only as a regulatory requirement, but also as a distin-

guishing factor: dialogue and clarity represent the basis of lasting relationships and a

good reputation.

THE ABILITY TO LISTEN AND RESPECT FOR CUSTOMERS

Banca Lombarda intends to present itself to customers as an attentive and professional

partner, well aware of the responsibilities that stem from its role as a financial and bank-

ing intermediary. In order to respect the true needs of customers, the Group believes it

to be of vital importance to listen to them and discuss their requirements. This helps to

direct the Bank’s competitive skills towards the creation of products and services that

meet the various profiles of demand.

INNOVATION

For the Group, innovation is a value on which to base its competitive ability. It is also the best

way to update products and services to reflect the changing needs of customers, while

exploiting to the full the technological developments that lower costs and improve the quali-

ty of internal processes.

RESPECT FOR LEGAL RIGHTS AND EQUAL OPPORTUNITY

The Group operates responsibly in compliance with the fundamental principles of the

Italian legal system, sharing the principles of legality, freedom of thought and equal

opportunity. The Group rejects any form of discrimination or prejudice, whether inside or

outside the organization, based on race, sex, religious confession, political beliefs or any

other social or personal condition, other than the fair and honest requisites needed to

operate within the law and achieve the Group’s business objectives.

TRADITION AND TERRITORIAL ROOTS

The Group is convinced that its business history, constant interaction with its territory, and

the mark left by its founders and later personalities, all constitute a valuable heritage. This

must not be forgotten, but kept alive and modern thanks to an innovative vision that is

open to change.

ACTIVITIES AND RESULTS

38 39Activities and results

ACTIVITIES AND RESULTS

Formed at the end of 1998, on the merger of Banca

San Paolo di Brescia and Credito Agrario

Bresciano, the Banca Lombarda Group has subse-

quently grown almost fivefold. In particular, total

assets have increased from about 8 billion euro to

38.3 billion euro at the end of 2005.

At that date, Banca Lombarda ranked 9th in Italy

for banking products (loans to customers, direct

and indirect deposits) and was placed 12th

among listed Italian credit institutions, with a

market capitalization at year end of almost 4 bil-

lion euro.

The federal model has played an important role in

supporting the aggregation process by which the

Group has reached its present size and configura-

tion, with seven federated commercial banks

operating in Italy.

The new Group structure facilitated the aggregat-

ing force of the Parent Bank and the rapid integration of other banks as they were acquired,

while safeguarding their brand names in view of their value in terms of customer loyalty.

The objectives of united and efficient management are guaranteed by Banca Lombarda as the

Parent Bank, which represents the Group’s “centre of governance and control”. Banca

Lombarda carries out all functions involving management policy, coordination and control. It

also performs the operational and support functions that have been centralised in order to

strengthen the organization and make management more effective, thus exploiting all syner-

gies to the full.

The formation of Lombarda Sistemi e Servizi at the beginning of 2001 completed the process

of centralizing and rationalizing the information & communication technology (ICT) functions,

as well as real estate and general services, with the achievement of significant economies of scale.

2002 saw the completion of the plan to rationalize the distribution networks of the Group’s

commercial banks, assigning a specific territory for each one to develop. The model of prod-

ucts and services on offer was also refined and focused on the specific needs of customers

by divisionalizing the commercial organization by customer segment (retail, private banking

and corporate).

Subsequently, a plan was implemented to restructure and simplify the near-banking compa-

nies. Veneta Factoring was absorbed by CBI Factor.

The network of financial consultants has been expanded over the past four years, rapidly

reaching the breakeven point; the network has virtually doubled from 308 consultants in 2001

to 553 in 2005.

1 The two Groups that together gave rise to the Banca Lombarda Group, prior to their merger, had total assets of 8.9 billion euro and7.3 bilion euro for, respectively, CAB and the Banca San Paolo Group.

2 Source: Prometeia.

41Activities and results

40

The following chart shows the structure of the Group at the end of 2005.

At the end of 2005, the Banca Lombarda Group had total loans of 28.2 billion euro, direct

deposits of 28.9 billion euro and indirect deposits of 46.8 billion euro.

The Group operates in various financial segments, in addition to the various activities that

comprise its core business: granting credit, taking deposits and managing collection and pay-

ment services. The operating segments include: asset management (indirect deposits of 26.2

billion euro managed in 2005), bancassurance (6.4 billion euro in insurance reserves, leasing

(1.7 billion euro in loans to customers), factoring (turnover of 3.8 billion euro) and consumer

credit (loans totaling 717 million euro).

The Banca Lombarda Group is one of the largest Italian banking groups in terms of loans and

direct deposits, with a market share that has grown over time to more than 2% (2.1% in asset

management).

It has a network of 787 branches (including two abroad, in France and Luxembourg) and 553

financial consultants. The Group’s territorial presence is concentrated in the north-west of Italy,

with particularly significant market shares in its provinces of origin: Brescia (28% of loans and

42.4% of deposits, including bonds issued), Cuneo (18.8% and 28.9%), Pavia (10.8% and 13.8%)

and Alessandria (10.3% and 12.2%).

The Group’s operations have the following characteristics:

• a significant level of profitability; ROE, i.e. the ratio of net income to equity, was 12% in 2005;

• a high level of efficiency: with a cost/income ratio, i.e. administrative costs as a proportion

of net interest and other banking income, of 58.1%;

• excellent quality of loans: the proportion of net non-performing loans to total loans is 0.80%;

• staff productivity is good and rising, both in terms of deposits and loans per capita and in

terms of net interest and other banking income per capita.

