2004 Annual GOCC financial report

62

2004 Annual Financial Report Government-Owned and/or Controlled Corporations Volume II-A

-

Upload

r-seachon-lanete -

Category

Documents

-

view

225 -

download

4

description

GOCCFinancialAFRPCSO

Transcript of 2004 Annual GOCC financial report

2004

Annual Financial Report

Government-Owned and/or Controlled Corporations

Volume II-A

TABLE OF CONTENTS

Page

I INTRODUCTION 1

II FINANCIAL STATEMENTS Condensed Balance Sheet 2 Condensed Statement of Income and Expenses 3 Condensed Statement of Cash Flows 4

III NOTES TO FINANCIAL STATEMENTS 5

IV FINANCIAL HIGHLIGHTS AND ANALYSES Executive Summary 10 Balance Sheet Assets 13 Liabilities 22 Deferred Credits 28 Equity 28 Statement of Income and Expenses Income 33 Subsidy Income 36 Expenses 38 Share of the National Government on the Income of GOCCs 42 Provision for Income Tax 42 Statement of Cash Flows Operating Activities 43 Investing Activities 44 Financing Activities 45

V LIST OF ACRONYMS 47

Introduction

I N T R O D U C T I O N

As part of the constitutional mandate provided in Section 4, Article IX-D of the Philippine Constitution, the Commission on Audit (COA) submits to the President and the Congress the Annual Financial Report (AFR) of Government-Owned and/or Controlled Corporations (GOCCs), including their subsidiaries and attached agencies. As required in Section 41 of Presidential Decree No. 1445, such report shall be submitted not later than September 30 of each year. This year’s AFR consists of consolidated condensed and detailed financial statements in comparative forms showing the financial position, performance, and inflows and outflows of cash of GOCCs. These statements are supported by textual and tabular analyses reflecting the increases and decreases in assets, liabilities, equity, income/revenues and expenses. The AFR presents the corporations with the biggest balances of selected asset and liability accounts. It also features the top ten income/revenue earning corporations and the ten corporations with the biggest expenses. The early submission of the AFR aims to provide the executive and legislative branches of government, the agency management and other users of financial statements with timely and relevant information which could be used in budget planning, preparation and legislation. The AFR is an effective tool for fiscal policy formulation and for informing the general public about the status of finances and operations of government corporations. More importantly, it helps determine whether agency management is efficient in the stewardship of government resources. This report was based from financial statements of 124 GOCCs submitted to COA through the Corporate Government Sector (CGS). All the financial statements used were audited except those of the Philippine National Oil Company. The following corporations which were non-operational in 2004, did not submit financial statements:

1. Luzon Integrated Services, Inc. 2. National Precision Cutting Tools, Inc. 3. National Slipways Corporation 4. National Stevedoring and Lighterage Corporation 5. National Trucking and Forwarding Corporation 6. Philippine National Lines 7. Tacoma Bay Shipping Company, Inc. 8. Inter-island Gas Service, Inc.

Northern Foods Corporation which adopts June 1 to May 31 as its accounting period was not included in this AFR because of non-submission of its financial statements. Also excluded were 433 Water Districts which were not audited by COA during fiscal year 2004. Restated figures of GOCCs financial statements as of December 31, 2003 were used in this report to make them comparable with the 2004 financial statements. This AFR is published in two volumes as follows:

Volume II-A – Comparative Condensed Financial Statements of the GOCCs, Notes to Financial Statements, Financial Highlights and Textual Analyses of the Financial Statements

Volume II-B – Comparative Detailed Consolidated Financial Statements By Cluster, Detailed Financial Statements by Corporation and Breakdown of Foreign Loans

1

Financial Statements

2003As Restated Amount Percent

Current Assets 1,660,041,070.0 1,597,465,814.7 62,575,255.3 3.9

International Reserves (Note 2) 356,000,378.0 372,867,809.0 (16,867,431.0) (4.5) Cash and Cash Equivalents (Note 3) 575,272,940.1 851,045,471.8 (275,772,531.6) (32.4) Short-Term Investments 285,709,095.0 41,778,029.4 243,931,065.5 583.9 Receivables - Net (Note 1c) 368,595,731.3 260,561,897.4 108,033,833.9 41.5 Inventories - Net (Note 1d) 64,314,954.2 61,783,531.5 2,531,422.7 4.1 Other Current Assets 10,147,971.3 9,429,075.5 718,895.8 7.6

Other Assets 206,667,921.0 249,780,664.3 (43,112,743.3) (17.3)

Miscellaneous Assets and Deferred Charges 65,412,814.3 61,779,898.4 3,632,916.0 5.9 Other Assets 141,255,106.7 188,000,765.9 (46,745,659.2) (24.9)

Contingent Assets 8,569,629.9 8,554,007.5 15,622.4 0.2

Investments and Fixed Assets 2,630,752,655.0 2,643,430,064.8 (12,677,409.8) (0.5)

Investments - Net 1,327,986,264.6 1,295,709,623.5 32,276,641.2 2.5 Fixed Assets - Net (Note 4) 1,302,766,390.4 1,347,720,441.3 (44,954,051.0) (3.3)

TOTAL ASSETS 4,506,031,276.0 4,499,230,551.2 6,800,724.7 0.2

Current Liabilities 1,242,970,458.1 1,205,441,325.1 37,529,133.0 3.1

Payables 331,016,005.9 299,874,713.1 31,141,292.8 10.4 Trust Liablities (Note 5) 20,090,360.7 20,895,702.2 (805,341.5) (3.9) Depository Liabilities 537,763,466.2 558,383,759.2 (20,620,292.9) (3.7) Other Current Liabilities 354,100,625.3 326,287,150.7 27,813,474.7 8.5

Contingent Liabilities 1,083,567.9 1,102,979.6 (19,411.7) (1.8)

Other Liabilities 174,542,079.8 213,954,495.9 (39,412,416.1) (18.4)

Long Term Liabilities 2,279,523,469.4 2,472,022,121.0 (192,498,651.6) (7.8)

3,698,119,575.3 3,892,520,921.6 (194,401,346.3) (5.0)

Deferred Credits 58,561,114.0 76,881,149.3 (18,320,035.3) (23.8)

Capital 476,332,841.5 272,641,432.1 203,691,409.4 74.7

Paid-in Capital 386,123,244.7 374,576,938.0 11,546,306.6 3.1 Retained Earnings(Deficit) (Note 6) (619,201,559.3) (758,146,144.6) 138,944,585.3 (18.3) Restricted Capital 709,411,156.1 656,210,638.7 53,200,517.5 8.1

Surplus 273,017,745.1 257,187,048.2 15,830,696.9 6.2

Donated Surplus 20,834,187.0 20,153,475.1 680,711.8 3.4 Invested Surplus 27,722,571.4 27,781,071.0 (58,499.6) (0.2) Appraisal Surplus 217,753,320.6 202,350,486.8 15,402,833.8 7.6 Contingent Surplus 6,707,666.3 6,902,015.3 (194,349.0) (2.8)

749,350,586.7 529,828,480.3 219,522,106.4 41.4

4,506,031,276.0 4,499,230,551.2 6,800,724.7 0.2

Difference between totals and sum of components is due to rounding off

ASSETS

EQUITY

TOTAL EQUITY

TOTAL LIABILITIES AND EQUITY

LIABILITIES AND EQUITY

LIABILITIES

TOTAL LIABILITIES

Increase (Decrease)

Republic of the PhilippinesGovernment Owned and/or Controlled Corporations

Condensed Balance SheetDecember 31, 2004

( in thousand pesos )

Particulars 2004

2

2003Restated Amount Percent

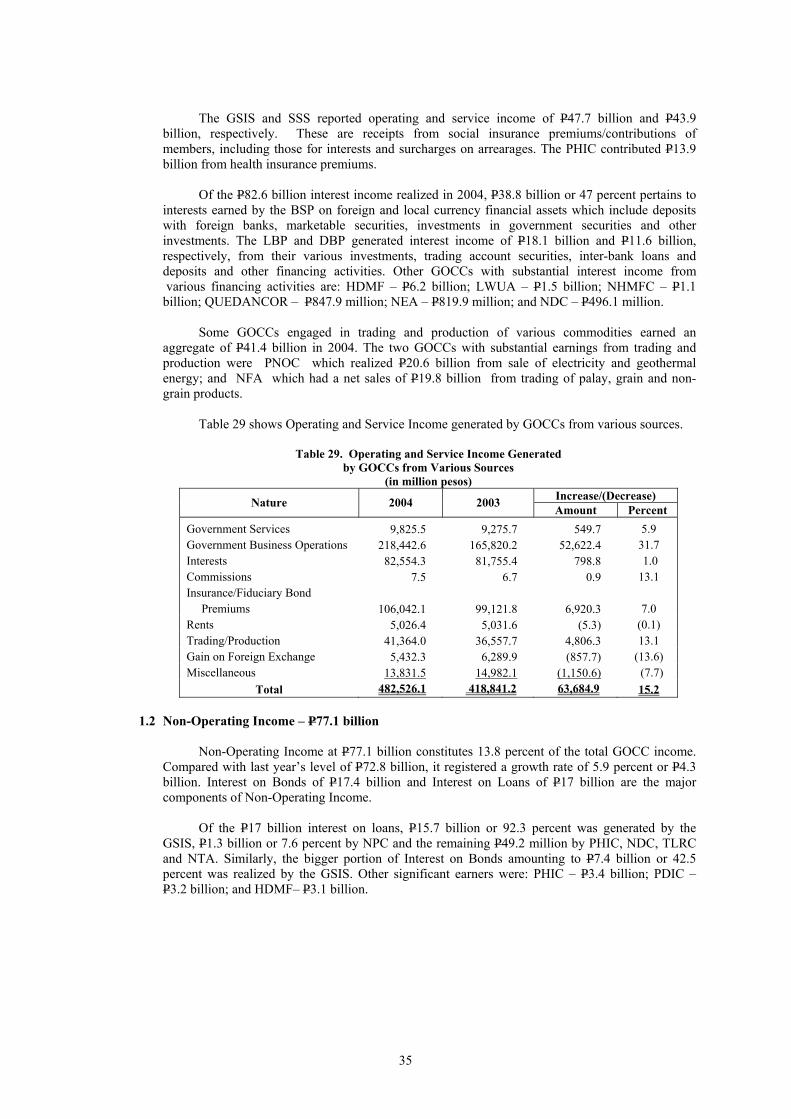

Income 559,632,333.5 491,612,261.9 68,020,071.7 13.8 Operating and Service Income (Note 7) 482,526,119.7 418,841,179.4 63,684,940.3 15.2 Non-Operating Income (Note 8) 77,106,213.9 72,771,082.5 4,335,131.4 6.0

Less: Share of the National Government (Note 9) 9,810,414.5 8,481,102.7 1,329,311.8 15.7 Income After Share of National Government 549,821,919.0 483,131,159.2 66,690,759.9 13.8

Expenses 532,489,420.9 559,797,647.3 (27,308,226.4) (4.9) Personal Services 44,675,821.7 43,191,533.3 1,484,288.4 3.4 Maintenance and Other Operating Expenses 486,945,270.4 515,885,531.0 (28,940,260.6) (5.6) Capital Expenditures (Note 10) 868,328.9 720,582.9 147,745.9 20.5

Net Income(Loss) Before Subsidy 17,332,498.1 (76,666,488.1) 93,998,986.2 (122.6) Add: Subsidy from National Government (Note 11a) 9,976,699.6 13,023,665.5 (3,046,965.9) (23.4) Subsidy from LGUs (Note 11b) 473,302.5 220,205.6 253,097.0 114.9 Subsidy from GOCCs (Note 11c) 1,111,935.3 93,912.5 1,018,022.7 1,084.0 Subsidy from Other Sources 7,042.7 7,958.1 (915.5) (11.5)

Net Income (Loss) Before Extraordinary Loss 28,901,478.2 (63,320,746.4) 92,222,224.5 (145.6) Less: Loss from Reclassification of Investments from

Investment in Associates to InvestmentAvailable for Sale Securities 7,519,938.0 (7,519,938.0) (100.0)

Net Income (Loss) Before Income Tax 28,901,478.2 (70,840,684.4) 99,742,162.5 (140.8) Less: Provision for Income Tax 3,953,578.6 3,692,202.8 261,375.9 7.1

NET INCOME (LOSS) AFTER TAX 24,947,899.5 (74,532,887.1) 99,480,786.7 (133.5)

Difference between totals and sum of components is due to rounding off

2004

Republic of the PhilippinesGovernment Owned and/or Controlled Corporations

Condensed Statement of Income and ExpensesFor the Year Ended December 31, 2004

(in thousand pesos)