* Joint venture with Cattolica Assicurazioni

BBaannccoo ddiiSSaann

GGiioorrggiioo

BBaannccaaRReeggiioonnaalleeEEuurrooppeeaa

CCaassssaa ddiiRRiissppaarrmmiiooddii TToorrttoonnaa

BBaannccaa ddiiVVaallllee

CCaammoonniiccaa

BBaannccaaLLoommbbaarrddaa

PPrriivvaatteeIInnvveessttmmeenntt

BBaannccaaLLoommbbaarrddaa

IInntt.. SSAA

CCBBII FFaaccttoorrFFiinnaanncciieerraa

VVeenneettaa

SSBBSSLLeeaassiinngg

SSIILLFF

LLoommbbaarrddaaVViittaa**

AAnnddrrooss

CCaappiittaallggeesstt GGrriiffooggeesstt

CCaappiittaallggeessttAAlltteerr.. IInnvv..

GGeessttiioonniiLLoommbbaarrddaa

((SSuuiissssee))SSAA

SSiiffrruu SSIIMM

LLoommbbaarrddaaAAddvviissoorryy

SSAA

SSoollooffiidd

AAsssseett MMaannaaggeemmeenntt NNeeaarr--bbaannkkiinngg BBaannccaassssuurraannccee

BBaannccoo ddiiBBrreesscciiaa

CCoommmmeerrcciiaall bbaannkk

LLoommbbaarrddaa SSiisstteemmii ee SSeerrvviizziiBBAANNCCAA LLOOMMBBAARRDDAA

GGEEOOGGRRAAPPHHIICCAALL DDIISSTTRRIIBBUUTTIIOONN OOFF TTHHEE BBAANNKKIINNGG BBRRAACCHHEESS

GGEEOOGGRRAAPPHHIICCAALL DDIISSTTRRIIBBUUTTIIOONN OOFF TTHHEE FFIINNAANNCCIIAALL CCOONNSSUULLTTAANNCCYY NNEETTWWOORRKK

778877 BBrraanncchheess 555533 FFiinnaanncciiaall ccoonnssuullttaannttss

35

29

15

122

442

176

1

41

60

22

2

66

19

18

69

52

1852

10

10831

4426

12

1

1 15

16

1

1

4

35

29

15

122

442

176

1

41

60

22

2

66

19

18

69

52

1852

10

10831

4426

12

1

1 15

16

1

1

4

43Activities and results

42

OBJECTIVES, PLANS AND STRATEGIES FOR THE FUTURE

The Group intends to pursue a growth path that ensure competitive performance, having

regard for the level of risk accepted, in order to properly remunerate the stockholders and

take pro-active responsibility in dealings with all stakeholders.

This combined objective translates into a plan to realign the various sources of profitabili-

ty, efficiency and risk, to achieve levels of excellence compared with the Group’s leading

competitors.

The principal areas of action for the pursuit of the Group’s objectives are:

• greater focus on traditional banking activities and on retail customers, partly by review-

ing and simplifying commercial policies and the product and services available, there-

by making a better use of capital and maximizing Economic Value Added (EVA);

• a search for economies of purpose and greater specialization, partly by reviewing and

enhancing the strategic alliances and agreements with external partners and other play-

ers, especially those involving activities that are expected to achieve the highest rates of

growth, such as consumer credit, leasing, bancassurance and supplementary pensions;

• the pursuit of economies of scale and greater effectiveness via the rationalisation and sim-

plification of the Group’s corporate and organizational structure, and the elimination of any

remaining duplications;

• the ongoing improvement of distribution channels, via technological and process innova-

tions and the territorial repositioning of the network, to take best advantage of the com-

plementary nature of the various channels.

The sustainability of these objectives over the medium/long term depends on the ability to consol-

idate and strengthen our image as a highly reliable Group, truly attentive to the needs of customers

and constantly in search of the highest quality.

This will enable us to consolidate and strengthen over time the confidence of an increasing number

of customers (present and future), who will recognize and accept the principles underlying our way

of being a bank.

All this must be achieved by identifying the concrete action to be taken and spreading a

corporate culture that guides and consistently enhances the value of the Group’s human

capital.

The action to enhance and direct the development of our Human Capital includes:

- the identification of potential;

- the activation of an assessment center for a population selected with reference to certain cri-

teria indicative of potential, in order to give priority to investment in the persons selected in a

specific and structured manner;

- the completion of the survey of knowledge, with a view to identifying gaps to be covered by

training activities;

- the definition of strategies for the professional development and management of personnel

in order to meet business requirements and cover turnover within the Group;

- consistent with the Group’s commercial and organizational objectives, training programs will

be expanded in terms of content and volume, providing both standard and personalized

courses having regard for the knowledge already acquired;

Other Groupwide action at all levels includes the improvement of internal communications,

and a project to sustain effectively the sense of belonging, corporate identity and external

image, thus facilitating the internal transfer of information and know-how.

Maximization of the measurable quality of the services provided is a strategic objective for

the maintenance of the value created over time. In this regard, a new project will guide the

search for maximum quality at all levels by defining quality in the various contexts and iden-

tifying agreed mechanisms for measuring it effectively.