Increase/(Decrease)Particulars

3

Amount Percent

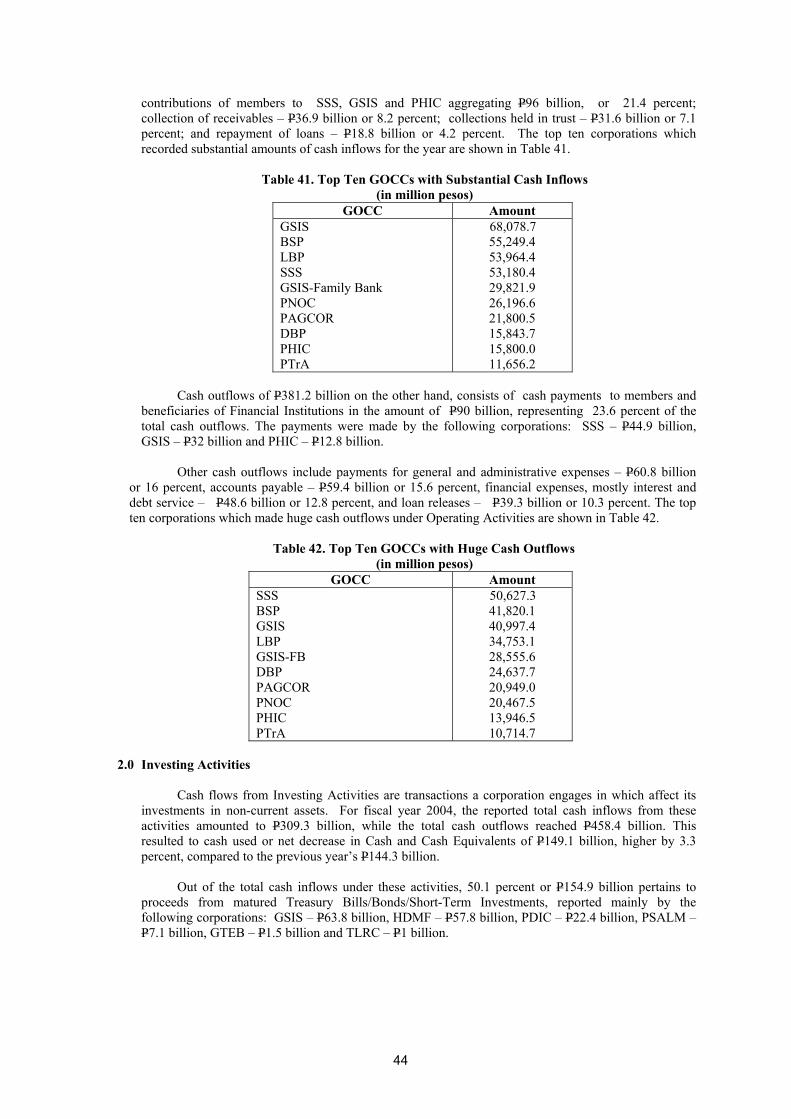

Cash Flows from Operating Activities:Cash Inflows 447,739,689.6 313,170,344.3 134,569,345.4 43.0 Cash Outflows 381,188,902.9 267,109,733.1 114,079,169.8 42.7

Cash Provided by (Used in) Operating Activities 66,550,786.7 46,060,611.2 20,490,175.5 44.5

Cash Flows from Investing Activities:Cash Inflows 309,293,905.7 224,355,541.7 84,938,363.9 37.9 Cash Outlows 458,400,074.3 368,633,459.0 89,766,615.3 24.4

Cash Provided by (Used in) Investing Activities (149,106,168.7) (144,277,917.3) (4,828,251.4) 3.3

Cash Flows from Financing Activities:Cash Inflows 306,168,472.5 287,860,908.0 18,307,564.5 6.4 Cash Outflows 291,905,219.5 154,696,890.1 137,208,329.3 88.7

Cash Provided by (Used in) Financing Activities 14,263,253.0 133,164,017.9 (118,900,764.9) (89.3)

Effects of Exchange Rate Changes on Cash and Cash Equivalents 1,683,962.7 19,293,700.7 (17,609,737.9) (91.3)

Increase (Decrease) in Cash and Cash Equivalents (66,608,166.3) 54,240,412.4 (120,848,578.7) (222.8)

Add: Cash and Cash Equivalents, Beginning 641,816,885.5 634,246,584.6 7,570,300.8 1.2

Cash and Cash Equivalents at the End 575,208,719.2 688,486,997.0 (113,278,277.8) (16.5)

Difference between totals and sum of components is due to rounding off

Increase (Decrease)20032004

Republic of the Philippines

Comparative Condensed Statement of Cash FlowsFor the Year Ended December 31, 2004

(in thousand pesos)

Government Owned and/or Controlled Corporations

Particulars

4

Notes to Financial Statements

NOTES TO FINANCIAL STATEMENTS

1. Summary of Significant Accounting Policies

a. Basis for Consolidation

The Consolidated Financial Statements show the total account balances of the financial statements submitted within the cut-off date by 124 GOCCs through the Corporate Government Sector of the Commission on Audit as shown below.

Submitted

Cluster

Total No. of GOCCs by Cluster

Total

Parent

Attached Agency

Subsidiary

I Financial A 15 15 4 2 9 II Financial B 31* 23 12 11 III Public Utilities 450** 17 9 8 IV Industrial and Area

Development and Regulatory

26

26

16

10

V Agricultural, Trading and Promotional

27

26

17

9

VI Social, Cultural and Scientific

17

17

17

__

___

Total 566 124 75 2 47

* Includes 8 Subsidiaries which are no longer operational ** Includes 433 Water Districts the financial transactions of which for fiscal year 2004 have not yet been audited as of date

The consolidated figures in this report include unaudited financial statements of PNOC, the

parent corporation, as of June 30, 2005.

Of the 121 Statements of Cash Flows submitted, 90 GOCCs used the Direct Method, while 31 used the Indirect Method.

b. Basis of Accounting for Income and Expenses

Majority of the GOCCs use the accrual method of recognizing income and expenses. Cash

basis is used only when accrual method is impractical. Other GOCCs apply the modified accrual, modified cash and the percentage of completion method for income from sale of condominium units and contract job, respectively. Under this method, the BCDA’s gross profit on the sale of condominium units is recognized only after the related obligations of the Joint Venture Partners are fulfilled, while NIA Consult, Incorporated’s amount of revenue is related to the percentage of the total project work that was performed during the period.

c. Allowance for Doubtful Accounts

The Allowance for Doubtful Accounts is provided based either on the age of the accounts,

collection experience of the corporations, past and expected loss experience and identified doubtful accounts. The rates are dependent upon the approval of their respective Boards.

d. Inventories

Consistently, inventories are valued by corporations using the First-in First-out, specific identification, moving average, Last-in First-out and historical cost.

For PEA, completed buildings which are for sale and those under construction are stated at construction cost. Land shares from joint venture arrangements are recorded based on agreed upon values. Expenditures incurred for further development of buildings are added as part of the cost.

5

e. Fixed Assets

Majority of the fixed assets of government corporations are carried at cost less depreciation

in pursuance to IAS No. 16. The useful life and methods of depreciation and amortization are being reviewed periodically to ensure that the period and methods of depreciation are consistent with the expected pattern of economic benefits from items of fixed assets. Under the Public Utilities Cluster, utility plant of PNOC, NPC and the MWSS are carried in the books at appraised values except for additions during the year which are recorded at cost. These assets in the case of the NPC are revalued in consonance with loan covenants with creditor banks and in pursuance to said standard which permits revaluation of properties, plant and equipment. These assets are depreciated on a straight-line method over their estimated useful life.

IAS No. 17 on Leases, which prescribes the accounting policies and disclosures, is applied to

finance and operating lease transactions of government corporations. Leasehold improvements are amortized over the estimated useful life of the improvements or the term of the related lease, whichever is shorter.

In the case of the NPC, electric plants under lease are carried at the amount equivalent to the

computed capacity fees of Built-Operate-Transfer (BOT) Projects for the duration of the cooperation period.

Construction in Progress is stated at cost and is not depreciated until such time that the assets are completed/or put into operational condition.

f. Foreign Currency Translation/Conversion

IAS No. 21 on the effects of changes in foreign exchange rates is adopted. It provides that exchange differences should be recognized as gain or loss in the period in which they arise. Transactions in foreign currency are translated to Philippine Peso using exchange rates applying on the value/settlement date of the transaction. For reporting purposes, foreign currency-denominated accounts (monetary assets and liabilities) are translated/converted into Philippine Peso using the closing exchange rate per BSP at reporting date. Gain or Loss arising from foreign exchange is included in the computation of the annual profits and losses.

g. Financial Statements Presentation

In compliance with IAS No. 13, Retained Earnings and related accounts of fiscal year 2003 are restated for comparative presentation with those accounts in fiscal year 2004.

2. International Reserves

This account consists of international reserves of P356,000,378,000 as reported by the BSP and

the CB-BOL, lower by P16,867,431,000 or 4.5 percent compared to fiscal year 2003. The amount includes profits realized and losses sustained from the revaluation of assets and liabilities in gold of foreign currencies as a result of changes in gold value of the peso or of changes in parities/exchange rates of foreign currencies in peso. The components of the international reserves excluding the amount of P564,763,358,000 which was considered in this report as cash and cash equivalent for the cash flow is shown below.

Amount (in pesos) Particulars 2004 2003 a. BSP (net of cash and cash equivalent)

Gold in bullion vault P30,287,582,000.00 P11,797,812,000.00 Gold with Foreign financial Institutions 145,049,614,000.00 177,650,005,000.00 International Monetary Fund Special Drawing Rights

56,283,000.00

98,517,000.00

Investments 151,753,027,000.00 147,809,638,000.00 Accrued Interest Receivables 3,534,356,000.00 4,404,836,000.00

Sub-Total 330,680,862,000.00 341,760,808,000.00b. CB-BOL Revaluation 25,319,516,000.00 31,107,001,000.00

Total (Net) P356,000,378,000.00 P372,867,809,000.00

6

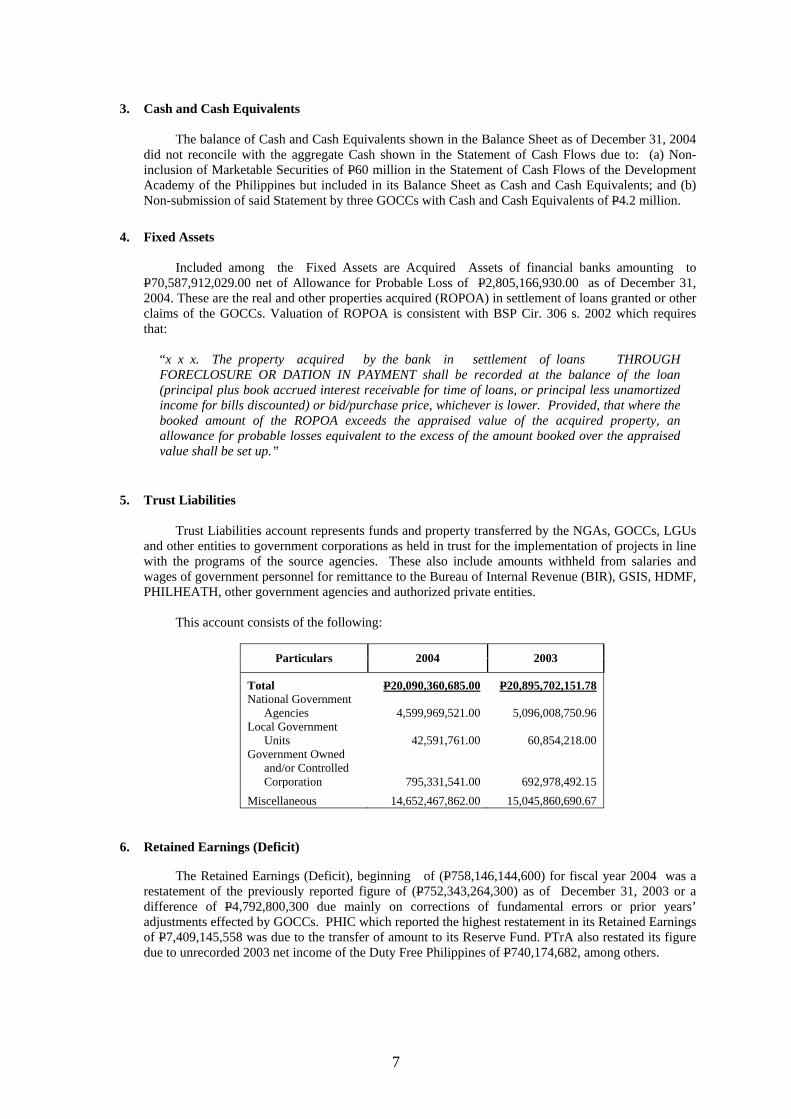

3. Cash and Cash Equivalents

The balance of Cash and Cash Equivalents shown in the Balance Sheet as of December 31, 2004

did not reconcile with the aggregate Cash shown in the Statement of Cash Flows due to: (a) Non-inclusion of Marketable Securities of P60 million in the Statement of Cash Flows of the Development Academy of the Philippines but included in its Balance Sheet as Cash and Cash Equivalents; and (b) Non-submission of said Statement by three GOCCs with Cash and Cash Equivalents of P4.2 million.

4. Fixed Assets

Included among the Fixed Assets are Acquired Assets of financial banks amounting to P70,587,912,029.00 net of Allowance for Probable Loss of P2,805,166,930.00 as of December 31, 2004. These are the real and other properties acquired (ROPOA) in settlement of loans granted or other claims of the GOCCs. Valuation of ROPOA is consistent with BSP Cir. 306 s. 2002 which requires that:

“x x x. The property acquired by the bank in settlement of loans THROUGH FORECLOSURE OR DATION IN PAYMENT shall be recorded at the balance of the loan (principal plus book accrued interest receivable for time of loans, or principal less unamortized income for bills discounted) or bid/purchase price, whichever is lower. Provided, that where the booked amount of the ROPOA exceeds the appraised value of the acquired property, an allowance for probable losses equivalent to the excess of the amount booked over the appraised value shall be set up.”

5. Trust Liabilities Trust Liabilities account represents funds and property transferred by the NGAs, GOCCs, LGUs

and other entities to government corporations as held in trust for the implementation of projects in line with the programs of the source agencies. These also include amounts withheld from salaries and wages of government personnel for remittance to the Bureau of Internal Revenue (BIR), GSIS, HDMF, PHILHEATH, other government agencies and authorized private entities.

This account consists of the following:

Particulars 2004 2003

Total P20,090,360,685.00 P20,895,702,151.78National Government

Agencies 4,599,969,521.00 5,096,008,750.96 Local Government

Units 42,591,761.00 60,854,218.00 Government Owned

and/or Controlled Corporation 795,331,541.00 692,978,492.15

Miscellaneous 14,652,467,862.00 15,045,860,690.67

6. Retained Earnings (Deficit)

The Retained Earnings (Deficit), beginning of (P758,146,144,600) for fiscal year 2004 was a restatement of the previously reported figure of (P752,343,264,300) as of December 31, 2003 or a difference of P4,792,800,300 due mainly on corrections of fundamental errors or prior years’ adjustments effected by GOCCs. PHIC which reported the highest restatement in its Retained Earnings of P7,409,145,558 was due to the transfer of amount to its Reserve Fund. PTrA also restated its figure due to unrecorded 2003 net income of the Duty Free Philippines of P740,174,682, among others.