3311//1122//22000055 3311//1122//22000044OOPPEERRAATTIINNGG IINNDDIICCAATTOORRSS

Indicators off employee efficiency (thousands of euro)

Loans to customers/average number of employees

Net interest and other banking income/average number of employees

Total customer deposit/average number of employees

Equity indices

Equity/Loans to customers

Equity/Total customer deposits

Capital adequacy ratio

Tier 1 ratio (Basic capital/Weighted assets)

Total capital ratio (Capital for supervisory purpose/Weighted assets)

Profitability indices

ROE (Return on Equity)

Cost/income ratio (Operating costs/net interest and other banking income )

Risk indicator

Net non-perfoming loans/net loans to custumers

Coverage of non-performing loans

Net problem loans/net loans to customers

3,734

181

10,008

7.1%

2.6%

5.8%

9.7%

12.0%

58.1%

0.80%

53.4%

1.03%

3,521

174

9,364

6.9%

2.6%

5.9%

10.1%

10.9%

61.7%

0.80%

50.4%

1.13%

3.THE SOCIAL AND ENVIRONMENTAL REPORT

3. THE SOCIAL ANDENVIRONMENTAL REPORT

VALUE IS CREATED EVERY DAY BY FOCUSING ON

THE QUALITY OF THE SERVICES PROVIDED TO

CUSTOMERS, CONSISTENT WITH THE VALUES

UNDERPINNING THE GROUP’S OPERATIONS

AND THE INTERESTS OF ALL STAKEHOLDERS““

THE SOCIAL AND ENVIRONMENTAL REPORT

48 49The social and environmental report

THE SOCIAL AND ENVIRONMENTAL REPORT

In carrying on its activities, the Banca Lombarda

Group deals with a wide range of counterparties

and legitimate interest groups, which are gene-

rally referred to as “stakeholders”. Certain of

these fall into well defined categories, while

others are not so clear and organized.

The stockholders provide the risk capital that makes it possible to do business and grow. They

determine the strategic direction and objectives to be pursued by the Group so that opera-

tions are oriented towards the stable, sustainable and lasting creation of value, in compliance

with the rules and professional ethics and full acceptance of the institutional responsibilities of

a banking group.

The Persons who work for the Group, whether as employees or financial consultants, contri-

bute their professionalism, skills and integrity and represent the principal asset of the business

and a critical factor for its success. The motivation and daily commitment of collaborators

makes a decisive contribution to the growth of the Group which, in turn, generates opportu-

nities for professional growth and security for their future.

Customers are the focus of business activities and the final recipients of the banking services

provided. The achievement of maximum customer satisfaction is a priority objective that dri-

ves operating decisions and commercial policies, while making every effort to inform and

educate them.

MAIN STAKEHOLDERS

Stakeholders Customers

Human resources Community and environment

Financial System

Suppliers

Public Institutions

51The social and environmental report

50

Relations with public institutions concern the regulatory sphere, giving rise to the obli-

gation to comply with all of the legal provisions that govern the Group’s activity, as well

as to pay taxes and social security contributions. For many years, the Group has also pro-

vided specific banking services to local authorities.

The Group’s relations with the financial and banking system derive from normal inter-

bank activities.

Relationships with institutional authorities (the Bank of Italy, Consob, Borsa Italiana and

other financial institutions) are of a regulatory nature, involving the punctual and com-

plete implementation by the Group of all regulatory instructions. The Group also colla-

borates with various trade associations.

The Group’s contribution to the development of the Community primarily involves the

performance of banking activities that contribute significantly to the development of the

local economy, remunerating the savings of families, granting loans and creating

employment, both directly (employees) and indirectly (businesses financed and sup-

pliers). The Group also contributes to the community via specific support for various ini-

tiatives in the artistic, cultural, educational and sporting fields, as well as for associations

and voluntary work.

The development of the Group’s activities, via the consolidation of its market position and the

growth of profitability, generates value for the benefit of all the above counterparts.

Value Added is defined as the increase in value generated by the production and distri-

bution of goods and services as a result of combining the various factors of production.

The allocation of the value added by the Group during 2005 among the various stake-

holders is shown in the value added schedule included in the “Economic Report”.

The format for this schedule is based on the model recommended by ABI, the Italian

Banking Association. Value Added derives from the difference between revenues (value

of production) and consumption.

The value added report comprises two sections:

• Schedule of Total Value Added determined by deducting consumption from net revenues3;

• Allocation of Total Value Added among the various categories of stakeholder.

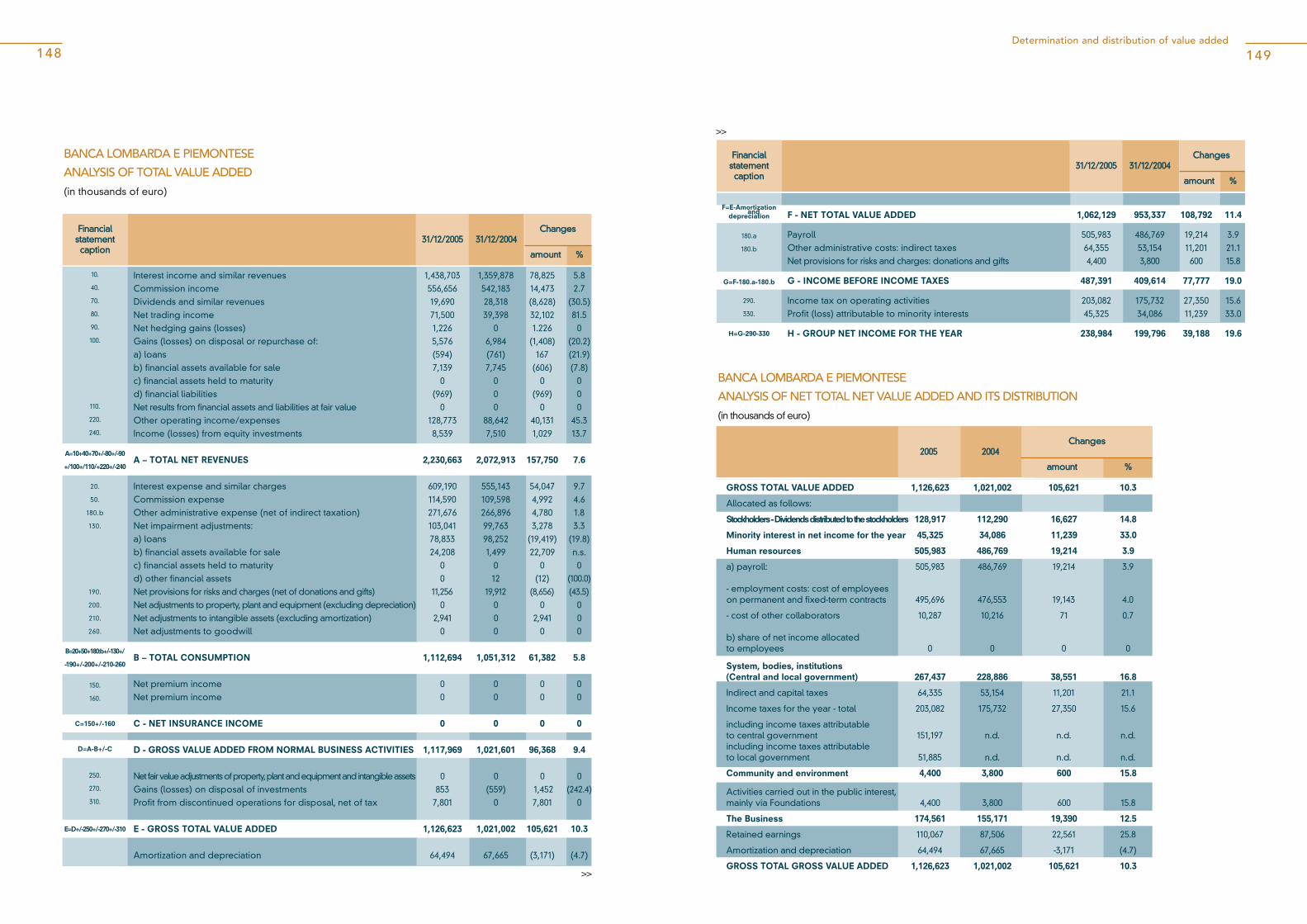

In 2005, the activities of the Banca Lombarda Group generated Gross Total Value Added of

1,126.6 million euro. This amount was allocated among the various stakeholders in the per-

centages shown in the following chart4.

Performance over the past two years reflects an increase in Gross Total Value Added of more

than 10%, despite unfavorable conditions in the economic cycle and the growing level of

competition in the banking sector.

This growth was principally due to the better performance of revenues (especially interest,

other income and trading activities) compared with the more modest increase in consump-

tion, assisted by the containment of administrative expenses and the cost of lending.

3 Revenues consist of interest and commission income, dividends, profits from trading, hedging and the sale of loans and assets,other operating income and income from equity investments; consumption, on the other hand, consists of interest and commissionexpense, other administrative expenses, value adjustments and provisions.

4 The component of value added referred to as “the Business” reflects the self-financing generated by the Group. More specifically,this represents the undistributed profits earned during the year plus depreciation and amortization.

TTOOTTAALL CCOONNSSOOLLIIDDAATTEEDD GGRROOSSSS VVAALLUUEE IINN 22000055 ((11,,112266..66 mmiilliioonn eeuurroo))

Minority interests4.0%

Stockholders11.4%

Business15.5%

Community0.4%

Public institutions23.7%

Human resources44.9%

53The social and environmental report

52

The value added generated for the various stakeholders has changed as follows:

• The value added attributable to the stockholders rose by 14.8% in 2005 to 128.9 million euro.

This reflects consolidated net income not reinvested and derives from the growth in net

income for the year.

• The value added allocated to human resources rose by 3.9% (to 506 million euro). This is

the most significant caption and includes not only payroll costs, but also the commissions

recognized to those involved in the placement of the Group’s products and services, and

the fees of the directors and statutory auditors5.

• The value added allocated to the Public Administration (267.4 million euro in 2005) has risen

by 16.8% due to the improvement in profitability, despite a modest reduction in the effec-

tive tax rate with respect to the prior year.

• The portion allocated to the community amounted to 4.4 million euro in 2005; this repre-

sents growth over the year of 15.8%.

• There was a significant increase (+12.5%) in the value added attributable to The Business

(174.6 million euro in 2005), which represents the self-financing retained by the Group. This

comprises undistributed net income, depreciation and amortization.

• Lastly, the portion of net income allocated to minority interests has increased by 11.2 mil-

lion euro (+33%), to 45.3 million euro at the end of 2005; this comprises the value genera-

ted by the Group for the minority stockholders of the Parent Bank’s direct and indirect

subsidiary companies; it mainly derives from the net income for the year of Banca

Regionale Europea.

See the section that follows the Social and Environmental Report for the detailed schedules

that show the calculation and allocation of value added.

5 The directors’ and statutory auditors’ fees are relatively low compared with the other amounts comprising the value added allo-cated to human resources.

TTOOTTAALL GGRROOSSSS VVAALLUUEE AADDDDEEDD ((iinn mmiilliioonn ooff eeuurroo))

112288,,99

TToottaall 11,,112266,,66 TToottaall 11,,002211,,00

22000055 22000044

SSttoocckkhhoollddeerr

MMiinnoorriittyy iinntteerreessttss

HHuummaann rreessoouurrcceess

BBuussiinneessss

CCoommmmuunniittyy

4455,,33

550066,,00

117744,,6644,,44

226677,,44PPuubblliicc eennttiittiieess

111122,,33

3344,,11

448866,,88

115555,,2233,,88

222288,,99

OUR STOCKHOLDERS ARE MAINLY SMALL

AND MEDIUM-SIZED SAVERS, FIRMS AND

ENTREPRENEURS, NON-PROFIT ORGANIZA-

TIONS AND FOUNDATIONS, ESSENTIALLY

BASED IN THE COMMUNITIES WHERE THE

GROUP HAS IT HISTORICAL ROOTS.