7

7. Operating and Service Income

The top ten corporations with the biggest amount of Operating and Service Income whose

combined earnings constitute 84.6 percent of the aggregate income of 124 GOCCs are the following:

Corporation Amount 1. NPC P167,275,848,371.00 2. SSS 43,935,823,635.00 3. BSP 43,777,882,000.00 4. GSIS-SIF 41,175,336,624.00 5. PNOC 24,104,806,584.00 6. PAGCOR 20,905,026,874.00 7. LBP 20,785,064,000.00 8. NFA 20,014,010,000.00 9. PHIC 13,958,173,728.00 10. DBP 12,265,584,000.00

Total P 408,197,555,816.00

Members’ contribution to the SSS and GSIS-SIF amounting to P43,935,823,635.00 and P39,508,002,512.00 were recorded as their Operating and Service Income.

8. Non-Operating Income

The following shows the nature/details of Non-Operating Income:

Nature 2004 2003

Income from Public Enterprises/Investments P58,394,754,422.80 P56,149,040,220.72

Miscellaneous Income 17,590,377,450.95 14,989,243,354.42 Fines and Penalties on Non-Tax Revenue 418,107,180.97 462,771,019.19 Capital Revenue 685,924,876.00 1,169,083,524.54 Grants and Aids 17,049,923.00 944,347.00

Total P77,106,213,853.72 P72,771,082,465.87

9. Share of the National Government from Income of PAGCOR and MIAA

This account refers to the share in income given by PAGCOR and MIAA to the National Government in compliance with Presidential Decree No. 1869 dated July 11, 1983 for PAGCOR and Executive Order No. 298 dated July 26, 1987 for MIAA. Comparative data for this income are shown below.

Corporation 2004 2003

PAGCOR P9,196,915,489.00 P7,871,201,671.00 MIAA 613,499,000.00 609,901,000.00 Total P9,810,414,489.00 P8,481,102,671.00

10. Capital Expenditures

This account pertains to PAGCOR’s acquisition of Property, Plant and Equipment (PPE) under

the modified cash basis of accounting wherein capital expenditures in a given period are immediately expensed so that depreciation is no longer provided. The modified cash basis of accounting was adopted by PAGCOR due to its commitment to transfer its net income to the Social Fund under the Office of the President effective August 1, 1988.

8

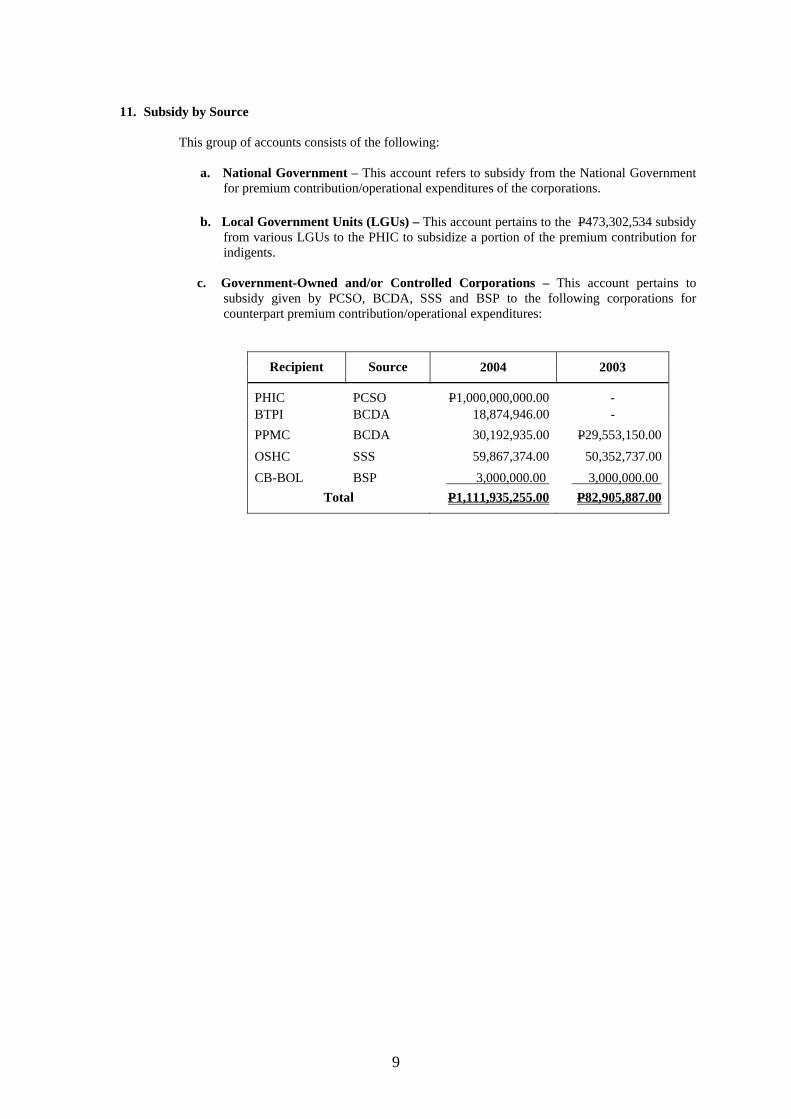

11. Subsidy by Source

This group of accounts consists of the following:

a. National Government – This account refers to subsidy from the National Government

for premium contribution/operational expenditures of the corporations.

b. Local Government Units (LGUs) – This account pertains to the P473,302,534 subsidy from various LGUs to the PHIC to subsidize a portion of the premium contribution for indigents.

c. Government-Owned and/or Controlled Corporations – This account pertains to

subsidy given by PCSO, BCDA, SSS and BSP to the following corporations for counterpart premium contribution/operational expenditures:

Recipient Source 2004 2003

PHIC PCSO P1,000,000,000.00 - BTPI BCDA 18,874,946.00 - PPMC BCDA 30,192,935.00 P29,553,150.00 OSHC SSS 59,867,374.00 50,352,737.00 CB-BOL BSP 3,000,000.00 3,000,000.00

Total P1,111,935,255.00 P82,905,887.00

9

Financial Highlights and Analyses

EXECUTIVE SUMMARY

1.0 BALANCE SHEET

1.1 Assets – P 4,506 billion

The Consolidated Balance Sheet of the government corporate sector reflected a total assets of P4,506 billion. This amount is higher by P6.8 billion or 0.2 percent than last year’s restated figure of P4,499.2 billion. Investments and Fixed Assets of P2,630.8 billion represents 58.4 percent of the total assets. Current Assets of P1,660 billion constitutes 36.8 percent while Other Assets of P206.7 billion and Contingent Assets of P8.6 billion share 4.6 percent and 0.2 percent, respectively.

1.2 Liabilities – P 3,698.1 billion

Total liabilities of P3,698.1 billion decreased by P194.4 billion or five percent from

previous year’s level of P3,892.5 billion, as restated. Liabilities consist of Long Term Liabilities – P2,279.5 billion or 61.6 percent, Current Liabilities – P1,243 billion or 33.6 percent, Other Liabilities – P174.5 billion or 4.7 percent and Contingent Liabilities – P1.1 billion or 0.02 percent.

1.3 Deferred Credits – P58.6 billion

Deferred Credits of P58.6 billion decreased by P18.3 billion or 23.8 percent. This account is composed of Deferred Credits – Miscellaneous of P35.9 billion or 61.4 percent, Deferred Credits to Income of P21.9 billion or 37.4 percent, and other components of P689.2 million or 1.2 percent.

1.4 Equity – P749.3 billion

Equity account totaled P749.3 billion. Net increase in Equity of P 203.7 resulted from increase in Paid-in Capital of P11.5 billion, increase in Restricted Capital of P53.2 billion and decrease in Deficit of P138.9 billion. Seventy nine corporations reported net income, while 44 incurred deficit.

On the aggregate, Surplus account also increased. Appraisal Surplus registered an

increment of P15.4 billion or 7.6 percent while Donated Surplus increased by P680.7 million or 3.4 percent. Contingent Surplus and Invested Surplus decreased by P194.3 million and P58.5 million, respectively.

2.0 STATEMENT OF INCOME AND EXPENSES

2.1 Income and Receipts

The Consolidated Statement of Income and Expenses showed a net income of P24.9 billion, or an increase of 133.4 percent compared to last year’s deficit of P74.5 billion, as restated.

Gross income totaled P559.6 billion, showing an increment of P68 billion or 13.8

percent over last year’s P491.6 billion, as restated. This consists of Operating and Service

10

Income – P482.5 billion or 86.2 percent and Non-Operating Income – P77.1 billion or 13.8 percent.

Income from Public Enterprises/Investments of P58.4 billion and Miscellaneous

Income of P17.6 billion are the two significant components of Non-Operating Income, representing 75.7 percent and 22.8 percent, respectively. Capital Revenue at a minimal figure of P685.9 million, posted a decline of 41.3 percent from last year’s restated figure of P1.2 billion. Grants and Aids amounted to P17 million, recording a P16.1 million growth from last year’s P0.9 million.

. Decrease in gross income of GOCCs by P9.8 billion resulted from remittance of the

National Government’s share from the operating income of PAGCOR and MIAA amounting to P9.2 billion and P6 million, respectively.

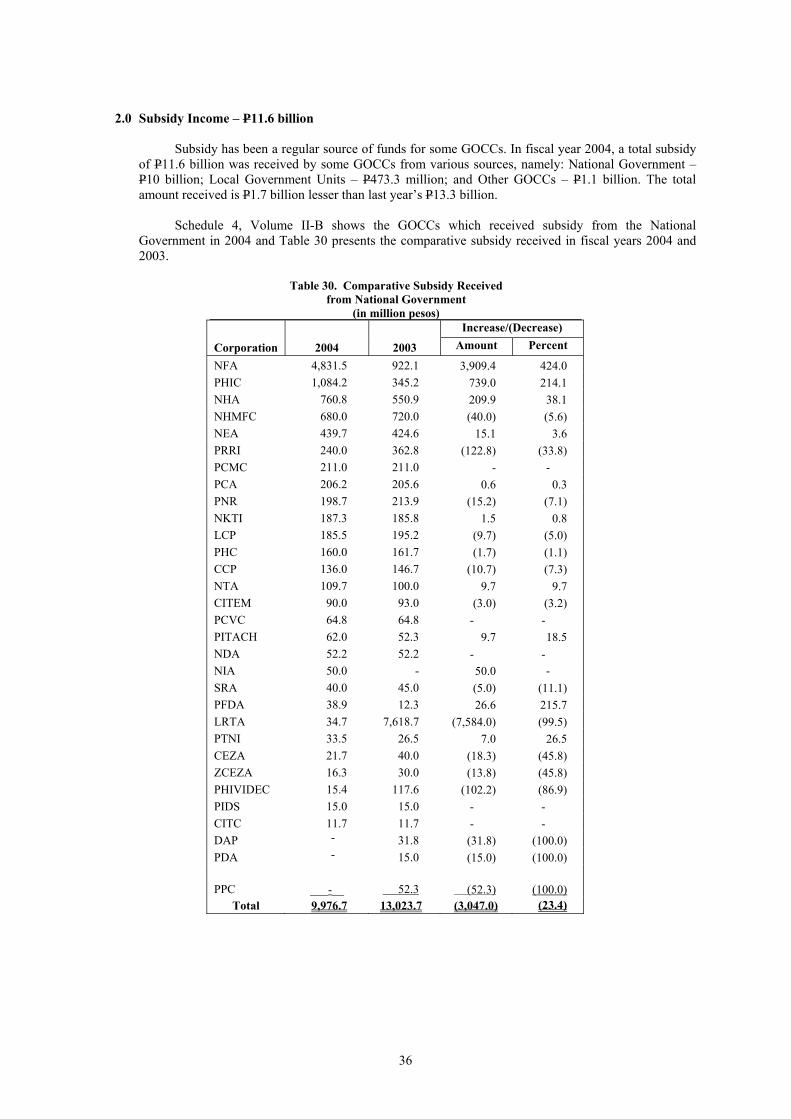

Subsidies to GOCCs amounting to P11.6 billion came from the following sources:

National Government – P10 billion, GOCCs – P1.1 billion, LGUs – P0.5 billion and other sources – P7 million. Thirty-three GOCCs benefited from these subsidies, 13 of which were spared from incurring overdraft in their operations and were even able to report net income because of the said subsidies. The following GOCCs were the recipients of substantial amounts of subsidies from the National Government: NFA – P4.8 billion, PHIC – P1.1 billion, NHA – P760.8 million, NHMFC – P680 million and NEA – P439.7 million.