BANCA LOMBARDA IS TRULY A “PUBLIC

COMPANY”, WITH A SHAREHOLDER BASE OF

AROUND 44,000 STOCKHOLDERS.

““STOCKHOLDERS

56 57Stockholders

BANCA LOMBARDA STOCK

BANCA LOMBARDA’S RATINGS

THE ETHICAL RATING OF BANCA LOMBARDA

COMMUNICATIONS

STOCKHOLDERS

The stockholders are almost equally split between

physical persons (44%) and legal persons (56%).

The first category essentially comprises small and

medium-sized savers, while the second consists of

companies, non-profit organizations and institutio-

nal investors. They principally derive from the

communities where the Group has it historical

roots (about 80% of the total are resident in the

provinces of Brescia, Cuneo and Milan). Foreign

investors hold a significant and stable interest in

the Group (about 8%, almost all of whom are

based in EU nations).

With regard to the stockholders that are legal persons, non-profit organizations and institutio-

nal investors represent 17.9% and 11.6% respectively of the overall total.

Physical persons hold an average of about 3,300 shares, essentially unchanged with respect to

2004, worth about 40,000 euro.

Analysis by age indicates a marked bias towards the older age brackets: more than 70% of the

stockholders who are physical persons are over 50 years of age, while 40% are over 65.

BBRREEAAKKDDOOWWNN OOFF TTHHEE CCAAPPIITTAALL SSTTOOCCKK

Individuals44.1%

Institutionalinvestitors

11.6%

Not-for-profit17.9%

Other legalentities26.4%

Legalentities55.9%

Centre-South3.1%

Aboroad7.9%

North-East5.2%

Other North-West0.6%

Prov. Cuneo6.5%

Other Lombardy3.6%

Prov. Milano13.4%

Prov. Brescia59.6%

2005

Centre-South2.7%

Aboroad7.4%

North-East6.5%

Other North-West0.6%

Prov. Cuneo6.3%

Other Lombardy3.6%

Prov. Milano14.2%

Prov. Brescia58.6%

2004

GGEEOOGGRRAAPPHHIICC BBRREEAACCKKDDOOWWNN

59Stockholders

58

From the creation of Banca Lombarda at the end of 1998, about 300 stockholders have been

members of a voting and blocking syndicate that strengthens the internal cohesion of the

Group and facilitates its growth.

At the end of 2005, syndicated shares represent about 48.7% of the total share capital.

This agreement, which is renewed every three years, covers the exercise of voting rights at

extraordinary meetings held to change the articles of association. It also restricts the transfer

of shares that have been syndicated.

The agreement that expired in 2004 was renewed until 31 December 2007.

At the end of 2005, Banca Lombarda’s share capital amounted to 322,292,258 euro, represen-

ted by 322,292,258 ordinary shares, par value 1 euro each.

A further 29.3 million shares were issued in 2006, with a total value of 342.8 million euro, pur-

suant to the mandate granted at the Extraordinary Meeting held in 2003, as part of imple-

mentation of the 2006-2008 Business Plan approved by the Board of Directors on 14 March

2006. The enthusiastic take up of the capital increase clearly demonstrated the confidence of

our stockholders in the Group, their appreciation of the results achieved and the underlying

professionalism and commitment displayed.

BANCA LOMBARDA STOCK

Banca Lombarda is listed on the MTA (Mercato Telematico Azionario), the official screen-

based equities market run by Borsa Italiana.

The bank is part of the “Blue Chip” segment, comprising securities with a market capitalization

of more than 800 million euro.

At the end of 2005, the total capitalization (number of shares in circulation multiplied by the

stockmarket price) was about 3.9 billion euro. Following the recent capital increase, the mar-

ket capitalization at the end of July 2006 was about 4.6 billion euro.

Banca Lombarda’s shares in recent years have offered stockholders a constant stream of divi-

dends and remarkable price stability, even at times of major market fluctuations.

This stability emerges clearly from a comparison of the stockmarket performance of Banca

Lombarda shares with the S&P/Mib basket and the Mib banking index over a sufficiently long

period of time.

For example, between the start of 2001 and the end of 2005, the Banca Lombarda share price

rose by 10%, compared with a fall during the same period of 10.2% in the Mibtel index and

5.3% in the Mib Banking index.

From April 2006, Banca Lombarda is part of the Midex, a synthetic index for the shares of listed

companies with a medium-sized capitalization; Banca Lombarda’s stock has the second-largest

weighting within this basket.

BBRREEAAKKDDOOWWNN OOFF IINNDDIIVVIIDDUUAALL SSTTOOCCKKHHOOLLDDEERR OOFF TTHHEE BBAANNCCAA LLOOMMBBAARRDDAA GGRROOUUPP BBYY AAGGEE

81 & over5.4%

Up to 356.2%

36-5020.5%

51-6533.8%

66-8034.1%

BBAANNCCAA LLOOMMBBAARRDDAA SSHHAARREE

112200

111100

110000

9900

8800

7700

6600

5500

4400

ggeenn--0011mmaagg--0011

sseett--0011sseett--0022

ggeenn--0022mmaagg--0022

sseett--0033ggeenn--0033

mmaagg--0033sseett--0044

ggeenn--0044mmaagg--0044

sseett--0055ggeenn--0055

mmaagg--0055

■■ BBAANNCCAA LLOOMMBBAARRDDAA ■■ MMIIBBTTEELL ■■ MMIIBB BBAANNKKIINNGG

61Stockholders

In May 2006, Standard & Poor’s revised its outlook for the Group from stable to positive,

reflecting the improvement in the capitalization of the Group, together with the good level of

efficiency and the quality of our assets.