2.2 Expenses and Provisions for Income Taxes

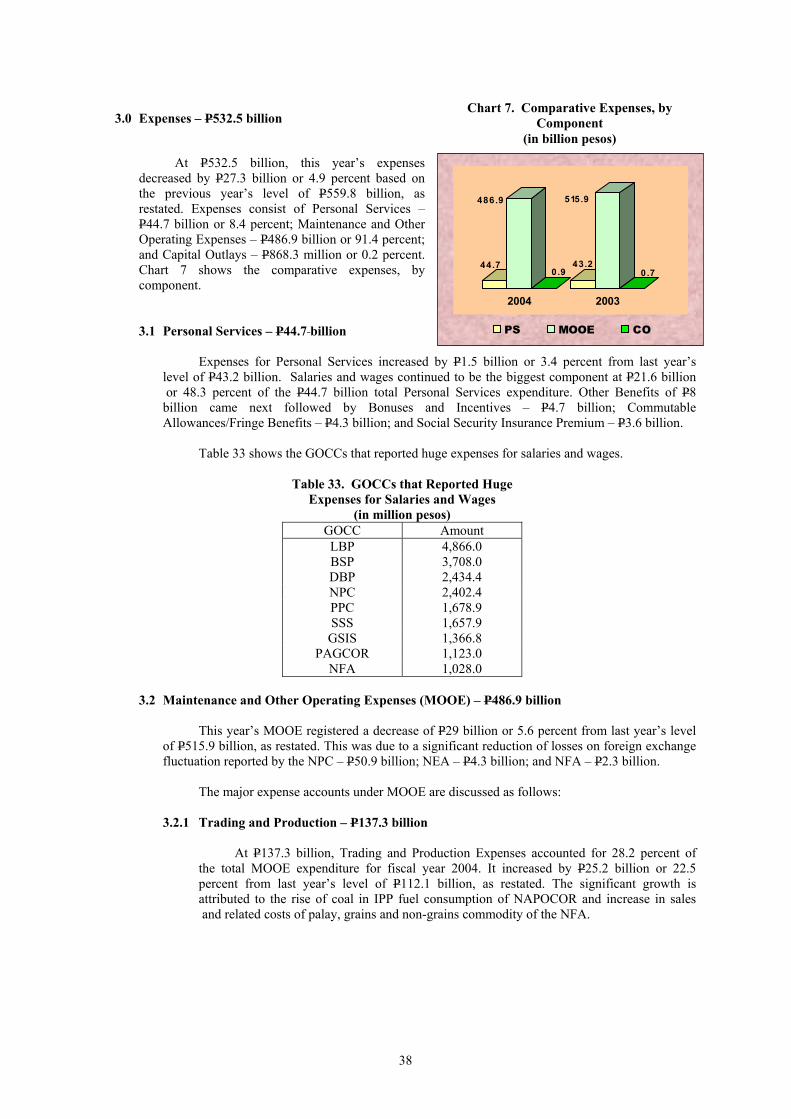

This year’s aggregate expenses of P532.5 billion decreased by P27.3 billion or 4.9 percent based on previous year’s restated amount of P559.8 billion. Personal Services amounted to P44.7 billion or 8.4 percent. Maintenance and Other Operating Expenses totaled P486.9 billion or 91.4 percent while Capital Expenditures amounted to only P868.3 million or 0.2 percent.

Thirty five corporations recorded a total of P4 billion provision for income taxes, higher

by P261.4 million or 7.1 percent than last year’s P3.7 billion, as restated. The combined provision for income taxes of PNOC and BSP of P2.6 billion accounted for 66 percent.

3.0 STATEMENT OF CASH FLOWS

The net effect of inflows and outflows of cash based on the Consolidated Statement of Cash Flows of GOCCs, inclusive of the effects of exchange rate changes, was a negative P66.6 billion for the three activities. Operating and Financing Activities had a positive net effect of P66.6 billion and P14.3 billion, respectively, while Investing Activities showed a negative P149.1 billion. The net effect of exchange rate changes amounted to P1.7 billion.

3.1 Cash Inflows

Cash inflows reflected in the Consolidated Statement totaled P1,063.2 billion, broken

down as follows: Operating – P447.7 billion, Investing – P309.3 billion, and Financing P306.2 billion.

11

3.2 Cash Outflows

Total cash outflows amounted to P1,131.5 billion, 40.5 percent or P458.4 billion of which resulted from Investing Activities, 33.7 percent or P381.2 billion from Operating Activities, and 25.8 percent or P291.9 billion from Financing Activities.

3.3 Cash and Cash Equivalents, End of Year

The accumulated Cash and Cash Equivalents totaled P575.2 billion. The largest amount of P482.5 billion belongs to Financial A Cluster. Figures pertaining to other Clusters in the order of the biggest to the lowest are as follows: Public Utilities – P35.6 billion; Financial B with P30.6 billion; Industrial and Area Development and Regulatory – P11.8 billion; Agricultural, Trading and Promotional and Social, Cultural and Scientific – P7.2 billion each.

12

BALANCE SHEET

1.0 ASSETS – P 4,506 billion

Cu

(in billion pesos)

The fiscal year 2004 Consolidated Balance Sheet of Government Owned and/or Controlled Corporations showed a total assets of P4,506 billion, total liabilities of P3,698.1 billion, a total

deferred credits of P58.6 billion and atotal equity of P749.3 billion. Compared with the restated figures of fiscal year 2003 Consolidated Balance Sheet, Assets and Equity accounts showed increases of P6.8 billion and P219.5 billion, respectively. Liability and Deferred Credits accountsreflected decreases of P194.4 billion and P18.3 billion, respectively. Chart 1 shows the comparative components of the Balance Sheet for fiscal years 2004 and 2003.

Total Assets of the 124 GOCCs reached P4,506 billion at the end of December 31, 2004. Investments and Fixed Assets aggregating P2,630.8 billion represents 58.4 percent of the total Assets.

4,506.0

3,698.1

58.6

749.3

4,499.2

3,892.5

76.9529.8

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2004 2003Assets Liabilities Deferred Credits Equity

(in billion pesos)

1,328.0 29.5%

1,302.8 28.9%

1,660.0 36.8%

206.7 4.6%

249.85.6%

1,597.535.5%

1,347.730.0%

1,295.728.8%

rrent Assets Other Assets Investments Fixed Assets

2004 2003

Table 1. Top Ten GOCCs with the Biggest Amoun (in million pesos)

GOCCs Am unt o GOCCs 1. BSP 1,259,133.4 6. HDMF 2. NPC 1,055,551.9 7. DBP 3. GSIS 309,199.4 8. PNOC 4. LBP 287,698.7 9. PDIC 5. SSS 175,731.2 10. BCDA

1.1 Current Assets – P1,660 billion

Current Assets amounting to P1,660 billion increased b

higher than the 2003 level of P1,597.5 billion. It consists ofP575.3 billion, International Reserves – P356.0 billion, Shobillion, Receivables (net) – P368.6 billion, Inventories (neCurrent Assets – P10.1 billion.

13

The balance of P1,875.2 billion is shared by accounts Current Assets –P1,660 billion, 36.8 percent; Other Assets – P206.7 billion or 4.6 percent and Contingent Assets –P8.6 billion or 0.2 percent. Chart 2 shows the comparative components of the Assets. Table 1 below presents the top ten GOCCs which recorded the biggest amount of Assets.

Chart 1. Components of the Balance Sheet

Chart 2. Components of Assets

t of Assets

Amount 163,595.9 157,121.8 134,462.9 127,619.1

80,453.3

y P62.6 billion or 3.9 percent Cash and Cash Equivalents – rt-term Investments – P285.7 t) – P64.3 billion, and Other

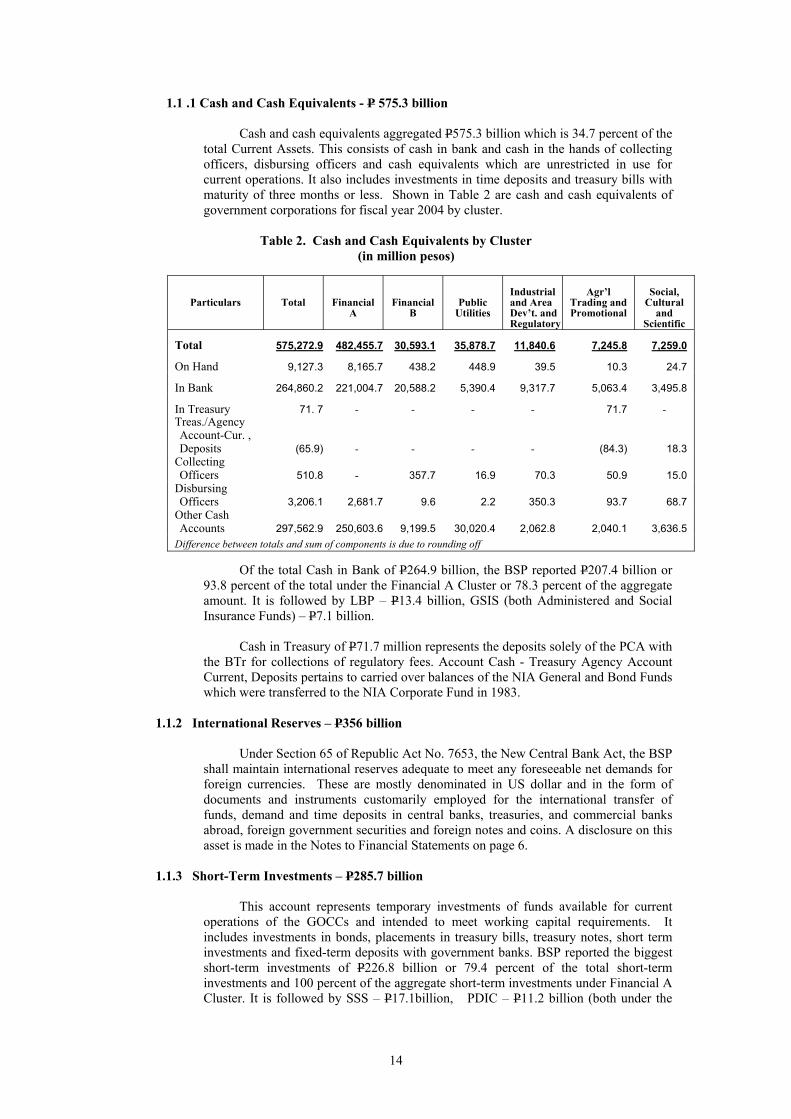

1.1 .1 Cash and Cash Equivalents - P 575.3 billion

Cash and cash equivalents aggregated P575.3 billion which is 34.7 percent of the total Current Assets. This consists of cash in bank and cash in the hands of collecting officers, disbursing officers and cash equivalents which are unrestricted in use for current operations. It also includes investments in time deposits and treasury bills with maturity of three months or less. Shown in Table 2 are cash and cash equivalents of government corporations for fiscal year 2004 by cluster.

Table 2. Cash and Cash Equivalents by Cluster

(in million pesos)

Particulars

Total

Financial A

Financial B

Public Utilities

Industrial and Area Dev’t. and Regulatory

Agr’l

Trading and Promotional

Social,

Cultural and

Scientific Total

575,272.9

482,455.7

30,593.1

35,878.7

11,840.6

7,245.8

7,259.0

On Hand

9,127.3

8,165.7

438.2

448.9

39.5

10.3

24.7

In Bank

264,860.2

221,004.7

20,588.2

5,390.4

9,317.7

5,063.4

3,495.8

In Treasury

71. 7

-

-

-

-

71.7

- Treas./Agency Account-Cur. , Deposits

(65.9)

-

-

-

-

(84.3)

18.3 Collecting Officers

510.8

-

357.7

16.9

70.3

50.9

15.0

Disbursing Officers

3,206.1

2,681.7

9.6

2.2

350.3

93.7

68.7

Other Cash Accounts 297,562.9 250,603.6 9,199.5 30,020.4 2,062.8 2,040.1 3,636.5

Difference between totals and sum of components is due to rounding off

Of the total Cash in Bank of P264.9 billion, the BSP reported P207.4 billion or 93.8 percent of the total under the Financial A Cluster or 78.3 percent of the aggregate amount. It is followed by LBP – P13.4 billion, GSIS (both Administered and Social Insurance Funds) – P7.1 billion.

Cash in Treasury of P71.7 million represents the deposits solely of the PCA with the BTr for collections of regulatory fees. Account Cash - Treasury Agency Account Current, Deposits pertains to carried over balances of the NIA General and Bond Funds which were transferred to the NIA Corporate Fund in 1983.

1.1.2 International Reserves – P356 billion

Under Section 65 of Republic Act No. 7653, the New Central Bank Act, the BSP shall maintain international reserves adequate to meet any foreseeable net demands for foreign currencies. These are mostly denominated in US dollar and in the form of documents and instruments customarily employed for the international transfer of funds, demand and time deposits in central banks, treasuries, and commercial banks abroad, foreign government securities and foreign notes and coins. A disclosure on this asset is made in the Notes to Financial Statements on page 6.

1.1.3 Short-Term Investments – P285.7 billion

This account represents temporary investments of funds available for current

operations of the GOCCs and intended to meet working capital requirements. It includes investments in bonds, placements in treasury bills, treasury notes, short term investments and fixed-term deposits with government banks. BSP reported the biggest short-term investments of P226.8 billion or 79.4 percent of the total short-term investments and 100 percent of the aggregate short-term investments under Financial A Cluster. It is followed by SSS – P17.1billion, PDIC – P11.2 billion (both under the

14

Financial B Cluster) and OWWA – P4.2 billion (Social, Cultural and Scientific Cluster).

1.1.4 Receivables (net) – P368.6 billion

Total Receivables accounted for 8.2 percent of the aggregate assets of

government corporations. From P260.6 billion in fiscal year 2003 an increase of P108 billion or 41.5 percent, net of Allowance for Doubtful Accounts of P20.3 billion was posted. The receivables represent 22.2 percent of the total current assets.

Table 3 presents the breakdown of receivables, by account and by cluster.

Table 3. Receivables by Cluster (in million pesos)

Particulars

Total

Financial

A

Financial

B

Public

Utilities

Industrial and Area Develop-ment

Agr’l, Trading

and Promotional

Social, Cultural,

and Scientific

Total 368,595.7 91,926.0 81,413.7 157,174.3 12,768.3 22,778.9 2,534.6 Accounts Receivable 170,195.2 25,688.2 12,655.1 131,108.9 177.7 124.2 441.1

Loans Receivable 27,563.2 3,556.0 17,717.0 1,670.3 468.7 4,131.6 19.6 Interest Receivable

18,213.8 7,440.7 5,765.7 4,746.0 46.1 33.1 182.2

Receivable-NGA 6,821.6 - 1,108.2 3,921.1 416.8 985.4 390.1 Receivable-LGU 64.2 - 4.6 - 42.4 1.0 16.2 Receivable-GOCCs 16,542.7 (0.1) 4,785.3 3,964.5 860.6 6,607.4 324.9

Advances to Officers/ Employees

174.1

0.1

6.2

66.9

32.0

12.3

56.7

Trade Business 28,778.0 25.4 445.7 13,932.2 5,609.5 7,812.5 952.7 Notes Receivable 3,157.9 1,370.2 1,430.4 - 16.7 186.0 154.6 Installment Receivable 3,230.0 2.9 213.3 - 815.2 2,198.6 -

Miscellaneous1 114,142.1 53,942.6 41,492.4 9,862.8 5,908.9 2,412.6 522.9 Allowance for Doubtful Accounts (20,287.2) (99.9) (4,210.3) (12,098.4) (1,626.3) (1,725.8) (526.5) Difference between totals and sum of components is due to rounding off 1 Includes account Claims Against GFIs and GSIS totaling P1.8 million

Corporations with the biggest recorded receivables are shown in Table 4.

Table 4. GOCCs with the Biggest Receivables

(in million pesos) GOCC Amount Nature

BSP 87,357.1 National Government’s share in the annual

revaluation of the IMF holdings of the Philippine peso with the BSP based on change in PHP/SDR exchange rate

GSIS 21,385.0 Contributions/Premium receivables

15

(Table 4, continued)

HDMF 40,564.9 Receivables from NG representing unpaid employer’s counterpart for PAG-IBIG contributions of government employees; advances to delinquent housing loan borrowers; loans extended to workers in government and public sectors

NPC 130,682.5 Receivables from customers for accrued utility revenue; tax credit certificates; receivables from fuel oil suppliers

PPC 1,791.2 Amounts due from foreign postal administrations and trade/business-postage charge account/lock box rental/bulk pre-sorted mails

DBP 3,408.5 Loans and placements granted to banks both foreign and domestic

NEA 1,682.6 Loans granted to electric cooperatives PHIC 2,387.9 Receivables from government agencies

representing unpaid employers’ contributions

1.1.5 Inventories – P64.3 billion

Ending Inventories of government corporations amounted to P64.3 billion, net of Allowance for Obsolescence amounting to P426 million. This account group is composed of the following: Items for Sale – P21.1 billion; Supplies and Materials – P19.6 billion; Raw Materials – P16.5 billion; Work-in-Process – P5.5 billion, and Other Inventories – P1.6 billion.

Corporations with significant amount balances for a specific inventory account

are shown in Table 5 below:

Table 5. GOCCs with Huge Amount of Inventories (in million pesos)

GOCC

Amount

Nature of Inventory

NPC P17,409.9 Supplies and Materials – Fuel and Non-fuel

BSP 16,453.2

Raw Materials – a) gold and silver for refining; b) materials for the printing of bank notes and other security documents such as checks, passports, land titles, BIR stamps; and c) materials and supplies for the production of circulation coins as well as special coinage and medals

3,295.8

Work-in-Process – held for printing and minting

NHA 7,870.1 Items for Sale – land and housing units

PRA (formerly PEA)

6,580.3 Items for Sale – reclaimed lands at the Central Business Park representing PRA’s in the Joint Venture Agreement with Shoemart, Inc.; reclaimed lands at the Seaside Channel and condominium units at the Coastal Plaza Condominium Project

NFA 5,338.7 Items for Sale – Palay, grain and non-grain

16

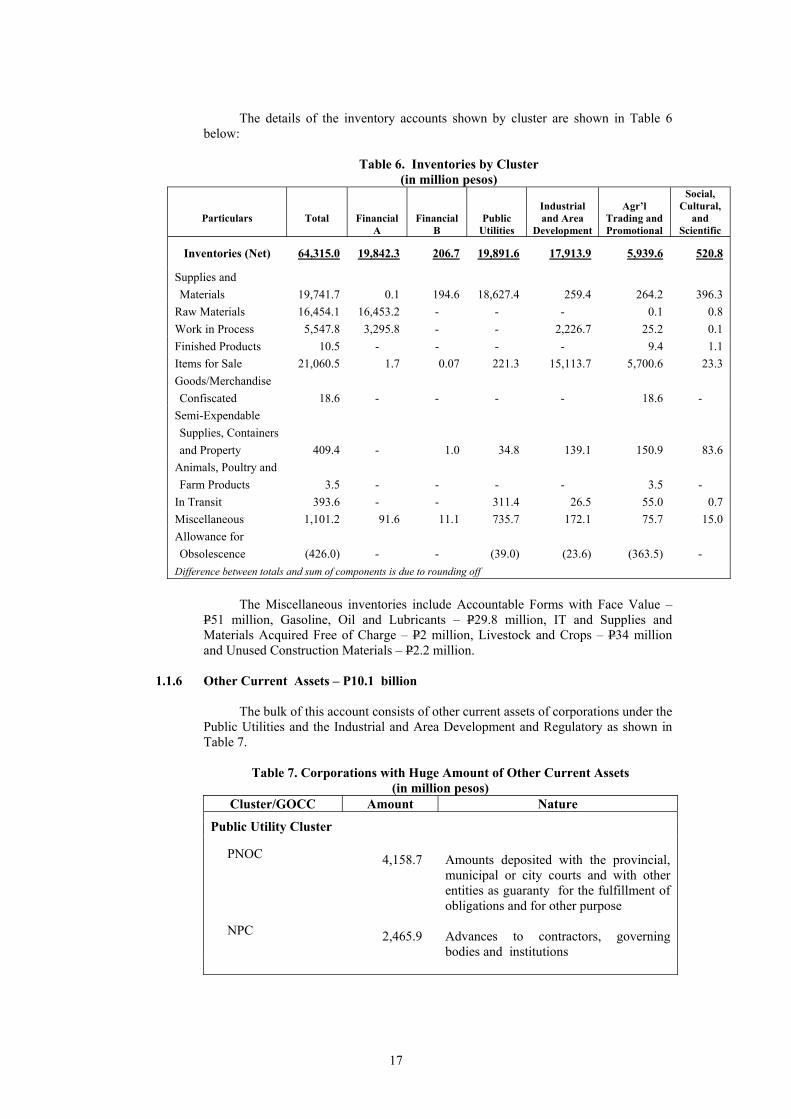

The details of the inventory accounts shown by cluster are shown in Table 6

below:

Table 6. Inventories by Cluster (in million pesos)

Particulars

Total

Financial

A

Financial

B Public

Utilities

Industrial and Area

Development

Agr’l Trading and Promotional

Social, Cultural,

and Scientific

Inventories (Net) 64,315.0 19,842.3 206.7 19,891.6 17,913.9 5,939.6 520.8

Supplies and Materials 19,741.7 0.1 194.6 18,627.4 259.4 264.2 396.3

Raw Materials 16,454.1 16,453.2 - - - 0.1 0.8 Work in Process 5,547.8 3,295.8 - - 2,226.7 25.2 0.1 Finished Products 10.5 - - - - 9.4 1.1 Items for Sale 21,060.5 1.7 0.07 221.3 15,113.7 5,700.6 23.3 Goods/Merchandise Confiscated 18.6 - - - - 18.6 -

Semi-Expendable Supplies, Containers and Property 409.4 - 1.0 34.8 139.1 150.9 83.6

Animals, Poultry and Farm Products 3.5 - - - - 3.5 -

In Transit 393.6 - - 311.4 26.5 55.0 0.7 Miscellaneous 1,101.2 91.6 11.1 735.7 172.1 75.7 15.0 Allowance for Obsolescence (426.0) - - (39.0) (23.6) (363.5) -

Difference between totals and sum of components is due to rounding off

The Miscellaneous inventories include Accountable Forms with Face Value –

P51 million, Gasoline, Oil and Lubricants – P29.8 million, IT and Supplies and Materials Acquired Free of Charge – P2 million, Livestock and Crops – P34 million and Unused Construction Materials – P2.2 million.

1.1.6 Other Current Assets – P10.1 billion

The bulk of this account consists of other current assets of corporations under the

Public Utilities and the Industrial and Area Development and Regulatory as shown in Table 7.

Table 7. Corporations with Huge Amount of Other Current Assets

(in million pesos) Cluster/GOCC Amount Nature

Public Utility Cluster PNOC

4,158.7

Amounts deposited with the provincial, municipal or city courts and with other entities as guaranty for the fulfillment of obligations and for other purpose

NPC

2,465.9

Advances to contractors, governing bodies and institutions

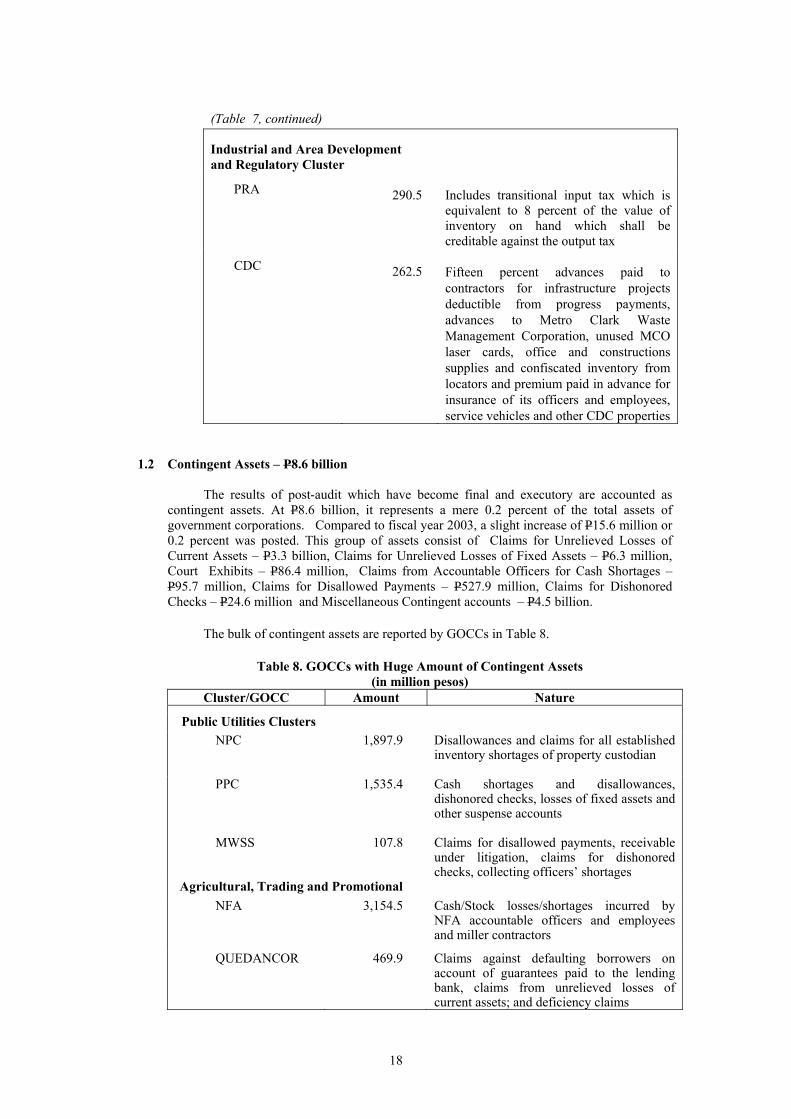

17

(Table 7, continued)

Industrial and Area Development and Regulatory Cluster

PRA

290.5

Includes transitional input tax which is equivalent to 8 percent of the value of inventory on hand which shall be creditable against the output tax

CDC

262.5

Fifteen percent advances paid to contractors for infrastructure projects deductible from progress payments, advances to Metro Clark Waste Management Corporation, unused MCO laser cards, office and constructions supplies and confiscated inventory from locators and premium paid in advance for insurance of its officers and employees, service vehicles and other CDC properties

1.2 Contingent Assets – P8.6 billion

The results of post-audit which have become final and executory are accounted as contingent assets. At P8.6 billion, it represents a mere 0.2 percent of the total assets of government corporations. Compared to fiscal year 2003, a slight increase of P15.6 million or 0.2 percent was posted. This group of assets consist of Claims for Unrelieved Losses of Current Assets – P3.3 billion, Claims for Unrelieved Losses of Fixed Assets – P6.3 million, Court Exhibits – P86.4 million, Claims from Accountable Officers for Cash Shortages – P95.7 million, Claims for Disallowed Payments – P527.9 million, Claims for Dishonored Checks – P24.6 million and Miscellaneous Contingent accounts – P4.5 billion.

The bulk of contingent assets are reported by GOCCs in Table 8.

Table 8. GOCCs with Huge Amount of Contingent Assets

(in million pesos) Cluster/GOCC Amount Nature

Public Utilities Clusters

NPC 1,897.9 Disallowances and claims for all established inventory shortages of property custodian

PPC

1,535.4

Cash shortages and disallowances, dishonored checks, losses of fixed assets and other suspense accounts

MWSS 107.8 Claims for disallowed payments, receivable under litigation, claims for dishonored checks, collecting officers’ shortages

Agricultural, Trading and Promotional NFA

3,154.5

Cash/Stock losses/shortages incurred by NFA accountable officers and employees and miller contractors

QUEDANCOR 469.9 Claims against defaulting borrowers on account of guarantees paid to the lending bank, claims from unrelieved losses of current assets; and deficiency claims

18

(Table 8, continued)

PTrA 156.1 Claims for disallowed payments and unrelieved losses of assets

PCA 137.4 Claims for disallowed payments made to various suppliers/creditors and officers and employees

Social, Cultural and Scientific TLRC

638.7

Claims for dishonored payments made, loans and accounts under litigation

1.3 Other Assets – P206.7 billion

This account consists of Miscellaneous Assets and Deferred Charges and Other Assets amounting to P206.7 billion. The components of Other Assets account are shown in Table 9.