The opinion of our Group expressed by all three agencies is undoubtedly positive, recogni-

sing our high asset quality, low risk profile and revenue stability.

For completeness, the rating of Banca Lombarda by the three agencies is presented

below against their individual rating scales.

60

The Group has always given preference to policy decisions that result in long-term and sustai-

nable value creation, avoiding any kind of speculative approach.

The results achieved are reflected both in higher net income and an increased dividend per share.

As stated in the 2006-2008 Business Plan, the stockholder remuneration policy is expected to

remain positive in the coming years; the payout ratio (percentage of net income allocated to

dividends) should remain around 50%.

BANCA LOMBARDA’S RATINGS

Ratings represent the assessment by independent, specialist private agencies of a firm’s cre-

dit risk or the ability of an issuer to meet its payment commitments. As shown below, the code

used varies depending on the agency concerned and belongs to two macrocategories:

investment and speculative. Banca Lombarda is considered to represent an investment, given

the very good level of solvency.

The three international rating agencies that current track Banca Lombarda confirmed their

ratings in 2005.

SSIIGGNNIIFFIICCAANNTT DDAATTAA AANNDD IINNDDIICCAATTOORRSS FFOORR BBAANNCCAA LLOOMMBBAARRDDAA SSHHAARREESS ((aammoouunnttss iinn EEuurroo))

22000055 IIAASS 22000044 IIAASS 22000033 BBEEFFOORREEIIAASS

AAGGEENNCCYY SSHHOORRTT--TTEERRMMDDEEBBTT

MMEEDDIIUUMM--LLOONNGG TTEERRMM

DDEEBBTTOOUUTTLLOOOOKK

FFIINNAANNCCIIAALLSSTTRREENNGGTTHH

((mmiinn.. EE--mmaaxx.. AA))

IINNDDIIVVIIDDUUAALL((mmiinn.. EE--mmaaxx.. AA))

SSUUPPPPOORRTT((mmiinn.. 11--mmaaxx.. 55))

Moody’s P-1 A2 Stable C+

Fitch Ratings F1 A Stable B/C 3

Standard & A-2 A- PositivePoor’s

Note that the indicator for “financial strength” provided by Moody’s reflects the possibility that the Bank might need external supportfrom the Group’s stockholders or official institutions.The “individual” index given by Fitch represents a summary rating of a bank’s intrinsic strength (profitability, financial equilibrium, mana-gement capability, operating context, commercial network), on the assumption that it cannot rely on obtaining any kind of external sup-port. The “support” indicator, on the other hand, concerns their view about access to concrete and timely external support (from theState or key institutional stockholders) should the Bank, in hypothetical circumstances, find itself in difficulty.Ratings at 30 June 2006

Market prices at year-end 12.04 9.82 10.08

Market cap. at year-end (in millions of euro) 3,881 3,150 3,191

Stockholders’ equity per share* 6.19 5.72 5.96

Consolidated earnings per share* 0.74 0.62 0.35

Dividend per share 0.40 0.35 0.30

*calculated using the no. of shares at year-end.

SSTTAANNDDAARRDD && PPOOOORR’’SS MMOOOODDYY’’SS FFIITTCCHHRRAATTIINNGGSS

SShhoorrtttteerrmm

A-1+A-1A-2A-3BCD

LLoonngg tteerrmmAAAAA+AAAA-A+AA-

BBB+BBBBBB-BB+BBBB-B+BB-

CCC+CCCCCC-CCC

SShhoorrtttteerrmm

Prime-1Prime-2Prime-3

Not prime

LLoonngg tteerrmmAaaAa1AA2AA3A1A2A3

BAA1BAA2BAA3BA1BA2BA3B1B2B3

CAACAC

SShhoorrtttteerrmm

F1+F1F2F3BCD

LLoonngg tteerrmmAAAAA+AAAA-A+AA-

BBB+BBBBBB-BB+BBBB-B+BB-

CCC+CCCCCC-CCC

DDDDDD

■■ RRAATTIINNGG BBAANNCCAA LLOOMMBBAARRDDAA ■■ SSPPEECCUULLAATTIIVVEE GGRRAADDEE

63Stockholders

62

THE ETHICAL RATING OF BANCA LOMBARDA

In addition to the important opinions of the above rating agencies, there are a number of

international agencies that provide opinions on the sustainability of results, social and envi-

ronmental performance, respect for the environment and the rights of employees.

These ratings generally make reference to samples drawn from companies with the largest

capitalizations, thus penalizing Banca Lombarda stock which is not covered by them.

The bank’s stock is however included in the AXIA CSR index, comprising the 30 Italian com-

panies with a CSR rating that falls within a given range of values, prepared by Axia Financial

Research; in particular, this agency has allocated a summary rating of “B++” to Banca

Lombarda, which reflects the good performance of the bank with respect to the reference

standards (especially the excellent approach to the local economy and the commitment to

respecting the principle of equal rights and opportunities for employees).

Although not present in the Ecapital indices (not due to a poor ethical rating, but for reasons

of comparability with other market indices), the stock has nevertheless received a good

“E+” rating, largely due to the strong performance regarding corporate governance and, in

general, relations with customers and stockholders.

COMMUNICATIONS

In addition to the timely market announcements made in accordance with the disclosure

requirements for listed companies, Banca Lombarda also organizes periodic meetings with

financial analysts and the press to provide more detailed insight into the Group’s results and

operating performance.