Table 9. Components of Other Assets

(in million pesos)

Particulars

Total

Financial A

Financial B

Public Utilities

Industrial and Area Dev. and

Regulatory

Agr’l Trading

and Promotional

Social, Cultural

and Scientific

Total 206,667.9 19,045.9 37,898.5 120,590.0 22,914.3 4,098.3 2,120.9 Misc. Assets and Deferred Charges

65,412.8 4.2 3,100.8 50,385.7 10,409.1 485.4 1,027.6

Prepayments 8,912.3 2.4 7.5 1,670.9 7,113.9 109.6 7.9 Organization Costs 5,415.5 - 386.2 4,967.0 59.1 3.3 -

Guaranty Deposits 422.4 1.3 93.8 136.6 168.2 12.0 10.5

Marginal Deposits 43.5 - - 2.9 40.5 0.1 a

Deposit on Containers 9.8 - - - 7.3 2.4 0.1

Backpay Certificates of Indebtedness

a - - - - a -

Stocks and Securities of Service Enterprises

1,414.7 a 6.4 1.1 1,404.1 2.4 0.6

Miscellaneous 49,194.6 0.5 2,606.9 43,607.2 1,616.1 355.5 1,008.4

Other Assets 141,255.1 19,041.7 34,797.7 70,204.3 12,505.2 3,612.9 1,093.3 Difference between totals and sum of components is due to rounding off a – below P35 thousand

1.4 Investments and Fixed Assets – P2,630.8 billion

Investments and Fixed Assets valued at P2,630.8 billion is net of Allowance for Doubtful Accounts, Long-Term Investments – P33.8 billion and Allowance for Decline in Value of Investments – P5.4 billion and Accumulated Depreciation/Depletion – P432.2 billion.

19

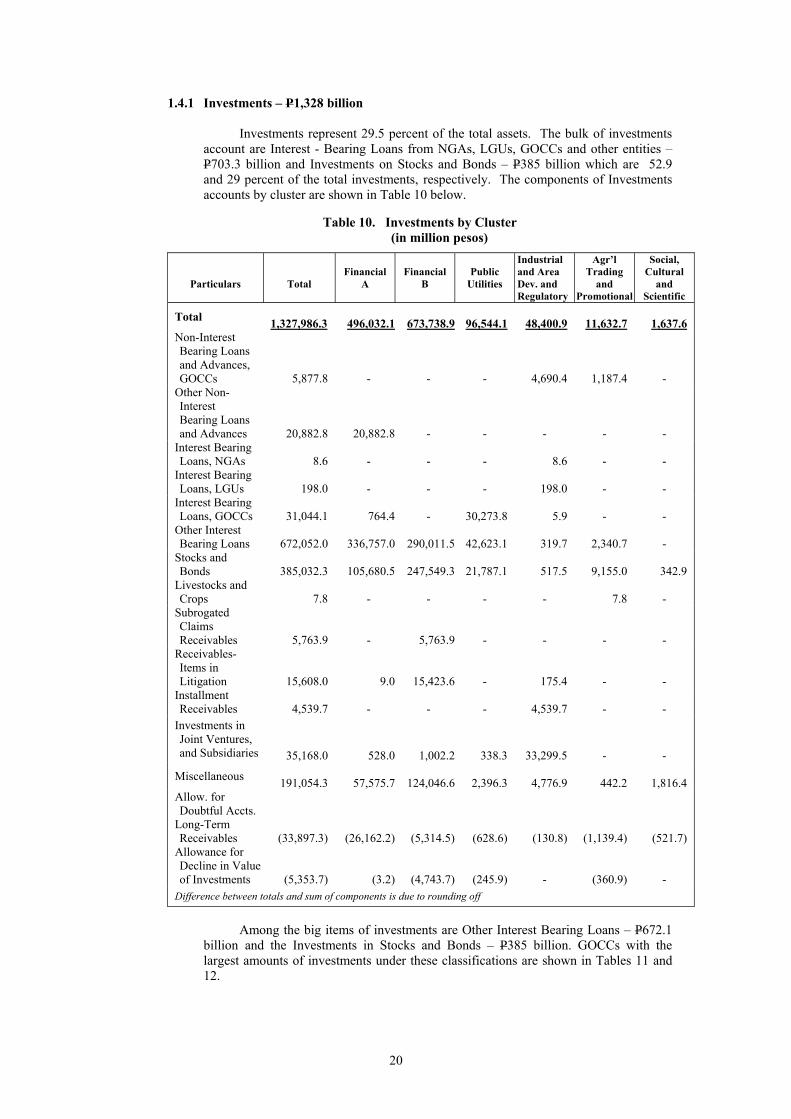

1.4.1 Investments – P1,328 billion

Investments represent 29.5 percent of the total assets. The bulk of investments account are Interest - Bearing Loans from NGAs, LGUs, GOCCs and other entities – P703.3 billion and Investments on Stocks and Bonds – P385 billion which are 52.9 and 29 percent of the total investments, respectively. The components of Investments accounts by cluster are shown in Table 10 below.

Table 10. Investments by Cluster (in million pesos)

Particulars

Total

Financial

A

Financial

B

Public

Utilities

Industrial and Area Dev. and Regulatory

Agr’l Trading

and Promotional

Social, Cultural

and Scientific

Total 1,327,986.3 496,032.1 673,738.9

96,544.1

48,400.9

11,632.7

1,637.6

Non-Interest Bearing Loans and Advances, GOCCs

5,877.8 - - -

4,690.4

1,187.4 -

Other Non-Interest Bearing Loans and Advances

20,882.8 20,882.8 - - - - -

Interest Bearing Loans, NGAs

8.6 - - - 8.6 - -

Interest Bearing Loans, LGUs

198.0 - - - 198.0 - -

Interest Bearing Loans, GOCCs

31,044.1 764.4 -

30,273.8 5.9 - -

Other Interest Bearing Loans

672,052.0 336,757.0 290,011.5

42,623.1 319.7

2,340.7 -

Stocks and Bonds

385,032.3 105,680.5 247,549.3

21,787.1 517.5

9,155.0

342.9

Livestocks and Crops

7.8 - - - -

7.8 -

Subrogated Claims Receivables

5,763.9 - 5,763.9 - - - -

Receivables-Items in Litigation

15,608.0 9.0 15,423.6 - 175.4 - -

Installment Receivables

4,539.7 - - - 4,539.7 - -

Investments in Joint Ventures, and Subsidiaries

35,168.0 528.0 1,002.2

338.3 33,299.5 - -

Miscellaneous 191,054.3 57,575.7 124,046.6

2,396.3

4,776.9

442.2

1,816.4

Allow. for Doubtful Accts.

Long-Term Receivables (33,897.3) (26,162.2) (5,314.5) (628.6) (130.8) (1,139.4) (521.7)

Allowance for Decline in Value of Investments (5,353.7) (3.2) (4,743.7) (245.9) - (360.9) -

Difference between totals and sum of components is due to rounding off

Among the big items of investments are Other Interest Bearing Loans – P672.1

billion and the Investments in Stocks and Bonds – P385 billion. GOCCs with the largest amounts of investments under these classifications are shown in Tables 11 and 12.

20

Table. 11 GOCCs with Other Interest Bearing Loans

(in million pesos) GOCC Amount Nature

LBP 151,299.3 Non-performing loans (including current

restructured loans) net of loans classified as loss which are fully covered by allowance for probable losses.

DBP 69,998.7 Consists of loans and discounts, underwritten debt securities purchased and bills purchased

BSP 109,373.5 Foreign currency loans and advances for special purpose and rediscounting; also local currency loans and advances to PDIC for re-lent ; financial assistance to distressed banks

GSIS-Social Insurance Fund

120,223.3

Various Loans granted to members of the GSIS

SSS 72,367.7 Loans to members and to other government agencies

Table. 12 GOCCs with Investments in Stocks and Bonds (in million pesos)

GOCC Amount Nature

LBP 80,594.2 Investments in bonds and other debt instruments

DBP 24,726.9 Investments in bonds and other debt instruments

GSIS Social Insurance Fund

109,029.0 Investments in subsidiaries – shares of stocks in which the GSIS holds at least 20% ownership interest or where it has the ability to exercise significant influence over the companies’ operating and financial affairs.

Investments in Commercial Papers and Government Securities

Investments in Traded Stocks – these are stocks for trading and available for sale

PHIC 35,132.4 Debenture bonds, MERALCO common stocks, Investment in PLDT stocks; Treasury Bonds with one year maturity

PDIC 35,073.4 Peso and dollar denominated Treasury Bonds and Preferred Stocks with PNB

HDMF 30,500.9 Treasury Bonds and Treasury Notes, Debenture Bonds

PSALM 19,851.9 On lending agreement –Tranches A and B with the NPC to cover its funding requirements for fiscal years 2002 and 2003

NFA 5,582.5 Zero Coupon bonds in DBP-EQPCIB, DBP-METRO BANK AND LBP, Investments in Stocks of the FTI

QUEDANCOR 2,943.5 Zero coupon issued by ROP with aggregate maturity of P5 billion for a term of 7 years to serve as security for a Syndicated Loan granted by the LBP/EPCIB

21

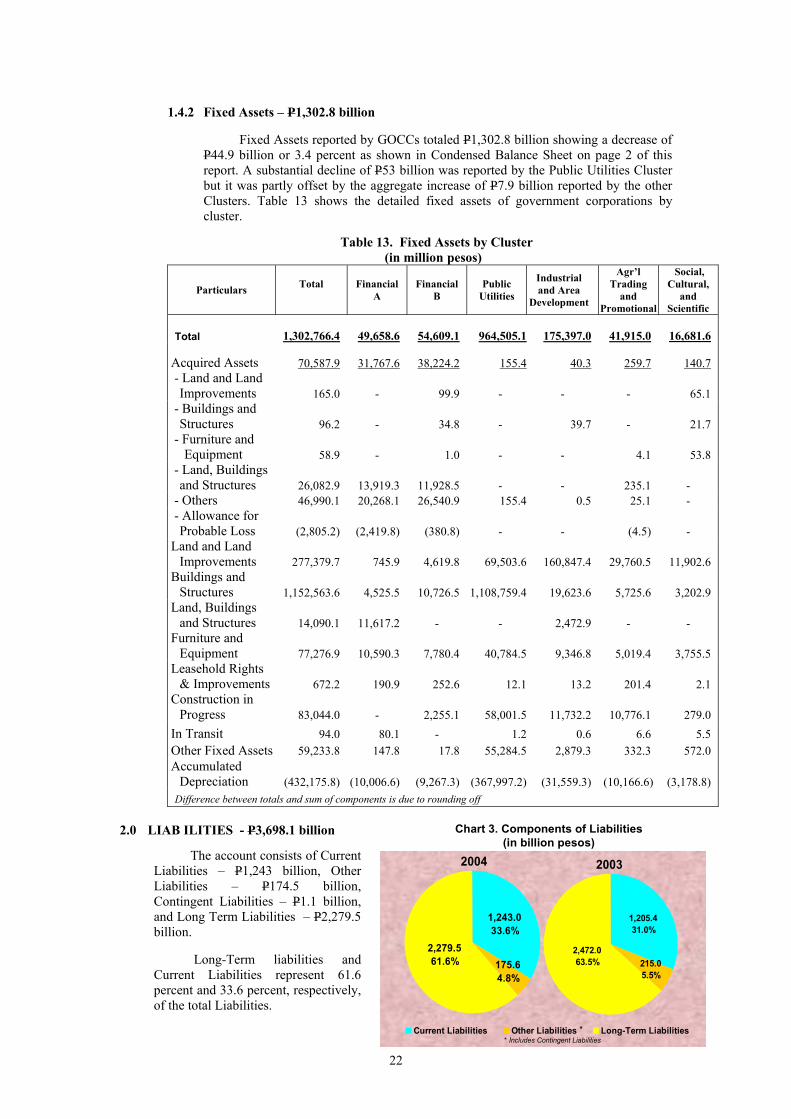

1.4.2 Fixed Assets – P1,302.8 billion

Fixed Assets reported by GOCCs totaled P1,302.8 billion showing a decrease of P44.9 billion or 3.4 percent as shown in Condensed Balance Sheet on page 2 of this report. A substantial decline of P53 billion was reported by the Public Utilities Cluster but it was partly offset by the aggregate increase of P7.9 billion reported by the other Clusters. Table 13 shows the detailed fixed assets of government corporations by cluster.

Table 13. Fixed Assets by Cluster

(in million pesos)

Particulars Total

Financial A

Financial B

Public Utilities

Industrial and Area

Development

Agr’l Trading

and Promotional

Social, Cultural,

and Scientific

Total 1,302,766.4 49,658.6 54,609.1 964,505.1 175,397.0 41,915.0

16,681.6

Acquired Assets

70,587.9

31,767.6

38,224.2 155.4

40.3

259.7

140.7 - Land and Land

Improvements 165.0 - 99.9 - - - 65.1 - Buildings and

Structures 96.2 - 34.8 - 39.7 - 21.7 - Furniture and Equipment 58.9 - 1.0 - - 4.1 53.8 - Land, Buildings

and Structures 26,082.9 13,919.3 11,928.5 - - 235.1 - - Others 46,990.1 20,268.1 26,540.9 155.4 0.5 25.1 - - Allowance for

Probable Loss (2,805.2) (2,419.8) (380.8) - - (4.5) - Land and Land

Improvements 277,379.7 745.9 4,619.8 69,503.6 160,847.4 29,760.5 11,902.6 Buildings and

Structures 1,152,563.6 4,525.5 10,726.5 1,108,759.4 19,623.6 5,725.6 3,202.9 Land, Buildings

and Structures 14,090.1 11,617.2 - - 2,472.9 - - Furniture and

Equipment 77,276.9 10,590.3 7,780.4 40,784.5 9,346.8 5,019.4 3,755.5 Leasehold Rights

& Improvements 672.2 190.9 252.6 12.1 13.2 201.4 2.1 Construction in

Progress 83,044.0 - 2,255.1 58,001.5 11,732.2 10,776.1 279.0 In Transit 94.0 80.1 - 1.2 0.6 6.6 5.5 Other Fixed Assets 59,233.8 147.8 17.8 55,284.5 2,879.3 332.3 572.0 Accumulated

Depreciation (432,175.8) (10,006.6) (9,267.3) (367,997.2) (31,559.3) (10,166.6) (3,178.8) Difference between totals and sum of components is due to rounding off

2.0 LIAB ILITIES - P3,698.1 billion

The account consists of Current Liabilities – P1,243 billion, Other Liabilities – P174.5 billion, Contingent Liabilities – P1.1 billion, and Long Term Liabilities – P2,279.5 billion. Long-Term liabilities and Current Liabilities represent 61.6 percent and 33.6 percent, respectively, of the total Liabilities.