Summaries of these meetings are published via press releases and reported on our institu-

tional website in a reserved area entitled “Investor Relations”, which also includes: informa-

tion on the annual, half-yearly and quarterly financial statements; press releases and various

documents of interest to stockholders and the general public.

During 2005, Banca Lombarda issued 24 press releases, including 11 of a financial nature

(annual report, interim results, acquisitions and corporate operations); 5 of a commercial natu-

re (launch of new products and agreements with institutional counterparts) and 8 of an insti-

tutional nature (appointments, calendar of stockholders’ meetings, opening of

Representative Office, etc.).

In particular, activities in support of the opening of the Representative Office in Shanghai inclu-

ded the involvement of top management and Brescia-based institutions.

External communications also took the form of interviews given by top management and

those in charge of the holding and Group companies.

The Group also attracted considerable attention from the press, with the publication of more

than 200 articles in the main national newspapers (Il Sole 24 Ore, Milano Finanza, Corriere della

Sera and others) and in local newspapers (Giornale di Brescia, Brescia Oggi, La Provincia

Pavese, Il Corriere d’Alba).

The news contained in our press releases was also published on the web by various sites spe-

cializing in economic and financial information.

In addition, Banca Lombarda publishes all these press releases on its own website

www.bancalombarda.it

The website was expanded considerably during 2006, as part of the constant improvement of

institutional communications, thus increasing the availability of corporate documentation in line

with best practice, while also improving accessibility, usability, speed and ease of navigation.

HUMAN RESOURCES ARE CONSIDERED TO BE OF

FUNDAMENTAL IMPORTANCE TO THE BUSINESS.

THE DEDICATION AND PROFESSIONALISM OF

EMPLOYEES ARE ESSENTIAL VALUES FOR THE

SHARING AND ACHIEVEMENT OF THE OBJECTI-

VES SET BY THE GROUP AND ALL THE COMPANIES

WITHIN IT.