Chart 3. Components of Liabilities

(in billion pesos)2004 2003

1,243.0 33.6%

2,279.5 61.6% 175.6

4.8%

2,472.063.5%

1,205.431.0%

215.05.5%

Current Liabilities Other Liabilities Long-Term Liabilities** Includes Contingent Liabilities

22

Compared with the restated figures of 2003, there was a net decrease of P194.4 billion or 5.2

percent. The Clusters which contributed to the decrease are the Public Utilities and Financial A Clusters with a combine decrease in their liabilities of P210.1 billion. As to specific corporations, NPC and BSP’s total liabilities decreased by P129.4 billion and P118.5 billion, respectively.

The top ten GOCCs which recorded the highest amount of liabilities or indebtedness are shown in Table 14.

Table 14. Top Ten GOCCs with Huge Amount of Liabilities (in million pesos)

GOCCs Amount GOCCs Amount

1. NPC 1,181,321.2 6. PNOC 107,368.9 2. BSP 1,037,530.8 7. PDIC 84,751.0 3. CB-BOL 416,757.2 8. PSALM 51,735.1 4. LBP 262,253.5 9. NHMFC 48,728.9 5. DBP 136,318.6 10. LRTA 45,828.3

2.1 Current Liabilities – P1,242.9 billion

Current Liabilities, composed of Payables – P331 billion, Trust Liabilities – P20.1

billion, Depository Liabilities – P537.8 billion, and Other Current Liabilities – P354.1 billion, constitutes 33.6 percent of the total liabilities.

2.1.1 Payables – P331 billion

Payables grew by 10 percent from last year’s level of P299.9 billion. Majority of

the accounts under this group of liabilities are Unliquidated Obligations/Accounts Payable – P102.5 billion, Loans Payable (current portion) – P52.5 billion and Lease Payable – P50.5 billion. The aggregate of these accounts constitutes 62.1 percent of total payables. The detailed composition of payables, by cluster is shown in Table 15.

Table 15. Payables by Cluster (in million pesos)

Particulars

Total

Financial

A

Financial

B

Public

Utilities

Industrial and Area

Development and Reg.

AgricultureTrading

and Promotional

Social, Cultural

and Scientific

Payables

331,016.0

25,394.2

34,507.0

208,876.9

15,474.1

43,820.8

2,943.1 National

Government Agencies

20,711.8

57.4

469.6

12,874.8

1,532.7

5,681.1

96.2

Local Government Units

861.0 -

6.6 -

816.5

14.7

23.2

Government Owned and/or Controlled Corporations

1,214.0

489.8

1,243.2

(1,163.7)

249.8

385.5

9.5

Unliquidated Obligations/ Accounts Payables

102,528.2

941.3

5,221.5

92,189.8

2,556.3

951.7

667.6

Interests Payable

18,896.3

8.1

5,644.3

13,082.0

54.2

5.6

102.1

Loans Payable

52,479.2

10,070.2

10,217.7

30,065.3

2,046.2

79.7 - Contracts

Payable

198.4 -

10.6 -

187.4

0.4 - Dividends

Payable

1,338.9 -

512.5

643.2

183.2 - - Bonds Payable

784.4 - -

780.0

4.4 - -

23

(Table 15, continued)

Lease Payable

50,538.2

114.0 -

50,393.3

30.9 - - Letters of Credit

1,405.4

1,391.6 - - -

13.8 -

Trade/Business

14,114.1 -

132.3

15.8

2,256.5 11,419.9

289.5 Notes and

Acceptances

18,015.1

22.2

13.0

1,406.7

62.0

16,511.3 - Supplies and

Materials Requisitioned for Stock

105.0 - - - - -

105.0

Accrued Expenses Payable

18,165.3

9,831.5

1,018.8

4,996.1

2,081.1

181.8

56.0

Income Tax Payable

158.8

4.0

0.3

28.5

76.8

36.4

12.8

Miscellaneous

29,501.7

2,464.1

10,016.5

3,565.2

3,336.1

8,538.7

1,581.0 Difference between totals and sum of components is due to rounding off

The bulk of Loans Payable pertains to current portion of Long-Term Loans

Payable of government corporations, namely: NPC – P20 billion, DBP – P9.9 billion, HDMF – P9.5 billion, PNOC – P5 billion and NEA – P1.1 billion.

The bulk of the Lease Payable of P44 billion was reported by NPC. This

represents the current portion of the lease obligation of P724.7 billion total capacity fees for BOT Plants for the duration of the cooperation period which is recorded as Electric Plant under capital lease.

2.1.2 Trust Liabilities – P20.1 billion

Trust Liabilities represents funds from government entities held in trust for the

implementation of government projects; deductions from employees’ salaries for remittances to the BIR, government corporations and other private entities; and donations from foreign institutions and private individuals for specific purposes as agreed under Memoranda of Understanding or equivalent documents.

This account amounting to P20.1 billion is 1.6 percent of the total current liabilities. The GOCCs with significant Trust Liabilities are shown in Table 16.

Table 16. GOCCs with Significant Trust Liabilities

(in million pesos) GOCC Amount Nature

NHA 2,697.4 Funds entrusted for Comprehensive and Integrated Shelter Financing Act and Poverty Alleviation Fund II

BCDA 2,288.5 Receipts from lease rental of Camp John Hay; proceeds from sale of portions of Airmen’s Village at Villamor Air Base; interest earned from investment

Full payment of Phil. State College of Aeronautics for the purchase of Villamor Air Base and other funds from various sources held in trust

PPC 2,052.5 Money order fund, international money order advance remittance and consigned goods

PCSO 2,053.3 Funds for prizes, charity, national shelter program; fund entrusted by the Commission on Higher Education and inter fund borrowings as in Charity Fund to Operating Fund per Board Resolution

24

(Table 16, continued) HGC 1,607.5 Represents funds held as designated trustee for

various housing /resettlement projects

NHMFC 935.2 Amount received from the National Government for amortization support and development financing in accordance with the implementing guidelines of RA No. 6846, as amended, creating the Abot-Kaya Pabahay Fund

2.1.3 Depository Liabilities – P537.8 billion Depository Liabilities solely of Miscellaneous account amounted to P537.8

billion. Ninety nine percent of the total amount was recorded in the books of three banks under the Financial A Cluster, namely BSP – P280 billion, LBP – P214.9 billion and DBP – P36.4 billion, consisting of time, demand and savings deposits in local and foreign currencies of the banks’ clients.

The biggest amount of BSP’s Depository Liabilities consists of the following:

National Government short-term and long-term deposits – P52.7 billion, demand deposits from banks/non-bank performing quasi-banking functions, reserve deposits and other deposits – P106.2 billion, and IMF and other financial institutions currency holdings– P97.8 billion.

2.2 Contingent Liabilities – P1.1billion

Contingent Accounts for fiscal year 2004 decreased by P19.4 million or 1.76 percent

from the previous year figure. This resulted from audit disallowances of accounts of officers and employees and those outside government service which became final and executory. Among the GOCCs with the highest amount of contingent liability accounts are shown in Table 17.

Table 17. Corporations with Biggest Contingent Liabilities

(in million pesos) GOCC Amount Cluster Nature

PPC

603.9 Public Utilities

Balance of the then Postal Service Office and all unreconciled accounts from June 1992 to December 31, 1998 awaiting final adjustment in the books of the Corporation

MWSS 197.6 Public Utilities Set up for possible loss and cost of damages in connection with existing lawsuits pending in court

CPA 183.0 Industrial and Area Dev. And Regulatory

Realty taxes due the City Government of Cebu which is being contested by the Authority in court and CPA’s share in its employees’ Provident Fund pending approval by DBM

2.3 Long-Term Liabilities – P2,279.5 billion

As of December 31, 2004, Long-Term Liabilities amounted to P2,279.5 billion, broken down as follows: Loans Payable-Foreign – P714.2 billion, Loans and Advances Payable (for NGAs, LGUs and GOCCs ) – P554.5 billion, Bonds Payable – P285 billion, Loans Payable-Domestic – P24.2 billion, Contracts Payable – P1.2 billion, Notes Payable – P279.5 million

25

and Miscellaneous – P700.1 billion. Table l8 shows the details of Long-Term Liabilities by cluster.

Table 18. Long-Term Liabilities by Cluster (in million pesos)

Particulars

Total

Financial A

Financial B

Public Utilities

Industrial and Area

Developmentand Reg.

Agriculture, Trading and Promotional

Social, Cultural

and Scientific

Total

2,279,523.5

800,281.2

156,831.0

1,246,564.9

46,228.2

28,480.8

1,137.3 Loans Payable, Foreign

714,152.9

340,246.0

5,865.6

333,989.5

30,815.3

2,099.2

1,137.3

Loans Payable, Domestic

24,154.9 -

1,850.3

7,259.2

898.7

14,146.7 -

Loans and Advances Payable, NGAs and

LGUs

403,240.0

367,957.1

157.1

19,499.0

5,718.7

9,908.22 - Loans and

Advances Payable, GOCCs

151,302.0

3,115.2

130,511.1

14,607.2

968.1

2,100.5 -

Bonds Payable

285,048.2

85,443.6

17,791.6

179,129.9 2,683.2 - - Contracts

Payable

1,216.9 -

9.2

1,196.3

1.4

10.0 -

Notes Payable

279.5 -

279.5 - - - -

Miscellaneous

700,129.0 3,519.4

366.6

690,883.8

5,142.9

216.3 - Difference between totals and sum of components is due to rounding off 2Includes P1 million Loans and Advances Payable under the Agriculture, Trading and Promotional Cluster

2.3.1 Loans Payable – P738.3 billion

Loans Payable to foreign and domestic creditors amounted to P714.2 billion and P24.2 billion, respectively or a total of P738.3 billion. For fiscal year 2004, there was a decrease in foreign loans by P51.5 billion or 6.7 percent from last year’s P765.6 billion. On the other hand, there was an increase in domestic loans by P14.6 billion or 152.1 percent. Government corporations with huge amount of foreign and domestic loans are shown in Tables 19 and 20.

Table 19. Top 20 GOCCs with Biggest Loans Payable - Foreign

(in million pesos)

GOCC 2004 2003 Increase/ (Decrease)

1. NPC 339,312.7 454,174.7 (114,862.0) 2. BSP 178,132.5 238,674.3 (60,541.8) 3. DBP 82,146.0 74,931.3 7,214.7 4. CB-BOL 48,489.9 60,541.1 (12,051.2) 5. PNOC ECD 44,575.6 41,632.6 2,943.0 6. LRTA 36,754.6 33,633.5 3,121.1 7. PSALM 33,715.5 32,035.9 1,679.6 8. LBP 28,725.4 27,538.1 1,187.3 9. MWSS 23,195.6 15,156.1 8,039.5 10. PNOC (Parent Corp.) 21,714.2 22,339.1 (624.9) 11. MIAA 8,873.7 9,073.0 (199.3) 12. LWUA 8,739.2 7,556.6 1,182.6 13. PPA 7,832.8 6,692.1 1,140.7 14. SBMA 5,474.6 4,799.7 674.9 15. PHIVIDEC Industrial Authority 3,876.2 2,948.3 927.9

26

(Table 19, continued) 16. NEA 2,798.6 3,147.7 (349.1) 17. PNR 2,028.8 5,856.7 (3827.9) 18. PCFC 1,516.4 1,620.7 (104.3) 19. PEZA 1,513.8 1,538.8 (25.0) 20. IGLF 1,235.8 1,381.9 (146.1)

The breakdown of foreign loans by source each of the government corporations

are shown in Volume II-B of this Report

Table 20. Top Five GOCCs with Outstanding Loans Payable - Domestic (in million pesos)

GOCC Amount Nature of Loan 1. NDC 1,173.8 Loans obtained from SSS, GSIS and LBP

for equity infusion and relending to the First Centennial Clark Corporation

2. NFA 9,100.6 Various loans from DBP, HSDC, LBP, DA, Equitable PCIBank, Metrobank and LBP

3. QUEDANCOR 5,000.0 LBP/Equitable PCIB Syndicated Loan

4. PNR 3,708.1 Relent Loans by National Government

5. LRTA 1,648.5 Loans obtained from LBP, Bond conversion and STCF loan converted into Treasury Bills. This is used to purchase the light rail vehicles and the construction of the LRT depot, stations and terminals and other structures.

2.3.2 Loans and Advances Payables – P554.5 billion

The balance of the Loans and Advances Payable is broken down as to National

Government Agencies – P403.2 billion, Government Owned and/or Controlled Corporations – P151.3 billion and Local Government Units – P1 million. Among the government corporations which reported the highest loans and advances payable are: CB-BOL – P367.9 billion representing, among others, payment of National Government for its liability; NPC – P9.3 billion ING Zero Coupon Bond and RP Bonds including payable to the Department of Energy representing the share of the government from the net proceeds or quarterly assigned petroleum from Malampaya; NEA – P5.7 billion relent loans; and LRTA – P4.6 billion, representing advances for the payment of principal and interest on foreign loans incurred for LRT Line 1.

2.3.3 Bonds Payable – P285 billion

Flotation of bonds is one of the sources of long-term liabilities. Out of the total

outstanding bonds payable for this year, 92.7 percent is shared by NPC – P145.1 billion, BSP – P85.4 billion and PSALM – P33.7 billion.