““HUMAN RESOURCES

67Human resources66

CREATION OF NEW JOBS

PERSONNEL SELECTION

TRAINING IN ORDER TO GROW AND COMPLETE

CAREER DEVELOPMENT AND INCENTIVES SYSTEMS

EQUAL OPPORTUNITIES

OTHER SOCIAL ASPECTS

EMPLOYMENT CONTRACTS

SUPPLEMENTARY PENSIONS AND ACCIDENT/HEALTHCARECOVER

STAFF BENEFITS

HEALTH AND SAFETY IN THE WORKPLACE

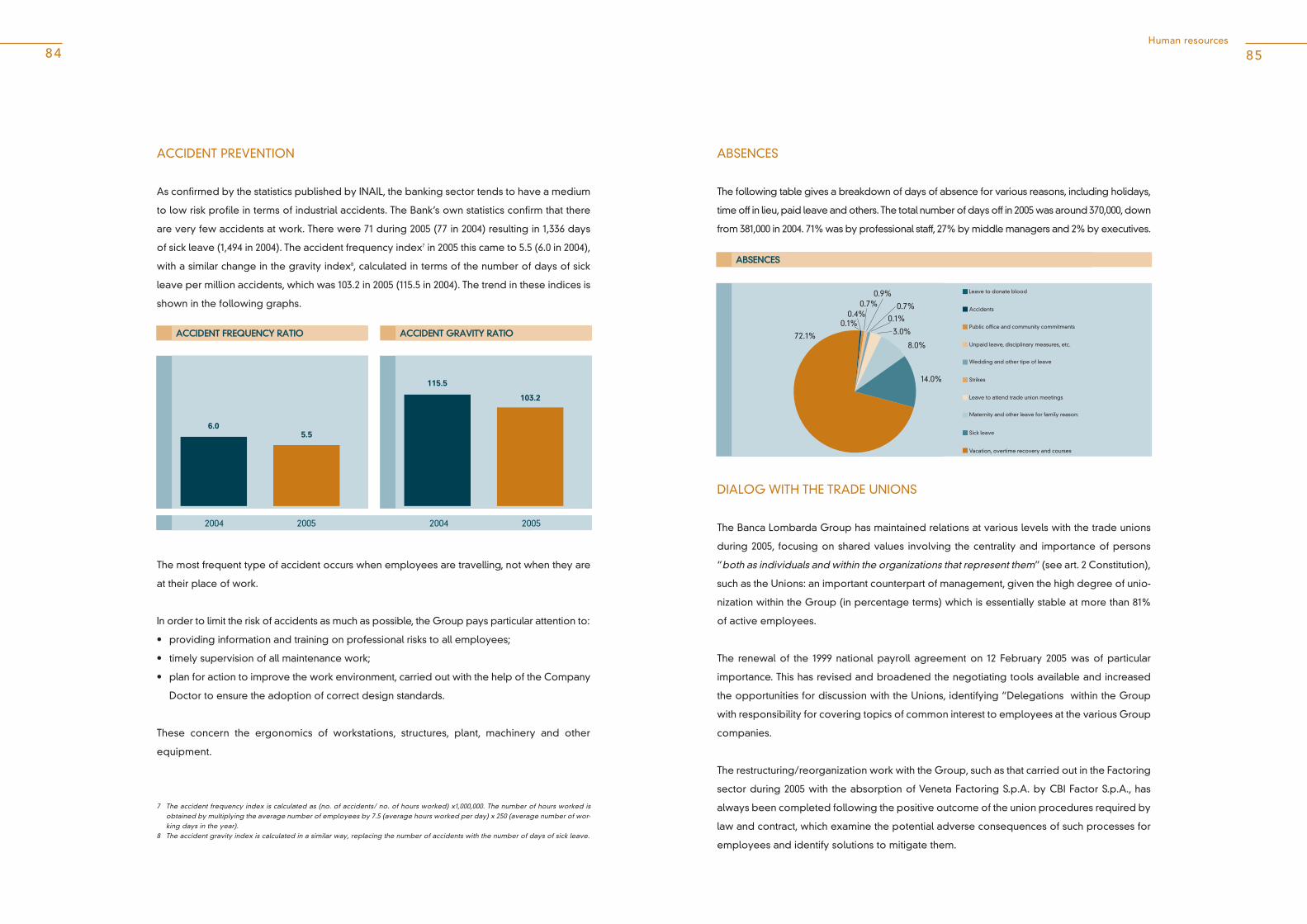

ACCIDENT PREVENTION

ABSENCES

DIALOG WITH THE TRADE UNIONS

HUMAN RESOURCES

The Group is therefore committed to develo-

ping the abilities and skills of each employee, so

that their energy and creativity can be fully

expressed in the realization of their potential. In

this context, the Group offers all employees the

same opportunities for professional growth,

ensuring that each is treated equally, based on

merit, without any discrimination due to gender,

age, disability, religion, nationality, ethnic origin,

political beliefs or union affiliation.

CREATION OF NEW JOBS

At the end of 2005 the Banca Lombarda Group had a

total of 7,562 employees, unchanged with respect to

2004 (7,562). Most employees live in the north-west of

Italy, although many reside in central Italy, confirming

the Group’s contribution towards the creation of jobs

in the main areas where we are present6.

In aggregate terms, net of intercompany transfers, 255 people were hired in 2005, including 2

deriving from the inclusion of the Representative Office in Shanghai (China) within the scope

of consolidation. There were 257 resignations during the year, partly due to normal staff tur-

nover and partly because they were able to access the Solidarity Fund.

These numbers highlight that voluntary early retirement has been accompanied by an appre-

ciable level of recruitment involving young persons starting work and others with experience.

The staff turnover ratio (the number of resignations during the year as a percentage of the

number of employees at the start of the year) was 3.4%, down from 5.0% in 2004. The figures

for resignations and recruitments do not include short-term contracts that were renewed on

expiry or converted into more permanent forms of employment.

6 The number of employees at the end of the year refers to those on the books of the Group companies included in the line-by-lineconsolidation. Moreover, new hires and resignations have been measured with reference to all Banca Lombarda Group compa-nies consolidated line-by-line, with the exclusion of foreign companies. For these, the net change in the number of employees bet-ween 31 December 2004 and 2005 has been considered. The following charts analyze employees by length of service, age, education, gender, grade and type of employment contract,based on the personnel on the books of the companies included in the line-by-line consolidation, with the exclusion of MercatiFinanziari, Banca Lombarda International, Veneta Finanziera, Gestioni Lombarda Suisse and 14 employees of Banco di Brescia’s andBanca Regionale Europea’s foreign branches. For the analysis of absences, reference has been made to the personnel on thebooks with the exclusion of Mercati Finanziari, Banca Lombarda International, Financiera Veneta, Gestioni Lombarda Suisse and 14employees of Banco di Brescia’s and Banca Regionale Europea’s foreign branches.

CCHHAANNGGEE IINN TTHHEE NNUUMMBBEERR OOFF EEMMPPLLOOYYEEEESS IINN 22000055

7,562

31.12.2004 New hires Leavers New Companies 31.12.2005

+255 -257 +2 7,562

69Human resources

68

Resignations as a proportion of the number of employees at the start of the year were stable

(1.8%), confirming the high level of loyalty to the Group.

The following analysis was made category by category to understand the reasons for peo-

ple leaving the Bank during 2005.

In 2005, the Group again made use of the Solidarity Fund as a way to achieve greater

flexibility in handling the process of corporate restructuring and reorganization.

Important projects involving Group companies have been discussed with trade union

representatives with a view to defining the means of access to the “Solidarity Fund to

support incomes, employment and retraining of banking personnel”.

Implementation of a framework protocol defined at Group level, together with subse-

quent enabling agreements signed at company level, made it possible during the

period for 51 employees, generally of a certain age, to take voluntary early retirement

or pre-retirement.

Against these departures, our replacement policy was to hire people only for those

positions envisaged by the new organizational model, with the recruitment of young

talent with special focus on the new forms of professional skill.

The hiring of these new resources has expanded the younger age bands; at present,

employees not over the age of 40 represent more than 50% of the total, while about

40% of staff have been with the Bank for not more than 10 years.

PERSONNEL SELECTION

The progressive consolidation of the Group demonstrates that human resources represent

the principal source of competitive advantage and are one of its fundamental assets.

Personnel research, recruitment and selection is an established and ongoing process

within the Group.

This process is well structured, with a view to identifying human resources with aptitude and

considerable potential.

The Human Resources Department of Banca Lombarda e Piemontese performs search,

recruitment and selection activities on behalf of the entire Group.

Candidates without any previous experience in banking are selected using suitable profiling

techniques that take account of the various needs of the bank and the professional expecta-

tions of individuals.

The selection process consists of two separate steps:

- a introductory one-to-one interview

- a group interview at the assessment center

Around 700 recruitment interviews were carried out in 2005. Of these, 320 candidates passed

% LEAVERS IN 2005 ON THE NUMBER OF EMPLOYEESAT THE START OF THE YEAR (TOTAL 3.4%)

% LEAVERS IN 2004 ON THE NUMBER OF EMPLOYEESAT THE START OF THE YEAR (TOTAL 5.0%)

0.2% other

pre-retirement

contract expiry

retirement

resignation

0.7%

0.2%

0.4%

1.8%

0.3% other

pre-retirement

contract expiry

retirement

resignation

2.1%

0.3%

0.6%

1.6%