2.3.4 Miscellaneous Long-Term Liabilities – P700.1 billion

Ninety seven percent of this long term liabilities pertains to the lease obligation

of NPC relative to the Built to Operate Transfer (BOT) projects amounting to P680.7 billion.

27

3.0 DEFERRED CREDITS – P58.6 billion Deferred Credits of P58.6 billion is composed of Deferred Credits to Income – P21.9

billion; Undistributed Collections – P618.2 million; Semi-Expendable Supplies, Containers and Property – P31.8 million; Goods/ Merchandise Confiscated and Gasoline, Oil and Lubricants – P0.6 million; Supplies and Materials Acquired Free of Charge and Charged to Appropriation – P38.6 million. This group of accounts except the Deferred Credits to Income and Undistributed Collections are contra accounts to the unused inventory accounts for supplies and materials including gasoline, oil and lubricants. Government corporations which reported a huge amount of Deferred Credits to Income are shown in Table 21.

Table 21. GOCCs with Biggest Deferred Credits to Income

(in million pesos) GOCC Amount Nat re u

PNOC 2,960.8 Net entitlement of the Company from the “Take-of-

Pay” transactions of SC 38 Malampaya Project. Under the Take-of-Pay agreement, the customers are obliged to pay even if there is no delivery or consumption – these are unearned revenue until the aforementioned delivery is actually effected

MWSS 2,076.4 These are penalties, by way of interests, imposed against the concessionaires due to delay in their payment of concession fees

BCDA 1,869.3 Advance rentals and earnest money from various lessees

SBMA 1,638.9 Unearned income on rentals received in advance from various investors/locators under long term lease

PRA 891.2 Value of unrealized land used in payment for the upgrading of the R1 expressway being amortized as income over 35 years; future income from the lease-purchase agreements with the Sandiganbayan, BIR and OP for the Presidential Action Center (PACE)

NIA 10,095.6 Income to be realized upon collection of previously billed irrigation fees and unearned income on installment sales, equipment rentals and Communal Irrigation System (CIS) amortizations

NFA 486.6 Advance payments from retailers, private and government institutions and other income received but not yet earned.

4.0 EQUITY – P749.3 billion

476.3

273.0 272.6 257.2

0

50

100

150

200

250

300

350

400

450

500

2004 2003

Capital Surplus

At year end, the total equity of all GOCCs amounted to P749.3billion with an increase of P219.5billion or 41.4 percent compared to that of fiscal year 2003 P529.8billion. It is composed of Capital and Surplus accounts at P476.3 billion and P273 billion, respectively. Chart 4 shows the comparison of the capital and surplus accounts while Table 22presents the composition of equity accounts for the year.

Chart 4. Components of Equity(in billion pesos)

28

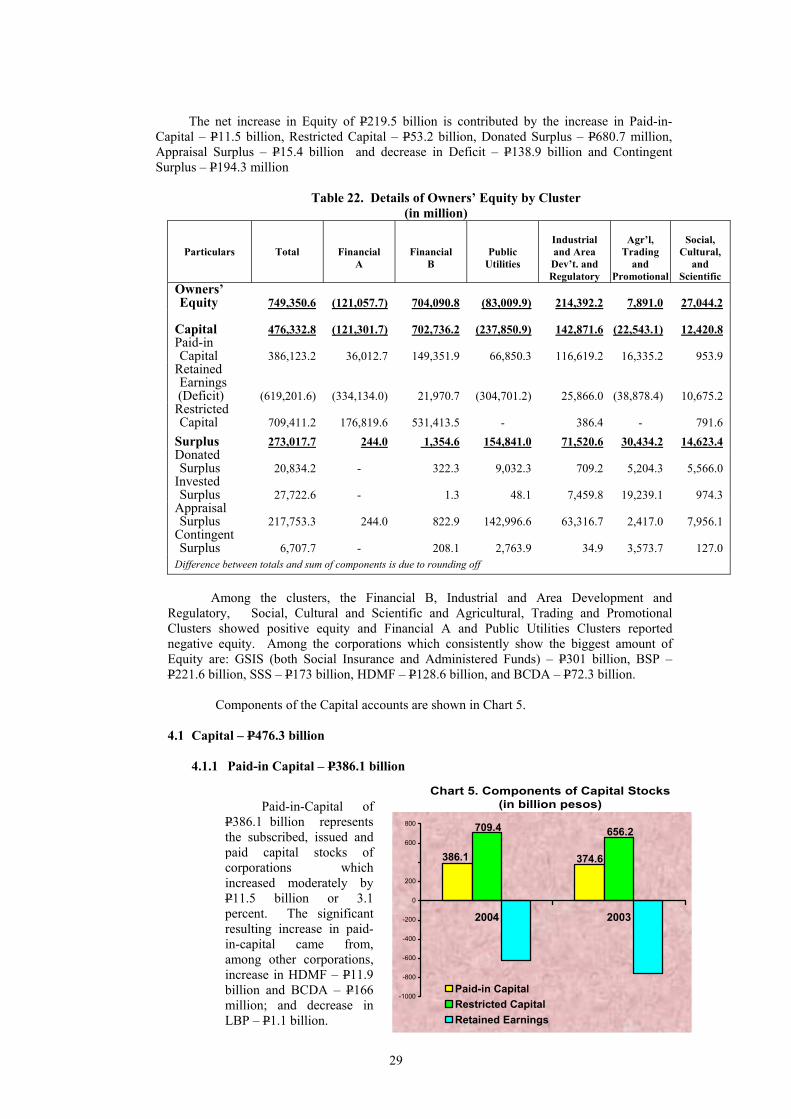

The net increase in Equity of P219.5 billion is contributed by the increase in Paid-in-Capital – P11.5 billion, Restricted Capital – P53.2 billion, Donated Surplus – P680.7 million, Appraisal Surplus – P15.4 billion and decrease in Deficit – P138.9 billion and Contingent Surplus – P194.3 million

Table 22. Details of Owners’ Equity by Cluster (in million)

Particulars

Total

Financial A

Financial B

Public Utilities

Industrial and Area Dev’t. and Regulatory

Agr’l,

Trading and

Promotional

Social,

Cultural, and

Scientific Owners’ Equity 749,350.6 (121,057.7) 704,090.8 (83,009.9) 214,392.2 7,891.0 27,044.2

Capital

476,332.8

(121,301.7)

702,736.2

(237,850.9)

142,871.6

(22,543.1)

12,420.8 Paid-in Capital

386,123.2

36,012.7

149,351.9

66,850.3

116,619.2

16,335.2

953.9

Retained Earnings

(Deficit)

(619,201.6)

(334,134.0)

21,970.7

(304,701.2)

25,866.0

(38,878.4)

10,675.2 Restricted Capital

709,411.2

176,819.6

531,413.5 -

386.4 -

791.6

Surplus 244.0 1,354.6 154,841.0 71,520.6 30,434.2 14,623.4 Donated Surplus

20,834.2 -

322.3

9,032.3

709.2

5,204.3

5,566.0

Invested Surplus

27,722.6 -

1.3

48.1

7,459.8

19,239.1

974.3

Appraisal Surplus

217,753.3

244.0

822.9

142,996.6

63,316.7

2,417.0

7,956.1

Contingent Surplus

6,707.7 -

208.1

2,763.9

34.9

3,573.7

127.0

Difference between totals and sum of components is due to rounding off

273,017.7

Among the clusters, the Financial B, Industrial and Area Development and Regulatory, Social, Cultural and Scientific and Agricultural, Trading and Promotional Clusters showed positive equity and Financial A and Public Utilities Clusters reported negative equity. Among the corporations which consistently show the biggest amount of Equity are: GSIS (both Social Insurance and Administered Funds) – P301 billion, BSP – P221.6 billion, SSS – P173 billion, HDMF – P128.6 billion, and BCDA – P72.3 billion. Components of the Capital accounts are shown in Chart 5.

4.1 Capital – P476.3 billion

(758.1) (619.2)

4.1.1 Paid-in Capital – P386.1 billion

Paid-in-Capital of P386.1 billion represents the subscribed, issued andpaid capital stocks of corporations which increased moderately by P11.5 billion or 3.1 percent. The significant resulting increase in paid-in-capital came from, among other corporations, increase in HDMF – P11.9 billion and BCDA – P166 million; and decrease in LBP – P1.1 billion.

400

Chart 5. Components of Capital Stocks(in billion pesos)

386.1 374.6

656.2709.4

-1000

-800

-600

-400

-200

0

200

600

800

2004 2003

Paid-in CapitalRestricted CapitalRetained Earnings

29

4.1.2 Retained Earnings (Deficit) – (P619.2 billion)

Deficit of P619.2 billion represents the cumulative balance of net income or loss, dividend contributions, fundamental errors and other capital adjustments. By cluster, huge deficit is shown under the Financial A amounting to P334.1 billion, followed by Public Utilities - P304.7 billion. This is shared consistently by CB-BOL, an institution under liquidation, and by NPC with a remarkable deficit of P390.5 billion and P266 billion, respectively.

Although NPC still showed a high deficit in 2004, there was a substantial

reduction of its deficit from P456 billion in 2003 to P266 billion in 2004. This is due mainly on account of the Government Debt Absorption of ROP Purchase Bonds by the National Government amounting to P200 billion as mandated under Republic Act No. 9136 otherwise known as the Electric Power Industry Reform Act (EPIRA) and Executive Order No. 370. A DBCC Resolution No. 2004-3 dated November 12, 2004 further approved this debt assumption process.

For this year, the total deficit decreased by P138.9 billion. The substantial

improvement in financial performance was contributed by NPC whose deficit decreased by P190 billion on account of the Government Debt Absorption of P200 billion as mentioned above.

Retained Earnings (Deficit) of all Clusters are shown below.

Table 23. Retained Earnings (Deficit) by Cluster

( in million pesos) Clusters Amount

Deficit ( 677,713.6) Financial A (334,134.0) Public Utilities (304,701.2) Agricultural Trading & Promotional (38,878.4) Retained Earnings 58,511.9 Financial B 21,970.7 Industrial & Area Dev't & Regulatory 25,866.0 Social, Cultural & Scientific 10,675.2 Balance (619,201.7)

4.1.3 Restricted Capital – P709.4 billion

Restricted Capital represents the amount earmarked from retained earnings

intended for various purposes, such as currency insurance, fidelity insurance, and medical benefit, and retirement benefit, fluctuations in foreign exchange rates, gold holdings and for contingency. Among the GOCCs which reported the huge amount of restricted capital are shown in Table 24.

30

Table 24. GOCCs With Huge Amount of Restricted Capital ( in million pesos)

GOCC Amount Nature GSIS 286,437.8 Actual reserves requirement set

for the various funds – Social Insurance, Optional Insurance, Employee Compensation Insurance, Pre-Need Insurance, General Insurance and Property Replacement

BSP 174,478.0 Capital Reserves as provisions for potential loss arising from the volatility of the exchange rates and price of gold

SSS 173,007.8 Reserved fund for property valuation and insurance

PDIC 36,578.2 Reserves for estimated insurance losses

PHIC 35,287.0 Represents the actuarial estimate for two years’ projected program expenditures

4.2 Surplus – P273 billion

4.2.1 Donated Surplus – P20.8 billion

Donated Surplus increased by P680.7 million or 3.4 percent, compared to the figure of fiscal year 2003. Government corporations which received the biggest donations are listed in Table 25.

Table 25. Corporations with Biggest Amount of Donated Capital

( in million pesos) GOCC Amount Nature

NPC 4,022.0 Represents grants received from foreign governments and lending institutions which were used to finance the implementation of various projects

PTrA 3,645.7 Donated lands for tourism purpose

LWUA 2,647.9 Represents subsidy support from the National Government for water supply projects.

MWSS 1,047.0 Represents waterworks facilities turned over by private subdivision by way of a deed of donation. Included herein is the grant from the Japan International Cooperation Agency for the rehabilitation of Balara Water Treatment Plant

31

(Table 25, continued) LCP 2,962.7 The 12-hectare lot donated by the NHA with an

appraisal value of P2.89 billion subject to reappraisal

CCP 1,464.2 Includes the vast parcels of reclaimed land where the CCP Complex is situated, the initial capitalization of CCP

NFA 471.8 Cash and fixed assets donated by various individuals, organizations and offices. The fixed assets are buildings and equipment mostly technical and scientific in nature received from Japanese government specially for Food Development Center

4.2.2 Invested Surplus – P27.7 billion

Compared to the previous year, there was a decrease in Invested Surplus in

the amount of P58.5 million. This account is a contra account of Investments and Fixed Assets accounts. Of the outstanding balance, 96 percent was reported by NIA and PRA of P19.2 billion and P7.4 billion, respectively. The Invested Surplus of NIA pertains to the asset accounts transferred by the DA and the DPWH since 1990. PRA’s surplus represent the appraised share of lands on various reclamation agreements entered into with private parties at no cost.

4.2.3 Appraisal Surplus – P217.8 billion

Appraisal Surplus is the excess of the sound value over the net book value of the corporations’ assets. This resulted from the appraisal of the Fixed Assets of GOCCs by independent appraisers. For this year, the corporations which accumulated the biggest appraisal surplus were: NPC – P95.8 billion or 44 percent; PPA – P51.8 billion or 23.8 percent; MWSS – P28.7 or 13.2 percent and PNOC – P17.5 or 8 percent.

4.2.4 Contingent Surplus – P 6.7 billion

Contingent Surplus amounting to P6.7 billion is the contra account of the

Contingent Assets and Contingent Liabilities. Of the amount, NFA and NPC recorded the highest amount of Contingent Surplus of P3.2 billion or 47.8 percent and P1.9 billion or 28.4 percent, respectively. These are disallowances in post audit, claims for unrelieved losses of properties and claims for all established inventory shortages of accountable officers.

32

STATEMENT OF INCOME AND EXPENSES